Cost-cuts send Gadoon’s bottom line soaring seven-fold 28 Cotton is no longer Pakistan’s White Gold. It is a ghost crop 30 Pakistan Aluminium Beverage Cans faring well, despite Coke and Pepsi boycotts

Pak Datacom revenue rises, even as Starlink business remains stalled

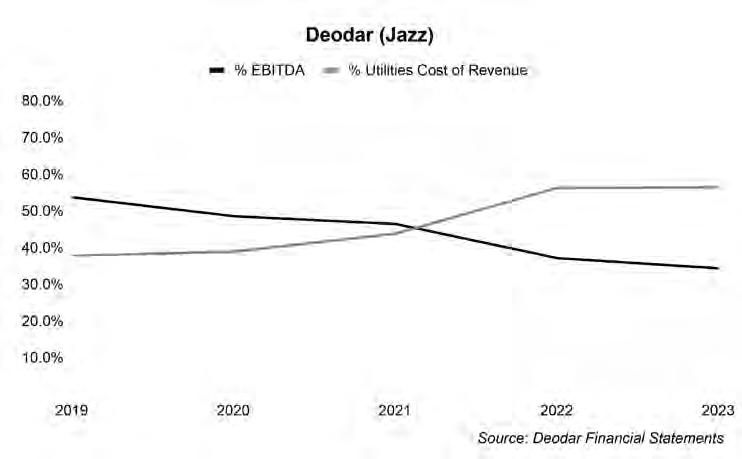

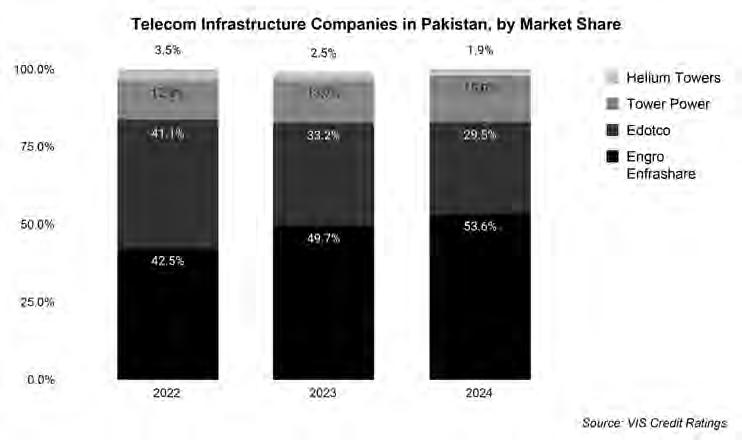

Engro makes bold bet on mobile towers as Jazz bows out

Brandon Timinisky’s new venture Zar raises $7M to bring stablecoins to local shops worldwide

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

By Umar Aziz Khan

The year isn’t 2025, but 1905. Two great powers, after some circling about, had finally gone to war the year before setting off one of the greatest naval wars in history, the details of which are still taught at military academies the world over. In the war’s second year, the final episode of the conflict plays out: the Battle of Tsushima.

It was no cakewalk, but resulted in a clear, unambiguous victory for Imperial Japan over the Russian Czarist Empire. The loss of almost every warship in the Baltic fleet had prompted the Russians to sue for peace. Not to imply they had much of a choice. The Japanese, on their end, lost no heavy ship, despite some casualties, and even those weren’t a fraction of the Russian casualties.

The war had significant geopolitical consequences, but the militaries of even those countries that were far away, who had little skin in the game, were watching, keenly awaiting reports, taking down notes.

You see, this was the first war between major conventional militaries after a bout of mechanisation and technological development had taken place. Here, the world was going to see some new technology actually being used in battle, like rapid-firing artillery and machine guns, as well as more accurate rifles, which were first tested on a mass scale. They were seeing how it would provide a template for the next great war. And it did. For a war that was, in fact, literally called The Great War (later on referred to, as World War One.)

Imperial Japan, for instance, was aided by the United Kingdom, who in an attempt to subdue the Russians in the Great Game, provided the Japanese Navy with computers

to do projectile calculations for their gunners; mechanical computers, of course, but excitingly new at that time, yielding rapid and accurate calculations. The British also provided wireless telegraphs to them (radio), a technology that both sides used. Innovations like these changed warfare thoroughly, and generals and admirals all over the world were watching with baited breath.

All that has at least some parallels with the recent events in the sub-continent. It wasn’t an unambiguous victory, despite what some of the readers of this magazine would like to imagine, nor what the odd Indian reading this (hello; no hard feelings) would be imagining.

The similarities, however: a bloated, seemingly complacent larger power fought a smaller country that was provided with modern technology by another nation that had an axe to grind with the larger power. India, Pakistan, China.

Similarity: the way the Battle of Tsushima had been, at that point, the largest naval battle in the steelship era, the India-Pakistan confrontation was perhaps one of the largest air battles in post-WW2 history and definitely the largest Beyond Visual Range (BVR) air battle in history.

Similarity: The world was watching as anxiously, as they should, when large militaries square off, yes, but generals the world over were only watching newer military gear in action.

The Pakistan Air Force didn’t quite do to the Indian Air Force’s fleet what the Imperial navy did to the Czarist fleet, but it shoot down more than a couple of the Indians’ shiny new, incredibly advanced Rafale jets, a development verified by foreign news agencies and all but verified by the Indian Airforce itself. Yes, a good day for the PAF, and not a good look for the overall shock-and-awe psy-war that the

Indians had intended. Also, would have cost them quite a packet.

The Indians’ strong point in this whole episode is contested, but it revolves around its rain of missiles and drones over Pakistani airbases and a claimed failure of the Pakistani air defence system, while the Pakistani retaliation, the Indians further claimed, was adequately addressed by Indian air defence.

That this may or may not be true is irrelevant to the scope of this article, because it wasn’t newer tech involved in this aspect of the scuffle. India’s BrahMos, with which they attacked Pakistani airbases; their Russian S-400 system, with which they protected their own airbases; and Pakistan’s Chinese-manufactured HQ-9 system, which they used to protect their own bases, were older tech that the world had already seen in action. These claims, if false, don’t matter; if true, matter to the situation itself, but not to those outsiders only observing the gear.

No, those eyes were on Pakistan’s new fleet of jets, like the one it developed with China, the JF-17 “Thunder” and, most importantly, the completely Chinese Chendgu J-10 “Dragon.” And, of course, the Chinese air-to-air PL-15 missile that the Chengdu was equipped with.

They did the job. No Rafale had been shot down before; now Pakistan had multiple kills.

But while the generals, admirals, air marshals and defence bureaucrats from the world over were sizing up Chinese military gear and figuring out how this changes the world of warcraft and supply chains, and what acquisitions to consider now, another group was also busily buzzing with activity: the suits and investors.

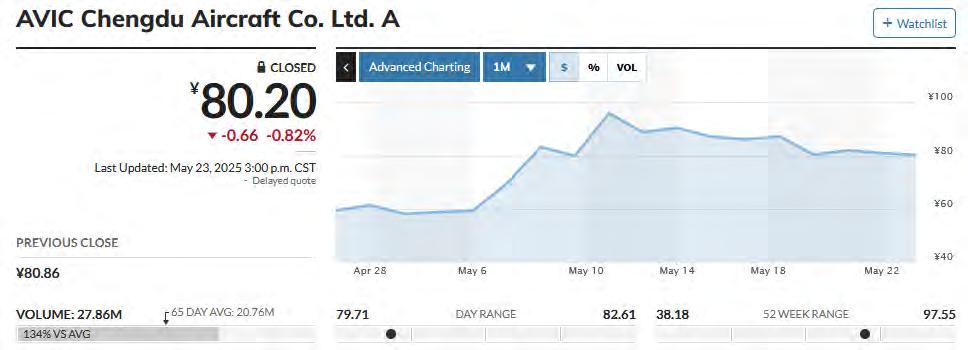

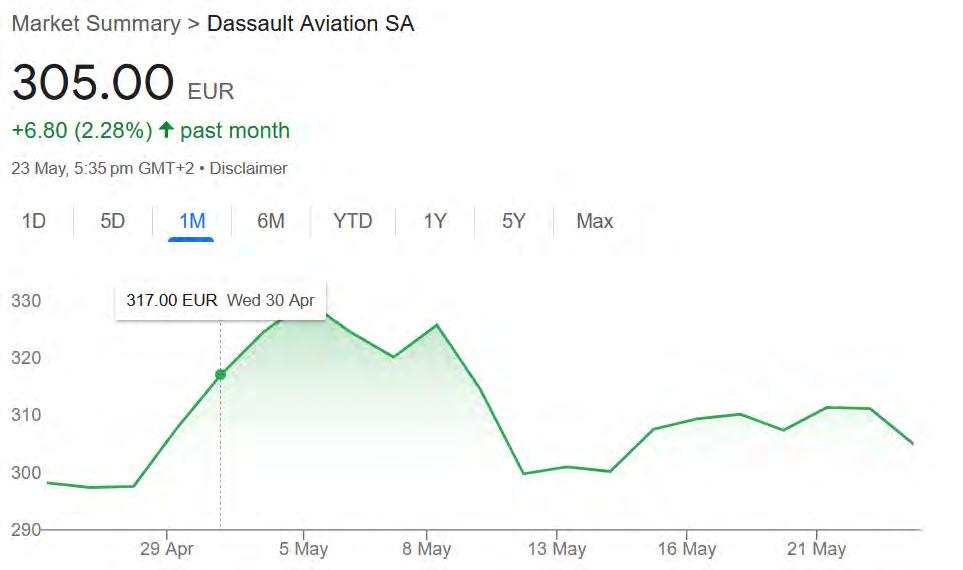

In a macabre play, perhaps even before the bodies of the innocent civilians caught in the crossfire were laid to rest, the stock of the AVIC Chengdu Aircraft Corporation and the French Dassault Aviation, which makes the Rafale jet, surged and dropped respectivelyand dramatically.

It’s all business here. Not buildings collapsing, not people dying, not national pride being hurt or assuaged. Just numbers going up and down, and money to be made.

Towers Go Down, Numbers Go up

The US stock market remained shut for four days after the attacks on September 11th, 2001. This was the longest unscheduled shutdown of the U.S. stock markets since the Great Depression. For obvious reasons.

When trading resumed on the 17th of September, the market reacted as many thought it would: horribly. The events were a massive symbolic swipe at the US’s commercial power (with the twin towers representing

corporate America - and, of course, military power, with the attack on the Pentagon.

Most stocks fell on the 17th. Defence stocks, however, spiked. Given the complicated situation of the debris and rubble in New York, again, it would be safe to say that these defence stocks were rallying before all the bodies had been buried.

The investors knew that someone, somewhere, was going to be attacked. They were right; three days later, George W Bush gave his famous with-us-or-against-us speech in Congress and two months later, on the 7th of October, he announced the beginning of military operations in Afghanistan.

Speaking of October 7th, but 22 years later, on October 7th, 2023, Hamas launched an attack in Israel. Lots of water - and blood - has flown under the bridge since then, but there is no denying that, regardless of how the public sentiment in the US is right now, on October 7th itself, the sheer might of AIPAC’s influence in US politics and the mainstream media ensured that vast segments of the American public believed, more or less, the Israeli narrative about the attacks. Many accounts of the specifics of the specifics of that attack, now debunked thoroughly, went unquestioned, and the average American was horrified.

It was a Saturday. On Monday, shares of defence stocks, including Northrop Grumman (NYSE: NOC), L3Harris Technologies (NYSE: LHX), Huntington Ingalls Industries (NYSE: HII), Lockheed Martin (NYSE: LMT) and General Dynamics (NYSE: GD) each gained at least 8% in the session, the most in more than three years.

The investor, to put it simply, is not horrified either way. But it is not just the saga of Israel versus children that gets investors’ hopes up. Consider the war in Ukraine.

The onset of the war was cause for concern in the financial world, driven by, amongst other things, how the showdown would affect the oil markets. But while the broader U.S. market was down by nearly 20%, many defence stocks saw their share price increase by double digits in percentage.

In 2022, the Invesco Aerospace and Defense ETF (NYSE: PPA) index gained 8.6%, outperforming the broader U.S. market by 28%. This rise was led by Allegheny Technologies (+87%), Maxar Technologies (+75%) and Northrop Grumman (+41%).

So, in the showdown in the sub-continent in May, could we find more about the two companies that were involved?

Watch out for Factory Number 132

One can’t possibly use the term “humble beginnings” to state projects. There’s always money sloshing about for those. It’s just

I wouldn’t necessarily attribute Pakistan’s higher kill count to Chinese fighter jets. But, I would attribute it to Pakistan’s investment in electronic warfare and airborne warning and control

Ryan McBeth, cybersecurity specialist and defence analyst

that bureaucracies sometimes bungle up that money; or political leaders shoot too far out for outcomes to be realistic. But they’re never quite bootstrapped startups.

No, Chengdu didn’t have humble origins other than it having an “untitled project” vibe, listed as Factory No. 132. It was set up with Soviet help, some years before tensions between the two communist countries commenced. These tensions weren’t ever enough to stop the cooperation between Russia and China over several projects, including this aviation project.

By 1964, Factory No. 132 had more than 500 hectares, more than 10 thousand employees, and had produced its first jet fighter, the J-5.

In later years, No. 132 started production of the J-7, variants of which were acquired by multiple militaries, the largest of them being the Pakistan Air Force. It is one of the peculiarities of the international arms trade that the J-7 was actually a licence-built version of the Soviet Mig-21, which was, till a long time the pride of the Indian Air Force and is still active in their fleet, despite being dubbed by some in the (till recently) relatively free Indian press as “flying coffins” and “widow makers.” So both the rival countries were flying the same plane, so to speak.

Well, it would be wrong to call them the same plane, as there are a lot of avionics and internal wiring, so to speak, that set planes apart, but broadly speaking the same system. Since press freedom and openness of the defence analysis commentariat in Pakistan doesn’t quite compare with that in India even now, the general public doesn’t quite know what the PAF itself thinks of the J-7.

It was in the 70s that the 132 really accelerated its research and indigenous design and production capabilities and, by the end of the decade, it revealed itself to the outside world as the Chengdu Aircraft Company and later on, it reorganised with “unified leadership and

decentralised management.”

In the early 80s, there was talk of the possibility of Chengdu building “the Chinese F-16,” meaning a Chinese version of a multirole fighter aircraft that was highly maneuverable and agile that could fulfill the role of the US F-16 and the Soviet Mig-29 Fulcrum.

Do keep in mind that this was the early 80s; China wasn’t yet the China that we know now. But the state lent even more autonomy to the factory and lent them more freedom in the whole sourcing process.

That resulted in the 4th generation and then 4.5th generation fighter we know as the J-10, flown today only by the Chinese and Pakistani air forces. The PAF’s faith in Chinese military gear wasn’t just this: it had also developed the JF-17 Thunder jet with Chengdu and had inducted it in the PAF in 2010.

That is not to mention Chengdu’s fifth generation J-20, said to be an equivalent of Lockheed’s F-35 and a highly secretive and much speculated about J-36.

But before recent events transpired, even 4th and 4.5th generation fighters hadn’t been tested in battle. Would a country shill out such substantial sums of money on something… well.. “Made in China”?

Marcel’s Machines

They couldn’t break him. The Germans, who were occupying France during World War 2, just could not get Marcel Bloch to cooperate with them. So they sent the aviation engineer to a concentration camp in Germany.

It was surprisingly difficult to break this brilliant engineer, who had his own aviation design and manufacturing company, Société des Avions Marcel Bloch, and whose engineering designs had been used by the French military as early as World War 1. They tortured him, beat him up, kept him in solitary confine-

ment and had disabled him to the extent that when the war ended, he could barely walk.

Perhaps it was his brother he drew inspiration from. General Darius Paul Bloch was in the French Resistance and his no de guerre was “Chardasso”, a play on the word char d’assaut (“assault tank.”)

Out from the war, Marcel Bloch, who had been told by doctors that he hadn’t much time to live, changed his surname, in his brother’s honour, to Dassault. And in 1971, after acquiring Breguet, formed the Dassault Aviation we know today, which now makes not just military jets but also business jets.

Though the company was, and is, a major contractor for the French military, from the 1950s exports became a major part of Dassault’s business. Both the Pakistan and Indian air forces were a part of this, with the former buying Mirages and the latter buying the Mystères.

In PAF, the Mirages were the “it” fighter before the acquisition of the F-16s in the ‘80s, and the PAF is accredited with utilising its fleet of Mirages effectively for much longer than they were thought they could be.

Later on, the Indians also got the Mirage 2000, a significantly different aircraft than the Mirages in Pakistan’s fleet.

The IAF, of course, later on acquired a fleet of Dassault’s most advanced fighter jet, one of the most effective combat systems in the world, the Rafale.

Though it had been involved in operations where it would have been in proximity with hostile air forces, like Libya’s in 2011, and air policing NATO missions, where there would have been proximity to Russian military aircraft, the rest of the Rafale’s engagement had been with asymmetric operations, much like those of the PAF’s Chinese fighters.

The only difference being the fact that Dassault was a known company, with a solid

track record of producing world leading fighter aircrafts, with the Rafale being its current best foot forward.

That all changed this May.

‘The most expensive advertisement in the world’

On the 7th of May, the Indian government launched Operation Sindoor and conducted airstrikes in Pakistani territory on alleged training camps of the Lashkar-e-Taiba and the Jaish-e-Muhammad. The PAF responded by hitting at the IAF jets involved in that air strike, while they were still in the air.

Subsequent details of Operation Sindoor, and Pakistan’s Operation Bunyan um Marsoos are, as discussed earlier, irrelevant to this particular article.

What matters is how Rafale fared and the Chinese technology on the other side fared. Pakistani claims of having downed several IAF jets were initially received with some suspicion even by Pakistani social media chatter, since the only details of the strikes that had emerged has been that both air forces had remained within their own airspaces, as opposed to the incursion six years ago. How, then, could Pakistan shoot down these several planes?

By the next day, international news media outlets did confirm, one after another, citing French and US intelligence sources, that the news was, indeed, true. Though the Indian media vehemently denied, the IAF’s operations director, in response to a direct question, all but admitted it.

The combination of the JF-10 and the Chinese PL-15 missile, says Indian defence analyst Pravin Sawhney, did the trick. As did the PAF’s electronic warfare infrastructure.

It was all a Beyond Visual Range air battle.

On the Shanghai Stock Exchange, shares of the Chengdu Aircraft Corporation surged by 20 per cent on May 12, with its stock reaching Chinese Yuan 95.86, a whopping 60% increase from the previous week!

Meanwhile, on the Euronext Paris stock market, the stock of Dassault Aviation dropped sharply. Dassault Aviation hit a 7 per cent intraday drop on Monday, reaching EUR 292. Throughout the day, the stocks kept fluctuating from EUR 291 to EUR 295. A 7 percent single-day drop isn’t small change for a USD 27 billion company.

But Dassault’s stock did rise later on, because of otherwise solid financial results. After all, Dassault Aviation had posted annual sales of EUR 6.24 billion and a net profit of EUR 924 million, while the leader French Aerospace and Defence sector had grown by 17.7 percent.

Dassault’s reputation wasn’t going to take a hit because of a one-off. As the PAF’s operations director himself said in a presser, “the Rafale is a very potent aircraft…if employed well.”

A perhaps unintentionally snide comment on the IAF but one amplified by the predictably acerbic social media accounts of Pakistan in their trading-of-barbs with their Indian counterparts. Though some suspect Dassault Aviation might be repeating those words, more or less, in earnest during their presentations to other potential clients.

Dassault Aviation, in any case, isn’t comparable, by a stretch, to the Chinese company. It’s as solid as a defence contractor could be.

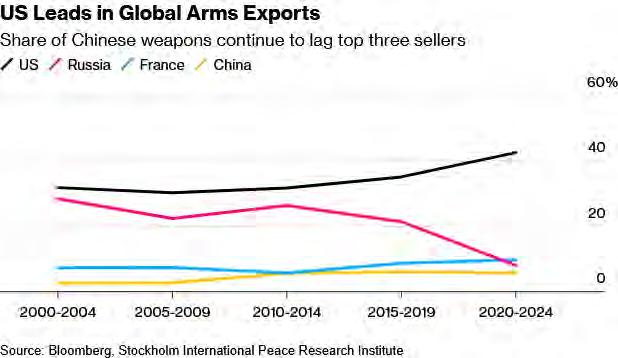

No, all eyes are on Chengdu and China’s broader defence ecosystem. There are going to be far more interested buyers. Consider the sheer value proposition: the cost of a Rafale jet can vary significantly, depending on the variant and also the buyer’s specific requirements, but a commonly cited price range is between USD

90 million and USD 120 million. The J-10C on the other hand, is said to range between USD 40 million and USD 60 million.

The value proposition does the talking - and the selling - is what the investors seem to have felt in the immediate aftermath of the air battle. But that is just a sentiment. It is the financial statements that record actual salesor the announcement of confirmed sales that haven’t made it to the financial statements yet, that will make the investors sit up and take much more notice than the surge that we saw.

Is there a Principal-Agent Problem in defence procurement?

You go to a doctor (or a mechanic, or a real estate agent or a…) and have to rely on their judgment and make spending decisions (in the doctor’s case: what medicine to buy, what test to get done, what procedure to sign up for) on what they say. The person doing the spending isn’t the one who is

making the decision on what to spend.

The problem is that these guys might not get you the best deal because it is not their very own money being spent. That, in economics, is called the Principal-Agent Problem. What does that have to do with defense sales? Well, who makes the spending decisions is key here.

Countries with relatively opaque defence procurement decisions (like Pakistan’s) and countries with relatively transparent protocols for it and that are subject to political oversight (like India’s), go about the defence procurement process differently.

It has been noted, of late, that Chinese companies, selling just about anything, have taken to a “360 approach” to sales. They will make traditional advertisements and sales pitches, yes, but they will now also leverage some rather non-traditional means as well.

To this effect, go the conjectures, the Chinese are throwing everything and the kitchen sink into the problem, including funny video skits skewering the Buyer’s Remorse of the Indian Air Force, for the general public to digest. You don’t need to understand the lyrics to find it funny, or to find what is being made fun of. The target audience might be the Egyptian public, or the Nigerian public, and through them, their governments. (The Egyptians have Rafales on order and the Nigerians already fly the Thunders.)

Policymaking politicians, on the other

hand, are not the sort swayed by short, funny videos. For those, there is the recent mushrooming of Chinese vloggers and online columnists who seem to make a rather decent case for Chinese military gear. The key words being ‘seem to.’ These supposed comment pieces can also be a part of a larger spiel.

Politicians and civilians, informed as they might be by the military brass, being the ultimate arbiters of defence spending is the best way, in principle, to go about things. Matters get complicated when this approach ends up, for however short a period, with populist politicians in charge who want to sell their vote-bank shinier toys that might not be the ones that the uniformed grownups running the defences want. Though usually, throughout the world, it is the other way around; it is the generals and air marshals and admirals that want more and newer gear and the politicians who are frugal. It is only when a ruling party goes berserk that the roles get switched.

That is the delicate balance between Principal and Agent in defence procurement. In working democracies, the defence establishment isn’t quite the Agent. The civilian overlords over at the defence ministries are both Agent and Principal; specific acquisitions are something that the generals try to convince the politicians about and then hope for the best. But even though that is lesser leeway than what the militaries of praetorian states enjoy, it is still massive enough to influence decisions.

And that can definitely cause problems for investors that based their decisions on that

extremely rudimentary bit of information: that the J-10s shot down some Rafales.

Because those actually in the know of what actually transpired on the night of the 7th, might not even be thinking about buying the jets to begin with.

Less exciting takeaways

“Iwouldn’t necessarily attribute Pakistan’s higher kill count to Chinese fighter jets,” says Ryan McBeth, a cybersecurity specialist, and defence analyst. “But, I would attribute it to Pakistan’s investment in electronic warfare and airborne warning and control.”

“No matter how good the Rafale is, you’re only as good as the information you’re getting as to where to point your jet and fire that missile, especially beyond visual range,” he adds.

After rattling off a list of both Indian and Pakistan electronic warfare and AWACS, he says that the fact that Pakistan has three times the electronic warfare and airborne warning control aircraft as India kind of lets us you know that “Pakistan is fighting a modern air war, while India is still fighting air wars as the way we might have done in Vietnam.”

“If you don’t have good sensors in the air, it doesn’t matter what fighter jets you have, it doesn’t matter how brave your fighter pilots are, it doesn’t matter how good the Rafale is. You’re going to get taken down from a 100 nautical miles away by some dude who’s talking to

an airborne warning control aircraft.”

The problem with AWACS is that they aren’t, according to McBeth, “sexy.”

“They don’t parade well, no one wants to see a flyover of the Super Bowl with AWACS. You want jet fighters because they are cool. But the AWACS are probably the most important piece of kit a military can have in its arsenal if it wants to fight a modern day conflict.”

Depending on where a country’s defense acquisition ecosystem lies on the Principal-Agent Problem - and the temperament of the government in charge there, we might see different types of sales.

Clued up military experts from around the world might advocate for buying the AWACS and EW systems, after all. Even there, the PAF has Chinese equipment (Shaanxi), but it also has Swedish equipment (Saab) and French equipment (Dassault, ironically) as well.

Perhaps, when the dust settles, and the orders are placed by actual users of the equipment, instead of investors merely following news, we will see other stocks showing activity and not (just) that of Chengdu.

At least, by how Ryan McBeth, Pravin Sawhney, the Indian defence analyst, and others have analysed it.

“I really do believe that this particular air war was a template for what the next war might look like in Taiwan,” says McBeth.

So, it could have been a template, just not only for Chinese military gear, but for future electronic warfare, with air battles of the “boring” variety. The wheel of time continues to turn. n

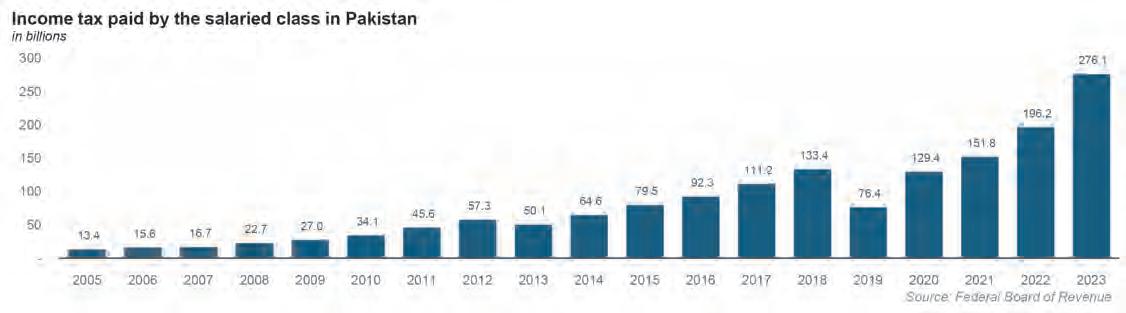

Salaried Pakistan

A regular monthly paycheck is still not the norm in the Pakistani labour force, but is steadily becoming more common. The financial services sector should begin preparing to serve this segment of the population

By Farooq Tirmizi

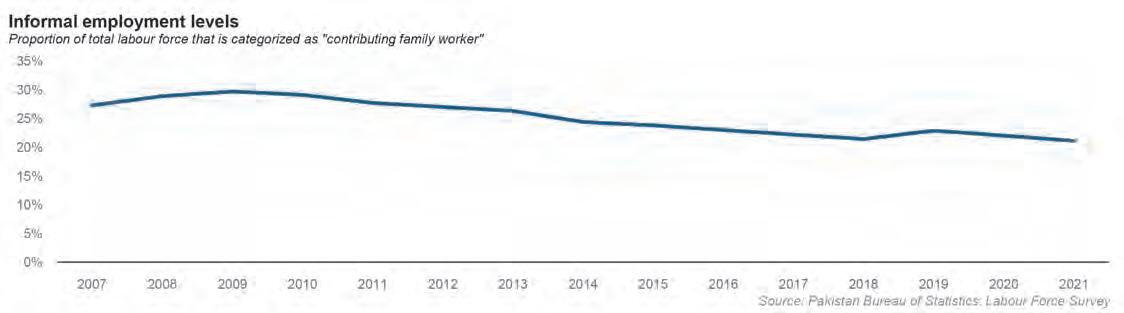

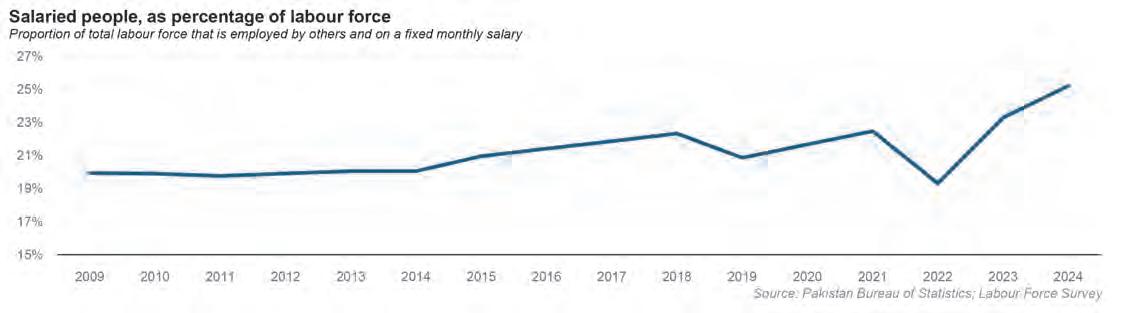

If you read this magazine, the odds are very high that you are a salaried individual in Pakistan. And the odds are just as high that you likely complain about your salary levels. You are, however, among the lucky ones in Pakistan in that you get paid in the form of a regular monthly salary. Less than one quarter of Pakistanis who work receive their compensation this way, That number, however, has been steadily rising, and with its rise will come the slow conversion of Pakistan’s informal employment sector into its formal employment sector.

While a handful of young professionals in the country work for global employers and offer their services to companies operating at the cutting edge of technology, the bulk of Pakistan’s labour force is actually quite premodern: informal employment arrangements, working in close proximity to family, and may not always be paid in cash, and generally tied to closely monitored output rather than a fixed monthly amount.

According to the 2021 Labour Force Survey, the most recent one conducted by the Pakistan Bureau of Statistics, about 22.5% of Pakistan’s labour force consists of employed individuals who receive a regular monthly salary. While the PBS has not historically tracked this number for previous years, Profit’s analysis of the data – as well as other data sources – suggests that this number is rising, and with it changing the composition of what being employed in Pakistan means.

Banking industry data indicates that growth in the number of salaried individuals may be considerably more rapid than what the labour force is implying: perhaps having doubled over the past five years. While we believe that rapid a pace of growth is unlikely, it is nonetheless true that Pakistan’s economic landscape is shifting towards more formalized employment arrangements.

So what does this mean for the country and its economy? The story starts with why a monthly salary is a preferable default for compensation for a country’s labour force. We then examine some of the data that shows how fast this category has been growing, followed by implications of what this might mean for the banking sector, the government, and other businesses.

Why a salary matters

Before we get into why a monthly salary job is good, consider the menu of options available to the vast majority of Pakistanis. There is the option of being self-employed and taking a risk every single day for how much money you can earn. There is the option of being a day labourer, which has at least some predictability with respect to income levels, but no security: you do not get paid on a day you are sick and cannot work.

And then there is the option that a majority of women in the labour force (55% to be precise) must live with: being unpaid labour helping male family members with their work on a farm, which your family may, or may not own.

Pakistanis are not just poor: the vast majority of us live with low wages and uncertainty of even receiving those wages. Quite simply, that is the worst of all worlds.

Having a larger share of the workforce earning a predictable monthly wage – even if those wages start out low – would be vastly better for the Pakistani economy, or really any developing economy, in the following three ways.

The first has to do with its effect on household consumption. When income arrives on a fixed schedule, families can plan food, schooling, transport and health spending with far less fear of sudden shortfalls. Because salaried workers feel confident about next month’s pay-cheque, they spend a higher fraction of their earnings, giving shops, utilities and service providers a more reliable demand base.

This, in turn, has an impact on the financial services sector. Steady pay-cheques flow into current and savings accounts, giving banks a pool

of low-cost, stable deposits that can be lent out long-term to businesses and infrastructure projects. Regular deposits show up in bank statements, making households eligible for formal credit (consumer loans, mortgages, etc.) at lower rates than informal lenders charge. That, in turn, amplifies durable-goods purchases and housing purchase activity.

Beyond the growth that comes from unlocking more credit, however, is the stability: even in economic downturns, salaried workers maintain at least part of their purchasing power, cushioning aggregate demand and shortening recessions. This also has the advantage of helping the government have a more predictable and stable source of tax revenue.

How many Pakistanis are salaried?

The Pakistan Bureau of Statistics has not published a labour force survey since 2021 (we will get into why we think that is later) and hence it is not possible to rely on a purely government estimate for what is the current number of salaried individuals in Pakistan. Profit utilized a combination of data from the PBS as well as bank deposit data from the State Bank of Pakistan to project the number of salaried individuals as well as their proportion relative to the total labour force.

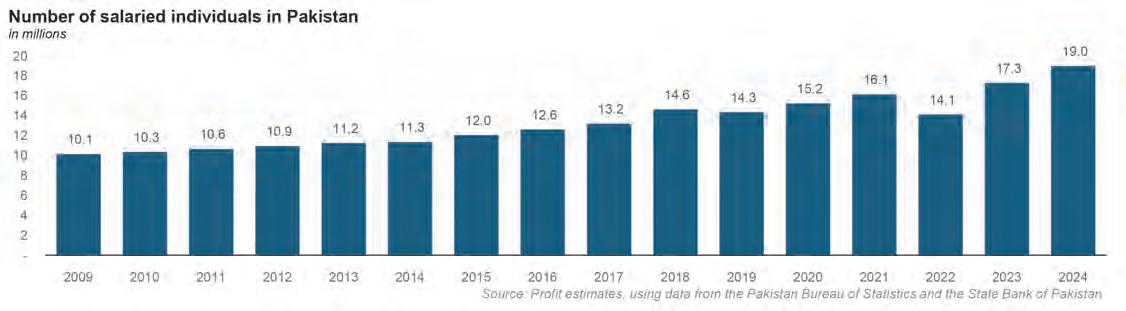

Our estimates indicate that as many as 19 million individuals in Pakistan – or about 25.2% of the total labour force – was employed in a position with a fixed monthly salary as of the end of 2024, up from about 20% as recently as a decade ago.

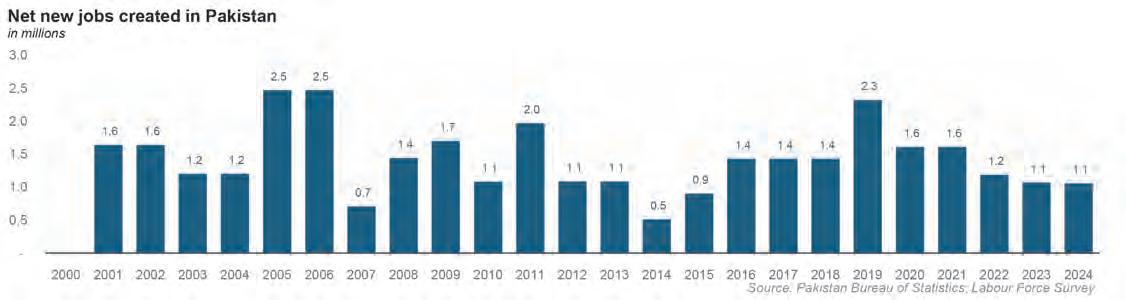

But here is where matters get more interesting: while the total proportion of salaried jobs in Pakistan is low, it is a much higher proportion of new jobs created in the economy.

It is by now cliché in Pakistan to talk about how many jobs the economy needs to create in order to absorb the youth who age into the labour force each year. Less fashionable is to talk about how many jobs do get created every year in Pakistan.

In the 15 years between 2009 and 2024,

again using a combination of PBS data and Profit’s projections, we estimate that the Pakistani economy has created 19.8 million net new jobs. Of those, 8.9 million jobs – or about 45% of the total created – were fixed monthly salary jobs. In absolute terms, the number of people with fixed monthly salary jobs almost doubled between 2009 and 2024.

This has enormous implications for the nature of the Pakistani economy. It means that we are on the cusp of having a majority of the jobs being created in the economy being good, stable jobs, even if they are not high-paying yet.

The nature of the job market

Economic commentary in Pakistan tends to focus on both the need to create jobs as well as the level of income offered by those jobs. This perspective is skewed by the college-educated elite who tend to do most of the talking about Pakistan’s labour market.

The reality facing the vast majority of Pakistanis hitting the job market is the following: low pay, high uncertainty. The proliferation of salaried jobs – even low-paying ones – has the virtue of getting rid of at least half the problem with Pakistan’s labour market.

The precarity of most employment in the country is best understood in times of economic duress. Consider, for example, the year 2018 and 2019, when the economy suffered a major crisis at the end of the third Nawaz Administration. The number of net new jobs created in fiscal year 2019 was 2.3 million, but that number hides a glaring weakness. During that same year, 2.4 million people moved back from their urban and non-agricultural jobs back to the farm: agricultural employment rose that year.

Had it not risen by that much – had people in Pakistan not had the option of going back to their ancestral village and working on their own or a relative’s farm – total employment in the economy would have dropped by about 100,000 jobs, which is bad enough in any economy but disastrous in one like Pakistan

where the labour force increases in size by over 1 million people per year.

The same thing happened in 2008 and 2009, when roughly 2 million people moved back to the family farm owing to economic conditions. The land really does feed the people of Pakistan in their hard times.

But those return-to-the-farm jobs are most likely a favour done by family members to each other, and not sources of economic security and advancement. Family ties substitute for economic growth.

This, by the way, explains why labour force survey data for years following 2021 is not yet available: these years have been chaotic for the economy, and we suspect the government is in no rush to provide evidence of just how badly the economy has been doing. A subsequent survey will likely reveal not just the extent of the damage to the labour market, but likely also the extent to which the labour market shrank as a sizeable proportion of it left for other countries.

Nonetheless, the recent damage notwithstanding, the long-term trend of labour market formalization is unmistakable: salaried jobs have doubled in absolute terms over the last 15 years, and have accounted for about half of the growth in total employment levels during that time.

So what does this mean for the economy?

The formal will dominate

This magazine has extensively covered the extent to which digital payments have begun to replace physical cash and paper-based payments, which indicates a greater willingness to operate in the documented portion of the economy. That formality is manifesting itself not just in transactions conducted by individuals, but also by entrepreneurs and employers who are creating more formal salaried jobs than ever before.

It is first and foremost a change in attitude: documentation may be painful and costly, but it is increasingly no longer seen as optional. It is the beginning of a multidecade

process that will likely culminate in Pakistan being a mostly documented economy.

One consequence for the government is that an increasing share of its revenue is coming in the form of taxes collected by employers from their employees’ regular salaries and deposited automatically with the government. This kind of automatic tax collection is still a relatively small proportion of total tax collection – about 2% of federal tax collection – but that proportion has doubled over the past decade.

In more advanced economies such as the United States, close to 90% of tax revenue comes from individual income taxes (though in the US, that also includes the passthrough income tax paid by business owners) so Pakistan has a long way to go in terms of shifting the nature of its tax regime. But at least a start has been made.

The banks will benefit

The part of the economy that will most directly stand to benefit from this development is the banking sector, which will see the benefits of a greater proportion of Pakistanis being able to have their income deposited into a bank account every month, and perhaps a small portion of it being left over after the month’s expenditures are accounted for.

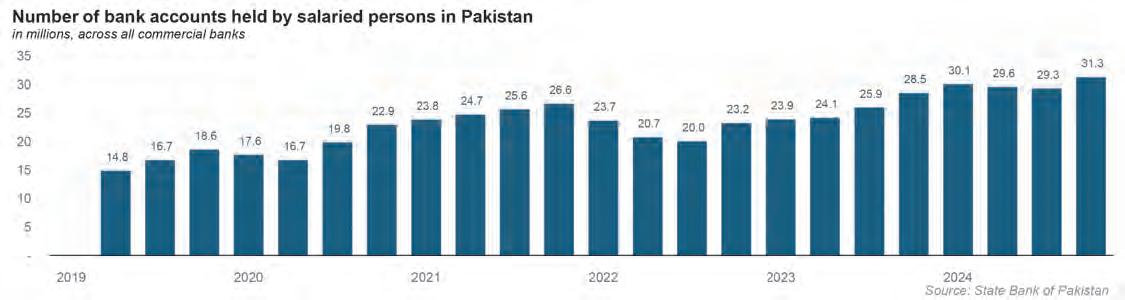

There are a total of 31.2 million bank accounts owned by salaried individuals in Pakistan as of December 31, 2024, according to data from the State Bank of Pakistan, a number that has more than doubled over the past five years. That rapid growth is likely due to the fact that a large number of Pakistani companies require employees to open bank accounts at the bank in which the company maintains its corporate bank account in order to receive

a salary, which means that people often have to create a new bank account every time they switch jobs.

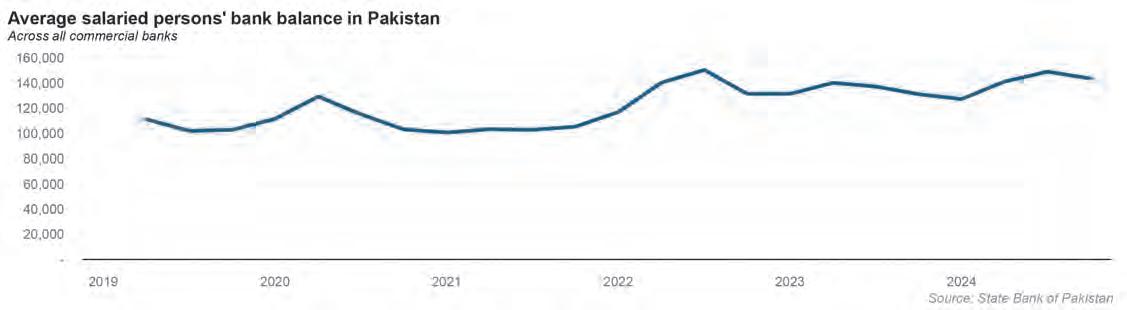

The average balance in these salaried accounts is Rs144,000 and since the bulk of these are likely current accounts, the cost of deposits for banks is likely to remain relatively low. The average deposit amount has actually risen over the past five years from around Rs102,000 in 2019, which suggests that the rise in number of accounts may not just be a case of individuals having to open more and more accounts as they switch jobs.

More than deposits, though, financial institutions have the ability to offer a much larger number of people their full suite of products. Mutual funds, life insurance, car loans, mortgages, etc. all require an individual to first and foremost have a bank account, which in turn is much easier to get if one has a salaried job.

Incomes will start rising

Ultimately, however, the biggest benefit to the rise of salaried jobs in Pakistan is the fact that they will create a virtuous circle where an increase in the number of salaried jobs increases demand levels in the economy for goods and services, as well as increased savings to finance the expansion of the economy’s productive capacity for providing those goods and services.

That expansion in capacity then leads to yet more increases in salaried jobs, and the cycles keeps on repeating itself.

What started off with low-paying jobs simply removing the uncertainty will soon turn into higher-paying jobs as employers begin

having to compete for talent and start bidding up wages. This process will be helped in Pakistan by the fact that a substantial proportion of the best talented part of the labour force is serving the US and European market as remote workers or outsourced services providers and hence have elevated income expectations.

Conclusion

Pakistan’s labour market is therefore at an inflection point: even though just one in four workers now enjoys a predictable pay cheque, salaried employment has already become the dominant engine of new job creation and is fast knitting the informal margins of the economy into its documented core.

That shift is not just a statistical curiosity; it is a structural pivot that will underwrite

steadier household consumption, broaden the country’s tax base, deepen its banking system and, in time, push wages higher as firms compete for increasingly mobile talent.

For policymakers, the priority should be to accelerate this virtuous cycle. The government could start by not trying to continually strangle the golden goose and ease some of the excessive tax burdens on the salaried class in Pakistan. It could also try to reduce the bureaucratic red tape around things like incorporating businesses, paying taxes, etc. to help encourage more businesses to accelerate along the path towards formalization.

The rise of the salaried class may feel incremental today, but it is the quiet revolution that will decide whether the next generation measures progress by the uncertainty it escaped or by the prosperity it secured. n

Fitch endorses what the government has been claiming

While the economy has transitioned from critical care to recovery ward, complete healing will take time

JBy Ahtasam Ahmad

ust over two years ago, Pakistan stood on the precipice of economic collapse. Credit rating agencies Fitch and Moody’s delivered a devastating blow, downgrading the country’s sovereign rating to levels not seen in decades.

The message from global markets was unmistakable: Pakistan had become toxic.

The eurobond market told the story in stark numbers. Bonds with a $100 face value were trading at just $35 in secondary markets, a fire sale that reflected investors’ desperate rush to offload what traders had written off as junk. Pakistan appeared destined to join the ranks of Ghana, Zambia, and Ethiopia in the club no nation wants to enter: sovereign default.

The crisis didn’t emerge overnight. While the foundations had been cracking for years, the perfect storm arrived in 2022. External shocks hammered the economy relentlessly. The Russia-Ukraine war sent Brent crude soaring to $130 per barrel, devastating floods submerged one-third of the country, and domestic political turmoil created policy paralysis. The rupee went into freefall, inflation spiked to 40%, energy costs became unbearable, and the government found itself with rapidly dwindling financing options.

Yet something interesting has happened over the past year. The economy that once seemed beyond salvation is showing signs of life. The chaos and desperation that defined Pakistan’s economic narrative just two years ago have given way to cautious optimism. This shift isn’t just wishful thinking. Fitch recently upgraded Pakistan’s sovereign rating to B+, marking the third upgrade in less than two years.

But what exactly has Pakistan done right? Is this turnaround sustainable, or merely a temporary reprieve before the next crisis hits?

The revival playbook

The turnaround didn’t happen by accident. Behind the improved credit ratings and stabilizing macroeconomics lies a series of difficult decisions that Pakistani policymakers finally had the courage to make when their backs were against the wall.

This time was different with the IMF. Pakistan didn’t just sign another deal and hope for the best. The country secured a substantial $7 billion Extended Fund Facility, coupled with a $1.3 billion Resilience and Sustainability Facility running until 2027. More importantly, Pakistan actually delivered on its promises. The government hit its quantitative performance targets agreed with the Fund, particu-

larly on reserve accumulation and achieving a primary budget surplus.

Even with a tax revenue growth that is likely to fall short of targets, the commitment to reform remains. After years of failed programs, Pakistan’s strong performance on its previous temporary arrangement, which expired in April 2024, gave international markets confidence that this wasn’t just another false dawn.

The numbers tell a story of fiscal discipline. Pakistan slashed its budget deficit from nearly 7% of GDP in FY24 to a projected 6% in FY25, with expectations of reaching around 5% over the medium term. The primary surplus more than doubled to over 2% of GDP, a stunning reversal for a country that had been hemorrhaging money.

The government made the hard choices that previous administrations had avoided. Provincial governments have legislated increases in agricultural income tax, touching a politically sensitive area that had been off-limits for decades. While tax revenues have disappointed due to lower inflation and imports, spending cuts and wider provincial surpluses are likely to fill the gap.

Perhaps the most visible success has been bringing inflation under control. From a crushing 20% average in FY23-FY24, inflation is expected to average just 5% in FY25. The State Bank of Pakistan did its job at the monetary front, cutting rates by a dramatic 11% between May 2024 and May 2025. The central bank is also likely to announce a bumper dividend for this fiscal year as well due, a windfall from the high interest rate environment.

The transformation of Pakistan’s external position also impresses. The country has posted a current account surplus of $700 million in the first eight months of FY25, driven by surging remittances and favorable import prices. Gross foreign exchange reserves climbed from a terrifying low of under $8 billion in early 2023 to just under $17 billion by May 2025, providing about two months of import cover. The current account deficit for FY25 is now estimated at a negligible $0.2 billion, or just 0.1% of GDP.

Additional external support is also likely to continue to materialize. Recent reports indicate China has committed to rolling over $3.7 billion in yuan-denominated facilities before June 30, 2025. Of this amount, $2.4 billion reaches maturity next month, while $1.3 billion was already repaid to ICBC during March-April 2025.

Unlike IMF funds that remain locked within the central bank for balance of payments purposes, these Chinese facilities will boost SBP reserves while simultaneously injecting liquidity into the domestic system.

Combined with anticipated multilateral and commercial inflows, these arrangements

should push SBP foreign exchange reserves toward the $13-14 billion range by fiscal yearend. But the caveat remains: Despite Pakistan recording a healthy current account surplus of $1.9 billion over the first ten months of FY25, reserve accumulation has been tempered by net outflows through the financial account.

Yet, the government debt fell from 75% of GDP in FY23 to 67% in FY24, with further gradual declines expected as tight fiscal policy combines with nominal growth and domestic debt repricing at lower rates. While the debt ratio will tick up temporarily in FY25 due to rapid disinflation, the trajectory is clearly improving. The interest payment burden, though still heavy at 59% of revenue in FY25, is finally moving in the right direction after years of relentless deterioration.

Investors, caution and beyond

Emerging market investors are taking notice as Pakistan’s macroeconomic uncertainties begin to clear. The multi-year IMF program running through 2027 provides a stabilizing framework, while Brent crude’s decline to around $60 per barrel has eased external pressures considerably.

Market valuations also tell a compelling story. The Karachi Stock Exchange index trades at just six times earnings, well below the MSCI emerging market benchmark, despite delivering remarkable 85% dollar returns in 2024. Investors in Pakistan’s sovereign bonds that entered in mid-2023 have reaped substantial profits as spreads compressed dramatically from crisis levels.

The opportunity continues to attract emerging market investors seeking outsized returns, though Pakistan’s traditional risk factors persist. Energy sector circular debt remains a massive fiscal burden, with Rs. 4.7 trillion in liabilities threatening budgetary stability. The pension crisis has intensified rapidly, with obligations surging from Rs. 0.5 trillion in FY22 to Rs. 1 trillion in FY25. These unfunded commitments to military and civilian personnel effectively expand Pakistan’s true debt burden well beyond official figures.

External risks include potential US tariff impacts, though Pakistan’s limited export base provides some insulation compared to more trade-dependent economies. Remittances, the economy’s primary foreign exchange lifeline, have historically proven resilient even during periods of domestic stress.

Political dynamics and regional tensions with India remain wild cards that could derail progress without warning. The upcoming budget announcement on June 10th will provide crucial insight into the government’s ability to balance demand restoration with continued fiscal discipline under IMF conditionalities. n

OPINION

Reminder: Maryam Nawaz’s crusade to turn Punjab into a dictatorship continues Abdullah Niazi

The appearance of billboards stuck in the middle of Liberty Chowk in Lahore proudly advertising the Punjab Enforcement and Regulatory Authority (PERA) is the first subtle hint to the public that Punjab is set to go down the path of a draconian principality.

The authority, known by its acronym PERA, has been a major agenda item for Chief Minister Maryam Nawaz since the beginning of 2024. The premise for setting up the authority was innocent enough. Since the beginning of her term, the Chief Minister said she wanted to set up an enforcement agency at the disposal of the bureaucracy and the Chief Minister to enforce price regulation and help retrieve encroached land, they claimed.

The issue with price controls

Even in this initial, tame introduction, the idea of such an authority is frustrating. It represents the worst of Punjab politics. The idea that the government can, without any consequences, set prices for commodities and force private traders in a supposedly free market to comply. There is also the assumption that such actions will convince voters to support whatever party is in power.

We have seen many manifestations of this upsetting side of provincial politics before. The story is pretty familiar. You have the Chief Minister conduct a ‘surprise’ visit to a Ramzan Bazaar with the usual crowd of lackeys and protocol flunkies hot on their heels. The CM

The writer is senior editor at Profit. He can be reached at abdullah.niazi@ pakistantody.com.pk

derides high prices, hears a few grievances, says a few random monosyllabic words about hoarding, and promises to bring down prices. The photographers of the Directorate-General of Public Relations (DGPR)–the government’s PR arm–click away, and press releases are forwarded to every newspaper known to man. So when Maryam Nawaz expressed an interest in visiting bazaars, announcing reductions in prices, and performing the press talk circuit, it was not too surprising. At best, it was her trying to be politically expedient given her party’s popularity problem. At worst, it was plain stupidity.

Price controls, of course, are a fairly stupid idea. Controlling prices was a policy introduced by the British during the Second World War, and implemented through their network of powerful district commissioners. When Partition happened soon after, India and Pakistan took different approaches to what they would do with this bureaucratic network.

Guided by Nehruvian Socialism, India continued the wartime efforts of the British and made price controls and rationing an integral feature in its economic policies. Pakistan took a different approach. Instead of focusing on using the bureaucracy as an economic management tool, the country’s military leadership focused on using it to monitor and govern for law and order. Economic policy largely favoured free market principles.

But the fear of inflation seems to dominate Pakistan’s discussion of many economic policies that have little to do with inflation or the cost of living. For example, both the public debate and the political debate over what prices the government should set for its agencies’ sales of wheat and fuels is dominated by a widespread belief that raising these prices, or using a flexible market-determined pricing policy, would cause inflation.

Look at it this way. Maryam Nawaz thinks the average voter that will determine her political future is poor and cannot afford basic commodities for their family. She decides she will, with a wave of her pen, cut prices down for certain commodities. But what is she hoping to achieve from this? In these conditions, the hope of the CM would be that people save money from this reduced price and buy other products. So if Maryam Nawaz has decreased the price of, say, cooking oil, people will try to use the money they save to buy more sugar.

Here’s the problem: if the set price for cooking oil is lower than what the market will bear, the producers of cooking oil–who have to buy their raw materials from outside Pakistan–will simply not have enough money to buy what they need to make their product. There will be a shortage of the product, which the government will claim is because of “hoarders”.

This basic economic principle was generally understood in Punjab for a long time. Sure, every major supermarket has a DC rate counter with exactly four bags of rice available, and there are still a few

utility stores run by the Punjab Government, but by and large the prices of commodities in marketplaces have been left to the whims of the free market. Much of this attitude was actually fostered during Shehbaz Sharif’s time as Chief Minister of Punjab. Sure, the younger Sharif is as fond as anyone else of a good photo-op (his extensive collection of hats and boots would indicate as much) but he kept his Ramzan Bazaars and Sasti Roti Schemes in the realm of official subsidies instead of treating them like a magic wand with which inflation could be brought down.

Why then would Maryam Nawaz want to stake her political career on PERA, which was supposedly going to go around controlling prices? Because unlike what she was claiming, PERA would go far beyond the already ridiculous concept of price controls.

Ringing the alarm

The alarm bells first started ringing when the Punjab Enforcement and Regulatory Authority (PERA) Bill was presented in the assembly in the summer of 2024. On the 11th of August 2024, lawmakers gathered in the provincial assembly for a special session to mark Minorities Day. The purpose, as described by Speaker Malik Ahmed Khan, was to have a general discussion on the rights of minorities and recognise their contributions towards Pakistan. On the agenda item was something else. While lawmakers were

busy giving generic speeches and providing the usual lip service, the assembly was introduced to the Punjab Enforcement and Regulation Bill 2024.

The government was trying to bludgeon it through.

Back in September, this publication covered the events leading up to the tabling of this bill and how a few well meaning members from within the PML-N played a role in delaying the bill. The initial cause for alarm was over how vaguely worded the bill was. What did the government mean by any special assignments given on their discretion? Why was a law so vaguely termed? The wording made it seem like this authority would have a role to play far beyond just prices and encroachments. So when the bill went to committee, more things started to come to the fore.

The bill proposes the establishment of the Punjab Enforcement Authority, in itself a dystopia name that clearly indicates the desire to set up a parallel structure of government. The purpose of the authority would be to “oversee, spearhead and monitor the implementation of the policy guidelines issued by the Government.”

Sounds a little vague? It is.

The wording has deliberately been kept this way to allow this authority leeway to interfere wherever it feels fit. As one lawmaker who is also a practising lawyer tells us, this means the authority would have jurisdiction to “implement” government policies in marketplac-

es, on government land, but also over private businesses and individuals that they feel are going against government policy.

It gets worse. The authority is set to have a central board chaired by the Chief Minister, with the deputy chair being the Chief Secretary. The rest of the members of the board, with the exception of three MPAs and three private members appointed by the government, are all the secretaries of different departments. A confederacy of bureaucratic ineptitude would suddenly be in control of Punjab through PERA.

The officers working under these bureaucrats will have an important economic function in terms of enforcing price controls, but they will essentially also have policing duties.

And it does not end there. Has an enforcement officer shut down your shop or made a raid on your place of business? Want to make a complaint? Well you are not supposed to go to a judge. Instead, you will go before a Hearing Officer. These officers also operate under the auspices of the Punjab Enforcement Authority, and will settle all matters investigated by enforcement officers. The bill includes provisions for Hearing Officers hearing cases related to fines, confiscation of carts, removal of any encroachments, and every other level of minor civil offence. It also has an overarching declaration to have the authority to hear any case that an enforcement officer may have picked up on.

They have also been given the power to “use reasonable force, in case of retaliation or obstruction in performing the functions under the

Act, and the power to collect evidence through electronic means to inquire or investigate, such as CCTV camera recording; video recording; audio recording; photographs; electronic data; caller data records; geo-fencing; mobile device tracking; cyber surveillance and monitoring; digital forensics; and, Artificial Intelligence detection.” On top of this, they will also have a corp of sergeants under their authority who will have the right to arms.

For all intents and purposes, the bill sets up an alternative system of policing and justice within the province. One that is entirely loyal and answerable to the Chief Minister.

Where things stand

Back when Profit first did this story in September 2024, there was still some hope. The bill had been met with resistance and was sent to committee. The resistance did not last long. On the 13th of October, the bill was railroaded through the Punjab Assembly on a day when the opposition was absent and the speaker suspended debates. That means PERA now exists. We are simply waiting for the implementation to be

finished. Maryam Nawaz is impatient to have it done. In December 2024, she announced she wanted it done in three months. That has not happened. There have been functional delays.

The latest development is that Maryam Nawaz has given a deadline of the 30th of September this year for PERA to be functional. That gives us around 3-4 months before there is a second system of policing and justice in the province. Throughout the delays, the government has gone through the functions of making PERA exist at least as an idea. The authority has an official .gov website, it has officials, a chairman, uniforms for their officers, marked vehicles and other such trapping. They also have a social media presence. On Twitter, for example, they have an account that posts videos of meetings (with no audio naturally) that cut regularly to the chief minister either dictating instructions or looking on thoughtfully. The appearance of billboards full with Maryam Nawaz and Nawaz Sharif’s faces plastered next to the strange emblem for the authority (which sports the head of an angry looking clipart eagle as its mascot) is simply part of the continued effort to familiarise and prepare people for what is to come.

Private businesses, shopkeepers, traders,

and others running small and medium businesses should brace themselves. It is an unfortunate situation because the Pakistani bureaucracy, particularly the district administration, has long missed the powers they had in the bureaucratic setup that the British left behind. Many of their political, policing, and magisterial powers were stripped by reforms made by the Bhutto administration, and later by the 18th Amendment signed and enacted during the government of Mr Bhutto’s son-in-law.

So every time a new government comes to power, one of the complaints the bureaucratic machine brings up ad nauseum is their inability to ‘implement’ directives of the government because of their lack of powers. In the near two decades since the 18th Amendment, they have failed to get these powers back. Through PERA, Maryam Nawaz has the distinction of being the first chief minister in any province to give into the bureaucracy. She would do well to remember, as her father and uncle will tell her too, that trusting these unelected individuals that once passed an exam will not win her any votes. Price controls won’t either. But what PERA will do is leave a dark stain on any chance she has on a legacy. n

Cost-cuts send Gadoon’s bottom line soaring seven-fold

The textile company was able to boost profits even as revenues were largely flat this year

Profit Report

Gadoon Textile Mills Limited (PSX: GADT) has just delivered one of the sharpest earnings rebounds on record: profit after tax for the nine months to March 2025 leapt to Rs2.0 billion, nearly seven times the Rs278 million booked a year earlier.

The turnaround rests squarely on an aggressive efficiency drive – new high-speed spinning frames, a 16.9 MW solar-power array (with another 10.8 MW under installation) and tighter working-capital discipline – that has whittled energy and financing outlays to their lowest in three years. Management says the solar switch alone is trimming its electricity bill by Rs5–7 per kWh, with a target blended tariff of Rs30/kWh once the second tranche is commissioned.

At its twin plants in Swabi (Khyber Pakhtunkhwa) and Landhi (Karachi), Gadoon spins a 75:25 blend of locally sourced and imported cotton into carded, combed and polyester-cotton yarn for export and for the group’s home-textile affiliates.

The company has recently begun stepping up its own value-added output – knitted

greige and dyed fabric – to protect margins from raw-cotton swings. In 2022 it ventured further afield, commissioning a midsized dairy farm and UHT processing unit aimed at the institutional wholesale market. The project has run into headwinds from new sales-tax levies on corporate dairy sales, but management insists it will “continue to build out a branded dairy footprint” once the tax regime stabilises.

Gadoon began life in 1988 as a government-incentivised mill in the newly created Gadoon-Amazai Industrial Estate, part of an effort to replace opium cultivation with legal jobs. Five years later the business was folded into the Yunus Brothers Group – one of Pakistan’s largest industrial conglomerates – ushering in a two-decade spree of spindle additions and vertical integration.

The group merged it with one of their Karachi-based mills, Fazal Textile, in 2014 which gave it a southern production hub and doubled capacity to today’s 300,000-plus spindles. Along the way Gadoon earned a reputation for operating discipline and a willingness to bet early on renewables; its in-house wind-solar mix now meets 13% of a 42 MW load.

Strip out the headlines and the latest numbers tell a more nuanced story. Net revenue in the nine months ending March 31,

2025 inched up only 2% to Rs55.4 billion, yet cost of sales fell 1% to Rs50.3 billion, widening the gross margin to 9% from 7% a year earlier. Much of that relief came from a fortuitous slide in raw-cotton prices – now averaging Rs18,000 per maund versus well above Rs20,000 last season – and the stronger rupee-euro crossrate on imported fibres.

The danger, analysts caution, is that input costs could rise faster than Gadoon can eke out further process savings once China’s mills restock or if El Niño crimps the local cotton crop.

Finance costs – another swing factor – dropped 38% year-on-year thanks to early debt retirement and cheaper Export Finance Scheme (EFS) lines, but will track policy rates if the State Bank tightens again later in 2025. In short, the seven-fold profit surge is real, but investors would be wise to remember that roughly two-thirds of the delta came from the cost-of-goods-sold line, a benefit Gadoon does not control in perpetuity.

If cotton turns, the mill’s new solar panels and spindle frames will have to prove they can keep the power and productivity savings compounding – because this year’s windfall may owe as much to good timing as to good management. n

Cotton is no longer Pakistan’s White Gold. It is a ghost crop.

Cotton is a crop in collapse and Pakistan is a country in denial. Will the government do anything other than offering band aids for a hemorrhage?

Profit Report

In a move that would be laughable if it were not so tragic, Pakistan’s government has finally decided to pay attention to the cotton crisis.

Of course what that means is that the government has been pressured enough to “mull over” half baked measures that might appease members of a textile industry that is in free fall rather than actually go to the heart of the problem and address the concerns of the farmers that grow the cotton in the first place.

The Ministry of National Food Security and Research has endorsed a set of proposals to lift the 18% sales tax on domestic cotton and its byproducts. Alternatively, they suggest that imports of cotton, yarn, and grey cloth be taxed at the same rate. This gesture, coming after urgent appeals from the Pakistan Cotton Ginners Association and the All Pakistan Textile Mills Association, reeks of too little, too late.

These proposals, hurriedly pushed forward to Prime Minister Shehbaz Sharif after a high-profile media campaign by the industry, are an attempt to resuscitate a sector that has been on life support for over a decade. But a tax adjustment is a Band-Aid on a hemorrhage, and that too for the wrong patient. The rot runs much deeper.

Only three ginning factories are currently operational in Punjab. A few more in Sindh are expected to begin operations. This is not revival. This is slow-motion decay. If the current trend continues, industry leaders warn that processing units could run at less than half their capacity in the coming season.

Cotton is not just another crop. It is the very thread that once stitched together Pakistan’s rural economy and industrial ambitions. It is one of five “major crops” in the government’s own agricultural classification. These five crops form the basic matrix of household security and national food economics. And among these, cotton has suffered the most severe decline, with a drop of more than 30 percent in yield this year alone.

Cotton has a very specific history in Pakistan. For decades, it was the favored crop of millions of farmers, an economic staple that supported the textile mills of Faisalabad and Multan and Karachi. During its golden era, from the 1980s through the early 2000s, cotton was the lifeblood of Pakistan’s largest export industry. In 2008, Pakistan achieved a record output of 15.6 million bales. Farmers grew it with confidence. Mill owners purchased it without hesitation. The system worked.

Then it began to unravel.

The global recession of 2008 was a breaking point. High energy costs, currency depreciation, and an increasingly expensive business environment squeezed Pakistan’s textile industry. Mills began to shut down. From over 450 units in 2009, the number fell to around 400 by 2019. Domestic demand for cotton started to shrink. With fewer buyers, farmers began to question the crop’s viability. Cotton began to lose ground to alternatives like sugarcane and maize.

But the structural flaws in cotton farming itself were just as damaging. Poor quality seed, unchecked pest infestations, lack of investment in research, and insufficient irrigation support made cotton yields increasingly unpredictable. For many farmers, the crop was no longer worth the risk.

As a result, the country has gone from being a proud cotton exporter to one that now imports most of the cotton used in its own textile industry. In the first nine months of the 2024-25 cycle alone, Pakistan imported over 300 million kilograms of cotton yarn and two million bales of raw cotton. The cost to the economy runs into billions of dollars. This is money Pakistan cannot afford to lose.

It did not have to be this way. In fact, the government was handed a golden opportunity just two years ago. The year 2023 brought an unexpected uptick in cotton fortunes. Cotton arrivals had already crossed 5 million bales with a full quarter left in the year. It was a remarkable recovery from the dismal 4.8 million bales of the year before.

The temporary turnaround was helped by a set of global circumstances. A drop in US cotton production due to heat and drought created a vacuum in international supply. Cotton prices in Pakistan rose. The Trading Corporation of Pakistan entered the market, promising to purchase one million bales to stabilize prices and ensure growers received a minimum support rate of Rs 8,500 per maund. The rains let up. Quality improved. Demand surged. For a brief moment, the system clicked into place.

This was the moment to act. The state had a real chance to institutionalize support mechanisms, fix long-standing structural inefficiencies, and assure farmers that cotton had a future. But that opportunity was squandered. The support price did not translate into consistent procurement. Bureaucratic inertia blocked long-term planning. Instead of reforming the seed supply system or improving pest resistance research, the government slipped back into neglect.

By 2024, the progress had evaporated. Once again, cotton production plummeted. The area under cultivation shrank. Farmers, having been burned too many times, turned their backs on cotton. And with global supply chains stabilizing, the one-off conditions that had briefly boosted Pakistan’s cotton were no longer in play.

Now, the country finds itself in a deepening crisis. The few functioning ginning factories are an exception, not the rule. The majority are still shuttered. The prices of raw cotton are high but volatile, trading between Rs 17,000 and Rs 17,500 per maund. These prices reflect scarcity, not prosperity. High prices without high volume mean nothing to a struggling farmer or a half-operating mill.

The Export Facilitation Scheme, which has allowed for duty-free imports of cotton and yarn, has added fuel to the fire. Local producers find themselves undercut by cheaper imports. Millers are not to blame. They need reliable inputs to keep their units running. But without a level playing field, local cotton will always lose. This is not a market. It is sabotage.

Even the Ministry’s latest recommendations reflect an inability to grapple with the bigger picture. Equalizing taxes is a surface-level solution. What the sector needs is a holistic policy. That includes investment in seed research, climate-resilient crop development, modernized ginning, and reliable procurement mechanisms. We do not need tax breaks. We need cotton farming that is viable, modern, and can meet international standards. Anything less is a placeholder.

Cotton is more than an export commodity. It supports millions of livelihoods across the rural belt of Punjab and Sindh. It fuels the textile mills that form the backbone of Pakistan’s exports. It is a source of edible oil and livestock feed. And it is dying.

The government’s attempt to rescue the crop through tax reforms is a response driven by industry lobbying, not agricultural insight. It is an act of survival for textile mills, not a strategy for long-term revival. And unless policymakers move beyond patchwork solutions, the white lint that once clothed the economy will continue to unravel.

The cotton story is one of promises made and promises broken. Of golden years wasted. Of crises turned into catastrophes through inaction. Cotton is no longer Pakistan’s white gold. It is a ghost crop. And unless this ghost is confronted with something more than half-hearted measures, it will keep haunting the future of an already brittle economy. n

has helped the supplier to global brands survive the boycotts better than its end market

Pakistan Aluminium Beverage Cans Limited (PABC) ended the January-March quarter with net sales of Rs4.65 billion, barely 1% higher than the same period last year –but crucially, not lower.

In an environment where Coca-Cola Pakistan and bottler Pepsi-Cola International have posted mid-single-digit volume declines in the domestic market, holding the top line steady amounts to an out-performance. Western soda brands suffered a region-wide 7% sales slide in the first half of 2024 as boycott calls over the Israel–Gaza war spread across Muslim-majority countries, including Pakistan.

PABC’s ability to keep its order book full while its two biggest clients faced headwinds is the clearest sign yet that the can-maker’s diversification strategy is working.

Beginning last October, social-media campaigns urged Pakistanis to shun global chains perceived as sympathetic to Israel. Cola drinks were an early target: hashtags calling for boycotts of Coke and Pepsi trended for weeks, and convenience-store data showed shoppers switching to local substitutes such as Cola Next and Pakola.

Market researcher NielsenIQ estimated a 7% drop for Western soda brands across the Middle East and South Asia in the first half of 2024.

For PABC – long thought of as a backend supplier chained to multinational fortunes – the episode could have been existential. Instead, the company leaned on a growing roster of regional

and domestic beverage producers that had already begun shifting from PET to aluminium cans.

Incorporated in 2015 and backed by Bahrain-based Ashmore Investment Management, PABC fired up Pakistan’s first purpose-built aluminium canning line at Faisalabad’s FIEDMC industrial estate in 2017. Coke and Pepsi accounted for more than 80% of early volumes, but management deliberately targeted export markets – Afghanistan, Tajikistan, Iraq – and local independents to dilute that concentration risk.

A debottlenecking completed this year lifts nameplate capacity to 1.3 billion cans, and the plant already runs at about 89% utilisation outside the October-to-January off-season. The customer list now ranges from energy-drink startups to dairy and iced-coffee brands, many of which have used the cola boycott to capture shelf space.

Flat revenue does not mean stagnant performance. The full-year CY 2024 top line actually climbed 17% to Rs23.1 billion, supported by high-single-digit export growth and better product mix. Cost of sales rose roughly in line with revenue, yet gross profit advanced 10%, leaving a still-hefty 37% gross-margin.

A Rs2.2 billion windfall in other income – largely exchange gains booked when the rupee strengthened late last year – helped lift net profit 22% to Rs6.1 billion and EPS to Rs16.9 (from 13.9). The margin picture is visible in the table on page 2 of the briefing notes, where operating profit held steady despite a doubling of selling expenses tied to regional marketing support.

Looking ahead, management guides to Rs22 billion in revenue on 890 million cans sold in FY 2025, assuming macro conditions stabilise and new local-brand launches absorb off-take once dominated by the cola duopoly. Aluminium price swings remain a risk, but most contracts are pass-through, and the company has hedged forex exposure on primary ingot imports.

By broadening its client roster before a storm it could not predict, PABC turned what might have been a catastrophic year into one of quiet consolidation: revenues are steady, margins healthy, capacity expanding and dependency on any single buyer at an all-time low. As long as local challengers keep capturing the shelf space vacated by Coke and Pepsi, the can-maker from Faisalabad looks set to keep its own growth story –quite literally – on tap. n

Pak Datacom revenue rises, even as Starlink business remains stalled

The company’s revenue is up 14% so far in 2025 on the back of rising demand from corporate clients reliant on connectivity in otherwise unconnected areas of the country

Profit Report

Nine-month results to March

2025 show Pak Datacom Ltd (PSX: PAKD) growing net revenue to Rs1.28 billion, up 14 % from Rs1.12 billion a year earlier. Management attributes the acceleration to a ramp-up of its new satellite-internet initiatives: revenue in 3QFY25 alone matched the combined total of the first two quarters as subscription billing for recently-signed customers began to flow.

While gross margins slipped to 24% on higher bandwidth costs, net profit still edged up to Rs110 million, underscoring how quickly the top line is scaling.

What Pak Datacom sells is VSAT connectivity. The company commands an estimated 30–35% share of Pakistan’s very-small-aperture-terminal market, supplying secure links to banks, oil companies and government agencies.

It also sells wholesale bandwidth and managed networks. It buys capacity from local carriers at bulk rates and resells it on multi-year contracts, with fees tiered to bandwidth usage.

The company also offers satellite broadband for the underserved, a new growth leg built around Ka-band capacity from global

players. And it also has a business line selling solar and power-backup kits, bundled with remote-site terminals for corporate and public-sector clients. In addition, it offers in-building coverage solutions which consist of smallcell and antenna systems being trial-run in offices where 4G signals struggle to penetrate.

The mix is deliberately asset-light: Pak Datacom finances expansion almost entirely from internal cash, and has very little bank debt and still maintains one of the highest dividend-payout ratios in the PSX tech cohort (61% average in recent years).

The company operates in partnership with major global telecoms players. It is the Pakistan representative of British Telecom (BT) & Orange, sourcing international bandwidth and exchanging enterprise traffic through their global MPLS clouds.

It is also partnered with Kacific, a Pacific-based operator whose high-throughput satellites deliver affordable broadband to rural Asia. The tie-up lets Pak Datacom offer speeds of 10–100 Mbps in areas where fibre roll-out is uneconomic.

Pak Datacom is also pursuing a deal with Starlink through BT. Starlink has sounded out Pak Datacom for a 12,000-terminal wholesale deal once Pakistan’s uplink-licensing rules are

met; negotiations with space agency SUPARCO on domestic gateway rights are under way.

These alliances mean the company can layer managed services, cybersecurity and solar-powered ground stations onto third-party spacecraft without the capital burden of owning satellites itself.

Created in the early 1990s as one of the region’s first private VSAT integrators, Pak Datacom built closed satellite networks for the Pakistan Army, Navy and Air Force, and later rolled out connectivity for NADRA’s ID-registration field offices and Sui Northern Gas’s telemetry grid. By the 2000s it had broadened into banking backbones and oil-field pipelines, always eschewing leverage and ploughing cash into network upgrades.