16 Corporate profits down 1% in 2024, but some sectors soar

20 Has Pakistan found a plan to turn its power liabilities into strategic assets?

24 OGDC and PPL’s commitments to Reko Diq take a step forward with feasibility study completion

25 Cement royalty hike in Khyber-Pakhtunkhwa: a price shock and legal deadlock await

27 What is driving crypto payment adoption?

28 Searle is lagging the pharmaceutical sector. Its recovery might be just around the corner.

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

The DOODH WALA is back!

Loose milk has always been the dominating force in Pakistan’s milk industry, but packaged milk has been on a mission to rout them out. With new taxes and rising inflation, the gawalas are in no mood for mercy

By Abdullah Niazi

Milk men are evil. In Pakistan they don’t come strolling to your doorbell with a six pack of milk bottles, bow tie slightly crooked, and humming a tune. In Pakistan, they arrive on a broken down Sohrab motorcycle, struggling to carry the weight of the huge copper drums slung carelessly on either side. The fumes from their ancient twostroke bike produce an evil black hue that undoubtedly affects the milk in some way or the other.

They also aspire to make sure your kids don’t grow tall. Which is why they all connive to mix water in your milk and inject their animals with the worst kind of steroids that will speed up your journey to the afterlife. That, at least, is the perception countless television exposes have fed to us, with reporters from small networks that nobody watches armed with a microphone and camera kicking down the doors of milk shops to test the quality of the milk inside them.

Perhaps no one symbolised this milk hysteria more than former Chief Justice of Pakistan (CJP) Justice Mian Saqib Nisar. While there were many issues his lordship took to heart during his glorious reign, liberally using his suo motu powers, his deep interest in and concern for the state of dairy in Pakistan was enough to grab international attention. When the economist profiled his honour, they captioned a full length picture of him with the words “judge, benefactor, milkman.”

These milkmen are central to a vast, largely informal network that provides milk in a country that is one of the largest producers (third) in the world, and has a population that consumes nearly 210 kilograms of milk per capita per year. They are also in a raging battle against major manufacturers of packaged milk such as Friesland Campina and Nestle.

And they are beating them to a pulp.

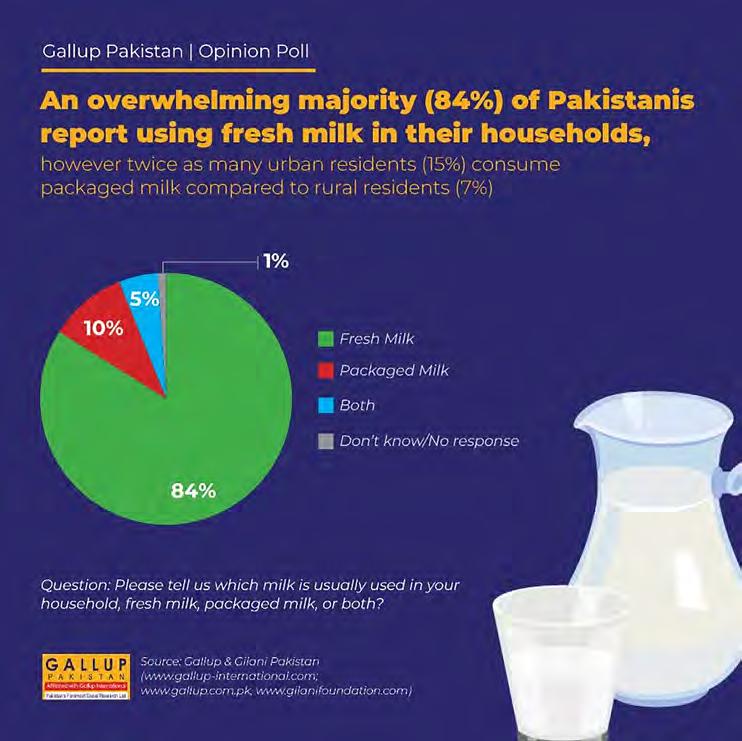

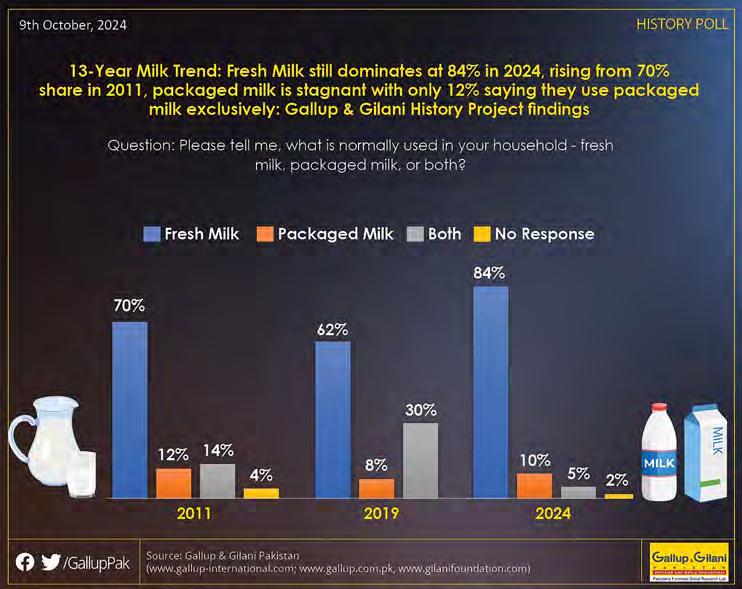

A recent survey conducted by Gallup Pakistan, an overwhelming majority of 84% of Pakistani households reported using fresh milk. In comparison, only 10% used packaged milk while a smaller proportion of 5% used both kinds of milk in their homes. The overwhelming dominance of fresh milk over packaged milk is not the surprising part. That has been the case for decades. As early as 2019, nearly 40% of households reported they used packaged milk at home.

The explanation is simple enough. Since at least 2021, milk along with other products has been affected by soaring inflation. In June 2024, the price of packaged milk in particular became subject to an 18% sales tax. Since then, according to a senior executive from Tetra Pak, the sale of packaged milk has fallen by 40%. Loose milk has always been the dominant force in Pakistan’s milk market. The vast network of gawalas and hole-in-the-wall milk shops sell a lot of milk.

The question is, what are companies like Nestle and Friesland Campina planning to do about this? Anyone that knows the milk industry knows that these companies can be cutthroat, and they are not

afraid of a streetfight against loose milk if it comes to it. But just for now it seems they are going through the motions of an age-old tradition in corporate Pakistan: complaining to the government.

A CEO walks into a bar …

ACEO, a Managing Director, a CFO, and the Chairman of an industry association walk into the office of a federal minister in Pakistan. This isn’t the setup for a joke—it’s a familiar scene in the country’s corporate landscape, where the executives of private companies band together to go crying and complaining to the government about taxes and all the other toils and troubles they face in the course of doing business.

Corporate lobbying, of course, is a part and parcel of doing business. In most countries it is regulated, and there is no harm in promoting one’s business interests with the government through industry associations and advocacy. In Pakistan, advocacy has more to do with who can complain the loudest and the longest.

Some industries are particularly prolific at this cribbing and crying. Large export oriented businesses such as textiles, cotton, sugar, and steel are known for the large operations they run to maintain a relationship with the government. While they are not one of those industry associations known for their prowess at this sort of thing, just a couple of weeks ago it was the Pakistan Dairy Association (PDA) lining up to have their grievances heard.

To be entirely fair to them, one can see why they would have cause for concern. As part of the 2024-25 budget, the government slapped on an 18% GST charge onto milk products. Traditionally, milk has remained an untaxed product. It is consumed in high volumes in Pakistan and is a staple product in most kitchens. Considering its importance, particularly in the development of young children, governments have tried to keep the product as cheap as the market allows without the added burden of taxation. By imposing the 18% GST, the price of milk went up by Rs 55 per litre overnight. The average Pakistani consumes more than 200 litres of milk every year. If we assume even half a litre consumed a day, it means a family of six consumes three litres of milk a day will see their monthly expense increase by almost Rs 5000.

The tax has been slapped on to a product that has already seen sales dip due to inflation. While overall revenues are up, many large scale milk companies have seen shrinking profits, with their sales falling significantly in terms of volume. While no hard data is available about this, a survey of a dozen milk shops in Lahore

A history of packaged milk

The history of packaged milk in Pakistan is concurrent with the history of packaging. The story starts with the establishment of Packages Ltd in 1956 by the Wazir Ali Group in collaboration with the Swedish packaging company, Tetra Pak. Initially focused on supplying packaging materials, Packages Ltd later identified an underutilized beverage packaging machine in 1976. Rather than discontinuing this business line, the company decided to vertically integrate by creating its own packaged milk brand, leading to the incorporation of Milkpak Ltd in 1979. The brand began production in 1981 and quickly became a market leader.

Milkpak expanded its product range in the 1980s, introducing fruit juices in 1984, butter in 1985, and packaged cream in 1986. A significant turning point came in 1988 when the Swiss multinational Nestlé acquired a controlling stake in Milkpak Ltd, rebranding it as Nestlé Milkpak Ltd. This acquisition brought substantial financial resources and technical expertise to the industry, helping to promote the growth of packaged foods in Pakistan. Nestlé, in collaboration with Packages Ltd, focused on educating consumers through television advertisements about the safety and health benefits of packaged milk.

This has always been the chosen strategy of packaged milk manufacturers. The idea was to take market share away from loose milk by portraying it as dangerous compared to packaged milk. In 2006, Engro Corporation launched Engro Foods, with its first product being Olpers, a direct competitor to Nestlé’s Milkpak. While initially seen as competition, Olpers helped expand the packaged milk market rather than simply taking away Nestlé’s market share. In 2005, before Engro entered the industry, packaged milk accounted for just 3% of total milk sales by value. By 2012, that share had grown to 7.8%, indicating a significant shift toward packaged milk consumption in Pakistan.

Despite these efforts, packaged milk remained a small portion of Pakistan’s overall milk consumption. Milk and dairy products were a major component of household spending, with milk alone accounting for 9.5% of monthly expenditures.

points towards a fall in demand for loose milk as well. Inflation has hit everyone hard, and since 2020, the price of loose milk per litre has doubled in some areas of the city. However, gawalas that buy milk from subsistence farmers and sell in the city as well as local milk shops are largely undocumented and deal in cash. This gives them a big advantage: their prices don’t include taxes.

Given how the past year has gone for the big packaged milk companies (more details on that later on), one can only assume a response to the Gawalas is in the works. And we’re pretty sure the script will be quite familiar.

David and Goliath

square off. But who is David?

Let us pause here for a moment and try to frame what we know of Pakistan’s milk industry. There are essentially three kinds of milk products available on the market. The first is your typical fresh milk from the gawala. Small peri-urban farmers raise herds that are often only three animals and sell to distributors which then sell the milk fresh on a daily basis to homes and milk shops. The second kind is fresh ‘pasteurized’ packaged milk. This is sold by companies like Anhaar and Prema. Pasteurized milk is usually sold by companies with large herds that use

machines to milk their cows, heat them at a low temperature, package them, and sell them in retail stores. Anhaar, which is owned by the Sharif family, has a herd of 4000 cows for example. This particular product while processed is still fresh. It needs to be refrigerated and has a (chilled) shelf life of a few days. Then there is Ultra High Temperature (UHT) Processed milk. This includes brands like Nestle’s Milkpak and Friesland’s Olpers brand. Milk that is UHT treated is heated at intense temperatures in short bursts, which kills microorganisms before being quickly cooled. The milk is then packaged in an airtight way, giving it a much longer shelf life and no need for refrigeration before the milk is opened.

All three kinds of milk have their own perceptions, problems, concerns, and benefits. All of the different players in the market play on these factors to try and promote their own product. The gawalas, for example, claim their milk is fresh and natural. However, large milk companies point towards the idea that milk is produced in unhygienic conditions and is often watered down. Companies like Nestle and Olpers claim their milk is produced in a highly monitored environment and packaged for safety. Their competitors cast doubts on whether or not their product is milk at all. Pasteurized milk brands like Anhaar and Prema try to position themselves as an alternative to both — fresh and hygienically packaged at the

same time.

These three kinds of milk and their sellers are locked in a constant battle for domination. The oldest players, of course, are the gawalas. There was a time when even relatively small households would have their own buffaloes to provide milk, and not just in rural areas. In Lahore, for example, private residential societies such as Model Town have bylaws to govern the raising of milk rearing animals — everything from how much area you need to leave in the backyard to how many animals you can keep depending on the size of your house and waste management.

As early as the early 2000s, a number of households still maintained their own animals at home in areas of Lahore considered posh. Of course, the main suppliers of milk in Pakistan are small scale dairy farmers. There are those that live in rural areas and have animals that give milk for their own subsistence level consumption. Then there are peri-urban farmers. They live close to the city, and use small herds that provide milk to local communities in the city.

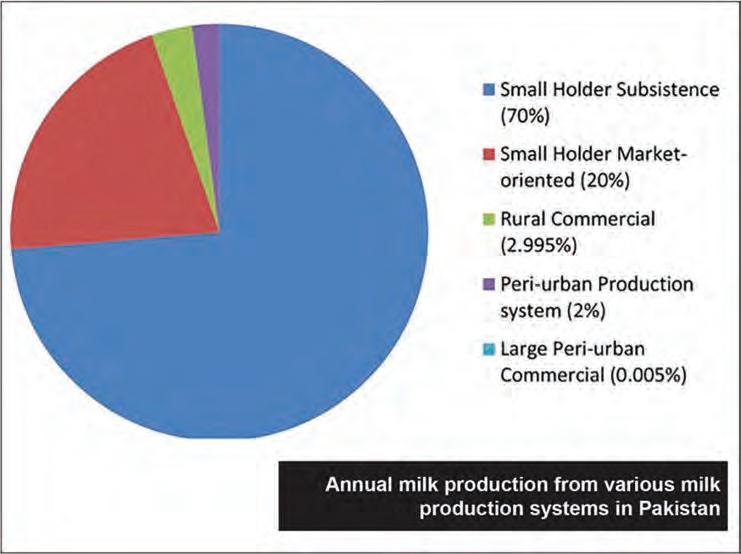

We do not have the exact numbers for this unfortunately. The last time an agricultural census took place in Pakistan was 2006, so the latest federal data is more than two decades old. What we do have, however, is a census conducted by the Punjab government in 2016. While even this data is dated at this point, it gives us a clearer picture of how things have developed. This provincial livestock census reported that a whopping 70% of the milk producers in Pakistan are subsistence based, compared to a miniscule 0.5% of large peri-urban commercial milk producers.

This means most of the milk produced in Pakistan comes from small farmers with herds of 5-15 animals. These farmers sell to shops, households, as well as large milk producers. Nestle, for example, does not have its own herd. Instead, they source their milk from 190,000 dairy farmers in Sindh and Punjab. Olpers does the same, sourcing milk from local farmers before transporting it to their facilities in Sahiwal in Punjab and Sukkur in Sindh. They also buy from large scale dairy farmers. Many of these big farms are owned by influential political families. The business itself involves imports (both of animals and bull semen) from places like Australia, and significant investment. It is also a business that makes sense for the landed elite, who have the space and capital to invest in the infrastructure for a large-scale farm including machines, breeding facilities, and veterinary costs.

In South Punjab, for example, one of the largest dairy farms is owned by Jahangir Tareen with a herd of nearly 2800 animals in Rahim Yar Khan. Prema Milk, the original pasteurized packaged milk brand that launched in

2008, is owned by the Chauhdry family of Gujrat. Prema in particular prides itself for only using pure Australian Cow’s milk. Similarly, as we have mentioned before, the brand Anhaar and its herd of 4000 animals is owned by the Sharif family.

The MNCs in plurality

Looking at Pakistan’s milk sector closely presents a pretty clear picture. Numerous small dairy farmers along with a few influential large scale dairy farms produce milk that they sell both to companies like Nestle and Friesland and to local communities. There is no reliable breakdown of the entire volume of sales of these products, but we can make some safe assumptions.

For starters, the Gallup poll we quoted in the beginning of this article sheds some light. An overwhelming majority of Pakistanis (84%) reported using fresh milk in their homes. Only about 10% used packaged milk, while 5% of households used both fresh and packaged milk. Most of the households that used packaged milk were in urban areas, where the usage of packaged milk was nearly double what it was in rural areas. What matters most is that these numbers have changed in recent years. As early as 2019, according to a Gallup poll that year, the number

of households using fresh milk only accounted for 62%. Only 8% of households used just packaged milk, but overall 30% of households used both packaged and fresh milk. This means the market has shrunk significantly.

It is a fact that the industry is deeply concerned about. In an interview with Dawn, Managing Director of Tetra Pak Pakistan Limited Awais Bin Nasim said that the penetration of packaged milk is only 3%. If accurate, this is significantly less than what was expected. Back in 2012, this number had gone up to nearly 8%, if it has gone down it means there is significantly less packaged milk being consumed, which would be in line with Gallup’s poll as well.

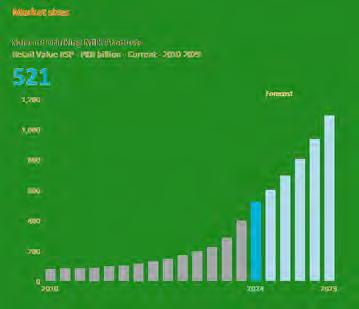

There have actually been some very interesting changes in the packaged milk industry. For starters, Olpers is now the market leader ahead of Milkpak. In total, according to a Euromonitor report, packaged milk accounted for sales worth Rs 521 billion, including powdered milk and flavoured milk 2023-24. Plain milk provided revenues of Rs 384.4 billion. Out of the overall sales, Friesland has a market share of 36.7% compared to Nestle’s 35.4%. When it comes to plain milk, Olpers has a clear edge over Milkpak with a 34% share compared to Milkpak’s 27%.

The overall retail sales are up significantly

from Rs 400 billion in 2022-23. However, this has not translated to increasing profits. The increased revenue is a function of increased prices because of inflation. Overall, sales of packaged milk fell between 2019-2024. And we are speaking about the dip in sales because of inflation without even getting to the post GST carnage.

It is a fact reflected even in the sale of loose milk. Recently, Profit visited peri-urban areas surrounding Faislabad and Lahore. Both

of these areas had colonies of dairy farmers and gawalas that collect milk from their animals and sell them in the city. Outside both these cities, there were more than 500 families each with 5-10 buffaloes to their name, and all of them live off the meagre fare selling this milk gets them. It is, essentially, a milk cottage industry.

Living in cloistered quarters in an area that can only be described as shambolic, this cottage industry provides nearly all of the

saleable milk in Pakistan. These are the same gawalas that are vilified as mixing water in milk and making people sick. They have also seen a dip in sales, with most reporting that houses once ordering 4 kilograms of milk a day have cut their demand down to half because of affordability.

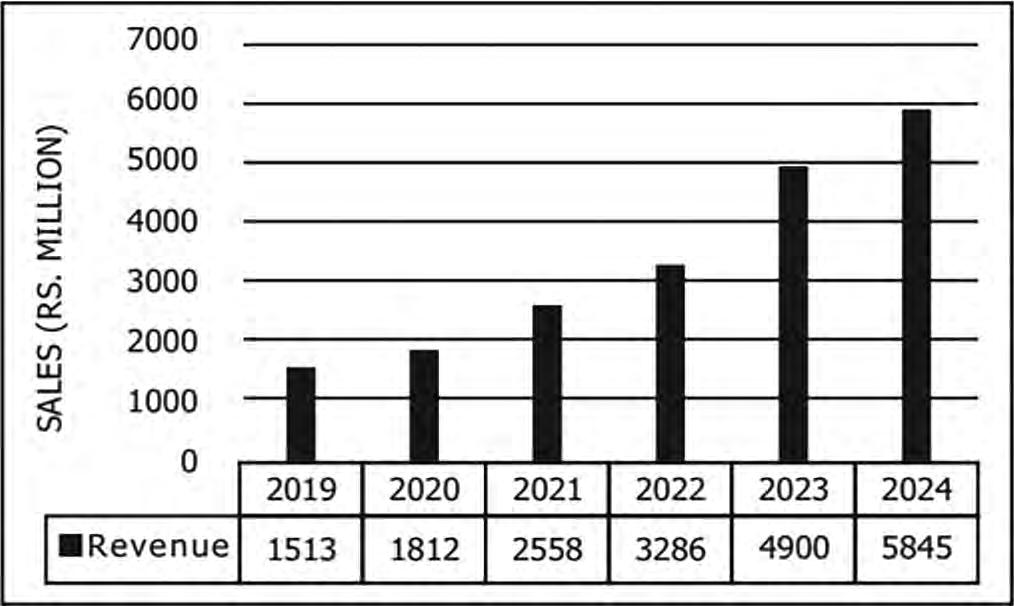

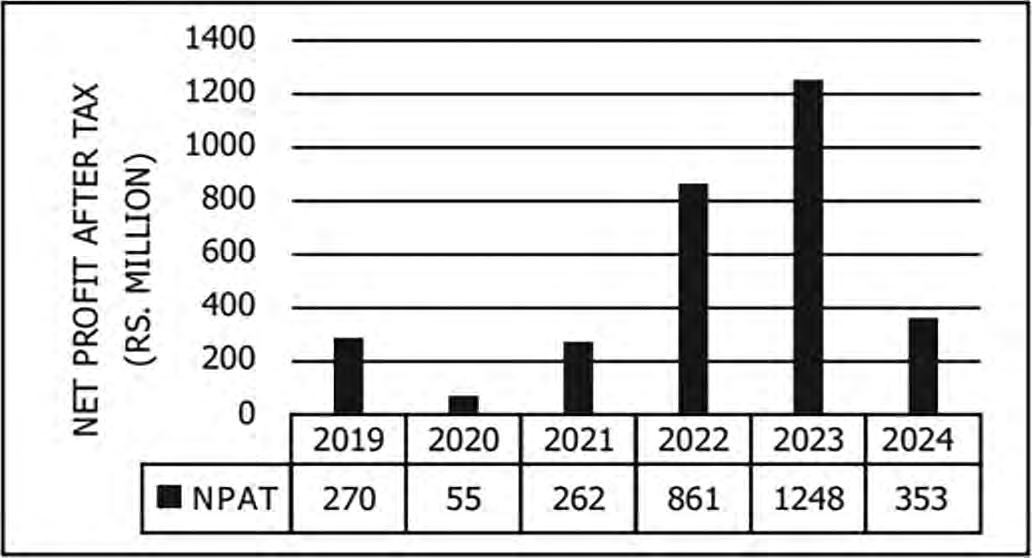

Perhaps the best indicator of this can be found in the financial statements of Prema Milk, the company founded in 2008 by the Chauhdry family of Gujrat which was listed on the PSX in 2015. In their annual report for 2023-24, the company reported that their overall sales had grown from nearly Rs 5 billion to Rs 6 billion. In fact, revenues have been growing with quite some consistency.

However, profitability has been falling. In 2023-24, the company was still profitable posting a profit after tax of Rs 35.3 crores. However, this profit after tax is down more than 70% from 2022-23 when it was Rs 124.8 crores. In fact, this is the lowest profit Prema has posted since it went public in 2015 other than in 2020, when covid absolutely decimated supply chains and retail shopping, which had an impact on perishable products such as pasteurized milk. In fact, 2020 was a good year for UHT packaged milk.

It is clear what is happening here — milk companies have been hit hard by inflation and have been unable to keep their profits as high as before, but they are still profitable. Prema admits as much in their annual report. Not only has inflation resulted in falling demand, the exchange rate disaster Pakistan went through from 2022 onwards, with the rupee crashing to Rs 320 per dollar at one point, the cost of biological assets (animals and insemination both) increased significantly since Prema only uses Australian Cows.

All of this is before the fact that the 2024-25 budget imposed an 18% GST on milk products. This has been a gamechanger. In the story published in Dawn, “sales of packaged milk have dropped by 40pc as inflation and the additional 18pc of tax have made the dairy product untenable for many of its consumers. Many have shifted to hybrid use, opting for loose milk for tea and packaged milk for drinking. If the tax remains in place for the next five years, the impact on the packaged milk sector will be ‘devastating,’ according to TetraPak’s Awais bin Nasim.” If the 40% dip in sales remains true, by that account the sales for this industry will fall to Rs 312 billion next year from Rs 521 billion this past year.

Waging war against the gawala

This is what it comes down to. Loose milk sold by gawalas and milk shops has stood the test of time as the main source of milk in Pakistan. This vast

network of milk distribution is backed by small scale dairy farmers, but large companies have constantly been trying to capture some of this market, and in some years have been quite successful.

The idea is to promote packaged milk as sanitary and loose milk as unsanitary. Some might make a legitimate argument for this, but in the past year, loose milk has had a very clear advantage over packaged milk when it comes to price. In an age of inflation, it is significantly more affordable than packaged milk which has

taken a beating.

What are the packaged milk producers going to do about this? They are already lobbying for a reduction in the GST in the next budget, but they are also on a mission to prove loose milk dirty. Already the Punjab Food Authority (PFA) is trying to implement a gradual ban on the sale of loose milk. Shops and suppliers are being registered and monitored for quality control, with self-important bureaucrats showing up with test tubes to milk shops thinking they are doing God’s work.

More than 8 million rural families are engaged in dairy production, which means around 35 to 40 million people are dependent on this sector. Dairy farming sustains their own food and nutritional needs, and the sale of surplus milk provides a key source of income. The milk produced by their cows and buffaloes accounts for over a third of the average farming family’s revenues. Besides that, the milk sold by small farmers provides a source of income for thousands of gawalas.

It needs to be understood that as far as milk supply is concerned, big dairy corporations like Nestle, Friesland Campina, Engro and Cargill account for a mere 5% while the remaining 15% is supplied by national commercial dairy companies like Nishat, Dairyland, Friendship, Sharif, Sapphire and Dada Dairies. The rest of the market is in the hands of small suppliers, and they are constantly the target of this multinational dairies which want control of the fifth largest dairy producing country in the world.

As things stand, the last year has been a good one for small dairies and gawalas because of the new tax. During Profit’s conversation with livestock farmers in Faisalabad, some said they had decreased their own consumption at home because there was increasing demand from within the city.

In the days to come, the multinationals and big dairies will fight back. The only question is whether or not they will be able to keep up with the vast cottage industry that provides the majority of milk in Pakistan. After all, they have not managed to get the kind of hold on the market they have wanted for decades. n

Corporate profits down 1% in 2024, but some sectors soar

Energy was the biggest drag, driven by volatile prices and demand; absent that laggard, profits at Corporate Pakistan rose 8% in 2024

PProfit Report

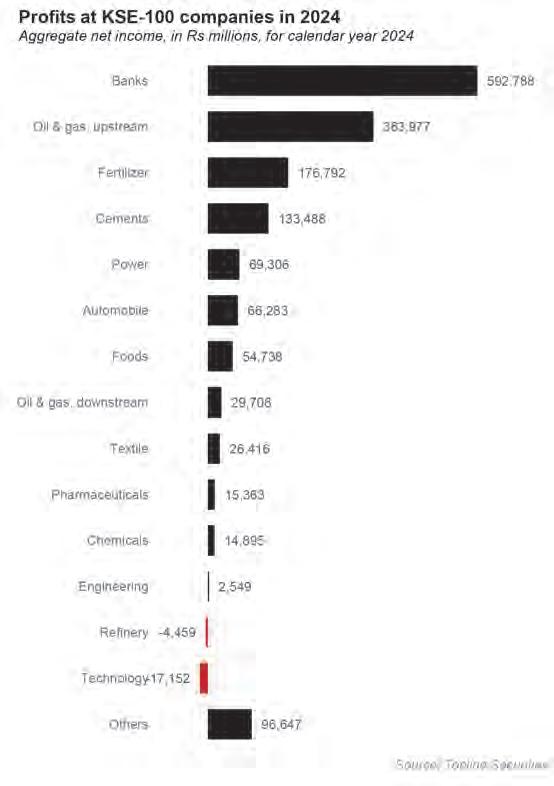

akistan’s corporate sector closed 2024 with a marginal decline in profitability, but beneath the surface, a tale of stark contrasts emerges. Data from Topline Securities reveals that while the overall profits of KSE-100 index companies fell by 1% year-on-year (YoY) to Rs1.62 trillion, several industries experienced significant swings— some surging to record highs, others tumbling.

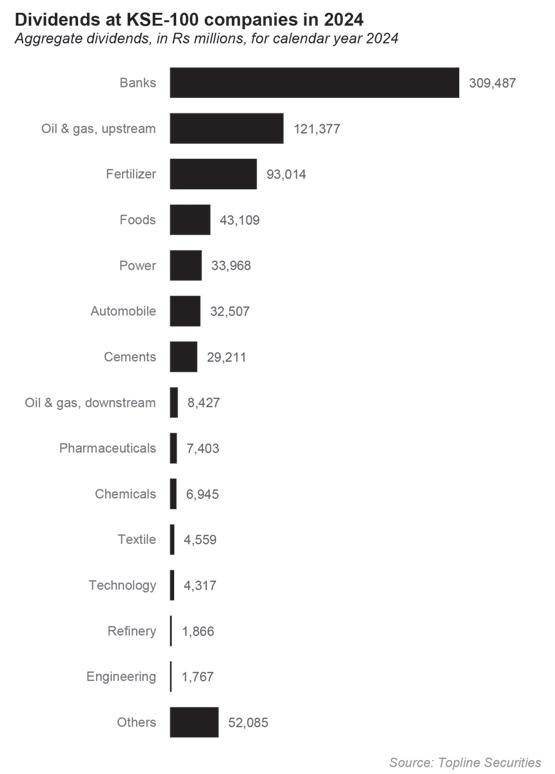

The energy sector weighed heavily on overall profitability, but banks, fertilisers, cement, and automobiles provided a strong counterbalance. Meanwhile, dividend payouts surged 27%, as companies sought to reward investors amid uncertain economic conditions. Total payouts rose to a record Rs750 billion in 2024, up from Rs592 billion in the prior year.

Here is a breakdown of what happened in each sector, and why.

Oil & Gas: A drag on market profitability

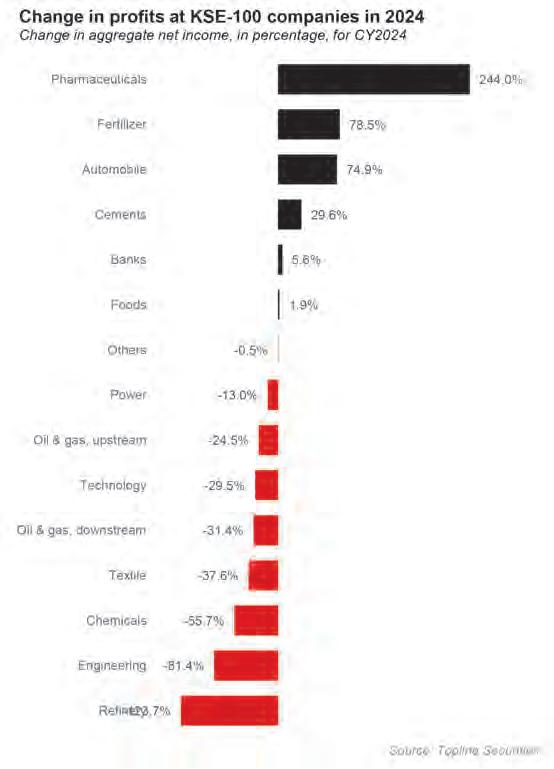

The upstream oil and gas exploration and production (E&P) sector bore the brunt of declining oil prices and lower production, with earnings slumping 24% YoY to Rs364 billion. This

marked a steep reversal for the sector, which has historically been a strong contributor to market profitability. Indeed, the decline in this upstream energy sector was so significant that, excluding this sector, the market’s profitability is up 8% for the calendar year 2024.

Oddly enough, dividends rose by 30% for the sector, from Rs93 billion to Rs121 billion. This is driven in large part by the fact that the largest companies in this sector – the Oil & Gas Development Company (OGDC) and Pakistan Petroleum Ltd (PPL) – are both stateowned entities, and the government can lean on them to pay out higher dividends in years of fiscal distress, even at the expense of capital expenditures in their future growth.

This is bad for both the government –the largest shareholder – and the country’s overall energy sector in the long term, but fills the government’s coffers in the short-run, and the government, being the substance-abusing addict that it is, will always choose the short term benefit over any long term considerations.

Pakistan does not really have an independent midstream sector, since most transportation and storage is conducted by downstream companies.

The downstream oil and gas sector – specifically the oil and gas marketing companies (OMCs) that manage large retail networks of petrol pumps – had an even worse year, with

profits declining by 31%, from Rs43 billion in 2023 to Rs30 billion in 2024. High prices and inflation – and the post-Covid acceptance of work-from-home – meant that as process rose, consumption went down, leading to lower sales and inventory losses on high cost products the companies then had to sell only when prices declined.

Again, given the dominance of the state-owned Pakistan State Oil in this sector, dividend payouts for this sector went up by 8% despite the decline in profitability.

See above about the government’s substance abuse problem.

Even worse performing was the perennially struggling oil refining sector, again dominated by state-owned players that have been used largely as dividend payout machines that have technology too antiquated to serve the market’s needs. The refining sector swung to a loss of Rs4.5 billion in 2024, from a profit of Rs19 billion in 2023. Nonetheless, the sector managed to eke out dividends of Rs1.9 billion, up 16.7% from the previous year.

Banking: The dominant force

The banking sector remained a pillar of strength, recording a 6% increase in profits to Rs593 billion, accounting for 37% of total KSE-100

profitability. This growth was powered by a rise in both net interest income (NII) and non-interest income.

Net interest income refers to the difference between the interest rates banks can charge on loans they give out to borrowers and the interest rates they have to pay out to depositors. This number tends to form the core of most banks’ revenue. Non-interest income refers to other fees that banks charge for financial services such as ATM fees, foreign exchange fees, commissions on distributing insurance and other non-banking financial products, etc.

High interest rates have meant that banks have enjoyed significantly higher net interest margins, since loans tend to reprice faster than deposits, and a large portion of the banks’ deposits are zero-cost current accounts.

Among the major contributors, United Bank Limited (UBL) led the pack with a Rs54 billion profit, followed by Meezan Bank (Rs50 billion) and MCB Bank (Rs42.6 billion).

This comes despite the banking sector facing significantly elevated taxation rates as the government levied a much higher tax on corporate income for banks at 44% compared

to the 29% for all other large companies, and 20% for companies defined as small businesses. That 44% was an increase from the 39% rate that banks normally face, but a step down from the 15% additional tax the government wanted to levy on the banks’ earnings from their lending to the government, which at this point accounts for the bulk of their revenue.

The surge in profits at the banks makes the rise in dividends less surprising, which rose by 27% to Rs309 billion in 2024 from Rs243 billion in 2023.

Fertiliser: grounds for growth

The fertiliser sector emerged as one of the biggest winners, posting a staggering 79% jump in profits to Rs177 billion. This growth was largely driven by higher prices of urea and diammonium phosphate (DAP), which rose by 39% and 9%, respectively. Fertiliser manufacturers in Pakistan have multi-decade guaranteed pricing in US dollars for their main raw material, which is natural gas. So any price increase tends to have a disproportionate effect on profitability.

Fauji Fertilizer (FFC) remained the

industry leader, announcing a hefty Rs49.6 billion profit, followed by Engro Fertilizers (Rs28.7 billion) and Fatima Fertilizer (Rs14.7 billion).

Dividend growth in the sector was also strong this year, with total payouts clocking in at Rs93 billion, up 61% from the previous year.

Pharmaceuticals: deregulation kicks in

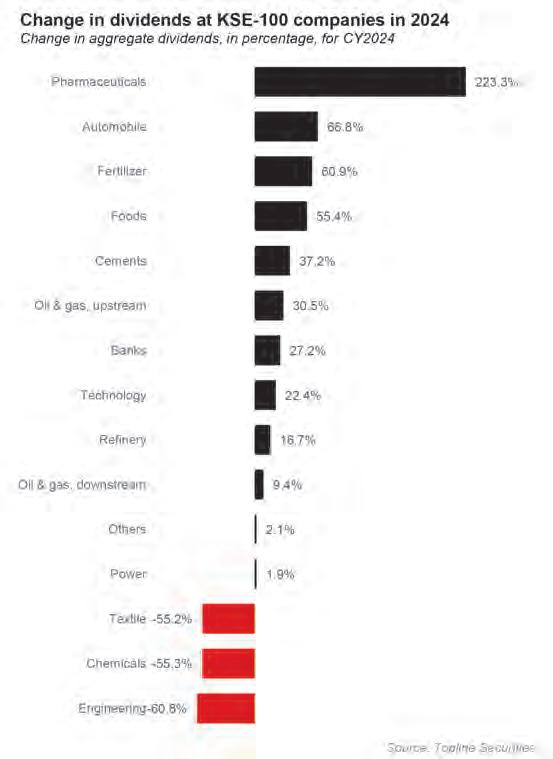

By far, the highest increase in profitability came in the pharmaceutical sector, which clocked in growth of 244% in profits, up to Rs15.3 billion in 2024. This has been driven almost entirely by the government finally allowing the sector to raise prices in a manner commensurate with their rising costs, at least for drugs deemed non-essential.

In February 2024, the government approved the deregulation of non-essential drug prices, allowing pharmaceutical companies to raise prices without any caps, unlike the previous drug policy, which allowed increases in non-essential drugs based on the Consumer Price Index (CPI) but capped at 10%. Meanwhile, prices for essential drugs

remain capped at a formula tied to 70% of CPI growth, with a 7% cap.

Additionally, the Ministry of National Health Services, Regulations, and Coordination (NHSR&C) approved price hikes for 146 essential drugs on February 6, 2024, further boosting revenue.

These price increases, coupled with a decline in raw material prices for many drugs and the appreciation of the Pakistani Rupee, led to an improvement in gross margins, which rose from 26% in 2023 to 36% in 2024. Importantly, however, this entire increase in profits came on the back of just a 15% increase in prices. As a result of this blockbuster profit growth, the sector also improved its dividend payouts, to Rs7.4 billion, up 223% from just Rs2.3 billion in the previous year.

The automobile sector staged a remarkable recovery, with earnings surging by 75% to Rs66.3 billion. This rebound was fueled by a 52%

increase in vehicle sales, as falling interest rates and improving economic activity boosted demand. Dividends surged to Rs32.5 billion in 2024, up 67% from the previous year.

Indus Motor dominated the sector’s dividend payouts with Rs12 billion, followed by Millat Tractors (Rs8.6 billion) and Atlas Honda (Rs7.6 billion).

The increase in sales was driven by the growing appetite for larger vehicles—a trend that underscores the economic resurgence among Pakistan’s upper middle class. Larger vehicles such as the Toyota Fortuner, Toyota Hilux, and Toyota Corolla Cross are not only commanding impressive sales numbers but are also indicative of shifting consumer priorities.

Buyers are now prioritizing enhanced safety, advanced features, and superior comfort, factors that are often associated with larger and more expensive models. This shift is a stark contrast to the previously dominant trend of smaller, more economical cars that catered primarily to the lower and middle-income groups.

Cement: Lower coal costs to the rescue

Cement manufacturers also had a strong year, with earnings rising 30% to Rs133.5 billion. Lower coal costs and an efficient power mix helped offset weaker local demand, allowing companies to improve their margins. Dividend payouts in the sector rose by 37% to Rs29 billion, up from Rs21 billion in the previous year.

Bestway Cement led the sector’s dividend payouts with Rs17.9 billion, followed by Lucky Cement (Rs4.3 billion) and Pioneer Cement (Rs3.4 billion).

The no-good, very-bad year for everyone else

Not all sectors shared in the gains. The engineering sector suffered an 81% collapse in profits, while chemicals (-56%) and textiles (-38%) also endured sharp declines. Similarly, power companies saw their earnings decline by 13% to Rs69.3 billion, indicating sector-wide challenges. n

Has Pakistan found a plan to turn its liabilitiespower into strategic assets?

Pakistan plans to use its excess electricity production for establishing Pakistan as a hub of blockchain technology but is it a viable solution?

By Hamza Aurangzeb

Once crippled by chronic power deficits, Pakistan now confronts an ironic twist: excess electricity generation alongside persistent blackouts and spiraling circular debt. While blackouts persist nationwide, especially during peak summer months, Pakistan has significant excess generation capacity compared to what it can currently consume.

This translates into the exacerbation of the government’s financial burden to the

mandatory capacity payments to power producers—payments based on installed generation capacity rather than actual consumption. Current plans to retire Rs1.5 trillion in circular debt through bank consortiums and budget allocations treat the symptom rather than addressing the underlying problem of excess capacity that created this financial quagmire.

In response, the government and the newly formed Pakistan Crypto Council are exploring an innovative approach: using surplus electricity to develop a blockchain industry and attract foreign investment—a proposal that warrants careful scrutiny regarding

its practicality, sustainability, and whether it represents a strategic use of this valuable yet paradoxically abundant resource.

Trump’s adoption of cryptocurrency and digital Assets

Although the US was one of the first countries to widely adopt cryptocurrencies, particularly bitcoin. However, in early March, the US President, Donal J. Trump signed an executive order for the establishment of a strategic

reserve of Bitcoin along with a digital asset stockpile which would include cryptocurrencies other than Bitcoin, namely Ethereum, XRP, Solana, and Cardano.

These funds and portfolios will typically contain digital assets that have been seized by the US government during proceedings for illegal activities. However, the US government will also experiment with innovative ideas to acquire additional cryptocurrency, particularly Bitcoin, without overwhelming the US taxpayer with additional cost. Trump has appointed crypto czar, David Sacks, which resonates with Trump’s aggressive advocacy for crypto during his presidential campaign.

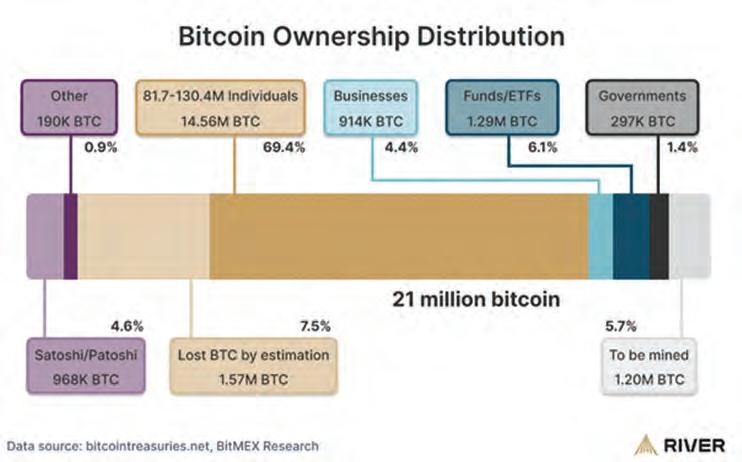

The White House is cognizant of the growing significance of cryptocurrency in the modern digital economy, particularly Bitcoin which has a finite supply of 21 million only and only 1.2 million coins remain to be mined. The US in accordance with its digital asset strategy is establishing this strategic reserve in order to have a centralized system to regulate, accurately track, and properly overlook the federal government’s digital asset holdings.

This plan is part of Trump’s strategy to revitalize economic growth in the country and establish the US as a technological leader in the world of cryptocurrency and blockchain, which showcases his commitment to establishing cryptocurrencies like Bitcoin as a widely adopted digital asset. The incumbent government’s favorable attitude towards cryptocurrency is likely to woo local and foreign Web3 companies to invest in the country.

This pivotal shift in US’s digital strategy has prompted several other governments and central banks to reevaluate their stance on decentralized digital assets. Countries like Argentina, Brazil, Hong Kong, Japan, Belarus are already exploring mechanisms to leverage the potential of cryptocurrencies. Similarly, Pakistan has also established the Pakistan Crypto Council to fully mobilize the potential of crypto currencies and related digital assets while transforming Pakistan into a focal point of this paradigm shift.

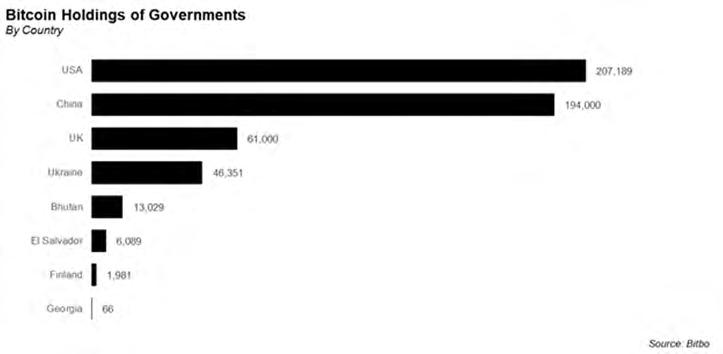

However, this is not the first time that governments across the globe are probing the realm of cryptocurrencies or digital assets. Several countries already hold gigantic amounts of bitcoin, while some countries obtained them through seizure while others intentionally accumulated them to develop strategic national reserves. The US leads the

list with 207,189 bitcoins, closely followed by China with 194,000 bitcoins, while the rest of the countries including the UK, Ukraine, Bhutan, El Salvador, Finland, and Georgia, cumulatively hold 128,516 bitcoins.

The government’s plan for emerging technologies

The Government of Pakistan in consultation with the Pakistan Crypto Council is conceiving a strategy that will facilitate and expedite investment in three particular sectors of the Web 3 economy in Pakistan, which includes crypto mining, blockchain based data centers, and tokenization of real world assets. This initiative will not only provide Pakistan an opportunity to foster the burgeoning industry of blockchain and digital assets but also enable it to efficiently utilize the excess capacity of electricity generation which has become an overwhelming burden on the country.

The government after deliberation with the power division and other relevant stakeholders intends to formulate an appealing electricity tariff for investors and companies operating in emerging digital industries of the Web 3 economy, albeit without government subsidies. So what’s the strategy then?

Since such industries consume massive amounts of electricity, the government believes that if it is able to attract significant investment in the relevant sectors of the Web3 economy, it will be able to provide companies and centers operating in the space, electricity at much more favorable rates than the contemporary rates due to economies of scale.

“In theory, the government can develop a policy for a lower electricity rate for the crypto mining and blockchain industry. However,

In theory, the government can develop a policy for a lower electricity rate for the crypto mining and blockchain industry. However, several safeguards must be put in place to ensure that cheaper electricity is not misused. The government interventions need to be well thought out to avoid distortions and excessive unintended consequences

Yousuf Farooq, Director Chase Securities

several safeguards must be put in place to ensure that cheaper electricity is not misused. The government interventions need to be well thought out to avoid distortions and excessive unintended consequences,” remarked, Yousuf Farooq, Director Chase Securities.

Recently the PM held a high level meeting with major stakeholders to discuss the prospects of the Web 3 economy like blockchain technology and asset tokenization in the country. The meeting was attended by participants like Marco Streng, Founder & CEO, and Dr. Marco Krohn, Co-Founder & Director of Genesis Group, one of the world’s largest Bitcoin mining firms that has mined over $1 billion worth of Bitcoin along with Vincent Kadar, CEO of Polymath Canada, a global leader in secure and compliant asset tokenization, responsible for tokenizing a diverse set of assets ranging from real estate to securities worth billions.

These veterans of the Web 3 economy put forth ambitious proposals for Pakistan, to construct a resilient and long lasting $3.5 billion infrastructure conducive for bitcoin mining and blockchain based data centers as well as initializing schemes for tokenization of assets. The progressive proposal aims to unlock Pakistan’s enormous potential of blockchain technology through attracting large sums of foreign investment, enhancing

economic resilience, and augmenting the financial system through adoption of latest innovations.

“The risk for crypto mining and digital assets should be borne by private firms and individuals, while the government itself should not use taxpayer money to make any investments or take on any risk,” Farooq added.

While it is still unclear how the government will earn through these emerging technology companies, whether it would be taxation or partnership for partial ownership of digital assets like cryptocurrency. However, we believe that the most prolific strategy will be a combination of the two for all stakeholders.

The government must provide tax incentives for companies to invest in Pakistan but receive partial ownership of the mined cryptocurrencies such as bitcoin. This would allow the government to generate tax revenue and build a strategic reserve of cryptocurrencies, whereas it would reduce costs for companies to do business in the country. Since everyone will have a stake it will lead to the establishment of a much more sustainable ecosystem.

The government and the Pakistan Crypto Council along with Web 3 companies are striving towards developing a plan for the implementation of proposed projects while discussing procedures for composing legislation for regulating cryptocurrency.

Why is the government launching this initiative?

As we have established that although the government will be able to manage the circular debt for now through raising new debt at below KIBOR rates from an alliance of banks, the fundamental issue of the power sector of electricity overproduction and excessive capacity will remain unresolved.

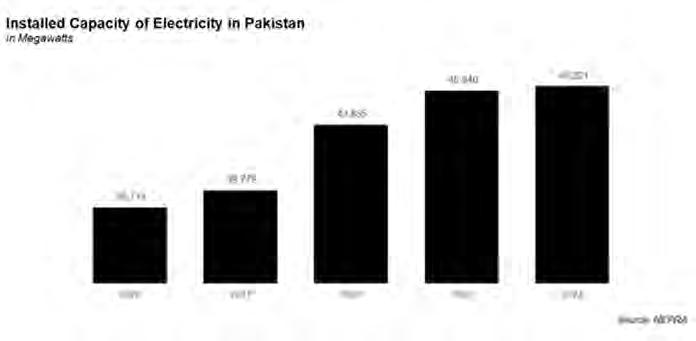

If we talk about Pakistan’s total installed capacity for electricity it stands at 46,221 MW, where the peak demand during winter stands at 12,000 MW, while the peak demand for electricity consumption during summers hovers around 30,000 MW. It means that even during the peak summer days Pakistan has an excess capacity of more than 16,000 MW, whereas this excess capacity goes beyond 34,000 MW during peak winter days.

The demand for electricity from the national grid has been decreasing post FY22, which is visible in the numbers for electricity consumption, which peaked at 89,361 GWh during Jul-Mar FY22, but is on a downward trend ever since. During FY24, Pakistan produced 127 TWh of electricity which is well below the country’s overall ability to generate electricity. The reason being that due to the lack of demand multiple power plants run below their capacity with utilization for some going as low as 5%.

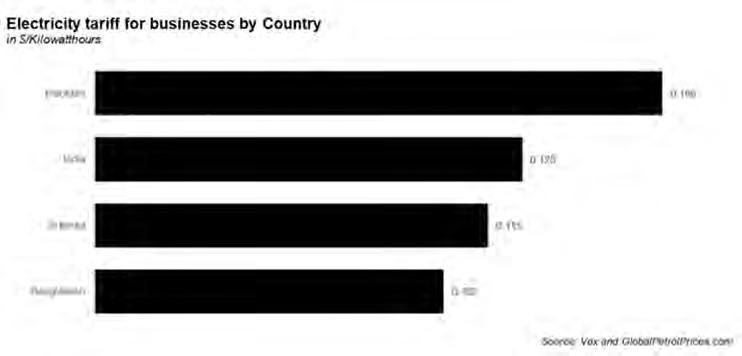

One of the major reasons for this declining demand is skyrocketing electricity prices which have increased on average by 155% over the past three years, where the electricity price for businesses has reached $0.166/KWh. This escalation in electricity price was observed due to high production costs triggered by the energy crisis of 2022, depreciating rupee due to low forex reserves, and rising financing costs due to accumulat-

ing circular debt.

As a result, there has been a major shift in the preference of customers in Pakistan, where an increasing number is installing rooftop solar for electricity consumption, liberating themselves from the woes of the national grid. Over the past five fiscal years, Pakistan has imported more than 20 GW of solar panels from China, which has left even the government scratching their heads.

Although these reasons have played a major role in persuading the government to utilize excess electricity for mining cryptocurrencies and blockchain based data centers in the country but this decision is not entirely based on ominous ramifications but the potential of digital assets and blockchain technology in the country has had a pivotal influence as well.

Pakistan is home to one of the largest populations of crypto enthusiasts. It ranks among the top 10 countries for crypto adoption with an estimated user base of more than 20 million. According to estimates, the country’s total transaction value for digital assets ranges from $18 billion to $25 billion per annum.

As per global trends, digital assets like cryptocurrency are particularly popular among the youth, which is corroborated by a survey conducted by KUcoin, which revealed that the largest group of crypto investors in Pakistan were males aged between 18 and 39. Since nearly two-thirds of Pakistan’s population is under the age of 30, it truly promises to be a hub for the blockchain industry and the Web 3 economy.

Challenges for the government’s scheme

Firstly, we need to understand that it will be a strenuous task for the government to convince a large number of Web 3 companies working on blockchain technology to invest in Pakistan. Foreign capitalists and entrepreneurs

consider investment in the country a high risk endeavor due to its precarious economic growth and mercurial governments. Such characteristics have historically inhibited the country from developing a robust economy immune to external shocks and cultivating a stable political environment, making foreign investors wary of Pakistan.

Now coming towards the electricity rate, local businesses and companies are purchasing electricity at exorbitant rates in the country. In fact the electricity rate in Pakistan is the highest among its neighboring South Asian countries and above the global average of $0.149/KWh. Hence the government must work out a tariff that is appealing to Web 3 companies, otherwise they have plenty of options within South Asia and around the globe which offer much cheaper electricity.

On top of expensive electricity, the national grid and distribution system of the country is highly inefficient, which leads to colossal losses. According to energy experts, around a quarter of the electricity produced is wasted due to the ineffective and deteriorating distribution system. This results in deprivation of electricity or widespread loadshedding across multiple regions in the country. The government needs to address this challenge and at least ensure that specific zones where emerging technology industries

like crypto mining and blockchain based data centers are going to operate receive uninterrupted electricity or else the government won’t be able to achieve the desired results.

Another key hindrance, which has adversely impacted the whole economy, but specifically the technology sector is frequent disruption of the internet. Since the entire existence of the Web 3 economy is contingent on the internet, it is essential that the government builds a resilient infrastructure that ensures companies receive unabated internet service. This is the most fundamental requirement for the industry and if the government can’t even fulfill this, then the government’s aspirations would merely remain a dream.

Lastly, Pakistan allows foreign companies to repatriate profits and dividends without any hassle during times of economic booms. However, when the music stops and things get tough, the State Bank of Pakistan imposes tight controls on capital outflows to protect the country’s foreign exchange reserves. This modus operandi of SBP was conspicuous during FY23 and FY24, which could be another concern for companies working on emerging technologies. Hence, the government in partnership with the SBP must conceive a plan that enables companies to repatriate profits, while preserving forex even during downturns.

The government’s plan to establish Pakistan as a cornerstone of the modern Web 3 economy through leveraging surplus electricity certainly has potential but there are several obstructions that could derail the government’s scheme. Hence, there is a need for the government to contemplate the contemporary economic landscape holistically and frame a blueprint that achieves its objectives. Nonetheless, it is worth a shot, as considering the myriad of complications in which the power sector finds itself, it won’t cost the government much in case of a failure. However, if the initiative succeeds, the government will kill two birds with one stone. n

OGDC and PPL’s commitments to Reko Diq take a step forward with feasibility study completion

The two companies have nothing to do with mining, but have forcibly been dragooned by the government into participating as equity stakeholders in the project with Canada’s Barrick Gold.

Profit Report

The Reko Diq mining project in Balochistan, Pakistan, has long been a focal point of both immense potential and significant controversy. Recent developments have seen two state-owned enterprises (SOEs), Oil and Gas Development Company Limited (OGDC) and Pakistan Petroleum Limited (PPL), traditionally known for their roles in the oil and gas sector, completing feasibility studies to participate in this monumental mining venture.

This strategic shift underscores the government's reliance on these cash-rich entities to finance its stake in the project, raising questions about the alignment of their core competencies with the demands of large-scale mining operations.

A glimpse into Reko Diq's troubled past

Situated in the Chagai District of Balochistan, the Reko Diq mine is among the world's largest undeveloped copper and gold deposits, boasting estimated

reserves of 5.9 billion tonnes of ore grading 0.41% copper and gold reserves amounting to 41.5 million ounces. The project's journey has been anything but smooth. Initially, the exploration rights were held by Tethyan Copper Company (TCC), a joint venture between Canada’s Barrick Gold Corporation and Chile’s Antofagasta PLC.

However, in 2011, the Government of Balochistan refused to grant a mining lease to TCC, leading to protracted legal disputes. The situation culminated in 2019 when the International Centre for Settlement of Investment Disputes (ICSID) imposed a $5.97 billion penalty on Pakistan for breaching its obligations under the Australia-Pakistan Bilateral Investment Treaty. This hefty fine underscored the complexities and challenges that have plagued the Reko Diq project over the years.

OGDC and PPL: Venturing beyond traditional boundaries

In a move that signifies a departure from their conventional domains, OGDC and PPL have completed feasibility studies for their involvement in the reconstitut-

ed Reko Diq project. Both companies, along with Government Holdings Private Limited (GHPL), hold an 8.33% stake each, collectively representing a 25% interest through a Special Purpose Vehicle (SPV) named Pakistan Minerals Limited. This SPV is set to acquire a 25% shareholding in the restructured project, with Barrick Gold retaining a 50% stake and the Government of Balochistan holding the remaining 25%.

The feasibility study outlines a twophase development plan for Reko Diq:

• Phase 1: Scheduled for completion in 2028, this phase entails a capital expenditure of $5.6 billion. Financing is expected to include a limited-recourse project financing facility of up to $3 billion, with the remaining $2.6 billion sourced from shareholder contributions. Upon completion, the mine will process 45 million tonnes per annum (Mtpa) of mill feed.

• Phase 2: Aimed at doubling the processing capacity to 90 Mtpa by 2034, this phase will be financed through a combination of revenues generated from Phase 1, additional project financing, and, if necessary, further shareholder contributions.

Over its projected 37-year lifespan, Reko Diq is expected to produce approximately

13.1 million tonnes of copper and 17.9 million ounces of gold. For OGDC and PPL, the financial implications are substantial. Post-project financing, each company's equity contribution is estimated at $349 million (approximately PKR 98 billion). As of December 2024, OGDC and PPL reported cash and cash equivalents of PKR 263 billion and PKR 140 billion, respectively, indicating their capacity to meet these financial commitments.

Strategic considerations: financial muscle vs. sectoral expertise

The government's decision to involve OGDC and PPL in the Reko Diq project appears to be driven primarily by their robust financial positions. While their financial contributions are undeniably valuable, it is essential to consider the strategic fit of these oil and gas giants in a mining context.

Mining operations, particularly those on the scale of Reko Diq, require specialized expertise in geology, mineral processing, and environmental management—areas that differ significantly from the competencies developed in the oil and gas sector. The transition from hydrocarbons to minerals is not merely a matter of financial investment but also involves navigating distinct operational challenges, regulatory frameworks, and market dynamics.

Moreover, the involvement of OGDC and PPL raises questions about opportunity costs. Allocating substantial resources to a mining venture may divert attention and capital from their core operations in oil and gas exploration and production, sectors that are critical to Pakistan's energy security and economic stability.

Potential benefits and risks

Despite these concerns, the participation of OGDC and PPL in Reko Diq could yield several benefits.

Firstly, there is the diversification. Engaging in mining allows these companies to diversify their portfolios, potentially mitigating risks associated with volatility in the oil and gas markets.

Secondly, it may end up contributing to economic development. Successful development of Reko Diq could contribute significantly to Pakistan's economy, creating jobs, enhancing local infrastructure, and generating substantial revenues.

However, these potential benefits must be weighed against the risks. The most obvious of these is the operational challenges. The lack of mining-specific expertise may lead to opera-

tional inefficiencies, cost overruns, and project delays. And the financial exposure is not without risk. The substantial financial commitments required could strain the companies' balance sheets, especially if the project encounters unforeseen challenges or fails to deliver projected returns.

Strategic alignment and capacity building

For OGDC and PPL to effectively contribute to and benefit from the Reko Diq project, a strategic approach is imperative. This includes

capacity building. Investing in acquiring mining expertise, either through partnerships, hiring experienced professionals, or training existing staff, to bridge the knowledge gap between oil and gas and mining operations.

Implementing robust risk assessment and management frameworks to navigate the complexities inherent in large-scale mining projects. And collaborating closely with Barrick Gold, the Government of Balochistan, and local communities to ensure that the project is developed in a socially responsible and environmentally sustainable manner. n

Cement royalty hike in Khyber-Pakhtunkhwa: a price shock and legal deadlock await

Peshawar attempts what Lahore has already tried: extracting more taxes out of the cement industry. The all-but-certain lawsuit and stay order are likely to make the bad policy idea ineffective anyway.

Profit Report

The government of Khyber-Pakhtunkhwa is pushing forward with a plan to revamp its royalty structure on cement manufacturing, shifting from an ore-based calculation to a bag-based formula. The move, which would bring the province in line with Punjab, is poised to significantly increase costs – the effective tax rate is going up six times the current rate – for cement manufacturers operating in Khyber-Pakhtunkhwa. However, as seen in Punjab, where cement firms successfully obtained a stay order against a similar policy, the legal fate of this proposal appears to be a foregone conclusion.

If implemented, the new royalty structure would have two major consequences: an inevitable increase in cement prices—driving up construction costs in the province—and a likely court battle that could delay or nullify the measure. The precedent set by Punjab’s manufacturers suggests that the latter is the more probable outcome.

From ore-based to bag-based: a costly transition

The proposal put forth by the Khyber-Pakhtunkhwa Mines & Minerals Department aims to shift cement royalties from the current ore-based structure, where manufacturers pay Rs250 per ton of limestone and argillaceous clay, to a bag-based calculation at 6% of the ex-factory sale value. This translates to an increase from approximately Rs12.5 per bag to a staggering Rs78 per bag, marking a more than six-fold rise in the royalty burden.

For context, Punjab adopted this model in August 2024, imposing a 6% levy on ex-factory prices. However, cement manufacturers there swiftly challenged the policy in court and obtained a stay order. Given that the judicial system has already deemed the policy contentious in one province, it is highly likely that Khyber-Pakhtunkhwa-based manufacturers will take a similar legal route.

The cement manufacturers affected by the proposed royalty hike include Lucky Cement, Kohat Cement, Bestway Cement, Cherat Cement, Fauji Cement, and Dewan Cement. These firms collectively represent a substantial portion of Pakistan’s northern cement market, supplying not only Khyber-Pakhtunkhwa but also Punjab, where they have historically enjoyed a cost advantage due to lower raw material costs.

Price hikes loom as manufacturers face profit squeeze

The new royalty structure would add approximately Rs1,100–1,200 per ton in raw material costs for Khyber-Pakhtunkhwa-based cement manufacturers, a stark increase from the current Rs250 per ton. Consequently, manufacturers would need to raise cement prices by around Rs66 per bag to offset the impact.

This comes on the heels of a recent Rs60 per bag price hike, which had already brought retail prices in the northern region to Rs1,380 per bag. Another increase of Rs66 per bag would push the price beyond Rs1,440 per bag, exacerbating inflationary pressures on the construction sector.

For a sector already grappling with high energy costs and economic instability, this additional burden could have far-reaching consequences. A surge in cement prices would inevitably raise the cost of housing and infrastructure projects, making construction less affordable for both private developers and government initiatives.

Given the projected impact on manufacturers, some of the biggest players stand to see substantial earnings erosion:

• Lucky Cement (LUCK): Rs14.0 per share hit

• Bestway Cement (BWCL): Rs4.4 per share hit

• Kohat Cement (KOHC): Rs10.2 per share hit

• Cherat Cement (CHCC): Rs9.3 per share hit

• Fauji Cement (FCCL): Rs0.6 per share hit

• Dewan Cement (DCL): Rs0.9 per share hit

While larger players such as Lucky Cement and Kohat Cement may have the financial resilience to absorb this shock in the short term, smaller firms will struggle to maintain profitability without passing the cost on to consumers.

Legal battle looms: a Punjab redux?

If history is any guide, Khyber-Pakhtunkhwa’s proposed royalty structure is unlikely to materialise anytime soon. When Punjab implemented a similar policy in 2024, manufacturers immediately

challenged it in court. The legal proceedings resulted in a stay order, with manufacturers required to furnish bank guarantees in lieu of immediate payments.

The same fate likely awaits Khyber-Pakhtunkhwa’s proposal. Cement companies have strong incentives to resist the move, and given the precedent set by Punjab, the courts are likely to entertain their objections. The legal argument hinges on whether a royalty based on ex-factory sale price—rather than raw material usage—can be justified as a fair levy. Manufacturers argue that such a shift disproportionately inflates their costs and lacks a strong legal foundation.

Even if Khyber-Pakhtunkhwa authorities push ahead, the royalty will remain a noncash expense until legal clarity is achieved. As observed in Punjab, companies are expected to provision for the increased costs in their financial statements but will not actually pay out the full amount unless compelled to do so by a court ruling.

Policy implications: uncertain future for cement pricing and taxation

The move by Khyber-Pakhtunkhwa’s government appears to be an attempt to level the playing field between its manufacturers and those in Punjab, where cement producers have been paying higher royalties. However, this attempt is fraught with risks:

Firstly, there is the likely inflationary pressures on construction. Higher cement prices will slow down real estate development and infrastructure expansion. Public sector projects may require budget revisions, delaying

critical infrastructure developments.

Then there is the legal uncertainty stalling implementation of the levy. If cement firms obtain a stay order, the government will lose immediate revenue from the new policy. Legal battles could drag on for months, as seen in Punjab.

Finally, there is the disproportionate impact on smaller players. While industry giants like Lucky Cement can absorb short-term losses, smaller manufacturers will struggle. This could reduce competition and lead to further price hikes in the long run.

A policy destined for limbo?

Khyber-Pakhtunkhwa’s attempt to introduce a Punjab-style royalty structure is a double-edged sword. On one hand, it aims to bring uniformity to cement taxation. On the other, it threatens to destabilise prices and spark legal battles that could drag on indefinitely.

Given the precedent set in Punjab, the likelihood of cement manufacturers securing a stay order against the proposed policy is high. If that happens, the actual implementation of the royalty increase will be delayed, and manufacturers will continue operating under the old system.

For consumers, the key concern is whether cement prices will rise as a result of the uncertainty. While a legal stay might prevent the immediate imposition of the new royalty, manufacturers could still preemptively increase prices in anticipation of higher costs down the line.

At a time when Pakistan’s construction sector is already burdened by economic volatility, interest rate hikes, and currency devaluation, an ill-timed policy move like this could exacerbate market instability. n

What is driving crypto payment adoption?

Many view crypto as a hedge against currency depreciation

By Taimoor Hassan

Pakistan is witnessing a significant shift towards cryptocurrency as users seek alternatives to traditional banking. With inflation concerns, limited financial access, and an evolving regulatory landscape, digital assets are becoming an increasingly attractive solution for financial transactions. Many Pakistanis view crypto as a hedge against currency depreciation, a tool for cross-border payments, and a means to achieve financial autonomy. A recent survey by BitGet wallet of 4,599 participants spanning Gen Z, millennials, and Gen X users provides insights into the motivations and barriers surrounding crypto adoption.

Speed and accessibility top the list of reasons for using digital assets, with 46% of South Asian users including Pakistanis citing transaction efficiency and 41% valuing global accessibility. In emerging markets like Pakistan, these factors play a crucial role in adoption, given the inefficiencies of traditional banking systems.

Crypto adoption in South Asia, particularly in Pakistan, is driven by various factors. A survey by KuCoin revealed that 33% of Pakistani crypto investors use digital assets to protect against the rupee’s declining value. Many Pakistani investors cite future aspirations (69%), wealth accumulation (44%), and transaction convenience (49%) as primary reasons for entering the crypto space. Trading remains the most common use case (46%), followed by holding assets (30%), peer-to-peer transactions (29%), and NFT purchases (22%).

According to the BitGet wallet survey, 37% of South Asian users prefer crypto assets due to their lower transaction fees compared to traditional payment systems. Limited access to traditional banking services - 59% of Indians called their banks “inefficient”- is fueling a shift to crypto, making digital assets a practical solution for faster and low-cost transactions in Pakistan as well.

Despite its growing popularity, crypto remains in legal limbo in Pakistan. The State

Bank of Pakistan (SBP) prohibits banks and financial institutions from dealing with virtual currencies, classifying them as unauthorized and illegal. However, Pakistan is shifting from this stance and planning regulatory frameworks. Bilal bin Saqib, CEO of Pakistan’s Crypto Council, has hinted at developing a structured approach to crypto regulations. Despite these restrictions, the estimated annual trading volume in Pakistan ranges between $18 billion and $25 billion, demonstrating strong demand for digital assets. Moreover, 32% of surveyed South Asians believe crypto enables seamless multi-currency payments, while 28% recognize its potential for value appreciation over time. While crypto is often seen as a cost-effective alternative, 38% of South Asians still cite high transaction fees as a major concern. When networks experience congestion, fees can spike, making small transactions impractical. For users who rely on crypto for daily spending or remittances, these unpredictable costs can become a significant barrier. The challenge lies in scaling blockchain networks to provide consistently low fees, ensuring that crypto remains accessible for all. Another key concern is security risks, with 34% of users worried about hacks and fraud. With crypto adoption growing rapidly, so do threats from scams, phishing attacks, and wallet breaches. Many first-time users lack proper education on securing their private keys or using decentralized platforms safely, leaving them vulnerable to financial loss. Strengthening user protections through awareness programs and improved security tools will be crucial for driving confidence in crypto payments. Additionally, 34% of South Asians are concerned about price volatility, making crypto an unpredictable option for everyday use. While many embrace it as an investment, rapid price swings discourage businesses and consumers from relying on it for payments. Stablecoins will be key to improving trust and usability. A stablecoin is a type of cryptocurrency designed to maintain a stable value by being pegged to a commodity or a currency. Though cash-based transactions are

still dominant, 38% of South Asians surveyed value the ability to spend crypto directly without converting it to fiat money - the paper based money. This reflects a growing shift toward treating digital assets as a functional currency rather than just an investment tool. Whether for peer-to-peer transactions, remittances, or digital commerce, crypto offers a seamless way to exchange value without the delays and costs associated with traditional financial systems. Beyond usability, 42% are drawn to crypto’s speed and efficiency, highlighting the region’s need for instant, reliable payments. With large populations dependent on remittances from overseas, crypto enables workers to send money home without the long waiting periods and high fees imposed by banks and money transfer services. The ability to move funds 24/7, without banking hours or intermediaries, makes crypto an increasingly attractive option.

Additionally, 37% see lower transaction fees as a key benefit, especially in economies where financial costs can be a barrier to economic participation. Small businesses, freelancers, and digital workers benefit from cheaper cross-border payments, allowing them to keep more of their earnings and reduce dependence on costly traditional banking services. Generational preferences and challenges also affect crypto adoption trends. Gen X (49%) prioritizes speed, making crypto an attractive option for fast transactions. Millennials (42%) and Gen Z (39%) favor borderless transactions, highlighting crypto’s role in international trade and freelancing payments. Security concerns are highest among Gen X (42%), whereas Gen Z (36%) is more sensitive to transaction fees. Usability challenges remain a hurdle, as younger users are more willing to integrate crypto into daily financial activities but struggle with platform complexities and the lack of financial infrastructure.

As Pakistan navigates its crypto adoption journey, balancing its usage with regulatory clarity will be key to unlocking the full throttle usage of digital assets in the financial ecosystem. n

Searle is lagging the pharmaceutical sector. Its recovery might

be

just around the corner.

The pharmaceutical company has had lackluster numbers in recent times. All that might be about to change

By Zain Naeem

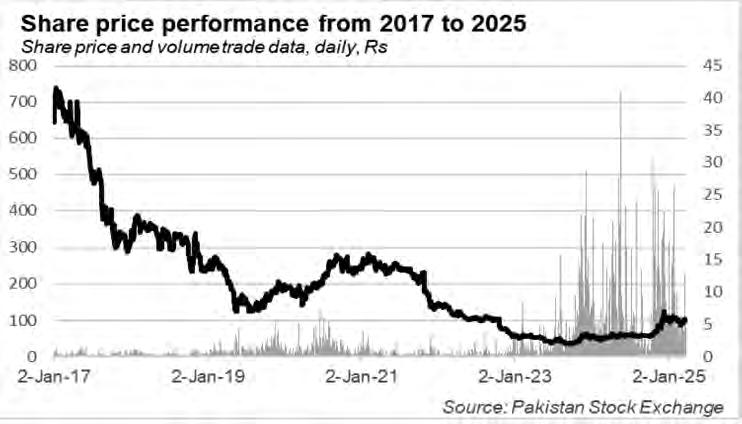

Think back to June 2023. It might seem like less than two years ago but in terms of the stock exchange, it feels like a lifetime. The index fell below the threshold of 40,000 points and there was a sense that the monotony would not break anytime soon. But then things did change and a rally was sparked. The rally that began in June of 2023 seems to be going strong still as the index is touching levels close to 120,000 in March of 2025. There are few indications that this rally has ended and there are experts who say that 125,000 is not far away either.

With the index tripling within two years, it is no wonder that the stocks listed in the market have also seen their prices increase manifolds. There are market performers which were languishing in the bear market but saw their prices increase steadily with the index. One such sector was the pharmaceutical industry which saw many of its scrips increase in value.

Companies like Liven Pharmaceuticals saw their share price jump by almost 20 times from Rs 9 in December of 2023 to Rs 220. The lower end of the spectrum saw returns of more than 200% as well in line with the increase in the index.

Pharmaceutical owed some of the increase to the fact that drug pricing was taken away from the purview of the Drug Regulatory Authority of Pakistan (DRAP) and handed over to the companies. This was a policy shift specifically for non essential medications which were being controlled and approved by DRAP in the past.

With the control of pricing being handed over to the companies, they were able to increase their revenues with the same levels of costs boosting their profits. The financials of many of the companies confirms this as they have seen their earnings jump upwards compared to last year. Better profitability

meant better earnings and an increase in their stock price.

Even in such an environment, there are companies like Searle which underperformed during this earnings bonanza and stock market rally. Searle has seen its price lag behind many of its competitors and the reason for this needs to be analyzed in detail to appreciate all the nuances of what has taken place. How has the company performed in recent years, what are the major headwinds the company is facing and how does it plan to overcome these challenges? This is a story of how Searle is looking forward to charting a new course while having an anchor pulling it downwards.

Searle’s history

Searle was established in Pakistan in October 1965 as a private limited company. It began as a subsidiary of G.D. Searle & Company, a global pharmaceutical firm, marking the company’s entry into the South Asian market. Initially based in Karachi, Searle focused on setting up manufacturing facilities and building a distribution network. The company quickly gained recognition for introducing innovative and high-quality medicines to the Pakistani market.

The company is involved in the manufacturing of pharmaceutical and other consumer products. In 1987, the company was acquired by local management, becoming an independent entity from its global parent company. Currently, International Brands (Private) Limited is the parent company, holding a 50.25% stake in Searle.

Under the umbrella of Searle itself, it has many subsidiary companies like IBL Healthcare, Searle Pakistan, Searle Pharmaceuticals, Searle Laboratories, Searle Bioscience, Nextar Pharma, IBL Future Technologies, Searle IV Solutions, Stellar Ventures, Mycart, IBL Frontier Markets and Prime Health.

Searle’s product range covers diverse therapeutic areas, including cardiovascular, respiratory care, gastroenterology, pain

management, central nervous system (CNS), orthopedics, neuropsychiatry, antibiotics, and nutritional care. Some of its flagship products include GlucoMet and GlucoMet-Forte for diabetes management and Nuberol Forte for pain relief.

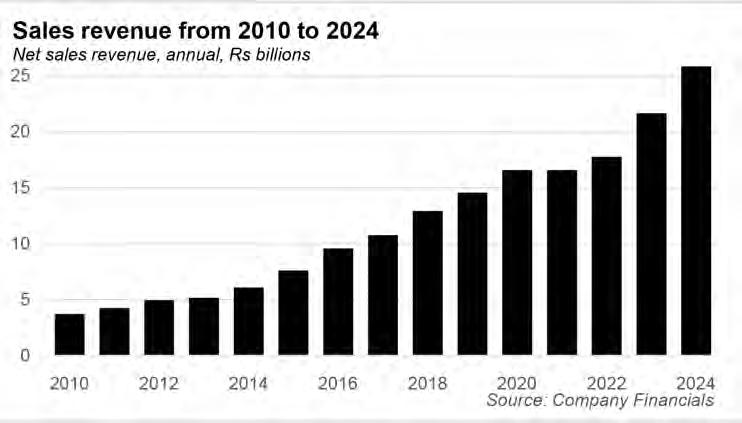

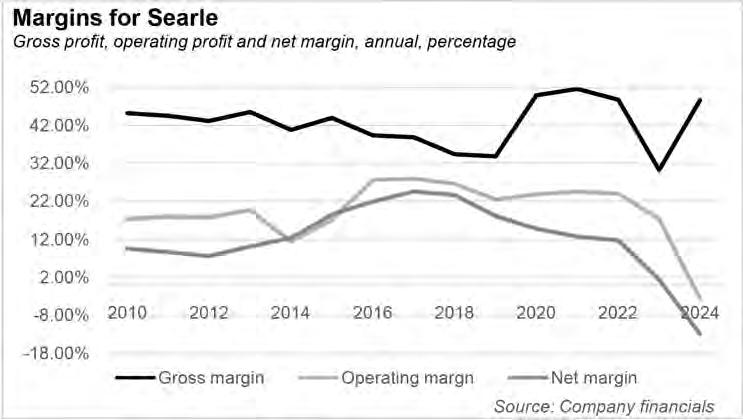

Going back all the way to 2006, the company registered healthy sales of Rs 2.4 billion. This coupled with retained earnings of Rs 1.3 billion showed that the company was profitable for some period of time. The asset base was worth Rs 1.9 billion which was mostly funded by the equity. In a space of 18 years, the company has been able to increase its revenues to around Rs 22 billion which is almost an increase of 10 times.

The revenues have been translated into huge gross margins as the company has, on average, retained gross margins of more than 42% throughout this period. In terms of the operating margin, the company also retained a ratio of 21% as the company was able to retain half of their gross margins. Lastly, the net margin of the company also came in around 14% for this period which shows that the company was earning a good amount of net income.

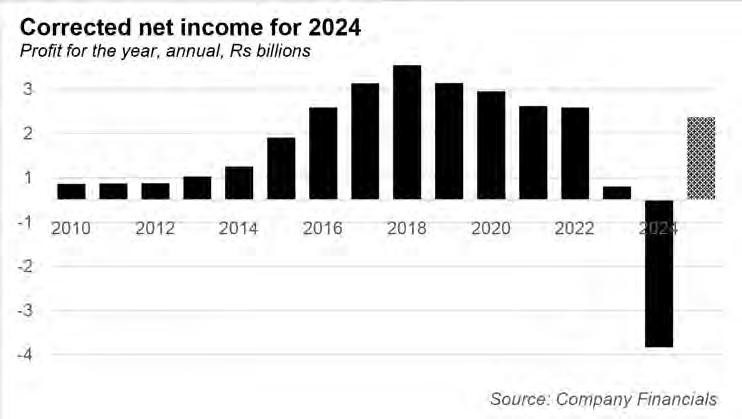

These results take into account 2023 as the last year where Searle actually saw its financial performance deteriorate. In 2023, the company saw their revenues increase from Rs 18 billion to Rs 22 billion, however, the gross margin fell from 49% in 2022 to 30% in 2023. This was also seen in the operating margin which fell from 24% to 17.4% in 2023. Lastly, the net margin almost became non-existent from 11.8% to 1.4%.

The share price performance of Searle seems to be taking into account the deteriorating performance of the company. From 2021 to 2023, the profitability of Searle worsened as the internal controls of the company were not able to maintain the margins. The market saw the share price decrease due to this development. In January of 2017, the share price was trading at Rs 732 which had fallen to Rs 40 by June of 2023.

Nuanced understanding of 2024

In comparison to 2023, a quick glance of the end of 2024 financials shows that Searle made a loss of Rs 3.3 billion which had only been a small profit of Rs 30 crores in 2023. Based on this alone, it might seem like that the bottom had fallen out of the company as it saw its profits turn into gigantic losses. It is only revealed after carrying out a line by line analysis which shows that actually the company had a better year compared to 2023.

In terms of revenues, Searle saw its revenues increase from Rs 21.6 billion to Rs 25.8 billion which was a jump of 19%. This increase was seen in the gross profit as well as the margin increased from 30% to 48.6%. Going further down the income statement, it is seen that the operating profit went from Rs 40 crores to a loss of Rs 4.5 billion. This was mimicked by the operating margin which fell from 17% to -3.5%. Lastly, net profit went from a profit of Rs 30 crores to a loss of Rs 3.3 billion. The net margin fell from 1.4% to -12.9% in 2024. Was this because of the company not being able to control its losses? Well, not exactly. What happened in 2024 was that Searle decided to sell one of its subsidiaries called Searle Pakistan. In a meeting held in May of 2024, the board approved the sale of its shareholding in Searle Pakistan to Ijara Capital Partners Limited and Noventa Pharma (Private) Limited. Once the approval was given, the terms of the sale had to be approved after regulatory approvals had been obtained. Subsequently, the Competition Commission of Pakistan gave their approval for the sale to go ahead.

The first impact of this sale was that Searle had to write down their investment in the subsidiary. In 2023, the investment in Searle Pakistan was valued at around Rs 16.4

billion. This was the amount that Searle had invested and valued it at that amount. Once the negotiations started, it became apparent that Searle would not be able to fetch the same amount from the acquirers. As the value realized would be lower, the cost of investment had to reflect that which meant that a loss of Rs 5.2 billion was being recorded in the accounts.

Due to this impairment, the operating profit ended up being a loss of Rs 4.5 billion which would otherwise have been an operating profit of Rs 72 crores. Nearly double to what it was last year. Similarly, net income would have been a profit of Rs 1.9 billion rather than a loss of Rs 3.3 billion which was recorded. This would have been 6 times more than the net income earned in 2023.

What this analysis shows is that the company has strong fundamentals at its core which have shown an improvement over the year. Much of this improvement has been masked by the impairment loss that the company has suffered caused by the sale of its subsidiary. The sudden shock in 2024 is

significant, however, once this loss and asset are removed from the books, the company has fundamental strength in the business itself.

The real amount of loss cannot be realized till the sale actually goes through and until that takes place, the financials will have to be studied with a caveat. Once the loss of Rs 5.2 billion was realized in 2024, the company showed a further loss of Rs 1 billion in the half year ending in December 2024 as well. Searle made similar sales in both the periods ending December 2023 and December 2024, however, they showed a loss of Rs 4 crores in December 2024 which had been a profit of Rs 22 crores in December 2023.

Once the impairment loss of Rs 1 billion is added back, operating profit increases to Rs 2.4 billion compared to Rs 2.2 billion last year. Net income increases to a profit of Rs 96 crores which had only been Rs 22 crores last year. This loss will only be finalized once the deal goes through. There is also a likelihood that this impairment can be reversed if Searle ends up getting a better deal.