IRON ORE: CHANGING DYNAMICS

WANTED: W. AFRICAN IRON ORE China’s push to move away from reliance on Australian iron ore has a strong focus on tapping high quality deposits in Guinea. But this requires establishing and investing in the best route to market. Andrew Penfold assesses the options

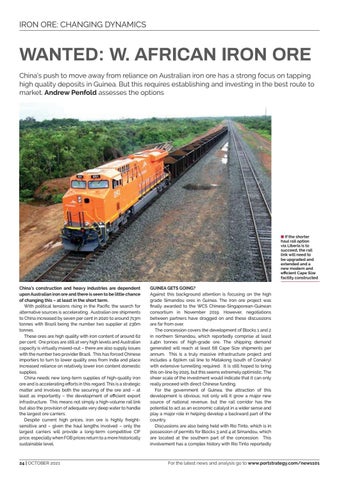

8 If the shorter haul rail option via Liberia is to succeed, the rail link will need to be upgraded and extended and a new modern and efficient Cape Size facility constructed

China’s construction and heavy industries are dependent upon Australian iron ore and there is seen to be little chance of changing this – at least in the short term. With political tensions rising in the Pacific the search for alternative sources is accelerating. Australian ore shipments to China increased by seven per cent in 2020 to around 713m tonnes with Brazil being the number two supplier at 236m tonnes. These ores are high quality with iron content of around 62 per cent. Ore prices are still at very high levels and Australian capacity is virtually maxed-out – there are also supply issues with the number two provider Brazil. This has forced Chinese importers to turn to lower quality ores from India and place increased reliance on relatively lower iron content domestic supplies. China needs new long-term supplies of high-quality iron ore and is accelerating efforts in this regard. This is a strategic matter and involves both the securing of the ore and – at least as importantly – the development of efficient export infrastructure. This means not simply a high-volume rail link but also the provision of adequate very deep water to handle the largest ore carriers. Despite current high prices, iron ore is highly freightsensitive and – given the haul lengths involved – only the largest carriers will provide a long-term competitive CIF price, especially when FOB prices return to a more historically sustainable level.

24 | OCTOBER 2021

GUINEA GETS GOING? Against this background attention is focusing on the high grade Simandou ores in Guinea. The iron ore project was finally awarded to the WCS Chinese-Singaporean-Guinean consortium in November 2019. However, negotiations between partners have dragged on and these discussions are far from over. The concession covers the development of Blocks 1 and 2 in northern Simandou, which reportedly comprise at least 2.4bn tonnes of high-grade ore. The shipping demand generated will reach at least 68 Cape Size shipments per annum. This is a truly massive infrastructure project and includes a 650km rail line to Matakong (south of Conakry) with extensive tunnelling required. It is still hoped to bring this on-line by 2025, but this seems extremely optimistic. The sheer scale of the investment would indicate that it can only really proceed with direct Chinese funding. For the government of Guinea, the attraction of this development is obvious; not only will it grow a major new source of national revenue, but the rail corridor has the potential to act as an economic catalyst in a wider sense and play a major role in helping develop a backward part of the country. Discussions are also being held with Rio Tinto, which is in possession of permits for Blocks 3 and 4 at Simandou, which are located at the southern part of the concession. This involvement has a complex history with Rio Tinto reportedly

For the latest news and analysis go to www.portstrategy.com/news101