Are hybrid cars being taxed out of their competitiveness?

Code, Cash, and Chaos: Inside the blindspots threatening Pakistani IT

At PSO, circular debt stops growing

Security Investment Bank lays out plans for Shariah compliance conversion

PEL revenue bounces back to record highs

Globe Textile Mills owners sue OBS to terminate merger agreement

When the taxman meets the tobacco baron

The govt is going to tax

Can they survive it?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

K-Electric: Asleep at the switch

A bruising board fight has left the management adrift, at a time when the company is unprepared to deal with the coming age of solar energy

By Farooq Tirmizi

It can seem unfair to criticize someone for doing a difficult job badly, but when that job is as essential as running an electric utility company, one must do so anyway. And there is no way to sugarcoat this: K-Electric is being rather badly run – for many reasons, many of which are outside the control of the current management – and the government of Pakistan appears to be providing some cover to this mismanagement.

The crux of the story is this: In the 2010s, K-Electric was the success story that was able to improve bill collection and reduce theft in an incredibly tough law and order environment in Karachi during one of the worst decades in the city’s history. In the 2020s, it appears to be the only utility company in the country that is now presiding over increasing bill evasion and theft.

So what happened?

Lots of details, but fundamentally, two things have hit K-Electric hard: a lack of clarity as to who has clear management control, which has meant that major decisions about the strategic direction of the company have not been made and cannot been made until that question is settled. And secondly, perhaps more importantly, that lack of direction has left K-Electric completely unprepared to deal with the world of distributed electricity generation brought about by the rise of solar electricity in Pakistan, but especially Karachi.

But first, let us take a look at the numbers to describe the symptoms of what ails K-Electric. To summarize, here is what happened: bill recovery rates have fallen sharply at K-Electric over the past two years, and this is driven largely by middle class and wealthier household consumers not paying their bills. None of the possible explanations of this change bode well for the company, and the bruising board fight means that while they can continue to manage the company on a day-to-day basis, the strategic decisions needed to confront the challenges facing the company are simply not being made.

The deterioration in bill collection

First, let us take a look at the scale of the problem.

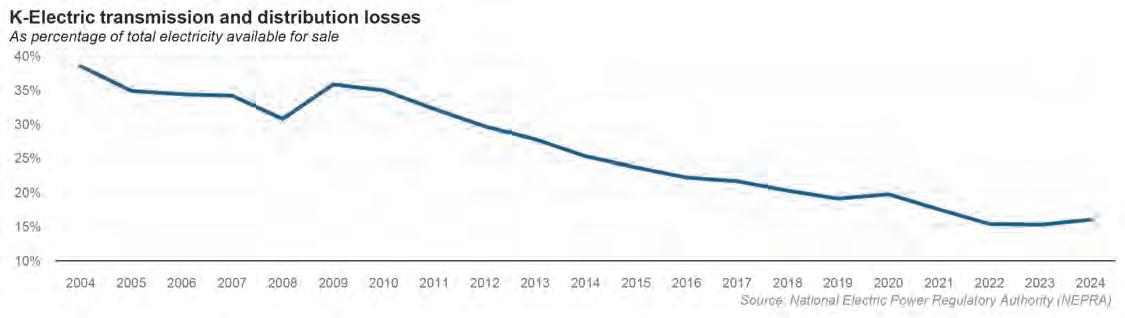

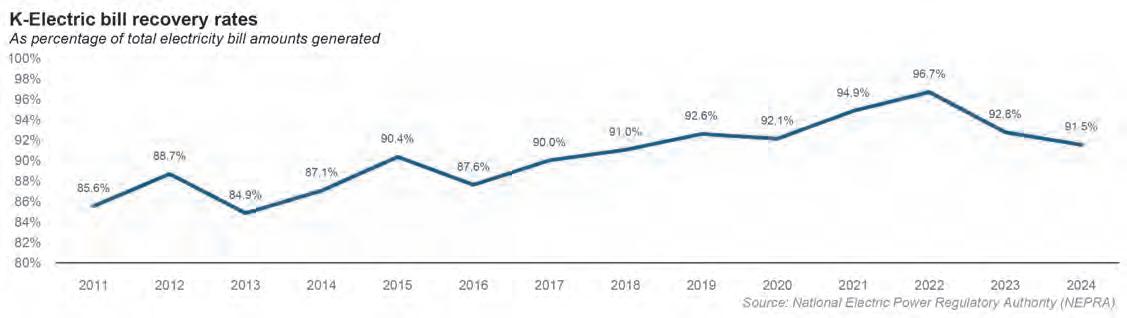

In fiscal year ending June 30, 2024, the latest full year for which data is available, K-Electric’s bill recovery rate – the total amount of bill payments collected as a percentage of the total amount of bills issued – was about 91.5% across all of its customers, according to data from the National Electric Power Regulatory Authority (NEPRA).

That number sounds impressive, and indeed represents a sharp increase in bill recovery rate relative to where the company was privatized in 2005, but is down from the 96.7% it had achieved just two years prior, in fiscal year 2022. And when one looks at the source of this decline, it is driven in very large part due to a decrease in collections from household consumers, which has seen a relatively sharp deterioration in the past four years, going from 92.2% collection in 2020 to just 82% in 2024.

This is bad, to say the least, and so bad, in fact, that K-Electric has gone from having a bill recovery rate about

700 basis points above the state-owned electricity companies’ average (which basically means all other companies in the country since K-Electric is the only privately-owned electric utility) in 2021 to now being 1,000 basis points below the state-owned companies. It is a 10% drop in just three years.

And it does not seem to be improving either. In the first half of the fiscal year ending June 30, 2025, K-Electric’s bill recovery rate dropped even further, with a household consumer bill recovery rate now at 78.4%, a sharp decline in just six months.

Who does the stealing?

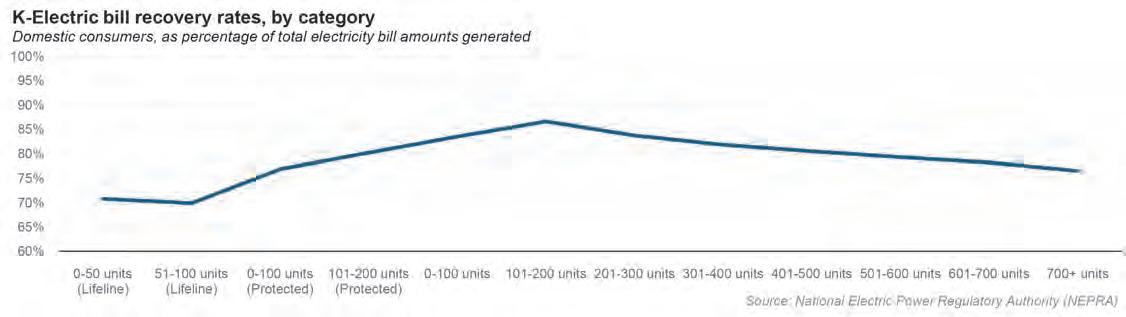

Here is where things get very interesting. One common narrative that the government has is that they resist raising electricity prices to their full economic cost because of a fear that the poor will react to rising prices by simply stealing more electricity. The data, however, yields a slightly more complicated picture.

It is true that billing recovery rates for the very lowest consumption levels – 100 units a month or less, or bills of around Rs1,500 per month or less – tend to be relatively high, but what is surprising is that the curve of bill recovery rates is n-shaped, meaning that the most honest bill payers are those whose bills are about 400 units per month (about Rs20,000 per month in bills), and then for those with higher bills than that, the recovery rate declines again.

Does this mean that the poor are more honest than the rich? Probably not, since a large proportion of the poor also just steal electricity without ever having a formal electricity connection, meaning there is no bill that they can decide not to pay. The higher-income households, with bills exceeding Rs30,000 per month, appear to be able to get away with no paying for months on end, with those in the middle being forced to pay in full and on time.

An analysis of the NEPRA data on electricity losses indicates that about 62% of the total losses from unpaid bills comes from those who have bills exceeding 400 units per month. What about the notion that Karachi has a law and order problem and large swathes of the city are difficult to even collect bills in? This is true, and a contributing factor to be sure, but less than one might think.

In 2009 and 2010, K-Electric – then known by its historical name of Karachi Electric Supply Company (KESC) – hired McKinsey & Company, the global consulting firm, to help it understand and map its system so that they could get a better handle of just where they lost money and at what part of the billing cycle. As a result, K-Electric now has a relatively complete picture of just where these losses come from.

When the company was first brought under the ownership of Abraaj, the now-bankrupt Dubai-based private equity firm, a majority of the city was considered high-loss, and only about 40% of its revenue came from low-loss areas. An analysis of K-Electric’s billing divisions called IBCs indicates that only about 15.4% of the company’s billing comes from parts of the city that can be described as having a law and order problem.

This implies that about 57% of the increased billing losses are coming from middle and higher income households in parts of the city where there is relatively better

law and order.

The best customers are leaving

Having laid out the case of just how much the operating performance of K-Electric has deteriorated, let us now present a counterargument that perhaps suggests that this is not entirely the management’s fault. Take a step back from this granular analysis, and one sees a different picture emerge which can be summarized with the following sentence.

K-Electric’s losses are not increasing because more customers are stealing or refusing to pay their bills; they are increasing because its best-paying customers are leaving the grid and so the company is left with a greater proportion of its bad customers.

Where are the good customers leaving to? Rooftop solar electricity, of course.

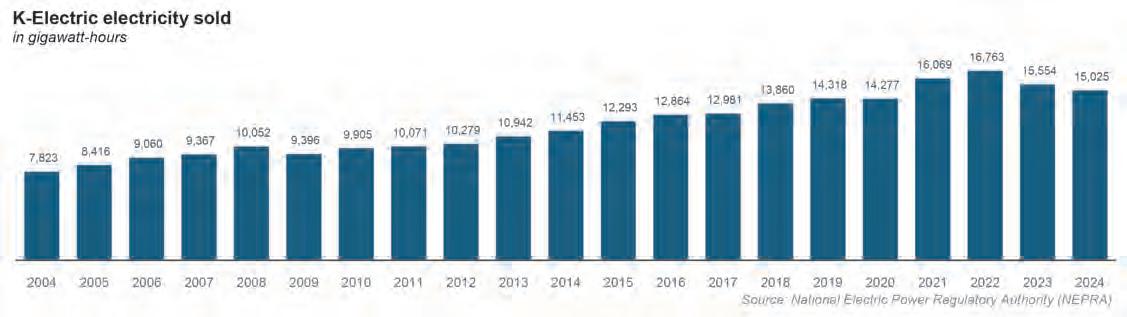

K-Electric in 2025 is a company that is approximately 11% smaller in terms of electricity sold than its peak just three years ago in 2022. The company sold 15,025 gigawatt-hours (GWh) in 2024, compared to 16,763 GWh in 2022, according to NEPRA data.

Karachi’s economy has been hit by the economic downturn of the past few years, but not so badly that it has shrunk by 11%. This reduction in electricity consumption is not just because people are using less electricity

(though there is certainly some of that), it is also because they are buying less of it from the grid and producing more of it themselves through solar panels.

This is in line with the change in the rest of the country. Total electricity generation for the rest of the grid has fallen by 10.8% between 2022 and 2024, according to NEPRA data.

The solar boom

By now, Pakistan’s solar electricity boom is a well-documented phenomenon. In 2024, the country imported 16,600 megawatts (MW) in power generation capacity in the form of solar panels, more than double the amount in 2023. And Karachi appears to be a little ahead of the rest of the country – though Lahore and Islamabad appear to have fast caught up to the trend.

Needless to say, this is bad for an electric utility company even though it represents a challenge they did not create. Managing the rise of solar electricity is something that many electric utility companies around the world have struggled to manage and it is not as though there is one universally recognized way of dealing with this challenge.

But what makes it inexcusable for K-Electric at least is the fact that this is a predictable challenge that they have known about for quite a while. Indeed, it is a challenge so long in the making that we at Profit ran a

cover story on it in November 2016, almost nine years ago.

Back then, we wrote: “It may be tempting to think of solar power as a niche product, but that would be a tremendous mistake. The numbers suggest that the market is growing incredibly rapidly… As more of the wealthier consumers – both domestic and industrial –shift to alternative energy, K-Electric will be left with the smaller, less profitable customers, typically in areas with theft rates that can often be up to four times higher than in the more affluent neighbourhooods. Not only would its addressable market shrink, but the utility would be left with the most bothersome portions of its customer base.”

This is exactly what has happened nine years later, and the company appears to not have much of a game plan to deal with the situation, even though they have observed it coming just as much as we had.

Solutions to this problem exist, of course, and one that we had proposed would involve some model where K-Electric takes more control over the solar conversion process, and instead of having people either buy solar panels up front, or borrow from banks, it would likely finance or lease out solar panels itself, in effect converting itself into a combination of an electric utility and a consumer finance company.

Of course, the company could have decided to pursue some other model instead of

this one, but it appears that the company chose to do nothing and instead just watched the biggest threat to its existence just continue to emerge. It should actively have been planning and experimenting with solutions to the problem of distributed solar power generation.

Why has this not happened? Mainly because of the drama with its management and ownership structure.

A bit of history

The Karachi Electric Supply Company (KESC) was founded in 1913 (rebranded in 2013 as K-Electric). It is the country’s only vertically integrated utility, with its own power generation, transmission, and distribution assets. Until the late 1960s, KESC was largely a financially self-sustaining entity. In the 1980s, the company briefly became a subsidiary of the Water and Power Development Authority (WAPDA) and was at one point placed under the management of the Pakistan Army.

In 2005, the Musharraf Administration sold off a 66.4% stake of the company to a consortium of the Al-Jomaih Holding Company, a diversified Saudi Conglomerate, and the National Industries Group, a publicly listed Kuwaiti financial conglomerate (which also owns a large stake in Meezan Bank). For three years, the Saudi-Kuwaiti conglomerate failed to make any headway in turning around the

company, finally turning in 2008 to Arif Naqvi, the former Karachiite who had gone on to create Abraaj Capital in Dubai.

In October 2008, Abraaj bought out half of the Jomaih-NIG stake in KESC, injecting $391 million into the company. Abraaj spared no expense in trying to turn around KESC, investing upwards of $1 billion in the company’s power generation and transmission infrastructure, which brought the utility’s power generation efficiency rate from 30% in 2008 to 37%. As per KE’s own numbers, from 2009 when Abraaj took over KE’s transmission and distribution (T&D) losses were 35.9%. By 2019 this number had fallen to just under 20%.

Abraaj was ready to reap their rewards. They had taken KE on at a time when the company was a loss making entity and turned it into a profitable power company. In 2016, they sold 66.4% of K-Electric to Shanghai Electric, the Chinese power company, for a whopping $1.7 billion making it the biggest acquisition of a Pakistani company in a decade.

But that happy ending was not to be.

The drama begins

Consistent delays on the part of the government meant the Shanghai deal could not go through. Despite a lot of political lobbying on the part of Abraaj’s Arif Naqvi, the deal was dead in its tracks. And then came the crash. In

2019, Arif Naqvi and Abraaj were involved in an international scandal that ended with the company utterly bankrupt. And along with it the Shanghai Electric deal went kaput. For six years Abraaj’s baggage weighed the Shanghai deal down and KE remained unsold.

Into this foray jumped in Shaheryar Chisty. The former highflying international banker was born in Lahore, raised in Karachi in a navy family, and came back to Pakistan in 2011 where he acquired ownership of Daewoo as well as interests in CPEC backed projects regarding Thar Coal. A self-described investor in orphan assets, Mr Chishty had been impressed by the Abraaj led turn around of KE and had tried to acquire the company.

Chishty was well connected in China and put together a consortium that would bid for control of KE. But Shanghai beat him to it. But when the opportunity presented itself again, Mr Chishty started making moves to acquire KE, which he did in the Cayman Islands. That is where matters got complicated.

Since KE was owned by Abraaj, which as a company has gone bankrupt, its assets are a little all over the place. Just take a look at the ownership structure of KE. When the Al Jomaih group entered the picture in 2005, they created KES Power Limited (KESP) which was a Cayman Islands company. This company paid the government of Pakistan directly and acquired a 66.4% stake in K-Electric in Pakistan.

So when Abraaj wanted to buy KE from Al Jomaih in 2009, they funnelled over $370 million in foreign direct investment into KE through the KESP company in Cayman. This money was channelled through the Infrastructure & Growth Capital Fund L.P. (“IGCF”), a $2 billion Cayman Islands private equity fund with investment contributed by over 100 different international investors, managed then by Abraaj Investment Management.

This means KE is owned by the KESP in the Caymans, which after Abraaj’s entry is now owned by the IGCF. So when Chishty wanted to acquire Abraaj’s stake in KE, it could not acquire KE in Pakistan. It had to go to the KESP in Cayman. Chishty’s company, AsiaPak Investments, created a special purpose company called Sage Venture Group Limited (Sage) and registered it in Cayman. Sage then bought out the Infrastructure Growth and Capital Fund LP (IGCF or the Fund), which holds an indirect material stake in K-Electric Limited. These transactions were authorised in proceedings at a court in the Cayman Islands, according to court documents.

This is where we get to the events of the last couple of years. Remember, what Mr Chishty has bought is a 53.8% stake in KESP, which is the company which owns 66.4% in KE. The remaining 46.2% of KESP is owned by Al-Jomaih Power, and Denham Investments. This is the same Al Jomaih that first bought KE through the KESP in 2005 before they sold it to Abraaj in 2008.

The situation currently is that AsiaPak essentially owns the same position in KE that Abraaj did up until it went bankrupt. And up until the Abraaj scandal blew up, the private equity fund had complete control over the KE board and could appoint its representatives onto it. This is something that through repeated legislation and stay order Mr Chishty’s AsiaPak has not been allowed to do.

Why that is the case is the subject of lengthy litigation, but fundamentally a dispute between the larger shareholders as to who should gain control.

Operational clarity, strategic limbo

Given that board fight, and lack of clarity as to who gets to set the strategic direction of the company, K-Electric is for the moment running with roughly the same strategy that Abraaj put in place almost a decade ago now. This has the effect of the company being able to run business as usual like a normal power company. But, of course, that is not enough for its current needs, which require the company to deal with significant strategic challenges and make important decisions.

Would Chishty be well-positioned to make those decisions? Difficult to say, since he has not even been given the opportunity to make his case yet. But the fact of the matter is that time is of the essence for K-Electric.

The speed with which solar power is being added to the grid in Pakistan is very rapid, and continuing to hemorrhage its best customers is not something any business can sustain for very long, let alone one that is so reliant on heavy capital investments like a utility company.

Pakistan’s largest city and financial capital cannot afford to have a utility company embroiled in such a massive board fight that the management is effectively rendered spectators to their own strategic challenges.

We asked K-Electric management to comment on this matter, and after two weeks – during which time we held off on publishing this story – they finally responded. Their response is published below, in full, and without any edits on our part, nor any commentary.

K-Electric’s response

“At the outset it is important to clearly separate shareholder-level issues from the company’s operational continuity and delivery. K-Electric’s (KE) board has remained fully functional and active throughout in all matters.

KE also remains fully functional, accountable, and operationally robust. Despite operating

in the most complex and theft-prone regions of the country in a regulated environment, KE has demonstrated consistent performance across key indicators—something that few, if any, utilities can claim, especially in times of national economic strain.

Amid COVID and severe economic challenges faced during the last control period, KE held its ground—maintaining and improving on its performance enabling KE to significantly outperform state-owned distribution companies in terms of T&D and AT&C loss reduction over the last 15 years. As a result, KE privatisation has provided benefit of Rs164 billion to the Government of Pakistan in FY 2024 alone in respect of reduction in AT&C losses.

With consistent hands-on management, the company has commissioned 900 MW BQPS-III plants, which is among the top five efficient power plants in the country, launched record-time infrastructure projects like the 500kV KKI Grid, received multi-year tariff and investment plan (c. USD 2 billion) approvals across all segments, and signed long-pending government agreements. It has also attracted Pakistan’s most competitive bids for renewable energy, reinforcing its role as a trusted platform for sustainable power.

These achievements are not isolated milestones—they reflect a deep-rooted culture of accountability, resilience, and forward-thinking. KE’s operational strategy is underpinned by a vision to create reliable, consistent and equitable access to energy for our 3.8 million customer base that is expected to grow to 5.0 million customers by 2030. To analyse KE’s performance, ground realities in areas where access is difficult due to poor infrastructure, slum settlements, and area hindrances should be considered. Losses including recovery losses are mainly concentrated in around 300 out of a total of 2,100 feeders of KE which are infested with such issues.

Through targeted investments and interventions including community engagement efforts, KE aims to bring down the AT&C losses to 15.6% by 2030 and having the MYT decisions duly approved will enable KE to reach that goal with purpose and clarity.” n

Are hybrid cars being taxed out of their competitiveness?

New taxes are set to take effect from July onwards. But what happens after that?

By Abdulhameed Niazi

Before the federal budget was announced, a whirlpool of rumours was circulating regarding the automotive industry. The overwhelming opinion was an expected drop in the price of locally manufactured vehicles. One popular belief was that a recent IMF recommendation pertaining to “free trade” would result in the slashing of import duties which would in turn drop the prices of locally assembled vehicles significantly.

This however was not the case. In the

classic status quo move, the federal government decided it would tax the general public by increasing sales tax on cars. The general sales tax for all vehicles was raised to a flat rate of 18% and a carbon tax of Rs 2.5 per litre was slapped on every poor soul that chose not to go electric and the hopes of potential car purchasers across Pakistan were dashed.

To add insult to injury the government did not make any official announcements in regards to reducing import duties only giving vague indications of reducing it to 15% over the next few years or so.

And so we wondered: What of the hybrids? Surely the government, which was so

vehemently pushing for a greener automobile policy, wouldn't tax arguably the best and most practical shift to cleaner and greener energy. But that was not the case. Hybrid vehicles have also been caught up in the general increase of sales tax to 18.5%. The tax on hybrid vehicles before this was 8.5% and the increase represents more than double what the original tax was.

The impact on pricing overall has been brutal but the hybrid market which in the past year or so had become so competitive has taken a particularly strong beating. The price jumps are estimated to be as follows:

• Kia’s Sorento 1.6T HEV AWD will top the

list with a staggering hike of over Rs 14 lakh (the cost of a new Suzuki Swift in 2016), while the FWD variant won't lag behind at Rs 12.9 lakhs.

• Hyundai’s Santa Fe Signature and Smart will climb by an estimated Rs 12.1 lakhs and Rs 10.9 lakhs respectively.

• Haval’s H6 HEV will probably see a jump of Rs 10.3 lakhs and the Tucson’s hybrid variants will rise by up to Rs 10.5 lakhs — on par with Kia’s Sportage L HEV.

• Even the more affordable hybrids won't be spared. The MG HS PHEV will see an increase of Rs 8.49 lakhs, and the Elantra Hybrid will see the same. The Corolla Cross HEV variants will go up by Rs 8.27 lakhs and the Haval Jolion HEV will go up by Rs 8.14 lakhs. Some prospective buyers had hoped they would be able to buy cars in June before the taxes kicked in, but most automakers had already run dry in terms of supply before the budget was announced. Toyota had no cars available saying that prices were fluid and they could not guarantee a delivery in June.KIA and

Haval similarly could not offer any guarantees on a June delivery. MG was an exception, with the MG HS PHEV ready for delivery within the week according to dealers. While Hyundai was the only brand still offering some variety and hope to consumers in the midst of this crisis — the Tucson FWD, Santa Fe, and Elantra were up for grabs. But for anyone hoping to grab a hybrid before the storm hit, the window for most options was already closed.

There was a slight caveat, however, to the dusty showroom floors so deprived of stock by “investors.” While the Corolla Cross was unavailable — with or without a “premium payment,” commonly known as own money — Kia, Haval, and MG dealerships had a plethora of “investor” cars available for purchase. Kia dealers informed us that a Rs 10 lakh premium could be paid for the Hybrid Sportage, with the Sorento being generally unavailable. Haval told us that the H6 HEV was similarly available if one paid a slightly higher premium of Rs 5 lakhs. Oddly enough, an MG representative claimed that investor cars were

Rs 100,000 cheaper than ones bought directly from the company. Dealers added another tidbit of news: this “premium pricing” is expected to increase further if the aforementioned tax reforms are passed by the National Assembly — a move that now seems all but certain.

In contrast, Hyundai and MG appear to be the only two companies genuinely attempting to cater to their customers amid the chaos. Hyundai representatives even stated they would still be offering June invoices for vehicles purchased on payment plans — a small yet meaningful relief for those racing to beat the July tax deadline.

As things stand, the hybrid market has gone from being one of the most promising segments of Pakistan’s auto industry to a cautionary tale of policy backlash. With investor manipulation, vanishing inventories, rising taxes, and uncertain pricing, those who hoped to go green now find themselves stuck in a financial grey zone — paying more for less in a market that seems to punish demand rather than reward it. n

What are we doing about our water?

The government has set out Rs 147.8 billion for water projects in this year’s PSDP. This is what all the projects look like

By Ahmad Ahmadani

In a significant push towards securing Pakistan’s water future and boosting hydropower generation, the federal government has proposed an allocation of Rs. 147.8 billion under the Public Sector Development Programme (PSDP) for the fiscal year 2025-26, targeting 42 ongoing water sector projects.

According to copies of the official documents, these projects encompass a mix of large dam construction, rehabilitation of aging hydropower infrastructure, flood protection schemes, irrigation systems modernisation, and detailed engineering studies.

The throw-forward liability of these projects as of July 1, 2025, stands at over Rs. 1.27 trillion, reflecting the long-term and capital-intensive nature of water sector initiatives. In government finance, “throw-forward liability” refers to the outstanding,

unspent portion of a budget allocation that is carried over to the next financial year. It represents a commitment or obligation from a previous year that the government must still honor.

The proposed allocation for the next fiscal year includes Rs. 51.78 billion in rupee cover and Rs. 96.03 billion in local financing. These funds aim to maintain momentum on strategic infrastructure schemes that are essential for water storage, agricultural irrigation, power generation, and disaster resilience.

The allocation comes at a time when major crops in the country saw a decrease in production of more than 13% which has directly had a negative impact on the country’s growth rate. On top of this, increasing tensions with India after their declaration that they would abrogate the Indus Water Treaty have made this a particularly pertinent issue.

What are the projects being proposed?

Anumber of new and old projects have been slated under this allocation, but there are serious questions about what the throw forward cost will mean and whether or not the government will be able to get any of these projects off the ground.

Among the flagship projects receiving the largest allocations is the Dasu Hydropower Project (Stage-1), located in Kohistan, Khyber Pakhtunkhwa, which has been earmarked Rs. 20 billion. This project is supported by IDA credit and additional financing from the World Bank, with total project cost estimated at over Rs. 510 billion …

Another major project, the Mohmand Dam Hydropower Project, has received a proposed allocation of Rs. 35.7 billion, indicating the government’s continued emphasis on

enhancing water storage capacity and clean energy output.

The Diamer Basha Dam Project, which is one of the most high-profile multipurpose mega-dams in the country, has two components — civil works and land acquisition and resettlement. The civil works component, including the Tangir Hydropower integration, has been allocated Rs. 35 billion while Rs. 7.78 billion has been proposed for land acquisition and resettlement.

The Tarbela 5th Extension Hydropower Project has been proposed to receive Rs. 3.4 billion to further improve energy output from the existing infrastructure. In a parallel effort, Rs. 5 billion has been allocated for refurbishment and upgradation of Mangla Power Station to raise its generation capacity from 1000 MW to 1310 MW. Rehabilitation work at Warsak Hydropower Station has been proposed Rs. 845 million.

In Balochistan, where water scarcity remains a critical concern, multiple dam construction projects have been prioritized. The Construction of Awaran Dam, with a total cost exceeding Rs. 18.8 billion, is set to receive Rs. 1.5 billion. The Panjgur, Shehzanik, Sunni Gar, Winder, Tapok, Gish Kaur, and Mara Tangi dam projects have collectively been allocated over Rs. 5 billion for FY26. Moreover, the package for the construction of 100 small dams in

Balochistan (Package-III and IV) continues to progress with a combined proposed allocation of Rs. 1.3 billion.

To strengthen water supply for Pakistan’s largest metropolis, Karachi, the government has proposed Rs. 8.2 billion for the Greater Karachi Bulk Water Supply Scheme (K-IV Phase-I), and an additional Rs. 9.47 billion for the Kalri Baghar Feeder and Keenjhar Lake improvement projects. The importance of these projects lies in addressing Karachi’s chronic water shortages and improving the reliability of supply to millions of residents.

The long-standing Kachhi Canal Project and its restoration works from the 2022 floods have also found their place in the budget, receiving Rs. 100 million and Rs. 620 million respectively. Similarly, the Chashma Right Bank Canal (Lift-cum-Gravity) project, intended to irrigate over 286,000 acres in Khyber Pakhtunkhwa, has been allocated Rs. 100 million.

Data driven water management?

The government has also placed a renewed focus on data-driven water management and climate resilience. Rs. 4.4 billion has been proposed for the installation of a real-time telemetry system on 27 key sites of the Indus Basin Irrigation System, aimed at improving discharge monitoring and reducing pilferage. The umbrella PC-I for the Flood Protection Sector Project-III, covering structural

and non-structural measures to combat flood risks, has been allocated Rs. 200 million. Additionally, Rs. 200 million has been proposed for a JICA-funded project to enhance flood management in the Indus Basin.

Meanwhile, a number of feasibility studies and preparatory works have also been funded to ensure timely readiness for future implementation. These include Rs. 150 million for the Hingol Dam design, Rs. 200 million for environmental studies linked to the Neelum-Jhelum Hydropower Project, and Rs. 200 million for the Project Planning and Development Unit. The government has also earmarked Rs. 300 million for the Naulong Multipurpose Dam in Jhal Magsi, Balochistan, and Rs. 1.87 billion for remodeling the Pat Feeder Canal System in Naseerabad, Balochistan.

With over Rs. 2.55 trillion in cumulative project costs and significant under-implementation liabilities, the water sector remains a critical development priority for Pakistan. The proposed PSDP 2025-26 allocation of Rs. 147.8 billion reflects a substantial investment in the country’s long-term water and energy security. As Pakistan faces mounting climate stress and rising water demand, the timely execution of these projects will be instrumental in building resilience, supporting agricultural growth, and expanding clean energy access across the country. n

A thriving IT industry risks stalling as policy uncertainty clouds Pakistan’s digital future

By Hamza Aurangzeb

While most of Pakistan’s economy struggles, IT has delivered consistent double-digit growth, absorbing talent and earning precious foreign exchange. Built by a resilient private sector and tech-savvy workforce capitalizing on post-COVID global demand, the industry finally has the momentum to compete on the world stage.

Then came the 2025-26 budget. Instead of supporting long-overdue tax reforms and policy frameworks that the sector desperately needs, the federal government chose neglect. This isn’t just poor timing, it’s economic malpractice. As global markets hunt for reliable outsourcing destinations and Pakistan sits closer than ever to meeting that demand, policy inaction threatens to derail the country’s most promising growth engine.

Profit examines how government failures are undermining Pakistan’s digital goldmine, the structural barriers choking export potential, and what must change before this rare economic bright spot dims. The world is watching, local talent is ready, but is Pakistan’s leadership?

The Dawn of Pakistan’s IT Industry

The inception of the Information Technology (IT) culture and industry in Pakistan goes back to 1964, when the first computer, an IBM 1620 mainframe, arrived in Pakistan, which was procured by the Pakistan Atomic Energy Commission (PAEC). Although it was intended for the PAEC office in Lahore, the machine was relocated to Dhaka simply because the only trained operator in the country at the time was based there. This detail, while minor on the surface, reflects the significant gap between technological acquisition and local expertise that Pakistan would need decades to overcome.

During the 1970s, computers began appearing in government departments and commercial banks, laying the groundwork for what would become a fledgling computer industry. The 1980s saw a trickle of desktop computers enter the homes of Pakistan’s upper-middle class. For a few early adopters, these machines were not just tools; they were gateways into a world of software and digital innovation.

In 1986, two brothers from Lahore, Amjad Farooq Alvi and Basit Farooq Alvi, created the world’s first known computer virus, “Brain.” It was an activity born out of intellectual curiosity and a desire to protect their medical software from piracy. The virus even included their real names, phone numbers, and addresses in Allama Iqbal Town, a symbol of their naivety and transparency. This moment, though controversial, put Pakistan on the global digital map and revealed a native spark of creativity and technical capability.

The transformation of Pakistan’s IT landscape truly began in the early 2000s, under the leadership of Dr. Ata-ur-Rehman, then serving as Minister for Science and Technology during General Pervez Musharraf’s government. Inspired by India’s booming IT outsourcing industry, Pakistan also launched a national strategy to replicate that success. Thus, the government rapidly

expanded computer science programs across public universities, invested in advanced computing infrastructure, and ensured access to fully licensed software from global firms like Microsoft, an unprecedented move at the time. These state-led initiatives reshaped the higher education sector. Every major university was connected to international academic repositories and equipped with modern, well-functioning computer labs. Although the government largely overlooked primary and secondary education, the growth of higher education, particularly in computer science, was driven primarily by public sector initiatives.

However, despite focused efforts and substantial investment, the strategy yielded limited early results. By the time Musharraf left office in 2008, India’s software and outsourcing exports had soared to $73 billion, while Pakistan’s exports remained limited to just $269 million.

Pakistan’s Digital Ascent

For nearly a decade after the Musharraf era, Pakistan’s tech and outsourcing sector grew steadily if not spectacularly. The industry showcased resilience and promise, despite being hampered by inconsistent federal policies and the absence of a coherent national strategy. Thus, growth was driven largely by the private sector, with occasional support from more forward-looking provincial governments. However, a breakthrough on the global stage remained elusive. The sector was maturing, but it hadn’t yet hit its moment. Then came 2020 and with it, a global disruption that changed everything.

The COVID-19 pandemic ushered in an unprecedented shift in how the world worked. Lockdowns and travel restrictions forced companies across developed economies to embrace remote work, often for the first time. Suddenly, physical location no longer mattered, and outsourcing went from being a cost-saving tactic to a business necessity. While giants like India captured a large share of this demand surge, Pakistan’s IT and tech-enabled services industry finally found a window of opportunity and seized it.

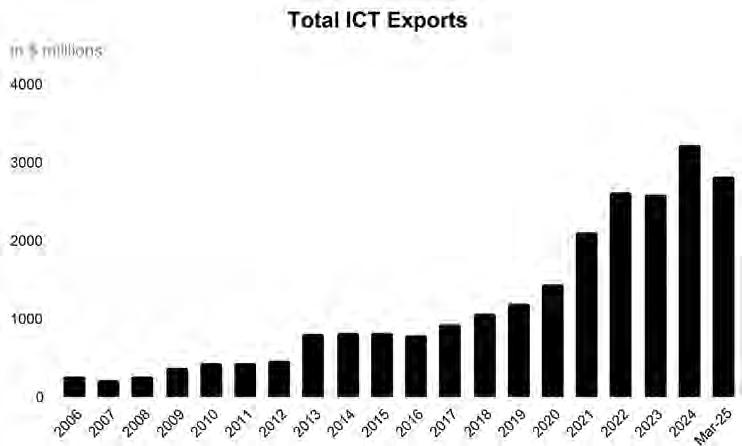

Before the pandemic, Pakistan’s annual tech exports hovered around $1.2 billion in 2019. But in 2020, exports jumped to $1.44 billion—a staggering 20.8% increase in just one year. More importantly, this growth wasn’t just a temporary spike; the very next year, the sector’s exports witnessed a growth of 46.3% in 2021, this growth signaled the beginning of a sustained momentum. During the current fiscal year of 2025, Pakistan’s IT services exports have reached $2.8 billion as of March 2025.

The core of this success lies in software development and IT services, which generated $2.4 billion alone. Remarkably, this segment has grown at an average annual rate of 21% since 2006, when it exported a mere $72 million worth of services. Software exports have grown 2.5x since 2019, when they first crossed the billion-dollar mark.

Call centers, once considered the backbone of tech outsourcing, now represent the slowest-growing segment. In the ongoing FY25, they have brought in $239.335 million, representing only 8.5% of the total ICT

exports. However, an additional amount of $1.3 billion was also added from a diverse and rapidly expanding category: tech-enabled services.

These are Pakistanis who may not be coders, but provide skilled services online, like graphic designers, digital marketers, virtual assistants, copywriters, accountants, legal consultants, and even Quran tutors. They represent the country’s expanding digital workforce, proving that Pakistan’s IT story is not just about code but rather about talent, adaptability, and a global mindset finding its voice in a connected world.

A budget that risks stalling the momentum

The IT sector is a rare success story in an otherwise sluggish economy of Pakistan. However, this rising sector was dealt a setback in the recently announced 2025-26 federal budget despite contributing billions in exports and employing hundreds of thousands of young professionals. The budget failed to address two key demands from the industry: a clear taxation framework for remote workers and long-term stability in the tax regime for formal IT exporters.

For years, the industry has called for a 10-year tax policy that would provide predictability, encourage investment, and enable tech firms to compete with global peers. Instead, the government has opted to extend the current reduced Final Tax Regime (FTR) rate of 0.25% under Section 154A for registered exporters with P@SHA only until June 2026. While this extension benefits compliant entities in the short term, the absence of long-term clarity has raised major concerns for investors and local firms planning to scale.

Meanwhile, the issue of taxing high-income remote workers remains unaddressed as well. These individuals, often full-time employees of foreign firms, continue to operate in a grey area and remain largely untaxed, while companies that create local jobs and train local talent face audits, regulation, and comparatively higher costs. This imbalance makes local hiring less attractive and encourages talent to shift towards informal or overseas opportunities.

Pakistan’s brain drain and its consequences have become conspicuous in recent years. In 2024 alone, over 727,000 skilled workers sought employment abroad, a figure that underscores the urgency of creating a business environment that retains and rewards talent. PASHA put forth a solution to classify individuals earning over Rs 2.5 million annually from fewer than three foreign sources as remote workers. This would impact only the top 5% of earners, while protecting freelancers and smaller service providers. Yet, the proposal

was ignored in the budget entirely. The lack of continuity in tax policy also threatens Pakistan’s ability to attract foreign investment.

While the IT industry has shown remarkable growth, exporting over $2.8 billion worth of services during FY25 thus far, and maintaining a strong upward trajectory, the federal budget sends a discouraging message to investors and companies. The federal budget was expected to reinforce Pakistan’s commitment to its digital future but rather it has created an environment of uncertainty and ambiguity at a time when consistency and confidence were critical.

Reimagining policy for IT export growth

Despite boasting consistent double-digit growth, Pakistan’s IT sector continues to fall short of its true export potential. A combination of structural inefficiencies, policy delays, and poor global branding has held the industry back from achieving breakout success.

One of the most critical steps the government must take is improving Pakistan’s international image, which is often characterized by political instability and security concerns discouraging foreign investment, despite the country offering a cost-effective and skilled workforce.

Pakistan’s tech sector lacks a focused branding strategy to counter these perceptions. A national campaign, such as the TechDestination Pakistan initiative, could be instrumental in reshaping global opinion. This campaign should highlight Pakistan’s digital strengths, promote its success stories on international forums, and focus on key target markets like the United States, where the demand for outsourcing and remote talent is substantial.

Moreover, alongside branding, ease of

doing business must be prioritized as well. While some procedural improvements have been made, many local IT firms continue to face hurdles that prevent them from operating at their full potential. The Special Technology Zones Authority (STZA), introduced in 2021, was designed to offer tax incentives, subsidized infrastructure, and regulatory simplification. Yet, more than three years later, most existing IT and ITeS companies are still unable to benefit from these zones due to delays in implementation and overly rigid criteria.

The government must act swiftly to operationalize STZs in a way that includes the broader IT industry. This includes establishing virtual technology zones that allow existing companies to participate, integrating STZA into local urban development plans, and relaxing land area requirements to include mid-tier cities. Furthermore, facilitating access for rental-based startups and SMEs by simplifying certificate requirements and offering subsidized land or infrastructure can help broaden participation and drive regional growth.

The government must also empower industry bodies to act as one-window facilitators for companies navigating STZA processes, which would reduce red tape and encourage formal sector expansion. Supporting small and medium-sized exporters with clear, consistent tax policies and streamlined regulatory support can make Pakistan more attractive to both local entrepreneurs and foreign investors.

For the IT sector, the talent, demand, and market potential are already in place. What’s missing is sustained government action to clear structural bottlenecks and broadcast attractive prospects of the sector to the world. If the right reforms are implemented now, the country can transform its tech industry from a growing segment into a cornerstone of its economic future. n

At PSO, circular debt stops growing

Consumer spending recovery helps stabilize company; better policy results in at least a stemming of the bleeding; and electric charging stations help prepare for the end of the age of oil

Profit Report

In a hopeful turn in a long-standing energy sector dilemma, Pakistan State Oil (PSO) has announced that circular debt – the entrenched, structural burden on Pakistan’s public energy companies – has not grown since February 2024 on its receivables from SNGPL. While overall receivables remain eye-wateringly high, this stabilisation represents a key milestone for the state-owned oil marketing giant, which also posted a solid 14% rise in profit for the first nine months of fiscal year 2025.

With total receivables standing at Rs732 billion as of March 2025, and late payment surcharge (LPS) claims exceeding Rs200 billion, the absence of new accruals on the SNGPL

side is a rare glimmer of fiscal discipline in a historically mismanaged space.

PSO reported a net profit of Rs15.27 billion in the nine months of fiscal year 2025, up from Rs13.40 billion in the same period last year – a 14% year-on-year increase. Earnings per share also improved to Rs32.52, up from Rs28.54. This rise came despite a 13% decline in sales revenue, from Rs2.67 trillion in the first nine months of fiscal year 2024 to Rs2.34 trillion this year.

The reason? While PSO and the broader industry suffered inventory losses due to falling international oil prices – down from USD 85.03/bbl to USD 76.43/bbl — the company managed to shield profitability through tight cost control, increased other income, and efficiency in operations. EBITDA excluding

inventory impacts rose to Rs74 billion from Rs68 billion.

For decades, Pakistan’s power and gas sectors have been choked by circular debt — a chain of unpaid bills stretching from end-users to power generators, to fuel suppliers like PSO. This has sapped liquidity, discouraged investment, and prompted repeated government bailouts.

But in what may be a sign of operational discipline, PSO management confirmed that since February 2024, there has been no fresh build-up of circular debt from SNGPL. A mutual understanding ensures payments are now made on a monthly basis. While OGDC and PPL receivables have increased, the stability on the SNGPL front is significant.

The principle owed by SNGPL alone is

Rs325 billion – nearly half of PSO’s total outstanding receivables. The company still awaits recovery of over Rs200 billion in LPS. However, this stabilisation, if sustained, could shift investor sentiment and ease PSO’s working capital pressure over time.

Founded in 1974, Pakistan State Oil was created through a merger of Pakistan National Oil and other government-owned entities, consolidating the country’s fragmented fuel supply under one umbrella. Today, PSO is the largest oil marketing company in Pakistan, with a network of over 3,600 retail outlets, 19 depots, nine installations, and 15 aviation refueling stations across the country.

The company handles more than half of Pakistan’s refined petroleum imports and manages over 1.24 million tonnes of storage capacity — a logistical backbone of national energy security. It also operates two lubricant blending plants with a combined annual capacity of 70,000 tonnes.

PSO has long served as both a commercial and strategic player in the energy value chain, balancing market competition with its role in ensuring uninterrupted fuel supply during crises — from geopolitical shocks to domestic floods.

In an era of energy transition, PSO is actively diversifying beyond fossil fuels. In 2024-25, the company launched electric vehicle (EV) charging stations in partnership with HUBCO Green at 25 locations, investing in chargers that cost between USD 20,000 and USD 25,000 apiece – significantly lower than earlier US and European technologies priced at over USD 50,000.

Management expects a 15–20% return on these charging stations, making them a feasible future revenue stream as EV adoption picks up pace. These stations are being complemented by “VIBE” convenience stores, aimed at increasing footfall and per-visit revenue.

To support the growth of its retail network, PSO commissioned 67 new outlets during the first nine months of fiscal year 2025. This expansion was facilitated by the lifting of OGRA’s restrictions, previously tied to storage capacity, which PSO enhanced through two newly constructed 25,000 MT tanks and the rehabilitation of four others.

Automation efforts have also been ramped up. PSO implemented automated dispatch systems at its Keamari terminal and entered long-term partnerships with Pakistan Railways at eight fueling sites, increasing efficiency and visibility across its supply chain.

According to PSO and industry data, the product mix of Pakistan’s liquid fuels continues to shift. In the first nine months of fiscal year 2025, nationwide consumption was dominated by Mogas (petrol) at 48.3% and High-Speed Diesel (HSD) at 41.9%. Furnace oil

dropped to just 5%, a welcome development for cleaner power generation, while jet fuel (JP-1) accounted for 4.3%.

PSO’s own product mix slightly diverges: Mogas accounted for 44% of its sales, HSD 43.7%, JP-1 was unusually high at 9.6% due to new aviation fueling contracts at Multan and Faisalabad, while furnace oil dropped to 1.9% — down from 4.2%.

This shift reflects broader economic and policy priorities. The reduced use of furnace oil is aligned with cleaner power goals, while higher JP-1 reflects an uptick in air travel and logistics. Mogas and diesel trends offer a proxy into middle-class consumption and industrial activity. Rising sales of petrol are a sign of stable consumer activity, even as smuggling — especially diesel from Iran — remains a challenge, estimated at 1,500 to 6,000 tonnes per day.

PSO’s future rests on its ability to navigate both legacy obligations and a changing energy landscape. Management has indicated a targeted organic growth of 3–5% in fiscal year 2026, based on retail expansion, digital payments, EV charging, and logistics automation.

That said, PSO faces stiff competition from private OMCs offering unsustainable discounts. While this pressured PSO’s market share in fiscal year 2024-25, management believes a realistic and sustainable share of 45–46% is achievable without chasing volume at the cost of margin.

The company also continues to explore

long-term import agreements, such as its recent deal with Azerbaijan’s SOCAR, which would provide cost visibility and supply stability. Additionally, its digital payments infrastructure — already capturing 12–13% of transactions, higher than peers — positions it well for a consumer-centric future.

EV adoption, while still nascent in Pakistan, is inevitable. PSO’s early entry into charging infrastructure gives it first-mover advantage. With capital investments becoming more efficient, and partnerships such as HUBCO providing green energy expertise, PSO could play a defining role in Pakistan’s transition.

The stabilisation of circular debt at PSO, even if only temporary, may mark a turning point in Pakistan’s energy finance story. Combined with solid profits, retail expansion, and forward-looking investments in EV charging, PSO appears to be turning a new page.

Yet challenges remain. The debt overhang is far from resolved. Margin pressures from smuggling and rival pricing tactics persist. But PSO’s multi-pronged strategy — from aviation to automation, from refinery logistics to renewable energy — underscores its intent not only to endure but to evolve.

As Pakistan — and the world — enters the twilight of the oil era, PSO’s story will be closely watched as a test case of how legacy giants can chart a new path in the age of energy transformation. n

Security Investment Bank lays out plans for Shariah compliance conversion

Having achieved financial stability, the financial institution seeks to capitalize on the Islamic finance growth in the country

Profit Report

Security Investment Bank Limited (SIBL), one of Pakistan’s smaller publicly listed investment banks, reported modest earnings growth for the calendar year 2024, supported by a strong investment performance and early signs of

success in its consumer financing strategy. The bank also revealed ambitious plans to fully transition into a Shariah-compliant institution, marking a potential turning point in its strategic direction and market positioning.

For CY24, SIBL posted earnings per share (EPS) of Rs1.35, up marginally from Rs1.31 in the previous year. In 1QCY25, EPS

stood at Rs0.26, slightly below the Rs0.30 posted in the same period last year, reflecting a more cautious start to the year.

Total revenue for CY24 came in at Rs126 million, a 9% decline from Rs139 million in CY23, driven by lower income from financing and reduced returns on securities. However, gains on the sale of investments rose sharply to Rs44 million from Rs15 million — a 193% increase — providing much-needed support to the bottom line. Administrative expenses were brought down significantly, by 32% year-onyear, helping sustain operating profitability.

The bank also booked a substantial unrealised gain of Rs34 million on investment remeasurement, further boosting profit before tax to Rs122 million — up 39% from the previous year. Despite higher taxation (Rs42 million, up from Rs11 million), net profit rose to Rs80 million from Rs77 million.

Security Investment Bank Limited (SIBL) is a small-scale but strategically nimble financial institution listed on the Pakistan Stock Exchange (symbol: SIBL). It operates within the category of Non-Banking Finance Companies (NBFCs) under Pakistan’s investment banking sector framework.

With a current share price of Rs8.40 and a market capitalisation of nearly Rs497 million, SIBL’s size is modest, but its reach is growing. The company has 59.14 million outstanding shares, of which 17.7 million are in free float. In the past year, its stock has ranged between Rs4.05 and Rs13.61, reflecting market optimism around its business model evolution.

The bank’s key activities include corporate and consumer financing, car leasing, and investment in a diversified portfolio of Shariah-compliant instruments including sukuk and treasury bills. In recent years, the bank has aimed to deepen its asset management partnerships and expand financial advisory services for clients.

In Pakistan, the term “investment bank” does not mirror the traditional Wall Street archetype. Under the regulatory framework of the Securities and Exchange Commission of Pakistan (SECP), investment banks are defined as NBFCs that engage in limited banking activities — chiefly asset-backed financing, leasing, corporate advisory, and portfolio investments.

Unlike commercial banks, investment banks in Pakistan are not allowed to accept deposits from the public. Their revenue streams tend to be generated from returns on proprietary investments, service fees, and structured financing. Importantly, Pakistani investment banks must register with the SECP and operate under a tailored regulatory code that emphasises capital adequacy, risk exposure, and corporate governance.

In this environment, the transition to a fully Shariah-compliant model — as SIBL

has now proposed — is not just a rebranding exercise but a fundamental shift in how financing products are structured, marketed, and risk-managed.

Security Investment Bank Limited was incorporated in the early 1990s, amid a wave of liberalisation that encouraged the growth of private sector financial intermediaries. It began as a conventional investment banking outfit, focusing on small-ticket leasing, private placements, and investment management.

Through the 2000s, SIBL expanded its operations into consumer finance, targeting middle-income households and SMEs. The company gradually built a portfolio that spanned both traditional and semi-structured products, including car leasing and asset-backed corporate financing.

In recent years, however, the shifting demographic and economic landscape — with rising demand for ethical and Islamic financial solutions — led the bank to pivot toward Shariah compliance. In 2024, SIBL submitted an official application to transition into a fully Shariah-compliant entity. As of May 2025, the application is under regulatory review.

The transition involves not only reclassifying existing products under Islamic contracts (e.g. Musharakah, Salam, Istisna) but also building internal Shariah oversight, risk models, and audit processes. For a company of SIBL’s size, the move represents both a logistical challenge and a competitive differentiator.

Looking ahead, SIBL’s strategic roadmap reflects an emphasis on diversification and liquidity management. The bank aims to expand its footprint in the high-yield consumer financing segment, particularly through Islamic auto and personal finance products. With the launch of financing tools structured around Salam (forward sale), Istisna (manufacturing contracts), and Running Musharakah (partnership-based working capital), SIBL is

targeting a larger share of Pakistan’s underserved yet faith-sensitive retail market.

The company’s total investment portfolio now stands at Rs700 million — a respectable size given its capital base. It includes a mix of sukuk (Islamic bonds), treasury bills, and various financing arrangements in the corporate and retail segments. Notably, a Rs120 million receivable related to the sale of real estate in DHA has already been partially recovered, boosting cash reserves and lowering balance sheet risk.

SIBL is also betting on the rise of outsourced financial planning. The management plans to expand its financial consultancy services, especially for corporate clients seeking liquidity management solutions. By channelling client surplus funds into high-rated Asset Management Companies (AMCs), SIBL hopes to build an annuity stream from service fees while strengthening client retention.

In terms of capital markets visibility, SIBL’s management has expressed confidence in maintaining a stable dividend outlook for CY25. This signal of earnings predictability may attract yield-seeking retail investors in Pakistan’s volatile equity environment.

Security Investment Bank may not be a household name, but it exemplifies the kind of specialised, agile financial firm that can thrive in Pakistan’s evolving capital landscape. Its pivot toward full Shariah compliance comes at a time when Islamic finance is expanding rapidly across the Muslim world — both as a consumer demand and as a regulatory priority. By streamlining its cost base, deepening its product mix, and targeting the high-growth Islamic retail segment, SIBL is positioning itself as a future-ready player. While earnings growth remains modest for now, its ability to adapt and focus may well secure its role in Pakistan’s next chapter of financial inclusion and innovation. n

PEL revenue bounces back to record highs

Company known mostly for its white goods brands has considerable success with its industrial electrical

equipment bids

Profit Report

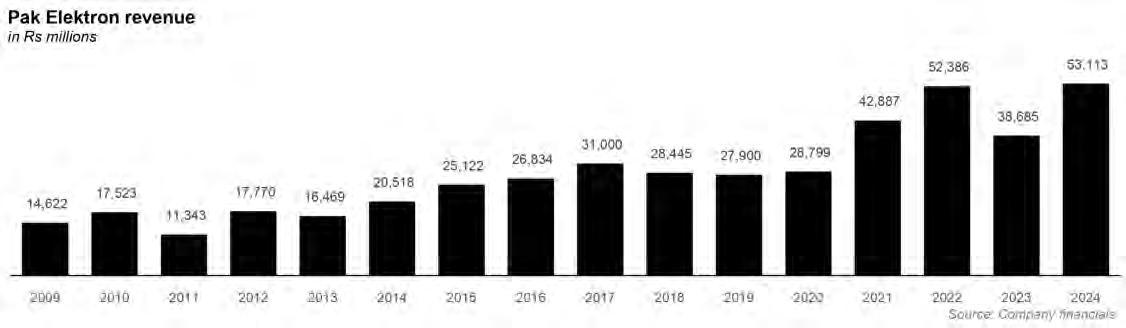

In a powerful sign of resurgence, Pak Elektron Limited (PAEL) has reported record-breaking financial results for the calendar year 2024, capping off a year of robust recovery for one of Pakistan’s most prominent electrical equipment and white goods manufacturers. The company’s net revenue soared to Rs53.1 billion – a 37% increase from the previous year – while net profit leapt by a stunning 79% to Rs2.37 billion.

This remarkable performance, particularly given the challenging macroeconomic environment, underscores the resilience of the domestic consumer appliances market and the increasing strength of Pakistan’s industrial base. As the company gears up for continued expansion in 2025, its resurgence holds broader implications for the economic narrative around consumer confidence and export-led industrial growth in Pakistan.

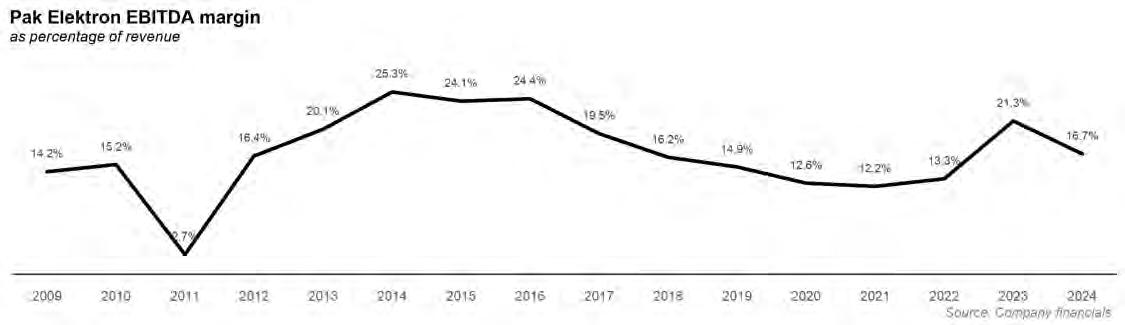

PAEL’s turnaround story in 2024 is nothing short of impressive. Net profit for the year jumped from Rs1.33 billion to Rs2.37 billion, with earnings per share climbing from Rs1.50 to Rs2.72. Gross profits rose by 27%, reaching Rs14.1 billion, despite a marginal dip in gross margins from 29% to 27% due to inflationary pressures and higher input costs.

Revenue growth was well-balanced across its two core segments: the Appliance Division contributed 57% to the topline, while the Power Division accounted for the remaining 43%. The Appliance Division alone reported gross sales of Rs40.1 billion, with another Rs13.1 billion already logged in Q1 of CY25 – signalling strong momentum heading into the new fiscal year.

The recovery of PAEL’s appliance sales is not just a corporate success story – it is also a window into the spending habits of Pakistani consumers. Appliance sales, particularly in categories like refrigerators, air conditioners, and deep freezers, witnessed substantial growth in volume, reflecting increased

consumer purchasing power and lifestyle upgrading, especially in urban areas.

In 2024, PAEL sold 220,082 refrigerators, 63,359 air conditioners, 28,779 deep freezers, and 122,657 other appliances. For CY25, the company has set aggressive targets, including 265,000 refrigerators (a 28% increase), 100,000 air conditioners (57% growth), and 40,000 deep freezers (33% growth). Such ambitious sales projections reflect underlying confidence in market demand and consumer appetite, even as price sensitivity remains a challenge in Pakistan’s inflation-prone economy.

Notably, 65% of washing machine sales comprised older models, though there is rising demand for automatic variants – suggesting a gradual shift in consumer preferences towards convenience and automation.

The strategic partnerships with global brands like Electrolux and Panasonic, forged in 2024, are expected to enhance design quality and brand perception in the white goods segment, enabling PEL to appeal to more discerning urban consumers.

Electrolux AB is a leading Swedish multinational home appliance manufacturer. Ranked consistently among the top appliance makers in the world by units sold, Electrolux operates under its own brand as well as a portfolio of others including AEG, Frigidaire, and Zanussi.

Electrolux specialises in manufacturing and selling a wide range of white goods such as refrigerators, washing machines, ovens, dishwashers, and vacuum cleaners. It serves both consumer and professional markets in over 120 countries.

The company has built a reputation for energy-efficient, ergonomic, and design-driven appliances. In recent years, Electrolux has also invested heavily in sustainability, focusing on lifecycle assessments and reducing environmental impact across its product lines.

Panasonic Corporation is a diversified Japanese multinational conglomerate with business interests in consumer electronics, home appliances, automotive solutions, indus-

trial devices, and housing systems.

Panasonic is well-known globally for its TVs, refrigerators, washing machines, air conditioners, microwave ovens, and personal care products. In addition to consumer appliances, the company plays a major role in automotive battery manufacturing, smart city development, and industrial automation systems.

Panasonic is a key global innovator in technologies promoting sustainability, smart living, and energy efficiency. Its partnerships span across various sectors, including collaborations with Tesla for lithium-ion battery production.

Both Electrolux and Panasonic bring deep technological expertise, trusted brand equity, and a global supply chain to their partnerships. Their collaboration with PEL is likely to introduce higher-spec products tailored for evolving Pakistani consumer preferences.

Pak Elektron Limited (PEL) is one of the oldest and most diversified players in Pakistan’s electrical and home appliance sectors. Founded in 1956, the company has evolved into a multi-divisional manufacturer with a wide portfolio of products ranging from household appliances to industrial electrical components such as transformers, switchgears, and energy meters.

The company is listed on the Pakistan Stock Exchange (symbol: PAEL) and boasts a market capitalisation of Rs40.68 billion, with over 923 million shares outstanding and a free float of 508 million shares.

Its two main business units – the Power Division and the Appliance Division – give it a rare advantage of capturing both industrial and consumer markets. The dual focus has not only helped diversify risk but also made PEL a barometer of both manufacturing activity and household consumption trends in Pakistan.

PEL’s history is intertwined with Pakistan’s post-independence industrialisation journey. Originally established through technical collaboration with AEG of Germany, the company started by producing electrical equipment like transformers and switchgears.

Over time, it diversified into home appliances, pioneering the local manufacturing of refrigerators and deep freezers.

The PEL brand grew into a household name in the 1980s and 1990s, becoming synonymous with reliability in a market that was largely dominated by imports. Despite facing competition from Chinese and Korean entrants in the 2000s, PEL maintained its market relevance through continuous product development and capacity enhancements.

Today, PEL commands market shares of 19% in refrigerators, 9% in air conditioners, 25% in water dispensers, and 4% in washing machines. In the industrial domain, it holds a commanding 90% share in power transformers, 17% in distribution transformers, 25% in switchgears, and 18% in energy meters.

One of the most compelling developments in 2024 was PEL’s entry into the global industrial supply chain. The company’s Power Division secured confirmed orders worth USD 44 million by May 2025, with a year-end target of USD 50 million.

Among the clients was none other than Tesla – a marquee name in the global tech-manufacturing ecosystem. While details of the order were not disclosed, its significance cannot be overstated. It signals PEL’s growing reputation as a credible supplier of high-quality electrical infrastructure.

The orders also include 3,800 distribu-

tion transformers (169% YoY growth expected in CY25), power transformers, and 544,000 energy meters – affirming PEL’s credentials as a serious industrial partner. With ongoing investments worth Rs1.5 to 1.8 billion to expand transformer manufacturing capacity, the Power Division is being positioned as a key engine for export-led growth.

This success is also tied to the company’s ability to pass on a 10% tariff increase under the current regime while maintaining competitiveness in both lead times and pricing. Export margins are reportedly higher than domestic ones, further incentivising this strategic focus.

Looking forward, PAEL’s management has laid out an aggressive expansion roadmap through 2025 and beyond. The company’s export ambitions are front and centre, with an annual export revenue target of USD 100 million. In addition, it aims to increase domestic market penetration across appliances, buoyed by urbanisation, population growth, and rising aspirations for modern living.

Product replacement cycles are shortening, and brand-consciousness is rising, creating a fertile ground for companies like PEL to innovate and lead. The introduction of new models and upgraded appliances – likely supported by its new partnerships – will be key to capturing mid- to high-income urban segments.

The company is also looking to boost LED lighting production, with a goal of manufacturing 15,000 units domestically – another nod to import substitution and energy efficiency initiatives.

In parallel, a broader shift is underway in the company’s sourcing strategy: while 70% of raw materials in the Appliance Division are still imported, PEL is exploring avenues for greater localisation. This transition, if successful, will not only enhance supply chain resilience but also buffer the company against foreign exchange volatility.

Pak Elektron’s record-breaking year in 2024 is more than just a recovery narrative – it’s a reaffirmation of Pakistan’s latent industrial and consumer potential. By leveraging both domestic demand and global opportunities, PEL has placed itself at the crossroads of economic transformation.

As the company navigates its next growth phase, its dual strength in industrial and consumer markets, strategic international linkages, and brand legacy make it one of the most exciting firms to watch in Pakistan’s evolving business landscape.

For investors, policy makers, and consumers alike, PEL’s success underscores a key message: with the right mix of innovation, strategic partnerships, and operational discipline, local firms can thrive – even in turbulent times. n

At Highnoon Laboratories, profits surge on export growth

Margin expansion, product line growth, and global

the company grow its top and bottom lines

Profit Report

Highnoon Laboratories Limited (HINOON), one of Pakistan’s most dynamic pharmaceutical firms, has announced its financial results for the calendar year

2024, revealing a stellar 35% increase in net profit that outpaced revenue growth – a clear signal of growing operating leverage and cost efficiency within the company.

The Lahore-based pharmaceutical company reported a net profit of Rs3.25 billion for CY24, a sharp increase from Rs2.40 billion in the previous year. Earnings per

markets

access help

share (EPS) rose from Rs45.35 to Rs61.41, underscoring strong profitability despite a competitive and volatile operating environment.

Highnoon’s revenue from customer contracts climbed to Rs23.3 billion, reflecting a 20% year-on-year increase from Rs19.4 billion in 2023. Gross profit grew by an even steeper

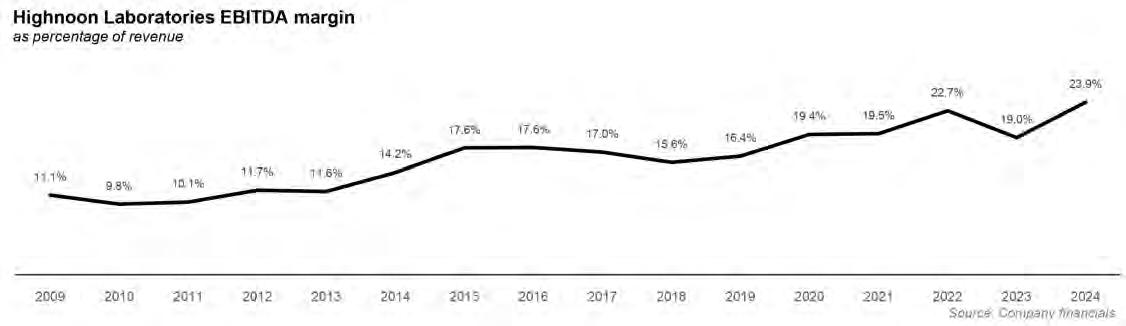

29%, supported by an improved gross margin of 51% – up from 48% in CY23. Analysts attribute this margin uplift to scale-driven efficiencies and strategic cost management in marketing and procurement.

These results suggest Highnoon is now firmly achieving operating leverage. Revenue is rising, but profits are growing faster.

Operationally, Highnoon saw an impressive 48% increase in profit from operations, climbing to Rs4.8 billion. Meanwhile, other income more than doubled, reaching Rs432 million, and despite a near tripling of finance costs, profit before tax rose 47% year-on-year.

Management attributed the expansion in margins to multiple factors. Firstly, the company’s marketing expenditure was strategically curtailed in certain therapeutic segments. Secondly, raw material costs remained favourable, partly due to softening Active Pharmaceutical Ingredient (API) prices amidst ongoing U.S.-China trade tensions. These trade dynamics allowed local manufacturers like Highnoon to benefit from improved import terms, especially as 90% of Highnoon’s APIs are sourced from Europe and China.

The government’s recent budgetary announcement to reduce customs duties on APIs is expected to support this margin trajectory further into 2025.

Highnoon continues to evolve as an innovation-driven enterprise. In 2024 alone, it launched 17 new products – 11 in chronic care and six in acute care – solidifying its positioning across key therapeutic domains. Leading brands such as Cyrocin (Rs1.9bn), Combivair (Rs1.8bn), and Tagipmet (Rs1.5bn) remain core revenue drivers. Management confirmed that over 50% of gross revenue is derived from just the top ten brands.

Looking forward, the company is targeting a 20–30% growth in sales for CY25, supported by a pipeline of upcoming launches, including biologics and advanced therapeutics. A major cornerstone of its expansion strategy is the development of a new

manufacturing facility at the Quaid-e-Azam Business Park. The design phase has been completed, and construction is expected to commence in the second half of 2025.

Highnoon’s leadership outlined ambitions to increase exports by 10% in 2025 and to ensure exports contribute 20% of total revenue within five years. Current exports account for 7% of sales, up from 5% in 2023, with the company distributing products to 19 international markets across Asia and Africa – including Kenya, Vietnam, Uzbekistan, Sri Lanka, and Mozambique.

The firm is also working on optimising its product portfolio, aiming for a balance between essential and non-essential medicines, to hedge against pricing and regulatory volatility.

Highnoon is widely recognised for its leadership in Cardiology, Diabetes, and Respiratory care. It ranked 12th among over 700 pharmaceutical firms in Pakistan as of December 2024. Its current product portfolio comprises Anti-Infectives (25%), Cardiovascular & Blood-related drugs (23%), Alimentary therapies (22%), Respiratory (17%), Diabetes (7%), Musculoskeletal (3%), and others (3%).

The company’s acute care focus is reflected in its portfolio split: 53% acute vs. 47% chronic care. Strategic investments in both therapeutic lines are designed to reinforce Highnoon’s standing in primary healthcare across Pakistan and enhance global competitiveness.

Founded in 1984, Highnoon Laboratories began its journey by acquiring a production facility in Lahore, initially to manufacture drugs under license from multinational corporations. Over the years, it transformed into a robust Pakistani-owned entity focused on manufacturing branded generics for both local and international markets.

Highnoon’s growth has outpaced the industry significantly. While the overall pharmaceutical market has grown at a compound annual growth rate (CAGR) of 10% over the past decade, Highnoon boasts

a 10-year CAGR of 23% in gross revenue. Its unit growth over the last three years stands at 7.3%, compared to an industry average of 2.9%.

This performance has been recognised with awards such as the Pharma PESA Award, further cementing its status as a top-tier pharmaceutical enterprise in Pakistan.

The backdrop to Highnoon’s stellar performance is a shifting regulatory environment in Pakistan’s healthcare sector. In recent years, the federal government has taken steps to deregulate the pricing of pharmaceutical products. Historically, Pakistan’s Drug Regulatory Authority tightly controlled drug prices, often causing misalignment between manufacturing costs and pricing ceilings.

This partial deregulation, while controversial, has been hailed by many industry leaders as a step towards aligning domestic prices with international norms and ensuring long-term viability for drug producers. It has also enabled companies to pass on some cost pressures to consumers, which in turn has incentivised further investment in product development and supply chain resilience.

According to analysts, this deregulated pricing regime – while still evolving – has benefited companies like Highnoon that possess strong brand equity, diversified portfolios, and export ambitions.

Highnoon Laboratories has demonstrated that strategic focus, global ambition, and disciplined financial management can deliver robust results, even in a challenging macroeconomic and regulatory environment. With a growing export base, sustained product innovation, and major infrastructure projects underway, the company appears well-poised to retain its momentum and possibly leapfrog into the top 10 pharmaceutical companies in Pakistan in the near future.

For stakeholders and investors alike, Highnoon’s 2024 performance underscores the potential of local champions to not only survive but thrive amidst deregulation, globalisation, and sectoral transformation. n

Globe Textile Mills owners sue OBS to terminate merger agreement

Pharma conglomerate aimed to use acquisition as a backdoor public listing, now appears to be unlikely to go through

Profit Report

In a significant development within Pakistan's corporate landscape, the majority shareholders of Globe Textile Mills Limited (PSX: GLOT) have initiated legal proceedings against OBS Pakistan, seeking to annul a previously agreed-upon acquisition deal. The lawsuit, filed in the Sindh High Court, alleges that OBS failed to fulfill certain undisclosed obligations stipulated in the merger agreement, prompting Globe Textile's owners to pursue termination of the contract.

The acquisition, initially announced in early 2024, was poised to mark OBS Pakistan's entry into the textile sector, diversifying its portfolio beyond pharmaceuticals. However, sources close to the matter indicate that OBS's inability to meet specific financial and operational commitments has led to the current legal impasse.

OBS Pakistan operates as a prominent entity within the nation's pharmaceutical industry. Established in 1963, the company has evolved into a key player, offering a range of healthcare products and services. OBS Pakistan functions under the umbrella of the OBS Group, a conglomerate with a significant presence in both Pakistan and Sri Lanka. The group is known for its strategic alliances with international pharmaceutical giants, including Merck & Co. Inc., Organon, and Schering-Plough.

The OBS Group's operations are diversified across several subsidiaries, such as AGP Limited and Aspin Pharma, each focusing on different segments of the healthcare market. AGP Limited, for instance, has been instrumental in marketing products from global partners like Mylan (USA) and Santen (Japan) within Pakistan. These collaborations have bolstered OBS's reputation as a reliable partner in the pharmaceutical sector.