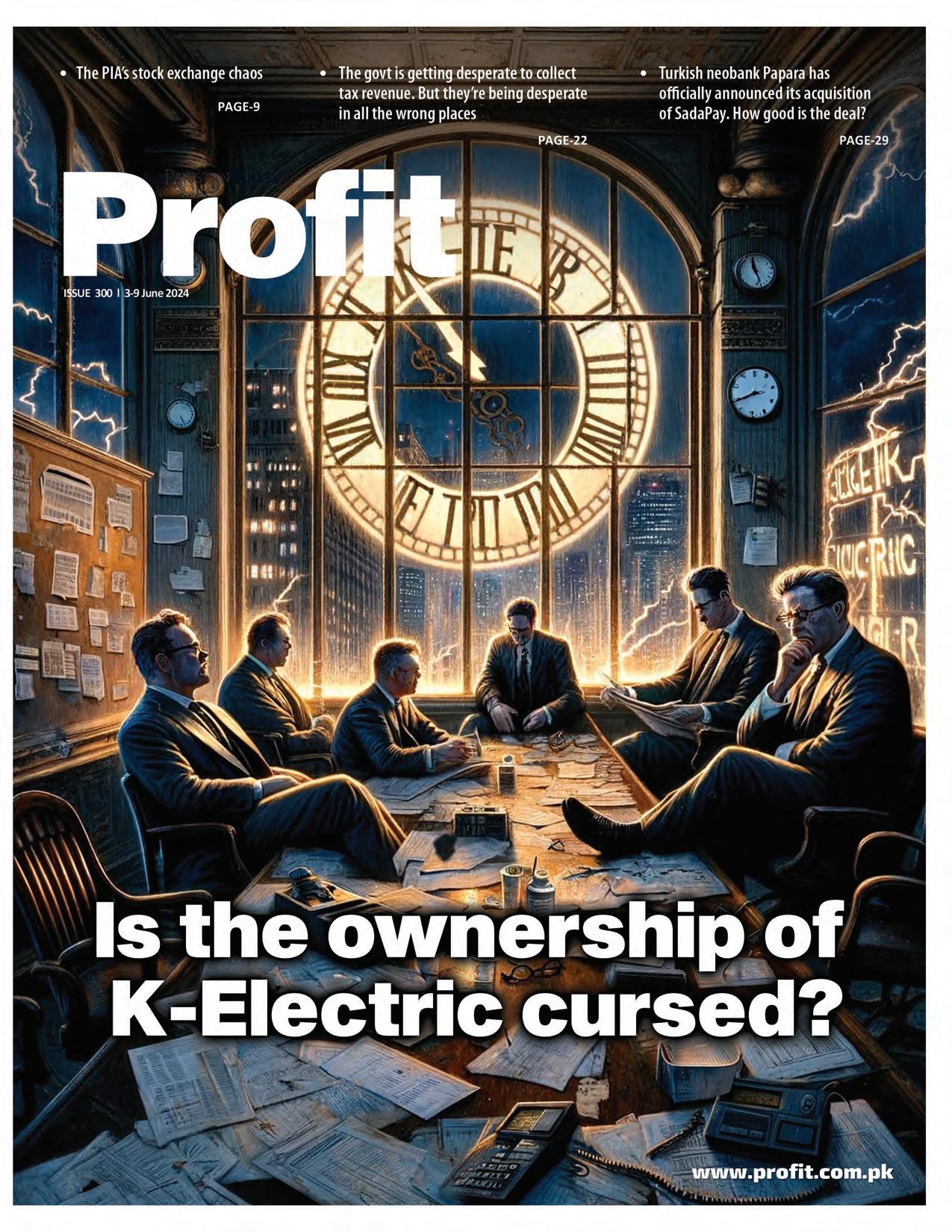

14 K-Electrics new owners still haven’t gotten management control. What will be left to control by the time they’re up to bat?

22 The govt is getting desperate to collect tax revenue. But they’re being desperate in all the wrong places

27 NAB just raided Bahria Town’s office in Pindi. With the company already on the brink of default, is Malik Riaz’s house of cards about to come tumbling down?

29 Turkish neobank Papara has officially announced its acquisition of SadaPay. How good is the deal?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

As Pakistan International Airlines (PIA) has been going through the process of privatization, the stock market recently felt the aftershocks of this decision. The events which started in August of 2023 snowballed into a mess which came into reckoning in May of 2024. With investors having to scramble at the last moment, questions are being raised in regards to the systems that have been put into place by the Pakistan Stock Exchange (PSX).

The PSX would contend that everything was done according to the law and that they had no other option. Investors are claiming they are facing massive losses. What ended up happening was a perfect storm of events in a case of everything happening all together. Critics feel that exceptions could have been made or the disaster could have been avoided altogether. Who is at

fault really? Profit explains the whole ordeal.

Please put your tray tables in an upright position and fasten your seatbelts.

Our story starts in the air conditioned halls of the Government of Pakistan. In August of 2023, it was decided that PIA was going to be privatized. The decision had been made to cut out much of the bureaucratic red tape and the deal was going to be made to plug in the hole which was draining the exchequer. The task was given to the Privatization Commission to do all that was necessary and in November of 2023, a financial adviser was tasked with carrying out the transaction. As PIA is a listed company, the formal announcement of the deal was made public on the 14th of December.

As soon as it was announced that PIA was

going to be privatized, the stock price jumped by 50% from Rs 6.22 to Rs 9.22 and the share price saw upper locks being hit everyday. There were buyers interested in buying the shares as they saw that the company had a higher value and once it was sold, they would be able to get a much better price for it. With buyers excited for the prospects of the company, the stock price had doubled from Rs. 6.22 to Rs 12.07 by January 2024.

Once the due diligence had been carried out, the financial adviser, EY Consulting LLC Dubai, proposed a legal segregation plan and based on that drafted a Scheme of Arrangement. This Scheme was presented to the Federal Cabinet who approved it and directed the Aviation Department and PIA to carry out the regulatory actions in order to implement this scheme. The approval was given on 19th of February 2024.

The market reacted to this announcement as the share price rallied again from Rs 10.8 on 29th of February to Rs 27.61 on 21st March

2024. This was an increase of 255% which saw the share price hit new highs. As the share price again started to lose some steam, on 26th March , the company announced that its board had approved the Scheme of Arrangement. This further pushed the share price to Rs 31.54 by 29th of March.

The system that has been designed by the PSX and the Securities and Exchange Commission of Pakistan (SECP) mandates that different requirements need to be met when a company is going through a restructuring process. In the case of PIA, the privatization would mean that different approvals are required by the SECP in order to make sure the investors are made aware of any developments.

On May 3rd, SECP approved the Scheme of Arrangement. In simple terms, the Scheme would have meant that shares of PIA would have been canceled and PIA Holding Company (PIAHCL) would be allowed to own 100% of the paid capital of PIA. This would have meant that Non-Core Undertaking of PIA would be transferred to PIAHCL while the aviation business is maintained by PIA. After this restructuring had been carried out, shareholders would be given the shares of PIAHCL in the same proportion as the ones they held in PIA before the restructuring had been carried out. This is a roundabout way of saying that some assets of PIA would be transferred to another company (PIAHCL) and the shareholders who held the share of PIA would be given shares of PIAHCL.

Seems simple enough.

But then who will get how many shares of the Holding Company? In order to determine this, companies are required to announce a date of book closure. What is a book closure? In the olden days, shares used to be physical and a complete record was kept by the share registrar of the company to make sure they had an accounting of who held how many shares.

As the system has become digital, shareholders hold shares in electronic form. There is still a registrar who sits in the middle to make sure his records are updated. Every day thousands of shares are traded and the registrar keeps track of these sales and purchases. Book closure is a date or a line in the sand that is set which states that all shareholders who held shares as on that date will be assumed to be the rightful owners of those shares. If the company has to give out any dividends, bonus shares or any other entitlement, the shareholders who actually hold the shares on that day will get that benefit. In the case of PIA, those shareholders will get the shares of the holding company who held the shares on 25th of May 2024.

The book closure date was also going to

be the date when the shares of the company would stop trading in the stock market as well. This would allow the shares of PIA to be delisted and the holding company would soon see its shares being traded in the market. It is like a date when a clean cut from the market can take place.

Are you with us so far? Good. Now is when the complicated part begins.

This all seems like the run-of-the-mill kind of stuff and comments on the efficiency of the stock market and the regulator that they have devised systems which are so effective that they can guarantee smooth operations without any glitches.

This seems to work until layers of complexity are layered on the top. This all starts with a notification released by the PSX on the 17th of May 2024 at 4 PM after the market has closed. The notice stated that as PIA had announced its own book closure on 16th of May, the PSX would pre-maturely expire the future contracts of PIA.

Confused? We know we have just introduced a huge concept into the mix. Let’s back up a little and explain what the future contracts actually are.

When the market is operating in a normal manner, shares of a company are being traded. While this market is functioning, there is also a future market that runs in parallel to the normal market. The price of the future contracts is linked to the regular market. The future market allows a buyer to buy a share in the future rather than buying it right now. The benefit? The investor does not have to put up the money right now. Let’s understand this with an example. Consider ABC is currently trading at Rs 100. An investor feels that the company will see a better share price in the future but does not want to put up the money for the share right now. So he goes to the market and buys a future contract of ABC-Feb at the start of February at Rs 101.

The future contract is usually trading at a higher price but the investors are not that concerned as he does not have to put up a total of Rs 101 for his shares right now. The market allows him to hold a position in the shares by only investing a fraction at the start. On the last Friday of each month, the investor has an option. Either he can put up the Rs 101 at which he was willing to buy the shares or roll over his position. This would mean he can buy the future contract in the next month which could be for Rs 103 and sell his position in the current month for Rs 102. He would lose out a bit as the contract he holds would be trading at a lower price and the contract for the next month would be expensive but again he does not have to put up all the money in one go. This allows the

investors to hold a position in a share without having to invest a large amount.

On the other end of the spectrum are investors who feel that the share of the company is being traded at a higher price. In normal markets, such investors can short the share. After the 2008 stock market crash, shorting the stock has been banned in Pakistan. A work around to this ban is that the investor can sell the shares in the future. An investor does not even need to own the shares currently as he can buy them later. Let’s say he sells the shares for Rs 200 in the market right now. He expects the share price to fall going forward. By the end of the month, he sees that the share price has actually fallen. He can buy the cheaper share in the regular market and sell it as he has contracted to do. This means that he ends up making a profit. Just like the buyer, a seller can also roll over his position indefinitely by selling the share in the next month and buying in the current month. This allows him to square his position in the current month and roll over his position into the next month.

PSX used to allow only one future contract in the past. Meaning you could only buy or sell a future contract for the next month. Recently, this has been changed and now it allows buyers and sellers to trade three future months simultaneously.

Are you still with us or do we have to go over something again?

Now that you are all caught up, let’s get back to the notification. The notification stated that as the shares of PIA were going to be delisted and a book closure date had been given, the PSX was going to end all future contracts prematurely. They were supposed to end on 31st May, however, now the contracts would end on 21st of May. The contracts of May, June and July would end trading in the market on a single day.

In normal circumstances, the investors would see only one contract ending and that would allow them to roll over their position into the next month.

This could not happen here. As all the future contracts were going to end, there was no option for investors to roll over.

When all the contracts were going to end, investors had two options left. As they had bought the shares, they were required to either put up the money and buy these shares in totality or they could sell these shares in the market. The notification also stated that the future contracts for the Holding company were going to be opened on the 3rd of June 2024. This would leave a gap of more than 10 days where no future contract for the company would be trading.

This is where the problem started. With no option to roll over, investors had to either procure the funds or sell the shares they have pledged to buy in the future.

This led to a panic situation in the market. The investors who had bought the shares in the

futures market scrambled to get funds in order to buy the shares and put up the money which was going to be required from them. They were willing to borrow money at 28% in the market in order to procure the finances.

On the other hand, they also had an option to sell. This option also proved to be a dud as everyone entered the market to sell their shares. This led to a fire sale where everyone was trying to liquidate their position as soon as possible. The market saw the price of the shares plunge from Rs 26.2 on 16th May to Rs 18.31 on 23rd of May. In 5 trading sessions, the share lost 30% of its value. Buyers were squeezed from both sides. On one hand they did not have the capacity to buy the shares and on the other they were not able to sell their positions either. With everyone entering the market at the same time, the lower lock was triggered which meant sellers were stumbling over each other to sell the shares while there were no buyers in the market.

The desperation in the situation can be seen by the fact that some investors sold their shares in the Negotiated Deal Market (NDM) at Rs 13.99 in order to sell their shares at any cost.

In such a situation, it can be easy to point the finger at the stock exchange. According to the laws on the books, the PSX had little it could do. The Scheme of Arrangement was sent to the SECP on the 3rd of May and it was approved. The ball was in the court of the company to announce a book closure date which suited it. This was done on 16th of May. PSX had little that it could do. As they were given 9 days of time, they had to announce a date at which the future contracts would stop trading. With Saturday and Sunday being off and the settlement schedule in place, it only had 3 days in which it had to pre-maturely expire the future contracts which it did. All the laws and regulations had been followed which is expected. Could it have been handled in a better manner though?

A situation similar takes place in the stock market on a quarterly basis. This is due to the fact that every earnings season,dividends are announced by a company. In order to determine the shareholders who should be entitled to the dividend, a book closure is given. After the book closure takes place, the dividend is credited to the account of shareholders. An example of this can be illustrated as follows. On 10th of October, a company states that it will give a dividend of Rs 1 to its shareholders and sets a book closure date of 15th October. What this means is that shareholders who hold the shares on 15th October will get a dividend. In terms of the share price, the share price will fall by Rs 1 as shareholders will get that in the form of cash dividend. Let’s say that on 15th of October, the share price was Rs 100. After the book closure date

passes, the share price will start trading from Rs 99. A shareholder who held the share on 15th of October will hold a share worth Rs 99 and would have gotten a dividend of Rs 1. He will be in the same position where he was when the share price was Rs 100.

Again this all seems simple enough. But what about the futures contract? The value of the futures contract is tied to the price of the share. On 15th of October, the future was worth Rs 101. Now when trading starts the next day, the future price cannot be reset to Rs 1 lower. What happens in that case is that as soon as dividend and book closure is announced, the PSX will list a B contract in the future. ABC-October will now have two contracts. ABC-October(A) and ABC-October(B). This allows the investor to roll over his position from Contract A to Contract B as he wishes to keep holding the future contract. Once the book closure takes place, Contract A will expire and B will continue trading in the future.

Investors who had to face a panic in the market state that something similar could have been done here. They state that a proxy could have been created where they could have rolled over their position from one contract to the other which was not allowed. PSX contends that as PIAHCL had not been listed and did not have a certificate of approval, no such proxy could have been created. No future contract could have been created for a share which was not listed in the market before that.

Again, the PSX is not wrong.

But the concern shown by the investors is correct. Not only for their own sake but for the sake of the whole market. In case the investors had not been able to cover their positions, this would have led to the whole system crumbling under pressure. What was the pressure? The case that cascading defaults would have taken place. If these investors had not been able to buy or sell their shares, they would have not honored the commitment that they had made in the market. An investor has promised that they would buy the share of PIA in July. Now that they were forced to buy it earlier, they could have backed out from this commitment as they did not have the necessary funds.

Similarly, someone had promised that they would sell their PIA shares to the buyer in July. Now, the PSX was mandating that the seller sell his shares while the buyer buys the shares. If the buyer would not have been able to buy the shares, they would have defaulted. The seller had the better position in such a situation as the stock price was crashing and he could easily buy the shares from the market. He had his pick as so many people were willing to sell their shares.

A default by a buyer can have a disastrous impact on the market. If one buyer defaults, the system is equipped to handle such a situation. The problem becomes larger when a lot of

investors end up defaulting. There is a chain of commitment that links brokerage houses and investors. Once a trade takes place, the buyer and seller commit to the fact that they will buy or sell their shares respectively. In case one of them does not follow through, the market mandates that they do so with different mechanisms. If a lot of participants end up defaulting, it might become a contagion risk where brokerage houses start to topple over in the form of dominoes. What the recent case highlights is that there is this risk that exists in the system. Maybe the market has been able to dodged a bullet for the time being. The actual impact of this incident will see ripples far into the future. The effects of the 2008 market freeze are still felt to this day. What needs to be pondered is that could exceptions have been made in this case where things could have been kicked down the road? Could a one-time exception have been made where PSX could have extended the date of book closure a few days to provide an easier escape to the investors. This would have eased some of the pain and panic which was seen in the market.

According to the data released by PSX itself, there were more than 33 millions shares that were active in the May and June futures markets. The book closure had been called by the company and PSX to only change the symbol of the company being used in the market. The book closure did not have any material impact in terms of dividends or stocks. In face of an action with such little consequence, maybe this could have been handled in a more delicate manner rather than doing it in such a hurry.

There is also speculation in the market that traders who had an inside track carried out blank sales in the future market. Around 22nd April, blank sales or short sales of future contract stood around 2.42 million which had increased to 8.64 million shares on 17th May. An insider who had knowledge of the book closure date could have used this information to their own advantage. They could have shorted the shares in the future in the lead up to the date of book closure. As the market panic would be triggered, the stock price would fall and they could buy the shares at a lower price pocketing the difference. There are concerns that as the Scheme had been passed on 3rd of May, an earlier book closure date could have been mandated seeing the future contract was trading.

The weight of the recent disaster was mostly borne by the investors which is the case most of the time. There was hue and cry over the sudden nature of these events. But this disaster also showed that there are vulnerabilities in the system which not only cost the investors but also have the potential to impact the whole market. Measures need to be devised by PSX to make sure similar episodes do not take place in the future. This will protect the investors and also look to protect the broader market as well.

K-Electrics new owners still haven’t gotten management control.

What will be left to control by the time they’re up to bat?

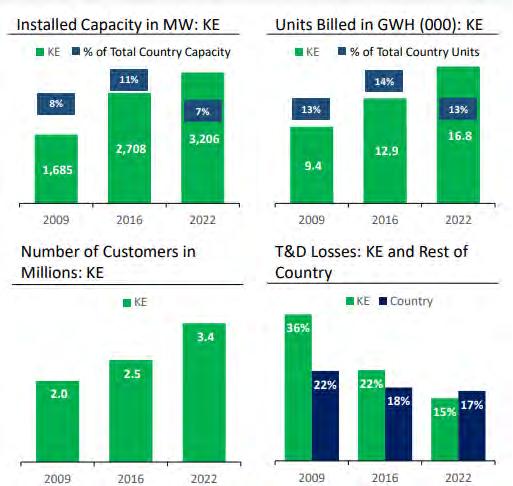

It has been more than a year since Shaheryar Chishty bought KE. Why hasn’t he gotten management control, and will he be inheriting a different company from the one he bought?By Abdullah Niazi

There was a rare bit of unity at the Karachi City Council in the middle of May. Packed into the assembly hall like sardines in the Karachi heat, members from the PTI, PPP, and JI were all united in their opposition to one entity: K-Electric (KE).

The anger came from hours of unscheduled load shedding in different parts of Karachi that had left the metropol’s population (the constituents of the good councillors) incensed. The power outages come from a years old strategy of KE and other distribution companies of revenue-based load shedding, in which these companies cut power in areas where electricity theft is high and the recovery of billables is low.

It is a strategy that has come under very particular scrutiny and controversy this year, and has pitted the federal government, NEPRA, Karachi’s local government, different political parties, and KE’s owners against each other.

What most might not realise is that this controversial back and forth is happening at a time when a massive cloud of uncertainty hangs over the future of Pakistan’s oldest and only vertically integrated electricity company. The uncertainty in question is over a disturbingly fundamental matter: Who owns K-Electric?

Back in 2023, the ownership of KE had changed hands. The company, once an Abraaj asset, was sold to AsiaPak Investments in a deal that took place in the Cayman Islands far away from Pakistani regulators and stakeholders. AsiaPak is run by Sheheryar Chishty, a former highflying banker who now owns Daewoo in Pakistan and has deep interests in Thar Energy.

Despite more than a year passing, Mr Chishty and his company have not been allowed to take the reins of the KE management. Behind this delay is a tussle between the new regime and some of the company’s minority shareholders. And as per the new owners, they have a plan for KE that might just turn things around. But if the status quo continues, how much of KE will be left for Mr Chishty to turn around?

Agreat deal can be seen through the company’s corporate history. Let’s start at the beginning.

Thirty-two years after Thomas Edison created the world’s first utility compa-

ny in Lower Manhattan, the Karachi Electric Supply Company (KESC) was founded in 1913 (rebranded in 2013 as K-Electric). It is the country’s only vertically integrated utility, with its own power generation, transmission, and distribution assets. Until the late 1960s, KESC was largely a financially self-sustaining entity. In the 1980s, the company briefly became a subsidiary of the Water and Power Development Authority (WAPDA) and was at one point placed under the management of the Pakistan Army.

The modern history of K-Electric that is relevant to us now begins after all of this. In 2005, the Musharraf Administration sold off a 66.4% stake of the company to a consortium of the Al-Jomaih Holding Company, a diversified Saudi Conglomerate, and the National Industries Group, a publicly listed Kuwaiti financial conglomerate (which also owns a large stake in Meezan Bank). For three years, the Saudi-Kuwaiti conglomerate failed to make any headway in turning around the compa-

ny, finally turning in 2008 to Arif Naqvi, the former Karachiite who had gone on to create Abraaj Capital in Dubai.

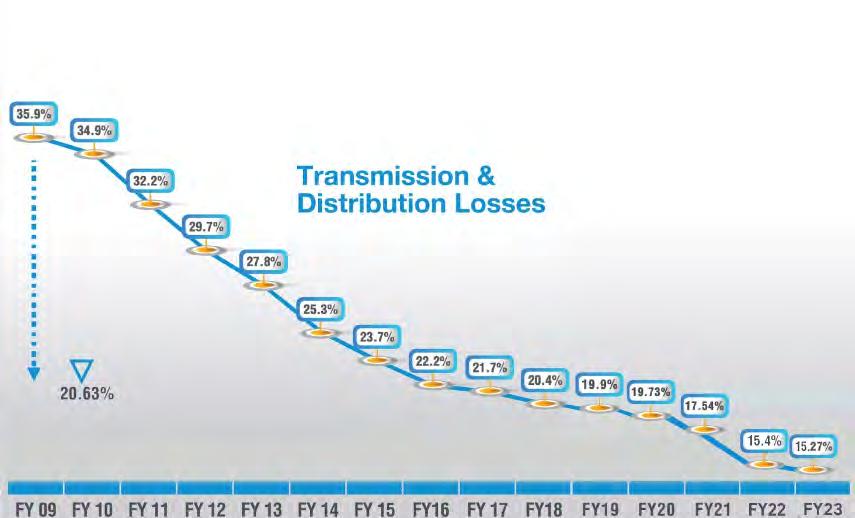

Abraaj was already the largest private equity firm in the Middle East by then, and had previously made forays into the Pakistani market before. In October 2008, Abraaj bought out half of the Jomaih-NIG stake in KESC, injecting $391 million into the company. It then began a turnaround effort the likes of which have never been seen in Pakistan before. Abraaj spared no expense in trying to turn around KESC, investing upwards of $1 billion in the company’s power generation and transmission infrastructure, which brought the utility’s power generation efficiency rate from 30% in 2008 to 37%. As per KE’s own numbers, from 2009 when Abraaj took over KE’s transmission and distribution (T&D) losses were 35.9%. By 2019 this number had fallen to just under 20%. This was a bonafide come-from-behind recovery.

During this journey, Abraaj was ready to

reap their rewards. They had taken KE on at a time when the company was a loss making entity (they made losses up until 2011-12) and turned it into a profitable power company. In 2016, they sold 66.4% of K-Electric to Shanghai Electric, the Chinese power company, for a whopping $1.7 billion making it the biggest acquisition of a Pakistani company in a decade.

This was always the plan for Abraaj. It is the very reason private equity firms came into existence in the first place. Abraaj came in, took control of a storied company with a unique economic purpose that had been sullied by bad management and turned it around through a combination of strategic capital investments and modern management techniques. Now they were ready to sell it off in a healthy, relatively unleveraged state to a strategic buyer.

Except what seemed like a deal made in the stars was cursed. To cut a very long story short, consistent delays on the part of the government meant the Shanghai deal could not go through. Despite a lot of political lobbying on the part of Abraaj’s Arif Naqvi, the deal was dead in its tracks. And then came the crash. In 2019, Arif Naqvi and Abraaj were involved in an international scandal that ended with the company utterly bankrupt. And along with it the Shanghai Electric deal went kaput. For six years Abraaj’s baggage weighed the Shanghai deal down and KE remained unsold.

As tough a year as it was for Arif Naqvi and Abraaj, 2019 was no bed of roses for K-Electric. Place the company in its context. For decades the company was a self-sustaining profitable entity. It met an unfortunate fate in the form of nationalisation and bounced around different government departments before finally being bought by a private equity company which set it straight and back to making money and providing its services efficiently. But when time came for a permanent new owner to take over, disaster struck.

At this time KE was under steady leadership. Moonis Alvi has been the CEO of the company since June 2018, a year before Abraaj came crashing down. Mr Alvi is an old hand at KE, and was one of the architects of its revival under Abraaj having been part of the team since 2008. He was the company’s CFO before his elevation to the top job.

So when it became clear Abraaj was done for, there was still a steady, stabilising hand available to keep the ship afloat. Mr Alvi continued in the same way that things had been going. Transmission and distribution losses continued to fall and have come down to as low as 15.27% compared to the 35.9% that existed when Abraaj first took over in 2008.

K-Electric is being treated as an orphan child by the shareholders, by the federal government, by the management and for whatever reason they are doing so is not my job to figure out

Shaheryar Chishty, CEO of AsiaPak Investments

But keeping things afloat can only go on for so long. From 2019 onwards KE was in a bit of a fix. It didn’t know exactly what to do with itself, so the focus became fixing losses and increasing efficiencies in other areas such as health, safety, and environmental (HSE) standards. None of this ends up helping the bottom line significantly, and to have any sort of long-term vision you need a long-term owner. For a while many thought Shanghai Electric would still be involved and interested, and the company did keep renewing their interest in keeping the deal alive every six months.

The baggage of Abraaj proved too much and kept weighing down the deal. and KE remained unsold. That is of course until a quiet, seemingly normal September day last year.

Shaheryar Chishty had been interested in K-Electric for a while. The former highflying international banker was born in Lahore, raised in Karachi in a

navy family, and came back to Pakistan in 2011 where he acquired ownership of Daewoo as well as interests in CPEC backed projects regarding Thar Coal. A self-described investor in orphan assets, Mr Chishty had been impressed by the Abraaj led turn around of KE and had tried to acquire the company. At that point, CPEC was at its peak and Chinese investors were deeply interested in putting money into Pakistan. Because of his involvement in CPEC projects in the past, particularly in Thar Coal, Chishty was well connected in China and put together a consortium that would bid for control of KE. But Shanghai beat him to it.

“There were Chinese investors, other Asian investors, and a couple others with interests in KE as well but in the end Abraaj ended up receiving a very good offer from Shanghai Electric,” Mr Chishty told Profit last year.

So when the opportunity presented itself again, Mr Chishty started making moves to acquire KE, which he did in the Cayman Islands.

The assumption was that the KE management and shareholders would be happy at the acquisition because it would mean direction. The Shanghai deal was clearly not happening, and KE was not doing too well either. Just look at their financials from 2023 where the company reported its first loss in 12 years. And it wasn’t some small dip in fortunes. K-Electric bled over Rs 31 billion last year in the wake of rising electricity prices and increasing line losses.

This was a dark moment in the history of the storied company. Its problems had caught up with it. These losses were ten times greater than the Rs 3 billion loss they incurred in 2020 because of the pandemic. Even though KE had been on a mission to cut line losses and make themselves more efficient, the company was always going to be a victim of the times. In the past couple of years, power prices have been raised by the government, the rupee has depreciated, inflation has soared, and the cost of borrowing from banks has risen sharply because of the very high interest rate that has been maintained for some time now.

Because of inflation, people are either using less electricity or they are not paying their bills or they are stealing. This has reduced KE’s recovery ratio from 96.7% in 2022 to 92.8% in 2023. The company also supplied 7.3% less power during the year “due to reduced economic activity”.

Despite all of this Mr Chishty and his other investors have not been allowed to take management control of KE. This does not mean they haven’t been trying, and the majority shareholders actually have a detailed plan with regards to how they want to go about best utilising KE. So why don’t they get a seat at the table?

What we have here is a legacy company that was in trouble, it was revived via private equity before falling victim to the very private equity firm that gave it a second life. Now, the company has new owners that have plans for it but somehow they are unable to get their foot in the door. Why is this so?

To understand this we must get to the bottom of how KE was acquired by these new owners. Profit covered this last year when the change in ownership first happened.

But to cut a long story short:

Since KE was owned by Abraaj, which as a company has gone bankrupt, its assets are a little all over the place. Just take a look at the ownership structure of KE. When the Al Jomaih group entered the picture in 2005, they

created KES Power Limited (KESP) which was a Cayman Islands company. This company paid the government of Pakistan directly and acquired a 66.4% stake in K-Electric in Pakistan.

So when Abraaj wanted to buy KE from Al Jomaih in 2009, they funnelled over $370 million in foreign direct investment into KE through the KESP company in Cayman. This money was channelled through the Infrastructure & Growth Capital Fund L.P. (“IGCF”), a $2 billion Cayman Islands private equity fund with investment contributed by over 100 different international investors, managed then by Abraaj Investment Management.

This means KE is owned by the KESP in the Caymans, which after Abraaj’s entry is now owned by the IGCF. So when Chishty wanted to acquire Abraaj’s stake in KE, it could not acquire KE in Pakistan. It had to go to the KESP in Cayman. Chishty’s company, AsiaPak Investments, created a special purpose company called Sage Venture Group Limited (Sage) and registered it in Cayman. Sage then bought out the Infrastructure Growth and Capital Fund LP (IGCF or the Fund), which holds an indirect material stake in K-Electric Limited. These transactions were authorised in proceedings at a court in the Cayman Islands, according to court documents.

This essentially meant that Mr Chishty and his AsiaPak Investments now owned the majority of the shares in K-Electric. This did not translate to them having control of the board of KE in Pakistan, but they could easily translate this into management control in Pakistan. Well, at least in theory they could. What they did not quite expect was that some of the minority shareholders would give them a real run for their money.

Now this is where things get interesting. Remember, what Mr Chishty has bought is a 53.8% stake in KESP, which is the company which owns 66.4% in KE. The remaining 46.2% of KESP is owned by Al-Jomaih Power, and Denham Investments. This is the same Al Jomaih that first bought KE through the KESP in 2005 before they sold it to Abraaj in 2008.

In August 2023, soon after AsiaPak acquired the IGCF which held the share in KESP (essentially Abraaj’s old position in KE), Al Jomaih used a special purpose vehicle by the name of White Crystals that had invested in the fund to bring arbitration against the general partner under an LCIA clause in the deed of limited partnership for IGCF. It is a complicated legal case that Profit has covered before.

The situation, however, is that AsiaPak essentially owns the same position in KE that Abraaj did up until it went bankrupt. And up until the Abraaj scandal blew up, the private equity fund had complete control over the KE board and could appoint its representatives onto it. This is something that through repeated legislation and stay order Mr Chishty’s AsiaPak has not been allowed to do.

Part of the reason could be the fact that the minority shareholders in question that form Al Jomaih have some serious influence within circles that matter in Pakistan. The Saudi and Kuwaiti investors that make up the consortium are people that the government does not necessarily want to get onto the bad side of. Perhaps nothing is more telling of this than reports of the Special Investment Facilitation

Council getting involved in this kerfuffle. As reported by The Friday Times back in October, the Executive Committee of SIFC had set up, on the instructions of high-ups, a three-member committee to resolve issues related to the power utility.

“K-Electric is being treated as an orphan child by the shareholders, by the federal government, by the management and for whatever reason they are doing so is not my job to figure out,” explains Mr Chishty in a conversation with Profit. During the interview, it was clear the process is frustrating. And why would it not be? When you buy something, you expect you’ll be able to apply it as you see fit. As a man with a plan, he feels very little is being done to set KE on the straight path.

This is what it boils down to for Mr Chishty and his AsiaPak Investments. In 2022, they bought an investment that they expected to have control of and run as they saw fit as majority shareholders. Instead, they have been denied this consistently. By the time they get control (if they do any time soon that is), what state will KE be in and will their plans be viable?

As Mr Chishty explains to us, his entire approach to the problem was to focus on high cost imported fuel that KE used to produce electricity. His plan was to use his influence and experience in Thar Coal to shift Karachi onto a cheaper fuel source for its electricity.

KE is plagued by many problems. The company is plagued by problems and is far from an investor’s dream. The only thing it has going for it is the monopoly it holds over electric supply in one of the world’s largest cities. Yet even this is under threat with people slowly coming to rely more and more on home based solar solutions. As things stand, Karachi is caught in a vicious cycle of energy being insufficient, unaffordable, uncompetitive, unre-

liable. Unaffordable energy reduces consumer purchasing power and lowers quality of life, leads to reduced tax base, as well as growing dissatisfaction with provincial and municipal leaders.

In response to these crises, Chishty has time and again made it clear he didn’t get into this to make a quick flip. His stated goal is to come on board as a long term owner and stay the ship. But with competing energy sources such as solar fast on the heels of KE, what does he plan on doing? The problems are clearly in front of us. Over the years, KE has become sluggish and inefficient. The number of people wanting electricity has increased. According to Chishty, the solution is to make K-Electric central to a modern, thriving metropolis. And that requires Karachi to change. One of his biggest claims is that the city itself is surrounded by ample area to utilise solar and wind power. The biggest problem with solar and wind is that it is very expensive to setup for the average household. So if a utilities company like K-Electric can harvest this energy it can provide significantly cheaper electricity to households.

According to KE estimates, in the case of solar there are 20% to 22%+ capacity factors easy to achieve. There are already well-developed ecosystems vendors, EPC contractors, and operating teams in Pakistan. There is also strong interest from international financiers. According to the company’s estimate, this would require around $1.8 billion in investment. Similarly for wind energy, there is a capacity factor of over 40% which is significant. Karachi is only 50 kilometres from one of the most high potential wind corridors; and there is also strong international investment interest in this as well. The estimated investment required would be around $1.3 billion.

And then there is the biggest card that Chishty has up his sleeve to save K-Electric; Thar Coal. When you think about it, the problem is actually very simple. Pakistan relies heavily on imported fuel sources such

as reliquified natural gas (RLNG) to produce electricity. Whenever there is an international crisis, such as the Russia-Ukraine war, Pakistan’s energy sector is rocked by the ripple effect. There is a simple solution. Cheaper fuel — something like coal perhaps. And the source is right there too. Spread over more than 9000 square kilometres, the Thar coal fields are one of the largest deposits of lignite coal in the world — with an estimated 175 billion tonnes of coal that according to some could solve Pakistan’s energy woes for, not decades, but centuries to come.

Discovered in the early 1990s by the Geological Survey of Pakistan (GSP), Thar Coal accounts for around 660 MW of electricity produced in the country. The potential is much greater. If new projects that are currently under construction become operational, in the next year electricity production from the Thar coalfields is expected to increase to as much as 2000MW. In short, Thar Coal offers a cheap, alternative, local source of energy that can be used to produce electricity and help Pakistan escape its topsy-turvy reliance on international markets to maintain its energy supply.

Chishty is naturally a big believer in Thar Coal. Two blocks of this project are already ready for operations. And according to a K-Electric document, the company feels they can easily be expanded at a low marginal cost. Located only 300 kilometres from Karachi, transportation is also not going to be a major expense. Already a rail line linking Thar to the national rail network is expected to be completed during 2023, and it will require an additional investment of just over $3 billion to produce 3600MW of electricity.

Using these three sources, K-Electric could increase domestic, industrial, and transport customers. And this isn’t where it ends. Chishty plans on also working with authorities in Karachi to build the City into a modern metropolis based on sustainable living. One of his goals is to introduce electric public transport and electric bikes with charging stations all over the city. Essentially, Chishty would also be synergizing his businesses. On the one hand he is in transport which can run the buses, on the other he owns KE which could provide the electricity, and he also has interest in Thar Coal which provides the raw material to create electricity in the first place.

It is a logical plan that makes sense. As the buyer of Abraaj’s position in KE, one would imagine Mr Chishty would easily be able to come in, take control, and at least see if his plan might work. Up until now, he has been denied that. As more time passes, the nature of KE will continue to change. Will the plans AsiaPak made to turn the company around still be relevant by that time? It depends entirely on how long this entire business takes. n

The govt is getting desperate to collect tax revenue. But they’re being desperate in all the wrong places

The new Tax Laws (Amendment) Act, 2024 has changed how tax cases are dealt with. While this may unlock some money, it doesn’t help widen the tax netBy Shahnawaz Ali

The government of Pakistan is getting desperate. But that isn’t exactly the problem. At this point in time, it is actually a good thing that the government is showing desperation. After all, Pakistan’s taxation system is broken.

Most people don’t realise that running a country is a pretty simple equation in the grander scheme of things. Governments need to regulate, provide a secure environment, social protection, and security to their citizens. To do this, they need money. And to provide these services they tax their citizens. For all of this to work, governments need to collect enough tax to spend as per their budget.

Pakistan consistently fails to do this. And they fail to do this by some margin. The reason, of course, is our persistent inability to collect taxes. The reasons for that are long and storied. But it seems rather than widening the tax net and devloving taxation powers beyond the FBR, the government finds new and creative ways to counter the problem.

The latest addition to the list of brilliant ideas, which includes such hits as blocking sims, is the amendment passed making changes to tax appeal laws in Pakistan. On May 6th, the Federal Board of Revenue (FBR) published a series of amendments called the Tax Laws (Amendment) Act 2024 in its official gazette. Interestingly, the act had been presented as a bill to the parliament only ten days earlier. This rapid progression raised several questions regarding the bill but the most important question that comes from the passage of this bill is the motivation behind the act. The act is not necessarily bad and could even help in improving recoveries, but it does not address the core issue.

What prompted the swift passage of the bill? What exactly does the Tax Amendment Act, 2024 entail? How will it affect the average Pakistani? And what implications does it hold for the future of businesses in Pakistan?

To understand what the amendments are, we first have to understand what the procedure is. The tax liability of any person

or entity is determined by a tax officer. Essentially, there is someone responsible for judging how much tax you as an individual or a company as an organisation owes the government.

An assessment order by a tax officer is a formal determination of a taxpayer’s tax liability for a specific assessment year. This order is issued after reviewing and examining the taxpayer’s filed documents, along with any additional information or documentation requested during the assessment process on any kinds of tax including income tax and sales tax.

The assessment order specifies the amount of tax due, including any additional taxes, penalties, or interest that the taxpayer must pay. It details the taxpayer’s income, deductions, and exemptions, as well as any adjustments or additions made by the tax officer. In the case of income tax, for example, the filer provides these details himself and the tax officer verifies/ signs off on them.

Hence that order includes a final calculation of the taxable income and corresponding tax liability based on applicable tax rates, and it provides payment instructions and information on the taxpayer’s right to appeal if they disagree with the findings.

This is where our story really kicks off. If a taxpayer disagrees with the tax order, they have the right to appeal this. Small claims often go to senior tax officers while larger claims can go into litigation all the way up to the Supreme Court and often take months and years languishing from appeal to appeal. On many occasions, in fact, tax cases can be some of the most complex judicial decisions to exist. Naturally, there are those that misuse this as well, by delaying having to pay taxes by contesting them over and over again.

This is why the appellant has to either provide a bank guarantee or some percentage of the assessed amount and can then appeal against the assessment.

To understand the problem at its core the readers also need to understand certain adjudicating bodies. The Commissioner Inland Revenue (Appeals), for instance, is an official responsible for hearing and deciding on appeals against tax assessments made by tax officers. They handle disputes related to income tax, sales tax, and federal excise

within specified monetary limits.

The Appellate Tribunal Inland Revenue (ATIR) is a high-level judicial body that adjudicates appeals against decisions made by the Commissioner Inland Revenue (Appeals). It handles cases involving significant tax disputes, including income tax, sales tax, and federal excise duty. ATIR aims to ensure fair resolution of tax-related conflicts and its decisions can be further appealed to higher courts.

Particularly, one could file a reference/ appeal with the Commissioner Inland Revenue (CIR) Appeals, and upon dissatisfaction re-appeal to Appellate Tribunal Inland Revenue, and so on to the respective High Court. But this was the case, until now. From now on, things are about to take a dramatic turn.

When presenting the bill to the parliament, the Federal Minister for Law and Justice Azam Nazeer Tarar revealed that there are pending tax cases amounting to Rs 2,700 billion across various appellate forums. These forums include Commissioner Inland Revenue (Appeals), Appellate Tribunals, High Courts, and the Supreme Court of Pakistan. The amendments hence aim to liquidate a significant number of these pending appeals, thereby freeing up substantial revenue. Over the years, the appellate system has faced issues such as arbitrary constitution of benches, inadequate number of benches, and delays in case fixation and disposal.

An arbitrary figure, tracking which back could take ages of old case files, led the parliament to pass the bill in a rush, and with an exemplary swiftness, which is testament to Pakistan’s renowned bureaucratic agility, the bill was given the presidential assent and then the status of an act within a week.

At its core, the Tax Amendment Act 2024 proposes significant changes to the handling of tax appeals, particularly focusing on the role and jurisdiction of the Commissioner Inland Revenue (Appeals) and the Appellate Tribunal Inland Revenue (ATIR).

Here, we delve into the details of these amendments only.

The Commissioner Inland Revenue

It is unconstitutional and against the command of the Supreme Court of Pakistan. No appellate forum should work under the administrative control of the Executive that is the Ministry of Law and JusticeDr Ikramul Haq, Supreme Court Lawyer, Partner at Huzaima Ikram & Co.

(Appeals) will now only handle income tax appeals involving amounts up to Rs 20 million for income tax, Rs 10 million for Sales Tax, and Rs 5 million for federal excise. For any tax appeal above the aforementioned threshold, the responsibility will shift to the Appellate Tribunal Inland Revenue (ATIR).

The ATIR is supposed to handle all appeals involving amounts above the specified thresholds (Rs20 million for income tax, Rs10 million for sales tax, and Rs 5 million for federal excise duty). The shift, as per the FBR, aims to streamline the appeals process and ensure quicker resolutions for high-value cases. What this means is that the higher the amount, the quicker the resolution and the quicker the realisation.

Unlike before, the time required for the filing of these appeals has also been reduced, from 60 to 30 days in hopes of making this process quicker. With all these big cases now shifted to the ATIR, the ATIR is mandated to decide on these transferred appeals within a six-month period. This is expected to clear the backlog of cases accumulated in tax appeals.

Similarly, all cases currently pending before the Commissioner Inland Revenue (Appeals) that exceed the new monetary limits will be transferred to the ATIR. The ATIR will begin addressing these cases from June 16, 2024, ensuring decisions are made within the stipulated six months.

One may wonder as to where would the ATIR, a small authority tasked with important decisions, run into such processing capabilities. By a careful estimate, this will increase the ATIR’s workload by twice if not more, considering that any disputed decision of the CIR(A) is also the ATIR’s responsibility. In a set of separate amendments, the composition of the ATIR is also going to change, one which will end the distinction between judicial and accountant members of the ATIR.

Moreover, the fee for filing an appeal or reference has been increased by at least 4x and at most 50x for the highest authority.

In other changes, the appeals to the Tribunal and references to the High Court

must be filed within 30 days of receiving the order. Moreover, the High Court is required to decide on these references within six months of filing, further ensuring timely resolution. Similarly, all the durations for appeals and stays have been either defined or reduced, making it mandatory to finish one year’s tax appeal within the same year.

Any appeal that hence asks for a stay in the high court is required to pay 30% of the tax determined by the ATIR.

The goal is to expand the tax base, which is essential for strengthening Pakistan’s economy. However, the amendments under question are only relevant to the set of taxpayers already paying their taxes. The bill applies to all individuals, entities and companies, whereas it has special provisions for StateOwned Entities which, for the purpose of simplicity, will not be discussed in this article.

Now, when the bill was presented in the parliament, the opposition Leader in the National Assembly, Omar Ayub, suggested that the proposed bill should be thoroughly discussed in the Finance Committee. This indicated the need for broader consensus and detailed scrutiny to ensure the amendments effectively address the issues at hand. Ironically, nothing of the sort was done.

The bill was bulldozed, and little to no time was given for technical discussions to be had by the elected representatives of the people. The bill gained the presidential assent on the 3rd of May and was published in the Gazette on the 6th of May, all after being presented in the parliament in the last week of April.

In this process to expedite the taxation process and then to expedite the Act, a few important factors were however overlooked. These anomalies that hence are apparent in these amendments might pose a serious question on their enactment. It gives rise to not just loopholes, but as found out by Profit through a series of interviews, genuine violations of the constitution itself.

The first and foremost problem arises with the dates of publishing and the date of presidential assent. Although this might not appear to be a major problem, tax professionals seem confused on the status of the appeals that were filed before the presidential assent and between the dates of presidential assent and the publication of the law.

There is a confusion about the date of operation (effective date) of the Tax Law Amendment Act. One perspective argues it is effective from May 3, 2024, while another viewpoint suggests it is effective from May 6, 2024. If the effective date is May 3, 2024, what recourse is available for taxpayers who filed appeals on May 3, 4, 5, or 6 at the wrong forum or after the specified time in the new law?

One of the problems as pointed out earlier is that of workload for the ATIR, despite the increased fees there is absolutely no “budget” available to track these payments that are to be made to the tax department. Moreover, the composition of the ATIR as given by the amendment is still the 5 members, with a much larger workload and increased number of cases, there are only two ways in which the ATIR can operate. One, by not reviewing the cases in detail and hence clearing the backlog or two by creating an even larger bottleneck, this time concentrated at the level two of the appeals hierarchy.

Another important issue that is pertinent to mention here was raised by renowned tax consultant Sharif ud din Khilji, while talking to Profit. He mentioned that there was an unclarity regarding the availability of a public budget for the increased adjournment and appeal fees. The adjournment fee from the ATIR i.e at least Rs. 50,000 (previously at least Rs. 1,000) and the Appeal fees i.e. Rs 20,000 previously (Rs 5,000) is to be made in the name of the tax department. It is unclear whether any of this amount can be budgeted yet.

There is also the establishment of a

political relationship between the government in power and the Chairman of the ATIR. Since the Federal Government will have the authority to dismiss the Chairman of the Appellate Tribunal on the performance committee’s recommendation, it creates a relationship of subordination of the Chairman to the performance review committee and in turn the Federal Government. We will later find out why that is a bad thing.

While the last point may seem like an anomaly to some, it can be construed as unconstitutional by many. Say a person has an appeal against the assessment of tax amounting to Rs 20,000. He feels that he does not owe this much and is rather rightfully only liable to pay Rs. 15,000. Then just to file this complaint twice, once with the CIR (A) and once with ATIR, that person will require Rs. 10,000.

Let us assume that due to any personal circumstance he has to adjourn or postpone the hearing, for this reason only, the person will have to pay up at least Rs 50,000. What will this average person do? Simple, he will just not file his taxes. And that is the core of the problem that the FBR has failed to address, the environment of mistrust, and the culture of lack of power with the common man. When another person with a tax liability in excess of 30 million walks scott-free and also gets to keep his money based on his contacts within the ATIR, then why would an average citizen be motivated to file?

Since the cost of getting a stay on any basis requires 30% of the determined tax, this just becomes a violation that has a price tag. Legal experts argue that the excessive fee increases and the 30% upfront payment go against the spirit of the constitution.

Dr. Ikramul Haq, a Supreme Court Lawyer, and Partner at Huzaima Ikram & Co. talking on the matter stated that “The enormous enhancement in the quantum of fees for filing appeals/references and compulsory payment of 30 percent of disputed demand for stay by High Court are unconstitutional, amounting to denying the fundamental right of free and unfettered access to justice. It goes against the article 10A of the constitution of Pakistan which affords every citizen a fair trial.”

It is a well-established fact in the tax world that mostly harsh, arbitrary and excessive orders are passed to show “performance” and “collection” by adjudicating officers that ultimately are adjudicated on in the Tribunal or by higher courts—only those sustains that are legal and based on reasons and evidence.

“The Appellate Tribunal shall consist of members who shall be appointed by the Federal Government in such numbers, in accordance with such procedure and on such terms and conditions as the Federal Government may prescribe by rules, which shall be made and take effect notwithstanding anything contained in section 237 of this Ordinance or the Federal Public Service Commission Ordinance, 1977 (XLV of 1977) or any other law or rules, for the time being in force”

Sub-section 2, Section 130 of the Amended Income Tax Ordinance 2001

Others become an opportunity of corruption for the Tribunal officers.

Higher appeal fees also means that the Bureau officers get more leverage to blackmail the taxpayers. Prospective taxpayers, to save themself from the high appeal fees and political judgement process, not to mention the serious toil of the legal process that comes with it, will find it easier to pay “rent” to the tax officers.

This brings us to another legislation that was passed in parallel with these amendments and is called the “Appellate Tribunal Inland Revenue (Appointments, Terms and Conditions of Service) Rules, 2024”. According to these rules not only will the composition of the Tribunal change (increase in number) but the salaries will also increase. So much so that members are now going to make salaries equivalent to those of high court judges, while the chairman will make as much as the salary of the Chief Justice of the High Court. Meanwhile members on deputation get Rs 700,000 in tribunal allowance along with their last drawn salary. Now that is a high incentive to work in the tribunal.

Just looking at the hirings in the last 1 year in Appellate Tribunals in the last two years, one could accuse them of political hirings but now these hirings will no longer be political. Since the new amendment allows for it!

According to the subsection (2) of the substituted section 130 of the Income Tax Ordinance, 2001: “The Appellate Tribunal shall consist of members who shall be appointed by the Federal Government in such numbers, in accordance with such procedure and on such terms and conditions as the Federal Government may prescribe by rules, which shall be made and take effect notwithstanding anything contained in section 237 of this Ordinance or the Federal Public Service Commission Ordinance, 1977 (XLV of 1977) or any

other law or rules, for the time being in force”.

Hence if the government did have any say in the matters of the Public Service Commission, it doesn’t need it anymore as far as tribunal hirings are concerned. With both the stakes and incentives this high, the tribunal is set to take on an allegedly political role. The increased number of hirings is also indicative of that.

Talking about this particular amendment Dr. Ikram states that, “It is unconstitutional and against the command of the Supreme Court of Pakistan. No appellate forum should work under the administrative control of the Executive that is the Ministry of Law and Justice. This principle was laid down by the Supreme Court of Pakistan in Government of Balochistan v Azizullah Memon PLD 1993 SC 31 that separation of judiciary from executive is the cornerstone of independence of judiciary. It is shocking to see how this clear command under Article 189 of the Constitution was ignored by the Ministry of Law and Attorney General of Pakistan, who also briefed the legislators on the importance of this amendment.”

Another factor that was pointed out while talking about these amendments was setting a time limit on the High Court. According to our sources, “Giving directions to the High Court, which is also a constitutional court, is blatant violation of the Constitution, and encroachment on the independence of judiciary. Since there is no mention as to what would happen in case a Court does not decide the reference within six months of the date of its filing, this provision is directory in nature and not mandatory.” This makes the entire process moot, as the appeals are likely to stack up at the high court level if not the ATIL level, and the FBR walks home with 30% of the tax, until the case is resolved, which as it seems is the prerogative of the high court. It is also worth noting that CIR (A) is

not an independent appellate forum yet the CIR (A) has now been made the final fact finding authority. No statutory remedy is now available on the question of fact determined by the CIR (A). This sure does expedite the process of appeals but does it make the process more or less just, remains a question that needs answering. Another problem that was pointed out by officials was the excessive adjournment fees without the provision for a case with genuine hardship.

The amendments, in general, can be termed extractive and not transformative.

Another ironic part of the amendment is the constitution of the adjudicating bodies. It is ironic that it is the same FBR officer who was once a tax officer and quite possibly once the Commissioner (Appeals) who will get promoted to the ATIR as the accountant member. By what logic will he suddenly have a change of heart and knowledge and become eligible to hear a case of a higher monetary threshold than he was before.

According to sources close to the developments in the Appellate Tribunal, more particularly in Punjab, it has been revealed that a lot of devout party workers have been appointed in the various tribunals across Punjab in particular making this another questionable step in a series of questionable steps.

With the growing concern of revenue shortfall, an amendment to remove the red tape in the appeals process can be seen as mandatory. Pakistan needs to run into some money, and it needs to do that fast. That is one of the reasons why the IMF is onto Pakistan for increasing the tax net, and the FBR is flapping its arms in all directions either by blocking the SIMs of non-filers or by shutting doors on justice seekers when it comes to value assessment. It is very likely that when asked, the FBR, the Federal Government or even the SIFC, present the IMF as a scapegoat for these amendments.

Sources told Profit that this is not the first time something like this will be tried under the guise of the IMF conditions, in fact it has been tried before a couple of decades ago. The only difference was that at that time, Pakistan was under a martial law and an active war.

The current government, contrary to the 18th amendment and the Supreme Court’s directives, instead of freeing the tax tribunals from the control of the executive, is further taming them, bringing them directly under their control.

Experts suggest that a writ petition in the High courts and eventually the Supreme

Court with reference to article 199 of the constitution shall be filed and the problematic amendments must be reversed.

By making the appeals expensive, not only has the government tried to close the doors on true assessment of value, but has provided added protection to the state machinery responsible for making these assessments. One could argue that these were necessary steps that needed to be taken, however, the question that is needed is. Does this increase the tax net? Does it bring new people into the net or does it discourage those entities already in the net to get out because they might not get a fair shot? If the latter is true, no service to the national exchequer will be done by putting these amendments in effect.

This is the fourth time we are ending a story on taxation with the exact same point. But we keep repeating the same point over and over again because it is true. No measures of this sort will matter unless Pakistan fixes its taxation philosophy, and fixing it is easy because we are not currently taxing in the spirit of our constitution.

The real problem is that Pakistanis are taxed unfairly and those that should be paying the lion’s share end up paying nothing. Just take a look at Pakistan’s tax structure. Tax structure refers to the share of each tax in total tax revenues. The highest share of tax revenues in Pakistan in 2020 was derived from value added taxes / goods and services tax (39.8%). The second-highest share of tax revenues in 2020 was derived from other taxes (33.3%).

In comparison to Pakistan, countries in the Asia-Pacific region only collect about 23% of their taxation from goods and services

taxes — meaning Pakistan’s average is almost double. Why is this the case? The biggest reason of course is that taxation in the country is centralised. The FBR collects almost all taxes (even the ones that should be collected by provinces under the 18th amendment) and then those collections are then given to the provinces in the form of the NFC award leaving the federal government with very little spending money. In an earlier interview former Finance Minister Dr. Hafiz Pasha, while talking to Profit, lamented that, “We as a country have failed to implement the beautiful 18th amendment. The implementation has been slow and weak.”

Since the share of the provincial governments, under the NFC awards, over the last few years has been increased from 40% to around 57%, it has provided the provinces with very little incentive to develop their own revenue sources. Despite having access to the two biggest cash cows, services and agriculture, the share of provincial tax revenue is close to 1% of the GDP. “You would be surprised to know that the corresponding number for Indian provinces is around 6% of the GDP, with similar fiscal powers,” says Dr. Pasha.

The solution of course is right in front of us: devolution. More than just being a third tier of democracy, having a local bodies system means having a new economic process. In essence, it is not just a new administrative stratification, but also involves the dispensation and spending of money. Things such as education and health that people automatically look towards the provincial government for would now be handled by local representatives. Perhaps most crucially, the ability of local governments to collect taxes and release their own schedule of taxation allows them to make their own money and spend it on themselves rather than waiting for the benevolence of the provincial or federal government. n

Days after Bahria Town founder Malik Riaz made cryptic tweets about not bowing to political pressure, the National Accountability Bureau has raided the offices of Bahria Town in Rawalpindi.

While NAB officials did not make a statement, seemingly wanting to keep the raid under wraps, there was confirmation from within the bureau of what had transpired. The raid was made to find documents and evidence related to the Al Qadir Trust case, in which Malik Riaz along with his son Ali Riaz Malik, are involved along with former prime minister Imran Khan and his wife Bushra Bibi.

The raid comes at an hour of great peril for Bahria Town, when the real estate development company is facing major losses in business, failing to attract new investors, and possibly even staring down the threat of default. New Bahria Town plots that were once fetching over Rs 1 crore per kanal are now failing to find buyers at Rs 60-70 lakhs. All this while the Supreme Court wants the company to pay Rs 460 billion in fines for its illegal acquisition of land to build Bahria Town Karachi.

With the involvement of its founder in a highly politicised case and fast changing business realities, is this the end of the road for Malik Riaz and Bahria Town? Profit uses

exclusive information to detail the teetering foundations of the once mighty Bahria Town.

For the longest time it seemed Bahria Town was untouchable. It was wildly successful, the people living there were happy with the services, property prices were soaring, and every new project was larger than the previous one. The company’s founder, Malik Riaz, seemed to have an in with the country’s corridors of power, forging relationships with every major politician and stakeholder.

But the troubles came for Bahria Town in 2019. This was the year the company was subject to a decision of the Supreme Court of Pakistan that fined it Rs 460 billion as well as an investigation of the United Kingdom’s National Crime Agency (NCA).

The first piece in this puzzle is Bahria Town’s troubles with the Supreme Court. To cut a very long story short, Bahria Town had acquired land from the Malir Development Authority for its superhighway project in Karachi. That land, originally owned by the Sindh government, was declared illegally acquired. In March 2019, the court accepted Bahria Town Karachi’s Rs 460 billion offer for the lands it occupies in the Malir district of Karachi and restrained the National Accountability Bureau (NAB) from filing references against it.

Bahria Town would have to make the

payments over the course of seven-and-a-halfyears. They would have to pay Rs 25 billion by August 2019, followed by monthly instalments of Rs 2.25 billion for the next three years. If they failed to make the payments for two months straight, the company would be considered a defaulter.

This placed Bahria Town under great pressure. They had to arrange the money and regularly pay their instalments or risk defaulting. At the same time, the company was facing another crisis. Malik Riaz and his family had been under investigation by the UK’s National Crime Agency (NCA). In December 2019, the NCA announced Malik Riaz had agreed to make a settlement worth £190 million.

The property tycoon’s family had been under the dirty money investigation for a few years which reached its conclusion with the settlement that was the largest ever in the history of the NCA. Not only did Bahria Town have to pay Rs 460 billion over seven years to the government, it also had to pay the NCA £190 million (around Rs 67 billion in rupee terms) as well.

Now Bahria Town was in trouble. They had two big bills to pay and the business did not necessarily have the legs to survive such payments. But then help came from unexpected

(or expected as some might argue) quarters. The £190 million that Malik Riaz paid the NCA was supposed to be repatriated back to the government of Pakistan. Instead, it was allegedly given back to Malik Riaz through a round-about way.

On the 5th of December 2019, the government of former prime minister Imran Khan announced £140 million of the money had been repatriated to Pakistan, but directly into the accounts of the Supreme Court. This is where the problem starts. The Supreme Court account that the money went into was designated for the payment Bahria Town was supposed to make regarding the transfer of land for Bahria Town Karachi for which the court had fined them the Rs 460 billion.

The direct transfer of the £140m into the special SC account raised alarm bells since it basically meant that the money Malik Riaz had paid to the NCA which was supposed to come back to Pakistan had simply gone back to Malik Riaz. On top of this, Bahria Town might have faced the threat of default if it had not paid the fine the SC had imposed.

The accusation is that the £140m that was repatriated to Pakistan after Shahzad Akbar’s intervention with the NCA on behalf of Malik Riaz went straight back into the bank account of the property tycoon. Mr Akbar allegedly did this with the connivance of then prime minister Imran Khan.

This matter would later prove to be the single most important legal challenge Imran Khan would face. After being ousted from office in 2022, Mr Khan was finally arrested in what has now come to be known as the Al-Qadir Trust Case on the 9th of May, a day that would go down in infamy.

The Al-Qadir Trust Case accused the former PM and his wife Bushra of accepting billions in cash and hundreds of kanals of land from Bahria Town in return for the help that Khan’s government gave to Riaz during his investigation by the NCA. Former interior minister Rana Sanaullah had claimed that Bahria Town entered an agreement and gave a 458-kanal land with an on-paper value of Rs 53 crores to a trust owned by Imran Khan and Bushra Bibi. The land was donated to Al-Qadir Trust, and the agreement bore signatures of the real estate’s donors and Bushra Bibi. Interestingly enough the amount being quoted by the prosecution witness as the value of the land transferred to Farhat Shahzadi is also just over Rs 53 crores.It is these 458-canals that have now come under the scrutiny of the accountability bureau.

In April this year, another bombshell

revelation came to light when a prosecution witness claimed during their testimony that the son of property tycoon Malik Riaz, Ali Riaz Malik, bought land for Farah Shahzadi in Bani Gali. Farah Shahzadi is a known associate of former first lady Bushra Bibi and has been linked in the case as well. According to the details provided by the witness, who is a patwari of Circle Mohra Noor (Banigala), claimed that nearly 245 Kanals of land in Bani Gala had been transferred in the name of Farah Shahzadi at a declared cost of Rs 53.28 crores.

Up until 2019, Bahria Town seemed untouchable. Even when the Supreme Court fined them Rs 460 billion for illegally acquiring land for Bahria Town Karachi, it seemed they had gotten away with it when through government channels they redirected another fine of £190 million towards paying that.

But the arrest of Imran Khan on the 8th of May in the Al-Qadir Trust Case changed everything. The highly politicised nature of the case along with the violent aftermath of his arrest have enveloped Bahria Town and Malik Riaz. Over at Bahria Town, property prices have fast been falling in newer projects. A Profit special report from December 2023 suggested plots that were worth over 1 crore four months ago are having a hard time finding buyers at Rs 60 – 70 lakhs. On top of this the group is facing troubles in their projects in Peshawar and Karachi where all manners of permits and bureaucratic hullabaloo is stopping them from creating the usual ugly but effective upper middle class communities they have come to be known for.

The reason behind this sudden downturn? Rumours that Bahria Town is in fact on the brink of default. On the ground property agents and land providers are both concerned that the downturn in the Bahria Town market is the direct result of the gamut of legal problems that the company and its divisive founder are facing. At the core of these troubles are the Rs 460 billion that Bahria Town is supposed to pay to the Supreme Court of Pakistan in a case that also has to do with the Al Qadir Trust that has gripped the nation.

All of this is happening in an environment where the property market in Pakistan is in a slump. As a result, Bahria Town’s projects are also seeing a dip. Now the two main ones that are ongoing are Bahria Town Peshawar and Bahria Town Karachi. On top of the declining market both of these projects are facing serious risks. Bahria Town Peshawar, for example, has not received an NOC or permission to conduct business at their project location. Normally this is something that happens to

very small scale projects. But in this case Bahria Town had marketed the project despite not receiving the NOC and their agents had collected investments as well. Now that the NOC has still not been received, all of those payments remain frozen. The investors are running after the agents and the agents have now been very openly complaining against Bahria Town and Malik Riaz — something unheard of until a couple of years ago.

Since the land in Peshawar where Bahria Town started its residential project was disputed, the project has practically been shut down. Many people booked plots for this project and paid money to the Bahria Town administration through different property dealers, but now they too are worried and uncertain about the future of this project.

In the middle of all this, Bahria Town has been in defence mode. Back when concerns began to be raised regarding their projects, they released a statement labelling the rumours as “Malicious Propaganda.”

The statement read, “Bahria Town is one of the most prestigious Real Estate brands in Asia, firmly rooted in its commitment to contribute to the progress and economic development of Pakistan. Despite facing malicious campaigns and unwarranted criticism from a misguided faction of the media, we persist in our dedication to serving the nation and delivering world-class projects. Through past challenges, we have weathered adversity, and our resolve to uplift Pakistan remains unwavering. Insha’Allah, this commitment will endure.”

In more recent events, Malik Riaz on Sunday claimed that he was being pressured for “political motives”, but asserted that he would not bow before anyone without mentioning where the pressure was coming from. But as reported by Dawn, it is widely believed that Malik Riaz was referring to Al Qadir Trust/University case, which was filed by NAB against PTI founder Imran Khan and his wife Bushra Bibi. They were the main accused in the £190 million corruption case. The case alleges that while PM, Imran Khan and his spouse obtained land spread over hundreds of kanals from Bahria Town Ltd to legalise Rs50 billion, which was identified and returned to the country by the UK authorities.

As things stand right now, Malik Riaz and his son along with other accused have their properties frozen. The public but cryptic reaction from him marks that he finds himself in trouble he can’t quite escape from. With Bahria Town already struggling and the recent raid by NAB, it seems the noose is tightening around Bahria Town. Will Malik Riaz be able to find a way out? Only time will tell. For now the future seems bleak for Bahria Town. n

Post acquisition, Pakistani users can expect a host of new SadaPay products and services such as savings and wealth management