DAIRY MARKET REPORT VOLUME 29 | ISSUE 2

2/26/2026

OVERVIEW Milk production is still strong, up 4.2% overall, with milkfat production up 5.6% year-over-year. Several signs of particularly strong domestic protein demand shone through in recently released November data: commercial disappearance of all products on a skim solids basis (which includes protein) rose 4.8% September–November 2025 over a year prior; cheese saw an increase in domestic use of 2% after several months of declines; and stocks of whey protein concentrate fell 16% as demand outpaces supply. Exports also rose, with butter exports nearly tripling (+199%), and American-type cheeses doubling (+119%). However, DMC margins fell to $9.42/cwt, just under the $9.50/cwt maximum coverage level. The Consumer Price Index eased month-over-month to 2.4% annually in January 2026, from 2.7% in December 2025, signaling cooling inflation. Dairy products continue to give consumers a break from inflation at the grocery store, with prices for almost all products falling since early 2025, exception for cheddar cheese.

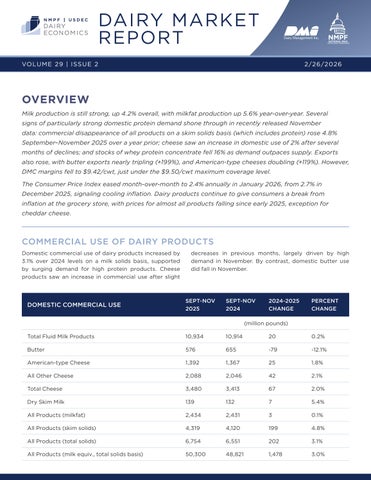

COMMERCIAL USE OF DAIRY PRODUCTS Domestic commercial use of dairy products increased by 3.1% over 2024 levels on a milk solids basis, supported by surging demand for high protein products. Cheese products saw an increase in commercial use after slight

DOMESTIC COMMERCIAL USE

decreases in previous months, largely driven by high demand in November. By contrast, domestic butter use did fall in November.

SEPT-NOV 2025

SEPT-NOV 2024

2024-2025 CHANGE

PERCENT CHANGE

(million pounds) Total Fluid Milk Products

10,934

10,914

20

0.2%

Butter

576

655

-79

-12.1%

American-type Cheese

1,392

1,367

25

1.8%

All Other Cheese

2,088

2,046

42

2.1%

Total Cheese

3,480

3,413

67

2.0%

Dry Skim Milk

139

132

7

5.4%

All Products (milkfat)

2,434

2,431

3

0.1%

All Products (skim solids)

4,319

4,120

199

4.8%

All Products (total solids)

6,754

6,551

202

3.1%

All Products (milk equiv., total solids basis)

50,300

48,821

1,478

3.0%