Bojan Šćepanović MCB Management Center Belgrade ICV Serbia

8th International Controller Congress Poland 2014 Poznan, March 2015

A very happy, natural and relaxed man

I have two kids (Milica, 17 and Pavle, 14) and a lovely wife (Sandra, 19, she is counting years from our 1st kiss). I enjoy all kinds of sports and especially the sports not recommended for my age (43) and weight of 100+ kg (snowboard, squash, diving, basketball...)

I am crazy for my son`s basketball matches and for my daughter’s school success. Of course, the most important thing is my wife and our country house ("Trešnja"). I am a real "cowboy" over weekends...

Besides, I try to do something in my professional life. Because I have never seen a "bad CV", now I have to talk about my "success, how I am a brilliant, natural genius, the best in the world" Blah, blah.

So, sorry... This is a boring and official part of me

I have been a professional trainer for Finance and Controlling for 13 years, with 950+ trainings. So, maybe I am the most experienced trainer in Serbia for Controlling... who knows?

Also, I have been a "bean counter" and a chartered accountant since 1998. I am President of ICV Serbia, and we are the biggest controlling working group outside Germany. Can you imagine 175 controllers in one place? I can.

I have more than 22 years of professional experience in Finance, Controlling and Management (accountant, chief accountant, controller, controlling manager, CFO, CEO).

I developed 15-20 different training courses in Controlling & Finance. Since 2011, I’ve been holding trainings under the program of Controller Akademie Munich and we are the only company that offers all 5 trainings of the Diploma Program

And now let me get back to my private life. My motto is edutainment, namely, education + entertainment. I try to enjoy life and I want the participants of my trainings to enjoy together with me. I believe that education must be entertaining and relaxed.

Bojan Šćepanović

CEO, MCB Management Centre Belgrade President, ICV Serbia mcb@eunet.rs +381 63 7004 518

Skype: bojan.scepanovic.mcb

LinkedIN, Facebook, Viber, WhatsApp, , etc

Act 1: Situation

The American concept Balanced Scorecard focuses on 4 main perspectives:

Customers

Finance

Processes

People

On the other hand, the concept of German Controller Akademie has three perspectives:

Growth

Development

Profit

In both approaches, one of the key things is processes.

Controlling may be viewed as a management process According to the International Group of Controlling (IGC), a controlling process may be split into 10 main sub-processes:

Operating planning and budgeting is one of the classic processes in controlling In fact, we can say that the introduction of controlling starts from the budgeting process. 2.

Operational planning and budgeting

Act 2: Complication

Budgeting process is necessary in companies but also has many shortcomings. Some managers like to view budget as a rigid, fixed thing Others think that they don’t need budget at all and that it cannot be planned

Budget...

Fixed rules!

The major problems arising in a budgeting process:

No budget at all?

Fixed character. Budget is brimming with rules: “you cannot spend more than 50 euros on materials... you can have 224.25 euros for entertainment costs in October 2015... you can hire two persons in July 2016...” A fixed budget does not encourage employee creativity.

Form over substance. Employees do the planning for the sake of form rather than substance.

Static character. Budget implies that the world is static and that it doesn’t change

High level of detail. Budgeting sometimes boils down to frantically chasing minute details Many companies have hundreds and thousands of cost centers, thousands of cost lines, charts of accounts, SKUs, products...

Costs It is estimated that the cost of budget preparation is 20 FTE per 1 MEUR of sales For example, if you have 100 MEUR in sales, then the cost of budgeting process is 2,500 FTE.

No direct link with strategy. Strategic planning takes place “somewhere up there”, while operating planning takes place “down there”. Strategists think in terms of their wonderful PPT slides, matrices, portfolios, visions and alike while, on the other hand, controllers are blocked in operating terms with a bunch of Excel files. There is no mutual cooperation and they look down on each other with disdain.

Time Budget preparation takes 3 to 6 months Or, as a controlling manager said: “We work for six months on budget preparation and then we prepare for another six months for the next budget”

New Year’s fever If a company has some money left in the budget, then this money is spent mercilessly shortly before the end of the year “You better spend the money now because you will not have it any more in the budget” Those who have saved any money in the budget are punished, for they will have a lower budget next year

History. Budgets are based on historical data rather than on future trends Controllers try to find the 54th way of extrapolating a past trend

“But the budgeting process at most companies has to be the most ineffective practice in management.

It sucks the energy, time, fun and big dreams out of an organization. (…)

And yet (….) companies sink countless hours into writing budgets. What a waste!”

Controllers get very frustrated when the word “budget” is mentioned. Budget usually means several months of frantic work, sleepless nights, anxiety and commotion.

A company should ensure a compromise between high goals and free people.

Act 3: Resolution

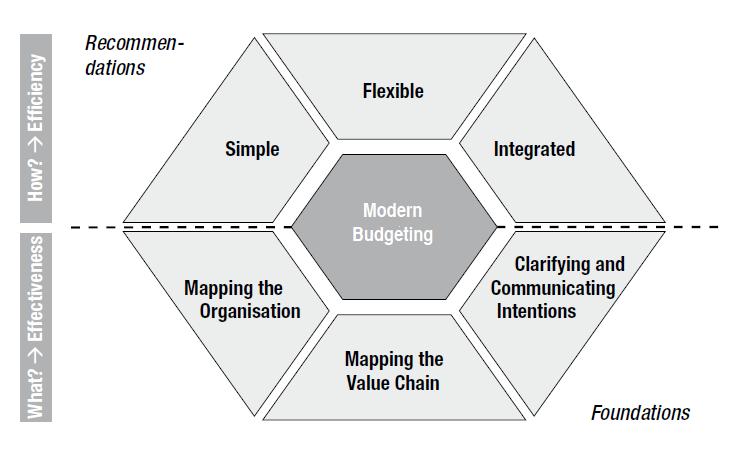

ICV recommends Modern Budgeting, which has 6 main parts:

ICV approach implies a mild revolution in the budgeting process

On the other hand, Beyond Budgeting implies a revolution in the budgeting process. Beyond Budgeting abolishes budget as a process

One common metaphor for explaining the changes in the budgeting process is a story of a crossroads in a small Danish town

Beyond Budgeting is a concept that was created during the 2000s. The main proponent of the concept is Beyond Budgeting Round Table. The BBRT is an international shared learning network of member organizations with a common interest in transforming their performance management models to enable sustained, superior performance. BBRT helps organizations learn from worldwide best practice studies and encourages them to share information, past successes and implementation experiences to move beyond command and control.

The BBRT promotes a set of principles that lead to more dynamic processes and front-line accountability. Organizations that follow this approach transform their management model in line with these principles, which are outlined in "The Leader's Dilemma: How to build an empowered and adaptive organization without losing control", by Jeremy Hope, Peter Bunce and Franz Röösli, published by Jossey-Bass.

Solvingaserious budgetconflict

Step1

Thebudgetpurposes Separate

Budget=

•Target

•Forecast

•Resource allocation

Target

Forecast

Resource allocation

“Samenumberconflictingpurposes“

„Different numbers“

Step2

Improve

•Ambitious

•RelativeKPI

•Holisticperspective

•Expectedoutcome

•Lessdetails

•Dynamic,noannual allocation

• KPItargets

• Trendmonitoring

„Eventdrive, notcalendardriven“

The BBRT is at the heart of a movement that is searching for ways to build lean, adaptive and ethical enterprises that can sustain superior competitive performance. Its aim is to spread the idea through a vibrant community.

Beyond Budgeting calls for a change in the way of thinking of the entire company. I usually say that Beyond Budgeting calls for a change in the way of thinking in HR (leadership) and in controllers (budgeting process).

The 10 Beyond Budgeting principles:

HR (Leadership)

1. Values Govern through a few clear values, goals and boundaries, not detailed rules and budgets

2. Performance Create a high performance climate based on relative success, not on meeting fixed targets

3. Transparency Promote open information for self-management, don’t restrict it hierarchically

4. Organization Organize as a network of lean, accountable teams, not around centralized functions

5. Autonomy Give teams the freedom and capability to act; don’t micro-manage them

Controller (Processes)

6. Customers. Focus everyone on improving customer outcomes, not on hierarchical relationships

7. Goals. Set relative goals for continuous improvement, don’t negotiate fixed performance contracts

8. Rewards. Reward shared success based on relative performance, not on meeting fixed targets

9. Planning. Make planning a continuous and inclusive process, not a top-down annual event

10. Coordination. Coordinate interactions dynamically, not through annual planning cycles

11. Resources. Make resources available as needed, not through annual budget allocations

12. Controls. Base controls on relative indicators and trends, not on variances against plan

Although the Beyond Budgeting approach seems unusual and strange to 99% of controllers, many companies have implement it