33 From Budapest to Karachi: Gabor George Burt’s vision for Pakistani startups is simple. Do what is achievable

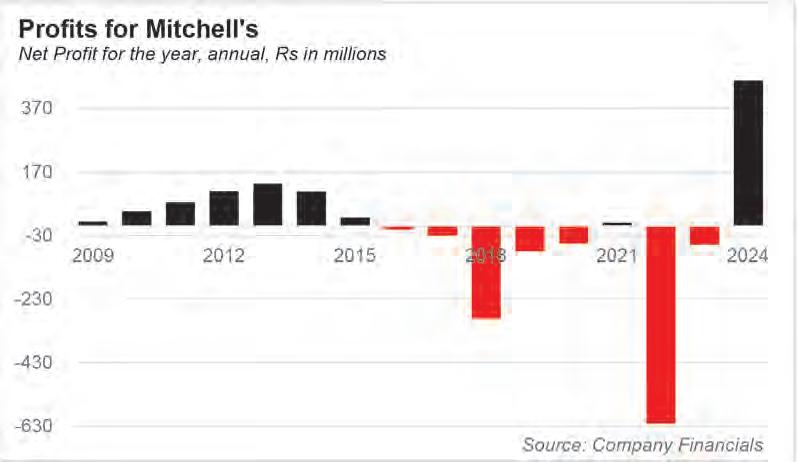

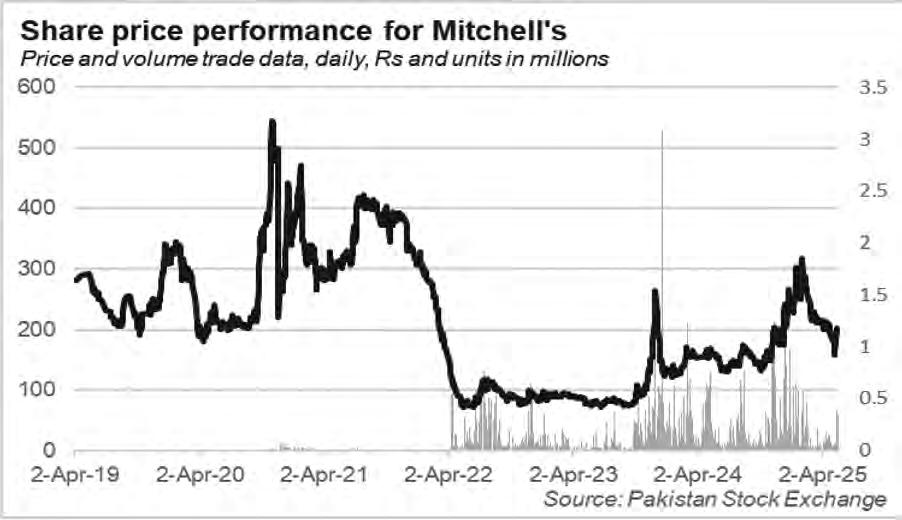

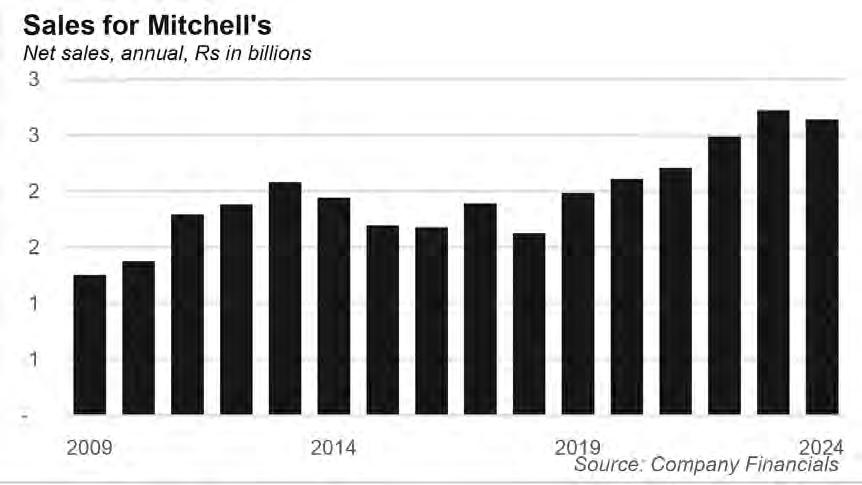

35 Sethi gets the job done at Mitchell’s

10 Pakistanis can now track their household carbon emissions

11 PTCL once again sees rising revenues and sinking profits. But is there a twist?

15 Bunny’s sets sights on the capital, plans bread plant in Islamabad

16 Pakistan’s major crops are going bust

20 Shield Corporation pulls the plug on diaper production

21 Investors giving Interloop’s zero credit for investments in growth

24 Igniting the Futures: H.G. Markets and the Dawn of Retail Participation in Pakistan’s Financial Landscape

28 The market is due for a fall. Are you ready?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

Pakistanis can now track their household carbon emissions

But what exactly can you do with this information, and is it enough to turn the tide?

Profit Report

Do you know your household’s carbon footprint? Most people don’t. Yet understanding your impact on the environment is the first step toward change. In Pakistan, where climate change hits hardest and air pollution is a daily reality, that knowledge is more urgent than ever.

Enter Carbonwise. Launched in November 2024, it is Pakistan’s first app dedicated to tracking household emissions. It aims to empower individuals with the tools to measure and reduce their carbon footprints. But the app is more than just a calculator.

Co-founded by Mahin Azam, Carbonwise offers a simple yet powerful idea. It makes climate action accessible at the grassroots level. Azam believes that if people don’t understand their impact, they won’t change. She says, “If you don’t understand your impact, how will you come up with a solution?”

The app evaluates emissions based on energy consumption, travel, waste, and other factors. But it does not stop there. It also provides practical steps to offset carbon footprints. One such initiative is a partnership with DeliveTree, which has already led to the planting of 60,000 trees in Lahore. The goal is not quick fixes but long-term change.

Pakistan’s climate problems are urgent. Smog chokes cities, waste piles up, and air quality deteriorates year after year. In Punjab, for example, the smog crisis has become bad enough that there is a recurring pattern of increased child hospitalisations with pneumonia and other respiratory diseases in the winter months. The data shows that these hospitalisations go far beyond what has been the normal rate of breathing trouble admissions for children in Lahore. Azam emphasizes that temporary measures won’t solve these issues. “The change won’t come if people aren’t aware

of it,” she says. To tackle air pollution and waste, Pakistan needs grassroots awareness and action.

The app’s sustainability marketplace is another key feature. It connects users with eco-friendly businesses, from solar energy firms to green startups. Azam envisions a space where individuals and companies can work together. “We see our app as a central forum for all things sustainable, where individuals and organizations alike can collaborate to combat climate change,” she says.

But progress is not without hurdles. A major challenge is the lack of localized data. Azam describes a frustrating landscape where government agencies are often unresponsive. “The government also isn’t doing enough, and I think that even as a society, we aren’t doing enough in terms of gathering and collating data,” she says. Without local data, making informed decisions remains difficult.

This systemic issue reflects a larger problem in Pakistan. The focus tends to be on short-term solutions. Long-term systemic change remains elusive. Azam sees her app as a tool to shift that mindset. “Unless we don’t start looking at how to change our lifestyle, how to come together for long-term solutions, the change won’t come,” she says.

The app’s dashboard feature is designed to foster accountability. It allows companies to track their employees’ emissions. Azam believes this can motivate organizations to adopt greener practices. “If you incentivize employees to reduce their carbon footprint, you’ll see results,” she suggests.

Azam’s vision goes beyond individual use. She wants the app to become a movement. She hopes people will challenge each other’s carbon scores and share their progress. Her ultimate goal is to make sustainability a social trend. Looking ahead, Carbonwise plans to expand. It

aims to include more offsetting options like solar projects and rural community initiatives. The focus is on reaching the most vulnerable and making climate action inclusive. Despite early promises, Azam admits changing consumer behavior in Pakistan remains tough. “People don’t care about climate change until it directly impacts them,” she says. Her solution is simple. Make sustainability easy and accessible. The app is designed to be a practical tool for future change.

Azam remains optimistic. She believes that individual action can spark larger systemic shifts. “Real change begins at the individual level. If we succeed in altering individual mindsets, organizations and governments will follow suit,” she says.

As Pakistan’s environmental challenges grow, Carbonwise stands as a beacon of hope. It is about more than tracking emissions. It is about inspiring a cultural shift. It is about giving everyone the power to make a difference.

With its partnerships—DeliveTree, PepsiCo, the Environment Protection and Climate Change Department, and others—Carbonwise is building a network of collective action. The goal is clear: turn awareness into action, and action into a movement.

In the end, Azam’s message is simple. “The key is making sustainability easy and making it a part of everyday life.” If Pakistan can embrace that, the country’s people might just lead the way in climate action. n

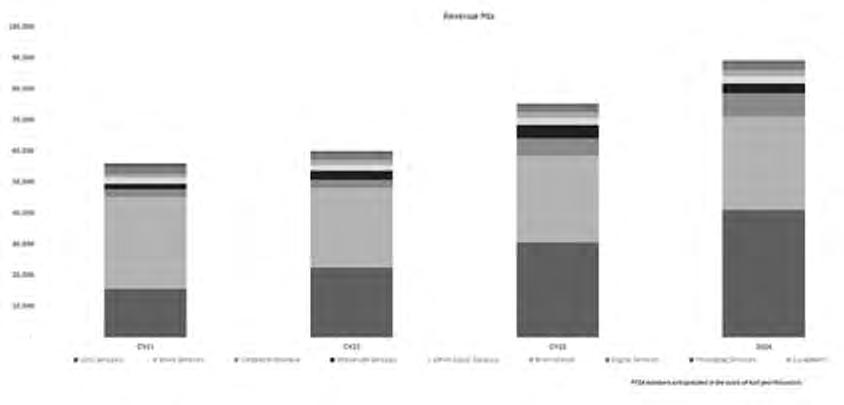

PTCL once again sees rising revenues and profits.sinking But is there a twist?

Every year, PTCL puts out an annual report that is painfully predictable. Their revenues increase and profits sink. But this year, one of their biggest liabilities, Ufone, has seen an improvement. What has changed?

By Hamza Aurangzeb

Every year, PTCL’s annual report reads like a script we’ve seen before: mixed performance, recurring challenges, and a sense of déjà vu. For years, the story has remained the same:

some divisions shine, others lag behind. The broadband, IPTV, and corporate and wholesale segments have consistently pulled their weight, keeping the enterprise afloat. But one unit in particular, Ufone, the Group’s mobile network operator, has been stuck in a rut for over a decade.

This year, however, there’s a twist.

Against the odds, Ufone showed real signs of life in 2024. According to PTCL’s 2024 annual report, revenue surged by an impressive 25%, with the pace of growth accelerating year after year. This unexpected boost didn’t just lift spirits; it played a vital role in strengthening the Group’s overall financial performance. Paired with the dependable

contributions from broadband, IPTV, and corporate services, the Group recorded its highest ever revenue: Rs. 220 billion, marking a solid 16% year on year growth.

But even as revenues hit new heights, the underlying story remains complex. The Group still posted a net loss of Rs. 14.39 billion, mostly due to hefty financing costs and non operating expenses. So while the momentum is promising, the recovery is still a work in progress.

So what are the forces driving this shift within PTCL? What is powering Ufone’s resurgence? How are other segments staying strong? And can this transformation steer the Group onto a more ambitious, sustainable path?

PTCL’s cornerstone

During CY24, PTCL delivered a 12% year-on-year revenue growth, an achievement primarily driven by the rapid expansion of its Fiber-tothe-Home (FTTH) services. FTTH’s revenue doubled to Rs. 9.7 billion, which elevated its share in the company’s fixed broadband (FBB) revenue to 46%.

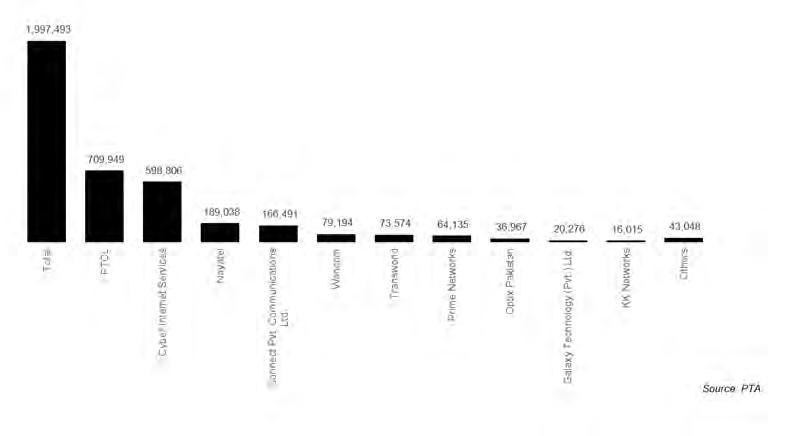

The fixed broadband segment as a whole posted a growth of 20%, while Shoq/ IPTV services expanded by 16%, reflecting broader digital adoption. However, FTTH stood out as the key growth engine. PTCL’s FTTH subscriber base surged by 65% yearon-year, reaching 678,000 users and capturing a 36% market share. Moreover, sales hit an all-time high of 281,000, with net additions of 266,000 that represented nearly half of all new FTTH subscribers across the industry. This performance was fueled by PTCL’s aggressive network rollout strategy.

By the end of CY24, FTTH coverage had expanded to 1.6 million homes, including 500,000 new rollouts within the year. As of March 2025, PTCL’s subscriber base had reached 709,949, maintaining its 36% market

share as the FTTH user base across the market approached the two-million mark. This was made possible through PTCL’s flagship FTTH brand, Flash Fiber, which recorded a spectacular 104% year-on-year growth.

Fixed broadband is making a strong comeback, fueled largely by shifting household behaviors. From 2014 to 2020, its adoption had steadily declined but that was until the global pandemic rewrote the rules of connectivity. As remote work became the norm and digital lifestyles took hold, household data consumption surged. Homes transformed into offices, and demand for seamless, highspeed internet grew.

Simultaneously, the rise of smart TVs and 4K streaming made uninterrupted connectivity a necessity across income groups, increasing screen time and content consumption. Moreover, the frequent mobile broadband disruptions, driven by load shedding and national security blackouts provided further impetus to the movement, making fixed broadband a more stable alternative. This resurgence is clearly reflected in the rising number of fixed broadband users and their growing data usage, which are expanding in many areas.

In fact, to meet this rising demand, PTCL is preparing to scale its infrastructure

with the upcoming Africa-1 submarine cable, which has successfully made its landfall at Pakistan Telecommunication Company Limited’s (PTCL) landing site at Sea View Beach, Karachi, however it is not operational yet. It will soon enhance PTCL’s ability to deliver faster and more reliable broadband across Pakistan. PTCL’s FTTH momentum has been impressive, its performance reflects its inherent strengths—such as early investment in infrastructure and a nationwide footprint.

All in all, FTTH didn’t just support PTCL’s topline growth in 2024 but it transformed the structure of its fixed broadband business. PTCL showcased strong execution through its FTTH brand, Flash Fibre, capitalizing on rising demand for fiber connectivity. This strategy proved pivotal in reshaping its revenue mix and strengthening its position in the digital future.

Although PTCL managed to augment its revenue through Flash Fibre, its net income halved during the year in comparison to last year primarily due to high interest costs for running finance, which increased 3.7 times, surging from Rs.1.74 billion to Rs. 6.9 billion within a year.

The broadband segment has been the traditional growth engine of the company. However, there are other segments as well which have had a notable impact.

The Evolution of PTCL’s Portfolio through Strategic Segments

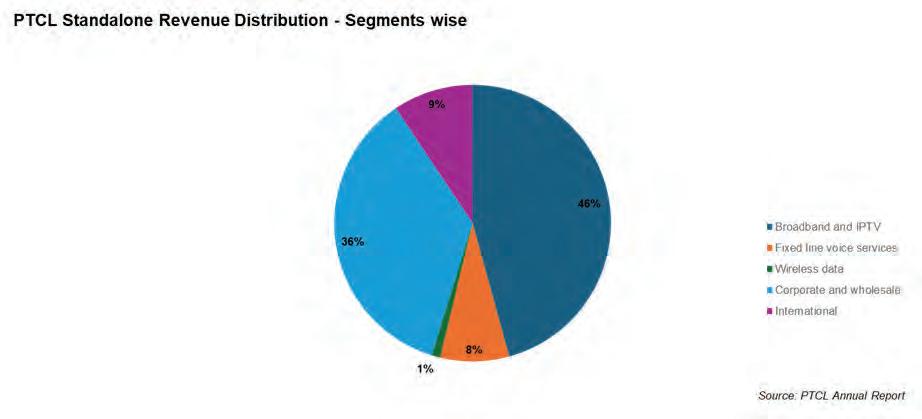

An analysis of PTCL’s operations on a standalone basis, reveals that it has a portfolio of five businesses, Broadband and IPTV, Corporate and wholesale, International services, Fixed line voice services, and Wireless data, where the segments have been arranged in descending order of size.

PTCL’s performance in FY2024 was anchored by steady growth and the expanding capabilities of its core segments, where

the distribution of the company’s revenue across key segments highlights both its legacy strengths and emerging areas of opportunity.

On the retail front, broadband and IPTV remained strong verticals, with revenue increasing by 20% year-on-year to Rs. 49.28 billion, driven largely by the rising adoption of FTTH and digital entertainment services. In contrast, wireless data services faced a steep decline of 36%, settling at Rs. 1.06 billion, reflecting the shift in consumer preference towards fixed high-speed internet due to better infrastructure and service delivery. Meanwhile voice revenue posted a modest 5% growth, reaching Rs. 8.69 billion, indicating some resilience in traditional services.

The retail segment continues to contribute a major share of revenue to PTCL but the company’s Corporate & Wholesale segment has also emerged as a catalyst for growth in recent years. In FY2024, the segment recorded an 11% year-on-year upsurge, reaching Rs. 38.62 billion, reflecting growing demand for enterprise-grade solutions across Pakistan’s evolving digital economy. This segment now represents 36% of PTCL’s overall revenue mix, which emphasizes its strategic importance.

Within the segment, Enterprise Solutions has displayed consistent momentum, where PTCL has expanded its service offerings across cloud, data center, and ICT domains, registering 29% growth in data center revenue, 92% in cloud services, and an impressive 103% in ICT solutions. Moreover, PTCL Business Solutions has also grown by 8%, handling 8.37 Tbps of domestic and international traffic. This growth was driven by increasing demand for enterprise connectivity, secure data infrastructure, and cloud-based applications across industries such as education, finance, healthcare, and FMCG.

The Enterprise portfolio has also evolved significantly, transitioning beyond basic connectivity to include IoT, Device-asa-Service (DaaS), and Terminal Management

Systems. PTCL has secured major clients in the fintech, retail, and security sectors, while powering surveillance infrastructure for public institutions and banks.

Lastly, we have PTCL’s “carrier of carriers” business in the segment, which enables other telecom operators and service providers to operate through its extensive fiber-optic and submarine cable infrastructure. The company now supports all major players in the telecom ecosystem, including CMOs, ISPs, and LDIs. Hence, PTCL is transitioning from a traditional telecom provider to a comprehensive digital infrastructure enabler by leveraging robust partnerships and the introduction of managed services such as DDoS, DNS, CDN-as-a-Service, and carrier-neutral IXP offerings.

Ufone’s recovery

PTCL’s key subsidiaries, Ufone and UBank, present two contrasting pictures as they navigate Pakistan’s complex telecom and financial

landscapes. While Ufone is showing signs of recovery after years of underperformance, UBank faces significant challenges despite deposit growth and operational scale.

Ufone, a laggard in the telecom industry, failed to keep up pace with its peers as it was the only operator in Pakistan that delayed the commencement of 4G services until 2019 and operated without a formal license until 2021. The year 2021 marked a turning point when the company secured its largest-ever syndicated loan to acquire 4G spectrum for $279 million, initiating a much-needed network overhaul. However, this debt-heavy strategy coincided with a harsh macroeconomic environment, including a surge in policy interest rates to 22% in 2023, which significantly increased the cost of borrowing for the company.

However, Ufone, despite these headwinds, rebalanced its business model between 2021 and 2024., where its data revenue rose from 28% to 46% of total revenue, while voice revenue declined from 53% to 34%, reflecting the broader market shift towards digital services. However, profitability remained elusive as operational and financial costs outpaced top-line growth.

Ufone has begun to realize the gains of its 4G playbook. In 2024, it reported a 25% year-on-year increase in revenue, driven by strong 4G adoption. Its 4G user base which climbed to nearly 16 million, and total data subscribers reached 18 million. Moreover, 4G traffic rose by 34%, and daily active users increased by 11% year-on-year.

This growth was enabled by a 148% expansion in its 4G tower base, from 4,077 in FY 2020-21 to 10,118 in FY 2022-23. Postpaid subscriptions expanded by 21%, and high-value customer sales rose by 5%. Most notably, Ufone returned to positive operating profitability for the first time in three years, a trend

expected to be sustainable through CY25 as financing costs gradually decline.

On the contrary, PTCL’s microfinance arm, UBank, continues to face considerable operational and financial challenges. During CY24, the bank’s bottom line deteriorated sharply despite a PKR 4.4 billion capital injection. While deposits grew 31% year-onyear to Rs. 136.6 billion and disbursements reached PKR 68.7 billion, revenue increased only marginally by 2.2% to Rs. 24.88 billion. UBank reported a staggering net loss of PKR 9.34 billion, down 1625.9% from the previous year, primarily due to a troubled lending portfolio.

To address these issues, UBank is undergoing a strategic shift—refocusing on gold-backed loan products and optimizing its branch network to manage risk and improve efficiency. These adjustments aim to stabilize the bank’s future operations; however, the turnaround may take time.

The Telenor merger

The management of PTCL seeks the acquisition of Telenor for improving operational efficiency and streamlining operational costs. The planned merger between Ufone and Telenor would mark a defining moment for PTCL Group, positioning it for scale, efficiency, and industry leadership in Pakistan’s highly competitive telecom sector. The regulatory approvals, particularly Phase II clearance from the Competition Commission of Pakistan (CCP) remain pending. However, PTCL still awaits for the green signal for the CCP despite its agitation due to a lengthy delay of the merger approval for more than a year.

Pakistan’s cellular market has long suffered from fragmentation, with four operators competing in a price-sensitive environment. As a result, its margins have consistently

ranked among the lowest globally. Telenor Pakistan’s exit is emblematic of these systemic pressures—its ARPU plummeted to just $0.70, far below the sustainability threshold of $1.5. In this context, consolidation isn’t just strategic—it’s necessary.

The Ufone-Telenor merger would propel the combined entity to a nearly 70.4 million subscriber base, placing it shoulder-to-shoulder with market leader Jazz. With a projected 30% share of industry revenues, the merged company would significantly alter the competitive landscape. Moreover, an initial ARPU of Rs. 253.33 per month presents strong monetization potential, especially as Telenor customers gain access to Ufone’s broader digital ecosystem, including OTT offerings like ‘Onic’.

Crucially, this merger is about more

than subscribers—it’s about assets, spectrum, and infrastructure. After the merger, the company will control 41% of the total retail market spectrum, the highest in the industry. Moreover, with dominant positions in critical bands like 900 MHz and 2100 MHz, and strategic presence across 1800 MHz and 850 MHz, the operator will be uniquely positioned to deliver superior mobile broadband services. Additionally, Spectrum refarming—transitioning legacy bandwidth into high-value broadband—would offer a scalable path to enhanced service quality, operational efficiency, and revenue growth.

On the infrastructure front, Ufone will inherit around 11,000 towers from Telenor, growing its footprint to 20,000 sites—the largest in Pakistan. This scale will enable the rationalization of overlapping assets while expanding into underserved rural regions by leveraging Telenor’s rural strength combined with Ufone’s urban concentration.

PTCL has a bold ambition for the future, which is to become Pakistan’s largest technology player by 2027 with the strategic monetization of non-core assets, investments in digital services, and leveraging infrastructure leadership for new revenue streams. However, the task is an onerous one due to the prevalence of stiff competition from rivals like Zong and Jazz. The Ufone-Telenor merger will certainly aid in transforming the Group into a full-spectrum digital entity ready for Pakistan’s digital future but despite that the company would require significant time, grit, and muscle to establish a fiefdom. The PTCL Group is indeed showing promising signs of improvement but it still has considerable ground to cover. n

Bunny’s sets sights on the capital, plans bread plant in Islamabad

Lahore-based baked goods manufacturer seeks expansion into the wider GT Road belt by setting up shop near the federal capital

Profit Report

Bunny’s Limited (PSX: BNL) told the Pakistan Stock Exchange late on 21 May that its board has approved the establishment of a new bread-manufacturing facility on the outskirts of Islamabad.

“The proposed plant will have an installed capacity equal to approximately 25 per cent of the company’s existing Lahore operations,” the notice reads. Management did not publish a capex figure, but said that it would be financed by the company’s internally generated free cash flow.

Founded in 1980 and listed via a reverse-merger in 2017, Bunny’s today sells a portfolio that ranges from staple sliced bread and buns to value-added items such as rusks, queen cakes, cookies and “Muncherz” snack foods.

Bread-related SKUs still generate about 90% of group turnover, with sliced loaves alone accounting for roughly 40%. Snacks contribute the remaining 10%. The company earned revenue of Rs7 billion for the year ended June 30, 2024. Nine-month sales to March 31, 2025 reached Rs5.504 billion, up 4.8% year-on-year, while gross profit nearly doubled thanks to cheaper wheat and cooking-oil inputs.

Although Bunny’s posted a net loss in

FY 2024 – mostly because of finance costs and one-off tax adjustments – it swung back to a Rs150 million profit in the first three quarters of FY 2025, easing balance-sheet pressure ahead of the Islamabad build-out.

At its single Lahore campus in Kot Lakhpat, Bunny’s runs automated lines that can turn out 13,500 tons of bakery products, and 1,800 tons of snack products per year.

Applying the company’s own “one-quarter” guide-post suggests the Islamabad line will be sized for roughly 3,750 tons – which would allow the company to cover demand in Islamabad-Rawalpindi and adjacent districts.

Bread’s two-day sell-by window makes freight from Lahore to Islamabad costly; a local oven trims delivery time from five hours to less than one, improving freshness and allowing the company to push deeper into Hazara and northern KP.

Consumption in the capital region has historically been met by Dawn Bread, which commissioned its own Islamabad bakery back in 1985 and still dominates corporate canteen and hotel orders. Bunny’s entry sets the stage for a two-horse race similar to the Lahore market.

Bunny’s move mirrors a broader trend of local FMCG brands expanding beyond home turf. Dawn Broad expanded into Faisalabad and Islamabad from its Lahore and Karachi

home bases in its initial decades. Gourmet has sought to expand from its Lahore base to all over Punjab and even into other provinces.

Rising inter-city motorway connectivity, modern cold-chain logistics and a 23-million-strong Islamabad-Rawalpindi commuter belt have made Pakistan’s twin cities the logical “next stop” for middle-tier food brands seeking scale without braving Karachi’s hyper-competitive landscape.

Bunny’s spent Rs188 million on plant and equipment in FY 2024 and a further Rs61 million in the nine months to March 2025. The Islamabad project will lift the capital-work-in-progress line again, but the company’s return to profitability and falling policy rates should keep gearing manageable.

At current utilisation, Kot Lakhpat generates about Rs7 billion in revenue. Adding a 25% satellite line could raise bread-division revenue by Rs1.4–1.6 billion annually once the plant is fully ramped.

For investors, the key question is execution: can Bunny’s replicate its Lahore route density in a market long served by Dawn? If it can, Islamabad may prove the template for a hub-and-spoke national network.

For now, the market’s verdict is cautiously optimistic: BNL shares added 4.3% in the two sessions following the disclosure, as traders wager that fresh capacity plus easing wheat prices will bake in a healthier 2026.

Pakistan’s major crops are going bust

The government can use all the projections and predictions it wants to, but increasing input costs and the vested interests of industrialists are eroding our agricultural output

By Abdullah Niazi

The government of Pakistan is lying to you.

But what else is new?

Last week, the National Accounts Committee (NAC) released the latest GDP data for Pakistan. Immediately there was attention on the fact that the NAC was indicating Pakistan had a GDP growth rate of 2.68%. This was a revision from the government’s previous GDP growth projections which had predicted GDP growth rate at around 3.6% for 2025.

Missing the target was not surprising. Global financial institutions were sceptical. The IMF had actually reviewed its projections earlier, predicting growth to be around 2.6% while the World Bank and the Asian Development Bank predicted it slightly higher at 2.8% in 2025.

The problem is even these revised projections from the government of 2.68% are far from accurate. At best, they are naive and hopeful. At worst they are deliberately misleading. In the numbers the government has released, GDP growth in the first three quarters has been 1.37%, 1.53%, and 2.4% respectively. While this indicates an increase in the growth rate with every quarter, it is still well short of the government’s projections of 2.68%. In fact, the average growth for these first three quarters is less than 2%. It was pointed out almost immediately by a number of individuals that the government was relying on a significantly increased projection of GDP growth in the ongoing fourth quarter being 5.47%

The projection of a sudden tide changing final quarter raises questions. On top of this, there is really very little in the NAC’s report that explains why the government would be this hopeful. Perhaps nothing indicates the dire situation Pakistan’s economy is facing more than the state of the agricultural sector. Overall, the agriculture sector increased by a very meagre 0.56% in this year.

This growth is not only partially based on projections, it is also only possible because Pakistan’s livestock sector

Livestock at a glance

saw a decent rise of 4.7% with fishing also increasing by 1.7%. What is concerning, however, is that major crops saw huge dips in production. Through a combination of senseless policies, water shortages, and increasing input costs, major crops have crashed out. The most prominent victim in this scenario was wheat, which saw a 8.9% decline in production, but other major crops were pretty far behind as well. The question is, how did such a dip go largely unnoticed, and why are we not producing as much of these crops?

Framing the agriculture sector

Our crops are failing. There is no other way to put it. We mentioned earlier that overall the agricultural sector has seen small growth of around 0.56%. This has been driven by livestock which has increased by 4.7% overall. Within the agriculture sector livestock is actually the biggest component, contributing around 60% to the overall sector.

This is actually a very interesting development since it has happened independent of any major policy shift or investment. Unfortunately, we do not have the exact numbers to account for this increase. The last time an agricultural census took place in Pakistan was 2006, so the latest federal data is more than two decades old. What we do have, however, is a census conducted by the Punjab government in 2016. While even this data is dated at this point, it gives us a clearer picture of how things have developed. This provincial livestock census reported that a whopping 70% of the milk producers in Pakistan are subsistence based, compared to a minuscule 0.5% of large peri-urban commercial milk producers. On top of this, packaged milk producers have actually suffered a major dip in sale in the past year ever since an 18% GST was added to milk. Since loose milk sells mostly in cash and through gawalas, more people are shifting to it. This might indicate that a lot of the boom in livestock production is coming from small to medium scale livestock producers.

And this is just to do with dairy farming. The numbers for frozen chicken and seafood being produced by Pakistan is also higher than one might imagine. In 2024, most consumer segments of the economy saw increasing revenues but declining sales and profits. This was because prices were higher due to inflation but the customer base shrunk since people had less money to spend. Despite this, according to a Euromonitor report from last year, in the processed and frozen meat and seafood segment there was a 29% increase in retail sales to over Rs 103 billion. The biggest player in this was K&Ns which had the lion’s share of 54%, but other smaller competitors like Big Bird, Sabroso, and PK Meat also made their mark. This has been a fast growing industry in Pakistan that has been doing remarkably well and deserves a story of its own.

5.1

million metric tonnes

And then there is cattle farming for meat. What we know locally as “barra and chota gosht” is a thriving industry that has actually become export oriented. Pakistan is a major producer of meat, with an output of 5.809 million metric tons in 2024. The country has carved out a significant market share in the Gulf Cooperation Council (GCC) countries, particularly in the fresh or chilled bovine meat segment. Recently, the markets opened to Pakistan with the success of The Organic Meat Company Limited (TOMCL), which has made a breakthrough in the Chinese market.

The livestock sector has been carrying Pakistan’s agricultural output number for a while now. And even though it

saw commendable growth this past year, it has not been enough to hide the major losses we have faced in traditional crop farming. That is because our major crops have taken an unprecedented hit in production.

What we call “major crops”

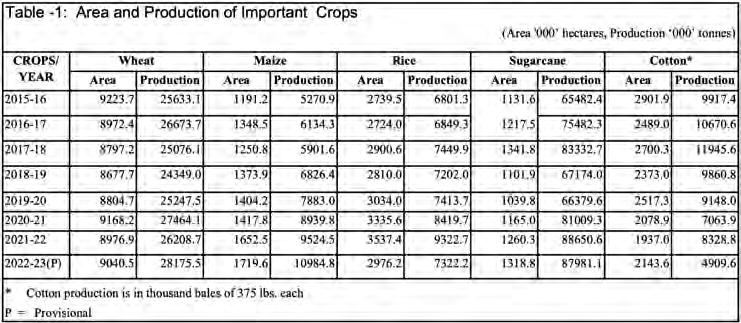

The government of Pakistan categorises around five crops as “major crops”. These are crops that they use as indicators because they are essential to food security and are used in a large quantity in the average Pakistani household. These basic items are wheat, rice, maize, sugarcane, and cotton. This basically covers the very barebones basic necessities of the average household. The production of these major crops has fallen by 13.5% this past year according to the latest data by the NAC.

Before we get into the specifics of what happened with each crop and why there was such a steep decline, it might be helpful to look at a table of information:

The graph table shows the area dedicated to the production of these major crops and their output. Straight from the get go one of the most noticeable things in this packet of information is the steep decline not just in the area on which wheat is being cultivated but the disproportionate effect this has had on yields. Cotton, of course, is a very specific story that also involves Pakistan’s textile industry and the energy crisis of 2008. But there are trends in other crops too. The area under cultivation for wheat has remained largely unchanged up until 2023 and production has also been quite stagnant. Maize has seen an increase in area under yield with the amount of maize produced doubling over the past decade. Rice has also seen a nominal increase in both yield and area under cultivation. Sugarcane, a dangerous water guzzling crop, has taken over a lot of the land once dedicated to cotton and has increased its yield as well.

What the data for the past decade tells us is that Pakistan has been woefully unable to increase its yields even when they desperately need to. In 2010, Pakistan’s population was still just under 20 crores. Today, it has inched up to 25 crores. That means we have 5 crore more mouths to feed and essentially no increase in crop output to show for it. In and of itself an increasing population in today’s world is not a bad thing for an economy. Pakistan has a high fertility rate at a time when major powers are struggling with their populations. A large, young, labour force can only be a good thing but you need to be able to feed them until they can contribute to society. This is a question that every nation in the modern world with an increasing population has to ask of itself. A state’s land is not

Fall

in production of major crops

kilograms, growers turned a healthy profit. That success gave them the confidence and the cash to invest in the next planting season. They bought expensive hybrid seeds, used proper doses of fertilizer, and even ran costly diesel powered irrigation systems. Their efforts paid off with record harvests of rice, maize, and cotton.

But the good times didn’t last.

In 2024, the government of Punjab, the country’s agricultural heartland, announced it would support wheat prices at the same level, Rs 3900. But when harvest time came, the government failed to buy the wheat it had promised to support. Left with few options, farmers were forced to sell their crop at rock bottom prices, sometimes as low as Rs 2400, far below the cost of production.

going to increase (short of the highly illegal idea of territorial expansion) and that means figuring out how to get more food out of the same amount of land. This requires dedicated research, modern farming practices, new seeds that are climate resilient, and a willingness to invest in food security.

All of this is based on data up until 2023. There was a slight blip in 2024 which actually saw farmers recovering from the devastating floods of 2022 and getting bumper crops. It was a time of great hope for a lot of farmers with many investing heavily in their crops that were meant to be harvested this year. The picture this year was starkly different. And it is worth looking at what happened crop by crop.

Cash strapped wheat farmers

One of the biggest crops affected was wheat, which saw a near 9% dip compared to last year. This marks a fall of nearly 3 million tonnes. Production last year was nearly 32 million tonnes. This year, all four provincial governments did not participate in wheat procurement, which they have been participating in for more than half a century. However, it was because of the IMF that they finally kicked this subsidy habit. There was a shift away from wheat this year because of this. There was a lot of anxiety amongst farmers that the wheat market will crash to Rs 1800 per maund this season against Rs 2900 per maund in 2024 and Rs 4000 in 2023. Astonishingly, the rate continued to hover around Rs 2550 but it still did not give farmers the kind of rates they have had in the past. In an inflationary environment, this makes life difficult for the farmers.

Think of it this way. In 2023, Pakistan’s farmers had a good year. Wheat, the country’s main food crop, was planted on nearly 24 million acres by more than six million farmers. With a strong market price of Rs 3900 for 40

Another blow came in July, when the government set district level price caps, limiting how much wheat could be sold for, all still below farmers’ break even point. Cash starved and demoralized, many farmers couldn’t afford the inputs needed for the next planting season. Fertilizer use dropped, irrigation suffered, and yields fell. The results are now visible in the country’s latest agricultural data: production is down, and the rural economy is hurting.

Wheat isn’t just another crop in Pakistan — it’s the backbone of the rural economy. When it stumbles, the rest of the agricultural sector follows.

As 2025 progresses, the crisis is only deepening. Experts warn that without serious reform, better access to farm credit, stronger private markets, improved grain storage, and tighter oversight of commodity pricing, Pakistan’s farmers could face another year of poor harvests and hard choices.

The water and resilience issues

In the case of wheat there was a clear trajectory in which the government bungled an unfortunate situation, resulting in farmers not having the capital to put more money into their production. But there were other crops facing tighter issues. Look at maize. While it might not be a crop as important as wheat or produced in as much quantity, its actually saw the single biggest dip amongst major crops.

Maize production fell 15.4% to 8.24 million tonnes from 9.74 million tonnes last year. Part of the reason for this is that crops are becoming increasingly affected by climate change, and the need for water has increased at a time when access to it is politicised. In 2024, Pakistan’s key summer crops — including maize, rice, cotton, and sesame — suffered under the weight of extreme weather. Unpredictable rainfall patterns, intense heatwaves, and rising temperatures all took a

toll on output. At the same time, many farmers lacked the tools and knowledge to adapt. Basic responses to climate stress, such as planting improved seed varieties designed to withstand tough conditions, remain out of reach for most.

One major issue that emerged last year was the widespread use of low quality seeds, especially for rice and cotton. These seeds were often unapproved and offered little resistance to pests or heat. Many failed to sprout properly. Poor seed quality, combined with worsening weather, meant that harvests were smaller than expected across large parts of the country.

Water shortages also piled pressure on the agricultural sector in the first half of the current fiscal year. Between April and the end of September, the amount of water available through Pakistan’s canal system dropped by over three percent compared to the previous year. This reduction hit parts of Sindh especially hard, where rice and cotton farms rely heavily on consistent irrigation.

Rainfall during the final months of 2024 made things worse. From September to December, precipitation was around 40% below normal. Much of the country experienced dry conditions, with some areas bordering on drought. Then came another setback: the cost of running electric tubewells shot up. In July 2024, electricity prices rose to record levels, about 20 percent higher than the year before. For many farmers already short on cash, this made irrigation even more difficult to manage.

As 2025 unfolds, the situation appears even more dire. Reservoirs are running low, and water supplies are expected to fall further. With less water available, farmers will likely plant fewer acres, and yields may decline again. These growing challenges point to another year of weak performance for Pakistan’s already struggling agriculture sector.

Why grow when you can import?

Of course then there are certain crops that have suffered purely out of the incompetence of the government. Take cotton for example. Once a proud producer, Pakistan now imports most of the cotton that is used for its once thriving textile industry. This has resulted in cotton being the biggest victim in the entire pile, and it saw the single largest dip among all of the major crops in question at more than 30%. Of course cotton saw a unique increase last year because of a oneoff set of circumstances in global trade that this publication has covered before. However, even by past standards, cotton is clearly suffering. There is now a rising concern that Pakistan’s cotton sector may be headed toward its worst financial crisis yet. The reason? A surge in tax-free imports of raw cotton and yarn, which local producers say is putting their

entire industry at risk.

Industry leaders are warning that if the current trend continues, cotton processing and textile units could run at less than half their normal capacity during the 2025 to 2026 growing season. Such a slowdown would not only hit jobs and exports but could also force the country to spend billions of dollars on importing cotton and edible oil.

At present, only three ginning factories have started operations in the Punjab towns of Khanewal and Burewala. A few more in Sindh, including in Tando Adam, are expected to begin work around late May.

Meanwhile, the first transactions for the season’s cotton crop are underway. Raw cotton is selling for between Rs 17000 and Rs 17500 per maund, while seed cotton is trading in the range of Rs 8300 to Rs 8500 per 40 kilograms.

In a surprising move, the federal government has allowed cotton seed imports for the first time in nearly five decades. Yet earlier test plantings using seeds from countries like China, Australia, the United States, and Brazil reportedly failed to deliver good results. However, it must be remembered that new seeds need to be trusted and adapted to local conditions by first using them on model farms. The last time there was life in Pakistan’s cotton production was two decades ago, when GMO seeds were first introduced to grow kapas.

The perfect disaster

Over the past few years, Pakistan’s farmers have gone through momentous changes. They have faced floods, change in decades old policy, rising costs, and erratic patterns of climate change that can be impossible to predict. This has resulted in high costs, and poor farm economics.

The result has already reached the population. A report from the UN’s FAO from 2023 shows that in an international ranking of the Global Hunger Index (GHI) this year, the country ranked 92 out of 116 nations, with

its hunger categorised as ‘serious.’ Pakistan currently faces a scenario in which it is largely food sufficient but not food secure.

This report came out in a year when Pakistan ranked 8th in producing wheat, 10th in rice, 5th in sugarcane, and 4th in milk production. What this last year has taught us is that our neglect of the agriculture sector has come to a boiling point. Forget about increasing yields, we are failing to even meet our past production. For decades, Pakistan Studies textbooks and government ads for fertilizer with dancing farmers in colourful turbans have taught the people of this country that our land has some kind of magic in it. No matter what happens, our farmers will grow food and we will be able to eat even if the rest of the world abandons us. All we need to do is cling to our nukes and our wheat and we will be able to live.

Well the wheat is going. It is slipping out of our hands and so is rice, maize, and cotton. We cannot do without them.

The government seems largely uninterested in fixing this growing problem. Their main concern seems to be window dressing performance numbers such as GDP growth that no one really cares about. While a government can put up as many happy looking advertisements in newspapers, robo calls in the PMs voice, and smiling faces on billboards, people will not care about nicely crafted pictures of a graph going up. They will only care about the availability and price of food products in the country.

The government has recently claimed that it is, for the first time, planning on introducing a climate-focused budget. These statements mean nothing when the government is actively not just trying to hide the facts from the public, but are trying to hide from the truth themselves. A 13.5% decline in major crops is not normal. A water crisis is not normal. The lack of a representative government that can truly take charge of this problem is not normal. And it will not be long before the obvious repercussions on this become apparent in the average household. n

Shield Corporation pulls the plug on diaper production

Stiff competition in an increasingly crowded market dominated by local subsidiaries of foreign multinationals made it difficult for Shield to stay in

Profit Report

Shield Corporation Limited (PSX: SCL) will shutter its loss-making diaper line next month in a sweeping reset of corporate priorities aimed at stabilising earnings and conserving cash.

In a notice to the Pakistan Stock Exchange issued on 21 May, the Karachi-based consumer-goods maker said its board had “authorised the Chief Executive Officer to initiate all necessary steps for discontinuing diaper production by 15 June 2025 or earlier” and to dispose of related machinery “in an orderly manner.” The communiqué added that the move follows “a comprehensive review of the segment’s operational performance, market dynamics and future outlook” and is “expected to contribute to an improvement in the company’s bottom line.”

Shield entered the disposable-diaper arena in 2014 with its Shield Premium range,

positioning the brand on an affordability-plus-quality plank against multinational heavyweights. A 2020 brochure described “three-times more absorbency” and vitamin-E-infused inner sheets as value-added selling points — evidence of the company’s early ambition to own a slice of the fast-growing hygiene segment.

Yet the brand never achieved the scale that Shield’s toothbrushes, baby bottles and soothers command in their niches. Management has long lamented the capital intensity of converting lines, the dollarised cost of fluff pulp and super-absorbent polymer, and a bruising price war at the economy end of the market.

Founded in 1975 and taken over by the Premier Group in 2002, Shield cut its teeth as Pakistan’s first local toothbrush manufacturer before expanding into baby feeders and, later, a broad baby-care portfolio. It listed on the Karachi bourse in 1977 and today operates an ISO-certified plant in Karachi’s Korangi industrial belt while marketing more than 300 SKUs nationwide.

In the financial year to June 2023 – its best year on record – net sales surged 64% to Rs4.36 billion as post-pandemic demand for oral- and baby-care products normalised and price hikes stuck. Gross margin inched up two percentage points to 26%, although soaring finance costs tied to double-digit policy rates eroded much of the operating gain. The years since have seen the company’s revenues plummet. For the 12 months ending March 31, 2025, revenues have slumped to Rs3 billion.

The company does not break out diaper-specific revenue.

Shield’s exit underscores how punishing the economics of Pakistan’s diaper market estimated to be worth $410 million in 2023 by JCR-VIS, a credit rating agency. JCR-VIS, in an industry note, pegs local manufacturers’ share of demand at roughly 90%, thanks in part to an import tariff of about 65% on finished diapers versus 0–11% on most inputs. That protective buffer, however, has spawned a crowded field where excess capacity and currency volatility compress margins.

Raw-material costs – denominated in dollars for fluff pulp, non-woven topsheets and elastics – have spiked since 2022, and a near40% slide in the rupee over the same period has compounded the pain. VIS estimates industry-wide gross margins fell from 15% in the fiscal year ending June 30, 2021 to under 9% in fiscal 2023 and warns that “weakening purchasing power is pushing consumers toward lower-margin Tier-III products,” a segment where Shield’s premium-leaning specs could not compete without discounting.

Competition is led by three multinationals that have sunk serious capital into Pakistani plants over the past decade:

• Procter & Gamble’s “Pampers” line is assembled at its multi-category campus in Port Qasim, Karachi.

• Belgium’s Ontex, maker of Canbebe, inaugurated the first foreign-owned diaper plant in 2013, also in Port Qasim, touting European-standard quality for local and export markets.

• Turkey’s Hayat Kimya, behind the Molfix brand, is investing $330 million in a 100-acre hygiene complex in Faisalabad’s M-3 Industrial City special economic zone – one of the largest greenfield FMCG bets in Pakistan in recent years.

Add to that a phalanx of home-grown producers such as Z&J Hygienic (Baby Master), Shield’s Karachi neighbour Santex (Butterfly Besties), and Lahore-based Dayimaan Hygiene, and the result is a market where retail shelf space is brutal to secure and television GRPs are auctioned at eye-watering rates.

Since early 2024, monthly energy surcharges and pulp prices crested simultaneously. While the company has not disclosed impairment charges, one can expect a modest one-time hit in fiscal year 2025 to write down specialised converting machines that may fetch less than book value on the secondary market. That said, scrap proceeds and the release of raw-material stocks could plug liquidity gaps without a rights issue.

The company emphasised that “all other lines of business will continue uninterrupted,” notably its flagship oral-care franchise (Shield, S-Mac) and BPA-free baby-feeding accessories, categories where it enjoys 30–60% market shares and healthier working-capital cycles.

Management’s medium-term roadmap, outlined in its 2023 corporate profile, centres on (a) distribution-led edge in tier-II and tier-III towns, (b) exploring export channels for baby feeders to Gulf markets, and (c) scouting “supplementary personal-care categories” that can be launched on existing equipment.

SCL’s thinly traded share drifted 0.7 % lower in Friday’s session to Rs274, broadly in line with the all-share index, signalling that the announcement had been partly priced

in after weeks of speculation. Still, skeptics caution that the company must guard against single-category dependence: oral care, while cash-generative, faces intensifying competition from imported value toothbrushes and herbal toothpastes.

Shield’s retreat is the second in the last two years by a local hygiene player: Ontex disclosed in September 2023 that it would exit Pakistan as part of a global emerging-markets divestment, although its Port Qasim plant continues to run under a transitional services agreement. The shakeout presages an era of consolidation where only operators with deep pockets, vertically integrated non-woven lines, or strong export corridors will thrive.

With birth rates still a robust 26 per 1,000 people – significantly higher than India’s 17 – Pakistan remains a prize, but the bar for efficiency is rising. Whether Hayat’s mega-site

or P&G’s regional hub can leverage scale to weather currency shocks may determine how long import-substitution tailwinds last. By jettisoning diapers, Shield is making a pragmatic – if belated – choice to live within its means and play to its strengths. The coming quarter will reveal the cost of exit and whether management can redeploy freed resources into higher-margin niches fast enough to offset lost topline.

For the broader consumer-goods landscape, the episode is a cautionary tale: tariff walls may invite investment, but only the fittest operators can survive when macro headwinds strip margins to the bone. Investors and industry watchers will now track two metrics – Shield’s gross margin rebound and its pace of new-product roll-outs – as barometers of whether the 50-year-old company can script a second act without one of its most ambitious wagers. n

Investors giving Interloop’s zero credit for investments in growth

The company’s profitability has faced pressure owing to investments in expanding its new product line; with the market focused on short-term profits, not long-term revenue

Profit Report

Interloop Limited (PSX: ILP) is having the kind of year every portfolio manager dreads. From 1 July 2024 through 23 May 2025, the country’s largest listed textile exporter has under-performed the KSE-100 index by a staggering 68 percentage points, according to the price-performance chart in Topline Securities’ latest company update. The share, which once traded above Rs84, now hovers near Rs57, even as the benchmark marches to record highs.

At first glance the market’s verdict seems rational: nine-month profit for the financial year ending June 30, 2025 collapsed 78% year-on-year after the company’s fledgling garment plant racked up heavy start-up losses and soaring interest rates chewed through free cash. But that same set of numbers also reveals why the sell-off may prove short-sighted.

Interloop has always been known

for socks, not shirts. Hosiery still supplies roughly two-thirds of revenue and enjoys gross margins north of 30%. Yet in fiscal 2024 the company increased its apparel capacity by 53% to 34 million pieces, kicking off trial production at a gleaming LEED-certified apparel park outside Faisalabad. Utilisation, however, averaged only 44%, pushing apparel gross margins to –19%. Those growing pains intensified in the current fiscal year. With output ramping to 60% utilisation on a still-learning workforce, apparel posted a gross loss of 26% in 9M FY 2025, dragging group margins down to 20.4% from 28% a year earlier. Investors recoiled; the stock followed.

Sell-side analysts, by contrast, are leaning in. Topline reiterates a “buy” with a June 2026 target price of Rs75 per share, which represents a 31% upside plus a 2% dividend yield for a 33% total return. Management guidance underpins that optimism. Revenue is expected to grow from Rs177 billion in 2025 to Rs276 billion in 2027, and

earnings per share is expected to go from Rs3 per share to Rs11.2 per share during the same period.

Put simply, analysts expect the apparel line to break even next year and swing to double-digit margins in 2027, lifting consolidated earnings at a 33% CAGR through FY 2029. At the current quote the share trades on 8 × FY 2026 and barely 5 × FY 2027 earnings, well below both its own five-year average forward P/E and the broader market.

Why the confidence? Because the garment plant is just one strand of a far larger expansion web. The Hosiery Plant 6 (commissioning 1Q FY 2026) adds 25% more sock capacity, taking the total to 91 million dozen pairs a year. Denim capacity will triple from 7 million to 18 million pieces by the fourth quarter of fiscal year 2026, positioning Interloop among South Asia’s largest value-added jeans exporters.

Yarn dyeing is rising 150% to 28 tonnes a day, ensuring colour consistency across the vertically integrated chain. And a further 4 megawatts (MW) of solar power lifts in-house renewable capacity to 16.6 MW, insulating margins from Pakistan’s volatile grid tariffs.

All told, management guides to a 21% sales CAGR between fiscal years 2026 and 2029, with hosiery and denim doing the heavy lifting while apparel utilisation climbs toward 75%.

Sceptics counter that the investment bill – more than Rs30 billion since FY 2023 – has saddled the balance-sheet with Rs87 billion of debt and driven finance costs to Rs10 billion this year. Yet policy rates have already fallen four percentage points from their 2024 peak; Topline models another two-point easing by mid-2026, slicing the interest burden by 25%.

The more stubborn expense is the “learning curve” in garments, where new lines historically take 18–24 months to hit steadystate efficiency. Interloop’s own track record in socks lends credibility: five hosiery plants scaled from 13 million pairs a month in 2003 to

73 million in 2024 while keeping segment margins north of 35%. Replicating that discipline in garments is the management team’s stated priority for FY 2026.

Topline’s discounted-cash-flow model, which assumes a WACC of 11.3% and terminal growth of 4%, values Interloop’s equity at Rs75 per share after netting Rs86 billion in debt. That implies the market currently prices in none of the step-change in free cash generation once the garment line crosses break-even and denim volumes treble.

Overlaying the earnings debate is the spectre of U.S. reciprocal tariffs ranging from 10% to 145% on selected imports – a populist gambit to shore up American manufacturing. Pakistan sits at a 29% duty versus India’s 26%, but crucially below Vietnam (46%) and far below China (up to 145%).

That matters because Interloop is the most U.S.-exposed name in Pakistan’s textile universe, deriving 51% of FY 2024 sales – about Rs80 billion – from American buyers such as Nike, Target and Walmart. Management argues, and most brokers agree, that punitive China levies actually expand the addressable pie for second-tier suppliers. U.S. sourcing teams scrambling to shift orders out of China are already redirecting volumes to Pakistan, India and Mexico, compressing lead times for tariff-free regions like Europe but leaving Interloop net-neutral – or even net-positive –on the U.S. front.

Political winds appear to be shifting anyway. Washington quietly signed a truce with the U.K. in April and granted Beijing a 90-day tariff pause to facilitate broader talks. Analysts therefore expect the current tariff matrix to settle into a more predictable regime that “will at the very least not render Interloop at a competitive disadvantage,” as Topline puts it.

Interloop’s investment cycle is not solely about capacity. The company now generates 12.6 MW of solar power and runs biomass boilers that cut CO₂ emissions by 52,000 tonnes a

year, according to its FY 2024 sustainability report. It funds healthcare, women’s training and wheelchair cricket, channels 4% of profits into community projects, and – for global fashion brands wary of “green-washing” – offers full traceability from yarn to finished garment.

Such credentials are already paying off: Interloop remains the only Pakistani textile mill included in the MSCI Frontier Markets Index and counts adidas, Nike and H&M among marquee clients. As Western retailers hard-wire ESG compliance into procurement scorecards, factories with solar roofs and wastewater recyclers are likely to command premium order flows and stickier relationships.

For all the upside, risks abound. Remove Pakistan’s GSP-Plus tariff waiver in Europe, spike the minimum wage, or let policy rates flat-line above 20% and DCF math unravels quickly. The company’s sensitivity to cotton prices and rupee depreciation is also well-documented. But the single most immediate swing factor remains apparel efficiency. Every fivepoint improvement in garment gross margin lifts FY 2027 EPS by roughly Rs2, based on Topline’s model – enough to justify another two turns of P/E multiple expansion.

Benjamin Graham called the market a voting machine in the short run and a weighing machine in the long run. Right now the “votes” on Interloop reflect fear: fear of debt, fear of tariffs, fear of execution mis-steps. Yet the “weight” of the numbers points the other way – toward a Rs275 billion revenue base, normalised margins and an equity value well north of current levels once the investment phase fades in the rear-view mirror.

If that thesis plays out, today’s depressed share price could look as much an anomaly as last year’s –68% relative performance. For investors willing to wait while management finishes stitching the final panels into its ambitious garment strategy, Interloop’s stock may yet prove that the real money is made in the hemming, not the hemming and hawing. n

the

and the Dawn of Retail Participation in Pakistan’s

Lahore Office

By Partner Content

The financial landscape of Pakistan is currently experiencing a transformative phase, marked by significant activity and the emergence of key players dedicated to unlocking its full potential. While displaying pockets of robust engagement, the nation’s futures trading industry holds substantial untapped potential. In the year 2024, the Pakistan Mercantile Exchange (PMEX) achieved a notable value traded of approximately PKR 7 trillion, indicating underlying market dynamism. With nearly PKR 1.2 trillion of value traded at PMEX in April 2025, it shattered all previous volume records and closed the month with an average daily traded value of PKR 50 billion. That’s nearly 70% increase compared to same period last year. However, this impressive figure coexists with a relatively low number of active Futures Brokers, numbering around 60 nationwide. Amidst this environment, H.G Markets Private Limited (HG), a constituent company of the esteemed Harvest Group, has distinguished itself as a dominant force, contributing over 40% of the total Value Traded on the entire Exchange. This article delves into the journey of HG and Harvest Group, their origins rooted from the Economic Reforms Act of Pakistan 1992, their role in introducing futures trading to the country, and their strategic vision for significantly augmenting retail participation in this vital market.

A Legacy Built on reform: Harvest Group and the Economic Reforms Act of 1992

In the early 1990s, the nation had recently emerged from periods of significant economic disruption and was poised for liberalization. A landmark piece of legislation, the Protection of Economic Reforms Act, 1992

(Act No. XII of 1992), was enacted by the Pakistani government with the explicit objective of furthering and protecting a series of economic reforms initiated from November 7, 1990, onwards. The Act aimed to cultivate a more liberal climate for savings and investments, foster confidence in the continuity of these reforms, and ultimately stimulate economic growth.

The preamble of the Act unequivocally stated the necessity to “create a liberal environment for savings and investments” and to provide “legal protection to these reforms in order to create confidence in the establishment and continuity of the liberal economic environment created thereby”. To achieve these goals, the Act encompassed several crucial provisions. It broadly defined “economic reforms” to include policies, programs, laws, and regulations implemented since November 7, 1990, covering areas such as privatization, promotion of savings and investments, fiscal incentives for industrialization, and the deregulation of investment, banking, finance, exchange, and payments systems. This comprehensive definition provided a legal framework for a wide array of liberalization measures.

A pivotal provision that significantly reshaped the financial landscape was the freedom granted to bring, hold, sell, and take out foreign currency. Section 4 of the Act bestowed upon all Pakistani citizens (resident within or outside Pakistan) and other persons the unfettered right to bring, hold, sell, transfer, and take foreign exchange in any form into or out of Pakistan. This eliminated the requirement for foreign currency declarations at any stage, thereby promoting greater freedom in managing foreign currency holdings. Furthermore, Section 5 provided significant immunities to foreign currency accounts held in Pakistan, guaranteeing immunity

from inquiry by taxation authorities regarding the source of funds, exemption from wealth tax and income tax on account balances and income, secrecy of banking transactions, and no restrictions by the State Bank of Pakistan or other banks on deposits and withdrawals.

The Act also included provisions for the protection of fiscal incentives for setting up industries, ensuring they would not be altered to the disadvantage of investors. It safeguarded the transfer of ownership to the private sector, preventing compulsory re-acquisition. Protection was extended to both foreign and Pakistani investments in various sectors, including industrial, commercial, shares, and financial institutions. Secrecy of banking transactions was mandated for all bona fide transactions, and the government’s financial obligations and contractual commitments were protected. Importantly, Section 3 declared that the provisions of the Economic Reforms Act would override anything contained in other existing laws, including the Foreign Exchange Regulation Act, 1947, the Customs Act, 1969, and the Income Tax Ordinance, 1979, highlighting the primacy of these new reform measures.

The Economic Reforms Act of 1992 played a crucial and direct role in setting the stage for the inception and early success of Harvest Group. The liberalization of foreign exchange regulations was the most significant immediate impact. Prior to this Act, foreign exchange transactions were subject to stringent controls. The 1992 Act deregulated the holding and movement of foreign currency, making it considerably easier for Pakistani citizens and entities to engage with international financial markets and services. This newfound freedom was a prerequisite for Harvest Group’s initial business model, which focused on facilitating clients’ access to international brokerage firms for trading in futures markets.

The Act’s broader aim to foster a liberal environment for savings and investments and provide legal protection to ongoing economic reforms instilled a greater sense of confidence

Japan Dojima Rice Exchange 1600s

among individuals and businesses in engaging with the financial sector, including exploring international market opportunities. The legal backing signaled the government’s commitment to a more open and market-oriented economy, encouraging entrepreneurial ventures like Harvest Group. The Act’s emphasis on the deregulation of banking and finance systems also contributed to a more conducive environment for the growth of financial services companies, paving the way for future developments in the Pakistani market. Mr. Muhammad Gulraze Mir, the visionary Founder & Chairman Emeritus of Harvest Group, recognizing these emerging opportunities within this environment of evolving financial liberalization, established the first Hong Kong – Pakistan joint venture firm under the Harvest Group banner in 1992. This pioneering initiative marked the beginning of the Group’s long journey, initially focused on introducing Futures trading to the local market by facilitating access to international brokerage firms.

The Global Evolution of Futures Trading: A Necessary Context

The market in which Harvest Group through its brokerage arm; H.G Markets operates in, has a rich and lengthy history, evolving from simple barter systems to today’s sophisticated electronic trading platforms. The origins can be traced back to ancient roots, with some of the earliest known forward contracts recorded in the Babylonian era around 1750 BC. These involved merchants agreeing in advance to deliver goods at a future date. While mentions of similar contracts exist in Ancient Greece and Rome, these were informal arrangements, not part of organized markets.

The first arguably formal futures market emerged in Japan in the 1600s. The Dōjima Rice Exchange in Osaka, established in the early 1700s, is often considered the first formal futures market. Japanese rice merchants and samurai utilized contracts to lock in rice prices

for future delivery, driven by market volatility. These contracts, known as “Cho-gomai” (rice coupons), helped samurai manage income and merchants hedge against price swings.

The birth of the modern futures market took place in the United States with the establishment of the Chicago Board of Trade (CBOT) in 1848. Chicago was a major grain hub, but issues with transportation and storage led to massive price volatility. Farmers, grain merchants, and processors needed a method to fix prices ahead of time. This initially led to forward contracts, informal agreements to buy or sell commodities at a future date. By the 1860s, the CBOT introduced the first standardized grain futures contracts, making them legally binding and tradable.

Futures trading remained primarily focused on agricultural commodities until the mid-20th century. A significant catalyst for expansion was the collapse of the Bretton Woods system between 1971 and 1973. The Bretton Woods Agreement, established in 1944, created a fixed exchange rate system where member currencies were pegged to the US dollar, which was convertible to gold at $35/oz. While fostering post-WWII stability, this rigid system proved unsustainable. In 1971, President Nixon suspended the convertibility of the dollar to gold (“Nixon Shock”), and by 1973, the system collapsed, leading most major currencies to adopt floating exchange rates.

The shift to floating exchange rates created currency volatility. Under Bretton Woods, fixed rates meant little need for currency hedging. After 1973, the unpredictability of floating currencies created a demand for hedging tools. This directly led to the birth of financial derivatives, particularly currency and interest rate futures. In 1972, even before the full collapse, the Chicago Mercantile Exchange (CME) launched the International Monetary Market (IMM), introducing the world’s first currency

futures contracts. The need to hedge interest rate risk also grew as central banks gained independence and rates became more volatile, leading to the emergence of interest rate futures in the late 1970s and 1980s. This period saw the rapid expansion of futures markets beyond commodities into financial instruments, energy, metals, and more recently, crypto futures.

H.G. Markets: Pioneering and Leading in Pakistan

In 1992, Harvest Group was one of the biggest subscribers of Reuters Money 2000 Terminal for the receiving of Reuters Financial Data, News, and Rates through satellite connections. At that time, the small dish apparatus and internet services were not available. We started with 200 Monitors and Slave Screens of Reuters Terminals in our Karachi and Lahore offices, making Harvest Group a unique financial entity besides the banking institutions who were receiving this information through satellite and terrestrial coaxial cable links.

In 2005, Harvest Group entered into a joint venture with one of the leading and largest brokers; CMC Markets UK, thus becoming the first in Pakistan to introduce online trading.

Built upon the foundation laid by Harvest Group and operating within the evolving global and domestic financial context, H.G Markets Private Limited (HG) was formally incorporated in the year 2013. As a constituent company of Harvest Group, HG inherited the pioneering spirit of the group which had already established a reputation for introducing futures trading in Pakistan by facilitating access to international markets.

Since its incorporation, HG has achieved significant milestones that solidify its position in the Pakistani financial market. The company is a licensed Futures Broker and Securities Broker by the Securities and Exchange Commission of Pakistan (SECP).

CBOT Exchange 1850s

Karachi Office

Via its PSX and PMEX based brokerage services, HG serves the investment and trading needs of customers across the country. Demonstrating consistent leadership and market penetration, HG has been Pakistan’s No. 1 Futures Broker by Traded Value according to the rankings of PMEX from 2014 to date. Their market-leading position in brokerage activities is supported by policies across all operations to enhance the overall trading experience for investors and traders. HG’s growth is also fueled by building the biggest sales and marketing workforce in the Pakistani financial industry. This workforce of around 400 professionals operates through registered offices branching over 5 cities of Pakistan, enabling significant domestic integration. HG has trained over 40,000 market professionals by conducting bimonthly trainings in all of its offices, ensuring high staff and client literacy. The scope of our trainings includes technical and fundamental analysis of the market by the Institute of Financial Markets of Pakistan (IFMP) certified trainers.

HG has consistently invested in technology and innovation being the first broker to introduce the MT4 and MT5 trading platforms which were later adopted by the PMEX. This ensured fast execution, transparency, and access to real-time data. Trading in mobile accessibility, client dashboards, and secure back-office systems have enhanced the overall experience of market participants, catering to the expectations of tech-savvy client-base.

Leveraged Trading: A Key Concept

Afundamental aspect of futures trading that often contributes to misunderstanding and hesitation among retail investors is leverage. Leveraged trading means controlling a large contract value with only a small upfront payment. In futures trading, this is possible because traders are not required to pay the full value of the contract upfront; instead, they post something called an initial margin. The initial margin is the upfront amount, typically a percentage of the total contract value that must be deposited to enter the trade. It is crucial to understand that the initial margin is not a down payment; it acts as a security deposit.

Leverage allows traders to trade a bigger position with a small amount of capital. For example, if trading a Crude Oil Futures contract with a size of 1,000 barrels at $80 per barrel, the total contract value is $80,000. If the initial margin requirement is 10%, the trader only needs to deposit $8,000 to control $80,000 worth of oil. This represents 10x leverage ($80,000 / $8,000).

The key characteristic of leverage is that it magnifies both profits and losses. Using the same example, if the oil price rises from $80 to

$82, the profit is $2 per barrel × 1,000 barrels = $2,000. On the $8,000 margin, this is a 25% return from just a 2.5% price move. However, if the price drops to $78, the trader loses $2,000, which is a 25% loss on the initial capital.

Traders must also be aware of the maintenance margin, which is the minimum amount that must be kept in the account to keep the position open. If losses cause the account balance to fall below the maintenance margin, the exchange may issue a margin call, requesting additional funds to top up the account. Failure to meet a margin call can result in the automatic liquidation of the position. Therefore, proper risk management, including the use of stop-losses and appropriate position sizing, is critically important when engaging in leveraged trading. Understanding this dynamic is vital for responsible participation in the futures market.

Price Action Explained

The international gold price trajectory from 2014 to 2025 demonstrates significant fluctuations influenced by global economic and geopolitical factors. The average gold price rose from $1,199.25/oz in 2014 to $2,656.35/oz in 2024. It has already marked a high of $3,509.90/oz in April 2025, with a forecast of $4,000.00/ oz for late 2025. Factors driving price changes include an impulsive U.S. dollar, interest rates, geopolitical uncertainties, market volatility, global economic uncertainties, the COVID-19 pandemic (increasing safe-haven demand), inflation concerns, and central bank purchases. Gold has demonstrated its role as a hedge against economic instability, and its upward trajectory in recent years underscores its continued relevance in diversified investment portfolios. The price of gold as of early May 2025, was approximately $3,395 per ounce. This context highlights the importance of gold futures trading as a tool for both speculation and hedging.

Strategic Vision for the Future

H.G Markets operates with a clear strategic vision and ambitious goals for the future of Pakistan’s financial market. A primary focus remains on augmenting the retail-base to increase the futures market participation rate. This vision extends beyond increasing trading volumes to empowering individual investors with the knowledge and tools for confident participation. Building on the pioneering efforts of Harvest Group, H.G Markets has established itself as a market leader by value. Their journey reflects a commitment to navigating challenges, adapting to technological advancements, and adhering to regulatory standards. However, they recognize that true market maturity and dynamism require broader participation, particularly from retail investors. HG’s strategic focus on enhancing retail participation through multi-channel education, accessibility, and trust-building initiatives is crucial for overcoming existing barriers and unlocking the immense potential of Pakistan’s futures market. By empowering individuals with knowledge and providing seamless trading solutions, H.G Markets is actively contributing to the evolution of a more vibrant, inclusive, and sophisticated financial future for Pakistanis enabling them to access local and international financial markets. n

Disclaimer:

H.G Markets Private Limited is not in investment advisory business and acts only as Member of Pakistan Mercantile Exchange and Pakistan Stock Exchange. Trading in securities and commodity futures is subjected to market risk. The amount you may lose is potentially unlimited and can exceed the amount you originally deposited. The information contained herein does not suggest or imply and should not be construed in any manner a guarantee of future performance and / or investment advice. Investors and traders are advised to read the risk disclosure document carefully along with the account opening form.

The market is due for a fall. ARE YOU READY?

With overstretched valuations, heightened volatility, and fears of a US recession, stocks may go into a long decline

By Muhammad Raafay Khan

It happens In the glossy boardrooms of Wall Street as much as it does in the stuffy offices of small brokerage houses in Karachi and at the desks of armchair investors sitting at home. A quiet spectacle unfolds each trading day of a game not unlike Jenga. That iconic tower of wooden blocks, so innocent in its premise and so ruinous in its end, offers a fitting metaphor for the modern stock market.

Each rally in the market, each new record high, adds another block to the structure. Stocks—blue chips, tech startups, meme darlings—are carefully balanced atop one another, pushed ever skyward by earnings reports, monetary policy, and investor euphoria. Confidence builds as the tower grows.

But much like in Jenga, elevation does not mean stability. The higher the tower climbs, the less secure it becomes. Each block removed to be repositioned like each stock