08 The changing nature of Pakistan’s Establishment

14 Hascol’s restructuring has excited the market. But does it address the company’s baggage?

20 Sugar industry wrestles with internal politics

23 Millat Tractors expecting a good year with government contracts

25 Interloop aiming to hit $700 million in revenue by 2026

26 When it comes to EMIs, many have tried. Few have succeeded. Here’s why

Profit

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

We talk in Pakistan as though we have an unchanging establishment, dominated by the military. Reality is far more complex, and changing very rapidly, driven by a changing economy.

By Farooq Tirmizi

When the political repression gets to a point where even the economic publications cannot ignore it, you know things are getting bad.

At Profit, we like to leave the political analysis to other publications and stick to our lane of business and economics, but given the state of Pakistan’s polity and the rank uncertainty prevailing even as the macroeconomy stabilizes, we must return for a second time to finish off an analysis we started two weeks ago: what is the core structure of Pakistan’s political economy, how has it changed over the past few decades, and what direction is it taking?

In the last piece, we argued that a core feature of Pakistan’s political economy from the 1880s through 2008 was feudalism, and that its time has essentially passed. We alluded to what changes would result from that transition. In this piece, we will delve into those changes in more detail and examine the possibilities of what could come next and explain, to some extent, why political repression in Pakistan getting worse may well be a sign that things are about to turn a corner.

We will also state our conclusion up front: we believe the current iteration of hybrid regime – however long it lasts – is the last time non-democratic government in Pakistan will work. Democracy is the only form of government that will deliver political stability to the country from here on out.

Yes, we are aware of who is in control of the country right now, and how absolute their control is for the moment. We still say this is the last time they will be able to make it work.

To understand why we say that, let us start with a discussion of patronage networks, and the legitimacy that they deliver to any governing regime that relies on them.

Patronage, and legitimacy

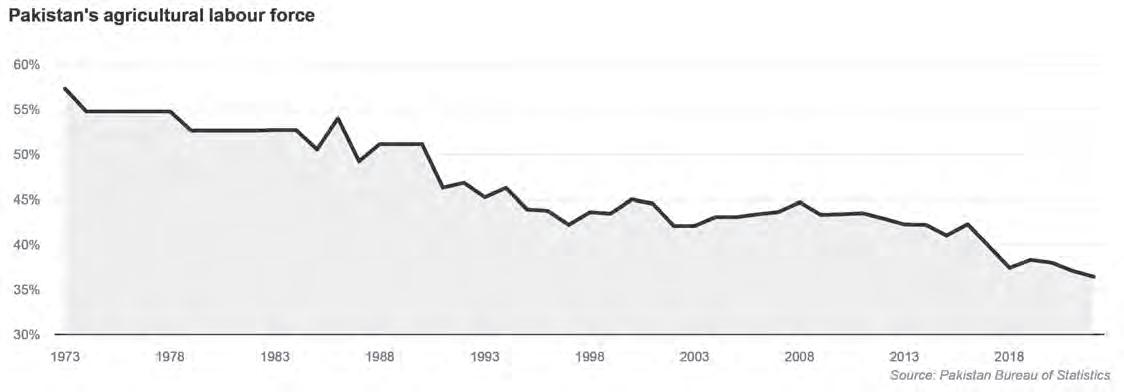

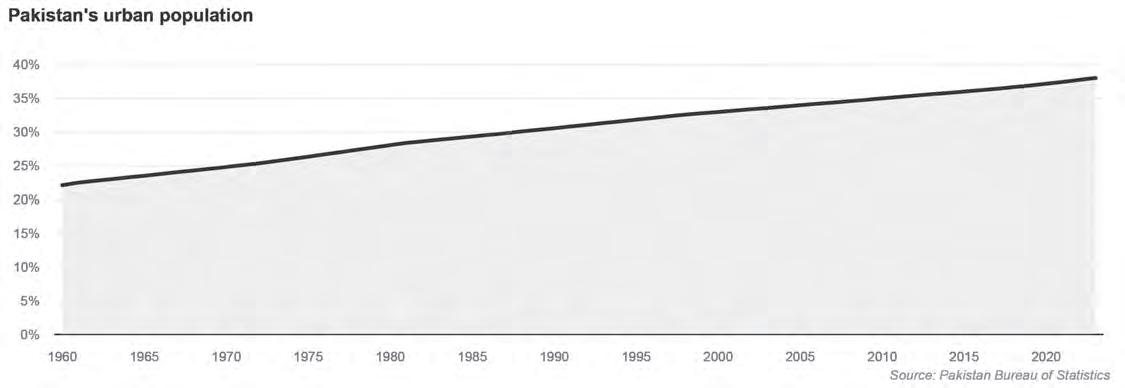

Consider Pakistan at Partition. The population was close 80% rural, and close to 60% of the labour force was employed in agriculture. Of the urban population, a sizeable portion was employed by the government, leaving only a tiny sliver of the population that was not in farming and not employed by the government. Any political regime that kept peace in that rural population was going to have staying power.

Now examine the position of the landed aristocrat and their relationship with the people in their area. The landlord controlled virtually the entirety of the economic resources in their region. This system of control is frequently described as coercive, mainly because it was. But coercion is far from the only thing that kept this regime together. There was a degree of symbiosis between coercive control and collaborative production the delivered a degree of legitimacy of this system.

Simply put, the landlord provided the land and capital, and the population provided the labour needed to produce income from the farms. This was the collaborative piece. The coercion kept social order in the region in the

absence of a strong state to provide that order. Did that order always benefit the landlord? Yes. Was there even the remotest shred of rule of law? Absolutely not.

But the system, in the absence of other economic opportunities and governance mechanism, worked and was broadly accepted as having legitimacy.

So when Pakistan first even contemplated having elections in the 1960s, the notion of anyone other than the landed aristocracy winning elections was not even remotely possible. Consider it a combination of sufficiently aligned incentives and a collective action problem.

If the state is going to be distributing resources, you the farmer want your man in the room where those decisions are made. And in the early decades of Pakistan, your landlord would want many of the same things that would benefit you: functioning canals for irrigation, electricity to run the tubewells, and better roads to reduce the cost of taking the harvest to market.

As the government divvied up the money to build all of that, you the farmer were sufficiently represented by the rural aristocrat who would also stand to benefit from those things.

Yes, you would also benefit from schools and hospitals that the aristocrat decidedly was not particularly keen on pursuing, but that is where the collective action problem comes in: if not the aristocrat, then who else do you vote for to represent your interests? Do you go with an unknown upstart who might push for everything you want, but get nowhere because he had no connections with any of the other rulers, or do you make peace with the aristocrat who gets you only part of what you need, but at least will get that part done?

In the absence of an alternative agreeable to the entire constituency, the aristocrat wins by default.

What we have just described above is a patronage system that delivers a degree of legitimacy to the system of aristocrat-dominat-

ed Pakistani politics, regardless of whether the person at the helm of that system was a civilian prime minister or a general (or field marshal).

But what happens when what the people need or want changes completely.

Declining agricultural labour force

Until 1991, a majority of Pakistan’s labour force was engaged in agriculture. As recently as 2018, more than 40% of Pakistan’s workforce was still engaged in agriculture. Even in 2022 – the latest year for which data is available – about 36% of the labour force is employed in agriculture, according to data from the Pakistan Bureau of Statistics.

Not only is non-agricultural employment on the rise, but the pace of change is accelerating. During the 20 years between 2001 and 2021, the Pakistani economy created approximately 31 million jobs, according to data from the Pakistan Bureau of Statistics. Of those 31 million, only 8 million were in agriculture, or a little over one-quarter. The rest were all in services or manufacturing, and the overwhelming majority of those jobs were in cities.

This is one of the most important changes that has taken place in society. At Partition, for a Pakistani villager to move to the city was a big endeavour for them and their family. Now, it is so common as to be part of the normal set of opportunities under consideration for most people born in rural Pakistan.

What does that do to their relationship with the rural aristocrat? The first thing it does is lower the stakes. The aristocrat’s ability to garner federal or provincial government money for resources for farming in the village is important, but if it does not happen, or does not happen enough to create the kind of income the villager needs, their attitude is more likely to be: “I’ll move to the city, just like my countless other relatives.”

The second thing is does is lower the importance of the rural aristocrat himself. If he speaks for an ever-shrinking portion of the population – and, as we covered two weeks ago, an even faster shrinking portion of the economic pie – then any viable strategy for a path to power must rely on much more than just winning over a sufficient number of rural aristocrats to one’s side.

One needs to win over the cities, and not just the voter who lives in the cities, but the voter who does not consider their economic opportunity set bound to the villages. How does one do that? It turns out that is a question to which the Pakistani Establishment does not yet have a clear answer.

The landed aristocrats still dominate the assemblies. That does not matter

Consider the following facts. In 1972, when Pakistan’s second elected assemblies (the Constituent Assembly was also elected) were first convening, the cabinet in most provinces, as well as the federation consisted of rural landowners. One of the richest men in Pakistan at the time was Ghulam Mustafa Jatoi, by virtue of the fact that he was then the largest landowner in Pakistan. Him becoming Sindh Chief Minister was hardly a surprise.

Can you name the largest rural landowner in Pakistan today? What political office does that person hold?

Let us go one step further. Consider the names of some of the largest rural landowners of Pakistan of the recent past. Where are they in the corridors of power? The grandchildren of the Nawab of Kalabagh Malik Amir Mohammad Khan have been members of the National Assembly as recently as 2013, but not since then.

There are still members of the Jatoi family in the Sindh Assembly. The Makhdooms of Hala

probably have some relatives in elected office. Can you name any of them?

Hina Rabbani Khar, niece of Ghulam Mustafa Khar, has recently served both as Minister of Foreign Affairs and Minister of State for Foreign Affairs. Aside from an occasionally well received public remark, did she actually have a meaningful impact on Pakistani foreign policy?

Name the politicians who have exercised real political power in Pakistan in the past 10 years, and then think of how many of them got to that point because of their lands. Do those people own land in rural areas from which they derive a considerable portion of their income? Yes. Is that why they exercise political power? No.

Now think of all the names that are coming to your mind of the politicians who are large rural landowners and are politically significant. Jahangir Tareen was last in elected office in 2017 and last in the cabinet in 2007. His cousins, the Akhtar brothers (Haroon and Humanyun) have also not been in elected office since 2007.

Admittedly, Shah Mahmood Qureshi has been in the federal cabinet as recently as 2022. Being the Sajjada Nashin of Hazrat Bahauddin Zakaria still has some staying power, it seems. The landed elite still dominates the national and provincial legislatures, and the majority of members of those legislatures own land in rural areas, including former Prime Minister Imran Khan.

But that is the result of the muscle memory of the voting public voting for names they know and recognize. Here is the thing about things that last based on memory: they fade away when the last person who remembers their origin dies. And in Pakistan, where we are about to encounter a demographic dividend, that turnover in memory is about to be faster than ever before.

As for the landowners themselves, they are in the assemblies not because they are landowners, but because they have passive income that allows them the luxury of pursuing political power. Power is shifting from being

dependent on rural politics to being dependent on urban politics. And that shift means that the old structure of relying on these old stalwarts is just not going to work anymore.

Increasingly urban politics

What happens to the voter when they reach a city? Does the importance of patronage networks disappear? Not completely, but it does change its nature.

The urban voter still wants things that are similar to what the rural voter wants. Oh, sure, the rural voter has demands for types of infrastructure that are not directly relevant to cities, but the urban voter fundamentally wants the same thing from the government: infrastructure that helps them live a better life.

In theory, a political patronage network can exist in an urban environment just like they do in rural environments. But the problem with cities is that it is much less clear who that specific patron will be. There is rarely a dominant economic actor because there tends to be a much wider set of opportunities open to urban voters, which in turn means that no single entity can create the kind of economic dominance that exists in rural areas with the rural aristocrats.

This means that there is more space for a disconnect between political power in urban areas than there is in rural areas. Middle class politics, in other words, tends to become important in any country with an increasingly urban population and rarely matters in any country with a mostly rural population.

Urban middle class politicians can still create patronage networks, of course, and Pakistan’s most predominantly urban middle class political party – the Muttahida Qaumi Movement (MQM) – created one that in many ways mirrored that of rural aristocrats in Pakistan’s most cosmopolitan city. But no other city in Pakistan aside from Karachi has seen the

rise of this kind of patronage, and there appears to be no movement in this direction either. And indeed, the MQM’s own patronage network in Karachi appears to have largely collapsed.

So Pakistani politics now finds itself in the position where rural patronage networks are less important than they used to be, and resulting in waning importance of rural aristocrats on the national political stage, but urban patronage networks appear to have no signs of coming into being in quite the same way, meaning that national politics is shifting to a location where the old model cannot be transplanted.

Which then begs the question: what comes next?

Who will be the new elite of Pakistan?

The military cannot rule Pakistan alone. It never has, and it never will. Which means that if your answer to the question of who will rule Pakistan after the collapse of the rural aristocrat-dominated order is the Pakistan Army alone, that is incorrect. There is no evidence the military can rule Pakistan on its own, and the increasingly draconian measures needed to keep even a thin civilian veneer in power demonstrates that the current situation does not represent a new paradigm. Even the military itself is aware that this is a stop-gap measure at best.

We do not claim to have a good answer to this question, but our best guess is that it will be a sub-segment of the old rural elite who can demonstrate to the urban voter that they have the capability to deliver on governance results: better schools, roads, water and sewage, healthcare, and most importantly: predictable rule of law that delivers both order and freedom. That sounds incredibly vague, so let us get a bit more specific. To be elected to the provincial and national assembly will still require any aspiring politician to be inde-

pendently wealthy and have some level of name recognition in their constituencies. That means the sons (and a few daughters) of old political and otherwise influential families.

However, which of the scions of these families gets to rule will not be decided in a backroom deal within their family or between rival political families. It will actually be decided at the ballot box. Why? Because there are now too many of these scions and because the voters now have real expectations when they go vote.

The Pakistani voter recognizes the reality that they are not yet in power but has come to believe, if not in democracy or republicanism, then at least in something more basic: that political legitimacy can only come from the consent of the governed. They believe that they should be the only ones to hire and fire politicians and that the mechanism through which that should take place is the ballot box.

A backroom deal can temporarily put one of those old aristocrats in power, and that aristocrat can then do the bidding of the old Establishment, but this is no longer the system of old where that aristocrat was the one bringing the political legitimacy. Now, all he is bringing is name recognition, and if he is bringing name recognition in service of a goal believed to be illegitimate, he is bringing reputational damage to all those who share that name, meaning their whole family.

Since nobody wants the trouble of making life difficult for their own family, the only people who will be willing to play this game with the Establishment are the most unscrupulous members of the old political families, right when the voter has elevated their expectations of which members of these families they intend to vote for. The ex-McKinsey partner grandson of Ghulam Ishaq Khan who actually did a good job in a provincial cabinet is acceptable to the voters. The snide meme-slinging son and grandson of former prime ministers of Pakistan is not.

And that the current hybrid is unsustainable is demonstrated by the fact that the

following has changed. It used to be that political control in Pakistan relied on the implied threat of force. Now, far from implied, it is actual use of force.

Implied threats are scalable. Actual use of force is not.

The weakest part of our argument

Thus far, we have assumed that the military-led Establishment will be pushed out by the changes we are describing above and will not be able to counter them. The reality is that the military has, in the past, successfully responded to changing circumstances in the country and remained at the helm of affairs, and there is every reason to believe that, as difficult as it is getting for them to maintain control, this may well prove to be a temporary setback from which they recover.

The military in Pakistan is strong for a reason, and that reason is that it has successfully established itself as the arbiter of disputes among Pakistan’s ruling elite, and there is a chance that – even when the ruling elite becomes more diffuse and numerous – that they will be able to retain this role.

Here is why we think this will not happen: this a brave new amorphous world where there is no such thing as permanent political legitimacy in any class of people, let alone specific individuals. If one intends to cobble together a coalition, one needs to deliver on what the voters want, and since one of the core demands of the voters is freedom – something a control-seeking military establishment will always struggle to relinquish – there is no scenario in which they will figure out how to keep their power in a game where the rules are not just different from before, but fundamentally opposed to their perceived self-interest.

This is the swan song of the old Establishment. n

Hascol’s restructuring has excited the market.

But does it address the baggage?company’s

The recent rally in stock price hints at successful restructuring but the fundamental problem still persists

By Zain Naeem

It would not be a stretch of the imagination to say Hascol had a bit of a touch-and-go moment back in 2019. It was the story of a dizzying high followed by what can only be described as an abysmal low.

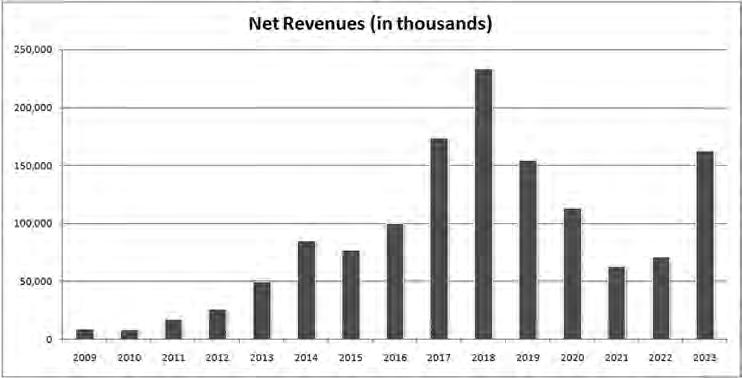

Up until 2018, Hascol was the second largest Oil Marketing Company (OMC) in Pakistan, trailing only the state owned Pakistan State Oil (PSO). In less than a decade from 2009 to 2018, they had grown their revenue from Rs 9 billion to Rs 254 billion. But the growth had come at a price. Hascol had been borrowing to make this growth happen, and in 2019 it turned out they did not quite have the means to pay back their creditors.

Behind this glittery rise and dramatic fall were a host of reasons. Exchange losses, the nature of the OMC business in Pakistan, and Hascol’s unique supply chain all contributed to the company’s crisis of 2019.

But what about now?

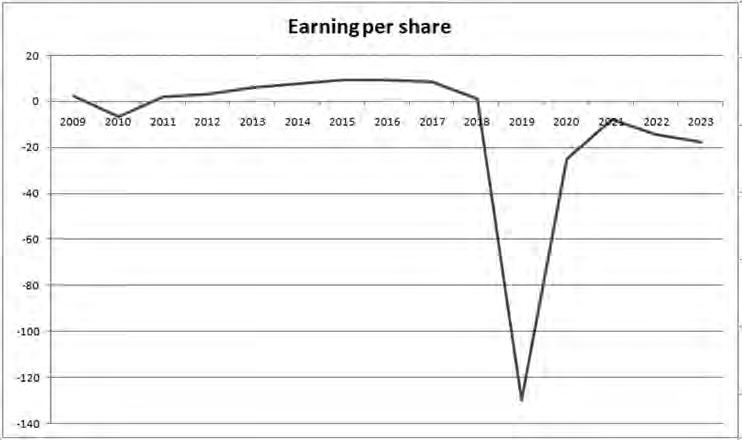

Well, it seems we have a recovery on our hands. For the first time in three years, Hascol’s share price has breached the Rs 10 mark after a wait of more than 3 years. In just a month, the company’s stock price has gone up 92% and the word in the market is that it will continue to increase. What compels a company that was in hot water with its creditors a few years ago suddenly to turn around? The recent rally is ascribed to a successful restructuring plan being passed which will help it get back on its feet.

It seems the restructuring has been enough to at least convince the market that the restructuring will help it to become profitable again. The only question is whether this restructuring will be enough to address the deep rooted issues that brought the company to this brink in the first place.

Understanding the OMC business

The first thing you need to know about Hascol Petroleum is that it is an oil marketing company (OMC). This means it operates its own petrol stations, licences franchisee stations and sells petroleum products throughout the country. It was granted its oil marketing licence in 2005 and saw a meteoric rise as it became the second largest OMC behind Pakistan State Oil by 2018. Guided by Saleem Butt, a veteran energy executive who was its COO and later CEO, the company was able to become the second biggest player in the market. Based on earliest accounts available, it was seen that it was earning net revenues of Rs 9 billion in 2009 which had increased to Rs 234 billion by 2018.

Now, the OMC business is interesting in Pakistan. In many countries around the world, prices of petroleum products are pegged to the price of oil. As the price of oil changes on a daily basis, the rates of the products are changed

regularly. In Pakistan, petroleum prices are determined and set by the Oil & Gas Regulatory Authority (OGRA) on a 15 day basis. This means that oil marketing companies have little to no control over the prices at which they sell. The problem is compounded in bearish markets when companies have bought the oil at a higher price and the local petroleum prices are revised downwards owing to oil markets receding.

In addition to that, oil is imported in its raw form by oil refineries who then sell the refined product to the marketing companies. As oil is traded in dollars, any depreciation of rupee means that even if oil prices remain the same, they cost more to the local companies. Hascol added another layer of complexity to the whole system. Not only were they limited by price increases and were exposed to dollar appreciations, the company was buying most of its fuel from foreign sources. Other OMCs were buying their product from local refinery companies which means their cost is mostly immune to dollar changes. Hascol was following the same model up till 2015 where it was buying most of its fuel from Pakistan Refinery Limited.

You see, in 2015, Hascol changed its model. Vitol, a Dutch energy giant, collaborated with the company to set up a storage facility which added 232,000 cubic metres of capacity. As this partnership developed, Hascol started to import its fuel rather than sourcing it from local refineries. In 2016, records show that it bought 77% of its fuel as import from Vitol Bahrain. By 2017, this had increased to 79%. In 2012, Hascol had bought 70% of its fuel from Pakistan Refinery which started to decrease and in a space of 6 years, imported fuel made up a bulk of its purchases. Vitol also ended up investing as it bought 25% of the shares by 2016. There was also a joint venture for Liquified Natural Gas (LNG) between the two companies as well.

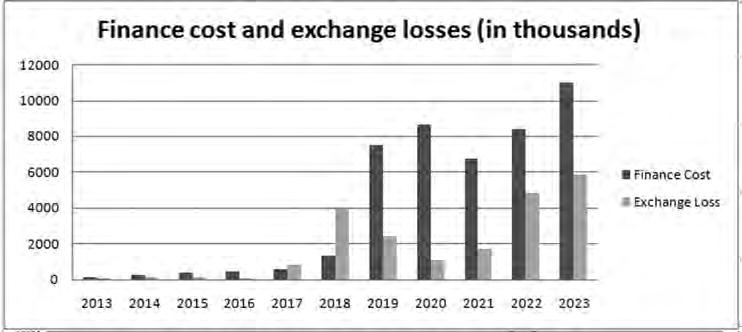

Shifting its source of fuel did not prove to be a problem initially as profits continued to grow. It was only in 2018 that Hascol started to see the impact of its decision. As the rupee started to depreciate, exchange losses jumped from Rs 4 crores to Rs 4 billion in a space of two years alone. Hascol could not increase its margins due to price restriction and as the rupee started to depreciate, the profits started to take a hit.

On top of this, as Hascol started to grow in size, the company started to take loans in order to fund much of its expansion as well. Hascol was able to see gross profits of Rs 10 billion, operating profit of Rs 6 billion due to increased revenues. As the revenues were increasing, Hascol was seeing improved profits, however, net profits actually fell from Rs 2.7 billion in 2017 to Rs 65 crores in 2018. This was primarily caused by exchange losses experienced due to rupee depreciation. To understand the internal workings of Hascol, a deeper understanding of the OMC industry in Pakistan needs to be gained.

It seemed like the worst had already happened but then 2019 rolled around.

The disaster of 2019

The depreciating currency and increasing costs of the companies are a legitimate reason that could lead to a fall in profitability of an OMC. Most of the other companies operating in this space saw losses in 2019 primarily caused by the exchange losses. But the performance at Hascol showed a completely different picture. Companies making losses can be considered to be part and parcel of the industry but Hascol saw losses of Rs 26 billion in 2019 where they had earned a profit of Rs 21 crores just a year ago. It ended up making a gross loss in 2019 of Rs 2 billion which meant that the company sold its products at a lower price which could not even cover its basic costs. In addition to that, additional losses of Rs 6 billion were recorded due to volatility in the oil market. This did not include exchange losses which were Rs 2.4 billion in a separate account and finance costs increased from Rs 1.3 billion to Rs 7.5 billion. The company had been pursuing an aggressive strategy of expanding by borrowing from banks which led to such a huge interest expense. All of these factors contributed to losses of Rs 26 billion being recorded.

The figure of Rs 6 billion in import losses is something that raised concern initially. The fact that the company is stating that it had to bear this loss due to volatility in the market holds little water as none of the other OMCs suffered losses to the same magnitude. Something else that needs to be considered here is that Hascol also restated their accounts for 2018 and 2017 as it felt that it had not transferred complete losses in the previous years. Restatements are normal, however, occurrence of them after the company making huge losses

can be considered a red flag as they can be used to spread losses of current years into past years. Rumours of a scam or a deceptionary scheme were rampant at the company and one way to hide such scams is to record losses. It was uncovered later that some company insiders had allegedly stolen from the company.

Seeing the magnitude of the losses, the creditors of Hascol started to get concerned. Most of the growth was fueled through the use of bank loans and borrowings had increased from Rs 59 crores in 2009 to Rs 92 billion in 2019. Even in the face of losses, more loans were taken in order to finance the working capital needs. As the lenders started to get antsy, there was little that could be done to pay back the loans. The management decided to issue right shares in order to shore up some capital. Vitol also showed trust in the company

as they took their shareholding from 28% to 40% as a show of strength.

With things looking bleak, the company was dealt the final blow in the form of the pandemic as demand for petroleum products plummeted further. Net revenues fell from Rs 154 billion to Rs 113 billion and the company started to see a sustained period of net losses on its books that has not stopped. As the losses had piled up, the company has seen its equity go into the red while its liabilities have ballooned out of control. In 2018, accumulated profits were at Rs 6.2 billion which have plummeted to Rs -107 billion while current liabilities have risen from Rs 56 billion to Rs 120 billion. In total, the liabilities of the company clocked in at Rs 129 billion while its total assets are worth Rs 42 billion.

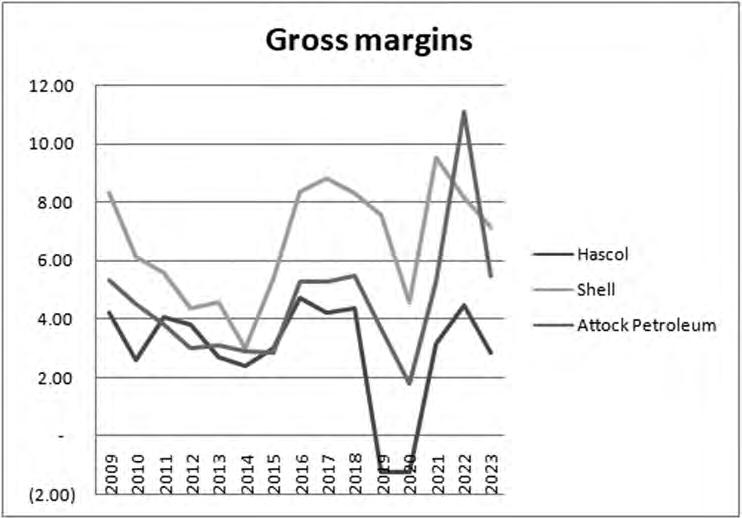

The fundamental flaw that has persisted at the company is that the company started to buy its fuel from foreign sources compared to other OMCs relying on local refineries. As Vitol started to sell to Hascol, the cost of the fuel was much higher compared to the remaining market. From 2009 to 2023, Hascol earned a gross profit margin of 2.96%. At the same time, companies like Shell and Attock Petroleum earned 6.64% and 4.57% respectively. The situation becomes bleaker when the period before Vitol’s investment is considered. From 2009 to 2015, Hascol earned a gross profit margin of 3.27% while in the later part it fell to 2.68%. In the same period, Shell saw a return of 5.33% before 2016 and 7.79% after 2016. Attock Petroleum also saw improved performance as its gross profit margin increased from 3.66% before 2016 to 5.29% after 2016. The only company that is earning similar gross margins as Hascol is Pakistan State Oil (PSO) which saw a similar ratio, however, the net revenues of PSO for 2023 came around Rs 3.6 trillion compared to Rs 162 billion for Hascol. Even if PSO is earning similar margins, the volume of its sales

more than makes up for its lower margins. Hascol does not have any similar saving grace.

This analysis shows that when other companies were seeing better gross margins, Hascol was seeing its gross margins actually fall which raises questions at the business model that the company has been following. While other companies have been able to earn greater gross profits on their margins, Hascol is lagging behind the industry as its gross margins are much lower than the market.

The basic flaw already existed at the company and then the performance of 2019 and the pandemic only made things worse. With debt piling up, even when the revenues have rebounded in 2023, the company is still being buried under higher finance costs resulting from its earlier decision making. The recent depreciation of the currency and the record high interest rates have hit Hascol like a perfect storm.

The rupee has depreciated further from Rs 150 to Rs 280 where it stands now and the interest rates that are being applied by the creditors have hit a record high of 22%. The company has been able to earn gross profits in the last 5 years, however, due to the costs associated, it has made consistent operating and net losses.

The business model chosen seems to be stuck between a rock and a hard place. At one end, Vitol has made a conscious decision to invest in Hascol and to sell oil refined at its subsidiaries to be sold to Hascol which bodes well for its subsidiary in Bahrain. While it does that, it is forcing Hascol to absorb huge losses that cannot be recovered based on the pricing structure that has been put into place. It seems Vitol is fine with maintaining losses on the books of Hascol while it allows its Bahrain subsidiary to earn.

What about all the other stakeholders?

At one end of the spectrum are the lenders who have lent to Hascol and want a path where they can expect to see these funds returned to them. With losses becoming part of the history on a consistent basis, the best course of action for them was

to file petitions against Hascol to recover their funds. The company was looking to restructure the loans of the banks to some extent back in 2019 and had even presented their plan to the courts in 2022 which are under consideration. The options that have been given to the creditors seem lopsided in favour of the company to say the least. The first option was to convert the short term loan into a long term loan to be paid back in 10 years with a grace period of 2 years. This option would not accrue any markup or interest and that all the loan will be paid off in 12 years. The second option is to allow the company to use the short term funds for working capital needs and they will be treated like running finance facilities which will be paid back in a minimum period of 10 years as well. The last option available is to take a 70% cut and to get the remaining 30% in order to waive off all the rest of the liability that is owed.

While this has been going on, the Federal Investigation Agency (FIA) and Securities and Exchange Commission of Pakistan (SECP) have also tried to carry out an investigation against the company to uncover whether something other than normal had taken place. FIA launched a probe into an alleged Rs 54 billion scam that had taken place at the company. The investigation stated that Hascol, Byco Petroleum and management at National Bank of Pakistan had conspired to gain loans

in violation of risk controls and banking practices. The SECP also wanted to launch their own investigation by carrying out a forensic audit which was thwarted by Hascol when it approached the Sindh High Court.

Some recent developments have come to light which might show that the situation at the company might be changing. First, Taj Petroleum stated that they were interested in taking over the company in 2023 and, a few months back, Millat Global Holdings showed an interest to buy the major shareholding from the substantial shareholder of the company. Neither of these negotiations amounted to anything but now it seems that there is interest in the company. For the first time in three years, the share price of the company has crossed the Rs 10 mark after languishing in single digits.

The restructuring gambit

The rise in the share price does signal towards the fact that some sort of restructuring will take place in the coming days, however, considering that as the cure to all the ills will be premature. The financial turmoil the company has faced is still persisting with losses being suffered and there is little in the way of better margins being earned by the company. Even if the courts and creditors accept the restructuring plan presented, it is evident that Hascol needs to address the Dutch elephant in the room. Banks waiving off any future interest will help the company earn some profits in the future and conditions can improve to some extent. However, the problem for the company is based on the fact that its business model is broken and cannot sustain itself. Importing fuel when cheaper local options are available is the primary reason the company is suffering losses in its recent past. Restructuring can be a band-aid for the situation but the gaping gunshot wound of haemorrhaging profits needs to be addressed as well before any recovery can be seen. n

Sugar industry wrestles with internal politics

Election of PSM Chairman becomes a point of contention in the midst of rising questions over the future of the sugarcane crop

Profit report

Members of Pakistan’s sugar industry have had a tough couple of months. For starters, there has been increasing heat on the position of sugar in the country’s agricultural mix.

Earlier in the month, Punjab Assembly Speaker Malik Muhammad Ahmed delivered a scathing indictment of the vested interests that have allowed politically powerful sugar barons to run amok with this water guzzling crop, edging out important crops like cotton. The speaker’s candid comments during a session of the house are an indication of just how fed-up many have become of how coddled the sugar industry is, especially since his own party leadership are some of the most prominent sugar mill owners in the country.

On top of this, the Pakistan Sugar Mills Association (PSMA) was also the site of a rather ugly battle for the position of the association’s chairman, with the matter eventually being settled by the Director General of Trade Organisations (DGTO).

So what is going on?

The election

Matters kicked off pretty much as they normally do. The Pakistan Sugar Mills Association (PSMA) is another one of the many industry associations that exist in the country to lobby and advocate for their particular sector. Much like the rest of these associations, the PSMA has its own constitution and governing laws. One of the central tenets of this is that the position of chairman is rotated amongst the different regions of the PSMA.

Which is why on the 7th of October this year, PSMA Khyber-Pakhtunkhwa (KPK) elected Abbas Sarfaraz Khan as the Central Chairman of PSMA for 2024-2026. Mr Khan is one of the most powerful sugar barons in the country, and definitely the most powerful one in KP, owning at least four of the six mills in the province. He is a direct descendant of King Dost Mohammed Khan of Afghanistan. He was also a caretaker federal minister.

But there was a problem with his election. Only a few days later on the 10th of October, PSMA (Central) issued a press release, according to which, PSMA had elected a new Chairman at a meeting of its Executive Committee of the Association. The official press further stated that through voting, the opinion of the Members of the Executive Committee was sought for the vacancy of the Chairman. Six out of nine executive members voted in favour of Faisal Ahmed Mukhtar who was elected by majority vote. The press release

has further claimed that the General Body of the association appreciated the decision of the executive committee and congratulated the new Chairman Faisal Mukhtar.

This naturally was not popular with the KP region of the association. They immediately took the matter to court, sending letters to the Registrars of SECP and DGTO.

According to the letters “under instructions from and on behalf of our client Rizwan Ullah Khan, Chairman KPK Zone, All Pakistan Sugar Mills Association and the member of Central Executive Committee, it is reported that as per principle of rotation of the Association, Abbas Sarfaraz Khan of Chashma Sugar Mills Limited from the KPK Zone has been elected as the Chairman of Pakistan Sugar Mills Association (Central) for the period 2024-26. A copy of the announcement of October 7, 2024 made by the Election Commission has also been shared with the Registrars of both Regulators.”

The matter was taken up by the DGTO, an arm of the Commerce Ministry and Securities and Exchange Commission of Pakistan (SECP). This body declared the election of Central Chairman, Pakistan Sugar Mills Association (PSMA), Faisal Ahmed Mukhar for the term of 2024-26 null and void and directed the Association that Chairman PSMA shall be elected by all members of the Executive Committee of PSMA.

The DGTO found that the election of Chairman PSMA (Central) was not supervised by the Election Commission as required under Rule 21 of the Trade Organisations Rules, 2013 and the provision of rotation under Article 18 (a) (iii) of Memorandum of Articles of Association has not been followed.

Following this, on the 21st of November, the PSM elected Abbas Sarfaraz Khan from Khyber Pakhtunkhwa (KPK) as its new Central Chairman for the term of 2024-26. According to a brief profile on the Wall Street Journal, Abbas Sarfaraz Khan is a businessperson who has been at the head of 5 different companies. Presently, he holds the position of Chairman for Chashma Sugar Mills Ltd., Chief Executive Officer & Executive Director at Premier Sugar Mills & Distillery Co. Ltd., Chief Executive Officer & Non-Executive Director at Arpak International Investments Ltd. and Chief Executive Officer for Syntronics Ltd. Abbas Sarfaraz Khan is also on the board of seven other companies.

However, there continue to be concerns regarding this election as well. Sources from within the PSMA have said that the election commission appointed for the PSMA elections 2024-26 have displayed a contradictory stance. For starters, the original stance was that the election process had been completed on 30th September, 2024 and a new Election

Commission was mandatory to be constituted under the rules. This very much did not happen. Rather than following this, on the very next day, the same election commission, under an illegal election schedule, declared Mr. Abbas Sarfaraz Khan was elected chairman of the association. This was done without even fulfilling the requirement of becoming a member of the executive committee of Khyber Pakhtunkhwa region. It may be noted that the majority members of the executive committee of the association have filed an appeal before the notified cabinet committee against the decision of the DGTO dated November 15th.

Powerful players

The ongoing drama is taking place in what is possibly the most politically powerful industry in all of Pakistan. Almost all of the 91 sugar mills in the country are owned by household name politicians and their families, all of whom belong to different political parties.

Most sugar mill owners are well known politicians who have had the good fortune of being elected to govern the country on a number of occasions. Prime Minister Nawaz Sharif, his family and relatives own the Abdullah Sugar Mills, Brother Sugar Mills, Channar Sugar Mills, Chaudhry Sugar Mills, Haseeb Waqas Sugar Mills, Ittefaq Sugar Mills, Kashmir Sugar Mills, Ramzan Sugar Mills and Yousaf Sugar Mills. The Kamalia Sugar Mills and Layyah Sugar Mills are also owned by PML-N leaders.

Former President Asif Ali Zardari’s family and PPP leaders are said to own Ansari Sugar Mills, Mirza Sugar Mills, Pangrio Sugar Mills, Sakrand Sugar Mills and Kiran Sugar Mills. Ashraf Sugar mills is owned by PPP leader and former Zarai Tarraqiati Bank Limited (ZTBL) President and current PCB Chairman Chaudhry Zaka Ashraf.

Former Federal Minister Abbas Sarfaraz from Khyber Pakhtunkhwa (KP) is also in this list. Nasrullah Khan Dareshak owns the Indus Sugar Mills while former Secretary General, Pakistan Tehreek-i-Insaf and current IPP leader Jehangir Khan Tareen, has two sugar mills, the JDW Sugar Mills and United Sugar Mills. PML-Q leader, Anwar Cheema, owns the National Sugar Mills. Senator Haroon Akhtar Khan, special assistant to the Finance Ministry on Revenue, owns the Tandianwala Sugar Mills while Pattoki Sugar Mills is owned by Mian Mohammad Azhar. Former Governor Punjab and currently a prominent figure in the PPP, Makhdoom Ahmad Mehmood is a major shareholder in JDW Sugar Mills. Chaudhry Muneer owns two mills in Rahimyar Khan district and former deputy PM Chaudhry Pervaiz Elahi and former Minister of State for Foreign Affairs, Khusro Bakhtiar have shares in these mills.

The rise of the sugar barons

Much like many other industries in the country, partition meant a new beginning. In August 1947, there were only two sugar factories in the newly minted state of Pakistan. Most of the sugar mills set up in the colonial era were on the Indian side of the border, and the two in Pakistan were not nearly enough to meet domestic supply.

This was an opportunity. For the first few years of the country’s existence sugar had to be imported which was a major drain on a new state with very little trading power. At the same time, sugar was a high-demand commodity in the subcontinent and plenty of sugarcane was grown in the new state. The 1947-48 production numbers for sugarcane in Pakistan were over 54 lakh tonnes. Nearly 75% of this sugarcane was grown in the Punjab. Since at the time the country’s landed elite were also its political elite, it became clear that many of these landowners that were growing sugarcane would now set up sugar mills, process the sugar and make more money.

The experiment was successful. Keeping in view the importance of the sugar industry, the government setup a commission in 1957 to frame a scheme for the development of the sugar industry. In this way the first mill was established at Tando Muhammad Khan in Sindh province in the year 1961. By 1962 there were six mills in the country and in 1964 the Pakistan Sugar Mills Association (PSMA) had been established and almost every single sugar mill in the country had a member of parliament on its board of directors.

The interests of the sugar industry were disproportionately represented in the legislature and the political patronage that came with this allowed the industry to boom. According to a report of the Competition Commission of Pakistan, the number of mills increased to 20 by 1971 during a period when cane cultivation was incentivized in Sindh through establishment of sugar mills. The size of the industry further increased to 34 by 1980.

But by this point mills were facing a problem. Pakistan’s sugarcane was uncompetitive. Production was low compared to the global average yields and so was sugar extract percentage. This meant imported sugar could actually compete with the local product. To counter this, government policies placed tariffs on imported sugar and even banned it while giving subsidies to local sugar mills. As a result, the number of mills grew and so did the number of farmers growing sugarcane.

In fact, the number of mills grew at such a rate that the government eventually had to stop giving licences because of capacity maximisation issues. Through political patronage and protec-

tion through tariff and non-tariff restrictions on imports and generous subsidies, Pakistan went from 41 mills in 1987 to 91 by the mid-2000s before a ban was placed on the establishment of new factories due to excess installed capacity.

During this era in particular the Sharif family was prominent in entering the sugar mill business. They started with the Ramzan Sugar Mills and continued on to establish Ittefaq Mills and many others. There was a crucial difference however. In the beginning, many of the mill owners had also been farmers. The Sharifs were hard-boiled industrialists with not a single green thumb in the entire family. This was also part of a rising trend of non-agriculturalists with political clout entering the country’s sugar industry. If one were to believe what was said in those days, the annual profit from one sugar unit in that period used to be more than enough for setting up a new one.

Up until the early 2000s there was no restriction on establishing a new sugar mill. However, around 2005 the government of Punjab decided that new mills could not legally be established. One reason for this was that a lot of the mills coming up were being set up in South Punjab near Muzaffargarh. This was a major part of Pakistan’s cotton belt — which the country’s largest export oriented sector, textiles, relied heavily on. This essentially froze the sugar industry, leaving it entirely in the hands of around 40 individuals and their families.

But what about the sugar crop?

And this is what it all boils down to. The sugar industry in Pakistan has been propped up on friendly policy making. Even this year in Sindh presents an alarming picture. According to a recent report in Dawn, the Sindh government has yet to notify the sugarcane’s indicative price for the 2024-25 sugarcane crops.

“No, the rate is not yet fixed,” said a Sindh agriculture officer while anticipating that sugar mills would be starting crushing by Nov 21 under the federal government’s decision. This decision, which allowed sugar to be exported by mills, also linked it to the commencement of crushing by this date.

Thirty-one sugar mills crushed cane in Sindh to produce 2.02m tonnes of sugar in 2023-24. A total of 19.28m tonnes of sugarcane were crushed, recording a 10.37pc recovery percentage. When compared with the 2022-23 crop season, 16.79m tonnes of sugarcane crop were crushed to produce 1.74m tonnes of sugar with a lesser recovery percentage of 10.16pc. This lesser acreage, as well as recovery in 2022-23, was apparently attributable to losses to crops in 2022 flooding and heavy rainfall. The price in Punjab has also not yet been notified by the provincial government. Punjab’s sugarcane

producers like Khalid Mehmood Khokhar, President of Pakistan Kissan Ittehad, explains, “It is felt that the Punjab government will not fix sugarcane’s indicative rate and wheat’s support price this year.” Mr Khokhar noted that the cost of production increased this year primarily due to a rise in electricity tariff.

All of this raises the question, away from the politics, how good is sugarcane for Pakistan’s agricultural economy? On the one hand one of the major issues raised over the relocation is that the mills would be moving to cotton districts. The battle between the delicate white lint of cotton and the sugary sweetness of sugarcane is an unexpected but harsh one. Over the past two decades, however, cotton has taken a backseat with farmers shifting in droves towards growing the more profitable but water-guzzling sugarcane. Cotton has fallen out of demand, become internationally uncompetitive, and output has fallen by a whopping 65% from 14 million bales being produced in 2005 to 4.9 million bales being produced in 2023. otton producers are losing interest and prefer crops like sugarcane and paddy while the government continues to be disinterested in reviving cotton. Sindh has seen growth in the sugar industry in cotton-growing areas, especially in Ghotki, where five sugar mills have been set up.

In an earlier interview with Profit, the son of Jehangir Tareen, Ali Tareen, had also agreed that a lot of farmers were shifting from cotton to sugarcane. The reason behind this, of course, is that sugarcane is much more profitable. Because the mills are around farmers, they have someone to sell to, unlike when they grow the cotton crop which is susceptible to disease and harder to sell.

“Rahim Yar Khan used to be a cotton growing area when we set up our mill,” says Ali. “Now it is the biggest sugarcane producing area in the region. That is because we came in and said from the get-go to the farmers that our goal is to have you grow lots of sugarcane for cheap and sell it to us at high rates. Before this, the relationship between the sugar mills and the farmers was that the mills would squeeze the farmers. Eventually, the farmers would simply stop growing sugarcane. And that’s why we provided cash loans, we gave seeds, we held training and sugarcane yield has never been higher,” Tareen told Profit in the earlier interview.

This is another issue. While water scarcity is an issue in central Punjab, many of the mills there had also gotten a bad reputation with farmers. The mills would make the farmers cue for hours to sell their crop and would not pay them on time. Deferred payments actually became a major bone of contention between farmers and mill owners.

But generally, sugarcane is a much safer bet than cotton. It is no wonder then, that sugarcane is seen as a ‘better’ alternative. Not only is it sturdier in the face of fluctuating weather, it requires less manpower in the fields. n

Millat Tractors expecting a good year with government contracts

Sales rising by 47% this past year, exports surging more than 66%, and new Punjab government contracts in the works

Profit Report

Millat Tractors (MTL), Pakistan’s leading tractor manufacturer, is ploughing through challenges with a bumper allocation of 5,800 units (61% of total) under Punjab’s Green Tractor Scheme. Deliveries are set to kick off this quarter, easing inventory woes and providing a cash flow boost.

After weathering a sales slump caused by tax refund delays and liquidity crunches among farmers, MTL’s fortunes are turning. Tractor sales soared 47% year-on-year in FY24, with the company’s own sales leaping 64% to 30,620 units. Exports surged 66%, driven by demand for its Massey Ferguson tractors and

power equipment.

MTL’s Rs8 billion in sales tax refund claims remains a thorn in its side, but management is optimistic about its merger with Millat Equipment Limited and resuming dividends soon. With its expanded spare parts network and deluxe tractor variants, MTL seems ready to harvest further growth.

Millat Tractors, a cornerstone of Pakistan’s agricultural machinery sector, has a rich history that spans nearly six decades. Founded in 1964 as Rana Tractors and Equipment Limited by the visionary brothers Rana Khudadad Khan and Rana Allahdaad Khan, the company began its journey as an importer and marketer of Massey Ferguson tractors in Pakistan. This venture marked the beginning of a transformative era in the country’s agricultural mechanization.

The company’s growth trajectory took a significant turn in 1967 when it established its first assembly plant in Lahore, assembling tractors from semi-knocked-down (SKD) kits. This move laid the foundation for domestic tractor production in Pakistan. However, the political landscape of the 1970s brought about substantial changes. In 1972, amidst a wave of nationalization, the company was renamed Millat Tractors and incorporated into the Pakistan Tractor Corporation (PTC), reflecting the government’s increased involvement in key industries.

The 1980s saw Millat Tractors making significant strides in manufacturing capabilities. Through collaboration with Massey Ferguson, the company set up manufacturing facilities for various tractor components. A major milestone was achieved in 1982 with the

development of the first engine assembly line in Pakistan, followed by the establishment of casting facilities and an in-house machining facility in 1984. These advancements positioned Millat Tractors at the forefront of domestic tractor production.

The early 1990s marked another pivotal moment in the company’s history. In 1992, as part of the government’s privatization scheme, Millat Tractors was acquired by its employees for 306 million rupees. This transition ushered in a new era of expansion and diversification. The company quickly established a tractor assembly plant with an annual capacity of 15,000 units and began acquiring stakes in complementary businesses. Notable acquisitions included a 51% stake in Bolan Casting Limited in 1993 and the establishment of Millat Equipment Limited for gear and shaft production in 1994.

As the new millennium dawned, Millat Tractors continued to diversify its portfolio. In 1999, it founded Millat Industrial Products Limited for battery and cell manufacturing, followed by the acquisition of Rex Barren Batteries in 2001 under the government’s privatization scheme. These strategic moves helped the company broaden its product range and strengthen its market position.

By 2015, Millat Tractors had evolved into a diversified manufacturer, offering a wide range of tractor models, industrial products, and agricultural implements. The company’s success and growth potential were recognized internationally when it was listed on Forbes Asia’s 200 Best Under a Billion in 2018. Continuing its expansion, Millat Tractors increased its annual production capacity to 30,000 tractors on a double-shift basis by 2022, cementing its status as a major player in

Pakistan’s agricultural sector. However, like many industries, Millat Tractors has faced challenges in recent years. In 2023, the company temporarily suspended plant operations due to decreased demand and cashflow constraints, reflecting the broader economic challenges facing Pakistan’s industrial sector.

Despite these hurdles, Millat Tractors remains a significant force in Pakistan’s agricultural mechanization. From its humble beginnings as an importer to becoming a leading manufacturer, the company’s journey mirrors the evolution of Pakistan’s industrial capabilities. With its focus on innovation, diversification, and adaptation to changing market conditions, Millat Tractors continues to play a crucial role in supporting Pakistan’s agricultural sector and contributing to the nation’s economic development. n

EFG Hermes completes merger with domestic brokerage

Egyptian investment bank has merged its subsidiary in Pakistan with Intermarket Securities

EProfit Report

FG Hermes, the Middle East and Africa’s financial services heavyweight, has announced that it has completed the merger of its equity brokerage subsidiary with Intermarket Securities, a local firm. The handover, effective November 25, 2024, marks the a new phase in the firm’s seven-year tenure in Pakistan’s financial ecosystem.

The Egyptian investment bank first stepped into Pakistan in 2017 with ambitions to tap into the country’s long-term growth potential. Its entry was heralded as a milestone, being the first foreign investment bank to establish a direct presence in Pakistan since 2008.

The merger marks a new chapter of a seven-year run in Pakistan, which began with the disappointment of the almost immediate disproving of its investment thesis: that Pakistan being upgraded to Emerging Market status by MSCI, the global equity markets index provider, would result in an immediate surge in trading volumes on the Pakistani market and therefore in revenues for brokerage

firms in Pakistan.

While Pakistan did re-enter the MSCI Emerging Markets Index in June 2017, just a few days after EFG Hermes closed on the transaction to buy Invest and Finance Securities Ltd. (IFSL) in May 2017, that change in status did not have any material impact on trading volumes on the Pakistan Stock Exchange.

This acquisition positioned the bank as a key player offering securities brokerage, research services, and investment banking advisory to local and international investors.

The move aligned with the firm’s broader expansion strategy—aimed at diversifying its revenue streams and replicating its growth trajectory from Egypt to other frontier markets. At the time, Pakistan’s anticipated upgrade to “emerging market” status and promising GDP growth, buoyed by the China-Pakistan Economic Corridor (CPEC), made it a natural choice for EFG Hermes’ regional ambitions.

The financial performance of EFG Hermes Pakistan over the past seven years reveals a challenging trajectory. Revenues fluctuated, peaking at Rs289 million in 2023 but accompanied by consistently high operating and financial expenses. The company posted

persistent after-tax losses from 2019 to 2023, with the largest loss of Rs108 million in 2023. Assets declined over time, reflecting a shrinking balance sheet, while the return on capital employed hit a low of -87.5% in 2023.

EFG Hermes’ interest in Pakistan dates back to 2010, when it unsuccessfully bid for the Pakistani operations of the Royal Bank of Scotland. Though outmatched by Faysal Bank in that effort, the company remained committed to entering the market.

Since its eventual establishment, EFG Hermes Pakistan gained recognition as a prominent brokerage. In 2022, the firm was named Best International Brokerage Firm in Pakistan by the Asiamoney Brokers Poll, a testament to its local influence.

Intermarket Securities, one of Pakistan’s leading brokerage houses, will inherit the operations of EFG Hermes Pakistan. For EFG Hermes, the merger allows the firm to gain a larger foothold in the market, albeit with a local partner to share the profits with.

The move is a poignant reminder of the complexities facing foreign investors in Pakistan, where economic turbulence and regulatory hurdles often temper the appeal of a growing, albeit unpredictable, economy. n

Interloop aiming to hit $700 million in revenue by 2026

Profit Report

Interloop Limited (ILP), one of Pakistan’s largest publicly listed textile firms, is charting an ambitious growth trajectory, aiming to hit $700 million in revenue by FY26. With knitwear and denim spearheading exports, the company projects these segments to generate $300 million collectively.

The expansion plan includes a $92 million in capital expenditures: $58 million allocated to a new hosiery plant by the third quarter of calendar year 2025, $18.8 million for denim capacity upgrades by during the second quarter of CY2026, $13.2 million for yarn dyeing by the third quarter of CY2025, and $2.1 million for renewable energy initiatives by the first quarter of calendar 2025.

As Western brands pivot away from China due to tariffs and reduce dependency on Bangladesh, Interloop seeks to capitalise on this reorientation. Its exports surged 26% year-on-year in FY24, outperforming Pakistan’s stagnant $17 billion textile export figure.

In fiscal year 2024, utilisation rates improved significantly: Hosiery reached 82%, denim 88%, and spinning 92%. The newer apparel segment is expected to hit full operational capacity by fiscal year ending June 30, 2026, with profitability anticipated as efficiency improves. However, wastage in the apparel division remains high at 20–22%, though management is optimistic about reducing losses

next year.

Sales rose 31% year-on-year to Rs156 billion, though net profits declined 20% to Rs16 billion due to rupee appreciation and rising costs. Margins remain under pressure, compounded by higher salaries and cotton costs.

Employing over 34,000 people across six countries, Interloop is experiencing robust sales growth at a compound annual growth rate (CAGR) of 44% since 2020. With growing demand and strategic investments, the company aims to cement its position as a key player in the global textile supply chain.

Interloop Limited is a vertically integrated, full-family clothing manufacturer and one of the world’s largest hosiery producers. The company specializes in manufacturing hosiery, denim, knitted apparel, and seamless activewear for leading international brands and retailers.

Interloop was founded in 1992 by two entrepreneurial brothers, Musadaq Zulqarnain and Navid Fazil, along with their friend Tariq Rashid. The company started humbly with just 10 knitting machines in Faisalabad, Pakistan.

In the 2000s and 2010s, Interloop underwent a series of expansions, becoming a vertically integrated company with state-ofthe-art spinning, yarn dyeing, knitting, and finishing facilities.

In 2019, the company listed on the Pakistan Stock Exchange, marking the largest private sector IPO in the country’s history until that time. That same year, it expanded

into denim apparel with a new manufacturing plant in Lahore.

The company has the capacity to produce 795 million pairs of socks and tights annually.

Interloop continues to expand its hosiery business while diversifying into related apparel segments, solidifying its position as a major player in the global textile industry. For decades, China’s dominance in the global textile market seemed unshakeable. But as the Trump Administration ushers in a wave of protectionist policies, including hefty tariffs on Chinese goods, cracks are appearing in the giant’s textile empire.

Global apparel brands are rethinking their sourcing strategies, shifting orders to alternatives like Vietnam, India, and even Pakistan. The move is not just about tariffs—it is a play for supply chain resilience amid intensifying Sino-American trade tensions.

Bangladesh and Vietnam are emerging as clear winners, leveraging their competitive pricing and trade agreements to lure contracts. Meanwhile, textile hubs in South Asia, such as Pakistan’s Interloop, are banking on expanding capacities to fill the void.

China is not retreating quietly. The country’s push into automation and eco-friendly textiles is a bid to maintain competitiveness, but rising costs and political headwinds pose challenges. For now, the global textile chessboard is being rearranged, with Beijing increasingly on the defensive.

When it comes to EMIs, many have tried. Few have succeeded. Here’s why.

What has led to the EMI license being a graveyard for financial services ambitions?

By Hamza Aurangzeb

Over the past two decades, Pakistan has emerged as a dynamic landscape of digital financial innovation, navigating a complex journey of regulatory evolution and technological disruption. The transformation began in 2008 with the introduction of branchless banking—a pivotal moment that laid the groundwork for a comprehensive digital financial services ecosystem.

The central bank’s strategic interventions have been instrumental in this metamorphosis. The National Financial Inclusion Strategy (NFIS) initiated a systematic approach to expanding formal financial services, while subsequent regulatory frameworks dramatically reshaped the digital payments landscape. Key milestones include the 2019 introduction of Electronic Money Institutions (EMIs), the 2021 Payment Service Provider licenses, and the 2022 launch of the micro-payment gateway “Raast”—each representing a calculated step towards digital financial democratization.

The results have been striking: digital payments by value surged from a mere 6% in 2020 to 17% in 2024, signaling unprecedented growth. However, this journey is far from a straightforward success story. While pioneers like JazzCash and Easypaisa have thrived, the EMI segment reveals a more nuanced narrative of opportunity and challenge.

Only a handful of EMIs, such as Sadapay and Nayapay, have successfully navigated Pakistan’s complex digital financial terrain. Multiple entrants have been forced to exit, underscoring the sector’s volatility. Yet, the recent in-principle approvals for new players like Toko Lab and PayMob suggest an enduring belief in the market’s potential.

So, is the EMI sector destined for failure, or a dormant goldmine awaiting strategic unlocking? Profit explores

The convoluted space of EMI regulations in Pakistan

In 2019, the State Bank of Pakistan (SBP) introduced Electronic Money Institutions (EMI) regulations to accelerate financial inclusion and digital payments. The framework allowed non-banking entities to offer digital financial services like e-money issuance and digital wallets, aiming to create a more innovative and accessible payment ecosystem.

Institutions like Sadapay and Nayapay emerged as early success stories, offering customers seamless digital account opening and international debit card services. Initially, EMIs were viewed as catalysts for a financial revolution, promising to rapidly digitize payments.

However, the sector’s promise quickly dimmed. Over the past two years, many enthusiastic EMI license holders either voluntarily withdrew, sold their operations, or had their licenses revoked by the regulator, revealing the challenging nature of this emerging market.

The story begins with TAG’s pilot operations being revoked by the SBP in October 2022, owing to regulatory violations and a variety of other issues. Afterwards, Checkout, a UK based company, let go of its EMI license due to

deteriorating macroeconomic conditions and painfully long bureaucratic procedures to commence commercial EMI operations in the country.

In August 2023, CareemPay followed a similar suit and voluntarily abandoned its license while in October 2023, Finja signed a deal with Opay International for its EMI operations and the latest addition to the list is Paymax, the only commercially live EMI which exited the market in July 2024.

Acquiring an EMI license and operating commercially in Pakistan is a long and taxing journey. The SBP grants an EMI license to entities in three stages, in principle approval, approval for pilot operations and, final approval for commercial operations.

As of now, only five EMIs have been granted licenses for commercial operations, which include Nayapay, Sadapay, Finja, AFT, and E-Processing Systems Ltd. The complicated web of regulatory procedures and lethargic red tape have certainly contributed to the ouster of several prospective EMIs. However, there are other factors, which coerced several entities to either exit the market or recalibrate their strategies.

Limited revenue sources for EMIs

EMIs in Pakistan have typically earned revenues through two sources of income, the first is investment in government securities like T-bills, which were offering a return of up to 23% in 2023, however, it has fallen to around 13% now. EMIs are allowed to invest up to 75% of the trailing three months’ daily average outstanding e-money balance in the government. securities, which was only 50% until June 2023. Moreover, as elaborated by experts like Umair Sheikh, Managing Director at Innovate 47, EMIs don’t have full control over their deposits as they require a trustee, which is a commercial bank to operate.

Thus, EMIs need to establish a partnership with commercial banks and require their approval to invest in government securities. However, despite those efforts, it still provides EMIs with limited revenue due to their low deposit base and modest interest rates. As of Sep 2024, EMIs had a deposit base of only Rs 5.7 billion, whereas scheduled banks held about Rs 31.3 trillion.

The other income source for EMIs is transaction fees earned through payment transactions like those for e-commerce or point-of-sale, where they typically charge merchants 1% to 2%. However, their merchant acquisition remains limited, contrasting sharply with players like JazzCash, which has boarded over 300,000 merchants through QR installations and captured a significant market share.

Moreover, the SBP has regulations in place that allow customers who have completed their biometric verification from NADRA to transact only up to Rs. 400,000 a month, although it could be enhanced to 1 million in certain cases. This further inhibits EMIs in Pakistan from earning substantial revenue from this income stream as it limits their transactions.

Traditional banks generate approximately three-

fourths of their income from interest-bearing sources such as government securities and loans, with around a quarter coming from feebased income. In contrast, Electronic Money Institutions (EMIs) are structurally prohibited from lending and, as a result, rely primarily on fee income as their main source of revenue.

To access lending and generate interest-based revenue streams, EMIs can obtain a non-banking financial institution (NBFI) license from the Securities and Exchange Commission of Pakistan (SECP), a path already explored by Finja.

Further, EMIs in Pakistan operate in a restricted segment, where they aren’t truly able to differentiate themselves from the rest of the financial institutions like commercial banks and microfinance banks as customers can make digital transactions and receive debit/credit cards from them as well and now we even have digital retail banks, which would offer the same services and more in the future.

However the agility of EMIs sets them apart from traditional banks. EMIs are perceived to offer a more refined customer experience, with a strong association with speed and convenience. This model has resonated particularly well with urban youth, including Gen Z. While this approach has helped EMIs like Sadapay and Nayapay scale, relying solely on fee income may not be sufficient for longterm sustainability. To ensure their growth, EMIs will need to diversify their offerings and engage in strategic partnerships with other key ecosystem players.

The target market for the EMIs

EMIs were introduced in Pakistan to promote financial inclusion and digital payments by focusing on the unbanked population in Pakistan, which doesn’t have access to formal financial services like people who engage in informal labor and conduct all of their transactions in cash.

However, almost all of the EMIs have ended up focusing on a completely different segment - urban middle and upper class. They have made a negligible impact on the second and third-tier cities. All of their marketing campaigns are in English and their social media strategy makes it abundantly clear that their niche is the upper echelons of society.

As of December 2023, Pakistan’s financial sector includes more than 200 million accounts across banks, Microfinance Banks (MFBs), branchless banking institutions, and EMIs, indicating a high degree of financial inclusion. However, a leading financial services consultant pointed out that many customers hold multiple accounts, which may give an inflated impression of the number of active bank accounts.

As of FY 2024, 91 million unique customer accounts were recorded of the approximately 140 million adult population (aged 15 years and above) according to the State Bank of Pakistan (SBP). These accounts include those held with scheduled banks, MFBs, Development Finance Institutions (DFIs), and EMIs. The term “unique customer account” refers to an individual having multiple accounts at the same or different institutions, but each customer is counted only once. This raises questions about whether EMIs have accurately assessed their market size and whether they will be able to generate significant revenue by targeting only the middle and upper-income segments.

In contrast, Jazzcash and Easypaisa have focused on reaching the unbanked population through their branchless banking (BB) services, achieving notable progress with their extensive network across the country. As of March 2024, the total number of BB agents

in Pakistan had reached 276,889, allowing these services to open more than 117 million accounts, of which approximately 60 million remain active. Furthermore, their operations extend beyond digital payments, with both Jazzcash and Easypaisa providing nano- and micro-lending services to their customers, where industry analysts elucidated they earn an annualized return of more than 200% on their lending products. Although micro-lending is still a relatively new concept with a non-traditional lending structure whose performance remains to be fully assessed.

The dynamics of EMI business in Pakistan

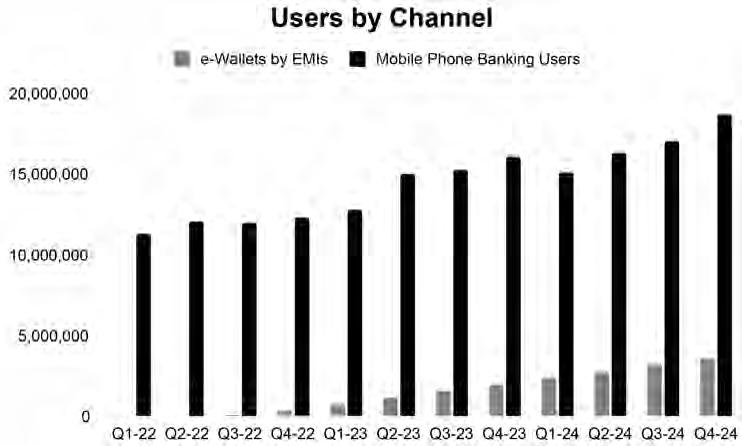

EMIs have definitely gained traction in Pakistan since the beginning of FY22 as the number of e-wallets has mushroomed since then. The number

of e-wallets in the country stands at 3.671 million, which is a remarkable achievement as three years ago there were no e-wallets in the country. Although this achievement is meaningful, the number of e-wallets still lags behind the number of mobile phone banking users by a mile. The number of mobile phone banking users currently stands at 18.678 million, 5x the number of e-wallets in the country.

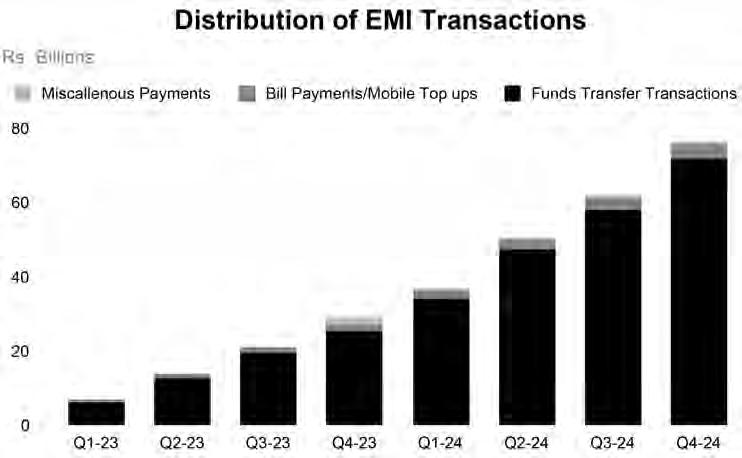

Moreover, if we look at the distribution of transactions conducted by customers through both platforms, there is a stark difference in how customers move funds through each channel. Customers typically utilize EMIs to move funds from their wallets to another wallet or another bank account.

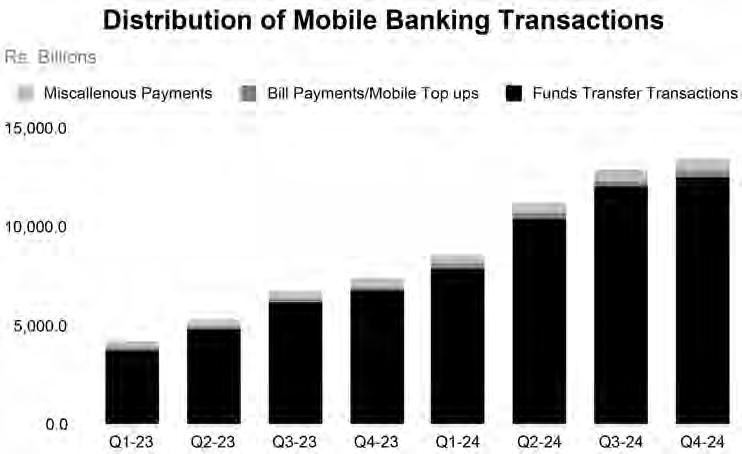

They made around 26.9 million transactions in Q4-24, which amounted to Rs76.7 billion. Around 75% of the transactions were initiated for funds transfer, which represented a value of Rs72.1 billion, while the rest of the 25% included transactions for miscellaneous payments, bill payments, and mobile top-ups, amounting to Rs4.6 billion. These funds transfer transactions have enabled EMIs to scale to such an extent, however, effectively, they don’t make money off these funds transfer transactions.

Customers usually use EMIs to pay for online services like food delivery, e-commerce purchases, and ride-hailing services which have small ticket sizes while they utilize their bank accounts for bigger payments and transactions. The average size of transactions for EMI during 4Q24 was Rs. 2,851.

On the contrary, we have mobile phone banking which is used by customers a lot more frequently, around 324 million transactions were made through mobile banking channels during 4Q24, which represented a gigantic sum of Rs13.5 trillion. Interestingly, 85% of transactions were for funds transfer, which amounted to Rs12.6 trillion, however, these funds transfer transactions are a substantial source of revenue for banks, unlike EMIs. The remaining 15% of transactions represented miscellaneous payments, bill payments, and mobile top-ups, which corresponded to a sum of Rs950 billion. Mobile banking constituted a mean transaction value of Rs41,723.

What lies ahead?

While EMIs have a very real income stream constraint, all is not dark and gloomy as the SBP revised the EMI regulations in June 2023, which broadened the scope of an EMI license.

An EMI is now capable of offering new payment services such as payments aggregation, bill/invoice aggregation, escrow services

for domestic e-commerce transactions, services via APIs to financial institutions/fintechs, and inward cross-border remittances.

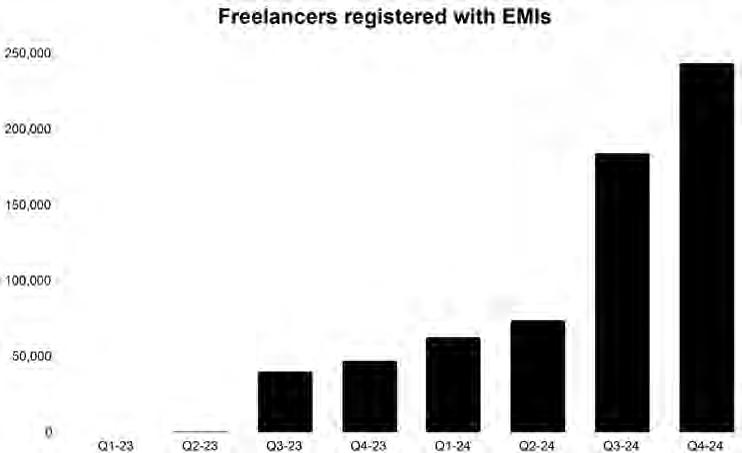

This revision in regulations has enabled them to commence offering services to freelancers as well. Freelancers make up a significant chunk of the customers of EMIs and are growing at a brisk pace due to the exceptional services offered by them.

EMIs like Sadapay are compatible with payment systems like Apple Pay and Google Pay, which allow freelancers in Pakistan to receive international payments in their local bank accounts. They charge 5% on these international transactions and offer better exchange rates than other platforms. Hence, the number of freelancers using Sadapay has increased from nil in 1Q23 to 243,639 by the end of 4Q24. Nevertheless, freelancers can’t store their funds in dollars. Moreover, EMIs need to

partner with one of the 31 SBP-approved commercial banks to deal with foreign exchange, which is a bit of a nuisance for them.

Experts suggest that EMIs can diversify their revenue by leveraging their customer base through partnerships with financial institutions. By enabling cross-selling and profit-sharing, EMIs could potentially access additional revenue streams. The ultimate goal would be acquiring an NBFI license, which would allow expansion into product distribution like mutual funds and insurance.

However, the evolving financial landscape—with enhanced digital services from commercial and microfinance banks, and emerging digital banks—makes digital payment services alone insufficient. EMIs must explore adjacent segments like lending and financial product distribution to remain relevant in the market. n