12 The federal government might abolish five ministries. That’s just scratching the surface

18 The story behind Pakistan’s biggest ever stock market dividend

22 Textile exporters denied tax relief; who to blame?

24 Can Artificial Intelligence make college counselling more equitable?

Profit

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

Who owns Pakistan’s digital wallet throne?

As the two DFS juggernauts compete for the top spot, we delve into determining whose claim is real

By Mariam Umar

In 2008, a seismic shift occurred in Pakistan’s financial services landscape with the introduction of Branchless Banking (BB). This innovation sparked a digital revolution, reshaping how millions of Pakistanis access and use financial services. By the end of 2023, this transformation had reached new heights, with BB accounts soaring to 114 million—an 18.1% increase from the previous year. Even more striking, active accounts surged by 50.9% to 64.1 million, underscoring the growing adoption of digital financial solutions. At the heart of this digital finance boom are two titans: Telenor Bank’s Easypaisa and Mobilink Bank’s JazzCash. These digital wallets have become household names, each

carving out a significant portion of the market. While JazzCash leverages its vast customer base and market reach, Easypaisa, as a pioneer, boasts an extensive network of agents and merchants. Their rivalry not only fuels innovation but also raises a compelling question: In this rapidly evolving landscape, who truly leads the digital wallet revolution in Pakistan?

Both companies claim market leadership. VEON’s 2023 annual report states, “JazzCash was the largest domestic fintech platform and the most popular mobile fintech application in Pakistan.” Conversely, Telenor Bank’s annual report asserts, “The bank continued to solidify its position as a leading player in Pakistan’s digital financial sector in 2023.”

Given these competing claims, how can we determine which company truly leads the market?

History of Easypaisa and JazzCash

The advent of branchless banking in Pakistan can be traced back to the mid 2000s. We had Tameer Bank (Now rebranded as Telenor Bank) which was suffering from high delinquencies and was looking for a way out. As fate would have it, SBP was also looking to introduce the branchless banking regime in the country.

Sensing the opportunity, the sponsors of Tameer went to Telenor to strike a partnership for the branchless banking operations. Negotiations went back & forth. Finally, Telenor put an offer on the table. and a deal was struck with the SBP to allow Telenor a 51% stake in Tameer Bank, subject to pricing, with an option to buy another 25% stake later. A year later in 2009, Tameer Microfinance Bank and Telenor Pakistan jointly launched Easypaisa, Pakistan’s first branchless banking solution.

A few years later in 2012, Mobilink Microfinance Bank Limited was incorporated in February. The Bank commenced its operations in April 2012 and launched branchless banking services under the brand name “MobiCash” in partnership with Pakistan Mobile Com-

munications Limited (Jazz), in November 2012. This was later renamed to JazzCash.

Performance of wallets

Profit reached to Telenor Bank and Mobilink Microfinance Bank, the companies behind Easypaisa and JazzCash respectively, to find out which metrics can help determine the biggest digital wallet in Pakistan.

Both players stated that a digital wallet’s success depends on user activity, measured by the number of transactions performed by users. Further, the specific measures including those around lending and deposits also indicate who owns the digital financial services space.

Profit looks at these metrics to find out exactly that.

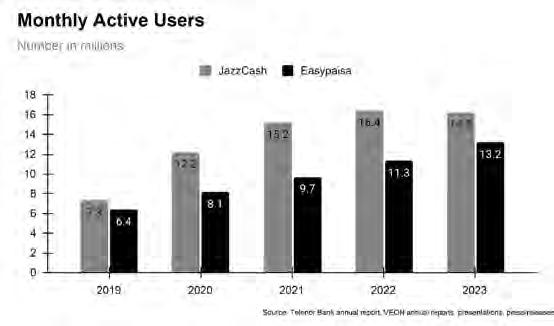

Monthly Active Users

As the name suggests, Monthly Active Users (MAU) is a key metric used to measure the number of unique users who engage with the wallet within a month. A user is classified as transaction active if he performs any debit or

credit transaction regardless of the transaction frequency.

As the chart shows, JazzCash leads in terms of Monthly Active Users (MAUs). Interestingly, the number of MAU for JazzCash dipped slightly in 2023. This can be linked to the rationalization of incentives on initiating transactions.

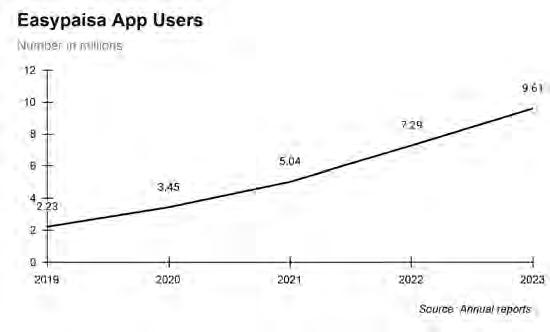

However, it’s important to note that not all of these active users are mobile application users. Both JazzCash and Easypaisa can be accessed through various channels, including the mobile app and USSD, the latter commonly used by branchless agents.

Easypaisa’s mobile application users has grown by around 34% over the past five years from 2.23 million users in 2019 to 9.61 million users in 2023. As per the company’s social media announcement in early March 2024, Easypaisa crossed 10 million active users. In 2023, active app users of JazzCash amounted to 9.3 million, just slightly below Easypaisa. Unfortunately, JazzCash does not release the breakdown of its monthly active users, making it difficult to determine the exact number of active mobile app users and USSD users. However, as per the latest announcement by the company Jazzcash has crossed the 11 million app user mark.

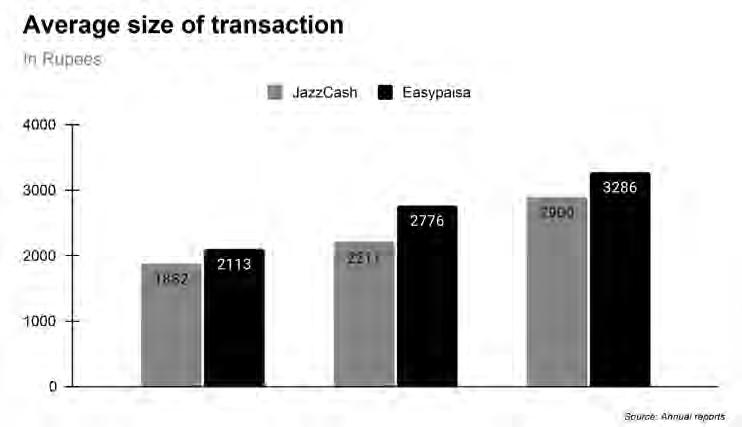

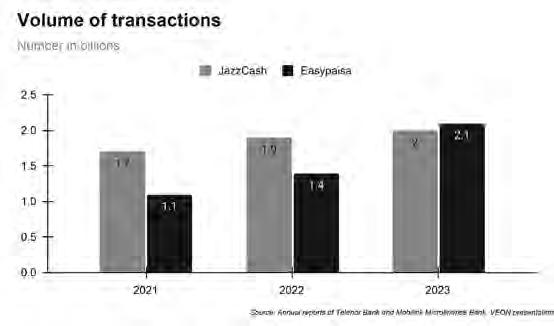

Number and value of transaction

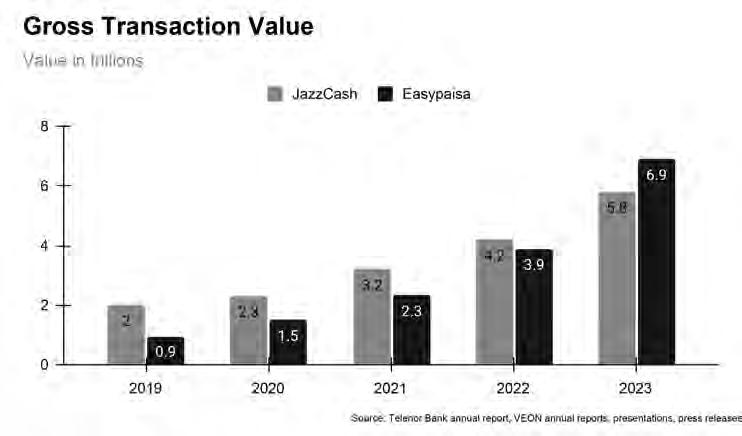

Another metric we will consider is the gross transaction value. Put simply, this represents the total value of transactions processed by a digital wallet in a year. It includes all transactions, regardless of their nature or origin, within a specific timeframe.

Between 2019-2022, JazzCash was leading in this forefront. However, in 2023, Easypaisa took the lead by a whopping Rs 1 trillion.

It is worth noting that this number is usually inflated. Digital wallets like JazzCash and Easypaisa typically give a free top-up in the wallet when a new customer signs up, an amount of around Rs 50 and other incentives. This allows users to initiate transactions, and it encourages user engagement and participation on the platform

When the customers would use this balance for whatever purpose, this would result in a debit transaction and hence will be added to the GTV, inflating the GTV.

However, in gross transaction value, Easypaisa has a legacy lead on OTC in terms of utility bill payments while it also counts

P2P transactions twice unlike Jazz which considers it a single transaction.

In terms of volume, JazzCash had a significant lead over Easypaisa in 2021 and 2022. However, Easypaisa’s transactions surged by 56% in 2023 to 2.1 billion transactions, inching up slightly as compared to JazzCash’s 2 billion transactions.

Digital/nano loans

In recent years, there has been a change in the strategy of both telco-led digital wallets. As per a report by Data Darbar, microfinance banks have been moving towards nano loans. The number of disbursed loans has increased while the amount has increased by a smaller percentage. Between March of 2016 and 2023, the value of disbursed loans to individuals has increased at a compound annual growth rate of 27.1% and the number at 44.2%.

JazzCash was the first one to give into the nano loan obsession. The Nano loans utilise enhanced technology and are applied for digitally, with disbursements made directly to the customer’s digital account, using automated scoring criteria.

In 2023, the JazzCash disbursed 21.7 million loans amounting to 73.3 billion in

2023.

On the other hand, Telenor Microfinance Bank has seen a somewhat bumpy ride. It started nano in 2018. However, as mentioned earlier, the bank had to scrap off its lending book due to fraud in microfinance lending and bullet loans. The bank’s management restructured and introduced nano loans at the end of 2021.

Resultantly, Easypaisa is behind Jazzcash in nano loan with a significant margin.

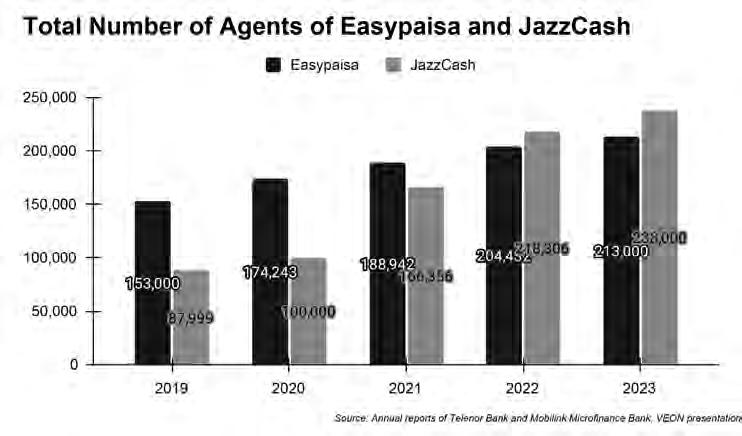

Total Agents

As per SBP, in 2023, the number of branchless banking agents amounted to around 650,000. Easypaisa and JazzCash cumulatively account for around 70% of the total branchless banking agents. The number of agents for Jazzcash stood at 238,000 in 2023 and 213,000 for Easypaisa at the end of the same period.

The Verdict

Determining the biggest digital wallet in Pakistan between JazzCash and Easypaisa isn’t straightforward, as both platforms excel in different metrics. JazzCash leads in Monthly Active Users (MAUs), demonstrating a strong user base and highest mobile app users of 11 million. Easypaisa has also reached over 10 million mobile application users. However, Easypaisa surpassed JazzCash in gross transaction value in 2023.

In terms of loans, JazzCash has led with its early adoption of nano loans, and Easypaisa is also focusing to increase its disbursements. Ultimately, both digital wallets have carved out substantial and unique niches in Pakistan’s fintech landscape. JazzCash’s broad user base and consistent transaction activity highlight its widespread adoption, while Easypaisa’s transaction value underscores its expanding presence. The competition between these two giants continues to drive innovation and growth in Pakistan’s digital financial sector, benefiting millions of users across the country. n

Institutional

reform in the federal government requires a gutting of the bureaucracy, the elimination of thousands of jobs, and strong political will

By Abdullah Niazi

The story goes that during an inspection of the army’s artillery regiment, an officer noticed five men manning a single gun. Curious as to what role each man fulfilled, the officer inquired as to what process they fired. The first man said his job was to load the gun with ammunition. The second said he was the one that set the trajectory of the fire. The third one explained he was to pull the gun into place. The fourth said he had his finger on the trigger at all times, prepared to pull the moment his Captain gave the order. The fifth said he was there to hold the reins of the horse because it would get skittish when the gun would fire.

The only problem was the conversation was taking place long after horses had stopped pulling artillery guns. There was no horse there for the fifth man to hold. The story, whether true or not, has been mythologised as an example of the inefficiencies of big government.

Ronald Reagan, the 40th President of the United States, famously said that government was not the solution, it was the problem. In Regan’s mind, the American government was too big, it spent too much money, and was far too involved in the lives of its citizens.

One wonders whether or not prime minister Shehbaz Sharif felt a hint of Regan in himself last week. For one, the good parliamentarian from NA-132 Kasur has a penchant for theatrics and the performing arts like Regan did, even if he didn’t make a career out of it. But perhaps more relevantly, he claims he is on a mission to reduce the size of his own government. On the 6th of July, the prime minister dispatched a letter to five different ministries asking them to justify their existence, and make suggestions for how they can be cut down to size or even abolished entirely.

The attempt at “rightsizing” as the government is branding it is a good 16 years too late. In Pakistan’s case, the federal government is bloated largely because it has never accepted what its constitutional role is after the 18th amendment. The current plan aims to cut down on the role of different federal ministries, entities, and departments, by either devolving them to the provinces or handing them over to the private sector.

This only scratches the surface. Institutional reforms in the federal government require a major operation that makes changes in the country’s bureaucracy and spending. And this isn’t the first time a government is trying to fix its bloating problem. In fact, an entire blueprint was prepared by the Imran Khan administration for institutional reforms back in 2021 which sheds some light on how this is achievable. The question is, what plans does this government have, how do they measure up to the plans in place, and do they have the political will and strength to execute them?

Rightsizing, not downsizing

The operating term that the federal government is using for their plans is “rightsizing.” That is the correct term to be using because when we talk about reforming different divisions of the federal government, it can either mean more or fewer employees. Take the example of the Federal Board of Revenue (FBR). The FBR works in a manner where citizens and businesses file their taxes by themselves by a process of self-accountability, and tax officers check these returns and conduct raids randomly through balloting since there are far more taxpayers than there are tax officers.

It would make sense that the more tax officers the FBR hires, the more people they can do checks on which will increase the number of people in the tax net. But it would also go without saying that the more tax officers you hire, the larger your salary bill would be. Eventually, a point would come where the salary bill of these officers would surpass the tax revenue they were collecting making the organisation bloated and inefficient.

This, of course, is true for any organisation, not just the government. When it comes to government divisions, the goal is having employees that give you the most productive returns. In Pakistan, there are two main problems with the federal government. The first and most obvious one is the bureaucracy. Federal officers of the state run everything from law and order to local government through the different branches of service. They are the officers that run ministries on the direction of elected officials. By all accounts, there are too many of these bureaucrats drawing salaries

and benefits for jobs that have very little impact. On top of that, the different divisions of government have layer upon layer of bureaucracy within them. Most divisions operate in a five tier bureaucratic system. A secretary will usually be accompanied by a couple of deputies, an additional secretary, and some other kind of secretary, all of whom need to sign off on files.

It is a problem for which serious reform has been suggested as well as attempted. It has failed on multiple occasions. The other problem is Pakistan’s federal government has failed to implement in letter and spirit the 18th amendment to the constitution. Under the 18th amendment, Pakistan is a three tiered democracy where the federation is responsible for defence, the economy, foreign policy, energy, security, and larger concerns that have to do with keeping the federation united and the international community. The provinces have been devolved authority on matters such as health and education, and are ideally supposed to further devolve these powers to local governments which they have entirely failed to do.

But one cannot quite hope for empowered local governments when the federal government has not truly devolved power to the provinces. For example, the federal government still has ministries for health and education. There are reasons for this, such as having drug regulatory authorities and a unified federal board, but these ministries often have functions and departments that have no business existing. It is this latter issue that the government is focusing on.

Sing for your supper

This story centres around a cabinet document. Early last week, a letter was sent out from the Institutional Reform Cell (IRC) of the prime minister’s office to five different ministries. Profit has seen this letter.

In the letter sent to the ministries, the IIRC sent a list of questions for them to answer. They asked for details on how many departments and bodies are within the ministry, what their budgets are, whether or not their function is of a federal nature, and how they can be cut down. At the end of the long questionnaire that details queries for each department, the letter asks the departments

The Cabinet Committee on Implementation that was the precursor for the CCIR held 37 meetings from 23rd July, 2019 to 9th July, 2020. The purpose of this compilation is to Capture institutional memory in a systematic and coherent manner, to have readily available reference material and a guideline for follow up

Dr Ishrat Husain

to give recommendations on whether they should be:

• Shut down entirely

• Retained by the federal government in its current form

• Retained by the federal government after havings its size and expenditure cut

• Handed over to Public-Private partnerships or entirely to the private sector Normally, in a country with an empowered and decisive prime minister, a letter of this nature would have employees of the ministries quaking in their boots. After all, they would be preparing a report that would downsize and possibly devolve their place of work. In Pakistan, the response has been lukewarm. Sources from within one of the ministries sent the dispatch said there were few concerns within different departments. Doubts have already been created by the prime minister’s decision of ignoring the recommendation of two austerity committees, which he himself had formed earlier, and assigning a third one under the chairmanship of finance minister to right-size the federal government, which has now sent the letters out.

The ministries in question include Information Technology, Kashmir Affairs, Ministry of SAFRON, Industries and Production, and Ministry of Health Services. Another ministry that has not been named but is reportedly under consideration for similar review is the education ministry. All of these ministries, their departments, the entities they manage, and their bureaucratic babus are essentially being asked to sing for their supper. And it is worth looking at why these particular ministries might be facing the chopping block.

Combinned, these six ministries (including education) have a PSDP allocation of Rs 309 billion in the federal budget 2024-25. This figure, of course, has to do with different development projects that these ministries are given money for.

But these figures do not quite illustrate just how large the expenditure on these ministries and their associated divisions can be.

PSDP ALLOCATIONS

Rs 74.5 billion

AJK and Kashmir Affairs

Rs 71.4 billion (SAFRON)

Rs 28.9 billion

IT ministry

Rs 4.9 billion

Industries and Production division

Rs 27 billion

Health

These figures do not include the cost of the bureaucrats that run them, nor of the many redundant jobs that can easily be finished, or the departments and entities that no longer serve any viable function other than providing cushy employment to different babus.

The scale of the bloating

To understand this completely, it is important to realise how the federal government is structured. Currently, the government has 33 ministries that help the prime minister run day to day affairs. These ministries often have divisions within them. For example, the finance ministry has the finance division which looks after economic policy, and then there is the revenue division which includes tax collection and the FBR. Similarly, the Energy ministry is divided into the power and petroleum divisions.

These divisions generally contain within them different kinds of bodies. There are executive bodies, constitutional bodies, and autonomous bodies among many

others. Executive departments can be created within the ambit of a ministry for a particular purpose. For example, the health ministry has around seven executive departments including the Pakistan Institute of Medical Sciences (PIMS). These departments function independently but under the control of the ministry. Then come constitutional bodies. These are mandated by the constitution and there are only five divisions (establishment, finance, inter provincial coordination, law, and parliamentary affairs) that have mandated constitutional bodies.

Where the party really gets going are the autonomous bodies that work under these divisions and ministries. When it comes to the major divisions, there are autonomous bodies that make sense since they operate in a very large national interest. For example, OGRA and PTA operate under the cabinet division, or the National Bank of Pakistan (and at one time the SBP) operated under the finance division, while the FBR operates under the revenue division.

But with 33 ministries on the roster, there are plenty of autonomous bodies that serve simply as a grazing ground for bureaucrats and nepo babies. Just take a look at the ministries in question for an idea of how many resources are devoted to them. The Health Ministry, for example, has a dozen autonomous bodies working under it. These include vital ones such as DRAP, to others such as the National Council for Homeopathy and the National Council for Tibb which are drains on logic as well as national resources.

Another example is the education ministry. The education ministry needs to exist on a federal level because students need a combined board, and a Higher Education Commission (HEC) that can convert their degrees so they can apply to different universities. They also need people to run federal government schools that operate all over the country.

All in all the scale of the problem is massive. Overall, the federal government in Pakistan at one point had 42 divisions and 441

attached departments, autonomous bodies, statutory bodies, and corporations.

Imran Khan takes a crack at the problem

As we mentioned earlier, this wasn’t the first time a government has tried to rightsize the government. In fact, when Imran Khan came to power in 2018 he appointed Dr Ishrat Husain as advisor to the PM on Institutional Reform and Austerity with the goal of reforming the federal government.

In the three years Dr Ishrat was around, his team came up with an elaborate plan to do exactly that. They recommended slashing useless jobs, finishing the five tier secretary structure in different departments, and lumping a number of state owned entities into a trust called Sarmaya e Pakistan which would take over the managerial control of all public sector companies.

But the results were horrific. Despite the common sense plan, great resistance was put up by the bureaucracy itself. According to a report in The News, the federal cabinet during the PTI government had approved a major restructuring plan for the federal government and had decided to retain 325 federal government entities out of the total 441. However, despite cabinet’s approval, the plan remained unimplemented because of bureaucracy’s reluctance.

Despite the cabinet having approved the proposals, and sanctioning the execution of the approved restructuring plan, it was never implemented. Dr Ishrat, who had already always said he would only do the job for three years because that is how long it would take, left the PTI government frustrated as his major reform work despite having been approved by the cabinet remained unimplemented because of lack of political will of the then government.

The solution in the drawer

The government’s current plan, it seems, is to start with a few ministries and work their way through all the many departments, bodies, and entities within them. The goal with picking these particular ministries is clear. They are all subjects that should by all rights be in the domain of the provinces entirely. For example, the ministry for AJK and GB only exists because the two areas do not have provincial status and are managed through the federal government. Similarly, the SAFRON ministry makes little sense since FATA and PATA have both been merged with KP and are a part of

We as a country have failed to implement the beautiful 18th amendment. The implementation has been slow and weak

Dr Hafeez Pasha

the province.

Similarly, health is a department that the provinces deal with independently. Already much of this devolution has taken place. The federal government has a health budget of just over Rs 28 billion. In comparison, Punjab alone has a health budget of Rs 539.2 billion. The major functions that the federal health ministry performs are regulatory such as through the existence of PIMS. The provision of health services are and should be a provincial matter.

All of this is just a very small step in what is a Gargantuan task. And already it is clear that the government has not shown the political will to implement it. The prime minister has already ignored the recommendations of two committees he created himself and now created a third one. What is to say that any of this will be implemented? Besides, Shehbaz Sharif is in a difficult position. He is beholden to his wavering allies and the impression that he does not have a mandate will make the bureaucracy even harder to deal with.

In such a situation, the answer can be found in the constitution, and that answer is devolution. Just look at the issue of taxation. Taxation is an issue that is dealt with by the FBR and the revenue division.

The real problem is that Pakistanis are taxed unfairly and those that should be paying the lion’s share end up paying nothing. Just take a look at Pakistan’s tax structure. Tax structure refers to the share of each tax in total tax revenues. The highest share of tax revenues in Pakistan in 2020 was derived from value added taxes / goods and services tax (39.8%). The second-highest share of tax revenues in 2020 was derived from other taxes (33.3%).

In comparison to Pakistan, countries in the Asia-Pacific region only collect about 23% of their taxation from goods and services taxes — meaning Pakistan’s average is almost double. Why is this the case? The biggest reason of course is that taxation in the country is centralised. The FBR collects almost all taxes (even the ones that should be collected

by provinces under the 18th amendment) and then those collections are then given to the provinces in the form of the NFC award leaving the federal government with very little spending money.

In an earlier interview former Finance Minister Dr. Hafiz Pasha, while talking to Profit, lamented that, “We as a country have failed to implement the beautiful 18th amendment. The implementation has been slow and weak.”

Since the share of the provincial governments, under the NFC awards, over the last few years has been increased from 40% to around 57%, it has provided the provinces with very little incentive to develop their own revenue sources. Despite having access to the two biggest cash cows, services and agriculture, the share of provincial tax revenue is close to 1% of the GDP. “You would be surprised to know that the corresponding number for Indian provinces is around 6% of the GDP, with similar fiscal powers,” says Dr. Pasha.

The solution of course is right in front of us: devolution. More than just being a third tier of democracy, having a local bodies system means having a new economic process. In essence, it is not just a new administrative stratification, but also involves the dispensation and spending of money. Things such as education and health that people automatically look towards the provincial government for would now be handled by local representatives. Perhaps most crucially, the ability of local governments to collect taxes and release their own schedule of taxation allows them to make their own money and spend it on themselves rather than waiting for the benevolence of the provincial or federal government. Devolution is the logical solution to shrink the size of the bloated federal government. While reform plans to reduce the size of ministries and reform the bureaucracy are important, simply giving way to a three tiered democracy may just be the silver bullet that a weak government needs to fix its woes. n

The behindstory Pakistan’s biggest ever stock market dividend.

A dividend of Rs 725 per share was given by PHDL soon after its Regent Plaza Hotel was acquired by SIUT

By Zain Naeem

Afew months ago, this publication did a story on Pakistan Hotel Developers Limited (PHDL) and how its share price had seen a meteoric rise. The crux of the previous story

revolved around the fact that the share price of the company went from Rs 83 as on 6th September to Rs 177 by the 20th of September. Seeing the unexplainable rise, the stock exchange inquired if the company had any material information that had not been made public. The company said that it was not aware of any such information. This was disclosed to

the exchange on the 22nd of September.

The share kept increasing in price as the company disclosed that there were parties which were interested in buying its hotel, Regent Plaza, but no firm offer had been received. Then, on 25th of September, the company announced that Sindh Institute of Urology and Transplantation (SIUT) was looking to buy

the hotel and were carrying out the necessary due diligence. After the announcement was made public, the share price kept increasing and settled at around Rs 523. The story concluded by saying that someone had prior knowledge of the talks going on between the company and SIUT and based on this, the shares were being accumulated before this information was made public. A case was made for the regulators to step in and investigate what had happened.

The recent development in this saga has been that the deal has finally gone through and the company has announced a dividend of Rs 725 per share. This is the biggest interim dividend announced by any company in the exchange if not the biggest entitlement ever announced. How has the company been able to give out such a huge dividend, why this has been done and who are the winners and losers of the dividend being given out. Profit tries to pick the bones out of the announcement being made.

Pakistan Hotel Developers Limited

PHDL is a company which is listed on the stock exchange and owns the Regent Plaza Hotel located on Shahrah-e-Faisal, Karachi. It might seem a little bit surprising that a hotel company is listed on the stock exchange. Even the company that owns Pearl Continental and Marriott chain of hotels is listed on the stock exchange under the ticker name Pakistan Services Limited (PSEL). The difference between PSEL and PHDL is that the latter only has one hotel property that it owns and operates.

The recent performance of Regent Plaza has been dismal. From being impacted by the pandemic to a fire that broke out on the premises, the profitability of the company has been severely impacted. The company has only one major asset on its books which accounted for 98.9% of its total assets at June end 2023. The hotel was valued at Rs 10 billion and was the sole asset of any note for the company.

The company had been evaluating the value of the property at regular intervals and an asset which had a value of Rs 2.4 billion in 2010 was worth 4 times that at the end of 2023. Based on accounting standards, companies are allowed to revalue their assets at regular intervals and any gain seen in its value of assets reflects on the health of the company. With an asset worth Rs 10 billion, the company showed a book value of Rs 542 in 2023 which was Rs 125 in 2010.

Even though the value of the asset was rising, the company was still seeing losses in its income statement which was due to the after effects of the pandemic and internal issues at the company itself. Due to the lackluster

performance of the company and a lack of motivation to sell the business, the share price of the company was hovering between Rs 20 and Rs 160 till August of 2023.

The deal being announced

In September 2023, it was announced that the company was interested in selling its only property and it had been approached by SIUT. Even before the announcement was made, the share price of the company started to increase. Once SUIT announced its interest in buying the hotel, the board of directors of PHDL met and decided to share the relevant documentation with SIUT to help in its valuation of the company. On 11th October, it was announced that a bid was received to buy the hotel for Rs 14.5 billion. A hotel which had been valued at Rs 10 billion was being sold for a premium of 45%. Why would that be?

SIUT explained that they were interested in buying the hotel as it had the infrastructure in place that would help them design a hospital around it. The non-profit organization was saying that they saw value in the building that already stood in its place and were willing to pay a higher price for the property. At that time, this was the highest value real estate transaction that was carried out in rupee terms and was going to be executed in due time.

The impact of this sale was going to be massive for PHDL. Based on the recent accounts, the company valued the property at Rs 542 in terms of its book value. Book value is what is left once the assets are used to pay off the liabilities. The book value is the amount the shareholders can expect to get after all the liabilities have been paid off. The deal stipulated that PHDL would end up getting Rs 14.5 billion for the hotel which would bring the book value per share to around Rs 786. There would be an instant increase in book value of 45%.

The market seemed less than enthused about the deal. From October till June, it seemed that the market was not very excited about the deal going through. This was caused by delays in the transaction being executed. Till June 26th 2024, the highest price recorded for the share was Rs 582 in March. Since then, the share is seeing renewed interest and the price reached Rs 606 on 5th of July.

What was the reason behind this renewed interest? That mystery was solved on the 1st of July when the company announced that all regulatory approvals had been received and that 90% of the sales proceeds had been received by the company with the remaining 10% to be received once the title was transferred to SIUT. Once this announcement was made, the share price increased to Rs 606. It seemed like the best was yet to come

when the company finally announced on 8th of July that it was giving out an interim dividend of Rs 725 per share.

In terms of Pakistan’s stock exchange this is nothing short of a seismic shift. No company in its history has declared such a huge dividend. It does seem apropos for the company that after it made the biggest real estate deal in history it would announce the biggest cash dividend in history as well. To put it in perspective, the biggest dividend the company had given in its history was Rs 5 in 2016. This was 145 times the largest dividend the company had given itself.

So why has the company done this and what does it mean for the company going forward?

The significance of the dividend

In order to understand the significance of this dividend, it would serve to consider the balance sheet of the company. In terms of the assets of the company, the company revalued the hotel that it owned and categorized it as an asset held for sale worth Rs. 14.5 billion in March 2024. Based on the total assets of the company, this made up around 89.36% of the assets. The reason for the fall in percentage of assets was due to the fact that the company received 10% of down payment which it was showing as part of cash received and creating a liability for this that had to be paid back.

As the deal with SIUT had been announced and 10% of the payment had been received, the company gave out four dividend payments from September 2023 to February 2024. The total amount of these dividends came to around Rs 11 per share in totality. With the deal close to completion, the company started to take out much of this investment in the form of dividends to its shareholders. With the addition of the recent announcement, the dividend given out in the last year comes to around Rs 736 per share.

So how will the company look like when so much of the funds within the company are distributed to its shareholders?

Once the payment is received by the company, the fixed assets will be transferred to the bank of the company and the company will have to carve out a dividend reserve from the capital or fair value reserve it had. The fair value reserve would stand at Rs 13.9 billion after the deal goes through. From this, the company will pay out the recent dividend which has been announced which will be valued at Rs 13 billion. Once the dividend is paid, the company will have assets worth Rs 1.6 billion left over. It can then use these funds to pay off any liabilities that it has. Once all the assets and liabilities have been converted

into cash, the company will end up with a bank balance of Rs 1.2 billion. On the equity side, the company will have a reserves of Rs 0.9 billion, unappropriated profits of 0.2 billion and equity of 0.1 billion.

When the dividend is paid out, the company will become a shell of its former self. With no assets and liabilities to talk about, the major part of the company will have funds in the bank against the investment made by the owners and the reserves it would still have left standing.

What can be next for the company? At this juncture, the next step can either be to buy new assets with the funds left in the company and start afresh. There would be no sense in the owners injecting new funds into the company when they are taking out dividends. When the dividends are announced, the shareholders lose out as tax is deducted from these dividends. If the company had any other investment opportunities in sight, it would have invested these funds rather than give them out.

Outside investors will have little interest in the company as the company would have no operations or sources of revenues and the most they can expect is interest income from the funds the company has left which will generate almost no revenue for the company. The best course of action would be to slowly keep taking these funds out over time in the form of dividends as the company still has the capacity to pay out dividends of Rs 55 going forward.

Another option could be that the company keeps these funds invested in a bank and earn interest on these funds. At the end of 2023, the company made a profit of Rs 44 million on assets worth around Rs 10 billion. If the company keeps the remaining balance of Rs 1.2 billion in an account, they can end up earning Rs 240 million and then distribute this to its investors who have bought the shares. It would be ironic that the company would increase its profits by 6 times after closing its core operations and business.

The future listing of the company will come into jeopardy and a voluntary buyback or delisting would seem likely in order to take the company off the stock exchange. With 88.63% of the company already in the hands of the directors and their relatives, the company can also look to pass the 90% threshold it requires to carry out a successful buyback and delisting of the company from the exchange. The situation will become clearer once the fresh shareholding is released at the end of June 2024. With shares trading in the market since June, it can be assumed that the company has gotten closer to the magic number of 90% since last year.

The company will slowly wither away as the core of the business is not left standing

anymore. So who are the winners and losers of this transaction?

Winners and losers

The biggest winner from this transaction seems to be the company itself. When SIUT came calling, the company already had an asset it was willing to sell and it was able to sell its core asset for a value that even it did not anticipate. Over time, the hotel had increased in value and even in those circumstances, SIUT placed a price tag much higher than the expectation of the company and its own valuation. The management of the company was able to offload its assets at a handsome profit and with the hospitality business suffering in recent years, this seems like a perfect scenario for the company going forward.

Another winner of this transaction could be SIUT which will be able to buy a hotel and turn it into a hospital. Even though it might seem like they are paying too much, the fact that the hotel infrastructure can be easily turned into a hospital seems to be a win for the non-profit organization. SIUT saw some strategic advantage in buying a pre-build structure which it could utilize rather than building something from scratch which would save time and resources of the company itself. It seems like SIUT also gained from this transaction and deal.

The patients who will benefit from the expansion of SIUT also seem to be the winners as they will get access to a better facility. As SIUT will expand, more and more patients can be treated and the benefit can reach a wider set of patients compared to before. It seems like this is one more party that will be better off after the deal has gone through.

The government will also benefit from the deal. There is a withholding tax of 15% that is placed on dividends. The company has given out a total of Rs 736 per share which can be linked to this deal. When the dividend is paid out, the government will end up earning Rs 110.4 per share. The rate is doubled if the dividend is earned by a non-filer and the withholding tax increases to 30%. Based on the dividends planned to be given out, the government will earn Rs 2 billion from the transaction alone. Meaning a considerable chunk of the Rs 14.5 billion will go into the coffers of the government from the dividend alone. PHDL is mandated to pay Rs 237 million by itself for the sale of assets that is carried out which will also be deposited into the exchequer.

The last beneficiary of this deal will be the shareholders of PHDL. Based on the shareholding of June 2023, 88.63% of the shares of the company were held by its directors or relatives of the directors. These individuals

would be the ones who would benefit from the dividend as they will end up making Rs. 11.7 billion amongst themselves from just the dividends that have been announced till now. At the end of June, 10.98% of the shares were held by minority shareholders but based on the volume that has been traded from June 2023 to July of 2024, it can be safely assumed that the directors and their relatives would have increased their shareholding accordingly. Latest shareholding once released for June 2024 will provide better guidance in these regards once the accounts are released.

At this point in time, there can only be one loser in the situation and that would be the fresh investor looking to invest in the company. The announcement of such a large dividend has many people take notice of the company and look to invest in it. With little to no basic understanding of the company and its operations, many investors will look to buy the shares at the time when these shares would cause more harm than good. Once the dividend was announced, the company’s share price shot up from Rs 607 and in two days of trading, it hit a high of Rs 728.

The company was going to be selling its core assets and once the dividend would be paid out, the company would end up nothing more than a shell of its former self. With money being taken out, nothing would remain in the company which can be seen as being investable. Investors would care little about that. With herd mentality and a lack of understanding they would be looking to buy the share. Even for investors who bought the share for Rs 727, the reality is that they paid too much. Let’s say the share price closes at Rs 727 on 15th July. Based on the record of the company, whoever owns the shares on the 15th will get the dividend announced by the company.

Once the dividend is given out, the share price of the company falls in value by the amount equivalent to the dividend. In this case, the share price would go from Rs 727 to Rs 2. The investors would lose out as they bought a share for Rs 727 and got a dividend of only Rs 616 per share as withholding tax is deducted from the dividend. Now they would have Rs 616 in their account in the form of dividend and a share which will start trading at Rs 2 from the next day of trading. The investor actually lost Rs 110 per share of his investment due to the taxation. WIth lack of basic understanding, they would lose out Rs 110 when they bought the shares at a price close to the amount of dividend announced.

In a deal which was seen to be historic as the largest real estate deal, it seems there are mostly winners who would reap the benefits of the transaction taking place, however, the losers would be the investors who always end up holding the short end of the stick in the end. n

Textile exporters denied tax relief; who to blame?

After years of protection to make the industry internationally competitive, govt has removed the cover from above textile exporters. Who will this affect the most?

By Shahnawaz Ali

Hardly anyone is happy with the latest federal budget.

Salaried class, factory owners, real estate developers, all have showcased their disappointment over the government’s lack of vision and exploitative policies. But one sector that is particularly unhappy, contrary to the status quo, is the textile exporters.

Over the years, due to a recurring balance of payments crisis, Pakistan has done its best to facilitate exporters. Not only have they been given tax breaks but major subsidies have been redirected their way to make them competitive in the international market. This year however, the government had to decide between cutting the exporters’ leisure or cutting their own and they decided to go with the former in the latest budget.

The government has taken away the exporter’s leisure of not giving tax on profits and imposed a tax rate of 29% on their profits. Meanwhile the previously applicable 1% tax on revenue has not been fully abolished but rather revised such that companies that do not make a profit will still have to pay it.

The decision has been heavily criticized by not only the industry itself but the larger business community including the sectors that have, over the years made a case for taxing the textile sector. So what is so bad about this new tax regime?

Textile Taxes over the years

Over the last two decades, the textile industry in Pakistan has seen a host of protections. It is perhaps these relaxations that have set an unfair number of expectations in the minds of the industry stakeholders.

Pakistan is a country that is often short on foreign reserves. On other occasions, the country always faces a direct balance of payments crisis, that it usually has to offset with the help of foreign aid. Any industry that hence provides any breathing room in terms of forex should be encouraged by default. Since 2005, textile, especially export oriented textile has

been that particular industry.

The industry has always had exemptions and concessions for export oriented textile mills, but in 2010, the minimum tax on turnover was introduced for these mills. This rate was fixed at 1%.

Several subsidies on utilities by the government, duty drawbacks, sales tax exemptions and export refinance scheme by the state bank, provided an umbrella for the industry over this period, failing to capture a sizable market share in global textile.

This was up until 2023, when a super tax was imposed on the industry after the country fell short on tax revenue. What came about as a 1 time measure, lingered making the industry only slightly in the global market.

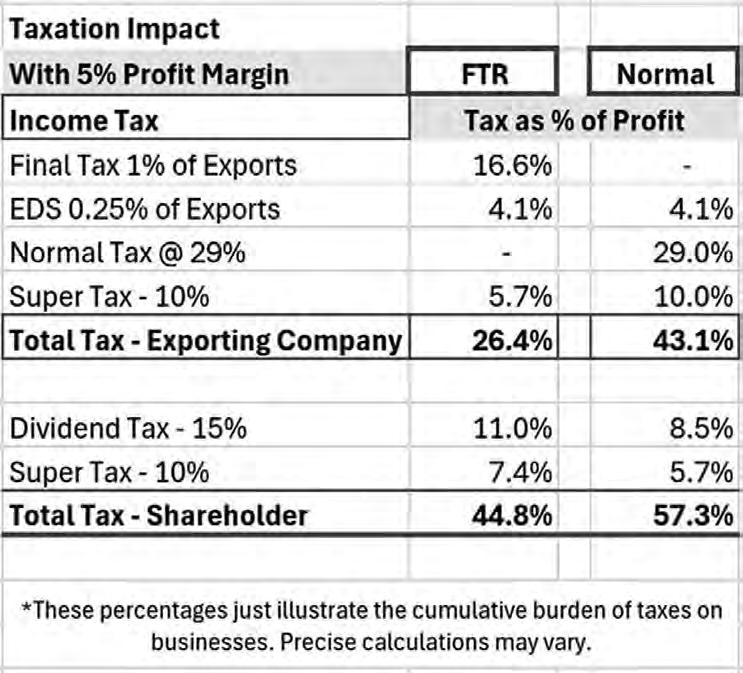

However the recent introduction of the 29% income tax rate on profit, puts the active tax rate well over 50% of the textile company’s profit margin, making it significantly non competitive in the global market.

More importantly, the government has now shifted from the previous Final Tax Regime (FTR) to a Normal Tax Regime (NTR) for the exporter. Previously, the exporters only paid 1% on turnover and under certain circumstances, a 0.25 on Export Development Fund/ Scheme (EDS).

Under this new regime, the exporters will also pay 0.25 % Export Development Fund (EDS) and this cost increase cannot be transferred to foreign buyers. Moreover, they will pay either of the two taxes, a 1% tax on turnover and 29% income tax on profits, depending upon their profits. In essence, the FTR hasn’t been abolished, it has been reimposed on top of the NTR.

The philosophy of being taxed

It is important to note that a company is expected to be taxed more than an individual. Similarly, bigger businesses intuitively pay more taxes than smaller companies due to their sheer size and profitability potential.

Imagine a company as a large farm and an individual as a small garden. The farm (corporation) has more resources and generates more produce (profits) compared to the garden (individual income). Since the farm uses more

public resources like roads for transportation and infrastructure for business, it’s fair for the farm to contribute more to their upkeep. This ensures the farm pays its share for the benefits it enjoys and supports the community.

Setting tax rates also involves balancing. If the farm’s taxes are too high, the owner might plant fewer crops (invest less), affecting the overall harvest and economic growth of his region. If too low, the neighborhood might not collect enough to maintain shared facilities. So, governments set corporate tax rates to encourage businesses to invest while ensuring they contribute adequately to the community’s needs.

Another thing that sets corporate taxes apart from individual taxes is that they represent the residual after expenses, meaning corporations have a better ability to pay. Individuals are taxed on their income, which often includes necessary living expenses, so their rates should generally be lower to avoid excessive burden.

But what if a company makes a loss? Typically, companies that make losses do not pay income tax in Pakistan. But the minimum turnover tax does not make that exception. Companies in the textile sector that have been making losses over the last few years, have been subject to paying an additional cost in terms of turnover tax.

Over the years, the textile industry has been an exception to these rules of corporate taxes. Minimum turnover tax meant that a company that had a profit margin of close to 10% would pay less than 10% in taxes. However this year the government has decided to correct that.

Not only did it not remove the minimum turnover tax, it also added a normal income tax at 29%. Any company had to pay at least the 1% turnover tax and at most the 29%+10% tax along with other withholding taxes, taking the rate to above 40%..

The real effect

4

0% is just the nominal effect. The real impact of this newest taxation regime is much higher. According to data shared by the Pakistan Business Council, the effective tax rate on the textile exporter will cross 43% of the profit, if their profit mar-

gin is 5%. Translate this onto the shareholder with the increased capital gains taxes, the effect crosses more than 57%.

The council makes the case that this will discourage not only the foreign investor but also force the local industrialist to close up shop from Pakistan and set it up somewhere else.

Increasing taxes on exports is a tricky exercise because when the tax on any industry is normally increased, they translate that into an increase in prices. The burden is passed on to the consumer and the industry takes only a small hit in demand. In export it is an entirely different game. Export-oriented companies compete with other companies from around the world.

Their products are supposed to be of a better quality and are hence not as well received in the local market. To make it big in the international market they have to be good but also competitive, i.e, cheap enough for the international buyer to prefer them over the others.

Pakistan’s competition currently is countries like Bangladesh, India, Vietnam and China etc. Despite giving special tax breaks to textile, it was nowhere near the competition even in the past. The Pakistani industry is using electricity almost two times as expensive as some of these countries, and have to pay a super tax on top of the regular tax.

According to State Bank of Pakistan’s (SBP) data in FY23, textiles accounted for around 60% of Pakistan’s exports, and in FY24 between July to May, they accounted for around 53% of the country’s entire tax portfolio. This was after

Who is behind the change?

So if leveling the taxes for the textile industry brings about so many complications, who came up with this idea? This is where it gets interesting. According to credible sources, the idea was given to the finance division by none other than All Pakistan Textile Mill Association (APTMA) itself.

But why would APTMA shoot itself in the foot? To answer this we first have to understand the types of textile mills. APTMA is a body that represents all textile mills. This includes spinners, weavers, and garment manufacturers etc). While the spinners are not a high value added producer and exporter in the industry, they are a large share of it. The others often have similar concerns and benefits and hence can be clumped together as non-spinners. Oftentimes the policy requirements of spinners and non-spinners has not been historically aligned. Now APTMA not only represents the best foot forward of all kinds of textile producers, it also mediates differences between them.

To understand just how important APT-

MA is, it is important to note that Gohar Ejaz, former commerce minister, was previously the chairman of APTMA, which some believe led to his political prominence.

Disputes within different kinds of textile millers have been common at APTMA, be it disputes on subsidies and tariffs or be it controversies on export of yarn. In 2011, a serious dispute over the export of cotton yarn was observed between spinners and non-spinners. Local spinners started exporting large quantities of yarn due to high international demand, leaving little for the domestic weavers and garment manufacturers. This eventually led to an export quota being set up by the government. It was believed that the decision was heavily influenced by lobbying from non-spinning sectors within APTMA.

Now ever since the rupee has become expensive in FY22, the value added sector has been making the bulk of the bank. As an example, in FY23 Interloop, a leading export-oriented textile company made a 17% after tax profit and saw a 63% growth in its profits. While the entire industry got to pay the 1% tax, the value added sector got the bulk of the benefit.

To compare, a spinning giant, Nishat Chunian, made a loss in the same year close to 1% of its revenue. And one of the things that the company would have really benefited from is the abolishment of the tax on turnover. It is believed that due to this disadvantageous market position, the spinners were the ones at the

forefront of the abolishment of the tax on turnover and reenactment of a normal corporate tax regime. The logic is that if a company makes a loss under that, they do not have to pay income tax and can also offset their tax expenses for the upcoming years.

It sounds like a perfect goal to lobby towards especially for loss making spinners. However a government which is severely short on cash did the exact thing that both factions did not want for themselves. An all encompassing tax that would hit turnover, if you made a loss and profits if you make a profit. On top of a flat 10% in the form of a super tax.

This put all the lobbyists and the interests they represented at a disadvantage.

What will happen now?

While this suppresses business and reduces exports, one serious concern that the government faces is the withdrawal of investment, such is the nature of industrial policy based on a free-market economy. So the government really needed to do something, and so it did.

The commerce ministry has formed a committee to address and accommodate the concern of the exporters. Will this committee and its findings amount to anything? No one can guarantee. n

Can Artificial Intelligence make college counselling more equitable?

Kollegio is building an AI driven platform to assist

candidates with their college applications

By Nisma Riaz

It is no secret that the label of a foreign degree counts for much in Pakistan. It doesn’t even have to be Harvard or Oxbridge. It could be a community college tucked in a cranny of a small state in the US, and a Pakistani parent would still proudly boast about their child getting a degree overseas.

Approximately 10,000 students from Pakistan go to the United States each year, often with the assistance of expensive college admissions counsellors. These counsellors can charge hundreds of thousands, sometimes even millions of rupees, making them affordable only to a small segment of society, which is an issue prevalent not only in Pakistan, but globally.

This situation restricts access to education, as those who can afford such costly counsellors are not necessarily the most deserving of scholarships compared to others but end up getting these scholarships. It’s not that they aren’t deserving at all, but it creates an inequitable system, where those lacking the social capital miss out on important guidance and assistance that would improve their chances of attending prestigious global universities. Consequently, the majority of Pakistanis find these services inaccessible and the class divide

between those who can and cannot afford fancy college counsellors, and later attend worldclass universities, becomes more palpable.

But can AI disrupt this sector and make access to counselling services more equitable?

Well, we don’t have the answer yet, but there is one company that is on a mission to revolutionise this sector.

Kollegio has created an app that uses AI to perform 90% of the tasks a college counsellor would perform, but better than a college counsellor would perform. Or so they claim.

In 2019, Profit reported on the much lucrative college counselling business that Dignosco runs. Let’s re-hatch this topic from a new AI-integrated lens and see how Kollegio’s AI-drive model can help address gaps in the traditional college counselling process.

What does the world of academic counselling currently look like?

Education consultancy businesses operate by advising students on securing admissions to both partner and non-partner universities. Under the partnership model, counsellors act as agents for their partner universities, earning a

promising

commission based on the number of students they send to these institutions.

Non-partner universities are top-tier institutions like Stanford, UC Berkeley, Ivy League schools in the US, and Oxford or Cambridge in the UK. These universities do not need partners due to their high global demand and competitive admissions process. Counsellors help students build strong applications for these universities and charge applicants heavily for their services.

“Different universities appoint agents worldwide to help with international student recruitment. This practice started in the UK and has spread to colleges in Canada, Australia, Turkey, Malaysia, and the US. Typically, the agent receives a commission based on the number of students they send to a university,” Abrar Rahman, founder of Dignosco told Profit in a 2019 interview.

Foreign universities appoint partners to attract international students, who bring in talent and stimulate the economy with their tuition and living expenses. Some countries promote agency models in developing countries to recruit these students.

According to International Consultants for Education and Fairs (ICEF), Pakistan sent nearly 40,000 students abroad for higher education in 2013, and the number has grown to about 50,000 or more annually. Assuming

each student spends an average of $30,000 per year, Pakistani students spend a conservative estimate of $1.2 billion on foreign education annually, benefiting developed economies due to the perceived inadequacy of local universities.

Dignosco, one of the most coveted education consultancies, does not handle local admissions but provides guidance on local universities to students also applying abroad. “We don’t deal with students targeting only local universities. Those applying abroad often apply locally as a backup,” Rahman highlighted.

Dignosco, previously only focusing on the non-partner segment, entered the partnership model around five years ago. While Dignosco has established a reputable business, other firms in the industry operate unregistered and may scam students with promises of foreign admission.

However, Dignosco addresses this concern by claiming to be ‘need blind’. This means that if a candidate has outstanding academic records but also has financial resources, they must still pay the full amount. However, if a candidate has similar grades but lacks the financial means, they would be subsidised by those who can afford to pay. The fee structure of Dignosco looks something like this– an aspiring applicant who walks in through the doors of Dignosco pays an initial consulting fee of Rs 5000 per session. For those who decide to register with Dignosco, depending on the span of services they need, pay between Rs 50,000 to 1.5 million.

There is discomfort around operations of Dignosco and its counterparts, possibly due to the realisation that wealthier students have easier access to these services because they can pay consultancies not only for assistance but also for completing their entire application, including writing their essays. This puts students lacking resources to pay hefty amounts to counsellors at a disadvantage, limiting their access to some of the best schools around the

world.

Despite concerns about fairness, college counselling has become a profitable business, creating demand and competition.

Can AI be a better academic counsellor than trained professionals?

Founder of Kollegio, Senan Khawaja answers this question, “Yes, that’s exactly what we’re focused on building at Kollegio right now.”

“Essentially, we leverage my three years of experience in the college counselling industry, where I’ve personally assisted over 100 students through my own small company. Additionally, I’ve collaborated with other former admissions officers and prominent firms to gather a wealth of knowledge. We’ve consolidated all this expertise into a completely AI-driven platform. This platform performs 90% of the tasks of a traditional college counsellor but at a significantly reduced cost.”

Let’s have a look at how Khawaja conceived the idea of building an AI platform that would allow aspiring students to access academic counselling services at the tip of their fingers and without spending a single penny.

Khawaja told Profit, “Having worked in the industry for years, I encountered a recurring challenge: many incredibly bright, hardworking students lacked access to resources available to those who could afford costly counselling services—often priced at 5 to ten lakh rupees or more. This disparity troubled me deeply about the industry as a whole.”

He acknowledged that counsellors’ time is valuable, as well, considering it is their bread and butter, but that does not justify the unequal opportunities that wealthy versus non-wealthy students get.

Naeem, a graduate of UC Berkeley, embarked on developing this platform. The company secured a pre-seed round totaling $750,000 with leading investors, like Tuesday Capital, known for backing giants like Uber and Airbnb. Additionally, Reach Capital, a renowned EdTech investor with stakes in educational platforms like Duolingo, Quizlet, and Desmos, also joined the round. Lastly, Aatif Awan from Indus Valley Capital, along with other angel investors were a part of Kollegio’s pre-seed funding round.

Khawaja disclosed that, “Within months, we launched it to over 3000 users, with our user base growing daily by hundreds. Our aim by year-end is to surpass 50,000 users.”

“When the generative AI boom emerged in late 2022, I saw an opportunity to merge these two worlds— generative AI and college admissions counselling—to significantly reduce costs and enhance accessibility, addressing a fundamental market issue.”

Khawaja, teaming up with his co-founder and CTO Saeed

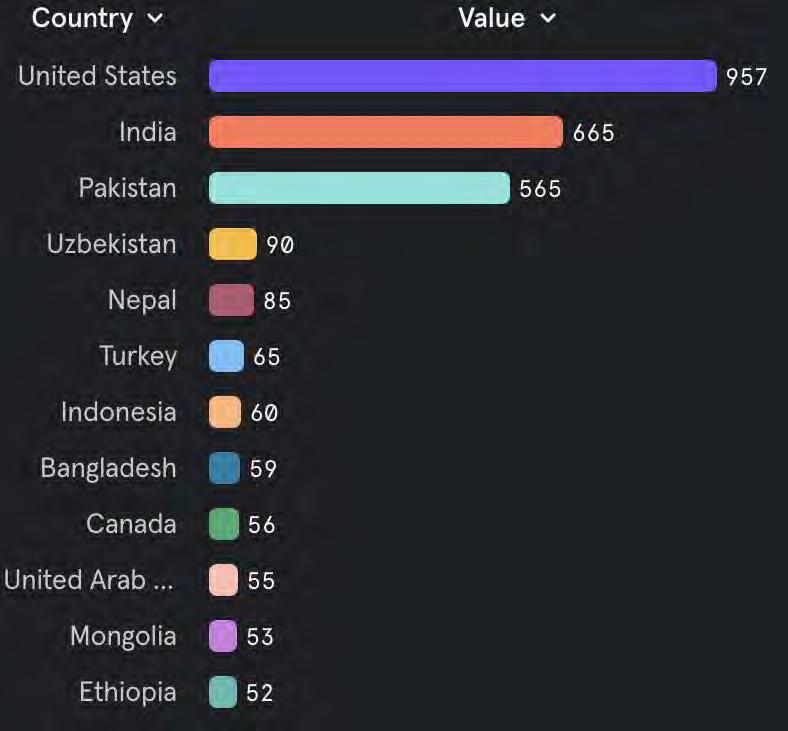

The app is available in 125 countries and over 40 states. The top three countries where Kollegio is currently popular are the US, followed by India, with Pakistan at number three. Uzbekistan, Nepal, Turkey, Indonesia, and several other nations also feature prominently.

The company is also in works to initiate a $500,000 seed round early next year.

As promising as this entire scheme sounds, you may be wondering how exactly it works. And whether it is actually completely free of cost?

Khawaja explains, “Kollegio operates as a completely free product. Our current priority is not monetization but rather fostering user growth and enhancing the product’s quality. We intend to keep Kollegio entirely free for the coming year, focusing solely on expanding our user base. While considering future strategies, such as potential monetization, it remains secondary to our current objective of providing

a high-quality, no-cost service.” The pre-seed VC funding rollout is currently enabling the company to offer their services for free.

When we raised eyebrows at the costfree service, Khawaja defended, “Our current focus is solely on growth as we’re in the startup’s growth stage. Our strategy revolves around achieving a milestone of 1 million students on the platform first, before exploring monetization strategies. Similar to Uber, which prioritised growth over profitability for several years, our approach resonates well with investors who prioritise scaling.”

How will Kollegio’s AI replace college counsellors?

Khawaja says that Kollegio is not out to replace college counsellors, however AI surely can take over several tasks performed by these individuals and do the job much more efficiently.

According to Khawaja, in a broader academic context, AI excels in aiding educators today.

“The software I’m developing not only supports independent consultants but also enhances the capabilities of teachers. AI thrives in roles that are supportive and involve repetitive tasks. What sets our software apart is its ability to perform 90% of the tasks of a traditional college admission counsellor—and in some cases, even outperform them,” he informed proudly.

He says that by analysing thousands of data points, Kollegio’s AI tool generates innovative ideas and solutions. He believes that AI has the potential to revolutionise the job market, particularly in replacing entry-level white-collar positions. “However, my aim is not to displace individuals working as college admissions counsellors, especially those serving affluent families who can afford their services. For the vast majority, 99%, of the global population, including Pakistan, who lack financial means, our platform seeks to level the playing field. We’re dedicated to making higher education accessible and equitable, regardless of economic background.”

Kollegio’s counselling tool is developed

with guidance from an esteemed ex-Yale admissions officer, therefore designed to be worldclass and accessible to all, free of charge. Whether users hail from wealthy families or remote rural areas, with limited resources, Khawaja says, their goal is universal education access. “This disruptive approach intends to reshape the higher education landscape, empowering schools with a broader pool of qualified applicants. We anticipate this shift will prompt institutions to rethink their admissions criteria, fostering collaboration to build a fairer system.”

Coming onto our next big concern, we asked Khawaja whether his AI is capable of tailoring the application process to every individual student’s personalised needs, considering that every applicant has a unique journey?

Profit was assured that AI excels surprisingly well in this regard.

“Imagine I’m your counsellor and I ask about your hobbies, challenges, and various aspects of your life. While human counsellors can manage about 20 students, AI has the capacity to remember every detail you share—a capability that might seem daunting but ensures personalised assistance,” Khawaja explained.

For instance, when crafting an essay for Princeton, AI can remember what skill you had fed into the system and suggest highlighting your role as captain of the rowing team, knowing Princeton values leadership. Meanwhile, college counsellors may not always be able to keep track of every skill of yours.

“This level of personalised feedback surpasses what a human counsellor can provide due to AI’s superior recall and access to extensive data points. Unlike humans who rely on imperfect memory and intuition, AI operates with a robust dataset, offering insights and guidance that are more comprehensive and tailored.”

so, in essence, AI can effectively handle 90% of tasks typically performed by human counsellors, and in many cases, it excels beyond human capabilities. Its ability to retain and analyse vast amounts of information ensures that each student receives personalised support that enhances their application strategies and overall success in the college admissions process.

But what is Kollegio’s solution for the remaining 10% of a counsellor’s tasks that their AI cannot currently do?

“At present, our product operates entirely on AI and data-driven principles, devoid of any human intervention. However, as we strive to maintain a free service, scaling up to accommodate our growing user base, which is projected to reach 50,000 by year-end. This sort of growth necessitates keeping costs minimal.” Khawaja elucidated, highlighting that introducing human involvement would inevitably lead to expenses that could translate into user charges.

However, the Kollegio team does include some employees, who fill in these gaps.

Khawaja said, “To enhance our AI’s capabilities, we’ve recently onboarded an ex-Yale admissions officer and a highly accomplished team member, who secured admissions to all eight Ivy League universities, plus MIT and Stanford.”

These experts are playing a crucial role in training Kollegio’s AI, to improve its capabilities from 90% proficiency toward 91%, 92%, and beyond, according to Khawaja.

While AI remains indispensable for its efficiency, it’s important to acknowledge its limitations compared to human intuition and adaptability. So, Kollegio’s realistic goal at the moment is to approach that level of human insight as closely as possible.

Deciding whether AI is a better academic counsellor than humans is beyond the scope of this article, however, based on early feedback Kollegio has received after less than a year of making its services available, around 95% of users claim to find this tool beneficial. “This positive sentiment is reflected in the satisfaction of returning students,” says Khawaja. n