08 From digital dollars to regulatory deadlock: Crypto’s moment of truth arrives

11 SNGP profits hit record high, curbing theft to 18-year low

12 Janana De Malucho: A case study in struggling textile spinning mills 14 The livestock sector is keeping Pakistani agriculture alive 19 Saif Power struggles in life outside guaranteed returns contracts 20 After stellar 2024, profits slowing down at Adamjee Life

The bidding war for Attock Cement

Asia Insurance doubles its profits, but no dividends yet

How big is the rave business in Pakistan?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

From digital dollars to regulatory deadlock: Crypto’s moment of truth arrives

Can Pakistan balance challenges and ambitions to become a crypto leader?

By Hamza Aurnagzeb

Pakistan has taken a bold step into the digital future by unveiling an ambitious national strategy to adopt cryptocurrency and blockchain technology. The country is signaling to the world its intent to become a serious player in the global digital asset economy through initiatives like the creation of a Strategic Bitcoin Reserve and high-level collaboration with the United States. For a nation like Pakistan that has perpetually remained constrained by financial instability, underbanking, and limited access to international capital, crypto offers not just innovation but reinvention.

This strategic shift promises significant benefits, including unlocking new sources of revenue, attracting investment into digital infrastructure, and empowering millions of unbanked citizens through decentralized financial tools. Moreover, Pakistan’s plan to convert surplus electricity into crypto-mining power and its outreach to global crypto leaders suggest a desire to leapfrog outdated financial systems and tap into a borderless, inclusive digital economy.

However, aspirations alone will prove to be inadequate. Pakistan faces considerable hurdles, from high electricity costs and poor infrastructure to regulatory uncertainty and international scrutiny over financial compliance. The country’s crypto strategy is as much a high-stakes bet as it is a vision for economic transformation.

In this story, Profit explores Pakistan’s crypto journey: the bold policy moves, the global alignments, and the structural weaknesses that need to be fixed to turn this grand vision into reality. As other nations cautiously step into the crypto era, Pakistan’s path offers a revealing case study of what it means to go all-in on the future of finance, while still wrestling with the realities of the present.

The Foundations

Powering the DeFi Revolution

The explosive rise of decentralized finance (DeFi) has redefined the very architecture of global finance and at the heart of this revolution lie two foundational technologies: blockchain and cryptocurrency. These are not mere buzzwords, they are the building blocks of a parallel financial ecosystem that is borderless, transparent, and permissionless.

At its core, blockchain is a decentralized digital ledger that records transactions across a network of computers in a way that is immutable and verifiable. This simple but profound innovation eliminates the need for

centralized intermediaries, banks, brokers, or payment processors, shifting power away from traditional institutions to users. Every transaction on a blockchain is traceable, timestamped, and irreversible, making fraud and manipulation significantly harder.

Cryptocurrencies like Bitcoin, Ethereum, and Solana serve as both the fuel and the currency of this new financial universe. While Bitcoin is celebrated as a store of value or “digital gold,” Ethereum introduced smart contracts, self-executing programs that run on the blockchain, enabling the creation of decentralized applications. These decentralized applications are the engines of DeFi platforms, powering everything from lending and borrowing services to decentralized exchanges (DEXs), synthetic assets, and stablecoins.

Implications for the DeFi applications are enormous as they allow anyone with an internet connection to lend, borrow, trade, and earn on their assets without relying on banks or financial institutions. In regions where traditional finance is inaccessible or unreliable, DeFi is not just innovation, it is effectively liberation. It unlocks capital for the unbanked, reduces fees, increases transparency, and provides full custody of assets to users.

Moreover, DeFi is programmable. This means that financial instruments can now be customized with logic-based conditions, enabling novel use-cases like instant loans, automated yield farming, and liquidity mining, all without human intervention. This is radically different from the slow, paper-heavy, and opaque systems of traditional finance.

However, DeFi, despite its great potential, also comes with significant risk. The absence of centralized authority or an intermediary means DeFi is also vulnerable to smart contract bugs, hacks, and volatility. Nevertheless, the sector is evolving rapidly, with improvements in audit practices, decentralized insurance models, and governance frameworks.

Ultimately, blockchain and cryptocurrency are not just enabling DeFi, they are redefining the idea of trust in finance. As the infrastructure matures and its adoption widens, DeFi could emerge as a permanent fixture of the global economy, offering a transparent, inclusive, and efficient alternative to the systems of the past.

Trump’s Strategic Turn Toward Cryptocurrency and Blockchain

While the United States was among the first nations to embrace cryptocurrencies, it took a bold new step in

March when President Donald J. Trump signed an executive order to establish a Strategic Bitcoin Reserve, accompanied by a broader digital asset stockpile that will include Ethereum, XRP, Solana, and Cardano. This initiative signaled a profound shift in how the U.S. government intends to engage with digital currencies in the future, where they will not merely be treated as seized assets from illicit activities, but as strategic holdings with long-term economic value.

Trump appointed tech investor and entrepreneur David Sacks to spearhead this effort, reflecting the administration’s aggressive pro-crypto stance and signaling its intention to lead in the blockchain era. The White House aims to build this reserve not only from seized assets but also through innovative acquisition mechanisms that minimize taxpayer burden. The core of the plan is to establish a transparent and centralized framework to track and manage federal digital holdings, especially Bitcoin, of which only 1.2 million remain to be mined out of the fixed supply of 21 million.

This move is part of a broader strategy to position the U.S. as a global hub for digital innovation, drawing in Web3 startups and crypto investors. Taking inspiration from Washington’s pivot, countries such as Argentina, Japan, and Hong Kong are reassessing their crypto policies and priorities. Pakistan has also established its own Pakistan Crypto Council, laying early groundwork to become a serious player in the emerging digital asset economy.

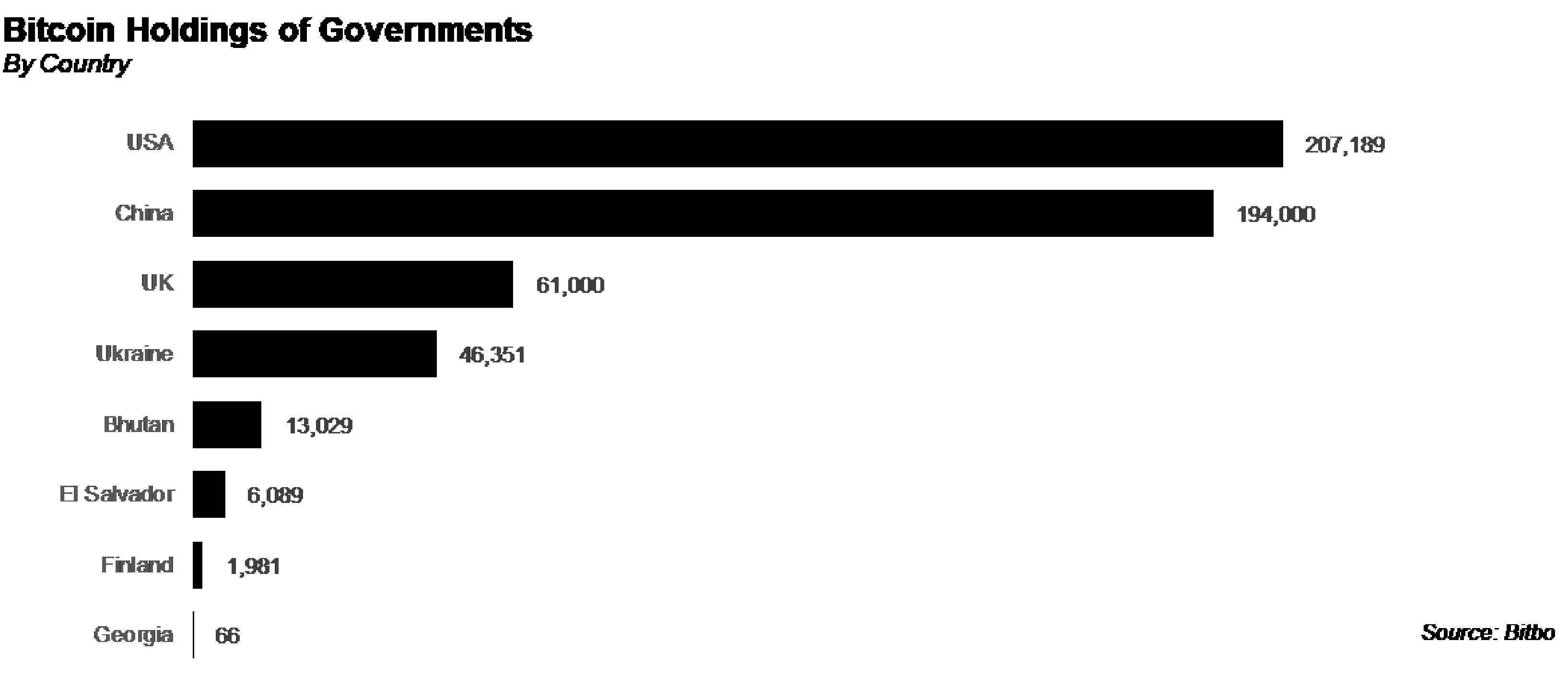

Governments around the world are no longer on the sidelines. Some have accumulated vast reserves of Bitcoin already through seizures or strategic purchases. The U.S. currently leads with 207,189 Bitcoins, followed closely by China at 194,000. Other nations like the UK, Ukraine, El Salvador, and Bhutan collectively hold over 128,000 Bitcoins, indicating a growing recognition of cryptocurrencies not just as financial instruments, but as strategic national assets.

Pakistan and U.S. Align on Crypto Strategy

Pakistan has taken a significant leap in its digital asset agenda, signaling a decisive shift towards becoming a leading force in the Global South’s crypto landscape. This vision took center stage during a recent high-level meeting in Washington between Bilal Bin Saqib, Pakistan’s Minister of State for Crypto & Blockchain and CEO of the Pakistan Crypto Council, and Robert “Bo” Hines, Executive Director of the U.S. President’s Council of Advisers for Digital Assets.

The meeting underscored growing bilateral collaboration on blockchain governance, digital currency policy, and regulatory synchronization. It comes on the heels of Pakistan’s unveiling of its Strategic Bitcoin Reserve (SBR) at the Bitcoin 2025 Conference in Las Vegas, positioning Pakistan among the first Asian countries to formally incorporate Bitcoin into its sovereign asset framework.

Pakistan’s strategy is not limited to symbolic gestures. The government has committed to mobilizing 2,000 megawatts of surplus electricity to power Bitcoin mining and AI-driven data infrastructure. This approach reflects a broader objective to convert underutilized resources into economic productivity, digital infrastructure, and employment. To reinforce its commitment, Pakistan also plans to establish an independent regulatory body to oversee its rapidly evolving digital finance ecosystem.

In Washington, discussions between the two sides focused on fostering innovation through decentralized technologies, achieving regulatory coherence, and using digital assets as tools for financial inclusion, especially among youth in underserved regions. The collaboration signals Pakistan’s intent to align with the United States, not only in policy frameworks but also in technological ambition.

Bo Hines, appointed by President Trump to shape U.S. digital asset policy, leads strategy alongside David Sacks as part of the White House’s broader pro-crypto shift. The meeting reflected mutual interest in building international partnerships to responsibly scale blockchain ecosystems and safeguard innovation.

As countries around the world race to define their roles in the digital asset economy,

Pakistan is positioning itself as a proactive player rather than a passive observer. With strategic reserves, regulatory infrastructure, and international outreach underway, the country aims to anchor its place in the next era of global finance and digital sovereignty.

Challenges and Risks in Pakistan’s Cryptocurrency Ambitions

Pakistan’s recent push towards cryptocurrency and crypto mining has sparked enthusiasm, but the initiative needs regulatory support to see the light of the day. The country lacks a clear and comprehensive policy framework to effectively guide the nascent sector despite bold government announcements and the creation of the Pakistan Crypto Council (PCC),

One of the biggest economic challenges for Pakistan is the high cost of electricity, which is critical for Bitcoin mining. Although the government has promised to allocate 2,000 megawatts of surplus power at concessionary rates to attract crypto miners, there are some voices questioning the practicality of this move. Pakistan’s electricity tariffs are among the highest in the region, and maintaining a competitive edge against other countries, particularly Gulf states offering cheaper and more reliable energy, will be difficult. The financial viability of largescale mining operations depends heavily on low-cost power, and to pull this off, Pakistan might have to turn to renewables.

Another significant challenge comes from the regulatory and compliance front.

Pakistan remains under the scrutiny from the Financial Action Task Force (FATF) for its weaknesses in combating money laundering and terror financing. The adoption of cryptocurrencies, which inherently facilitates pseudonymous transactions, poses potential risks for illicit financial flows. Thus, digital assets could become channels for money laundering and other financial crimes, without robust and FATF-compliant regulatory frameworks, further complicating Pakistan’s international financial standing.

Moreover, currently, there is no legal framework vetting cryptocurrencies position as a legal tender in Pakistan, nor does the central bank explicitly authorize the government’s strategic Bitcoin Reserve plans. This legal ambiguity is a challenge that would require a fix before the government moves forward with its crypto ambitions. The absence of clear legal protections for investors and users also creates uncertainty that could deter foreign and domestic investment.

Pakistan’s fervent embrace of blockchain and cryptocurrency signals an ambitious leap towards digital financial sovereignty, aligning itself with global leaders like the US in the crypto space. The country is positioning itself as a key player in the emerging digital economy with initiatives like the Strategic Bitcoin Reserve and international collaborations. However, this ambition must be tempered with realism as high energy costs, regulatory ambiguities, and FATF-related compliance risks present significant hurdles.

Hence, the country must prioritize coherent policy frameworks, legal clarity, and robust infrastructure in order to transform its crypto aspirations from a promising start into a sustainable transformation. n

SNGP profits hit record high, curbing theft to 18-year low

UFG losses fall below 5%, and the company has significantly slow its increase in accumulation of circular debt

Profit Report

Sui Northern Gas Pipelines Ltd (SNGP) has reported the strongest earnings in its six-decade history. Net profit for the financial year ending June 2024 surged to Rs18.98 billion (EPS Rs29.92), an 80% jump over the previous year’s Rs10.56 billion.

Management attributes the windfall largely to a dramatic reduction in unaccounted-for-gas (UFG) – the catch-all term that covers technical losses, leakage and outright theft. UFG slipped to 4.93% of volumes, the lowest level in 18 years . Every percentage-point shaved off this metric adds roughly Rs4–5 billion to the bottom line, analysts estimate, so an 18-year low translates directly into record profits.

Behind the headline number lies a threepronged campaign. Pipeline rehabilitation across Punjab and Khyber Pakhtunkhwa, focusing on vintage steel mains that accounted for two-thirds of distribution losses a decade ago. Advanced metering at bulk connections, which

has cut “commercial losses” (i.e., theft) by double digits. And targeted enforcement with law-enforcement agencies in known theft hotspots –particularly the textile clusters of Faisalabad and the brick-kiln belts outside Lahore.

These measures have pushed SNGP’s UFG below the 5% regulatory benchmark for the first time since 2006, narrowing the revenue gap that regulators previously disallowed when setting tariffs.

New molecules, new markets

While plugging leaks fattened margins, top-line growth was no fluke. Sales revenue climbed 27% to Rs1.37 trillion, bolstered by tariff revisions and fresh supplies from newly-connected fields. The company incorporated 95 mmcfd from the Shaheed Fashad Ashfaq cluster and tied in both Bannu-West I and the Wali gas field, adding badly-needed indigenous molecules at a time

when LNG import prices remain volatile.

Other fiscal year 2024 highlights include a distribution project in Gilgit – logistically SNGP’s most challenging undertaking ever – which brought piped gas to the mountain town for the first time, replacing thousands of inefficient LPG cylinders and diesel heaters.

A digital map and customer-service dashboard, giving field staff real-time leak detection and consumers live billing. And its LPG trading arm, launched during fiscal year 2024, which leverages idle LNG storage capacity to import pressurised LPG cargoes, adding a modest – but fast-growing – ancillary revenue stream.

Looking ahead, SNGP is rolling out the Kot Palak Gas Project – 265 km of new 24-inch pipe that will carry 45 mmcfd from yet another discovery – and a 63 km reinforcement line to ease chronic low pressure in Islamabad and Rawalpindi. Management expects these projects, financed from an annual capex envelope of roughly Rs30 billion, to push UFG even lower once completed.

SNGP’s history

SNGP traces its roots to the Sui Gas Transmission Company, set up in 1954 to handle the giant Sui field in Balochistan. In 1963 the northern network was de-merged and incorporated as Sui Northern Gas Pipelines Ltd, listing on the Karachi Stock Exchange a year later.

In the 1960s–70s, rapid grid expansion took place throughout Punjab; Lahore became the first Asian city entirely heated by natural gas. In 1985, the completion of the 1,060 km Sui–Multan–Lahore trunk line created a true north-south corridor.

In the 1990s, a privatisation drive stalled; the government retained a 56% shareholding, ensuring the firm remained majority-state-owned even after secondary offerings. During the 2010s, reliance on imported LNG grew as domestic output peaked; high imported prices exposed flaws in the tariff system and sowed the seeds of the circular-debt crisis.

In this decade, an aggressive UFG reduction push and partial integration into LPG trading mark a strategic pivot away from being a “plain-vanilla pipe company” toward a diversified gas logistics enterprise.

The circular-debt conundrum

Natural gas may burn clean, but its balance-sheet legacy in Pakistan is anything but. The gas circular debt – arrears that flow from regulated tariffs set below actual supply costs – surpassed Rs1.5 trillion by end-2023, according to Energy Ministry data. It originates when exploration & production (E&P) firms bill the gas utilities at cost-plus prices. Utilities are allowed to recover only a portion of that cost in consumer tariffs set by the Oil & Gas Regulatory Authority (Ogra).

Government compensation for the shortfall (the Gas Development Surcharge and subsidies) is delayed, forcing utilities to postpone payments to E&P firms.

SNGP’s management concedes that the “old circular debt remains a challenge” but insists that “new circular debt is not piling up” thanks to price increases enacted over the past two years and faster recovery of arrears from large consumers . The company even managed to pay more than 95% of invoices to E&P suppliers during fiscal year 2024, a feat unseen in the past decade .

Several factors have arrested the circular-debt build-up. OGRA now adjusts sale prices four times a year instead of once, narrowing the lag between cost spikes and retail recovery. There are also higher protected-consumer slab rates. Previously, nearly five million “protected” domestic users paid less than half

the cost of supply. After tariff rationalisation, that subsidy burden has shrunk.

The crackdown on theft has resulted in lower UFG. Every rupee saved through loss reduction trims the funding gap. And government cash injections linked to IMF performance criteria have compelled Islamabad to clear legacy liabilities in giant, one-off settlements.

As a result, while the stock of circular debt remains high, the flow – the monthly accretion – has slowed to a trickle.

At the heart of the turnaround is the government’s move toward a Weighted Average Cost of Gas (WACOG) regime. Under WACOG, locally produced gas and expensive imported LNG are pooled to produce a single blended cost, eliminating provincial disputes over “who pays for LNG.” The Senate passed enabling legislation in February 2022, calling it a “historic reform” that would secure energy supplies.

Implementation, however, proved tricky. In April 2024 Prime Minister Shehbaz Sharif formed an inter-ministerial committee to iron out the final framework and assess sector-wise impacts. Early estimates suggest WACOG could raise domestic tariffs by up to 91% while cutting industrial and power tariffs by roughly a quarter.

For SNGP, the policy promises three big wins. A blended price allows full cost passthrough, slashing future circular-debt accumulation. Cheaper gas for industry keeps large, credit-worthy customers on the grid, lifting volumes. And pedictable cash flows justify the Rs30 billion-per-year expansion plan.

Yet WACOG is politically fraught. Provinces rich in gas reserves fear subsidising

consumers in Punjab, and a sharp jump in household tariffs could trigger public backlash. Whether Islamabad can phase it in without social upheaval remains the billion-rupee question.

Can SNGP keep the momentum?

SNGP now supplies 69% of the country’s gas and 28% of its total primary-energy mix. With UFG already below 5%, future gains must come from bringing more discoveries online quickly – the Kot Palak pipe alone will add 45 mmcfd.

Digitally optimising pressure management can squeeze another fraction off losses. And diversifying into LPG and potentially hydrogen blends as global energy transition accelerates.

Analysts caution that finance costs climbed 40% in fiscal year 2024 on the back of high policy rates. If interest rates stay lofty, debt-funded capex could eat into margins. Even so, robust operating cash and improving receivables give SNGP more breathing room than most state-owned utilities.

In short, plugging leaks has bought SNGP time – perhaps the most precious commodity in Pakistan’s energy sector. Whether it can use that respite to reinvent itself before domestic gas reserves deplete and climate pressures intensify will define the company’s next chapter. For now, the record profit headline is not just a statistical quirk; it is proof that structural fixes, though often painful, do eventually pay dividends. n

Janana De Malucho: A case study in struggling textile spinning mills

Competition from imported yarn from China and Vietnam, and rising energy costs, caused losses to increase five-fold

Profit Report

Janana De Malucho Textile Mills Ltd (JDMT) closed its fiscal year 2024 books with a net loss of Rs467.6 million, more than five times the Rs80.3 million lost the previous year, and its loss-per-share ballooned from Rs11.61 to Rs67.61 per year.

Three mutually-reinforcing factors explain the plunge. There is the shrinking top-line. Net turnover slipped by Rs131.8 million as cheaper Chinese and Vietnamese yarn crowded the domestic market, eroding both volumes and pricing power.

The second major factor is a run-up in energy costs. Power and fuel expenses leapt 60% to Rs1.16 billion (fiscal year 2023:

Rs721 million) after a cumulative 150% hike in government-administered gas tariffs – up to Rs2,750 per MMBtu by February 2024.

Finally, there are the inflation-driven payroll pressures. A steep rise in wages and salaries, coupled with higher input costs, turned a Rs347 million gross profit in fiscal year 2023 into a Rs25 million gross loss and pushed the gross margin to zero .

Management’s response was drastic: the board suspended production citing untenable power tariffs, falling sales and piling inventories . A feasibility study for a 1 MW renewable-energy mix is on the table, but only conditional on new working capital becoming available.

Why JDMT’s woes mirror Pakistan’s spinning crisis

JDMT’s story is not an isolated mishap; it epitomises the broader unravelling of Pakistan’s spinning sub-sector.

Cheaper imports from China and Vietnam had flooded the market. Pakistan’s yarn imports quadrupled from 8 million kg in January 2024 to 32 million kg in January 2025, thanks to a tax regime that makes imported yarn duty-free while slapping 18% sales tax on local supplies.

Factory closures across the industry mean that the whole industry may be operating at a much lower scale than before. The All Pakistan Textile Mills Association (APTMA) says over 100 spinning mills – about 40% of capacity – have already shut, with the survivors running below half-tilt.

Then there is the energy and finance double bind. Record gas prices, chronic power cuts and policy-driven interest rates north of 20% have stripped mills of whatever labour-cost advantage they once enjoyed.

For years the sector competed largely on cheap labour: Pakistan’s monthly minimum wage is still a fraction of equivalent rates in China or Vietnam. But with sophisticated ring frames and auto-coners now standard in Asia, energy intensity – and the cost of capital required to upgrade – matter far more than headcount. As JDMT’s example shows, relying on low wages while paying world-beating energy prices is an untenable business model.

From Kohat pioneer to cautionary tale

Founded on October 6, 1960 by the late Lt Gen M. Habibullah Khan Khattak, Janana De Malucho set up shop in **Habibabad, Kohat – 53 km south of Peshawar – **with 12,500 spindles and 250 looms (jdm.com.pk). Commercial production

began in 1963, capacity doubled by 1968, and a further 25,000 spindles were added through the 1990s.

The mill once occupied a linchpin position in the upstream textile chain, spinning super-fine counts such as 80s and 100s combed yarn for exporters of premium fabrics. But a series of structural blows gradually chipped away at that niche

First, there was the 1980s textile crisis. Sector-wide turbulence saw JDMT shutter its weaving and processing units in 1983.

The next challenge was the quota-free world, post-2005. When quotas vanished under the WTO Agreement on Textiles & Clothing, global buyers consolidated supplies, favouring fully integrated vendors who could offer design-to-delivery solutions.

And now, there is the challenge of technological catch-up elsewhere. Today the same Murata and Rieter machinery JDMT boasts of is commonplace in competing mills across Asia, neutralising any early-mover advantage.

JDMT’s decision to halt production in 2024 thus completes a long arc – from pioneer to survival mode – capturing, in microcosm, the travails of Pakistan’s upstream spinners.

Moving up the value chain – the path to resilience

While spinners bleed, vertically-integrated or value-added players are faring demonstrably better. Faisalabad-based Interloop Ltd, for instance, grew textile and apparel exports 9.5% year-on-year in the first quarter of FY25, with knitwear sales up

14.1% despite its own margin squeeze . Nishat Chunian, Gul Ahmed and several home-textile exporters have reported similar resilience, aided by direct retail relationships, branding efforts and an ability to pass some costs downstream to international buyers.

The lesson is plain: “spin-only” mills that sell undifferentiated yarn into a global buyers’ market have little leverage. Conversely, firms that weave, dye, stitch and even design garments command higher margins, hedge currency swings with export invoicing, and bargain for energy at larger scale.

Energy parity is urgent. Bringing industrial gas tariffs closer to regional peers would stem the immediate haemorrhage. Selective protection, not blanket subsidies. APTMA’s call for anti-dumping duties on yarn may provide breathing room, but only innovation and integration will ensure long-term competitiveness. There is also a need to incentivise up-gradation. Concessional financing tied to modern looms, garment units and renewable-energy retrofits would accelerate the climb up the value ladder.

Management says it will reopen once “conditions permit”, exploring renewables and niche yarn varieties . Yet without a strategic pivot towards higher-value segments – or an outright takeover by an integrated group – the mill risks becoming another casualty in Pakistan’s thinning roster of standalone spinners.

In short, JDMT’s fiscal year 2024 numbers read like a balance-sheet autopsy, but the broader diagnosis is an industry outpaced by global change. The mills that survive the current storm will be those that spin less yarn and weave more stories – of design, branding and fully-fashioned garments – for the world’s demanding consumers. n

THE LIVESTOCK SECTOR IS KEEPING PAKISTANI AGRICULTURE ALIVE

At a time when Pakistan’s major crops are failing, the country’s livestock sector is thriving against all odds. Could it be enough to keep us food secure?

By Abdullah Niazi

In 1998 Pakistan was an international pariah. It was the most isolated the country had been in its entire history. Following the decision to go ahead with the Chaghai Nuclear Weapons test, the United States imposed sanctions on Pakistan. The sanctions were swift and harsh Before Pakistan conducted its tests, the Clinton Administration had been laying it on thick with the Pakistani government. There were offers of investment, military equipment, and even discussions of defence pacts. The Americans all but slid a suitcase stuffed with hundred dollar bills across Nawaz Sharif’s desk.

Which is why when Pakistan went ahead with their plans despite all the goodies dangled in front of the government, the condemnations from the US and its allies were fast. The decision was one that the Sharif administration laboured over for quite some time. The offers from the United States were attractive enough that the military leadership of the time had left it in the hands of the prime minister. Nawaz Sharif, who is actually a very decisive administrator despite his oafish reputation amongst the electorate, wrestled with what to do in the last few days of May. One former federal minister close to Mian Nawaz at the time recalls that his confidence in Pakistan’s agriculture sector helped him make the final decision.

“There was always an understanding that our people would not starve. Even if we were sanctioned to hell and back, Pakistan’s farmers would make enough for us to eat a basic meal of daal and chawal,” he says.

The isolation, as we know now, did not last long. Neither did Mian Nawaz’s government. In only three years, Mian Nawaz would be in exile and Pervez Musharraf would be standing next to George Bush as a major ally in the war against terror. But the confidence in Pakistan’s farmers that thrust us into becoming a nuclear power was not based on nothing.

After all, Pakistan is an agrarian economy. This little factoid is drilled into our heads from our earliest school days. It is plastered front and center in social studies books, and is most likely the first thing you learn about Pakistan’s economy and topography. This agrarian identity goes to the core of how we try to portray ourselves as a country.

Behind all the bluster, behind the terrors and blacklists and nuclear arsenals, there stands the folksy farmer. He wakes up with the sunrise, ploughs his field, feeds his cattle, wistfully roams his fields and takes in the fresh air. Disconnected and unconcerned with all of the chaos of the city, it is a good,

simple life. No matter what happens, he will tend the land and keep us all alive.

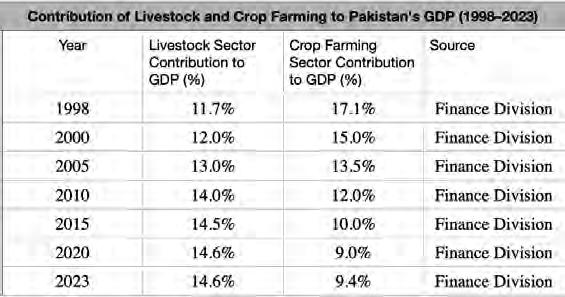

In 1998 agriculture was a major contributor to Pakistan’s GDP. Not only was it over a third of the GDP, if you count the cotton produced as a core product for the textile industry, it was contributing to more than 75% of all exports from Pakistan. What did this agriculture industry look like? Of the almost 30% that agriculture contributed to the GDP, crops accounted for around 18%. Livestock also did some heavylifting with an 11% GDP contribution, but it was clear that our ability to produce crops was our strength.

Fast forward a quarter of a century to today and that has changed drastically. Only a few weeks ago, this publication’s cover story declared Pakistan’s major crops were going bust.

For at least the past five years, confidence in Pakistan’s farming has plummeted. Reliance on the country’s crop farming infrastructure is (rightfully) not what it was in very recent living memory. And with major crops dipping by 13.5% since last year, our food security is no longer a guarantee. The reasons for this decline are manyfold and have been discussed by this publication ad nauseum. However, one thing that has escaped in-depth attention is actually a positive: Pakistan’s livestock sector.

The livestock sector actually accounts for at least 62% of the overall agricultural sector. That is a stark reversal from 1998 when crop farming accounted for 61% and livestock had a 39% share. How did we get to this point? On the one hand, Pakistan’s crops have been languishing for two decades. There has been a shocking lack of seed research, no concentrated effort to fight climate change, and inconsistent policies for farmers. That confidence in Pakistan’s ability to grow food seems to have become over confidence. And while crops have

the NAC was indicating Pakistan had a GDP growth rate of 2.68%. This was a revision from the government’s previous GDP growth projections which had predicted GDP growth rate at around 3.6% for 2025.

The problem is even these revised projections from the government of 2.68% are far from accurate. At best, they are naive and hopeful. At worst they are deliberately misleading. In the numbers the government has released, GDP growth in the first three quarters has been 1.37%, 1.53%, and 2.4% respectively. While this indicates an increase in the growth rate with every quarter, it is still well short of the government’s projections of 2.68%. In fact, the average growth for these first three quarters is less than 2%. It was pointed out almost immediately by a number of individuals that the government was relying on a significantly increased projection of GDP growth in the ongoing fourth quarter being 5.47%

The projection of a sudden tide changing final quarter raises questions. On top of this, there is really very little in the NAC’s report that explains why the government would be this hopeful. Perhaps nothing indicates the dire situation Pakistan’s economy is facing more than the state of the agricultural sector. Overall, the agriculture sector increased by a very meagre 0.56% in this year. This growth is not only partially based on projections, it is also only possible because Pakistan’s livestock sector saw a decent rise of 4.7% with fishing also increasing by 1.7%. What is concerning, however, is that major crops saw huge dips in production. Through a combination of senseless policies, water shortages, and increasing input costs, major crops crashed out and declined by 13.5%.

This recent crash is a marker of a trend that has been going on much longer. Look at the table below:

been taken for granted, a series of private enterprises have turned livestock into a thriving business. Pakistan produces milk, meat, and eggs in massive quantities. Most of this goes to feeding our population, but value added and export oriented products have been consistently increasing. All of this has happened despite, not because of, official policymaking.

A changing trend

Last week, the National Accounts Committee (NAC) released the latest GDP data for Pakistan. Immediately there was attention on the fact that

It shows us the distribution of which sector within the agriculture industry has what share. But then take a look at a compilation of data taken from data available with the finance ministry and many successive editions of the Pakistan Economic Review:

The data shows that fromm 1998 to 2005, the livestock sector’s contribution to GDP gradually increased, while the crop farming sector’s share declined. After 2005, the livestock sector continued its upward trajectory, reaching 14.5% by 2015. Concurrently, the crop farming sector’s contribution further decreased, highlighting structural changes in the agricultural sector. By 2025, the livestock sector maintained its 14.6% contribution to GDP, while the crop farming sector’s share remained at 9.4%. This stability suggests a consolidation of livestock’s dominant role in the agricultural economy.

How livestock took over

We have here a very simple equation. In the last twenty-five years, livestock and crops have switched positions in Pakistan’s agricultural industry. Why has this happened? It might help to understand what the agricultural sector actually looks like right now.

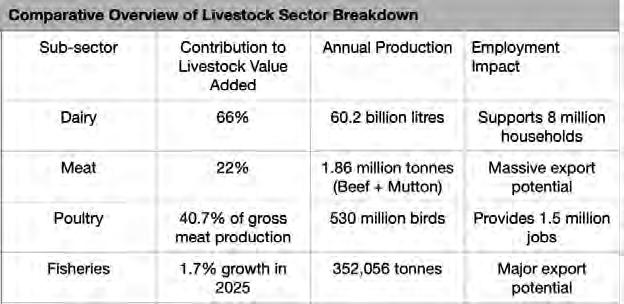

Dairy farming

The single biggest sub sector of the livestock sector is dairy farming. Every year, Pakistan produces more than 60 billion litres of milk making this country one of the largest producers of milk in the world. The big reason for this is that Pakistanis drink a whole lot of milk.

There are essentially three kinds of milk products available on the market. The first is your typical fresh milk from the gawala. Small peri-urban farmers raise herds that are often only three animals and sell to distributors which then sell the milk fresh on a daily basis to homes and milk shops. The second kind is fresh ‘pasteurized’ packaged milk. This is sold by companies like Anhaar and Prema. Pasteurized milk is usually sold by companies with large herds that use machines to milk their cows, heat them at a low temperature, package them, and sell them in retail stores. Anhaar, which is owned by the Sharif family, has a herd of 4000 cows for example. This particular product

while processed is still fresh. It needs to be refrigerated and has a (chilled) shelf life of a few days. Then there is Ultra High Temperature (UHT) Processed milk. This includes brands like Nestle’s Milkpak and Friesland’s Olpers brand. Milk that is UHT treated is heated at intense temperatures in short bursts, which kills microorganisms before being quickly cooled. The milk is then packaged in an airtight way, giving it a much longer shelf life and no need for refrigeration before the milk is opened.

All three kinds of milk have their own perceptions, problems, concerns, and benefits. All of the different players in the market play on these factors to try and promote their own product. The gawalas, for example, claim their milk is fresh and natural. However, large milk companies point towards the idea that milk is produced in unhygienic conditions and is often watered down.

Most of the milk produced in Pakistan comes from small farmers with herds of 5-15 animals. These farmers sell to shops, households, as well as large milk producers. Nestle, for example, does not have its own herd. Instead, they source their milk from 190,000 dairy farmers in Sindh and Punjab. Olpers does the same, sourcing milk from local farmers before transporting it to their facilities in Sahiwal in Punjab and Sukkur in Sindh. They also buy from large scale dairy farmers. Many of these big farms are owned by influential political families. The business itself involves imports (both of animals and bull semen) from places like Australia, and significant investment.

It is also a business that makes sense for the landed elite, who have the space and capital to invest in the infrastructure for a large-scale farm including machines, breeding facilities, and veterinary costs. In South Punjab, for example, one of the largest dairy farms is owned by Jahangir Tareen with a herd of nearly 2800 animals in Rahim Yar Khan. Prema

Milk, the original pasteurized packaged milk brand that launched in 2008, is owned by the Chauhdry family of Gujrat. Prema in particular prides itself for only using pure Australian Cow’s milk. Similarly, as we have mentioned before, the brand Anhaar and its herd of 4000 animals is owned by the Sharif family.

Meat industry

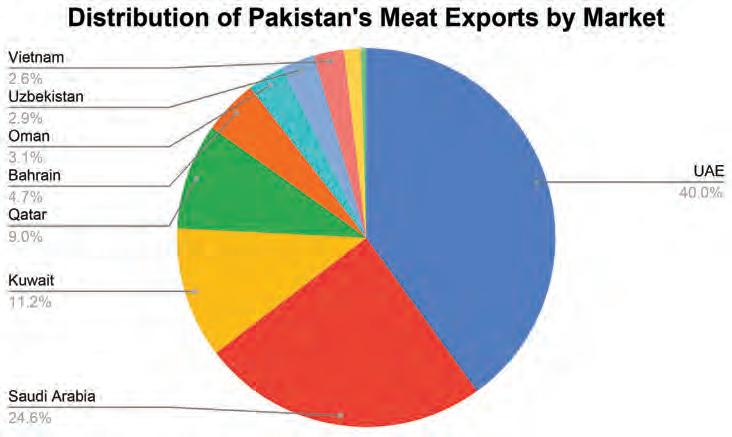

After dairy, the next biggest contributor to the sector is meat. Pakistan’s meat industry stands at a critical juncture, facing both significant challenges and promising opportunities. Despite being a major producer of meat, with an output of 5.809 million metric tons in 2024, the country’s export potential remains largely untapped due to structural issues plaguing the sector. These challenges range from the absence of a robust livestock traceability system to the prevalence of Foot and Mouth Disease (FMD), and from the lack of large-scale feedlots to the persistence of informal, undocumented supply chains.

of its meat despite the prevalence of FMD in its livestock. Pakistan’s export destinations are led by six GCC countries, which include the United Arab Emirates, Saudi Arabia, Qatar, Bahrain, Kuwait, and Oman. These countries account for $444 million (92.7%) of Pakistan’s total meat exports, while 88% of Pakistan’s meat exports are concentrated in the category of fresh or chilled carcasses and half carcasses for both beef and mutton, with beef and mutton representing shares of 82.3% and 17.7%, respectively.

Meat production for the domestic market continues at a massive scale. Pakistan produced around 5.809 million metric tons of meat in 2024, where 2.630 million metric tons of beef, 2.362 million metric tons of poultry meat, and 0.817 million metric tons of mutton were produced.

Pakistan’s meat exports are limited to only a handful of markets that permit the import

Source: International Trade Centre

Pakistan is the largest supplier of fresh or chilled bovine meat to the GCC countries, it controls a market share of around 45%. Fresh or chilled carcasses of bovine meat exported to GCC countries amounted to $348.417 million, approximately 72.7% of the total meat exports of Pakistan in 2023. Nevertheless, this moat is limited to the segment of bovine meat products that have not been processed further like carcasses, half carcasses, and cuts with bone in. Pakistan has no share in the space of boneless fresh or chilled bovine meat segment.

Poultry

Chicken is important to Pakistan, and this is not a particularly old phenomenon. Commercial poultry production in Pakistan started in the 1960’s and has been providing a significant portion of daily proteins to the Pakistani population ever since. In fact, up until the 1960s, chicken was a meat more expensive than beef.

Prior to 1963, all chickens were of the colourful ‘desi’ variety that we still hear of today that has gamier, redder meat compared to the farm-fed white chickens often referred to as “broiler.” Prior to 1963 the native breed “Desi” was mainly raised which produced a maximum of 73 eggs per year under local conditions. In 1966, however, there was a major breakthrough. The department of Poultry Husbandry at the University of Agriculture in Faisalabad had been working on a new breed of chicken to which they gave the name “Lyallpur Silver Black” which was evolved at this time. This new chicken was capable of gaining 1.4 kg weight in 12 weeks of age under favourable management and feeding conditions. It also

produced more than 150 eggs per year.

As a result of this new variety of chicken, more people took up poultry farming and chicken meat became more frequent in the market and also proved to be cheaper. Watching this, the government introduced a number of favourable policies that allowed chicken farming to grow as a business. In this same era, the government announced a tax exemption policy on the income derived from poultry farming. Pakistan International Airlines (PIA) in collaboration with Shaver Poultry Breeding Farms of Canada started the first commercial hatchery in Karachi. Simultaneously, a commercial poultry feed mill was started by Lever Brothers (Pvt), Pakistan Ltd., at Rahim Yar Khan, which was followed by other pioneers like Arbor Acres Ltd. Poultry research institutes were also established at Karachi and Rawalpindi through Food and Agricultural Organization (FAO) of the United Nations to facilitate research services specifically concerning disease control programmes.

As this initial boost got the sector on its feet, it very quickly began to institutionalise. A major milestone in this was the establishment of the Federal Poultry Board in 1972. Then came a boom. The government of Sindh followed a policy to attract investment in poultry farming by offering estate land under 10 year leases. At the same time, the nationalisation of other industries contributing the entry of capital into the poultry industry, particularly in the Punjab, resulted in the poultry production boom. Commercial egg production increased from 624 million eggs in 1976 to 1223 million eggs in 1980. Broiler production increased from 7.2 million birds to 17.4 million birds during the same period.

Over the next few decades, the poultry industry faced its share of issues. Disease in the birds and crumbling infrastructure all contributed to the boom being followed by a bit of a slump. Despite this, chicken very quickly became the main source of protein for most Pakistanis and was cheaper than both mutton and beef. In a 2020 report, the planning commission even pointed this out. “Mutton prices are about 100% higher than beef prices whereas poultry prices are 50% lower than beef (Table 3). This price trend has induced poultry meat consumption while discouraging mutton and beef consumption during the period,” it reads.

“The prices of all types of meat are increasing, but the increases in mutton and beef prices are the highest, higher than the CPI, while the increase in poultry price is lower than that in CPI. Partly beef and mainly poultry can fill the gap created by the declining mutton consumption in the country because of the exorbitant increase in price of the latter and relatively cheaper prices of the former two

meats. A common observation is that the red meat butcher shops have added chicken to their offering.”

Poultry has attained an incredible status in the rural economy and is the second largest industry in Pakistan and means of livelihood for millions. Poultry meat and eggs are cheaper sources of protein. It contributes about 29% of the total meat production in the country and plays a vital role in soothing demands of mutton and beef.

The poultry sector plays a crucial role in Pakistan’s livestock industry, contributing around 40.7% of the country’s total meat production. This makes it one of the most important sub-sectors, reflecting the growing demand for poultry products like chicken and eggs. With over 530 million birds produced annually, the industry is expansive, incorporating both commercial operations and rural poultry farming. The sector has experienced steady growth, driven by increasing consumer demand, particularly in urban areas, where poultry products are an affordable and preferred source of protein. The expansion of poultry farming has led to the development of a comprehensive supply chain, supporting everything from hatcheries to processing plants, further solidifying its importance in the nation’s agricultural landscape.

Economically, the poultry industry provides employment to more than 1.5 million people across various roles, from farm workers to processing staff. Over the past decade, the sector has grown at an average annual rate of 7.3%, driven by both domestic consumption and export potential. This growth has been fueled by improved farming practices, better feed production, and advancements in breeding techniques. As a result, the poultry sector not only plays a vital part in the nation’s food security but also serves as a significant contributor to rural livelihoods and the broader economy. The sector’s continued development promises to meet both local and international demand, ensuring its key role in Pakistan’s agricultural future.

The problems

This success in the agriculture sector has been achieved through private enterprise. In the dairy sector you have countless small herds all over the country used by subsistence farmers, but more than a few major players that have their own dairy farms. When it comes to meat, listed companies like The Organic Meat Company Limited have made strides in opening Pakistani meat up not just to the GCC market, but also to newere markets like China. When it comes to poultry, companies like K&Ns have been leaders in value added products such as frozen and processed chick-

en, which they also do very well to export. While fisheries are still a nascent industry, the farming of high quality crabs and shrimps along with traditional fish is seeing an increasing trend in Pakistan. But all of these industries face their own issues.

Take dairy for example. In the last budget, the government imposed an 18% GST on milk. This made the sale of packaged milk fall by at least 40% as people once again shifted to the cash based gawala system, but this has serious health implications as well. Continued lobbying from the packaged milk industry continues to make this an environment that is not exactly stable.

Pakistan’s meat export potential is hindered by several systemic issues. One major challenge is the lack of traceability in livestock due to the absence of a tagging system and national livestock database, which farmers are unwilling to invest in. Additionally, the meat value chain remains informal and fragmented, making traceability even more difficult.

Another issue is the prevalence of Foot and Mouth Disease (FMD) due to inadequate veterinary infrastructure, especially in rural areas. Without a national FMD control program or disease-free zones, Pakistan struggles to meet the stringent requirements of high-income markets like the U.S., EU, and Japan.

Farmers also focus on livestock for milk production rather than meat, leading to a lack of large-scale feedlots. This results in poor feed conversion rates and low meat yields. Furthermore, the smuggling of livestock into neighboring countries exacerbates the domestic supply shortage, despite a government ban on live animal exports since 2013.

These structural barriers prevent Pakistan from tapping into its vast meat export potential.

Poultry has its own list of issues. Take the years between 2021-25 for example. During this time, the government banned the import of soybeans from the United States. This was a major issue because US Soyeabs, produced through GMO seeds, are the cheapest way to effectively increase the protein quality and volume in chicken.

These are only a few examples. Of course, the data discussed in this story has only been possible because of the enterprising spirit of a large number of people, in particular the millions of subsistence dairy farmers that are the backbone of this growing industry. They, along with larger corporations that have played a role in this change, deserve to have their stories told separately on a later date. For now, what we do know is Pakistan’s livestock industry is looking up. With our crops facing a crisis larger than we have the capacity to deal with, our food security might start depending more and more on our herds and bird farms. n

Saif Power struggles in life outside guaranteed returns contracts

Profits exist, but margins are meager relative to the old heyday, and the company has no clear plans for growth

Profit Report

Saif Power Ltd (SPWL) began calendar-year 2025 with what at first glance looks like a respectable rebound. First-quarter net turnover rose 40% year-on-year to Rs1.49 billion, yet the surge in fuel and maintenance costs meant cost of sales almost doubled (+99%) and the gross margin collapsed from 43% to 19%. After finance costs, the company eked out only Rs36 million in net profit – just 2.4% of revenue – even though that figure is 16-times the Rs2 million booked a year earlier.

Look further back and the picture is no prettier. Full-year 2024 revenue halved to Rs9.67 billion from Rs19.04 billion in 2023 as plant utilisation sank to an abysmal 8.23%, despite an impressive 94.2% availability

factor. In other words, the 225 MW combined-cycle plant was mechanically ready but seldom dispatched by the grid operator.

The perpetual curse of Pakistan’s independent power producers – ballooning receivables from the Central Power Purchasing Agency (CPPA-G) – is back with a vengeance. Although a landmark settlement in early 2025 released Rs5.2 billion of overdue invoices, receivables had already rebuilt to between Rs2 billion and Rs2.5 billion by May . As of 31 December 2024, the figure still stood at Rs8.2 billion, even after management voluntarily waived Rs1.36 billion in late-payment interest to secure the deal .

The cash crunch is visible in shareholder payouts. The board declared no final dividend for 2024, leaving the annual distribution at just Rs1.25 per share (a 12.5% payout ratio) versus Rs4.29 per share the

previous year – dividends financed almost entirely from capacity-payment cashflows rather than genuine operating profit.

Operationally, Saif’s plant retains enviable engineering credentials: reliability was 100% and availability 94% last year, thanks to General Electric’s long-term operations and maintenance contract. But high technical uptime is of little use when system dispatch drops in favour of cheaper renewables or captive generation.

The shifting ground under Pakistan’s IPPs

For two decades, Pakistan wooed investors with 30-year power-purchase agreements (PPAs) denominated in dollars and indexed to inflation – a formula that guaranteed double-digit returns so

long as plants remained available. That bargain is unravelling.

In 2024 Islamabad struck a deal with Saif Power and other 2002 Power Policy IPPs to rebase returns and cut future capacity-payment obligations. Return on equity will now be paid on a “hybrid take-and-pay” basis; O&M and working-capital allowances have been trimmed; and insurance premia are capped at 0.9% of EPC cost. In exchange, the government withdrew arbitration claims and promised to clear verified receivables quickly.

Call it what it was, though: negotiation at the barrel of a gun. The government functionally reneged on its sovereign guarantees and contracts, and the power companies had no choice but to agree to the new regime in the hope of making some meager amounts of money from their massive investments in power generation.

The overhaul forms part of a broader attempt to arrest Pakistan’s Rs2.4 trillion circular-debt mountain. The authorities hope the Competitive Trading Bilateral Contract Market (CTBCM) – essentially a wholesale spot market – will eventually replace the single-buyer model. Saif has signalled it is willing to participate, but only through direct bilateral deals with bulk consumers rather than selling everything through CPPA-G.

For generators like Saif, the paradigm shift is existential. Under the old rules, fixed capacity payments insulated equity returns even when dispatch was near zero. The new framework preserves some capacity compensation but increasingly exposes IPPs to demand risk – and to the merit order of cheaper solar, wind and hydropower.

Analysts estimate that if utilisation remains stuck below 10%, Saif’s annual net margin could hover in the low single digits despite the tariff reset. Management’s presentation to investors acknowledged as much, warning that “capacity utilisation is expected to remain under pressure due to the shift towards renewables, economic slowdown and weather conditions”.

A short corporate

history: from textile dynasty to power pioneer

Saif Power springboards from the Saif Group, a diversified conglomerate founded in the 1930s with roots in textiles, healthcare and real estate. In 2004 the group incorporated Saif Power Ltd to develop a 225 MW, dual-fuel (natural-gas and high-speed diesel) combined-cycle plant near Sahiwal, Punjab. Financial close was achieved in 2007; commercial operations began in 2010 under a 30-year PPA with the National Transmission & Despatch Company (NTDC).

The project’s original capital cost of $211

million was financed by a consortium led by the Asian Development Bank. Technology partners included GE France for the two LM6000 gas turbines and Siemens Sweden for the steam turbine, while GE still provides long-term O&M services. For its first decade Saif Power epitomised the success of Pakistan’s IPP model: predictable US-dollar returns, generous debt amortisation windows and limited operational headaches. That idyll ended when slower demand growth, a surge of imported coal and RLNG capacity, and foreign-exchange devaluation combined to make capacity payments fiscally unsustainable.

Where does Saif go from here?

With the tariff notification for the renegotiated contract still pending at the energy regulator (NEPRA), shareholders have little visibility on future cashflows. Meanwhile, the company is studying Pakistan’s nascent open-access rules to sign direct supply agreements with large industrial buyers – an option that could yield higher dispatch but will also expose Saif to counterparty and fuel-price risk.

Management is also counting on a macro-economic recovery to lift demand in 2025 as inflation and interest rates ebb. Yet even under that optimistic scenario, analysts forecast that net profit margins will remain in the 3–4% range, far below the double-digit returns enjoyed under the original PPA.

In the interim, Saif has pledged to distribute “any excess surplus cash” to investors, a tacit acknowledgement that growth capex makes little sense until the CTBCM architecture is fully operational.

Saif Power’s latest numbers tell a cautionary tale. Revenue is rising again as dispatch inches up, but almost all of that gain is being eaten by fuel, maintenance and debt-service costs, leaving shareholders with crumbs. The plant itself remains a well-run, reliable asset; the problem is an evolving policy landscape that values flexibility over guaranteed capacity.

As Pakistan rewrites the rulebook for private power generation, Saif Power must learn to thrive on efficiency, customer intimacy and fuel-management savvy rather than the comfort of locked-in returns. Whether the company can complete that transformation before receivables once again overwhelm its balance-sheet will determine whether the coming decade looks any brighter than the one just past. n

After stellar 2024, profits slowing down at Adamjee Life

Growth will be more challenging as markets slow down and heavy bond portfolio is likely to see smaller gains in a low-interest rate environment

Profit Report

After dazzling investors with a 71% jump in earnings per share to Rs6.22 during calendar-year 2024, Adamjee Life Assurance Company Ltd (ALIFE) has hit the brakes. In the first quarter of 2025 (1QCY25) the insurer’s EPS slid to Rs0.49, less than half the Rs1.22 earned in the same period last year (SPLY).

The top line told a very different story. Gross written premium soared 45% yearon-year to Rs9.47 billion, while net premium climbed by a similar margin to Rs9.29

billion . Yet profits shrank because costs rose even faster. Profit before tax plunged 60% to Rs201 million as higher claims, acquisition expenses and a hefty actuarial provisioning charge ate into margins . Net claims advanced 21%, broadly in step with the expanding book, but the change in insurance liabilities jumped 17%, reflecting more conservative actuarial assumptions under the impending IFRS 17 regime. Financing cost, though small in absolute terms, spiked almost nine-fold on short-term working-capital lines – an echo of Pakistan’s double-digit interest-rate cycle .

An equity research analyst note by

Chase Securities, a brokerage firm, lists three near-term headwinds: The first is falling interest rates. With the State Bank expected to begin an easing cycle in the second half of the year, the reinvestment yield on Adamjee Life’s bond-heavy portfolio will decline, squeezing the investment margin that underpinned 2024’s bumper results .

There is also the sales-tax cloud. A long-running dispute over provincial sales tax on insurance and re-insurance services remains sub judice, creating uncertainty around expense assumptions and pricing .

Finally, there is the cost of compliance. The company is midway through Phase 4 of its IFRS 17 parallel run, working with an international consultant on new actuarial and accounting systems – a project that is raising overheads before it delivers any operational benefit .

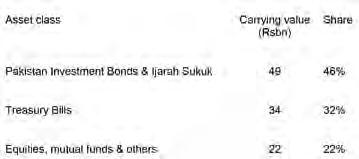

A bond-heavy balance-sheet

Despite the earnings wobble, Adamjee Life’s investment war-chest continues to swell. Total invested assets stand at Rs105.75 billion, almost 17 times the company’s reported equity. The portfolio leans heavily towards sovereign fixed income:

This conservative mix served shareholders well during 2024’s high-rate environment, delivering a revaluation windfall that fattened the bottom line. The flip-side is growing re-investment risk: maturing short-term T-bills will have to be rolled over at progressively lower yields if the policy rate retreats, echoing the analyst’s caution that “sustaining the high investment returns witnessed in recent years” will be difficult.

Management is nonetheless guiding to gross premiums of Rs30.97 billion and an underwriting surplus of Rs2.56 billion for fullyear 2025, betting that volume gains and fee income from new digital distribution channels will soften the investment hit .

From joint venture to fully-fledged subsidiary

Adamjee Life was incorporated on August 4, 2008 and commenced business in April 2009 as a joint venture between Adamjee Insur-

ance Company Ltd (AICL) and South Africa’s Hollard Life Assurance Co Ltd – itself acting on behalf of Dutch investor IVM Intersurer BV. AICL initially held 74% but gradually injected fresh capital and in 2019 bought out the foreign partner, turning Adamjee Life into a wholly-owned subsidiary before finally listing it on the Pakistan Stock Exchange in 2022 (dps.psx.com.pk).

Key milestones include its 2016 grant of a licence for Window Family Takaful operations, allowing the company to sell Sharia-compliant products, its 2021 successful Rs1.5 billion rights issue to fund digital infrastructure and meet solvency buffers, and itsrapid scale-up of micro-insurance and embedded-insurance partnerships with telcos and fintechs, broadening the client base beyond the traditional urban salaried segment in 2023–24.

While still modest in size compared with market leader Jubilee Life, Adamjee Life has carved out an enviable niche in unit-linked savings plans marketed through banks – an area in which it claims a 22% share of the bancassurance market .

The life insurance market

Pakistan’s life-insurance landscape presents a paradox: a population of 240 million, but penetration below 1% of GDP – just 0.87% in 2022, compared with roughly 4% in India and China. The sector remains dominated by state-owned State Life, although eight private insurers – including Jubilee, EFU Life, Adamjee Life and Alfalah Life – have captured most of the growth over the past decade.

The low base offers enormous upside. A median age of 22 fuels demand for education and retirement products. Smartphone penetration above 50% enables mobile-first micro-policies. And the Securities & Exchange Commission of Pakistan (SECP) is rolling out risk-based capital and IFRS 17, which should enhance solvency transparency and investor confidence.

Yet the challenges are equally stark: chronic macro-volatility erodes household savings; provincial stamp duties and sales taxes add complexity; and policy lapses remain high because of aggressive front-loaded charges on savings-oriented products.

The bancassurance criticism

Since the mid-2000s bancassurance has been the engine of private-sector life-insurance growth. Banks provide a ready-made affluent customer base

and a nationwide branch network; insurers supply unit-linked savings plans offering modest life cover plus exposure to government bonds and equity funds.

But the model is showing cracks. An academic survey notes that SECP has received “numerous reports of mis-selling cases”, with policies often “offered as banking products rather than insurance” . Front-loaded commissions – sometimes more than the first year’s premium – and opaque surrender penalties leave many policy-holders nursing losses if they exit early. The same paper warns that “aggressive selling” calls for tighter consumer-protection rules and better disclosure .

Regulators have begun to respond. Draft SECP guidelines propose capping total commission and bank-share ratios in the early years of a policy, cooling-off periods with full premium refunds, and standardised benefit illustrations using low and mid-case investment returns.

For Adamjee Life, which relies on bancassurance for roughly a fifth of premium income, any cap on commissions could force a rethink of product mix. Management argues that digital channels and group-life schemes will pick up the slack, but these avenues are competitive and margin-thin.

Looking ahead

Even with slower earnings growth, Adamjee Life remains one of the better-capitalised plays on Pakistan’s under-penetrated life-insurance story. The immediate task is to navigate three moving targets.

Interest-rate risk remains big, and locking in yields before the monetary easing cycle gathers pace will be important. The IFRS 17 go-live is also critical to manage; it is a technology and actuarial overhaul that could reset reported equity and profit patterns. Finally, shifting from high-commission bancassurance to lower-cost digital and group business without sacrificing scale will also be an important transition to manage.

The company’s projection of Rs30.97 billion in gross premiums for 2025 suggests management still expects double-digit topline growth even in a softer macro-cycle. Whether that translates into bottom-line traction will depend on how quickly Adamjee Life can recalibrate products, costs and investment strategy for a lower-yield world.

In 2024 the insurer surfed the bond-market wave to record profits; in 2025 it must prove it can thrive when that tide recedes. For Pakistan’s fledgling life-insurance market, the results will be watched closely as a bell-wether of the industry’s next phase of maturation. n

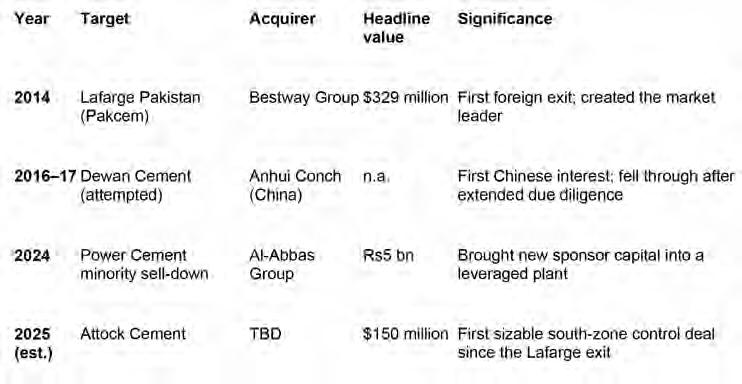

The bidding war for Attock Cement

Five parties are bidding for the Pharaon asset in Pakistan as the heirs of the Saudi-Lebanese billionaire look to offload their sizeable Pakistan presence

Profit Report

Afully-fledged auction has broken out for Attock Cement Pakistan Ltd. (ACPL), with five separate parties either filing a formal Public Announcement of Intention (PAI) or being named by the company’s financial adviser as active in the process.

Fauji Foundation & Kot Addu Power Company (KAPCO) filed a joint PAI on 3 June, stating their plan to buy 84.06% of ACPL (42.03% each) and then launch a mandatory public offer for the free float.

Alpha Cement Company Ltd., a newly-incorporated Karachi-based vehicle, entered the race the same week, likewise targeting 84.06% of the shares and signalling it could go as high as 92% through a follow-on offer.

Cherat Cement Company Ltd. and Bestway Group/Bestway Cement were both cited by Bloomberg and subsequently by Business Recorder as having received data-room access in late May, following expressions of interest

lodged with Standard Chartered Bank, the sell-side adviser. Bestway was later informed it would not advance to Phase II, but remains a stalking-horse in the background.

The presence of energy, military-linked and established cement players in one bidding cohort highlights how coveted ACPL’s 3-million-tonne southern footprint has become at a time when most rivals are landlocked in the north and exports out of Karachi’s port are reviving.

Who is selling –and why?

ACPL is 84.06% owned by Pharaon Investment Group Ltd. Holding (PIGL), Lebanon, the investment arm of the late Saudi-Lebanese tycoon Ghaith Pharaon. His heirs – now two generations removed from the founding patriarch – signalled in December that they were “evaluating strategic options” for the Pakistani cement stake as part of a broader refocusing on energy and hospitality assets.

Two factors are believed to be driving the exit. The Pharaon family trust has spent the past three years unbundling cross-holdings scattered across the Middle East and South Asia. Divesting a minority-listed Pakistani cement company simplifies the capital structure.

ACPL’s latest capacity expansion – an additional 1.275 million-tonne line commissioned in April 2024 – has pushed group leverage close to three times EBITDA. A cash sale would delever PIGL’s balance-sheet ahead of an anticipated push into renewables in the Gulf. Standard Chartered’s Karachi team is running a two-stage auction: non-binding offers (completed) followed by limited due diligence and binding bids targeted for July-end.

Attock Cement in profile

Established on October 14, 1981 and headquartered in Karachi, Attock Cement – better known for its Falcon brand – started commercial produc-

tion at Hub, Balochistan in 1988 with 0.6 million tpa of clinker capacity. A succession of debottlenecking projects has lifted capacity to around 3 million tpa, with the latest line coming on-stream in April 2024.

Key milestones include its 2002 listing on the (then) Karachi Stock Exchange, its 2018 entry into grinding in Iraq (since earmarked for sale), and its 2024 completion of the LineIV expansion boosting export-grade clinker output.

Financially, ACPL booked fiscal year 2024 revenue of Rs30.5 billion and net profit of Rs3.6 billion, translating into a solid 12% net margin despite the southern market’s price volatility. Its strategic attraction lies in the fact that it is the only sizable plant west of Karachi port, giving it a freight edge on exports to East Africa and the Gulf.

It has brand strength in Sindh and Balochistan, where it commands an estimated 24% market share in bagged cement. And all four lines are FLSmidth dry-process plants with waste-heat recovery, keeping variable cost per tonne among the lowest in the country.

Who are the bidders?

Fauji Foundation and KAPCO have launched a joint bid in a marriage of military pension wealth and power-sector cash flows.

Fauji Foundation, through Fauji Cement Company Ltd. (FCCL), already runs 8.6 million tpa of cement capacity in the north. Adding ACPL would deliver an instant southern footprint and de-risk its earnings from cyclical demand up-country.

Kot Addu Power Company (KAPCO), Pakistan’s largest IPP by capacity, is sitting on cash as its original power purchase agreement winds down. Diversifying into building materials extends its useful life as a listed entity while keeping exposure to infrastructure.

The consortium intends to split the equity 50-50 and lever up the asset at ring-fenced level, using KAPCO’s banking relationships for debt and Fauji’s operational know-how for plant optimisation.

Alpha Cement Company is a Karachi-registered special-purpose vehicle formed in May-2025, Alpha Cement has no operating assets of its own. Its PAI describes a mandate to “produce, manufacture and deal in all kinds of cement products” and names Arif Habib Ltd. as manager to the offer.

Cherat Cement Company is part of the Ghulam Faruque Group, Cherat has 4.5 million tpa capacity in Nowshera and leads the Khyber Pakhtunkhwa market. Management has long coveted a southern plant to balance its portfolio, but previous green-field attempts near Dadu stalled on land acquisition. An ACPL buy would solve that instantly.

Bloomberg named Cherat as one of the first parties invited into the data-room.

Bestway Cement is part of the UKbased Bestway Group already became Pakistan’s largest cement maker when it acquired Lafarge Pakistan (Pakcem) for $329 million in 2014. Although Bestway submitted a non-binding offer, it was “not invited to participate in the second phase” of the Attock sale after Alpha Cement’s PAI, according to its own PSX notice. Even on the sidelines, however, the group’s interest has raised the competitive temperature.

Fauji Cement is also launching a bid separate from the Fauji-KAPCO consortium, sector sources say Fauji Cement has kept the option of a solo or alternate consortium bid alive, should KAPCO hesitate over regulatory hurdles. Bloomberg’s initial report flagged such a possibility, though no separate PAI has yet surfaced.

A common thread in these deals is the pursuit of geographic diversification within a country whose demand is sharply split between the northern and southern zones, and where export corridors differ markedly.

What is Attock Cement worth?

At the 5 June closing price of Rs300 per share, ACPL’s equity is valued at Rs41.2 billion ($146 million at Rs282/US$). The Pharaon block represents 84.06%, implying a Rs34.7 billion ticket.

Control deals in Pakistani cement have historically cleared at 20-30% premiums. Applying a mid-point 25% premium lifts the indicative cheque to about Rs43 billion ($154 million). Any buyer will also assume around Rs10 billion of net debt, taking enterprise value to roughly Rs53 billion ($190 million) –just under 5x trailing EBITDA, broadly in line with the Lafarge precedent after adjusting for

cycle and capacity.

Fauji/KAPCO bring the lowest cost of capital thanks to KAPCO’s cash pile and Fauji Foundation’s AAA balance-sheet. Their edge could allow a higher all-cash offer. Alpha Cement may pitch a leaner bid but leverage it higher, banking on export margins to service debt. Cherat carries synergies on spare southern clinker grinding and marketing, potentially allowing it to pay more in value-in-use terms. Bestway, even if formally out, could resurface if pricing looks attractive – it remains Pakistan’s most acquisitive cement player.

The wildcard is regulatory. Any takeover that concentrates more than 25% of national capacity in one group triggers Competition Commission of Pakistan (CCP) scrutiny. Fauji and Attock would reach 12%, Cherat and Attock 9%, while Bestway+ Attock would cross 17% – all below the critical threshold, but the CCP could still probe regional dominance in the south.

Binding bids are expected by late July, with signing targeted before the end of FY2025 to allow Pharaon to book proceeds within the current financial year. Analysts expect at least two fully financed offers to be tabled.

For whichever buyer prevails, ACPL offers a modern, energy-efficient southern anchor asset, immediate export optionality into the UAE and East Africa, and upside from integrating the new Line-IV and selling the Iraqi grinding stake.

For Pakistan’s cement sector, the transaction will be only the second outright foreign exit after Lafarge – and a litmus test of whether local or Gulf-sourced capital is now the driving force in a market once dominated by European multinationals.

At stake is more than a single factory at Hub. The bidding war for Attock Cement is a referendum on the sector’s next decade: whether scale, geography or vertical integration will decide who pours Pakistan’s concrete future. n

Asia Insurance doubles its profits, but no dividends yet

Regulatory requirements to raise capital means the company needs to conserve cash in order to boost its book value

Profit Report

Pakistan’s general-insurance minnow Asia Insurance Company Ltd. (PSX: ASIC) has just delivered the sort of earnings spurt that typically prompts champagne corks to pop in boardrooms. Net profit for calendar year 2024 soared to Rs168.4 million, almost twice the Rs85.7 million it earned a year earlier , a 96% leap also con-

firmed in the company’s detailed financial table . Yet shareholders will see none of that bounty in the form of dividends – because a much sterner regulator now wants insurers to bulk up their capital buffers.

At first glance the story looks simple: top-line strength fed the bottom line. Net insurance premium income climbed 20% to Rs991 million in 2024 from Rs827 million a year earlier . But the real turbo-charger was a 182% jump in investment income, which bal-

looned from Rs54 million to Rs152 million . The underwriting result did improve –rising to Rs16 million from a mere Rs7 million – yet claims grew faster than premiums and management expenses edged up only modestly. In other words, underwriting alone could not have produced a near-doubling in earnings. Instead, the exceptional year enjoyed by Pakistan’s capital markets did the heavy lifting.

The benchmark KSE-100 Index finished 2024 up an eye-watering 84%, its best showing

in 22 years. Government-bond prices also rallied as the State Bank of Pakistan shifted from a policy rate of 22% in late-2023 to successive cuts before a temporary pause at 12% in March 2025. Falling yields lifted the mark-to-market value of Asia Insurance’s holdings in Pakistan Investment Bonds (PIBs) and Treasury Bills, while the stock-market surge boosted its 13% allocation to equities.

Management’s investment stance is detailed in the briefing notes: a Rs816 million portfolio split across equities (13%), government securities (10%), fixed PIBs (17%), savings accounts (5%), term deposits (50%) and properties (5%). Locking half the portfolio into long-term deposits at still-generous rates was timely, protecting yields as KIBOR headed south.

Why the board kept the cheque book shut

Shareholders hoping for a payout were likely to be disappointed when the company announced no final dividend despite the profit windfall. The reason lies in new minimum-capital rules approved by the Securities and Exchange Commission of Pakistan (SECP) in February. Non-life insurers must raise their paid-up capital to Rs2 billion –nearly quadruple the prior threshold – by 2030.

Asia Insurance, whose paid-up equity currently stands a shade above Rs1 billion, needs to conserve earnings to meet that target. The company’s own briefing bluntly notes that “ASIC did not declare a dividend in CY24, as insurers are required to enhance their paid-up capital by 2030”.

That capital call reflects the regulator’s desire to build a sturdier industry with the balance-sheet muscle to absorb large catastrophe losses and comply with risk-based solvency standards that are edging closer to international norms such as IFRS-17.

From modest beginnings to a diversified insurer

Asia Insurance’s journey began in 1979, founded as a small property-and-casualty underwriter when Pakistan’s insurance penetration hovered near zero. Over four and a half decades the firm has dodged bouts of macroeconomic upheaval, military rule and global financial crises. Yet its most dramatic transformation came in 2020 when the German development bank KfW, through the AAA-rated InsuResilience Investment Fund managed by BlueOrchard, injected Rs350 million for a 25.4% stake, lifting the company’s equity to more than Rs1 billion. That strategic investment was not only