08 The govt is finally trying to fix Pakistan’s increasingly worrying pension problem. Is it too little too late?

12 Privatising DISCOs is agenda item number one. Maybe it shouldn’t be

18 DISCOS – Is there a way out of the existential quagmire? Asif Saad

21 The budget has quashed any rumors about high taxes on stock market earnings. What does the ensuing rally mean for the year to come?

23 The govt is punishing filers and non-filers alike. The only difference is the latter might manage to escape

25 Changes to look out for in the banking sector for the next fiscal year

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

The

govt is

finally trying to fix Pakistan’s increasingly worrying

pension

problem.

it too

The federal pension bill exceeds Rs 1 trillion mark. What are the reforms being implemented, and are the measures strong enough given how bad things have gotten?

By Shahnawaz AliAmassive federal budget worth Rs 18.88 trillion was presented in the national assembly by the finance minister on the 12th of June. While there are many features of this proposed

budget that have raised eyebrows, one thing that has been the subject of public debate for the last six months is the pension bill.

Over the last five years, the federal pension bill has ballooned by almost four times and has become a growing concern for the lawmakers. However not much has been done to alleviate the national exchequer of this

high cost. The estimated amount proposed in the federal budget for FY25 is Rs 1.014 trillion, marking a 26% increase from the previous year’s budget.

Over the last six months, the government has been touting a series of reforms that will presumably take place to alleviate the pension burden. A similar stance was taken by the

The new budget has announced pension reforms but they should have mentioned how this started off in KP, and it would have helped had they followed our model. The next step was putting new employees on a contributory pension scheme. But these employees won’t be getting pensions for 40 years. What of all the employees today? Their pension is still fixed

Taimur Jhagra, former finance minister of KP

finance minister Muhammad Aurangzeb in his budget speech. He mentioned a three-pronged strategy in line with the international best practices; however, both the speech and the annual budget statement was devoid of the details on this strategy.

In the same breath, the finance minister also announced a 15% flat increase in the pensions of government employees. While this is merely a corrective measure to catch up with inflation, no difference in increase between lower and higher grade retired officers was announced. Nominally, this increase alone, adds Rs 122 billion or more than 12% to the pension bill.

To contextualise this, we first have to look at the problems that plagues the revenue account in the form of pensions.

The new proposals presented by the Finance Minister hint towards a three pronged approach in order to address this issue. One of the biggest expenses that the government gives out on an yearly basis is the pension funds to its ex-employees. The pension system of the country is broken to be frank. As an employee of a private organization, a worker will see his salary after a part of it has been deducted in the form of provident fund contribution. This is known as a contributed fund where the employee contributes himself into the pension fund.

The company can look to match his contribution but the key fact is that these are funded pension funds which have something coming into them. The way the pension system is designed in Pakistan’s public sector, most of the pensions are unfunded. Meaning for all the government employees from Grade 1 to 22, none of the employees see any of their pay deducted when they get their salaries. So how does the system get funded?

It is the government which ends up paying the whole pension. Consider an employee workforce of 1,000 people. Once these

people retire, the government has to pay for the pension of all of these employees the next year. The next year, as more employees retire, the expenses increase and this cycle keeps on going. Once cost of living adjustment and increments are added of roughly 15% per year, the cost balloons out of control.

There is also a complication that the pension system is not monitored and designed in such a way that once the deserving person passes away, his wife becomes entitled to this pension. Once the wife passes away, the daughter or son becomes entitled and the pension expenses keep getting inflated. This is an unlimited burden on the exchequer and has the potential to snowball out of control.

The government has come up with three parts of the solution. The first part is to follow international best practices and to reform the system which is expected to restrict the pension liabilities in the coming decades. The exact specifics have not been given but it seems that some of the controls of this scheme will be tightened to address this. The second part of the scheme would be to have a contributory pension scheme for the new employees. As these employees are part of the new system, they will contribute into the scheme which will make this scheme fully funded. This will bring the practise inline with the private sector practises and will cost less to the government. Lastly, a pension fund will be created which will look to address the liability of the company.

The idea seems solid at this stage and will cut down much of the burden which is currently on the government solely. The scheme will try to bring it in line with the public sector that exists and will look to reduce wastage and slack that has been built into the system. Lastly, having a pension fund would mean that these contributions can be invested. A conservative fund can park these in a bank account to earn a steady return while some of these funds can be diverted to the mutual fund industry which will benefit the capital markets as well. The return earned on these funds will also compliment the pension fund without being costly for the government.

To get to its root we go back to 2009, when the government, for the first time included future retirees in the receivers of the increment awarded in 2009. In the following years, the same act was repeated more than 6 times. This means that any increment in these 6 terms was to be added to the pensions of not only the previously retired officers, but also the officers that were to retire after it.

The step compounds increments for retirees, leaving service after 2020 for up to 6 times even before any of the latest increment is added to their basic pension. This causes the pension figures to balloon to the levels that they are currently at. It is important to note that even if the government does not make future retirees a party to the current increments, the 6 increments in the past can not be undone in a budget document.

However that is just the tip of the iceberg, there is precedent of such policies being enacted in various parts of the world but in most of these cases, the pension of retirees is funded by a pool of money, contributed by either both the employee and the government, or in some cases just the government, over the years of the employee’s service. Basically a pension fund.

Pakistan on the other hand follows a version of the defined benefits in pensions that demands the disbursement directly through the revenue account. Most of the developed world works on either a defined contribution model or a funded defined benefit. From this explanation it seems that the only way in which Pakistan can reduce its pension expense is by travelling back in time by at least 20 years. However, all is still not lost. The country can still offset some of its pension liability by funding it through a pension fund that incrementally increases in size.

Last year, the federal government announced the setting up of such a fund by setting aside Rs 10 billion. As the year progressed, Pakistan could not follow up on its overly optimistic budget, resulting in the slashing of

the fund amount by Rs 5 billion. Even with the remaining Rs 5 billion, the setting up of a fund remained a topic of ambiguity amongst other bigger concerns. The government has pledged to add another Rs 10 billion to that fund in the FY25 budget.

It is important to note that to make a sizable dent in the pension bill, even in the short-term, Pakistan needs not 10, not 100 but at least a Rs 1,000 billion fund, an amount that no politically sane government can afford even half of.

With the current pension bill at almost 6% of the estimated total revenue and 8% of the estimated tax revenue, the government might just have to revise the funding sources of this revenue account expenditure.

Not to mention that with a flat 15% increment, the pension for 17-22 grade officers would increase at a much higher rate. Not to mention the compounded effect of these increments takes the pensions of some of the retired officers to an obscenely high level.

As Pakistan was approaching the announcement of its FY25 budget, the escalating pension liability was a critical issue for the nation’s fiscal health. The finance ministry had already shared a comprehensive pension reform program with the International Monetary Fund (IMF) to curb the burgeoning pension expenditure, since the consolidated federal and provincial pension spending was projected to increase by over 20%, from Rs1.252 trillion last year to Rs 1.5 trillion plus this year.

Keeping that in mind several reform points were raised which are as follows.

Firstly, future increases would be based on either gross or net values at retirement time, indexed to the Consumer Price Index (80% of the CPI over the past three years), capped at a 10% annual increase.

Secondly, while government employees could currently retire early with full benefits, this would be discouraged in the future, with penalties ranging from 3% to 10% imposed on early retirees.

Third, pensions would be determined by averaging the salaries of the past 36 months, resulting in a lower pension amount. Fourth, the current commutation/pension ratio of 35:65% would change to 25:75%. This means that the lump sum amount taken at the time of retirement would be increased, relieving the government from a long term financial liability Fifth, the option to restore full pension after a certain number of years will be discontinued.

Sixth, the current defined benefit model, fully funded by the government, will transition to a pension fund model, as planned by the previous government.

Another few significant changes included the stipulation that if a deceased employee’s spouse is also a government employee, the spouse would not receive a pension. Additionally, rehired retired employees would have to choose between pension and salary. The reforms also propose indexing pension increases to the Consumer Price Index, with a maximum allowable increase of 10% per year.

But according to media reports earlier this year, even these measures faced resistance from the Establishment Division, which argued that they would disadvantage and discourage civil servants. As a result, these reforms were not implemented.

The reform initiative, therefore, ended up to be nothing but a reincarnation of the three measures proposed by ex-finance minister Ishaq Dar in the budget for the FY24. This is the very “three-pronged” strategy presented by Muhammad Aurangzeb in his budget speech.

One new step that the government has however announced is forming a contributory fund for newly appointed federal employees. The time it would take to realise this step however, is at least 35 years, if one is optimistic.

It is important to point out that the public-sector pension liability now exceeds government spending on development projects, underscoring the urgent need for sustainable reform.

Taimur Khan Jhagra, a former finance minister of Khyber Pakhtunkhwa, launched a contributory pension scheme for provincial employees hired since July 1, 2022, marking a significant departure from traditional practices. He notes that India adopted similar reforms in 2004 under a World Bank project, which failed in Pakistan, leaving a Rs1.5 trillion pension bill for FY24, a third of which is military pensions.

Jhagra while talking to the media warned that without reforms, the pension bill is projected to grow at 22-25% annually for the next 35 years. He underscores that the national pension bill has increased fiftyfold over the past 20 years, doubling approximately every four years. This exponential growth threatens to bankrupt the pension system within a decade if left unaddressed.

“The new budget has announced pension reforms but they should have mentioned how this started off in KP, and it would have helped had they followed our model. The next step was putting new employees on a contributory pension scheme. But these employees won’t be getting pensions for 40 years. What of all the employees today? Their pension is still fixed,” he says.

The State Bank of Pakistan’s 2021 report highlighted the unsustainable rise in federal pension expenditure, noting a Compounded Annual Growth Rate (CAGR) of nearly 14% between 2012 and 2023, a trend that has since

picked up.

If Pakistan is to continue under the current set of pension mechanisms, the bill, as per the CAGR of the pension bill will close in on Rs 4 trillion by the end of 2035. While the details of any reforms addressed at the administrative level are yet to be shared by the government, the financial projection looks bleak. It becomes a point of introspection for financial policy makers in the finance division and the establishment division, for which they might have to set aside their personal retirement privileges. A difficult call has already been made yet more difficult steps have to be taken to save Pakistan from this fast approaching headwind.

The past three decades show that there have been significant changes in pension schemes in most developed and emerging markets. As per international best practices, the Pakistan Government’s DB and unfunded pension arrangements are out of line. Non-contributory, or DB, schemes are reducing and many countries have switched to DC plans due to financial stress caused by large pension bills.

The advantage of such a switch is that the financing burden can be spread across different periods in a more stable and predictable manner. New accounting standards have helped Governments to better understand the underlying accrued liabilities and the longterm costs of their pension arrangements. DC pension programs, therefore, are replacing DB plans. The DC system by its very nature ensures that the accrual of benefits are fully funded. Thus, employers are guaranteed that no unfunded liabilities would emerge.

However, this could have an adverse impact on employees since the value of their accumulated pension assets are not defined, and because they depend on the investment performance of underlying pension funds. Most importantly, DC schemes allow employees to play a role in the investment decisions. This allows individual risk/reward preferences as well as leaves room for other considerations like wanting to invest only in Islamic securities. The employee will essentially become masters of their own destiny with respect to investment decisions about their retirement benefits, and may fetch more satisfying returns (both financially and otherwise) than they could have under the guaranteed DB system.

The DB system is easier and safer, but the DC system is not a burden and it also allows for more freedom. n

Everyone seems agreed on the privatisation of our DISCOS. But has anyone bothered to look at what is best for these companies and the consumers?

It seems of all the debates that are constantly raging in the corridors of ‘power’, the one issue that seems settled is the privatisation of our distribution companies (DISCOs). In recent times, it seems everyone across the political divide, within the bureaucracy, and other stakeholders have fallen in line that the solution to our DISCOs is to privatise them.

The DISCOs themselves have a long and interesting history that this publication has covered in the past. The basic problem on our hands is that these distribution companies have faced major losses and have been far from efficiently managed. For example, one of the biggest problems in particular has been the theft of electricity and how difficult it is to make recoveries from consumers. Does the answer lay with the private sector? The government would have you believe yes, but when the government itself has been unable to thwart electricity theft with law enforcement at their command how will the private sector?

These are the questions that nobody seems to be asking. Most seem convinced that privatisation is the answer. They are focusing on how best to go about the privatisation instead of wondering whether it is the best route forward. This is not to say privatisation does not have its benefits, but the reality is that this silver bullet should instead be a contentious issue.

This week, Profit delves into the privatisation of our DISCOs, and confronts whether this is the best solution possible or not. Our answer is complicated, and nowhere near as simple as the government would make it out to be. To start, we go to the beginning of how power distribution works in this country, with a little thing called ‘Take and Pay.’

Pakistan's power sector confronts a formidable challenge - an overabundance of 'Take or Pay' generation capacity. The 'Take or Pay' system is a contractual arrangement commonly used in various industries, including the energy sector, to manage supply and demand. In the power sector, the 'Take or Pay' system stipulates that the purchaser must either "take" a specified quantity of power from the supplier or "pay" a predetermined fee for the unused portion.

In Pakistan’s energy sector, the Central Power Purchasing Authority Guarantee (CPPA-G) Limited is the purchaser which procures power from generation companies. It does so on behalf of 10 distribution companies, colloquially called DISCOs, which are companies such as LESCO etc. These companies are

in the business of providing electricity to the end consumer. They set up the infrastructure, figure out the billing, and collect the amounts payable. Since they are to provide this electricity, they give forecasts to the CPPA-G which then procures electricity for them accordingly. The rates at which this power is procured are determined by National Electric Power Regulatory Authority (NEPRA).

Under the ‘Take or Pay’ arrangement, the purchaser commits to purchasing a fixed amount of power from the supplier, regardless of whether they actually consume or utilise that amount. If the buyer fails to take the agreed-upon quantity of power, they are still obligated to pay for it as per the terms of the contract. This ensures a guaranteed revenue stream for the supplier, providing them with financial certainty.

Another way to look at how ‘Take or Pay’ works is rental cars. If you rent a car for say five days, you incur two types of costs if you travel: fuel cost and car rental. While you can save on fuel costs by limiting your travel for those five days, you can not save the rental cost.

Under 'Take or Pay' contractual agreements in Pakistan’s energy sector, power producers receive two types of payments: capacity charges and energy charges. Capacity charges are payments for the availability of the power plant, regardless of whether the electricity is actually utilised by consumers. These charges cover the fixed costs of maintaining and operating the power plant as well as cover debt costs associated with setting up the plant, ensuring that it is ready to generate electricity when needed. Energy charges, on the other hand, pertain to the actual production and supply of electricity based on consumption

The 'Take or Pay' system is often employed in long-term power purchase agreements between power generators and distribution companies or utilities. It serves as a risk management mechanism for both parties, as it provides the supplier with revenue certainty while allowing the buyer to secure stable and reliable power supply.

However, while this system offers such benefits, it can pose challenges particularly for buyers. In situations where there is excess capacity or a decline in demand, buyers may be obligated to pay for power that they do not need or cannot use, leading to financial strain and inefficiencies in the power sector.

To cover the costs associated with 'Take or Pay' contracts, DISCOs may pass on the financial burden to consumers through higher electricity tariffs. This practice is necessary to cover both the capacity charges and the energy charges. Capacity charges, in particular, can be substantial because they are incurred even if the power plants remain idle and do not generate electricity. This ensures that power

producers receive a stable revenue stream, but it can impose a significant financial burden on DISCOs, which must be reflected in the tariffs charged to consumers.

In the current financial year 2023-24, the electricity consumers are estimated to be paying Rs1.3 trillion, an appalling number, in capacity costs to those power plants regardless of the time when they are not producing any power.

This figure represents the payments made to power plants that have remained shut or underutilised. Despite not generating electricity, these power plants still receive capacity payments, highlighting a critical issue within the 'Take or Pay' framework.

Because the ‘Take or Pay’ elevates the costs, the end tariff for customers is high, which leads to another big problem which is at the centre of the privatisation debate. This issue pertains to theft and the inability of DISCOs to even bill electricity that was sent out. Because higher capacity payments lead to increased electricity bills for consumers, this can result in public dissatisfaction and reduced affordability of electricity, particularly for low-income households.

This is actually a very human problem. A vast majority of the bills that DISCOs aren’t able to collect come from domestic users, not commercial ones. In a country like Pakistan, what do you do when you can’t foot the electricity bill? Either you don’t pay, or you start stealing electricity. And this is where DISCOs start having problems.

This inability of the users to afford such electricity leads to electricity theft and electricity that is simply not billed, translating into losses for DISCOs called AT&C losses (aggregate technical and commercial) losses. AT&C losses are basically losses on account of electricity that was sent out but not actually billed, called transmission and distribution (T&D) losses, and electricity that was billed but not recovered, known in technical terms as rate of recovery.

DISCOs that already have to pass on the expensive capacity charges to consumers also have massive losses on this account, leading further to the electricity getting expensive. These losses are more than prevalent in Pakistan’s power sector. According to NEPRA State of the Industry Report 2023, the 10 DISCOs in the country collectively had 16.45% in transmission and distribution losses against a target of 11.81% set by NEPRA. In rupee terms, this 16.45% was Rs160.49 billion that is borne by the DISCOs.

In some cases DISCOs try not to bear this loss. A NEPRA inquiry into the matter

In our part of the world, the government continues to suppress prices of commodities, particularly energy commodities to keep the populace happy. DISCO privatisation now is imminent because of the politics of energy that we played

Kamran Kamal, CEO of HUBCO

revealed that DISCOs resorted to load-shedding not because of unavailability of electricity but rather because of AT&C losses, which was a violation of regulatory standards. Such load-shedding is called revenue-based load shedding. DISCOs resort to load-shedding in high AT&C loss areas as a way to manage these losses. This means they intentionally cut off electricity supply to regions where high losses are expected, regardless of the actual availability of electricity. This inefficient practice not only impacted consumers but also impeded overall sales growth, exacerbating the issue of capacity charges.

Load-shedding in high AT&C loss areas reduces overall electricity sales because power supply is intentionally cut off. With sales growth stunted, the fixed costs associated with capacity charges remain high. These charges do not decrease with lower electricity sales, leading to higher per-unit costs for consumers.

Reduced sales directly impact revenue, making it harder for DISCOs to cover their operating costs and invest in infrastructure improvements. On the other hand, this is a form of collective punishment where some people resort to theft of electricity in a community but their actions lead to those that pay bills timely also bear the brunt. NEPRA has even gone on to say that such load shedding is illegal.

At the centre of the privatisation proposition is the inability of the government to reduce public dissatisfaction, improve the economic situation of communities that resort to electricity theft and lack of enforcement of law and order.

Everybody’s solution to this problem seems to be the privatisation of the DISCOs. The idea simply seems to be that if the private sector takes over it will be profit driven and hence find a way out. It is the same old tale about market forces and what not. Now, there are ways to make such

a privatisation successful, but as of now the government seems less interested in that and more so in washing their hands of the DISCOs. So before we get into the potential of privatisation, let us look at the problems it poses.

If the government can not enforce its writ and stop theft and leakages which lead to losses, the bright idea is to give it to the private sector. This is what makes it a messy proposition you see because of a myriad of complexities associated with the power sector. If the government can not enforce its writ, how would the private sector do it?

The proposal for privatisation in Pakistan's energy sector stems from a recognition of the deep-rooted challenges that have plagued the industry for years. Despite various attempts at reform, issues related to law and order, enforcement, and administrative incompetence persist, hindering the sector's ability to operate effectively. In many instances, these problems have proven to be systemic and resistant to traditional solutions, prompting a reevaluation of the government's role in managing the sector.

One of the primary concerns driving the push for privatisation is the law and order situation surrounding energy distribution. In many areas, particularly those with high losses and widespread electricity theft, the presence of armed groups and violent resistance to enforcement efforts has created a hostile environment for utility workers and law enforcement alike. This poses significant safety risks and operational challenges for government-run distribution companies, impeding their ability to effectively manage and maintain infrastructure.

Moreover, enforcement of regulations and collection of electricity payments have been marred by administrative incompetence and inefficiency within the public sector. The lack of accountability and transparency in decision-making processes further exacerbates these issues, leading to a cycle of debt and financial instability within the sector.

The pertinent questions that arise then are if the state can not enforce its writ and ensure law and order that leads to the recovery of electricity bills, how

would the private sector be able to do that?

The private sector does not have its own law enforcement agencies and neither the legal cover to raid a locality and catch electricity thieves.

Then there is the issue of cross-subsidization of DISCOs. In the power sector, some DISCOs subsidise others primarily through a uniform tariff system mandated by the government. Currently, the way NEPRA calculates tariff for end consumers is by adding generation cost which includes electricity and capacity charges, distribution cost of bringing the electricity to customers, margin of DISCOs and any losses associated in this arrangement. While the tariff is calculated individually for each DISCO initially, based on the government’s directives, this tariff is then averaged out and a uniform tariff is determined which is then applicable to all consumers all across Pakistan, regardless of the DISCO they are a customer of.

This system entails that all consumers across the country pay the same tariff rate for electricity, regardless of the actual cost of supply or the financial performance of their respective DISCO. As a result, DISCOs operating in regions with higher operational costs or greater losses may require subsidies to cover the gap between revenue generated from tariffs and the actual cost of providing electricity.

PESCO (Peshawar Electricity Supply Corporation) for instance had 37.40% T&D losses against a target of 20.24%, worth Rs 77.35 billion. In comparison, FESCO (Faisalabad Electricity Supply Corporation) had only 8.59% T&D losses against a target of 8.87%. As a difference between target and actual, FESCO users actually saved Rs1.45 billion. But since the government mandates a uniform tariff rate for electricity across the country, this means that consumers in areas served by FESCO, with lower operational costs and losses end up paying the same tariff rate as those in areas with higher costs and losses. Some DISCOs actually generate profits - they are public limited companies that are required to generate profits for the government of Pakistan. MEPCO for

If LESCO were privatised and ceased to subsidise the other DISCOs, the government would face increased financial pressure to support the remaining state-run DISCOs. This scenario highlights the government’s lack of cash, which is the very reason for pursuing privatisation. Selling profitable DISCOs like LESCO would leave the government with the underperforming ones, requiring even more subsidies to cover their losses

Tauseef Farooqi, former chairman of NEPRA

instance generated a profit of Rs10 billion in 2021 according to its financial statements.

So DISCOs with better financial performance, lower losses, and higher revenue collection end up subsidising DISCOs facing operational challenges and revenue shortfalls, because of the uniform tariff.

DISCOs operating in areas with higher losses and lower revenue collection face a financial burden that cannot be fully covered by the revenue generated from tariffs alone. These DISCOs may require financial support from the government to bridge the gap between revenue and operational costs.

The uniform tariff system and subsidisation of DISCOs have significant policy implications for the power sector. It affects the financial sustainability of DISCOs, government budget allocations for subsidies, and overall sectoral performance and efficiency. This is also one of main reasons for calling for privatisation of DISCOs, but is a problem at the same time: any potential investor might be able to get their hands on a DISCO that is less loss making or is profitable but then this DISCO is no longer a cash cow for the government that will subsidise other DISCOs anymore. Remember that the subsidies the government gives to loss making DISCOs is to cover losses which will bring down electricity tariff for the end consumer.

“For far too long we have focused on the generation side of things. Now we are realising that we need to look at the complete value chain,” says Kamran Kamal, CEO of HUBCO. “DISCOs around the world are very few that have government ownership.”

“In our part of the world, the government continues to suppress prices of commodities, particularly energy commodities to keep the populace happy. DISCO privatisation now is imminent because of the politics of energy that we played.”

Proponents of privatisation including Kamran argue that transferring DISCOs into private hands will inject much-needed efficiency, innovation, and accountability into

their operations. However, the reality could be far more complex. According to Asif Saad, the former chief operating officer distribution at K-Electric(KE), “The deep-rooted nature of DISCO losses suggests that a mere change of ownership may not address underlying systemic issues.”

The shining example that gives hope and becomes a basis for argument that privatisation can work is K-Electric, privatised nearly two decades ago, which often serves as a case study in the discourse surrounding DISCO privatisation for making notable strides in certain areas.

In a recent Pakistan Federal Public Expenditure Review released by the World Bank, the bank noted that K-Electric was a successful privatisation model.

In the report, the World Bank outlined that K-Electric’s performance since privatisation had improved. The bank was of the view that the company’s privatisation saved around Rs 900 billion for consumers and the government, driven by substantial investments, workforce optimisation and operational efficiencies.

The report pointed out that K-Electric invested around $4.4 billion across its value chain, resulting in improved operational efficiency. This led to AT&C losses coming down from 43% in 2009 to 21% in 2023, while T&D losses decreased from 35% to 15.3% in the same time period.

The bank emphasised that K-Electric had been prioritising digitisation and customer centricity, leading to a transparent billing system, improved customer service and digital connectivity for over 1 million of its 3.5 million customers. This endorsement by a reputable international organisation adds further credibility to the K-Electric model for future privatisation efforts.

But Asif Saad argues that K-Electric operates under a different business model, integrating both generation and distribution, unlike the state-owned DISCOs which are only involved in distribution. This raises the question of whether the T&D business alone is vi-

able without the integration with generation and the incentive for private investment in the T&D sector alone remains unproven.

Moreover, sceptics also say that even K-Electric resorts to completely shutting down electricity in areas where there are high losses. This brings into question the state’s responsibility of provisioning of electricity for all and ensuring that a private company does not penalise everyone for delinquencies of some users in an area.

If the situation at the centre is about recovering losses without using the state’s law enforcement power, then the model of privatisation needs to be an innovative one with a policy masterstroke that eliminates the need of law enforcement, brings in private investors and also ensures state’s responsibility of providing electricity to masses is also fulfilled.

Imagine a scenario where a private investor expresses interest in acquiring a distribution company. Of course if a DISCO is unable to generate profits, that is not what is going to entice the investor so the government would have to come up with some relaxations and reforms for the investor.

The investor might ask for a condition of having total control over pricing and the distribution of electricity so that she/he can make profits. The investor demands complete authority to shut down electricity in areas with high losses. This would necessitate the government to fully deregulate the sector, granting the private entity the power to make all operational decisions independently. However, if the investor decides to cut off electricity to loss-making areas, the government's role in ensuring universal electricity provision comes into question.

In this scenario, the primary concern is balancing investor autonomy with the government's responsibility to provide essential ser-

vices to all citizens, regardless of the economic viability of specific regions. Total deregulation might incentivize efficiency and reduce losses in profitable areas, but it could also lead to significant disparities in electricity access. Regions with high losses, often characterised by low-income populations, would suffer the most, exacerbating existing inequalities and potentially leading to social unrest.

“The biggest challenge, from the government’s perspective, to such privatisation of Pakistan's DISCOs is maintaining a uniform tariff across the power sector,” says Tauseef Farooqi, former chairman of NEPRA.

He says that currently, Punjab’s DISCOs are subsidising the tariffs for the rest of the country. In contrast, DISCOs like PESCO (Peshawar Electric Supply Company), TESCO (Tribal Areas Electric Supply Company), HESCO (Hyderabad Electric Supply Company), and SEPCO (Sukkur Electric Supply Company) face high tariffs and low recovery rates, making them not financially viable without support.

So for instance, if a business tycoon like Mian Mansha were to purchase LESCO, his primary demand would likely be full control over tariff settings, ensuring that LESCO could compete independently without having to subsidise other DISCOs. This would mean the end of a uniform tariff system, as private owners would not be willing to subsidise other regions.

According to Tauseef, currently, 75% of consumers are subsidised, and with an already high bill, any change in this system could lead to significant consumer backlash.

“If LESCO were privatised and ceased to subsidise the other DISCOs, the government would face increased financial pressure to support the remaining state-run DISCOs. The privatisation scenario highlights the government's lack of cash, which is the very reason for pursuing privatisation. Selling profitable DISCOs like LESCO would leave the government with the underperforming ones, requiring even more subsidies to cover their losses,” says Farooqi.

As mentioned above, the core issue of losses stems from two main problems: people connected to the grid but not paying their bills, and those not connected to metres at all. Privatisation could potentially address these issues through stricter enforcement and better management, but it also risks creating a system where only the profitable DISCOs are privatised, leaving the government to deal with the rest. This situation would exacerbate financial pressures and potentially lead to higher overall costs for consumers in other DISCOs.

To address these issues, the government could look to examples from other countries that have successfully combined private sector

The deep-rooted nature of DISCO losses suggests that a mere change of ownership may not address underlying systemic issues

Asif Saad, former COO of K-Electric Distribution

efficiency with public service obligations. For instance, in Brazil, the energy sector was privatised with strict regulatory oversight. The government established clear service standards and performance metrics that private companies had to meet, ensuring that even less profitable areas received adequate electricity supply. Moreover, subsidies were provided to support the provision of electricity to low-income households, funded through a mix of public funds and cross-subsidization from more profitable regions.

Another example is the United Kingdom, where privatisation of the energy sector came with a strong regulatory framework overseen by Ofgem, the office of gas and electricity markets. The regulator ensures that private companies operate efficiently while meeting the social obligation of providing electricity to all regions. Ofgem imposes penalties for non-compliance and sets price caps to protect consumers from excessive rates, ensuring that the benefits of privatisation do not come at the expense of public welfare.

Privatisation of power in Pakistan can not achieve anything if meaningful reforms are not introduced along. If private investors are to make money from owning DISCOs, it is going to come with giving them complete control over what they do with DISCO operations. In this case, it would be the government's responsibility to ensure that electricity is provided to the masses regardless of the ambitions of the private investor.

How could this be achieved in Pakistan? Some measures could be the following: Mini-grids: Mini-grids are localized electricity distribution networks that generate and distribute power to a small, geographically concentrated group of consumers where private investors are unwilling to supply electricity due to high losses. These systems typically operate independently of the main power grid and are designed to serve communities that are not easily accessible or economically viable for connection to the central grid.

Mini-grids can be powered by various

sources of energy, including solar, wind, hydro, diesel, or biomass. The choice of energy source depends on factors such as location, availability of resources, and local demand. Renewable energy sources like solar and wind are increasingly popular due to their sustainability and decreasing costs.

Mini-grid operators may implement various payment models, including prepaid metres or monthly subscription fees, to collect revenue from consumers. Tariffs are often tailored to reflect the cost of generation, distribution, and maintenance, as well as the community's ability to pay. This would provide electricity to a financially vulnerable community that would otherwise not be able to afford expensive electricity from the privatised DISCO.

Management Concession: The government can hand over DISCOs to private companies for a certain period of time without fully privatising them under certain terms and conditions which include ensuring provisioning of electricity to all is ensured. The private companies are responsible for the financial performance and the DISCOs remain a utility under the ownership of the Government of Pakistan.

Targeted Subsidies: Beneficiaries of programs like the Benazir Income Support Program (BISP) in areas with high losses could receive targeted subsidies, improving their ability to pay for electricity.

Increased Electricity Sales: DISCOs need to focus on selling the extra capacity in the system, which is currently underutilised. They should adopt business strategies to increase electricity consumption, such as offering lower prices to industries. In this way, better financial performance would decrease willingness towards collective punishment.

There are other ways too. The issue remains that privatisation seems less a solution and more an opportunity to get rid of a challenge instead of taking it on. And until this approach is abandoned, no privatisation will work because it will not in earnest be to fix the woes of our DISCOs. n

The current discussion on economic issues in government circles as well as business networks seems to be focused upon the host of energy issues being faced by the country. One of the major ones pertains to the distribution companies (DISCOS) and what to do with the constant losses burdening the public finances. For many years, across various governments and consistently advocated in IMF programs, the problem of DISCO losses is to be solved by selling these companies to the private sector.

The question arises - will privatization solve the problem? How does a change in ownership put an end to the perennial issue of financial losses? And why would a private investor venture into a sector where there is no previous example of successful returns for the investor? To be clear, I am not against the role of the private sector. In my opinion, the state is not capable of exercising control over the economy and therefore needs to create many public private partnerships to enhance performance viz its civic responsibilities.

Specifically In the context of the DISCOS, the issue is about

The writer is a strategy consultant who has previously worked at various C-level positions for national and multinational corporations

the type of change of control/privatization which needs to be undertaken to fix the DISCOS while providing adequate returns for private investors.

Before we venture further into the change of ownership discussion, let’s clarify what is the nature of problems with electricity distribution. Anyone who has basic knowledge of DISCO operations understands that the business suffers from a large amount of electricity theft coupled with low recovery rates. Both of these occur mostly in remote areas, city outskirts and urban slums where overall lawlessness is rampant and is caused by decades of economic deprivation and poverty.

According to the NEPRA State of the Industry report 2023, the 4 DISCOS with the largest quantum of Transmission & Distribution (T&D) losses as well as recovery deficits are (not necessarily in any order) Peshawar, Sukkur, Hyderabad and Quetta. If we were to note the respective geographical coverage of these DISCOS, we would see a wide expanse of sparsely populated rural areas or city outskirts. What is common amongst these areas, as well as urban slums, is the inability of the state to provide economic opportunities and hold the population accountable per the laws of the country.

While we do not have access to detailed T&D/recovery performance data, I would imagine the same would be the case with all DISCOS, including K Electric.

Therefore, how are we to deal with the issue of electricity theft? Is it a management or administrative issue or is it largely an economic problem? I would argue it is the latter and any attempt to solve this problem via only administrative measures will not succeed. It’s like saying we will solve the deep-rooted issue of inflation with price controls! Can it ever work?

Acase in point is to look at K Electric which was given into private hands almost 20 years ago. While KE has been successful in improving some aspects (full disclosure – I have been associated with this organization in the past), its T&D and recovery performance (according to NEPRA state of the industry reports) surpasses only the large loss-making DISCOS, and it is almost at par with most of the better-performing DISCOS.

But in the context of the future privatization of DISCOS, the relevant issue is not KE’s

performance. Instead, it is the fact that it follows a completely different business model as compared to the state-owned DISCOS.

The pertinent question to be asked, therefore, for our current discussion, is whether the transmission & distribution (T&D) business can be sustained on its own and if the private sector can be attracted to invest in it –if it was owned and run independently of the generation business.

The vertically integrated KE business model has stood against the highly regarded and internationally recommended reforms undertaken by Pakistan in the eventful 90’s decade. Is it a case against those reforms which saw a break up of WAPDA businesses - into GENCOS, NTDC and DISCOS?

One cannot try to answer this question without the perspective of the policymakers who orchestrated those reforms – but surely the financial viability of the transmission and distribution businesses on their own is unproven.

To date, the incentive to invest in T&D business does not exist and future owners will be aware of the same.

From the discussion above it is apparent that only a change of ownership of DISCOS may be a case of solving the wrong problem. We cannot improve the financial performance of DISCOS without dealing with the geographically poor and backward areas.

There is ample data available with the DISCOS which will point out the areas where feeders are underperforming in terms of theft and recovery. Instead of accusing the entire area of being thieves and criminals, their capacity to pay needs to be assessed and matched

with their electricity needs.

NEPRA, in its State of the Industry reports, recognizes and suggests distributed generation / solar power as a possible way out for outskirts and remote areas. The same applies to urban slums.

Perhaps beneficiaries of the Benazir Income Support program could be identified in these areas and some sort of concession be provided via BISP. State investment in basic infrastructure in these areas could also be given special attention.

Once these areas are marked for different types of interventions by the state, the relevant DISCO can proceed to improve the quality of its other business by crafting strategies based on some simple business fundamentals.

DISCOS need to sell the extra capacity in the system. This is what the country is paying for via “take or pay” based electricity generation and it can only be solved by selling/ consuming more units of electricity. It is not a complex problem when you think about running any business – building topline sales revenue is a fundamental requirement.

Electricity sales must be a targeted number not different from a small shop owner who knows he has to achieve sales of xxx rupees to meet overheads and generate a profit.

For that to happen, the shop owner can have many avenues; he can look for new customers, have a larger share of his current customers’ business, reduce prices for its large customers etc.

A DISCO is no different; it needs to

devise strategies to sell more electricity. If it can sell more to industries at a lower price, it should be allowed to do so. If a customer wants to purchase its electricity requirement from another provider, it must be allowed to do so. Some recommendations on these lines have already been made by various industrial chambers and ought to be considered seriously.

In the recent past, NEPRA has been able to split the “wire” business from the overall “distribution” business as well as move to create a wholesale market. These steps should allow DISCO monopolies to be phased out, and gradually relax the regulator’s hold on electricity pricing. Privatization ought to imply that the state will also do away with price controls and help create a competitive electricity market.

Despite the well-intentioned work done periodically by NEPRA and the Ministry of Energy, DISCOS’s performance cannot be improved without accountability to the citizens. Ever since the advent of the 18Th amendment, governments across the 4 provinces are increasingly showing more responsive behaviour and there is no reason to think they would not be more mindful of their citizens’ needs for this basic utility.

Therefore, the regulatory and ministerial custody of DISCOS needs to be shifted to provincial and local governments. However, this can only be a gradual process since they currently have limited capability. This learning needs to be expedited -they could learn from the Chinese model of communes where powerful incentives were created within the public sector to improve delivery.

In due course, the current DISCOS will need to be broken up into smaller and more manageable entities which become more receptive to their local consumer.

To conclude, the challenge is to take the required strengths of both – the public sector for regulatory and governance frameworks and the private sector to bring in professionalism, accountability and incentives to make good returns.

The matter of DISCOs privatization needs to be dealt with carefully and ought not to be a simple case of handing over ownership. Unless backed by strong and urgent policy reforms which focus on the separation of high loss/ low recovery areas, creating a competitive electricity market, incentivizing private management and devolution of regulatory and ministerial custody, it is unlikely to succeed. n

COMMENT

The

benchmark index has been on a rout and there are few signs that it is going to stop any time soon

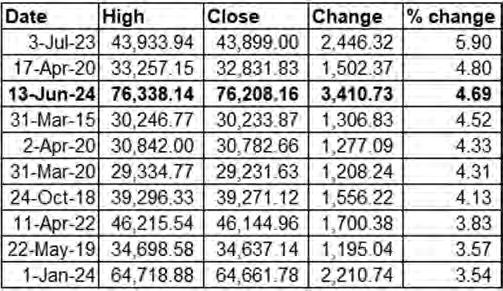

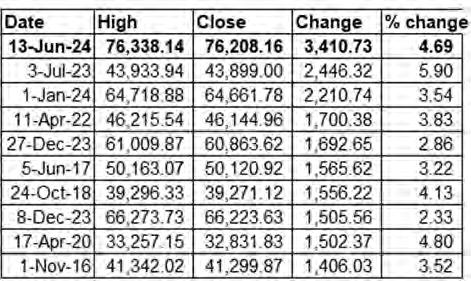

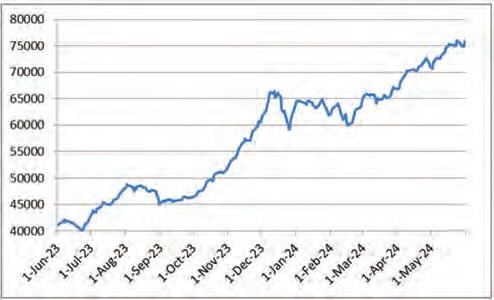

By Zain NaeemThe budget was announced on the 12th of June 2024 and it would be an understatement to say that the Pakistan Stock Exchange was happy. The benchmark index saw an increase of 3,410 points from its previous day close and was able to cross the psychological thresholds of 73,000 to 76,000 points in a single day. At its highest moment, the market saw a high of 3,540 points where the index was touching the nose bleeding levels of 76,208 points. This sentiment has further been strengthened as the next session saw an increase of 1,100 points taking it past the 77,000 level.

Suffice it to say that the market has welcomed and approved the budget. The question then starts to be raised whether this is the highest the market has ever achieved and what was the reason behind the market reacting this way. Let’s break down both these questions and give a perspective on both of them separately.

In regards to absolute terms, it can be seen that an increase of 3,410 is the most seen by the market. The previous highest point increase the market saw was around 2,446 points which were seen on 3rd of July 2023. There have actually only been three trading days where the index saw an increase of more

than 2,000 points with 1st of January 2024 being the third such day. After this, the points increased between 1,700 points and 1,400 points which were seen at varied dates.

In terms of percentages, it can be seen that 13th was only the 3rd highest price increase which was seen. In terms of percentage, the 13th of June saw a percentage increase of 4.69%. There have been two days which saw a higher increase taking place on 3rd of July 2023 and 17 April 2020 which saw the index increasing by 5.9% and 4.8% respectively.

The fact still remains that this is no small achievement that has taken place. So now that we have explained the what, let’s consider the why and how of the increase taking place.

In terms of the short term reaction, the budget can be seen as being business friendly. In the last few budgets presented, the corporate sector saw imposition of super tax, stringent taxing measures and steps taken to expand the tax bill on the corporations. The recent budget has shifted some of that focus. The finance ministry feels that most of the corporate sector is paying its fair share of taxation and so the new budget proposes tax measures which revolve more around personal income tax and sales tax.

One of the biggest victims of the new budget is the non-filer who is going to see his non-salaried income taxed up to 45%, capital gains tax from real estate and securities will be taxed up to 45% and they will be barred from traveling. Additional restrictions will see their mobile connection and utility connections being cut as well.

Some of the burden has also been shifted to the salaried class which will see their tax deduction rise with people earning up to Rs 200,000 seeing their tax expense rise by around 40%. Similar deduction will be seen for salaried class up to Rs 500,000 monthly salary which will see its tax expense rise by 25% as well. This adds on to the burden that this class already bears as the last paisa is squeezed out of them.

In addition to that, the general sales tax is going through a huge revision. Until the last budget, there were many industries which were exempt from sales tax or had reduced sales tax charges. Many of these exemptions have been taken away in this budget which would mean that industries will see a rise in their collection of sales tax. Why isn’t the corporate sector much concerned? Well it’s because of the fact that they can easily transfer this burden to the consumers and collect this sales tax from them. They increase the price of their product and make sure that they do not have to pay any tax from their pocket.

So it is clear that this budget will hurt the companies less than the consumers who have to pay additional taxes in the form of income tax and sales tax. The stock exchange is reflecting much of the same sentiment. The stock exchange is a collection of views and future outlook of people in relation to their expectation relating to the future performance of the company. The reaction by the market investors shows that they feel the budget is friendly

for the corporate sector in general. The major weight is actually carried by the investors who are investing in the market who are seeing their purchasing power and ability to invest shrink as a result of the budget.

That is not to say that certain sectors are not being impacted. One of the industries which is seeing higher taxes being levied on them is the cigarette manufacturers. Federal Excise Duty (FED) is being levied on acetate tow, nicotine pouches, e-liquids and filter rods which will see a rise in their cost and tax burden. FED is also being charged on cement bags which will raise the cost burden on the cement manufacturers. FED is also being charged when sugar is supplied to manufacturers which will raise the raw material cost for food industry related companies. One of the biggest changes being made is to take away the special status of exporting companies as they will be brought under the same corporate regime of 29% corporate tax and additional super tax in terms of revenues generated by them. Even when the index is improving, companies like Interloop are seeing their share price plummet as they are hit by this provision.

To say that the budget is the only contributing factor for the increase would be a stretch. The market is impacted by thousands of factors on a daily basis and naming one factor would be unfair to all the remaining factors. There are other factors that are also playing their role in this increase and they need to be seen as well.

Still, it can be seen that the general perspective of the investors is that the state of the corporate sector is healthy and the market will see further improvement in the coming months. What’s the reason behind this optimism?

In order to see into the future, there is a need to gain some insights by looking into the past. The previous budget was given by Ishaq Dar on 9th of June 2023. At that point in time, the KSE-100 index was trading at 41,904. The interest rates were hovering at 21% and they would be increased to historic high

levels of 22% in less than a month. The government was negotiating with the IMF as the second installment of the Standby Agreement (SBA) was being worked on.

Considering the corporate landscape of the country, companies were making record profits. The last time the index had hit an all time high was back in May of 2017 when the index touched 52,876. The company earnings around this time were lower and the market was trading in an overweight territory. The picture had completely changed in June of 2023 when it was felt that the corporate sector was making historic profits. Companies were beating the market expectations around their earnings on a constant basis.

The market was ripe for a rally which was not coming due to the political uncertainty prevailing in the country. The market started to rise from 40,065 on 23rd June and the interest rate increase was announced on 26th of June. Even though it dampened the mood for the day, it seemed like the idea of a market rally had come and could not be denied. From June 2023 to May of 2024, the index had gained 35,726 points which meant a return of almost 90% in a span of 11 months. The rally that was seen after the budget has some of its roots leading back to the momentum that was seen in the market already.

It seemed like the party for the index was over at the start of June. Rumors were already spreading around that the budget was going to be tax heavy and that all segments of the economy were going to be impacted. With an already spooked market, the tweets by two journalists made this into a full blown panic. First, Kamran Khan tweeted on 5th of June that there were rumors that the government had decided to substantially increase taxation on stock dividends and capital gains tax. He sourced his information to the State Minister for Finance and Revenue, Ali Pervez Malik. He also stated that there was massive selling going on based on this rumor by a Lahore based stock broker. More rumours started filtering in about how the capital gains and dividend were going to be equalized to standard personal income and that people earning more than Rs 500,000 per month could see a marginal tax rate of 45%.

that rumors of enhanced taxes on capital gains tax and dividends would end the stock market. He backed it up by showing that the market had already lost 4,000 points in a span of a week caused by these rumors. This was tweeted at 10:28AM. The Friday session saw the index tumble by 2,080 after the tweet was made. In today’s era, this tweet was shared multiple times on Watsapp groups which became a self fulfilling prophecy. The market had started to become afraid of its own shadow by now.

The panic finally subsided when only 3 and a half hours later Khan tweeted that he had talked to the Finance Minister who had poo pooed the whole idea and quashed this rumor. The market gained back 2,000 points it had lost as the chaos finally ended.

Coming back to the point.

After the second tweet was made, the market was still truly spooked so much so that even an interest rate cut of 150 basis points was not able to bring it out of its hole. The market was expecting a rate cut of only 100 basis points, however, the State Bank of Pakistan beat these expectations. Still, the market had all of its focus on the budget.

From 3rd June to 12th June, the market had lost more than 3,000 points. After the market closed and the budget was announced, the market showed its positive response and the market saw the rally that it did.

So what can be the contributing factors?

Part of this can be linked to the fact that the budget jitters had finally ended which brought the market to the levels it was trading at before the budget expectations creeped in. Some of the response can be down to the fact that the worst fears of the market had finally been allayed and that the budget was not as bad as it was expected. Well, at least for the corporate sector. Salaried people still have a case for the way they have been treated.

The panic reached fever pitch weh Kamran again tweeted on the 7th of June

Part of the optimism can even be down to the fact that the budget has been made while keeping in mind that the IMF will give the next facility based on this budget. Once a budget this tax heavy is passed, the road will be paved for the next facility being granted. There are also positive sentiments in regards to the interest rates that will be seen going forward. The recent cut in interest rates and the inflation tapering off does show that there are chances that the interest rate will come down further which is being factored into the index as well. Falling interest rates bode well for the private sector and their financing cost going down in the future which will have a positive impact on their profitability.

With the index currently trading at 77,197 mark and the market seeing a point increase of almost another 1,000 points, it can be said that the party at the PSX is not going to end any time soon. n

There is an incoherence between the treatment of the formal and informal sectors of the economy. And those documented can’t escape

By Zain NaeemWith the halls of the assembly not echoing with the shouts of the opposition and the table thumping of the treasury benches, it is now time to evaluate the budget that has been presented. In a span of two days, the government gave out its Economic Survey for the last year and then presented a plan on how it was looking to achieve those goals. Much of the speech seems like the same old same old that is presented by the Finance Ministry every year.

After all, the budget is the same struggle every year. The government plays catch up with rising expenses and to deal with them they find new sources of revenue. The main hope is to collect this money through taxation. This year, the government has chosen to do this through two methods. The first part of this two pronged approach has been to further tax the already burdened formal parts of the economy. These are salaried individuals, exporters, importers, listed companies, and all other businesses that are already registered with tax authorities and are documented.

These individuals will understandably be upset. It seems the government of Pakistan consistently fails to bring a majority of people into the tax net, and every year instead of fixing this problem their answer is to further squeeze those already in their grasp. Filing your taxes is essentially a punishment at this point.

And while salaried individuals and registered businesses have just cause for concern, there is some hope. The government is promising this year to make life a living hell for non-filers by increasing taxes on them, blocking their sims, and any other number of measures. But are these just words? If there is one thing about the government of Pakistan, it is that its word cannot be trusted.

It is a cyclical conundrum. The government instead of incentivising being a filer punishes being a non-filer. But they make it so dire that people find new ways to evade their taxes. In response, the government punishes filers, which makes non-filers want to file even less. The loft targets the government have set seem overambitious, and they might know it themselves. As a result, the formal sector will face most of the pain from the budget while the informal sector will try to evade coming into the tax net as much as possible.

The budget that has been presented can be divided into two broad categories. One is the implications it will have on the formal sector while the other deals with the informal part of the economy. Till date, the problem with the taxation system is that the formal economy is taxed at every possible avenue while the informal sector gets to evade coming into the tax base of the country. As the weight on the formal sector keeps increasing, stricter measures are used in order to bring the informal sector into the taxing fold. Sadly, this does not happen. The reason? Lack of enforcement. The apex body for taxing and enforcing tax laws is busy being Nero while the country burns.

Let’s consider an example. Cigarette manufacturing is a legitimate business that is carried out. With companies like Philip Morris Pakistan and Pakistan Tobacco, there are companies which are involved in producing cigarettes at a mass scale. They are part of the formal segment of the economy and have tax laws that are applicable on them. On

the other hand is the illicit cigarette trade which takes place. Smuggled cigarettes from across the border are brought into the country and then sold at the local dhabas to the customers. Both these businesses are raking in the cash from their business. However, there is only one who is giving out Federal Excise Duty (FED), General Sales Tax (GST) and then corporate tax on their income. No points for guessing who this might be.

So what has been given in the new budget for these cigarette manufacturers?

Let’s start from one end of the cigarette. Literally. The filter of the cigarette uses a cellulose acetate fiber tows through which the smoke is filtered and then inhaled. According to the minister, this duty will not have an impact on the formal sector as most of the informal sector will end up paying this price. Similarly, the filter rod used, which is the cigarette body casing, will see its FED increased by Rs 1,500 per kg to take it to Rs 80,000 per kg. A good thing for the cigarette manufacturers is that the price threshold was increased from Rs 9,000 to Rs 12,500. What is the price threshold? In simple terms, if the price of 1,000 cigarettes crosses Rs 12,500, a higher FED is applied. This allows manufacturers to be able to increase the price of each of their cigarettes to Rs 12.5 without having additional FED imposed on them.

As smoking becomes unfashionable and expensive, companies are looking to diversify their product portfolio by offering vapes and nicotine pouches. Consumers get their nicotine fix without having to suck on the harmful chemicals. The government has also looked to impose FED on nicotine pouches of Rs 1,200 per kg and e-liquids will also be enhanced further.

The goal of the government is to collect more taxes from the formal sector and this will be seen as cigarette manufacturers will have to document their production and sales. As they have to disclose all this information, the taxes will be collected.

So what about the other part of the budget? What will happen to the informal sector selling illicit and smuggled cigarettes? In terms of the proposals, the government has used stern words in order to show how serious it is in dealing with non compliant sellers. They have granted themselves the powers to seal any business premises of retailers who are selling these illicit cigarettes. The problem? The enforcement of these measures.

Theodore Roosevelt used to have a saying associated with him. Speak softly and carry a big stick and you will go far. It seems that the Q-block looks to go in the opposite direction. They speak loudly and, to their credit, very boldly but the stick they carry is too little or of any consequence. The speaking loudly is the rhetoric part that is used by the dear minister in the assemblies giving their speeches. The little

stick is the part where agencies and authorities have to implement the laws that are already on the books.

And this phenomenon is not just restricted to cigarette manufacturing. One of the biggest sectors which generates a huge amount of income is the real estate sector. It is no hidden secret that the sector generates huge revenues which are not taxed to the rate they should be. Most of the deals that are carried out are under the table and carried out in cash. Even when the deals are disclosed, the value of these transactions are understated by as much as 50% in order to decrease the tax liability that is payable on them.

So what have the geniuses at the Ministry come up with?

They have placed an FED of 5% on plots, commercial and residential properties. Barring the fact that the values used to calculate will be lopsided, there will still be some generation of tax revenues. This is again going to target the formal part of the economy which is disclosing the information mandated on it. What about the non-filers who are going to be buying these properties?

In terms of paying income tax on buying and selling of property, non-filers will be charged 12%, 16% and 20% for properties valued up to Rs 50 million, between Rs 50 to Rs 100 million and exceeding Rs 100 million respectively. This compares to 3%, 3.5% and 4% for filers on the same slabs. For any gains made on the sale of the property, the minimum tax suggested is 15% for non-filers which can go as high as 45%.

Big words by the big man.

Something similar seems to be taking place here as well. The Ministry is setting ambitious goals in terms of bringing non-filers into the tax net and giving them an incentive to do so. The measures can only work once implementation of the laws is carried out. Who in their right mind would want to become a tax filer when they can easily stay non-filers and evade paying taxes. If they need to buy or sell a property at a profit, the best solution is to understate the values and avoid paying any taxes for the income that they have earned.

Your salary just dropped. Literally.

One of the worst examples of treatment of the two sectors of the economy would be epitomized by the salaried persons and people earning from other sources. Even after giving constant assurances that taxes would not be increased, the salaried slabs have seen an increase in their

tax rates. Other than people earning below Rs 50,000 a month, all the remaining five slabs see their tax rates range from 5% to 35%. The impact of this change is such that anyone earning a salary below Rs. 200,000 per month will see their tax expense increase by almost 40%.

Even for people earning Rs 500,000 per month, the tax expense is expected to increase by at least 25% as they will end up paying a higher amount of tax. The sad reality of the situation is that the government knows this and still uses these measures. Under the hollow rhetoric of coming down hard against the non-filers and no formal sector of the economy, the government knows that this is the best way to extract tax revenues.

Non-salaried people having income from other sources will see tax rates ranging from 14% to 45% but again these seem like empty words as there is an incentive for these people to circumvent the laws and avoid paying any tax at all. The formal sector has to disclose everything to the government and due to that they cannot use the same ploys and tactics that can be used by the informal sector.

What ends up happening is that tax revenues increase as the formal sector is taxed further while the government lauds the efforts of the FBR in reaching a bigger target every year while the formal sector languishes. The government can look to window dress its efforts and measures as much as they want. When they still have to increase the petroleum levy by 33% from Rs 60 to Rs 80 per liter, someone needs to tell the foreign Finance Minister that the emperor is wearing no clothes. Probably the IMF.

One more example of how the budget is more fluff than action is the fact that non-filers are seeing restrictions being increased on them. Recently, there was a suggestion to block the sims of non-filers in order to bring them into compliance. The backlash faced by the government from the phone companies alone showed how half cooked of an idea it was. This is an example of how difficult it is for the government to implement their decisions. Now it is being suggested to cut the utility connections and foreign travel of these individuals. Even the agencies who would be responsible for doing the aforementioned can be reprimanded for not doing their job. Retailers who do not become part of the Tajir Dost Scheme can see their shops closed and legal action can be taken against them.

Don’t get us wrong. We will be one of the first ones to ask for implementation of the laws and regulations on the books which can boost tax revenues generated by the government. But having such soaring goals without effective implementation means they fall flat on the face. Mr Aurangzeb needs to get a bigger stick if he needs the non-filers and informal sector to fall in line. n

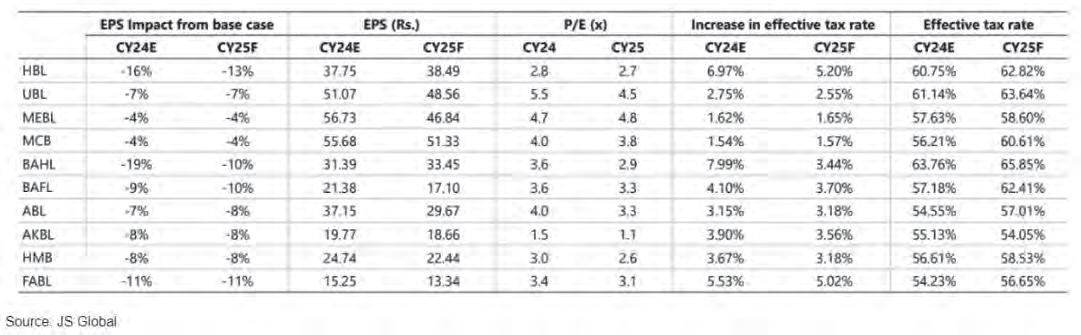

On 12 June 2024, Finance Minister Aurangzeb presented the budget for fiscal year 2024-2025 in parliament. Before the budget, just like other sectors, the banking sector was also anticipating new taxes. The only question was what shape these taxes would take.

Industry experts seemed to have their eyes peeled on what would become of three taxes in particular:

1. Tax on lower Advance Deposit Ratio (ADR)

2. A 10% Super Tax

3. Tax rates on government securities i.e. T-Bill/PIBs

All three of these are taxes that banks have had to deal with in recent years. Not so long ago Muhamaad Aurangzeb himself, then the CEO and President of HBL, would have been hoping the banking sector would avoid these taxes. So how did they come out in the budget? Profit looks at what the banking sector gained and lost from this year’s budget.

The ADR has been a contentious issue for the past couple of years. Very basically explained, a bank’s business is to accept deposits from customers and lend funds to other customers. But over the past few years, the interest rate in Pakistan has been so high that banks have found it

easier to accept deposits compared to lending money.

So what do the banks do? They lend to the one entity that does constantly need money no matter what: the government. This proved a pretty good system for the banks which have been making huge profits. But the government felt this was bad business. In a bid to force banks to lend more rather than just buy government-backed securities, the government placed an additional tax on any bank with an ADR lower than 50% in 2022. ADR is basically advances (lending) divided by deposits. Banks had to pay a 10% additional tax if the ADR is between 40% and 50%, a 16% additional tax if the ADR falls below 40%, and no additional tax if the ADR is above 50%. This additional tax was applicable on income from federal government securities.

This was seemingly a way to encourage banks to lend more and encourage business at a time when the economy has been in the doldrums. But a lot went down behind the scenes, and the banks were able to window dress their accounts to avoid these taxes despite successive finance ministers doubling down on it. That is why the policy did not last too long. In 2023, banks were exempted from this tax as announced in the fiscal year 2024 budget, so that banks had enough liquidity to lend to the cash-strapped government.

However, analysts were anticipating that the banking sector will not be exempted from this tax in 2024 in the fiscal year 2025 budget.

Yet, as per a report by Dawn, the banking industry was hopeful that the upcoming budget would eliminate the Federal Board of Revenue (FBR)’s ADR-linked tax policy. As per the report, the Pakistan Banks Association (PBA) had remained engaged with the finance ministry and the FBR on the ADR-linked taxation and other levies on the banks in recent weeks. PBA chief executive officer (CEO) Muneer Kamal was hopeful that the “serious discussions” with the FBR would yield results and lead to a solution.

However, contrary to the hopes of the sector, in the budget, the government stayed mum on the ADR-based tax and did not eliminate the tax for the fiscal year 2025. And similarly, there also seems to have been no change when it comes to the Super Tax, which the government actually imposed to avoid the situation that arose with the ADR-based tax back in 2023.