27 24

27 24

08 Is the Track and Trace system a fraud or is there fraud within the system?

14 In the ever-raging battle between Coca Cola and Pepsico, Sting is King

21 Changes are afoot at Careem. What do they mean for the fast changing ride-hailing sector?

24 Highnoon Laboratories and the curious (court) case of Related Party Transactions

27 The banking sector has been reaping the rewards of high inflation. Is their winning streak coming to an end?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

Is the Track and Trace system a fraud or is there fraud within the system?

Deep inside Pakistan’s track and trace problem, a story of inefficiency, judicial interference and conflict of interest unfoldsBy Shahnawaz Ali

Pakistan is a country where the bureaucracy hardly gets reprimanded for their mistakes. So when the Prime Minister of the country offers stern criticism to the Federal Board of Revenue over something, it is meant to be taken seriously. A few days ago, PM Shehbaz Sharif, while talking to his federal cabinet called the track and trace system put in place in 2019, a complete fraud with the nation.

He said that it was a cruel joke that was played with the nation and demanded through investigation of the implementation of track and trace.

Since then the track and trace system has made the news quite often. An inquiry committee was formed and up until the filing of this story, two esteemed officers, one of them the current chairman of the Federal Board of Revenue, were found responsible for the “delays” in the enforcement of the track and trace system.

To understand what went wrong with what was promised to be a revolution in sales taxes, Profit followed the tracks of the implementation of this system. What unfolded was nothing short of an indictment of the Pakistani bureaucracy. A tale of red tape, inefficiency, kickbacks, controversies and allegations.

For readers who are not yet aware of what this system does, following is a simple explanation of what track and trace does:

Manufacturers frequently underreport their production figures to avoid taxes, initiating a problematic cycle. For instance, let’s consider a hypothetical scenario: a fertiliser manufacturer produces 500 bags of Urea, yet the demand stands at only 400 bags. If all 500 bags enter the market, oversupply occurs, leading to price depreciation. To circumvent taxation on each bag sold, the manufacturer opts to report a pro-

duction of 400 bags officially, concealing the surplus 100 bags, which are then sold at lower prices without tax liability.

This practice generates artificial shortages, prevalent across various industries, including Urea, cigarettes, cement, and sugar, which are also prone to smuggling operations. Recently, the FBR’s customs department intercepted significant quantities of urea and sugar in Balochistan, amounting to a total value of Rs 392 million. Such instances underscore the pervasive nature of underreporting and its ramifications, contributing to an undocumented shadow economy estimated to range between 40-80% of Pakistan’s GDP.

Addressing this issue, the Track and Trace (T&T) system advocates for direct tax collection at the production source. In the case of fertiliser production, for example, the government implemented a T&T system requiring manufacturers to invest in stamping each bag with unique identifiers. These identifiers are scanned upon sale, with data transmitted to the FBR for taxation based on actual production figures.

T&T solutions, commonly utilised globally, aim to streamline tax collection processes. However, the effectiveness of such measures, particularly in industries like fertiliser, cigarettes, cement, and sugar, warrants examination. Has the implementation of the T&T system yielded tangible results, and how have these industries responded to regulatory interventions? These are crucial questions that merit further exploration.

Essentially, the system would fix more than 5 billion stamps on various products at the production stage which was meant to enable the FBR to track goods throughout the supply chain. Essentially, industries would stamp their products right after packaging them and then scan each one before selling it so that the data for production volumes goes directly to the FBR.

The system was first put in place in Pakistan in 2019 and has alluded to a thorough implementation despite the passage of 5 years. The Prime Minister, most recently, had asked an inquiry committee to look into the reasons as to what is the delay. Alongside the Prime Minister has taken part in his fair share of belittling of the system itself. The inquiry committee has come forward with the conclusion that the awarding of a contract worth Rs 25 billion was due to mismanagement by the project director and two former chairmen of the FBR. The answer might suffice for the federal cabinet but in our eyes, it raises more questions than it answers. And this is where the story begins.

Let us start with who this vendor is. When awarding the contract, the FBR took 2 years to decide who the vendor was going to be

This

Track and Trace System is nothing, but a fraud. The TTS was enforced in the PTI tenure. A committee has been formed for the system’s failure

Shehbaz Sharif, Prime Minister of Pakistanand the process which was followed exposes the nature of this problem.

Many, to this day, believe, or are made to believe that track and trace was a project brought about by the Pakistan Tehreek-e-Insaaf (PTI) government. It is also believed that the reason the system could not work is because of the change of governments in 2022 and political vindication of subsequent ruling parties.

However, that is far from the truth. The system was not only a part of the IMF’s reform agenda that Pakistan agreed to for its 22nd IMF program, but was also carried out and sponsored by the World Bank under its Pakistan Raises Revenue (PRR) program.

The backlash from the industry was almost certain when the track and trace started. And that could be seen from the onset of the system. When the FBR released a public notice for a licence that was to be awarded to a vendor who had the requisite technical capabilities, problems started ensuing.

The licensee was supposed to be responsible for end-to-end installation and operation of a Track and Trace System/ Solutions connecting manufacturing sites and import stations to the FBR’s Central Control Room (CCR). Initially the system was to be implemented only on the sale of tobacco.

A total of 13 bids were received for the said vendor by the FBR and upon the criteria set by the FBR, one was chosen to be the licence. The winner of the licence was a consortium of the following four companies. National Radio and Telecommunication Corporation (NRTC), Evolution Track and Trace (Pvt) Ltd, INEXTO (Switzerland), and PERUM PERCETAKAN UANG RI (Indonesia).

However, there was one peculiarity in the process. According to the bid evaluation report, the price offered per 1000 stamps was

taken as the eventual selection criteria. In this, the NRTC consortium had provided a price of Rs 0.731/ 1000 stamps. For context, the next best bid by NIFT was at Rs 868/ 1000 stamps, almost 1200 times more.

The NRTC later contended that the price in its bid was an accidental slip, the real price it wanted to extend was Rs 731/ 1000 tracking stamps. The excuse was hastily admitted and the licence was awarded however, the NIFT consortium, consisting of Opsec Security Limited, Security Papers Limited and Imprensa Nacional-Casa da Moeda, S.A (Portugal), took the matter to court and got the licence set aside.

The Islamabad High Court ruled in favour of NIFT and Authentix, another bidder who had taken the decision of the FBR to the court. Hence a rebidding was in order.

One would think that if a process is done for the second time, it would be done more diligently, however somehow the FBR managed to make it much worse the second time it carried out the bidding.

Upon the completion of evaluation of bids AJCL (Pvt) Ltd got the licence but this time there were more problems. Starting off as a company under the Jaffer group of companies, it was only as late as 2017 that AJCL became a separate company. Even then the directors of the company remain the members of the same family.

AJCL also owned the entire shareholding in AJCL Global Holdings Limited (registered in the United Kingdom) which in turn owned 75% shares in Claiser Trading Limited (registered in the United Kingdom in 2018). Claiser Trading Limited is said to have established an office in

Sharjah, United Arab Emirates (UAE) and was trading under the name of Claiser Trading FZE. Claiser Trading FZE had documented trade ties with the sugar industry in Pakistan.

This obvious conflict of interest was taken to court once again by two of the other bidders because it was against the terms of the Invitation for Licence (IFL). In order to avoid conflict of interest between the licensee and industry sectors of the goods, clause 4.7 of the Invitation for License (IFL) required the bidders to provide a declaration and full disclosure demonstrating that the applicant has no material conflict of interest with the respective four industry sectors of the goods. Apparently upon review of the documents provided by the AJCL, no such conflict was highlighted by the Licensing Committee headed by Karamatullah Khan Chaudhary.

In order to prove this claim against AJCL, two bills of lading dated for consignments of ethanol (a byproduct of sugar) showing Claiser Trading Limited as the consignee and Shakar Ganj Limited, a sugar mill in Pakistan, as the shipper were presented as evidence.

But this is not where it ends. Let us go back to where AJCL comes from. AJCL Pvt Ltd, for the longest time was a family owned business of none other than the famous business family and conglomerate Jaffer group. In 2017, AJCL was declared as a separate business entity with some share of the family still in the business. But more than shares in AJCL, it is a question of influence. The kind of influence on direct or indirect stakeholder can have on such a process. To this day, the members of the board for AJCL are certain members of the Jaffer family.

For readers who do not know, the Jaffer family/group is one of the biggest conglomerates and has a stake in almost every major industry in Pakistan. One might remember the family’s name from a harrowing murder that a member of the family committed in 2021, but the businesses of the family go far beyond any shame that a murder can bring to the family name. For example, in the pretext of track and trace, Jaffer group is directly involved in the construction business with its company Murshid Brothers (Pvt) Ltd making it privy to the cement industry. Jaffer Agro Services, also trades in and supplies fertilisers in large quantities to agricultural clients. Moreover, the group is directly involved in the import of fertilisers within the country.

The link between the companies can also be established from the fact that during the first round the bidder referred to by the name of AJCL was also a consortium between Athentix US, Jaffer Brothers and AJCL. However, when bidding for the second time around, Jaffer Brothers was replaced by MITAS Corporation. Which brings into question the involve-

We as a country have failed to implement the beautiful 18th amendment. The implementation has been slow and weak

Dr Hafiz Pasha, former finance minister

ment of the Jaffer brothers. It was argued that this makes all the bidders questionable. NIFT for example is itself a consortium of six banks, some of which have cement subsidiaries. The argument is fair, yet somehow it does not refute the link and in turn the conflict of interest.

But that is a rather indirect relationship. Reliance IT, one of the petitioners against the award to AJCL, makes the case that AJCL’s own website shows that it has long standing relationships with some of the leading producers of rice, sugar and wheat in Pakistan. AJCL itself admits that it is actively involved in the indenting, import and export of several commodities. The list of its clients includes a few sugar mills. How could the FBR have overlooked that?

The petition by Reliance also pointed towards irregularities in the process of selection of AJCL, it stated that for choosing the firm with the best technical capabilities the FBR was supposed to hire a consultant on the guidelines given by the World Bank. However, the FBR, set aside the World Bank process which involved tender and bidding and unanimously selected one firm for the purpose namely IDECO, a South African Company. The IHC ruling categorically confirms that the appointment of IDECO was not in line with the principles.

Reliance IT, in its petition made the case that the purpose of bringing in IDECO was to select AJCL and it did so by awarding it higher technical points. It is important to note that in the round one of bidding, when IDECO was not the consultant, the technical points given to Reliance were the highest while others closely followed. However, the second evaluation showed that AJCL was leaps and bounds ahead of the others in its technical capabilities. 33 points higher than Reliance (out of total 160) and 22 points higher than the second best

NIFT were awarded to AJCL in the process. This remarkable improvement in AJCL’s technological capabilities over the span of only six to eight months was something that NIFT and Reliance were not buying.

Upon complaint to the Grievance Resolution Committee (GRC) of the Public Procurement Regulatory Authority (PPRA), it was maintained that the criteria to award these marks/points was confidential and could not be revealed.

Another and perhaps the most important contention of all was regarding the Unique Identification Markings (UIM). Readers who have had an experience with tobacco or distribution stage wheat or Sugar might be familiar with a small sticker that has started to appear on cigarette packs and other commodities, ever since track and trace has been put in practice. That sticker in essence, along with other hidden components is known as the UIM.

The clause 3.5 of the IFL provides that the UIMs shall utilise core material which must be made of an anti-tampering substrate so that any attempt to tamper with or to remove a UIM will crumble a portion of the UIM, which will be clearly and immediately recognized. Clause 3.7 listed the minimum security features that the UIMs were required to contain. These security features included one overt material security feature visible by the naked eye and one semi-overt material security feature visible through a simple and very low cost device. Clause 3.9 requires a bidder to provide specimens of these UIMs with details including full description of the security features. IFL requires real-time specimens to be presented with details and full description of the security features to the FBR. According to the IFL, these UIMs were to be given marks out of 30.

In an alarming revelation Reliance stated

that the FBR officials refused to accept the box containing these UIMs along with the application, yet somehow in the evaluation report, they themselves gained 29.3 marks. This meant that the FBR gave them lump sum marks making the whole marking process contentious.

Since the account of events quoted by Reliance went against the IFL. The exact reason for which the first round of bids was aborted. Surprisingly, during the court proceedings, the FBR conceded that it did not actually collect the samples from 3 other bidders due to late submission on account of interference by costume (Reliance had to import its stamps).

There is also a comic value to the fact that the customs seizure lasted up until the day of submission deadline after which the stamps were released. But how did FBR give points? It was stated that the samples were not of as much “paramount importance” but rather the evaluation framework upon which the overt and semi-overt features worked.

Coincidentally, AJCL’s stamps were not seized by the costume authorities and were released well before the deadline granting them the most marks. Despite having violated the terms of the IFL, and admitting to violating these terms, the IHC ruling remained in favour of the FBR.

In fact, despite some serious allegations against AJCL, both the petitions were dismissed by the IHC due to lack of evidence. It was also noted by the IHC that since the petition filed was against the Grievance Resolution Committee, and its oversight in responding to the complaints of the petitioners, the court did not find the GRC guilty of doing that. Whether the awarding of licence to AJCL was justified, or hiring of IDECO as the consultant to evaluate the bidding process was legal are entirely different cases.

Profit also found out that an appeal against the judgement was filed in the Supreme Court of Pakistan, a short time after the judgement. To this day, not a single hearing has taken place on the matter. Hence, AJCL got the licence of installing and operating the track and trace system for Tobacco, Cement, Sugar and Fertiliser industry.

One of the main reasons that the FBR gave for expediting the process, in bypassing due procedure for bringing in a consultant and denying complaints by competent bidders, was the urgency with which Pakistan had to put the track and trace system into place.

The FBR maintained that the IMF wanted this system in place before June 2020 but due to the COVID-19 pandemic, the IMF had

relaxed the deadline till June 2021. Since both these cases were heard very close to the provided deadline, sources close to the development believe that Pakistan could not have afforded a renewed bidding process, in fact that is the very reason for which no follow up cases had been filed.

Anyhow, with all its question marks and flaws, the system was put into effect by the AJCL consortium. But it became very clear right away that making the system operational as quickly as possible was never FBR’s priority. The board wanted the nod from the IMF for its review back in the day and once it got that nod, the track and trace was at the mercy of the wind.

The system faced quite a backlash when it was put in place. Pakistani producers are not in the habit of sharing their numbers and when someone asks them to do it, they are defensive.

An incident of dispute occurred with Khyber Tobacco. The AJCL consortium found itself in dispute with Khyber Tobacco over who would pay for the adhesive in the stamp, and the release of a large consignment before implementing the TTS. A case that was later set aside by the IHC since the IFL clearly made it the licensee’s responsibility.

But it became clear that the lack of quality in the adhesive material ingrained in the UIMs provided by the AJCL was going to cause problems especially in the sugar and fertiliser industry. It was found that the specifications of adhesive material as specified in the IFL were not met and stickiness to polymer bags was a bone of contention.

FBR in its directions clearly stated that the tax stamp needs to be applied on the surface of the product in a location that is most accessible based upon the presentation of the bags to the applicator.

On the other hand, manufacturers also need to provide high speed internet connectivity so that once a stamp is scanned the data goes directly to the board. This then also requires a suitable location for the installation of equipment, an isolated power terminal point of 220v 15 Amp and floor space for the Unique Identifying Mark applicator that is used to put the stamps on. And the industry which already needed an excuse to not have its production traced would never go out of their way to install a stamp that was faulty.

Viral videos on social media platforms have also made the case for the questions raised on the TTS. Videos with gentlemen placing fake UIMs on counterfeit cigarette packs with the help of their saliva bring into question not only the licensee but the authority (FBR) responsible to carry out this tracking and tracing. Is the industry investing in a flawed technology altogether?

In November 2022, the fertiliser sector

banded together to complain about problems with the stamp system. In a letter to Federal Finance Minister Ishaq Dar and Chairman FBR Asim Ahmad, fertiliser manufacturers of Pakistan Advisory Council (FMPAC) claimed that the technology being used by the FBR (which the board had strongly armed the industry into investing in) did not work. They claimed, for example, that less than half of the stamps actually scanned even though the scanning efficiency was supposed to be 99%.

According to media reports, one of the proposals put forward by the cabinet inquiry committee is to terminate the licence of the vendor AJCL and bring a new “world class” vendor with the requisite technological expertise. Infact AJCL itself employs the services of Authentix a US based company, specialising in these services.

It is important to note that of the initial 13 bidders, almost all had the services of a foreign company except for NRTC, which was using the technological expertise of SEPL, a state owned enterprise. The question is, how will this hypothetical world class vendor be selected?

It appears that after wasting a vast amount of industry and World Bank money, Pakistan is back to square one in its implementation of the track and trace system.

Our story about Track and Trace is pretty much over. And this is once again an example of Profit beating the same drum it always does time and again, but it is important to make this point in this problem.

Scheme like Track and Trace will never be the most effective solution to Pakistan’s taxation problems precisely because they do not address the core problems in our taxation philosophy.

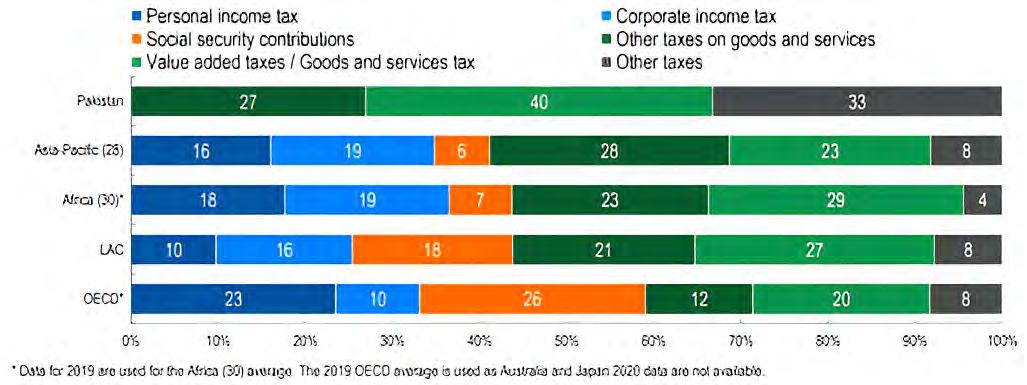

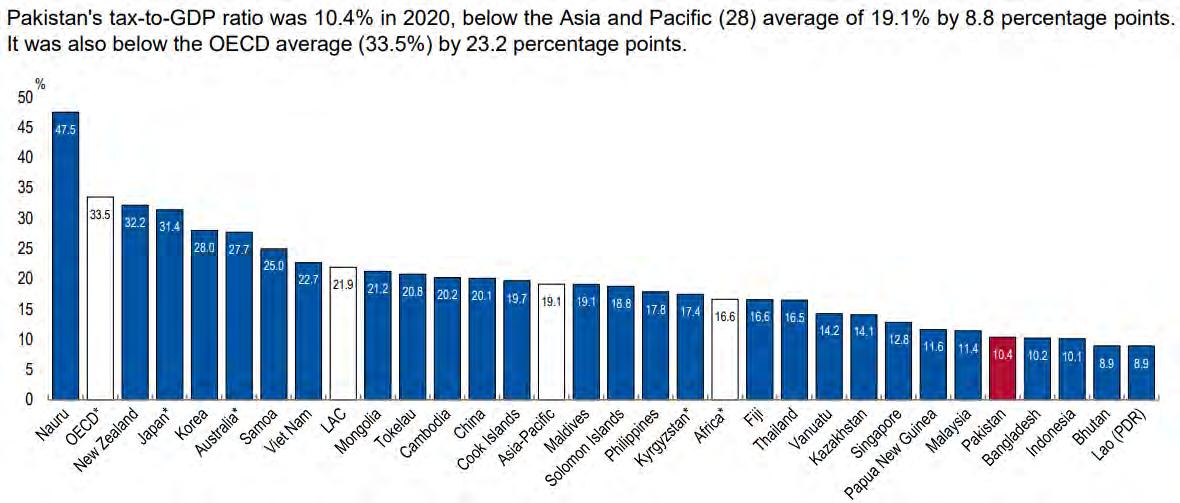

The real problem is that Pakistanis are taxed unfairly and those that should be paying the lion’s share end up paying nothing. Just take a look at Pakistan’s tax structure. Tax structure refers to the share of each tax in total tax revenues. The highest share of tax revenues in Pakistan in 2020 was derived from value added taxes / goods and services tax (39.8%). The second-highest share of tax revenues in 2020 was derived from other taxes (33.3%).

In comparison to Pakistan, countries in the Asia-Pacific region only collect about 23% of their taxation from goods and services taxes — meaning Pakistan’s average is almost double. Why is this the case? The biggest reason of course is that taxation in the country is centralised. The FBR collects almost all taxes (even the ones that should be collected by

provinces under the 18th amendment) and then those collections are then given to the provinces in the form of the NFC award leaving the federal government with very little spending money. In an earlier interview former Finance Minister Dr. Hafiz Pasha, while talking to Profit, lamented that, “We as a country have failed to implement the beautiful 18th amendment. The implementation has been slow and weak.”

Since the share of the provincial governments, under the NFC awards, over the last few years has been increased from 40% to around 57%, it has provided the provinces with very little incentive to develop their own revenue sources. Despite having access to the two biggest cash cows, services and agriculture, the share of provincial tax revenue is close to 1% of the GDP. “You would be surprised to know that the corresponding number for Indian provinces is around 6% of the GDP, with similar fiscal powers,” says Dr. Pasha.

The solution of course is right in front of us: devolution. More than just being a third tier of democracy, having a local bodies system

means having a new economic process. In essence, it is not just a new administrative stratification, but also involves the dispensation and spending of money. Things such as education and health that people automatically look towards the provincial government for would now be handled by local representatives. Perhaps most crucially, the ability of local governments to collect taxes and release their own schedule of taxation allows them to make their own money and spend it on themselves

rather than waiting for the benevolence of the provincial or federal government.

Of course, devolution to local governments is still a long way away. In the meantime, the Track and Trace system needs to be better implemented with proper feasibility studies before tech is brought into the country. Otherwise this will be another in a long list of failures where the state will be unable to improve our tax collection mechanisms and widen the cast of its net. n

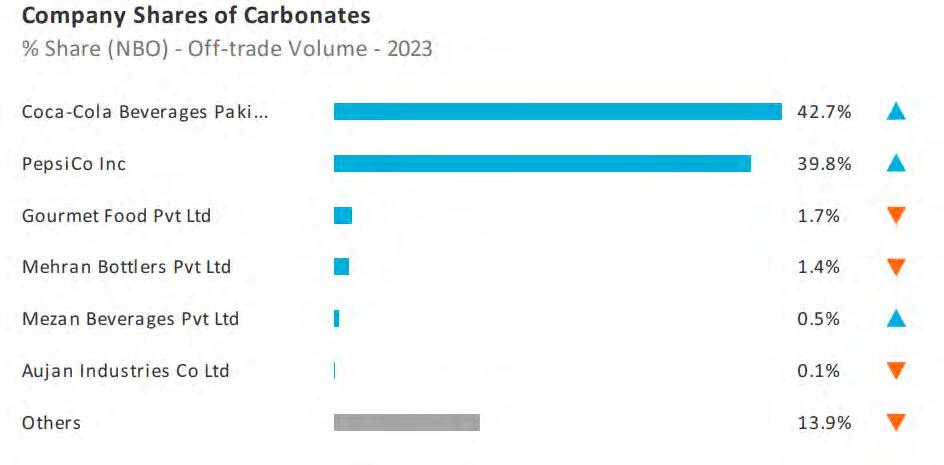

There has been a major change in Pakistan’s carbonated drinks industry. In the year 2023, Coca Cola was the most sold carbonated drink in the country. Just over 451 million litres of Coke were sold in the last calendar year.

This beat out Pepsi, once the biggest carbonated drink in Pakistan, which sold just over 372 million litres in 2023. This is seemingly a major shift in consumer preference. Besides the flagship products, Coca Cola also had the bigger share of the overall carbonated drinks market.

Of the overall 1.33 billion litres of carbonated drinks sold in Pakistan last year, including all of the other brands these two companies operate such as 7Up and Sprite, Coke Pakistan had a market share of 42.7%, while Pepsico was close behind with 39.8%.

But even though Coke Pakistan technically has more sales than Pepsico in the carbonate beverages department, Pepsico is well ahead of Coke off the back of one single product.

Sting.

Pepsico launched the iconic energy drink in Pakistan back in 2010. Since it is considered an energy drink, or a “stimulant drink” as it is legally labelled in Punjab, it falls under a separate category of product entirely. Over the years it has become abundantly clear that Sting’s competition is not Redbull or other canned energy drinks with ginseng (the product present in most energy drinks), but rather Coca Cola and Pepsi.

In the 14 years since it has been around, Sting has become the fourth largest drink in Pakistan after Coca Cola, Pepsi and 7Up. And it is fast catching up with 7Up. This means it sells more than Sprite, Mirinda, Mountain Dew, and Fanta. In fact, according to the sales numbers available for 2023, Sting has sold more litres than Mountain Dew and Fanta combined.

This is all despite the fact that Sting does not (yet) come in packaging of over 500ml. Currently, this 500ml litre bottle of Sting costs Rs 100. Its competitors like Fanta, Mountain Dew, Sprite, 7Up all come in packaging of 1 litre, 1.5 litre, and in some cases even 2.25 litres and are cheaper per litre in larger packaging. These drinks are also more in demand because they are served at weddings, corporate events, and other such gatherings. Sting is not a drink of choice for such occasions.

This presents us with a unique situation. It means Sting, despite billing itself as an energy drink, is directly in competition

with carbonated drinks such as Coca Cola and Pepsi. Whatever it may claim, Sting also looks, tastes, and behaves more like a carbonated drink than an energy drink. But food and health authorities treat it as an energy drink, which can often mean regulatory scrutiny. But it seems the marketing benefit of Sting being labelled an energy drink is well worth it to Pepsico. After all, it is keeping them ahead of the competition.

So how do we get to the bottom of the Sting miracle? Easy, we start at the beginning and move on to the numbers.

There isn’t really any major competition to Coca Cola and Pepsi. Sure, there are a few anomalies in the world where local brands compete with the two multinationals. In fact, Peru is possibly the only country in the world where a local soda seller, Inca Cola, outsells both Coca Cola and Pepsi. But these are all outliers. Everywhere in the world the market for carbonated drinks is almost evenly split between these two Global Giants.

Pakistan is no exception. Coca Cola first hit the Pakistani market way back in 1953. Pepsi followed not long after. The logic from the global headquarters of both Coke and Pepsico is simple. Since they are each other’s eternal competition, wherever one goes the other follows. Whatever pricing strategy one follows the other copies. However much one spends on marketing, the other tries to one-up. Wherever there is Coca Cola, there must be Pepsi.

And sure, both companies have a whole host of other products too. Mirinda and Fanta in the orange soda category, and Sprite and 7Up in the lemon soda category are the most recognizable brands. But the main event is always between Pepsi and Coca Cola. In Pakistan, Pepsi has almost always had a bit of an edge. Regional preferences within the country have differed for long periods also because of the supply lines that the companies maintain.

Coca Cola has significant presence in Punjab and Khyber Pakhtunkhwa, while Pepsi has a strong foothold in Sindh, particularly off the back of the success that has been found by their Pakistan Beverages Limited franchise in Karachi. This is because Coca Cola has five out of six of its production facilities in these provinces while the sixth and smallest is in Karachi,Sindh. Pepsico, on the other hand, has significant production facilities in Karachi. As per a report seen by Profit, Pepsico generally partners with one distributor per city, while Coke Pakistan has multiple distribution partners within a city, with areas divided according to sales volume.

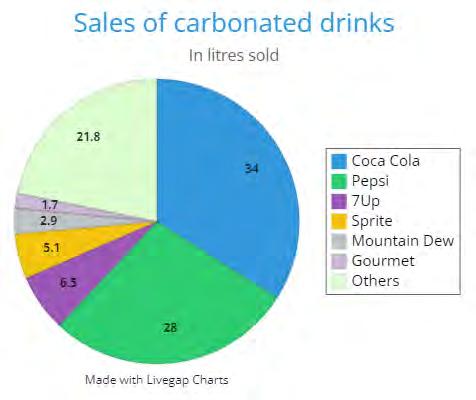

So how has this global rivalry played out in Pakistan? According to the latest market data analysis by Euromonitor, there were 1.329 billion litres of carbonated drinks sold in Pakistan in 2023. This includes all products by Coke Pakistan and Pepsico as well as local competitors such as Gourmet Cola, Cola Next, Sufi, and others. This is actually a rare year in which the overall sales volumes of carbonated drinks have fallen. In 2022, the total sales volume of carbonated drinks was 1.38 billion litres, which indicates a 4% decrease. What is interesting is that carbonated drinks have seen consistently increasing sales volumes (around 18% annually) in at least the last 15 years for which accurate data is available.

The leading company in this entire mix was Coke Pakistan, which sold nearly 567.5

million litres of carbonated drinks. The biggest component of this was 451 million litres of Coca Cola, which makes up around 80% of the overall sales that Coke Pakistan made in 2023. Of the remaining 20%, over 11% (around 68 million litres) was made up by sales of Sprite, and the remaining 9% was made up of their other products including Mirinda, Coca Cola Light, and Sprite Zero.

Pepsico sold just over 528 million litres of carbonated drink, giving them a total market share of 39.2% compared to Coke’s 42.7%. The breakup of their sales shows that Pepsi was their hottest seller at around 70% of their total sales.Their second biggest seller was 7Up, which sold over 86 million litres making up 16% of their total sales. The remainder of the 14% of sales were made up by Fanta, Mountain Dew, Pepsi Black, and 7Up Sugar Free.

Sale of carbonated drinks

Overall sales

1.329

86 million litres

68

38.5 million litres

22.5 million litres

22.5 million litres

Others

268 million litres

This actually paints a very interesting picture of the two companies. Coke Pakistan has clearly outdone Pepsico when it comes to selling cola, the flagship product of both companies. But Pepsico has done a better job at selling their other products such as 7Up. This is despite the fact that 7Up is sold mostly in 500ml packaging and Sprite dominates the 1.5 litre packaging. Similarly, Pepsico is also ahead of Coke Pakistan in the sale of Fanta, which outsells Mirinda by nearly 25%. On top of this, Pepsico has a more diverse profile of products. One of the reasons for the relative success of the Fanta in 2023 was the decision to reintroduce Fanta’s Red Apple flavour. Coke Pakistan has not introduced any similar products even though there is a market for it as has been proven by Murree Brewery, which has its “Big Apple” as one of its most iconic non-alcoholic products. Pepsico also produces and sells Mountain Dew, for which Coke Pakistan doesn’t offer a clear alternative.

Despite this, as we’ve seen earlier, Coke Pakistan has managed to outsell Pepsico off the back of Coca Cola outperforming Pepsi. Pepsico has managed to close some of this gap through its other products. The percentage gap between the drinks Coca Cola and Pepsi is 6%, but the overall difference in sales for all products is just under 3%.

So how did Coke Pakistan manage to pull this off? For many years Pepsico’s Pepsi was far ahead of Coca Cola. Over the past decade or so, Coke Pakistan has been making a slow but steady comeback. One of the possible reasons is that Coca Cola was not the preferred taste for most consumers. Pepsi has always been known as the sweeter drink. And even though Coca Cola has been preferred more globally, Pakistani preferences leaned towards the sweeter Pepsi. One explanation from insider sources in Pepsico has been that Pakistani tastebuds have become aligned with the global trends. In fact, that is why Pepsico

has introduced a new combination of Pepsi that they’re marketing as stronger and more fizzy. The new formula was previously being used in the UAE, and Pepsico is clearly trying to fight back against Coca Cola’s encroachment on their once strongly held market.

And while Pepsico is fighting back, there is on difference. On the surface Coke Pakistan has outsold Pepsico in 2023. But the data we have presented to you is for carbonated drinks in Pakistan. It shows that Coke Pakistan is on top but just barely, and Pepsico has a more diverse portfolio. But this just tells us how these companies are competing with each other in this one category. They have other competing business interests too. For example, Coca Cola sells mineral water under the brand name Dasani and Pepsico sells mineral water under the brand name Aquafina. But in the water segment, their competition is not just each other but other players like Nestle, Sufi, Murree, and Gourmet. Similarly, Pepsico has a very robust snacks segment with their signature Lays brand - something that Coke Pakistan does not have or compete with Pepsico in.

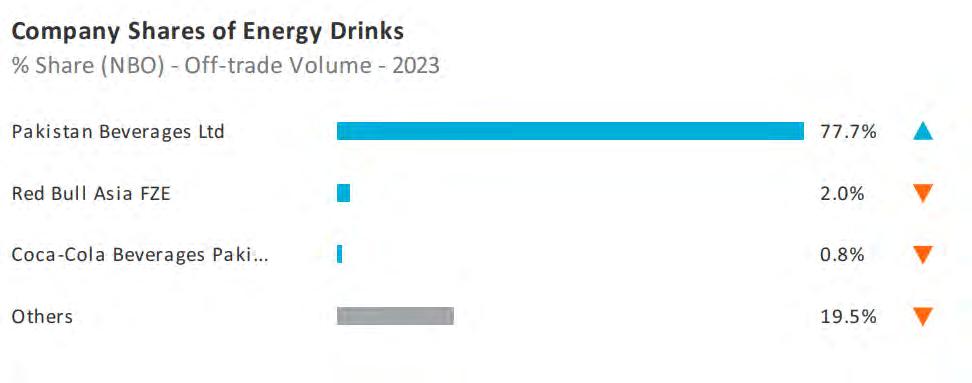

But there is one other segment that is comparable. Not only is this segment one where they are direct competitors, but it is very similar to the carbonated beverages segment. And in this particular segment Pepsico is ahead of Coke Pakistan. Well ahead actually. So much so that they hold more than three quarters of the market share while Coke Pakistan is lagging behind with less than one whole of the market share. The segment is quite small compared to carbonated beverages, but Pepsico’s lead is enough that it tips the overall scales in favour of Pepsico. In fact, we would argue that this segment should probably be lumped in together with carbonated beverages in the first place. The sector in question, of course, is energy drinks.

This is where things get really interesting. You see for better or for worse, energy drinks are a separate category in the corporate sector. They are distinct from carbonated drinks.

Both products contain many common ingredients. Water, sugar, acidifiers, flavouring, and carbonation exist in both soft drinks and in energy drinks. But energy drinks often contain higher quantities of caffeine as well as additional ingredients such as taurine (an amino acid meant to give the body a quick boost) or ginseng (a root indigenous to Asia which reduces fatigue and allows those consuming it to stay alert longer).

It is taurine and ginseng which gives energy drinks their taste. In Pakistan, the concept of energy drinks was not new. Red Bull had been around, at least as an imported product, since the early 2000s. Red Bull officially launched their product in Pakistan in 2001, and much like elsewhere in the world, the concept of energy drinks was synonymous with Red Bull.

Now, Red Bull stood out amongst the existing carbonated drinks options. For starters, it only came in a can. It wasn’t crafted to taste appealing but rather to provide a hit - in a way similar to how coffee is an acquired taste. It was also significantly more expensive, and its marketing promoted the product as an energy boost that could be used by students, professionals, and athletes.

For nearly a decade, this was Pakistan’s only energy drink of any note. That is until 2010, when Pepsico launched a massive campaign for Sting. They billed this new product

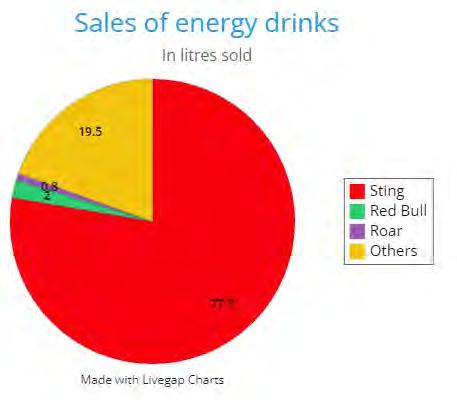

Sale of energy drinks

Overall sales

100 million litres Sting

77.7 million litres

2 million litres Roar

800,000 litres

Others

19.5 million litres

as an energy drink. But it was very different from Red Bull. For starters, Sting would not come in expensive canned packaging. It would be bottled in 500ml plastic bottles. It was also introduced in a shocking red and gold colour, with flavours called “Berry Blast” and “Gold Rush” (even though they would colloquially come to be known as “red wali aur yellow wali).

Even though Sting was supposed to be an energy drink, it appeared to be more like a new kind of soft drink being introduced by Pepsico. The colours were attractive, and the mass marketing campaign promoted it as a tasty alternative to other energy drinks such as Red Bull. What’s more, it was also significantly cheaper. Pepsico actually marketed Sting brilliantly. They made it into a perfect blend of energy and soft drink. A big part of this was their recipe. Rather than focus on ginseng and taurine, they pumped Sting full of extra sugar as food authority studies would go to show years later. The drink became a staple particularly at khokhas and kiryana stores. The introduction of the glass disposable bottle made it a regular haunt particularly for young boys smoking next to different corner shops. And since it was heavily marketed as an energy drink, it was a cheap alternative to the four times more expensive Red Bull which came in a 350ml can only.

The results are quite obvious. The market for energy drinks is not particularly large in Pakistan. Whereas the total volume of carbonated drinks was 1.32 billion litres in 2023, the total volume of energy drinks sold in the country was around 100 million litres - less than a 10th of the carbonated drinks market. Now, this is a mere 100 million litres. But the difference between Coke Pakistan and Pepsico’s overall sales in 2023 was just under 40 million litres. And by dominating the energy drinks space with what is a glorified carbonated soft drink, Sting has managed to keep Pepsico on top.

Of the 100 million litres sold, Sting had a massive market share of 77.7 percent,

meaning they sold 77.7 million litres of Sting. Coke Pakistan also has a direct stake in all of this. Noticing the massive ground Sting had gained since 2010, Coke introduced Roar in 2019 with a shabang. This was a product like Sting. It was technically an energy drink but didn’t taste like one. But the product was not liked. Most people thought this was Coke’s answer to Mountain Dew, not Sting, and Roar never managed to establish itself as an “energy drink.” As a result their sales have been awfully low. In 2023 they only had 0.8% of the market share, which in turn means they sold only 8 lakh litres of Roar. Roar also only comes in packaging of 500ml, which means overall they sold around 16 lakh bottles of the drink. Compare this with Sting. Now, Sting comes in three different packings. A 250ml can, a 300 ml bottle, a 500ml bottle, and a disposable glass bottle. We unfortunately do not have the breakdown of which kind of packing sold in what numbers. But the most economical packing is the 500ml original bottle. It is priced at Rs 100 and that gives a per litre cost of Rs 200. If you assume that only 500ml bottles were sold, it will give us the minimum retail sales figure for Sting in Pakistan. The amount comes out to Rs 15.54 billion. In comparison, the total retail sale figure for Roar all over Pakistan in 2023 was Rs 16 crore. That means Pepsico sold Rs 1500 crore worth of its energy drinks, while Coke only managed to sell Rs 16 crore. This vast discrepancy means Coke has some serious introspection to do in terms of its Roar product.

Because of this massive gap, if Roar and Sting are counted as carbonated drinks (which they very much also are), then Pepsico’s overall sales surpass Coke. If these two drinks are included, then Pepsico sold 605.7 million litres of their drinks. In comparison, Coke Pakistan only sold 568.4 million litres of their drinks. And if we combine these two markets, that means Pepsico is the overall leader with a 42.3% market share.

Of course, this would add another play -

er in the carbonated beverages market: Red Bull. The iconic energy drink is second on the list of market leaders in the energy drinks segment. However, they are a very, very distant second with a market share of 2%. While that is more than double the market share of Roar, it is still ridiculously less than the hold Sting has on the market. Red Bull, of course, is significantly more expensive. A single can of Red Bull costs nearly Rs 500 and contains 250ml. This means Red Bull has a per litre cost of Rs 2000. With a 2% market share, Red Bull sold 2 million litres or somewhere around 80 lakh cans. This would give them a total retail revenue of somewhere around Rs 4 billion. While this is pretty high, it is less than a third of our minimum total retail revenue estimated for Sting.

This makes it very clear Sting is in a category in and of its own. Just look at it this way. In comparison to Sting, Sprite, which is Coke’s second biggest brand, sold just over 67 million litres, which is 10 million litres less than Sting.

We have a very clear conclusion here. Coca Cola has performed better than Pepsi last year, and because of that Coke Pakistan has technically beaten out Pepsico in the carbonated drinks section. But Sting, which should rightfully be in that segment, has put Pepsico ahead of Coke for all intents and purposes. And it is also clearly competing not with other energy drinks but rather with traditional soft drinks.

Why then is this an energy drink? Well, on the one hand Pepsico has clearly managed

to use the branding and marketing of Sting as an energy drink to great effect. But this also comes with its dangers.

Regulatory dangers.

Just take a glance back to 2018. Back then the government of Punjab ordered energy-drink manufacturers including Red Bull to remove the word “energy” from their labels, saying it is scientifically misleading and encourages a population unaware of the beverages’ contents to guzzle them in potentially dangerous quantities. The order comes amid an international regulatory pushback against the highly caffeinated fizzy drink market, and is believed to be the first in the world to censor the term “energy” – a key part of the drinks’ appeal.

As a report by The Guardian noted, the scientific advisory panel of the Punjab Food Authority said rather than provide the body with nutritional energy, the large quantities of caffeine, taurine and guarana contained in energy-drinks simply stimulate the swift release of existing reserves.

Under the PFA’s order, makers of energy drinks have until the end of the year to replace the word “energy” with “stimulant” on their labels, and add a series of warnings in Urdu, the national language, against consumption by pregnant women and children under the age of 12. The PFA has also demanded that energy drink manufacturers, who sell about 312m cans each year in Punjab, must limit caffeine to 200 parts per million (ppm), about half the amount that Red Bull currently contains.

The move to have these drinks relabeled and not associated with the word energy came as the result of serious lobbying. According to some, the move was in part orchestrated by Coke, which sought to curb the

success of Sting. But despite this, Sting kept selling, which is why Roar was introduced a year later in 2019 when it became apparent changing the label was not going to have an effect.

Profit is in a tricky situation doing this story. The tricky situation is that the latest date we have available is from 2023. Now, normally this data would be recent enough. Especially since we are only a few months into 2024. The only problem is that a major shift has occurred on the carbonate market since October 2023.

As a result of the genocidal actions of the Israeli entity in Gaza and the Occupied West Bank, many in Pakistan have chosen to boycott MNCs like Coke and Pepsico. As a result, initial reports are emerging that there will be a further dip in the amount that these MNCs are able to sell in Pakistan.

This may mark a watershed moment. Remember, there are other local makers of energy drinks that make up for nearly 20 million of the litres of energy drinks sold in Pakistan. Even in the carbonate drink segment, brands like Gourmet, Sufi, and Mehran Brothers have a 5-6% share of the market. This is likely to grow.

Over the past decade, Sting has made its presence known in Pakistan. It has muscled its way into the market, become a contender for the third largest drink in the country, and has single handedly kept Pespsico ahead of CokePakistan in overall sales volumes. If there was ever a moment for local non-MNCs to step up and possibly muscle their own way into the segment. n

Mr. Rehmat Ali Hasnie, President National Bank of Pakistan (NBP), inaugurated the newly renovated Main Branch in Multan. Staff members, regional officials, and guests attended the inauguration ceremony. Mr. Hasnie extended his heartfelt congratulations to all contributors to the renovation project, with special recognition given to Mr. Imran Gul, the General Manager of Southern Punjab, and Mr. Aurangzeb Ahmed Shaikh, the Group Head, Engineering for their exceptional dedication and leadership. During the event, NBP president expressed genuine appreciation for the hard work and commitment of the bank’s staff. He also engaged with junior staff members and took keen interest in the first login case of Solar Finance.

Inflation has meant lots of changes in all segments including transport. Careem is responding through their pricingBy Nisma Riaz

A lot has happened at Careem recently. Uber, which had acquired Careem Rides for $3.1 billion in 2019, recently exited the Pakistani market. Even though this does not change a lot for Careem Pakistan and its operations, it did garner attention in the news.

Another recent event at Careem was their new, and perhaps belated, flexible fare offering. It has been a few months since the new offering was launched and Profit was interested in finding how the bidding model is working out for Careem.

And lastly, we wanted to verify whether the claim that Careem is too expensive, compared to other apps, holds any truth to it.

Profit explores.

Surprisingly, it was the pioneer of ride hailing in Pakistan that was the last one to introduce a bidding model for its customers. Previously, Careem only offered a marketplace variable fare model for pricing, whereby neither Careem’s captains, nor its customers had any control over the fares they paid. But was it the fear of missing out or something else that made Careem introduce its new Flexi Ride offering?

According to Careem Pakistan’s Country General Manager (GM) Muhammad Imran Saleem, the decision had to do with the very premise of why the company operates in Pakistan. “The decision to introduce Flexi Rides had to do with Careem’s heavy sell on being localised and addressing the needs of the market. We’ve spent almost a decade setting this industry up, experimenting with a lot of different things along the way. It’s a very different Careem than what it was two to four years ago,” Salem stated.

He believes that the company’s evolution

has been an ongoing process and over the course of the last few years, one thing that became very apparent was that the purchasing patterns and the economic situation have changed drastically. “The changing costs of owning and maintaining a car, fuel prices, and the overall condition of the transport infrastructure in the country had a big role to play in the decision, along with the purchasing power of course,” he explained.

Continuing the same point, Saleem relayed, “The positioning of Careem historically has been that we place ourselves at a premium. We want to provide an exceptional experience, which we couple with safety and support. However, we came to the realisation that there is a big segment of the market that requires a little bit more in terms of value for money, which wasn’t something that we indulged in, in the beginning.”

Eventually, Careem realised that there is a demand for a product that offers better value for money, allowing all stakeholders to be a little bit more flexible than their previous offering. And as with any type of organisation, evolution becomes very important. “The decision to include this feature wasn’t made just a few weeks before launch. It involved extensive software development over a period of about a year and a half. Even after launching it, we’re constantly refining the product based on ongoing learning. We initially rolled it out in smaller cities before expanding, recognizing that each city has its unique dynamics,” Saleem concluded.

Since this was not a new feature in the market, Profit was curious how Careem’s stakeholder responded to Flexi’s phased launch.

Saleem informed, “So there are several facets of the offerings that we have. Of course, there is the hailables offering, the motorbikes and the rickshaws, and then we have small cars with AC, small cars without AC and then premium cars, as well. So we launched Flexi in a couple of, what we refer to, tier two cities, which are smaller cities– Multan and Faisala-

bad. However, these are still huge markets.”

Saleem said that they observed a good response with the initial launch and the premise of introducing it in smaller cities was to give the company a chance to figure out the user interface and user experience. They conducted A-B testing in Faisalabad and Multan to determine optimal button placement, text, and pricing methods. Based on the findings, Flexi was launched in two variants, Flexi Air Condition and Flexi Mini, in Islamabad and Rawalpindi, catering to different consumer preferences and budgets to test what worked best.

He divulged an interesting finding here, “The combination of both Flexi AC and non-AC rides revealed a preference among customers for the non-AC option, highlighting an important insight. To cater to those seeking greater value with reduced prices, particularly those uninterested in air-conditioned rides, we initially introduced a non-AC mini product exclusively in Lahore.”

When inquired about the adoption rate of the new bidding model, Saleem shared, “So in Lahore, when you want a Flexi ride, you’ll be able to get one without air conditioning and the results of this feature were immediate. I’d say 80% of the people or more, who were actually using the mini product at a marketplace level, were now actually diverting and using the Flexi model.”

In the initial weeks, adoption of the product increased gradually over time through marketing and incentives, particularly for the low-value non-AC option. Customers experimented with it alongside the previous product, indicating a fluid usage pattern where they alternated between the two offerings.

Saleem also told us that even customers who typically used cars with AC shifted to the non-AC option during certain times, such as mornings and evenings in the colder months, appreciating its affordability. However, they still had the flexibility to opt for air-conditioned

rides during hotter afternoons,justifying why the company kept both models operational. “The core principle remains empowering both captains and customers to make their own choices, leveraging their extensive experience with ride-hailing services,” he said.

Well, this reflects that the reception of the new offering was positive among Careem’s customers, but what about the other most important stakeholder?

We asked Saleem about some major concerns raised by Captains, pertaining to both pricing models.

He answered, saying that, “Captains prefer the flexibility to switch between models based on different cycles within the month. The traditional marketplace model offers higher commissions along with bonuses for ride volume, like receiving additional earnings for completing a set number of rides, albeit with a higher commission rate of around 15% plus tax. This contrasts with the Flexi model, which offers lower commission levels and lacks similar bonuses. This preference for flexibility reflects a shift in the mindset of captains, who appreciate the ability to choose between models based on their earning goals and circumstances.”

He informed that In the alternative model, captains are charged a 5% commission with no bonuses attached, presenting distinct nuances. Full-time drivers meeting their targets can switch to this model for lower commission rates. Part-time drivers, like office commuters, find it advantageous due to lower commissions and absence of trip targets. Captains appreciate the flexibility of alternating between models, which is why we have this mechanism in place.

The commissions, 5% for Flexi model and 15% for the regular model, are exclusive of taxes. Saleem shared that taxes vary by province, ranging from 4% to 5%. Islamabad, as a central territory, has no tax, while Sindh has 4% and Punjab has 5%.

Profit learnt that Careem conducted rigorous educational efforts for captains through various communication channels and training sessions for its Captains, familiarising them with the new tool.

One issue that captains had with Flexi was the constant vigilance required to combat competition dynamics, prompting the need for a flexible model allowing captains to opt out of actively selecting rides. Concerns regarding potential earnings impact due to customer-set pricing were addressed by introducing a lower commission rate for the Flexi model, ensuring profitability as well.

In contrast, the traditional marketplace model faced criticism for its lack of flexibility in ride assignments, which the Flexi model aimed to alleviate by offering more freedom in choosing destinations. While some technological features allowed captains to set preferences for ride locations, these were restricted to certain times to maintain overall service availability. Despite initial challenges and earning concerns, the introduction of the Flexi model aimed to provide captains with greater autonomy and address customer demands for flexibility, ultimately contributing to a more dynamic and responsive ride-hailing ecosystem, according to Saleem.

Pricing is perhaps the most important aspect for users of ride hailing apps. A slight fluctuation can make customers switch to a competitor app.

Profit asked Saleem how exactly Careem positions itself in the market, especially with rising competition, especially with recent entrants like Yango that offer extremely low fares?

He said, “Pricing dynamically adjusts based on trip variables.The system learns market demand and supply, employing basic economic principles to maintain equilibrium. It determines pricing to address imbalances, attracting more captains to areas of high demand by raising prices and adjusting prices downwards where supply exceeds demand. This

adaptive strategy, developed over many years in Pakistan, reflects our deep understanding of pricing dynamics.”

He also insisted that Careem is in fact not as expensive as the general perception goes, adding that the fares are determined in a way that neither party is exploited.

We also asked Saleem how the captains feel about Careem’s pricing strategy, since competitors such as Yango do not display the fares before a ride starts, taking all control away from their drivers.

Saleem said, “Of course, our captains have a basic understanding, but we take it further by educating them on fare calculations. Captains are aware of the base minimum fare and earn a set amount per kilometre travelled and per hour or minute spent in the ride. Each trip’s variability is acknowledged; while we provide an initial fare estimate, the actual fare may differ due to factors like traffic or route changes, a feature captains appreciate. For example, if a trip is agreed upon at 300 rupees and encounters extensive traffic, the fare remains 300 for the customer, but the captain’s costs increase significantly. This transparency distinguishes our pricing model from competitors, as we provide not just estimates but also a comprehensive breakdown before the trip, empowering captains to anticipate potential earnings based on trip parameters. Captains understand that a trip’s distance and traffic conditions directly impact their earnings, allowing them to make informed decisions about accepting rides.”

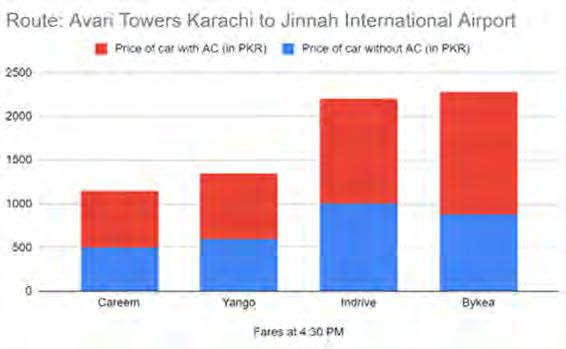

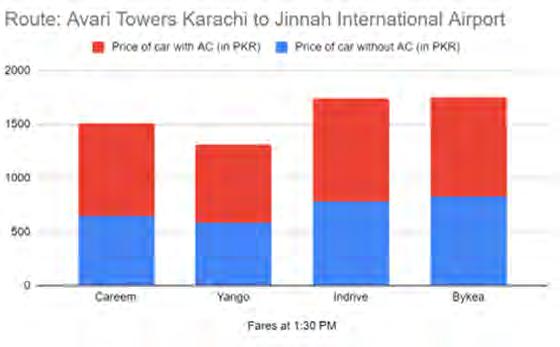

Profit engaged in a comparative exercise to determine whether Careem is the most expensive ride hailing app in Pakistan or is this belief in fact a false one. We selected a 16.5 kilometre route in Karachi from Avari Towers to the Jinnah International Airport at two different times of the day. We included two types of rides, AC and non-AC.

The results revealed that during peak hours (4:30 PM), Bykea and InDrive offered the most expensive rides in both car categories.

The same two companies were also the most expensive during non-peak hours.

Yango offered the cheapest rides, howev-

er, based on the review of 20 frequent users of ride hailing applications, the low price was not worth “the horrendous travel experience”. All 20 users agreed that they valued their safety and time significantly more than the few hundred rupees they would save with Yango.

The numbers show that Careem has actually managed to strike a balance between too high and too low fares, offering an acceptable rate to customers, while making sure that drivers are not taking cuts in their earnings.

Profit also calculated the estimated fuel cost of going from Avari Towers to the airport in different cars that are most commonly driven by ride-hailing drivers. The average fuel cost ranges from Rs 250 to Rs 476, depending on the car and model.

Even with bigger cars like a Toyota Corolla, the fuel cost does not exceed Rs 500. You will not get this rate even on the cheapest non-AC car if you opt to use a ride hailing service. However, it is understandable that the fares will be higher than the minimum fuel cost of travelling, considering that along with driver’s cuts, the companies also need to make profits.

When ride hailing first became a thing in Pakistan, commuters did not have many options.

They could only choose between Careem and Uber’s very similar offerings. However, as the sector developed, several other players entered the market. Both local and international ones. With Bykea’s strong delivery presence and InDrive’s global experience, one would imagine that things got a little difficult for Careem.

We asked Saleem to share how Careem deals with the market getting saturated by the minute.

He said he wanted to address this question from an industry standpoint rather than as someone associated with Careem. “In my view, having multiple options available in the market is beneficial for several reasons. Firstly, it fosters healthy competition, keeping all players vigilant. Additionally, with diverse market segments, specialisation can be advantageous without causing harm. As internet penetration in Pakistan improves, a significant portion of the population now possesses smartphones or internet access. However, the adoption of online financial transactions, whether for e-commerce or ride-hailing, remains low due to trust issues. Offering three to four alternatives can help overcome this barrier by gradually building consumer confidence in the available products and services.”

Secondly, he added that more players

in the market allow better lobbying power to influence regulations that impact the sector. “Having multiple options available also enables a stronger industry representation in dealings with regulators and the government. Contrary to common perception, collaboration among ride-hailing companies allows for unified advocacy and lobbying efforts when engaging with government entities, ensuring that industry perspectives are adequately considered in policy-making and legislative processes.”

Well, maybe healthy competition keeps Careem on its toes, but we wonder what it is doing to stay on top of its game.

According to Saleem, there are two main reasons why he believes customers would choose Careem over its competitors.

“We differentiate ourselves particularly through our deep understanding of the Pakistani market and our ability to swiftly localise our services to meet customer preferences. As pioneers of ride-hailing in Pakistan, our extensive institutional knowledge and strong ties to the country allow us to tailor our product offerings and marketing strategies uniquely. Unlike competitors, we prioritise authenticity and cultural resonance. Even our marketing campaigns and slogans reflect a cheeky and fun yet distinctly Pakistani approach, unlike others who a lot of times just translate taglines from their campaigns abroad to Urdu. This deep connection resonates with both customers and captains, providing us with a competitive advantage in the industry.”

Secondly, Saleem said that a great focus on security is an aspect that sets Careem apart from others. “Our commitment to safety encompasses processes including rigorous vetting of captains, involving collaboration with law enforcement agencies and thorough physical verification. We prioritise customer security with dedicated safety teams ready to respond to any incidents promptly. This dedication to safety resonates strongly with our customer base, particularly women, who comprise a significant portion of our loyal clientele.”

He said that Careem’s regular outreach to top customers, predominantly women, underscores their trust in Careem’s safety measures, reinforcing their continued use of the app. “Beyond safety, our commitment extends to in-ride support, addressing various concerns such as navigating through traffic or handling unforeseen issues like fuel shortages or punctures. This comprehensive approach ensures a superior customer experience, exemplifying

a concierge service that guarantees customers reach their destinations seamlessly. These initiatives not only differentiate us from competitors but also reflect our unwavering commitment to prioritise safety and enhance the overall journey experience for our valued customers.”

Even though safety concerns trump most other concerns for Pakistani commuters, sometimes security features can be, well, really annoying! For instance, InDrive’s new in app calling feature that lets you connect to your driver through an encrypted call through the InDrive application, so the driver does not get access to your personal contact details.

The issue, you ask? Well, the quality of these calls is so bad that you end up taking the driver’s number and calling them directly. It also takes ages to connect the call, only to hang up in frustration and hope that the driver is competent enough to follow the directions on the map correctly.

We asked Saleem how Careem ensures safety, without compromising on the overall experience of users?

He explained, “Balancing safety and convenience is paramount, and our approach emphasises customer choice. For instance, our in-app calling feature offers three options: calling through the app, direct captain calling, or contacting our support centre. This flexibility caters to diverse preferences, acknowledging that what constitutes an excellent experience varies for each customer. Over our nearly decade-long presence in Pakistan, we’ve learned that prioritising flexibility ensures customer satisfaction, recognizing that individual preferences may differ. Ultimately, our goal is to empower customers with options that align with their safety and convenience preferences, ensuring a seamless and personalised experience for all.”

Over the years of operation, Careem claims to have enhanced efficiencies and reduced costs in advertising and digital marketing due to business scale. However, safety remains a significant investment, therefore no monetary compromises are made when it comes to spending on security features and services. n

The recent announcement of an Annual General Meeting has raised more questions than answered themBy Zain Naeem

There are certain announcements and incidents that take place in the corporate landscape that seem innocuous in the beginning. It is only when you start to scratch the surface and get to the nitty gritty of the issue when you realize that things are not as innocent as they seem to be.

The recent announcement by Highnoon Laboratories is one such example. It was seemingly a simple announcement calling the company’s Annual General Meeting (AGM). The notice also mentioned how Highnoon wants to get their related party transactions approved by the shareholders.

Sounds pretty simple, right? But behind

this seemingly simple notification are six years worth of related party transactions worth billions of rupees that are now the subject of a legal battle in the Lahore High Court, with certain Highnoon shareholders claiming the company’s management transferred value from their company to another one.

So let’s scratch the surface of this supposedly innocuous announcement that might just have gone entirely unnoticed on the stock exchange.

In the business realm, companies commonly engage in transactions with one another, such as supplying raw materials for manufacturing or procuring goods

and services.

When two or more companies share ownership, management, or significant voting power, they are categorized as associated companies, according to the Securities and Exchange Commission of Pakistan (SECP). These interconnected relationships can influence decision-making and require enhanced scrutiny of transactions to prevent any potential conflicts of interest

In simple terms, these are two companies which are owned and controlled by the same people and as these people have a say in the operations of both the companies, these companies are considered to be associated with each other. The decision making at one company can have an impact on the other and they need to be qualified as such.

Suppose there is Company A, serving

as a raw material supplier for the paper manufacturing industry, and engages in transactions with Company B, which shares common shareholders or management, these transactions fall under the category of related party transactions. Given the intertwined nature of these dealings, they warrant heightened scrutiny due to the absence of external oversight or formal mechanisms for determining fair pricing.

This close association between the two entities raises concerns about the potential for one company to exploit the relationship to the detriment of the other, highlighting the importance of ensuring transparency and fairness in such interconnected business interactions.

The situation becomes even more complicated when there is a private limited and public limited company involved. A private limited company has investors and owners who have put up their own money and investment and would look to make sure that

they profit from any and all transactions that are being carried out.

In a public listed company, the owners are not only the individuals who own most of the shares but also investors who have bought shares in the company. If the private limited company is transacting with the listed company, there is potential that the private company will end up selling their raw material at an inflated price which will mean that the listed company will end up paying more. This will reduce the profit earned by the listed company while the private company will end up earning more.

But is it really that simple? Won’t the substantial shareholders at the public listed company also make a loss? Wouldn’t they be disadvantaged as well? Yes, they will be disadvantaged but as they have ownership in the private company as well, they will still end up making a profit from these transactions.

So it is obvious that this can be an avenue where shareholders can lose out. There is a clear conflict of interest and shareholders need to be protected in such a case.

The best course of action would be to disclose these transactions and to inform the market about all the aspects of the trades to let the market decide on the objectivity and accuracy of these transactions. By giving this information to the investors, the company can give a more holistic view of the company to everyone.

So what is done to not allow this to happen? SECP has given out rules and regulations that dictate the area of related party transactions.

Section 208 of the Companies Act 2017 mandates that a company can only enter into a contract with a related party based on a board-approved policy. The law requires the board to justify such contracts to shareholders and maintain detailed records as per SECP regulations. Approval from the board or members at an AGM must be obtained within ninety days of entering into the contract.

Failure to secure approval renders the contract voidable, and the director involved must indemnify the company for any losses incurred. This regulatory framework aims to prevent conflicts of interest and ensure transparency in related party transactions, allowing shareholders to address concerns through formal channels if necessary.

So what exactly happened at Highnoon Laboratories?

Highnoon Laboratories is a pharmaceutical company which was founded by Ghulam Hussain Khan in 1968 as a partnership. It was incorporated in 1984, was publicly listed in 1985, and had its shares listed on the PSX in 1994. The company is involved in the manufacturing, sale and import of pharmaceutical and related consumer products. The company recently featured in Forbes magazine’s Asia’s Best Under a Billion List for the fourth time. The company also received the Pharma Export Award at the 6th Pharma Export Summit & Awards 2023.

In its latest notice of AGM, the company announced that they were looking to ratify and pass all related party transactions that it had carried out with its associated companies. Considering the hundreds of companies which announce their AGMs and their agenda items show that it is a normal course of action for a company to ratify these transactions.

“The Company be and is hereby authorized to enter into arrangements or carry out transactions from time to time including, but not limited to, for the purchase and sale of goods and material with different related parties to the extent deemed fit and/or approved by the Board of Directors. The members have noted that for the aforesaid arrangements and transactions there may be interested directors. Notwithstanding the same, the members hereby grant an advance authorization and approval to the Board Audit Committee and the Board of Directors of the Company, including under Section 207 and/or 208 of the Companies Act, 2017 (to the extent applicable) to review and approve all related party transactions as per the quantum approved by the Board of Directors from time to time,” read the resolution.

So what was out of the ordinary?

The first sign that something is not normal is the fact that the policy of the company has been to approve these transactions through its board. The annual reports of the company state that the Audit Committee working under the Board of Directors approves any related party transactions based on their set policy and once that is done, the board approves these transactions as well. The company has been pursuing this policy and this meets the requirements of the SECP. Looking at any previous agenda items set for the AGM shows that no approval from shareholders was sought before the one in 2023.

Why this change in policy? Has the company finally started to follow the precedence of the market and start to get all of these transactions approved by the board and the shareholders?

Another fact that is out of the ordinary

is that the approval is being taken from the shareholders for not only 2023 but the agenda item also states that any future transactions which will be carried out have been approved already as well.

As per the resolution,“The related party transactions, for the period ending December 31st, 2024, shall be deemed to have been approved by the members, and shall subsequently be placed before the members in the next Annual General Meeting for ratification and confirmation.”

Why the urgency to get future transactions approved a year before? Why is the company looking to get transactions that it will carry out with its associates till 31st December 2024 before they have even occurred?

Lastly, in its agenda item, the company is stating all the past transactions that have been carried out from 2018 to 2022 when they are getting the recent ones approved? There is little evidence that shows that these transactions were approved in previous AGMs. If the board has already approved them and a minimum obligation to the laws has been met, then why are these transactions being stated again?

When reached to get a reply on these exact questions, the company secretary at the company failed to reply or provide any justification.

The transactions that have been highlighted by the company pertain to transactions carried out between Highnoon and Route2Health (Private) Limited. From 2017 to 2023, the values presented by the company itself state that they have purchased materials worth Rs 4.1 billion with Route2Health (Pvt) Limited. For the 1st quarter of 2024, no transactions have been carried out but the approval already exists from the shareholders as the special resolution was passed by the shareholders.

So why not file a case against the company and its directors?

Well that is exactly what has happened now. Ghulam Hussain Khan, the initial founder of the company, filed a case against Tausif Ahmed Khan, the current chairman of the board. The case alleges that Tausif Ahmed Khan has transferred value from Highnoon to Route2Health which is a company where Tausif Ahmed Khan holds directorship and shares. The transfer of value is taking place allegedly where invoices are being presented from Route2Health to Highnoon without provision of any products being sold and these are being recorded in the financial statements of the listed company.

Even though this can seem like a victimless crime, the loss of profitability, cash

reserves and retained earnings of Highnoon is hurting the shareholders who bought the shares of the company thinking that its owners and directors will work for the betterment of the company. The case alleges that the chairman has gotten his family members elected on the board and is now transferring wealth from Highnoon to his other venture.

A huge point of contention in the case is the fact that the transactions are being approved by the Audit Committee. Two of the members on the Audit Committee in the past were Nael Najam and Zainub Abbas. These individuals were also directors and shareholders at Route2Health. Zainub Abbas is still part of the Audit Committee while she has served as a director and a shareholder at Route2Health. Nael Najam was in the board and the Audit Committee till December 2022 after which she resigned. Nael Najam is no longer a board member at Route2Health but still holds shares of the company.

Essentially, the same people were approving the transactions at Highnoon while they were benefiting from these same transactions on the other side. Despite an active conflict of interest, they were able to vote on these issues and get these resolutions passed when they should have recused themselves.

In addition to that, once these transactions were passed, no evidence or documents relating to these related party transactions was given to the directors of the company which shows mala fide on the part of the committee and the remaining board members. For example for 2022, board resolutions were passed in the board meeting held in April of 2022. When minutes were to be confirmed in the next meeting, Hussain Khan raised the issue that he had not been provided the necessary documentation for the approval from the last meeting. These documents were not given. This was a common occurrence at the company where the Company Secretary did not provide the documentation on time to all the directors. The company secretary at Highnoon is also the company secretary at Route2Health (Pvt) Limited.

The petitioner kept raising the fact that transactions were being approved by the board with related parties and no documentation was being provided to all the directors which was against the rules and regulations. From April 2022 to December 2022, the petitioner was stonewalled and not given rationale and reasoning for the transactions being approved. Hussain Khan also raised the issue that Nael Najam, an independent director at the company, was not independent as she was a shareholder at Route2Health and was approving trades with the associate company. Based on this objection, Najam resigned from the board in December 2022. After this, multiple

attempts were made to check the share register, record their protest to the affairs at the company and raise concerns to the appropriate authorities but it seems that all pleas fell on deaf ears.

Now a case is proceeding at the Lahore High Court.