16 Red flags galore at Al Shaheer as Sunridge calls for an election

21 Panther Tyres: the quiet growth story in the automotive industry

22 Unity Foods to expand Sunridge retail presence as its core growth strategy

24 Treet continues its struggle, despite some favourable tailwinds

25 Despite deregulated prices, Searle swings to a loss

27 The GMO oilseed saga is not quite over

30 Sazgar and its ability to adapt is reaping dividends

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

Why, counterintuitively, fewer competitors might mean better choices for mobile telecommunications consumers in Pakistan

By Ahtasam Ahmad & Hamza Aurangzeb

Conventional wisdom has it that the more choices consumers have, the better off they will be.

So when a competition regulator like, say, the Competition Commission of Pakistan, is examining a merger, one would expect them to examine the transaction on the basis of a single question: will this increase or decrease market competition? But an examination using metrics like the number of competitors, or even the more sophisticated analytical tools like the Herfindahl-Hirschman Index would be simplistic, and lead one to arrive at precisely the wrong conclusion.

It is our contention that an analysis of the market structure of mobile telecommunications in Pakistan – and the world – would lead one to conclude that the acquisition of Telenor Pakistan by Pakistan Telecommunication Company Ltd (PTCL) is more likely that not going to benefit consumers in the country.

PTCL formally made its bid to acquire Telenor Pakistan in December 2023, and the Competition Commission of Pakistan (CCP) naturally had some questions. They are expected to rule on the matter in latter half of December 2024, and while we have no indication of which way the ruling is headed, we would argue that a ruling that allows the transaction to go through would benefit Pakistan’s consumers.

Our analysis will examine the dynamics of the industry, why competition has been going down over the past decade or so, and why a PTCL acquisition of Telenor Pakistan – specifically the merger of Ufone and Telenor – will likely be a net positive for Pakistani consumers.

The punchline: Jazz is far too dominant in the Pakistani market right now, and this merger will add heft to its competitors in a highly capital-intensive industry where scale is the key to being competitive.

And if the CCP is looking for case studies to bolster a decision to allow the merger, we will offer evidence from the United States

where the exact same situation occurred (four players consolidating into three) and both prices and quality of services improved from the consumer perspective.

But first, a brief overview of how to think about competition in an industry.

The interplay of complex submarkets

Network effects are a defining characteristic of the telecommunications industry, where the value of a product or service exponentially increases with the number of customers. This phenomenon creates a unique dynamic where each new subscriber enhances the network’s overall utility without incurring additional transaction costs. In competition economics, this is termed “network externality” — a scenario where the network’s value grows proportionally with its user base.

The telecom market is fundamentally a “two-sided” ecosystem, where multiple subscriber groups interact, and network value appreciates as more participants join. This creates a self-reinforcing cycle of network expansion and value creation.

From a competitive landscape perspective, on the surface, Pakistan’s retail mobile telecommunications market exhibits an oligopolistic structure with high market concentration. As we shall see later, however, this level of concentration is the norm in industries like mobile telecommunications which have high upfront capital investment costs.

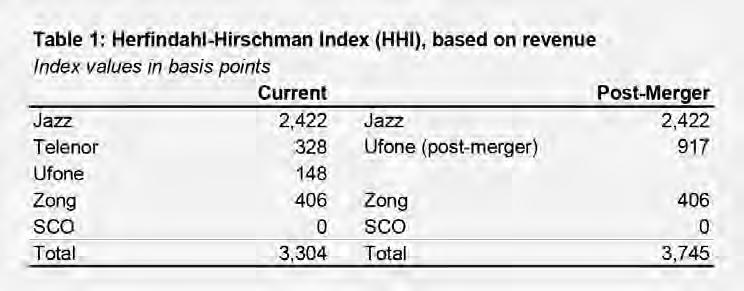

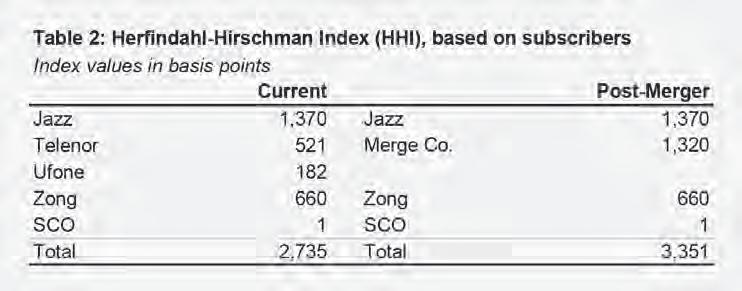

Nonetheless, let us look at exactly how concentrated the industry is. To quantify this concentration, we have utilized the Herfindahl-Hirschman Index (HHI), which provides a comprehensive measure of market competitiveness by analyzing both subscriber and revenue shares. The HHI is the preferred method of examining market concentration levels by several regulators, including the Federal Trade Commission in the United States, which is the US regulatory body upon which the CCP is modeled.

The Herfindahl-Hirschman Index is the sum of the squared values of each firm’s market

share. It is believed that a lower value of the index indicates a competitive industry whereas a higher value reflects a highly concentrated industry.

HHI = (Market Share of Firm 1)² + (Market Share of Firm 2)² + … + (Market Share of Firm n)²

The market shares are expressed in decimals (so a 25% market share means 0.25) and then squared and summed. An HHI of 1 indicates a complete monopoly of one firm, and an HHI asymptotically approaching 0 means a large number of very small firms. Sometimes, to make the analysis easier to follow along, the HHI is multiplied by 10,000 to yield a number that is then expressed in “points”.

If one were to calculate the index on the basis of the market share by 2023 revenues, the HHI of the telecom industry in Pakistan stood at 0.33 (or 3,304 points) before the merger but after the merger, it will go up to 0.37 (or 3,745 points). This means that the index will increase by 0.04 (or 441 points), which means that, on this measure alone, the telecom market of Pakistan will become more concentrated than before.

The position could be corroborated by another variant of HHI which is calculated by the number of subscribers. As per the number of subscribers of telcos as well, the telecom market of Pakistan will become more concentrated after the merger of PTCL and Telenor. The index currently stands at 2,735 points before the acquisition of Telenor, however after the conclusion of the transaction it will jump to 3,351, an increase of 616 points, once again showing that concentration levels are expected to rise.

But beyond these analytical outcomes, what would be the true impact of this merger on the telecom landscape? This can be assessed by analysing the post-merger scenario for different submarkets in the sector.

Mobile Network Operators Market

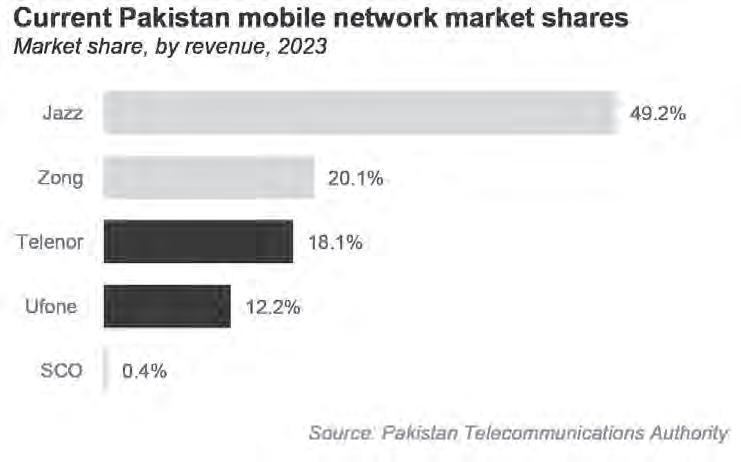

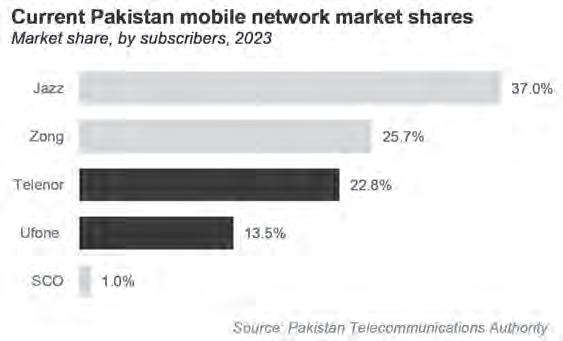

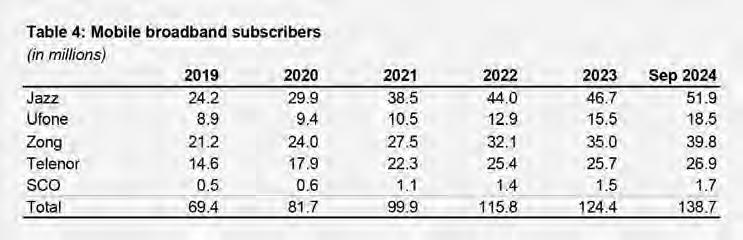

In the cellular mobile landscape, Jazz dominates the market with a commanding 46.4% market share, while Zong and Telenor trail with 22.1% and 19.5% respectively. Ufone occupies around 11.6% of the market. This sector has long been characterized by overcrowding, with industry experts consistently arguing that the market could not sustainably support four telecom operators.

Indeed, as we will point out later: there may be something about the telecom market that lends itself to naturally consolidating towards three players. Even the largest free market in the world – the United States – has only been able to sustain three network operators. Why do we think Pakistan can support more? This hyper-competitive environment

drove market dynamics to extreme limits, pushing operational margins to some of the lowest globally. Telenor Pakistan’s exit epitomizes these challenges. The company’s Average Revenue Per User (ARPU) had dramatically declined to just $0.70 — a stark contrast to the $1.5 ARPU required to maintain a viable business model.

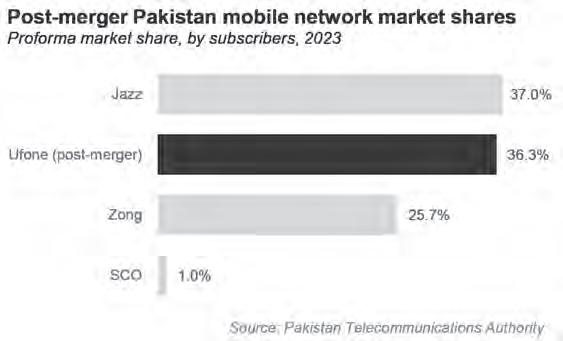

In terms of customer base, Jazz leads the pack with an impressive 71.6 million customers, while Zong follows with 49.6 million subscribers and Telenor maintains 44.1 million users. Ufone, traditionally the smallest player, currently serves approximately 26.1 million subscribers. However, the impending merger between Ufone and Telenor is set to flip the tables. Upon completion, Ufone’s subscriber base is projected to surge to 71.4 million— nearly matching Jazz’s market position.

By combining revenues, the merged company will command approximately 30% of cellular industries revenues and start to offer some real competition to Jazz’s dominant market position.

The merged company’s initial ARPU is estimated at Rs. 207.8 per month, with substantial growth potential as subscribers from both networks gain access to an expanded service ecosystem. A compelling illustration of this enhanced value proposition is the opportunity for Telenor’s customers to now utilize Ufone’s over-the-top (OTT) services, including its digital brand ‘Onic’.

But, beyond just subscribers, PTCL and Ufone would benefit from acquiring critical telecom assets including additional spectrum and tower sites.

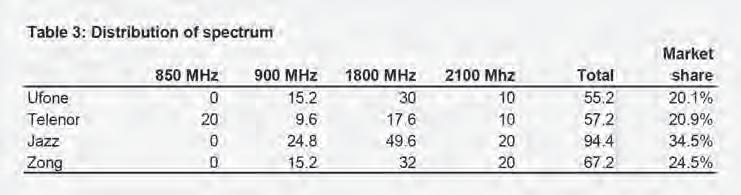

Analyzing the distribution of spectrum in Pakistan, we found that about 34.5% of spectrum of the retail mobile market is controlled by Jazz, while Zong holds 24.5% and Ufone and Telenor utilize 20.1% and 20.9%, respectively. This means that the merged company which will emerge after the amalgamation of Ufone and Telenor will become the leader of the market in terms of spectrum as it will hold about 41% of the total retail market spectrum.

Ufone’s post-merger spectrum portfolio

would position it as a force to reckon with in Pakistan’s telecommunications market. By acquiring the largest shares across two critical frequency bands—900 MHz, and 2100 MHz. A close second in 1800 MHz and the only player in 850 MHz. The company would enjoy a unique strategic advantage that extends far

beyond mere market share.

The most significant potential lies in spectrum refarming, a sophisticated strategy that would allow the telco to progressively transition from legacy technologies to high-value mobile broadband services. By strategically reallocating bandwidth resources, the company can optimize network efficiency, enhance service quality, and generate substantially higher revenue streams. This approach is particularly advantageous in a rapidly digitizing market like Pakistan, where mobile broadband represents not just a technology upgrade, but a critical infrastructure for economic development and digital inclusion.

The merger between Ufone and Telenor will also create a telecommunications infrastructure powerhouse, with Ufone inheriting approximately 11,000 towers from Telenor and bringing its total tower portfolio to around 20,000—the largest cell site infrastructure

in Pakistan. This extensive network will enable strategic infrastructure rationalization, allowing the merged company to eliminate redundant sites in close proximity and expand coverage into new regions. Telenor’s strong infrastructure presence in rural areas perfectly complements Ufone’s urban-centric network, creating a comprehensive nationwide coverage strategy.

The merger introduces significant disruption to the TowerCo industry’s existing business models. Unlike Telenor, Ufone has historically been reluctant to share tower infrastructure, which will potentially undermine the viability of infrastructure-sharing companies in the telecommunications segment.

The TowerCo industry currently operates under two primary business models: the Sales & Leaseback Model and the Built-ToSuit (BTS) Model. The Sales & Leaseback Model involves purchasing, upgrading, and developing existing towers, with revenue generated through tower rentals and an average lease residual life of 10 years. The BTS Model involves constructing, owning, and operating towers through agreements with telecommunications companies, with the flexibility to lease to multiple providers.

Under these models, telecommunications companies install their antennas and wireless equipment on rented sites, while infrastructure companies maintain ownership of passive infrastructure such as fences, shelters, air conditioning units, generators, and batteries. The telecommunications companies retain exclusive ownership of active components like antennas and wireless technology. The Ufone-Telenor merger has the potential

to fundamentally reshape these established infrastructure-sharing dynamics.

In the cellular operator market, Ufone is also likely to benefit from Mobile Termination Rate (MTR) changes. When a Ufone user calls a user from another network, Ufone pays termination charges. However, with the merger, on-net calls will increase, reducing costs and enabling Ufone to generate more revenue through MTR charges from other operators. The Pakistan Telecommunication Authority (PTA) last revised MTR rates in July 2023, setting them at Rs0.30 per minute.

The Broadband Market

The broadband market comprises fixed and mobile segments, with fixed broadband delivered through technologies like DSL, fiber, satellite, and wireless. Pakistan possesses 66,000 Km of long-haul optical fiber cable (OFC) and 90,000 Km of metro OFC, where 60,000 Km of the metro OFC is owned by PTCL giving it control over 66.7% of the market.

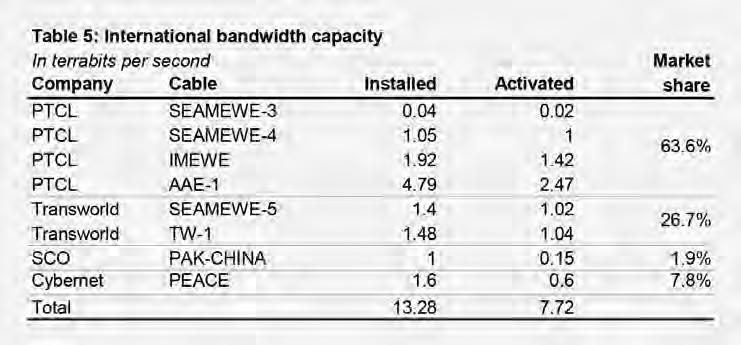

The country’s international bandwidth capacity is 13.3 Tbps (installed) and 7.7 Tbps (activated), supported by seven submarine cables, a Pak-China fiber optic link, and 19 cross-border terrestrial connections. PTCL dominates international bandwidth, holding 58.7% of installed and 63.6% of activated capacity, with other key players including Transworld Associates, Cybernet, and Special Communication Organization.

PTCL dominates the Fiber to the Home (FTTH) market through its Flash Fiber ini-

tiative, which has revitalized fixed broadband in Pakistan. With 605,387 subscribers, PTCL holds 34.1% of the market, closely followed by Cybernet with 524,916 subscribers and 29.6% market share. But as Telenor is not really involved in this segment, the merger does not change the dynamics much.

But where the tables turn is the mobile broadband segment. Jazz has cemented its place as the leader of the pack. As of 2023 It controls a market share of 48.1%, Zong’s share stands at 21.5%, while Telenor and Ufone hold shares of 21.3% and 8.9%, respectively.

This means that the merger will consolidate the newly merged company’s position in the mobile broadband market, where it will control around 30.2% of the market share and its number of broadband subscribers will increase to 45.4 million, only second to Jazz’s 52 million customers. It will also help the company improve its share of 4G subscribers from 11% to 31% as currently, it lags behind its competitors in the 4G race due to its late transition towards the technology.

LDI, Local Loop, and Backhaul

Communications Market

Long Distance and International (LDI) Operators are licensed to provide nationwide long-distance and international telephony services. Pakistan has around 21 operational LDI licensees, with PTCL holding an integrated license. Currently, PTCL commands 50.5% of the retail LDI fixedline market, a share expected to increase to 61% following its acquisition of Telenor.

Wholesale Domestic Leased Lines are semi-permanent communication links that connect geographically distant telecommunication network elements. These private transmission resources facilitate interconnection between offices, mobile switches, and telecom infrastructure across Pakistan, supporting cellular, fixed-line, data, and internet services.

In the wholesale IP bandwidth market, four major overseas cable operators—PTCL, Transworld Associates (TWA), Cybernet, and SCO—provide services to other operators. Downstream providers, including fixedline and cellular mobile operators, purchase international bandwidth wholesale and resell it to home and corporate customers. PTA has already designated PTCL and TWA as Significant Market Power (SMP) operators in this segment.

PTCL is positioned to dominate the markets, controlling 68% of wholesale IP bandwidth and 42.7% of domestic leased lines. In this scenario, Wateen is the one set to lose significantly as it was the one providing fiber optic lines to Telenor, which will likely halt using its services after the merger. Moreover, other telcos would also face increased competition as through preferential pricing, PTCL can now provide better rates for its backhaul services to the merged Ufone-Telenor company.

In the Pakistani local loop market, services can be fixed (FLL) or wireless (WLL), involving network construction and telecommunications services in a licensed region. PTCL dominates the market, holding 85.1% of the Fixed Local Loop segment and 49.6% of the Wireless Local Loop segment. While facing competition from Wateen, which controls 45.3% of the wireless market, PTCL’s competitive landscape is expected to shift following its acquisition of Telenor, potentially reducing Wateen’s market share.

The US case study

As may be evident from the analysis above, more than anything else, the merger of Ufone and Telenor will provide a stronger competitor to the market leader, which in turn will create real competition in terms of prices and service quality, likely to the benefit of consumers.

It is this same logic that led the US court system to allow the merger of the third and fourth largest mobile operators – T-Mobile and

Sprint – in April 2020, despite several lawsuits and challenges by the US Federal Communications Commission, and several US state-level governments. The logic went something like this: the two largest US mobile operators – Verizon and AT&T – were effectively a duopoly, which the third and fourth largest providers were struggling to compete against. By allowing them to merge, it would create a real three-way rivalry, which would legitimately improve consumer outcomes.

The US courts took the bet that this would be how it would play out. We now have four years of data to examine the results. So how did it turn out?

Contrary to some analysts’ predictions of reduced competition, the merger appears to have had a positive impact on the market. With respect to trends in prices, in the three years following the merger, real mobile subscription fees declined by nearly 12%, compared to an 8% decline in the three years prior, meaning prices started to decline even faster than before the merger.

And in terms of service quality, by early 2023, T-Mobile’s data download speeds had increased more than threefold, with 50% of its connections utilizing 5G technology.

In other words, the market consolidated, but because the telecommunications market is one that requires high capital expenditures, it lends itself to fewer natural competitors, and trying to keep four players alive was not the right move for US consumers. By moving to three companies instead of four, US consumers had three very strong choices to pick from, in-

stead of two strong choices and two obviously weaker ones.

Applications for the Pakistani market

The same is likely to be true in Pakistan. Right now, there is effectively one very strong choice in Pakistan – Jazz – and then various shades of weaker ones in the form of Telenor, Ufone, and Zong. By allowing two of those to merge, the post-merger Ufone will be a real competitor to Jazz, and Zong’s parent company – China Mobile – will be forced to invest more in its subsidiary or else watch it whither on the vine.

Could Pakistani consumers be forced to pay more? In theory, fewer players allow for greater collusion on prices, but the fact that is that four is hardly a very large number of companies. If collusion was going to happen, it would probably at least have been seriously attempted for a period of time already. The fact that it has never really happened thus far and that Pakistani prices have continued to collapse in real terms indicates that the market’s competitiveness is not determined by the number of players, but by the fact that switching costs for consumers are low and have been rendered even lower by the mobile number portability system.

What the merger will do is allow for the consolidated entity to be able to shed costs and spread the remaining operating costs on a larger base of revenue and consumers, allowing it greater profit margins and cash flows, which then can be plowed into better network technology to continue to compete on both price and service quality for consumer market share.

Having two companies with nearly equal war chests is also likely to improve the odds of a successful auction of 5G spectrum, and may also improve network reliability. Meanwhile, Zong will have to get even more aggressive with its pricing strategies, which is likely to ensure that at the very least prices will not increase.

When you need as much money to compete as you do in mobile telecommunications, what increases competition is to allow one or more of the players to bulk up through mergers and acquisitions. Allowing this merger would be a justifiable decision on the part of the CCP. n

Red flags galore at Al Shaheer as Sunridge calls for an election

Amidst board room meltdown, Sunridge tries to bring some normalcy to the company

By Zain Naeem

It was not long ago when Al Shaheer was seen as one of the stars of the stock exchange. The company was one of the first ones to be listed on the market which was involved in distribution and marketing of meat products for the local and international market. Now it seems that the company has been plummeting towards its demise.

The company touched new highs in 2016 recording highest profits in its short history and showed net profits of Rs 36 crores. This came on the back of sustained growth and profitability being seen at the company. 2023 saw the company have its worst year in its history as the company started to see its losses accumulate and reach Rs -1.8 billion leading to loss per share of Rs 5.5. The situation would have been much worse if the company had not recorded other income that it was generating which was attributed to exchange gain the company was earning due to its export business. The core business at the company had been slowly decaying and recent results would have shown a loss of Rs 2 billion if it had not been for the other income component.

While the company has seem worsening financial performance, the boardroom at the company has seen a complete meltdown as well. In the last year or so, the company has seen all of its directors resign one after another. This has taken place while the company has fired its own CEO, CFO and the company secretary has resigned as well. The last board of director elections were held on the 4th of November 2022 and seven directors were elected. From June 2023 to 2024, the company saw a mass exodus take place at the company which signalled that things were not fine. Zillay Nawab, Qaysar Alam, Babur Sultan, Sabeen Fazli and Imtiaz Jameel left the company in a span of one year. In place of the five, the new board only appointed Muhammad Altaf and Amir Shehzad who also resigned later in the year.

The board also chose to appoint a new CEO in place of Kamran Khalili who was the person responsible for taking the company to new heights in its past. Khalili also served as one of the directors and he was replaced by Muhammad Harris on the board. The last surviving director from the previous elections was Umair Khalili who was also shown the door and his place was taken by Muhammad Idress. When the dust settled, the company had no CEO, no CFO and only two directors with a company secretary named Mubasshar Asif. This was the situation that existed at the company at June end 2024. On October 11th 2024, even the remaining directors and company secretary resigned and it seemed like the company had no one in its board room.

While the financial performance was deteriorating and the board room was seeing a revolving door, the company also started to lag behind in terms of filing its accounts. The company submitted its last annual report in November of 2023 and has only filed its 1st quarter results for 2024 as far back as December of 2023. The results showed that the company had made a loss per share of Rs 2.41 where it had earned a profit just a year before. The half year accounts should have been filed by the company by February of 2024 according to the rules and regulations of Securities and Exchange Commission of Pakistan (SECP). The company asked for an extension in the date for the filing which was rejected by the regulator.

Al Shaheer seems to be fighting a war on three fronts

and seems to be losing on all of them. First of all, the company is suffering from losses which have been accumulating over time. The company has also been falling behind in terms of its regulatory obligations by filing its accounts and the board room is also being deserted by the directors of the company. Al Shaheer seems to have three huge gaping wounds and does not have the resources to plug any of them properly.

Trying to rationalize and understand the reason behind the mass exodus looks to be difficult but it can be seen that there is some sort of power struggle that is going on inside the company. A board which was standing together by December end of 2023. Kamran Khalil and Umair Khalili resigned as directors in February of 2024. Kamran was also fired as the CEO and the position was left open until a new CEO was appointed. A board meeting was called on the 6th of June which was later postponed due to lack of quorum. At this point, five directors were still active and serving on the board. After this, three more directors resigned which hints towards the fact that they had reservations in regards to the agenda that was being presented in the board meetings. As three of the members abstained from attending the meetings, the quorum would not be fulfilled and no agenda items could be passed as board resolutions. Over time, it has been seen that even the two directors left have resigned which has left the whole board to be vacant for now.

In such a chaotic environment, there is some normalcy that is being restored at the company. Sunridge Foods (Private) Limited as a subsidiary of Unity Foods which chose to invest in Al Shaheer. By September of 2023, the company held 69 million shares making up 18.42% of the shareholding. The investment was a vote of confidence being shown by Sunridge in Al Shaheer which was expected to lead to mutual benefit for both the companies. Since the investment was formalized, Al Shaheer saw a free fall in their board room. Hedging some of its losses, Sunridge first chose to sell some of their stock in Al Shaheer as it sold 10 million shares in July of 2024.

Sunridge has now requested that Al Shaheer call new elections for its board. Section 133 of the Companies Act 2017 dictates that a shareholder holding more than 10% of the issued share capital can use his powers to call an Extraordinary General Meeting to discuss certain matters that they can put on the agenda. In this case, Sunridge has asked the company to hold elections as mandated under Section 159 of Companies Act 2017 which outline how elections of directors are supposed to be carried out. In the normal course of business, elections are mandated after three years which would have meant elections taking place in 2025, however, due to extenuating circumstances, they are being called early.

This announcement needs to be made by the management at the company as well, however, as it has no company secretary present, no such disclosure or announcement has been communicated to the market. The shareholders have been informed by the share registrar of the company, Central Depository Company, through an email. The elections are expected to be held on the 17th of December in Karachi and the direction the company goes in will become apparent once the elections are carried out. With a lack of financial records from December 2023 to June 2024, nothing can be said with any certainty. Hopefully, new elections would be the solution that will jump start and bring the past glory back to the company.

In 2000, the SECP passed an order.

It took 24 years for the IHC to uphold it

The Islamabad High Court has ruled in favour of the apex regulator and the investing public. But is this a case of too little too late, or better late than never?

By Profit Report

Victories enjoyed by the Securities and Exchange Commission of Pakistan (SECP) are few and far between when it comes to the capital markets. When they do end up getting a win in their column, it is a cause of celebration. Even if it comes 24 years after the original order was given.

That is exactly what happened earlier this month, when the IHC gave a verdict on a decision that was long overdue. Back in the year 2000, the SECP had passed a decision

pertaining to shares sold by a particular broker in the stock exchange. So what exactly is the verdict and what are the details of the case in relation to the verdict? To understand it, we need to know how the stock market in Pakistan worked 24 years ago.

Back in the day …

In order to comprehend what has happened, there is a need to go back in time. In the 90s and the early 2000s, the capital markets of Pakistan were like the Wild West. There was little that existed in terms of rules and regulations and there was a blase at-

titude towards having a formalized manner of trading. Brokers were not mandated to ask the source of financing for the client, trading could be carried out without any sort of uniform account opening and custody of shares was mostly kept by the brokers rather than giving them over to the clients.

Much of this has changed since. Accounts are only opened after a thorough Know Your Client (KYC) procedure has been carried out. Brokers need to record the orders being placed with them by the client and the shares of the clients are deposited with the Central Depository Company (CDC) once they are bought or sold. Any movement in these

shares is communicated to the clients on that day and, in case they feel something untoward has happened, they can report this discrepancy to the relevant authorities.

Back in the early 2000s, none of these systems were in place. In order to place an order with the broker, the client would contact their agent and place a trade with them. These agents are people who have been hired by the brokerage house and act as a liaison between the company and the client. The client would contact the agent and ask them to place a trade. Any trust the client had in the brokerage house was based on his relationship with the agent and the agent would be the only point of contact. As the controls were not stringent, the agent could buy the shares for the client and place them in their own account rather than being mandated to deposit them in the client’s account. This is where the story of this case starts.

The case in question

Our story begins in 2000 when a client by the name of Abdul Wahab Memon was trading through the brokerage house of Siddiq Moti. Memon had a system in which he would buy shares for himself through a man called Nadeem Hussain. Nadeem Hussain would take the funds from Memon and then buy shares on his behalf. As Nadeem Hussain was the man in contact with the brokerage house, he was considered the de facto authority in regards to investments being made by Memon. Hussain would not contact the brokerage house or Moti himself. The way things work at the stock exchange is that the broker hires agents who are the sole point of contact between the client and the broker. They act as the liaison between the two parties. Many times, the trust that the client has in a broker is based on his rapport and relationship with the agent rather than the owner of the brokerage house. The agent in this case was named Junaid Ali.

In the course of business it was seen that shares that had been bought by Memon had been sold by the broker without any prior approval. At this juncture, it might seem absurd that how can an asset be sold without getting the necessary approvals from the clients themselves. This reflects on how unregulated the market was that the agent and the broker had the power and authority to sell the client’s shares so easily. Seeing that his shares had been sold, Memon contacted the then Karachi Stock Exchange to resolve his issue. In light of the issue being raised, the SECP launched its own investigation to get to the bottom of the case and to compensate the aggrieved party. When Siddiq Moti was asked regarding the unauthorized sale, he stated that the shares had been transferred to Junaid Ali at the behest

of Naeem Hussain who was acting on the implied authority given to him by the client. This authority was implied as Hussain was already dealing and instructing on behalf of Memon with Moti’s brokerage house.

The broker was not able to present any signed or validated authorization that was given to him by the client and that no such sale had been instructed by him to transfer the shares to Junaid Ali or Naeem Hussain. One additional wrinkle that was present in the case was the fact that the account opening form of the brokerage house stated that at any time, Siddiq Moti was authorized to move or sell shares for settlement purposes if the client was not able to meet the dues pending on his side. Even though this had been codified in the form, Moti’s counsel was not able to substantiate the sale which would have been authorized against any outstanding dues. The SECP felt that the shares had been transferred wrongfully and they needed to be given back to the client accordingly.

What happened next

The SECP issued that original order on 1st of March 2001 and expected the client to be compensated in a rightful manner. The expectation was that the broker would accommodate the client by transferring the shares that had been taken away. In the face of these circumstances, the broker decided to appeal the decision before the appellate bench at the SECP. The bench heard both sides of the argument and saw that Siddiq Moti had been in the wrong. The appellate bench dismissed the appeal by June of 2001. The bench also stated that the actions taken by Hussain could lead to separate legal proceedings against him as well.

The last statement became prophetic as another subsequent order was passed by the SECP against Sidddiq Moti in September 2009. This time, the complaint was filed by Nadeem Hussain himself who was lodging a complaint against Siddiq Moti. The new complaint stated that Nadeem Hussain had been working with the brokerage house for many years and had built a rapport with Junaid Ali. As Hussain had knowledge regarding trading in the exchange, many of his relatives also started to give him money to invest on their behalf. On 19th of May 2000, the CDC report taken by Hussain showed that his position was accurately being represented. Later, he was asked by his relatives to sell their shares to give them back their investment. When Hussain contacted Ali to sell his shares, he was told that no such shares existed and that his investment had made a loss. When the CDC report was checked again, many of the shares had been sold or transferred without prior approval or authorization.

As the new complaint had been filed, the

SECP stepped in again and tried to gather the facts of the case. After their investigation, they issued an order in favour of Nadeem Hussain. Siddiq Moti again appealed this order and went in front of appellate bench to contest the punishment handed down. Moti and his counsel contended that they had not been given a fair chance to present their case and that any such dispute should have been placed in front of the arbitration body of the Karachi Stock Exchange. The counsel also stated that the new complaint filed in 2006 was different to the one filed in 2000 and contradicted the one that was made earlier. The appellate bench stressed yet again that the main complaint raised by the client was that their shares had been transferred without any authorisation which was underlined in Section 24(2) of Central Depository Act 1997. When Moti’s counsel was asked to provide any evidence of such authorisation, they failed to provide any document. On 22nd of May 2015, the bench dismissed the appeal and maintained the order issued by the SECP.

Once Moti had exhausted his legal options for appealing the decision with SECP, an appeal was filed in the Islamabad High Court to resolve this issue. The Court looked at all the aspects of the cases and determined that the broker had broken the pact that existed between the client and himself which had been codified in laws of Central Depository Act of 1997 and the shares have to be given or transferred back to the client. Siddiq Moti has passed away so the appeal was filed by his legal heirs.

The fact that this is a victory for the SECP still stands true, even though the loopholes that existed back in 2000 have been closed to a huge extent. The goal of the regulator is to build confidence of the investing public in the markets and this goes a step in the right direction. The Court also approved of the fact that the Commission had carried out its proceedings without any procedural or legal flaws. Since 2000, the account opening forms have been standardized and the language has been tightened to make sure no grey areas exist in regards to brokers using their client’s shares. Affidavit and signed authority is mandated before any trade for the client can be carried out. In addition to these steps, clients are updated regarding their trade activity on a daily basis and they can access their account reports by themselves as well. In regards to the broker, the SECP mandates the broker to maintain records and report clients’ assets segregation on a fortnightly basis to make sure client’s assets are protected. All these measures have been implemented by SECP to make sure the markets are protected and that red flags are raised in case any broker tries to circumvent or break the rules in a proactive manner.

the quiet growth story in the automotive industry Panther Tyres:

The company grew revenues by 38% in fiscal 2024 even as the industry struggled with slowing sales of cars and other automobiles

PProfit Report

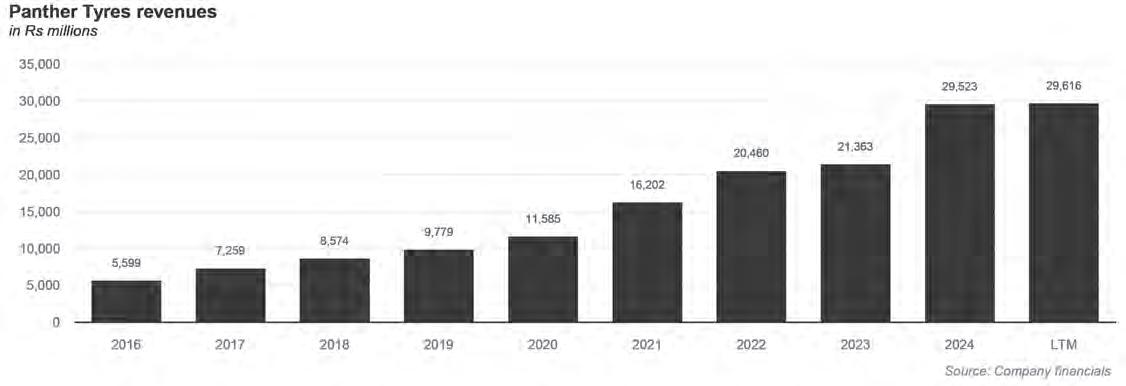

anther Tyres Ltd. (PTL), a leading manufacturer of tyres and automotive components in Pakistan, reported a robust 38% year-onyear increase in revenue for the fiscal year ending June 30, 2024, driven by higher sales volumes and strong performance across domestic and export markets.

The company’s topline reached Rs29.5 billion in fiscal year 2024, compared with Rs21.4 billion the previous year, a 38% increase. Approximately 70% of sales stemmed from the replacement market, 15% from original equipment manufacturers (OEMs), and 15% from exports.

Export sales rose to Rs3.6 billion in fiscal year 2024, up from Rs3.1 billion in fiscal year 2023, with Turkey, Egypt, and Brazil emerging as key markets. Panther Tyres exported its full product portfolio, including tractor, off-theroad (OTR), and motorcycle tyres, highlighting its expanding global footprint.

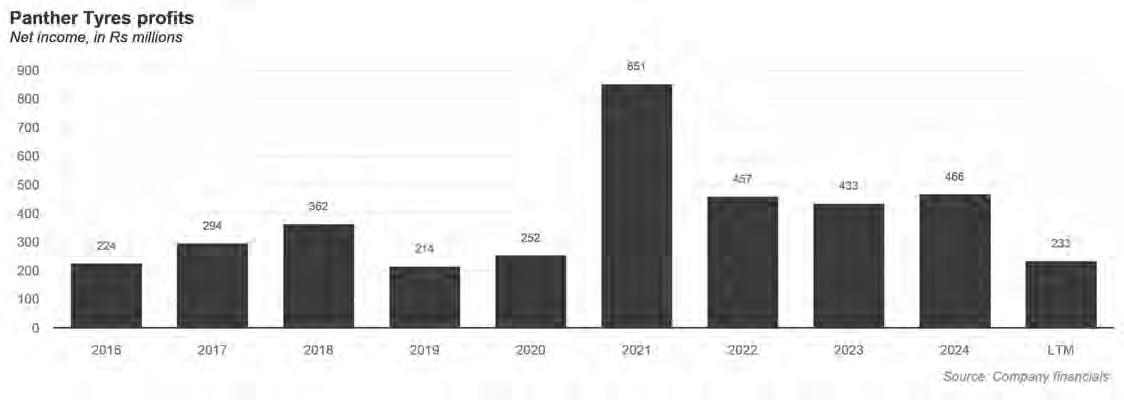

Net earnings grew by 7.6% to Rs466 million (EPS: Rs2.77) in fiscal year 2024, compared with Rs433 million (EPS: Rs2.58) in

fiscal year 2023. Despite the surge in revenue, higher financing costs limited profit growth. Gross margins remained flat at 14.6% versus 14.5% in fiscal year 2023, as the company prioritised volume growth.

However, gross margins for the first quarter of fiscal year 2025 dipped to 11.5%, reflecting a surge in international rubber prices that the company was unable to fully pass on to consumers. Management expects a seasonal reduction in demand and falling rubber prices to ease margin pressures in the coming quarters.

“We believe the declining international rubber prices would help improve profitability of the company. Moreover, demand outlook from the replacement market seems promising amid improving economic indicators,” wrote Osama Naeem, an equity research analyst at AKD Securities, an investment bank, in a note issued to clients last week.

Panther Tyres significantly ramped up its production capacity in fiscal year 2024, completing capital expenditures in its mixing department and machinery upgrades. Tyre capacity increased to 9.7 million units, up from 8.1 million in fiscal year 2023, while produc-

tion jumped 44% to 6.3 million units.

Similarly, tube capacity rose to 40.6 million units from 31.5 million, although production saw a marginal 1% decline to 21.2 million units. Management anticipates these investments will yield greater returns in the next fiscal year.

The company grappled with market challenges, including smuggling and under-invoicing, which erode profitability. Government efforts to curb smuggling have shown progress, but under-invoicing remains a persistent problem.

Looking ahead, Panther Tyres plans to commission new machinery for OTR tyre production by year-end, potentially unlocking additional revenue streams in fiscal year 2025.

To meet its energy needs, the company relies on a mix of grid power (11 MW) and captive generation (7–8 MW), ensuring operational continuity amid Pakistan’s energy constraints.

Founded in 1983 and listed on the Pakistan Stock Exchange since 2021, Panther Tyres is among Pakistan’s largest tyre manufacturers. Panther Tyres, originally established as Mian Tyre and Rubber Company Limited,

changed its name to Panther Tyres Limited in October 2011. The company converted to a public limited company in 2003 and was listed on the Pakistan Stock Exchange in February 2021.

Panther Tyres Limited was the first player in Pakistan to introduce local manufacturing of tyres for two and three wheelers and currently has a stronghold in the two and three wheeler tyre market. Over time, the Company has also expanded into other segments of the auto industry including tyres for tractors, light commercial vehicles, trucks, buses and earth movers.

Today, the company offers a wide range of products, including tyres and tubes for motorcycles, tractors, rickshaws, trucks, buses,

and earth movers, motorcycle and diesel engine oils, auto parts such as chains, sprockets, brake shoes, and air filters.

Panther Tyres serves both original equipment manufacturers (OEMs) and replacement markets. It has established strong partnerships with major motorcycle manufacturers like Suzuki, Honda, and Yamaha.

Fundamentally, though, it is a replacement tyre manufacturer, which has a special significance in a country like Pakistan where people keep their cars and motorcycles running for decades, meaning that they tend to need replacement parts several times over the course of their useful lives. Panther is the leading tyre replacement manufacturer.

Think of it this way: you buy a new

Honda or Yamaha motorcycle and it has all original parts for at least the first few years. As you need more replacement parts, you are likely to turn not to original Honda or Yamaha parts, but to off-brand parts, and among those “off-brand” manufacturers, Panther is one of the largest ones for tyres.

Panther Tyres was also the first tyre exporter of Pakistan. The Company started exporting “Made in Pakistan” wheelbarrow tyres and tubes to European markets as early as in 1996. Today, the company has a significant export presence, selling its products to various countries across Asia, the Middle East, Africa, and Europe. As of 2023, Panther Tyres was exporting to 14 countries, with export sales constituting 14.6% of its total sales mix. n

Unity Foods to expand Sunridge retail presence as its core growth strategy

Long

a

manufacturer

of

food product ingredients for other industrial food companies, Unity is seeking to expand its own retail brand presence

Profit Report

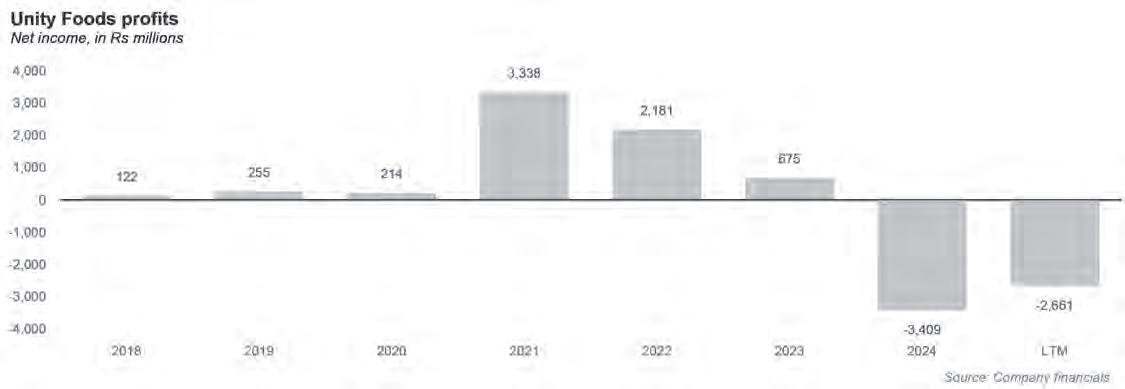

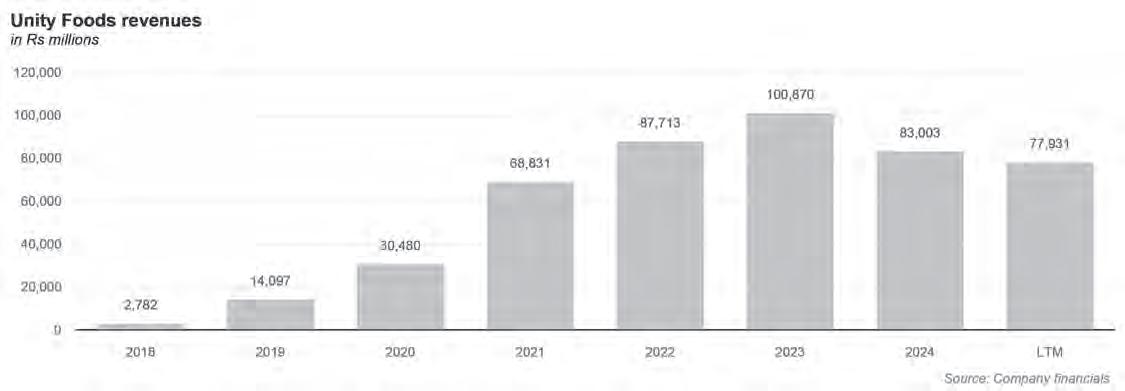

Unity Foods, one of Pakistan’s leading food conglomerates, is doubling down on its Sunridge brand, a fast-growing player in the wheat flour segment. The company’s retail strategy saw significant gains in fiscal year 2024, as it expanded its footprint with new Sunridge-branded outlets and diversified its product offerings.

Sunridge, which accounted for 27% of Unity’s Rs83 billion revenue in fiscal year 2024—up sharply from 11% in fiscal year

2023—has become a cornerstone of the company’s transition from an edible oil-focused business to a comprehensive staples provider. To bolster brand awareness, Unity launched seven dedicated Sunridge marts and four kiosks in fiscal year 2024, showcasing over 100 stock-keeping units (SKUs).

The company views these retail outlets as a superior branding tool compared to traditional advertising. Plans are already in motion to extend this retail strategy to Lahore, a key metropolitan market.

Despite Sunridge’s growth, edible oil remained Unity’s largest revenue driver, contributing 48% to fiscal year 2024 sales. However,

the segment saw challenges, with consumer pack sales declining due to high interest rates and extended cash cycles. The edible oil business was further pressured by a supply glut from increased palm oil imports in fiscal year 2023.

Unity is optimistic about recovery, with management projecting 80-85% capacity utilisation for edible oil and wheat in fiscal years 2025 and 2026.

Unity’s export revenues surged to Rs7.86 billion in fiscal year 2024, a dramatic rise from Rs0.86 billion the previous year, with the company now exporting to eight countries. Management sees significant export potential,

particularly in rice and confectionery, as it scales operations.

Additionally, Unity has invested in capacity expansions across multiple categories, including edible oil, flour, rice, and confectionery, and installed a 2MW solar plant to reduce energy costs.

Like many businesses, Unity grappled with inflation and high borrowing costs in fiscal year 2024, which drove up finance expenses to Rs7.44 billion from Rs3.56 billion in fiscal year 2023. Distribution and administrative expenses as a percentage of sales also rose due to product diversification and export-related costs.

Management anticipates cost relief as interest rates decline in the near term. Meanwhile, international palm oil prices are expected to remain stable despite volatile weather patterns impacting supply.

Unity’s strategy signals a pivot toward becoming a full-spectrum staples provider, with the Sunridge brand at the forefront. With its retail footprint expanding and export markets growing, the company is poised for steady growth.

The company known today as Unity Foods originally started its life as Taha Spinning Mills, a textile company that went bankrupt in

2008. In 2016, a new ownership and management team agreed to buy out the company in a backdoor IPO of sorts, and in 2017, the company raised Rs1.65 billion through a rights share offering that helped it finance an expansion of its edible oil production business.

The company today offers a wide range of food products, including edible oils and fats, staples such as flour, rice, lentils, and pulses, industrial fats, animal feed ingredients for poultry and livestock, and specialty fats for chocolate, confectionery, and bakery products

The company markets its products under several brand names, including sunridge (for staples like atta, all-purpose flour, chickpea flour, semolina, salt, and rice), Dastak, Ehtimam, Zauqeen, Lagan, and Unity Oil (for oils and banaspati products), and Pure (for animal feed products).

Unity Foods has a large domestic presence in Pakistan and has expanded its reach to international markets. The company exports its products to various countries across Asia, the Middle East, Africa, and Europe, including Sri Lanka, Malaysia, Vietnam, Bangladesh, the United Arab Emirates, China, and Singapore.

In early 2024, a significant stake in the company was acquired by Wilmar International

Ltd, a Singaporean food processing and investment holding company with more than 300 subsidiary companies. Founded in 1991, it is one of Asia's leading agribusiness groups alongside the COFCO Group. It ranks amongst the largest listed companies by market capitalisation on the Singapore Exchange (SGX).

Wilmar had been part of the initial acquisition of the company in 2016, and its increased shareholding this year was viewed by the market as a sign that the company’s prospects were viewed favourably by its foreign investors, a rarity in the Pakistani market these days, where many longstanding foreign investors have faced years-long delays in being able to repatriate their profits back to their home countries.

Wilmar International business activities include oil palm cultivation, edible oils refining, oilseeds crushing, consumer pack edible oils processing and merchandising, specialty fats, oleochemicals, and biodiesel manufacturing, grains processing and merchandising, and sugar milling and refining. It has over 500 manufacturing plants and an extensive distribution network covering China, Indonesia, India and some 50 other countries. The group employs a multinational workforce of more than 100,000 people. n

Treet continues its struggle, despite some favourable tailwinds

The company’s razor blade division continues its sluggish growth, but even the battery division has failed to take advantage of the skyrocketing demand for rooftop solar energy systems in Pakistan

Profit Report

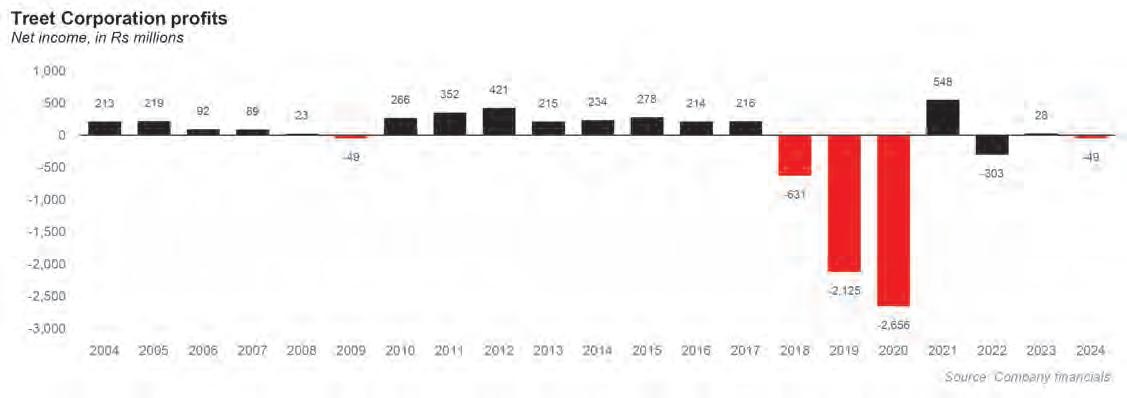

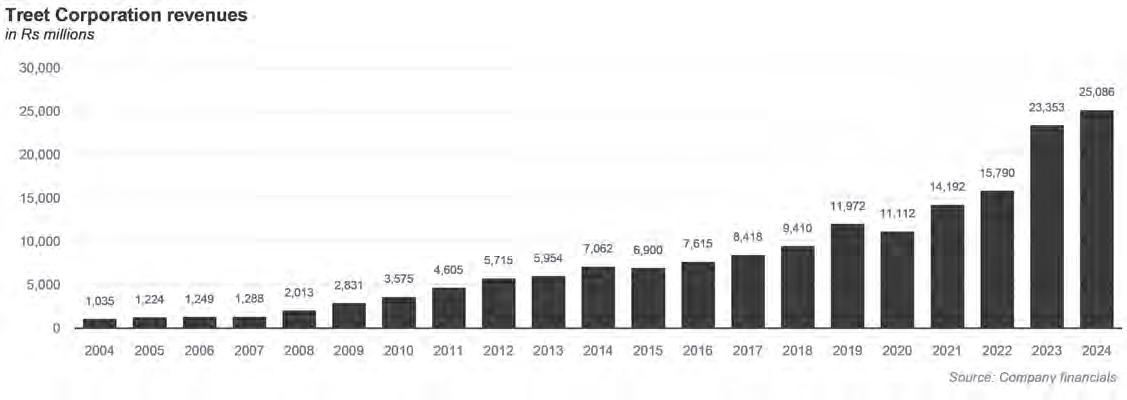

Treet Corporation Ltd., one Pakistan's leading razor blade manufacturers, is facing headwinds in its core business. The company reported a loss of Rs131 million for fiscal year 2024, despite a 7.4% increase in overall revenue to Rs25 billion.

Treet's flagship razor and blade segment, which accounts for over 40% of its revenue, has seen sluggish growth in recent years. Industry analysts attribute this trend to the growing popularity of beards among Pakistani men, influenced by religious and cultural factors. This shift has led to reduced demand for razor blades, forcing the company to explore diversification strategies.

"We've changed our philosophy from high volume, low profitability to high profitability and low volumes," said Syed Sheharyar Ali, CEO of Treet Corporation, in a recent interview. "While the number of units are less, the value of the topline will be higher."

In an effort to offset the challenges in its core business, Treet has been expanding into other sectors, including battery manufacturing through its subsidiary, Treet Battery Ltd. (TBL). However, despite the booming solar

energy market in Pakistan, which has seen a surge in demand for batteries, TBL reported a loss of 286 million rupees ($1 million) for the fiscal year.

The loss at TBL comes as a surprise to many industry observers, given Pakistan's rapidly growing solar energy sector. The country imported an unprecedented 13 gigawatts of solar modules in the first half of 2023, making it the third-largest destination for Chinese solar exporters. This solar boom was expected to drive demand for batteries, which are crucial for energy storage in solar power systems.

Treet's management attributed TBL's losses to higher warranty and advertisement expenses, despite a 41% year-on-year increase in operating profit to 859 million rupees ($3 million). The company faces stiff competition in the battery market and has been investing heavily in marketing to establish its brand presence.

The corporation's diversification efforts have shown some promise in other areas. Its pharmaceutical subsidiary, Renacon Pharma Ltd., reported a 181% increase in net profit to 188 million rupees ($0.66 million), driven by higher unit prices and growing exports. Additionally, First Treet Modaraba, another subsidiary, saw a 61% rise in net profit to 266 million rupees ($0.93 million).

Treet Corporation is also expanding internationally, having established a wholly-owned subsidiary, Treet Trading LLC, in the United Arab Emirates for general trading of the company's products.

As Treet navigates the changing landscape of consumer preferences and emerging markets, investors and industry watchers will be keenly observing how the company adapts its strategy to return to profitability in its core business while capitalizing on the opportunities presented by Pakistan's growing renewable energy sector.

Treet is a storied Pakistani company and has the same roots as Packages. The family’s history begins with Syed Wazir Ali, who set up Wazir Industries by serving British troops in pre-colonial India. His son, Syed Maratib Ali, would go on to grow this business by supplying goods to the Raj. After partition, his two sons, Syed Babar Ali and Syed Wajid Ali, would take over their father’s business. Over time, Babar Ali would go on to hold most of the Packages Group while his brother Wajid Ali took control of the Treet Group.

Initially, Treet was the sole assembler of cars for the Ford Car Company in South Asia. The company then went on to manufacture oil and vegetable ghee under the name of Khopra Oil Mills and Wazir Ali Industries. But they

really struck gold with carbon steel blades, which they began to produce in 1954 in a Hyderabad plant. This was a time when the clean shaven look was not just in fashion but a professional requirement. People needed to shave, and the safety razor (invented in 1904) was not common in Pakistan yet. In fact, most of the English would have their own shaving supplies that weren’t locally produced.

Treet made a fortune by providing high quality and cleanly packaged blades to every corner store barber, hotel saloons, and even those sitting under trees with a chair and a mirror offering shaving services. The blade

business was a success, and for a very long time it stayed that way. In 1984, they started producing stainless steel blades at a plant in Lahore. In 1986, as consumer trends caught up and disposable razors became more common, they began to produce those too.

The upward trajectory of its success can be gauged by the fact that by 1996 Treet had started to export blades and razors. By the year 2000, they were able to launch industrial blades for all kinds of machinery and hard tools.

The company started to diversify in order to reduce its dependence on the company’s traditional products. The goal was to find new

revenue streams by capitalizing on the strong brand name and financial position of the company. This was going to serve as the launch pad which would ensure long term growth and stability to the company.

This drive saw the company setting up a corrugated packaging plant in 2006. This was actually one of Sheharyar’s first efforts in diversifying his family’s business. For four years before this, he had worked at his uncle Babar Ali’s company Packages. Here he had learned the ropes of the packaging business, and wanted to set up a similar business for his own immediate family’s corporate interests. n

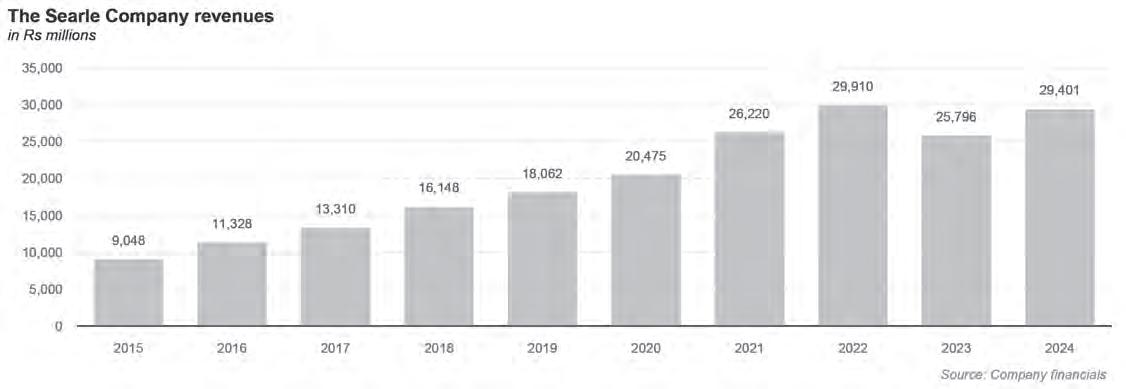

Despite deregulated prices, Searle swings to a loss

Price increases were not enough to compensate for increases in operating costs, despite a gross profit margin expansion

Profit Report

The deregulation of prices may have resulted in a significant increase in revenues for The Searle Company, but losses widened as costs continued to skyrocket for the company.

The company reported a 14% year-overyear increase in revenue, reaching Rs29.4 billion in the financial year ending June 30, 2024, up from Rs26.2 billion in the previous financial year. This growth was primarily driven by price

increases following the deregulation of non-essential drugs and a one-time price hike for essential medications. Despite the revenue boost, Searle posted a significant loss of Rs2.3 billion for the year, translating to a loss of Rs4.46 per share. This marks a substantial decline from the previous year's loss of Rs0.6 billion.

On a positive note, gross margins improved to 47.4% from 41.3% in fiscal 2023, reflecting the impact of price adjustments and operational efficiencies. The company's export business contributed 11% to total sales, with products now reaching 12 countries.

Searle is actively pursuing international expansion, having recently obtained registration to sell products in Uzbekistan and Azerbaijan. The company has also registered a facility in the Gulf Cooperation Council region, anticipating increased demand from these markets.

In a strategic move to diversify its portfolio, Searle has entered the monoclonal antibody segment with the launch of 'Adalimumab', boasting impressive margins between 65-80%. The company currently faces no local competition in this high-value segment and

has additional monoclonal antibody products in development.

Looking ahead, Searle is preparing to launch 'Semaglutide', a diabetes medication, with production facilities already secured. The product is expected to hit the market next year in pen form, potentially opening new revenue streams for the company.

While Searle navigates challenges in profitability, its focus on expanding into new markets and high-margin product segments suggests a strategic approach to long-term growth in the competitive pharmaceutical industry.

Searle's product range covers diverse therapeutic areas, including cardiovascular, respiratory care, gastroenterology, pain management, central nervous system (CNS), orthopedics, neuropsychiatry, antibiotics, and nutritional care. Some of its flagship products include GlucoMet and GlucoMet-Forte for diabetes management and Nuberol Forte for pain relief.

The Searle Company Limited was established in Pakistan in October 1965 as a private limited company. It began as a subsidiary of G.D. Searle & Company, a global pharmaceutical firm, marking the company's entry into the South Asian market.

Initially based in Karachi, Searle focused on setting up manufacturing facilities and building a distribution network. The company quickly gained recognition for introducing innovative and high-quality medicines to the Pakistani market.

Throughout the 1970s and 1980s, Searle expanded its product portfolio to cover a wide range of therapeutic areas, including cardiovascular, gastrointestinal, metabolic disorders, respiratory, and infectious diseases.

In November 1993, the company was converted into a public limited company under the Companies Ordinance, 1984 (now Companies Act, 2017).

In the 1980s, Searle introduced GlucoMet and GlucoMet-Forte for diabetes management, which became flagship products. The 1990s saw the launch of Nuberol Forte, which quickly became one of Pakistan's most popular pain relief medications.

In 1987, the company was acquired by local management, becoming an independent entity from its global parent company.

Currently, International Brands (Private) Limited is the parent company, holding a 56.32% stake in Searle.

By 2020, Searle had grown to command

a 6.5% market share in Pakistan's pharmaceutical sector, up from 5.3% the previous year. That same year, the company began importing remdesivir, one of the drugs used in treating Covid-19, from a manufacturer in Bangladesh. The move was a direct attempt at competing against Ferzonsons Laboratories, which had entered into a direct agreement with US-based life sciences giant Gilead Sciences to manufacture remdesivir in Pakistan.

The company has been expanding its global footprint, with exports to 12 countries as of 2024. It has recently obtained registration to sell products in Uzbekistan and Azerbaijan and has registered a facility in the Gulf Cooperation Council region.

Searle has entered the monoclonal antibody segment with the launch of 'Adalimumab' and is preparing to introduce 'Semaglutide', a diabetes medication.

Today, The Searle Company operates three manufacturing plants in Karachi and Lahore, along with various warehouses and storage facilities across Pakistan. It continues to be a major player in Pakistan's pharmaceutical industry, focusing on manufacturing and selling pharmaceutical, consumer health, and nutritional products. n

The GMO oilseed saga is not quite over

After the Climate Change Ministry gave its approval to 55 importers, the food ministry is unhappy with the new quagmire coming its way

By Ghulam Abbas

It seems that the controversy that has surrounded the import of Genetically Modified (GMO) oilseeds in Pakistan has not quite died out, despite the government giving the all clear to a number of importers in October.

The two-year long struggle that has seen GMO soybeans coming from the United States of America become a major point of contention between Pakistan’s local solvent

extraction industry and the federal government, particularly the Ministry for National Food Security & Research and the Climate Change Ministry. Soybeans are an important component in the manufacturing of edible oil, but more importantly are the key input in Pakistan’s poultry industry, which uses meals made from these seeds to feed their birds. Back in the latter half of 2022, the import of these soybeans had been halted by the government because the beans were genetically modi-

fied, causing significant strain to the poultry industry. However, the government raised concerns over the entry of GMO products into Pakistan because of its participation in the international Cartagena protocol.

The ban was lifted last month following robust advocacy and lobbying not just from Pakistan’s poultry industry, which benefits from the cheaper GMO beans, but also from exporters based in the United States as well as the United States Embassy in Islamabad, which has been playing a role in pushing the

While all of these efforts bore fruits, sources from within the food ministry have told Profit that the ministry is struggling to deal with the load of allowing these imports while also maintaining conducting risk assessments for 47 gene events in local conditions, as mandated by Article 15 of the Cartagena Protocol. So what exactly is going on, what are the concerns surrounding it, and are there any answers?

The buildup

The equation here is a very simple one. Pakistan is a very major importer of oilseeds like soybeans and palm oil. The vast majority of these $4 billion imports are made up of palm oil, which is used to make Vanaspati Ghee. However, other oilseeds like Canola, Sunflower, and Soybean are used to extract edible oil as well as make poultry meals. Even cotton seeds are used to make these poultry meals. This is the main purpose of importing soybeans to Pakistan.

Now, the United States is a major grower of soybeans across its farming belt in states such as Illinois, Kansas, Iowa, and Missouri. These soybeans are genetically modified and give higher yields making them cheaper. The US uses these beans domestically but also exports them to a number of countries including Sri Lanka, Bangladesh, and India which use them in their poultry production. Pakistan was also among these importers, but in December 2022, a dramatic episode took place which Profit covered in depth.

To cut a very long story short, It all started with a technicality — but a technicality that was being ignored for a few years. On October 20, 2022, two shipments were stopped at Port Qasim in Karachi. The shipments contained GMO oilseeds worth some $100 million on board. And despite the very vocal protestations of the importers that had paid for the consignments, they stayed stuck at the port pending a single certification from the ministry of climate change. The climate ministry was concerned that the oilseeds were GMOs. In the months that followed, more vessels joined the two stuck at Karachi and the value of the oilseeds piling up at the port grew over $300 million.

The lobbying begins

This naturally led to importers whose consignments were stuck panicking. They would have to suffer losses if they re-exported the containers to countries where the import of GMO products was allowed. Immediately, they began to try to convince the government to remove the ban. The ban had been put in place by the En-

Are GMOs safe?

There is a general fear of GMOs in many places across the globe, fears that are completely unfounded and not based on any scientific research. The reality is that farmers and agricultural scientists have been involved in genetically modifying the food we eat for a very long time.

“For many decades, in addition to traditional crossbreeding, agricultural scientists have used radiation and chemicals to induce gene mutations in edible crops in attempts to achieve desired characteristics,” reads an article by Jane Brody published in The New York Times back in 2018. This is where there is a parting of ways, and one that is very important to understand. Everyone agrees that genetic modification has been in place for centuries now. Farmers have used cross-breeding or both livestock and crops to achieve better yields and resistance to weather. What is new, however, is that there are now possibilities of extracting genes from other organisms and including them in different organisms. For example, to make a certain maize crop more resistant to cold, scientists might extract a gene from a fish that swims in icy waters and inject it in the maize. It really is a scientific marvel, and at the same time it makes sense that eyebrows would be raised over this level of interference in nature. But by and large, the scientific community has upheld that GMOs are safe.

“Although about 90% of scientists believe GMOs are safe — a view endorsed by the American Medical Association, the National Academy of Sciences, the American Association for the Advancement of Science and the World Health Organization — only slightly more than a third of consumers share this belief,” states a report from the United States Food and Drug Administration (FDA). And that is the crux of the problem. Even though the scientific evidence is overwhelmingly in the favour of GMOs, the public perception of GMOs is unfavourable. This is mostly coming from the same brand of pseudo-science that promotes homoeopathic remedies over actual, tested, medicine that works and peddles crystal therapy and all manners of snake-oil.

Robert Goldberg, a plant molecular biologist at the University of California, Los Angeles, says that such fears have not yet been quelled despite “hundreds of millions of genetic experiments involving every type of organism on earth and people eating billions of meals without a problem.” The main problem is that science rarely uses definitive language when a sample size is small or relatively new. In the case of GMOs, for example, scientists maintain a regular level of human error and make statements like “foods have not shown any harmful effect,” rather than saying categorically that a certain food does not have harmful effects.

vironmental Protection Agency (EPA) of the Climate Change Ministry. The decision was taken even though GMO soybeans were being imported to Pakistan from the US since 2015, and the volume of this trade had reached $1.5 billion.

The sudden decision to claim that GMO imports violate international protocols or pose health risks, such as cancer, led both importers and the exporting country to push for the resumption of the trade at any cost. And while the importers were well connected, with a number of politically influential families involved in the poultry business such as the Prime Minister’s son, Hamza Shehbaz, who has a poultry business in Lahore. However, the heavyweight here was the lobbying effort made by the US exporters through US functionaries present in Pakistan.

The issue remained under discussion at various government forums and in courts for months, with the influence of importers and influence even on an ambassadorial level evident. An official source from the Ministry of Commerce confirmed that the United States had raised the issue of GMO soybeans multiple times at various forums, including the

Trade and Investment Framework Agreement (TIFA) signed by the two countries in 2003. As Pakistan’s major export destination, with over $4 billion in exports, the U.S. reportedly told the relevant authorities to resolve the soybean issue swiftly.

The current concerns

This is where things stand. Back in December 2022, when the government first banned the imports, it was a hastily taken decision. In response, importers and the exporters banned together to lobby for resumption of imports. In December 2023, the government allowed the import again but kept delaying releasing shipments, but they finally did so in October this year, and the government has since given 55 licences to importers. However, a number of sources within both ministries have raised suspicions over the actions of the concerned ministries

The central issue here is that the government earlier raised the point of the Cartagena Protocol, which is a Convention on Biological Diversity, signed in 2001 and

ratified in 2009 that Pakistan is party to. The Cartagena Protocol is an international treaty governing the movements of living modified organisms (LMOs) resulting from modern biotechnology from one country to another.

Now, the protocol leaves room for countries to devise their own policies. It also allows them to import GMO grains under the Food or Feed or Processing (FFP) category, and addressed requirements for cultivation only which are understandably much more complex. However, the ministries now seem confused about the necessary process for clearing GMO seeds—whether for food, processing, feed, or cultivation—appears not to have been followed. The Environmental Protection Agency (EPA), under the Ministry of Climate Change, admitted that the licensing process and the subsequent steps were based on decisions made by the previous caretaker government. Officials from the Ministry of National Food Security and Research even expressed reservations about the import of GMO oilseeds.

The licenses granted to over 40 importers are based on approval from the caretaker government’s cabinet, as confirmed by an official source at the Ministry of Climate Change. This raises the question of why an elected government was hesitant to approve this, if such approval was necessary.

Criticism of regulatory procedures

Criticism of the approval process has been widespread. The National Biosafety Committee (NBC), chaired by Secretary Eazaz A. Dar of the Ministry of Climate Change, approved the GMO soybean imports allegedly without conducting risk assessments under local conditions as mandated by Annex-III of the Cartagena Protocol. This move marks a departure from Pakistan’s previously non-GMO status, despite objections from previous prime ministers, such as Nawaz Sharif and Imran Khan, as well as reservations from the Ministry of National Food Security and Research.

Officials at Pakistan Environmental Protection Agency (Pak-EPA), a subsidiary of the Ministry of Climate Change, acknowledged that the approvals were granted based on decisions made by the previous caretaker government. Importantly, the Environmental Protection Council (PEPC), which is mandated to oversee such decisions under the Pakistan Environmental Protection Act of 1997, was reportedly not consulted.

On top of this, Pakistan does have a robust biosafety framework, including 15 institutional biosafety committees (IBCs)

and updated Pakistan Plant Quarantine Rules (2019). However, these resources seem to have been bypassed. Of the licenses granted, only Quaid-e-Azam University’s Department of Environmental Protection conducted a risk assessment. Experts have questioned the scientific rigor and independence of this assessment, completed in just two months. The government has also not informed whether or not there has been any communication with the Biosafety Clearing-House (BCH) and the Cartagena Protocol Secretariat regarding risk assessments and approvals.

Why all these concerns?

Let us get one thing straight. The import of GMO soybeans definitely gives Pakistan’s poultry market a boost, and importing products should not be a complicated process. The main concern raised by alarmists is that if Pakistan imports these GMO seeds, they will not meet the conditions of the Cartagena Protocol. As a result, certain export markets for Pakistani grown products like rice, wheat, and corn, might close their doors out of fear of phytosanitary standards and GMO contamination.

The revised SOP for GMO soybean imports, implemented by NBC, exempts TAC, NBC, and Pak-EPA from responsibility for any harm caused by these imports, holding importers solely accountable for any ecological and public health damages—though the regulations lack penalties for such consequences.

What is important here is for the government to be clear. Pakistan’s poultry industry already has GMO input. Since 2005, Pakistan has been using GMO cotton seeds and these have been used to make poultry meals. But the government first banned the import of GMO seeds without much explanation and have now unbanned them with as little fanfare and explanation. What is needed here is for the government to take the logical step, but also explain itself and make all overtures to the international organisations, and make sure different ministries are doing the work to ensure Pakistan is compliant with international standards and regulations.

Efforts to contact the Ministry of National Food Security and Research for an official stance were unsuccessful, though a relevant official claimed that the ministry opposed GMO imports due to biosafety risks.

However, as one EPA official, speaking on condition of anonymity, stated that the complaint regarding GMOs is based on false accusations. It indicates that the current crisis might also involve some level of jurisdictional head butting between the EPA and

the food ministry. The complaint has been received by the Prime Minister’s office and the relevant ministries, but no action has been taken as of yet. The official further asserted that the decision to allow GMO soybean imports was based on the caretaker government’s cabinet decision, with relevant forums approving it in line with established rules.

Latest Development

After approving over 55 import licenses, the Ministry of Climate Change prompted the Ministry of National Food Security and Research (NFSR) to convene a consultative meeting on Friday, November 29, 2024. The meeting focused on devising strategies to protect and manage the import of GMO soybean, mitigating risks of contamination and spread from the port to processing areas. Chaired by Federal Minister Rana Tanveer, the session included representatives from importing companies, the poultry association, and relevant officials.

Insiders revealed that the food ministry, tasked with ensuring national food security, is facing challenges in making GMO seed imports entirely risk-free. The ministry is currently evaluating measures to minimize spillage during the receipt and processing stages. However, according to sources, the primary responsibility for preventing spillage rests with the importers.

During the meeting, officials proposed the devitalization of imported seeds in the exporting country as a precautionary measure. This process would help reduce the risks associated with GMO seeds. All GMO soybean consignments will undergo strict supervision by the Department of Plant Protection (DPP) during arrival, treatment at accredited facilities, and the devitalization process. Importers are required to transport sealed containers securely to processing sites after completing the devitalization treatment.

The ministry and the DPP have also suggested covering GMO oilseed consignments with polythene bags during transit from the port to processing facilities to prevent leakage. Additionally, importing crushed GMO seeds instead of whole seeds has been discussed as an option to mitigate risks further.

The NFSR, with DPP’s assistance, is finalizing a comprehensive safety mechanism for handling GMO imports. However, an official source admitted that no safety mechanism is entirely risk-free, and the import of GMO soybean will continue to pose a potential threat of contamination and spread. Furthermore, the ministry is yet to conduct a thorough analysis of the risks GMO soybean byproducts may pose to human health. n

Sazgar

and

its ability

to adapt is reaping dividends

The only constants at the company are change and profits

By Zain Naeem

If someone is asked to define the auto sector of Pakistan, the last adjective that would come to mind would be fast-moving. From the early 1990s to now, the Big 3 have sold outdated and antiquated models of cars and the consumers have had little choice in looking for an alternative. Now it seems that the consumers are changing their preferences as they feel their voice is not heard by the traditional manufacturers.

In recent years, the auto industry has been through tough times. In terms of cars sold, June 2022 saw more than 234,000 cars being sold in the country which shrunk to 96,000 by 2023 and further fell to just above 81,000 in June of 2024. This was the worst year in the last two decades which saw sustained growth in the industry. There were a myriad of factors which led to this decrease. Shrinking income, rising prices, depreciating rupee and a limit on imports meant that both supply and demand were impacted. Facing these tough conditions, auto assemblers had two options. They could either choose to reduce prices in order to generate demand or increase the prices in order to earn higher profits. Stuck between a rock and a hard place, they all chose to raise their prices even when their costs fell.

While the Big 3 had to languish with falling sales, Sazgar was able to see not only rising sales but was also able to sell at higher prices. In a space of two years, the company has been the toast of

the town. The company was able to sell 1,600 units in 2023 which grew to 5,300 in 2024. In just the 4 months of 2025, the company has already sold 3,600 units compared to less than a thousand a year ago. The success at the company is not a fluke or out of luck. Engrained in the DNA of Sazgar is a constant need to change and look for the next big thing. The company is adaptive and welcomes change compared to its competitors who choose to ignore it.