18 Large difference among average tax rates on different fuels Coal

Biofuels & waste

Natural gas

Oil products

250

Tax rate (EUR per tCO2)

200

150

100

IDN

RUS

BRA

USA

IND

CHN

CAN

ZAF

CHL

EST

AUS

CZE

MEX

POL

LVA

ARG

JPN

KOR

SVK

FIN

TUR

HUN

NZL

DEU

BEL

AUT

ESP

SWE

PRT

GRC

DNK

NLD

IRL

SVN

FRA

ITA

ISR

ISL

GBR

LUX

CHE

0

NOR

50

Source: OECD (2018) Taxing Energy Use 2018.

The transition to a low-carbon economy interacts with tax policy. Recent work by the OECD and the International Transport Forum shows that tax revenue from diesel and gasoline use in private cars could decline substantially in the coming decades as future verhicles rely less on fossil fuels. This would put stress on government budgets, particularly in countries where fuel tax revenues represent a large share of total revenue. Broader use of distance-based charges can contribute to help sustain tax revenues, while also improving environmental and mobility outcomes (see Van Dender, 2019 and OECD/ITF, 2019).

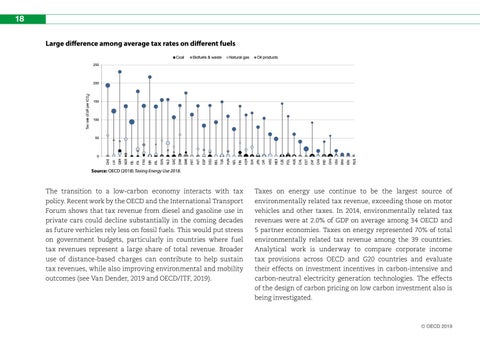

Taxes on energy use continue to be the largest source of environmentally related tax revenue, exceeding those on motor vehicles and other taxes. In 2014, environmentally related tax revenues were at 2.0% of GDP on average among 34 OECD and 5 partner economies. Taxes on energy represented 70% of total environmentally related tax revenue among the 39 countries. Analytical work is underway to compare corporate income tax provisions across OECD and G20 countries and evaluate their effects on investment incentives in carbon-intensive and carbon-neutral electricity generation technologies. The effects of the design of carbon pricing on low carbon investment also is being investigated.

Š OECD 2019