12 The Battle of the Sugar Barons has yielded its first victim

19 Brace for impact: The grid is in a nose dive

22 Coffee nation

26 Bank Makramah sells headquarters building in Karachi for Rs12 billion

27 Gul Ahmed profits dragged down by energy costs, declining US and UK sales

29 Mari profits rise on the back of increased production

30 Mughal profit outlook dims on lower copper sales

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

Always the pitch deck, never the unicorn

Pakistan may have carved out some space for itself in the global tech landscape, but what is stopping it from realising its full potential?

By Nisma Riaz

With the advent of the current digital global economy, startup ecosystems around the world have evolved into more than just hotbeds of innovation. Now, they are the benchmarks of economic competitiveness and resilience. The StartupBlink Global Startup Ecosystem Index 2025, analysing data from over 1,000 cities and 100 countries, maps the changing patterns of entrepreneurship.

While traditional leaders like the United States face stagnation, emerging players such as Singapore, Saudi Arabia, and to some extent even Pakistan, are heavily focused on technological innovation, by proxy, redrawing the global tech landscape.

The United States may be retaining the top spot in global rankings, however, its influence is waning. The country’s ecosystem growth rate is just 18.2%, with a notable decline in the number of cities represented in the global top 1,000. Meanwhile, the Asia-Pacific and MENA regions are gaining ground.

Singapore, now ranked fourth globally, posted an impressive 44.9% growth rate. Saudi Arabia climbed 37 spots to reach 38th place, fueled by its Vision 2030 reforms. China, stable at 13th, is

seeing city-level growth exceeding 30%.

These shifts hint to a broader decentralisation of global innovation. Pakistan, ranked 72nd in 2025, dropping one spot from 2024,

illustrates a story of wasted potential and a litany of opportunities.

Baby steps towards betterment

Despite its slight drop in rankings, Pakistan continues to lay the groundwork for a robust startup ecosystem. With a population exceeding 240 million, 60% under the age of 30, Pakistan is primed for entrepreneurial growth. According to Startup Blink’s Global Startup Ecosystem Index 2025, Lahore is showing the strongest momentum, with a 31.5% rise in rankings, followed by Islamabad with a 15.9% increase. Karachi, the highest-ranked Pakistani city at 190th, has slowed, indicating the need for renewed investment and support.

According to the same report, in 2025, Pakistan is holding its first 5G spectrum auction, a milestone for digital infrastructure. Easypaisa’s licensing as the first digital retail bank and the establishment of Special Technology Zones (STZs) further reinforce the country’s ambitions. These STZs offer tax exemptions, custom duty relief, and foreign exchange flexibility to attract tech investments. Government initiatives such as the Ignite National Technology Fund and the Pakistan Startup Fund aim to reduce risk for early-stage startups. Legal frameworks introduced through the Companies (Amendment) Act 2021 and the Digital Banking Policy are helping create more business-friendly conditions. Pakistan’s recognition as “Tech Destination of the Year” at GITEX 2024 highlights its growing international presence.

However this doesn’t mean that challenges do not persist. Despite over $1 billion raised in the past decade and more than 525 startups registered by April 2025, Pakistan has

yet to produce a homegrown unicorn. Startups like Airlift shutting down underscore the system’s fragility, and macroeconomic volatility, unclear tax policies, and infrastructure gaps continue to constrain progress.

The two sides of Pakistan’s infrastructure

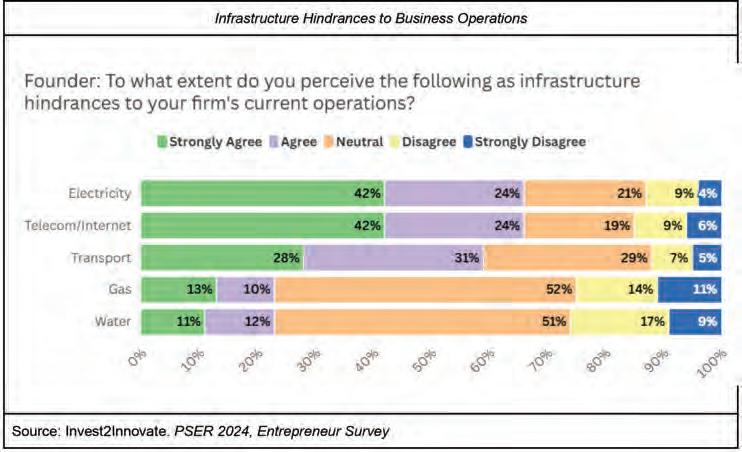

According to data presented in invest2innovate’s Pakistan Startup Ecosystem Report 2024, Pakistan’s technology infrastructure is both its bedrock and bottleneck.

Ranked 125th on the Global Innovation Index (GII) in 2024, the country lags behind regional peers. Internet connectivity remains unreliable, with 47% of the population offline, and fiber teledensity just 0.45%. Of the seven submarine cables connecting Pakistan, two are non-functional, creating vulnerability, making infrastructure a bottleneck hindering faster growth.

Pakistan’s fiber network, though spanning 164,000 km, connects only 1.1 million homes and fewer than 11% of cellular towers. Frequent internet disruptions, often politically driven, cost the economy $238 million in 2023. More recently, widespread speed throttling and ambiguous government statements regarding surveillance have further damaged trust.

Electricity infrastructure is equally fragile. While the generation capacity is 46,000 MW, the transmission grid can handle only about 23,000 MW. Load-shedding is common, and costly stopgap measures such as emergency LNG imports have depleted foreign reserves, necessitating IMF assistance.

On the other hand, telecom improvements have been modest. By late 2024, mobile subscriptions reached 193 million, and 3G/4G penetration increased. Telecom providers are expanding into digital payments and smart tech, while fiber broadband remains limited to a few urban players like Nayatel and Cybernet.

Transport infrastructure, crucial for logistics startups, is also underdeveloped. Despite 96% of freight moving by road, only 2.4% of the road network comprises highways, which handle 80% of the traffic. Aging trucking fleets and poor cold-chain infrastructure lead to spoilage of up to 40% of perishable goods. While startups like Truck It In and BridgeLinx are innovating in this space, rail freight remains underutilized.

While the country’s infrastructure is far from supportive, there has been a rise in tech and entrepreneurial support systems over the years.

National events like the P@SHA ICT Awards, Shell Tameer Awards, and the Pakistan Startup Cup have played key roles in highlighting innovation, while tech conferences like 021Disrupt and Future Fest provide networking and investor exposure.

From a single incubator at NUST in 2005, Pakistan now has nearly 90 incubators and accelerators, including the NIC network

backed by Ignite. NICs in cities like Islamabad, Lahore, and Quetta have supported 1,300+ startups, created over 126,000 jobs, and facilitated $79 million in investment. Sector-specific initiatives like NICAT (for aerospace) and agritech incubators in Faisalabad show a move toward targeted support. Hybrid spaces like COLABS and Kickstart now double as coworking hubs and investor platforms, showing the growth of tech support infrastructure and superstructure in the last two decades.

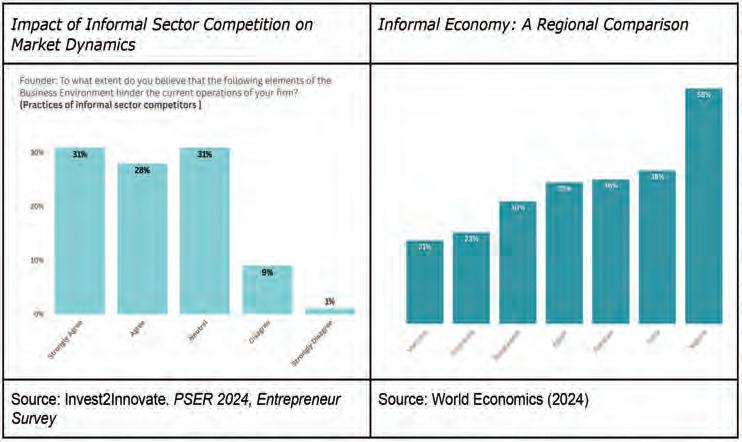

Yet, challenges remain. Many incubators use standardised cohort models with limited customisation. i2i data shows that only 27% of investors funded incubator graduates within two years. Founders value community and

mentorship, but few feel equipped in branding, legal strategy, or investor negotiation. Access to expert consultants and advisors also remains limited.

Market and the informal economy

Pakistan’s informal economy, estimated at 36% of GDP, presents a dual-edged sword. While informal trade fosters entrepreneurship and enables access, it also undermines formal sector growth and tax compliance. Retail is highly fragmented, with over 2.5 million small shops and minimal use of consumer credit.

High inflation, cash-dominated transactions, and complex distribution networks hinder scaling. Yet, companies like PostEx are creatively solving these issues by combining logistics and fintech. Their model of offering upfront payment on COD orders helps improve liquidity and gathers data to drive smart lending decisions.

The global startup ecosystem is becoming multipolar. Cities like Medellín, Riyadh, and Ho Chi Minh City are emerging rapidly. Sectors such as Foodtech, IoT, and Green Energy are defining the next wave of innovation. Pakistan, with strategic investments in AI, climate tech, and digital transformation, has a chance to lead in these areas. According to PwC, AI could contribute 5.6% to Pakistan’s GDP by 2030. A Google report suggests that embracing digital transformation could unlock up to Rs 9.7 trillion in economic value.

Pakistan’s story is one of promise tempered by challenges. The infrastructure gaps are real but so is the entrepreneurial spirit. If regulatory clarity, investor readiness, and digital infrastructure are prioritised, Pakistan could potentially rise from regional underdog to global competitor. n

The Battle of the Sugar Barons has yielded its first victim

The PSX has mandated that Haseeb Waqas Sugar Mills needs to buy back its shares. For once, the sugar manufacturer has decided to let up

By Abdullah Niazi

The azan rings out from minarets of Masjid Sakina tul Sughra as the village of Jatoi in Muzaffargarh begins to stir with the break of day. Jatoi is one of the lucky towns in the Punjab that has one canal of the Indus river’s irrigation system flowing through it. This small remnant of British Imperialism makes the farmland surrounding Jatoi rich and fertile.

The canal in Jatoi also makes it ideal for water guzzling sugarcane. Perhaps no crop has done as much damage to Pakistan as sugarcane. It has wasted water, fostered bad habits and sugar dependence within the country, and has created what is perhaps the single most influential lobby in the country. It is also why the once serene, rural splendor of Jatoi now has an ugly, gray, concrete monstrosity in its midst.

The long shadow cast by the mournful structure of the Haseeb Waqas Sugar Mill represents the worst of Pakistani agriculture, politics, and industry. The plant was first set up in Jatoi in 2015. The idea was to have a vertically integrated setup that would be involved in every aspect of sugar manufacturing from farming to harvesting and refining it. What happened instead was a protracted legal battle that pitted Pakistan’s most powerful political factions against each other.

The Hasseb Waqas Mill is owned by the extended Sharif family. It is one of the many mills that the Sharifs have owned either directly or indirectly since the 1990s when they first came to power. Founded in 1992, Haseeb Waqas Sugar was initially located in Nankanasahib. It was the shift of this mill from Nankanasahib to Jatoi that has been a major bone of contention. The political ramifications, legal battles, history, and eventual resolution of this conflict has been covered by Profit before.

It was a business battle fought along political lines and eventually settled along political lines as well. In the decade since Haseeb Waqas Sugar moved from Nankanasahib to Jatoi, its financials have only suffered. The company has seen dips in its stock prices, farmers are knocking at their doors claiming the mill owes them hundreds of millions of rupees, and their operations have faced

consistent losses. With the political conflict largely settled and major players willing to cooperate rather than make each other feel the heat, it might be time for Haseeb Waqas Sugar to make a dignified exit.

Sugar’s bitter conflict

Pakistan’s sugar industry is possibly the most powerful and influential lobby in the country. Almost all of the 91 sugar mills in the country are owned by household name politicians and their families, all of whom belong to different political parties. Almost every sugar mill in the country has at least an MPA with some shareholding in it. Of course, all of these mills are owned by politicians from different political parties.

Historically, these politicians have worked together to promote their common interests. In August 1947, there were only two sugar factories in the newly minted state of Pakistan. Most of the sugar mills set up in the colonial era were on the Indian side of the border, and the two in Pakistan were not nearly enough to meet domestic supply.

This was an opportunity. For the first few years of the country’s existence sugar had to be imported which was a major drain on a new state with very little trading power. At the same time, sugar was a high-demand commodity in the subcontinent and plenty of sugarcane was grown in the new state. The 1947-48 production numbers for sugarcane in Pakistan were over 54 lakh tonnes. Nearly 75% of this sugarcane was grown in the Punjab. Since at the time the country’s landed elite were also its political elite, it became clear that many of these landowners that were growing sugarcane would now set up sugar mills, process the sugar and make more money.

The experiment was successful. By 1962 there were six mills in the country and in 1964 the Pakistan Sugar Mills Association (PSMA) had been established and almost every single sugar mill in the country had a member of parliament on its board of directors. The interests of the sugar industry were disproportionately represented in the legislature and the political patronage that came with this allowed the industry to boom. According to a report of the Competition Commission of Pakistan, the number of mills increased to 20 by 1971 during a period when cane cultivation was

incentivized in Sindh through establishment of sugar mills. The size of the industry further increased to 34 by 1980.

Enter the Sharifs

Up until the 1990s, the sugar business was pretty simple. The landed elite would set up mills and feed them with raw sugarcane that they often grew on their own lands. But there was a new political force on the scene by this point. Nawaz Sharif first became Chief Minister of Punjab in 1985, completed his five year term and graduated to Prime Minister in November 1990. Mian Nawaz was the first major political force in Pakistan to not come from the landed elite. His industrialist background did not deter him or his family from getting in on the sugar business.

In the 1990s, the Sharif family was prominent in entering the sugar mill business. They started with the Ramzan Sugar Mills and continued on to establish Ittefaq Mills and many others. Haseeb Waqas Sugar Mill was set up by relatives of the Sharifs in 1992. One of the common accusations levelled by the political opponents of the Sharif Family is that they helped their extended family in setting up these mills by giving them favours and licences. There was a crucial difference however. In the beginning, many of the mill owners had also been farmers. The Sharifs were hard-boiled industrialists with not a single green thumb in the entire family. This was also part of a rising trend of non-agriculturalists with political clout entering the country’s sugar industry. If one were to believe what was said in those days, the annual profit from one sugar unit in that period used to be more than enough for setting up a new one. From 34 mills in 1980, to 41 mills by 1987. By the time the Sharifs entered the picture, the number of mills went from 41 in 1987 to 91 by the mid 2000s.

Of course, the problem was that most of this was a bubble. Pakistan’s sugarcane was uncompetitive. Production was low compared to the global average yields and so was sugar extract percentage. This meant imported sugar could actually compete with the local product. Despite this, through political patronage and protection through tariff and non-tariff restrictions on imports and generous subsidies, the sugar industry continued to thrive. Government policies placed tariffs on imported sugar

and even banned it while giving subsidies to local sugar mills. As a result, the number of mills grew and so did the number of farmers growing sugarcane.

Eventually, however, the party had to end. Once Pakistan reached 91 mills, the government had to impose a ban on new licenses for mills because of the excess capacity in the existing mills and pressure from imported sugar. This was a point of diversion. There was no longer enough for everyone to go around, and the conflicting business interests of the high-powered owners of these mills began to materialise like their political conflicts.

The woes of Haseeb Waqas Sugar Mill

In the midst of all this was the Haseeb Waqas Sugar Mill. Established in 1992, the mill was situated at Merajabad in Nankana Sahib in central Punjab. The company saw good profits in the initial days, but the weakening returns of Pakistan’s sugarcane crop meant they kept fluctuating between profits and loss based on the crop yield for the year. In years where sugar crushing was ample, the company earned profits. In years of low yield, losses were seen.

The dip in the performance of Haseeb Waqas also has links to the economic reality that the company was operating in as well. As we have mentioned, up until the early 2000s, there was no restriction on a sugar mill from being established. This caused a glut of factories being set up near Muzaffargarh which was previously the cotton belt of the country. As the number of mills rose, there was a risk that the water guzzling crop could eat into the cotton production of the country. Pakistan’s largest exports come from textiles which rely on cotton. Something had to be done in order to protect this crop. On top of this, when there were so many mills in the area, sugarcane farmers had more buyers to sell to and could get higher prices.

Due to this, the Government of Punjab decided that no new sugar mills could be established in this region. Another reason for the restriction was that mills already established in the Southern region of Punjab wanted to protect themselves from mills from other areas. In the early 2000s, sugar cane production was falling in Central Punjab as water scarcity was rising. It was lucrative for companies in the centre to move to the south in order to get better access to sugar cane.

In terms of analyzing the profitability of Haseeb Waqas, the shareholders’ equity of the company went through the whole gambit, seeing profits in some years while seeing losses in others. Due to non-availability of detailed accounts, the shareholders’ equity provides a

good estimate of the profits which were more than the share capital in periods of profits while fell below the share capital when losses were experienced.

In terms of the business model of Haseeb Waqas, it could be seen that the company was always operating on razor thin margins. In 2002, the gross margin being earned by the company was around 17.8%. After taking indirect costs in account, the net margin only stood at 1.3%. As the company was earning very thin margins, in periods of low sales, this would lead to the company making losses of large magnitudes. In 2007, for example, the gross margin fell to only 0.25% with the net margin standing at -12.6%.

The reason for the low margins was the fact that the sugar industry can be seen as being ultra competitive with larger companies being able to survive on lower margins. This leads to a dog-eat-dog atmosphere where it is survival of the fittest. As smaller companies are not able to compete for a long term, it becomes a case of attrition with the smaller companies falling away.

If the period from 2002 to 2007 was bad, the next 7 years proved to be even worse as losses started to become a mainstay at the company. Haseeb Waqas was barely able to keep its head above the water from 2009 to 2012 after which it was not even able to do that. From 2012 to 2014, Haseeb Waqas started to suffer massive losses as its net margin went from -10.5% to -28.7%. For every rupee of revenues it was earning, the company was making a net loss of Rs 0.27. This was compounded by the fact that from 2013 onwards, it was not even able to earn a gross profit and lost money for every rupee of revenue it was earning. The

worst year was 2014 where the company had a gross margin of -18.8%.

As soon as the company starts to make a gross loss, it is a sign that the operations of the company are not generating any value and it would be better to stop production altogether. As losses started to accumulate, the impact was seen on the balance sheet as well. The shareholders’ equity of the company was around Rs 76 crores in the red and liabilities were being used in order to plug this financing gap.

In terms of the assets, it only had Rs 3.6 billion of fixed assets and Rs 1.1 billion of current assets. Against this, it had borrowing of Rs 5.4 billion which had to be paid back. With losses becoming a norm and assets being valued lower than the liabilities, the creditors start to get nervous as there is a chance that they will not be able to get their loans back in full. The auditors also start to raise red flags as they consider the company not to be a going concern and expect the company to shut down rather than continue in the foreseeable future.

The big shift

So what did Haseeb Waqas Sugar plan to do about this? Well, even though the government had placed a ban on opening new mills and giving licenses, Haseeb Waqas had a bright idea: they would simply shift from central Punjab to South Punjab. In 2014, they were not the only sugar mill planning this. In fact, there were five mills planning similar moves south. The five mills in question, namely Haseeb Waqas Sugar Mills, Chaudhry Sugar Mills, Abdullah Yousaf Sugar Mills, Abdullah Sugar Mills, and Ittefaq Sugar Mills, are all either owned directly by the Sha-

Politics and Sugar Barons

Most sugar mill owners are well known politicians who have had the good fortune of being elected to govern the country on a number of occasions. Prime Minister Nawaz Sharif, his family and relatives own the Abdullah Sugar Mills, Brother Sugar Mills, Channar Sugar Mills, Chaudhry Sugar Mills, Haseeb Waqas Sugar Mills, Ittefaq Sugar Mills, Kashmir Sugar Mills, Ramzan Sugar Mills and Yousaf Sugar Mills. The Kamalia Sugar Mills and Layyah Sugar Mills are also owned by PML-N leaders.

Former President Asif Ali Zardari’s family and PPP leaders are said to own Ansari Sugar Mills, Mirza Sugar Mills, Pangrio Sugar Mills, Sakrand Sugar Mills and Kiran Sugar Mills. Ashraf Sugar mills is owned by PPP leader and former Zarai Tarraqiati Bank Limited (ZTBL) President and current PCB Chairman Chaudhry Zaka Ashraf.

Former Federal Minister Abbas Sarfaraz owns five out of six sugar mills in Khyber Pakhtunkhwa (KP). Nasrullah Khan Dareshak owns the Indus Sugar Mills while former Secretary General, Pakistan Tehreek-i-Insaf and current IPP leader Jehangir Khan Tareen, has two sugar mills, the JDW Sugar Mills and United Sugar Mills. PML-Q leader, Anwar Cheema, owns the National Sugar Mills. Senator Haroon Akhtar Khan, special assistant to the Finance Ministry on Revenue, owns the Tandianwala Sugar Mills while Pattoki Sugar Mills is owned by Mian Mohammad Azhar. Former Governor Punjab and currently a prominent figure in the PPP, Makhdoom Ahmad Mehmood is a major shareholder in JDW Sugar Mills. Chaudhry Muneer owns two mills in Rahimyar Khan district and former deputy PM Chaudhry Pervaiz Elahi and former Minister of State for Foreign Affairs, Khusro Bakhtiar have shares in these mills.

rif family or by their extended relatives. Back in 2016, these mills relocated from different locations in central Punjab to districts in South Punjab near Muzaffargarh after getting special permission from the Punjab government.

The normally rigid and slow Punjab Government infrastructure did not prove a hurdle for these mills. Of course, Shehbaz Sharif was Chief Minister at this time and was in the middle of a second term where he enjoyed wide popular support across the province. In the case of Haseb Waqas, this could prove to be beneficial as it would improve the situation at the company and bring it back into profits once again. The decision was taken and the new location started to see equipment, machinery and new buildings being constructed.

In order to circumvent the restriction on building a new plant, the company contended that they were relocating their old facility rather than establishing a new one. This meant that rather than constructing a new factory, the old factory at Nankana Sahib was being dismantled and the equipment was being moved to the new area. As trucks moved from one location to the other, the new plant came into existence and the relocation was carried out.

Of course, there were already sugar barons in South Punjab, and they were not lightweights either. They might not have been in government, but with Jehangir Tareen among their ranks, the South Punjab sugar manufac-

Sugar Mills: A timeline

turers decided to take this battle to the courts. They went to the courts and argued that the restriction was put in place by the government to make sure that there was no over concentration in one region while protecting the water resources. The relocation followed the letter but not the spirit of the law. The fact that the factory was even allowed to relocate can be traced to the fact that the sugar mill had links to the Sharif family and, with the young brother of the family at the helm, the permission was granted due to the connections.

The gruelling legal battle

As soon as the relocation was carried out, the courts stepped in to take matters into their own hands. Justice Shahid Karim came down hard on the breach and the Lahore High Court ruled in 2017 that this action was carried out with complete disregard for the court’s orders. In addition to that, petitions were filed by leading mill owners who wanted the relocation to be declared illegal.

At one hand, the petitioners felt that relocation was the same as the establishment of a new mill which had been disallowed by law. The defense contended that they had simply relocated their mills and that this could not be seen as the building of a new mill.

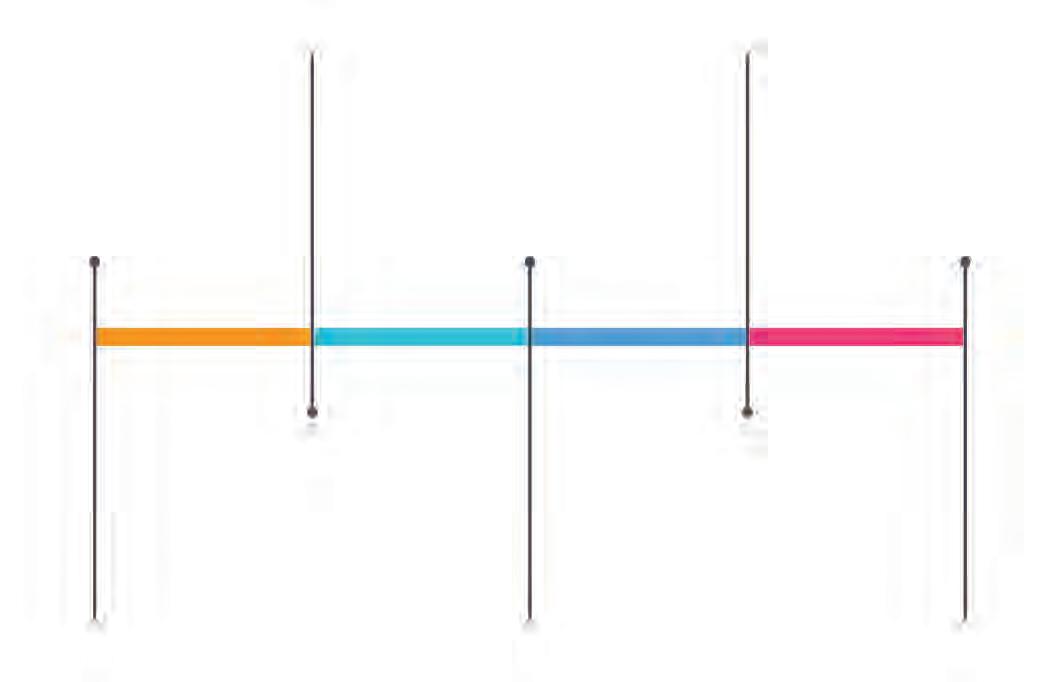

The new state of Pakistan has a problem. The country is a major sugarcane producer but only has two mills. Most of the refined sugar being consumed is imported from India or other neighbouring countries

1948

1951

With more than 54 lakh tonnes of sugarcane being grown, a number of Pakistan’s landed elites set up mills to refine the sugar they grow on their own lands

As the petitions started to move through the courts, Justice Ayesha Malik barred any further relocation to be carried out as Haseeb Waqas was just one of the five mills which were being shifted by the close relatives of the Sharif family.

With the courts getting involved, operations at the new mills were halted as no production could be carried out. For Haseeb Waqas, this proved to be the killer blow as it was already suffering huge losses. As the plant was shut down, no crushing could be carried out and as these were relocated factories, the mill effectively shut down with no production being possible.

The next course of action was to appeal the decision that was passed by the Lahore High Court and an appeal was filed at the Supreme Court. The Supreme Court heard the arguments and struck down the appeal in 2018 ordering the factories to be moved back to their original location. Even a review petition was rejected in 2019 and it seemed that there was no other option left. While the case was moving through the court system, Haseeb Waqas showed the signs of decay in their accounts.

From 2014 to 2018, the company was able to earn some revenues as they were able to crush sugar during their season. However, these revenues were dwarfed by the costs associated as the losses started to pile up in the accounts. In a period of 5 years, the company collectively suffered losses of Rs 3.1 billion.

Six mills have appeared all over Pakistan but there is room for more.

The Pakistan Sugarmills Association is formed

1962

1971

According to a report of the Competition Commission of Pakistan, the number of mills increased to 20 during a period when cane cultivation was incentivized in Sindh through establishment of sugar mills. The size of the industry further increased to 34 by 1980

These amounted to average losses of around Rs 60 crores per year. Ironically, the company shut down completely in 2019 where it saw losses of only Rs 33 crores. The company was making more losses when it was operational compared to when it was shut down.

The losses started to eat into the equity of the company as well as the sponsors had to start giving a loan in order to make the company sustainable. By 2019, the sponsors had injected Rs 84 crores into the company in the form of a loan as its accumulated losses had surpassed Rs 3.5 billion. Even with a revaluation reserve of Rs 1.4 billion, the shareholders’ equity was still negative at almost Rs 1 billion. This gap was filled with liabilities totalling at Rs 4.5 billion with assets of only Rs 3.5 billion.

It was evident by this time that the company was not going to be sustainable for much longer and that something had to give. With no operations and losses accumulating in the future, the company had to do something drastic in order to turn itself around.

Impact of the plant shut down

As the company fought its legal battle, there were lives that were being impacted from this legal fight as well. The new plant was supposed to bring hope and opportunity to the new farmers who

could now sell their produce to multiple buyers rather than just one. This was going to increase their bargaining power and get a good price for their harvest. This reality was never realized as the farmers started to see the opposite.

As the mill was shut down and operations were closed, Haseeb Waqas could not generate revenues which could be used to pay off the farmers. This meant that the company failed to pay for the harvest and the company ended up owing millions to the farmers.

There were also investors who had invested in the company who were now seeing their investment crumble in front of their eyes. Haseeb Waqas is a listed company which means that investors in the market saw it as an attractive company to invest in. First the losses and then the subsequent shutdown of the company meant that investors could do little but see their investment lose value.

In June of 2008, Haseeb Waqas saw its share trading at Rs 64.5 as it was able to retain some of its revenues in profits. From then on, the share price went downhill. The inability to earn profits, the relocation of the plant and then the court battle meant that the future prospects of the share started to diminish leading to a decrease in the share price.

The last nail in the coffin was the auditor’s opinion which stated that the company was no longer considered a going concern. The losses persisting and the shutting down of the plant

meant that there was little hope that the company would be able to survive into the future.

The stock exchange protection

The role of the stock exchange in this matter is that it looks to protect and inform the shareholders relating to the risks that an investment entails. Companies which have doubtful accounts, suspended operations or have failed to submit their financial statements need to be singled out as being riskier in terms of their risk profile. In order to highlight such companies, the stock exchange has created a non-compliant segment.

According to PSX Rulebook clause 5.11.1, companies can be declared non-compliant if they have suspended operations for a continuous period of one year, unable to hold its Annual General Meeting on time, failed to submit its financial statements, failed to pay fees payable to the exchange, the license has been revoked or the auditor has given an adverse opinion. What all these non-compliances show is that the company cannot be considered the same as the other listed companies on the exchange and the investors need to be prudent and cautious when they are willing to invest in such a company. This is a protection mechanism that has been put into place to inform the

With Nawaz Sharif in power in Punjab, the sugar industry has continued to grow. The overall number of mills has increased to 47

1987

1990s

The Sharif Family entered the sugar industry with Ramzan Sugar Mills. Their extended family also starts sugar mills in areas such as Nankanasahib, which is the site for the Haseeb Waqas Sugar Mill. Concerns begin to arise over the reliability of Pakistan’s sugarcane crop

By the early 2000s, the sugar industry is in crisis. The government has kept incentivising new mills through tariffs on imports and subsidies to growers, but there are 91 mills and capacity has been exceeded. The government places a ban on new sugar mills in Punjab

2000s 2016

Completely decimated by other mills in the region, five mills owned by the Sharif Family and its extended members decide to shift from Central Punjab where crop growth is low to the South of Punjab. South Punjab sugar millers take them to court, including Haseeb Waqas

Justice Ayesha Malik rules against the shift of mills from central to south Punjab. The mills appeal but a review petition is rejected in 2019

2017

investor and to make sure they are cognizant of the investment they are making.

In regards to Haseeb Waqas, the factory has completely shut down their production since 2019 and the auditors have given an adverse opinion in terms of them being a going concern. The rulebook then gives further detail of what happens if the non-compliance is not corrected. Clause 5.11.3 states that notices are issued to the company and they are asked to resolve these non-compliances. If this is not carried out in 90 days, the company is issued a risk warning alert which increases the risk attached to the company further.

If there is still no action carried out, the last option for the exchange is to issue a compulsory buy back direction to the majority shareholder who has control of the company. Once this buy back has been carried out, the shares are delisted and the company is removed from the exchange.

The laws have been made in such a manner that they allow the investors to be able to sell their investment at a reasonable price while forcing the buy back to be carried out. Haseeb Waqas was suffering losses and they could do little to change the situation. They had two options at their disposal. Either look to liquidate the company’s assets, pay off the creditors and then give any excess to the shareholders. This would have meant that the company would have to be wound up and sold piece by piece.

The other option is to allow the shareholders to get a return on their investment which is falling in value in the market and allow them an honourable exit while the sponsors look to revive the company. This allows the investors to get off the hook and sell their position while the original owners get to turn the company around on their own terms. At this juncture, there can be investors who would feel that they cannot maintain their investment for any longer and cannot wait for the company to turn around in the near future. This is a winwin for both sides as they can choose on the path they want to take in this matter.

Could the buyback suit Haseeb Waqas?

The price mechanism that will be followed applicable for the buy back is the one that is used for the voluntary delisting process used by the exchange. The stock exchange intimated to the company on the 13th of June 2025 that they had to either rectify their non-compliances or carry out a buy back of their shares. Considering the state of affairs, the management felt that there was little chance that they would be able to turn the company around.

The goal of the relocation was to improve

the financial performance of the company, however, once the factory was closed and the court decided against the company, there was little chance that the situation would improve. The court ordered the mill to be moved back which led to huge losses for the mill and there was a need to arrange capital to recoup the losses.

With no chance of any such capital being raised, the company felt that the best option was to buy back the shares. The sponsors had endorsed this action and it would be carried out to allow the shareholders a chance to sell their shares. The rate that is decided in this case is dictated by the stock exchange which determines the price that will need to be paid. Once the buy back was carried out, the shares would be delisted from the exchange as well.

While the buy back price is being determined, the question can be raised that a company with such huge losses and closed operations, what is the plan for the company once it has carried out the buy back? On the outside, it makes little sense in spending precious funds to buy back the shares which can be used to finance the operations of the company. Use of these funds to buy the shares does seem imprudent for the time being. There can be two reasons for the buyback to be carried out. On one hand, the sponsors are realizing that the assets of the company are worth much more than what they have been recorded at.

The sponsors feel that they can sell the company piece by piece and generate more funds which will justify the buy back in the first place. The second reason can be that the sponsors have secured funding from financial institutions which can mean that they can restart production in the coming days. The working capital requirements can be fulfilled by these finances which can lead to profitability for the mill. Carrying out such a drastic move of delisting and buy back of shares does signal a development has taken place that the sponsors or insiders are privy to that has not been disclosed to the market yet.

The most recent development that was disclosed to the public was the fact that the company had been granted permission to operate its mill at its relocated premises. The aim of the management was to follow a wait and see policy and try to get permission to operate its mill. In relation to this, they filed an application to the Director General of Industries under Section 3 of the Punjab Industries (Control on Establishment and Enlargement) Amendment Act 2002. The application requested for the mill to be made regularise the mill. This permission was granted on February 6th of 2023 and the approval was given. The mill was still not running, however, as it had no access to working capital and funding to do so.

Whatever the case may be, the buy back has led to the share price seeing a jump from

Rs 11.62 on 26th of June to Rs 17.03 on 2nd of July which is only in a space of 5 trading days. The rate that has to be fixed by the stock exchange still needs to be given which can be expected in the first half of July. Even in that case, the buy back and delisting will only become successful if a reasonable price is given and shareholders agree to that price. Haseeb Waqas needs a buyback of at least 90% to make its buyback successful in order to go above and beyond the threshold set by the stock exchange. If the shareholders feel they deserve a better return, they can hold out and not sell at a price they do not agree with.

The reason for the buy back will be revealed over time and the fate of the mill will require time to unfold. For now, Haseeb Waqas is being given a honourable exit by the exchange that they have chosen to take in the interest of the shareholders.

The battle behind the scenes

It is not news that many of the complex entanglements of the sugar industry have been solved because of a general timidness that has appeared in politics in the last few years. Former foes have become friends again and there is no structured opposition to the Sharif family in Punjab or at the centre.

Once again, it is an issue that has been covered before. And while the PSX is offering a way out to Haseeb Waqas, it is worth remembering that the sugar industry overall is still plagued by corruption. Barely a week ago, the PTI criticised the government, alleging it has brought the country’s economic wheel to a “grinding halt, turning the lives of the rank and file miserable” and demanded accountability for sugar mill owners evading taxes.

Alleging billions of rupees in tax evasion, PTI Central Information Secretary Sheikh Waqas Akram, in a statement, urged swift action against eight sugar mills owned by politically influential individuals and their ‘abettors and facilitators’. Mr Akram noted the government exported nearly 750,000 metric tons “only to announce the import of the same quantity within the same fiscal year — a move that has led to a sharp spike in domestic prices, directly benefiting sugar mill owners”. Describing such decisions as “criminal”, he demanded a full-scale investigation.

Such investigations have been called for before as well. The unfortunate part is that the sugar barons have their interests tied so deeply into the industry that they often ascend beyond politics to work together. It is unfortunate that Pakistan’s political elite chose sugar as their common ground: a crop that is bad in every conceivable way, and for which we do not have the water to grow it. n

By Ahtasam Ahmad

Pakistan’s power sector stands as a stark testament to the consequences of years of mismanagement and flawed planning. What began as policy missteps has evolved into a crisis so complex that even the country’s brightest minds struggle to untangle the web of interconnected problems.

Like a patient surviving only on life support, the sector depends entirely on massive government subsidies and temporary fixes to function, leading renowned economist Dr. Atif

Brace for impact: The grid is in a nose dive

Short-term tariff relief masks the long-term challenge

Mian to aptly describe it as a “zombie sector” –one that continues to drain national resources while showing little sign of genuine recovery. The current crisis didn’t emerge overnight but represents the culmination of systematic failures spanning decades. At its heart lies a fundamental mismatch between supply and demand, compounded by a series of shortsighted policy decisions that consistently favored quick remedies over sustainable, longterm solutions. Today, Pakistan’s installed power generation capacity reaches approximately 46,000 megawatts, dramatically exceeding the peak national demand of around 30,000 MW. This glaring disparity perfectly

encapsulates the sector’s core inefficiency and highlights how far removed planning has become from actual needs.

This supply-demand imbalance has created what industry experts term a “capacity trap,” where fixed costs for underutilized power plants – many with payments denominated in US dollars – continue accumulating regardless of actual electricity production. The government’s historical strategy of attracting private investment through comprehensive risk transfer mechanisms has resulted in generation costs that are 87-140% higher than those in neighboring countries, making Pakistani electricity among the most expensive in

region.

The challenges extend well beyond generation capacity to encompass fundamental inadequacies in transmission infrastructure. Pakistan’s aging electrical grid struggles with what experts call the “south-north barrier,” referring to geographical constraints that prevent efficient power distribution across regions. These transmission bottlenecks create the paradoxical situation where the country simultaneously curtails cheaper renewable energy sources due to grid limitations while maintaining expensive thermal plants to meet demand. The result is a system where some areas experience power shortages while others possess surplus capacity that cannot be effectively distributed.

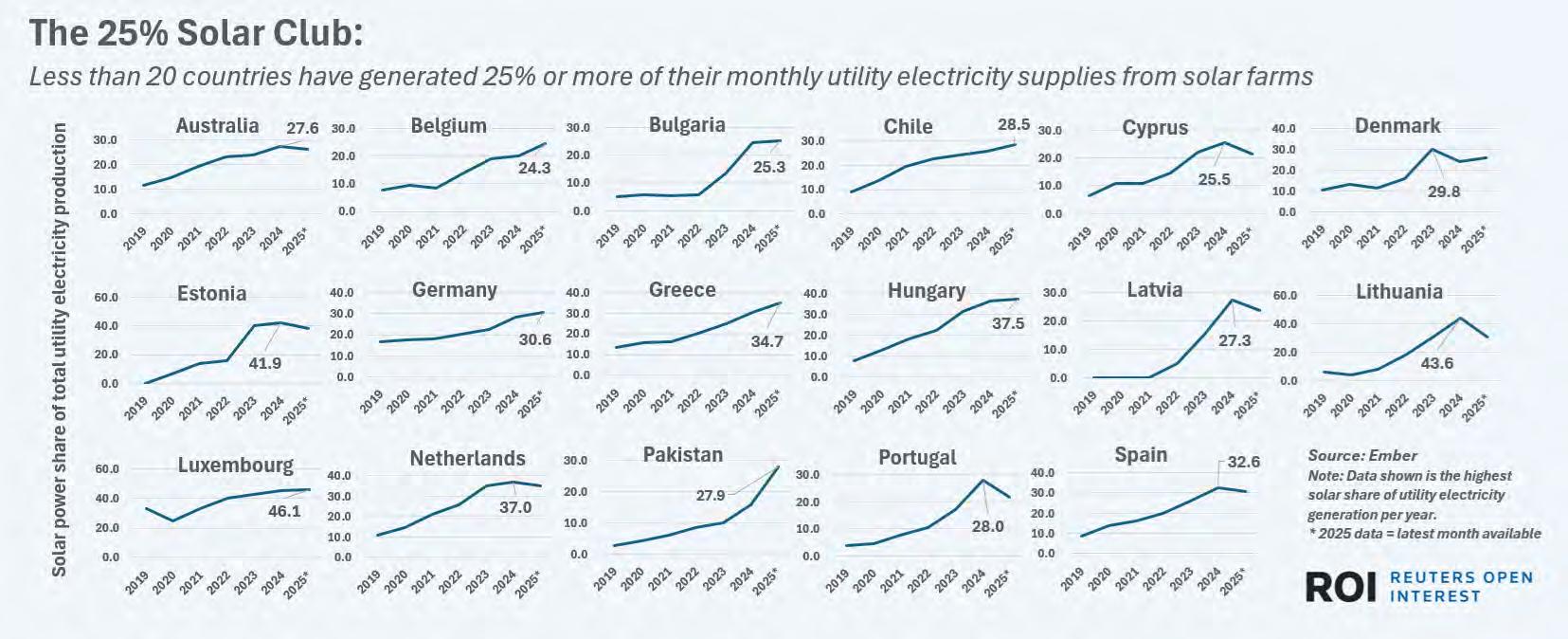

This complex web of interconnected problems would challenge any administration, and the current government finds itself grappling with the consequences of decisions made over a decade ago. Recent weeks have seen renewed efforts to address these deep-seated issues, with the government announcing reference consumer tariffs for Fiscal Year (FY) 2026 following a budget that included several crucial power sector reforms. Meanwhile, Pakistan’s remarkable solar energy adoption continues unabated, with the country now generating more than 25% of its electricity through solar installations, both on-grid and off-grid combined.

Given the power sector’s critical importance to Pakistan’s fiscal stability and economic future, understanding the current dynamics and reform efforts becomes essential for grasping the broader challenges facing the nation’s development trajectory.

Setting the tariff right

Pakistan employs a top-down electricity pricing mechanism where the regulator establishes an annual reference tariff, subsequently modified through quarterly tariff adjustments and monthly fuel price adjustments throughout the year. The system responds to fluctuations in key economic indicators including fuel costs for power generation, prevailing interest rates, exchange rate movements between the rupee and dollar, projected electricity demand, and broader inflationary pressures.

This complex pricing architecture stems directly from Pakistan’s cost-plus regulatory framework operating within a single-buyer market structure, where the government serves as the sole purchaser of electricity and determines tariffs based on accumulated costs rather than market-driven supply and demand dynamics. This approach creates a problematic feedback loop where rising costs trigger higher electricity prices, which in turn suppress consumer demand and force the

same cost base to be distributed across fewer units of electricity sold, further inflating perunit prices.

The situation becomes particularly acute given that approximately two-thirds of Pakistan’s electricity generation costs are fixed expenses that remain constant regardless of actual power output. When demand falls due to price increases, these unchanging fixed costs must be spread across a smaller volume of electricity units, creating a situation where cost-plus pricing simultaneously reduces consumption while increasing per-unit costs.

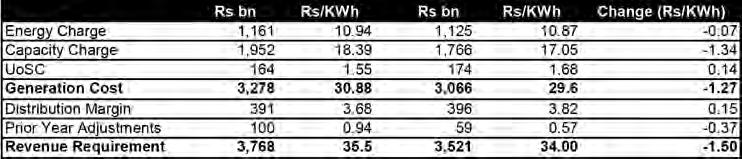

The current reference tariff including cost of generating, transmitting, and distributing electricity across Pakistan averages approximately Rs. 34 per kilowatt-hour (KWh). This breaks down into an average energy cost of Rs. 10.9 per unit, capacity payments of Rs. 17.05 per unit, transmission expenses of Rs. 1.68 per unit, and distribution costs of Rs. 4.4 per unit. Any additional charges appearing on consumer electricity bills typically represent a combination of system losses from theft and technical inefficiencies, various taxes and levies, and cross-subsidy mechanisms designed to support different consumer categories.

The government’s electricity sales projections for fiscal year 2025-26 anticipate 116.4 billion kilowatt-hours delivered to Distribution Companies (DISCOs), with an allowance for 11.0% system losses bringing net distributable units to 103.6 billion KWh. This represents a 2.5% decline compared to the previous year’s distribution levels, reflecting ongoing demand challenges within the sector.

Energy charges are expected to decrease to Rs. 1,125 billion from Rs. 1,161 billion in fiscal year 2025, primarily driven by lower fuel costs that have provided some relief to the overall tariff burden. Capacity charges are projected at Rs. 1,766 billion representing a 9.5% year-over-year decrease. This decline in capacity payments stems from recent power purchase agreement terminations, successful tariff renegotiations with independent power producers, and the benefit of lower prevailing interest rates.

Meanwhile, Use of System Charges are anticipated to rise 6.1% to Rs. 174 billion from the previous year’s Rs. 164 billion, reflecting ongoing transmission and distribution infrastructure costs.

At the consumption front, domestic consumers, while representing an overwhelming 89% of total grid connections, account

for approximately half of all electricity consumption. Industrial users emerge as the second-largest consumption category, contributing 24% of total electricity usage. The agricultural sector accounts for 9% of national electricity consumption, while commercial establishments represent 8% of total usage. The remaining 10% of grid-supplied electricity serves various other consumer categories.

The looming threat

While the tariff breakdown illuminates the structural complexities of Pakistan’s electricity pricing mechanism, it simultaneously exposes the sector’s fundamental vulnerabilities. Given the predominantly fixed nature of power sector expenses outlined earlier, accurate demand forecasting becomes absolutely critical to the system’s financial viability.

When projections fall short of reality, the government faces an uncomfortable dilemma: either absorb the unrecovered costs through subsidies that strain an already stretched fiscal position, or pass these additional expenses directly to consumers who are increasingly struggling with affordability.

What can render these projections void is grid defection, as consumers increasingly adopt solar over expensive grid electricity. While this provides the perfect segue to elaborate on what’s happening at the distributed generation level in Pakistan, one point worth highlighting concerns the arrangement to resolve the country’s circular debt.

While consumers are being extended a Rs. 1.15 per KWh reduction in tariffs, there is an additional surcharge added on top of the Rs. 34 tariff, amounting to Rs. 3.23 per KWh, to service the recent debt accumulated to pay off around Rs. 1.25 trillion in outstanding circular debt.

According to sources, the 18 banks lending to the government have finalized the modalities, and disbursements will take place in the coming days to clear outstanding dues of multiple parties within Pakistan’s power sector supply chain.

Factoring in solar

If you’ve been following Pakistani social media and encountered the phrase “The Grid is Cooked,” then what’s firing it is undoubtedly solar power.

Pakistan’s rapid ascent as one of the leading adopters of distributed solar energy among emerging economies represents a remarkable achievement. According to energy think tank EMBER, Pakistan now generates more than 25% of its electricity from solar installations, with the majority operating off-grid and independent of the national electricity system.

This crowdfunded solar revolution reached extraordinary momentum during FY2024, when Pakistan imported 16 gigawatts of solar photovoltaic equipment valued at $2.1 billion. The pace has only intensified since then, with 12.7 GW imported during just the first three quarters of FY2025.

By March 2025, cumulative solar imports over the preceding five years had reached an impressive 39 GW – representing more than three-quarters of Pakistan’s entire national generation capacity. What makes this transition particularly significant is its distributed nature: despite these massive import volumes, only 780 MW has been deployed at utility scale, meaning the vast majority of solar installations consist of rooftop systems, small commercial setups, and off-grid solutions directly serving end users.

The profound impact of this solar surge extends well beyond electricity generation statistics. Pakistan now finds itself in the unprecedented position of potentially selling excess liquefied natural gas amid a supply glut that has curtailed local gas production. Gas-fired power plants, which historically consumed the lion’s share of the country’s LNG imports, have experienced declining output for three consecutive years through 2024. This shift reflects how dramatically cheaper solar power has displaced gas-fired generation, fundamentally altering Pakistan’s energy consumption patterns.

Complementing this solar revolution is the rapidly accelerating adoption of battery storage systems across Pakistan’s residential, commercial, and industrial sectors. Driven by persistently high electricity costs and the continued decline in solar component prices, consumers are increasingly pairing solar installations with Battery Energy Storage Systems (BESS) to achieve greater grid independence, reduce energy expenses, and enhance power reliability.

This convergence of solar and storage technologies is expected to gain further momentum as battery economics continue improving and technology costs decline. The scale of this storage transformation is becoming increasingly significant for Pakistan’s energy landscape.

According to the Institute for Energy Economics and Financial Analysis, Pakistan imported an estimated 1.25 gigawatt-hours of BESS capacity in 2024 alone. The institute projects that under current trends, this figure could surge to 8.75 GWh by 2030, representing approximately 26% of the country’s projected peak electricity demand. Such a dramatic shift toward distributed storage could potentially strand existing peak generation assets and exacerbate financial losses for the national grid system.

However, it also warns that “unmanaged BESS growth could destabilize Pakistan’s national grid by reducing demand and raising capacity payments.” To harness the benefits while mitigating risks, the analysis emphasizes that “timely investments in grid modernization, smart metering, and regulatory updates can enable decentralized solar plus BESS configurations, avoiding expensive generation expansion and supporting strategic power planning.”

What did we learn?

While there are legitimate reasons to celebrate the reduction in reference tariffs, particularly given that power purchase costs have doubled over the past five years, this achievement reflects more pragmatic regulatory approaches than fundamental sector reform. The regulator’s adoption of more grounded and realistic assumptions for setting the power purchase price, evidenced by NEPRA’s request for an eighth scenario beyond the CPPA’s original seven projections covering electricity demand, rupee-dollar parity, fuel prices, and hydrology, demonstrates improved planning methodology. However, these incremental improvements cannot mask the underlying challenge that makes accurate projections increasingly elusive: the rapidly evolving energy landscape driven by mass solar adoption and grid defection. The government’s limited toolkit for addressing structural overcapacity remains constrained to power purchase agreement renegotiations and contract terminations, yet progress on these fronts has fallen well short of initial projections and promises. This reality underscores the need for a more comprehensive transformation that extends far beyond tariff adjustments. According to sector experts, Pakistan requires a fundamental reimagining of its power system architecture, including the implementation of bottom-up, feeder-wise load forecasting to capture localized demand patterns and distributed energy impacts, a temporary moratorium on new centralized generation while assessing solar-plus-battery economics, updated regulatory frameworks to support battery integration, extensive grid modernization through smart infrastructure, and the aggregation of distributed battery systems into virtual power plants capable of providing grid services. n

Coffee nation

The rise of cafe culture across upper middle class neighborhoods throughout urban Pakistan

TBy Farooq Tirmizi

his is the story of two drugs: caffeine, and sugar. Pakistanis consume both, but the proportions in which we consume them – and the reasons for doing so – are shifting, and they are shifting because of the changing nature of the what Pakistanis do for a living.

This is the story of the journey from doodh patti to black coffee.

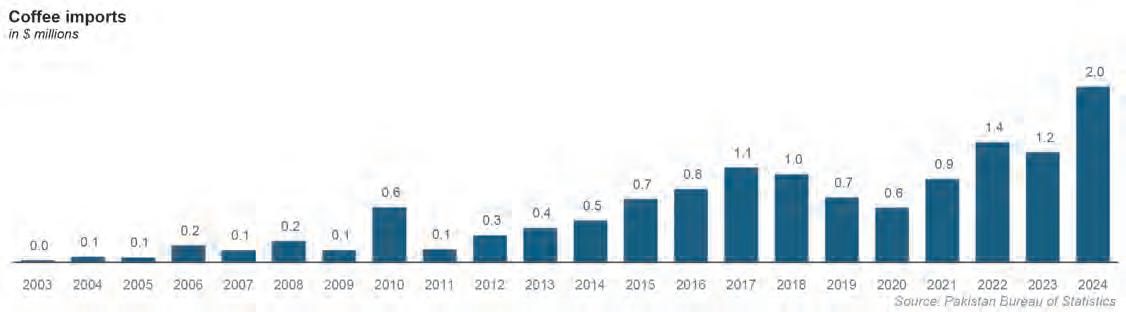

We should also confess to something: our headline is premature. Coffee in Pakistan is still a very niche phenomenon. How niche? For every cup of coffee consumed in Pakistan, we consume 735 cups of tea, based on Profit’s analysis of data from the Pakistan Bureau of Statistics on the country’s imports of both commodities for the year 2024, the latest year for which complete figures are available.

But in markets, while size matters, sometimes momentum can matter more, and the consumption of coffee is rising sharply. Just ten years ago, in 2014, the difference was 1,900 cups of tea for every cup of coffee, and in 2004, the difference was even more massive: almost 14,000 cups of tea for every cup of coffee.

From a very, very low base, coffee is clearly gaining share.

On a purely commercial basis, this is not a particularly important story. The total amount of coffee imported into Pakistan in 2024 was around $2 million. This is, of course, just the imported value, and for the average cup of coffee you buy at a café in Karachi or Lahore, the cost of the actual coffee itself is likely about 5-10% of the price you pay. Sales of coffee itself are approximately a $20 million market in Pakistan.

For comparison, the average sales per store for Starbucks, the US-based coffee giant, was about $1.2 million a year, which means that a handful of stores in the US sell more coffee than all of Pakistan’s cafes combined.

But what makes this story interesting is who is having the coffee, and why, because it represents a new way of working, a new way of socializing, and a larger class of people with disposable income.

To understand this change and its significance, it helps to understand the status quo.

The morning chai and the drawing room

Tea is the social lubricant of Pakistan. Of that, there is no question. It is the drink that, if people offer it and you say no, will result in you being seen with some degree of suspicion. Which makes it so odd that this most Pakistani of traditions involves a beverage that does not come from Pakistan at all.

Nearly all tea consumed in Pakistan comes from Kenya, which itself had no tea cultivation until 1903, when the British began planting it there. The plant, and beverage, are originally Chinese and spread to different parts of East Asia through Chinese influence. It began to be cultivated in what is now India also by the British

East India Company in the 1820s in the northeast part of India.

Tea exists in Pakistan not because of some ancient tradition that is an inherent part of our culture. You drink it because sophistication in this country is defined by what the British used to do while they were here. And tea in particular is part of a handful of imperial Chinese traditions that the British brought to India. The other big one that we still live with is a unified civil service selected through competitive exams, and the two are inextricably linked. Try visiting an officer of the Civil Service of Pakistan and leaving without having a cup of tea.

While the British were in India, tea was consumed by them and by the colonial elite, but after their departure came the democratization of tea consumption. Unilever decided to hire some very smart young graduates of IBA in the 1950s who then were able to convince virtually everyone in the country that they should drink tea.

But it was not just marketing genius that convinced Pakistanis to make tea an essential part of their daily routine. Ultimately, it served two very valuable purposes.

For the working class, the morning and afternoon cups of tea serve a very important role. It is milk, sugar, water, and tee that serves about 150-200 calories in energy content and about 40-60 milligrams of caffeine, which serves as an alertness boost to get through a working day but costs very little relative to any other source of calories that might be available to a working man or woman. Add in a dry roti, and that is about 400 calories of tolerable grub that can get you through a large part of the day.

For all classes – but especially the middle class –it also serves a social function: it is the beverage to serve on social occasions, the acceptable excuse to grab a few minutes of someone’s time (especially important for people who work in sales roles), and the thing to reach for during awkward silences.

The government tracks the price of everything in your morning tea very carefully for this reason: it is an important part of the caloric intake of the average Pakistani.

The economics of tea

Based on projections using the Household Integrated Economic Surveys conducted by the Pakistan Bureau of Statistics, and inflation data, Profit estimates that Pakistani households spend approximately Rs800 per month on tea, and yes this includes households in the poorest income quintiles.

Tea occupies perhaps an outsized importance in the minds of government bureaucrats, who have become enamoured by the concept of growing Pakistan’s tea requirements domestically. Yet despite nearly four decades of effort, mainly by Unilever, the total amount of land brought into cultivation for tea is less than 900 hectares.

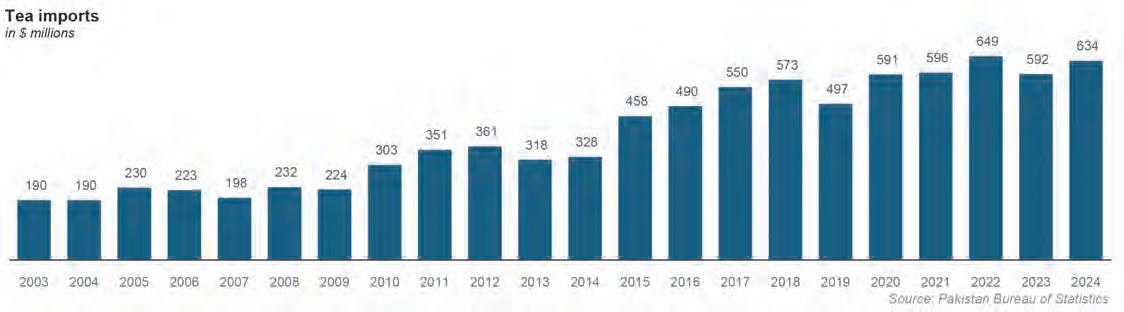

Pakistan’s domestic production of tea is a meager 25 tons per year. The country imported about 244,000 tons of tea in 2024, spending $634 million to do so. The

domestic production is not even a drop in the bucket. We are the largest importer of tea in the world.

Why do we grow so little tea? We seem to not grow enough, which means the economics of it simply do not make sense.

The growth of tea proved to not be profitable in Pakistan because the price of plucked leaves (raw material for black tea) at Rs46 per kg is much higher in Pakistan than that in the international market i.e. between Rs20-22 per kg (Unilever based at Mansehra). Pakistan could have become competitive with the international prices by bringing maximum area under tea cultivation (at least 10,000 ha), introducing value addition and taking cost reducing measures at all the segments across the value chain. However, this would have required continued political patronage for a while which was missing.

Pakistan gets only 40% of the world average yield. Although the net price at farm gate is higher in Pakistan at Rs46 per kg as compared to that in India and Bangladesh at Rs22.90 and Rs27.0 per kg, respectively but the net return per ha in Pakistan is low at $1,360 compared to international $1,600 due to low per ha productivity.

The rise of the café

The scale of change in Pakistan is sometimes hard to understand, so it is important to state the following: up until the 1990s, the vast majority of even what would be considered upper middle class Pakistanis would go out to restaurant about once a month or less. The idea of meeting a friend at a café on a weeknight was not possible because there would be no café in any city in the country and you would not have the disposable income in your pocket to make that an idea that would even occur to you.

Yes, dhabas have long existed, but their purpose then was what it primarily remains even today: a place for the day labourer to get food during the work day, and for truckers or other labourers to get a meal at the end of a long work day. They were mostly not frequent-

ed by middle class people. Social interaction mostly took place in other people’s homes. Coffee itself was not unheard of, but rare to be available outside Army messes. (The famous phinti coffee was invented in a British Indian Army mess.)

The café as a place to get coffee, and to socialize without a full meal, was just not something that most people did. Again, if you do not have a large population of people with meaningful disposable income, the idea of going to a place and not having a full meal accounted for would go against the grain of the scarcity mindset that poor societies tend to live with.

By most accounts, the first café that really tried to be a coffeehouse in the fullest sense of the word was Espresso’s first branch in Zamzama, Karachi, which opened in 2006. If you manage to ignore the trash (less bad now, used to be terrible back in 2006), Zamzama was the closest you get to narrow European-style streets in an upper middle class neighbourhood in Karachi. (Plenty of such streets exist in working class neighbourhoods.) The shops are small, and most of them were not really built to be able to house places to eat.

In one of these lanes, in a tiny outlet, Espresso open a different concept entirely: small tables not meant to have large plates full of food, but instead just cups of coffee, and maybe a small plate of snacks. The seats were much closer together because they were optimizing for being able to hear the person you are there to meet, and not space for arms to move while eating. Seats meant to be comfortable to sit in, and not necessarily geared towards making it easy to lean over the table to take a bite.

Notably, Espresso also tried something that had previously not been done before: a place for men and women to mingle safely, without the threat of harassment. They implemented a “no men unaccompanied by women after 7pm” policy which was meant to ensure that the rising number of women occupying upper middle income positions in corporate Pakistan would make it their default place to

hang out, and the men courting them would follow suit. It worked.

This is a café as it exists in most parts of the world today, and a thing that originated in Damascus around the 1400s. For their first century of existence, coffeehouses were restricted mainly to Damascus and Mecca, and did not spread outside those two cities until the 1500s, when Sulaiman, the Ottoman emperor, visited Mecca and his imperial retinue decided to take the concept back to Istanbul.

From Istanbul, coffeehouses spread as a concept to Europe, notably to Vienna, where they became a hub of intellectual activity in the city, and to London, where they served a similar function. Many of the ideas that powered the European Enlightenment period were born out of discussions at coffeehouses on the continent.

The cafes that exist in Pakistan are more similar to that concept – a place to gather and talk while sharing a non-alcoholic beverage –than the American concept of a place to secure one’s caffeine supply. Cafes in America open absurdly early. The café closest to my apartment in a very residential part of Manhattan opens at 5am every day. Yes, including Saturday and Sunday. The American upper middle class wakes up very early and needs their coffee immediately.

The American model of coffee

We bring up the American approach to coffee for a reason. Americans may enjoy their coffee and be discerning consumers of it, but they also have no illusions about what it is: first and foremost, a source of caffeine. Yes, Starbucks sells the caramel macchiato – a very high calorie, high sugar drink – but its staple is a cup of black coffee: which contains about 200 mg of caffeine and close to zero calories. The workaholic American says: give me my caffeine so that I can grind out work in a high concentration state of mind. The taste of it is secondary, the pleasantries

unnecessary, the caffeine vital above all.

Americans are so obsessed with caffeine cold brew coffee is ubiquitous across the country. Cold brew is not yet in Pakistan – some cafes will try to pass off iced coffee as cold brew. It is not. Cold brew, for the uninitiated, is the kind of thing that makes you wonder why people do cocaine to boost their energy levels when this stuff is legal.

This model of caffeine as a necessary drug to rewire one’s brain to work hard is not yet in Pakistan, but about to be.

A small, but growing proportion of Pakistanis are now looking at the café as something more than just a nice place to meet friends: it is a place to work on a remote job with people in a different time zone.

Here is a fact to remember about globalization: when people of many cultures have to work together, the culture they all default to is American, even if there are no Americans on the team.

About 2% of Pakistan’s work force now works either as freelancers for global clients or remote employees for companies based outside the country. They are operating in a work culture and environment that is different from that of the on-shore economy: more competitive, higher pressure, tighter deadlines, longer nights (and not just because of time zone differences).

When working with those high cognitive requirements – where the brain needs to operate at peak alertness levels for long stretches of time – the caffeine content of tea will just not cut it. Coffee becomes the beverage of necessity.

This, perhaps, explains why coworking spaces in Pakistan frequently stock coffee along with tea for their denizens, and why there are now some coworking spaces in Karachi that are experimenting with having a café as part of the coworking location. It still is not possible to go to a café to grab an early morning coffee even at 9am, let alone 7am or earlier. But is absolutely possible to pour another cup of coffee at 6pm when you know you have a long night ahead of you.

The business of caffeinating Pakistan

As we estimated earlier, we suspect total coffee sales in Pakistan do not exceed $20 million, though of course, that is likely a small fraction of the total revenue earned by cafes across the country. It is certainly becoming a larger business, and is attracting more capital.

A web scrape by Profit indicates that 256 new cafes opened up across Pakistan over the past three years, of varying quality and price points. It is not clear how many of these remain extant.

But the business has grown enough that franchises of successful brands from other parts of the world continue to thrive in Pakistan. Perhaps the most successful of these is Gloria Jean’s Coffees.

Originally founded in a suburb of Chicago, Gloria Jean’s is now an Australian coffee franchise chain that now has 56 locations across Pakistan. It is likely the largest coffee chain in the country, largely built off the fact that it offers sub-franchises for locations across the country. This means that if you are a person of some means in Sargodha, you can help Gloria Jean’s come to your town, as indeed has happened.

The iconic Canadian chain Tim Horton’s opened up its first location in Lahore in February 2023 and now has 16 locations in several cities in Pakistan.

The British chain Costa Coffee is currently on its second attempt at making franchises in Pakistan work. The first attempt was during the Musharraf era, when a location opened up in Karachi and lasted about three years before shutting down. This second attempt was initiated in December 2022 and the chain currently operates three stores in Pakistan.

Then there are the many standalone cafes and attempts at coffee chains besides the original Espresso Café that are still around and thriving. Caffeinating Pakistanis appears to be

a growing business. But how big will it grow? Will coffee overtake tea as Pakistan’s beverage of choice?

Crossing the Atlantic in Pakistan

One of the important undercurrents of Pakistan’s elite culture has been the shift from looking to Britain as the metropole to looking at America for that same role. In different avenues of effort, this shift has taken place at different times. Shahnawaz Bhutto sent his son to Oxford. That son sent his daughter to Harvard.

What does this have to do with tea versus coffee? Because ever since the Boston Tea Party, the Americans decided that if the British were going to drink tea, the Americans would drink coffee. And if the story of Pakistan’s elite culture – which eventually percolates down to other strata of society – is that of a jettisoning of British mores and the adoption of American ones, the rise of coffee may be more than just a fad.

It may be the move towards a more Americanized work culture, adapted for our non-alcohol consuming ways (hence the consumption of coffee later in the day and not early in the morning).

Coffee is a very small part of the market right now, but look at who is having it. And who will want to copy the behaviours of these early adopters?

This may yet end up being just another phase. We have seen one previous wave of cafes opening up in Pakistan and then fading away, which happened around 2006 through 2010.

But there is reason to believe this more recent wave may have more staying power: it started in 2020, when Pakistan’s freelancer / remote worker population really started taking off. The advent of cafes is to serve the independent night owl who makes good money and is temperamentally the most American part of Pakistan’s work force, right down to the dollars in their bank accounts. n

Bank Makramah sells headquarters building in Karachi for Rs12 billion

The deal would be the second largest commercial real estate transaction in Pakistan by rupee value, third largest by dollar value

BProfit Report

ank Makramah Limited (BML)

– the institution formerly known as Summit Bank – has signed a sale and purchase agreement to dispose of its landmark head office property, Summit Tower in Clifton, Karachi, to Sumya Builders & Developers for Rs12 billion, according to a statutory filing with the Pakistan Stock Exchange on Monday. The notice says the deal was executed on 2 July and is expected to be completed within the current quarter, subject to all requisite regulatory and third party approvals. The bank, which occupies the upper half of the 12 storey mixed use tower at Plot G 2, Block 2, Clifton, will lease back approximately 60% of the space for an interim period while it scouts for a smaller, purpose built premises. Management anticipates recording a pre tax gain of just under Rs5 billion once the transaction closes, a figure that will swing to roughly Rs3.4 billion after tax and transaction costs. Proceeds will be received in two equal tranches: the first on completion, the second on fulfilment of post closing obligations. HBL Asset Management has been appointed escrow agent, while Mohsin Tayebaly & Co. acted as legal adviser to the vendor and Mandviwalla & Zafar to the purchaser. Sumya will assume responsibility for all external maintenance immediately; internal refurbishment costs will be shared pro rata until the bank’s phased exit, targeted for mid 2026.

Bolstering a thin capital cushion

The sale is the latest leg in an ambitious, multi pronged recapitalisation plan designed to haul the troubled lender back into regulatory compliance. At end March 2022 the bank’s paid up capital was a negative Rs22.6 billion, while its Capital Adequacy Ratio (CAR) languished at 94.9% against the State Bank of Pakistan’s 11.5% minimum. The position has improved after UAE businessman Nasser Abdulla Hussain Lootah injected Rs10 billion in fresh equity and took a 51% stake,

but BML is still short of the finish line.

In December shareholders voted overwhelmingly in favour of a Scheme of Arrangement that will lift net assets by Rs29.39 billion through a combination of share premium transfers, Tier II capital instruments and real estate disposals. The Summit Tower off load represents the first major asset sale under that programme.

Apart from equity injections and asset disposals, the bank has lined up a Rs6 billion Additional Tier I Sukuk and has secured SBP approval to reclassify Rs3.5 billion of subordinated debt as hybrid capital. The combined measures should push the CAR above 12% by June 2026, paving the way for full Islamic conversion and an eventual return to profitability.

Summit Tower in context

Completed in 2010, Summit Tower is a mid rise, glass and granite block comprising approximately 180,000 square feet of lettable

space across 12 office floors above a mezzanine and two basement parking levels. Its corner site abuts Beaumount and Dr Ziauddin Ahmed Roads, a location long prized for proximity to the Defence and Clifton commercial districts.

The headline figure also stands out when benchmarked against other marquee real estate deals involving financial institutions:

What makes the latest deal unusual is direction of travel: historically, Pakistani banks have been net acquirers of flagship real estate – vernacular statements of corporate muscle – rather than sellers. UBL bought the 23 storey UBL Tower in 2015, Bank Al Habib snapped up Centrepoint in 2021, and HBL constructed its LEED Silver HBL Mega Tower the following year. By contrast, BML is liquidating bricks and mortar to free up regulatory capital, reflecting both the urgency of its balance sheet repair and a broader shift towards asset light operating models in the digital banking era.

The buyer, Sumya Builders & Developers, is part of the Hiba Group of Companies, a Karachi based conglomerate best known for mid market apartment projects along University Road and Shaheed e Millat Expressway. Led by CEO Altaf Abdul Sattar Kantawala – a vice chairman of the Association of Builders and Developers (ABAD) in 2021 22 – the firm has delivered more than 2,000 residential units under the Sumya Chandni Residency and Sumya Avenue brands.

Sumya’s business model targets the city’s aspirational but price sensitive middle class: limited amenity towers with compact 1,200–1,800 sq ft flats, sold off plan on extended payment schedules.

What happens next for Bank Makramah?

The Rs12 billion windfall, coupled with the AT I Sukuk and a planned Rs4 billion rights issue to minority shareholders, should allow BML to meet the SBP’s minimum paid up capital (Rs10 billion) and CAR (11.5%) well before the December 2026 deadline. Once that hurdle is cleared, the bank will proceed with its long signalled conversion into a full fledged Islamic bank – a process the SBP has already approved in principle.

BML intends to rationalise its sprawling branch network – currently 170 outlets – by shuttering or franchising roughly 30 loss making locations in low density rural markets. The savings are earmarked for a wholesale upgrade of the core banking platform, mobile app and digital onboarding stack. Analysts at AKD Securities estimate the technology overhaul could cost Rs2.5–3 billion but save up to Rs1 billion a year in back office expenses once complete.