United Distributors hit with anti trust action by CCP

Ideal Spinning Mills shuts its looms on cost crunch

Airlink’s earnings outlook slashed as mobile demand softens

Kohat Cement to enter the real estate development market

Power sector circular debt has reached its Rubicon

Dolmen

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

Joint family: not going anywhere

Solo living, and the attendant loneliness, is on the rise everywhere in the world… except in Pakistan.

By Farooq Tirmizi

In the end, Humaira Asghar Ali will get a family funeral and burial.

The story of a young professional woman, living alone in an apartment in Karachi, and found dead having passed away perhaps as much as nine months ago, has been shocking to just about everyone in Pakistan, prompting the question: how did nobody notice for nine months that she was no longer alive?

The estrangement from family is something that press accounts have dwelled upon substantially, but perhaps more shocking than that was something else implicit in this account: she must have been incredibly lonely for at least the last year of her life. Indeed, lonely to a degree that is exceedingly uncommon in Pakistan and would be uncommon even in much more individualistic societies in Europe and North America.

The account of her passing – and exceedingly delayed discovery of it – has prompted

us to ask the question: does this incident mark the arrival of the global disease of loneliness in Pakistan? Or is it an isolated incident that is not representative of broader trends?

After all, this was the second such case that occurred in Karachi in just the past few weeks. In late June, the actress Ayesha Khan’s body was found several days after having passed away.

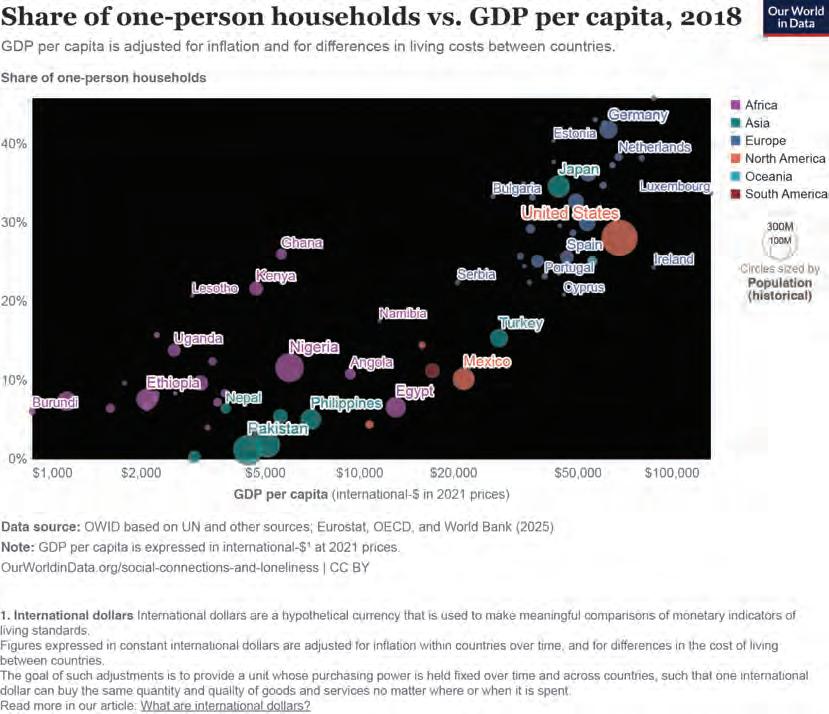

Based on Profit’s analysis of recent demographic trends, our answer for the moment appears to be: these are both isolated incidents. Among countries for which data is available, Pakistanis appear to be far less likely to live alone, and somewhat more surprisingly, the trend does not appear to have increased over the past three decades for which data is available.

In this story, we examine what solo living is, and how common it is around the world. We then dive into why it has failed to take off in Pakistan, with hypotheses for both the economic and non-economic reasons. Finally, we look at what the economic effects of joint

family living has been for Pakistan.

The global rise of solo living

Living alone is hardly something that has been uncommon throughout history, but for most countries that consistently track the data over time, the trend is clear: more and more people live alone. Two reasons appear to explain why this is the case:

1. Societies that grow richer have more people who can afford more individual space, and hence the probability that a given individual will live alone rises. Poverty and individualism cannot coexist.

2. Societies that are aging also see an increase in solo living: a person is most likely to live with other people in their youth (with their parents) and middle age (with their own children).

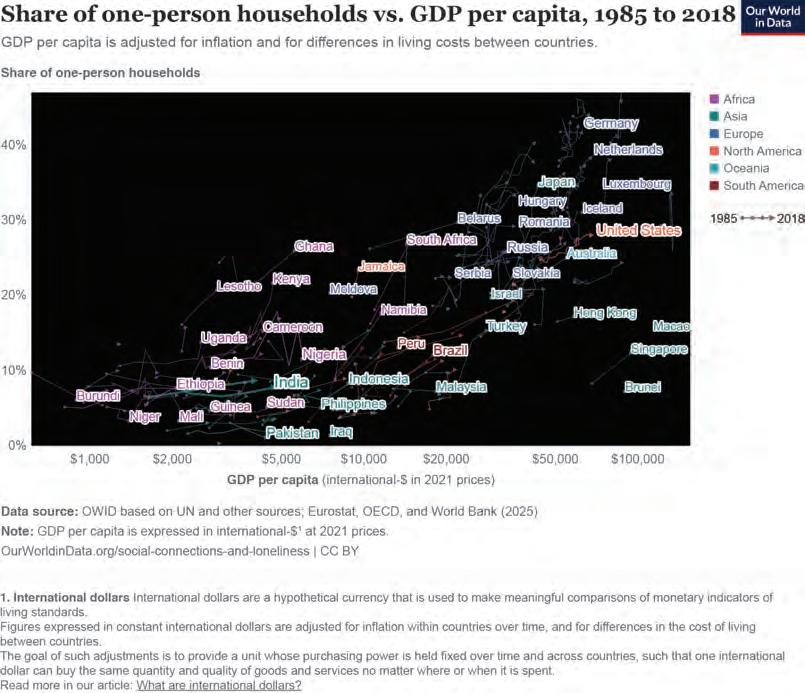

Global data makes this abundantly clear: there appears to be an approximately logarithmic relationship between a country’s per capita income and the proportion of households that consist of a single individual. The richer you get, the more people want their own space and can afford it, and hence more and more people choose to live alone.

The loneliest country appears to be Norway, where approximately 46% of all households consist of an individual. This does not mean that 46% of Norwegians live alone. By definition, the proportion of actual people who live alone is smaller, since the households with more people will account for a greater proportion of the overall population.

It is also evident in the data that countries see a higher incidence of solo living as they get richer. The United States, for instance, has seen its share of solo households double over the past 50 years, a period during which its per capita income also nearly doubled.

The differences in household structures can become even more stark if one examines the rural versus urban divide. The place with the highest number of solo households appears to be Stockholm in Sweden, where 60% of households consist of a single person living alone. The numbers for London are not much further behind.

By comparison, even Manhattan in New York, widely popularized in American media as a place of libertine living, only has about 23% of its households consisting of individuals.

The impact of aging is quite stark as well. The country that tracks this most thoroughly is the United States, and what we see in US data is quite stark. Older Americans are much more likely to live alone than any other demographic group in that country, which means that as societies age, it may become more common for many people to end up alone as their spouse dies and their children move away from home.

The soul-crushing loneliness of old age is increasingly a topic of conversation among people in high income countries. Having a person come in and check on you to see if you are alive or have needs to be attended to is increasingly a standard part of the benefits package in US old-age health insurance plans called Medicare Advantage.

But take a closer look at the chart and one notices that Pakistan has among the lowest rates of solo households in the world. Indeed, Pakistan’s rate of solo households – which account for only about 1% of total households and just 0.2% of people – is an order of magnitude lower than many countries that are far poorer than us. This implies that it is not just economics that keeps Pakistanis from living alone.

Compare this to India, where the average household size is 4.4 people as of 2021, almost two full people per household less than Pakistan. The proportion of Indian households that consist of a single individual was approximately 7.7% of households.

Solo living – or lack thereof – in Pakistan

The total number of people in Pakistan who live alone is approximately 425,000 as of 2020, the latest year for which a Household Integrated Economic Survey was available to make the calculation. For that year, that represented less than 0.2% of all people in Pakistan.

In absolute terms, 425,000 is a lot of people. But relative to the overall population, it is tiny. What is interesting about this number is that it has stayed virtually the same over the past two decades. As of 1999, the proportion of the Pakistani population that lived alone was about 0.24% of people.

On the surface, the structure of the Pakistani household looks remarkably stable. In the 1998 census, the average household size was 6.8 people. By the 2023 census – a full 25 years later – it had dropped by just 7.4% to 6.3 people per household.

Granted, India is now richer on a per capita basis than Pakistan and has been for about two decades. But even countries like Ethiopia, Tanzania, and Uganda – all with lower per capita incomes than Pakistan – have more people living in solo households than us. What accounts for the difference?

One possible explanation is that the per capita income is an insufficient amount of data to understand the full picture. It could be that real estate prices in Pakistan – relative to per capita incomes – are higher than they are in other countries, causing more people to stay in joint families rather than trying to move into separate homes.

While international comparisons on real estate prices are admittedly tough, the most readily available metrics from a variety of sources indicate that while property prices in Pakistan are high relative to incomes – the median home price is about 13.3 times the average household income in 2024, according to one measure – they are not that much higher than India, where the comparable number is

11.1 times the average household income.

High real estate prices, in other words, do not explain Pakistanis’ propensity for living in joint families. It is also not a disconnect between home prices and rental prices, because in fact, rents in Pakistan are very low relative to the price of the home that one may be renting.

At some level, it comes down to the fact that Pakistanis may simply prefer living in joint families in a way that other countries do not.

There is one other potential explanation: at least some Pakistanis do like living alone, but the ones most likely to live alone do not do so inside the country. They move out.

Data on emigrants from Pakistan does not describe their living situations, nor their household sizes, so we are reduced to looking at proxies. One such proxy where the data is rather stark is the population pyramid of the United Arab Emirates, host to one of the largest populations of expatriate Pakistanis in the world.

It is an astonishingly distorted pyramid where the number of men in their 20s through their 50s vastly outnumbers women. Literally two to three times as many men in some of those middle age cohorts as women indicates that the vast majority of these men are living in

the UAE without their families. They may have roommates to help them defray the cost of rent. But in some ways, that is a form of solo living: away from family and social obligations.

Of course, a similar phenomenon does exist within the country as well, with many men moving to larger cities, especially Karachi, to earn a living while leaving their families behind. Yet the census data shows that this appears to be a relatively less common feature of domestic migration and it is becoming much more common for labourers to either migrate with family, or else have their family join them at their destination shortly after arriving.

The changing structure of the Pakistani household

This is not to say that the structure of Pakistani households is not changing at all. It is just changing much more slowly than other places around the world that might be comparable in some ways to our economy and culture. And, somewhat uniquely, it is not changing in a way that would accommodate more solo living.

Indeed, Humaira Asghar lived in perhaps one of the very few neighbourhoods in all of Pakistan that have a large enough share of solo households where her passing could have gone unnoticed for quite so long. The Ittehad Commercial part of DHA Karachi has a large concentration of very small apartments – more so than even other parts of DHA Karachi – which are preferred by the relatively small number of young professionals who move to Karachi from other parts of the country for work and do not live with their families.

Karachi has more apartments than the rest of the country combined, and apartments tend to be the favoured housing of solo households. But the vast majority of Karachi’s apartments house families.

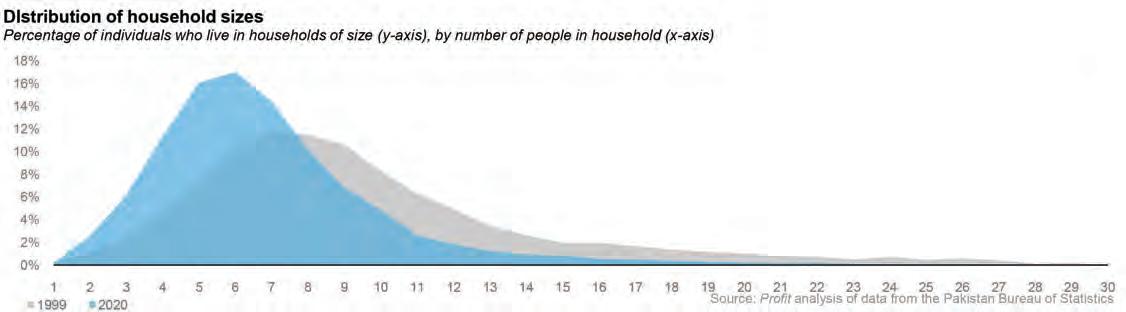

But while solo households are not becoming any more common, what is perhaps becoming a little more common is the nuclear family. In 1999, the proportion of households

that had 5 people or less was less than 16% of the total population, according to Profit’s analysis of data from the Pakistan Bureau of Statistics. By 2021, that proportion had risen to 36.5% of the country’s population. (Not households, but total population).

Nearly two-thirds of the population still lives in households with 6 or more people, which implies that the vast majority of Pakistanis still live in joint families.

But the super-large joint family that was the norm one generation ago appears to largely be gone. In 1999, about 40% of Pakistanis lived in households with 10 people or more. In 2020, that number was down to just over 15% of Pakistanis. Households in Pakistan are now more alike than ever before because people are living in a narrower cluster of living arrangements.

The joint family labour cost subsidy may go away

Here is the underappreciated aspect of joint families: the norm of joint families serves as a labour cost subsidy to employers. Wages are set by both demand and supply, and while many factors go into each side of that equation, at least a portion of labour market supply is determined by the cost of living that the labour supplier wishes to cover.

If a large enough proportion of the population lives in joint families – as is currently still the case in Pakistan – then each individual’s requirement for income generation is lower than it would be if nuclear families were the norm. In other words, joint families allow for multiple earners in a single household while reducing average cost per individual consumer, and also the average income demanded by each individual earner.

Put another way: the average Pakistani employer can afford to pay low salaries to their employees because the majority of employees are in their 20s and live in the same house as their parents, and potentially other siblings

who also have an income. They do not have to pay rent, and since there is at least one – and possibly more – other earners in the household, the amount they have to contribute is less than if they lived with a spouse and dependent children.

What happens, however, if the nuclear family becomes the norm? Two big things: employees would get much more picky about wages. Initially wages would not move as the historical norm continues, but each individual employee becomes much more sensitive to even the slightest wage increase available from job switching, which then forces employers to increase wages in order to reduce employee turnover.

Of course, wages cannot rise above the marginal productivity of labour, so there are limits to how much they could rise, which probably restricts the number of people who can move towards nuclear families. But the fact that the nuclear family is rising in frequency suggests that the marginal productivity of Pakistani labour is rising – even if it is not rising inside Pakistan. Presumably a substantial number of employed Pakistanis work outside the country.

Conclusion

The bottom line: the Pakistani joint family undergirds a lot of implicit costs in the country, and while it is changing somewhat, it is by no means going away. More re-assuring is the fact that while more space is being created for individualism, it is not yet veering into the extreme where loneliness starts to become the norm. Households are getting somewhat smaller, in part because of fewer children and in part because of greater household formation (more people able to move out of their family homes).

All of these are good things. The recent unfortunate news brings forward a stark reminder that not everyone is fortunate enough to live close to family and loved ones, but that happily, this is still the norm in Pakistan.

We still do not have much as a country. But we do have our families. n

By Abdullah Niazi

It is truly mind boggling when you think about just how much of our world is made out of plastic. Take a look around wherever you are reading this, something or the other is definitely plastic. Whether it is the cup you are drinking from, the toilet seat you are sitting on, the case protecting your phone (because print is dead and you are most probably reading a digital copy) or just the bottles that contain your shampoo or soft drink or God knows what else.

And to think, if someone from early in the last century were to show up, they would not recognise so much of what we have surrounding us. Plastic was first discovered in some capacity in the 17th century, and again made appearances during the industrial age. But it was only after the First World War that improvements in chemical technology led to an explosion in new forms of plastics, with mass production beginning in the 1940s and 1950s. In 2018, the world celebrated the centenary of the end of the Great War, and in the 100 years since, plastic has taken over and may be brimming to destroy us.

Punjab continues to struggle against plastic

From banning plastic bags to introducing plastic recycling machines, the government is finding out it is harder to get rid of plastic than they might have accounted for

Let us not kid ourselves. This is a global problem, and one that is pervasive in Pakistan. According to the Pakistan Plastic Manufacturers Association (PPMA), there are nearly 8,000 industries and units that make products related to plastic.The largest among this group of manufacturers are those that produce polyethylene bags. In the past five years, these manufacturers have been the object of the Government of Punjab’s attempts to deal with plastic waste and pollution. The only problem is that the government’s strategies have been all over the place, and implementation, as always, has remained a key struggle.

Sizing up the industry

We don’t really know exactly how big the plastic industry is in Pakistan. In fact, we cannot even make a very good guess since a big part of the entire industry is dependent on small scale units that operate in cash and are rarely regulated. What we do know is that it is big. In fact, according to officials of the PPMA, even the smallest units manufacturing plastics have 20-25 employees. The larger ones have a work force in the hundreds.

The PPMA’s estimates hold that there are

63,000 shopkeepers selling shopping bags in bulk across Pakistan. Meanwhile, the amount of people working in factories and industries is estimated in the hundreds of thousands. Around 3 lakh families work in this industry.

The PPMA has also claimed (with the flimsiest of evidence that relies on the ignorance of their audience) that the plastic industry is one of the five largest industries in Pakistan. By what measure, we are not told. This is an industry that gives billions of rupees in taxes to the national exchequer every year, presumably in the form of taxes, though given the fact that a significant proportion of them are small, informal sector producers, that stretches credulity. The industry’s lobby believes that the government collects an estimated Rs60 billion because of imports by the plastic industry, while more than Rs70 billion are collected in other forms of taxation.

In Lahore’s Shah Alam Market, Muhammad Arsalan Sheikh is a major plastic grain trader. According to him, people from all over Pakistan involved in the plastic industry have invested Rs150 billion in the form of machinery, market, and buildings. The plastic grain used to produce these products is imported from Dubai, Iran, KSA and other countries

The usage of eco-friendly cloth and paper bags is being promoted instead of plastic bags in the province. Plastic bags give a little convenience to the people in their daily lives, but they cause colossal destruction by remaining in the environment for centuries

that are oil producers since plastic grain is a byproduct that can be developed from the petroleum trade.

Over time as the plastic industry has grown, the environmental consequences of continuing to use plastic have been devastating and may soon overwhelm natural resources. Environmental, ecological and infrastructural damages are rife because of them, and it is estimated that nearly 70% of produced bags are currently lying around in the form of garbage, of which a lot if burnt, causing serious air pollution and the release of carcinogens and other harmful substances.

According to another study, these bags will account for 12 billion tons of non degradable waste that will be polluting the planet by 2050. The problem is bad enough that associations like the PPMA or the Plastic Bag Association (PBA) do admit it.

The ban and everything since

There are a few stages to how plastic has been treated by the government. The first significant move came in 2014. Plastic manufacturers everywhere have always known their product is difficult to deal with. But there are a few categories of plastic products to account for. Things like bottles, cups, containers are all products that can either be used again or are recyclable. They contain some weight as well, and the role of the kabariya has been to find the best recyclable plastics and either sell them back to large corporations that have environment focused buyback options or recycle them to companies that then use them to make different products. Plastic furniture, for example, is often made with recycled plastics. Those green benches and tables that seem to be in every school and park in Punjab? Made from old bottles you’ve squeezed your shampoo out of and all other manner of containers.

But perhaps the biggest problem area has been plastic shopping bags. Light weight, a menace to collect and recycle, and amounting to basically nothing in weight they are the

Maryam Nawaz, chief minister of Punjab

worst of fast consumption. People use them and throw them at will and they don’t go anywhere for centuries.

The environmental concerns caused by shopping bags is an international phenomenon, which is why Oxo Biodegradable technology was introduced, the industry thought they had a saviour. Two or three other technologies had been introduced before this, but this proved to be the most successful and feasible one yet. With the help of this tech, the hundreds of years that plastic takes to degrade was brought down to a matter of a few months. This is why it is called controlled life plastic technology. The way it works is that it is also made in the shape of plastic grain, and during the process of making plastic, a specific amount of this material is added, which makes the plastic environmentally friendly.

The first interventions

In Pakistan, it was introduced on 1 April 2014, and other than Punjab and Islamabad, using this technology was made mandatory under law in the rest of the country. Meanwhile, this technique started being used in the preparation of plastic bags in Lahore and other cities of the Punjab. This was the first intervention in regulating plastics by the government. But the problem was once again the market, and how it responded.

In an earlier interview with Profit, the distributor of this technology in Pakistan, Amir Yusuf, said this innovation was a godsend in making plastic bags environmentally friendly. In Pakistan, large multinationals and exporters of plastic bags are using this technology, and hundreds of tons have already been made.

On the other hand, Khalid Zuberi – a plastic factory owner on Sheikhupura Road in Lahore – said that this technology is useful, but using it in plastic means a hike in price of plastic products. “Because of this, people look for cheap plastic instead of responsible plastic. Until legislation is made to make this kind of plastic mandatory, it simply is not competitive on the market. In the provinces

where there is legislation, even fruit sellers use degradable bags” he said.

It was clear by now that the government was interested in this issue, particularly since they were often responsible for the cleanup strategy of the indiscriminate use of plastics.

Going for the bag

The next big move came in 2020. The government began by gradually phasing out plastic bags beginning from Islamabad. This ban was also placed in high-income neighbourhoods of Lahore, such as Model Town and Gulberg. The argument was that plastic shopping bags were causing environmental, ecological and infrastructural damage in the form of hurting animals and the sewage system. Naseemur Rehman, the director of the Punjab Environment Protection Department at the time, said that the greatest reason for environmental problems are small and low grade plastic bags.

“Not only are they very cheap, and thus used without thinking, but it also has no recycle value. You can collect them all day and they will not amount to more than 1KG in weight but it will cause great harm to the environment,” he told Profit. “The percentage of plastic in shopping bags being lessened decreases the environmental impact and this is the good practice as established globally.”

The PPMA bemoaned the loss of business as expected.

“This committee has given many suggestions to the government to tackle the problem together and responsibly. In a recent meeting with government stakeholders, it was also decided that plastic bags would be as thick as 45-50 micrometers, while their size would be 12×15 inches. We are doing this despite the fact that polyethene bags were used all over the world as an FDA approved product, including US, Europe, Canada have not banned plastic bags. In fact, they used similar suggestions to what we at the PBA are saying to the government.”

“Other than Kenya, no country has imposed an outright ban on shopping bags. This

has caused a fall in revenue, unemployment and shutdown of industry in Kenya,” they say. “Because of their many jungles, they have been able to use paper bags. We hope that the government will listen to the concerns of the PBA.

The kill shot

In 2023, the government took its most aggressive stance yet against plastic pollution, implementing a sweeping ban on disposable plastic products across Punjab. This move, which struck at the heart of industries reliant on single-use plastics, particularly food and packaging sectors, came as a shock to many. The ban, encompassing items such as cups, spoons, food containers, straws, and even multi-layered packaging commonly used for chips and biscuits, sparked significant pushback from manufacturers and business owners.

Industry voices, particularly from the PPMA, lamented that this decision had been made without adequate consultation with stakeholders. They warned that the ban would endanger the livelihoods of thousands, with the potential for widespread economic fallout, including revenue loss and unemployment. Even more concerning was the potential domino effect it could trigger across related sectors, including beverages and confectionery, leaving them uncertain about their future.

Supporters of plastic use, including some prominent international voices from the UAE, China, and Saudi Arabia, defended the necessity of single-use plastics for hygiene and health reasons, especially in food handling. These countries, they argued, had not banned plastic and relied on it for its sanitary benefits. Despite this, Pakistan moved forward with its plan, citing environmental and infrastructural concerns.

In response to growing opposition, the Punjab Environment Protection Department (EPD) doubled down on its commitment, classifying the production, use, and distribution of single-use plastics as a criminal act under the Environment Protection Act, with penalties reaching up to Rs 1 million. The move was further backed by the Punjab Governor, signaling a firm stance on environmental sustainability.

The ban covered 15 types of plastic products, a drastic step in the government’s broader effort to curb plastic pollution. As part of the ‘Beat the Plastic’ campaign, this initiative was designed to phase out the use of non-degradable plastics. A key part of this was the federal government’s directive to plastic manufacturers to cease the production of non-degradable plastics by August 1, 2023.

What happens next?

The incumbent government of Maryam Nawaz has introduced a new scheme at the beginning of this month Under the programme, residents can deposit

empty plastic bottles into Reverse Vending Machines (RVMs) and earn up to Rs1,000 in “Green Credit” per kilogram of plastic — roughly 20 one-and-a-half litre bottles.

The project, led by ISP Environmental Solutions with support from the Intratech Group and the World Bank, is part of Punjab’s Environmental Protection Agency’s Green Credit Program. The project aims to transform how urban waste is managed and perceived by offering financial incentives in exchange for used plastic.

Lahore produces about 500 tons of plastic waste daily, much of which pollutes waterways and landfills, according to Intratech Group Chairperson Gulfam Abid.

“These new Reverse Vending Machines will collect single-use plastic items, including bottles, cups and plates,” he explained. “The collected material will be repurposed into raw materials for footpaths, road repairs and environmentally sustainable bricks.”

This, of course, is only the latest step in trying to mitigate plastic waste. There have been some other intelligent solutions as well, such as what was done to Lahore’s garbage dump at Mehmood Booti. Just last month, the Punjab Government again vowed to make the province plastic free.

“The usage of eco-friendly cloth and paper bags is being promoted instead of plastic bags in the province. Plastic bags give a little convenience to the people in their daily lives, but they cause colossal destruction by remaining in the environment for centuries,” said

Maryam Nawaz in June. She added that plastic bags could cause loss of soil fertility, clog drainage systems and exterminate aquatic life.

The usage of plastic can cause cancer and other fatal diseases as well, she said and added that, “A culture of implementing environmental laws is being strictly enforced in the markets and factories to eliminate the trend of usage of plastic bags across Punjab”.

The spirit of this environmentalism is well and good in statements. What is actually needed is cold hard steps. But according to a recent damning report, the bans we have described above have failed miserably in their purpose. More than 15,000 shopping bag manufacturing units, both large and small, are operating in Lahore, Multan, Faisalabad, Gujranwala, Rawalpindi, Sargodha, and D.G. Khan, with 20,000 to 25,000 tonnes of plastic bags manufactured daily in the provincial capital. Documents further revealed that although Lahore alone generates 65,000 tonnes of waste daily, with 20% or 18,000 tonnes consisting of shopping bags, the government only has the capacity to collect 19,000 tonnes hence leading to pollution and disruption of the sanitation system.

All of these measures have been taken and have failed in their implementation across different governments. This one has made some tall claims, but so did the previous ones. In the midst of increasing criticism, this alone could be something Maryam Nawaz can turn to in her search for a legacy beyond marketing campaigns. n

United Distributors hit with anti trust action by CCP

Distribution company admits fault in failing to file requisite paperwork by the deadline; may be fined by CCP unless it is able to rectify

Profit Report

The Competition Commission of Pakistan (CCP) has imposed a cumulative penalty of Rs42 million on United Distributors Pakistan Ltd (PSX: UDPL) and its related party International Brands (Pvt) Ltd (IBL) for entering into – and giving effect to – a three year non compete agreement that contravened Section 4 of the Competition Act, 2010. In a detailed order issued on 2 July 2025, the watchdog found that the pact prevented UDPL from taking up distribution of human pharmaceutical products anywhere in Pakistan between 2022 and 2025. In return, IBL had agreed to pay Rs1.131 billion to UDPL as compensation for foregoing that line of business.

The contravention came to light after UDPL itself disclosed the arrangement in a letter to the Pakistan Stock Exchange (PSX). The company admitted that it had failed to file a timely exemption application with the CCP – a prerequisite under the Act for any potentially restrictive commercial arrangement. Although management emphasised that implementation of the non compete “was (and continues to be) subject to seeking the requisite exemption”, the watchdog ruled that simply executing the agreement without prior clearance constituted an offence. Each company has been ordered to pay Rs21 million within sixty days and to modify the agreement in line with competition law.

Both firms have stated that they are reviewing the order and reserve the right to pursue legal remedies. Nevertheless, UDPL’s notice to shareholders struck an unusually contrite tone, acknowledging an “internal delay” and pledging to rectify matters by filing the exemption “at the earliest”. On the trading floor, UDPL’s share price slipped 1.6 per cent during the week but recovered some ground after assurances that day to day operations and cash flows remain intact.

Corporate Pakistan is not renowned for forthright mea culpas. When confronted with regulatory censure, listed companies typically respond with blanket denials, oblique legalese or silence until the mandatory disclosure clock forces their hand. Against that backdrop, UDPL’s direct admission of error – and its promise to regularise the paperwork – stands out.

Voluntary disclosure and acceptance of oversight are still the exception, not the norm. The conventional playbook is to appeal, litigate,

or blame a ‘misinterpretation’ of the rules. UDPL has instead front footed the issue, which may mitigate reputational damage in the long run.

The CCP usually grants concessions – such as reduced penalties – when undertakings co operate early and demonstrate genuine intent to comply.

UDPL’s approach also speaks to the growing influence of environmental, social and governance (ESG) metrics among institutional investors. Asset managers tracking the Karachi based KSE 100 and KMI 30 indices have begun screening for regulatory compliance histories. By signalling transparency, UDPL may be seeking to reassure shareholders that the lapse was procedural rather than wilful market manipulation.

United Distributors traces its roots back to 1981, when the Abdulla family – one of the country’s oldest trading dynasties – incorporated the company to serve Pakistan’s agricultural sector. What started as a distribution partner for Dow AgroSciences and FMC quickly evolved into a fully fledged agribusiness, encompassing formulation, warehousing and last mile delivery of crop protection chemicals, fertilisers, and micronutrients.

Today UDPL operates a formulation plant in Karachi, a network of provincial warehouses, and an on ground sales force that reaches more than 40,000 farmers nationwide. The company’s stated mission is to “nurture a network of 50,000 UDPL ambassador farmers” by 2030 – a goal underpinned by precision agriculture advisory services and digital trading pilots.

Financially, UDPL remains small by KSE standards – last year’s revenue stood at Rs6.8 billion – but the business boasts a lean capital structure and a double digit operating margin thanks to its asset light distribution model. The Board comprises both Abdulla family members and independent professionals, while corporate offshoots include Trax Online (e commerce logistics) and Intelligen (market research). The current Chief Executive, Asmer Beg, joined in 2021 after two decades at Syngenta and Procter & Gamble. IBL emerged in 1991 following a strategic split within the original United Distributors (UDL) empire. Tasked with broadening the group’s horizons beyond pure distribution, IBL built one of Pakistan’s largest sales and logistics platforms, servicing over 150,000 retail outlets across both pharmaceutical and fast moving consumer goods channels.

A landmark move came in 1993, when

IBL acquired the local operations of American pharma manufacturer G.D. Searle. That acquisition laid the groundwork for what is now The Searle Company Ltd, a listed pharmaceutical major in which the Abdulla family retains a controlling stake.

Over the years, IBL has diversified into energy drinks, personal care products and franchised food retail (including Dunkin’ Donuts) while retaining a core warehousing and distribution backbone. Structurally, IBL sits at the apex of the IBL Group, whose subsidiaries include IBL Operations (distribution services), International Franchises Ltd (quick service restaurants) and multiple joint ventures with multinational brands. The group employs over 9,000 people and reported consolidated turnover of Rs56 billion in FY 2024. Despite remaining unlisted, IBL’s bonds and short term sukuk are rated A+ by VIS Credit Rating Co., reflecting solid cash flows from anchor contracts with global principals.

Established in 2007, the CCP is mandated to promote competition, protect consumers and penalise anti competitive conduct.

The UDPL IBL order is the first high profile case in 2025 targeting a vertical restraint rather than traditional price fixing or deceptive advertising. The decision sends a clear signal that non compete clauses – common in mergers, joint ventures and distribution contracts – will face strict scrutiny if they restrict market entry without demonstrable consumer benefits.

The immediate financial hit to UDPL and IBL is manageable, amounting to less than 1 per cent of combined FY 2024 profits. The larger question is whether the CCP’s decision will prompt other conglomerates to re examine existing non compete provisions – particularly those memorialised years ago without formal exemption applications. With the regulator now brandishing both investigative heft and punitive teeth, Pakistan Inc. may need to clear out its legal cupboards sooner rather than later.

For UDPL, the episode is a reputation stress test. Its candid admission, coupled with a commitment to seek retrospective clearance, could mollify investors and regulators alike. Success will hinge on demonstrating that governance reforms are substantive, not merely rhetorical. As Pakistan’s competition regime matures, transparency may prove the cheapest form of compliance insurance. n

Ideal Spinning Mills shuts its looms on cost crunch

Companies further up the value chain have begun preferring cheaper Chinese cotton yarn imports, making life difficult for Pakistani yarn manufacturers

Profit Report

Ideal Spinning Mills Limited (PSX: IDSM) has become the latest casualty of the sector wide squeeze on Pakistan’s once thriving textile industry, announcing the closure of its core spinning division and the planned sale of most of the segment’s plant and machinery. The dramatic retreat, disclosed in a notice to the Pakistan Stock Exchange on Friday, will leave the company relying on its weaving and socks businesses while it waits for market conditions to improve.

In a board meeting held on 11 July 2025, directors “approved the sale/disposal of the spinning segment’s major portion of plant and machinery,” according to the regulatory filing. Management cited “unfavourable market con-

ditions” and “rising costs of operations” that have rendered the yarn manufacturing unit loss making for several quarters. Despite export rebates and an uptick in global cotton prices, local energy tariffs, high working capital costs, and subdued demand have combined to push the segment into negative gross margins. The board will now convene an Extraordinary General Meeting (EoGM) to seek shareholder approval for the asset sale and to formalise the permanent shutdown of the spinning sheds.

The decision comes just weeks after industry associations sounded the alarm over new tax measures in the federal budget and warned that “continued inaction could disrupt exports and weaken exporters’ confidence.” The conditions they flagged – tight liquidity, energy rationing, and punitive withholding taxes – have crystallised at Ideal Spinning

sooner than many expected.

Spinning is the upstream anchor of Pakistan’s US$25 billion textile and clothing chain, converting raw cotton into yarn for downstream weaving, knitting, and garmenting units. But it is also the most energy intensive, making it acutely sensitive to electricity and gas tariffs, which have risen by more than 65% in rupee terms since January 2024. Meanwhile, elevated inflation has eroded domestic purchasing power, dampening demand for yarn among local fabric producers.

Export markets have offered little respite: slowing apparel orders from the United States and Europe have cascaded up the supply chain, depressing yarn prices. According to the All Pakistan Textile Mills Association (APTMA), industry wide spindle utilisation fell below 60% in the March quarter, the lowest

since the Covid 19 lockdowns of 2020.

For Ideal Spinning, the shutdown is both a cost containment measure and a strategic pivot. Company insiders say the plant has been operating at barely half capacity for the past year, incurring losses that wiped out gains from the socks division – a unit that enjoys higher margins and a more diversified customer base.

With the spinning machinery idled and slated for auction, management expects to free up cash, cut electricity consumption by nearly 40%, and reduce the head count by about 350 workers. Severance packages are being negotiated with the Labour Department in Faisalabad. While the company has not disclosed a valuation for the assets, brokers estimate the sale could raise up to Rs1.2 billion, depending on international demand for second hand ring frames and carding machines.

Market reaction was swift: IDSM shares slid to their lower circuit at Rs28.01 early Friday trading before recovering partly to close down 3.8%. Investors fear the company could slip into a revenue trough in the short term, even as the shutdown staunches operating losses.

Founded in 1989, Ideal Spinning Mills was the flagship enterprise of the Faisalabad based Ideal Group. Over three and a half decades, it expanded from a modest 14,400 spindle set up into a vertically integrated complex comprising spinning, weaving and socks facilities. At its peak, the spinning unit boasted 34,000 spindles producing combed and carded cotton yarn for both domestic and export customers.

Yet the path has rarely been smooth. The company weathered the post MFA (Multi Fibre Arrangement) slump in 2005, the chronic energy shortages of the early 2010s, and the rupee’s sharp depreciation in 2018. Each time, management diversified downstream – first into greige fabric, then into hosiery – and invested in ISO certified quality controls to keep Western buyers on its roster.

The most recent financial statements, for the quarter ended 31 March 2025, showed a Rs91 million net loss on revenue of Rs2.4 billion, with the spinning segment accounting for the bulk of the red ink. By contrast, the socks business, which exports to big box retailers in Europe, remained profitable, cushioning the blow.

The company’s notice states that spinning operations will be “discontinued” upon shareholder approval, after which the machinery will be dismantled and sold, either piecemeal or as a going concern package to domestic or regional buyers. Banking sources say several mills in Bangladesh and Vietnam have expressed preliminary interest.

Ideal will channel proceeds into three

areas: (1) working capital relief for the weaving and socks divisions, (2) debt reduction – the company carried Rs2.7 billion in short term borrowings at end March – and (3) selective modernisation of its circular knitting machines to capture higher value export orders.

Ideal’s withdrawal underscores a broader structural shake out. Since January, at least six mid tier spinning mills – among them Kohinoor Spinning and Bannu Woollen – have either suspended operations or announced capacity cuts.

The government, for its part, has yet to respond. Textile lobbies are pressing for a regionally competitive energy tariff (RCET) and the reinstatement of previous zero rating regimes for export oriented units. Without such measures, they argue, the high cost spinning link could permanently migrate to countries with cheaper power and more stable fiscal regimes.

Whether Ideal Spinning’s decision proves prescient or premature will hinge on two variables: international cotton prices and domestic energy policy. If tariffs stabilise and yarn demand rebounds, the company could, in theory, re enter spinning by leasing modern, energy efficient frames rather than owning them outright. Management has kept that option open, noting that the board’s resolution refers only to the current plant and machinery, not the spinning business per se.

For now, however, Ideal is placing its bets on value added textiles – an ironic inversion of the traditional Pakistani narrative that begins with raw yarn and ends with finished garments. Investors nursing losses will hope the gamble pays off. For the thousands of workers whose livelihoods depend on the sector, Ideal’s closure is a sobering reminder that, in textiles as in fashion, what is in vogue today can unravel tomorrow.

Airlink’s earnings outlook slashed as mobile demand softens

Mobile phone assembler, recently a favourite of investors, has come under pressure after changes to its tax regime

Profit Report

Airlink Communication Ltd (PSX: AIRLINK) faces a sharp downgrade in earnings forecasts after a difficult nine month trading spell characterised by weaker smart phone sales and a ballooning working capital bill. In a note circulated to institutional investors this week, brokerage house Topline Securities cut its profit estimates for the Lahore based assembler distributor by 41% for fiscal year 2025 and 36% for fiscal year 2026, citing a “perfect storm” of subdued consumer demand, margin compression, and higher finance costs.

The bearish turn follows the release of Airlink’s first nine months of fiscal year 2025 results, which showed revenue

sliding 8% year on year to Rs85 billion and net profit decelerating more sharply than the market had anticipated. Management blamed an industry wide slowdown in handset turnover. Pakistan Telecommunication Authority (PTA) data underline the trend: local manufacturers assembled 26.09 million handsets in the first nine months of fiscal year 2025, down 8% on the comparable period. Analysts point to three overlapping headwinds:

1. A high base effect: fiscal year 2024 witnessed a post import restriction rebound as inventories were replenished, making year on year comparisons unforgiving.

2. An elongated replacement cycle: with global flagship launches offering incremental upgrades, Pakistani consumers are holding on to devices for longer.

3. Shrinking discretionary spend:

headline inflation, though moderating, has eroded purchasing power over the past three years, forcing households to prioritise essentials.

Against that macro backdrop, Topline now projects Airlink will close fiscal year 2025 with turnover of Rs110 billion, well below its previous forecast of Rs139 billion. The brokerage’s fiscal year 2026 sales projection has similarly been trimmed from Rs168 billion to Rs130 billion.

The revenue downdraft is only half the story. Sluggish sales have wreaked havoc on Airlink’s cash conversion cycle. Channel checks suggest the company has been compelled to extend credit terms to retailers to 40 days, up from 15–20 days previously, in a bid to defend market share. Yet payments to component suppliers continue on schedule, forcing management to lean heavily on short term bank lines.

As a result, short term borrowings nearly doubled to Rs28 billion by the March quarter, up from Rs16 billion at end September. Servicing that bulge added a sizeable chunk to finance costs, squeezing net margins already under strain from promotional expenditure. Topline forecasts borrowing levels to normalise around Rs15 billion in fiscal year 2027 once sell through stabilises, but concedes that the intervening quarters will test liquidity nerves.

In an effort to shore up long term competitiveness, Airlink has quietly acquired an eight acre plot in the Sundar Green Special Economic Zone on Lahore’s southern fringe. Construction is under way, and management hopes to shift assembly lines to the new campus by the second half of fiscal year 2026. The carrot is substantial: enterprises operating within the zone enjoy a 10 year income tax holiday and a one time sales tax exemption on imported machinery. Engineers estimate that relocating could lift net profit margins by 150–200 basis points once fully ramped.

The SEZ move aligns with the government’s localisation drive. But execution risk is real – especially if the shift overlaps with another consumer down cycle.

Despite cutting numbers, Topline retains its BUY rating, arguing that the sell off – Airlink’s shares have slid 18% since January – already prices in much of the pain. The brokerage’s discounted cash flow (DCF) target price

comes down to Rs200 a share from Rs230, but still implies a 32% upside to Thursday’s close. On the revised estimates, the stock trades on 17.7 times fiscal year 2025 earnings and 11.2 times fiscal year 2026, falling to 14.6 times at the TP.

The resulting P/E profile, while hardly bargain basement, looks tolerable relative to peers Searle and Systems Ltd, which fetch north of 20 times forward earnings. Bulls also stress Airlink’s entrenched distribution footprint and relationships with OEM heavyweights such as Samsung, Xiaomi and Tecno.

That optimism, however, is hedged by a laundry list of caveats. Topline flags five principal risks:

• Deeper than expected demand erosion if inflation rekindles or real incomes contract further.

• Import bottlenecks – already a headache in 2022 – could resurface if dollar liquidity tightens and the central bank reinstates administrative restrictions on parts.

• Rupee depreciation: the currency has held around Rs296 to the dollar this year, but a disorderly slide would inflate input costs and crimp margins.

• Rising competitive heat from newer assemblers lured by the government’s Mobile Device Manufacturing Policy.

• Technological obsolescence: failure to pivot swiftly to emerging form factors – foldables or AI centric devices – could erode brand relevance.

One catalyst conspicuously absent from Topline’s base case model is mobile phone

exports. Pakistan’s Ministry of Commerce is drafting a policy framework that could clear the regulatory smog inhibiting outbound shipments. If approvals land, Airlink – already running several international quality SMT lines – would be among the first to benefit. Even a modest export quota of one million units could add Rs6–7 billion to annual revenue, analysts reckon, materially altering the earnings trajectory.

For now, the narrative is unambiguously one of adjustment. The company that dazzled investors with record profits in fiscal year 2023 is confronting a consumer electronics cycle whose zenith may be in the rear view mirror. Yet the bones of the business remain sound: a scalable assembly platform, preferential access to global brands, and a management team with a track record of capital discipline.

The next six quarters will be pivotal. Success depends on synchronising three moving parts: stabilising domestic demand, executing a seamless factory migration, and navigating a highly politicised import regime. If management threads that needle, the current earnings wobble could be remembered as little more than a speed bump on the road to Pakistan’s first true mobile export champion.

For investors, then, Airlink offers a classic cyclical quandary: buy into weakness on the promise of secular upside, or wait for clearer skies at the cost of missing the turn. As things stand, Topline’s revised numbers suggest that patience could still be rewarded – albeit on a longer glide path than originally envisaged. n

Kohat Cement to enter the real estate development market

Manufacturer seeks to follow the footsteps of industry leader Lucky Cement, though it is unclear if it will tap the residential or commercial market first

Profit Report

Kohat Cement Company

Limited (PSX: KOHC) has announced that it will venture into Pakistan’s real estate sector by incorporating a wholly owned subsidiary dedicated to property development.

In a notice dispatched to shareholders and published by the Pakistan Stock Exchange on 11 July 2025, the Board of Directors confirmed that the new entity will “undertake real estate development and all allied works” with an initial paid up capital of Rs750 million. The company has not publicly stated what the subsidiary will focus on developing.

The disclosure marks the second time a major cement producer in Pakistan has formally carved out a separate platform for property development. Lucky Cement has been a highly successful real estate developer with its Lucky One Mall in Karachi and now Lucky Mall Lahore.

Kohat Cement’s entry into property development represents a classic case of downstream vertical integration. Cement is the single largest bulk input in most construction projects, accounting for roughly 20 percent of structural costs. By aligning its manufacturing operations directly with real estate development, Kohat can internalise its own demand, stabilise kiln utilisation rates, and hedge against cyclical slowdowns in the standalone cement market.

From a supply chain standpoint, the syn-

ergies are intuitive. A captive development arm guarantees a base load off take for the parent’s clinker, while the developer subsidiary secures consistent input at cost plus pricing.

There are, however, execution risks. Real estate is capital intensive, subject to lengthy approvals, and exposed to sharp swings in demand tied to interest rate movements and consumer confidence. While Pakistan’s urban housing deficit – estimated at 12 million units by the World Bank – creates a structural opportunity, project delays and liquidity mismatches have historically eroded returns for new entrants.

Pakistan’s cement manufacturers already enjoy some indirect exposure to property via bulk supply contracts. The dedicated subsidiary model raises the stakes: Kohat Cement will now carry land bank acquisition costs, development expenditures, and marketing risk on its own books. Governance specialists will be watching related party transactions, particularly the transfer pricing mechanism for cement supplied to the subsidiary, to ensure minority shareholder protections remain intact.

Founded in 1980 under the auspices of the State Cement Corporation, Kohat Cement was privatised in 1992 and subsequently acquired by the Saifullah family, one of Khyber Pakhtunkhwa’s most prominent industrial groups. The company operates an integrated plant located 70 kilometres south west of Peshawar, strategically positioned to serve both the northern and central regions of Pakistan as well as export markets in Afghanistan.

Starting with a single 500 tonne per day

wet process line, Kohat Cement has undergone four major expansion phases. The most recent, commissioned in 2023, added a 7,800 tonne per day dry process kiln equipped with waste heat recovery. Total installed clinker capacity now stands at 6.2 million tonnes per annum, placing KOHC among the country’s top five producers.

The company’s product portfolio includes Ordinary Portland Cement, Sulphate Resistant Cement, and Low Alkali Portland Cement, catering to residential, infrastructure, and specialised oil well markets. A dedicated research division collaborates with universities to develop low carbon blended cements in line with global decarbonisation trends.

KOHC has also been a reliable dividend payer, distributing 40–60 percent of earnings in cash over the last five years.

Kohat Cement’s foray into property development embodies the broader diversification wave sweeping Pakistan’s industrial sector. If executed prudently, the strategy could unlock a virtuous cycle: integrated project pipelines ensuring steady cement demand, lower construction input costs enhancing project margins, and a new asset class augmenting earnings visibility. Conversely, missteps in land acquisition, regulatory approvals, or project delivery could expose the group to unfamiliar hazards and dilute its historically stable returns.

For now, investors appear encouraged by the board’s methodical approach – ring fencing the new business in a separate corporate vehicle, maintaining a debt light capital structure, and leveraging existing cash reserves. n

A nervous hush has fallen over policy circles as Pakistan’s circular debt resolution approaches its defining moment

By Ahtasam Ahmad and Ahmad Ahmadani

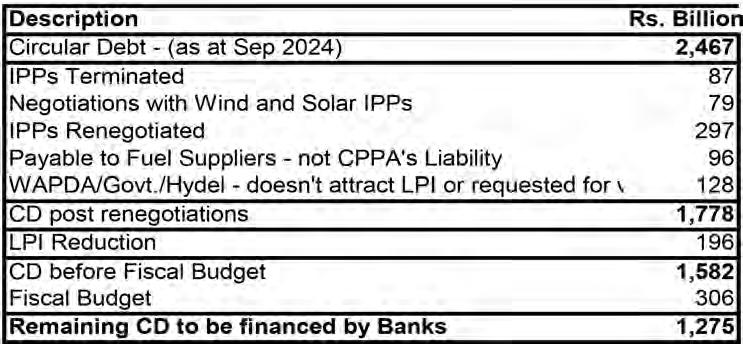

Just months ago, Pakistan’s government was celebrating what appeared to be a breakthrough in the country’s intractable circular debt crisis. The fanfare reached its peak in March w hen a special government taskforce \ announced it had secured Rs1.275 trillion in below-market financing from commercial banks, a deal that promised to finally untangle the web of unpaid dues choking the power sector. The cabinet followed up by approving the financing arrangement to clear outstanding payments across the entire power sector supply chain.

But the celebrations have given way to an uncomfortable silence. News reports now suggest the much-vaunted solution is hitting unexpected snags, with some Independent Power Producers (IPPs) refusing to accept the discounted payments that were central to the government’s strategy. The roadblocks underscore a troubling reality: Pakistan’s circular debt problem has proven remarkably resilient to previous reform attempts.

created a perfect storm in Pakistan’s power sector. High power generation costs have severely undermined DISCOs’ ability to effectively collect revenues and manage their operations, creating a persistent gap between costs and collections.

Compounding this problem are the chronic issues and delays in tariff determination, which have left the sector struggling to maintain financial equilibrium. The situation is further exacerbated by high transmission and distribution losses, coupled with poor revenue collection by the DISCOs, which have steadily widened the funding gap beyond sustainable levels.

The government’s partial and often delayed payment of tariff differential subsidies has added another layer of complexity to the sector’s financial woes, while high borrowing costs for PHPL and expensive late-payment penalties on CPPA-G’s payables have created an additional burden that seems almost impossible to overcome.

In Pakistan’s power market, consumer-end tariffs are deliberately set below actual electricity supply costs, with government subsidies attempting to bridge the gap. However, as costs persistently exceed revenues, the sector’s financial deficits have averaged an alarming 2.8% of GDP during FY14–FY24.

Source: Asian Development Bank

As the latest effort to resolve the crisis appears to hit a roadblock, it’s worth examining how Pakistan’s power sector became trapped in this cycle of unpaid dues, why past solutions have failed, and whether the current approach can succeed where others have not.

Making of the crisis

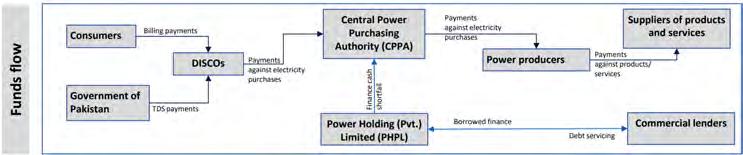

Pakistan’s power sector struggles with a persistent circular debt problem rooted in a complex web of unpaid obligations that has grown increasingly intricate over the years. At its core lies the unfunded outstanding liability of power distribution companies (DISCOs) and K-Electric (KE) to the Central Power Purchasing Authority-Guarantee (CPPA-G), a situation that has become more precarious with each passing year.

When DISCOs fail to clear their dues to CPPA-G, it creates a cash shortfall, prompting Power Holding Private Limited (PHPL) to borrow funds to cover CPPA-G’s liabilities. This cycle of delayed payments represents the accumulated circular debt in the country.

The growth of this circular debt can be attributed to five fundamental factors that have

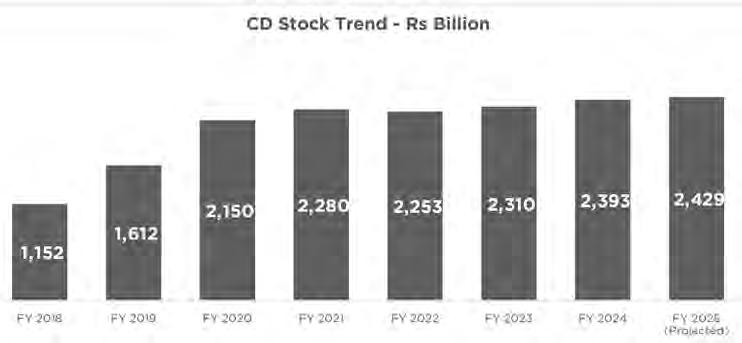

By June 2024, the total circular debt reached Rs2.4 trillion, equivalent to 2.3% of GDP, representing an almost 50% growth from FY19. This rapid acceleration in debt accumulation began in earnest in 2018 with the signing of “take-or-pay” contracts for imported coal and gas power plants, a decision that increased capacity payments by 50% and exposed the country to the volatile whims of international fuel prices, a vulnerability that became painfully apparent during the global energy crisis of 2022.

The implications of these structural energy sector problems extend far beyond the power industry itself, creating a complex web of challenges that affect Pakistan’s entire economic landscape.

The macro and micro fallout

At the macroeconomic level, the impact is particularly severe in three critical areas. First, the combination of unreliable energy supply and soaring costs has dealt a significant blow to industrial operations and export competitiveness. Consumer tariffs have increased more than sevenfold between 2007 and 2024, with additional surcharges for PHPL liabilities and late payment penalties add-

ing to the burden. This situation has become even more challenging under IMF conditions that require increased consumer tariffs to curb circular debt accumulation, creating an almost impossible balance between fiscal sustainability and consumer affordability.

The second major macroeconomic impact stems from the power sector’s massive drain on fiscal resources, which has effectively diverted crucial funds from vital development projects. Power sector subsidies have dominated government subsidy outlays, averaging over 80% during FY13-FY24.

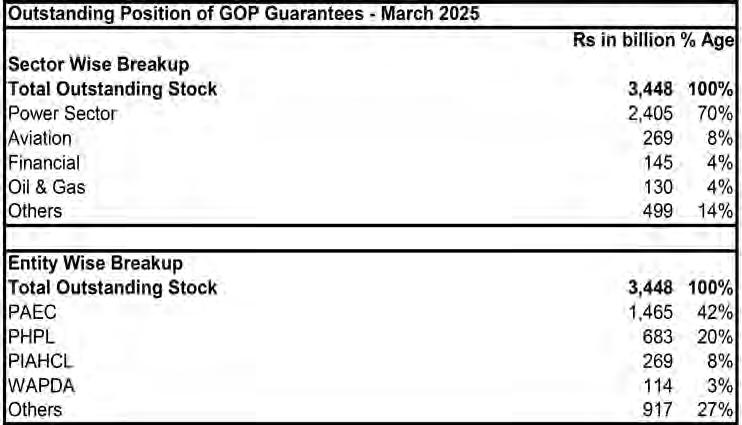

This concentration of subsidies in a single sector has severely limited the government’s ability to invest in other critical areas such as education, healthcare, and infrastructure, creating a development deficit that could take generations to overcome. The government’s guarantee exposure presents an equally concerning picture, with the power sector accounting for 70% of the total Rs3.45 trillion guarantee stock as of March 2025, where PHPL alone represents one-fifth of the total guarantees.

At the microeconomic level, the repercussions ripple through the financial sector and corporate landscape with far-reaching consequences. Banks’ high exposure to energy sector loans, has effectively crowded out private sector borrowing for productive activities, stifling economic growth and innovation. Further, the quantum of government guarantees extended to the power sector means that priority sectors like SMEs and agriculture remain deprived of the necessary guarantee cover, which could have been a possible growth catalyst for these sectors.

The accumulation of circular debt particularly strains energy supply chain companies’ financial health, many of which are listed on the stock exchange and have retail investors, affecting their operational efficiency and investment capacity. Pakistan State Oil (PSO) serves as a prime example of this predicament, carrying power sector receivables of billions and relying on costly bridge financing to maintain operations. This situation has created a

cascade of financial inefficiencies, as companies throughout the supply chain face working capital constraints and increased financing costs.

The circular debt problem has also created significant challenges in financial reporting, forcing regulators to find creative solutions to manage the situation. Securities and Exchange Commission of Pakistan (SECP) has deferred the applicability of the International Financial Reporting Standard (IFRS) 9 until December 31, 2025, for financial assets directly / ultimately due to the government of Pakistan, in response to the outstanding circular debt.

The government’s plan

The government’s roadmap to resolve this long-standing issue encompasses multiple fronts: terminating IPP contracts, renegotiating terms with renewable projects and other independent power producers, securing waivers from state-owned generation companies (GENCOs), eliminating Late Payment Interest (LPI) surcharges, and injecting fiscal resources.

At the heart of this strategy lies the

recently secured bank financing, a Rs1.275 trillion arrangement that promises to fundamentally reshape the sector’s cost structure. The new financing will replace expensive PHPL borrowing at KIBOR+2% and IPP payables carrying markup rates as high as KIBOR+4% with significantly cheaper debt at KIBOR-0.9%. This refinancing alone is projected to generate annual savings of Rs200 billion.

The disbursement plan allocates Rs683 billion toward retiring PHPL liabilities, Rs280 billion for nuclear plants, and Rs220 billion for RLNG-based IPPs. The remaining Rs720 billion gap will be addressed through renegotiated IPP terms and waivers granted to stateowned hydel plants.

To fund this restructuring, the government has introduced a surcharge of Rs3.23 per kilowatt-hour, an iteration of the previous levy that covered only interest costs, as this new charge will service both principal and interest repayments. The plan also incorporates a fiscal allocation of Rs250 billion earmarked in the FY26 budget to support the restructuring process.

Based on country’s projected electricity sales, the Rs3.23 per unit surcharge is projected to generate approximately Rs342.8 billion annually. After covering the new arrangement’s annual financing costs of Rs138.75 billion, this leaves Rs204.1 billion available for principal repayment. If this surplus is consistently applied to debt reduction, the government could potentially clear the entire obligation within six years, though the actual timeline will depend on prevailing KIBOR rates, which could either accelerate or delay the repayment process.

The financing consortium spans Pakistan’s banking sector, including major institutions such as Meezan Bank, Habib Bank Limited, National Bank of Pakistan, Allied Bank Limited, United Bank Limited, MCB Bank Limited, and eleven other participating banks ranging from conventional lenders to

Islamic banking institutions.

The urgency of this refinancing becomes apparent when considering that some of the PHPL debt dates back to 2012 and has already been rolled over four times and restructured multiple times.

However, a significant hurdle remains: securing agreement from all Independent Power Producers to waive late payment interest charges, including crucially important projects under the China-Pakistan Economic Corridor (CPEC). Recent reports suggest the government has taken a firm stance, indicating that funds cannot be disbursed unless CPEC projects agree to discounts on their outstanding payments, a critical condition given that a substantial portion of the loan is earmarked for CPEC-related energy projects. However, these reports remain unverified by official sources.

Déjà vu

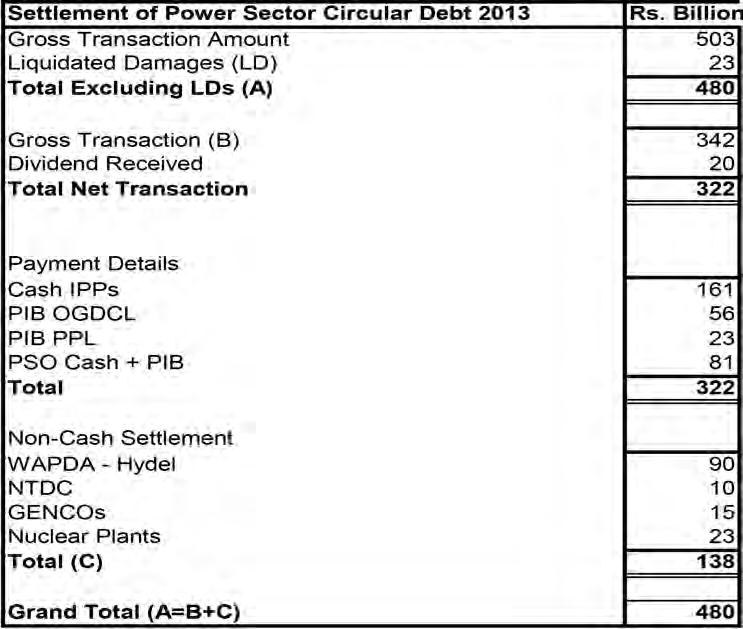

This is not the first time the government has turned to debt markets to tackle the circular debt crisis. The precedent was set in 2009 with the creation of PHPL, a Special Purpose Vehicle designed to park the government-owned power sector’s long-term debts. At that time, the circular debt burden stood at approximately Rs300 billion. To clear these accumulated dues, PHPL raised Rs85 billion through Term Finance Certificates (TFCs), distributing the funds among oil and gas public sector companies, Independent Power Producers, and banks to settle outstanding obligations to Distribution Companies (DISCOs).

The arrangement also involved transferring existing loans totaling Rs141 billion, Rs80 billion from NTDC, Rs37 billion from WAPDA, and Rs24 billion from DISCOs, onto PHPL’s books.

The relief proved temporary. Just four years later, the circular debt had regenerated to such an extent that the government was forced to intervene again, this time clearing Rs480 billion in accumulated dues to power producing entities. This second bailout required tapping

debt markets through Pakistan Investment Bonds (PIBs), demonstrating that the structural issues driving circular debt formation remained unaddressed.

What follows?

Beyond debt clearance, Pakistan has launched comprehensive structural reforms targeting the root causes of circular debt accumulation. The strategy is grounded in the acknowledgement that sustainable resolution requires fundamental changes to how the power sector operates.

The privatization drive leads to this transformation. Six Distribution Companies (DISCOs) will be privatized, starting with IESCO, GEPCO, and FESCO by end-December

2025, while three others will receive private management concessions. Early results are promising: power sector losses dropped by Rs191.2 billion in fiscal year 2024-25, falling from Rs590.9 billion to Rs399.7 billion. Merit-based appointments to DISCO boards replaced political favoritism, boosting recovery rates from 92.4% to 96.6% and recovering Rs11 billion worth of stolen electricity.

Transmission reforms are equally critical. The National Transmission and Dispatch Company (NTDC) will be split into three specialized entities: ISMO, EIDMC, and NGC, by end-December 2025 to improve efficiency and governance.

Market-based solutions are also in the works, with the Competitive Trading and Bilateral Contract Market (CTBCM) allowing bulk consumers to choose suppliers, starting with 800 MW capacity to drive down wholesale prices.

The government has also adopted a more disciplined approach to capacity expansion, refusing new additions without corresponding transmission infrastructure and full utilization of existing plants, a departure from past practices that fueled the crisis.

However, success depends on sustained political will to implement potentially unpopular reforms across multiple electoral cycles. The stakes are high: failure to permanently resolve circular debt risks not only the power sector’s viability but Pakistan’s broader economic stability. n

Legal battle casts shadow on cement recovery

The industry has kept itself afloat despite consistently falling domestic demand. Could an unfavourable verdict change the shape of the industry forever?

Profit Report

A legal battle that began nearly a year ago between the Punjab Government and the province’s cement manufacturers has reached its final stage: wait and watch.

The dispute began when the Punjab Government decided it was going to peg the rate of royalties paid by cement manufacturers to the provincial government at 6% of ex-factory price net of sales tax and excise duty. You see when cement manufacturers extract raw materials, they also have byproducts such as limestone. These products are sold on the market, and the provincial government takes a cut.

This year has proven to be a tough one for the cement industry. Cost for manufacturers has increased because governments in both KP and Punjab have decided to raise their royalty rates on these byproducts. KP, for example, raised their royalty from Rs 250 per tonne to Rs 350 per tonne. While this is a big jump, the Punjab government’s new formula would mean that the royalty would be somewhere between Rs 1000-1500 per tonne.

It is a story this publication has covered earlier as well. While the details of the legal battle and its impact on different cement manufacturers is important, and we will get into what has happened since our last article, it is worth looking at the larger context surrounding the cement industry and the impact of the ongoing legal battle on its shaky recovery.

Export oriented

The cement industry in Pakistan has faced a tough road over the past few years, with demand stagnating and domestic sales on a downward trend. The fall in demand was a natural consequence of the high inflation Pakistan saw from 2021-203. Rising costs don’t exactly foster the kind of confidence in investors to build high rises, and people generally tend to build fewer houses when their purchasing power is evaporating into thin hair.

The industry, however, has managed to stay afloat by focusing on growing their exports. As pointed out in a recent report, a combination of strong pricing power and a disciplined approach to cost has helped them in looking outwards for their sales. Just look at the sector’s performance in 2025. Cement sales grew overall by 2% compared to last year. On the surface this seems miniscule, but look deeper and you will see there was actually a decrease in domestic sales. It is a decrease that has been seen every year for the past few years. But the overall growth in sales clocked in at 2% because exports surged by 30%, making up 20% of all total sales. This is a big shift considering exports were a relatively small part of the overall sales just a few years ago. In 2022, exports made up only 10% of the sales. By 2024 they had increased to 16%. In the face of weak domestic demand, cement manufacturers found alternative markets abroad, which has proven to be a smart move. It’s an approach that has helped them weather the storm as local demand dwindles. As a result, cement companies managed to maintain profitability by raising prices, even as domestic sales faltered. The past five years tell a story of rising prices and falling sales. Since 2021, cement prices have more than doubled.

A recovery on the cards?

There is clearly reason for cautious optimism within the cement industry. Domestic demand might have been weak in the past few years, but it could see a revival as economic indicators improve. Even if that does not happen, there is no reason why exports would fall from where they have been recently. The growing international market for Pakistani cement could

continue to provide a steady source of revenue, even if domestic sales remain sluggish. With coal prices under control, cement manufacturers are in a better position to manage costs and reduce risks. The next few years will be pivotal. The cement industry has shown remarkable adaptability in the face of adversity, but its future hinges on the broader economic recovery and the success of government policies aimed at reviving construction and real estate. For now, though, the industry is taking a wait-and-see approach.

The hanging sword

Of course, there is a larger issue that might shake up the industry from the inside. Pakistan’s 79-million-tonne cement industry is geographically split into two informal trading blocs. The northern bloc – encompassing Punjab and Khyber-Pakhtunkhwa – competes fiercely for the populous central and up-country markets of Lahore, Gujranwala, Islamabad–Rawalpindi and Peshawar. The southern bloc, anchored in Karachi and adjoining Thatta district, largely serves Sindh and Balochistan and exports through the ports.

Historically, freight economics already gave Khyber-Pakhtunkhwa mills a freight advantage into the upper-Punjab districts adjoining their plants, while Punjab mills enjoyed scale economies in the densely populated central zone. The royalty ruling adds a second wedge: a Khyber-Pakhtunkhwa producer trucking clinker 150–200 km into Punjab can now undercut a local rival by Rs25–30 per bag and still pocket superior margins. Analysts fear this could ignite a fresh round of price competition just when the industry is digesting its largest capacity expansion cycle in a decade.

When the Punjab Government first went to the Lahore High Court, they were granted a stay order which kept them in business for the time being. When the court ruled against them a few weeks ago, there was a bit of a scare. Many of the companies in Punjab had submitted bonds as surety in exchange for the stay order and the Minerals Department could now cash those in. That is why, even though there were concerns the Supreme Court would be uninterested in getting too involved in provincial matters, they had no choice but to go to the superior court.

The SC granted them another two week stay order, but those two weeks expired a few days ago. For now, there seems to be a lull with no clarity over what will happen next. What we do know is that if a ruling comes immediately against the Punjab manufacturers, there will be an immediate impact. Just look at what happened when the Punjab Government first reevaluated their royalty formula. In 2024, amid looming fear of a further hike in the price of cement after an increase in royalty rates on raw materials by the Punjab government, domestic sales shrank by 11.41% to 2.463 million tonnes in July from 2.78m tonnes in the same month in 2023.

Some industry stakeholders have warned that if the royalty remains tied to cement prices, margins for Punjab-based plants could come under acute pressure. The fear is that even one aggressive move from a lower-cost Khyber Pakhtunkhwa producer could erode profitability for its rivals by several hundred basis points in a single quarter.

The legal battle has now shifted to the Supreme Court, which may ultimately determine whether the Punjab government’s royalty formula constitutes a sales tax—potentially encroaching on federal jurisdiction—or remains a valid provincial levy under the Mines Act. For now, the status quo remains the new SC granted stay order. This has swiftly neutralised the problem for the time being. As the next hearing looms, manufacturers and investors alike await clarity on whether the current two-speed pricing environment in Pakistan’s northern cement market will be institutionalised or neutralised.

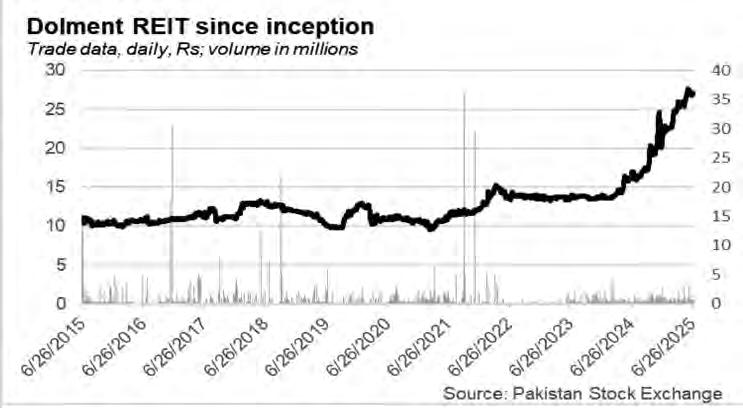

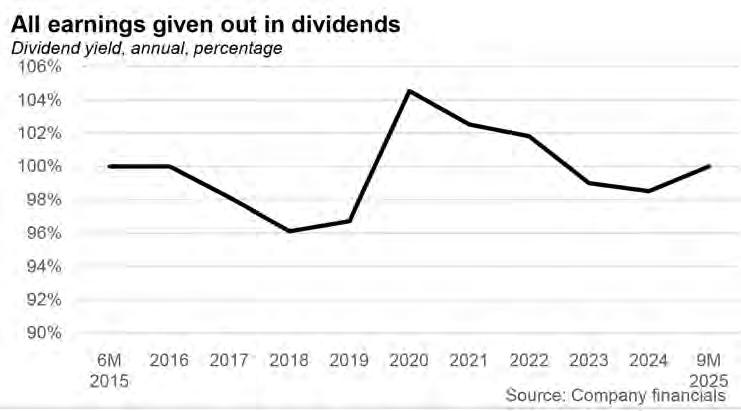

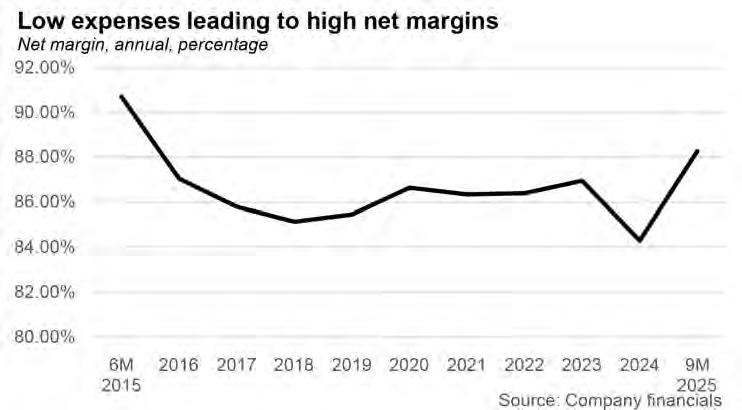

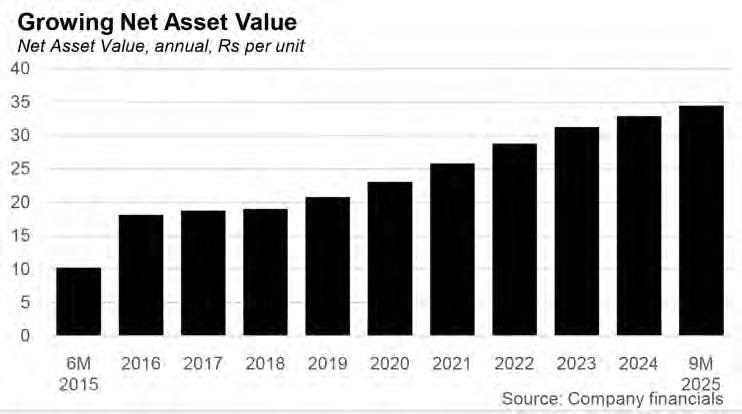

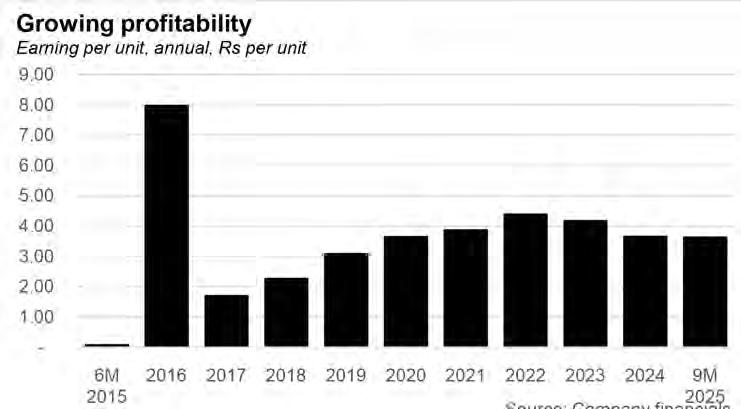

Dolmen REIT shines through

The performance of Dolmen REIT is going from strength to strength and the recent year might be its best one yet

By Zain Naeem

Drive past the Tomb of Abdullah Shah Ghazi and one cannot ignore the building that slowly rises from nowhere. As the smell of the ocean starts to take over and the sound of waves crashing fills the ears, the view is dominated by Dolmen Mall Clifton and the Harbour Front property. It looks like the last remnant of the City of Atlantis as it towers over the horizon. Just like the building seems to rise out of the sea, the stock performance of the company has seen a similar towering rise in its price in recent years. With the company expected to have its best year in its history, it can be expected that this rise will continue for the foreseeable future.

The stock rally for the generations

In recent years, the stock market has been able to show a rally with little signs of abating. Just go back 3 years and you would see something much different. The index was trading at just around 45,000 points and investors were booking losses as share prices were stagnant for a long period of time. The heady times of 2017 had long subsided and investors were skeptical to invest. Any signs of recovery had been decimated due to the pandemic and it seemed like a miracle would be required before things could change.