JIM NABORS, CMC, CVLS, CREV, CFMP

Have you ever heard the term “Tempus Fugit?” It’s Latin for “Time Flees,” now more popularly called “Time Flies.” In my case time has flown by much faster than I ever thought. The privilege of being NAMB President ends in just a few days.

Irene Duford, Loan Team Training

Jason Dickinson, CIC

Direct all inquiries to NM editor & publisher Jilly MacDowell: magazine@namb.org The National Association of Mortgage Brokers is the voice of the mortgage industry, representing the interests of mortgage professionals and homebuyers since 1973.

How’d it go? I know that I tried to do my best in representing our great association & we’ve had some successes. Our board, employees & contractors brought their best and were a pleasure to work with. I do mean work with as they didn’t work for me but for NAMB & the entire mortgage brokerage industry

NAMB has always had two types of members: those who pay dues & those who don’t, and that’s never going to change. “NAMB: VOLUNTEER LED, MEMBERSHIP DRIVEN SINCE 1973” says it all. Get involved, take a side & help us make things better for all homeowners and all of our colleagues in mortgage.

We realized early that communication is key. We need to spread the word on what’s important to us as mortgage brokers & let people know where we stand on an evergrowing list of issues that a ect us all. Communications Chair Je Parry & his committee worked tirelessly to promote & clarify what NAMB is doing & why.

Our Industry Partners committee, under chair Kimber White (who will be President when you read this), added ten new industry partners who have either increased their involvement in NAMB or who chose to join our team for the first time.

Chairman Steve Scott & our Technology committee members have reviewed & recommended sixteen Strategic Alliances to help our members grow their businesses and improve their marketing & education opportunities. He’s also personally gotten me to use ChatGTP, Revive & Inshot. If you haven’t already given them a try, you’re missing some great stu .

Mike Farrell, our incoming President-Elect & Membership committee chair, and his team have increased our head count by 300 percent in the last two years. They’ve also added a liated state associations in California, Texas, Florida & the Carolinas. And they’ve recently established the YP (Young Professionals) committee for LOs under 35 to gain knowledge & guidance to grow their business. Mike also spent hours on TAFAC (The Appraisal Foundation Advisory Committee) so that NAMB now has a partner’s seat on its Board of Trustees.

Helping you grow your business is key to NAMB’s success and Ray Edwards & our Education Committee have overseen some tremendous growth. They recently added a Credit Certification class that will be rolling out before the end of the month. Additionally they worked to add more certification instructors to our CVLS & CFMP programs. Finally, expanding our NMLS continuing education classes has been a huge project that they have done a great job on.

Loan Advisor/Military Specialist, Rate, Inc.

San Luis Obispo, CA & Columbus, OH

• Military spouse

• NAMB member since 2023

• Certified Veteran Lending Specialist class instructor

• Ohio Association of Mortgage Professionals board member

What motivates you in your current position? Serving Veterans at a higher level & providing education to Veterans & the industry is my passion. It’s important to overcome industry myths surrounding the VA loan. I just taught my first CVLS class for NAMB in Newport Beach. It was great!

nia & Ohio markets. I created my own presentation around the curriculum.

But it’s not just that class on that day — you get ongoing support calls & a community to bounce ideas o of, plus a take-home CVLS handbook. You’re not going to remember every single thing the instructor said so it’s a great resource. I still pull mine out every couple of months & I know right where to find the information I need!

What if it’s a one-time thing? You still need to know what you’re doing. If you think you know it all, if you’re wondering if you should take the class, do it! There’s always something more to learn!

Describe your professional mentor. Michael Fischer, with the Veteran Mortgage Advisor Program, completely changed my career. He taught me a good portion of what I know about the VA loan and, through that knowledge & the marketing I learned, I was able to niche myself as a VA lender, which has opened up a lot of opportunities for me.

So you have experience speaking in public? I love teaching. I’ve been teaching realtors & Veterans regularly in the Califor-

But you can do VA without the class, right? Loan o cers shouldn’t be doing any VA loans without this training because they’re so incredibly di erent from other types of loans. Take the training first to honor the Veteran community by doing the work & getting the education required to call yourself an expert.

Favorite vacation spot? Europe! I’m an avid traveler & love to explore new places. NM The CVLS class is free for NAMB Veteran members! Renew every 2 years to keep current. �� namb.org/cvls �� namb.org/nn25

If you're an MLO, you know the drill. Every year means completing continuing education (CE) to renew your license. By 2025, some of you might feel like you've been taking the same courses year after year. (We’ve heard the groans!)

The good news is that the core requirements stay consistent, but there are ways to make it feel less like déjà vu. Let’s break down what you need for 2025 and how Empire Learning is keeping CE fresh & engaging.

First, the basics. The Nationwide Mortgage Licensing System (NMLS) requires statelicensed MLOs to complete 8 hours of NMLS-approved CE each year. These 8 hours are not just random topics, rather they’re divided into specific categories mandated by the SAFE Act. In 2025, your CE must include:

• 3 hours of Federal Law & Regulations: Covering the latest rules and updates from federal mortgage laws (including ~10 topics that the NMLS asks CE providers to cover each year due to complaints from previous years).

• 2 hours of Ethics: This includes content on fraud, fair lending, consumer protection, and generally how to stay out of trouble while doing the right thing.

• 2 hours of Non-Traditional Mortgage Lending: Focusing on loan products and lending practices that go beyond the plain-vanilla 30-year fixed mortgage.

• 1 hour of Elective: A topic of your choice (or your course provider’s choice) related to mortgage origination, which gives a little flexibility for something interesting or new.

BY CHRISTIAN HILL

All together, that's the standard 8-hour CE package every MLO in the country has to complete annually. Complete these, and you're covering the national requirement.

But what about state-specific needs?

On top of the national 8-hour CE, some states require additional “state-specific” education each year. In fact, 25 states (including DC) currently mandate that MLOs take a state-specific course to cover local laws or rules. If you’re licensed in one of these states, you’ll need to add that extra hour (or more) to your yearly training.

Which states are we talking about? Here’s a list of the states that expect a little extra local learning:

BY IRENE DUFORD

You can’t grow if you’re carrying the whole load alone. And yet, many loan o cers are still trying to do it all themselves. Or worse, they’re surrounded by a “team” that slows them down, stresses them out, and keeps them stuck.

The truth is your business will never outgrow the quality of the people around you. Whether you’re just starting to build a team or looking to grow even more, here’s how to ensure you’re creating a dream team — not a drain team!

It’s tempting to hire someone “just like you.” Someone who talks the talk, moves fast & gets it done. But if you already wear the sales hat, you don’t need another rainmaker. You need someone who brings complementary strengths.

Your dream team is made up of people who:

• Love the details you dread

• Deliver an amazing client experience

• Take ownership & don’t wait to be told what to do

• Handle the loan process so you can focus on what you do best

A high-performing loan partner is the driver of the file, making sure clients are cared for and deadlines are met while you’re out building relationships & bringing in new business.

Hiring the right person is only the first step. The real magic happens when you train them well. Most team members underperform not because they’re incapable, but because no one ever took the time to:

• Show them how you want things done

• Explain your systems & flow

• Teach them what a WOW experience really means

It’s not fair to expect someone to deliver exceptional results with no roadmap. When you invest in training early, you stop problems before they start & you build trust fast.

When roles are fuzzy, everything feels harder. You jump in where you shouldn’t, and your team gets stuck waiting for direction, or worse, duplicating work.

Your loan partner or assistant should know:

• What’s fully theirs to own

• What decisions they can make without you

• What client communication should come from them vs. you

When roles are clear, you can let go without losing control — your team gains confidence & you gain peace of mind.

You can teach mortgage skills. You can’t teach work ethic, attitude or willingness to grow. If someone constantly blames, complains or resists they’ll drain your energy (and your business).

Your dream team members:

• Want to grow with you

• Care deeply about the client experience

• Take pride in doing excellent work

• Show up with positivity & professionalism Culture fit isn’t flu , it’s the glue that holds your systems & service together. If you’re noticing repeated frustration with your team, ask yourself:

• Am I giving clear direction?

• Am I consistent in my expectations?

• Do I model calm, kind & focused communication?

The strongest leaders don’t do it all. They equip & empower others to succeed — because a dream team doesn’t just make life easier, they multiply your impact. They help you grow with peace, not pressure. With trust, not micromanagement. Once you’ve got the right people in the right seats, trained & empowered to own their role, you get to do what you do best.

So, ask yourself honestly, “Is my current team propelling me forward or holding me back”? If it’s the latter, it’s not too late to turn it around. Start by hiring & training well and leading with clarity. Because when you build the right team, success isn’t just possible. It’s inevitable. NM

Irene Duford is the founder of Loan Team Training & a nationally recognized trainer, speaker & consultant. She’s passionate about helping LOs hire, train & build amazing teams, and teaching the mindset & self-talk strategies that fuel confidence, clarity & long-term success. �� LoanTeamTraining.com

Most of us in the mortgage industry know by now that FHFA Director Bill Pulte announced that VantageScore 4.0 would be allowed by Fannie Mae & Freddie Mac for mortgage credit score.

“We are making the credit score industry competitive to benefit the American people,” Pulte wrote on X. “Here are some answers as we deliver ‘choice’ for the American people.”

There were few details provided, which left many questions from mortgage professionals — what is the di erence between VantageScore 4.0 and FICO scores, will VantageScore 4.0 have a lower cost, and how does the mortgage industry implement a new scoring model?

The surprise announcement has raised questions in the mortgage industry on how to best implement. While the answers are not crystal clear, there is some information available about VantageScore 4.0 as we await guidance & clarity. We all must be patient to ensure the GSEs develop a final framework.

It’s not a complete surprise though, because in 2022, after extensive testing & review by the Enterprises, FHFA announced the validation of two new credit score models — VantageScore 4.0 & FICO 10T. These new models take into account additional sources of data, including the possibility of some rent payment history, trended data of the

BY JASON DICKINSON

past 24 months of balance & payment history. Most Loan Origination Systems (LOS) will need to make adjustments. AUS systems need to be able to definitively accept Vantage Score. Third Party Credit Reporting Agencies will need guidelines on how to deliver the scores.

The score simulator company ScoreNavigator has a product that can help mortgage companies simulate score improvement for the VantageScore 4.0 score as well as the FICO Score. A credit vendor such as CIC Credit has a ScoreNavigator score simulator tool integrated in its software for mortgage companies to utilize.

Vantage Score 4.0 is based on a score range of 300-850, much like the FICO score models

are. VantageScore 4.0 may help more consumers with ‘thin files’ that lack credit history to potentially qualify for loans. It can provide a score after only one month of credit card history as opposed to a more commonly used 6 months of history with other score models to predict future chance of positive payments.

Vantage Score doesn’t reduce a score much for paid collections. The percentage of payment history, balance to high credit ratio, payment history di ers from what the industry has been using.

There is talk of rental history & utility history being used in VantageScore 4.0 — but there are many questions about this. At this time, individual landlords cannot simply report one history to a database that we know of. There are rent reporting services & most have a minimum number of rentals to be reported; some charge a fee to the reporting rental company & some services don’t report this info to all three bureaus.

Utilities are fairly similar with a few third party companies that consumers can use & some of the bureaus’ self-reporting programs. We’re looking forward to more information on how rent or utilities may e ect the scores.

As of this publication, there is no set timeframe or ETA. The Enterprises are working on the steps for delivery of loans scored using VantageScore 4.0. As more information is provided about how VantageScore 4.0 will be used by the mortgage companies, we will keep you updated. NM

Jason Dickinson is an account executive with CIC Credit. �� CICCredit.com

Our growth has also improved our financial situation and Treasurer Ross Miller, along with our Finance committee, have done a great job of investing our funds to get the maximum return. Ross also heads our Flood Insurance taskforce, which has evolved to encompass not only flood, but also disaster, wildfires, and the increased cost of homeowners insurance for most Americans.

Last October I was told to get rid of DEI. Well, we kind of did. We changed the name, but not the mission. Co-chairs Cathy Lee & Marvin Hudson have worked hard with the Expanding Lending Opportunities committee, looking for ways to help more Americans accomplish the goal of home ownership. This is still the greatest factor in the growth of generational wealth. The videos the team has been working on for our library will be a great help to our members for years to come.

When I joined NAMB in 1993 it was about Government A airs and protection. NAMB understands that legislators & regulators play an important part in our survival. Working hard with our Government A airs chair Lauren Patterson, NAMBPAC chair Mike DeSantis, and their committees have given us some great opportunities this past year, from unanimously passing the Homebuyers Privacy Protect Act to stepping forward when the VASP rescue plan was scrapped.

NAMB worked with both the Senate & House Veterans A airs committees and the result was the VA Home Loan Program Reform Act of 2025, designed to stop unnecessary foreclosures on veterans. We’ve met with FHFA sta to talk about the cost of credit & with many congressman on raising AMI from 80% back to 100% or even 130% to make a ordable housing available to more Americans. But, a new year brings new challenges — and under Kimber White, NAMB will advance the goals that benefit our entire industry.

Growth caused the need for professional sta & hiring both Valerie Saunders as our Chief Executive Strategist and Rocke Andrews as our Chief Financial O cer was just the start. They will play a huge part in helping the Board continue to lay the foundation necessary to expand our membership, education, Industry Partners, communications & strategic alliances, while also helping us to continue to build on our GA successes.

Last but certainly not least, I have to thank Harry Dinham whom I’ve known for the last 30-plus years. When I was President in 2005, Harry was the President-Elect. Now in 2025 he has graciously served as Immediate Past President. It’s been great to have someone who can give you guidance & speak honestly with you on every issue that a ects our industry. I can never thank Harry enough for his guidance, honesty & most importantly friendship.

I’d also like to thank all NAMB members for their support — who knows, maybe 19 years from now I’ll get another chance to be President of the oldest & greatest association promoting the interest of all mortgage originators.

Stay healthy, Jim Nabors

• One-hour state-specific CE: States like Arizona, California (DFPI), Connecticut, Florida, Georgia, Hawaii, Idaho, Kentucky, Maryland, Massachusetts, Minnesota, Missouri, New Mexico, North Carolina, Pennsylvania, Rhode Island, South Carolina (both BFI and DCA agencies), Utah (DRE), Washington (state), and Washington D.C. each require a 1-hour state-specific course annually covering their unique rules.

• Two-hour state-specific CE: A smaller group including New Jersey, Oregon, and West Virginia requires 2 hours on state law topics.

• Three-hour state-specific CE: New York stands out here, with 3 hours of NY-specific CE needed for renewal.

If you hold licenses in multiple states, you’ll have to meet each state’s requirement. The key is to know your states. If you’re not sure, providers like us (Empire Learning) have a handy “state selector” tool on our website where you can select your state(s) & all the courses you need show up automatically! It’s a lifesaver so you don’t accidentally skip that one important hour.

Sitting through similar courses on federal law & ethics every year can get a bit tedious. MLOs are professionals, many in the business for years. After the third (or tenth!) time hearing the same guidelines, you’re probably itching for something new.

Empire Learning takes this approach to heart. For 2025, we’ve rolled out a completely updated 8-hour SAFE Comprehensive course called “Balancing AI and the Human Element (2025).”

As the name suggests, we’re diving into one of the hottest topics in the industry right now: the rise of artificial intelligence in mortgage lending. But we promise we kept it light & practical, not technical. This NMLS-approved course covers your required 7 hours of federal law, ethics & non-traditional lending, and then adds a brand-new 1-hour elective on AI in the mortgage industry.

No algorithm can replace the personal touch an MLO provides, and that’s exactly the conversation we tackle in the elective. How do you leverage new tech to work smarter, without losing the human element that clients trust? That’s the kind of fresh, forward-looking topic that can actually make your elective hour interesting & relevant to your day-to-day work.

The trick to not dreading CE is finding a course that doesn’t bore you to tears. We know you’ve heard some of it before, so we strive to present it in a fresh way with new examples, and sprinkle in timely topics like AI to keep things relevant. The goal is to have you finish your 8+ hours actually having learned something useful.

So knock out your required 8 hours (and any state-specific add-ons) well before the deadline, and choose a course that values your time. NM

Empire Learning is o ering an exclusive 30% discount on all 2025 CE packages for NAMB members. Just use code NAMB30 at checkout! �� empirelearning.com

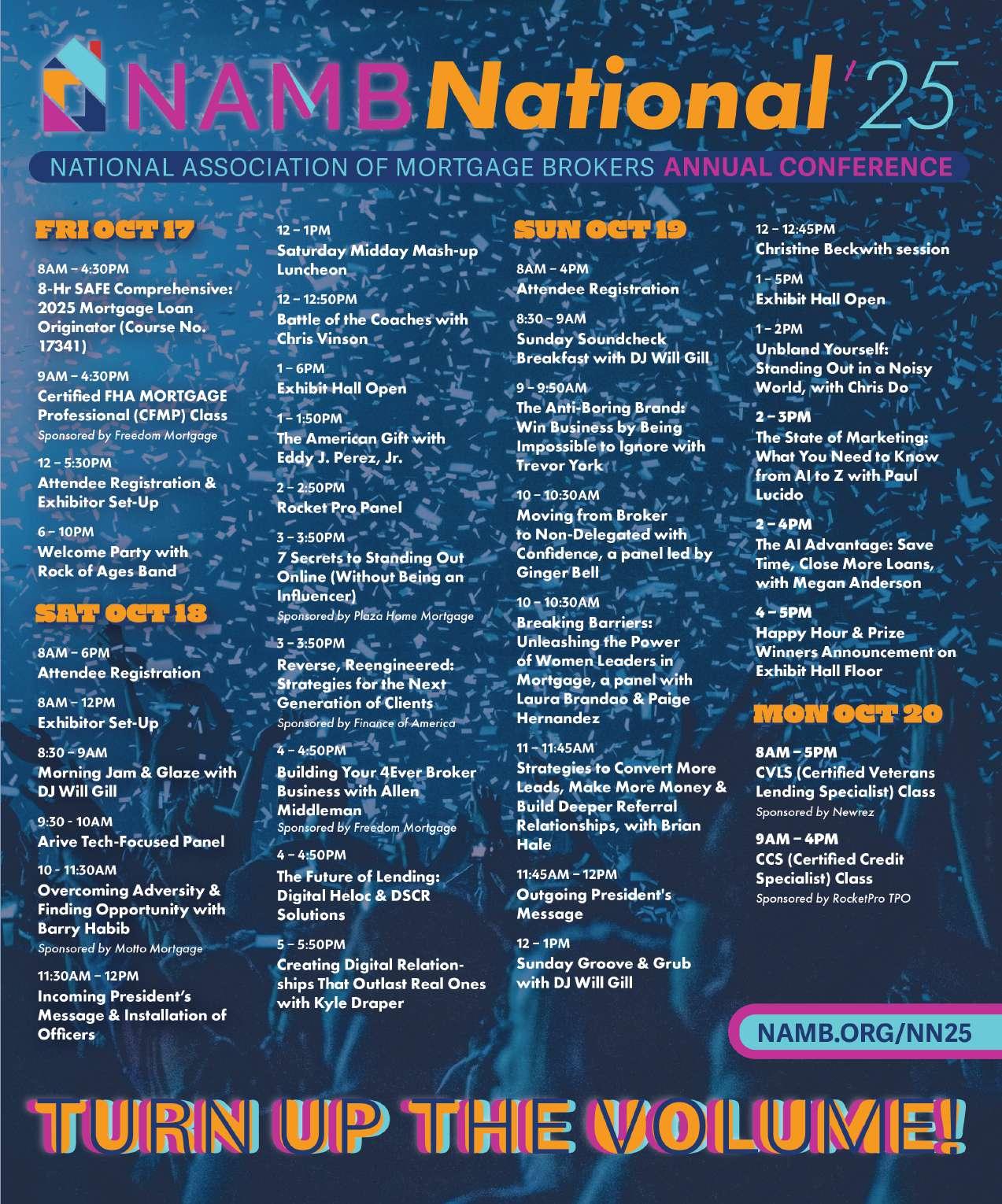

ROOM BLOCK IS GOING FAST! ACT NOW!