• Over 450 years of experience - Zygmut August founded the Royal Post in 1558.

• over 90 000 employees

• Over 8 200 posts

• Active on the regulated market

• National operator obliged to provide "universal services"

Capital Group of Poczta Polska S.A.

ABC in Poczta Polska S.A. - beginnings

• 2004 - beginning of works

• The need to fulfill obligations resulting from the III Postal Directive

• Benchmark - 12 from 15 posts from the "old UE" have implemented ABC

• 2006 - new operational structures in PP S.A.fundamental change of the conception

• 2009 - ABC model ready for implementation

ABC in PP S.A. - beginnings

• 2009 - external audit of data sources for the ABC Model - a partial change of data sources was recommended

• 2010-2011 - change of data sources, reconstructing the Model

• 01.01.2012 - ABC as the only activity-based costing in Poczta Polska

Why ABC?

• ABC can be applied only in production - myths about activity-based costing

• Indirect costs in service companies

• Fixed costs in service companies

• The paradox of marginal costs in services

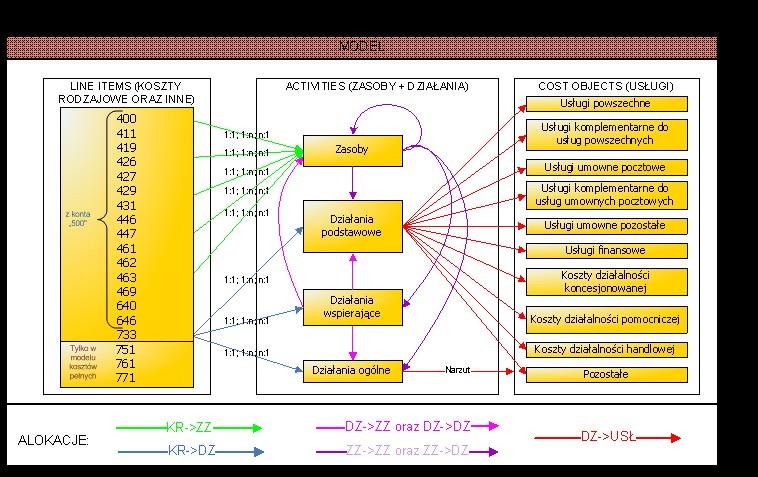

The flow of costs scheme

costs resources activities services

• In order to provide services certain actions are taken

• Taking actions triggers use of resources, which incur costs

• All costs are allocated to individual services provided by PP S.A. (incoming costs equal outcoming costs)

The flow of costs scheme

Activities in PP S.A.

• Basic activities - directly connected to the process of providing services:

• Supplementary activities - fulfill a supplementary function with regard to other activities or resources; costs allocated to the supported activities and resources

• General activities - lack of possibility to establish a direct connection to services (and other activities or resources); costs accounted by charges on services, general activities appear in two variations:

• allocated to all services of PP S.A. (e.g. "Organization Management")

• allocated to all services of organizational units in which the given activity is performed (general activities - specific - e.g. "Markting and Trade Activities in Logistics"),

Grouping activities into technological phases

Sending phase - receiving in various formats

Shipment and sorting phase - sorting, exchange, back-up activities

Return phase - delivery, handing over at the counter

Transportation phase - transferring of packages in Poland and abroad

Process- the ABC

Elementary level- technological operations

• The technological process of every service is divided into operations assigned to them :

– Internal instructions and regulations

– Working with technologists and operational employees

– Direct observations in close to 100 posts of all kinds

• A standard set for every piece of service

• The structure of process description is precisely fitted to the structure of the Model

• Periodical updating of operational standards

Elementary level - flow of streams

• Technological process of each service after dividing into operations was examined with regard to frequency of their occurrence

– Internal instructions and regulations

– Works with technologists and operational employees

– Direct observations in close to 100 posts of various kinds

• Use of data from systems and statistical research

• Cyclical updating (using average results from 3 turns of research)

Process cost - evaluation

• It is calculated for the whole volume of the given

Advantages of TDABC over ABC • Easier Model maintenance and its updating

• Simplification of the Model • Better correlation with Process Management

TDABC elements in PP S.A.

• There are over 150 carriers used by PP S.A. for costs accounting in ABC

– Wages costs, number of employees, area, energy consumption, number of kilometers, etc.

– Considerable reduction of the surveys importance

• For over 70% of costs time is the carrier

• Measuring the duration of operations and statistical research regarding the flow of streams (basing on strictly followed rigorous methodology)

ABC model complexity in PP S.A.

Plans

• Model extension enabling valuation (apart from currently available costs of: operations, activities, phases, products) as well as valuation basing on segments and individual clients

• Building the System of Managerial Information and the ABC integration as one of the reporting perspectives (product perspectives; the other perspectives are client perspective and PP S.A. post perspective)

• Updating the Model on account of the changes planned in Post Law

• Dr Tomasz Cicirko – Office Manager

Office of Managerial Accounting and Financial Liquidity

tomasz.cicirko@warszawa.poczta-polska.pl

• Karol Sikora – Head of Department for Managerial Information

Office of Managerial Accounting and Financial Liquidity karol.sikora@centrala.poczta-polska.pl