Competition in the Cloud?

Dr. Cecilia Rikap IIPP, University College London

Dr. Cecilia Rikap IIPP, University College London

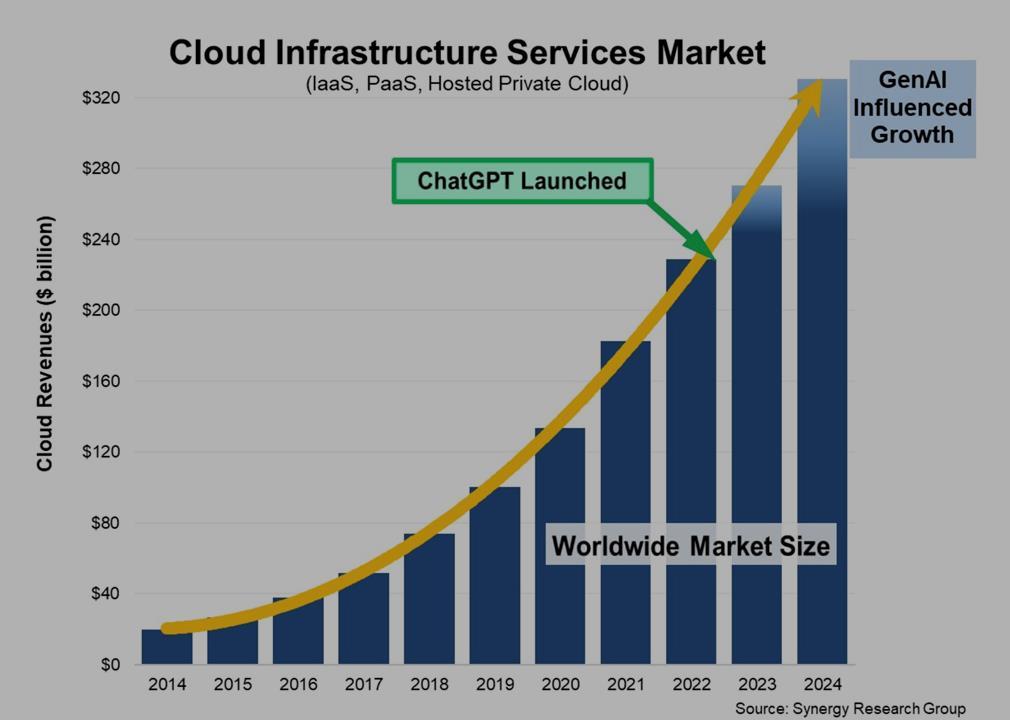

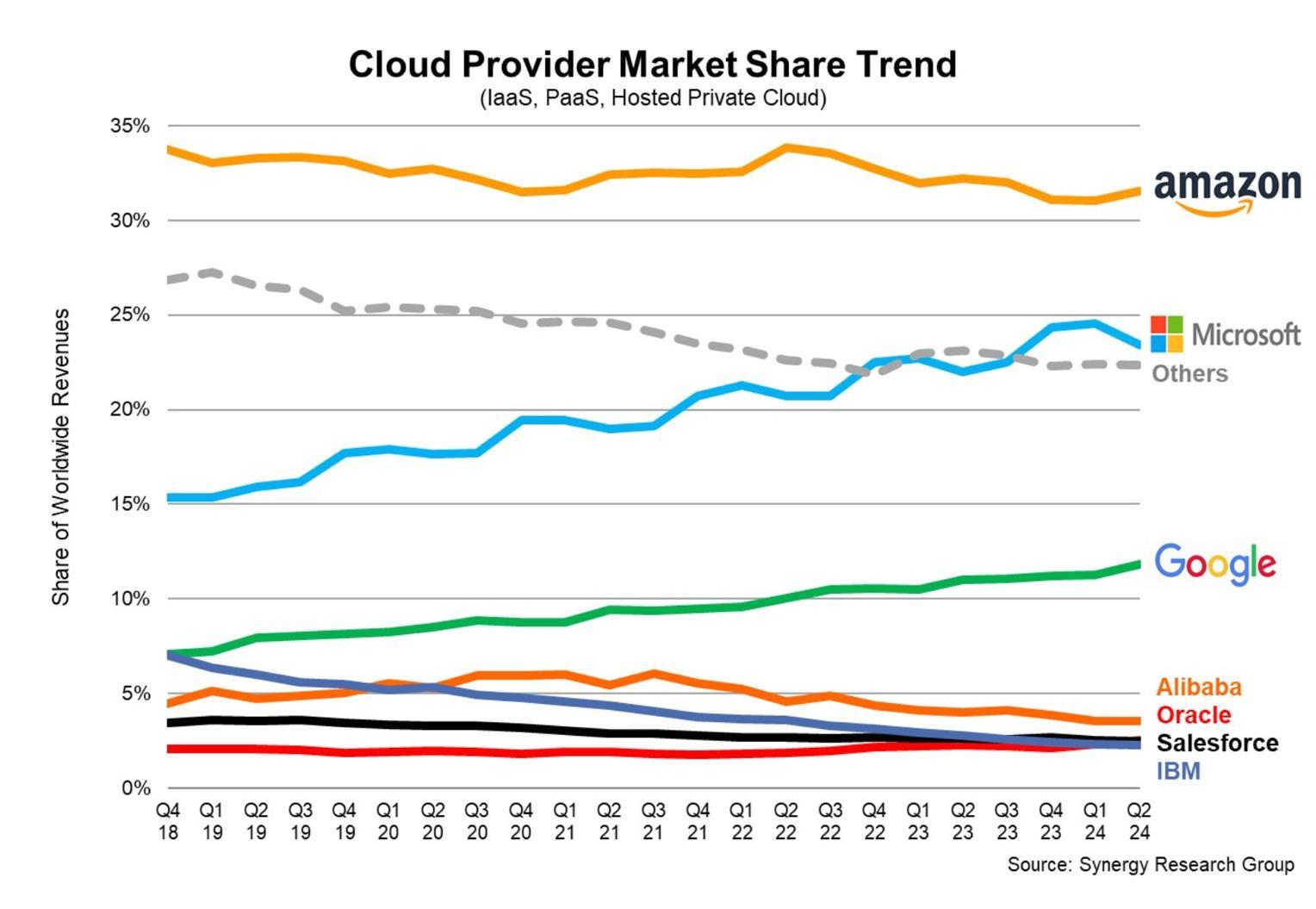

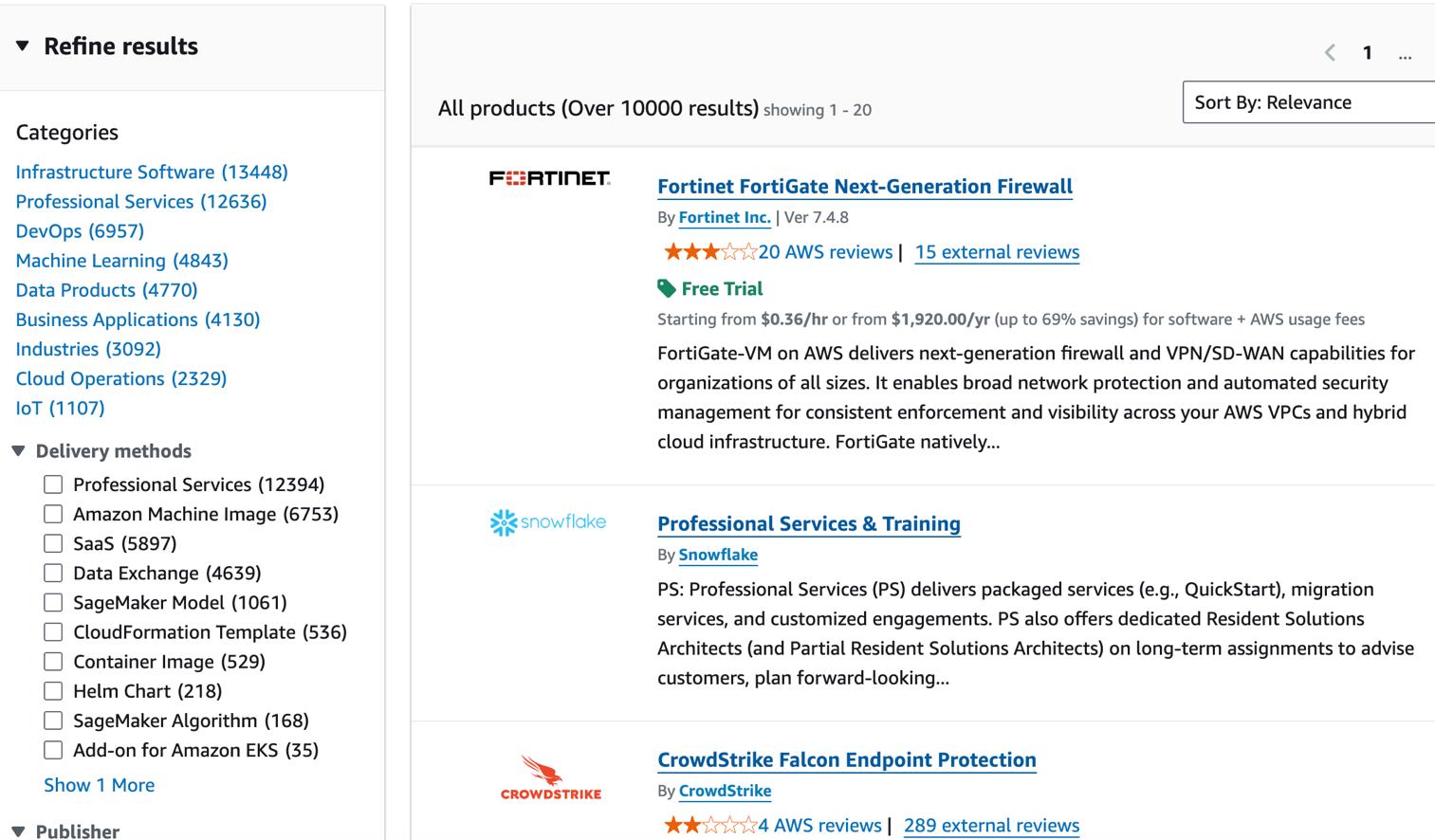

Digital tech supermarket

50,832 services in AWS (Apr-2025)

“Partners”: users & sellers

Digital technologies are produced, exchanged & consumed in their clouds

Digital tech supermarket

50,832 services in AWS (Apr-2025)

“Partners”: users & sellers

Digital technologies are produced, exchanged & consumed in their clouds

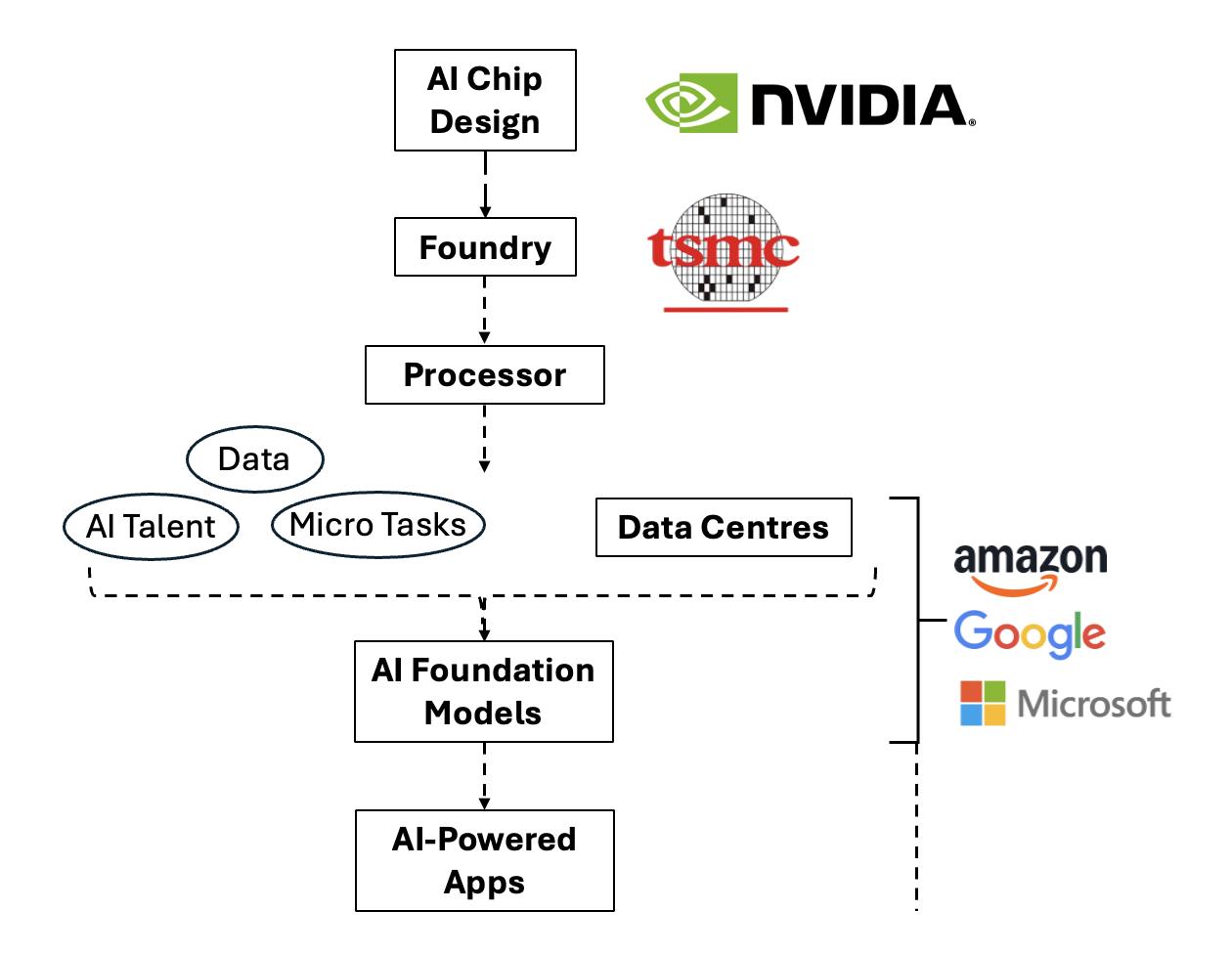

Black boxes: use without access

→ Public & corporate dependences

Amazon has a lot of SaaS and tries to increase the stickiness of the system. (…) It is not in your control to switch to other companies easily. (…) If you want to move from one cloud provider to the other, it takes months of planning (AWS senior software engineer).

1) Keep employees happy

2) Access reusable code for private software

3) Get users’ feedback in advance

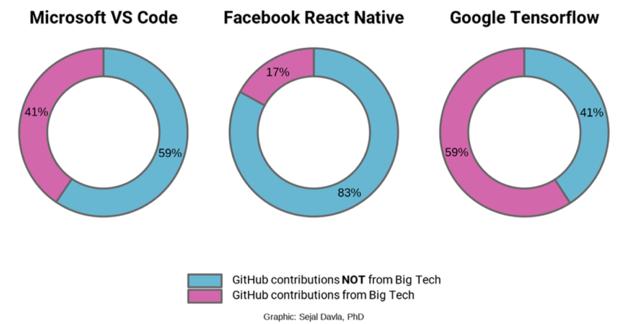

4) Profit from developers’ free work

5) Offer adjacent or complementary services

6) Create and control an ecosystem

7) Become the norm and standards

open sourcing improves our models, and because there's still significant work to turn our models into products, because there will be other open source models available anyway, (…) more specifically, there are several strategic benefits. (…) more compute efficient to operate due to all the ongoing feedback, scrutiny, and development from the community. (…).

Second, open source software often becomes an industry standard, (…) on building with our stack, that then becomes easier to integrate new innovations into our products. That’s subtle, but the ability to learn and improve quickly is a huge advantage and being an industry standard enables that. Third, open source is hugely popular with developers and researchers. (…) so this helps us recruit the best people at Meta, which is a very big deal for leading in any new technology area. And again, we typically have unique data and build unique product integrations anyway, so providing infrastructure like Llama as open source doesn't reduce our main advantages.

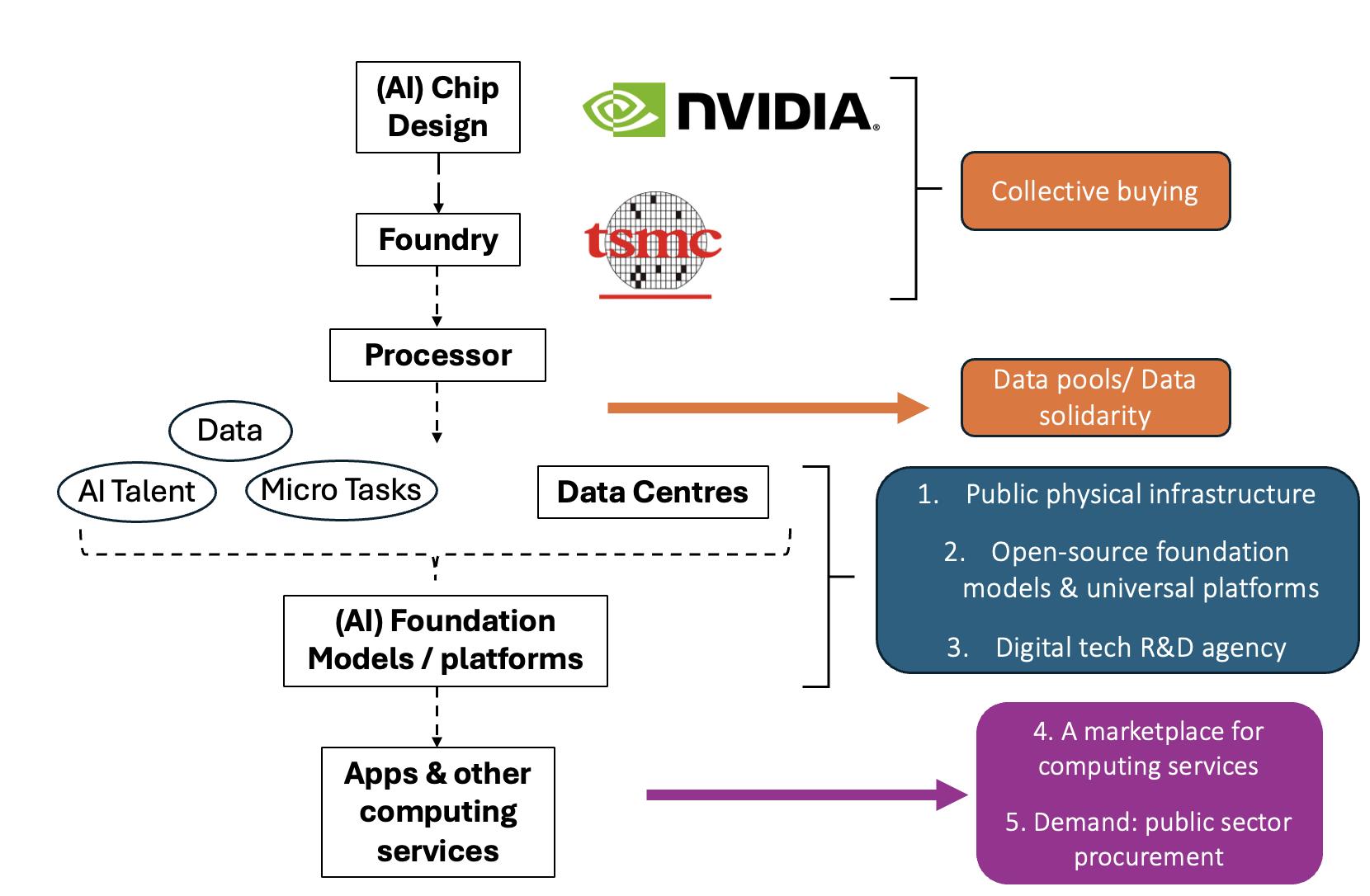

A systemic view of the (digital) economy

Ecosystemic, coordinated regulation

Identify power positions in networks

Integrate information sources

Taxing Big Tech:

Revenues (higher min corporate tax)

Data concentration/ Digital Services/ Datacenters

From IP to incentives & compensation

Compensate the network for innovation

Public access to data, models, etc.

Open standards, interoperability

Classic cartel: 7 sisters (Big Oil)

Intermediary case: differentiation through brand-building

A networked cartel in the AI stack Classic Cartel (7 sisters)

Cartel (AI IMs)

Scope Individual market Network (GPN; ecosystem; stack)

Strategic Alliance One among every lead player Many different agreements -not necessarily for market variables- among the different lead players

prices)

Social costs

consumer welfare; no or very slow innovation; more between inequality; nature extractivism

&

Knowledge and data extractivism; nature extractivism; innovation but for more control; + within inequality; tax avoidance; expanded labour segmentation (worse employment for most)

(yet with limited growth & less than what it could be)

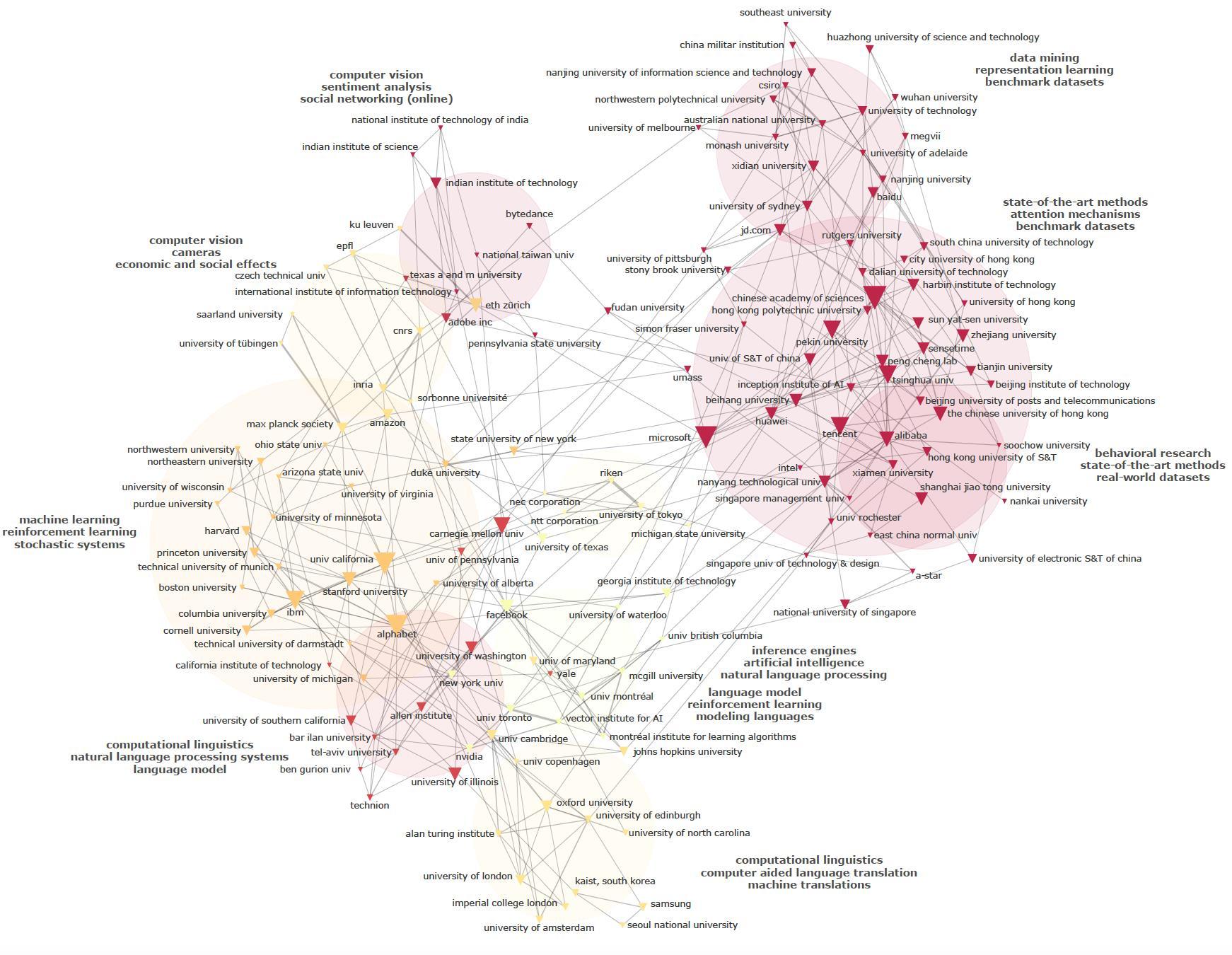

Source:Rikap(2024)–Scopus

(2023)-WebofScience(2012-2021)