08 How the wheat import scandal was brushed under the carpet

12 The Big Three oligarchy in Pakistani automobiles is over

17 Is the govt about to let go of its control on petrol prices?

20 Honda Car had a stellar first quarter but profits are still on the lower side

22 The double whammy of declining electricity demand and increased consumer tariffs

25 If equity injection is a drug, Microfinance Banks are an addict Ahtasam Ahmad

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

How the wheat import scandal was brushed under the carpet

The government has pinned the blame on a bunch of bureaucrats and let the murky matter go which was causing serious divisions within the ruling party

By Ghulam Abbas

Less than three months after the wheat import scandal that rocked the federal government and caused serious fissures within the ruling PML-N, it seems the government has decided to quietly bury the matter by dismissing and shuffling around a few bureaucrats.

Like so many other wheat and sugar scandals that have been polluting the country for decades, the government has fixed responsibility on irrelevant officials to save the real beneficiaries of the scandal.

The wheat crisis hit the PML-N led government around mid-April 2024 when the farmers of the Punjab started violent demonstrations and protests for not procuring their wheat produce by the Punjab Government on support price.

Prime Minister Shehbaz Sharif ordered an inquiry regarding the import of excess wheat in Pakistan during the food year 20232024. The member federal public service commission led committee conducted an enquiry and declared wheat import in the country an “institutional failure”. However, it did not fix any particular person responsible. Now, it seems the government wants to quietly bury the matter.

What happened with the wheat scandal

The origins of the wheat scam go back to an amount of 1.2 million tonnes of wheat more than what was necessary to import. Back in 2022, devastating floods ruined Pakistan’s domestic wheat production. As a result, in 2023, the government decided to import more wheat to make up for the shortfall. The shortfall was around 2.4 million tons, but the government instead allowed the private sector to import 3.6 million tonnes.

The accusation is that the caretaker government took kickbacks to allow this. As a result, there was an extra billion dollars tagged onto the import bill at a time when the economy was facing a dire shortage of foreign reserves. The problem was that earlier this year the chickens came home to roost, but the owner of the barn was different.

The government of Pakistan and its provincial governments have a strange relationship with its farmers. Before the 18th amendment, the federal government would set the wheat support price. Now, the provincial food departments and PASSCO procure wheat in harvest months at the government’s announced price. The provincial food departments release wheat in lean months at the ‘issue price’. Until recently, issue price was the same through-

out the year and now the government has introduced a cascading price mechanism to smooth out seasonal variation and cover the transaction cost. The public sector procures on average about six million tons of wheat, or nearly 24% of total production.

But this year there was a surplus of wheat because the government had allowed the import of extra wheat last year. As a result, the Punjab government announced it would not be commencing or buying its regular amount of wheat. This was at a time when wheat had seen a bumper crop in Pakistan. The farmers protested, the Punjab government brought down the lathi on the protesting farmers, and negative sentiments prevailed.

The typical response

The response was as one might expect. The prime minister formed an inquiry committee. At the same time, a lot of talking heads on television and social media started bringing up how the extra import had come during the caretaker setup.

But the wheat import scandal was going to cause political problems within the ruling party. Tensions rose within the PML-N on how to handle the billion dollar wheat import scam. The spats were quite public, with the party’s senior leadership making decisions, taking them back, and painting an overall picture of complete disarray.

In private, the situation is even bleaker. Mian Nawaz Sharif has publicly stated that he supports strict action against the preceding caretaker government, which is a key suspect in the wheat import scandal that has taken hold of the country’s news cycle. But it seems his younger brother the prime minister is more reluctant to involve Anwar ul Haq Kakar’s caretaker setup in any sort of federal criminal investigation, especially since the Punjab CM from the caretaker era, Mohsin Naqvi, serves as interior minister in his cabinet.

Mian Nawaz keen to hold the previous government accountable because the wheat scam is proving to be the first major challenge for his daughter Maryam’s government in Punjab. The ire of farmers over the scandal has been directed largely towards the Punjab government because of its failure to purchase the wheat from the farmers. The initial response has been heavy handed and could cause future political damage. The prime minister, the head of a weak coalition in Islamabad, is afraid of the consequences of taking on the caretakers who are thought to have been very close with the country’s establishment, according to one high ranking source within the PML-N. How did all of this unfold?

Mian Nawaz immediately wanted to take strict action. “The inquiry committee was set up but the response was not strong enough

for Mian Sahib’s liking,” explains one source privy to the information. As a result, Mian Nawaz called a party meeting on the 6th of May. The meeting was to be attended by Punjab’s Minister of Food, secretary food and other concerned officials. The elder Sharif directed that this very provincial level committee would deliberate on the findings of the federal inquiry committee. It seemed that Mian Nawaz had essentially sent a message to his younger brother that he was taking charge on this particular matter. It was decided that the prime minister would present the inquiry committee’s report to Nawaz Sharif who will decide the matter pertaining to the wheat issue.

Within a day, however, reports started filtering in that Nawaz Sharif had chosen to take a step back and allow the prime minister to handle the matter as he sees fit. Party sources claimed that Mian Nawaz decided it would be appropriate to not give any direction on the matter. But then his younger brother the prime minister hesitated in taking the necessary steps.

According to sources, the Shehbaz Sharif led federal government is allegedly not willing to take action against the caretaker premier Anwaarul Haq Kakar and his federal cabinet. However, the members of the Shehbaz cabinet and bureaucracy have suggested to the Prime Minister to solve the issue of wheat import scandal in a “better way”. In fact, after the first meeting of the fact finding committee, information minister Atta Tarar said that no one had been called or interviewed by the committee in this regard including former caretaker prime minister Anwaarul Haq Kakar, ex-finance minister Sham¬shad Akhtar, and incumbent Interior Minister Mohsin Naqvi (ex-CM of Punjab).

The inquiry committee and its happenings

Later the premier constituted Mr. Kamran Ali Afzal, Secretary Cabinet led four-member another inquiry committee with the terms of reference “To ascertain the responsibilities for opening of LCs and allowing import of excess wheat than ascertained demand after February 2024.”

According to reliable sources, Mr. Kamran Ali Afzal, was given names of three irrelevant officials (two of them were not holding any relevant official position during the relevant period and even one was without even any official position during relevant time and one was neither member of wheat board nor mandated for import of wheat) to include in the inquiry report by some influential bureaucrats in order to cover and remove names of Capt. Retd. Muhammad Mehmood, who remained secretary MNFSR from August 2023 to 25 January 2024 and who initiated wheat

import summary on 10 October 2023 without capping on quantity and time of wheat import and pressed for import of wheat through only private sector, caretaker prime minister who approved the wheat import summary, Dr. Kosar Abdullah Malik, Ex-Federal Minister of caretaker government who as chairman wheat board approved import of 17 excess wheat vessel in Pakistan till 31st March 2024 after import of 2.4 million tons shortfall wheat in January 2024 and Waqas Ali Mehmood, Ex-Additional Secretary-I of MNFSR for proposing import of 17 vessel bringing in surplus wheat in Pakistan even after knowing this fact that 2.4 million tons shortfall wheat estimated by MNFSR have been arrived in Pakistan.

The inclusion of irrelevant officials in the inquiry report further prompted their suspension on 17 May, 2024 along with Capt. Retd. Muhammad Asif, who was made Acting secretary MNFSR, (for one and half month). Among the four officials suspended so far, only Mr. Imtiaz Ali Gopang FSC-II, may be considered one responsible accused official for wheat crises being a member of wheat board and involved in wheat import process from start till the crisis emerged.

According to insiders, the nomination of irrelevant officers, who have been suspended, has puzzled another OSD BS-22 officer (former secretary Commerce Saleh Farooqui) tasked with completing the inquiry as an authorized officer and submitting a report with complete findings and recommendations.

Understandably annoyed, these officials in their replies to the charge sheets said they could not be held responsible for surplus import of wheat after February 2024 because they were holding any relevant official position.

Dr. Waseem ul Hassan, Food Security Commissioner-I (suspended) was dealing with minor crops whereas wheat is a major crop in the government of Pakistan’s inane categorisations. As such, wheat import would not fall within his job description and mandate of FSC-I. It rather falls within jurisdiction of FSC-II. Further, on 12 October 2023, Dr. Waseem ul Hassan was made OSD by Capt. Retd. Muhammad Mehmood, ex-secretary MNFSR and ordered to report to Admin Section-I of the MNFSR. Later, he was posted as Managing Director, Pakistan OilSeed Board where he remained posted till 19 March 2024 and thereafter, he was again transferred and posted as Food Security Commissioner-I. Dr. Mohsin Saleem remained posted as Food Security Commissioner-I from 12 October 2023 to 19 March 2024 during the most relevant period of wheat import but he was not included in the accused officers list if FSC-I was considered responsible for wheat crises in any way by first or second inquiry committee. Meanwhile Muhammad Asif was performing duties in

MNFSR as Deputy Food Security Commissioner-II from 2nd January 2024 to 31st March 2024, peak surplus wheat import period.

Mr. Sohail Shahzad, Director Technical of Department of Plant Protection (DPP) had been on attachment from DPP to MNFSR from 04-05-2023 to 06-05-2024 and was OSD and reporting to Admin Section-I from 25-09-2023 to 06-05-2024 was not holding any official position or relevant positing during relevant period of import of excess wheat in Pakistan. During peak wheat import period from 22 December 2023 to 6 March 2024, Dr. Muhammad Qasim Khan Kakar, Director Admin on deputation in DPP from Agriculture Research Institute of Agriculture and Cooperatives Department of Balochistan was holding the charge of post of Director Quarantine granted to him by the former secretary Mehmood and was regulating import of wheat in Pakistan.

Another suspended official, Allah Ditta Abid, Director General of the DPP was neither member of the wheat board nor mandated to decide quantity and time for import and export of wheat or ban in the country. He as DG DPP was responsible under rules of business to prevent entry of exotic and alien biosecurity risks associated with the import of wheat in the country. During the entire wheat import period, wheat cargoes after ensuring complete freedom from pests were allowed biosecurity clearance.

The wheat board

The Federal Government has notified a “Wheat Board” consisting of one chairman and 26 members in the MNFSR to monitor demand and supply of wheat in the country and decide import of wheat foreseeing shortage in the country to ensure food security. The Federal Minister for MNFSR acts as chairman of the board.

According to notification, Plant Protection Adviser and Director General DPP and the farmers are not members of the wheat board. The premier chairing meeting of the wheat board on 11 July 2024 ordered reconstitution of the composition of the wheat board and instructed to include farmers in it.

It is pertinent to point out that there was neither any restriction nor any ban nor levied any regulatory duty on import of wheat in Pakistan during food year 2023-2024 in accordance with import policy order 2022. Thus, the private sector was at liberty to import wheat without any further concession from the federal government. Finally, realizing this fact that excess quantity of wheat in Pakistan can only be regulated and restricted by incorporating condition of ban on import of wheat in Pakistan in import policy order, the Ministry of Commerce with the approval of the Federal Government has issued notification vide dated

11 July 2024 for imposing ban on import of wheat in Pakistan by making relevant amendments in SRO.

Details of the scandal

Sources earlier informed Profit that despite surplus domestic stocks, the import of more than 35,87,373 metric tons of wheat from September 2023 to March 2024 has allegedly caused loss of $1 billion of foreign exchange to the country. They said that the Ministry of National Food Security has facilitated the import of wheat allegedly in league with flour mafia and wheat importers and defrauded the country of more than one billion dollars of foreign exchange. They said this import has inflicted a loss of above Rs 300 billion to the farmers and Rs 104 billion to the government exchequer, according to sources privy to the development.

Sharing details, the sources said wheat stocks with PASSCO and provincial food departments were 43,65,220 metric tons on April 1, 2024 and there was no need for private import of wheat. They said as the private sector and flour millers imported wheat, PASSCO and provincial food departments could not sell their stocks of 43,65,220 metric ton and have incurred average incidental charges of Rs 950 per maund/40 kg, and total loss to government because of incidental amounted to Rs 104 billion which has allegedly indirectly gone to the pockets of flour millers, traders and bureaucracy. They said due to unnecessary and unwanted import, prices of wheat have crashed to Rs 2800-3000 per maund against government price of Rs 39,000/maund and the farmers will be forced to sell 50 percent i-e 16 million metric tons out of estimated 32 million metric tons of total produce as government is allegedly purchasing very little wheat. Thus, more than Rs 300 billion will allegedly be looted from the farmers and will go to the pockets of flour millers, import traders and bureaucracy, according to our sources.

The import was kept uncapped and ships continued to dock at Karachi even during the entire month of March, 2024 when wheat from Sindh province was coming to market, sources added. It is also learnt from the sources that 71 cargos of wheat were imported from Russia, Ukraine, Bulgaria and private importers continued the import of wheat till March 31 instead of March 15. They said that over 3.5 million tons of wheat was imported under the pretext of importing one million tons of wheat. They said live insects were found during the inspection in 26 cargoes of wheat out of 71 cargoes of wheat imported from September 2023 to March 2024. Inspection of imported wheat was done by a subordinate department of the Ministry of National Food Security, said sources. n

Having dominated the market since the 1980s, the three Japanese automakers face stiff competition from Korean and Chinese automakers, and their own lethargy in adjusting to consumer preferences

By Zain Naeem

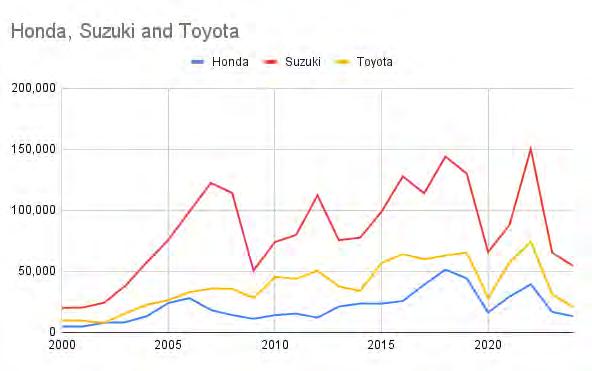

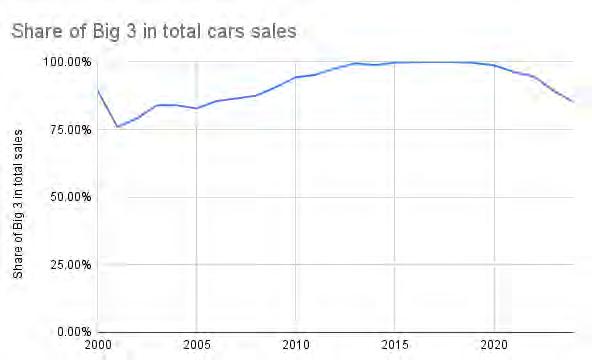

For all the talk of “elite capture” and “rent seeking” in Pakistan, the country has been watching an oligopoly slowly break down over the past five years. For almost every single year since fiscal year 2019, the Big Three automobile assemblers in Pakistan – Toyota, Suzuki, and Honda – have been losing market share in the cars and sports utility vehicles (SUV) segment of the market.

This is a story of incumbents that rested on their laurels, failed to take the threat of competition seriously, and took the customer for granted, not catering to changing preferences and instead adopting the attitude: “you will buy what we produce, on terms that we dictate, on timelines that we please, and you will dare not complain.”

Well, the customer noticed, and when the government decided to finally incentivize newer players to enter the market, the consumer has flocked to them in droves.

For the fiscal year ending June 30, 2024, the Big Three have sold 85,681 cars and SUVs combined, a number lower than their total sales during fiscal year 2009, according to data from the Pakistan Automotive Manufacturers Association and Lucky Motor Corporation (the only major car company in Pakistan not to be a member of PAMA, and hence reporting its data separately). To be clear, the entire automotive industry has seen volumes collapse by 60.3% since the peak achieved during fiscal year 2022, a change driven entirely by the combined effects of skyrocketing inflation and high interest rates causing a sharp decline in auto lending by the banks.

But the Big Three have been even more badly affected. The industry may be down 60% off its peak volumes, but the Big Three saw their volumes decline by nearly 66% over the past two years. Their market share has also been taking a hit. From a near total dominance of the car and SUV market in 2018, their collective share – in terms of number of vehicles sold – is now down to just over 76% during fiscal 2024.

So how has this been happening? And what comes next? The story starts with hubris born of decades-long unchallenged dominance, protected by government policy.

Cars in Pakistan – a brief history

The region that now constitutes Pakistan was one of the least industrialised parts of pre-Partition India. As a result, at the time of independence, there was absolutely no vehicle assembling capacity in the country. That changed shortly afterwards. In 1949, while India was experimenting with Nehruvian socialism, Pakistan had taken a decidedly capitalist approach to organizing its economy and thus was able to attract General Motors that year.

GM began to assemble Bedford trucks and Vauxhaul cars (a British brand of cars they had bought in 1925). Soon, Pakistani companies began partnering with other American companies to begin assembling other American brands in the country. In 1955, Ford partnered with Ali Automobiles to assemble its cars in Pakistan, Chrysler partnered with Haroon Industries in 1956, and American Motors partnered with Kandawalla Industries in 1962.

These companies never actually manufactured any parts in the country. They were simply assemblers of products manufactured in the United States, or in US-owned plants in Europe. During this period, car ownership was understandably rare, but the few cars that were owned by Pakistanis tended to be American.

(There were, of course, the odd old-school elitists who reminisced about the British era and so kept their loyalty to Rolls Royce. But they were a distinct, if filthy stinking rich, minority.)

That American flavor to Pakistani cars came crashing down in 1972, when the left-leaning Prime Minister Zulfikar Ali Bhutto decided to nationalize all large industrial units in the country. All of the assemblers were consolidated into one organisation, the Pakistan Automotive Cooperate, or PACO, as socialist a name as it gets.

The results of this nationalization were predictable, to say the least. Production and quality cratered, and the up and coming Pakistani middle class relied even more heavily on imported cars to fulfil their needs than ever before. The government was able to achieve somewhat greater localization of the components of the cars, but remained far short of its 75% target. And what localization did happen significantly diminished the quality. It was, after all, a government-controlled company, which meant that supply contracts were available to those with the political connections to go after them, quality be damned.

In 1980, the government decided to start a partial privatization of PACO. Suzuki was the first company to jump into this market, leading to the creation of Pak Suzuki Motor Company, which initially had just a 12.5% stake from Suzu-

ki, with the rest owned by the government. The company started off with the capacity to manufacture 45,000 cars a year by taking some of the plants owned by PACO. By 1990, PSMC built a new plant at Port Qasim, an industrial suburb of Karachi, which took production capacity up to 50,000 cars a year.

In 1992, the government decided to allow private sector companies to outright own auto companies in the country, and placed minimal localization requirements on them. As a result, Suzuki bought out a majority of PSMC, taking its eventual share up to 74%, which is where it stands today. That same year, Honda extended its partnership with Atlas Group, which had been its partner in motorcycles since 1962, to passenger cars and created Honda Atlas Cars.

And in 1993, Toyota partnered with the Habib family to create Indus Motor Company.

There were a cast of other companies that came and went. Ghandhara Industries partnered with Isuzu to make trucks, and with Nissan to make cars. Dewan Farooque Motors worked with Hyundai and Kia to make hatchbacks and sedans. None of them ended up mattering, at least through the late 2010s.

From the early 1990s, the Big Three – as they soon became – came to a tacit agreement. Suzuki kept its monopoly on the hatchback category and Honda and Toyota slugged it out for the sedans. If any new entrants came onto the market (and many tried), they were quickly sullied and sent packing.

In this way, for nearly three decades there were essentially only six options for locally assembled ‘family cars’ in Pakistan. Suzuki at any given time was assembling three to four hatchbacks, with mainstays including the Mehran, the Alto, and the Cultus. Meanwhile Honda produced its cheaper sedan the Honda City, and it’s more expensive competitor to the Toyota Corolla the Honda Civic. Toyota focused on making just one car, albeit in different variants

with different engine sizes.

Car production and domestic sales kept limping along at levels below 50,000 vehicles sold in the entire country per year until about the mid-2000s, when the Musharraf Administration’s privatization of banks resulting in the rapid expansion of consumer credit, and car loans became available en masse for the first time in Pakistani history. Car sales took off from under 70,000 in 2003 to nearly 185,000 in 2007, an astonishing pace of growth.

The 2008 financial crisis brought that lending to a halt, and with it came crashing down car sales to a mere 85,000 units in fiscal 2009. Sales slowly crawled back up as both the economy and lending recovered, but were then supercharged during the latter half of the Imran Khan Administration, which encouraged the central bank to loosen regulatory requirements for auto lending, which led to a record-breaking pace of sales. The total number of cars and SUVs sold in Pakistan almost hit 284,000 in fiscal 2022.

The breaking of the oligopoly

By 2022, however, the dominance of the Big Three was already breaking. In 2016, the Nawaz Administration overcame staunch opposition by the Big Three to launch a new automotive policy designed to offer incentives to new manufacturers in the country and introduce both more consumer choice and more competition.

Then came Lucky Group with Lucky Motor Corporation, which launched an assembly partnership with Kia, introducing new lines of small and mid-sized SUVs into the country. The Nishat Group partnered with Hyundai and did the same. This came at a time when globally, Kia and Hyundai have been taking market share from the major American and Japanese automakers even in developed markets.

Then in 2018, Sazgar Engineering, previously only known as an assembler of rickshaws, announced a partnership with Chinese car manufacturer Great Wall Motors, maker of the Haval brand of vehicles, launching its first locally assembled cars in fiscal year 2023.

But it was not just the competition that hit these companies. From late 2021, inflation started to skyrocket as the Imran Khan Administration printed money and subsidized fuel consumption in a bid to stay in power amidst political protests by the opposition. In a bid to control the outflow of foreign exchange, the government in 2021 started placing restrictions on the import of automotive components, meaning that the local assemblers could not import parts from other countries in order to assemble in Pakistan.

With both demand being low and supply being restricted, companies chose to shut down as there were few signs that the situation

was going to improve.

Only in the last year, the three companies have seen plant closures with Honda closing the plant for 17 days, Pak Suzuki closing for 55 days Indus Motors closing its plant for a whopping 90 days. That means Indus Motors closed its plant for a quarter of the time in the last year.

And then came the hybrid boom.

The demand for hybrids and SUVs

One more nail in the coffin seems to be the incentives given in the latest federal budget: concessionary sales tax rates were announced for hybrids while advanced income tax was increased on locally assembled cars, increasing their prices.

While this is not designed to weaken the power of the Big Three, it had that effect nonetheless. Among them, only Toyota assembles a hybrid vehicle in Pakistan. The lower sales tax – and rising fuel prices – were a killer combination of incentives for manufacturers of hybrid and electric vehicles, which in Pakistan do not include Honda and Suzuki, and even Toyota has very limited offerings in this segment.

Then there is the fact that a larger and larger proportion of the Pakistani upper middle class is not satisfied with sedans and wants affordable SUVs. The only one among the Big Three that even offers a locally assembled SUV is Toyota, with the Fortuner.

Kia and Hyundai launched in Pakistan with a small and mid-sized SUV focused strategy and began to eat into the market particularly for the more expensive end of sedans, such as the Toyota Corolla and the Honda Civic.

And then the Chinese companies came in with their cars that are both cheaper, and also offer what the consumer wants: hybrid SUVs.

Sazgar and Haval

One of the biggest success stories of the past two years is the sales of H6 and Jolion branded cars being sold by Sazgar Engineering. These cars are originally manufactured by Great Wall Motors in China and they are being assembled in the country by Sazgar Engineering. In a period when sales of many of the assemblers have shrunk from last year, Haval has seen its sales actually grow by more than 3 times in the same period. The company saw sales of 1,657 units in 2023 which jumped to 5,319 in 2024. This success story has not gone unnoticed by investors. The share price of the company was languishing at Rs50 as recently as June 27, 2023. It nearly touched the Rs1,200 per share mark in a span of one year. This was a gain of 2,400% on an investment made last year. To put it in context, the stock market itself has only increased by 100% in the same period. So what is Sazgar Engineering and what is their secret sauce?

Sazgar is a company that has been in the market since the 1990s. A few years ago, the company name was synonymous with green coloured three-wheeled rickshaws buzzing around the country. The company established its first plant for manufacturing of three-wheeler vehicles at Raiwand Road and recently set up its car plant near Sundar, both industrial estates near Lahore, as well.

After the auto policy 2016-21 was announced, the company ventured into the four wheel market with the introduction of Haval brand in the country. The company has also entered the Hybrid Electric Vehicle market now by launching the Haval-HEV which will be locally produced/assembled.

How has the company performed in recent times? Both revenue and profits have been going up dramatically.

During the nine months of the fiscal year ending June 30, 2024 – the latest period for which financials are available – the company recorded revenue of Rs35 billion, compared to just Rs18 billion in the same period last year. The company has actually increased its gross profits from Rs 2.5 billion to Rs 9 billion and its gross margin has increased to 26% for the year. The company also saw its operating profit go to Rs 7 billion from Rs 1.5 billion in the whole of last year. The company has also improved its operating profit margin from 8% to 21% while the company was able to retain Rs 4.4 billion in net profits compared to Rs 0.9 billion in 2023. This meant that its net margin also more than doubled from 5.5% to 12.9%.

A caveat that needs to be attached here is that these 9 month sales figures represent sales of 10,000 units of rickshaws and 3,172 units of cars. The actual figures at June end for rickshaws came to around 15,014 and for cars it came to 5,319. Based on the upward trajectory, it can only be expected that these numbers will improve further. This would mean that a company which had an earning per share of 1.95 per

share in 2022 will see an earning per share of more than Rs 73.59 which was recorded for the 9 months period ending in March 2024.

In order to show just how important car sales were for the company, out of total sales of Rs35 billion, cars made up Rs 30 billion in terms of revenue for the company. In terms of operating profits, the company earned Rs 7.5 billion from the cars segment out of Rs 7.6 billion for the company combined.

“Alhamdulillah it has been a great run so far and a divine hand was surely at play for the success we have received. There is a growing shift in the consumer base for New Energy Vehicles and being the first mover in this new segment was a big advantage for us. We currently have the biggest NEV lineup to choose from in Pakistan - Jolion HEV, H6 HEV, Ora 03 BEV, Tank 500 HEV.” states Ammar Hameed, Director Marketing at Sazgar, commenting on the performance of the company and its share price.

The latest annual accounts available for the company are till June 2023 which means that these accounts reflect the sales that were seen by the company for that period which were around 1,657. The company will release its annual accounts for the most recent year in a few months which will show the profitability of the company when it sold a record 5,319 units in 2024.

Over the past year, there have been developments which have helped the company grow further. The Punjab government recently started licensing electric rickshaws which has seen an increase in sales. In addition to that, the company has invested in a 130 Kanal facility in order to expand its car plant further seeing the increasing demand for its products. The company has also gotten its cars ISO certified and its credit rating has been upgraded to A for long term and A-2 for short term. The company has also introduced the ORA and tank-500 which further enhances the product portfolio it provides. Lastly, the company has also started booking for Haval Jolion HEV which has seen people book them in large quantities.

Pivot or Perish

Based on these matters, there can be a few conclusions that can be drawn. First of all, after the implementation of the auto policy, new car companies have entered the market which has broken the monopoly seen by the Big 3 in the past. Consumers feel that they can get a better product at a better price and they need to be wooed in order to be attracted to the old options they were given before. Based on the price point of many of the Big 3, it seems they have little to offer in return. In addition to that, it seems consumers are moving towards bigger SUVs which offer something in addition to the variety that they previously had. There is a significant shift towards people moving from buying Corollas and Civics to buying Tuscons, Sportage and Haval branded cars which not only offer better value for their money but also adhere to a better quality standard. The fact that there are models of Suzuki Alto that do not have power windows shows that the Big 3 are trying to sail on their name for too long.

Another shift which is being seen in the market is consumers moving towards Hybrid Electric Vehicles. With the cost of fuel reaching sky high levels, there is a demand to cut down

Sazgar Price increase

on some of this cost by investing in a HEV which does make some economic sense. This move has gotten so much traction that Indus Motors recently introduced its 4th generation Toyota Corolla Cross Hybrid Electric Vehicle which is both a SUV and an HEV.

The example of Sazgar shows that there is a market where consumers are willing to pay top dollar in order to get access to better cars and better technology. The Big 3 seem to have missed a trick by not keeping close tabs to the consumer market and trying to impose their products on a dynamic and changing market. Now it seems they stand at a crossroads going forward into the future.

Suzuki might be the best place in the Big 3 to be able to weather some of the storm going forward. The company made up more than 61% of the total cars sold by the Big 3 and saw a decrease of only 17% in terms of its sales last year. It seems there will always be a market for the company as most of its sales are made up of Alto being sold which is the cheapest car available currently.

As mentioned before, Toyota has tried to react by launching an HEV version of its Corolla Cross which might seem to sustain the company to some extent. The company has also decided to source most of its material locally in order to protect it from shocks that it suffered in the last two years. With imports being restricted, companies had to shut down due to lack of raw material required for their production. With Rs 3 billion being invested, it can be seen that the company is looking to pivot to some extent.

The worst placed company in the face of this is Honda which was only able to sell 13,214 units in the last year. The company has no EV based vehicle that they manufacture and even the SUV they assemble, the BR-V, has seen dismal sales figures in the recent past. At this juncture the Big 3 have a decision to make. Either they pivot and try to hold onto their market share or perish in the situation that exists. n

Is the govt about to let go of its control on petrol prices?

The PM claims he is about to deregulate petrol prices. The govt was barely in control anyways

By Ahmad Ahmadani

Perhaps one of the most infuriatingly frustrating features of Pakistani politics is fuel pricing. What makes this particular facet of governance particularly annoying is the lack of control that any government can exert on the issue of fuel prices. Pakistan does not produce its own fuel and its consumption is entirely dependent on imports. As such, Pakistani consumers are beholden to international fuel prices which play out in pedantic and predictable ways. If the international price of oil foils, whoever is

in father touts it as a win. If the prices are on their way up, whoever is in the opposition runs with it.

There have long been calls to stop the politicisation of this subject. All have fallen on deaf ears. One reasons, of course, is that the government does regulate petrol prices to some extent. They charge levies and taxes on it and also make sure the price of petrol is uniform across the country.

Until now.

The government is making efforts to relinquish its role in setting petroleum product prices. It has been reliably learned by Profit that Prime Minister Shehbaz Sharif has directed the petroleum division to finalise and

present the deregulation framework for petroleum products. A meeting about this topic was supposed to be held on the 25th of July but no details have emerged since. What we do know is that the Petroleum Division, in a letter dated July 24, 2024, has asked OGRA Chairman to present the matter along with analysis, implications, and the way forward for deregulation of the petroleum sector.

What will this look like? Consumers near courts and refineries would benefit and attention would be diverted largely towards Oil Marketing Companies (OMCs) rather than the government. Or that is what they are hoping for. The question is, could it work?

How it works right now

Petrol prices in Pakistan are determined by a number of factors. The main input is the international price of crude oil, which is imported into the country by oil refineries which then process it and turn it into fuel. The price of fuel after processing is what is known as the ex-refinery price. But then other things get tagged along onto this. A margin is added to make sure the price is uniform throughout the country and not cheaper in areas close to the refinery, distributors naturally take a cut, and then dealers and petrol pumps also charge their own service premiums. On top of this, the government also takes a cut. Petrol is currently subject to a petroleum levy of around Rs 40 per litre.

The base price is the imported price, in the case of oil imports, or the ex-refinery price in the case of domestic oil production. On top of that, there are retailer and freight costs which include the inland freight equalisation margin, OMC profit margins (what PSO, Shell, etc. earn), and dealer commissions (what the petrol pump owners get to make). Lastly, comes the taxation which includes general sales tax and the petroleum development levy. The ex-refinery price is the price at which refineries can sell their fuel to OMCs and the price at which importers can sell distillates within Pakistan. One of the first additions that happens to this initial pricing are the commissions that retailers and dealers receive.

The next significant addition is the Inland Freight Equalization Margin (IEFM), which is the cost of inland movement incurred by a refinery for the transportation of crude oil from the source to the refinery. It also includes the cost incurred by an OMC while transporting the finished product to various depots across the country. This basically includes all transport costs within the company. The purpose of this margin is to establish and maintain parity in the prices of fuel throughout the country. The money collected from this margin goes on to create a pool.

After all of these pricing tools, we finally come to taxes, because the last two additions to the price the consumer sees at the gas station are the general sales tax (GST) and the petroleum development levy.

The GST is a ratio rather than an absolute number, it varies with a change in the price of petrol. The levy, on the other hand, is a surcharge and set as an absolute rupee amount per litre, though the government does vary how much it charges under this tax relatively frequently. It is used as an instrument to bring about stability in the price of petrol by offsetting the impact of drastically changing import prices and costs associated with fuel. The levy,

however, is often seen as a political and fiscal tool to either pass on ‘relief’ to consumers during an election year or to generate more revenue in other years.

The role of the OMCs

The prices of fuel in the country are decided based on the average price available through Platts plus PSO’s premium. The weighted average cost of supply is calculated by OGRA, the oil sector regulator every fortnight the cost build up for the marketing companies is then applied to this average to include margins for OMCs and inland freight equalisation, commissions for the dealers, petroleum development levy and so on. The retail price is set by the regulator in this way. OMCs can make their money from the margin allowed to them in the cost build up, or by hunting down sources of supply cheaper than the weighted average cost calculated by the regulator.

As of now, the government controls and caps many of these margins. But under the new proposition being heard, all this would change. How would it affect things?

While the final framework will need approval from the federal cabinet and the Special Investment Facilitation Council (SIFC), deregulating petrol and high-speed diesel (HSD) prices will end uniform pricing across the country, allowing oil companies to set their own prices for different locations, they added.

As per sources, the government has faced public criticism for rising petroleum prices and is accelerating the deregulation process to shift public discontent towards the OMCs. Currently, the government announces fortnightly fuel prices based on OGRA’s calculations, which reflect international market fluctuations and exchange rates.

In the past, the government only notified

kerosene prices, while petrol, HSD, and light diesel oil prices were influenced by notified tax rates and fixed profit margins for dealers and marketing companies. The oil industry sets its own rates for furnace oil and high-octane blending components (HOBC).

Now, the government plans to fully deregulate petrol and diesel prices, including OMC and dealer commissions, similar to HOBC. The IFEM mechanism is also expected to be deregulated, leading to significant price variations between cities and oil companies. Consumers near ports and refineries may benefit from lower prices, while those further away may face higher costs, with differences ranging from Rs3 to Rs8 per liter.

On the other hand, regarding the government’s proposal to deregulate the petroleum industry, the Pakistan Petroleum Dealers Association (PPDA) expressed concerns that deregulating diesel and petrol prices and profits could lead to a monopoly by oil marketing companies (OMCs).

Sources have indicated that petroleum dealers might oppose transferring price-setting authority to oil marketing companies (OMCs) due to concerns about potential unfair profiteering by the OMCs.

Nauman Ali But, a senior leader of the PPDA while talking to Profit said that even under the current regulated system, OMCs are involved in illegal activities, irregularities, and the exploitation of dealers’ margins. Applications highlighting these issues have already been submitted to the Competition Commission of Pakistan through the Chairman Senate and Secretary Petroleum.

The PPDA warned that giving OMCs free rein could cause widespread anxiety and anger among dealers. They emphasised that dealers, as key stakeholders, should be included in any decisions regarding this sudden change.

“OGRA, OMCs, and representatives of the PPDA should all be part of this process,” said Nauman Ali Butt, senior representative of the PPDA.

It is relevant to note that the Oil Companies Advisory Council (OCAC), representing over three dozen oil companies and refineries, previously warned the government about the impact of smuggled petroleum products from Iran on local investment and refinery operations. In a letter to the SIFC, the council highlighted the risks to upcoming investment projects due to ongoing smuggling.

It is pertinent to mention that the government has been under public criticism for rising petroleum product prices. However, with rising fuel prices and industry complaints about smuggled oil products, the government is expediting the deregulation process to shift the burden of public criticism the OMCs. n

By Zain Naeem

It seems like Honda Car is being impacted by the same downturn that has been plaguing the other two major car assemblers in the country. Namely the fact that they are seeing declining sales. The latest figures show that the company was only able to sell 13,214 units from July 2023 to June 2024. This was the worst year for the company since it broke through the 13,000 units threshold back in 2012. Since then, the company saw sustained increase in sales reaching a peak of 51,494 in 2018. Since then, the company had some good years while others were bad. Even during the early years of the pandemic, the company was able to sell more than 16,000 units. The recent figures show how bad the situation has become for the company as it has seen its sales decrease by around 66% from where they were in 2022.

The decline in its sales can be attributed to the fact that consumers are moving away from the generic cars that were being provided by these companies and are preferring to buy hybrid electric vehicles which are being offered in the market. In addition to that, as income is stagnant and prices of cars have shot upwards, people are spending less and less on big ticket items. That coupled with record high interest rates have meant that demand has been low for auto financing as well.

The consequence of these decisions is becoming more apparent in terms of the financial performance of the company. The latest annual accounts show that the company has seen its revenues fall by nearly half from where they were last year. Sales of Rs 95 billion were made last year which have contracted to Rs 55 billion this year. Similarly, gross profits have fallen from Rs 7 billion to Rs 4.5 billion for the current year. A bright spot is the fact that the company saw its gross profit margin improve from 7.5% to 8% this year.

The biggest gain that the company saw was that last year they recorded exchange losses of Rs 5 billion due to the currency fluctuations that had taken place. With a stable rupee, the company saw exchange losses of only Rs 0.4 billion this year. The company has also made some shrewd investments with some of its assets which gave a gain or Rs 2.3 billion last year and clocked in the same for this year as well. If exchange loss decreased, the company paid heavily in terms of its finance cost as the finance cost quadrupled from Rs 0.3 billion last year to Rs 1.2 billion this year. This meant that profit before tax was Rs 2 billion last year and actually increased to Rs 2.7 billion this year owing to the exchange losses decreasing. After taxation was taken into account, the company saw its net profit jump from Rs 0.3 billion to Rs 2.3 billion. Due to the increase in net profits, the company saw its net margin go from 0.3% to 4.2% for the year.

Looking at the latest quarter numbers, it seems Honda Car has been able to claw back some

of the lost ground compared to last year. In the first quarter of the latest financial year, the company was able to sell 3,285 units which was only 601 units last year. The higher number of sales was reflected in the revenues earned by the company which were Rs 16 billion this year compared to only Rs 3.8 billion last year for the same period. The company saw a gross profit of Rs 1 billion for the latest quarter where they had actually made a gross loss of Rs 0.1 billion for the same quarter. The gross margin came to around 6.3% which was -3.9% last year. In terms of expenses, the company saw a decreased earning from its investments and its finance costs increased by 6 times due to its size of short term borrowings. This meant that even though the company made a healthy gross profit, net profit only came to around Rs 0.2 billion which was Rs 0.14 billion last year for the quarter.

In terms of the performance of the company, it has become evident that its sales trajectory is on a downward slope and seeing the situation in the market, the problem affecting the other two major assemblers namely Pak Suzuki and Indus Motors is also impacting Honda Car. Pak Suzuki sells nearly half the cars in the Big 3 which means that they will be able to weather the storm to some extent going into the future. With consumers demanding better and efficient cars, Indus Motors has also introduced the Toyota Corolla Cross which is a Sports Utility Vehicle (SUV) and a Hybrid Electric Car (HEV) which is being demanded by the market. Honda Car seems most vulnerable at this point as it is mostly relying on selling its Civic and City model cars while response to its SUV has been mild to say the least.

In the face of this situation, the company carried out its corporate briefing session and discussed how it was looking towards the future. The company has announced that they are looking to launch hybrid electric vehicles in the near future in order to capitalize on the opportunity that exists. The company plans to introduce Completely Built Units (CBUs) initially and once it can gauge the demand, it has plans to set up its own plant. The company is looking to invest capital expenditure of around Rs 5 billion in the coming year or so to develop an assembly line.

The company also expects some recovery in the market for its current product portfolio which can see higher demand in the next two to three years. In regards to the latest quarter showing lower gross margins, a representative at the company stated that due to the recent tax policy introduced by the government, the goal was to cut the margins of its cars in order to reduce the tax expense. The government recently imposed a tax whereby cars selling for more than Rs 4 million would be levied an additional tax. In order to provide a relief to its customers, the company cut margins on its City variant of cars which meant that its gross margins fell for the quarter even though sales increased. n

The double whammy of declining electricity demand and increased consumer tariffs

Electricity generation in the country dropped by 10%, while capacity payments surged by a whooping 29% in FY 23

By Nisma Riaz

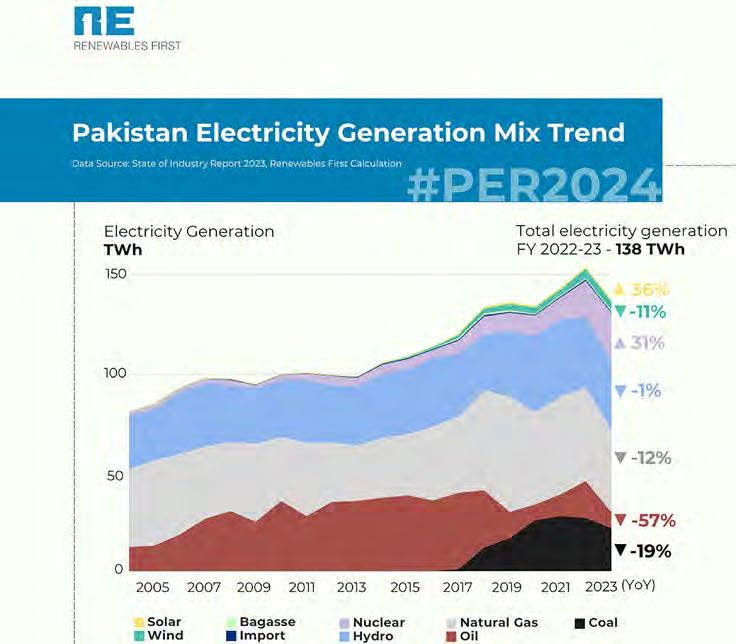

The fiscal year 2023 witnessed a puzzling conundrum where electricity generation in the country plummeted by over 10%, capacity payments soared by a staggering 29%. This surprising divergence, where installed capacity grew amidst shrinking demand and soaring costs, highlights a critical turn for the country’s energy landscape.

A recent review of the year that was for the power sector paints a grim picture of the current state of the country’s power sector. In an event, attended by a mix of both local and international experts, the think tank provided an in-depth look at the electricity sector’s turbulent year, from July 2022 to June 2023.

Trends in Pakistan’s electricity and power sector

According to the electricity review presented by Rabia Babar from Renewables First, there was a significant decline of 10.4% in electricity generation, primarily due to a decrease in fossil fuel generation. Specifically, generation from oil saw a reduction of 57%. This decline in fossil fuel generation can be attributed to increased fuel prices following the Russia-Ukraine War, higher KIBOR and LIBOR rates, increased CPI rates, and PKR currency devaluation.

In terms of renewables, wind energy

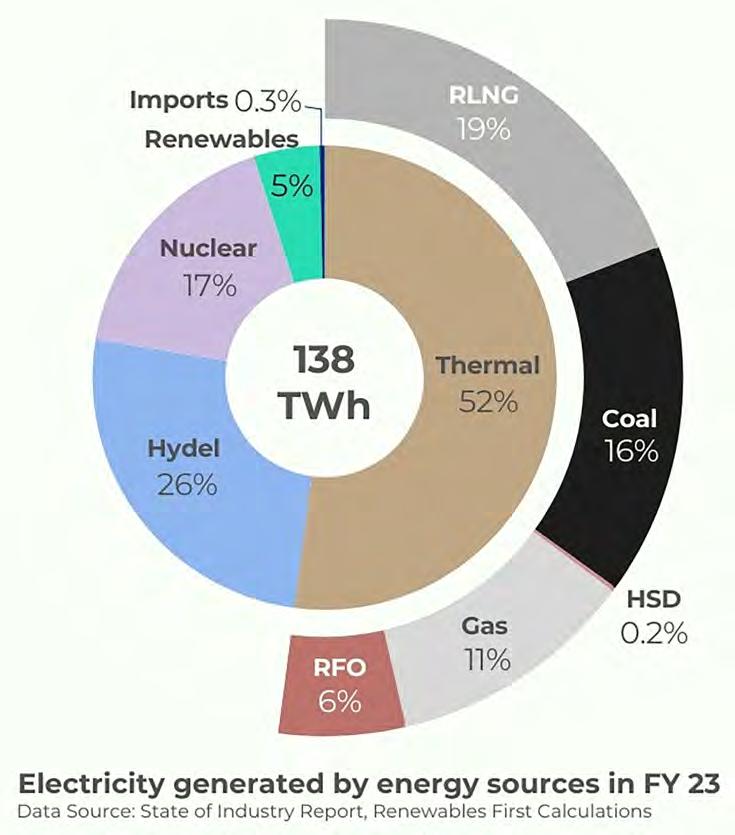

generation significantly declined from 4.5 terawatt hours to 4 terawatt hours, possibly due to wind curtailment in the power sector. Examining the generation mix for the recent fiscal year, thermal energy accounted for 52% of total electricity generation, with the highest contribution from regasified liquefied natural gas (RLNG) at 19%, followed by coal at 16%. Renewable energy held a 5% share, while nuclear energy increased to a 17% share in the generation mix. It must be noted that there are seasonal variations in the use of different energy sources.

Hydroelectric generation plays a crucial role during the summer months when river water flow is high, coinciding with Pakistan’s peak electricity demand. In contrast, during winter months, when hydro generation is low, thermal generation primarily meets the demand. Renewable energy sources such as solar and wind can serve as reliable substitutes for flexible loads during periods of low hydroelectric generation and a complement during high demand in the summer. Additionally, pumped storage can be explored as a solution to address intermittency issues associated with wind and solar power generation and to supplement peak demand.

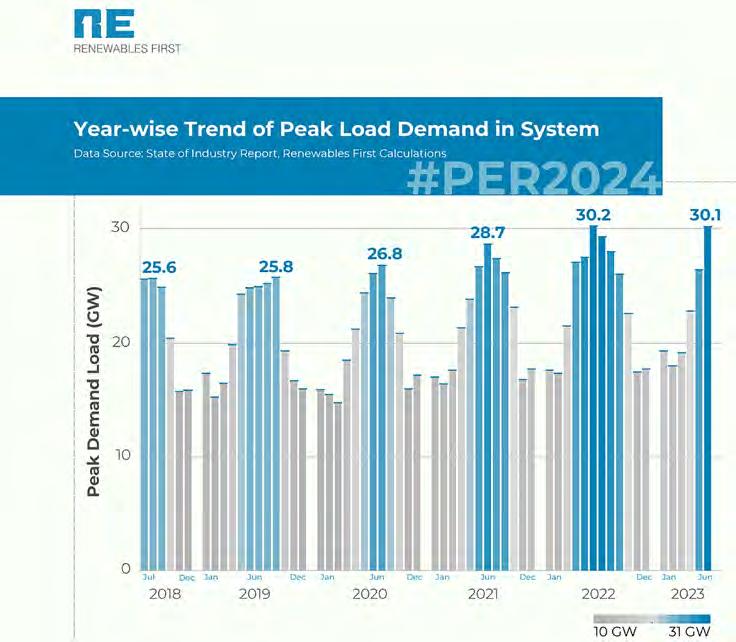

The trends of peak load demand are greatly impacted by the challenging economic conditions in Pakistan.

From 2018 to 2022, there was a gradual increase in peak load demand. In 2018, the peak demand load was 25.6 GW, which steadily increased to 30.3 GW by 2022. However, in the recent fiscal year, the peak demand load saw a slight decline of 0.3%. During summer months, peak demand is managed through fuel-based peaker plants, which remain idle outside peak periods. An interesting trend is the rise in solar and wind generation during summer, with wind generation ranging between 500-600 GWh. Exploring renewable energy hybrid solutions could help address peak demands and mitigate this issue

Electricity sales growth also shows a decreasing trend.

In fiscal year 2023, electricity sales experienced a significant decline of 10% yearon-year, reflecting the earlier discussed trend of reduced electricity generation. Despite an increase in the number of electricity users, sales dropped sharply, primarily among domestic and industrial users. For domestic users, high electricity costs led to reduced usage and a shift towards distributed generation through rooftop solar installations to decrease dependency on the national grid. The decline in industrial consumption can be attributed to multiple factors, including a slowdown in GDP growth, which mirrors the decline in electricity consumption. Additionally, industries increasingly rely on captive power plants and solar power to meet their energy needs.

Addressing reliable energy needs and clean energy requirements is crucial for industries to cope with scope 2 emissions and

comply with the Carbon Border Adjustment Mechanism (CBAM) to remain competitive in the international market. High electricity costs are a significant factor driving consumers away from the national grid.

The power purchase prices comprises two main components: the Energy Purchase Price (EPP) and the Capacity Purchase Price (CPP). The EP primarily covers fuel charges and variable operation and maintenance (O&M) costs of generation plants. In contrast, the CPP is the capacity payment for each generation plant in the fleet. In fiscal year 2023, the CPP experienced a significant growth of 29% year-on-year, emerging as a crucial factor driving up tariffs across the country. This increase in capacity payments has contributed significantly to higher electricity costs.

These trends are a direct result of high inflation and the government’s need to appease the International Monetary Fund’s (IMF) demands, in order to secure a substantial bail out, the costs of which are paid by the public. Given the rising electricity costs,

policies to boost sales growth are essential. Efforts should focus on bringing consumers back to the national grid, as a shrinking consumer base would further strain the power sector’s revenue.

Capacity Payments Trend Over the Years

The increase in capacity payments over the years has not been solely due to thermal plants; nuclear and hydro capacity additions have also played significant roles. For instance, in fiscal year 2023, the thermal share in capacity payments increased by 38% yearon-year, largely due to the addition of three coal-based plants to the generation fleet. Additionally, the inclusion of K-2 and K-3 nuclear plants in recent years has increased the nuclear share in capacity purchase payments.

The electricity review provides insights into the power purchase price projection, as well as a forecast of electricity generation for the current and next year.

A comparison of power purchase projections for fiscal years 2024 and 2025 indicates a reduction in overall electricity generation from 139 terawatt hours in FY 2024 to 135 terawatt hours in FY 2025. When examining the percentage change in energy sources over these two fiscal years, the share of renewables is projected to decrease from 6% to 5%, while the share of RLNG is expected to increase by 12%. This shift will likely add to the country’s fuel import bill.

For fiscal year 2025, the national average power purchase price, after adjusting for losses, system charges, and the market operator fee, is projected to be PKR 27 per kilowatt hour. Examining energy source-wise pricing, the power purchase projection for solar has increased significantly, while the price for RLNG is projected to decrease by 35% compared to fiscal year 2024.

The fiscal year 2023 was marked by challenges in managing capacity payments, power purchase prices, and shifts in energy generation sources. With capacity payments rising significantly and a forecasted increase in power purchase prices, addressing these issues through strategic planning and policy interventions is crucial for ensuring the sector’s financial viability and sustainability.

Why is Pakistan in this crisis and what needs to be done?

It is clear that Pakistan’s recent power sector planning has faltered, leading to soaring tariffs, regulatory pressures, and utility crises. To address these issues, it’s crucial to overhaul the planning process with a strong foundation in data-driven strategies.

Sohaib Malik, an energy analyst at a

European renewable energy company, commenting on the cycle of grid abandonment and rising costs during the current economic crisis, said, “Examining the current dynamics of the power grid, it’s clear that while reliability has improved, evidenced by reduced load shedding, the cost of electricity remains a significant concern.”

“As a consumer and energy analyst, I see that the trade-off for better reliability has been higher costs, impacting both consumers and industries. Although capacity has increased, the expected GDP growth and demand haven’t materialised, partly due to rising reliance on imported fuels. This discrepancy has led to decreased demand and heightened affordability issues, creating a cycle where high prices discourage consumption. Addressing these challenges is crucial to ensuring both affordability and effective grid utilisation,” Malik said.

Pakistan’s utility sector is trapped in, what Malik calls, the “utility death spiral,” where declining profitability accelerates its financial collapse, hindering its ability to meet revenue needs and remain operational.

One of the biggest reasons why we find ourselves in a utility death spiral is because when the IMF program began, the government chose to pass all power sector costs to consumers. This led to reduced production, demand, and GDP growth while exiting the crisis. Alternatively, continuing support for

industry and incentivizing electricity use could have utilised idle capacity, potentially spurring economic development and GDP growth.

Speaking on the matter, Abubakar Ismail, a local energy and industry expert, said, “To advance under the IMF program, Pakistan must address tariff design and capacity payments. And discussions are underway to eliminate cross-subsidization by passing subsidies directly to consumers and improving the efficiency of tariffs and capacity utilisation.”

Ismail highlighted that the ideal policy would have been to establish an open market five years ago, allowing the purchase of energy for critical times and summer months while adding about 60% to 70% capacity. “Currently, with over 50% of capacity controlled by outdated government-owned plants, scrapping these inefficient units and reallocating their manpower could improve efficiency,” he said.

Continuing on possible solutions, he also shared that, “The current debate involves four RLNG plants: two owned by the federal government and two by Punjab. Tariffs have decreased from 16% to 12% dollar-based returns, but the government still requires dollar-based returns to attract foreign investment. To address this, the dollar rate could be fixed at 200 rupees, and returns adjusted accordingly. Reducing certain capacities and

focusing investment on transmission and distribution infrastructure for the next two to three years could enhance regional tariff competitiveness, particularly in textiles, and improve overall consumption.”

Ismail stressed that there is a compelling case for considering the early retirement of certain energy projects, such as those using RFO, RLNG, or imported coal. Despite their relatively recent installations, their utilisation rates are low. Engaging in discussions about this, supported by international financing mechanisms, could drive down costs significantly and attract interest from global stakeholders.

When asked whether it’s possible to address this issue during the IPP renegotiation process that Pakistan is about to initiate, Malik responded, “To tackle Pakistan’s energy challenges, several strategic actions are crucial. Firstly, the government should examine successful international models, such as Indonesia’s Just Energy Transition Program and ongoing discussions with countries like Vietnam and South Africa, to draw valuable insights.”

“Engaging with key partners, both international and local, is essential to develop and execute effective solutions. Additionally, creating an integrated energy plan is vital, one that balances sustainability, affordability, and reliability by carefully assessing capacity needs and addressing seasonal consumption patterns. Emphasising long-term sustainability involves planning for a shift towards a more sustainable energy mix while managing the current reliance on base load power. Finally, it’s important to continually refine and update the energy strategy based on evolving demand profiles and technological advancements, ensuring the plan remains effective and responsive to changing conditions,” he concluded.

He highlighted that the government needs a more educated and informed strategy, while the private sector must recognise that if they don’t contribute to stabilising the sector, it risks collapsing, which will ultimately impact them as well.

Moreover, during the panel discussion, Dr. Fiaz Chaudhry from LUMS Energy Institute discussed the challenge of managing peak demand, which exceeds 30,000 MW primarily due to cooling needs. Despite a system capacity of 30,000 MW, the current supply only meets 25,000-27,000 MW. With utilisation remaining low at 23% outside peak months, concerns about cost recovery and tariff adjustments arise, likening the situation to charging fares for empty bus seats. For effective supply, both generation and comprehensive transmission infrastructure, from bulk to local distribution, must be fully aligned and operational. n

OPINION

Ahtasam Ahmad

If equity injection is a drug, Microfinance Banks are an addict

Sponsors step in as MFBs grapple with capitalization crunch

The landscape of microfinance banking in Pakistan is a complex one, combining both skepticism and optimism. The sector faces challenges due to its exposure to economic shocks that can impact low-income borrowers. It is essential to carefully analyze the vulnerabilities of institutions operating in this segment.

Nevertheless, the pivotal role of the microfinance banking sector in providing financial services to underserved populations in Pakistan is a notable accomplishment. This underscores the critical importance of microfinance in promoting financial inclusion and economic empowerment within the country’s most vulnerable communities.

Microfinance banking in Pakistan dates back to the inception of Khushali Bank in 2000, which was established under a special ordinance. The subsequent MFI Ordinance of 2001 laid the regulatory foundation for microfinance institutions, with a specific focus on providing financial support to micro-enterprises and marginalized individuals as part of a sustainable poverty alleviation strategy.

What sets MFIs apart from traditional commercial banks is their unique approach to lending. They provide a substantial portion of their financing without collateral, catering to various economic activities, including housing.

This model allows them to serve clients who might otherwise be excluded from formal financial systems. MFIs typically deal in smaller loan amounts compared to commercial banks, with general loans capped at Rs. 350,000 and housing loans limited to Rs. 3 million.

The writer is an Editorial Consultant at Profit and can be reached at ahtasam.ahmad@ pakistantoday.com.pk

Remember the unique characteristics that set microfinance operators apart from commercial banks? It seems this very uniqueness is now pushing the sector into troubled waters. At the core of MFBs’ business model is unsecured lending - money lent without collateral, relying solely on personal guarantees and expectations of

But, the sector has had its own share of troubles over the past few years and there is no respite in sight.

The state of play

Currently, there are 12 Microfinance Banks (MFBs) in the country, with HBL Microfinance Bank, UBank, and Khushali Bank being the largest in terms of lending book size. The industry’s prominent sponsors include commercial banks, NGOs, and telecom operators, reflecting a diverse range of stakeholders. MFBs have demonstrated significant progress over the past five years. The asset base of MFBs has shown robust growth, with an average year-on-year growth of 19.1%.

Equally impressive is the substantial increase in the gross loan portfolio, which has doubled from Rs. 214 billion in December 2019 to Rs. 427 billion in December 2023.

This growth is not just financial; it’s also reflected in the sector’s expanding reach. The number of active borrowers has increased significantly, rising from 3.6 million to 6.3 million during the same period.

But, there is more to it

Though the expansion numbers might seem impressive, there’s a significant caveat: MFBs have recorded losses for the fifth consecutive year in 2023. While this might surprise those unfamiliar with the segment, industry observers are well aware of its inherent vulnerabilities.

borrowers’ future cash flows. Currently, it constitutes more than 50% of the sector’s lending.

This model functioned relatively well until 2020 when the pandemic unleashed economic chaos. The situation worsened with the catastrophic floods of 2022, which dealt a severe blow to the agri sector - the primary borrower base for MFBs. Consequently, banks had to restructure loans twice: first in 2020 and again in 2022. The recoverability of these loans remains questionable, and as MFBs provide for potential losses in their financials, it has pushed earnings into negative territory.

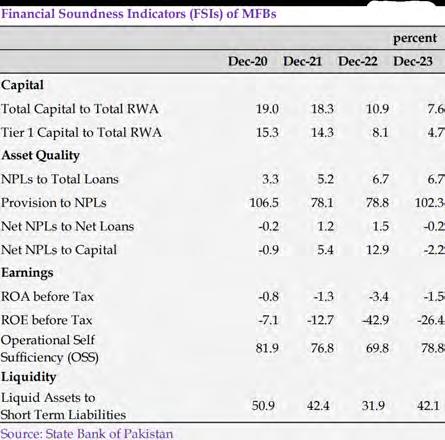

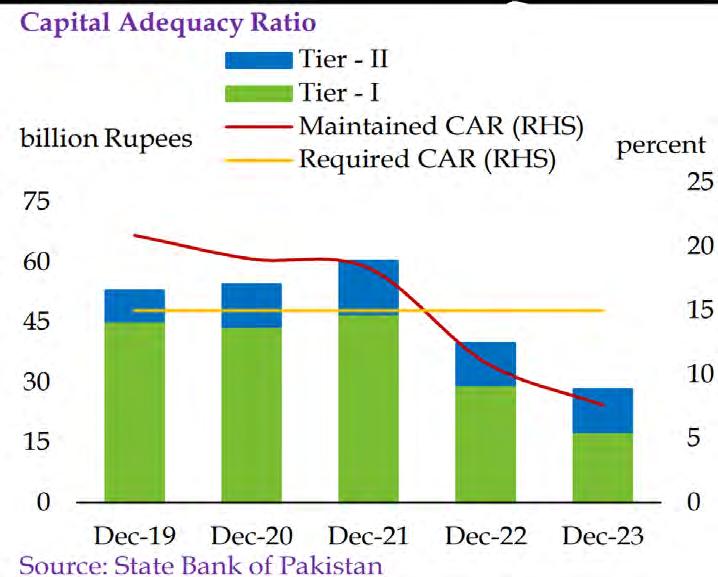

This financial strain has taken a toll on the MFBs’ capital base. Unsurprisingly, the sector as a whole is now undercapitalized, with a Capital Adequacy Ratio (CAR) of 7.6% - almost half of the State Bank of Pakistan’s (SBP) regulatory limit of 15%.

Adding to these concerns, both the International Monetary Fund (IMF) and the World Bank have flagged vulnerabilities in the segment. The IMF went so far as to block the government from extending deposit protection insurance to MFB customers. Their rationale? Undercapitalized banks in the sector pose a real risk of failure, which could result in a significant fiscal hit for the government if such insurance were extended.

Who’s sick? The business model!

While it’s true that not all MFBs are undercapitalized, it is the conventional business model of MFBs that is struggling in Pakistan. As of the end of 2023, several major

players - Khushali, Ubank, NRSP, FINCA, and APNA - remained undercapitalized, highlighting the widespread nature of the challenge. The MFBs that have maintained relatively better capitalization fall into two main categories. First are the telecom-backed institutions like Mobilink Bank and Telenor Bank. These have shifted their focus away from conventional microfinance banking to digital financial services products such as Jazzcash and Easypaisa, leveraging their parent companies’ technological infrastructure and customer base.

The second category comprises provincial or district-level banks with significantly smaller lending books.

HBL Microfinance Bank stands as a notable exception to these two categories. The MFB barely met the capitalization threshold with a CAR of 15.3% at the end of 2023. However, this comes at a cost. The bank has required almost Rs. 10 billion in equity injection over the past four years, including a recent announcement of Rs. 6 billion. To put this in perspective, Rs. 10 billion is the amount required to set up an entirely new commercial bank in Pakistan.

So where are we going with this?

Before delving into potential outcomes, it’s crucial to reiterate the importance of the microfinance sector. Despite representing only 1.3% of financial sector assets, these banks serve over 70% of all borrowers in the financial sector and account for approximately a third of all outstanding agriculture loans.

Now, turning to the troubled players in the sector, different strategies are emerging. For some, equity injections are likely to continue. Take Ubank, for instance. Its CAR further declined to 9.4% in the first quarter of 2024.

Subsequently, its board approved the conversion of its sponsor’s (PTCL) preference shares into ordinary share capital of Rs. 1 billion, and subordinated debt of Rs. 1.2 billion was also converted into ordinary share capital. Additionally, there was a cash equity injection of Rs. 1.2 billion.

For banks like NRSP and Khushali, which carry negative equity, the road to recovery appears longer and more challenging.

NRSP, for example, obtained in-principle approval from shareholders last year for the issuance of rights shares amounting to Rs. 3.5 billion. Of this amount, Rs. 1 billion has already been injected through advances against the bank’s rights issue. However, the issuance of the remaining Rs. 2.5 billion remains uncertain.

While Khushali Bank’s Board of Directors has approved two major plans to address recent losses: the Long-Term Strategic Plan 2024-2030 and the Self-sustaining Restructuring Plan 2024-2030.

The Long-Term Strategic Plan aims to boost growth and profitability of the Bank with Rs. 8 billion in capital injections. The Self-sustaining Restructuring Plan serves as a backup strategy in case new capital cannot be secured. The Bank is currently raising fresh capital from existing shareholders through a right issue.

For smaller players, it seems like the end of the road. Egypt-based fintech MNT-Halan has already acquired Advans Microfinance. While not officially confirmed, MNT-Halan is likely to leverage Advans’ license and operational infrastructure to enter Pakistan’s digital financial services market, rather than expanding microfinance operations.

Meanwhile, another fintech company ABHI, in partnership with TPL Corporation, is considering the acquisition of FINCA Bank.

Could it have been any better?

Looking back, it’s easy to spot where things went wrong. What really jumps out is how fast MFBs were growing. Sure, they were following the SBP’s push for financial inclusion, but they seemed to forget about the “sustainably” part of that directive.

Now it’s pretty clear that this growth was kind of reckless. These banks didn’t have solid risk management in place and were handing out loans left and right without much thought. When two major crises hit within just two years, it really exposed how shaky their foundation was. n