Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

DEATH GROUND: WHAT COMES AFTER THE INDUS TREATY

BRINKSMANSHIP, ARTILLERY BATTLES ALONG THE LINE OF CONTROL, EVEN DOG FIGHTING OVER PUNJAB ARE NOTHING COMPARED TO THE DANGER LURKING BEHIND THE SUSPENSION OF THE INDUS WATER TREATY. TO UNDERSTAND WHAT COMES NEXT, WE MUST FIRST UNDERSTAND THE RIVER THAT MADE PAKISTAN

By Abdullah Niazi

In 1950, the American lawyer David Lilienthal travelled to Pakistan and India to report on the emerging disputes between the two new nation states. Lilienthal was a prominent public servant in the United States. In the post war atomic era, he had been appointed to lead the United States Atomic Energy Commission. His visit to India and Pakistan, however, happened because of his credentials as director of the Tennessee Valley Authority, where he was responsible for managing flood control on the Tennessee River and charting plans to harness this mighty river for hydroelectric power.

During his time in the two countries, Lilienthal made some decisive observations. In a report written for Collier’s Magazine, he claimed that the Kashmir dispute was intractable, but there were other areas of mutual concern of the two nations where agreement could be found - such as the allotment of the water of the Indus River. The issue of water, Lilienthal felt, was the most vital to the future stability of the region, and it was Pakistan in particular that stood threatened.

“No armies with bombs and shellfire could devastate a land so thoroughly as Pakistan could be devastated by the simple expedient of India’s permanently shutting off the source of waters that keep the fields and people of Pakistan green,” he wrote in a report that would later become vital in efforts by the World Bank to broker the Indus Water Treaty of 1960.

That devastation is now knocking at our door.

The past few weeks have seen India and Pakistan engage in an armed conflict that overflowed into major cities, caused civilian deaths, and was the closest the region has been to all out war since both countries became nuclear armed. There is little need to recount the events of what transpired over the course of four days from the 7th to 11th of May seeing as most of our readers will have lived through it and any who did not will have anxiously followed every update. What is worth noting is that the public mood since the ceasefire was announced has been celebratory.

Yes the government and military leadership are enjoying their moment in the sun with billboards, full page newspaper advertisements, jet shows, television events and all the other thrills and frills of claiming victory in war — that is all well and true. But it has also become clear that most Pakistanis have walked away from this conflict with an overwhelming sensation of triumph and security.

The danger, however, is far from over. The biggest blow to Pakistan was already delivered well before the first airstrike was launched when India announced it was going to be pulling out of the Indus Water Treaty.

To put this in context, the Indus Water Treaty was signed in 1960 between President Ayub Khan and Prime Minister Jawaharlal Nehru. In 1964, Nehru died and in 1965 Pakistan and India went to war again. Despite the newness of his government, Nehru’s successor Lal Bahadur Shastri did not abrogate the treaty. Here is how ironclad the treaty is: as part of its provisions, India was meant to pay Pakistan £62 million in 10 equal installments. One of the installments was due in October 1965, which India paid despite the fact that the two countries had fought a war just three weeks prior!

The treaty continued to be in place through the 1971 war and again up until the Kargil conflict of 1999. The treaty has survived terror attacks and rising tensions between the two nations for decades. As global treaties go, it is as inviolable as they come.

Which is why India’s announcement in the wake of the Pahalgam Attack that they were exiting the treaty is unprecedented. It was not an announcement made lightly. Even though active hostilities have ended, the Indian state machinery is rapidly moving to choke Pakistan’s waterways. While Pakistan might celebrate what it views as a diplomatic and military victory, the country’s leadership would do well to remember chest thumping cannot drown out the very real threat of India squeezing Pakistan’s rivers dry.

While it might take years for India to do this, if they remain committed to this bit the results for Pakistan’s economy and society would be absolutely devastating. In the years to come, Pakistan will need firm and sensible leadership that can understand the issue of the Indus Water Treaty, parlay with India and be able to diplomatically find a solution to sharing natural resources, particularly at a time when climate change is making the region’s river systems severely unpredictable.

Right now the only person we have to offer for such a job is Ishaq Dar. This fact alone should strike more fear into the heart of the average Pakistani than the threat of any kind of missile, drone, or artillery fire. So how do we go about Pakistan’s problems with its rivers? The first step is to understand how the Indus flows, and why India has the valve that can cut us off.

A precarious lifeline

About 50 million years ago, in the Mesozoic era, the shallow sandy Tethys Sea upfolded and formed the Great Himalayan Ranges because of the collision of the Indian plate and the Siberian plate. The Indus basin comprised lofty Himalayan mountains in the north and flat plains of Punjab and Sindh in the east and south. These mountains with immense snow cover gave birth to the Indus River and its tributaries.

The river originates from Lake Mansarovar in Tibet, China, which stretches over 3200 kilometres. It flows through the Hindukush, joined by tributaries from Gilgit, Swat and Kabul, before flowing into the Punjab near Kalabagh. This is where five different freshwater tributaries which give the Punjab its name — Jhelum, Chenab, Ravi, Beas, and Sutlej — join the Indus before flowing together in a single mighty river all the way down Sindh and into the Arabian sea.

For centuries this has been the flow of the Indus. It has changed course, warped itself around cities, and spurned them when they have grown too large. It has, at the same time, been open to the manipulations of human civilization.

As the river stands today, a basic geography reminder might be pertinent to understand how each of the river’s tributaries flow in Pakistan and how they are related to India: Chenab: Originating in the Himalayas in India’s Himachal Pradesh, the Chenab flows through Jammu and Kashmir and into Pakistan’s Punjab, where it joins the Indus near Chiniot.

Jhelum: Flowing from Indian-administered Jammu and Kashmir, the Jhelum River winds through Muzaf-

farabad in AJK, and enters Punjab, meeting the Indus near Mithankot.

Ravi: The shortest of the major tributaries, the Ravi also originates in India and enters Pakistan, where it converges with the Chenab and Indus near Jhang.

Sutlej: The Sutlej begins in the Tibetan Plateau and flows through India’s Himachal Pradesh and Punjab before entering Pakistan, where it joins the Indus at Muzzafargarh.

Together, these rivers form a network of canals, lakes, and distributaries that feed the Indus Basin. The region around Multan, Sahiwal, and Faisalabad has some of the most vital and expensive agricultural land in Pakistan as a result of the direct access to the water from these rivers. With vast stretches of wheat, cotton, and rice fields irrigated by the waters of the Indus and its tributaries, a large portion of Pakistan’s agrarian economy is sustained through these select locations.

During the Raj, the British realised the strategic importance of controlling the Indus waters. They spearheaded one of the most ambitious irrigation projects in world history, transforming the Indus from a seasonal, often unpredictable river into the primary lifeline for millions of acres of farmland. The British constructed the Punjab Canal Colonies, a series of canals that diverted water from the Indus and its tributaries to create fertile farmland in what was once arid land. These efforts created a massive agrarian economy in Punjab, which produced wheat, cotton, and rice for the British Empire.

The canal network, while a technological marvel, also had significant ecological consequences. The waters of the Indus were diverted in a manner that dramatically altered its natural flow, causing the river to become more regulated and often less seasonal, yet prone to both floods and droughts due to the sudden changes in flow patterns. The extensive irrigation systems developed by the British paved the way for Pakistan, which would rely heavily on the river for decades to come.

By the time that the British left, the Indus River System was divided by political borders. Pakistan inherited the lower half of the system, but with a major issue: the majority of the river’s tributaries and control over much of its upper reaches were now in India. This led to tensions over water allocation, which have only been exacerbated by growing populations, climate change, and the increasing need for irrigation in an agrarian economy.

The Indus Water Treaty

The brutality of partition went far beyond communal violence. Not only had the British displaced millions of people and forced the

greatest mass migration in history, they had also cleaved a great country into two. One of the most fascinating aspects of studying geography is how scholars that study rivers see them as living beings. They have personalities, will, history, and life in them. The Indus was a river that had long been suffering already. Since the middle of the 19th century, it had been going through a series of unnatural changes as described above with the introduction of the Punjab Canal Colonies. Partition made this worse.

When the British Empire receded from the Indian subcontinent in 1947, it left behind more than a jagged border. It cleaved a living river system in two. The Indus River and its tributaries—lifelines that had irrigated fields, fed civilizations, and defined regions for millennia—now flowed through two hostile states, one upstream, the other downstream. The birth of India and Pakistan brought with it the question: Who owns a river that does not respect the lines on a map?

The geography behind the Indus Waters Treaty (IWT) is central to understanding its power and fragility. As we have mentioned above, the Indus River system originates in the Tibetan Plateau and flows through the Indian-administered region of Jammu and Kashmir before descending into Pakistan, where it fans out into the fertile plains of Punjab and Sindh before meeting the Arabian Sea. The system consists of six rivers: the Indus itself, along with the Jhelum, Chenab, Ravi, Beas, and Sutlej.

At Partition, India inherited control of the headwaters of all six rivers. The new border placed Pakistan downstream—a precarious position for a nation whose economy was, and remains, overwhelmingly agricultural. In the words of Pakistani water expert Daanish Mustafa, “Partition turned a hydrographic reality into a geopolitical liability.”

This upstream-downstream dynamic meant India, at least in theory, could alter or interrupt the flow of rivers on which Pakistan’s survival depended. In April 1948, India temporarily stopped the flow of water to Pakistani canals from the Ferozepur headworks on the Sutlej, asserting sovereign rights over the eastern rivers. This was a bombshell event that had never before been expected while India was whole. At the time, the operating theory in international relations was the “water wars rationale” that held countries would go to war when their water resources were threatened. This, however, proved to be an exception to the rule. Liaqat Ali Khan made a phone call to Nehru requesting the water flow be restored, and Nehru personally intervened with the West Punjab government to have the water up and running again. It was a moment that gave hope to future water sharing negotiations.

Though the interruption lasted only a few weeks, it sparked panic in Pakistan and revealed the high stakes of river politics. While the water war never went kinetic and both countries maintained diplomatic lines over this issue, the threat did loom large. Recognizing the danger, the World Bank — then known as the International Bank for Reconstruction and Development — stepped in. Eugene Black, its president at the time, offered to mediate. Negotiations began in 1952 and stretched on for eight years.

The eventual result was the Indus Waters Treaty, signed in 1960 by Indian Prime Minister Jawaharlal Nehru and Pakistani President Ayub Khan in Karachi. The treaty was quite simple. India would retain control of the three eastern rivers, the Ravi, Beas, and Sutlej. Pakistan would have rights over the three western rivers, the Indus, Jhelum, and Chenab.

While India agreed to allow “unrestricted flow” of the western rivers to Pakistan, it retained limited rights for domestic, non-consumptive use, and to develop run-of-the-river hydroelectric projects—projects that, by design, cannot store water. As political scientist John Briscoe notes, “The treaty is notable in that it allocated not just water, but entire rivers,” making it unique in the history of international water-sharing agreements.

At first glance, it appears India gave away a strategic advantage. So why agree? For starters, it was clear to everyone involved that if an agreement was not reached there would be war. India had control of the tap at the top, and if they were to use it, Pakistan would feel they had no option but to fight back.

Sun Tzu, in The Art of War, describes a concept called “Death Ground”: placing one’s enemy in a position where they have no choice but to fight because to not fight means accepting death. India’s post-Partition leadership was sensible enough to realise that, to not have a clearly defined treaty governing the rivers would mean putting Pakistan on death ground.

At the signing, Nehru tried to frame India’s rationale for signing the treaty as being for peace and stability. He said “We may have to make some sacrifices to ensure peace in the subcontinent,” at the occasion. But there were practical considerations as well. India’s water needs were being met by the three rivers it ended up getting, and the World Bank was offering substantial funding to develop infrastructure that would help both countries manage their allotted rivers.

For India, the treaty clarified its rights over the eastern rivers and paved the way for the development of projects like the Bhakra-Nangal Dam, which became a symbol of modern India’s engineering ambitions. In essence, the treaty exchanged some of India’s

theoretical control over the western rivers for clear legal authority over the eastern ones. It also got them international goodwill and the funding that came with it.

For Pakistan, the treaty was nothing short of existential. At the time of signing, 80% of its irrigated agriculture depended on the Indus system. Without guaranteed access to water, its economy — and food security — would be devastated. Pakistani negotiators viewed the treaty as a “life insurance policy.”

The funding it unlocked allowed Pakistan to build the Mangla and Tarbela dams, part of a vast replacement works project that re-engineered its irrigation system around the new division of rivers.

Even today, over 90% of Pakistan’s water use is for agriculture, much of it tied to the Indus Basin. The treaty, then, is not just a legal document. It is of vital importance to national security as well as food security. As such, the modern Pakistani economy we know today is possible

only because of the Indus Water Treaty. While in both countries, it enabled largescale agricultural expansion, hydropower generation, and rural development, it is disproportionately more important for Pakistan than India.

As things stand

This, to sum it up, has been a long winding explanation of both the Indus River and the treaty that governs it between two sovereign nations.

This is not to say that the treaty has been perfect. There have been many calls to renegotiate the agreement and revisit what was set out in 1960. While the treaty was heralded as a peaceful resolution of water issues between the two countries and was seen as serving the purpose for the last five decades. Even during full-fledged war the treaty remained enforced and effective. However, India, taking advantage of the provisions of the treaty, initiated some projects including Kishanganga, Baglihar and Wullar that (dams) revived, rather heightened water related tensions.

India’s current moves are similar to this historic trend. Because they have the ability to stop the water, India continues to rationalise exercising this power. Recent visits by this correspondent to barrages across Punjab and Sindh revealed a stark contrast in water quality, flow, and infrastructure — exposing a deepening crisis that directly affects millions of farmers and rural communities.

Other witnesses also present a bleak picture. At Sulemanki Barrage, the Sutlej River once a lifeline for southern Punjab has become a carrier of death. The water runs black, laced with white chemical froth. Local officials confirm that during winter, particularly in January and February, no actual river water reaches the barrage, only raw sewage. In these months, the river to wastewater ratio plunges to 0:100. The stench can be unbearable; standing near the barrage is described as nearly impossible.

Groundwater in the region is saline, making canal water the only source for drinking, cooking, and farming. The people of nearby Cholistan, one of Pakistan’s harshest deserts, depend on this tainted water often boiling it before use, but with no alternative in sight. This is not just environmental degradation; it is a slow burning humanitarian crisis.

The pollution is both domestic and transboundary. The Hudaira Drain, infamous for carrying untreated waste from India into Pakistan, delivers a toxic load from both sides of the border. Indian industrial and urban effluents flow into the Ravi River, combining with sewage from Lahore, Faisalabad, and Kasur including waste from tanneries before spilling into the Sutlej. This upstream activity reduces clean water availability for Pakistan in the critical winter season, when snowmelt from the Himalayas is minimal.

At Head Islam and Punjnad Barrages, the story remains grim. Polluted, low flow water reaches farmers too late or in quantities too small to matter. Irrigation officials spend most of their time mediating disputes over dwindling supply.

In stark contrast, Sindh tells a different story. At Guddu Barrage, the Indus flows clean and strong. The Pat Feeder and Ghotki Feeder canals were operating during the visit, and the

water was visibly healthier. At Sukkur Barrage, the world’s largest irrigation system, water still commands respect. While right bank canals like the Nara Canal flowed with strength, left bank canals were noticeably weaker as a result of post 2010 flood changes and sediment shifts that have tilted the river’s natural flow.

The contrast between Punjab and Sindh is not merely ecological but geopolitical. India, as the upstream country, controls the flow of the eastern rivers including the Sutlej and Ravi under the Indus Waters Treaty. During winter, when India’s use for irrigation and hydropower increases, the outflow to Pakistan decreases. While permitted under the treaty, the timing and volume of water releases can have devastating effects downstream when no clean water arrives to dilute pollution.

This is not just a local environmental tragedy. It is a test of regional cooperation, science, and governance. Without serious bilateral engagement and investment in pollution control, the rivers of Punjab may soon carry little more than poison if they carry any water at all.

What happens now

This is a description of the scenario as it has existed for the past few years, where pollution flows heavily in from India but water is regularly restricted. Now, India is making moves to develop its river infrastructure in a way that gives it even more control.

After the April 22 attack, Indian Prime Minister Narendra Modi ordered officials to expedite planning and execution of projects on the Chenab, Jhelum and Indus rivers, three bodies of water in the Indus system that are designated primarily for Pakistan’s use, six people told Reuters.

One of the key plans under discussion involves doubling to 120km the length of the Ranbir canal on the Chenab, which runs through India to Pakistan’s agricultural powerhouse of Punjab, two of the people said. The canal was built in the 19th century, long before the treaty was signed.

This would be a major struggle for Pakistan. As explained by one official from IRSA, India is allowed under the Indus Waters Treaty to take a limited amount of water from the Chenab River for irrigation. However, officials familiar with internal discussions say that India is planning to expand the Ranbir Canal, which would significantly increase how much water can be diverted. Right now, about 40 cubic meters of water per second is drawn, but the new canal could allow up to 150 cubic meters per second. Experts say this kind of expansion would take years to build.

These internal discussions reportedly began last month and are continuing, even after

the recent ceasefire between the two countries. Officials from India’s water and foreign ministries, as well as the prime minister’s office, have not made any public comments about the project.

If India continues to ignore the treaty, they will embark on the path to building low dams and hydropower projects that will dry up water in the Western Rivers Pakistan is supposed to have control over.

Death ground

The Indus Waters Treaty is often praised as one of the world’s most successful water-sharing agreements. It has survived wars, coups, and near collapse. Yet it is also a fragile peace. Climate change, population growth, and upstream development are increasing tensions. Academic observers caution that while the IWT remains a “resilient legal framework,” it is under stress. As geographer Isha Ray puts it, “The treaty assumes stationarity in both hydrology and politics, which is an assumption that no longer holds”.

For Pakistan, the logic is quite simple: if India makes efforts to hinder the supply of water to which Pakistan is entitled under the treaty, and on which it is wholly dependent, that is tantamount to putting Pakistan on death ground. Pakistan has no choice but to fight India because to not fight means to accept death.

India’s leadership has long understood this and also that much as they may loathe Pakistan’s leadership, the two countries are stuck next to each other, and to put Pakistan in that position means foreclosing the option of a peaceful coexistence. This generation of Indian leadership, however, appears to be unburdened by such weighty considerations of wise statesmanship.

To them, causing Pakistan pain in increasing doses will cause Pakistan to yield. The problem with that theory is that Pakistan has to believe that India’s demands will be reasonable, and when complied with, the pain will stop. That implies some level of ability to trust.

When someone threatens your water, and therefore your very ability to live, the question of trust is gone. At that point, the choice is simple: fight, or die.

We want to make it very clear: India has NOT yet put Pakistan in this position, merely mused about it. And while Pakistan should use diplomatic means to dissuade India from undertaking any actions against the letter and spirit of the Indus Water Treaty, the language should also make it plain: do not put Pakistan in a position of having to fight for its life.

We are not a nation that will go gentle into that good night. n

Lucky Cement’s new Iraq plant comes online

One of the largest cement manufacturers in Pakistan is now also a major player in the Iraq market

LProfit Report

ucky Cement’s decision to light a second kiln at Samawah, Iraq, on 13 May 2025 marks a watershed moment in the global ambitions of Pakistan’s best known construction materials group. In a short notice to the Pakistan Stock Exchange the company confirmed that the new 1.82 million tonne per annum clinker line, built alongside the 1.31 Mtpa unit commissioned in 2021, has entered hot run testing and is expected to reach commercial dispatches in July.

The achievement is not simply an engineering milestone; it pushes Lucky’s consolidated name plate capacity above 21 million tonnes a year across three countries and demonstrates that Pakistani industrial capital, honed in the hills of Khyber Pakhtunkhwa, can thrive in the post war economy of the Middle East.

The Samawah expansion is housed in Najmat Al Samawah, a 50 50 joint venture between Lucky Cement and the UAE based Al Shumookh Group. Built by China’s Sinoma International, the second line can fire 5,800 tonnes of clinker a day on a fuel mix dominated by southern Iraqi natural gas, supplemented by up to twenty per cent alternative fuels such as rice husk and shredded tyres. A 25 MW captive power plant hums next door and a waste heat recovery unit—planned for 2026—should whittle electrical consumption by another twenty five kilowatt hours per tonne. When a 0.65 Mtpa grinding and packing facility at Umm Qasr comes on line, probably early in 2026, the Samawah complex will supply cement and clinker to an arc that stretches from Baghdad and Basra to Kuwait, Bahrain and the Horn of Africa.

If geography explains part of the attraction, economics seal the deal. Iraq’s appetite for cement has bounced back to roughly twenty five million tonnes a year on the back of state funded housing, oil field infrastructure schemes and the continuing reconstruction of Mosul. Many of the country’s legacy state owned plants remain crippled by under investment, so effective domestic capacity is

materially below the notional forty million tonne figure often cited by officials.

Imports from Iran and Turkey still plug a three to four million tonne gap. A Samawah produced tonne of clinker delivered to a central Iraqi mill is six to eight US dollars cheaper than an imported tonne once transport and duties are included; the arbitrage is larger still in Kuwait, which has capped its own carbon heavy cement production. As Lucky is paid largely in US dollars, the company also gains a natural hedge against the chronic depreciation of the Pakistani rupee.

The Iraqi strategy meshes neatly with Lucky’s plan to create self contained regional clusters. The forthcoming Basra grinding mill will be fed entirely by Samawah clinker, sheltering it from the import tariff Baghdad imposed in 2024 to nurture fledgling local production. Surplus material from Samawah can travel by rail and road into Kuwait or move as coastal shipments to East Africa. Conversely, if Pakistani coal prices spike, management has hinted it might ship Iraqi clinker back to its Karachi plant, turning a foreign asset into a domestic hedge.

This outward push is the culmination of three decades of restless growth. Lucky started in 1993 with a modest kiln at Pezu, spent the early 2000s layering on debottlenecking projects, and by 2012 had emerged as Pakistan’s largest cement producer. It then hedged its bets abroad: a 1.31 Mtpa plant in the Democratic Republic of Congo in 2017, the first Samawah line four years later, solar and wind farms in Sindh, and a majority stake in Kia Lucky Motors at Port Qasim. The latest Iraqi kiln lifts foreign operations to twenty eight per cent of group EBITDA; the board wants that figure above a third by 2027.

No foreign venture is free of risk and Iraq carries more than most. A disruption to the Basra gas pipeline could force the plant onto costlier imported coal; Baghdad’s intermittent price controls might crimp margins; and the security situation, though calmer in Al Muthanna than in the north, still demands expensive convoy protocols for spare parts sourced via Kuwait. Perhaps the biggest long term threat is the next capacity cycle: at least

eight million tonnes of new Iraqi and Saudi capacity is slated to appear between 2026 and 2028, and another supply wave could push clinker discounts wider unless the economy keeps expanding.

The broader Iraqi chessboard is becoming more crowded. Lafarge Iraq runs six million tonnes of capacity at Karbala and Bazian; Northern Region Cement of Saudi Arabia has commissioned a 1.3 Mtpa line; Sinoma and Al Diyar expect to fire a 1.8 million tonne kiln in Samawah later this year; and Chinese backed projects are sprouting in Erbil. Effective utilisation will hinge on whether Iraq can sustain gas supplies, keep its reconstruction budget funded and restrain regional competition. Lucky’s early mover advantage—and Al Shumookh’s local political heft—give it a head start, but vigilance will be required to protect margins.

Seen through the lens of capital allocation, the second Iraqi line is a calculated gamble—but one Lucky appears well placed to manage. The Al Nabulsi family controlling Al Shumookh brings deep political networks in Samawah; the region’s natural gas bounty lowers the plant’s carbon and cost footprints; and Lucky’s in house engineering division has accumulated a store of expertise in building kilns quickly and cheaply. If the group can navigate sovereign risk shocks and the cyclical vagaries of cement, Samawah could supply dollar earnings for a generation and serve as a template for other Pakistani conglomerates venturing abroad.

For Iraq, the 1.82 million tonne addition reduces dependence on imports, supports an embryonic construction boom and signals that serious foreign capital—albeit from a frontier market peer rather than a Western multinational—judges its risk reward equation acceptable. For Pakistan, it proves that local know how, born of decades of coping with energy shortages and currency swings, can compete— and win—far from home. And for Lucky’s shareholders, it reaffirms a strategic credo that has served them well for thirty years: in a commodity business, staying one kiln ahead of the competition is often the surest path to durable returns. n

Powering progress: Finance with purpose

Ayla Majid, ACCA’s first South Asian President, on sustainability, gender equity, and the future of the profession

By Partner Content

Sustainability

How does ACCA plan to integrate sustainability into its global operations and member services?

Sustainability is central to ACCA’s mission and strategy and reflects our commitment to shaping a better world. Our ambition to achieve Net Zero by 2030 guides our operational decisions, with annual reports detailing our environmental footprint. Beyond internal operations, we support our members with practical resources, CPD modules, and thought leadership to embed sustainability within the profession. Our “Accounting for a Better World” report outlines ACCA’s sustainability roadmap, reaffirming our dedication to the Sustainable Development Goals (SDGs) and stakeholder engagement across markets. In

addition to this, we’ve launched a Climate Hub for members, offering practical tools, policy updates, and expert webinars in order to integrate sustainability into their practices and enhance their capabilities in sustainability reporting and climate finance.

What initiatives will you prioritise to promote sustainability reporting among ACCA members?

As ACCA Global President, I believe in advancing sustainability reporting across our global membership particularly as the adoption of ISSB’s IFRS S1 and S2 gains momentum. In Pakistan, the SECP has already announced phased implementation of these standards which highlights the urgent need for finance professionals to align reporting with global best practices. High-quality sustainability disclosures lead to greater transparency, enhance corporate credibility, and create pathways to sustainable investment and financing. These

are no longer just compliance measures rather are critical tools for long-term business resilience and global competitiveness.

To support our members, ACCA has launched initiatives such as the Sustainability Reporting: Enhancing Transparency and Accountability report, as well as practical learning pathways like the Certificate in Sustainability for Finance (Cert SF) and our CPD course Sustainability Reporting in Practice. These initiatives remain a top priority under my leadership, with a focus on raising awareness, building capability, and ensuring that ACCA members are equipped to lead the transition towards integrated, accountable, and future-focused corporate reporting.

How can accountants play a pivotal role in addressing climate change and economic inequality?

Finance professionals and accountants play a very crucial role in addressing climate change

and economic inequality as they are at the center of capital allocation and strategic decision-making. This makes them connected to all stakeholders,boards, investors, regulators, and communities which allows them to integrate environmental and social risks into financial planning and business strategy. By integrating such sustainability measures into their performance metrics, reporting, and resource management, they help in driving transparency, enabling smarter decisions, and help organizations align with long-term, inclusive growth. ACCA’s Green Finance Skills: The Guide and Climate Finance CPD pathway supports our members to lead this transition with the right tools and expertise.

What strategies will ACCA employ to enhance its qualifications in sustainability and climate tech?

ACCA is strengthening its qualifications to prepare professionals for the future of finance where sustainability and climate action are central. Core modules like Strategic Business Leader (SBL) and Advanced Performance Management (APM) now incorporate key themes around climate risk, ESG reporting, and sustainable strategy. SBL trains individuals to think like boardroom leaders, integrating ethical and sustainable thinking into long-term business planning, while APM focuses on how performance is measured and improved, including the use of data and non-financial metrics to drive sustainable outcomes.

Moreover,, ACCA offers a growing portfolio of specialised learning such as the Certificate in Sustainability for Finance (Cert SF), the Diploma in Sustainability, and a new micro-learning series, Finance and the Net Zero Transition. These programmes go beyond technical skills to equip learners with the tools to understand climate science, manage sustainability-related risks, and deliver meaningful impact. As climate change reshapes global markets, ACCA’s approach ensures that both current and future finance professionals are not just keeping up but are also leading the way.

How does ACCA’s focus on sustainability align with global goals like the SDGs?

ACCA’s commitment to sustainability is deeply rooted in our mission which naturally aligns with the Sustainable Development Goals. Our qualifications, thought leadership, and advocacy efforts support key SDGs such as Quality Education, Gender Equality, Decent Work and Economic Growth, and Climate Action. We believe that finance and accounting professionals play a crucial role in shaping inclusive, sustainable economies. Through initiatives like our ‘SDG Disclosures’ report, and by working closely with UN agencies and global development partners,

we’re not only promoting better reporting but are encouraging action that leads to meaningful progress on the ground. Our vision is to ensure that sustainability is not a standalone concept rather is integrated into the core of business, policy, and professional practice.

What role do you see ACCA playing in promoting sustainable business practices in emerging markets?

In emerging markets and developing countries, ACCA serves as both a catalyst and collaborator. Sustainability is not just a necessity rather it is a powerful opportunity to build more resilient, inclusive economies. ACCA sees a vital role for finance professionals in unlocking this potential, whether through sustainable finance, integrated planning, circular economy models, or greener supply chains. We believe that finance professionals and accountants are uniquely positioned to integrate these practices into business strategy and governance. Through market-specific insights such as ‘Finance Professionals in Africa: Building Resilient Economies’ and ‘Sustainable SMEs in Asia Pacific’, we tailor our guidance to local realities. Our on-ground dialogues, policy roundtables, and academic partnerships help ensure that capability building in these regions is practical, scalable, and aligned with global sustainability ambitions.

How will ACCA support its members in navigating the challenges of energy transition and decarbonisation?

The urgency of energy transition and decarbonisation cannot be overstated.According to the IEA (International Energy Agency), globally the CO2 emissions reached over 37 billion tonnes in 2023 for the energy sector highlighting the need for decisive action. ACCA recognises this challenge and is committed to empowering finance professionals to lead in this transformation. Through a combination of knowledge resources, continuous learning, and policy advocacy, we support our members at every stage. Our ‘Finance and the Energy Transition’ insight series addresses sector-specific risks and opportunities, while CPD courses in carbon accounting, transition finance, and ESG investing provide practical tools. We also work alongside regulators and policy makers to ensure finance professionals are not just adapting but are creating resilient, and impactful decarbonisation strategies within their organisations.

Can you discuss any recent successes or challenges in implementing sustainable practices within ACCA?

One notable success is our measurable progress towards our Net Zero 2030 ambition,

including reductions in business travel and digital carbon footprint. We’ve also embedded sustainability principles in our decision-making at both Board and operational levels. A challenge remains the pace of change, especially harmonising efforts across diverse regions. However, our collaboration with bodies such as IFAC and the UN Global Compact has helped us in reaching consistency.

Women in Leadership

How do you see your leadership role influencing the representation of women in governance positions globally?

I believe that every time a woman steps into a leadership role, she holds the door open for many more to follow. As ACCA’s first South Asian President, I see this not just as a personal milestone rather a shared moment for countless individuals around the world especially in underrepresented regions that leadership doesn’t come with one shape, and it certainly isn’t limited by geography or gender.

At ACCA, we don’t just advocate for inclusion; we institutionalise it. Our global initiatives like Leading Inclusion and the Women’s Leadership & Wellbeing in the Workplace dialogues aren’t just events, they’re part of a system designed to amplify women’s voices and break barriers across industries. I have seen how visibility translates into opportunity. And if my presence in this role helps more women envision themselves at the decision-making table, then that, to me, is leadership with purpose.

What advice would you give to aspiring female leaders in the accountancy profession?

I believe that women should have confidence in their potential, and build the skills to match it. Whether in accountancy, sustainability, finance, or tech, leadership today demands agility, curiosity, and courage. My advice to women is to invest in both competence and confidence and seek out knowledge and expertise, along with remaining adaptable to change.

Women should surround themselves with networks that uplift and challenge them. Mentors, communities, and platforms like ACCA’s leadership CPDs can help develop the emotional intelligence, strategic thinking, and resilience needed to thrive in complex environments. Most importantly, let your values be your compass. When you lead with purpose, others will follow and together, we move closer to a world where leadership truly reflects the talent it holds.

How does ACCA support women in achieving leadership roles within the organisation and beyond?

ACCA ensures that its internal policies reflect fairness and equity by offering flexible working arrangements, parental support, and inclusive talent pathways. Beyond that, we collaborate with partners like the 30% Club and UN Women to drive structural change across industries. ACCA’s Leading Inclusion report, piloted in key regions, provides organisations with actionable insights to measure and improve their gender and inclusion performance. Our regional Women’s Networks offer space for collaboration, visibility, and mentorship which helps women build influence and shape their leadership journeys.

What initiatives has ACCA undertaken to promote gender equality and inclusion in the workplace?

Our inclusion goals are backed by governance and accountability. Internally, we conduct annual diversity audits and publish gender pay gap data. Externally, we support organisations with inclusive recruitment tools, unconscious bias training, and research such as Generation Next, which explores challenges and enablers for diverse talent. Our Diversity and Inclusion Hub is a growing resource for members and employers, featuring tools, webinars, and case studies that promote inclusive culture and leadership.

How do you believe your appointment as the first South Asian and Muslim President of ACCA impacts diversity and inclusion efforts?

It sends a powerful message: diversity in leadership is not only possible but it’s necessary. My presidency reflects the global diversity of our 180+ country footprint and reinforces the value of authenticity in leadership. It also signals to organisations that inclusive governance strengthens decision-making and better reflects the communities we serve. Leadership must mirror the complexity and richness of the world we’re building for.

Intersection of Sustainability and Women in Leadership

How can women in leadership positions contribute to advancing sustainability goals within their organisations?

Women in leadership often bring a systems-thinking approach-connecting environmental, social, and governance priorities. They

tend to lead with collaboration, long-term thinking, and purpose all key elements to sustainable business. ACCA spotlights this in our inclusion and sustainability reports, featuring women who are driving ESG innovation across sectors. Our Sustainability Hub also shares stories and strategies that highlight inclusive leadership as a catalyst for sustainability.

What role do you think women should play in shaping sustainable business strategies and policies?

Women must be at the center of shaping sustainable business strategies not just as participants, but as decision-makers. Whether as policymakers, entrepreneurs, board members, or community leaders, women bring a systems-thinking mindset that naturally links social impact with long-term business resilience. Their lived experiences often lead to more inclusive, equitable, and forward-thinking solutions.

We are seeing women redefine what leadership looks like by integrating sustainability into the core operations of organisations which are helping in driving innovation in clean energy, circular economy models, and responsible governance. As the world moves toward a more sustainable and inclusive future, it is essential to integrate diverse perspectives into strategy and policy-making. Women are already leading in this space, and it is important that they are included in the forums and institutions where critical decisions are shaped.

How does ACCA’s focus on sustainability intersect with its efforts to promote women in leadership roles?

They’re two sides of the same coin—part of a broader vision for a profession that drives public value. A sustainable future demands inclusive leadership. ACCA’s core pillars - integrity, innovation, inclusion are interconnected. This is reflected in our advocacy for regulatory reforms that support both climate disclosures and board diversity. Our qualifications and insights are designed to prepare professionals to lead in this intersection.

Recent Events and ACCA Initiatives

How did PLC 2025 in Pakistan contribute to ACCA’s sustainability goals, and what were some key takeaways?

PLC 2025 brought together business, finance, and policy leaders to chart a sustainable future for Pakistan. One key takeaway was the recognition that climate risk is financial

risk and that finance professionals must be at the forefront of ESG integration. The event also spotlighted a strong appetite for learning, which we’re addressing through regional rollouts of the ProDipSust and Cert SF qualifications, ensuring that local professionals are equipped to lead.

What new initiatives or programmes is ACCA planning to launch in support of sustainability and women’s leadership in the coming year?

We are scaling the reach of the Professional Diploma in Sustainability and Certificate in Sustainability for Finance globally, with new regional content tailored to local markets. On women’s leadership, we are expanding our Women in Finance forums and launching new research into leadership pathways and barriers. These will be available via our Events page and CPD Hub, giving members access to global expertise and support networks.

How will ACCA leverage its global network to amplify the impact of its sustainability and leadership initiatives?

With over 250,000 members and a presence in more than 181 countries, ACCA’s true strength lies in its people who are driving change across sectors and borders. We extend our sustainability and leadership initiatives through collaborative models that bring together members, employers, regulators, and global institutions. Through platforms like our Professional Insights hub, MyACCA, and ACCA Careers, we enable knowledge-sharing and peer learning. Our partnerships with IFAC, ISSB, and WBCSD, along with regional roundtables, webinars, and think tanks, help us localise global strategies to ensure they are impactful and relevant on the ground.

What message do you hope to convey to ACCA members and stakeholders regarding the importance of sustainability and inclusive leadership in the profession?

This is a pivotal moment for our profession. As people of trust, transparency, and long-term value, accountants are called not just to participate but to lead. Leadership today must be inclusive, future-focused, and rooted in purpose. Sustainability and equity are not side agendas rather they are fundamental to how we redefine success in the 21st century. My message to ACCA members and stakeholders is that we have the expertise, and the global reach, and now we must drive the change our world urgently needs. ACCA will continue to support and advocate for leadership every step of the way. n

Three parties now bidding for Rafhan Maize

Some of the country’s leading industrial conglomerates – Nishat, Sapphire, Shirazi, and Ghulam Farooq Group – have thrown their respective hats in the ring

Profit Report

The fight for Ingredion’s 71% holding in Rafhan Maize Products Company Ltd. (RMPL) has turned into a full-blown bidding war. In the space of eight days three very different suitors have filed “public announcements of intention” with the Pakistan Stock Exchange (PSX):

• Nishat Hotels & Properties Ltd. (NHPL), part of billionaire Mian Muhammad Mansha’s Nishat Group, acting through Next Capital as

manager to the offer

• The previously disclosed Cherat Cement–Shirazi Investments consortium that pairs the Ghulam Faruque and Atlas groups;

• Sapphire Fibres Ltd. (SFL), the flagship textile company of Lahore’s Sapphire Group.

Each notice seeks regulatory leave to acquire up to 6.99 million shares, or 75.69 percent of Rafhan’s paid-up capital, meaning any two could, in theory, buy out Ingredion and the public float in one swoop. A formal share-purchase agreement (SPA) and a mandatory tender offer will follow once due diligence

wraps up and the Competition Commission of Pakistan (CCP) issues clearances.

Rafhan’s thinly traded stock closed at Rs8,911 on 13 May 2025 after drifting between Rs8,500 and Rs9,700 over the past month. Using the 28-day volume-weighted average price of Rs8,962 quoted in the Cherat-Atlas filing, a full 75.69 percent block is worth Rs62.7 billion ($223 million). Ingredion’s core holding of 71 percent—essentially the shares it wants to exit—would fetch just over Rs58 billion before negotiations on a control premium.

Rafhan is debt-free and sat on net cash of

roughly Rs8 billion at December 2024, so on an enterprise basis the equity cheques translate into 4.5–4.8x trailing EBITDA—a bargain relative to regional specialty-ingredients peers that change hands at 8–12x.

Founded in Faisalabad in 1953 by CPC International, Rafhan pioneered wet-milling in Pakistan and now grinds 400,000 t of corn a year into industrial starches, liquid glucose, dextrose, dextrins and gluten meals sold to the food, textile, paper and pharma sectors. Although it is strictly a B2B ingredients maker, the Rafhan name conjures images of custard powder, cornflour and jelly mixes—retail brands created by CPC in the 1970s and sold to Unilever in 1998. The industrial company still licenses the trademark, so every tin of Rafhan Custard keeps the goodwill alive.

Rafhan posted Rs69.9 billion revenue and Rs7.5 billion net profit in 2024, keeping its decade-long double-digit margin run alive; Q1-2025 earnings were another Rs1.96 billion. The firm pays Pakistan’s most reliable dividend—1,000 percent a year in cash—and sports a 21 percent gross margin despite agricultural price swings.

Nishat’s bid

The Nishat Group began as a textile mill in 1951 and under chairman Mian Muhammad Mansha morphed into Pakistan’s largest private conglomerate with assets across textiles, banking (MCB Bank), cement (DG Khan), autos (Hyundai-Nishat), power, insurance, and hospitality.

Nishat Hotels & Properties Ltd. owns two five-star hotels in Lahore, the Emporium Mall and real-estate projects in London and Islamabad. Its PSX notice seeks the full 75.69 percent stake in Rafhan. The strategic logic might include three potential reasons.

The first is food-service integration: Nishat’s malls, banquet halls and planned quick-service restaurant franchises buy tonnes of starches and sweeteners. Owning Rafhan secures supply and can spawn new retail SKUs under a brand Pakistan already trusts.

The second is as a diversification of its currency hedge. Nishat Group exporters earn dollars via textiles; Rafhan exports starch syrups to the Middle East, which could be a way to diversify export dollar inflows.

Finally, there is the simple case of deploying balance-sheet firepower: MCB Bank’s dividend stream gives Nishat ample debt capacity — useful if a bidding war inflates the price.

Sapphire Fibres’ bid

Sapphire Fibres Ltd. (PSX: SFL) was set up in 1979 and is today one of Pakistan’s five largest textile exporters as well as an emerging energy investor with over

230 MW of wind and gas-based power assets. In April it closed the purchase of half of the UCH-I and UCH-II gas plants, signalling hunger for cash-generating diversification. Why would it want to buy Rafhan? There is the supply-chain adjacency. Textile sizing uses industrial starch; Sapphire already imports some of those inputs. Backward integration could shave costs at its Sheikhupura and Lahore mills. Then there are the export synergies. The group’s global yarn customer network overlaps with food conglomerates that buy Rafhan’s glucose and maltodextrin in the Gulf and Africa.

Finally, there are compulsions of trying to smooth out the conglomerate cashflows. Textiles’ earnings swing with cotton and power tariffs; Rafhan’s consumer-linked demand and dividend habit smooth the ride.

The Cherat Cement–

Atlas (Shirazi) joint bid

Started in 1981 and expanded to 4.5 million t p.a. capacity by 2019, Cherat is a top-six cement maker with a 7% national market share and a reputation for frugal, energy-efficient kilns in Nowshera. Shirazi Investments (Pvt.) Ltd. is the holding company behind the Atlas Group, whose units include Atlas Honda (motorcycles, 70% share), Atlas Battery, Atlas Insurance and 275 MW of power plants. Founded in 1962 by the late Yusuf H. Shirazi, Atlas prides itself on long-term JVs with Japanese partners and on maintaining an investment-grade balance sheet. Their logic might include diversification away from cement cyclicality and two-stroke electrification pressures. There is also the attraction of dollar revenues: Rafhan’s exports and foreign customer base offer a hedge against rupee volatility — vital for groups that import coal (Cherat) or CKD kits (Atlas Honda). Finally, there is the infrastructure overlap. Cherat’s rail-and-road logistics for clinker exports can back-haul corn and finished ingredients, trimming freight costs.

Price tension

With three credible groups at the table and each notice allowing them to buy the entire 75.69 percent, Ingredion is poised to extract a premium. A 10 percent bump over volume-weighted average price (VWAP) — taking the per-share tag toward Rs9,900 — is plausible if bids escalate, which would lift equity value for the Ingredion block to Rs64–69 billion.

There also appear to be relatively few regulatory hurdles. A review by the Competition Commission of Pakistan (CCP) should be straightforward: none of the bidders makes

starch, and the deal will not lessen competition in any existing market.

There may be some difficulties paying Ingredion, given the fact that the Chicago-headquartered company is likely to want to get paid in US dollars, and the State Bank of Pakistan may make it difficult to remit quite so much in dollars out of the country.

Finally, there are the public-interest optics. Rafhan is Punjab’s largest corn buyer from smallholder farmers; policymakers may favour a buyer promising capex and farmer extension services.

There are also possible wild cards. Middle East-based ingredient giants may yet decide to throw their hats into the ring. And there is the interesting, if somewhat unlikely possibility of Unilever Pakistan, the owner of the Rafhan Custard brand, seeking to reunify the industrial and retail franchises. The consumer-goods giant has not signalled interest.

Why this sale matters

Ingredion’s exit will end the longest continuous foreign manufacturing investment in Pakistan (73 years) and transfer a strategic agri-industrial asset to local owners. Whoever prevails will control a 50-hectare wet-milling complex in Faisalabad, satellite plants at Jaranwala and Kotri, and an R&D centre in Karachi; annual procurement of 500,000 tons of Punjab corn by 2027 under expansion plans, impacting thousands of farmers, and a platform to branch into plant-based proteins, glucose-fructose syrups and biodegradable packaging resins that feed consumer megatrends.

For investors, the tussle signals a maturing of Pakistan’s capital markets: three home-grown conglomerates — textile, cement, diversified — are ready to write $220-plus-million cheques without foreign partners. For policymakers, it is a litmus test of how smoothly large-ticket M&A can clear regulatory hoops in a frontier economy hungry for investment.

With Nishat, Sapphire and the Cherat-Atlas joint venture now circling Rafhan Maize, the Chicago-based seller holds the stronger hand — but only until one bidder blinks. All three see in Pakistan’s starch champion a chance to derisk their existing portfolios, lock in dollar earnings and tap the consumer magic of a 70-year-old pantry brand.

Over the next few weeks data rooms will buzz, bankers will model synergies, and corn farmers from Faisalabad to Jaranwala will watch to see which corporate flag is hoisted over the country’s most prized wet-mill. One thing is certain: rare is the Pakistani deal that aligns food, textiles, cement, motorcycles and hotels under a single asset — making this three-way battle one of the most keenly watched takeovers of 2025. n

Why a Dutch beer veteran owns a Pakistani personal care brand

A long-time executive of Heineken owns the maker of the soap brand Capri from the descendants of Syed Wajid Ali. What could he possibly want with it?

Profit Report

Dubai-based Dutch national Dr Salomon Jacobus “Cobus” van Rooijen has snapped up an 84.84 % voting stake in Karachi-listed ZIL Ltd., the 71-year-old maker of Capri beauty soap and other personal-care staples.

In a notice to the Pakistan Stock Exchange dated 15 May 2025, ZIL disclosed that Van Rooijen’s vehicle TWF Holding LLC-FZ purchased 5,194,514 shares at Rs297.50 apiece on 12 May, valuing the block at Rs1.55 billion ($5.5 million). The seller, intriguingly, is New Future Consumer International General Trading LLC, another single-member UAE company also wholly owned by Van Rooijen.

The internal reshuffle hands the 59-yearold executive direct control of Pakistan’s oldest private soap maker and positions him as board chairman. Yet the match-up of a career beer salesman with a consumer-goods minnow in a country where alcohol is largely prohibited raises more questions than the terse PSX filing answers.

Van Rooijen is no stranger to consumer brands — but almost all of them fizz. According to the résumé published on ZIL’s website, he spent the 2000s running Castle Brewing Namibia and sat on the executive boards of Heineken Russia and Amber Beverage Group Latvia. Earlier still, he was global exports director at SABMiller. He later added stints in Dutch wax-print fashion house Vlisco BV, but his professional centre of gravity has been beer: route-to-market overhauls, acquisition due diligence and emergency turnarounds from Africa to Eastern Europe.

Today he operates from Dubai as managing director of New Future Consumer International (NFCI), hunting for fast-moving-consumer-goods (FMCG) assets and joint ventures. His personal holding outfits (NFCI and now TWF) are the ones funding the ZIL play.

ZIL Ltd: A Hyderabad soap pot that never stopped simmering

ZIL’s origins trace back to 1954, when the Ali family — led by industrial patriarch Syed Wajid Ali — opened a small soap works in Hyderabad. The aim was simple: substitute imported toilet

soaps with a local brand Pakistanis could afford. Over the decades the factory expanded from copper kettles to continuous saponification lines, changed its legal name from Zulfeqar Industries to ZIL Ltd. in 1986, and seeded brands such as Capri, Opal, Hype and Hypro.

The Alis controlled the business for six decades before gradually cashing out. In 2023 they sold 61% of equity — and subsequently more — to UAE-registered NFCI at roughly Rs301 per share. That transaction installed Van Rooijen on the board but left day-to-day operations to company veterans in Karachi and Hyderabad. The company’s brand portfolio today includes Capri gel, beauty-bar and hand-wash lines are the flagship, positioned as mid-tier fragrant soaps for young women; Hype which targets teenagers with bright colour; Hypro, which is a germ-protection entry-price bar. It also owns Opal, a glycerine transparent soap aimed at niche shoppers.

ZIL also runs a contract-manufacturing arm that makes private-label laundry products for local retailers. Public filings show net sales rose 12 % to Rs6.37 billion in 2024, but rising tallow and palm-stearin prices slashed net profit 83 % to Rs42.9 million (EPS Rs7.01). The company declared a 25 % cash dividend anyway, financed largely from working-capital improvements. Margins are thin: gross at 27.7 %, net below 1 %. Leverage is low, but so is free cash flow once the dividend is paid. For Van Rooijen, ZIL is less a cash-cow than a platform needing capital, marketing muscle and — perhaps — an exit route.

Why would a beer executive fancy Pakistani soap?

Pakistan banned alcohol sales to Muslims in April 1977, a prohibition later reinforced under Gen Zia-ul-Haq’s Hudood ordinances. While bootleg liquor and Murree Brewery supply a grey market, legitimate per-capita beer consumption hovers near zero. A lifetime brewing professional, then, gains no obvious synergy from a stake in a soap maker operating in a dry market.

There are, however, several potential reasons why this stake still makes sense. The first is pure portfolio diversification. Van Roo-

ijen’s beer résumé disguises a broader FMCG skill-set. Soap, like beer, rides on brand equity, distribution reach and raw-material arbitrage.

The second is the low-priced entry ticket. Just Rs1.55 billion buys a controlling stake in a listed company with physical assets, nationwide distribution and decades-old trademarks — cheaper than a craft brewery.

There is also the regional export play. Capri already ships small volumes to the Gulf. A Dubai-based owner could use UAE free-zone warehouses to push soaps into Africa, where Van Rooijen’s beer contacts run deep.

The share transfer from NFCI to TWF shows he is shuffling assets among his own vehicles, possibly to prepare ZIL for debt funding or a future strategic sale.

The founding Alis retain a small public float but no board seat. Family scions like Syed Asad Ali now direct philanthropic and textile interests. The sale marks another classic Pakistani tale: pioneering industrialists hand off to foreign investors when succession or capital limitations bite.v

The PSX notice reveals the buyer and seller share a beneficial owner; in effect Van Rooijen bought the shares from himself. Why? TWF-FZ may offer looser disclosure regimes or tax advantages versus NFCI. A new vehicle can pledge shares for bank financing or invite minority partners later. Direct shareholding lets him consolidate voting power without having to filter decisions through NFCI’s governance.

Regardless, the deal triggers takeover-code disclosures but not a mandatory tender offer, because no change of control occurred in substance.

Can ZIL grow under Dutch stewardship?

The Hyderabad plant runs legacy batch kettles alongside one modern continuous line; converting fully to energy-efficient processes could cost Rs1 billion. Given thin margins, internal cash generation is unlikely to fund that without new equity.

Capri’s share in beauty bars has slid to single digits as Unilever’s Lux and P&G’s Safeguard flood TV screens. Digital-first campaigns and line extensions into shower gels might arrest the slide, but require marketing budgets far above current levels.

SAFTA preferences allow zero-duty soap

exports to Sri Lanka and Bangladesh, markets Van Rooijen’s African beer networks do not cover. Whether the new owner can assemble a trade team and secure shelf space abroad remains to be seen. ZIL’s new chairman built his reputation selling lager from Namibia to Novosibirsk, only to arrive in a country where Muslims — 96 % of the population — face legal penalties for drinking. The contrast invites irony.

Beer marketing thrives on pub culture; Pakistani soap ads lean on family purity and modesty. The government that blocks Heineken bottles at customs welcomes a Heineken alumnus as majority owner of a local FMCG firm. Yet the paradox may be overstated. Multinationals from Diageo to AB InBev park billions

in soft-drink and snack subsidiaries worldwide. Commerce, after all, often trumps categories.

What next?

Van Rooijen already chairs the board; expect fresh appointments of consumer-marketing specialists and supply-chain veterans. For now, minority holders can only watch. The PSX symbol ZIL has risen 25 % since the notice, flirting with its highest level in a decade. Whether that is justified will depend on how quickly the Dutchman turns suds into serious cash.

The ex-Heineken troubleshooter into the

heart of Pakistan’s personal-care business — an arena where local consumers buy four billion soap bars a year but multinationals wield the advertising clout. The acquisition price is small change by global standards, yet the strategic puzzle is large: can a man steeped in lager rekindle the sparkle of Capri beauty soap?

Sceptics cite cultural dissonance and razor-thin margins; optimists see a seasoned FMCG tactician entering at a bargain valuation. Either way, the transaction underscores two truths about Pakistan’s consumer market: legacy family brands are up for grabs, and even in a country where beer is verboten, the man who once sold it can still make a bold bet — this time, on bubbles that are perfectly halal. n

Ali Asghar Textile to set up solar power plant

Profit Report

Ali Asghar Textile Mills Ltd. (AATM) is about to make an uncharacteristically bright splash on Pakistan’s renewable-energy map. In a material-information notice uploaded to the Pakistan Stock Exchange on 16 May 2025, the Karachi-based logistics-and-warehousing company said its board has authorised construction of a 1,250-kilowatt (1.25 MW) grid-tied solar-photovoltaic plant that will sit on the rooftop and vacant setbacks of its Korangi Industrial Area campus. T he array—five times larger than the 250 kW pilot AATM switched on two years ago— will be built in one phase, financed largely from internal cash and a concessionary “green-banking” loan the company has negotiated with JS Bank. First kWh are targeted for the fourth quarter of 2026.

On a national grid where generating units are usually measured in hundreds of megawatts, 1.25 MW may sound modest. Yet for an SME with a paid-up capital of barely ₨22 million and revenue of ₨66 million from its core logistics business last year, the venture is almost audacious. To grasp why Ali Asghar Textile is betting so heavily on rooftop solar, one must revisit its transformation story. Founded in 1969 as a medium-scale ring-spinning mill, the company prospered through the 1980s on exports of coarse cotton yarn before the quota-free era ushered in ferocious competition from larger composite groups.

In 2011 the board took the rare decision to exit spinning altogether and repurpose the 20acre Korangi site into a bonded warehousing and third-party logistics hub. A change in the company’s memorandum re-categorised its principal

line of business; spinning frames were scrapped, and warehousing sheds rose in their place.

That pivot paid off: AATM’s other income—largely long-term rentals—hit Rs 226 million in FY-2024, dwarfing its operating revenue and propelling after-tax profit to Rs 100 million. Even so, a volatile grid tariff and frequent voltage sags ate into margins and alarmed prospective tenants like pharmaceutical major Getz Pharma, which demanded power-quality guarantees before signing a seven-year lease.

The firm’s first flirtation with photovoltaics came in late-2023 when it installed a 200 kW pilot array. According to slides from the 2024 corporate-briefing session, that system generated 520 MWh in its first 14 months and avoided 461 tonnes of CO₨ equivalent.

Building on that success, the board drafted a staged expansion plan: jump to 250 kW in early-2024, then break the megawatt barrier once government permits cleared. Those licences finally arrived in Q1-2025, prompting the leap to 1.25 MW rather than the originally mooted 1 MW. The incremental 250 kW allows AATM to cover 100 percent of its peak daytime load, export a small surplus on Sundays, and future-proof the site against fully automated, refrigeration-heavy warehousing now being designed for biomedical clients.

Beyond cost arithmetic, the plant will slash AATM’s scope-2 emissions by about 1,450 tonnes of CO₨ a year, reinforcing its pitch to multinational tenants for whom decarbonised logistics capacity is becoming non-negotiable. The company already displays real-time solar dashboards in its client portal and aims to issue third-party-verified renewable-energy certificates once generation exceeds on-site demand. That green veneer dovetails with marketing efforts to attract

IT firms to the two floors of shared office space in AATM’s new headquarters block.

AATM’s foray comes as corporate Pakistan, spooked by the highest power tariffs in South Asia and persistent grid instability, scrambles for embedded generation. Textile giants such as Yunus-Textile and Interloop now run 10–20 MW captive solar parks; food and personal-care firms are chasing similar schemes. Yet until now smaller listed companies rarely dared anything beyond a few hundred kilowatts. If Ali Asghar Textile succeeds, it could validate megawatt-scale rooftop solar as a viable hedge even for mid-cap enterprises.

The government’s net-metering regime, introduced in 2017, allows surplus solar power to be sold back to Disco networks at the National Average Power Purchase Price, adjusted annually. That framework underpins AATM’s pay-back calculus but is under review as the Ministry of Energy grapples with ballooning capacity charges. The company concedes that any sharp downward revision in the net-metering tariff could extend project pay-back by up to 18 months. Similarly, the interim ban on net-metering system sizes above 5 MW, imposed earlier this year, is a reminder that policy can both spur and stall corporate solar adoption.

Intriguingly, the board resolution hints at a “Phase II ground-mounted extension” on leased land outside Karachi should the 1.25 MW unit perform as modelled. That would push total capacity toward 3 MW and open the door to selling clean power to third-party off-takers under Pakistan’s new wheeling regulations. Such ambition would transform a once-humble spinning mill into a boutique independent power producer, albeit on the fringes of the energy market. n

Yes, PIA turned a profit. No, it’s not a turnaround.

The national carrier seems to have turned profitable, surprising everyone. Why it should be taken with a pinch of salt

By Zain Naeem

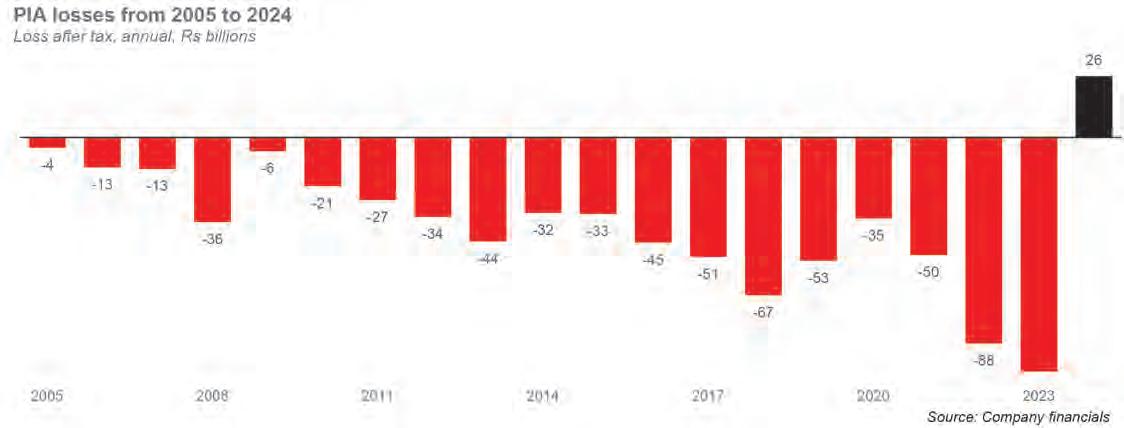

The recent results released by Pakistan International Airline (PIA) and the jubilation around its profitability seems to have taken everyone by surprise. The profits announced for the year ended December 2024 show that operating profits registered around Rs9.4 billion while net profit was recorded at Rs26.2 billion. The earning per share of Rs5.01 per share seems to be a far cry from just a year ago when the company had a loss of Rs104 billion at the end of 2023 coming to around a loss of Rs20 per share.

The sudden turnaround in the fortunes can be attributed to certain efficiencies being put into place, however, a closer look at the consolidated accounts show that the company is still in need of further steps before it can be labelled as becoming profitable.

The recent history of the company dampens some of the optimism that surrounds the release of the accounts. The loss seen in 2023 was not a one time blip as the airline had been suffering losses for 21 years. The last time PIA was able to record a profit was back in 2004 when it recorded profit after tax of Rs2.3 billion. Since then, there has been a consistent slope downwards as losses of more than Rs600 billion were recorded from 2005 to 2024.The

recent results show signs of a turnaround but these are just signs and the complete turnaround is yet to be seen.

So why all the confetti and commotion?

Reason to celebrate

The celebration around the results is a PR move that is being used by the ministers to amplify what they see as the revival of the company. The PR push is well warranted as there is a drive to sell the loss making State Owned Enterprise to the highest bidder. Just last year, the ruling government was left with egg on their face when they could not get the desired bid from

the interested parties and had to go back to the drawing board to make things happen. With the profits being announced, it has given an opening to the ministers to tout the improvement in order to get a better price this time.

Having said that, there are metrics which point in the positive direction. Based on the latest available consolidated financial information, it can be seen that the company has been able to see improvement in its performance. These improvements can be attributed to workforce being laid off, cutting of loss making routes and carrying out efficiency based measures.

From January to September 2023, the company earned revenues of Rs186 billion which were seen to be around Rs183 billion for the same period this year. Through cost cutting measures, the gross profit almost doubled from Rs21 billion last year to Rs39 billion in the same period this year.

In terms of the operating profit, the company stood at Rs10 billion last year improving to Rs18 billion in 2024. The biggest expenses that were recorded last year were exchange losses of Rs26 billion and finance cost of Rs58 billion. Due to these costs, net loss fell to Rs76 billion for the year. In the current year, the finance costs decreased as restructuring was carried out, decreasing these expenses to only Rs21 billion. Exchange losses also decreased to Rs2 billion which meant net loss for the nine months ended September 2024 was Rs8 billion.

There were active efforts that were carried out by the management to negotiate better terms with the banks which reduced its financial burden while efficient uses of resources also meant that the airline was able to enjoy better profitability in the recent year. Some credit needs to be given to the management in carrying out these steps which did help the company overall to be able to cut down its losses by 90% and see better performance in the latest year. A better picture will emerge

once the annual results are announced which will show the consolidated performance of the airline as a whole.

But now the question arises that if the consolidated earnings are showing operating profit of Rs18 billion and a net loss of Rs7.5 billion at September end, where are the figures that are being quoted in the media?

The mechanics of the restructuring

Well for that we need to go back to the time when the restructuring was being carried out. The government was well aware of the fact that PIA was suffering from losses on a consistent basis. As the losses began to pile up, the government stepped in at different stages to bail out the airline company and kept lending it additional liabilities to make sure the company could stay afloat. The losses kept on increasing as the company had internal inefficiencies which were not being addressed. Hiring additional employees, giving out free benefits to politicians and bureaucracy, lack of quality service and use of leased assets meant that the costs kept increasing while revenues were restricted.

The killer blow came when aviation authorities in Europe and UK decided to ban flights being flown by PIA which meant revenues streams started to become curtailed. Due to the airline suffering losses, the equity of the company had become negative and bailouts had to be given by the government to make sure the airline could stay afloat. With privatization becoming imminent, the solution was quite simple.

By June of 2023, the situation had deteriorated to such an extent that the company had assets of Rs160 billion while its losses alone had racked up to Rs712 billion. This meant

that liabilities had to be used in order to fill this gap. In June of 2023, the total liabilities were Rs809 billion. The government realized that this situation was not sustainable and something had to give.

The government would cut out the best parts of the airline and leave the cancerous losses and debts parked on the books of another. The scalpel was taken out which sliced the corporation into two parts. The goal was to create a company that could be promoted to potential buyers. Such a sale would not only stop the bailout packages from being handed out on an yearly basis but will actually lead to generation of sales revenue which could boost the fiscal resources.

The privatization drive that the government is going through was imposed on it by the International Monetary Fund (IMF) which asked the government to restructure loss bearing state owned enterprises in an attempt to raise funds from these sales. The mandate of these sales was to limit the leakage of funds from the government in these financial blackholes and generate much needed revenues which could be used for other purposes.

This led to the creation of two new companies. One would hold all the core assets linked to the aviation business while the other would house most of the strategic investments carried out by PIA over the years. This would be the holding company which will hold these assets. The holding company was also burdened with the debt and the accrued markup that was due on PIA previously.

The non-core assets which were handed over to the holding company were made up of many investments that had been carried out. In addition to that, many of the immovable properties characterised by the sales office of PIA and land was transferred. In regards to the non-core liabilities, many of the loans taken from financial institutions and govern-

ment were given to the holding company. The retirement benefits and accrued markup of the loans taken was completely transferred as the burden was shifted.

The restructuring goes off balance