08

07

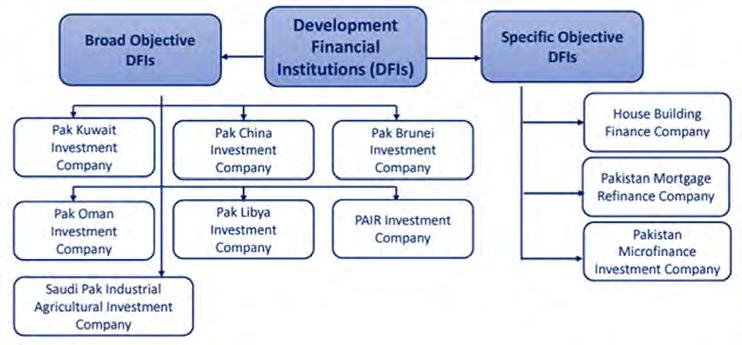

08 Does the D in DFIs stand for Debt?

07 This is the fastest growing sport in the world. Can it take root in Pakistan?

12 Board composition – do you have the right people for your business? Asif Saad

11 A policy abyss Ammar H. Khan

14 Mitchell’s sees most profitable quarter since 2021

14

15 Shezan Q2 2024 sees third worst quarter since 2020

14 Time of Death: Pakistan’s Super-App Dream

16 The SIFC and the Dar problem Abdullah Niazi

16 How inflation killed Retailistan

17 Watch out! Jazz is bringing its digital telco ‘Rox’ out to play

19

20 Different rules for different players prevail in the fertiliser industry

19 Productive policies or PR fluff — How useful were the interim government’s IT initiatives?

23 Is PTCL throttling one of its competitors through anticompetitive practices?

23 Need raw materials? Zaraye hopes you’ll turn to them

24 Can Legends tap Pakistan’s untapped sports potential?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Sub-Editor: Basit Munawar - Video Editors: Talha Farooqi | Fawad Shakeel

Business Reporters: Daniyal Ahmad | Shahab Omer | Zain Naeem | Saneela Jawad | Ghulam Abbass | Ahmad Ahmadani

Shehzad Paracha | Aziz Buneri | Nisma Riaz | Mariam Umar | Urooj Imran | Shahnawaz Ali | Meerub Amir

Regional Heads of Marketing: Mudassir Alam (Khi) | Sohail Abbas (Lhe) | Malik Israr (Isb)

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

TENTS

CON

Profit Profit CONTENTS

08

20 20 24

15

Does the D in DFIs stand for Debt?

The financial institutions have overhauled their strategy and now resemble a leveraged fixed-income fund

8

By Ahtasam Ahmad & Mariam Umar

They say there is a great big lever that exists somewhere in the building of the State Bank of Pakistan (SBP). While the central bank performs countless functions from granting approvals to regulating the financial sector, its most prominent and closely watched responsibility is this lever.

The SBP’s governor is the custodian of this lever and pulls it either way with the help of his Monetary Policy Committee. The lever either increases or decreases the rate of interest in the country. Now, Profit’s more discerning readers might have picked up on the fact that this publication has been more critical than usual of the state bank’s use of this lever. It seems to us that the SBP has adopted a reactive monetary approach, resulting in inflation peaking at around 30% last year and still exceeding 20%.

This has been going on since at least 2021. At first, it even seemed prudent as a measure to curb inflation. But it now seems almost rehearsed and as a result predictable. It seems that the SBP has decided to be quite reactionary in their pulling of the lever. The problem with this is that a lot hinges on which direction the lever moves. Already the persistent increases in the policy rate have inflicted significant damage on the corporate sector and consumer purchasing power during this period.

Another consequence of the policy directives in recent years is a notable shift in the business strategies of companies, particularly in the financial sector.

The publication has already discussed how commercial banks have shifted away from traditional banking practices towards becoming investment firms. Surprisingly, we have also observed a similar trend in a sector that bears the responsibility of serving segments overlooked by commercial banks.

Read: Has UBL paved the way for other banks to maximize arbitrage opportunities?

We are referring to the Development Finance Institutions (DFIs), a sector that states its primary objective as contributing to capital formation and economic development in the country by providing long-term financing.

However, over the past year and a half, the majority of players in the sector have adopted a strategy that resembles a leveraged fixed income fund rather than a DFI.

What has contributed to this shift? Let’s delve deeper and explore.

State of play

Presently, there are two categories of DFIs operating in Pakistan: broad objective DFIs and specific objectives DFIs. Broad objective DFIs are also known as joint venture financial institutions (JVFIs). They have been established in cooperation with bilateral partners and are majority-owned by national governments to implement the government’s foreign development policies.

The shareholding structure of JVFIs consists of 50% ownership by the Government of Pakistan, through either the Ministry of Finance or State Bank of Pakistan. The remaining 50% is owned by the respective foreign governments through relevant institutions.

On the other hand, specific objective DFIs are created for the development of a specific sector. Their ownership structures are more varied, with shareholding held by national and international financial and developmental institutions.

(We will focus on JV DFI in this story)

In Pakistan, there are seven JV DFIs: Pak Kuwait Investment Company (PKIC), Pak China Investment Company, Pak Brunei Investment Company, Pak Oman Investment Company, Pak Libya Investment Company, PAIR (Pakistan-Iran) Investment Company and Saudi Pak Industrial Agricultural Investment Company. PKIC is the largest DFI of Pakistan.

“All DFIs are relatively small except for PKIC. PKIC’s advantage lies in its 30% stake in

Meezan Bank, from which it receives dividends of around 12-13 billion rupees. PKIC’s profitability compared to other industry players will be significantly different due to these high dividends,’’ explained an industry source.

The change in fortunes

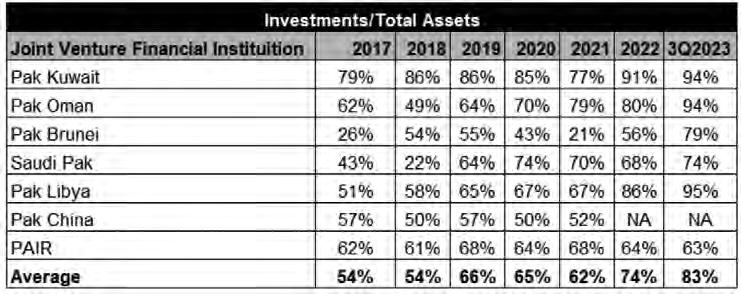

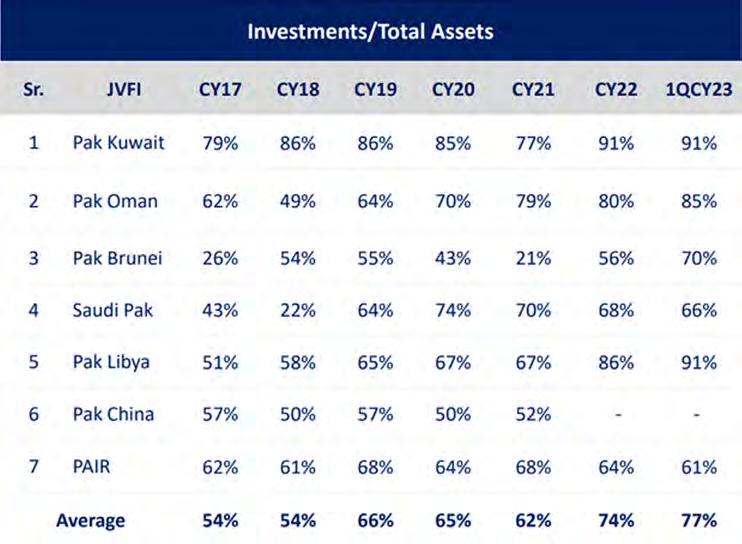

The sector has historically managed to grow its asset base steadily with investments dominating the asset mix followed by advances. The latter averaged around less than half of the investments over the years.

However, since 2022, there has been a meteoric rise in this trend. “The share of investments in the total asset base has grown steadily over the years (CY17-22), and clocked in at 74% in CY22, up from 54% from CY17-18 and 62% the previous year. This was spurred by the increase in investments in government securities, which occupy the largest share in investments,” read a sector study by PACRA.

“The average share of the segment’s federal investments in their total investments portfolio stood at 73.8% in CY22 (CY21: 62%). In absolute terms, the segment’s total investments in federal securities clocked in at Rs 881 billion in CY22, 6x the levels in CY21, when they had amounted to Rs 155 billion. The share of investments in total assets of the segment rose to further 77% during 1QCY23,” it added.

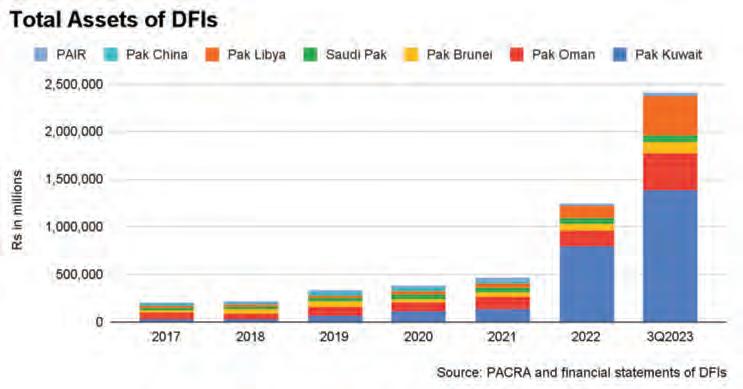

The figures above illustrate a growth of over 600% in the asset base in less than two

Source: PACRA

Source: PACRA

FINANCE

Note: Prior to June 2022, repo borrowings constitute of banking market transactions

Source: PACRA & Company Financials

years, driven by investments in government securities. If this seems familiar, you’re not alone. We have traversed a similar path before, albeit in a different sector

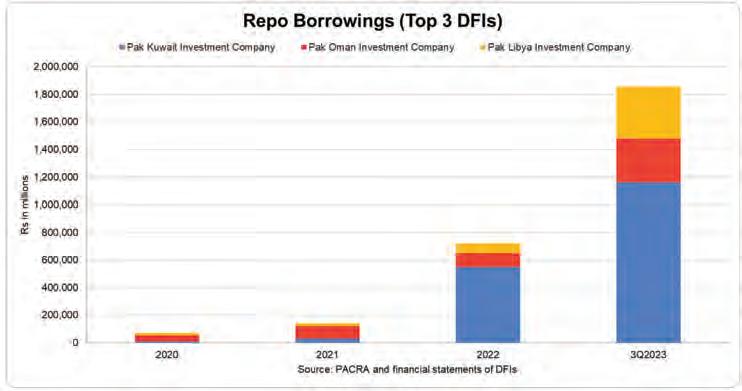

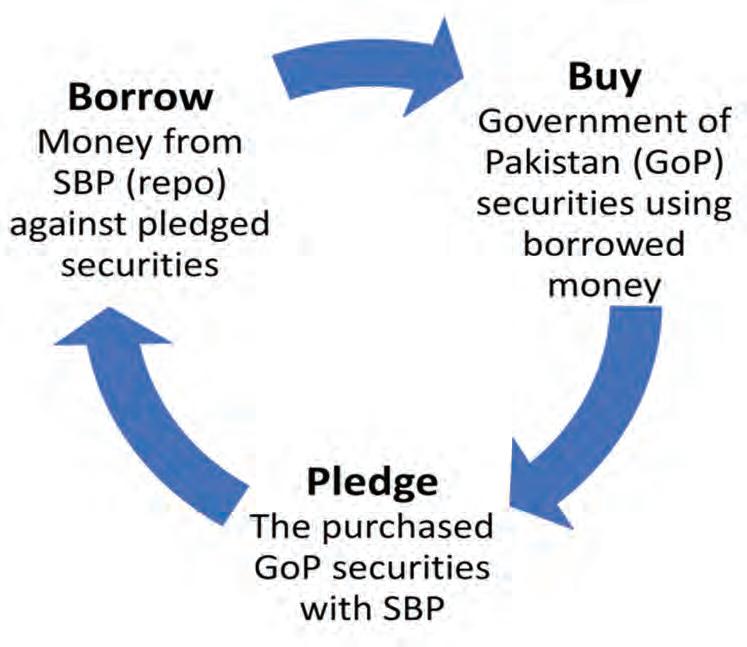

Raising eye“borrows”

The sector’s investment surge was fueled by the good old repo borrowings. Similar to commercial banks, DFIs borrowed from the SBP using government securities as collateral to fund additional government securities purchases. These securities, in turn, act as collateral for more borrowing, thus perpetuating the cycle.

However, unlike banks, DFIs have only recently gained the privilege to conduct transactions in this manner and scale. In June 2022, the SBP allowed all DFIs to participate in Open Market Operations (OMOs) to facilitate DFIs in their “liquidity management”.

Read: SBP allows DFIs to participate in OMOs

The top 3 DFIs that have the sector’s majority exposure to these transactions have now resorted to earning spreads available between borrowings from SBP vs investing in government papers.

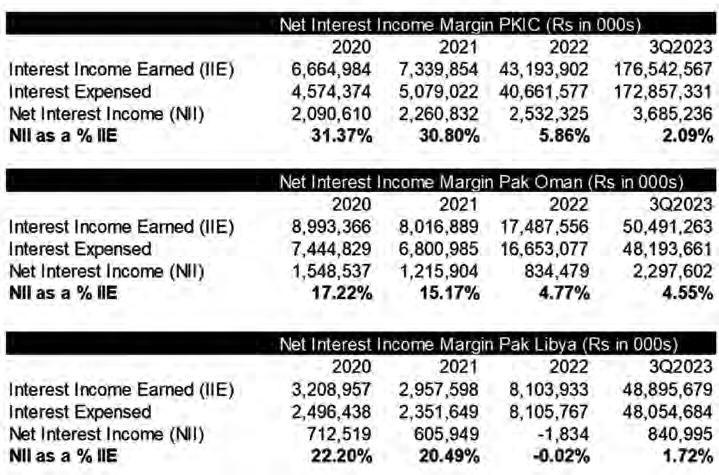

As per a note in PKIC’s financial statements for the third quarter of 2023, “The Company has arranged borrowing from financial institutions against sale and repurchase of government securities. The mark-up rates on these borrowings are between 21.50% and 22.15% per annum (December 31, 2022: 15.22% and 16.21%per annum) with maturities between two days to fifty five days (December 31, 2022: sixty three to seventy days).”

Consequently, the borrowing rate is exceptionally high and nearly equals the returns on government securities. This results in narrow margins, making it essential to focus on volume to enhance profitability.

The DFIs have followed this strategy religiously. The quantum of repo borrowings, particularly among the industry leaders, is substantial. The top 3 players have accumulated borrowings of approximately Rs. 1.8 trillion by the third quarter of 2023. During the same period, the outstanding OMO positions by the SBP stood around Rs. 5.9 trillion. Therefore, almost 30% of this was parked with these three entities with the majority being held by PKIC.

This has transpired into healthy profitability growth for the sector players as the volume play has yielded dividends. However, this strategy comes at the expense of DFIs neglecting their primary objective of serving as enablers of development finance.

One might expect regulatory intervention, but in this instance, the central bank is actually one of the primary enablers of this trend. By simply issuing the circular mentioned earlier in this story, the SBP created another

10

avenue for lending to the government to meet the federation’s perpetual need for deficit financing.

The flip side

It is important to consider why DFIs felt compelled to engage in this program. These institutions rely solely on term deposits and investment certificates as sources of funding, which may not be adequate. Thus, they must depend on borrowings and their own equity for financing.

“We borrow from commercial banks and then we lend to the same clientele that already has access to commercial banks. In other words, we are competing against commercial banks after borrowing from the same commercial banks. We can’t compete. Our cost of funding will definitely be higher. Commercial banks lend to us at Kibor plus some spread. So we will be lending at costly rates for commercial borrowers”, lamented a CEO of one of the leading DFIs.

Hence, the biggest challenge faced by DFIs is the lack of cheap sources of funding. “DFIs around the world receive funding from their governments, which is not the case here”, remarked a CEO of a DFI.

Furthermore, high interest rates have emerged as a significant obstacle, making long-term financing at 25-26% interest rates unviable.

Securing funding from international sources presents another challenge due to Pakistan’s elevated country risk. International funding typically involves receipts in dollars, necessitating dollar repayment.

Over the past 1.5 years, Pakistan has experienced significant liquidity issues, with foreign exchange reserves decreasing to approximately $4.5 billion in June 2023, barely sufficient to cover a month’s worth of imports. To address dwindling reserves, the SBP implemented restrictions to manage foreign exchange

Source: PACRA

Source: PACRA

outflows. As a result, Pakistani corporations were unable to repatriate dividends to their overseas parent companies, undermining investor confidence.

Similarly, the support of SBP is also crucial. “SBP does not support DFIs the way they should be,” lamented an industry source. “For example, TERF should have been pushed through DFIs because long-term financing is much more riskier. However, DFIs got a negligible share. Our allocations were rejected despite being strong in capitalisation ”, the source expounded.

TERF — which stands for Temporary Economic Relief Facility — was launched in 2020 during the peak COVID-19 pandemic. It was essentially a facility launched by the SBP with the help of the government that provided nearly interest-free loans to businesses so they could keep the wheels turning and not lay off their employees. Over time, more than 600 businesses took advantage of this facility and the SBP lent over $3 billion for this purpose. Major businesses took them up on this offer, including giants such as Interloop, Nishat, the Lucky Group, Ismail Industries, and many others.

Despite the lack of external support, DFIs still possess the capability to take the initiative. The key lies not in focusing on what is lacking, but in maximizing the potential of existing resources: DFIs are backed by sovereign entities, and if effectively promoted, this support can be leveraged to raise funds at favorable rates. n

FINANCE

Asif Saad

Board composition –do you have the right people for your business?

Most

medium to large-scale

businesses need to think deeply about the different types of talent required for their boards

Boards of directors can play a crucial role in building companies. They act as a strategic asset that can help guide management while providing the knowledge and experience necessary to navigate a variety of challenges. In addition to supporting management, boards also help to ensure that the interests of shareholders, whom they represent, are protected, as well as those of employees, customers, and other stakeholders.

I wrote an article a couple of years back about the lack of independence of the so-called independent directors on company boards in Pakistan (link here from profit editors) While that piece was written with the larger listed corporate entities in mind, in today’s article, I would like to focus on the needs of medium to large-scale family businesses, which may or may not be listed, but are now the mainstay of the country’s business and economic

The writer is a strategy consultant who has previously worked at various C-level positions for national and multinational corporations

structure.

Many of these family entities don’t see the need for boards, thinking that they ought not to tolerate outside influence. But several family groups, those who have acquired the wisdom to understand the importance of opinions, other than their own, have created corporate structures with functioning boards (or advisory boards) for their businesses. This is a step in the right direction and these companies can benefit from such structures, provided they can define their needs, attract the right talent on their boards and think of the process as a journey rather than an end state.

It is a journey because of the scale and evolution of the business. Think of an entrepreneurial venture which needs the time and space to grow and for this growth, the entrepreneur should be making most of the decisions, with some advice from family and friends, if needed. You would not wish for start-upbusinesses to be saddled with bureaucratic controls which kill the risk-taking required for scaling up.

Even if startups need to give board seats to venture capital representatives, these investor directors need to ensure that they allow the founder/entrepreneur to make decisions and remain nimble. Most reasonable Venture Capital firms understand that having too many VC reps on a board isn’t helpful and are willing to accept that.

Coming back to family businesses, once some scale is achieved by the business, it needs to start to think about the next level of growth. This is where I find many family businesses to be stuck – they have a proven business model and have built a profitable business which has the potential to be scaled up, in different directions perhaps using dissimilar ways.

These companies are at a stage where the business needs a broadening of vision, a strategic direction, qualitative enhancement of management capabilities, and technological innovation coupled with some control to ensure better governance. They need all this to grow further and build a sustainable business, continuing for future generations of family members.At least, this is the desire of most current family members. And this is exactly where outside directors can play a vital role.

But this is also where these companies need to carefully evaluate what type of outside board members are required. Businesses which are at the initial stage of board creation and associated governance processes require people who have the time and are willing to support the business in many ways, certainly beyond attending quarterly meetings. This should be one of the first requirements for a business venturing into this area.

The business should also be able to benefit from leadership qualities which support management teams and can hold them accountable. This is a fundamental issue especially where fami-

12

OPINION

ly members are themselves running/controlling businesses. In such cases, the need for independence should be carefully measured against management’s willingness to be challenged.

There has been a push in recent years to ensure greater diversity on boards of directors. Given that our business leaders are very often middle or senior-aged men, the best way to achieve that diversity may well be through your choice of independent directors.

There are a few common mistakes that I see companies make when building their boards. The first is confusing board members with skills missing in the organization. A company may recognize marketing as a weak point for the business, and conclude that it should add a marketer to the board when in fact what it needs is a new CMO. That does not mean that it does not bring a director with marketing expertise to help support the management. It should certainly do so if they find the right person. However, it is important not to confuse businessoperating needs with your

strategic advisory needs. Remember, board members give advice, while employees produce deliverables.

At the other end of the spectrum, some companiesmake the mistake of hiring trophy board members. There are organizations whose boards are composed of former CEOs, retired bureaucrats and other seemingly highly desirable board members. As impressive as these people may be, it is unlikely that they meet the first criteria of being able to give the time required and having the energy to understand the organization’s needs deeply.

Mature organizations tend to have trophy board members who tend to stay for several terms. It’s not unusual to have independent directors stay on for a decade, provided that they can continue to be helpful and provide value at the different stages of the business’s evolution. That said, it is helpful to get fresh perspectives and opinions. Being able to cycle in new directors can be very beneficial, so there is a need to always weigh the pros and cons of

keeping existing directors versus bringing on new ones.

It would be unwise to have trophy directors for a business which is just building these governance and management processes and vying for fast-paced growth. These businesses ought to be looking for a different type of hand-holding from their independentdirectors.

Most of the requirements for the organizations which have recently inducted themselves in corporate governance processes can be best met by talented senior executives who may have never sat on a corporate board but who would still make incredible board members given their breadth of experience and expertise. More companies just need to be willing to give them the chance to do so.

Additionally, the relatively younger lot is more connected to the new cultural ground realities. If we wish to change the diversity in the leadership ranks of corporate Pakistan, widening the funnel of director candidates is a good way to start. n

COMMENT

Mitchell’s sees most profitable quarter since 2021

The confectionery manufacturer’s financial turnaround was fueled by prudent spending but cashflow remains a concern

By Saneela Jawad

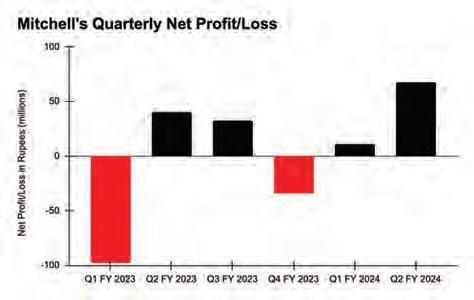

Mitchell’s, under the leadership of Najam Sethi, has navigated a tumultuous journey since his takeover. However, the recent unveiling of their quarterly results for the second quarter of 2024, ending in December 2023, has sent ripples of astonishment through the market, marking the company's most profitable quarter since 2021, with a net profit of Rs 67 million.

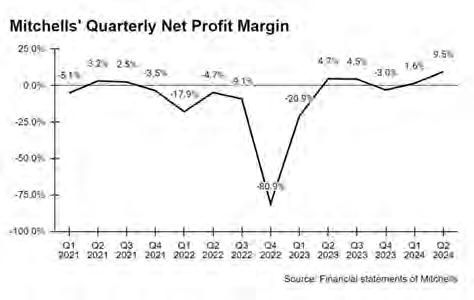

Despite a decline in sales from Rs 856 million in the same quarter of the previous year to Rs 707 million this year, Mitchell’s has displayed adept management of expenses. Notably, the gross profit margin surged from 28% to 30% year on year, and the operating profit margin rose from 9.5% to 12.6% over the same period. The company also tightened its administrative expenses, decreasing from 18% to 17%.

However, a notable setback was the doubling of finance costs, escalating from 2.2% to 3.7%, attributed to higher interest rates prevailing in the economy. The decrease in administrative costs came after the company considerably cut down on its marketing and distribution expenses.

“Due to these efforts, the margins have registered a healthy growth, admin costs have been rationalised and distribution expenses have been drastically brought down. The cost of financing is at its peak in the country which is the reason for the phenomenal increase in finance costs. On the other hand, due to cashflow

challenges, we have not been able to undertake any major marketing advertisement activity which is essential for attaining volume growth. Due to this, volume decrease in local sales is more as compared to export sales which remain steadier at over USD 1 Million level during this period,” read the latest director’s report.

Furthermore, Mitchell’s witnessed a significant uptick in other income, soaring from Rs 8.5 million to Rs 22 million, while simultaneously reducing other operating expenses from Rs 20 million to Rs 7 million. Consequently, the net profit margin experienced a remarkable surge from 4.7% in the second quarter of 2023 to 9.5% in the recent quarter. This improvement was mirrored in the earnings per share (EPS), escalating from 1.77 per share to 2.95 per share.

Profit in an earlier report stated that the fluctuating efforts of Sethi as the CEO with glimpses of hope discernible in the quarterly results of 2023, sparking anticipation of a potential shift in the company's trajectory come the new fiscal year.

During the first quarter of 2024, Mitchell’s secured a profit of Rs 11.1 million, with a gross profit margin of 24.9%. Despite this, the earnings per share (EPS) remained modest at Rs 0.49. However, projections indicate an expected EPS of approximately Rs 2 by the end of the fiscal year.

Following the release of the recent quarterly results, Mitchell’s, yet again, witnessed a notable surge in its stock price, soaring from Rs 132 on February 7 to Rs 171 on February 29, the day the results were disclosed. This remarkable increase sparked speculation regarding a potential sale, which was swiftly quelled by an insider from the company, attributing the rise solely to the commendable performance of Mitchell’s.

Building on the momentum, the company plans to layoff redundant assets and generate additional cashflows.

“With a view to inject some much-needed capital into the business, addressing working capital shortages and reduce the interest costs, the company, with Board approval, entered into a sale agreement on 15 January 2024 to sell a portion of its land. The transaction is expected to complete in March 2024, with the first tranche of the money received in January. The piece of land being sold was not adding any value to the company, the price obtained was excellent and whilst being less than 15% of total company land, sets an attractive realised benchmark valuation for the residual 39+ acres which are not valued on our balance sheet,” the directors emphasised in the quarterly report.

The Sethi factor

Since 2020, Mitchell’s fortunes have been run by one man in varying capacities:

Najam Sethi as the Chairman and as the CEO. In 2020, net sales stood at Rs 2.1 billion, while cost of sales stood at Rs 1.7 billion. Consequently, net loss stood at Rs 55 million.

The next year, in 2021, Mitchell’s actually managed to experience a bright spot. Net sales increased to Rs 2.2 billion, while cost of sales stayed around the Rs 1.7 billion mark. Additionally, a slight dip in administrative costs that year meant that Mitchell’s just managed to scrape a profit of Rs 10.4 million.

2022 proved to be the worst year in Mitchell’s history. Net sales slightly increased to Rs 2.4 billion, but the cost of sales ballooned to Rs 2.3 billion. Other costs like distribution costs and administrative expenses also ballooned, leading to a net loss of Rs 622 million – the greatest in the company’s history.

14

After this, Sethi took charge as CEO and according to the annual report 2023, in the first quarter, the company experienced a loss of Rs 98 million. Following his ascension, the subsequent two quarters showed profitability: profit in the second quarter stood at Rs 40.5 million, and in the third quarter stood at Rs 32.4 million.

However, despite the positive trajectory in the second and third quarters, the company faced challenges in the last quarter with a loss of around Rs 34 million. The year’s total annual

loss stood at Rs 59 million. The good news was that the revenue went up to Rs 2.7 billion, and gross profits managed to rise from Rs 193 million in 2022 to Rs 648 million in 2023.

Mitchell’s underwent a turbulent phase in 2018 when the family-owned company contemplated a sale due to internal discord and management issues, enlisting Habib Bank Ltd as sell-side investment bankers. By July 2019, negotiations with Bioexyte Foods, a subsidiary of Getz Pharmaceuticals, to assume management control of Mitchell’s were nearing

fruition. However, the onset of the coronavirus pandemic in early 2020 resulted in the collapse of the deal. Consequently, Mitchell’s stock price, which had surged by 77% during the deal announcement to Rs 345 per share, witnessed a steep decline post-collapse, albeit remaining slightly above pre-announcement levels.

Najam Sethi's tenure as CEO has been marked by strategic pricing revamps and a meticulous overhaul of revenue streams, propelling Mitchell’s into a marginally healthier financial standing. n

Shezan Q2 2024 sees third worst quarter since 2020

Economic headwinds coupled with high financing cost take a toll on the bottom line of the F&B giant

By Saneela Jawad

Shezan International Limited, a key player in Pakistan's food and beverage sector, has recently disclosed its financial report for the second quarter of 2024, revealing a challenging period characterized by a notable decline in sales and overall net profit. This downturn marks the third worst quarter for the company since 2020, with a loss of Rs 204 million, following the setbacks faced during the peak of the COVID-19 pandemic.

The quarterly figures spanning back to 2019 illustrate a consistent trend of subdued performance during the second quarter, which falls between September and December. This seasonally slow period aligns with the colder weather, impacting the demand for beverages like juices, which are core products for Shezan. Notably, the recent quarter's loss ranks third in severity since 2019, with only Q2 and Q3 of 2020 surpassing it, reflecting the unprecedented challenges posed by the pandemic.

A report by Profit Magazine highlighted a recurring pattern of decreased sales during the second quarters of 2021 to 2023. This trend correlates with the winter season, during which consumer demand for Shezan's popular products, such as bottled juices and tetra packs, tends to diminish. Conversely, the quarters ending in March, June, and to some extent, September, typically witness an upswing in sales, driven by more favorable weather conditions stimulating consumer demand.

Comparing the two quarters of 2024 reveals a substantial decline in sales from Rs 2.1 million in Q1 to Rs 1.4 million in Q2, accompanied by a corresponding decrease in gross profit from Rs 438 million to Rs 226 million. Consequently, the net profit margin plummeted from -1.3% to -14.8% between the two quarters. However, the data over the years suggest that despite losses in the second quarter, Shezan tends to recover in subsequent quarters, offsetting the annual net profit, with the exception of 2020, when the pandemic severely impacted operations.

While the company reported a profit of Rs 113 million in 2019, it faced a significant downturn in 2020, resulting in a loss of Rs 235 million. Subsequent years saw gradual recovery, with profits of Rs 123 million and Rs 80 million in 2021 and 2022, respectively, albeit still below the 2019 level. However, 2023 saw a marginal net profit of only Rs 38 million, indicating ongoing challenges in maintaining profitability.

One persistent issue contributing to Shezan's financial struggles is the escalating finance costs, which have surged from Rs 68 million in 2019 to Rs 280 million in 2023. This rise has eroded the net profit margin, dropping from 1.5% in 2019 to 0.4% in 2023, underscoring the adverse impact of mounting financial obligations on overall profitability.

Looking ahead, the forecast for Q3 2024

suggests continued pressure on profitability, as sales have declined over the past six months while administrative expenses have risen from Rs 92 million in Q1 to Rs 101 million in Q2.. Despite relatively stable finance costs between Q1 and Q2 from Rs 85 million to Rs 80 million, the significant net loss incurred during this period of Rs 28 million and Rs 204 million is expected to weigh on the upcoming quarter's net profit.

In its 2023 annual report, Shezan attributed its financial challenges to economic downturns, regulatory changes, such as the imposition of excise duty, and inflationary trends. However, despite these headwinds, the company's annual sales trajectory has shown resilience, increasing from Rs 7.7 billion in 2019 to Rs 8.7 billion in 2023. Moreover, gross profit witnessed a steady growth, rising from Rs 1.5 billion in 2019 to Rs 2 billion in 2023, indicating underlying strength in operational performance amidst challenging market conditions. n

Abdullah Niazi

Pakistan has just had a close brush with Dar, but it seems that the worst is over. While Prime Minister Shehbaz Sharif has been slow to announce his picks for cabinet, it has become increasingly clear that former finance minister Ishaq Dar will not be asked to head the finance ministry for a record fifth time.

Of course, Mr Dar will not be absent from cabinet entirely. His party has gone so far as to indicate that the position of Deputy Prime Minister (a job nearly as useless but not quite so useless as President) might be revived for the good senator. If not that he might even be given a shot at the finance ministry where he would have the opportunity to do far more damage.

For most close observers of Pakistan’s economy the decision to keep Dar away from it elicited a sense of veritable relief. There is not yet any guarantee as to his replacement. The CEO of Pakistan’s largest bank has been touted as a possible replacement. The name of the caretaker finance minister and former SBP Governor Dr Shamshad Akhtar has also been under consideration.

Whatever happens the general sentiment is that no matter who comes in they will be better Dar. But we must at some point pause and ask a truly terrifying question. A question that mothers use to scare their kids to sleep and which keeps economists up at night.

What if we get a finance minister worse than Dar?

Normally one would shudder, put the thought away, and hope nothing of the sort happens again. But for this new government there is one fresh factor that will have some impact or other on the powers of the finance ministry: The Special Investment Facilitation Council (SIFC). For a very long time the country’s military leadership has been sharing power with their civilian counterparts. Over time this complicated relationship has arrived at a general understanding by which the

writer is senior editor at Profit. He can be reached at abdullah.niazi@ pakistantody.com.pk

military is allowed to independently run its own affairs while having a sizable influence on Pakistan’s foreign policy. In exchange, civilian setups have every now and then been allowed to run the economy and policy in areas such as health, education, and other service sectors with relative independence.

There is much to be said simply in terms of historical fact about how we got here. But let us set that aside for the sake of ease, security and understanding. Let us forget matters of what should be and what shouldn’t be. Of right and wrong, and of constitutional and unconstitutional and instead focus on realities. What we do know is that even in periods where military dictators were directly exercising executive power they largely relied on technocrats, bankers, and economists to manage the country’s finances for them.

But over the past year or so the country’s military leadership has taken a more direct role in managing the economy than it has even done during periods of direct military rule. There is nothing more indicative of this newfound interest in financial management than the Special Investment Facilitation Council (SIFC) that has been designed, spearheaded, and launched by the country’s military leadership.

What exactly does the SIFC do? It is supposed to be a council composed of civil and military leadership that operates almost like a second, empowered, commerce and investment ministry. The council provides opportunities and easy terms of investment and cuts through the inefficiencies with a vast array of powers. It is, essentially, a way to ensure consistent economic and business policies for foreign and domestic investors.

It is as much a failsafe as it is anything else. Just look at Mr Dar’s last term as finance minister. After taking charge of the finance ministry in September, Senator Dar spent a good few months trying to prop up the rupee, stomp on inflation, and build a platform for the PML-N to build an election campaign off of. Any criticism of his actions or suggestions that they could derail the hard fought IMF agreement were met with macho posturing and aggressive chest thumping.

All of the buffoonish antics ended when the IMF did not respond kindly to Mr Dar’s tactics. When it became clear there was no recourse, the government ended up blinking in the stare off and an IMF team arrived in Pakistan by February and left without signing a staff level agreement. From here on in the fund had the upper hand and ended up essentially dictating the country’s budget.

The SIFC, as of now, cannot of course participate in matters such as negotiations with the IMF. It is simply a vessel for private investment. But as time has passed, the council has continued to gain increasing power and influence in the country. There is, of course, no answer better than democratic, representative, leadership. What we can know for sure in the meantime is that unless whoever becomes finance minister is clear, decisive, and quick with their decision makers some other entity will carve out some of the job for itself whether it be the SIFC or some other body.

16 COMMENT

The SIFC and the Dar problem OPINION

Watch out! Jazz is bringing its digital telco out to play

Months after Ufone introduced Onic to Pakistan, Jazz is gearing up to give them a competitor

By Shahnawaz Ali

“V

ibe-hai”. That is the ambiguous-enough-to-intrigue but not-so-ambiguous-as-to-disenchant tagline Jazz has chosen for its new sub-brand by the name of Rox. The new brand promises to give its users a seamless digital lifestyle. But what exactly does that mean?

What is the vibe? What does vibe even mean?

Profit spoke to Jazz and they confirmed that Rox was the company’s attempt at launching a digital brand. The market that Jazz is walking into is at a very interesting stage. On the one hand, the idea of a digital telco is relatively new in Pakistan. On the other they will not have a first-mover advantage since that was already taken by Onic — Ufone’s

digital telco brand launched just a few months ago. But Jazz must have thought of something, right? After all, when the country’s biggest telecom network comes up with a product, it means that they mean business.

The only question is, how will Pakistan’s biggest telco fare as the second entrant into a still new market that customers aren’t familiar with? And let’s actually begin by starting off with that question. What in the world is a ‘digital telco’ company supposed to be in the first place?

If you can’t beat ‘em, join ‘em

The relationship between customer and telecommunications network is changing. There was a time all around the world when people choosing their phone carrier would base it off a few factors. What network were their friends and family using? Which network was

most reliable and had the best signals in their area? Which one was offering the best rates? It was a simple equation. A telco would provide good services at a good rate and it would gain a customer.

It is still somewhat that way in Pakistan. Except the winds of change seem to be rising in the sails. Understanding what the term ‘digital telcos’ means is a bit of a tough task because there is no one definition in particular. But very simply (and broadly) put a digital telco is when a telecom brand co-opts digital solutions to stay ahead of the curve in a business that has lost some of its lustre.

For all intents and purposes telcos have been forced to go digital. Over the past decades the telecommunications sector has seen its fortunes dwindle. What was once the hottest business of the 1990s has become close to obsolete. The concept of SMSs and voice messages, once the highest sources of revenue for these companies, have been replaced by messaging services. One might imagine that they have

17 TELCOS

In Pakistan, with 64% of the population under the age of 30, there is a significant demand for digital-first experiences. ROX delivers a combination of content and services to engage the digital-first generation of the country. With Jazz’s wide portfolio of digital services and experience in providing a seamless digital experience to our customers, and with the learnings in our Group based on the success of other digital-first brands, we are confident that we are uniquely positioned to meet this demand

Kaan Terzioglu, CEO of VEON Group

since shifted to making money from mobile data and broadband, but the profit margins on mobile data continue to narrow on the back of downward price pressures and competition. A simple example of this is that just like a consumer would take a mere second to jump onto a whatsapp call if the cost of the voice call goes beyond a certain margin, they would jump to WiFi if their “mobile data” is expensive or slow.

It is a problem well illustrated in the Pakistani market. As of October 2023, average revenue per user for a telco in Pakistan came to $0.8/month. Meaning that every individual who uses a mobile phone in Pakistan provides less than a dollar in revenue to their telecom company, what they give them in Profit, is of course lower.

As a result, there aren’t really any new telcos lining up for licences. Instead, the existing players in the market are trying to find digital answers to the existential questions they face. Rather than fighting the digital world, they started embracing digital businesses as a saving grace. This meant that they would indulge into a wide variety of digital businesses. These businesses range from things that were entirely in a telco’s domain to things that… just got the cash rolling. And that is essentially what a digital telco is.

Digital telcos often bundle telecom services with other digital offerings, such as streaming content, cloud storage, or smart home services etc. Other than that, digital telcos around the world sometimes employ data analytics, automation and AI to make agile operations, improving and automating the user experience. So where you’d spend hours to get a response on your email, a digital chatbot will solve your query right away with its integrated manual. These brands also tend to make use of up and coming technologies like 5G computing and network slicing. These technologies upgrade their services and take them a notch above the traditional telco. This falls in line

with improving the technology on the back of which their voice and data services would also flourish.

Meeting the competition halfway

The first signs in Pakistan came through Onic. Back in September 2023, Profit reported in a detailed feature how Ufone, a company that had seen a drought of profits, was trying to turn things around through a new brand they were billing as a digital telco called Onic. It was an attempt to resuscitate and some felt it came at a time when Ufone should have been pleading for a DNR.

The picture has since changed quite a bit. Onic, right now, is not only the first digital telecom brand of Pakistan but after Telenor’s sale to Ufone, it also becomes the flagship digital telecom brand of Pakistan, backed by an endless balance sheet of global giant e&, and sitting on the biggest telecom infrastructure in the country.

The market clearly called for competition. And being the market leader, the biggest player by far and the most astute one, Jazz had to answer. Rox will now be going head-tohead with Onic in this fledgling market.

“Offering a fully digital journey, ROX is a digital lifestyle brand that allows users to seamlessly manage their connectivity and rewards. It has partnered with leading lifestyle brands like foodpanda, Careem, Bookme, and Golootlo to offer users exciting, exclusive deals and discounts,” the company’s spokesperson told Profit in a written statement.

So how does Jazz plan on using Rox to trounce Onic? As we’ve mentioned already, there is an advntage to being a first-mover in any business. And while breaking into the business becomes harder for a new entrant, there are some advantages too. For starters, you can learn from the mistakes of your com-

petitors. Taking what works and fixing what doesn’t work is a technique that will win you customers. And when the second entrant has the resources that Jazz does, the competition gets hot fast.

Making the best use of its second mover’s advantage, Rox has everything that Onic or PTML lacked to be a good digital telco, as pointed out by Profit’s earlier piece.But as we’ve mentioned earlier, it can be difficult to define what a digital telco is. Onic’s definition might vary from Rox. So what exactly is Jazz’s take on a digital telco going to look like?

A “Lifestyle sub-brand”

What makes a good digital telco, does Rox fit the bill and how will they square up against the competition. That is the crux of the matter. To understand how Jazz has chosen what Rox is, we need to first understand what a digital telecom operator is. Any brand can be a lifestyle brand. Lifestyle branding, in its essence, is a marketing strategy. Any brand that embodies a certain way of life, and can then offer services or merely an autopia of that way of life is called a lifestyle brand. As an example, Apple is a lifestyle brand for smart gadgets.

When asked, the company representative told Profit that in this case Rox is considered a lifestyle sub-brand because it is “tailored to serve as the all-encompassing lifestyle partner of the nation’s digital-first generation.”

As Gen-Z prefers convenience and has certain numbers of needs, the app and the bundles cater to all those needs. Partnering up with top-of-the-market external ride hailing, delivery, and booking companies, Rox’s bundles come with convenient offers for all these services. Besides it has in-app subscription to Jazz’s top apps like Tamasha — country’s larg¬est homegrown digital enter¬tainment

18

platform, Bajao — a leading digital music stream¬ing service in Pakistan, and GameNow — a revolutionary gaming platform, elevating their digital experience.

One thing that is however a defining feature of Rox is a SIM card. A SIM card that would lead you to subscribe to different voice and data bundles that come with added benefits. This automatically leads us back to our earlier definition of what a digital telco is. These defining features make Rox effectively the biggest and most innovative digital telco of Pakistan.

What does Rox offer?

This takes us back to why Rox is doing more than its competition. The position taken in Profit’s earlier article was that there is not enough that Onic offers in terms of services to be characterised as a good digital telco. In Fact anything that Onic offered, other conventional telcos were already offering or were offering better, despite being non-digital.

As mentioned above, a digital telco clumps together a host of services, not just for convenience but also as a perk.

Before coming to the voice and internet bundles, here are the additional things that Rox has to offer. An in app subscription of the Subscription Video On Demand (SVOD) versions of Tamasha and Bajao, Jazz’s premium OTT and Audio streaming platforms, both of which not only offer entertainment, but quality entertainment such that they have made a name for themselves in a very short span of time.

Apart from this all the bundles of Rox come with a free subscription of Panda Pro, a version of delivery giant foodpanda which offers free food deliveries and discounts. Similarly it comes with Pro or gold subscriptions of Bookme, a booking platform and Golootlo, a discount aggregator company. Rox subscription also offers Rs 200 off on Careem, Pakistan’s premiere ride-hailing app.

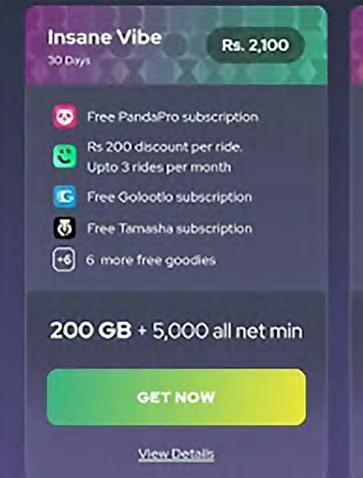

In voice and data, Rox offers three plans, the basic, crazy and insane vibe. The basic one constitutes 25GB data and 2000 all-net minutes. The crazy and insane bundles offer 75 and 200 GB data, and 2500 and 5000 minutes respectively. The price tags for basic, crazy and insane bundles are Rs 1500, Rs 1800 and Rs 2100 respectively.

Individually, all the external and internal features, calculated separately, cost upwards of Rs 800. Provided that these features cost Jazz marginally less owing to mutual deals, this makes the voice and data bundles that Rox offers, nothing to write home about in terms of price. With other brands offering cheaper data and calls at comparable and lesser prices, convenience, simplicity and transparency are

the USPs of Rox’s

user experience.

The Launch-Strategy and Target Market

When a sentence has the words “vibe”, “Roxtar” and others, there is only one market that it aims to appeal to. And these digital brands seem to be going after that market only. That market is the Gen-Z. The Gen-Z, as many already know, is not just an age group. It is an urban demographic that belongs to the upper and upper-middle social strata of cities and have come off age recently.

This is the first generation that identifies itself with the digital age. According to PTA, 77% of smartphone users in Pakistan are between the ages of 21-30. This technologically literate, TikTok and Instagram addicted generation has the internet down there with water and oxygen in their Maslow’s hierarchy of needs.

The use of words in the ad campaign is just one element. The bold colours, flashy webpages and anti-design elements all exude a novelty that Rox associates itself with. Rox has made sure that its campaign also remains native to the internet. Just a month before the launch, it had the people guessing what the “Vibe” was. The marketing post-launch however has not only been subdued but also confusing.

“In Pakistan, with 64% of the population under the age of 30, there is a significant demand for digital-first experiences. ROX delivers a combination of content and services to engage the digital-first generation of the country. With Jazz’s wide portfolio of digital services and experience in providing a seamless digital experience to our customers, and with the learnings in our Group based on the

success of other digital-first brands, we are confident that we are uniquely positioned to meet this demand.” explains Kaan Terzioglu, CEO of VEON Group.

VEON’s Strategy

Jazz Pakistan (Formerly Mobilink) is owned by an international tech giant VEON. The company, headquartered in the Netherlands is one of the most successful companies operating in the space. Targeting almost 7% of the entire world’s population with its various telecom brands, VEON provides its services to more than 150 million customers worldwide.

The digital operator received GSMA’s Global Mobile Award for Best Mobile Operator Service for Connected Consumers with its Digital Operator 1440 model - DO1440, at the Mobile World Congress 2023.

In the Digital Operator 1440 model, Veon Group companies combine mobile connectivity with a complete digital product portfolio that suits local needs and services. This includes mobile financial services, entertainment, health, education and others. Veon said this model has led to greater engagement and value generation among Veon’s customers.

The launch of ROX is part of VEON’s digital operator strategy, or DO1440, and builds on the company’s success in pioneering other digital-first brands - IZI in Kazakhstan and OQ in Uzbekistan.

IZI, VEON’s first digital-first operator, has over 500 thousand monthly active users (MAUs). In Uzbekistan, the OQ was launched in October 2023 and had already gained 177 thousand MAUs by December 31st.

Conclusion

As of now Rox has made its impact as a digital-first telecom brand. But as past examples suggest, remaining ahead of competition is always the key to not just excel but also survive in the telco market. The ball is now in the competition’s court. Will ChinaMobile launch its first digital telecom in Pakistan, and bring its 5G-based “Cloud Phone” technology to rival the others?

Would Onic onboard external partners, to increase its service provision? Because for every bookme.pk, there is a Bookkaru, for every Careem there is an InDrive and for every Golootlo, there is Vouch365.

When it comes to technology, Jazz has always remained ahead of the curve, compared to the competition. It is therefore important to see how Jazz’s Rox performs over time, to maintain the same stature in the market. “ROX is available nationwide at all experience centres. We are planning nationwide new availability hotspots as well.”, stated the Rox spokesperson. n

TELCOS

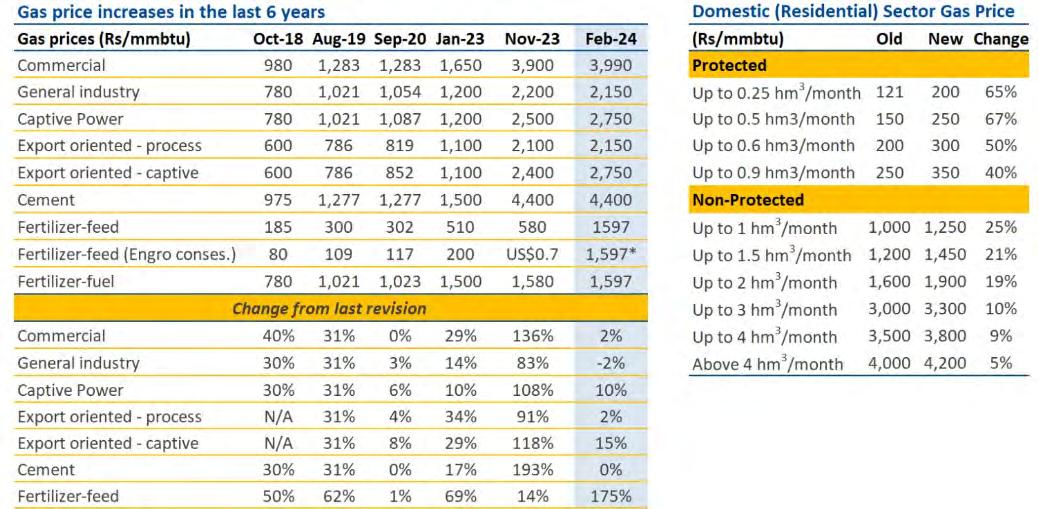

The recent change in gas prices has been welcomed by the fertiliser industry with one caveat

By Abdullah Niazi

Something strange is happening in Pakistan’s fertiliser industry. On the 15th of February the caretaker government announced a massive increase in the prices of gas, both for domestic and industrial consumers. The increase was part of an IMF mandated move to rationalise gas prices in the country and end the complex web of cross subsidies that the government provides to different industries through cheap gas.

As part of the increase, the price of gas to the fertiliser sector was increased from Rs 580 per mmbtu to Rs 1597 per mmbtu marking a sudden jump of over 175%. One would assume that the fertiliser industry, like most others, would be opposed to such a measure. After all, natural gas is the single biggest input cost for producing fertiliser, and increasing the price will without any doubt increase the price of Urea and DAP in Pakistan — the two major fertiliser products that are vital to Pakistan’s agricultural output.

In reality, most players in Pakistan’s fertiliser industry have long been calling for increasing the prices of gas and removing the subsidies that the industry receives from the government through discounted gas prices.

Since the increase, Engro has gone as far as releasing a press statement commending the increase saying the policy shift offers an opportunity for the sector to demonstrate global competitiveness without reliance on government subsidies. The government of Pakistan is also expected to save Rs 150 billion as a result. (Editor’s note: Don’t be fooled into thinking that Engro does not want any kind of government subsidy. It is just that they want the money to be spent more smartly.)

But there is a catch here. Right now two different realities exist for different fertiliser plants across the country. You see gas comes from two different sources to fertiliser plants. One is through the Sui Southern Gas Company (SSGC). The other is directly from the Mari gas fields through Mari Petroleum. The problem is that the increase in price has only been notified to the SSGC, meaning Mari is providing gas at the same subsidised rate as before.

And there are some that are getting more benefit from this arrangement than the others.

Why gas is important

There are a few things to understand here about the fertiliser business. For starters, gas is a major input. In fact around 80% of the cost of making fertiliser is the cost of gas. This means that the

price of fertiliser on the market is directly dependent on the price of gas that the company is receiving.

Most of the gas that fertiliser companies get is indigenous. It is also low grade gas that would be unusable for domestic consumers. For a very long time this gas has been provided to the sector at a subsidised rate. The idea was that to promote farming in the country, a subsidy should be given directly to fertiliser manufacturers so they could then pass on this price cut to farmers. Now remember, the demand for fertiliser does not grow with the population as happens with the demand for food. Instead, the fertiliser industry is dependent on how much land is under cultivation in a country.

This means that within the fertiliser business there is really only one way to make money: Efficiency. If all companies are being provided the inputs (mainly gas) at the same price, then it is a question of which company can use the least amount of gas to make the most fertiliser. They can do this with latest production techniques, updating their machinery, and finding the right experts. All of that is irrelevant. The point is that a fertiliser company’s success depends on how well they can make and market their product. But for this ideal situation to be in place, there has to be a level playing field.

20

Different players different rules

Let’s take a small break from the fertiliser business and look instead at Pakistan’s gas supply. We don’t have a lot of it and we use it like we do. The reason the IMF wants to address the issue of gas prices is that Pakistan is using its natural gas in very unproductive ways. For example we provide gas to domestic consumers who use it to heat their water and cook their food. In the winter months when the domestic demand increases, the government scrambles to find ways to provide it because not doing so would hurt their vote bank. It is a populist curse.

What the IMF wants and what the government is begrudgingly trying to do is find the best use for every molecule of gas we have. And the general consensus is that it should be provided to industries such as the textile industry or the fertiliser industry that can

either boost exports or food production. Now even within industrialists and commercial users there are different categories and webs of cross subsidies that are sometimes difficult to understand.

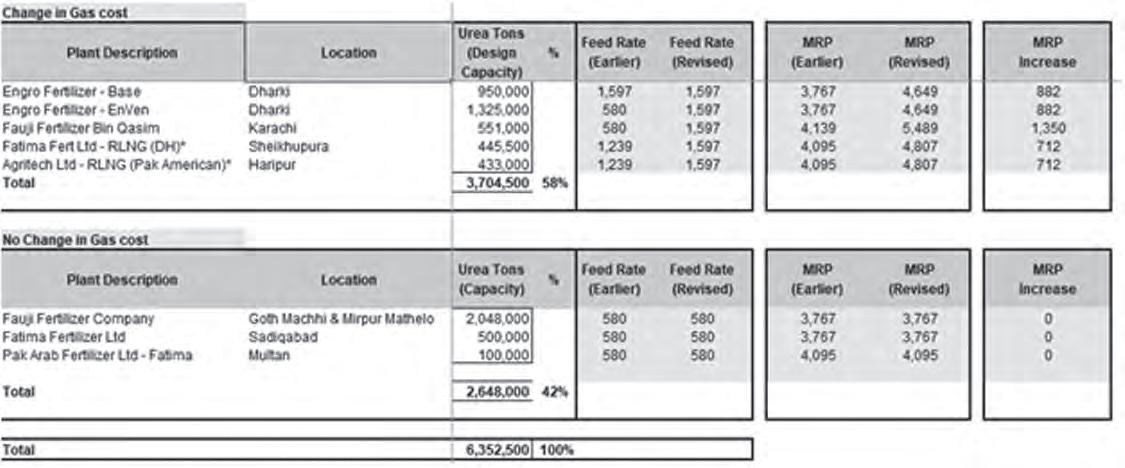

As we’ve mentioned, the fertiliser industry was getting gas at Rs 580 per mmbtu which has now been increased to Rs 1597 per mmbtu. But it hasn’t been done across the entire industry. You see 80% of the gas that comes to fertiliser plants comes from the Mari Gas fields. While the source is the same, there are two different pipeline networks through which this gas is provided to the fertiliser plants. One is the network of the Sui companies and the other is Mari’s own network.

There are currently ten fertiliser plants in Pakistan. Out of these, six of them receive dedicated supplies from Mari’s network. The remaining four are provided gas through the network of SSGC. Of these six fertiliser plants receiving a dedicated supply from the Mari network, a majority belong to Fauji Fertilis-

er. Back in December 2023, some of this was rationalised when the price for three of these plants was increased from Rs 580 mmbtu to Rs 1580 mmbtu.

In the recent price increase, however, the remaining three Mari network plants are continuing to get gas at the older rate of Rs 580 mmbtu. These three plants belong to Fauji and Fatima Fertiliser, while Engro has entirely been shifted to the Rs 1597 mmbtu price.

This means that while gas prices for SSGC and SNGPL network have increased by around 200 percent, the manufacturers on Mari network (FFC and Fatima) are still receiving gas on the subsidised price of PKR 580/mmbtu.

“This discriminatory gas pricing in the industry has led to multiple prices in the market and will not help the government achieve its fiscal objectives,” said Engro Fertiliser’s CFO Ali Rathore in a recent media interaction in Karachi.

But why the discrepancy? “All suppliers have their own cost of gas purchases which is to be fully recovered from consumers,” explains one senior government official. “For SSGC/SNGPL it is Rs. 1597/mmbtu. For MPCL, there are two gas costs i.e. Rs. 555/ mmbtu and $5.6/mmbtu. Recently price for SSGC/SNGPL based plants has been revised to Rs. 1597/mmbtu i.e, Fauji Bin Qasim (w.e.f 01.02.24), Engro Enven (w.e.f 01.03.24), FatimaFert and Agritech Rs. 1597/mmbtu w.e.f 01.04.24. The gas price for 4 plants i.e FFC I to III and Fatima Fertilizer was revised to Rs. 580/mmbtu feed and Rs. 1580 for fuel on October 23 but its lower than Rs. 1597 price. Engro (base plant) and PakrArab Plants have signed contracts for purchase of gas at $5.6/mmbtu. If the government decides to designate one gas supplier for all plants then one gas price concept can be worked out.” n

ENERGY

Is PTCL throttling one of its competitors through anticompetitive practices?

This isn’t the first time the state-owned company has done this. And this isn’t the first time they would get away with it

This isn’t the first time you will read about the anticompetitive market practices of the Pakistan Telecommunication Company Limited (PTCL). The majority government-owned telecommunication company has been accused of abusing its dominant market power to resort to predatory pricing, collusion and using underhanded tactics to maintain its monopoly more than a few times.

For instance in 2006, PTCL was taken to the Competition Commission of Pakistan (CCP) for charging abnormally high bandwidth tarriffs to internet service providers. In 2010, Internet Service Providers Association of Pakistan (ISPAK), LINKdotNET and Micronet filed a complaint to the Pakistan Telecommunication Authority (PTA) in which they accused PTCL of charging very high wholesale internet bandwidth tarrif due to which operators were suffering losses.

In 2012, the CCP found out that PTCL had abused its dominant position in the market for the provision of DSL services through the practices of predatory pricing and refusal to deal, ultimately resulting in forcing five out of 11 of PTCL’s competitors out of market.

In 2013, PTCL was fined a massive Rs8.30 billion for violation of Competition Act. In 2016, PTCL was accused of colluding with Bahria Town to keep internet service providers from laying fiber infrastructure, giving PTCL a monopoly in Bahria Town.

In yet another instance of abuse of dominant position, PTCL has been accused of throttling another one of its competitors, Nayatel, through aggressive pricing and forcing other vendors to not sell services to Nayatel.

PTCL versus Nayatel

So what happened now? In a letter written to the Pakistan Telecommunication Authority (PTA) on February 14, 2024, Nayatel accused PTCL of not

only selling it wholesale internet bandwidth at exorbitant rates, it was also forcing others to not sell it to Nayatel.

Internet service providers like Nayatel buy internet bandwidth on wholesale rates from providers like PTCL and then sell the internet to consumers on retail rates. There are only two wholesale internet bandwidth providers through undersea cables in the country. which are Pakistan Telecommunication Company Limited and Transworld Associates. Nayatel had been buying internet bandwidth from both the providers but drew back from PTCL in November last year because of high prices charged by the monopolist.

Now here is what the internet service providers do: to add redundancy in their network, that is to say providing multiple paths for traffic so that data can keep flowing in the event of a failure, they try to get the internet bandwidth from more than one providers. Nayatel tried to do that. It tried to get the internet bandwidth from Zong and Telenor, both of which buy the internet bandwidth from PTCL and then resell it.

However, Nayatel alleges it found out during testing with China Mobile Pakistan that PTCL was not allowing Nayatel’s IP addresses advertised by CMPak. According to details in the letter, despite repeated requests by China Mobile Pakistan, PTCL did not allow Nayatel traffic to pass through its network, obstructing Nayatel to buy bandwidth at competitive prices. A copy of an email from Zong, available with Profit, reads that Zong was unable to get Nayatel’s IPs approved from PTCL and hence could not proceed with Nayatel’s request of giving it the internet bandwidth as a reseller from PTCL.

Likewise, Nayatel also alleges that PTCL refused Telenor to allow Nayatel IPs through Telenor on PTCL’s network. According to Nayatel, the excuse PTCL has for holding others from providing internet to Nayatel is because they had commercial agreement with Zong and Telenor that they

will not resell PTCL’s bandwidth to PTCL’s existing customers.

Nayatel contends, however, that it isn’t PTCL’s existing customer anymore but the state-owned company was still taking such coercive measures in garb of commercial agreement, which is illegal according to the PTA and CCP laws.

Why else could PTCL logically be doing this? To force Nayatel to buy the internet bandwidth from PTCL directly, rather than through the two resellers, at inflated rates which had already pushed Nayatel to withdraw from PTCL earlier. And why would PTCL be selling the wholesale internet service to Nayatel specifically at inflated prices? Because Nayatel is not only a customer but also a competitor of PTCL.

In conversation with Profit, Wahaj Siraj, the CEO of Nayatel said that his company competed with PTCL in fiber to the home (FTTH) market, which is broadband service provider through optical fiber. According to Wahaj, it is a market with a total of around 1 million broadband customers in which PTCL has around 400,000 active customers and Nayatel has 160,000. The other providers in this space are names like Stormfiber, Transworld, Wateen and Multinet. The case of PTCL throttling only Nayatel’s internet is reportedly not the c ase with other broadband providers but Nayatel does complain that while it is being throttled, PTCL is selling internet bandwidth to some of the other providers on favourable rates.

No response has yet been received by PTCL on the issue.

There hasn’t been a strong directive from the Pakistan Telecommunication Authority, the telecom regulator. According to a letter seen by Profit, the PTA has only asked the relevant stakeholders; PTCL, Nayatel, Zong and Telenor to resolve their issues withing three working days. But that is perhaps what the PTA can at most do. PTCL has earlier been able to block moves by the PTA as well as the CCP by taking stay orders from the court. n

23

Can Legends tap Pakistan’s untapped sports potential?

This new stadium in Karachi has unveiled the long ignored potential of commercial sports facilities in Pakistan

By Nisma Riaz

If you are a resident of Karachi, who has been to DHA’s Khadda Market before summer 2023 and haven’t visited again, you’re in for a surprise. And if you did go back to Khadda Market after August 2023, you were most likely taken aback by how the place has drastically transformed from a dead end to a lively neighbourhood.

All thanks to the Legends Arena.

This new stadium in Karachi is perhaps the largest commercial sports facility in the country and the ripples of its impact have been far-reaching. If its popularity is anything to go by, the new stadium did not only unlock the potential of commercial sporting facilities in the city, but also unintentionally and quite unexpectedly had a positive impact on the surrounding market.

The Legends Arena offered to the people of Karachi something they did not realise they even needed– a membership-free club that offers an array of sports, along with a welcoming environment, giving recreation a new meaning to the city’s inhabitants.

Allow Profit to take you on a virtual tour of the Legends Arena through this article.

What is the Legends Arena and what makes it so legendary?

In conversation with Profit, the chief executive officer (CEO) of Legends Arena

Talal Shah Khan shared that the primary goal behind introducing Legends Arena was to develop sports infrastructure in Pakistan that accommodates a large number of people, addressing a significant gap in available facilities. He believes that Legends Arena is actively

transforming and modernising recreational sports activities and facilities throughout Pakistan. In agreement with Khan, Yousuf Ghaznavi, CMO of Legends said, “The potential of building commercial stadiums, like Legends, in Pakistan is huge!”

Currently, there is a huge void in the market when it comes to commercial sports facilities. Even though there are quite a few facilities, especially in Punjab, there is still a lack of infrastructure that would satisfy international standards. Moreover, existing facilities in the country lack proper management systems for professional coaching or mentorship.

However, the Legends Arena owes its popularity to one niche sport– Padel Tennis.

Even though there were a few residential padel courts installed in Pakistan, there were no commercial courts that could be accessed by everyone and by bringing padel to the country, Legends set itself up for unexpected success.

“We have established the first commercial padel courts in the country at the Legends Arena in Karachi, marking a noteworthy milestone. Our expansion plans include reaching various localities, locations, and cities, which demonstrates our commitment to making recreational sports accessible across diverse regions,” said Khan.

Adding this Khan’s point, Ghaznavi highlighted, “Our expansion plans are in place and headway has been made to take Legends Arena pan Pakistan. Lahore, Islamabad, Faisalabad, Hyderabad and Peshawar are some cities where we are in talks for expansion.”

Let’s start from the beginning.

The parent company of Legends Arena, TS Builders, is a company that specialises in sports construction dating back to 1983, having successfully completed over a thousand projects throughout Pakistan.

Ghaznavi told Profit, “In terms of specialisation, the company not only constructs but also operates the facilities. To streamline these

efforts, a distinct entity named Total Sports was established, focusing on sports facility construction and management. It’s noteworthy to mention that Total Sports emerged from the legacy of TS Builders, underlining the extensive experience in construction.”

In the Total Sports framework, Talal Shah Khan, the CEO of TS Builders, is also the CEO Total Sports. Meanwhile, Jahangir Khan, the renowned squash legend, is not only one of the directors, but also serves as the chairman of Total Sports. This strategic collaboration and integration of roles have facilitated the seamless execution of various projects, according to Ghaznavi. According to the founders, the city requires about 15 or 16 similar facilities to meet the needs of the large population.

Khan proudly shared, “We take pride in being the benchmark facility, prompting others to consider creating spaces of standard quality, even in limited areas, to enhance people’s enjoyment of sports.”

“The stadium was also made with the idea of having a padel court. Initially the idea was to have about four padel courts but since we were coming to the market for the first time, we started with two and based on the reaction, we have now installed five padel courts,” Khan highlighted.

TS Builders always knew how to make top-notch sports places on a global level. The only thing holding them back was finding the right land. “We’ve been thinking about making something big, meeting international standards, for the past five years. Finally, we decided to go for it,” chimed Ghaznavi, adding that, “We chose a piece of land that had been barren for over 20 years – it used to be an abandoned hockey stadium, mostly unused, only occasionally for carnivals or weddings.”

Even though the defining feature of the Legends Arena has now become padel tennis, considering that it houses the best courts in

24

Our futsal turfs hold FIFA approval, the basketball and multipurpose turfs are endorsed by various federations, and our cricket turf mirrors the one used by the English cricket board in their indoor facility. Even the multi-purpose turf is approved by the tennis federation. While these investments may seem significant, they align with our mission for long-term sustainability, emphasising a focus on enduring quality rather than immediate returns on investment

Talal Shah Khan, CEO of Legends Arena

the city, the initial idea, however, wasn’t just about padel sports. They wanted to create a place with facilities for various sports. Currently, Legends Arena has four football fields, one multi-functional field where you can play volleyball, cricket, hockey, and tennis. They also have two indoor cricket arenas, enclosed on all sides to keep the ball in play. And obviously the five padel courts that are the USP of the stadium.

“We also added a 330 metre jogging track and within it, a 100 metre sprint track with five lanes. This setup allows us to host school sports days and other events. The facility itself has seating for about 1200 people, making it perfect for hosting events because it’s so spacious,” Khan said, adding that sometimes people even book the entire stadium to host wedding events, such as a game night between the bride and the groom’s families.

Because of such high demand, the stadium is not only functional around the clock, but also offers different price options, depending on the timings and the days. Unlike exclusive clubs and membership-based institutions, Legends caters to diverse schedules, including early morning activities.

A state of the art facility

The Legends Arena is structured into three phases. The current phase, phase one, is the complete outdoor facility. The second phase will introduce an upcoming gym building housing a full fledged gym, multipurpose fitness studios, crossfit and a sports rehabilitation centre, while the third phase will feature a substantial indoor children’s play area. This space will encompass a large jungle gym with an inflatable zone, a trampoline area, and a Ninja Warrior park, covering about 20,000 square feet. It’s set to become one of the largest indoor sports facilities in Pakistan, according to Khan.

In terms of financials, the investment required for phase one was around Rs 150 million, or slightly more due to currency devaluation. Similar amounts will be invested in both phase two and phase three, reflecting a significant overall investment of over Rs 450 million to build the entire facility. “Despite the substantial costs, our city has a strong appetite for entertainment. Traditionally, food has been the primary form of entertainment here. Many venture into the restaurant business, which can be risky as initial success may decline without a consistent customer base,” Khan explained.

Ghaznavi, adding on to Khan’s point, said, “And we’re not looking to exit quickly, right? So, it’s a long-term play. We don’t want to launch a business, get the money out and go. Hence, we’ve invested a lot and it’s on the higher side for a reason.”

Prioritising quality in their facility by investing in durable turfs that meet international standards, Total Sports has been a game changer for Pakistan’s recreational sports scene. “Whether it’s for padel, cricket, futsal, or the multi-purpose turf accommodating various sports, all our turfs are accredited and approved by the respective sports governing bodies. Despite the higher cost associated with certified and internationally recognized turfs, we were committed to delivering top-notch facilities without cutting corners. Notably, none of the smaller facilities in the city boast these accredited turfs,” Khan explained. And this is, perhaps, why the Legends Arena has become so popular among its regular visitors. Some individuals who frequent the arena have drawn parallels with facilities they had only visited abroad.

“Our futsal turfs hold FIFA approval, the basketball and multi-purpose turfs are endorsed by various federations, and our cricket turf mirrors the one used by the English cricket board in their indoor facility. Even the multi-purpose turf is approved by the tennis federation. While these investments may seem significant, they align with our mission for long-term sustain-

ability, emphasising a focus on enduring quality rather than immediate returns on investment,” Khan concluded.

This explains why, currently, the stadium is operating on a net size, but considering the substantial investment made, it will take some time to break even. However, they insist the potential is significant. “We’ve become a trendsetter in the market, being emulated by others, which is always a positive thing,” Ghaznavi exclaimed.

Weekdays, peak hours, and off-peak hours, each have varying costs. “The facility is well-lit even at night, incurring additional electrical expenses. To address this, the venue has been equipped with solar panels, aligning with a focus on renewable energy and reducing operational costs,” Ghaznavi pointed out.

Lastly, Legends has given special attention in building something that most facilities have way below on their priority list; bathrooms and changing rooms! “Special attention has been given to the changing facilities and showers, ensuring a state-of-the-art and high-quality experience for users,” Ghaznavi highlighted.

The stadium has drawn nothing but a positive response from the people of Karachi. A response which has been possible due to the meticulous attention to detail characterising every nook and cranny of Legends Arena.

Forging productive partnerships

The Legends Arena has not only introduced the highly addictive sport of padel to Pakistanis, but also done valuable work for the sports community, providing people with the opportunity to be better at the sport they enjoy.

They have collaborated with some schools to utilise the facility, addressing the challenge many educational institutes face in lacking sufficient space for proper games. This partnership enables schools to access quality

SPORTS

sports facilities for their students.

Ghaznavi shared, “We are in discussions with educational institutes, we plan to offer sports scholarships, a novel approach in Pakistan. Unlike traditional scholarships, we not only assess talent but also provide training facilities. The unique aspect is offering not just scholarships based on talent but also dedicated training spaces. Seeking partnerships with corporate entities with CSR budgets, we aim to expand our initiative, contributing to the development of underprivileged and privileged youth excelling in sports.”

Legend’s Youth Development Program, a CSR initiative, supports talented underprivileged and privileged individuals in sports, guiding them from grooming to skill development. Led by experts like Adil Rizki for football, Shahid Afridi for cricket, and mentorship from Jahangir Khan, the program provides comprehensive training, according to Khan.

“Our academy collaborations further enhance our sports offerings. Shahid Afridi is heading our cricket operations, launching his academy in partnership with Legends Arena for the first time. The cricket academy provides a platform for aspiring cricketers,” Khan said.

Adding, “For football, we have partnered with Karachi City Football Club (KCFC), led by Adeel Rizki, who not only heads the academy but also serves as the head coach of the women’s national team. In alignment with our commitment to promoting sports and empowerment, we extend our facility to the women’s team, offering it free of charge for their camps and training. KCFC’s women’s team also benefits from training here at no cost.”

Nameer Shamsi Tennis Academy also collaborates with Legends for tennis operations and coaching, including padel coaching. While in squash, they have a collaboration with ASB Squash, a company associated with Legend’s parent company. It has led to the creation of around 800 squash courts across Pakistan. “The chairman of our company is the renowned Mr. Jahangir Khan, a true legend in sports. Holding the remarkable record of being undefeated for 555 consecutive matches over 10 years, he earned the title of the true legend. With his association, our brand derives its name, JK 555, commemorating his unparalleled achievement,” Khan concluded.

By getting experts from all over the sports industry and forging productive partnerships, Legends Arena aims to provide the best sports facilities and training to its clients.

Interestingly, Total Sports is also exploring the option of franchising. “We have established a franchise model, similar to multinational chains like McDonald’s or KFC, and other local brands, expanding across different locations. Under this model, we encourage investors to join our pool, contribute funds, and

We’re not looking to exit quickly, right? So, it’s a long-term play. We don’t want to launch a business, get the money out and go. Hence, we’ve invested a lot and it’s on the higher side for a reason

Yousuf Ghaznavi, CMO of Legends Arena

allow us to oversee services, manage facilities, and construct the necessary infrastructure.”