The great digital divide in Pakistan’s connectivity

18 Bank Alfalah signs off on sale of Alfalah Securities to Optimus Capital for Rs 313 million

20 Breaking barriers: Once paralysed, Dr Saira completes $6 million raise for health tech company MedIQ

21 Ingredion considering offers for a sale of Rafhan Maize majority stake

The Chashma-Jhelum Link Canal Question Syed Faisal

26 Pak Suzuki’s profits boomed in 2024, right after its buyback. Minority shareholders won’t be happy

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

By Farooq Tirmizi

If you compare Karachi and Lahore as two cities, Karachi remains the larger, and more economically significant of Pakistan’s two largest cities. But compare them as the core of their respective economic regions within the country, and it is not even close: the economic region of which Lahore is the center is, by far, the larger of the two, and is one of the densest mega regions in the world.

Because while Karachi is a bright lone star on the coast of the Arabian Sea, Lahore is the beating heart of the Lahore Megalopolis, the largest city in a belt that runs from Peshawar through GT Road down to Lahore and then on to Multan, with a small off-shoot in Faisalabad.

In this article, we at Profit are putting forward a new proposition: that the Lahore megalopolis should be added to the global list of mega regions, and that its existence represents both a testimonial to the modest successes of some economic policies of the government of decades past and its still nascent status represents what work must be done to make Pakistan an economically prosperous country.

We would also like to state at the outset what this does not mean: it does not mean that the key to Pakistan’s economic future is to keep spending the bulk of the country’s infrastructure budget developing Lahore, as has been the Sharif Brothers’ modus operandi.

What it does mean, however, is that Pakistan’s economic geography is changing and that some of those changes point to opportunities for how to continue the country’s growth trajec-

tory and perhaps even accelerate it. Because while encouraging exports must remain a focus of the government’s economic policy, it should probably be aware of this large and growing domestic market that could also serve as an engine of economic progress.

In this story, we will begin by defining a mega region, defining the limits of the Lahore megalopolis and why we consider it to be one, laying out measures of the extent to which the Lahore megalopolis is economically integrated and the ways in which it has not integrated, and the implications of these changes for the Pakistani economy.

What is a megalopolis (or a mega region)?

Defining what constitutes a mega region is somewhat difficult to do with any level of consistency, but it is generally recognized as a series of contiguous metropolitan areas where one blends through to the next with little rural or empty space between them. They tend to have broadly integrated markets, represented by movement of people, and the expansion of businesses from one part of the megalopolis to the other. Typically, they tend to have good transportation links.

One of the easiest definitions – though hardly a scientific one – of a megalopolis is to look at the world at night, when the lights are on: the megalopolis’ look like one integrated web of lights, distinct from other such webs of light. Crude, but perhaps the most consistent way of defining what is a megalopolis and what is not.

The earliest known use of the term was in the late 1950s by the French political scientist Jean Gottman, who first put forward a theory to explain the linkages between what he saw as the mega region on the northeast coast of the United States and stretches from Boston in the north to Washington DC in the south. The region’s core city is New York, which is almost halfway between those other two cities. This region is connected by the only high speed railway link in the United States, known as the Acela.

The New York megalopolis, more commonly known as the Northeastern mega region, is the richest such region in the world, as measured by total economic output and just about any measure of wealth. It is not, of course, the only such region, and by population, it is not the largest.

That distinction belongs to the Yangtze River Delta region in China, the core city of which is Shanghai. It stretches over an area of 350,000 square kilometers (about half the size of Pakistan) and contains as many people as all of Pakistan: about 240 million.

Indeed, four of the top five mega regions

in the world by population are all in China, centered around the cities of Shanghai, Beijing, Wuhan, and Chengdu. The only non-Chinese one is what is called the Blue Banana in Europe: a region that includes the industrial belt stretching from Northern Italy, through France, Germany, Belgium, the Netherlands, and into the industrial heartland of England.

All of these regions are enormously significant economically, with strong transportation links, fluid labour markets, integrated business networks and supply chains, and often some sort of coordination between their regional governments.

What these – and most – mega regions have in common is a shared history and geography, including a longstanding history of economic ties. The Yangze River Delta has long been the most important economic region of China. The German part of the Blue Banana was so important that France decided to occupy it after World War I to punish Germany for starting the war. And the Blue Banana forms the core of what later became the European Union.

If our definition of the Lahore megalopolis becomes widely adopted, it would be the sixth largest mega region in the world by population, though of course, far from being anywhere near even the top 50 in terms of economic significance.

The Lahore megalopolis

Look at an image of Pakistan from space at night, and the Lahore megalopolis becomes unmistakable: you can see the bright concentration around Lahore, and then bright lines stretching up towards Rawalpindi and Islamabad onto Peshawar and down towards Multan.

Place those lights on a map and you get the districts of Peshawar and Nowshera in Khyber-Pakhtunkwa, the Islamabad Capital Territory, and then the districts of Attock, Rawalpindi, Jhelum, Chakwal, Mandi Bahauddin, Gujrat, Hafizabad, Gujranwala, Sialkot, Narowal, Sheikhupura, Lahore, Nankana Sahib, Faisalabad, Kasure, Okara, Sahiwal, Khanewal, and Multan in Punjab.

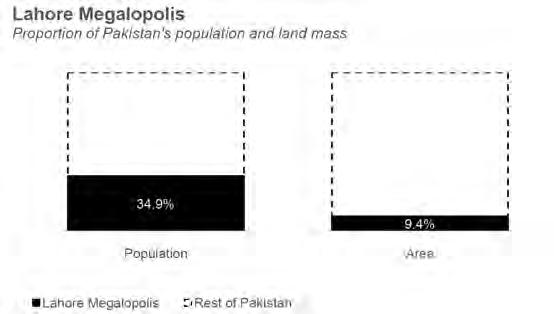

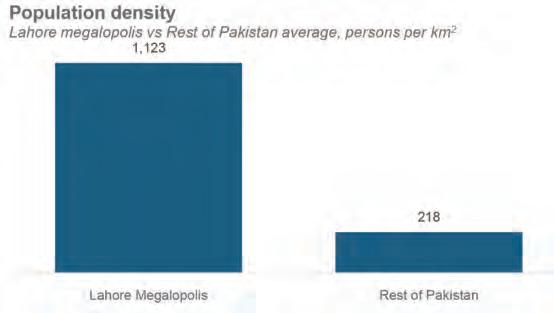

All told, this is 21 districts, and the ICT (which can be considered a district for the purpose of this analysis) across the country. As of the 2023 census, this region has a population of 84.1 million people, which is about 35% of the population of Pakistan.

This is also a very densely populated region of the country. This 35% of the country’s population lives on just 9.4% of the land mass of the country. The population density of this region comes out to about 1,123 people per square kilometre. It is also a very well-connected part of the country. Excluding the two districts in Khyber-Pakhtunkhwa, and nearly

everyone who lives in this region is within a 4-hour driving distance to Lahore.

And the integrated nature of this region itself has a long history. Look closely and you see that nearly the entirety of this megalopolis is basically the Pakistan portion of the ancient Grand Trunk Road, which runs from Kabul in Afghanistan to Teknaf in Bangladesh.

The history of this road run deep: it was built by Chandragupta Maurya in the third century BC over what legend has it was an even older road. Sher Shah Suri expanded and rerouted it to its current route, and then the British began paving it in the 1830s, giving it its current shape. Traveling along GT Road is one of the oldest things that South Asians could do that we still do.

The distance from the Wagah to the Khyber Pass is approximately 613 kilometers. The actual road itself is maintained by the National Highway Authority as the N-5 highway. Drive on the N-5 from Peshawar to Multan and you would essentially have covered the entire length of the Lahore megalopolis.

The centrality of the old N-5 highway to the connectivity of this region might make one think that the motorways have nothing to do with why this region is becoming a megalopolis, but the fact of the matter is that the terminal ends of this megalopolis are well connected precisely because of the motorway. The shrinking of distances between the ends through the M-1, M-2, and M-4 motorways is what allowed the density along the N-5 highway to be more feasible.

How integrated is the Lahore megalopolis

There are four dimensions on which a megalopolis can be said to be integrated.

1. Geographic contiguity: how close together are the constituent metropolitan areas and are they well-linked by transportation links?

2. Labour market mobility: How closely-knit is the labour market? Do people frequently move from one part of the megalopolis to another?

3. Integrated supply chains: The business-to-business suppliers of a megalopolis have a tendency to serve the whole, or a large proportion of the region.

4. Integrated consumer markets: If people move around frequently between different parts of the megalopolis, and the supply chains are integrated, you tend to start seeing consumer-facing businesses expand throughout a mega region.

The road linkages between this region are well established, as we discussed above, and the picture from space shows clear geographic contiguity.

Umair Javed, a professor of sociology and politics at the Lahore University of Management Sciences, believes that the region has a ways to go before it has climbed that full ladder of integration. “If you look at the space photographs, it is clearly one region. If you look at the migration data in the census, it is clear that people are moving between the region and its labour market is integrating. But supply chains, and the extent to which you see businesses from one part of the region move to another part is still something we do not see much of,” he said in an interview with Profit.

“Take one example. You do not see many restaurants from one part of the region open up locations in other parts. The multinationals and consumer goods companies might see it as a single region, but the local businesses are not yet moving across the region,” he added.

The migration data, however, does indicate that the labour market is becoming more integrated, with Lahore in particular serving as the center of gravity that is sucking in people from surrounding districts. As of 2023, about 1.9 million of the 13 million people living in Lahore were not born there. That number is not far behind Karachi’s 2.3 million domestic migrants.

But while Karachi’s migration comes mainly from parts of the country further away from the city itself, the overwhelming majority of the migration into Lahore has been from people from within Punjab, according to data from the 2023 census. And Lahore is hardly alone in the megalopolis. Rawalpindi, Islamabad, and Sheikhupura all attracted more than a sixth of the populations from other districts. Overall, 8.7% of this region’s population was not born in the district they currently live in.

Transit is the one area where there is clearly some local agglomeration effect. There are bus lines that primarily service this region, such as the Daewoo bus lines. The highways blanketing this region have oil retailers setting up petrol pumps at rest stops, which in turn has led to the rise of major new oil marketing companies in Pakistan such as Hascol, Attock Petroleum, Bakri Trading, etc.

And Gourmet Bakery is a chain that now

exists in virtually every major city within the megalopolis (as well as some cities outside of it.)

But besides these more visible factors, the most visible effects are at the level of business-to-business supply chains. Take, for instance, the fact that chicken is much cheaper in this part of the country than most other parts of the country. Sure, you might mutter something about Hamza Shahbaz, but that is not a serious explanation.

The serious explanation is the fact that this region now has the supply of everything you need to set up a high efficiency modern chicken farm that can produce chicken for consumption at a much lower cost than before mechanized chicken farming came to the region. The road network connecting the whole region means that distributors in every district in the megalopolis have access to every component (feed, immunizations, modern coops, etc.) even if they are not produced in the district itself.

Do you, dear resident of the megalopolis, know the names of any of these B2B manufacturers and distributors? No. But your chicken prices reflect the fact that they exist. (You may complain about inflation overall, and the macroeconomic situation certainly did not exempt you from the price increases, but they are lower than other parts of the country, which is what living in a megalopolis gives you.)

Is this evidence of serious agglomeration effects? Not yet, but the beginnings of agglomeration effects would look exactly like what we are seeing happening in this region right now. It would just be happening in many more industries.

Why the megalopolis matters for Pakistan

No country has gone from being a primarily agrarian economy to an industrialized economy without the agglomeration effects of a lot of small businesses being located close to each other, sharing trade secrets and techniques for how to do things better. Simply put, the death

of distance has done nothing to ameliorate the advantage of being physically proximate to people in the same business as you that you can learn from.

What a megalopolis like the one centered around Lahore can do is help create a completely domestic vector for productivity gains in the economy that will, over time, improve the country’s economic competitiveness. It is also likely to have capital formation effects, in the following way. Think about why Gourmet was able to expand to hundreds of outlets across Punjab. The highways mean that the cost of transporting its raw materials is cheaper, and the wholesale markets more accessible, meaning it can earn higher gross margins on its products. Those higher gross margins generate more free cash flow to allow the company to invest in store expansion, which results in yet more free cash flow.

Over time, that expanded free cash flow increases to a point where the company can start to consider products and service lines considerably more ambitious than simply one more outlet for its bakery. This can go into vanity projects like a television news channel (they actually did that), or it can go towards more productive investments such as manufacturing of its bakery products (they also do that).

Would it be better if a small business owner with two successful shops in Lahore could go to a bank and get a loan to open his third outlet in Sheikhupura? Yes, but we do not live in that country yet. In the absence of more formal access to capital, we are left with the slower, but still non-zero effects of lower costs reducing the barriers to expansion, which in turn increases the capital available in the economy over time.

More to the point, having a concentrated base of economic activity is not something available to every economy in the world. It is an advantage that Pakistan should seek to utilize in its growth strategy. And its emergence represents part of the many tectonic shifts taking place in Pakistan’s broader political economy. n

The great digital divide in Pakistan’s connectivity

Is a lopsided development in Pakistan’s digital infrastructure constraining Pakistan’s digital potential?

By Hamza Aurangzeb

Over the past few years, Pakistan has undergone a spectacular digital transformation that has altered the country’s economy significantly. The technological advancements have provided impetus to the digital economy to flourish at an exceptional rate, where IT services exports are expand-

ing at a brisk pace, digital transactions are multiplying daily, and an increasing number of digital government initiatives are being launched. This unprecedented growth has instigated a remarkable surge in demand for connectivity and digital infrastructure in Pakistan.

Although Pakistan’s digital economy has made considerable progress, it is highly concentrated in metropolises due to the absence of equitable digital infrastructure and connectivity across the country. The standards of digital connectivity vary with each district in the country due to flimsy connections to the national internet backbone, while broadband connections, whether mobile or fixed, remain beyond the reach of millions due to high prices. Moreover, low digital literacy across numerous regions and segments of society along with high cost of devices have stymied digital adoption within the country, undermining Pakistan’s techno-

logical competitiveness at the global level. Profit presents the story of the stark digital divide prevalent in the connectivity landscape of Pakistan, exploring the core underlying issues and proposing relevant recommendations to resolve them.

Significance of digital connectivity for inclusive economic growth

Digital connectivity catalyzes promotion of inclusive growth in emerging markets like Pakistan, empowering a diverse range of communities that have remained underdeveloped historically. It is an agency which has the potential to augment productivity, foster innovation, and expand market participation across a multitude of sectors. Moreover, expanding digital connectivity offers a pathway to accelerate development and diminish poverty for countries like Pakistan that are characterized by sluggish growth, high inequality, and limited access to quality public services.

A robust digital access boosts economic potential across all segments of the economy, where it opens new markets, enhances efficiency, and supports participation in global digital value chains for businesses, especially in underserved regions. It also shortens gaps in employment, education, healthcare, and financial access for underdeveloped and marginalized communities. The positive impact of digital connectivity is bolstered by studies based on 14 low-middle income countries, which showcase that a 10-percentage point increase in 3G coverage increases employment rates by 2.1 percentage points. Evidence suggests that the introduction of fast speed internet in Africa increased the probability of employment for an individual by up to 13.2%, improved total employment by firm by up to 22%, and enhanced firm exports by almost four times. Furthermore, enhancing digital connectivity has proven to be effective for enhancing female’s access to better employment, particularly in countries like Pakistan which have a low female labor force participation.

Parvaiz Iftikhar, a senior ICT consultant stated that, “In today’s digital age, every sector of the economy is dependent on robust connectivity to thrive. It drives productivity, enables automation, expands market access, and generates new employment opportunities—especially through online platforms. Hence, Pakistan must expedite its efforts to strengthen digital infrastructure and bridge connectivity gaps to remain competitive in the region.”

Although Pakistan’s ICT sector has

been booming, it only contributed 3% to Pakistan’s overall GDP during FY24 and provided minimal support to the country’s economic growth during the past decade. Its digital exports make up about 10% of the total but account for less than 0.1% of world digital exports. Thus, scaling digital access is essential for dramatically increasing exports and employment, especially among youth and women.

The blockade of low digital connectivity in Pakistan

Although the wave of digital transformation is gaining increasing traction across the globe, Pakistan continues to face serious challenges in ensuring equitable, high-quality digital connectivity across the country due to a variety of impediments, including inadequate infrastructure gaps, affordability issues, and deeply entrenched social inequalities. All of these obstacles have coalesced into a significant threat to the country’s ambitions for inclusive digital growth and economic modernization.

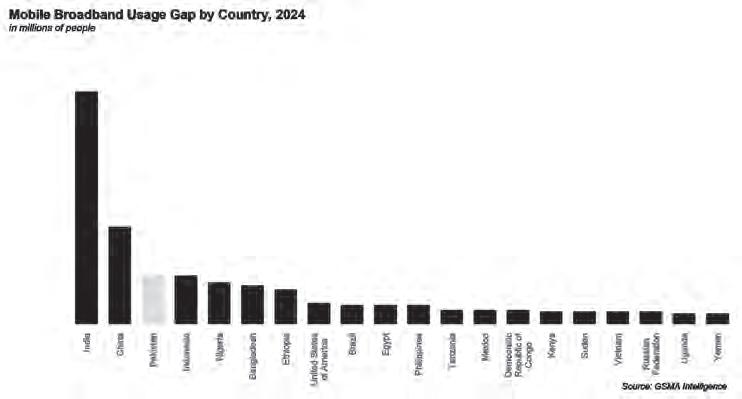

Pakistan lags behind its peers when it comes to internet penetration. In fact, Pakistan has the third-largest broadband usage gap in the world, where a staggering 140 million people live within areas that have mobile broadband coverage areas but are not connected to it, which signifies a major disconnect between availability and adoption, rooted in broader structural issues such as affordability, digital literacy, and social norms.

Moreover, connectivity gaps are compounded by patchy mobile broadband coverage. Around 17% of Pakistan’s population still lives outside of mobile broadband range. Pakistan’s 3G and 4G coverage rates stand

at 74.9% and 83.6%, respectively, which is below the South Asian regional average of 88.1% and 90.9%, respectively. Although 4G has become the benchmark across the nation, one-third of the population still remains stuck on archaic 2G networks, while 5G remains unavailable in the country due to low fiber penetration and insufficient tower density. However, multiple countries like India, Maldives, Bhutan, and Sri Lanka have already rolled out the technology on a massive scale.

The Pakistan Social and Living Standards Measurement Survey 2019–20 indicates a conspicuous imbalance in digital device possession and internet connectivity between urban and rural populations, where internet access in rural households stands at 23%, which is less than half of urban ones that hovers around 48%. The Global System for Mobile Communications Association (GSMA) surveys reveal that around 80% of the urban population owns a mobile phone and 53% uses mobile internet in contrast to the rural population, where only 64% of the population owns a phone and about 38% of the people engage with the mobile internet.

Iftikhar added, “Pakistan has one of the largest broadband usage gaps globally, as accessing broadband—whether fixed or mobile—requires either a router or a smartphone, both of which remain unaffordable for many due to high import duties and taxes (eg: 18% Sales Tax on Smartphones). Additionally, limited digital literacy and a lack of awareness about the benefits of broadband further hinder widespread adoption, especially in underserved communities.”

Nevertheless, this digital divide is not restricted to urban and rural populations but also prevalent among genders. Multiple reports like the Global Gender Gap Report 2024, the Mobile Connectivity Index 2023, and the Inclusive Internet Index, all have placed Pakistan among countries

with the lowest gender parity and digital inclusion. The reports identified several key gaps, including female education, mobile ownership, and Internet usage, which exacerbate the digital divide and obstruct equitable access to technology for women. As per PTA Annual Report 2024, there is a digital gender gap of 38% in terms of both mobile ownership and mobile internet adoption in the country.

The highly concentrated broadband infrastructure

Pakistan’s digital connectivity challenges not only stem from limited technological access at the user level but are also deeply rooted in upstream infrastructure bottlenecks that undermine the quality, coverage, and resilience of internet services nationwide. The country has a fragile and highly concentrated national broadband backbone, which fails to adequately serve several large parts of the country.

The bulk of Pakistan’s backbone infrastructure is concentrated along a single corridor, the north-south route following the Indus River—connecting major cities while leaving peripheral regions, particularly in the west, underserved. However, there are a variety of reasons that have led to the development of broadband infrastructure in the said

manner. Firstly, around 80% of Pakistan’s population lives in the Indus Basin and about the same portion of Pakistan’s GDP is also concentrated along the provinces of Punjab and Sindh, which are adjacent to the Indus river. Hence, this concentration of population and economic activity makes establishing broadband infrastructure in the region a commercially viable endeavor for internet service providers, unlike the western provinces of Khyber Pakhtunkhwa and Balochistan. However, it’s worth noting that security concerns and difficult terrain also contribute to delays in the expansion of broadband infrastructure in the western provinces.

Source: GSMA

Iftikhar explained that a large share of Pakistan’s population resides along the Indus River, a region well-connected by transport networks, making it commercially attractive for digital service providers. As a result, broadband infrastructure is heavily concentrated in the north-south corridor. However, it is essential to expand infrastructure along alternative routes, particularly in underserved regions in the west, while also investing in digital literacy and awareness to ensure equitable digital access and drive meaningful demand.

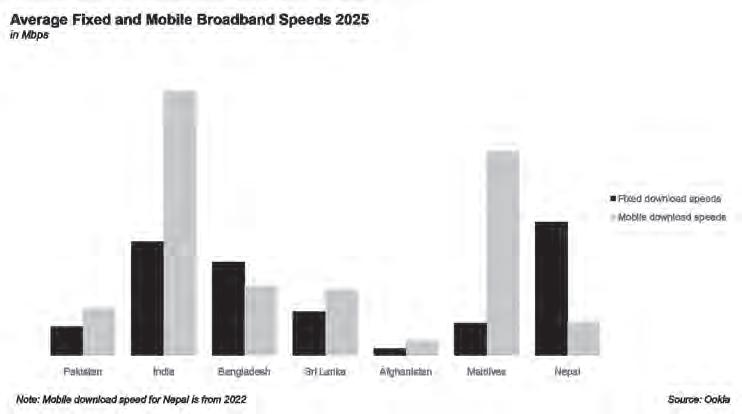

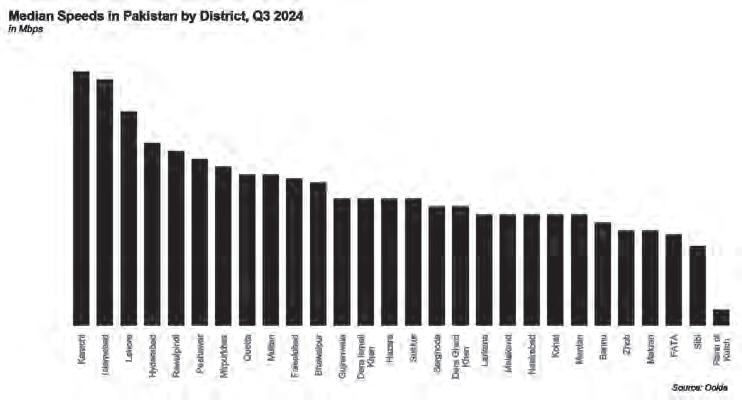

Furthermore, the deployment of fiber optic infrastructure has been hampered by bureaucratic hurdles significantly, where internet service providers have to acquire multiple right-of-way (RoW) permissions and pay hefty fees to multiple government bodies These regulatory challenges discourage private investment, where Internet Service Providers (ISPs) and mobile network operators (MNOs) refrain from building independent nationwide networks. Consequently, Pakistan Telecommunications Company Limited (PTCL) remains the sole operator with a comprehensive national network, creating a monopoly on which ISPs and MNOs depend. However, this centralization means that any disruption in the north-south route along the Indus River, such as the flood-related backbone cuts in August 2022, can paralyze internet access across the country. These upstream constraints have direct downstream effects on the quality and affordability of internet services in the country. Pakistan ranks third last in South Asia for both fixed and mobile broadband speeds with average speeds of 16 Mbps for fixed and 20 Mbps for mobile, which is barely sufficient for modern digital applications. Not to mention that average speeds in metropolises are twice the average speeds accorded in median districts—8 Mbps.

On top of that, broadband costs also

remain disproportionately high, where fixed broadband prices gobble up over 11% of average Gross Monthly Income (GNI) per capita, far above the international affordability benchmark of 2%, while basic mobile broadband packages could be bought for 1.8% average Gross Monthly Income (GNI) per capita. Although these plans are cheaper, they remain inaccessible to many in low-income and rural areas, who receive poor internet signals and face frequent disruption due to lack of fibre connectivity to the internet backbone.

While discussing relatively lower internet speeds in Pakistan, Iftikhar highlighted that only 14% of Pakistan’s cell towers are connected via fiber optic cables, compared to 30% in India, 27% in Bangladesh and 45% in Malaysia. Over 85% of Pakistan’s towers rely on microwave links, which offer significantly lower data capacity than fiber. Furthermore, Pakistan trails behind regional peers in terms of available spectrum, with allocations at nearly half the regional average—largely due to prohibitively high spectrum prices.

Furthermore, Pakistan is significantly behind in Fiber-to-the-Home (FTTH) deployment. At the current pace, it would take the country 30 years to reach the levels seen in high-income countries. In fact, as per IFC, even to just close half of the existing gap with regional peers like Bangladesh, Egypt, India, Indonesia, and the Philippines, Pakistan would need to invest at least $2.5 billion in fixed broadband infrastructure by 2027.

The government roadmap for achieving digital equity

Expanding broadband access in Pakistan is not just a technical or financial challenge—it is a strategic necessity for achieving inclusive economic growth, digital transformation, and social equity. Pakistan continues to grapple with inadequate and uneven digital infrastructure and curtailing these gaps will require a coordinated public-private approach, targeted reforms, and sustained investment in both erecting physical infrastructure and building human capacity.

A foundational step in the direction could be the accelerated implementation of Pakistan’s upcoming National Fiberization Plan (NFP), which is still underdevelopment. This strategy must address both supply and demand-side barriers, focusing on expanding infrastructure particularly in underserved regions, while improving financial feasibility and durability to climate-related disruptions.

The government must take the lead in mobilizing private capital to expand infra-

structure in regions that have been disregarded historically. This involves more than just financing—it requires streamlining processes and creating a conducive environment that reduces investment risk and regulatory uncertainty for private investors.

As per the World Bank, a digital market segmentation approach, as piloted in Khyber Pakhtunkhwa (KP), can help identify areas where regulatory reform alone is sufficient, where one-time capital subsidies are required, and where perpetual support is essential to ensure universal broadband access. In KP, this approach demonstrated that every $1 of public investment could attract up to $1.80 in private capital, significantly expanding fiber-to-the-home (FTTH) lines. Such public-private financing models should be scaled nationwide.

Iftikhar elaborated that the government is heavily taxing the telecom sector and must reduce this burden. Moreover, it should incentivize private investors to deploy capital in closing digital infrastructure gaps in underdeveloped regions by offering subsidies and simplifying approval processes.

The contemporary excessive dependence on a single north-south corridor leaves the nationwide network vulnerable to climate related adversities and excludes large rural and western regions. Thus, it is imperative to expand the national backbone beyond the north-south corridor into underserved rural western and northwestern areas. Moreover, it must be ensured that such regions receive non-discriminatory and transparent access to national backbone as it will catalyze competition among smaller ISPs and reduce consumer costs. Likewise, extending fibre optic infrastructure between cell towers is vital, where connecting them with fiber instead of microwave backhaul—would significantly improve speed, reliability, and network resilience.

Regulatory reforms to remove market inefficiencies is an essential enabler of private

investment, particularly for infrastructure deployment. Pakistan’s fragmented Rightof-Way (RoW) approval system is a major barrier, which varies across provinces and creates costly delays and uncertainty for private investors. To address this, the government must streamline procedures, ensuring consistent fee structures and transparent approval processes nationwide. This will reduce deployment costs, boost investor confidence, and unlock private capital needed for scaling broadband infrastructure.

Nevertheless, infrastructure alone is insufficient to eliminate Pakistan’s digital divide. The government must pursue demand-side reforms in parallel. This includes promoting digital literacy and skills, particularly through schools, community centers, and regional language content. While countering gender-based digital exclusion through community-based initiatives, female-led digital access points, and family engagement programs can help overcome restrictive norms and empower women and girls to participate in the digital economy.

Finally, the government needs to focus on satellite technology that offers a complementary pathway to reach the most isolated areas of the country. Although fiber remains the backbone of future-ready connectivity, low-earth orbit satellite systems can deliver last-mile access, enable disaster communication, and support digital inclusion in rural and mountainous regions. Pakistan’s Universal Service Fund should proactively launch initiatives to improve broadband connectivity of regions through satellite-based services where fiber structures are impractical.

In a nutshell, bridging Pakistan’s broadband gap is not a question of public or private action but rather a matter of effective partnership. Pakistan can build a truly digital future that benefits all only by harmonizing its strategic objectives, investment policies, and pluralism drives. n

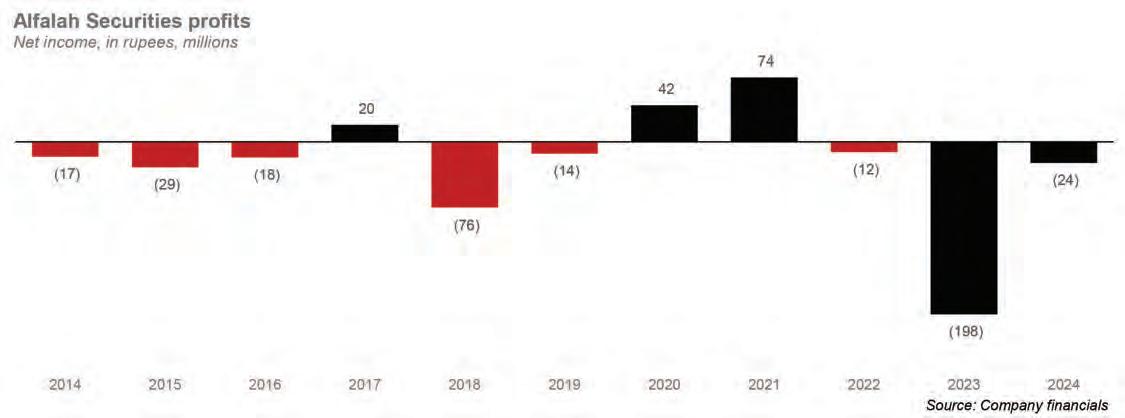

Bank Alfalah signs off on sale of Alfalah Securities to Optimus Capital for Rs 313 million

Deal closes the curtain on a seven‑year experiment with a foreign partner and hands Optimus a platform for bulking up its cash‑equities franchise

BProfit Report

ank Alfalah Ltd (BAFL) has completed the sale of 95.59% of the issued share capital of its wholly owned brokerage arm, Alfalah Securities (Private) Ltd, to Optimus Capital Management (Private) Ltd (OCM) for Rs 313 million in cash, following clearance from the Competition Commission of Pakistan in January and fulfilment of customary closing conditions in March.

The transaction, executed through a share purchase agreement covering

324.999 million shares, transfers operational control with immediate effect; BAFL retains a nominal 4.41% stake for regulatory continuity.

For Pakistan’s equity market ecosystem the sale is modest in rupee terms but significant for what it signals: the orderly retreat of a universal bank from a volatile ancillary business and the simultaneous rise of an aggressive independent brokerage looking to consolidate market share.

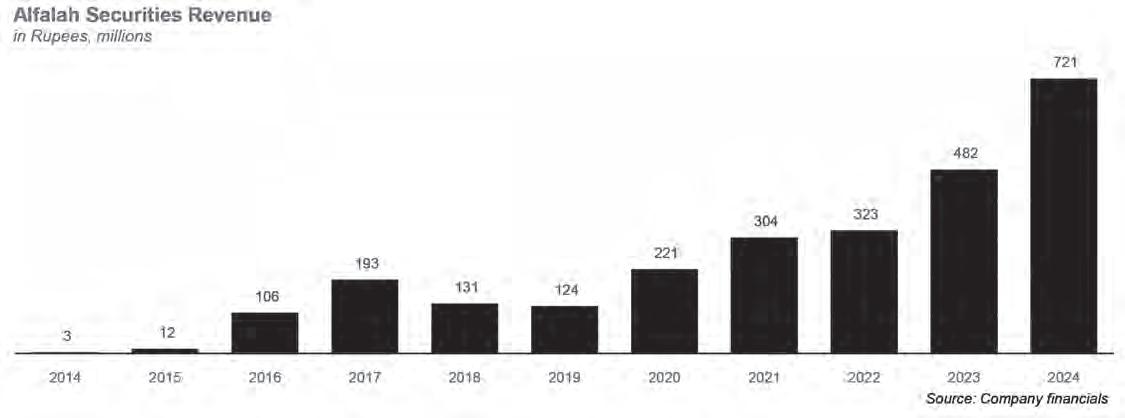

Why would Bank Alfalah want to sell? Some potential reasons include explosive but uneven revenue growth: From a tiny base in 2014 to Rs 721 million in 2024, the compound

annual growth rate works out to 74%—yet five of the eleven years registered negative or single digit growth.

The firm reported a net profit in only three of the past eleven years (2017, 2020, 2021). Average annual bottom line result: a loss of Rs 23 million. Finally, the annus horribilis of 2023: A Rs 197 million loss—linked to proprietary book mis trades and a sharp equity market draw down—erased nearly all retained earnings and forced BAFL to inject fresh capital.

The data underline why a systemic commercial bank might regard full ownership of

an equity brokerage as sub optimal in a capital constrained environment.

BAFL launched Alfalah Securities in 2002 to give its corporate and private bank clients direct access to the Karachi Stock Exchange (now PSX). The subsidiary obtained a Trading Rights Entitlement Certificate and, for its first decade, operated as a mid tier broker riding on the bank’s balance sheet credibility.

In 2018 BAFL signed a landmark deal to sell 24.9% of the brokerage to CLSA Ltd, the Hong Kong headquartered investment bank now owned by CITIC Securities. The venture was billed as a gateway for Chinese capital chasing Belt and Road opportunities in Pakistan: the firm was re branded Alfalah CLSA Securities and began distributing CLSA’s renowned research to local institutions. CLSA, founded in 1986 by ex journalists Jim Walker and Gary Coull and sold to CITIC for US $1.3 billion in 2013, had ambitions to build an ASEAN to South Asia cash equities network.

Two blows undermined the marriage. The 2018 and 2023 loss cycles forced BAFL to pump in cumulative fresh equity of ~Rs 1.2 billion to keep regulatory capital intact, diluting CLSA below its original 24.9%. And a strategic realignment happened at CITIC CLSA. Focus shifted to North Asia block trades and cross border debt capital markets, leaving Pakistan a peripheral priority.

By early 2024 Bank Alfalah had clawed its stake back to ~91%; CLSA remained a passive minority but with little operational presence. When BAFL launched a strategic review last autumn, CLSA declined to exercise pre emption rights—paving the way for a full exit.

Founded in 2004 as Millennium Capital and re branded in 2011, Optimus Capital Management is a privately owned brokerage and corporate finance boutique based in Karachi. The firm holds a full PSX trading licence, employs 80 professionals, and ranks among

the top five dealers of government debt on the exchange’s Bond Automated Trading System.

Optimus currently has three business lines. It equities business offers institutional cash equities and online retail trading through the Optimus Trade platform. Its equity research business offers 28 listed companies under coverage, with a focus on energy, fast moving consumer goods and banks. And its investment banking division does brisk business as well, and was most recently the lead manager on the Rs 6 billion initial public offering of Cnergyico (2023) and adviser on multiple sukuk issuances.

The Alfalah Securities acquisition gives Optimus a coveted top tier settlement slot, boosting its combined market share in PSX volumes from an estimated 3% to 7%. It also gives them a ready made foreign institutional client book, thanks to residual CLSA connectivity.

At first glance, Rs 313 million is a fraction of the Rs 1.2 billion emergency funding BAFL injected barely a year ago. Yet three factors explain the markdown. By December 2024 the subsidiary held net liquid assets of just Rs 230 million after settling proprietary positions. PSX reforms mandate higher net capital balance requirements from July 2025, forcing many smaller brokers to seek deep pocketed owners. And the brokerage’s return on equity averaged 9% over the past decade—below BAFL’s group ROE of 18%—making divestment a rational capital allocation call.

For Optimus, however, the price equates to 0.65x 2024 revenue and offers scope to extract cost synergies of at least Rs 60 million per year, implying a payback period of under four years.

Three datapoints from Alfalah Securities’ historical series illuminate what Optimus must fix. Proprietary trading swings accounted for up to 40% of gross revenue in peak years, magnifying volatility. Optimus plans to cap prop book exposure at 10% of equity. Averaged

122% between 2019 and 2024 because of duplicate research desks (BAFL domestic, CLSA offshore). Streamlining could cut that to 80%. Retail active accounts fell from 12,000 in 2021 to 7,500 in 2023 amid service disruptions. Optimus’ online interface and call centre capacity are expected to arrest attrition.

BAFL remains Pakistan’s sixth largest private bank, with total assets of Rs 2.2 trillion and ambitions in payments, consumer finance and digital lending. Jettisoning a brokerage subsidiary Frees up Rs 600 million in risk weighted assets (RWA), modest in group context but helpful for Basel III capital ratios.

The bank retains an arm’s length brokerage arrangement with Optimus for its private banking clients, ensuring continuity of execution.

The CLSA episode underscores how cross border joint ventures can struggle when Pakistan’s average daily traded value is scarcely US $30 million, too small for a global broker’s cost base. Currency devaluations (the rupee lost 55% versus the dollar since 2022) and political volatility lengthen breakeven horizons. Retail investors now prefer low touch mobile platforms; a high touch, research heavy model becomes harder to monetise.

Even after consolidation, the combined entity will rank behind AKD Securities, Topline, Foundation Securities and Arif Habib in volume terms.

The Rs 313 million price tag may look like spare change, but the transfer of Alfalah Securities to Optimus Capital is emblematic of a wider rotation underway in Pakistan’s capital markets infrastructure—from bank sponsored, balance sheet heavy broker dealers to nimble, tech enabled specialists.

For BAFL it is a housekeeping move; for Optimus it is a springboard; for the market it is a prompt to rethink how brokerage houses can achieve scale without compromising profitability in a frontier economy where every rupee of capital must earn its keep. n

Breaking barriers: Once paralysed, Dr Saira completes $6 million raise for health tech company MedIQ

Founded in 2020 in Pakistan, MedIQ is now eyeing AI-powered patient care across the GCC countries

By Taimoor Hassan

In 2019, Dr. Saira found herself lying motionless in a hospital bed, paralysed from a near-fatal car accident that resulted in the death of the driver. A public health expert with a PhD in health economics and a career that spanned the World Bank and Punjab’s Health

Care Commission, she had always been on the policy side of healthcare. But now, she was the patient and for the next year, she would remain one.

“I didn’t need to be in a hospital that long,” she reflects. “I needed rehabilitation, monitoring, and continuity of care, not just a bed. If systems were connected digitally, that could be achieved.”

That realisation sparked the idea for MedIQ, a healthcare startup that combines digital infrastructure, AI, and on-ground services to enable integrated patient care across the full spectrum of healthcare providers. Today the company announced raising $6 million from Rasmal Ventures in Qatar and Joa Capital in Saudi Arabia, with follow-on investment from existing backers.

Founded in Pakistan in 2020, MedIQ expanded to the Kingdom of Saudi Arabia in 2023, building momentum in healthcare across the region.

The MedIQ vision

To understand MedIQ’s vision, it’s crucial to understand Pakistan’s healthcare infrastructure. Pakistan’s healthcare system is chronically underfunded, deeply fragmented, and heavily skewed toward urban centers. With less than 1 doctor per 1,000 people, a patchy referral system, and underdeveloped digital health infrastructure, continuity of care is rare. Outof-pocket spending remains high, especially for outpatient services, which make up a significant burden for middle-income households.

Public hospitals are overcrowded; private care is expensive and inconsistent. Digital health records are virtually non-existent at scale, and interoperability is unheard of. In rural areas, patients often travel long distances just for basic consultations and there’s little data continuity across providers.

“In Pakistan, patients fall through the cracks all the time,” says Dr. Saira. “As someone who’s led public initiatives, I saw it from the inside. As a patient, I felt it. That gap is where MedIQ was born.”

Launched in 2020, MedIQ was built on a principle many startups ignore. That the unit economics matter. “We didn’t believe in deep discounting or chasing users with offers,” says Dr Saira. This has resulted in the company approaching EBITDA positive level at a crucial time.

Things haven’t been easy following the expansion into Saudi Arabia where Vision 2030 mandates complete digitisation of healthcare. Dr Saira cautions that entering the MENA region especially from Pakistan requires a lot of effort to build trust in the market before a company can gain trust of locals, investors as well as customers. There is a prevailing perception in the MENA region that Pakistani companies don’t stay for long, as far as her experience goes.

“Raising capital as a Pakistani company in the MENA region is extremely hard,” says Dr. Saira. “There’s a perception risk — no one knows if you’ll even stay in the market longterm.”

MedIQ had to spend a full year just establishing a presence in Saudi Arabia. They provided services for free to hospitals, insurance providers, and clinics, slowly building local credibility.

Their breakthrough came when Joa Capital, a local VC, decided to back them with a bridge round. “Once Joa came in, it changed everything. Suddenly, we had local validation — and the rest of the funding followed.”

Operational metrics and growth plans

Dr Saira disclosed that MedIQ’s operating margins were 17–18% in the early days through service delivery for corporations. MedIQ eventually commercialised the technology that they were using to boost gross margins to 45%, with the SaaS segment hitting 70%. On net level, the margins hovers at 25-25%.

Their hybrid model includes providing online-offline services via provision of tele-consultation services to corporations such as telcos and insurance companies in Pakistan. The other vertical includes selling white-label SaaS solutions that serve as backend systems for hospitals and clinics in both Saudi and Pakistan.

Dr Saira says that the lack of focus on B2C — selling products or services directly to individual customers - is what preserved their margins by eliminating the need to offer discounts to acquire customers. Unlike other B2C health startups that burn through capital offering subsidised care, MedIQ focuses solely on enterprise clients and insurers from the start — a strategy that keeps operations profit-

able and scalable.

On the revenue side, it grew from $2,000 to $55,000, to $200,000 following the expansion into Saudi Arabia. Now, MedIQ is generating $1 million per year in Saudi alone and growing at 30% month-over-month.

Despite the rapid growth, the competitive landscape in Saudi hasn’t changed. “It’s still the same old players. But while others are limited to Pakistan, we’ve gone regional and that’s made all the difference.”

Now preparing for its Series B, MedIQ plans to scale both geographically and technologically. Their next goal is to launch AI-powered automation of patient–doctor interactions and interoperable electronic health records that seamlessly link all providers.

“Customer acquisition in Saudi is expensive, and so is AI development,” Dr. Saira explains. “But to stay ahead of the curve — especially as Vision 2030 accelerates — we’re investing heavily in that.”

Under the plan, MedIQ would automate patient-doctor interactions using AI. The company is also eyeing expansion into Qatar and smaller GCC countries, establishing early beachheads as health tech adoption rises. n

Ingredion considering offers for a sale of Rafhan Maize majority stake

The Chicago-based company is considering a divestment of its decades-old holdings in the consumer goods company

Profit Report

Chicago based Ingredion Inc. has begun entertaining non binding offers for the 71% shareholding it holds in Rafhan Maize Products Company Ltd. (RMPL), its long standing Pakistani subsidiary listed on the Pakistan Stock Exchange (PSX), in a notice sent to shareholders this past week. Management is now weighing whether to open a formal auction or negotiate privately. Ingredion and Rafhan Maize have made no

public filings so far, but the company’s 71% ownership is disclosed in its own investor material.

Rafhan Maize grinds more than 400,000 tons of corn a year to produce industrial starches, liquid glucose, dextrose, dextrins and gluten meals that feed Pakistan’s food, textile, paper and pharmaceutical sectors. Although RMPL itself is an industrial ingredients business, the Rafhan name evokes warm, very consumer facing memories: Rafhan Custard, cornflour, jelly and pudding powders—household staples that generations of Pakistanis grew up on. Those

packaged dessert lines were created by CPC/ Ingredion decades ago but were sold to Unilever in 1998; the licensing link means the custard tins found in every pantry still carry the Rafhan name and sustain enormous brand equity for the industrial company that shares it.

Rafhan Maize’s story begins in 1953, barely six years after Pakistan’s independence, when U.S. based Corn Products Company (the forerunner of CPC International) established the country’s first commercial wet milling plant on the banks of the Rakh Branch Canal in Faisalabad (then Lyallpur). The venture was conceived to turn surplus corn from Punjab’s fields into industrial starch and glucose for a textile sector that was just finding its feet. Within a decade the operation had become part of CPC’s global footprint: company chronicles note that by 1963 CPC was already “manufacturing starch in Pakistan,” making the Faisalabad mill one of the earliest outside North America.

As Pakistan’s economy industrialised, Rafhan ramped up capacity. A 1967 entry on Ingredion’s corporate timeline highlights the “largest corn refining business in Pakistan” joining the Corn Products network, signalling major brown field debottlenecking and the introduction of high fructose corn syrup know how imported from the company’s Argo plant in Illinois. The mill’s output—native starches for textiles and paper, liquid glucose for confectionery—quickly made Rafhan a strategic supplier to Lahore’s looms and Karachi’s sweetshops alike.

By the early 1980s Rafhan Maize had outgrown its single plant roots, adding a dextrose dryer in Faisalabad and a second wet mill in Kotri, Sindh, to be closer to Karachi’s port. In 1985 the subsidiary was converted into a public limited company and listed on what is today the Pakistan Stock Exchange—one of the first agro industrial firms to float shares locally. The float enlarged the public float to 29 %, with CPC retaining a controlling stake.

Throughout the 1970s and 1980s Rafhan became a household name thanks to its consumer line—custard powder, cornflour, jellies— marketed under the same Rafhan banner as the industrial company. When CPC decided to exit fast moving consumer brands worldwide, it sold the Rafhan, Knorr and Energile franchises in Pakistan to Unilever (then Bestfoods) in 1998. The industrial business kept the Rafhan trademark under licence, while Unilever ran with retail products, explaining why today’s tins of Rafhan Custard sit on shelves next to but legally apart from Rafhan Maize.

CPC split in 1997, hiving off its global starch arm as Corn Products International (CPI). CPI re branded to Ingredion in 2012, but maintained its 71 % holding in Rafhan Maize— still its highest margin subsidiary, thanks to a rigorous dividend policy and near zero gearing. During these years Rafhan installed a state of

the art germ separation line, commissioned Pakistan’s first tapioca starch blend plant and opened an applications laboratory in Karachi to develop customised binders for snack foods and pharmaceuticals. Three production sites— Faisalabad, Jaranwala and Kotri—now process more than 400,000 t of maize a year. Ingredion’s 71% block is complemented by roughly 20% held by Pakistani retail investors and 6% by the founding management families; the free float trades under the ticker RMPL and boasts the highest dividend yield of any non bank on the PSX. Regular board participation from Chicago ensures technology transfer, while an all Pakistani executive team manages procurement from more than 10,000 smallholder farmers.

Beyond balance sheet strength, Rafhan Maize helped Pakistani consumers discover convenience desserts, supplied the starch that stiffened generations of school uniforms, and today underpins everything from bio degradable packaging to low glycaemic sweeteners. Eight decades on, the company’s arc mirrors Pakistan’s own industrial journey—from import substitution to globally integrated supply chains―and its pending sale by Ingredion would mark the end of the longest continuous foreign investment in the country’s manufacturing sector.

Rafhan Maize closed 2024 with net sales of ― 70 billion and a record profit after tax of ― 7 billion, up 8 % on the previous year as it held its enviable double digit margin despite raw corn inflation. Momentum has continued into 2025: first quarter earnings came in at ― 1.96 billion, 8 % higher year on year. The PSX quotes Rafhan Maize’s gross margin at 20.9 % and net margin at 10.7 % for 2024, underscoring a cash rich, dividend heavy balance sheet.

Rafhan Maize’s current market capitalisation on the PSX is roughly ― 82.7 billion (about US $295 million at ~― 281/US$). Ingredion’s 71 % block therefore carries an equity value near ― 58.7 billion (≈ US $210 million), before any control premium that a strategic buyer might

pay. Private equity suitors would also factor in the company’s net cash position, its 1,000 % annual dividend, and the cost of taking out the mandatory public float.

Ingredion itself started life in 1906 as the Corn Products Refining Company, morphed into Corn Products International after a 1997 CPC spin off, and adopted the Ingredion name in 2012 to reflect its move into high margin specialty ingredients. Today it runs 44 plants in 14 countries, employs 12,000 people and is pushing hard into plant based proteins and stevia sweeteners under CEO Jim Zallie.

Several motives for a possible sale line up:

• Currency and capital controls fatigue. Tight dollar liquidity and repatriation hurdles have made Pakistan a difficult jurisdiction for multinationals to fund capex or upstream dividends in hard currency.

• Portfolio pruning. Ingredion has been divesting non core, lower growth assets to finance acquisitions in plant protein and sugar reduction technologies.

• Precedent from other multinationals. Shell plc agreed in late 2023 to sell its 77 % stake in Shell Pakistan to Saudi based Wafi Energy, citing FX losses and working capital pressures—an exit that closed in 2024. TotalEnergies likewise disposed of its 50 % interest in Total PARCO last year, while Reckitt, Colgate Palmolive and others have trimmed local footprints.

• Local buyer appetite. A cash flush, family owned Pakistan conglomerate or a Middle East industrial player could use RMPL to secure a domestic supply of starches and sweeteners at a time when food security narratives dominate boardrooms.

If Ingredion presses ahead, the Rafhan Maize sale would mark Pakistan’s largest private industrial transaction since 2023 and reshape an ingredient market that touches everything from packaged desserts to pharmaceutical tablets. n

Syed Faisal Hasan

The Chashma-Jhelum Link Canal Question

While the Indus Water Treaty is under threat, we must focus on implementing its spirit domestically

The Indus Water Treaty (IWT) of 1960 was a watershed agreement that divided the Indus River basin between India and Pakistan. Under its terms, Pakistan relinquished claims to the three eastern rivers (Ravi, Beas, Sutlej) in exchange for the three western rivers (Indus, Jhelum, Chenab).

To mitigate the impact of losing the eastern rivers, Pakistan undertook a massive infrastructure project to transfer water from the western rivers to canal systems that had historically depended on the eastern rivers.

The Chashma Jhelum (C.J.) Link Canal, designed to divert water from the Indus River to the Jhelum River, has since become a major point of contention between the provinces of Sindh and Punjab.

The Indus River and Partition

The Indus River, known locally as Sindhu, was not navigable for the British due to its risky nature. Instead, the colonial government dammed, canalized, and barraged the river for irrigation. The coastal communities of the Indus delta, who can be described as the true low riparian, suffered the most due to reduced freshwater flows and increased seawater intrusion.

In some areas of upper Sindh Indus water flows in the canals and then it also flows in the fields to remove high salt content. The high salt content water ends up in lower Sindh through drainage canals. Lower Sindh suffers from sea water intrusion and also from salty drainage water intrusion from upper Sindh. Following the

The writer is a farmer

Partition of India in 1947, the rivers were divided, with the three eastern rivers going to India and the western rivers to Pakistan. Pakistan surrendered rights to the eastern rivers to secure the western rivers. This necessitated further damming and barraging of the western rivers to divert water to canals previously fed by the eastern rivers through six interlinking canals.

The Indus Water Treaty and the C.J. Link Canal

The Indus Basin Development Fund Agreement, signed alongside the IWT, outlined the projects to transfer water from the western rivers to replace the eastern river supplies. The project’s objectives were to:

• Transfer water from the western rivers (Indus, Jhelum, Chenab) to meet existing irrigation uses in Pakistan, which had previously depended on the eastern rivers (Ravi, Beas, Sutlej). This would release the whole flow of the three eastern rivers for irrigation developments in India.

• Provide substantial additional irrigation development in West Pakistan.

• Develop 300,000 KW of hydroelectric potential for West Pakistan.

• Make an important contribution of soil reclamation and drainage in West Pakistan by lowering ground water levels in water-logged and saline areas.

• Afford a measure of flood protection in West Pakistan.

The C.J. Link Canal was specifically designed to supply water from the Indus to canals off-taking at Trimmu, compensating for the loss of the Sutlej River waters. The design capacity of the C.J. Link Canal was estimated at 21,550 cusecs to meet the requirements of the Haveli Canal, Rangpur Canal, reclamation efforts at Trimmu, the Trimmu–Downstream Islam Link, and account for pond and river losses.

The canal was designed for seasonal operation, with varying discharges throughout the year. Table 3 in the design report specifies the monthly discharge requirements:

Annual total volume: 11.10 million Acre Feet (MAF). One cusec is a flow rate unit meaning one cubic foot of water flowing per second.

MAF stands for million-acre feet a unit of volume used to measure large quantity of water. One MAF of water is roughly equivalent to a flow of 500,000 sustained for 24 hours.(Chat-gpt)

Questions and Contentions

The central questions in the Sindh-Punjab water dispute revolve around the C.J. Link Canal: Was it constructed under the IWT implementation plan? Is it solely a flood canal, or can Punjab use it at will? Who decides when the canal opens and closes, and have these decisions been fair to Punjab?

Sindh considers the C.J. Link Canal a “flood canal” and refers to the 1945 water agreement between Sindh and Punjab, arguing that the canal was not constructed under the Indus Water Treaty. Conversely, Punjab refers to the 1960 Indus Water Treaty between India and

The operation of the C.J. Link has been affected by interprovincial water rivalries. The implementation of the treaty and its impact on Pakistan’s internal water distribution system highlight the challenges faced

1970: India Stopped Water in Ravi and Sutlej for canals after 10 years as per Treaty.

1971: Chashma Jhelum Link canal ready to replace flows in canal

1972: Indus Water Treaty Totally Ignored by Federal Government and Sindh Province.

Two accords were signed between Sindh and Punjab in 1972 and 1974 on when to use the Chashma Jhelum link canal.

These accords by itself were betrayal of 1960 I.W. Treaty between India and Pakistan. In 1973, Governor of Punjab, Ghulam Mustafa Khar, stated that the canal was constructed for continuous operation, countering the notion that it was merely a flood canal

As a result, from 1971 onwards Sindh Government’s permission was sought annually until 1985, a year of acute water shortage. Despite claims of Punjab acting unilaterally, the canal was opened in 1985 with the approval of the then Prime Minister of Pakistan, Muhammad Khan Junejo, and the acknowledgment of Sindh’s Chief Minister.

However, Mr Palejo claim that throughout the history of Pakistan, the policies of the Pakistan establishment, dominated by the Punjab elites and authorities has all along been to impose its peculiar hegemonic demands and decisions through autocratic means. From this point on there were two more phases: 1985-1991: Ad Hoc arrangement to open C.J Link

Trimmu and Sidhnai Rangpur Link

1991: The IRSA Accord formally known as the water Apportionment accord of 1991 is historic agreement amongPakistan four provinces to allocate the waters of the Indus River System fairly. The committee had five-members four from the provinces and one from the federal government. 1991- till now: Unfortunately, Chashma Jhelum link canal is run politically and not according to 1960 Indus Water Treaty.

The way forward

If Chashma Jhelum Link is part of Indus water treaty and was built with Indus basin development fund agreement, then it should be operated as per the spirit of the agreement,

to compensate for the loss of Sutlej River, to canals off taking at Trimmu.

The C.J. Link Canal was constructed under the IWT to replace water supplies from the eastern rivers. Its operation has been mired in interprovincial disputes, with Sindh viewing it as a flood canal and Punjab considering it essential for year-round irrigation.

The canal is a link canal between Indus and Jhelum to replace waters for canals that were being fed by Islam barrage on river Sutlej. The treaty tried to safeguard the interests of the farmers whose canal waters were going to be shut from Sutlej and Ravi going dry.

The working of C.J link is not based on the spirit and working of 1960 Indus water treaty but based on interprovincial water rivalries. Sindh is still stuck in 1945 water agreement between Punjab and Sindh. Punjab looks at 1960 Indus water treaty between India and Pakistan.

Resolving this conflict requires addressing the grievances of Sindh while acknowledging the treaty-backed necessity of the canal for Punjab’s irrigation needs. A cooperative, transparent, and equitable approach is essential to ensure sustainable water management and reduce tensions in the region. n

Haveli

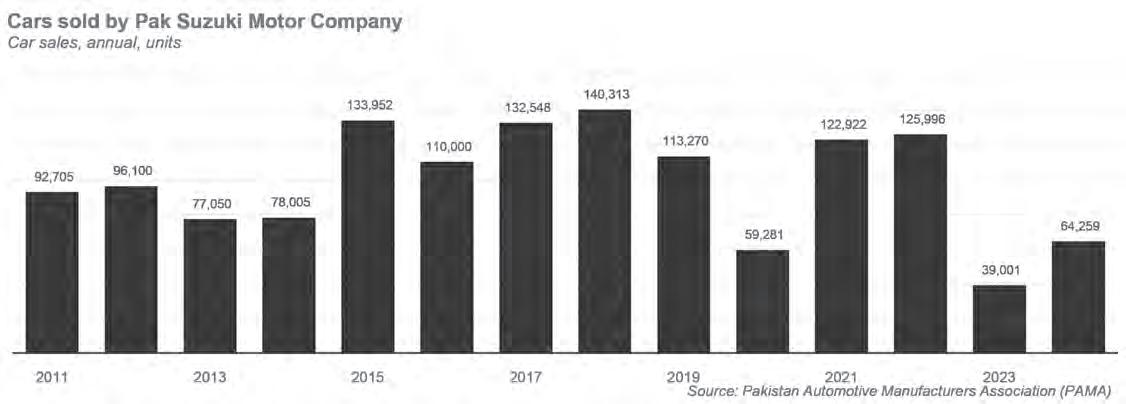

Pak Suzuki’s profits boomed in 2024, right after its buyback. Minority shareholders won’t be happy

After the buyback and delisting, it seems the auto assembler has finally become profitable in its latest financial statements

By Zain Naeem

Ramada Hotel in Karachi. April 29, 2024. With the commercial airline jets flying overhead, the conference room is getting heated by the second. Suddenly one of the minority shareholders gets up and says “Agar ek bud dua lag gai tu paeer sa chappal bhi nikal jai gi” and further added, “apko kafan bhi naseeb nahi ho ga.”

These words would seem appropriate for an overdramatized soap opera in an argument between the evil saas and disobedient bahu. Not in an Annual General Meeting of a publicly listed company. The rebuke becomes even starker when it is considered that Pak Suzuki is a company with Japanese directors and shareholders for whom respect is codified as sonkei from a very early age. The act of bowing, speaking politely and using proper honorifics is at the core of the culture. So what was the reason that such strong words were being used?

For the beginnings of this contentious issue, we have to go back even further. The issue began when Suzuki Motor Company in Japan announced that they were the largest shareholder of Pak Suzuki were interested in buying back the shares of the company and delisting it from the Pakistan Stock Exchange on a voluntary basis. The treatment of the minority shareholders during the buyback and the way it was carried out left a bad taste in the mouth.

It has almost been a whole year since the buyback of Pak Suzuki was carried out and it seems that there are still aftershocks and bad blood that has continued between the two parties. The latest development in this story is the release of the latest financial statements which has created a new schism between the two sides.

From the outset of the buyback being announced, there were allegations that the company was looking to carry out the buyback at a price favourable to itself and was short changing the minority shareholders while doing so. With the release of its latest financial statements, the doubt over the claims made seems to have reared their ugly head yet again as the company has been able to declare a profit after many years. The company will contend that the rebound is

legitimate and warranted. The minority will disagree. Where does the truth actually lie?

The buyback being announced

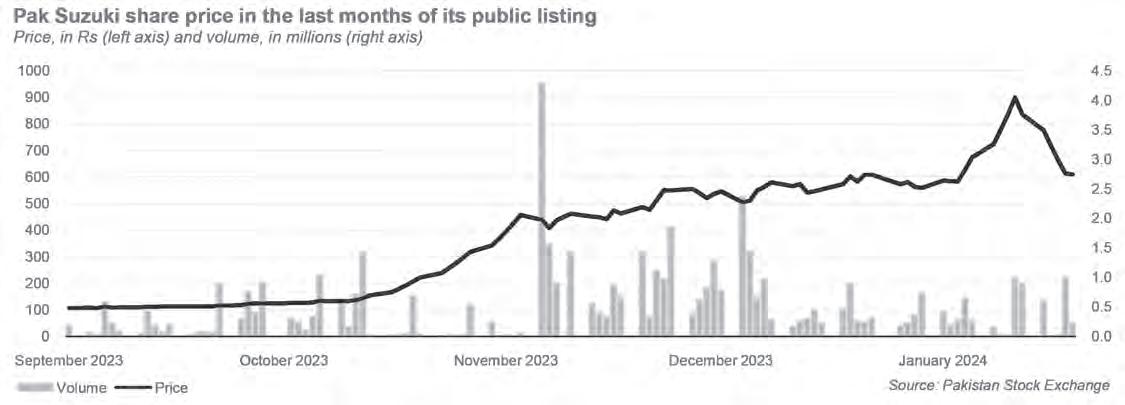

The interest in the company started way back in October of 2023 when the share price was hovering at around Rs136. In a span of three months, the price had increased to Rs 898 and there were signs that this momentum was going to continue. The reason behind the increase in the price was due to the voluntary delisting and buyback that had been called.

The rally in the market was showing that the investors were valuing the company at around Rs900 even when the company had floated its initial buyback offer at price of Rs406 per share. In simple terms, it could be called opening salvos in the negotiation battle as the two sides were looking out for their best interest.

The discrepancy in the two valuations was based on the fact that the company felt it had a lower value as the industry was under pressure. High inflation, depreciating rupee, restriction on imports and low disposal income meant that demand and supply was low for the auto sector. This led to shut downs being carried out as production was not feasible or possible under the circumstances. This coupled with high interest rates meant that auto lending was also depreciated during this period. In such an environment, the buyback was stipulating a low price based on the prospects of the industry.

On the other end were the minority shareholders who felt that there was inherent value within a company like Pak Suzuki and, once the economy rebounded, the sales would start to increase yet again. The temporary nature of the import restrictions and inflation would end and the company would be able to return to its old days of market domination. Pak Suzuki is known to produce small cars which are affordable in a developing country like Pakistan. Once the economy improves, Pak Suzuki will see its profitability return. Due to the tussle, the fate of the buyback hung in the balance. The majority owners of Pak Suzuki wanted to quote a lower price while the minority shareholders decided to band together in order to present a stiff opposition to the buyback being

successful. Under the PSX Rulebook, the majority shareholder has to buy 90% of the shares available in the market. A small band of minority shareholders grouped together and ended up owning 15% of the shares from the market.

The reason for the buyback was that Pak Suzuki had been suffering losses and had recorded a negative earning per share for three of the last four years with the share price trading at historic lows. The buyback would provide a good exit to the investors to earn back some of their investment and make a gain in such circumstances. At the time of the announcement, Suzuki Motors Company Japan owned 73.1% of the shares while the market had the remaining 26.9%.

The valuation of Rs 409 per share was carried out by an independent valuation firm – Iqbal A Nanjee & Company – who said that this was the price that should be paid.

The market was valuing the same shares for nearly Rs900. Due to the discrepancy, the final word lay with the Pakistan Stock Exchange which has a Voluntary Delisting Committee (VDC) which can add any other factors to the valuation that they deem appropriate. Based on this valuation, the majority shareholder has the right to appeal while the minority can simply choose not to sell and demand a higher price for their shares.

With both sides standing by their valuation, Pak Suzuki accepted the valuation determined by the VDC which was around Rs 609. The success of the buyback hinged on the fact that they had to buy 90% of their outstanding shares. The last option for the minority was to not let the company go past the 90% threshold and that is exactly what they did. A group of small investors came together and collected 15.39% of the shares to make sure that they were given a better price or they would let the buyback fail.

Allegations by the minority

There was a feeling amongst the smaller shareholders that the company had parked most of their losses in the previous three years and 2023 would end with much of the same. There were allegations made that the company was using the historic low price and the

losses on its accounts to force the price to be depreciated. Based on the low prices, the buyback would be carried out at depressed rates and the company would be able to pull the wool over the investors eyes.

Even while the buyback was being carried out, Pak Suzuki had disclosed a loss of Rs12.9 billion for the first quarter of calendar year 2023. By the third quarter of 2023, the company was profitable again, with a net income of Rs3.8 billion. The past losses, and now this turnaround, was almost entirely due to an improvement in the macroeconomic environment of the country.

Most of the past losses could be attributed to the exchange losses that the company had suffered. As the rupee had stabilized, much of these losses had been recorded and now the company could look towards better profitability in the future.

In a scathing letter sent to the PSX by the block of minority shareholders that they were concerned by the way the buyback was being carried out. The letter rejected the price being offered and alleged that the company was operating in an unlawful and oppressive manner. The letter alleged that profits had been siphoned off the balance sheet of Pak Suzuki by its parent company and were evading accountability in order to carry out the buyback.

It alleged that with the use of transfer pricing, discounts, commissions, loyalty and technical fees, Suzuki Motor Company Japan had been able to take away a significant portion of the profits of Pak Suzuki leading to losses. It was also alleged that the profits being seen in 2023 were down to the fact that the company had changed its auditors who were now showing the true picture of the company which was earning profits. The shareholders also felt that their views were being ignored and they were not made a part of the negotiations.

Not with a bang but with a whimper

With neither side willing to give in, Pak Suzuki looked to go through with a buyback which required approval from all of its shareholders. An Extraordinary General Meeting (EOGM) was going to be held on February 9, 2024 and the buyback rate was going to be finalized and approved.

Things had finally come to a head between the two sides as the company looked to approve the agenda that had been set out by them. In the EOGM held, the price was approved, however, the shareholders also made their voices heard. In the video surfacing from the meeting, it was seen that the minority shareholders lambasted the company and protested the price that was being quoted. It felt like the stalemate was going to persist as neither side was looking to take a step back.

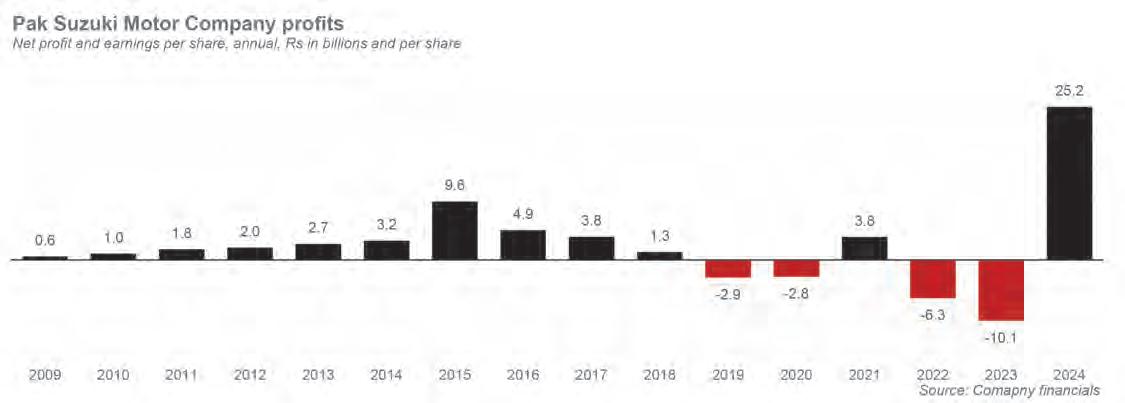

However, as the deadline for the buyback offer neared expiry, a compromise seemed to have been reached and the buyback was going to be carried out. In April of 2024, Pak Suzuki released its most recent annual accounts which showed that the company had ended 2023 as its worst year in history. Pak Suzuki ended up suffering a loss of Rs10 billion or Rs122 per share.

By September of 2023, it seemed like the company was finally turning around its losses in previous years and might end up recording a small profit. The actual results seemed to have been against the expectations.

At the end of 2022, the company saw financial charges of Rs11 billion due to charges owed to customers for late delivery, exchange losses and demurrage charges. Demurrage charges are those charged by ports when a

company is not able to clear its goods out of the ports in time. In the case of Pak Suzuki, this happened because the government of Pakistan refused to allow them permission to clear their own property from the ports, despite all taxes and dues being paid.

In addition to that, increasing interest rates and depreciating rupee meant that Pak Suzuki suffered from costs out of its own control. The same financial charges had only been Rs1 billion in 2021. During 2022, the rupee depreciated by 27.2% which compounded the finance charges.

Similar trends continued in the first quarter of 2023 where the rupee further depreciated by 25.4% which led to the finance cost being recorded at Rs13 billion in just the first three months. The trend turned in the next two quarters as the rupee stabilized and it now seemed like exchange losses were going to be lower by the end of 2023. So what was the reason that profits of the three quarters turned into losses?

At the end of 2023, the company recognized provision for doubtful advances of Rs1.9 billion caused by discontinuation of one of its car models. The reason this expense was such an outlier was that it had never been recorded in the past and all of a sudden an amount of Rs1.9 billion was being recorded out of the blue. Even after this provision, a profit of Rs4 billion was made.

Pak Suzuki eliminated its deferred tax asset of previous years which stood at Rs7.3 billion in 2023. The company felt that this asset was not sustainable and had to be written off. Both these amounts ended up turning a profit into a loss. If these two amounts were added back, the loss would have been less than Rs1 billion and loss per share would have been around Rs11 per share.

Whether the results played a role in making the mind of the shareholders or whether they gave in at the end, the buyback

was successful once the shares were sold to the parent company.With the company being delisted and with few shareholders left, the issue seems to have been resolved with both sides showing scars from the skirmishes.

With the release of the latest accounts, a new flash point seems to have been ignited.

What is in the latest financials?

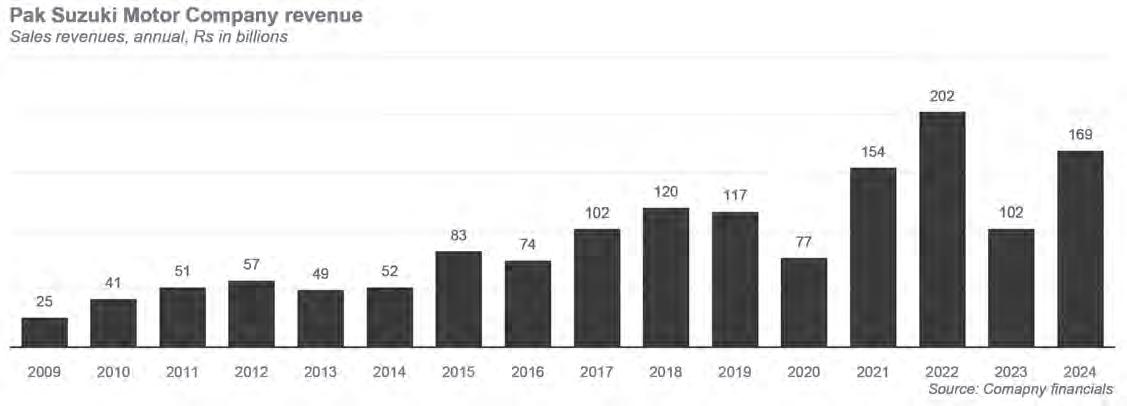

At the end of 2024, it can be seen that Pak Suzuki has been able to boost its revenues from Rs102 billion to Rs169 billion in 2024. This was an increase of around 65% from last year but still lagged behind the sales seen in 2022 of Rs202 billion.

In terms of the gross profit margin, it was seen that in 2022 the company was only able to retain 5.8% as its gross profit margin increased to 16.9% in 2023 and further to 19.5% in the latest financial year. This shows that the company has been increasing the

price of its cars and has been able to widen the gap between its costs and revenues being earned.

Going further down the income statement, the company saw its operating profits in 2022 of Rs5.3 billion grow to Rs24.7 billion in 2024. In terms of margin, operating margin went from 2.6% to 10.8% in 2023 and 14.6% in 2024. This shows that Pak Suzuki has been able to control much of its distribution, marketing and administrative expenses which has led to a higher retention of operating profits.

The biggest expense that the company recorded in 2022 and 2023 was finance cost which was Rs 11.6 billion in 2022 and Rs 11 billion in 2023. In 2024, this cost decreased to only Rs32 crores which meant much of these costs were reduced. Finance costs for Suzuki revolve around exchange loss caused by rupee depreciation, markup on late delivery and demurrage costs. As these costs have stabilized in 2024, the company has seen increased profits.

This coupled with other income being earned of Rs 3.3 billion in 2024 meant that the company was able to convert a loss of Rs 10 billion into a profit of Rs 25 billion from 2023 to 2024. The turnaround looks even bigger when it is seen that in 2023, loss per share was Rs 122 which became a profit of Rs 307 per share in 2024.’

Breaking down the turnaround

The mind boggling performance of Pak Suzuki in 2024 can be attributed to three key factors. These are the factors which will be touted by the company itself in order to defend the turnaround that has taken place.

The first factor is that the company was able to sell 65,000 cars in 2024 which had only been 39,000 in 2023. The increase in sales of cars was attributed to the stable prices, decreasing inflation and the reduction in the policy rate.

All these factors combined to stabilize supply and increase demand which led to the revenues of the company growing. The 65% growth in revenues can be directly linked to the growth in sales of the company.

Other than the increase in sales revenue, the gross profit earned by Pak Suzuki per car has also jumped from where it was a few years ago. In 2011, the company earned Rs22,000 of gross profit per car that it was able to sell.

As the profit began to increase, it touched a high of Rs87,000 per car in 2015 before reaching a low of Rs18,000 in 2019. Since then, it almost doubled to Rs93,000 in 2022 and touched a high of Rs512,000 in 2024.

This shows that not only is the company able to control its costs but has also been able to increase the price of its product line leading to higher sales revenue.

The second reason behind the improvement in 2024 is down to the finance costs which were huge in 2022 and 2023. Due to the falling rupee and the high interest rates prevailing in the economy, the cost incurred was around Rs11.6 billion and Rs11 billion for 2022 and 2023 respectively. In 2024, the biggest decrease is in this amount as Pak Suzuki only recorded a cost of Rs0.3 billion in comparison. The savings made in 2024 have allowed the profits to increase.

Lastly, the tax expense that was seen in 2023 was also abnormally high. As the company erased its deferred tax asset, it saw profits decrease by Rs7.3 billion. In the latest year, the company has recorded tax liability of Rs2.4 billion which has helped in increasing the profits to their highest level in the company’s history.

The earning per share of Rs307 is equal to the profits the company earned in the six year period from 2013 to 2018.

The (bad) memory remains