Hatton National Bank withdraws bid for Bank Alfalah’s Bangladesh

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

Is

it still a timegoodto open Padela Court?

Despite the rising number of padel courts opening around the country, it may be a while before the supply of courts outruns the demand

By Nisma Riaz

Two years ago, the rhythm of urban leisure was predictable and comfortable. After long work days or during slow weekends, the routine was familiar: returning home, shedding the day’s fatigue, and settling into your sofas or at the nearest chai dhaba. Today, that landscape has dramatically shifted. The city pulses with a new energy, where every spare moment is now a potential opportunity to play padel. Dinner is no longer a leisurely affair, but a rushed prelude to padel bookings. Conversations have transformed from idle chat to passionate discussions about court availability, playing techniques, and the next tournament. Where once we sought comfort, we now chase the adrenaline of a fast-paced game, our social calendars revolving around the unmistakable bounce of a padel ball.

When padel first arrived in Pakistan, it was an exciting novelty, drawing fitness enthusiasts, former tennis and squash players, and social sports fans alike. Fast forward a year, and the market has transformed into a high-growth industry with investors pouring in money, courts appearing in every major city, and competition reaching new heights. But within this rapid expansion, hides a critical question: is it still a profitable business to open a padel court today?

Is the Investment Worth It?

It is not cheap to make a padel court. In fact, it is quite expensive to build a padel court, especially if you want a world class turf and don’t cut corners.

Last year Profit did a feature on padel tennis, the world’s fastest growing sport, and learnt that it requires around Rs 15

million to build a padel court that meets international standards. Considering this figure, even if one was to make a subpar court, the investment would be sizable.

Yousuf Ghaznavi, CMO of Legends Arena, highlighted, “We construct padel courts ourselves, since TS Builders, the parent company of Legends, are a certified sports construction company, so our investment is lower than standard market costs. We currently have nine paddle courts, and since we focus on high-end builds, each one typically costs between 8 to 9 million rupees.”

But are the returns on this investment (ROI) as significant?

For the early entrants, the answer is a resounding yes. When Legends Arena first opened its courts, it charged Rs 4,000 to 6,500 per hour. With an average court booking of 6-8 hours per day, early investors quickly recouped their investments. Now the hourly rate is around Rs 8000 across most padel courts in Karachi, with the majority of them booked around the clock.

Ghaznavi confirms this success, “We reinvested most of our earnings because we see long-term growth in padel. The demand has been consistent, and our premium experience ensures customers return.”

For newer entrants, however, the ROI is becoming trickier. With increased competition, pricing wars have begun, forcing some courts to lower rates. The key to success now lies in differentiation; offering better facilities, prime locations, or strategic partnerships to maintain a steady revenue stream.

This is evident in some new facilities, like Padelverse in Karachi. They have built Karachi’s first and biggest indoor padel club in a huge warehouse in Korangi.

Safinah Danish Elahi, cofounder of Padelverse, told Profit, “My cofounder Jaffar Hashim originally had the idea for an innovative padel court. With 11 years at P&G and two years in the Philippines, he was exposed to the sport at a more advanced stage. Upon returning, he introduced the idea, and given our shared background in sports and long-standing friendship, we decided to pursue it.”

She divulged that the duo spent six months searching for the right location, considering several sites in Karachi before settling on their current space. “Initially, we planned for a smaller setup, but recognising the potential, we expanded to a fully air-conditioned, temperature-controlled facility with seven courts, a social zone, and Evergreen café.”

Paddle is the fastest-growing sport globally, surpassing squash and even tennis in some regions. Inspired by international models, particularly indoor warehouse-style clubs in Dubai, the founders of Pdelverse wanted to introduce this advanced concept in Pakistan.

“The challenge with outdoor courts was extreme heat, limiting playtime. Our indoor facility solved this, making paddle accessible throughout the day,” Jaffer Hashim, cofounder of Padelverse, shared.

Even though the owners politely declined to share the total investment that went into Padelverse, we estimate the investment to be around Rs 80 to 90 million for the fully air conditioned seven court facility.

Some concerns about the location of Padelverse were raised, considering that even though it is located 10 minutes away from DHA, the Korangi site is a low income area with a supposed security risk.

Elahi countered, stating that, “Initially, the location in Korangi did create some hesitation, with people waiting for others to visit first before deciding to come. However, over time, this concern faded. Now, in our third month, footfall is strong, and the location is no longer a deterrent for regular visitors.”

Continuing, she added, “First, while Korangi is large, our facility is right at its edge, making it easily accessible, just a 10-minute drive from DHA. Second, the club is inside a gated community with multiple security checkpoints, ensuring a safe and controlled environment. Lastly, the ambiance we’ve created is welcoming and family-friendly, with social spaces, kids playing areas, and a well-known café attracting a diverse crowd. Bringing female players to the venue required effort, but through social media, word-of-mouth, and active participation in the paddle community, more women started visiting. Hosting major tournaments with hundreds of attendees further normalised the location. Today, even late-night slots are in high demand, and players, including families, feel safe.”

It is still too soon to estimate their ROI since it has been less than three months to its launch. However, with expansion plans already in motion, our assumption is that the returns are attractive. “The return on investment (ROI) has exceeded expectations. When launching the facility, projections were made based on anticipated interest, and so far, demand has been higher than expected, especially during Ramadan,” Elahi stated.

While there are cheaper and even free padel court options in parks and residential compounds, the appeal of padel lies in its social nature and the overall playing experience. A well-designed facility enhances that experience, making it a key factor in attracting and retaining players.

Beyond these major players with investments ranging from Rs 100 million to Rs 400 million, several smaller contenders are entering the padel market, aiming to establish themselves with more modest investments of Rs 20 million to Rs 50 million.

Padel Park, a smaller facility compared to Legends and Padelverse, opened in Lahore in July last year with two padel courts. As one of the first three padel facilities in the city, it set itself apart with a cozy sitting area and a welcoming ambiance.

According to co-founder Saad Mujeeb, the two-court setup required an investment of approximately Rs 20 million. With the market booming, Padel Park quickly became one of Lahore’s top-performing courts, achieving a payback period of less than a year, far exceeding initial expectations of 1 to 1.5 years.

The legacy of Legends

As we see this new sport take the country by storm, it is no secret that more investment will be poured into padel courts. Everyone wants a piece of this cake while it’s still fresh.

The question is; is the cake still fresh?

Being the first to establish itself in the commercial padel market gave Legends a clear advantage. Early brand recognition, customer loyalty, and a premium reputation have solidified its standing despite the influx of new competitors.

Ghaznavi agrees, “Yes, Legends certainly benefits from an early entrant advantage. Beyond just offering paddle courts, we have prioritised exceptional client service, fostering strong relationships that ensure high retention. Our focus on customer experience, how we engage with and take care of our clients, has been a key factor in our sustained success.”

Not to forget, its ambiance and social atmosphere sets Legends apart. It’s more than just a sports facility; it’s a social hub where people from similar backgrounds come together, making it a preferred gathering spot. “Our spacious setup allows us to accommodate more visitors comfortably, and even when there’s a wait, guests enjoy the overall environment and various other activities available.”

Unlike venues that offer just one activity, Legends provides a well-rounded experience, which keeps people coming back. The combination of high-quality service, strong community ties, and a dynamic social setting makes Legends a standout destination, reinforcing its early mover advantage in the industry.

“We offer an entire experience, not just padel,” said Ghaznavi. “That’s why they’re willing to pay higher rates here instead of going to cheaper alternatives.”

Legends’ ability to expand beyond its flagship location is another key differentiator. Smaller competitors are still adding courts at the same site, while Legends is opening entire new branches, cementing its dominance in the market.

Is There Still Room for Growth?

The Legends Arena introduced padel to Pakistan when they built the first commercial padel courts in the country in 2023.

Exactly a year ago, in conversation with Profit, the CEO of Legends Arena Talal Shah Khan said, “The city requires about 15 or 16 similar facilities to meet the needs of the large population.”

Fast forward a year later, the city may not have seen any other sports arenas matching the scale of Legends pop up.

Today, 20 months since Legends opened its doors to the public, Karachi alone houses over a 100 courts. The market has expanded at an unprecedented rate, perhaps even faster than we had predicted last year.

Documenting the rise of padel is one aspect, while another important consideration is the question whether the supply of padel courts is close to outstripping its demand.

Ghaznavi argues that saturation isn’t a concern yet. “The sport is growing as fast as the courts. Every day, new players are discovering padel. So while competition is high, demand is still strong.”

He shared how Legends has expanded over the last 20 months and manages to build and operate more courts across the city, without having to build massive arenas, “We operate sports facilities under a franchise-like model, managing operations, marketing, and overall management while investors provide the funding.”

Unlike smaller competitors focused solely on adding courts, Legends has taken a strategic approach to expansion through partnerships, introducing the Cross Court and Padel Up by Legends. Ghaznavi shared, “As we started out, we had just two courts, then added a third. When we spoke last year, we were in the process of constructing our fourth and fifth courts. After that, we introduced two championship courts, bringing our total to seven. Just last month, we expanded again, adding two more, so now we have nine courts at this location alone.”

Across all locations, Legends currently operates 20 courts. That includes the nine at Legends, plus several other key sites, including Cross Court, which has three courts, Jahangir Khan Club has two, Paddle Up has two and HMR has two.

Ghaznavi added, “We just opened two new courts in Islamabad last Sunday. And we’re not stopping there. We’re now expanding beyond Karachi, heading to Hyderabad, and have already locked in a deal with DHA Lahore.”

This innovative approach allows inves-

tors to fund new courts while Legends handles operations, branding, and marketing, ensuring a premium playing experience.

Currently managing 20 courts across six locations in Karachi and Islamabad, Legends continues to set itself apart. More than just increasing court numbers, the brand is dedicated to fostering a thriving padel community through tournaments, corporate events, and academies, cementing its position as a leader in the sport’s growth.

“Our business strategy revolves around reinvesting most of our earnings because we see significant future potential in sports. The sports industry continues to grow, with new players constantly emerging. Paddle, for instance, has skyrocketed in popularity, with Karachi alone seeing 100 new courts in just 20 months,” he added.

Ghaznavi explained how TS Builders specialise in sports construction and receive multiple inquiries daily about building paddle courts. “We don’t view other court owners as competitors but as clients, contributing to the sport’s expansion. Initially, we had just two courts, but as demand grew, we expanded. Given Karachi’s vast population, it’s unrealistic for everyone to play at Legends, so more courts in different locations help the sport thrive.”

According to Ghaznavi, the market isn’t becoming saturated; instead, it’s growing. More courts mean more accessibility, bringing in new players. “This benefits our construction business, TS Builders, as every new court project becomes another business opportunity.”

Agreeing with this assertion, Elahi said, “With just two and a half months into operations, our expansion plans are already in motion and we have announced Wasim Akram as a partner. While still in the early stages, the goal is to develop a scalable model that can be implemented in Karachi, other cities in Pakistan, or even internationally.”

Regarding market strategy, Hashim added that there are two approaches: competing for existing players or growing the overall player base. “Given Pakistan’s current padel landscape, the latter is the focus. While many new courts have opened, demand still exceeds supply, with booking slots often unavailable. The increasing number of amateur and beginner players indicates strong growth potential too.”

To stand out, the founders prioritised differentiation, investing in a fully indoor facility. This ensures a unique offering, particularly in extreme weather conditions, where their courts remain the only viable option for daytime play. This model would be extremely successful in cities like Lahore and Islamabad since they experience extremely hot summers.

Similarly, Mujeeb shared that Padel Park is also expanding and adding three additional courts soon bringing the total number of their

padel courts to five. Mujeeb acknowledges that the market in Lahore is becoming increasingly saturated, with growing competition, especially when the market in Lahore is not as big as that of Karachi, yet. The land adjacent to Padel Park has been acquired by others to open similar facilities. While these new courts may not match Padel Park in quality, they have aggressively lowered their prices to compete.

We learnt that the market has not been saturated yet but it is evolving. As more courts are built, the number of players is also increasing, which helps balance the high demand. According to Ghaznavi, the trend suggests saturation could happen eventually, but for now, the market continues to grow.

However, with five courts opening every month in Karachi alone, the industry may reach a tipping point soon. Investors must now be more strategic, choosing prime locations, targeting new demographics, and offering unique services to stand out or risk being yet another unkempt padel court that is one’s last resort when better courts are at full occupancy.

Has Demand Kept Up with Supply?

Well, to answer the question simply, yes. The demand for a free padel slot is as high as it has ever been.

Even with the increasing number of courts, finding available slots remains a challenge, especially during peak hours. Many people are still struggling to secure their preferred time slots, indicating that demand is outpacing supply. While more courts provide additional options, prime-time slots are consistently booked, reinforcing the sport’s sustained popularity.

Despite this, the present demand has impacted the price of playing padel.

While slashing rates to compete is not as evident in Karachi, some courts in Lahore are resorting to competitive pricing.

Mujeeb highlights, “Lahore’s market dynamics differ from Karachi’s. Club Padel, for instance, initially charged Rs 7,000 per session but lacked enough courts to accommodate the surge in players. Now, they offer hourly slots at Rs 5,000, yet still have some vacancies. In contrast, Karachi’s larger market sees demand consistently outpacing supply.”

Another strategy has been to increase market size, encouraging casual players to play more often through discounts and deals. Many facilities now offer membership bundles and loyalty programs to boost frequency among existing customers.

To strengthen its position, Padel Park has leveraged WhatsApp for community building, using group chats to foster engagement among players. Additionally, they have

introduced padel coaching to attract beginners and expand their customer base.

Padel Park has also driven growth through strategic partnerships and events, including collaborations with Endeavor and other tournaments. Their latest partnership with Kickstart further strengthens their outreach.

Bank deals and discounts are a popular strategy to keep up with the growing supply, without having to slash hourly slot rates.

Padel Park offers a 15% discount through Bank Alfalah, which also supports their marketing efforts. A partnership with Bank of Punjab is set to go live after Eid, providing discounts ranging from 30% to 50%, with costs shared between the bank and Padel Park.

To explain the growing size of the market for padel, Ghaznavi explained, “Before Legends’ Padel Academy, we had a tennis academy. But as players grew in padel and awareness spread, parents moved their kids from tennis to battle. Now, in just a year, our battle academy is bigger than the tennis academy. We haven’t really gone out of our way to push it. No heavy ads, no extra effort. In the last 20 months, I’ve spent maybe Rs 300,000 rupees on ads, which is nothing.”

At Legends, occupancy rates remain high, with courts booked until late at night. The facility operates 22 hours a day, with some slots extending to 3-5 a.m. on weekends. Even with the rise in competition, premium facilities maintain their appeal.

“When games are spread across nine courts instead of seven or five, they finish earlier, around 3 a.m. instead of 5 a.m. However, on weekends, play can last until 5 a.m. Courts rarely remain empty, as 95–97% of slots are pre-booked. Players prefer Legends as their first choice, and its courts tend to be fully occupied before others,” Ghaznavi shared, indicating that the occupancy has remained high despite increasing options.

With the influx of new courts, pricing has become a major battleground. While Legends Arena has maintained premium rates due to its brand positioning, many newer courts have had to slash prices to attract customers. In some areas, hourly rates have dropped from Rs 7,000-8,000 to Rs 4,000-5,000.

To combat this, Legends has leveraged strategic partnerships with banks, offering discounts and loyalty programs to retain high-value customers. Ghaznavi noted, “Through bank collaborations, we offer discounts that make us competitive, even with lower-end courts. People prefer quality and are willing to pay a bit more for a superior experience.”

Some players may choose cheaper alternatives, but serious paddle players prioritise quality. Smaller facilities often lack top-tier courts, making a world-class facility more appealing. Long-time customers continue to book

courts at Legends, showing that price isn’t the main factor, experience matters more. Many are willing to pay Rs 2,000 extra for a better experience, as the price reflects the quality they receive.

Supporting a similar argument, Hashim also detailed, “ The pricing strategy for Padelverse’s indoor facility aligns with other multi-sport, multi-court clubs in Karachi, despite the significantly higher overhead costs. While initially considering a premium pricing model due to the high expenses associated with an air-conditioned indoor venue, the goal of making padel more accessible led to a competitive price structure. The facility ensures affordability by securing substantial bank discounts, with partnerships that offer up to 50% off, bringing peak-hour rates down to Rs 4,000 per hour.”

They argue that the value proposition extends beyond just pricing. Players benefit from a top-tier facility featuring well-maintained courts, temperature control, and a clean, secure environment, enhancing the overall playing experience. Maintaining an indoor club requires significant investment, particularly in electricity costs, court upkeep, and providing additional services like ball boys, which are a standard offering in Karachi.

“Despite perceptions that indoor venues cater to an elite clientele, the pricing is comparable to outdoor clubs, some of which have higher base rates, especially during peak hours. Unlike a high-end club in Lahore that charges Rs 12,000 for a 1.5-hour slot without ball boys, Padelverse offers a premium experience at a lower price. By balancing affordability with top-class service, the club successfully attracts a broad audience while sustaining a viable business model.” Hashim concluded.

Lower-tier courts in less prime locations have begun experiencing vacant slots, particularly on weekdays. While weekend demand remains strong, weekday afternoons and late nights see fewer bookings. This trend suggests that while padel’s popularity is rising, investors need to consider location and customer convenience carefully.

Paddling into the future

Padel’s future in Pakistan depends on whether it can move beyond being a passing craze and establish itself as a sustainable business. The market is currently divided between two types of investors, established players like Legends, who prioritise quality, customer experience, and longterm viability, and smaller investors looking for quick returns, which has led to inconsistent court quality and the risk of oversaturation. While countries like Spain and Dubai have

sustained padel as a dominant sport for years, its success in Pakistan will rely on accessibility and affordability. If prices remain high, it may remain exclusive to the elite, but if facilities become more affordable, the sport could see widespread adoption, ensuring its longevity.

Beyond its business potential, padel’s biggest strength lies in its social and community-driven nature. Unlike individual sports such as squash, padel is played in doubles, fostering engagement, networking, and a sense of belonging. Legends has capitalised on this by hosting corporate events, academies, and social tournaments to grow a strong player base. “We recently hosted a YPO (Young Professional Organization) event, bringing together top entrepreneurs and executives for a padel tournament,” says Ghaznavi. “It’s not just about sports, it’s about building a culture.” By partnering with schools, universities, and corporations, Legends is ensuring that padel doesn’t just remain a short-term trend but becomes a long-term fixture in Pakistan’s sports landscape.

Similarly, other padel courts are also engaging in partnerships, as well as corporate events. Elahi shared, ““We’re actively organising tournaments, which are sponsored by multiple brands. In addition to that, we’re hosting various events, like the District 19 event that happened recently.”

People are booking our courts for birthday parties, corporate gatherings, and mini tournaments. Padelverse also shared that they are planning pop-ups at their tournaments, giving sponsors an opportunity for visibility, whether through point-of-sale setups or general brand awareness. “So overall, we’re engaged in a mix of competitive and social events, creating a dynamic experience for both players and partners,” Elahi concluded.

For investors considering entering the market now, the opportunity is still there— but the approach must evolve. Simply setting up a court is no longer enough. Success will depend on location, differentiation, and a strong long-term strategy. Established players, with their brand loyalty, premium facilities, and strategic expansion, are well-positioned for continued growth. However, new entrants must take a more calculated approach, focusing either on high-quality experiences or competitive pricing to survive in a rapidly growing and increasingly competitive market.

As Ghaznavi puts it, “It’s not too late to enter, but it’s not as easy as it was a year ago. Investors must innovate. Those who do will succeed; those who don’t will struggle.”

In the end, padel’s boom in Pakistan is far from over, but its future will be shaped by those who adapt, innovate, and build beyond the hype. The smartest players, both on and off the court, will be the ones who truly win. n

By Farooq Tirmizi

The hardest thing to predict in global politics is what Donald Trump will do next. So it is entirely possible that by the time you read these sentences, Donald Trump may have reversed a substantial portion of his newly announced tariff policy on global trade with the United States (we think it is more likely that he will keep the policy, but who knows?)

Even if he does walk back some of the more extreme measures on tariff policy, one thing is for certain: the world that America has built over the past 80 years is gone, largely because America has lost the appetite to keep it going.

The Tariff Bomb shell

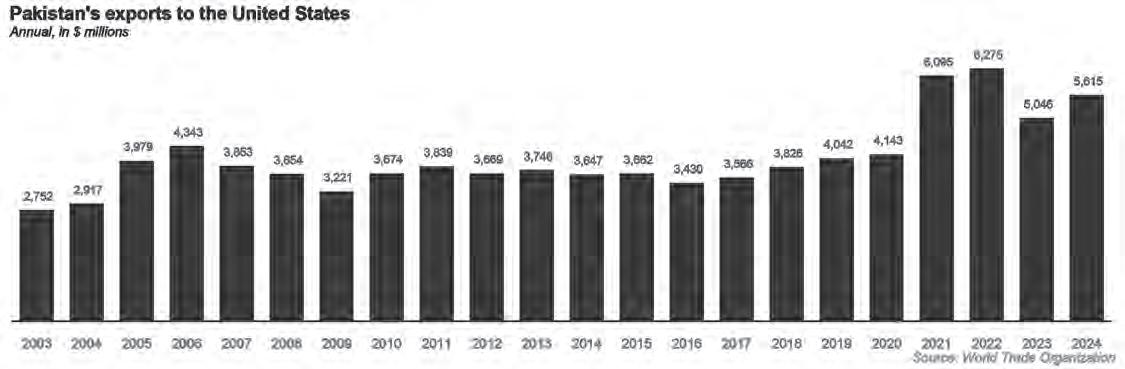

At the most basic level, this could be a story about the 18% of Paki-

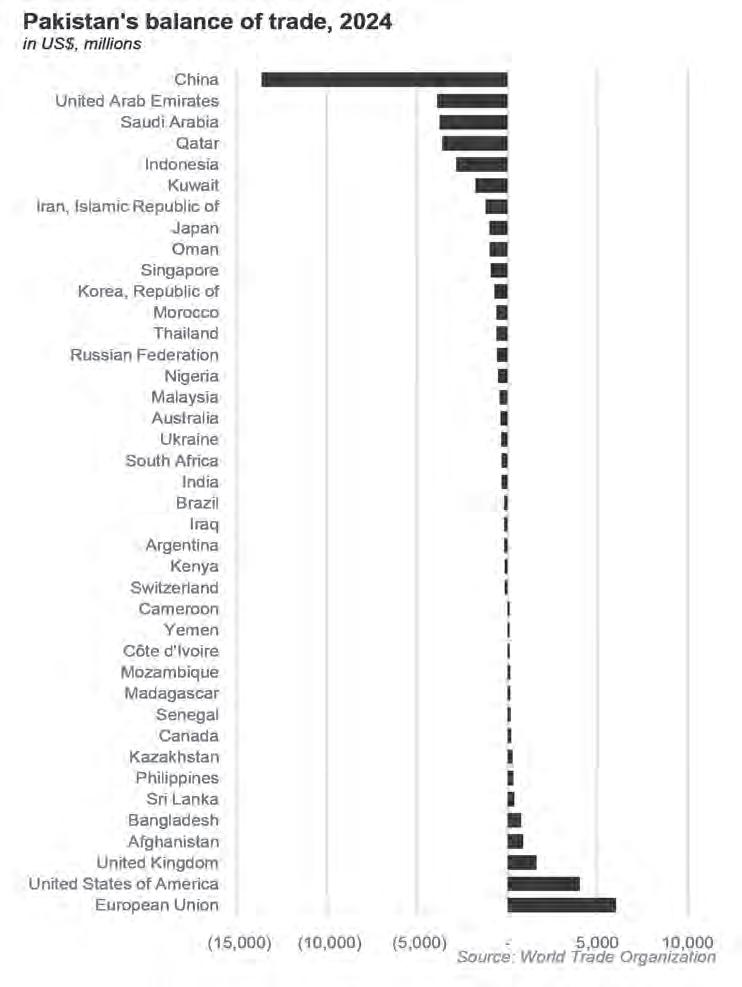

stan’s exports – about $5 billion a year – that go to the United States, and what is likely to happen to them now that the United States government has imposed a 29% tariff on them. But that would be too simplistic a story.

This is about more than tariffs, after all. It is about a whole institutional architecture that governed the world order as we have known it for almost a century, and that architecture is well and truly gone. Pax Americana is over, and while most readers of this magazine may fancy themselves anti-imperialists who will bid it good riddance, we can assure you that you will like what comes next a lot less.

This is a story of trying to unravel what comes next. But before we do that, we will examine what America built, why they built it, why they no longer want to maintain it, and what comes next for Pakistan. At the end of this story, we hope you will understand just how dependent the whole world – not just Pakistan – has been on the United States to maintain the basic structure of how the world works. Once the Americans start pulling back, every country in the world will start to see themselves vulnerable to shocks in ways they have no living memory of anymore.

This is a story about a lot more than the tariffs from America. It is about our ability to export at all, our ability to import anything we need, even the ability of Pakistani expats to earn money abroad.

But while it is a story of vulnerabilities, it is not a story of doom. If the world is going to come crashing down, you would much rather watch it happen from Pakistan than most other countries on the planet. Because the end of the American Empire can be survived, and Pakistan may be one of the handful of countries in the world that is positioned to be able to weather the coming storm. To understand what comes next, however, you first need to understand what existed until just a few years ago, and why it is about to disappear.

From the Confident American to the Anxious American

Almost exactly 80 years ago, on April 12, 1945, Harry S Truman became President of the United States after Franklin Delano Roosevelt died in office just months before World War II ended. Truman would go on to preside over the end of the war, and the order that was to come after it, and as such, was probably the most pow-

erful man in human history because he led the most powerful empire the world has ever seen at the absolute apex of its power.

At the end of the war, America was not just a victor, it was absolutely dominant. America had not just won the war, it had proved its superior might in every single way. While its enemies would ration food to fend off the spectre of starvation, the United States Navy built a special ship that could manufacture and supply fresh ice cream to its fighting men in the Pacific Ocean in the middle of the war.

Yes, you read that correctly. The Americans had so dominant an advantage in terms of resources that the literally built an ice cream ship for a war zone. Because why not?

In 1945, America was not just the victor, it was richer and more powerful than the rest of the world combined. Its Air Force was larger than all other air forces put together. Its Army was better equipped, and it had more money than the rest of the world put together, plus another 50%. No empire in human history has been that dominant. But unlikely any other empire in human history, America was a nation governed by the rule of law. The man who presided over that empire at its peak – Harry Truman – did not cling on to power after his term was up, but left office in accordance with the law. What makes this even more extraordinary is that Truman was reliant on just a junior Army officer’s pension for his income, and was once so desperate for money that he asked the foreman of a construction site in his home town for a job only a few years after having been the most powerful person in history.

And unlike any other empire, America chose in that moment not just to not abuse that power, but to actively share it. The world had been shattered by war so it built the World Bank to help finance reconstruction. The world had previously engaged in beggar-thy-neighbour currency warfare, so it created the International Monetary Fund to help stabilize cross-border movement of money. The world had no standing markets left, so America opened up its markets to the world so that people could try to earn the

money to pay America back and build up their countries again.

Whereas previous empires used their relative might to crush their rivals, America was so completely dominant and unscathed in a world so thoroughly shattered by war, it could afford something no other dominant power had previously been able to afford: magnanimity.

And America did one other thing that largely goes unnoticed, but is just as important: it deployed its navy to patrol the entire world’s oceans so that all countries in the world could trade with each other. Why do this? Because if countries could reliably trade with each other, they would no longer need to go to war to gain control over the resources that they needed.

This was the era of the Confident American. The US was not threatened by anybody and so could afford to not be burdened by insecurities. They sat down and examined the causes of both world wars and actively sought to create a world where such massive global conflict would not happen again. The system had many flaws, but for the past 80 years, they have succeeded in preventing another world war from erupting. That success was possible because the American defined their national interest in a broader way than simply being able to control what they wanted. They defined it as living in a world where America’s prosperity and security was not a walled garden but part of a widely shared prosperity so that more of the world could live in peace, and there would be less temptation to go to war. The Confident American who built that world is now gone. Probably forever. What has come in its place is the Anxious American, someone who is much more insecure about his place in the world, and faces much more competition from countries that are much closer in national power to the United States than its more recent rivals.

While Donald Trump is the most raw expression of that insecurity, even members of the opposition party in the Unites States have expressed scepticism about the value of engaging with the rest of the world for the US, and have expressed a comfort with pulling back

from America’s military commitments and trade relationships.

Why the shift? Because this is a generation of Americans who have watched the relentless rise of China, and the hollowing out of American domestic manufacturing capability and decided that the status quo cannot continue. The United States is getting older, more indebted, and needs to make choices about where it can deploy its economic and military might rather than assuming it can remain the dominant global power indefinitely.

The most extreme of Trump’s tariff measures may be scaled back, but the larger move away from the post-1945 world order is not going anywhere. Americans do not want their market to be open for the world world, and the absolutely do not want to be reliant on imports of manufactured products from other parts of the world. And they do not have a desire to send their Army to defend Europe, or their Navy to defend the global sea lanes.

That has massive implications for every country around the world, including Pakistan.

A world without open seas

Embedded inside every theory you have ever read about import substitutions versus export-led growth or any other theory of global economics is the assumption that if a ship gets loaded at a port in one part of the world, most of the time, it will reliably arrive at its destination without incident. Underpinning that assumption is the fact that the United States Navy patrols literally every single ocean on the planet and has a military base on at least one side of every major choke point on the world’s oceans.

And the United States Navy keeps the sea lanes open not just for ships serving the American economy, but all countries in the world, including its most bitter rivals.

As the US scales back its commitments around the world, this assumption will rapidly not hold true anymore, which means that it

will no longer be possible to assume that trade between any two countries is possible without first examining what route across the seas it would need to take, and if there are pirates or other threat along the way.

No open seas, no remittances

Of course, the United States may be run by the Anxious American, but it remains a very powerful country, so it goes without saying that where American interests are directly threatened, expect a quick American response. But where America has previously treated the interests of its allies as those of itself, the US is likely to define national interest much more narrowly than in periods past.

What does this mean for Pakistan? Most directly, what it means is that there may be a hit to remittances from expatriate Pakistanis. How, you might be wondering. Here is how this works: the vast majority of Pakistani expats work in Saudi Arabia or the United Arab Emirates. While those economies are diversifying, they are still largely dependent on oil exports, and contrary to common perception, the vast majority of that oil does not go to the United States anymore. Since 2018, the largest destination for Saudi and Emirati oil has been China.

What are the odds that the United States will continue to deploy its military to defend the energy supplies to its biggest economic and political rival? And the Saudis and Emiratis are able to sell less oil because more of their ships get capture or blown up by Yemeni pirates, what is likely to happen to the number of Pakistani expat workers – and therefore expat remittances – from those countries to Pakistan?

This is one of the many examples of significant downstream effects of American withdrawal from its hegemonic stabilization role: dependencies that other countries have on US military strength will get exposed and fixed, sometimes in odd ways.

But of course, beyond the remittances, there is the tariffs themselves, and their potential impact on Pakistan’s trade balance.

Who gets affected by the tariffs? And how much?

While Pakistan is not particularly important to the United States, the US is a very important economic relationship for Pakistan. Despite accounting for just 0.16% of total U.S. imports, the American market holds outsize significance for Pakistan’s export economy, serving as its single largest export destination with an annual volume of around $6 billion

— roughly 18% of Pakistan’s total exports.

Many Pakistani analysts have been examining the tariffs placed on Pakistani exports in the context of how high the tariffs are on countries that compete in the same export sectors. There is certainly at least some value to measuring that number. However, one important way to think about the potential impact on global trade from these tariffs is to consider not just whether they will shift demand away from Vietnam and towards Pakistan, but rather to ask what will be the absolute level of tariff impact. If history is any guide, the results could be quite catastrophic.

One of the reasons why there has been such a strong consensus in favour of free trade in the post-World War II era was that the Great Depression around the world was widely believed to have aggravated by the Smoot-Hawley tariffs imposed by the United States in 1930, as a means of both raising revenue and protecting

domestic US industry.

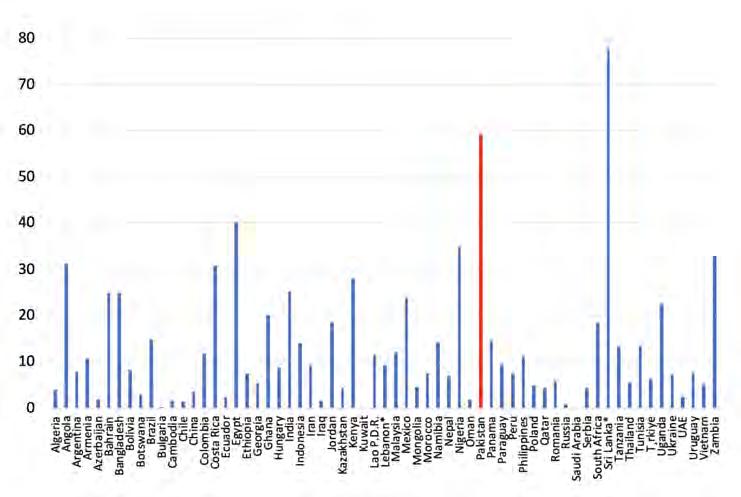

When the Smoot-Hawley tariffs were imposed in 1930, international trade dropped by 60% within 12 months. The Smoot-Hawley tariffs were set at 20%. The Trump tariffs are around 27%, based on analysis by JPMorgan, an investment bank.

The tariffs, in other words, will not just shift demand in the United States for Pakistani products. They will end it.

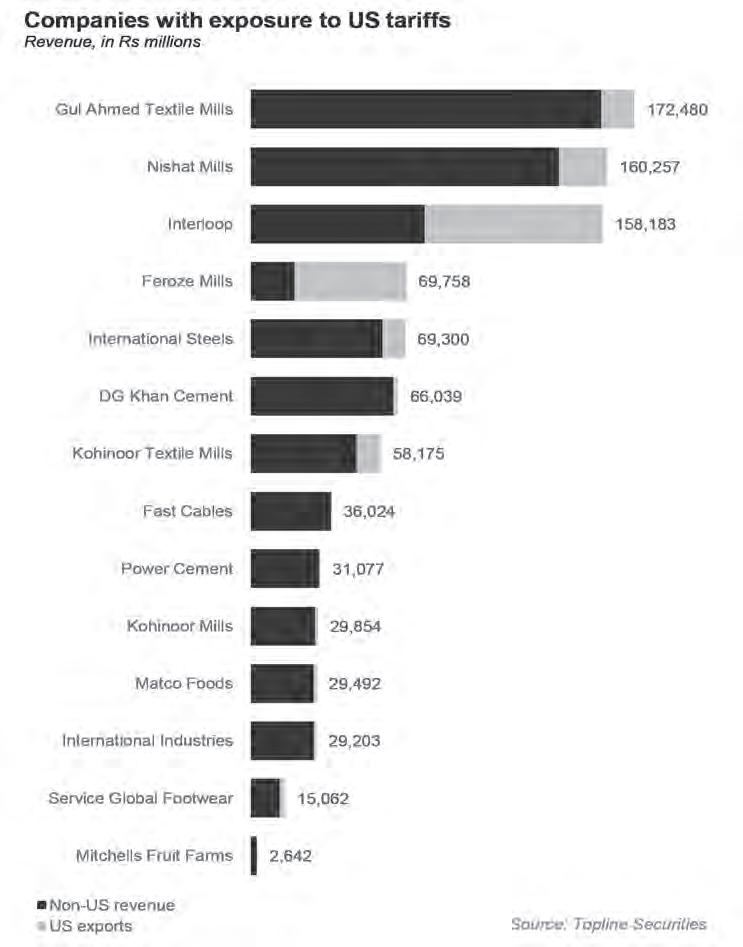

So who in Pakistan is particularly exposed to US tariffs on imports from Pakistan? Primarily textile exporters, since about 87% of Pakistan’s exports to the United States are textiles and related products, according to an analysis of trade data conducted by Topline Securities, an investment bank based in Karachi. And it is not just going to the United States where this measure will have effect. As Chinese, Vietnamese, and Bangladeshi exporters seek alternatives to the U.S. due to higher tariffs,

they may pivot toward Europe — intensifying pressure on Pakistani exporters and potentially squeezing margins. As for which companies are most directly affect by the tariff, by far the most directly impacted company will be the stock market darling, Interloop, which gets over 51% of its revenue from the United States. That revenue may not disappear overnight, but is likely to be diminished significantly unless the tariff measure is at least partially reversed. That is still not as bad as Feroze Mills, which derives 72% of its revenue from the United States.

As these giants look to make headway in markets other than the US, that is likely to have a downstream impact on other textile companies that are already present in those markets, creating downward pressure on prices, and squeezing margins for the industry as a whole.

Curiously, however, there appears to have been no move towards restricting imports of services by the United States, which means software houses such as Systems Ltd and Pakistan’s large and growing freelance software and outsourced business services providers are likely to see minimal disruption. It appears that the United States is only opposed to physical goods moving across borders. Bits and bytes are still welcome.

What comes next?

Even now, there are news reports that US President Donald Trump is taking meetings with foreign leaders to strike deals that might lower the tariff rates for each respective country. While some countries, which have competent diplomats and statesmen representing their interests may view this as an opportunity, Pakistan is likely to be represented in this matter by Foreign Minister Ishaq Dar and would be lucky if we came away with the tariffs not increased further.

But even beyond this episode, it is becoming clearer that the US market is at the very least less open for business than it once was, and consequently, other countries are likely to follow suit as well, meaning export markets as a whole are likely to decrease in size.

What does this mean for countries like Pakistan, which have been advised ad nauseum by development consultants to adopt an export-led growth strategy? Well, for starters, it means that less of the export pie is available to Pakistan than was available to the Asian Tigers when they started developing, meaning Pakistan’s economic progress will be slower than theirs. But in circumstances such as this, there are even more pressing concerns: is Pakistan dependent on international trade for material goods without which its economy cannot survive? The answer to that question is yes, though there may be reason to believe that Pakistan’s most necessary imports are unlikely

to be very badly affected by the US Navy ceasing its patrols of the oceans.

Pakistan’s biggest import category by far is fuel, which is mainly imported from Saudi Arabia and the UAE, and essentially only needs to cross from the Persian Gulf through the Straits of Hormuz before it effectively hits Pakistani territorial waters. There is almost no piracy on that route, and unlikely to be any in the near future meaning Pakistan’s energy imports are likely safe from disruption.

Pakistan is also lucky enough to be one of a handful of countries that can – for the most part – produce its own supply of food. Combined with the energy imports, this means that as global trade routes are shutting down, Pakistan is not going to be dependent on far-flung sources for its food, and has relatively secure access to its energy needs.

There is, of course, more to life than food and energy, but these basics being accounted for even in a post-secure trade world is not some-

thing that Pakistanis should take for granted.

What comes after establishing the security of that baseline is harder to quantify, but the most obvious solution to pursue – assuming it ever becomes viable in the short to medium term – would be trying to open up trade with India. Given the disinterest in this in New Delhi, this is not easily achieved, of course, but nonetheless not something Pakistan can afford to give up on, especially now.

Aside from regional trade, the one other thing Pakistan can do is something it is already doing: building out a more robust services export sector.

All of this is tantamount to damage control, but at least it is damage control from a position of relative security. As the world watches its hegemon abandon its leadership role, we look upon a more difficult, slower growing path to prosperity. But at least we are not on the path to penury. Therein lies at least some small mercy. n

Imagine a nation of 250 million people trapped in a cycle of fiscal imprudence: chronically failing to optimize internal resources while periodically embarking on unsustainable spending sprees. The inevitable result? An ever-mounting public debt burden with seemingly no resolution in sight.

This precisely describes Pakistan’s predicament. The country consistently struggles to generate sufficient revenue to overcome its fiscal deficit, while its balance of payments

remains stubbornly negative—unable to attract enough foreign exchange to meet import demands and other external obligations.

The consequences of these structural weaknesses are starkly evident in the Ministry of Finance’s December 2024 debt bulletin. Pakistan’s public debt has reached alarming proportions, creating formidable obstacles to economic stability and growth potential. Even with recent positive developments, including a primary balance surplus of 2.9% for July-December 2024, the overwhelming debt burden continues to severely restrict fiscal space and impede meaningful economic development.

As we delve into the recent figures and composition of Pakistan’s public debt, it’s essential to examine the structural factors that have perpetuated this crisis and evaluate the increasingly limited options available to the country.

Not for the first time

At the heart of Pakistan’s debt crisis lies a fundamental structural weakness: a chronic fiscal imbalance that has persisted for decades. The country’s inability to generate sufficient revenue

to meet its expenditure needs has created a dangerous dependency on debt accumulation simply to remain solvent.

By fiscal year 2019—even before the pandemic’s economic devastation—public debt had swelled to approximately 80% of GDP, representing an astonishing seven times the government’s annual revenue intake. During this pre-pandemic period, government expenditures exceeded revenue by two-thirds, placing Pakistan among the countries with the highest deficits in the emerging market landscape.

This perpetual imbalance has created what economists term “fiscal dominance”—a condition eloquently described by economist Dr. Atif Mian as occurring “when concerns about government debt start ‘dominating’ everything else—like an autoimmune disease that starts attacking the body’s own organs.” The financial system becomes oriented primarily around financing government deficits rather than supporting productive economic activity.

Compounding this precarious situation is a substantial burden of government guarantees and unfunded pension liabilities that, while often overlooked in conventional debt discussions, significantly add to the country’s overall financial obligations.

To fully comprehend the gravity of Pakistan’s current debt predicament, historical context is essential. The problem is not merely cyclical but deeply entrenched and systemic. With each passing year of fiscal imbalance, the debt service burden grows heavier.

By fiscal year 2019, interest payments alone were consuming nearly 40 percent of government revenue—an extraordinary proportion that severely limits the state’s capacity to provide essential public services or

invest in development.

The severity of this situation becomes clearer through international comparison. In his Atlantic Council white paper “Rescuing Pakistan’s Economy,” Aasim M. Husain notes: “Historical patterns from other countries indicate that maintaining a ratio above 25 percent for a prolonged period is uncommon. Indeed, in the decade leading up to the global pandemic, Pakistan was one of only five emerging markets or developing economies, out of a sample of more than sixty countries, that saw this ratio reach or exceed 40 percent.”

Husain further emphasizes that “only one other country ever even reached 30 percent, and only three others went beyond 25 percent during 2010–2019. Thus, international

experience suggests that it is important not to let the interest-revenue ratio rise above 25 percent.” Most alarmingly, following Pakistan’s latest economic crisis and the subsequent escalation in borrowing costs, this ratio has soared to 60 percent—again placing the country as an extreme outlier globally and creating conditions that are “clearly unsustainable, both fiscally and from a social stability perspective.”

Where are we headed?

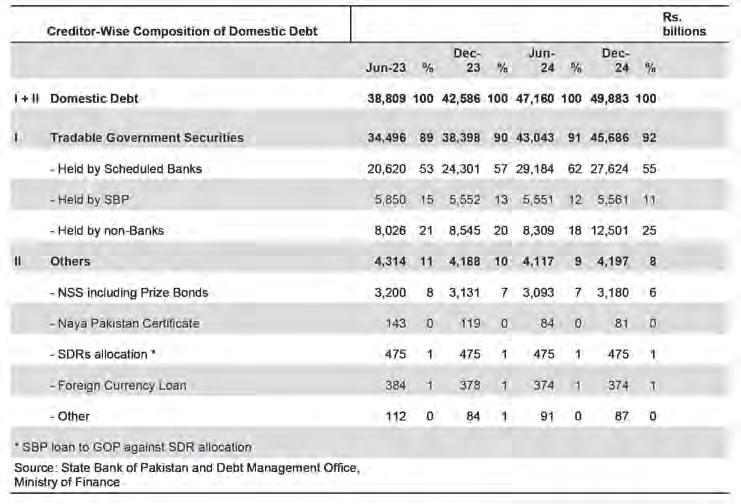

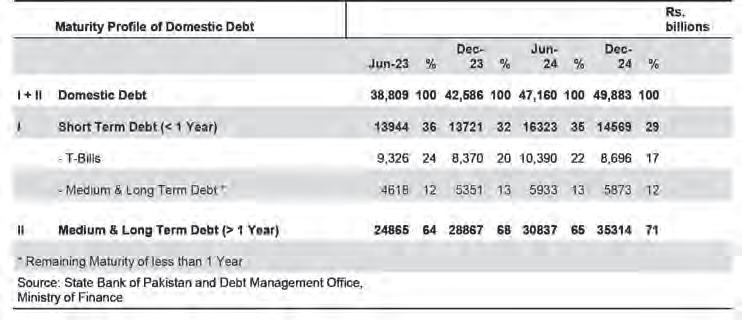

Pakistan’s public debt burden reached Rs.74 trillion by the end of 2024, marking a 10 percent increase from the previous year despite ongoing fiscal consolidation efforts.

Domestic debt constitutes 67% of the total debt, with external debt accounting for the remaining 33%. Domestic debt can be further categorized into three distinct components: permanent debt (instruments with maturity exceeding one year, such as Pakistan Investment Bonds), floating debt (short-term borrowing up to one year through market treasury bills), and unfunded debt (primarily National Savings Schemes instruments).

A significant shift has occurred in the domestic debt ownership structure, as highlighted in the recent bulletin: “The share of scheduled banks in tradeable government securities declined from 62% in June 2024 to 55% by December 2024, while the non-banking sector’s share rose from 18% to 25% during the same period.” Despite this diversification effort, the overall dependence on tradable government securities remains substantial at 92% of total domestic debt. The bulletin notes

Source: Atlantic Council

that “the declining share of banks and rising participation of non-banking institutions reflects the government’s strategic initiative to broaden the debt market, which aims to enhance liquidity and mitigate concentration risks over the long term.”

The maturity profile of Pakistan’s domestic debt also reveals a deliberate and strategic pivot toward medium and long-term borrowing instruments. This shift has significantly reduced the country’s dependence on short-term Treasury Bills, the proportion of which declined substantially from 24% in June 2023 to just 17% by December 2024. Correspondingly, medium and long-term debt instruments grew from 64% to 71% during this same period—an attempt to strengthen debt sustainability by extending duration and substantially mitigating rollover risks.

This restructuring was achieved primarily through the Ministry of Finance’s innovative Buyback and Exchange Program, implemented as a central component of its strategic Liability Management Operations (LMOs) in interbank treasury markets. The initiative led the government to repurchase approximately Rs.1 trillion in treasury securities, generating significant interest servicing savings of Rs.31 billion.

Initiated in the final quarter of 2024, the buyback strategy was precisely timed to capitalize on changing market conditions and reprofile government debt by exchanging higher-cost securities for more affordable alternatives. The targeted T-bills were scheduled to mature within three months and had been issued during a high interest rate environment at yields of approximately 20-21%. When market yields subsequently fell to around 16% in October 2024, the government seized this opportunity to retire these expensive short-term obligations, avoiding the exorbitant interest costs they would have incurred and achieving substantial debt servicing savings while simultaneously improving the overall maturity profile.

What even further elevates the role of the domestic debt is the fact that the federal

fiscal deficit was financed almost primarily through domestic sources.

The fallacy of default

While the government portrays the current debt situation optimistically, the reality presents a more challenging picture. The scarcity of concessional financing from external sources ensures that interest payments will remain prohibitively high, continuing to crowd out vital private investment across the economy.

As external creditors maintain rather than increase their exposure through rollovers, domestic markets at non-concessional rates have become the de facto source of new borrowing. This dynamic inevitably places upward pressure on interest rates throughout the financial system.

Even after five years of severe austerity measures under the Extended Fund Facility (EFF) program, government interest payments are projected to remain above 30% of revenue—a clear indicator of persistent sustainability risks by international standards. This precarious financial position threatens to severely constrain economic growth potential and further exacerbate social instability.

For analysts who might let instincts drive recommendations, default may appear to be a tempting solution to the mounting debt burden. However, Pakistan’s specific debt composition significantly limits any potential benefits while imposing substantial costs. With over 85% of interest payments directed to domestic creditors, even a complete suspension of external debt payments would leave the overall interest burden largely unchanged.

Moreover, defaulting on external debt would trigger a cascade of additional challenges, including restricted access to international capital markets, potential damage to the banking sector, currency depreciation, and broader economic isolation—consequences that would ultimately harm the most vulnerable segments of society while offering minimal fiscal relief

Restructuring domestic debt presents equally challenging obstacles. As explained earlier, more than 50% of the government’s domestic debt is held by banks, and these government constitute above 50% of total bank assets.

Therefore, the challenge at hand as explained by Husain is, “Even a modest 10-percent haircut would wipe out the capital base of the banking system, though individual banks would experience varying degrees of impact. The resulting disruptions would be severe, affecting bank shareholders, depositors, and other government debt holders, including households and insurance and pension funds. Given these risks, restructuring domestic debt should be considered only as a last resort.”

The way out

Asustainable path forward demands a balanced approach combining gradual fiscal consolidation with significant new concessional financing. While tax reforms and spending rationalization are essential, it’s abundantly clear that the interest-to-revenue ratio will simply never fall below the critical 25% threshold by the end of the decade unless a substantial portion of new borrowing is secured on concessional terms.

This undeniably necessitates coordinated action among bilateral and multilateral lenders, who must move beyond their timid approach of merely rolling over existing loans to temporarily increasing their exposures. Such coordination, bolstered by enhanced data transparency, unquestionably serves creditors’ collective interests by improving Pakistan’s prospects for overcoming its debt challenges. Concessional financing should be aggressively channeled toward infrastructure and climate resilience initiatives to maximize economic growth and job creation. A significant portion of external funding should be allocated to retiring, at a discount, those obsolete high-emission energy projects that have become glaringly uncompetitive compared to clean solar alternatives but continue to drain resources purely to cover debt service costs.

Pakistan’s debt crisis demands nothing less than a multifaceted solution addressing both immediate fiscal pressures and the deeply entrenched structural weaknesses that have plagued the economy for decades. While recent initiatives show modest promise, sustainable debt management will require unwavering fiscal discipline, dramatically strengthened revenue mobilization, bold and coordinated international support, and strategic investment in growth-enhancing sectors. The status quo is simply untenable, and halfhearted measures will inevitably fail. n

OPINION

Syed

Faisal Hassan

A Farmer’s Journey Through Pakistan’s Barrages

The lifeblood of Pakistan’s agriculture—the mighty Indus River and its tributaries—is under threat. In a recent journey across key barrages in Punjab and Sindh, I witnessed a stark contrast in water quality, flow, and infrastructure—exposing a deepening crisis that directly affects millions of farmers and rural communities.

Sulemanki & Islam Barrages: A Toxic Reality

On March 26, 2025, I set off from Lahore before dawn, heading toward the Sulemanki Barrage via Okara. What greeted me there was appalling: black, polluted water laced with white toxic froth. While the stench was bearable, the visual impact was devastating. I was told January and February are the worst, with only sewage flowing during those months. Locals and officials confirmed that standing near the barrage during winter is nearly impossible due to the foul odor.

Water for agriculture is critically scarce. Groundwater is brackish and unsuitable, making canal water the only viable source. Yet, during the winter, the ratio of river water to wastewater deteriorates drastically, often reaching 0:100.

Pollution sources span both India and Pakistan. The infamous Hudaira Drain—carrying industrial and urban waste from both countries—is a primary contributor. Lahore’s sewage, nearly half of Faisalabad’s waste, and effluents from Kasur’s tanneries all find their way into the Sutlej via the Ravi, poisoning downstream regions like Sulemanki and Islam Barrages.

Cholistan’s Disturbing Dependence on Polluted Water

What struck me most was the disturbing reality in remote Cholistan: this same contaminated water is used for drinking (after boiling), cooking, and washing. This is a

The writer is a farmer

humanitarian crisis in the making.

During my stop near the Sulemanki border, I paid tribute at the memorial of Major Shabbir Sharif Shaheed (N.H., S.J.), a symbol of courage and sacrifice. His legacy deserves better than polluted waters flowing past our national frontiers.

Punjab’s Water Woes: Scarcity Amid Pollution

Iproceeded to Head Islam in the evening and found a repeat of Sulemanki’s toxic tale—severely polluted water and insufficient flow for farmers. The situation was slightly better at PunjnadBarrage, where pollution levels were lower, yet water scarcity remained stark. Officials at all barrages spent their time managing water distribution requests, highlighting the systemic strain on already limited resources.

Sindh Barrages: A Tale of Serene Contrast

Crossing into Sindh the next morning, I arrived at GudduBarrage—a breath of fresh air. Clean, energetic flows of the Indus reminded me of what this river once represented. Of the four off-taking canals, Pat Feeder and Ghotki Feeder were actively flowing. The sight was rejuvenating. The only canal on Guddu and Sukkur was the Rainee Canal which was closed off. At Sukkur Barrage, I was moved. It was majestic. Despite being in the dry season, the Indus flowed gracefully. Sukkur, the world’s largest irrigation system, services over 8 million acres through seven major canals. While the right-bank canals, especially the mighty Nara Canal, were thriving, the left-bank canals received noticeably less flow—partially due to natural changes post-2010 floods.

All left bank canals were flowing with gates slightly open. Kirther had more flow, Rice and Dadu canals had slightly less flow. The left-bank canals, however, looked like the neglected stepchildren. Post-2010 floods, a large island formed near the left side of the barrage, changing the river’s natural flow. Whether it’s science or politics, the result is the same: rightbank canals get the lion’s share while the left gets table scraps.

Still, I must say—Nara Canal in winter is graceful, silent, and dangerously underrated. The work being done on Nara Canal is commendable: cemented embankments and modernized infrastructure. Just one humble request to Sukkur authorities: fence it before a curious kid decides to take a swim and discovers it’s deeper than their dreams.

Karachi Wastewater and the Indus Delta: A Missed Opportunity?

Akey question lingers: if Punjab is forced to use all its wastewater for agriculture, why can’t Karachi’s wastewater be repurposed to rejuvenate the Indus Delta and support mangroves? The ecological and agricultural benefits could be immense.

A Call to Action: Visit, Witness, and Reform

Driving back toward Lahore, I noticed dry canals and distributaries reappearing across Punjab. Bahari Distributary, the last one I passed before nightfall, was bone-dry.

I urge every stakeholder—policymakers, environmentalists, engineers, and ordinary citizens—to visit these barrages, especially Sukkur and Sulemanki. See the truth for yourself.

The time for policy papers and desk discussions is over. Action is needed now. n

Hatton National Bank withdraws bid for Bank Alfalah’s Bangladesh operations

Sri Lankan bank was seen as leading contender to acquire the Bangladesh branches for BAFL, which have been up for sale for years

Profit Report

Sri Lanka's Hatton National Bank PLC (HNB) has withdrawn its non-binding offer to acquire the Bangladesh operations of Pakistan's Bank Alfalah Ltd(BAFL). This decision brings an end to months of speculation and due diligence efforts aimed at expanding HNB's footprint into the Bangladeshi market.

In August 2024, HNB expressed interest in acquiring BAFL's Bangladesh operations, submitting a non-binding offer and initiating discussions pending regulatory approvals. By November 2024, both the State Bank of Pakistan and Bangladesh Bank granted in-principle approvals, allowing HNB to conduct due diligence on BAFL's Bangladeshi assets and liabilities.

BAFL's presence in Bangladesh dates back to 2005, when it acquired the Dhaka branch of Shamil Bank of Bahrain for $17.9 million, marking its first foray outside Pakistan. Over the years, BAFL expanded to seven branches across major cities, including Dhaka, Chittagong, and Sylhet.

Despite a modest branch network, BA-

FL's Bangladesh operations have demonstrated profitability. In 2024, the branches reported profits of Rs2.1 billion, a 22.3% increase from the previous year. However, deposit growth has remained stagnant at approximately Rs55 billion over the past few years, indicating challenges in expanding the deposit base.

HNB, established in 1888, is a leading private sector bank in Sri Lanka with a network of over 250 branches and 820 ATMs nationwide. The proposed acquisition was seen as a strategic move to diversify HNB's operations and tap into the growing Bangladeshi economy. Fitch Ratings had noted that the acquisition would have a modest impact on HNB's capital, estimating less than a 1 percentage point drop in capital ratios due to increased risk-weighted assets.

Despite these considerations, HNB has decided to retract its bid. While specific reasons were not disclosed, industry analysts speculate that factors such as regulatory complexities, alignment of business strategies, and economic conditions in both Sri Lanka and Bangladesh may have influenced the decision.

For BAFL, HNB's withdrawal means the continuation of its operations in Bangladesh, at least in the short term. The bank may explore

other potential buyers or strategic partnerships to divest its Bangladeshi assets. Alternatively, BAFL might focus on revitalizing its Bangladesh operations to address challenges like stagnant deposit growth while leveraging the profitability of its existing branches.

The Bangladeshi banking sector, characterized by a mix of local and foreign banks, remains competitive. HNB's initial interest had signaled confidence in the market's potential, and its withdrawal may prompt other regional banks to reassess opportunities within Bangladesh.

HNB's decision to withdraw its bid for BAFL's Bangladesh operations underscores the complexities inherent in cross-border banking acquisitions. While the move halts HNB's immediate expansion plans into Bangladesh, it leaves the door open for other strategic initiatives in the region. For BAFL, the focus may now shift to enhancing its operational performance in Bangladesh or seeking alternative avenues for divestment.

As the South Asian banking landscape continues to evolve, such developments highlight the dynamic interplay of strategy, regulation, and market conditions influencing financial institutions' decisions in the region. n

Philip Morris Pakistan posts 77.5% revenue growth in 2024

The company’s surge comes amid export boom and new product launches, though much of the increase domestically came from price increases

PProfit Report

hilip Morris (Pakistan) Ltd (PMPKL), a subsidiary of the global tobacco giant Philip Morris International (PMI), has posted a remarkable 77.5% year-on-year increase in net turnover for the fiscal year ended December 31, 2024. The strong topline performance was primarily driven by a more than doubling in export turnover, alongside modest growth in domestic cigarette sales and the company’s entry into the emerging category of smoke-free nicotine products.

In a filing submitted to the Pakistan Stock Exchange (PSX) on March 27, 2025, the company reported a net turnover of Rs32.3 billion, up from Rs18.2 billion in 2023. Of this, domestic turnover contributed Rs17.8 billion (55%), while exports made up Rs14.4 billion (45%).

While top-line growth paints a robust picture, the company’s profit after tax declined by over 33% year-on-year, falling to Rs254.7 million in 2024 from Rs379.8 million in the previous year — a result that management attributed to cost pressures, competitive market dynamics, and investments in new product segments.

According to the management commentary, the domestic cigarette business registered a 5.3% volume growth compared to the prior year, showing signs of recovery after the February 2023 excise duty hike severely dented legal sector sales. This moderate resurgence suggests some stability returning to the regulated market.

A particularly noteworthy development in PMPKL’s revenue composition is the growing contribution from new product categories. In 2024, nicotine pouches — part of the company’s pivot towards smoke-free products — accounted for 2.5% of domestic net turnover, indicating early traction in a category that Philip Morris International globally champions as part of its “smoke-free future” vision.

Meanwhile, exports exploded, registering a growth of over 100% versus 2023, likely buoyed by contract manufacturing for PMI’s international markets. While the company has not disclosed destination markets or products, industry insiders point to a rising trend in PMI outsourcing production to cost-competitive jurisdictions like Pakistan to serve select regions

in the Middle East and Africa.

Despite narrowing profits, Philip Morris Pakistan continued to play a significant fiscal role. In 2024, the company contributed a total of Rs47.9 billion to the national exchequer — up 25.8% from the previous year — through excise duties, sales taxes, income taxes, and other levies.

This figure reflects the company’s status as one of the leading contributors to Pakistan’s tax base, particularly at a time when the government is battling a chronic fiscal deficit and seeking to enhance documentation and compliance in the tobacco industry, where the illicit trade remains rampant. Philip Morris Pakistan’s evolution into a key pillar of PMI’s global supply chain and its domestic pivot to innovation has been a long journey, rooted in its origins as Lakson Tobacco Company Ltd— part of Pakistan’s Lakson Group.

In 2007, PMI acquired a majority stake in Lakson Tobacco for $338 million, rebranding it as Philip Morris (Pakistan) Ltdand integrating it into its global network. At the time, this was seen as a bold strategic move, providing PMI with a foothold in a major South Asian market.

However, since then, the company has faced headwinds including frequent excise duty hikes, a growing illicit cigarette trade that commands over 35% of the market according to some estimates, and shifting consumer preferences. These pressures prompted PMPKL to shutter its Kotri factory in 2017 and consolidate operations to optimize costs.

More recently, the focus has shifted to innovation and exports, both of which appear to be paying dividends in the form of new revenue streams.

While the company’s turnover growth is undoubtedly impressive, the sharp drop in profitability raises questions about underlying cost structures and competitive dynamics. Although detailed margin data wasn’t included in the PSX filing, analysts believe that rising input costs, higher freight expenses for exports, and investments into new product lines may be weighing on the bottom line.

One of the biggest risks PMPKL continues to face is regulatory uncertainty. Tobacco remains a politically sensitive industry in Pakistan, with the government often turning to excise hikes to shore up revenues. In early 2023, a steep

increase in excise duties led to a surge in prices of legal brands, pushing many consumers toward illicit and untaxed alternatives.

While the company has managed to stage a partial recovery in volumes, the risk of further taxation remains high, especially in light of ongoing IMF negotiations and fiscal consolidation goals. Additionally, the illicit trade continues to erode market share from regulated players. Despite government crackdowns and tax stamp initiatives, enforcement remains patchy. Industry stakeholders have repeatedly called for stronger action to level the playing field between tax-compliant manufacturers and illegal operators.

Globally, PMI has declared its intent to become a “majority smoke-free company” by 2030, with reduced-risk products like IQOS and nicotine pouches leading the charge. While IQOS is not yet commercially available in Pakistan, the company’s initial steps into the nicotine pouch segment signal its intent to eventually align the local business with PMI’s broader transformation agenda.

For now, the domestic contribution of nicotine pouches is modest — just 2.5% of net turnover — but management appears optimistic about the long-term potential.

For 2025, the company is expected to build on its export momentum, deepen its footprint in the nicotine pouch market, and continue defending its domestic share in an increasingly competitive and taxed environment. Much will depend on whether the government maintains a stable fiscal framework for the industry, and whether enforcement against illicit trade improves.

In the medium to long term, PMPKL’s ability to diversify away from traditional combustible tobacco, align with PMI’s global smoke-free transformation, and defend margins will determine whether its recent top-line success translates into sustainable value creation for shareholders.

As it stands, Philip Morris Pakistan is a company in transition — one with impressive revenue growth, but also clear challenges ahead. Its 2024 performance offers a mixed bag of promise and caution, emblematic of a sector grappling with both legacy burdens and emerging opportunities. n

Petroleum sales surge 5% in March due to Ramazan and Eid

Intercity travel, coupled with general increased consumption led to volumetric increase in sales for fuel retailers

Profit Report

Pakistan’s petroleum consumption witnessed a robust year-on-year growth of 5% in March 2025, with total sales climbing to 1.22 million tons, according to a detailed research report by Arif Habib Ltd (AHL). Authored by equity research analysts Muhammad Iqbal and Menka Kirpalani, the report attributes the surge to a confluence of seasonal demand, price-driven consumption, and tighter control over smuggled petroleum products.

The analysts noted that Ramadan and Eid festivities played a pivotal role in this upswing, as intercity travel and economic activity surged, particularly during the latter half of the month. With March marking both the end of Ramadan and the onset of Eid holidays, road and freight traffic rose significantly, boosting demand for motor spirit (MS) and high-speed diesel (HSD).

The 5% year-on-year increase in overall petroleum sales in March was fueled by several key drivers:

1. Festive Mobility: Increased intercity movement due to Eid led to a spike in fuel demand, particularly MS.

2. Seasonal Economic Activity: The Ramadan period typically sees elevated economic activity, particularly in wholesale and retail sectors, pushing freight demand higher.

3. Price Reductions: A 9.7% drop in HSD prices and 8.6% decrease in MS prices compared to the previous year incentivized higher consumption.

4. Smuggling Curtailment: Crackdowns on Iranian petroleum smuggling contributed to higher demand for domestically supplied fuel.

5. Rising Vehicle Sales: A noticeable uptick in automobile sales added to the consumer base for retail fuel sales.

The product-wise breakdown paints an interesting picture. Sales of motor spirit – known colloquially as petrol, and used mostly for cars – rose by 1% YoY to 0.58 million tons, aided by reduced prices and Eid travel. High-Speed Diesel (HSD) volumes grew by 5% YoY to 0.49 million tons, supported by a price cut and increased freight demand. And surprisingly, Furnace Oil (FO sales) posted a 22% YoY growth, reaching

0.05 million tons, largely due to higher reliance on FO-based power generation amid rising electricity demand.

Month-on-month (MoM) data further showed a 7% increase in total petroleum sales compared to February, highlighting the impact of the longer month and festive season. HSD led the MoM gains with a 14% jump, while MS and FO followed with 4% and 2% increases, respectively.

On a cumulative basis, petroleum sales during the first nine months of FY25 (July–March) rose by 4% YoY, totaling 11.76 million tons versus 11.34 million tons in the same period last year. Motor spirit clocked in at 5.51 million tons, up 4% YoY. For HSD, the number was 4.98 million tons, up 9% YoY. And for FO, it was 0.51 million tons, down 39% YoY.

The dramatic fall in FO volumes for the July 2024 to March 2025 period reflects the overall shift in Pakistan’s energy generation mix, although the March bump signals temporary reversals based on energy shortages or regional demand fluctuations. The report provided a deep dive into the performance of leading Oil Marketing Companies (OMCs):

For Pakistan State Oil (PSO), March 2025 sales dropped 14% YoY to 0.51 million tons. Sharp declines were recorded in MS (-21%), HSD (-12%), and FO (-27%). 9MFY25 sales also fell 7% YoY, with PSO’s market share shrinking from 50% in 9MFY24 to 45% this year.

At Attock Petroleum Ltd (APL), March sales rose 2% YoY, totaling 0.11 million tons. For the first nine months of fiscal year 2025 sales declined by 10% YoY, with market share dropping from 10% to 9%.

Shell Pakistan Ltd (SHEL) posted a 7% YoY decline in March volumes. Its market share remained stable at 7%, but 9MFY25 volumes were down 18% YoY.

Meanwhile, Hascol Petroleum was a standout performer in the period, Hascol registered a 95% YoY increase in March sales. For the first nine months of fiscal year 2025, volumes grew 6% YoY, indicating a gradual turnaround for the company. Market share remained flat at 4%, but momentum has clearly returned.

Gas and Oil Pakistan (GO) was the big gainer in market share. GO jumped from 3% in the first nine months of fiscal year 2025 to 10% in 9MFY25, reflecting aggressive expansion and

better distribution reach. However, its sales in March dipped 9.9% YoY, hinting at volatility in its monthly performance.

The report also shed light on fiscal developments linked to petroleum consumption. Petroleum Development Levy (PDL) collections stood at PKR 819 billion in the first nine months of FY25 — averaging PKR 91 billion per month.

The federal government has set a PDL target of PKR 1,281 billion for FY25, translating to a monthly target of around PKR 107 billion. Given current trends, the government may miss its annual target unless consumption continues to accelerate in the final quarter.

Despite the March surge, analysts at Arif Habib Ltd. remain cautious about the sector’s medium-term prospects. Key challenges include volatility in global oil prices. Unpredictable crude markets could impact local pricing, affecting consumer demand.

However, upside drivers such as better economic recovery, infrastructure investment, and continued enforcement against smuggled fuel could offer support to the formal fuel marketing sector.

Iqbal and Kirpalani note in their commentary that “March’s numbers were exceptional due to favorable seasonal and pricing factors, but structural challenges remain.” They emphasize that while sales spikes during festivals and travel seasons are welcome, sustainable demand growth will depend on macroeconomic stability and regulatory clarity. The March 2025 petroleum sales data offers a much-needed boost to Pakistan’s oil and gas marketing sector. While celebratory spending and lower pump prices provided temporary momentum, the path ahead remains uncertain. Market consolidation, evolving energy trends, and fiscal pressures will all play a role in shaping the industry’s trajectory over the coming quarters.

Still, the surge reflects the resilience of demand during festive and high-mobility periods, and it underscores the potential of the sector when supported by sensible pricing and supply chain discipline. As the government eyes further fiscal space through levies and the economy slowly climbs out of stagnation, how the sector evolves in the post-Ramadan months will be a key signal of broader economic sentiment and household resilience. n

Pakistan’s maize exports crash 87.19%

Food ministry issues new SOPs to address falling corn export

By Ghulam Abbas

Pakistan’s maize exports have suffered a drastic 87.19% decline in the first three months of 2025, following a remarkable surge in 2024, as revealed by the latest trade data from the Department of Plant Protection (DPP). This sharp downturn has raised concerns among farmers, traders, and economists regarding sustainability, market stability, and the government’s mismanagement of phytosanitary policies that regulate the export of maize and other agricultural commodities.