6 minute read

The Money Doctor WHY YOUR SAVINGS RATE MATTERS

The past few months many headlines are shining a spotlight on some negative personal finance trends. Here are a few examples:

“Americans are pulling money out of their 401(k) plans at an alarming rate”

Advertisement

“Americans credit card debt hits a record $1 trillion for first time”

“Americans are saving far less than normal in 2023”

It has been a tough time with 2022 inflation running at the highest it has been in over 30 years. Now in 2023, many Americans are feeling the squeeze, but we are encouraging people to review their family savings rate to help stay on track.

How much should you be saving? Let’s take a deeper dive to help you understand the importance of your savings rate.

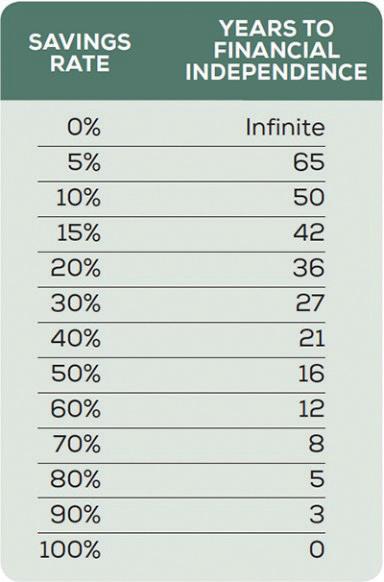

Your savings rate is the percentage of personal income saved based on your total gross personal income received during a period of time. A negative rate means you spend more than you receive. So, if you receive $5,000 this month and save $1,000 your personal savings rate equals 20 percent. For those in the accumulation phase, we like to see a 15-20 percent savings rate toward retirement. Your overall savings rate may be more than 20 percent when you include all other savings goals and debt payoff. Why the 15-20 percent savings rate?

The math behind reaching financial independence is fairly simple. By making a few basic assumptions, in this case a 5 percent real investment return and 4 percent real withdrawal rate, the following chart is the result.

Using the chart you can see how it works. If you make $100,000 per year and save

50 percent, then you only need your investments to provide $50,000 per year in income and you can reach that point after about 16 years. If you save 10 percent, t hen you need your investments to provide $90,000 of income, which would require 50 years of savings. For a person who starts working around the age of 18 to 22, saving 15-20 percent each year will help you reach financial independence in 36 to 42 years or between 55 and 65 years of ageld. When you are young, starting the saving habit from day one, doing it consistently each year and not touching the money are key. As your savings start to add up, working with a financial planner to help you understand all the other items you need to consider will help keep you on track.

It is important to note that the chart and example above oversimplify retirement planning, as it excludes pensions, Social Security, tax planning, long-term care planning, and many other factors that should be considered when planning for retirement or other saving goals. The numbers in the chart give you a feel for how important saving consistently over time can be. They also demonstrate how living below your means and on a smaller part of your income helps you save more and reach future goals more quickly. Beyond reaching financial goals, saving money as part of your lifestyle has other significant benefits. by Clayton Quamme, CFP® a financial planner with AP Wealth Management, LLC (www.apwealth.com). AP Wealth is a financial planning and investment advisory firm with offices in Augusta, GA and Columbia, SC. and y planes. It does not include the z plane, the up and down portion of the equation, because we walked for ages — far more than a quarter mile — and as we got to the very bottom, I stepped wrong and hurt the ball of my right foot. I was already suffering with plantar fasciitis in my left foot, so the thought of going back up the trail and especially up the steps struck terror in me. It was at this point that I started getting suspicious about the increased life insurance. I know, I am a little slow. Anyway, I demanded a helicopter for the trip back up, but she paid me no mind, so I had to go back up mostly using the ball of my left foot and the heel of my right foot. I assure you that the pain of the trek back up wiped out any of the humor I may have found in the situation, but that wasn’t true for observers of my torture. I think I remember hearing my better half calling it The Ministry of Silly Walks (Google it if you don’t know), but it may have just been heatstroke. I survived the trip, but I was considerably more winded this time despite the “shorter” trail with fewer steps. I think that was because of the odd way I had to make my way back up the trail. Feet just aren’t designed to work that way.

Psychologists have studied the impact of individuals’ financial habits on their overall health and wellbeing for many years. They have found that practicing good financial habits such as having a healthy saving rate will help you experience lower levels of stress.

In addition, children learn the majority of their financial habits from family and friends, parents in particular. It is especially important that we take the time to monitor our own saving habits, which will help us demonstrate and teach future generations the habits which will lead to a healthy lifestyle.

Savings rates are something we really enjoy helping clients evaluate and understand. The discussions we have with clients provide peace of mind, promote living a healthy lifestyle, and ensure they pass on positive habits to future generations.

This fall is a great time to evaluate your savings rate. You may be surprised by what you find! A few small changes can make a big difference over time, not just for your financial picture, but also for the health of all members in your family.

Once we got home from the trip, my lovely wife bought me a new pair of sneakers to better support my arches and they are making a big difference. I got back to the gym after the trip and seem to be fully recovered. The lessons from this story for me are manifold:

• Make exercise a part of your routine, and start now because now is better than tomorrow, and tomorrow is better than never.

• Find a reliable friend to exercise with and enjoy the mutual encouragement.

• Take time to walk the trails and see the sights of life with your loved ones while you can.

• Never trust your spouse when they promise no hikes that day

• Get good sneakers before exercising.

• Check with your physician before beginning an exercise regimen. (The lawyers made me add this one.)

J.B. Collum is a local novelist, humorist and columnist who wants to be Mark Twain when he grows up. He may be reached at johnbcollum@gmail.co

Our Next Issue Date

More Americans have died on US roads since 2006 than in World Wars I & II combined

This is a very short story about Amy Groves. When Amy was five years old she lived in Berlin, Germany with her parents and brother Billy. Her father was an officer in the US Army’s elite Berlin Brigade. The Groves family lived in a house at Bibersteig 2 on a large residential city block. Passing traffic sometimes moved very fast and Amy was not allowed to cross the street by herself.

The year was 1977 and the Cold War was indeed very much alive. Jimmy Carter was President and our relationships with countries behind the Iron Curtain, especially the communist German Democratic Republic (East Germany), were not very cordial to say the least. Berlin was 110 miles inside a hostile East Germany, so Americans were very isolated. No matter where you lived in West Berlin, you were never very far from the Berlin Wall and its dastardly implications.

Berlin is very far north, and in the summer full daylight comes very early, around 3 o’clock. Early one June morning, about 5 o’clock, Amy’s mother awoke with a strange feeling — probably mother’s intuition — and discovered that Amy was not in her bed. The front door was wide open. She quickly searched the house. Amy was gone! She woke up Amy’s father and brother, and the search quickly moved outside as thoughts of every parent’s worst nightmare began to race through their collective minds. Was she kidnapped? Taken by East German agents? Did she just wander off into the Grunewald, a large wooded city park just down the street that was home to wild boar?

As her forlorn family stood in the front yard for a time period that seemed as if it were forever but was probably just a few minutes at most, Amy appeared in the distance. She was jogging! She had on her very stylish German jogging outfit and was just chugging along. She had gone around the block several times and was very surprised at her family’s welcome. All were very relieved that she was safe. Amy’s first words were, “But I didn’t cross the street!” And indeed, she had not.

+

— by Col. William C.

Groves