What we learned at NACFB Expo Lessons from a bumper day of networking 16 CROSSING THE BOUNDARY Broker guidance as FCA Consumer Duty deadline looms 28 Issue 111 JULY 2023 DIGGING FOR VICTORY The UK SMEs seeking to access home-grown finance 36 40 SECOND TO NONE AN AI FOR AN EYE? How artificial intelligence is reshaping lending processes Normalising second charge loans in commercial lending The award-winning magazine for the National Association of Commercial Finance Brokers Broker COMMERCIAL

Up to 75% LTV available AVMs available up to 60% LTV, and with no fee No maximum loan amount Regulated and non-regulated Dedicated bridging underwriting team

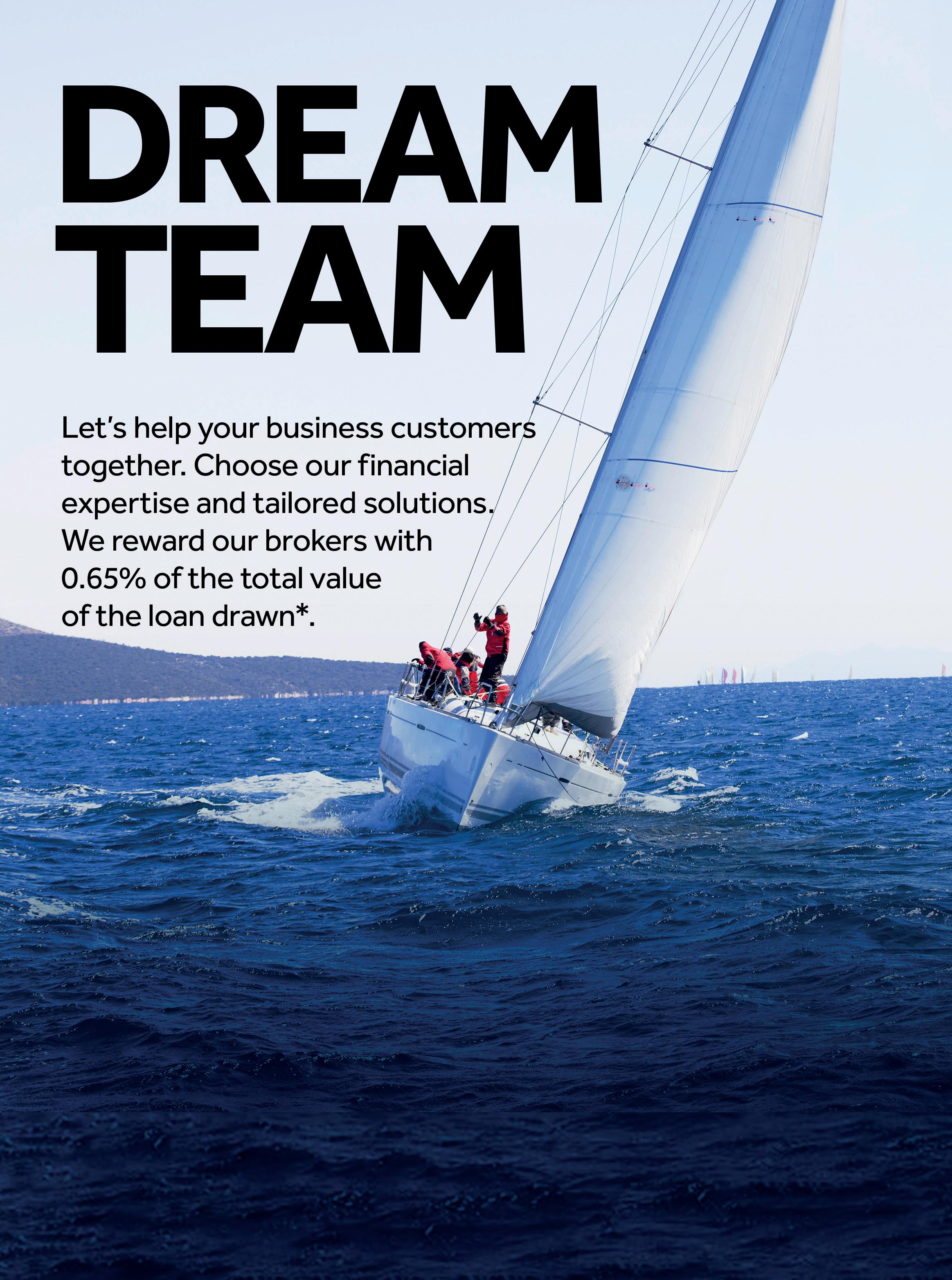

FOR INTERMEDIARIES ONLY - Correct as at 19/06/23 02-09-04 (4) MKT001728-014 Bridging finance

Bridging f inance with a fast turnaround?

In this July issue

Special

Further Information

KIERAN JONES

Editor & Feature Writer

33 Eastcheap | London | EC3M 1DT Kieran.Jones@nacfb.org.uk

JENNY BARRETT

Communications Consultant

33 Eastcheap | London | EC3M 1DT Jenny.Barrett@nacfb.org.uk

LAURA MILLS

Graphic Designer

33 Eastcheap | London | EC3M 1DT Laura.Mills@nacfb.org.uk

MAGAZINE ADVERTISING

T 02071 010359 Magazine@nacfb.org.uk

MACKMAN

Design & Production

T 01787 388038 mackman.co.uk

14 NACFB News 4 Note from Norman Chambers 6 Updates from the Association 8 Note from headline sponsor, Allica Bank 10-11 Industry news round-up 12 Membership news

Contents NACFB | 3 Ask the Expert 18 InPD: Nurturing the next generation of brokers Patron Profile 14-15 Devon & Cornwall Securities: Life begins at 40 Compliance Update 16-17 NACFB: Crossing the boundary 34

Features

Lloyds Bank: Building stronger relationships 22-27 NACFB: What we learned at NACFB Expo 28-29 Federation of Small Businesses (FSB): Digging for victory 30 Reward Finance Group: What’s the big idea? 31 Cynergy Bank: In the know 32-33 Haydock Finance: At a crossroads Industry Insight 34 TAB: The full story 36-37 Somo: Second to none? 40 Opinion & Commentary

Moorgate Finance: Scalability over serviceability 40-41 Evolution AI: An AI for an eye? 42 Shawbrook Bank: The rise of the EoT 44 Listicle: Five signs an SME is in distress 46 Five minutes with: Anastasia Ttofis, Co-Founder & CEO, iLA

20-21

38-39

Norman’s Note

Norman Chambers Managing Director | NACFB

It’s remarkable how life keeps surprising us with one great event after another. Just when we think we’ve experienced the pinnacle of greatness, another extraordinary occasion comes along, leaving us in awe. Such is the nature of progress and innovation.

Looking back, we can’t help but reminisce about the incredible success of the NACFB’s Commercial Finance Expo. What a day it was. The energy, the connections made, and the knowledge shared were simply unparalleled. We want to extend our heartfelt thanks to each and every one of you who attended, supported, and contributed to the NACFB Expo’s resounding triumph.

The event was more than just a gathering of industry professionals – it was a testament to the strength of our community. We saw firsthand the unwavering passion and dedication that drives our industry forward. From the engaging panel discussions to the bustling exhibition hall, every aspect of the event showcased the remarkable talent and expertise within our ranks.

But here’s the exciting part: as extraordinary as last month’s show was, we firmly believe that we have only scratched the surface of what’s possible. We’re throwing down the gauntlet, challenging ourselves and our community to take things to the next level in the years to come. It’s a thrilling prospect, and we know that with your support and involvement, we can surpass even our loftiest expectations.

Our commitment to you, the commercial brokers who make this industry thrive, remains unwavering. We will continue to provide you with valuable insights, expert advice, and opportunities to connect and collaborate. Together, we can shape the future of commercial finance, creating an environment that fosters growth, innovation, and shared success.

So, fasten your seatbelts, because the journey has only just begun. We invite you to join us as we embark on this exciting chapter, pushing boundaries and redefining what’s possible in commercial finance. Thank you for being an integral part of the NACFB community. I can’t wait to see what incredible things we’ll accomplish together.

Welcome 4 | NACFB

WE HELP YOUR CLIENTS TO SPREAD THEIR WINGS Let’s talk. 0344 225 3939 borrow@ccbank.co.uk ccbank.co.uk For intermediary use only. Cambridge & Counties Bank Limited. Registered office: Charnwood Court, 5B New Walk, Leicester LE1 6TE United Kingdom. Registered number 07972522. Registered in England and Wales. We are authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Financial Services Register No: 579415 Whether it’s commercial investment or owner occupier, our knowledgeable relationship managers are here to help your clients continue building a portfolio through straightforward and simple solutions. We’re always here for you. Our flexible finance solutions are perfect for property professionals looking to expand their portfolio

Association updates for July 2023

NACFB News

Consumer Duty: Less than a month to go

With the implementation of the Financial Conduct Authority’s (FCA) Consumer Duty now less than a month away, the NACFB has collated a selection of frequently asked questions from Members, addressing key concerns and providing further clarity.

Forming part of the trade body’s Consumer Duty hub, the online FAQ – which will continue to be updated throughout the coming weeks – can be found alongside video content and downloadable template documentation.

Rob Levitt, NACFB compliance officer, recommended that the trade body’s Members take full advantage of the Consumer Duty hub: “Our Members are committed to providing the best service to their clients, and they want to ensure they fully understand their obligations under the Consumer Duty. The collated FAQs have been informed by our membership readiness survey and highlight areas that required further clarity or where there was any misunderstanding.”

The Association’s support remains available to all Member firms and comes as the NACFB highlighted concerns over some commercial lenders withdrawing their servicing of regulated transactions and not providing the necessary product information in anticipation of the Duty’s implementation deadline.

If you or your firm does not feel prepared ahead of July 31st, then the NACFB’s compliance team is on hand to support, both via the online dedicated Consumer Duty hub – nacfb.org/consumer-duty-hub –and directly via compliance@nacfb.org.uk

MPs launch inquiry into the financing of SMEs

Announced earlier this month, a cross-party Committee of MPs will examine the key challenges SMEs face when seeking finance, the regulation of small business lending, and the role the government can play in enhancing lending to small businesses.

In the wide-ranging new inquiry, the MPs will investigate the accessibility of finance, the role of financial innovation in business lending, and the role of the Bank of England’s Term Funding Scheme, credit reference agencies and government state aid in encouraging small business lending. The MPs are also set to consider the role the government can play in enhancing access to small business finance, the impact of COVID schemes on businesses, and the role of the British Business Bank.

The Committee has invited written evidence submissions on the inquiry terms of reference, to which the NACFB will be responding.

Commenting on the inquiry’s launch, NACFB Chair, Paul Goodman said: “The NACFB stands ready to actively participate in this inquiry, sharing our expertise and insights garnered from working closely within the very heart of the UK commercial finance ecosystem.

“We firmly believe that by collaborating with policymakers, industry experts, and other stakeholders, we can shape an environment that empowers SMEs, enhances access to capital, and fuels economic growth.”

6 | NACFB NACFB News

0800 470 0430 borrow@assetzcapital.co.uk Assetz SME Capital Limited is a company registered in England and Wales with company number 08007287. Assetz SME Capital Ltd is authorised and regulated by the Financial Conduct Authority in respect of its peer-to-peer lending platform only. ’Assetz Capital’ is a trading name of Assetz SME Capital Ltd. Assetz SME Capital is registered with the Office of the Information Commissioner (Reg No: Z3338899) for data protection purposes. View our product guide *Subject to a maximum £5k repaid to borrower upon drawdown of loan. Subject to change & criteria. Free valuations all summer!*

Unlocking green investment with the RLS

Brandon Hall Head of Asset Finance Sales Allica Bank

As the UK looks to become a greener and more self-sufficient energy consumer, it was promising to read in a recent Allica Bank poll of 324 of our asset finance and commercial mortgage brokers that, in the last six months, 60% of them had seen a growing number of enquiries from businesses looking to improve their sustainability. 23% said they’d seen a “significant increase”.

The business community is clearly on board with the green transformation, whether that’s for business or environmental reasons. However, worryingly, nearly half of respondents said that, despite the appetite among business owners to go green, they aren’t convinced there’s enough sustainable funding out there to do so.

This is a big problem. Concerns around green assets having little secondary market value or quickly becoming obsolete, for example, have made it difficult for many lenders to fund them. And when it comes to taxation, it’s also sometimes unclear what does and does not count as a green asset. But if the demand is there, banks like Allica must find ways to help businesses capitalise on it.

Going green with the RLS

Thankfully, the British Business Bank’s Recovery Loan Scheme (RLS) – which provides a 70% guarantee to the lender on a loan supported by the scheme – could be one answer to this. Enabling lenders to lend outside their usual credit appetite, its latest iteration no longer requires borrowers to be in recovery to be eligible.

Instead, it’s geared around driving business growth, and helping a firm acquire green assets to hit sustainability targets or to unlock capital to improve the energy efficiency of their premises could certainly qualify for that.

At Allica, for example, we have funded many electric cars and LCVs, including a whole fleet, as part of our ongoing green asset programme. However, the RLS has allowed us to widen our scope, such as to help a customer reduce their overheads by installing solar panels, or enable another customer to refinance various green assets – things we would have otherwise not been able to do.

To be eligible, your client must be based in the UK and have a turnover up to £45 million. There is no guarantee they’ll be approved, but with there only being one short form to fill in to apply, we encourage you to keep the RLS in mind when exploring their options. After all, it could be the difference between a business taking an opportunity to invest and grow, or not.

8 | NACFB

Note from our Sponsor

Industry News

1. Lenders urged to act on savings rates

The chief executives of the UK’s four biggest banks will meet with the Financial Conduct Authority (FCA) to address concerns that savings rates are not rising as fast as mortgages. This comes with the Treasury Committee having written to HSBC, Barclays, Lloyds, and NatWest to voice concern that savings rates remain too low, with Committee member Angela Eagle accusing lenders of “blatant profiteering.” Committee chair Harriet Baldwin highlighted that while the Bank of England’s base rate has risen to 5%, the big four banks offer rates between 0.9% and 1.75%.

3. Mortgage rescue deal to exclude BTL properties

The mortgage rescue deal the Chancellor has agreed with banks will exclude landlords. The Sunday Telegraph says the small print shows that the Mortgage Charter does not apply to buy-to-let mortgages. Shadow chancellor Rachel Reeves said opting not to include rental properties in the agreement with lenders “...could have severe consequences, because not only will landlords potentially hand higher costs directly onto renters, increasing the risk of evictions, it may also result in a rush to sell buy-to-let properties.”

4. FCA raises greenwashing concerns over sustainable loans

5. New AI-powered tool predicts loan approval for SMEs

Swiss peer-to-peer lending platform CG24 Group has introduced an AI-powered loan predictor tool that provides real-time information on the likelihood of loan approval for SMEs. The tool combines company details and external creditworthiness data, with an algorithm to generate a percentage-based probability of loan approval. Future development plans for the tool include comprehensive decisionmaking to minimise verification steps and empower SMEs to take informed decisions. Founder Christoph M. Mueller, said the goal is to make the lending industry more accessible, efficient and transparent.

2. Brexit rules and EV rollout failure could

A Society of Motor Manufacturers and Traders (SMMT) report suggests fractured supply chains for electric cars and looming post-Brexit tariffs could cost the UK’s car industry over £100 billion in growth. Mike Hawes, SMMT’s chief executive, said: “The Government has set the industry tough targets and we are committed to meeting them. But we are in the middle of the most fiercely competitive investment landscape of a generation and need a UK response, urgently, using every policy, every fiscal and regulatory lever, to make Britain the most attractive place to invest.”

The FCA has identified concerns around the market for sustainability-linked loans (SLLs). Among these were weak incentives, potential conflicts of interest, and apparent low ambition and poor design in some SLLs. The watchdog said market participants “...believe that a more prescriptive framework would improve market integrity and reduce the threat of greenwashing accusations.” Andrew Stanfield, banking counsel at Linklaters, commented: “Greenwashing risks are right at the top of the agenda. Closer scrutiny of sustainability provisions is the natural consequence.”

6. Economy grew by 0.1% in Q1 reports ONS

Office for National Statistics data shows that the economy grew by 0.1% in Q1. The report shows that GDP was up by 0.2% in April, having fallen by 0.3% in March. Ashley Webb, an economist at Capital Economics, said that while the economy steered clear of a recession in Q1, “...with around 60% of the drag from higher interest rates yet to be felt, we still think the economy will tip into one in the second half of this year.”

7. Haldane says inflation could take four years to hit target

Former Bank of England chief economist Andy Haldane says it could be up to four years before inflation hits the Bank’s 2% target. Asked about the target on ITV’s Peston, Mr Haldane said: “In ordinary times getting there in two years is fine. When you get shocks of this type and this size you flex the framework.” He added: “You say, ‘Let’s not do it in 18 months or two years, let’s do it in three years or four years and take our time’.”

cost £100bn

10 | NACFB

2 4 Industry News

8. Bankers: Higher rates needed to tackle inflation

The European Central Bank’s (ECB) annual policy conference has seen central bankers say rates will stay high until inflation eases. Bank of England governor Andrew Bailey said the drag on the UK economy from high inflation would be a “worse outcome” than the hit from higher borrowing costs. ECB president Christine Lagarde said: “I think we have to be as persistent as inflation is persistent,” while US Federal Reserve chair Jerome Powell said that “...the bottom line is that policy hasn’t been restrictive enough for long enough.”

9. IMF: Corporate profits have driven inflation

Analysis by the International Monetary Fund (IMF) indicates that a rise in corporate profits had a greater impact on sending inflation up in Europe than the energy crisis brought on by the conflict in Ukraine. Gita Gopinath, the IMF’s deputy managing director, said: “If inflation is to fall quickly, firms must allow their profit margins – which have shot up during the past two years – to decline and absorb some of the expected rise in labour costs.”

10. Food price inflation eases finds British Retail Consortium

Food price inflation eased for the second consecutive month in June to 14.6% from 15.4% in May and 15.7% in April, according to the British Retail Consortium. Overall shop price inflation also declined in June to 8.4% from 9%. Retailers cut the price of staples such as milk, cheese and eggs, leading to the deceleration. “Households up and down the country will welcome the easing of shop price inflation in June,” said Helen Dickinson, chief executive of the BRC.

Membership News

SMEs in profit despite battling late payment finds Purbeck LendInvest announces £500 million funding partnership

The resilience of the UK’s small business community should not be underestimated, despite ongoing cost challenges including the continuing rise in the cost of borrowing and the scourge of late payment. Purbeck Personal Guarantee Insurance surveyed directors and owners of SMEs across the UK to reveal that 78% are currently turning a profit while just 3% are loss-making and 1% close to insolvency.

The path to profitability has not been easy, however, as on top of general economic uncertainty, 81% of business directors report that they have been affected by the plague of late payment.

A quarter say the constant frustration of late payment has got worse in the last year and 5% of business directors in the survey said it is affecting their business significantly.

Purbeck’s findings come as the Federation of Small Businesses continues to lobby Government for greater measures to hold big businesses to account over the endemic problem of late payment.

Commenting, Todd Davison, managing director of the NACFB Partner, said: “Working with small business leaders, it comes as no surprise that many continue to knock down seemingly insurmountable hurdles. When securing new finance, for example, many are now mitigating the risk of a personal guarantee backed loan through personal guarantee insurance.”

LendInvest has announced a £500 million investment to fund part of its future mortgage originations for its buy-to-let and residential mortgage products from Chetwood Financial Limited. This new funding will further the growth of the NACFB Patron’s offering to private residential landlords and its recently launched residential mortgage businesses.

Chetwood joins the growing roster of global financial institutions choosing to support LendInvest’s mortgage products, including Barclays Bank, BNP Paribas, Citi, HSBC, JP Morgan, Lloyds, National Australia Bank and Wells Fargo.

Rod Lockhart, chief executive officer at LendInvest, commented: “We are delighted to receive this funding from Chetwood to support the scaling of our BTL and residential mortgage products. This funding follows our recent sale of a portfolio of residential buy-to-let mortgages to Chetwood for £243 million, and further strengthens our partnership with the business.”

He said that the commitment from Chetwood underscored the growing confidence and trust that numerous financial partners have placed in LendInvest.

It is hoped that the investment will strengthen the lender’s buy-to-let proposition as well as its newly launched residential mortgage product, with the aim of empowering LendInvest to provide competitive products to professional landlords and prospective homeowners across the nation.

C M Y CM MY CY CMY K 12 | NACFB Membership News

Life begins at 40

Four decades of specialist property lending

Daniel Sproull Director Devon & Cornwall Securities

We have lent on some weird and wonderful properties over the years including an uninhabited Scottish island. It was an interesting site visit!

In fact, at least one of the directors of Devon & Cornwall Securities (DCS) visits every property on which we lend. It’s part of the attention to detail which, we like to think, has led to us celebrating 40 years in business.

Established back in 1983 by solicitor, Dugald Sproull (who is also my father), and finance broker, Peter Cameron, we started trading with a small, £150,000 facility from the Commercial Bank of Wales and grew steadily from there. Today, we provide long-term, truly non-status commercial finance secured on commercial and non-regulated residential property not just in the Southwest but throughout England and Wales.

These days we have a wholesale facility with Shawbrook Bank and like my father, I am also a solicitor, although we are not a legal practice, nor are we regulated by the Solicitors Regulation Authority. However, the fact that we can call on our legal knowledge makes the process of completing loans very different from that of many lenders because the legal position can be considered from the outset thus reducing the potential for last minute hiccups.

It is great to reach our fortieth year of continuous lending. We have been here through thick and thin, through recessions and the banking crisis and today’s uncertain times. While our facilities are naturally more expensive than a high street bank, we like to think that we have helped many borrowers through difficulties when perhaps their credit rating would mean they could not raise facilities elsewhere. We know that many small business owners see us as a stepping stone to getting back on their feet. We offer them the breathing space to regroup before being able to work with their broker to re-enter the more traditional commercial lending market.

There is much talk of artificial intelligence at the moment –immediate online decisions and automated valuations are becoming increasingly popular and advertised as having great advantages over more traditional methods. But there is room in the market for

14 | NACFB Patron Profile

“

A quick completion is usually what everybody wants – the borrower gets the advance, and the broker gets paid their commission

both approaches and here at DCS, we choose to underwrite all cases manually, meaning that, with the assistance of an experienced broker, a clear understanding of the case is gleaned at the outset.

For commercial brokers who have not worked with us before, our offering is simple. We only have one product, and we can lend up to 65% of a 90-day value of any commercial or non-regulated residential property in England and Wales. The only exceptions are we do not do development finance and we do not lend on filling stations.

The fact that one of our directors visits every property we lend on, gives us an invaluable insight into the case and aids a swift completion. Once funds are drawn down, interest must be paid monthly, but there is no fixed repayment date. This means that unlike a bridging loan, there is no cliff edge where rates can increase dramatically when the term expires. With DCS, the borrower is able to retain the facility as long as desired, usually until more traditional (and cheaper) funds are available.

We have been dealing with many of our brokers for years – decades in some cases. We do have an online application form, but in the first

instance many brokers give me a call or drop me an email with some brief details. We really like working this way. Not only does it help to deepen relationships, we find that it helps brokers to really get a feeling for the types of cases we can accommodate. If the case fits, we issue a Decision in Principle and if that finds favour, an offer follows. Our solicitors work very quickly, and completion must take place within 28 days of a satisfactory valuation being received. A quick completion is usually what everybody wants – the borrower gets the advance, and the broker gets paid their commission.

With rising interest rates there is significant competition in the market. We lend at as competitive a rate as we can but are wary of the ‘race to the bottom’. Those lenders who cut their rates too far may be attractive at the moment, but as we celebrate our first 40 years, I think we will still be here for many years to come. Some cheaper lenders may not. We offer a product which I do not think can be found anywhere else. Having been here for four decades, we must be doing something right. We’re excited to support the NACFB in its goal of making the UK commercial finance market second to none.

“

NACFB | 15

Those lenders who cut their rates too far may be attractive at the moment, but as we celebrate our first 40 years, I think we will still be here for many years to come

Crossing the boundary

Last minute broker guidance as FCA deadline looms

James Hinch Head of Compliance NACFB

The Ashes has returned to our shores. Perhaps test cricket’s finest spectacle showcases the game’s best players and places a famous rivalry on centre stage for summer months. All being well, the series will draw to a close on 31st July, by which time we’ll know which team can confidently hold that historic urn aloft and take home bragging rights – and it’s not gotten off to the best of starts for England so far.

The commercial finance industry – indeed more than 60,000 firms across the financial services sector – similarly face a crucial delivery date, for the Financial Conduct Authority’s (FCA) Consumer Duty deadline also falls on 31st July. Just like a well-prepared cricket team, brokers must have their strategies in place, taking the lead, and making sure they have received the necessary information from commercial lenders.

Assessing readiness

After an April survey reviewing firms’ implementation plans, the FCA reported that “…some firms may be further behind in their thinking and planning for the Duty.” This highlighted a risk that some firms may not be ready in time, or they may struggle to embed the Duty effectively throughout their business.

Commercial intermediaries that are at risk of falling short of the immediate requirements need to think carefully – and quickly –about how and when they can catch up. Firms that were feeling optimistic about initial implementations should ensure that their confidence is justified, by examining more closely how their implementation programmes are being executed across the entire organisation.

The focus to date has been on tactical priorities, such as naming ‘Consumer Duty champions’, training staff, conducting product reviews, and assessing management information. Those are undoubtedly important steps. However, the FCA noted from its survey and discussions with executives across the industry, that there is still less than a full understanding of what is required for the July deadline, particularly in terms of communications between manufacturers and distributors.

Ask yourself, are you ready?

The regulator has developed a series of questions that professionals should now be asking themselves ahead of the July 31st deadline. The questions should help firms to reflect on their implementation of the Consumer Duty and identify gaps or areas for improvement. Firms can also expect to be asked questions like these in their interactions with the regulator. Remember, intermediaries can be both manufacturers of their own services as credit brokers, as well as distributors for lenders, so be sure to mull over your response to each question from both perspectives.

16 | NACFB Compliance

10 key questions for broker firms to consider

1. Are you satisfied your products and services are well designed to meet the needs of consumers in the target market, and perform as expected? What testing has been conducted?

2. Do your products or services have features that could risk harm for groups of customers with characteristics of vulnerability? If so, what changes to the design of your products and services are you making?

3. What action have you taken as a result of your fair value assessments, and how are you ensuring this action is effective in improving consumer outcomes?

4. What data, MI and other intelligence are you using to monitor the fair value of your products and services on an ongoing basis?

5. How are you testing the effectiveness of your communications? How are you acting on these results?

As cricket fans watch the Ashes this summer, commercial brokers face their own match with the FCA’s Consumer Duty deadline. To knock the ball out of the park, brokers should have undertaken best endeavours to receive relevant product information from commercial lenders, understood the responsibilities of intermediaries within the distribution chain, and ensured they meet the minimum requirements. By fully embracing a customer-centric approach, conducting suitability assessments, managing conflicts of interest, and investing in professional development, brokers can easily pick-up quick and easy runs within the Consumer Duty regulations.

If you or your firm does not feel prepared ahead of July 31st, then fret not, the NACFB’s compliance team is on hand to support, via the dedicated Consumer Duty hub – nacfb.org/consumer-duty-hub –and directly via compliance@nacfb.org.uk

6. How do you adapt your communications to meet the needs of customers with characteristics of vulnerability, and how do you know these adaptions are effective?

7. What assessment have you made about whether your customer support is meeting the needs of customers with characteristics of vulnerability? What data, MI and customer feedback is being used to support this assessment?

8. How have you satisfied yourself that the quality and availability of any post-sale support you have is as good as your pre-sale support?

9. Do individuals throughout your firm – including those in control and support functions – understand their role and responsibility in delivering the Duty?

10. Have you identified the key risks to your ability to deliver good outcomes to customers and put appropriate mitigants in place?

NACFB | 17

As cricket fans watch the Ashes this summer, commercial brokers face their own match with the FCA’s Consumer Duty deadline

“

Stewart McCombe Course Tutor InPD

Over the past year, a dozen students have successfully navigated their way through the NACFB’s groundbreaking Broker Academy. In September, they will proudly graduate, armed with a Level 3 NACFB Certification of Commercial Finance Broking (Cert CFB). Developed in collaboration with the Chartered Management Institute (CMI), and delivered in partnership with In Professional Development (InPD), the bespoke qualification aims to expand the knowledge and professionalism of both aspiring and established brokers, forging the future leaders of the industry.

Nurturing the next generation of brokers Q

We spoke with Stewart McCombe, InPD’s expert finance tutor, to gain deeper insights into the Broker Academy as it gears up for a second round of student intake.

What does the NACFB’s Broker Academy offer aspiring commercial brokers?

The course adopts a blended learning approach, combining virtual classroom sessions with digital learning modules. Additionally, there are in-person elements throughout the programme. The modules cover a wide range of topics, including

product knowledge seminars encompassing the entire spectrum of commercial lending, as well as workshops on sales negotiation skills. Each student is also paired with a dedicated NACFB mentor, who offers invaluable support, guidance, and direction throughout their learning journey.

What are the key modules covered in the training programme?

At the core of the course are fundamental modules designed to provide a solid foundation of intermediary-led commercial lending. They cover areas such as sales negotiation, proposal writing, the transactional process, as well as leadership and management skills. Moreover, specific sectors within commercial finance, such as asset and leasing finance or commercial property finance, are also addressed, allowing students to tailor their studies to their interests.

What sets the NACFB’s Broker Academy apart from other training options?

&

The NACFB’s Broker Academy boasts the endorsement of the industry’s leading commercial lenders. The bespoke course has also been designed by brokers, for brokers, and therefore shaped by some of the most experienced intermediaries in the field. Moreover, upon graduation, you will be honoured at the prestigious Commercial Broker Awards, a testament to the industry’s warm embrace and commitment to nurturing a new generation of talent.

Could you share some success stories or lessons learned from the first year’s intake of students?

One standout experience was during the fully practical session, where the students applied theoretical concepts to real-world selling scenarios. Their commitment to both their personal growth and the development of their industry peers was exceptional. Being part of this journey has been an absolute joy, not just for the students, but also for the learning support staff.

A

What advice would you give to individuals who are undecided about joining the Broker Academy?

Opportunities like the NACFB Broker Academy are truly rare. If you find yourself on the fence or facing resistance from management, paint a compelling picture of how this knowledge and qualification can transform your brokerage. There is a solid business case demonstrating that possessing a nationally recognised qualification enhances both output and reputation, attracting lenders and clients alike.

The NACFB is currently accepting applications for this year’s intake of aspiring finance professionals, commencing in September. Limited places remain, so secure your spot and find out more by visiting nacfb.org/broker-academy

18 | NACFB Ask the Expert

This one’s for the brokers

Introducing our Broker Direct service.

our local centre of excellence at brokerteam@natwest.com

18s

We’re making it even easier to do business with us, with a new, bespoke service specifically for lending requests under £150,000. Our bank of knowledge is open Monday to Friday, 9am to 5pm. And now with our specialist team on hand, you and your customers can expect clear timing plans from the get-go. Contact

Security may be required. Product fees may apply. Over

only. Subject to status, business use only.

Building stronger relationships

Helping brokers to succeed and innovate

Keith

According to the NACFB’s 2022 survey results, intermediary channels have experienced significant growth compared to other direct channels, which is a demonstration of the contributions made by brokers to the overall resilience of the economy and the support offered to clients.

An evolving market

Amid the uncertainty of the last 18 months, resilience has been the watchword and there are signs that this resilience looks to be gradually evolving into optimism. Official estimates are that inflation will start to decrease towards the end of this year, which should be a welcome boost to confidence levels.

In the recent edition of our Business Barometer, a proprietary survey of 1,200 UK companies designed to equip businesses with the information they need to make confident decisions, they share this optimism. Feedback confirms how, in the coming year, evolving products, staff investment, entering new markets, supporting new technology, and investing in sustainability will be important areas to focus on.

We believe these are areas of interest for the broker channel and highlight further areas where we can support clients with their business and future planning.

Meanwhile, we are committed to listening to broker feedback, making use of our roundtables and webinars, involving senior members of the Lloyds Bank team, from credit, product and pricing. A notable outcome from these conversations is the introduction of our 40 year

partially amortising loan in the real estate team, which can help reduce customer repayments.

Value-driven solutions

We are listening and adapting to the market, which is why we have enhanced our credit policies to support a broader range of clients. We have made pricing adjustments to reshape our broker proposition, for example, for certain sectors like real estate and trading, we have launched an enhanced commission scheme across 2023 that offers a more favourable split of fees (67% in favour of the intermediary).

Our evolving approach is always based on broker feedback. It comes back to building strong relationships, and being there to support you when, how, and wherever needed. Our focus is on providing a strategy that works for brokers and helps them to diversify their product offerings to clients. That’s why we have dedicated relationship teams that stretch across healthcare, real estate, trading, Asset Finance, Invoice Finance and Merchant Services.

Always-on support

Commercially, finding ways for us to say yes to transactions is a priority, and if a decision can’t be made in favour of a transaction,

Special Feature

20 | NACFB

Advertising Feature

“ Our evolving approach is always based on broker feedback

Softly Head of Business and Commercial Banking Intermediaries Lloyds Bank

we can quickly advise. I’m proud that as a through-the-cycle lender, we always take a long-term view to support brokers. We seek to build trust through transparency.

In this vein, our relationship management teams are sharing insights on social media. You can learn more about some of the deals we have done in your area by following your business development manager on LinkedIn.

Working with commercial brokers

Obviously, there are still unknowns around the UK and global economies and these won’t go away overnight. But we remain energised by the opportunity to collaborate, to build relationships, and to offer solutions that help brokers and their clients navigate the challenges ahead.

All lending is subject to status. Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority under Registration Number 119278.

lloydsbank.com/businessintermediaries

In a country that’s always changing, banks and brokers need to work together to help businesses grow. That’s why we offer the breadth of finance and level of service you and your clients can trust.

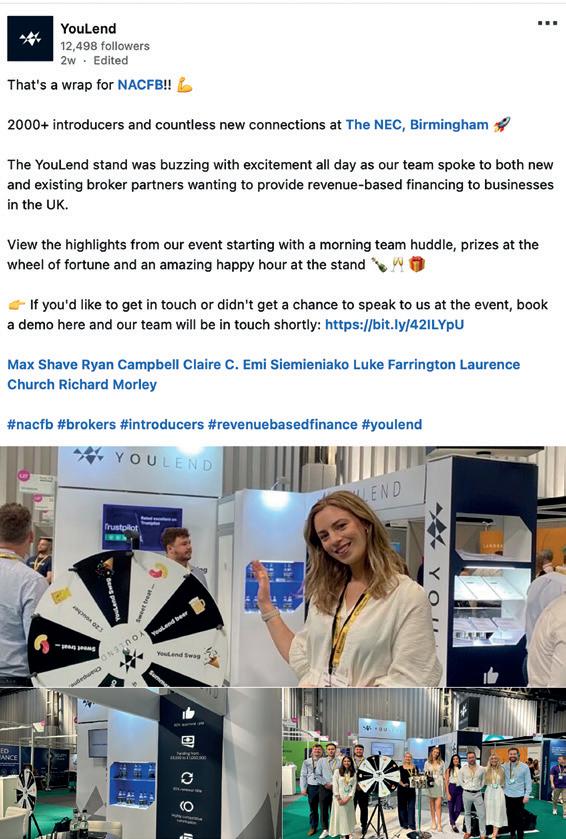

What we learned at NACFB Expo

Lessons from a bumper day of networking

#CFE2023

COMMERCIAL FINANCE

It feels like a distant memory now, doesn’t it? Just a little over a month ago, the NACFB Commercial Finance Expo 2023 returned to its rightful home in Hall 3A of Birmingham’s NEC. Renowned for its immense scale, electrifying energy, and profound impact on the commercial lending sector, this event remains the pinnacle of intermediary-led finance gatherings.

Under one roof, industry titans, driven delegates, and exhibitors from far and wide converged to create an unforgettable experience. In the pages ahead, we have compiled the most significant insights and invaluable learnings shared by these influential figures. We have distilled the crucial facts that shaped the day, highlighted the most impactful social media posts, and revelled in the resonating quotes that echoed through the conference theatre.

Join us as we step through a meticulously curated and retrospective list of learnings and key takeaways, capturing the essence of the NACFB’s flagship event. Whether you were in attendance or not, we aim to inspire you to join the team and your peers in Birmingham next year. Prepare to delve deep into the vibrant tapestry of the NACFB Commercial Finance Expo and we hope you’ll be as captivated as we are by the spirit of this extraordinary day.

1,799 delegates were scanned through registration over seven hours. Impressive.

20 delegates a minute were collecting their lanyards and bags at registration’s – sponsored by Atom bank – busiest point. Buzz.

41% of the broker delegates said their primary area of business activity was in the property-led space. 32% of brokers shared that they operated primarily within the asset and leasing or business finance sectors. Spectrum.

“With NACFB Members having facilitated £45 billion of borrowing last year, all of you here today –brokers, lenders, and borrowers – are key collaborators in helping small businesses achieve their objective.” – Louis Taylor, British Business Bank CEO, celebrates the NACFB community in his keynote address. Backing.

143 different exhibitors were gathered under one roof inhabiting nearly 1,000 square metres of space. 93% of exhibitors were commercial lenders. Community.

424 miles – the distance from Birmingham to Aberdeen. The furthest any single delegate was known to have travelled from to attend this year’s NACFB Expo. Dedicated.

11 – the number of trains that did not meet their scheduled arrival time at Birmingham International station on the morning of NACFB Expo. Signal.

£

#

“Your expert knowledge, understanding, and advice is of great value and is reflected in the faith business owners and funders place in the broker community.” – Brandon Hall, head of sales for broker asset finance at headline sponsor Allica Bank, shares why intermediary-led lending continues to thrive. Driven.

1,152 – The total number of logins made to the NACFB Expo app –sponsored by Keystone Property Finance – on the day. Mobile.

“There are too many people to thank for making the day what it is. It’s a remarkable collaborative effort, an event of this scale doesn’t just come together: it takes months of planning, engagement and overcoming hurdles to deliver what we see today.” – Norman Chambers, NACFB managing director. Gratitude.

3,176 – the number of photos taken by the event photographer on the day. Snap.

NatWest’s James Holian on bank responsiveness: “I don’t think it’s as black and white as high-streets being really slow and challengers being really quick. The reality is each transaction is still judged on its own merits.” Value.

123 decibels – the highest noise levels ever recorded at any NACFB Expo. Apparently, that’s as loud as a rock concert or a motorcycle. Bustle.

25% of delegates who attended the conference theatre session on developing a broker manifesto shared that Consumer Duty requirements are having the biggest impact on their brokerage. Policy.

“It is clear there has been a shift to challenger and specialist lenders, the high-street banks are perhaps wisely taking a step back and undertaking a period of adjustment. At the same time, SME customers are becoming more aware of alternative options.” – Charissa Chang of Allica Bank shared that there is still space in the market for both high-street and challenger banks. Options.

128 gigabytes – the amount of raw footage the event’s videographers shot on the day –totalling two hours. Rolling.

24 | NACFB

#CFE2023 # #

“The fact that there is this lingering inflation and higher than expected interest rates, we are seeing it start to rock small business confidence”

– Martin McTague, national Chair of the Federation of Small Businesses (FSB) shares insight from their members. Caution.

“I am bursting with pride to see just how far we have come as both a community and as a trade body. I am equally as excited to see where this upward trajectory takes us.” – Paul Goodman, NACFB Chair. Leader.

“The SME lending market cannot survive without both high-street and challenger banks being active in it. Customer expectations have changed over the years, and I don’t think the high-streets have quite caught up. Customers used to be driven largely by price, they’re now more driven by speed and certainty.” – Roger Fenwick of NACFB brokerage Mantra Group reflects on the merits of different lender types and shifting borrower expectations. Evolution.

Theodora Hadjimichael, CEO at Responsible Finance on decentralised funding across a more United Kingdom: “What we’ve seen over the last few years is that CDFIs are lending more, and they’re particularly able to reach places and people that find it more challenging to get a business loan.” Scope.

11.34 am – the time by which all 1,500 tote bags – sponsored by Funding Circle – had been handed out to delegates. Handy.

“We have way too many policies and way too many initiatives coming out of government at the moment, they’re introduced too fast and with not enough consultation and not enough commitment over the longer term to make them work for small businesses.” – Jennifer Tankard, principal, invoice finance and commercial finance at UK Finance on her broker manifesto. Clarity.

25 golden tickets for the NACFB’s Summer Party were handed out to delegates. Lucky.

28 live quotes for Professional Indemnity insurance were generated for the trade body’s Members over on the NACFB’s Mutual stand. Covered.

“A lot of the loans transacted through a CDFI are from SMEs that have previously been turned down by another Bank.” – Paul Wain, director of origination and relationship management at the British Business Bank, on why approval rates are lower for CDFIs, and why this is not always viewed as a concern. Context.

#

“Most of the CDFI market is seeing year-on-year growth, and I think that’s something we can expect to see continue in the future.” –

Nicola Parker, senior business manager at SWIG Finance, on the expectation that Community Development Finance Institutions will continue to enhance their national presence. Opportunity.

255 – The total number of submissions made by brokers to the NACFB’s Commercial Broker Awards within a week after the event. The Association’s team were on hand to provide last minute guidance on what makes a successful entry. Merit.

676 – The total number of social media posts made across LinkedIn and Twitter on the day of NACFB Expo that tagged in the trade body or used the event hashtag #CFE2023. Shared.

“The winners are winning more and more, and the losers are losing more and more.” – Nicola Headlam, economist at Red Flag Alert, reflects on the scale of successes and failures of small business owners and why data can help improve outcomes. Casino.

62% of those who attended the conference theatre session on decentralising UK funding said they had engaged with a CDFI in the last 12 months. Levelling.

32,255 steps were recorded by show organiser Ruth Dunn on the day of NACFB Expo, which equates to over half a marathon. Boots.

“AI-powered automation technology will have a direct impact on commercial finance, making the lending process more efficient and seamless for customers and lenders alike.” –Dr Martin Goodson, CEO and chief scientist at Evolution AI seeks to decode artificial intelligence and its impact on business lending processes. Insight.

19°C – the average room temperature in the NEC’s Hall 3A, a full ten degrees cooler than the peak temperature outside recorded that day at Birmingham Airport. “Thank you, air conditioning,” shared known perspirer and NACFB team member Kieran Jones. Damp.

623 – the number of coffees sold via all outlets – including the NACFB Members’ Lounge sponsored by Together and YouLend – throughout the event. Alert.

26 | NACFB

#CFE2023 # #

34% of conference theatre attendees believed that ongoing economic uncertainty was the main reason behind any reduction in SME borrowing. Appetite.

A single sock was the most unusual item turned over to lost property at the end of the day. Other findings include two vapes, one lunch box, and a diary. Mystery.

“It’s behaviours that cause problems for firms, not whether you break a rule or not specifically.” – Julie Ampadu, director, at Chameleon Compliance, outlines why culture is as important – if not more – than pure adherence to regulations in her presentation. Outlook.

91% of delegates in the conference theatre shared that they had experienced a decrease in lending appetite from the high-street lenders on their panel. Challenge.

Friend of the NACFB, Professor Trevor Williams of the University of Derby: “We need a lending revolution. We need more capital to be made available. There needs to be a longer-term commitment to businesses with growth ambitions.” Vision.

2024 – the NACFB Commercial Finance Expo will return next summer. Sign-up to the NACFB’s Morning Briefing to be among the very first to both find out the exact date and secure your place. Thank you.

By 13.15, 103 juices had been handed out at the MFS stall. Mango Dream was the most popular. Tasty.

By 13.15, 103 juices had been handed out at the MFS stall. Mango Dream was the most popular. Tasty.

? # #

Digging for victory

How UK SMEs are accessing home-grown finance

Martin McTague National Chair Federation of Small Businesses (FSB)

Martin McTague National Chair Federation of Small Businesses (FSB)

When buffeted by storms, you batten down the hatches. Translate that into small business terms, and the economic and financial turbulence witnessed over the past few years has seen most small business owners understandably focusing on keeping their ventures going rather than expanding into new areas, with finance taken out in many cases for survival rather than investment.

The pandemic saw demand for credit among small businesses rise considerably. FSB’s Small Business Index (SBI) saw a peak in finance applications in Q2 2020, with a third of small firms applying for funds, well above the pre-COVID trend of around one in seven in any given quarter.

This borrowing to keep businesses going amid lockdowns, trading restrictions, changes to working practices, the need to refit premises, and much more, has left small and medium-sized enterprises (SMEs)

with a collective debt burden (as of May 2023) of £191.6 billion, which is £24.6 billion higher than it was in January 2020, according to the Bank of England. This is, however, around half as large as the excess debt level hit in March 2021 of £49 billion extra, showing that SMEs are gradually digging their way out of the debt pit.

Only one in eight small firms rated the availability and affordability of credit positively in Q1 2023, down from one in five in the same quarter in 2022. Conversely, half of small firms rated credit’s availability and affordability negatively, up from over one in three in Q1 2022.

Over three in ten small businesses applying for credit were offered a rate of 10% or more in Q1 2023, something encountered by only

Special Feature

28 | NACFB Special

“

SMEs are gradually digging their way out of the debt pit

one in twelve would-be borrowers in the same quarter last year. Only one in 20 was offered a rate of up to 4% in the most recent figures, a sharp drop from the 44% who were offered the same in Q1 2022.

The proportion of small business credit applications which were approved in the first quarter was 45%, a very slight improvement from 44% in Q4 2022 but still the third-lowest reading since Q4 2013, highlighting the tight credit conditions faced by businesses at present.

The predicted peak for interest rates has risen steadily over the course of the year to date, each time ratcheting up the pressure on small business borrowers on index-linked rates and making it that much harder for firms and entrepreneurs thinking about expansion to make the sums in their business plan add up.

Adding to these financing woes, we have heard increasing reports from small business owners who have been seeking loans for business-related investment or costs, that lenders are now demanding personal guarantees far more frequently than in the past, even for relatively low amounts. This is having a chilling effect on would-be borrowers’ willingness to take out loans to fund business expansion –which is bad news for the UK economy.

Brokers by their nature will understand the needs of small businesses and are well-placed to help them source the right finance at the right rate. For small firms, the length of the application form for finance is the biggest barrier to taking out credit, cited by three in five –is there something you as a broker can do to simplify the application process for clients? Over one in three say they struggle as they can’t speak to someone about their application, so make sure you’re able to help with any questions. A quarter say the application requires information they can’t access, so clearly set out to clients what will be needed before the process is started, to save later frustration and abandoned attempts.

Many small businesses will first approach their lender, likely a high street bank, for a business loan, and may have lower knowledge of the other types of finance and finance provider which are out there. Challenger banks are keen to grab even more market share, while more established lenders have shaken up how they present their product offering to small businesses in response. There are opportunities here for brokers, especially as rates rise and success rates falter.

The healthy flow of credit into the small business community is a vital prerequisite if this group, 5.5 million-strong and accounting for around half of UK private sector turnover, is to thrive and drive the recovery needed to get us out of the economic doldrums.

NACFB | 29

“ Lenders are now demanding personal guarantees far more frequently than in the past, even for relatively low amounts

What’s the big idea?

Supporting Midlands SMEs at the forefront of innovation

Steph Brown Regional Director, Midlands Reward Finance Group

From technology through to manufacturing, there are many SMEs in the Midlands looking to innovate and are continually working to develop that next big idea to drive growth or disrupt their market.

With that big idea naturally comes a degree of instability in terms of future business success and often an immediate need to acquire commercial finance to fuel growth.

Innovation is not restricted to entrepreneurs or businesses in the early start-up phase. Many established SMEs continually develop fresh ideas, launch new products or harness new technology to propel their business to the next level.

SMEs built on creativity and innovation require specialist advice and expertise from both brokers and lenders who can work collaboratively to help these businesses secure the right funding and guide them when the working facility is in place. To help with this, we’ve developed the following tips to assist brokers who are increasingly working with SMEs in the innovation space.

Share key information

Always advise the SME to develop and share a business growth plan, financial forecasts and other key information from the outset, to demonstrate to you and the lender that they can successfully create and grow a profitable business.

Estimate cash flow requirements

If the client is looking to use a revolving credit facility, they will be drawing down different amounts (or indeed repaying) from the funding facility over a set period. Therefore, request that they estimate their expected cash flow requirements and anticipate any financial issues for the business over the forthcoming 12 months.

Be transparent

Encourage your client to be as transparent as possible. It’s key that the SME relationship between brokers and lenders is built on trust so the business must be able to quantifiably demonstrate – from the outset – that it can afford the loan repayments.

Communicate clearly

Businesses looking to borrow to innovate need to clearly communicate their ideas and expansion plans so that both the broker and lender are confident that the innovation is going to be in high market demand and can even generate potential employment opportunities.

Be honest about how much is needed

Many innovative SMEs we work with need short-term, flexible working capital to bring new ideas to market at speed, so it’s important they’re honest with the broker and lender about the loan amount they need to borrow and the timeframe that is right for their business needs.

If the business is on the verge of that next big innovation, a onesize-fits-all approach to lending clearly will not work. Both broker and lender need to get into the mindset of the SME in terms of the short to long-term challenges the business may face when borrowing, so that the best commercial finance solution can be found which works for all parties concerned.

Special Feature

30 | NACFB Special

In the know

A look at EPC requirements for landlords

James Herron Director Lending Products Cynergy Bank

James Herron Director Lending Products Cynergy Bank

We still expect to see new Minimum Energy Efficiency Standard (MEES) rules introduced in the foreseeable future. These potentially mean that UK landlords may not be able to arrange a new tenancy on any home that fails to get at least a C rating on its Energy Performance Certificate (EPC).

According to Derek Johnson, head of building surveying at Sillence Hurn Building Consultancy, over two-thirds of rented residential property in the UK does not currently have an EPC rating of C or above – so there’s a lot of work to be done.

But these requirements shouldn’t be viewed purely as the latest example of costly and unnecessary red tape imposed on professional property owners. For many landlords, such changes might instead be an opportunity to create more desirable homes and increase demand from tenants.

The MEES is part of the government’s efforts to decarbonise Britain’s housing stock in order to meet its long-term net zero goals. Alongside transport-related emissions, the carbon produced by heating and lighting Britain’s buildings is the most significant source of greenhouse gases (GHGs) in this country, and ministers are understandably keen to promote changes such as better insulation and more widespread use of renewable power sources like domestic solar panels.

In the midst of a cost-of-living crisis driven by soaring gas and electricity bills, energy-efficiency upgrades are even more appealing to renters: by reducing the amount of energy needed to power a home, landlords can deliver significant savings to their tenants. Recent research,

by Legal and General, reinforces this point and the findings show a growing desire for more energy-efficient properties among both buyers and renters, with tenants happy to pay an average premium of 13% for such homes. Increasingly, the size of your monthly energy bills is seen as more important than the size of your house or flat –and landlords who are willing to make improvements beyond MEES requirements could gain in terms of more robust tenant demand and higher rents in the years ahead.

These are not the only potential benefits. Over the next few years, banks all over the world are expected to face greater pressure – from regulators as well as their customers – to decarbonise their loan books. This could mean that landlords whose portfolios meet higher environmental standards might in future be able to get better deals on their mortgages.

The next few years may well see significant changes in the private rented sector, with many landlords choosing to sell up in the face of rising costs and increasing bureaucracy. But for property owners who are willing to go the extra mile to provide homes that meet or even exceed tenants’ needs in terms of energy efficiency, the potential opportunities and rewards are likely to be substantial.

31 | NACFB Special Feature

“

In the midst of a cost-of-living crisis driven by soaring gas and electricity bills, energy-efficiency upgrades are even more appealing to renters

At a crossroads

Analysing the choices car dealerships are facing

Simon Bryant Head

Simon Bryant Head

It is a new era for used car and light commercial vehicle dealerships. Despite the challenges of high inflation and rising interest rates, the used market remains buoyant as more consumers are switching to a used vehicle instead of new. This is due to a variety of reasons including opting for greater affordability amid rising living costs and wanting to avoid long manufacturer lead times.

The global semi-conductor shortage, which caused huge shortfalls in new vehicle production, has had an enormous knock-on effect on used vehicle stock. The parc is reported to be a couple of million short on late used vehicles compared to pre-pandemic levels. Many people ask when will supply return to normal, but the opinion is that there will be unprecedented changes to the used vehicle parc for many years to come.

Whilst there are signs that the new car and van supply is steadily increasing, prices are still holding as the volumes remain restrained. Franchised dealers are holding on to older vehicles to keep their forecourts stocked, instead of allowing them to filter down to the independents. At auction, dealers are having to pay over trade value to stock their forecourt which has a knock-on effect with the retail price for consumers. It is also the reason why many dealers are not willing to negotiate on price as they cannot replace their stock for the same money. There is now more pressure to augment traditional buying routes, searching for private sales, which in today’s digital age, consumes time needed to be invested in producing high quality images and video walk-arounds.

One solution to support dealers to buy and hold stock from either an auction, private sale or trade in, is to have a stocking funding facility.

This facility can help dealers to stock the vehicles they need to achieve their growth plans without having to utilise their own funds.

Working with our broker partners, we have helped dealers to improve their stock profile and put cash back into their business to ease working capital pressure. Simon Pittuck and Angus Griffin, from Mint Asset Finance, said: “Haydock’s stocking facility was straightforward to arrange, they did the majority of the work once we had given them the basic information and the ongoing administration works like clockwork.”

The Financial Conduct Authority’s (FCA) Consumer Duty comes into force from 31st July 2023 which puts the onus on the best outcome for the consumer in retail finance transactions. Many independent dealers have stock funding with retail funders and are therefore under an obligation to provide reciprocal retail business to that funder. Is there a chance that in striving to fulfil that obligation, some dealers may not be able to give some consumers the best outcome? This is where working with a stand-alone stock funder may play a vital role as it will enable the dealer to place their retail finance with a supplier who provides the best outcome for the consumer.

Special Feature

32 | NACFB

“

Advertising Feature

Whilst there are signs that the new car and van supply is steadily increasing, prices are still holding as the volumes remain restrained

of Stock Finance Haydock Finance

The full story

Empowering brokers to submit successful borrowing proposals

Nick

Nick

In the fast-paced world of short-term lending and development finance, speed and clarity are crucial for success.

Lenders recognise how important it is to the broker that borrowing proposals are evaluated quickly and the lending decision is communicated clearly. To achieve this, it is essential for lenders to receive comprehensive information that allows them to assess the transaction effectively.

If the information provided is too sparse, the feedback to the broker will only ever be as detailed or precise as the information provided. Without doubt, this causes delay and can be frustrating for all concerned. Open and direct communication is essential, and in these instances, many lenders will reach out to the broker as soon as possible to gain a deeper understanding of the proposal and identify the specific details required to structure terms. By providing this information quickly, brokers allow lenders to put their best foot forward, which ultimately means smoother discussions with their clients and can eliminate potential surprises down the line.

Alternatively, lenders can simplify the process by providing enquiry forms that act as a checklist, ensuring brokers furnish the proposal with all the essential information required. This more streamlined approach expedites the evaluation process, increasing the likelihood of receiving a prompt decision.

The importance of providing comprehensive information upfront cannot be overstated. To this end, we often encourage brokers to present the downsides of a deal first. By addressing potential challenges from the outset, we can work collaboratively with brokers to find solutions.

For us and many other short-term finance lenders, it is important to go beyond a narrow focus on assets and place greater value on understanding the borrower’s story with all its nuances. This is where the broker plays a crucial role – providing a 360-degree view enables better lending decisions, for the lender, the borrower and the broker. For lenders, it is always reassuring when brokers can paint a compelling picture that captures the essence of the transaction. Of course, the asset (or assets) acting as security are important too and in our experience, brokers are very good a presenting the information for this part of the proposals.

Through all parties embracing a holistic view of borrowing proposals, putting collaboration at the centre of the deal, and ensuring all the information is on the table, the lending process can be collectively streamlined. This approach not only benefits lenders and brokers but also leads to successful outcomes for borrowers which is, after all, the aim.

34 | NACFB

Industry Insight

“

We often encourage brokers to present the downsides of a deal first. By addressing potential challenges from the outset, we can work collaboratively with brokers to find solutions

Russell Sales Director TAB

Built on strong foundations

Reliable development finance that is bespoke to your client’s new build or refurbishment project. With loans from £500k to £30m, we consistently deliver across a comprehensive range of UK-wide development opportunities.

And you can be confident that their funding will be available as and when they need it, all the way to completion.

INTERMEDIARIES ONLY Get in touch

Scan me for further information

FOR

0330 123 0487 DevFinNewBusiness@shawbrook.co.uk

Second to none?

Normalising second charge loans

Jade Keval Sales Director Somo

For landlords, business and home owners looking to raise capital, remortgaging used to be a great solution. But as interest rates and the cost of living continue to rise and house sales slow, its appeal is waning. Increasingly, borrowers are keen to hold onto their fixed rate mortgage or buy-to-let deal.

But that hasn’t stopped borrowers from needing to access cash and whilst there are lots of solutions on the market, in the past, many commercial finance brokers rarely considered recommending a second charge mortgage to their clients.

Today, however, we are starting to see second charge loans become a more common option for borrowers in need of finance. Many have increased equity in their property due to skyrocketing prices over the last few decades, so second charge loans simply make sense. In the current market, they can be cheaper and quicker than remortgaging too.

For those new to the industry, as the name suggests, a second charge mortgage means that the borrower has a second mortgage secured against their property. For the avoidance of doubt, it is a completely

separate loan, often from a different lender, and not an increase on the existing mortgage.

The possibilities are endless

Second charge loans can be used by businesses for a variety of purposes: from upgrading an IT system, to paying off a tax bill, purchasing a buy-to-let property or simply growing a business with new premises, materials or marketing, loan purposes range from those you would expect to some you definitely wouldn’t.

If the possibilities are endless, why aren’t more brokers and intermediaries using them?

36 | NACFB

Industry Insight

“

At Somo, we’re on a mission to make second charge borrowing as normal as walking into a high street bank for a loan

It’s still a niche market. This means that lenders need to be doing more to educate brokers on what they are and how they can be utilised, so that they become an essential tool in the intermediary kit bag of solutions to offer to landlords and business owners. At Somo, we’re on a mission to make second charge borrowing as normal as walking into a high street bank for a loan.

How is it going?

The Office for National Statistics (ONS) reports that annual inflation fell less than expected in March to just 10.1% as opposed to the 9.8% that economists had forecast. Landlord Today recently reported that the typical monthly interest payments on buy-to-let mortgages have soared by an average 75.7% in the past year, and landlords making a full mortgage repayment each month have seen an increase of 31.6%. Despite this, we know there are landlords who have an appetite to continue to buy or convert property. A second charge loan could be a good option for them.

When making a lending decision some lenders like to understand the borrower’s profile in great details. Others, including Somo, prefer to lend based on the value of the property, whether that’s the borrower’s home or a buy-to-let. This means that a second charge can be a good option where brokers’ clients have adverse credit or a short business trading history.

Of course, getting a deal done is not always straightforward, especially

as some first charge lenders have a general rule that they won’t grant consent. Brokers need not necessarily be deterred – we’ll look to lend even when consent has been refused by the first charge lender.

Lots of opportunities for brokers

As interest rates increase and loan costs get higher, it is likely to make 2023 a year of homeowners and landlords staying put and utilising their existing equity for business uses. For brokers, this means there is lots of business to be won through second charge lending, so knowledge of this solution is paramount if they are to reap the rewards.

But it’s not just brokers who need to know more. Borrowers should be asking about second charge loans too which means we need to amplify our message around second charge and educate on the varied purposes, real benefits and possible risks of this loan solution. It’s important that borrowers can make a considered decision that could release equity and maintain their mortgage status.

A recent trends piece by lender MT Finance, reported second charge loans making up 13.7% of the market in 2022. Here at Somo, second charge bridging accounts for around half of our lending and we cover almost every business need, borrower profile and loan scenario. Somo has been an integral part of a wider movement to change the perception of bridging as a viable, accessible alternative form of finance and we’re looking forward to continuing our mission to create a world where second charge lending is standard.

NACFB | 37

Scalability over serviceability

Why brokers shouldn’t lose sight of their purpose

Broker Voice

Adam Drawwater Sales Director Moorgate

As lenders move to new portal-based systems and regulation becomes increasingly defined by duties to consumers, the time has come to invest in systems that truly support your business efficiency and offering. With more and more of an administrative burden chewing through a broker’s day, there is less time to spend with your valued customers making sure that you can deliver the best possible solutions to them.

Ask yourself what you’d rather be doing: back-office admin, or helping your customers with the deals they need to thrive and grow? Ultimately, us brokers are salespeople at heart and the passion for our role is often driven by securing exciting deals for valued customers. Without the right systems in place, our time available for this will only shrink.

The move to portal-based loading has already been made by many asset finance lenders and BDMs, looking after an ever-increasing number of brokers. This ensures that they have the right systems in place to propose and track deals, minimise any unnecessary manual work, and create a faster, more efficient process. This itself presents an opportunity to scale further, but we must ask – at what cost? With larger brokers and networks looking to integrate lenders directly into their CRM via APIs, and a conscious move to automate and therefore de-complicate the process, we must wonder if this could lead to de-humanisation of the industry and the sidelining of smaller brokerage firms.

Ask yourselves: why we are here? Fundamentally, it could be argued, because the clearing banks lack the ability and inclination to process ‘complex’ transactions at the scale they would be required to do so if they solely owned the market. Without us, these types of transactions could lack the level of service needed to see them through or be left undealt with altogether.

We therefore continue to exist as an alternative funding market that has exactly the abilities that these large banks are lacking. We are willing to be agile, to be flexible, to innovate and to adapt to consumer, regulatory and economic conditions as and when required, with the customer always kept in mind.

When you think about it plainly, the clearing banks continue to lose ground to us due to being too process driven and under a much-tootightened structure. Their focus is heavily on quantity over quality, and they are ultimately too afraid of nuance to cater to the ever-evolving market that is their reality. For clarity, this is less likely because they are asleep at the wheel and more likely due to the burdens imposed on them from the multi-faceted regulations and regulatory bodies. Lengthy reporting requirements from shareholders, industry bodies, and regulators all take their toll. The issues accompanying scale alone must be hugely constricting for banks, not to mention the over-arching banking regulations that exist alongside this. Ultimately, it is unrealistic to think that these issues could be resolved any time soon and, on a scale large enough to make any difference. As with many things, the burdens and regulations that exist for banks don’t necessarily fit the world that we live in today but continue to exist and hinder with their requirements.

And our response? We make ourselves more process driven, we focus on quantity to suit the lenders and we run extra fast from nuance, which given what we have previously discussed makes no sense.

Whilst we do need to retain some of these qualities, we need to widen what we believe is possible and work innovatively to find the perfect balance. We do not necessarily have to do so at an organisation level, but as an industry we need to make sure that we are effectively covering all the bases that matter to ensure business efficiency and sustainability. If we hope to build more market power and deal with the most exciting, complex and rewarding deals, then innovation and streamlined processing is where a large part of our attention needs to be.

In today’s world, we need to work closer together to be inclusive, bringing the next generation through whilst maintaining and providing an extensive knowledge base and experience from the heart of the industry. How do we do that? Collaboration amongst varying sized brokerages with a common goal, without taking away the competitiveness which drives great results and innovative solutions for our customers.

NACFB | 39

“ We need to work closer together to be inclusive, bringing the next generation through whilst maintaining and providing an extensive knowledge base

Finance

“

Without us, these types of [complex] transactions could lack the level of service needed to see them through or be left undealt with altogether

An AI for an eye?

Dr Martin Goodson Chief Scientist/CEO Evolution AI

Dr Martin Goodson Chief Scientist/CEO Evolution AI

Aside from the intense media attention, artificial intelligence (AI) is quietly transforming the business landscape. As it continues to advance, AI-powered automation brings significant benefits to the finance and banking industries, with several compelling applications within commercial finance.

The power of automation is no longer limited to traditional rule-based systems. These rule-based systems, like Optical Character Recognition (OCR) data extraction technology, are restricted by clear preset rules and instructions (for example, OCR frequently struggles to decode documents in a different font or style than the documents it was trained on).

Unlike traditional automation, AI brings human-like flexibility and adaptability, empowering organisations to automate business processes that were previously thought to be resistant to automation. Also unlike traditional automation, AI can navigate unfamiliar situations it hasn’t

been explicitly trained for, making it a powerful tool in complex business scenarios. Traditional automation’s reliance on a ruleset makes it brittle and entails extensive intervention and correction by human employees.

Though rapid decision-making has always been a goal of lending, it’s becoming increasingly important to deliver near-instantaneous decisions. Behind the scenes, manual processes, such as obtaining and checking documentation from customers, can be laborious and time-consuming. Frequently, important documents are missing or incomplete, further impeding the decision-making process. Teams of skilled underwriters spend a considerable portion of their time – up to 80% – manually reviewing documents and then extracting from them.

“

40 | NACFB Opinion

Consider, in particular, how AI-powered automation is already transforming asset finance