08 08 Last call for Summit Bank and Silkbank in new IMF commitments 10 Crop damage: The case of onions 16 16 Floods and microfinance: Lessons from the past Ammar H. Sheikh 18 The lost glory of I. I Chundrigar Road Ariba Shahid 20 Astounding damage to agriculture needs immediate response Uzair Younus 22 22 Demystifying Pakistan’s high electricity prices Jalees ur Rehman 24 Cards not accepted here: Why fuel stations are turning on digital pay28mentsWhy are some cars being sold for below showroom price 24 28 10 CONTENTS Publishing Editor: Babar Nizami - Editor: Khurram Husain - Joint Editor: Yousaf Nizami Assistant Editors: Abdullah Niazi I Sabina Qazi - Sub-Editors: Mariam Zermina | Basit Munawar Editor Multimedia: Umar Aziz - Video Editors: Talha Farooqi I Fawad Shakeel Reporters: Ariba Shahid I Taimoor Hassan l Shahab Omer l Ghulam Abbass l Ahmad Ahmadani Shehzad Paracha l Aziz Buneri | Maliha Abidi | Daniyal Ahmad | Ahtasam Ahmad | Asad Kamran Chief of Staff: Maliha Abidi - Regional Heads of Marketing: Mudassir Alam (Khi) | Zufiqar Butt (Lhe) | Malik Israr (Isb) Business, Economic & Financial news by 'Pakistan Today' Contact: profit@pakistantoday.com.pk Profit

FROM THE EDITOR Khurram Husain Editor

Above all else, the flooding disaster to hit Pakistan is about climate change

How do you plan for a 100-kilometre wide inland lake that has opened up in Sindh as the flood waters roared down the Indus? The lake has been pictured by NASA’s MODIS satellite and the image carried by major international media and beamed around the world. Millions of people live in the area that the lake has now covered. The city of Dadu alone is home to an estimated 1.5 million people if you include the rural areas around it, and it is currently under eight feet of water as per news reports. What kind of zoning regulations would have saved this area from the devastation? What kind of infrastructure would have prevented the flood waters from reaching this catastrophic level? Do people who are advancing the “governance” argument seriously think that Pakistan should evacuate entire cities as part of a flood mitigation plan? Or should the government try to wall up the Indus river south of Chashma so it can carry over a million cusecs of water without breaching any embankments?

7 Editor’s note

It is true that superior governance could have played a role in mitigating some of the damage, but this would have been on the mar gins only. How much lower would the floodwater deluge in Dadu be with superior governance? Perhaps, instead of being eight feet underwater, it would have been only seven feet? Given superior governance, perhaps, instead of one third of the country being flooded, this would have been 29%? Or 25%? Maybe residents in Swat would have received an alert about a possible flood 48 hours ahead of time instead of one hour, but by how much would the devastation have been reduced? If illegal construction had not been allowed close to the river it would undoubtedly have reduced some of the devastation. But images from places like Bahrain in Swat show devastation in the main bazaar that make the place look like a war zone. Of course superior governance could have mitigated some of the damage. But the scale of the disaster would still have been massive.

With one third of Pakistan submerged as a result of the floods, it is hard to figure out what type of “governance” could have prevented this disaster. Those pointing out that the problem with the unusually massive rainfall and the resultant flooding in the country is primarily a “governance” problem need to first take stock of things before running too far with this argu ment. Of course, superior governance – such as improved forecasting, faster response times at the local level, better zoning restrictions along floodwater evacuation channels and other such measures – could have reduced the number of people impacted and perhaps, mitigated some of the damage caused by the floodwaters. But this argument should not be allowed to overshadow the more massive truth here; that the rains were so intense, and the quantity of water they dropped on the country so massive, that no amount of superior governance could have miti gated the disaster in any significant way.

Let us all be very clear in assessing what has just happened in Pakistan. The country has been hit by a climate-related catastrophe so massive that even the best run country would struggle in dealing with it. We must ask our rul ers to take climate change more seriously and do more to build resilience in our country. But that will not solve the problem. It will only reduce its impact by a little bit. Above all else, this is about climate change.

Climate change vs Governance

Govt commits to send both banks into “resolution” capitalization problems

if longstanding

Last call for Summit Bank and Silkbank in new IMF commitments

are not sorted by March 2023

8 BANKING By Khurram Husain

The government has committed to the IMF that Summit Bank and Silkbank will be sent into “resolution” by May 2023 if they don’t complete the first stage of their recapitalization plan by March of the same year. If this happens, these banks could be the next to be forcibly restructured or even sold off altogether like KASB Bank was in 2015. “We remain closely engaged with two undercapitalized private banks and are committed to ensuring compliance with the minimum capital requirements” the government says in the Memorandum of Economic and Financial Policies released late on Thursday night. The two banks are not named but it is clear it is Silkbank and Summit Bank being referred“Dueto. to unanticipated delays in the process, the first-stage recapitalization of the two private sector banks will not be completed on time” it continues. The “first stage recapi talization” plan requires an injection sufficient to cover 50 percent of the capital shortfall for both banks as of September 30, 2021, according to the MEFP. It is not clear from the language which capital shortfall is being referred to. Banks are required to maintain a Minimum Capital Requirement of Rs10 billion, and various Capital Adequacy Ratios have to comply with standards that measure capital against Risk Weighted Assets. A State Bank source told Profit that the minimum capital being referred to in the IMF document was neither one of these two, but would not specify further except to say it is connected with the Net Assets on the banks’ balance sheets. “On March 18, 2022, a public offer was made for an equity injection into one of the private banks” the MEFP continues, referring to Summit Bank’s announcement to its share holders that UAE national Abdulla Hussein Lootah had agreed to acquire 51 percent shares in the bank. Based on the numbers of shares being acquired and the price offered, Lootah’s capital injection into Summit Bank would have been exactly“However,Rs15bn.the process could not be completed by end-May because of a legal dispute. The legal dispute is expected to be resolved shortly paving the way for equity injection, which would likely result in the bank achieving positive capital by end-September 2022, meeting the first stage recapitalization requirement” the MEFP says. But things are more uncertain for Silkbank, owned largely by former finance minister Shaukat Tarin. “For the second private bank, the capital process was hampered but the bank has now identified an investor and a public announcement of intention has been made for an equity injection on May 31, 2022”. In May of this year Silkbank announced to its shareholders that M/S Park View, owned by estranged PTI politician Aleem Khan, had offered a capital injection of Rs12bn against 51 percent shares in the bank. Both deals are subject to State Bank approval, particularly the rigorous “fit-andproper” test, where the regulator uses strict standards to determine whether the applicant is trustworthy enough to be allowed to hold the general public’s deposits against a banking license. Aleem Khan is facing a NAB case in La hore which could complicate his application.

Once these deals are completed “the first-stage recapitalization of both banks will be complete by end-March 2023” the MEFP says. This was originally a structural benchmark in the MEFP signed by Shaukat Tarin himself back in January, and was supposed to be completed by May. This time the MEFP has gone a step further. Should the recapitalization plans not materialize, it has committed to the fund that both banks will be moved into “resolution”, a process that could potentially see a forced restructuring, amalgamation or outright sale. “[W]e will initiate orderly resolution of either or both of these two banks by end-May 2023 should remaintheyundercapitalized at that point” the MEFP says. This is the first time the government has set a deadline for these banks to bring their capital ratios into compliance or face punitive action, possibly of the sort that was taken against KASB in 2015, when the whole bank was sold to Bank Islami for Rs 1000. Both banks have seen their Tier 1 capital fall massively against their Risk Weighted Assets in the past few years. Summit Bank has seen its CAR drop from negative 46pc in 2020 to negative 65pc in 2021, according to the bank’s annual reports. Much of the deteriora tion in its Tier 1 capital appears to be driven by unappropriated losses and regulatory adjust ments.Meanwhile, Silkbank saw provisions and write-offs on bad loans jump from Rs2.4 billion in 2019 to Rs9.9 billion in 2020 (the last year for which the bank has filed any results), leading to its loss after tax to rise by 66 percent in that year. “Provisions were taken against specific borrowers engaged primarily in the real estate businesses which were secured against mortgages of land,” the bank said in its Annual Report for 2020. To restore its capital, the bank claims it is working on “recovery of real estate loans along with non-banking assets held by the bank, through the Development Real Estate Investment Trust (REIT) schemes” along with seeking a Rs12 capital injection from real estate magnate Aleem Khan, to whom the bank had sold its headquarters back in 2015 for Rs2.37 billion. The balance payment of Rs2.25 billion from that sale had not come in till 2020, when it was due. The Annual Report said only that “the agreement is further extended for the period of one Silkbank’syear.”capital adequacy ratio has fallen from 10.92pc in 2018 to 5.81pc in 2019 to negative 4.45pc in 2020. In that same year, its Minimum Capital Requirement was short by around Rs6.5bn from the requirement of Rs10bn. n

10

COVER STORY

The child handed the onions over to his father. “These are the only ones I could find, the others are all gone,” he said. That, as Salim tells it, is when he finally wept. Both for the crop that was lost and for the aeons it would take for both the farm and its people to recover from the destruction. “The Baloch country is arid. Rain-fed areas are regularly short of water since most water channels belong to the sardars. But the onion is a special crop to us. Not only does it grow on our land, it thrives here more than anywhere else.”

The onion, as Salim explains it, is a rough vegetable by the time it is harvested but incredibly delicate during its growing period. The stem hold ing the bulb is fragile, and a single tread too heavy can dislodge the onion and wilt it within hours. Still, Salim held his nerve. When the rains went on for a week, the hill torrents in the north came crashing down and the water started piling up on his farm, he knew the crop was gone. His wife was concerned, pacing up and down. Still Salim did not shed a tear.

Onions make you cry. Whether you’re making an omelette, or preparing a salan, the moment you cut into the onion, its cells release a compound that is a form of sulfuric acid. The fumes rise up and irritate the nerves around the human eye, causing it to water up. Of course, onions can make you cry for other reasons as well. In Balochistan’s Chagai district, Salim Ahmad tells us the story of the first time he cried during this year’s flood. It was late early August, and the rains had been pouring down for over a week at that point.

The impact of the destruction of the onion crop will be far reaching in Pakistan

The onion is a much bigger deal than one might think. Calorically, it is not the most nutritious or efficient food. Onions are nearly 90% water, and raw onions contain only 40 calories per 100 grams. By fresh weight, it contains 89% water, 9% carbs and negligible

By Abdullah Niazi

12

It was near the 10th day, when the rain abated for a moment that Salim and a few of the people working on the farm went out to see wheth er anything could be salvaged. “One of the farm workers had his young son with him. The boy had never seen anything of the sort, when we were inspecting one cluster of the onions, he wandered off without anyone notic ing. When he came back, he had with him exactly three dented onions that he found floating or submerged in the water.”

The Pakistani onion

The weepmakeonionswaysmanyyou

A majority of this year’s onion crop has already been decimated, and prices have already shot up in urban markets by more than 40%, and will continue to do so, even as the government is banking its hopes on importing onions and tomatoes from across the western borders with Iran and Afghanistan. While import duty has been removed on these two products, it will still mean a major staple good will see significant inflation.

Chagai was one of the first places to be hit by the floods in Baloch istan. On the first day of the monsoon, Salim remembers thinking these were some of the heaviest rains he had seen in his lifetime. By day three, he knew it would be disastrous for the onions and melons he was growing on nearly 12 acres of the land he manages.

And it may not be just Salim that is crying. The onion supply-chain is susceptible to delays and difficulties in good years, particularly in the winter months when the onion has to be imported. In the months to come, the extent of the damage of the floods will become clear. With Sindh and Balochistan, the two main onion providing provinces, entirely devastated rising prices of onions will cause strife both in urban and rural areas.

COVER STORY amounts of fibre, protein, and fat. But along with tomatoes, onions hold a unique place in Pakistan’s culinary (and hence its agricultural) space. As one of the main components of salan, onions are in-demand throughout the year. For most months, locally grown onions are enough to meet the demand. Onions are grown on around 136,000 hectares of land, with the 2020 figures showing a total yield of 1.74 million tonnes across all the provinces and regions of Pakistan.The citadel of this humble condiment is Sindh, which contributes about 38% in area and 44% in onion production of the country followed by Balochistan which contributes about 21% in area and 33% in production. Punjab actually has more land dedicated to growing onions than Balochistan, but because the province has lower yield and produces a drier, less-red variety of onion its yield is less. Overall, the average yield in Pakistan stands at an estimated 12.8 tonnes per hectare. The province-wise breakdown of onion yield presents a fascinating picture. The latest available data is from 2016-17, but according to officials from the Ministry for National Food Security the patterns of onion production have not changed significantly in the past five years. Balochistan has the highest yield per hectare with 18.8 tonnes per hectare, while Punjab has the lowest yield at a measly 7.3 tonnes per hectare. KP also has a high yield at 16.4 tonnes per hectare, but has the lowest area that is under cultivation at only 12,300 hectares under cultivation.Forall intents and purposes, onions are grown in Pakistan in what can only be described as three clusters. Much like there is a ‘kapas’ belt running from South Punjab to Sindh and a mago belt running alongside the Indus through the same region, onions have their select regions. The cluster in Sindh consists of Mirpurkhas, Umerkot, Jamshoro, Matiari, Sanghar and S. Benazirabad with Mirpurkhas as its centre point. In Balochistan, Changai on the tip of the Balochistan tail is the onion headquarters, with the cluster stretching eastwards along Mastung, Kalat, Turbat, Nasirabad, Kuzdar, Kharan, Quetta and K.S. Ullah.

The woes of the onion These nearly 13 tonnes of onions that Pakistan produces are usually enough for most part of the year. However, because onions are such a staple requirement throughout the year and an im portant caloric input in the average Pakistani diet, they are needed throughout the year. That is where the clusters come in. The cluster districts in Sindh are the tail area of all the canals and mostly soil of the district is sandy loam to clay. In the cluster, sugar cane, banana and many other vegetable crops are grown with onion crops. The main focus of Sindh cluster is international markets through ships or cargo services. The nearest domestic markets for KP clusters stretch from Islamabad to Lahore. The Baluchistan cluster covers the urban centres of Sindh and South Punjab. The cluster has a lot of potential. For the export window, the Sindh cluster can reach European and Middle Eastern countries. The Swat cluster can position itself for the China market, while the Balochistan cluster can target the Middle East Unfortunately,markets.however, the supply of onions has been dogged for a while. The last time modern varieties were introduced successfully in the country was in 1992. In our three clusters, Pakistani onion growers almost exclusively focus on red onions. In these, there are four varieties. There are the Nasarpuri and Phulkari which are grown in Sindh largely, and were a modern variety introduced in the 1980s. Then there is the Swat-1 variety which was introduced in 1992 to bolster production in the Swat and Balochistan regions. A lot has changed since then, especially with regards to the climate but more resistant varieties have not found their way to the market. Back in the 1990s, the effect of the new variety was clear. In the period following the introduction of the Swat-1 variety, from 1993 to 1999, there was a significant increase in both the area under yield for onion production and the overall yield per hectare. Onion varieties cultivated by farmers originate from a smaller pool of genetic material, which degenerate and degrade overtime, and there is very little infrastructure to replenish them. According to a report of the Planning Commission from 2020, “The Pakistan Agricul ture Research Council (PARC) has regularly failed to supply sufficient germplasm and develop new onion varieties. The available resources are spent on buildings, personnel and over heads, and there is no money left for research and development. This means highly qualified scientists are just sitting at their desks.” This is not where the failings end. Seeds used and distributed are subpar, farmers are giv en the wrong kind of fertilisers by self-serving commission agents, and all in all the crop suffers where the area and yield both could be much higher. Onions are harvested manually in all

*All data, facts, figures, and tables have been taken from the Planning Commission of Pakistan and the Ministry of National Food Security & Researc

In recent years, the overall area that has been under yield for onions has fallen. People in the onion business claim that it is no longer a reliable source of income because of the shortage of water. Due to shortage of the crop, the price of the produce in the local market was higher than the last couple of years. While the onion could actually be a major export oriented crop for Pakistan, it is instead languish ing with its export potential not even close to reached.There is a clear path ahead of us here, and there are not really any two ways about it. On the one hand, we can choose to fund agricultural research, improve the linkage between farmers and research bodies, and see Pakistan becoming not just stable on the food security front, but also hopefully in a position to be able to export as well. The other path is continued apathy, on which we have been for decades. The results will not be pretty. And yes, it will be more than the onions making us weep then. n

The government has gone back to relying on imports to try and cut the prices. They have also exempted sales tax and withholding tax on the import of tomatoes and onions for a period of four months, especially from Afghanistan and Iran, to arrest the skyrocketing prices of the vegetables in the domestic market in the aftermath of heavy rains and floods.Perhaps the biggest window into just how serious the shortage could be is that the government may have to consider the possibility of importing from India.

14 COVER STORY clusters, despite the urgent need to mechanise.

What can we do for our onions? Let us be straight if harsh for a second. These floods are a natural disaster that have been caused by climate change. The problem is, this will not be the end of it. Next year, a different climate related disaster could stare us down and bring our agriculture to its knees. That is not to say the scale will be this big every year, but the change will beTemperaturesvisible. will rise. As we keep being told, this is the coolest summer of the rest of our lives. Water will go from being short to being too much. As a result, crops will suffer. Many people do not understand this but the science of agriculture and the art of farming are separated. The science of agriculture is a technical one, full of genetic engineering and hard data. The art of farming has to do with the soul. Only a farmer that has spent their entire life planting a certain crop knows not just technicalities like what its sowing time is and how much water it needs, but really what the personality of that crop is. Go back to Salim Ahmed from Chagai with whom we started this story. Think about how he described the onion — as a rough, hard vegetable once it is harvested but a delicate, fragile sapling that is swaddled by the very soft earth that it thrives in. It is a vegetable that has ‘nakhray’ as the farmer tells us. Yet at the same time it is resilient, having a thicker skin (both literally and figuratively) against things like pests and disease. To fix where we stand, we must use the science of agriculture to complement the art of farming. Our farmers know their land best, but they are facing an era in which the land is fast changing and so is the environment. Science must help them adapt to it. We must use better seeds. We must use more adaptable varieties of these plants and make sure that they get the right amount of water at the right time through not just proper scheduling, but techniques such as drip irrigation.

The supplyonionchain Since the sowing and harvesting times vary for all of these clusters, there is often a shortage in different areas of the country and prices fluctuate geographically. But the market gets particularly hot during the winter months, with inflation by as much as 5 times in some dry months. So for example if the crop is in the sowing period in KP, it will be more expensive in Islamabad and north Punjab, and onions will either have to be imported or brought in from Sindh. But since Sindh produces very fine, export quality, red onions are expensive within the country as well. The onion crop is technically a Rabi one, which means it is sown in the winter around mid-November and harvested in late Aprilearly may.“There are three distinct ways of growing onions. The first is sowing seed directly in the field where the crop is to mature. The second is to sow in a seedbed from which the plants are transplanted later to the field, and the last popular method is planting pre-grown sets. A grower may buy these sets, or grow them from seed himself. The transplanting method is used more commonly for early production,” explains Khalid Mahmud Khokhar of the Pakistan Agriculture Council. “The nursery for the autumn crop of onions is raised in the first week of July and the seedlings are transplanted in the field in the middle of August for harvesting of bulbs during December. It is difficult to manage nursery seedlings of autumn crops because of high temperature and monsoon rains. Some times, the heavy rains cause severe damage to nurseryEssentially,seedlings.”what this means is that while onions are grown at different times, one of the major periods in which a large part of the overall yield is harvested is around July-August. Even in normal years, the supply of onions falls short during December-January and prices soar to more than five times compared with normal season. Normally, the government mitigates this through the import of onions and toma toes from across the border in Afghanistan and Iran. It would, of course, be a much simpler process if trade were active with india. This year, because of the floods, the onion crop along with other crops in Sindh and Balochistan was wiped away almost complete ly. To get a measure of this, that means around 77% of the all onions grown in Pakistan. And since this was close to one of the harvest peri ods, the supply chain has already been affected immediately. The price of onions in the federal capital shot up to Rs 300/KG within days while in Lahore it went up to Rs 400/KG.

The threat posed by climate change to the onion is massive. The Sindh, Balochistan, and KP clusters are all very different, but they have similar issues which makes it easier to make a cohesive policy. Water shortage, humidity, monsoon rains and dust storms causing lower yield in Sindh cluster. Late frost in and strong dusty/sandy winds and storms in Balochistan during flowering/ blooming season greatly impact the yield and quality of production. Cli mate change related impacts, such as new diseases and shifts in crop cycle are also emerging issues in the regions. In Swat, the cool tempera ture and snowfall affects the yield of onions.

• Most MFPs have already collected the installment for the month of August (up to 90%), however, collection for the next few months will remain a challenge in the flood-affected districts. Due to the challenges highlighted above, MFPs working in the above-men tioned districts:

International and National Best Practices:

• Offer non-financial emergency services to improve customers’ well-being and connect them with local relief and rehabilitation authorities. Link clients and communities with the PDMA, health and other public departments to ensure all public services are made available to the affected communities. Provision of vegetable seeds and fodder to farmers for the period between two major crop cycles to revive their farms.

Insights from the recent COVID-19 have shown that though an outright moratorium in the short term seems like the best option to provide relief to the clients in the medium to long term such a step adversely affects the credit discipline and welfare of the clients. At the same time, it has huge financial implications for the government and disrupts the sustainabil ity of MFPs.

The communities at the bottom of the economic pyramid are more vulnerable and face the brunt of such disasters. The microfinance sector provides financial services to such communities and has extended loans of Rs 400 billion to almost eight million clients. The table below presents a province wise distribution of flood affected districts (66 total affected districts -- NDMA) along with the total portfolio deployed and clients served by the MFPs. Pakistan Microfinance Investment Company (PMIC), Pakistan Microfinance Network (PMN) and MFPs are proactively evaluating the situation and taking stock of the loss of livelihoods and assets of the clients affected by the floods. MFPs on the ground are currently involved with relief work for the clients they serve and shall have a better understanding of the true impact of the catastrophe once the flood waters recede and clients can re turn to their houses. The initial assessment suggests the following:

• Houses have been severely damaged, and people are being forced to live in temporary shelters.

• May face issues with maintaining liquidity, portfolio quality and profit ability which will affect their ability to meet minimum capital requirements, covenants with financiers and the ability to mobilise more funds.

Experiences and studies on disasters from India, Bangladesh and Pakistan have shown that efforts and resources by the government and NGOs are mostly focused on rescue and relief efforts, however, rehabilitation and revival of livelihoods of the affected communities also require equal atten tion and resources. Important lessons learned from past disasters applicable to the microfinance sector are as follows:

• Will experience problems in making timely repayments to their lenders.

• Allow borrowers to withdraw savings/fixed deposits without any penalties.

• Ensure business continuity and disbursement to clients to rebuild their businesses and livelihoods. Blend grants, fresh loans and deferment of existing loans to provide capital to clients to re-establish their business es.

In the last two decades, the country has faced numer ous catastrophes including floods, droughts, torrential rains and heatwaves. These natural disasters have badly impacted Pakistan’s economic wellbeing. However, the prevalent situation due to the floods in 2022 has been unprecedented with huge losses in lives and businesses.

Floods and microfinance: Lessons from the past Ammar H. Khan OPINION

• Establish close contact with clients as soon as possible, and maintain communication with them more frequently.

• Immediately carry out a rapid assessment of potential portfolio losses once the flood affected areas are accessible.

• Businesses and enterprises in urban areas will be adversely affected in the coming months due to a lack of demand and the disruption in the supply chain from rural areas.

• Organisations switched from group liability to individual loans.

16 COMMENT

• Continuity of the business operations will remain a challenge for the institutions as access to branches and offices remain limited because of standing water.

• Non-connectivity with clients who are displaced from their homes and villages will pose challenges to MFPs in maintain ing contact.

• Regulators to review the situation closely and provide regulatory relief to those MFPs which are genuinely affected by floods.

The writer is an energyandmacroeconomistindependentanalyst.

• Financiers to MFPs provide additional liquidity to meet additional demand from clients for business revival and to manage their operations.

• Reschedule loans on a case-by-case basis rather than offering a blanket moratorium on loans by regulators. Deferment of loans (on a case-tocase basis) for clients that have lost their crops, shops and other means of livelihoods based on the assessment by the MFPs.

• The cotton and chili crops have been badly damaged by the floods. In contrast the crops of banana and sugarcane have been damaged partially.

• Creation of a disaster management fund to provide grant funding to those clients who are severely affected and are unable to restart their businesses without financial support. Provision of grants and loans for restoration of their houses. For this purpose, bilateral and multilateral financial institutions and other development agencies should be approached. Furthermore, NSER data could also be used to target clients for various financial interventions.

Pakistan is amongst the top five countries affected by climate change making it vulnerable to natural disasters.

• Farmers are forced to sell their livestock at cheaper prices because of lack of fodder and drinking water.

The writer is a business journalist at Profit. She can be reached at com/AribaShahidcom.pkshahid@pakistantoday.ariba.orattwitter.

For starters, the traffic is a nightmare. Back when the road was made, the number of vehicles out there was limited. However, in the absence of decent public transportation, what other option does one have than to take their car to work?

In 1969, the road was renamed Ibrahim Ismail Chundrigar Road. Chundrugar was the sixth prime minister of Pakistan and served for a period of just 55 days (an interesting fact is that isn’t the shortest tenure for a Pakistani PM, Shujaat Hussain and Nurul Amin served for 54 and 13 days respectively).

OPINION

Profit itself has had very particular rules about how the road is treated in our writing. This publication’s former Manag ing Editor, Farooq Tirmizi, insisted we refer to I. I Chundrigar by its old name, McLeod Road. The road was initially named in honor of John McLeod, the Deputy Collector of Customs in Karachi during the 1850s. {Note from the editorial staff: In addition to this, I.I. Chundrigar road holds another unique position in Profit’s style-sheet. Anytime a road is mentioned in a story, the city that this road is in must be mentioned. For example, if Ferozpur Road is being mentioned, it has to be written as ‘Ferozpur Road, Lahore. The only two exceptions to this rule? I.I Chundrigar road in Karachi and Constitution Avenue in Islamabad.} There is another story about the road’s origins howev er. Some think it was named after James John McLeod Innes, The lost glory of I. I Chundrigar Road Ariba Shahid

All this just tells you just how important the road has been for not just decades, but centuries. Walking down the road you cannot help but see the amalgam of different eras just by observing the architecture. On one hand, you’ll find the flashy modern UBL building, you’ll find the classing HBL plaza, and you’ll also find relics of the British Raj such as the Standard Chartered Office.

You can spend a good half hour just making your way from one end of Chundrigar to the other during peak hours. This is because there are just not enough tracks to offset the large amounts of traffic.

What started from cotton warehouses, a cotton exchange, railway tracks, and a station; in the 1870s eventually turned into a hub of commercial activity with a number of European banks and companies setting up shop along the street. What this means is, that I. I Chundrigar Road was of utmost importance even before Pakistan was conceived.

The train station proved to be pivotal in the growth of the road. In 1935, McLeod station was set up which helped businessmen and employees commute; but also helped goods make their way from the port to their destination. The station has now been renamed Karachi City Railway Station.

It is a lucrative business in the area. Parking itself starts at Rs 5,000 a month. This gives you somewhat of an idea of how big of an issue it potentially is.

18 a Lieutenant General that had received the Victoria Cross (the highest and most prestigious award of the British honors system) for his ‘services’ during the War of Independence 1857. Considering the British respect for the subcontinent, it seems more likely that a British war hero is a muse behind the name of the road.

Despite all this, Chundrigar has lost its charm. No one wants to be there anymore. It is just too much work to be at Chundrigar.

The parking situation is another issue that cannot be ignored. Offices just aren’t built keeping the num ber of cars employees bring in mind. You’ll find cars parked on the sidewalks, alleys, anywhere you can fit one.

The road, however, has also been vastly ignored. Remember the charpai beds you see outdoors or in your villages? The charpai threads are used to demarcate the two sides of traffic. That is the state of the road that brings in more money than most districts.

If you’re over 35 and have a job in Karachi, chances are you’ve spent a significant amount of time at I. I Chundrigar road. For some, that may be because your offices were located there. For others, you might have been caught up in traffic. Both are likely scenarios on this once mighty avenue that is the central business district not just of Karachi but of Pakistan.

The road is inextricably tied to the world of finance. There is prestige and recognition associated with its name, but its current state of dilapidation means it is no longer a desired office location. That, to put it mildly, is sad. For a road with a legacy to fall into disrepair is one thing. That is fixable. For it to become undesirable is another can of worms entirely.

COMMENT

However, these issues exacerbate when it rains. You know how they say, it never rains - it pours? Well, that is how one describes rain at Chundrigar. It is one of the first roads to flood in the city. You’d think this means ankle depth, or maybe even knee deep, but in 2022 the water levels at Chundrigar road reached 5 feet. For context, I am 5 feet 5 inches. The situation was so bad, that floatable boats were brought in to save people and prevent them from being electrocuted from the walls of buildings that had caught the electric current. This is why no one wants to work at Chundrigar anymore, the same way no one truly wants to live in Karachi - it takes a toll on you and leaves you drained. While it used to be a hub of financial professionals considering all banks, the central bank and the PSX were lined on the road; it also housed all major me dia houses such as Jung, Geo, Dawn, Express, ARY, etc. For this very reason, a number of offices have moved off of Chundrigar. HBL, while keeping the HBL plaza has set up an office at teen talwar where the executives sit, primarily to avoid traffic. Similarly, banks have now realized that you do not have to have your headquarters at Chundrigar anymore. Physical proximity to the State Bank of Pakistan (SBP) is no longer needed in today’s digital world. That’s why banks have set up offices all over the city. Now you may be wondering where everyone is going. There is no new Chundrigar road in the making. Businesses and corporations are not lining up on the same road anymore. However, a key recipient of all this traffic from Chundrigar is the Harbor Front, Dolmen Executive Towers, and Sky Towers all in the same compound as the Dolmen City Mall. While it may not be logistically convenient to commute to work all the way across town for many, the fact that you do not have to deal with a clogged road, troublesome parking, or worry about drowning makes any place seem better.Thishowever begs the question, will Chundrigar Road ever regain its lost charis ma and charm? Will I ever be able to invite someone to Profit’s office without them saying, “Oh no, not Chundrigar; let’s meet somewhere else?”? Will anyone care about its historical and cultural significance? Will anyone finally care about the employee lugging his or her way to the exhaustive location? And more importantly, if this is the concern for the road that accounts for a major commercial activity, one must wonder whether anything is truly ever cherished or valued. n

ust when it could not have got any worse, it did. What was light at the end of the tunnel turned out to be a fast-moving train that has hit Pakistan, running over a country that was already down for the count. When the final assessments are done, the devastation caused by the 2022 floods in the country will be in the global record books. Based on a preliminary and evolving assessment conducted by myself and Ammar Khan – with a lot of input from people within and outside Pakistan – we estimate that the financial damages and reconstruction costs of these floods is already over $13 billion. This assessment does not include the full range of categories including education and healthcare, but it does include big-ticket categories such as housing, road infrastructure, and agriculture. In terms of agriculture alone, the damages are astounding, totaling between $1.7 and $2.9 billion for major agricultural products across the four provinces. Sindh is the hardest hit, with widespread devastation in the province’s cotton and rice belt. Based on our analysis, which looks at the historical output of cotton, rice, onions, tomatoes, and potatoes produced across districts in Sindh, we esti mate losses to range between $750 million and $1.2 billion. Within the province, Badin and Larkana are likely to be the worst-hit, nearing losses of between $75-100 million; over 30% of the total cropped area in the province is estimated to have been affected in the floods. Balochistan is almost tied in terms of damages and may likely suffer more than Sindh when the final data comes out. This is likely because much of the road infrastructure connecting the province to the rest of Pakistan has not been operational, meaning that whatev er product survives may rot in the coming days. The total damages across all districts are estimated to be between $600 million to over $1 billion; lack of district-level data on how much land has been affected makes this exercise more challenging in the province. In total, we

Crises are an opportunity and while the scale of this disaster is unimaginable, Pakistanis should not lose hope. The reconstruction efforts to follow will require a whole of nation approach. It is also an opportunity to leapfrog various sectors, especially agriculture. The opportunity should not go to waste, because if it does, we will only have ourselves to blame.

This exercise also reveals the significant limitations Pakistan has in terms of building the knowledge infrastructure to deal with calamities such as the ongoing floods. Given that climate change makes such catastrophes more, not less, likely, it is vital for the federal and provincial governments to improve and standardise their data collec tion and dissemination platforms. This can allow quicker, more robust analysis to be conducted, which will only make policymaking, disaster response, and reconstruction efforts more efficient.

As anyone who has worked in Pakistan can tell you, data quality is always a major hurdle, meaning that our model is only as good as the data we get access to. Over the coming weeks, more rigorous analysis will be required, and the state machinery is best placed to conduct it; open-source analysis like the one we have conducted can only offer a ballpark picture that can inform more rigorous analysis.

J

The writer is Director of the Pakistan Initiative at the Atlantic Council, a Washington D.C.-based think tank, and host of the podcast Pakistonomy. He tweets @uzairyounus.

Astounding damage to agriculture needs immediate response

Uzair Younus OPINION

It is also important here to point out the limitation of the early exercise that we have carried out. Our estimates rely on publicly available information gleaned from reports provided by the NDMA and PDMAs across the province; we also relied on historical agricul tural data published by various ministries and departments, which also include nominal value of output for various products, and the many local sources who were willing to answer our questions and share information.

is likely to lose between $300 to $500 million in agricultural output because of the flooding, with fruits being the vast majority of losses. At the time of writing this analysis, district-level data for the province was not available and as we get access to this data, we will be able to paint a more specific picture of losses across districts in the province. Given the flow of floods southwards, it is no surprise that Pun jab has been spared the brunt of the damages. Our estimates suggest that Punjab will lose between $65 to $150 million in output losses, primarily in the cotton and rice-growing regions of Rajanpur and DG Khan, who have been the hardest-hit in the province. Recovering from this devastation will take time and resourc es. These resources must focus on kickstarting agricultural credit markets, providing seeds and fertiliser to farmers whose livelihoods have been destroyed, and funds to district governments to rehabil itate lands and roads across affected districts. By our estimation, a complete package for the agricultural sector across the country will cost almost $1 billion and will have to be equitably distributed to provinces and districts that have been hardest hit. Delays in getting these resources to the grassroots level will only increase losses, fuel food inflation, and undermine the overall economic recovery from these floods.

20 COMMENT estimate that nearly 70 % of the losses are in the fruits category, with the Killa Saifullah region suffering the brunt of losses, which we place at over $200 Khyber-Pakhtunkhwamillion.

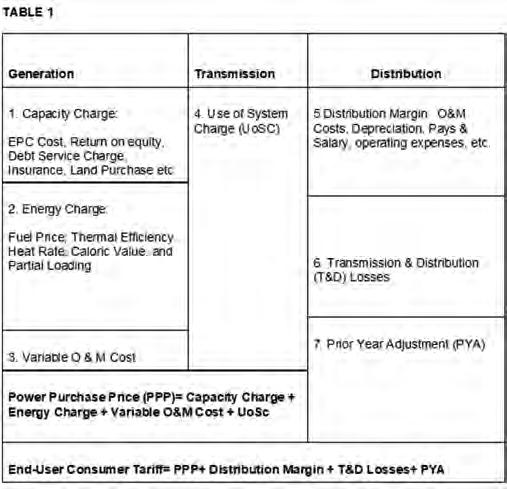

Now to understand the table’s components.

At the generation level, there are three components. The price of fuel as well as operation and maintenance (O&M) costs are variable components, which depend on fuel mix used for generation, for example gas, coal, RLNG, along with the amount of electricity pro duced and sold. On the other hand, the capacity charge component is a fixed cost, which is indexed quarterly or annually with multiple parameters, such as exchange rate, London Interbank Offered Rate (Libor), as well as local and U.S. consumer price index (CPI).

Demystifying Pakistan’s high electricity prices Jalees ur Rehman

Why the rise?

Now that we know the components, we’ll discuss the rise in costs, as reflected in the table below, using Nepra the last decade, we have addressed our power shortfall and blackout woes by doubling installed electricity from 22,813 MW in June 2013 to 41,557 MW in May 2022, according to the finance ministry’s economic survey. In addition to this, the generation mix is being diversified by reducing dependence on residual fuel oil (RFO) by replacing it with regasified liquefied natural gas (RLNG). Similarly, cheap sources of energy, such as renewable energy and coal-based power, are synchronised to the national grids. However, despite this, electricity prices are continuously growing. Average power tariffs have almost doubled in the same period. The cost components To understand why, one needs to understand the composi tion of the price – that is, the “end-user consumer tariff.” An illustration of this is provided in the table below with costs and charges incurred at different stages of the electricity supply chain, according to the National Electric Power Regulatory Authority (Nepra).

OPINION

The writer is an Engineer & Business graduate working for K-Electric. He has over 14 years of experience in power utility, Oil refinery and IPPs Despite increasing installed capacity and diversifying the generation mix prices are rising… and here’s why

22

In

Finally, at the distribution level, there are three components. DISCOs are allowed distribution margins to cover R&M, pay and allowances, depreciation, and other expenses. Then there is the transmission and distri bution loss component, as well as prior-year adjustment (PYA) component.

At the transmission level, National Transmission and Des patch Company (NTDC) imposes a Use of System Charge (UoSC) for providing a carrier between power producers and distribution companies (DISCOs). UoSc is applied by NTDC to cover its return on investment (ROI), repair and maintenance (R&M) costs, administration expens es, corporate taxes and debt servicing.

All of this is used to come to the end-user tariff.

The shares of variable fuel, O&M, distribution margin and T&D are almost stagnant over the same period. This also bursts the myth that T&D losses are the main drivers for increasing power rates. Data suggests that the contribution of T&D losses to tariff is stagnant if not declining.Understanding capacity payments is also important. Over the years, we have developed a capacity market to ensure sufficient capacity to meet peak demand at all times. In turn, investors are incentivised by paying them capacity payments to install base load power plants with plant factors exceeding 85%. The flip side of the capacity plants is that the capacity charge is a fixed cost which is charged in consumer bills even if not a single unit is produced. Similarly, depreciation of the rupee to the dollar increases the capacity payments as it is indexed to the dollar due to debt servicing, ROE, insurance costs etc.

Currently, we are facing a double jeop ardy situation because the efficient base load power plants recently added to the national grids use imported fuel for generation. Due to higher fuel costs, these plants are underutilised and consequently unable to recover their capacity costs and the country is facing acute power shortages despite availability of capaci ty to produce.Goingforward, we must learn from the current precarious situation and correct our policy decision making for future electricity generation. Foremost, base load plants should have local fuel – that is, indigenous coal, hydro, nuclear, and long-term contract RLNG. By doing so, the energy purchase price (EPP) will be reduced substantially, and subse quently capacity purchase price (CPP) will be recovered, henceforth not contributing power tariff hikes. Secondly, the overall purchase price (EPP+CPP) should be used for determining the Economic Merit Order (EMO). Thirdly, investment in the transmission network is required to remove bottlenecks so that the EMO is not violated. Moreover, preferential addition of renewable energy in the national grid be made to reduce overall average tariff. With a major policy shift, we can make the electricity sector more affordable for end consumers and increase power consumption per capita. n

COMMENT

data, which shows the end-user consumer tariff has almost doubled in the last 10 years from an average price of Rs 13.50 per kilowatt hour (Rs/KWH) to Rs 24.82. In 2015, variable costs of fuel and O&M constituted almost 56%, that is Rs 7.53, of the cost. The capacity charge share was a meagre Rs 2.49, almost 18%. However, the capacity charge has quadrupled to Rs 9.77 and is the main contributor to the exorbitant tariff rate of 24.82 Rs/KWH. Importantly, capacity charges, which stood at almost Rs 188 billion in 2013, have ballooned to a whopping Rs 1,250 billion at a com pound annual growth rate (CAGR) of 23.43%.

Acrisis is brewing in the petroleum industry, and it may result in you being unable to pay for fuel using a credit or debit card at petrol stations. Oil marketing companies (OMCs) have already started stifling card payments at petrol stations, dealing a blow to digital payments which had only recently started kicking off. But why are petrol stations not accept ing card payments, and what does it matter to OMCs how end-consumers pay for fuel? Because there is a cost associated with selling fuel on card payments, and it is a burden that has put OMCs under a stress test. That is why they have been stifling card payments all together, and are making a quick buck while they doWhileit. this has all been brewing in the background, it came to a head officially in a letter sent by the Oil Companies Advisory Council (OCAC) to the State Bank, asking its governor to decrease the charges paid by OMCs on card transactions. The problem is for the entire industry but PSO only has so far been the one to tell its dealers that it will no longer be able to foot its share of the MDR bill. Dealers can either continue accepting card payments at their own expense or discontinue accepting cards

By Taimoor Hassan, Ariba Shahid

24

OMCs are in a conundrum, and will face the possibility of a constriction in overall volumes

DIGITAL PAYMENTS completely. Dealers on the other hand have been ingenious: they have either stopped accepting card payments, or have started passing it ontoTheconsumers.effecthas been enormous. From numbers obtained by Profit, card transactions at PSO declined from 145 million transactions on August 31 to 60 million on September 1. That is at PSO alone. Shell has also said that they have received reports of Shell dealers either not accepting cards or charging customers on top, while Shell has not given its dealers any clear guideline to do so. No numbers were shared by them of volumes or value of cardbased Thistransactions.hasputOMCs

Earnings by a whisker In July this year, the Pakistan Petroleum Dealer Association (PPDA) went on a nationwide strike to demand that the government increase the commission of dealers . The association wanted this com mission to be increased from 3.5% to 6% as promised earlier by the government. There are various components that help determine the price of fuel in the country. Dealership margins are the margins a dealer (a pump owner in this case) gets. These used to be in the form of percentages but have now been fixed per litre. Back in November, the dealers went on a strike asking for revised margins. Petrol pumps would earn PKR 3.91 per litre on petrol and PKR 3.30 per litre on diesel. Profit made by petrol pumps per litre was 2.75% which the PPDA had demanded be increased to 6%. If this demand was met, the profit made by pumps on petrol would be PKR 8.75 per litre and PKR 8.5 on diesel. Instead, the government negotiated with the dealers and they would now charge PKR 4.90 per litre of petrol. Essentially, an enhancement of 99 paisa in the existing margin of petrol and 83 paisa in the existing margin of high-speed diesel. In 2016, the Economic Coordination Committee (ECC) decided that margins will be revised annually by the amount of average Consumer Price Index (CPI). The period for this average changed in 2019, but the rule remained the same. Despite that, over the past five years, the margin was only revised four times for petrol and three times for diesel. There have been threats of strikes every time. Before November 2022, a revision in margins took place in April 2021 which was after a delay of nine months for petrol. The government, over the past few months, has been delaying the revision stating that the PIDE study would be used as a gauge to revise margins. The study, however, is completed yet the government was still not keen to revise rates. In addition, if you link this to the fuel shortage of June 2020, the government’s relationship with fuel pumps isn’t that great to begin with. While inflation remains a concern and with fuel prices rising internationally, the government feels compelled to make fuel pump ownersPetrolwait.pumps can be company-owned, for instance by PSO, Shell, Byco or Total, or these OMCs could have dealerships to run it. Dealer-owned petrol pumps are where an individual buys a “franchise” of a petrol pump, follows all legal procedures, and sells fuel on behalf of an OMC. They earn through the dealership margin, which was revised after the strike by the association. On the other hand, OMC margins are fixed flat at Rs3.68 per litre. The bulk of the transactions on fuel stations are cash-based. But because the volume of sales of petroleum products, high speed diesel and petrol is so high, even a small percentage of card payments would translate into billions of rupees worth of transactions paid through payment cards. There is no uniform number of how much of fuel sales are paid through card but we will try to give readers a sense of proportion of card based payments against cash payments through some estimates received by AccordingProfit.to an official at an OMC, the overall card transactions for fueling transac tions would be around 15% of the overall sales.

According to one of Profit’s sources, PSO last year made sales worth Rs18 billion on payment cards, which is estimated to be about 30% of its total sales on retail fuel stations. PSO has not responded to Profit’s request for comments on the breakdown of card sales against cash. While the estimates of 15% sales on cards is a number overall for the country, this number is significantly higher in urban centres such as Karachi, Lahore and Islamabad where the demographic is relatively affluent and own bank accounts and linked payment cards such as debit and credit cards. The proportion of sales on cards could be as high as 30%, with some days touching 50%, according to a PSO dealer operating a fuel station near Lahore’s Ganga Ram AccordingHospital.tosome conservative esti mates provided by another petroleum industry

in a disarray: While card payments form a good chunk of overall sales especially in the urban centres like Ka rachi, Lahore and Islamabad, OMC’s inability to foot the bill means they will see a drop in volumes on card sales because it constricts their margins.Theproblem is double-barrelled, howev er. The central bank has for long been gunning to push digital payments and in January last year adjusted the merchant discount rate (MDR) to make POS acquiring a worthwhile business. OMCs now want that MDR revised for the petroleum industry and be fixed at 0.3%, according to the OCAC letter to the central bank. This is not only going to pull down volumes of digital payments, the bottleneck here is that if the SBP revises the MDR to that much, it would impact acquiring business as well as PSO/PSPs and payment schemes. The situation is a confusing one where dealers are not willing to accept card pay ments, killing card payments at pumps, unless MDR charges are reduced. And if card charges are reduced, those in the payments business would be unwilling to push card payments, killing digital payments again. The eventual casualty is digital payments which the State Bank has long been gunning to push. How does the MDR work and how does it affect earnings of OMCs and their dealers? It all lies in margins.

If you go to a Shell fuel station today and buy one litre of petrol priced at Rs234, only Rs3.68 go to the OMCs. That’s a margin of 1.5% that OMCs earn per litre of petrol. On the other hand, dealers get Rs7 per litre out of the total price, which is a 2.99% margin for the dealers. Now take the case of Shell, which on average is charged 1-1.2% MDR depending on the bank or fintech company it uses the POS machines for acceptance of card payments. OMCs run retail fuel stations on their own as well through dealers. At the stations that are company operated, the OMC bears all the MDR charges itself but at dealer operated stations, the oil marketing company shares the MDR charges with the dealers at pre negotiated rates.The arrangement can vary for each OMC with its dealers. For the sake of understanding, let’s say that Shell bears 50% of the MDR and its dealers bear the remaining 50%. So if it is 1.2% MDR charged to Shell per litre, that is Rs2.80 on a debit card. (Note: MDR on credit cards is higher than debit cards. But since credit cards are very small in number as compared to debit cards in Pakistan, this analysis is restricted to debit cards only)Ina50/50 arrangement, Shell pays Rs1.4 per litre extra for accepting payments on a debit card of a certain bank. Its earnings per li tre come down from Rs3.68 per litre to Rs2.28, or a margin of 0.97% per litre. A Shell dealer’s margins on the other hand falls from Rs7 to Rs5.6 or 2.3% before FED charges. To understand the scale of the problem, lets broaden it to the total estimates for the sales on bank cards. According to our source in the industry, Rs92 billion worth of sales are on payment cards. At 1.5% margin for OMCs, only Rs1.38 billion can be earned as margin for OMCs. Assuming a 1% average MDR, though MDR can be even higher than this, Rs920 million goes in MDR charges and OMCs only get Rs460 million.

OMCs’ case against the MDR that they pay right now is very well-grounded. The volumetric sales of petrol and high speed diesel have remained steady over the course of the past 12 months. However increases or decreases in the regulated pricing of these products has affected the overall sales of the industry.

The State Bank of Pakistan is the de-facto regulator of everything banking and financial technology, and as a regulator wants to see digital payments thrive. In the current macroeconomic scenario, however, OCAC’s stance is that in the current arrangement, digital payments at retail fuel stations are going to suffer if the MDR is not fixed. And instead of each OMC going individually to banks to negotiate MDR which the banks would most likely refuse because it reduces their business from payments, it is perhaps more convenient that the SBP itself tells the banks to fix the merchant discount rate, otherwise digital payments will suffer. What was not officially communicated, however, and it would have perhaps eventually going to come to this, and in our case it came only a week later that the OMCs would not be willing to continue bearing charges on card payments while their own margins were reg ulated by the government. Consequently, the biggest OMC in the industry, the state-run Pa kistan State Oil (PSO), informed its dealer-run fuel stations that it had exhausted its funds and could not make further allocation towards MDR charges it shares with the dealers.

An interesting insight that can be derived from the OCAC data on sales of these products is that sales of both petrol and diesel spiked immediately following the onset of the Russia-Ukraine war. Even though globally oil prices had spiked, the government of Pakistan at the time announced a blanket subsidy by fixing fuel prices well below the market rates.

The OCAC official communication requested the State Bank to fix the MDR at 0.3% for the petroleum industry.

The OCAC pleaded its case that because of being regulated, OMCs and dealers worked on fixed margins set by the government and any costs incurred in their operations could not be passed on to the consumers like they can be in other sectors. In the letter, the OCAC apprised the governor that the MDR being charged by banks was eating away the gross profits of OMCs as well as their dealers.

How is that exactly happening?

Killing makingpaymentsdigital(andaquick buck while you do it!)

The petroleum industry operates on thin margins and slightest additions of costs make the margins razor thin. The industry is already facing a meteoric fall in demand while costs of operating a fuel station have increased. Consequently, the OMCs have had it rough on digital payments and decided to do something about it. On August 22, the Oil Companies Advisory Council (OCAC), the of ficial body representing the oil industry stakeholders such as refineries and OMCs, wrote a letter to the State Bank governor apprising him that the petroleum industry was bearing the brunt of being regulated by the government.

This caused the sales to rapidly increase at the expense of the national exchequer. Since then, however, the Pakistan Tehreek-e-Insaf (PTI) government relinquished reigns to a coalition government which, to acquire the much needed IMF loan, started increasing fuel prices in May this year. Following this increase in prices, the volumetric sales of the industry have dipped to their lowest point over the past year.

The average monthly sales volume for high speed diesel and petrol for the past year amounted to 998 trillion and 1,024 trillion

26 official, about Rs92 billion worth of sales are made on debit and credit cards yearly at fuel stations across the country. From what OMCs earn from the Rs92 billion worth of transac tions, MDR charges eat away most of it. With such high volumes on cards in ur ban centres, OMCs are worried that the MDR being charged right now is eating away their margins especially because their own mar gins are regulated by the government and the increase in fuel prices hasn’t really increased their margins. On the other hand, dealers negotiated their margins with the government but contend they are not enough, and that the MDR they pay on card transactions is eating away their margins.

DIGITAL PAYMENTS litres respectively. Whereas looking at the latest data, monthly sales currently stand at 618 trillion and 829 trillion litres respectively for high speed diesel and petrol. The dip is a significant one, which would put anyone in the business on the backfoot. There is a significant shift in demand which can likely turn chaotic because of the recent flooding. There is also no guarantee that the government will not increase fuel prices in the future. What’s certain is that the petroleum industry is bearing the brunt of an economic downturn and wants to cut costs wherever possible. The effects could be magnanimous, however.

So on the one hand, dealers are shirk ing on paying MDR that is already low and killing acceptance of cards, and on the other, the OMCs are asking for MDR to be lowered which is going to disincentive almost every payments player in this arrangement and would kill digital payments. In the meanwhile, people like you and me are going to scramble through our wallets, ask for the nearest ATM in embarrassment as our cards are declinedquite literally.

You see an OMC, like PSO, has a tiny margin to begin with. Rs3.68 per litre or 1.5% in the case of petrol currently priced at Rs234. So it has a good reason to not pay that. But if OMCs back out from paying their share of MDR, dealer margins, though better than OMCs, shrink by the percentage OMCs refuse paying. This arrangement seems unacceptable to dealers. They have already went on a strike against the margins initially allowed to them and they would not bat an eye at taking steps necessary to secure their margins. It has only been two days that PSO has communicated that it will not pay its share of MDR and the PSO dealers have either stopped accepting cards completely or have started charging an extra amount on card payments - in some cases even more than the share of banks towards the MDR, and are making a quick buck while they do it by passing their costs on to consumers.

n PSO was willing to respond with comments on this story but could not do so until the publishing of this article. Their comments will be incorporated into the article as soon as they are Additionalreceived.reporting by Asad Ullah Kamran

Our own PSO dealer in Lahore’s Queen Road plans to charge 2% extra on card transactions, while the bank share of MDR would be less than 1%. In only a day, card transactions on PSO stations have fallen from 145 million on August 31 to only 60 million on September 1. PSO right now is the only one that has pulled itself out of the arrangement with its dealers. While it is the only one right now, it is also the biggest. More OMCs can follow suit. At least Shell Petroleum told Profit that they do not plan to withdraw from paying their share of MDR to dealers, but communi cated their frustration of paying an MDR while the government had capped their margins. More than anything, the state of disarray in the petroleum industry has more than one casualty. If dealers start creating deterrence in acceptance of card payments, one obvious casualty is the goal of spurring digital payments, followed by payment schemes that earn an interchange on these payments, the PSO/PSPs providing systems for acceptance of these payments, the acquirers and the issuers. You see the petroleum industry is being given merchant discount rates that are already below the floor set by the State Bank of Pakistan. In its famous circular issued in January 2020, the SBP allowed the MDR to be charged within a range of 1.5-2.5% from an earlier fixed percentage of 1.5%. The SBP had also increased the percentage acquirers, the banks or fintech companies that acquire merchants and deploy POS machines for acceptance of payment cards, could get out of this arrangement. The entire premise then was that for card payments to thrive, acquirers need to be incentivised so that they can cover the costs of deploying POS machines which run in hundreds of dollars and make a profit on top. Banks, however, have already given lower MDR rates to OMCs because of the nuances in this sector which is regulated.

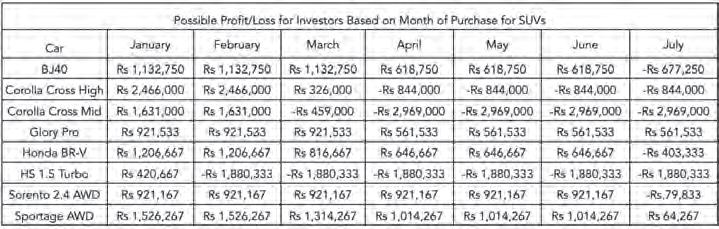

Whilst the sector is in a shambles, customersautomotivemighthave lucked out as investors have held onto a few cars for a bit too long

priceshowroomforbeingsomearecarssoldbelow

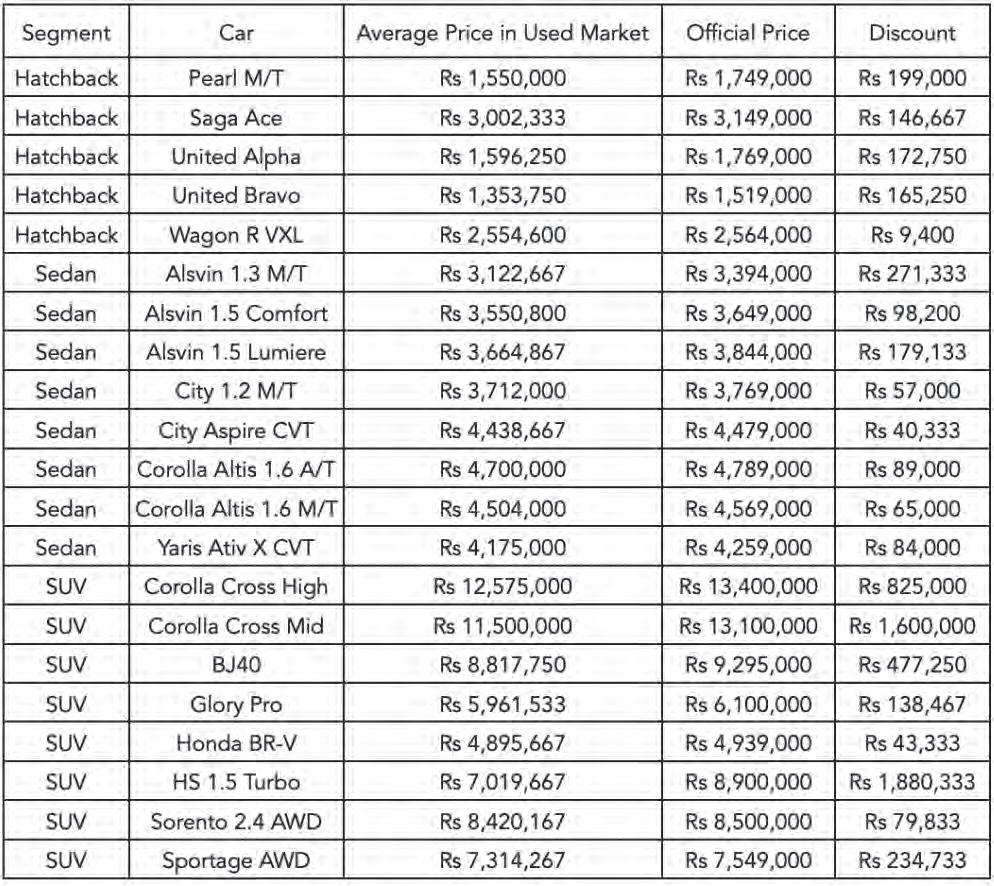

The car market is probably not the place where customers would normally imagine finding bargains and discounts. However, in their greed, automotive investors may have hoarded too many cars and also missed the right time to sell them. What this means is that now they have to sell them for discount prices. For the uninitiated in the Pakistani automotive space, cars are an asset class in Pakistan. Profit has already documented this in detail for those interested.Read more: The lopsided market structure of the automobile industry. As with any asset class, you also have investors in the automotive space. Investors constitute a sizable portion of car purchases. They make their gains when demand for cars outstrips supply. However, this situation does not arise normally given the production models in the industry. Thus, investors obtain cars in bulk to create artificial shortages, and then ration them out to the highest bidder for what is colloquially known as ‘on-premiums’. It’s a model that’s as old as the Pakistani car market itself. However, Profit has identified 21 different models that are selling for below their official prices. How did we find this?

28 Why

By Daniyal Ahmad

I see volume down 40-50% in 2022-23. I would like to be wrong

Muhammad Faisal, President of the Automotive Division at Lucky Motors

Why are some cars selling for ‘off’?

Profit looked at the prices of 1,036 cars from 83 different models across 14 brands being sold in the second-hand car market to determine the discounts. Or as we term them, ‘off-prices’.Weset the average price of a model by looking at a sample size of 15, wherever possi ble, for the particular variant. All cars that we looked at were the latest (2022) edition of the car to ensure that the vehicle was bought in January of this year or later. No cut-off point for mileage in particular was applied due to the fact that cars are, well, cars at the end of the day. Some investors may want to actually enjoy their vehicle before selling it off. However, preference was given to cars with lower mileage in the sample size to ensure the prices captured were particularly for vehicles bought for resale. So, what’s going on then? Profit inves tigates how customers may have lucked out in the automotive market at a time when, perhaps, everything else was in a shambles.

Setting the price of a car, or its premium in our case, boils down to the fact that it is both a car and an asset at the end of the day. Companies, and investors in our case, that do not get this right tend to encounter problems.

To look at an instance of when a company got this wrong, read more: The KIA Sorento 101 – How not to price a car. With the premise established, let’s take a look at what’s happened. Profit can point to wards two notable phenomena for the current situation: Inflation and the rupees’s current stability against the dollar. Firstly, inflation figures for August clocked in at a 47-year high. “Customers cut demand on cars first as everything becomes ex pensive.” said Asghar Ali Jamali, CEO Toyota Indus Motor Company, in conversation with Profit. Jamali’s statement seems correct when we look at automotive sales for July. Cars operate in a competitive market. Chances are that many in the market for a new car either already have one or can pur chase something more affordable in times of inflation. Therefore, investors have to really selectively pick which cars to place their bets on. Investors with the aforementioned 21 cars drew a losing hand. Profit can say this because according to research every car not in this list is still going for some amount of on-premium, for now at Secondly,least.most automotive companies reduced their prices in August on account of the rupee appreciating against the dollar. So the tl;dr edition of Profit’s aforementioned de tailed reason for why cars are an asset class in Pakistan is that they rely on imports. A lot. Thus, their prices are directly linked with the rupee’s value against the dollar. The rupee’s stability reduces the like lihood of prices increasing which makes cars not the best asset to invest in. Furthermore, Pakistan’s IMF’s deal has led to the possibility of the rupee appreciating further. This would lead to automotive manufacturers reducing their prices further based on what happened in August and this in turn would make cars quite a bad asset to have. Recap time. Investors hoarded cars that customers can no longer afford, which may also AUTOMOBILES

“On payments had ended in 2019, but were revived because of the imbalance in demand and supply caused Covid-19”by Suneel Munj, Founder of PakWheels

Probably. “Demand will reduce going forward by 40-50%,” said Jamali when Profit asked him about how the industry will fare in the coming year. “I see volume down 40-50% in 2022-23. I would like to be wrong,” said Muhammad Faisal, President of the Automotive Division at Lucky Motors, when Profit questioned him as well.Given customer demand is on the precipice of collapse, on-pre miums are likely to contract going forward. It’s very likely that we’ll see investors set the clearing price of their stock to below official levels because of their reserves as customers simply opt to buy fewer cars on account of the economic situation. In the situation that the rupee does depreciate against the dollar, we still may see some similar bargains. It’s true that the underlying asset (the car) investors possess will increase in value but they won’t really be able to sell it. This in turn will lead to them having capital tied up as well. So long as the clearing price is above the price the investor bought the car for, investors will continue to sell below the official price. “On payments had ended in 2019, but were revived because of the imbalance in demand and supply caused by Covid-19,” said Suneel Munj, Founder of PakWheels, in a video. Thus, this is not a new phenomena per se in Pakistan. The sheer quantity of cars that may be sold for off-payments, given the sales figures for FY 2021-22, would be new. Maybe even a pleasant surprise for many for those who held out on buying a car on the notion that “sabr ka phal meetha hota hai”. n 30

AUTOMOBILES

“Customers cut demand on cars first as everything becomes expensive. Demand will reduce going forward by 40-50%”

reduce in value in the future. So, what have investors decided to do in this situation then? They have decided to cut their losses. They have decided to do this by undercutting the official value of the vehicles to recoup their original investment with whatever gains they have made. Why would investors shoot themselves in the foot? This entire situation is perhaps best encapsulated by the age old saying of ‘lalach buri bala hai’. The ques tion one might ask then is, how bad are the losses? Well, it depends on when the investor acquired one of the aforementioned 21 cars in 2022. Not leaving anything to speculation, Profit has done the math to see whether any of the cars selling for discounts were profitable bets, and for how long that remained the case. In looking at the gains and/or losses made, Profit used the ex-factory price of the vehicle in the possible month purchase. We then subtracted the ex-factory price from the current average price for which the car can be found in the second-hand market. The earlier the investor got in the fray, the higher his returns based on our findings. It is likely that it is with return expectations such as these that investors continued to purchase cars for the remainder of the year and ended up in the situation where they are now. In the end investors possibly got good returns, and customers will now get bargains. So, everything works out right? Can we expect more bargains in the future?

Asghar Ali Jamali, CEO Toyota Indus Motor Company