A Commercial Real Estate Publication at the Intersection of Information and Innovation

The AI Advantage

Kyle Matthews’ Toolkit for Winning CRE in 2026 & Beyond

A Commercial Real Estate Publication at the Intersection of Information and Innovation

The AI Advantage

Kyle Matthews’ Toolkit for Winning CRE in 2026 & Beyond

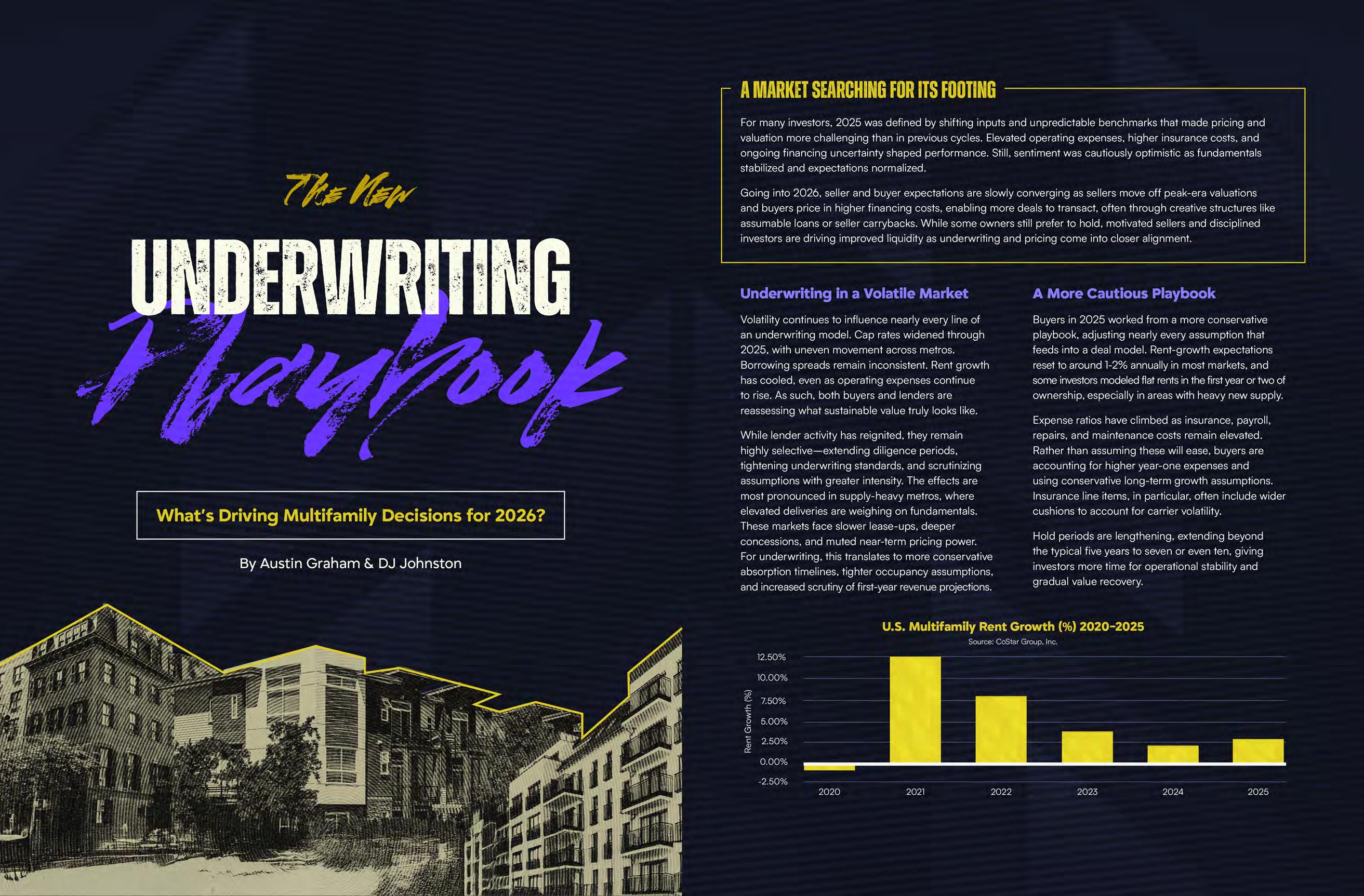

Top 10

Multifamily Markets for 2026

Retailers Driving National Growth

Multifamily in Transition Supply Imbalances, Capital Re-Engagement, & a New Underwriting Era

Emerging

Reawakening

Publications Leanne

McKenna

Research

Daniel

The AI Advantage

Kyle Matthews’ Toolkit For Winning CRE in 2026 & Beyond

Tenant Radar 10 Retailers Driving National Growth

Multifamily Supply Paradox Too Much, Too Fast

Top 10 Multifamily Markets For 2026

Institutional Capital Returns to Multifamily

The New Underwriting Playbook What’s Driving Multifamily Decisions for 2026?

As I reflect on our journey over the last decade, I’m filled with gratitude for your trust, your loyalty, and your role in helping us grow into one of the nation’s leading names in commercial real estate. Last year we shared the next chapter in that journey, one that’s as much about honoring our legacy as it is about shaping our future.

Matthews Real Estate Investment Services™ will simply be known as Matthews™.

This rebrand was more than a name change. We’ve long operated as a modern, agile, tech-forward company. Now, we’ve simply put a name to what we’ve already become: a firm built for the speed and complexity of today’s market, without ever compromising the expertise, hardwork, and clientfirst mindset that defines Matthews™.

The world is evolving and so is commercial real estate. As technology reshapes how business is done and expectations around speed, access, and intelligence grow, we knew it was time to evolve the Matthews™ brand to better reflect the company we are building. A brand that’s bold, streamlined, and digital-first, rooted in deep market expertise and a forward-thinking approach.

Dropping “Real Estate Investment Services” from our name allows us to express a more focused, modern identity—one that better resonates with our clients, our agents, and the markets we serve.

We also refreshed our visual identity. Our new darker blue palette communicates a deeper sense of strength, confidence, and sophistication, while still staying true to who we have always been. It’s a subtle but meaningful change that aligns with the energy and direction of the Matthews™ brand.

This darker tone mirrors our unwavering commitment to excellence and bold thinking. It sets the stage for innovation while underscoring our promise to deliver value, integrity, and long-term success in every interaction.

While our look and name evolved, our mission remained constant: to be the most trusted, hardestworking, and tech-driven firm in the business.

We still and always will be hyper-focused on client success. Relentless in pushing boundaries. And rooted in the relationships that got us here.

Thank you for being part of our story. The future of Matthews™ is bold, dynamic, and just getting started. We’re honored to have you with us along the way.

With appreciation,

PROPERTIES

DEALS

INSIGHTS

TRANSFORMING

How We Prospect, Market, & Close

DELIVERING Instant Market Clarity with Precision-Curated Insights

Brokerage is evolving, and today’s top producers are leaning into better tools and smarter systems not to reinvent the business, but to elevate how they operate. AI and modern systems now enable brokers to identify the right opportunities faster, stay consistently engaged with their relationships, and walk into every conversation better prepared. As the market becomes more competitive and information-rich, the brokers who master these tools will operate with clarity and efficiency, which compounds into stronger deal flow over time. The following Q&A with Kyle Matthews explores how these shifts are shaping the way brokers work, compete, and win.

“Winning smarter means ruthless efficiency. It’s about eliminating 80% of the work that doesn’t help produce revenue,” Matthews says.

Productivity now hinges on action, not accumulation. Speed isn’t just an advantage—it’s the differentiator between a deal that closes and one that stalls.

“In 2025, the smart broker isn’t the one who spends six hours building the perfect property analysis. It’s the one who uses modern tools and spends the other 5.5 hours prospecting. Winning smarter is about leveraging technology to automate timeconsuming, low-effort work, freeing up that primetime cognitive energy for originating new business.”

By 2026, AI is no longer a toy; it’s the ultimate assistant. This shift from passive to proactive brokerage is where AI delivers its greatest value.

“I expect AI to be our broker’s prospecting engine. It should be sifting through public records, loan maturity data, and market trends to build a “hot list” every single morning. It should be telling my broker, ‘This owner is 80% likely to sell in the next 12 months. Here’s their contact info.’”

He continues:

“AI’s job is to tee up the ball. The broker’s job is to hit the ball. The technology does the heavy lifting. This allows them to move from reactive brokerage (waiting for a call) to proactive deal-making, all while freeing up time to call their agent network for offmarket intel.”

In practical terms, brokers aren’t just reacting to the market anymore—they’re anticipating it. Instead of spending hours assembling fragmented intelligence, brokers start their day with a curated set of opportunities that actually matter. They’re not chasing leads; they’re prioritizing the ones most likely to convert.

This shift also transforms how brokers approach clients. Rather than relying on broad outreach, they can open conversations with specific, data-backed insights that immediately differentiate them. When a broker shows up with clarity on a seller’s timing or a buyer’s emerging criteria, they demonstrate value from the start. Those who embrace these tools consistently show up earlier, better informed, and more confident, qualities that compound quickly and directly influence deal volume.

“Technology doesn’t create deal flow. Brokers create deal flow. Technology’s job is to create the system for consistency,” Matthews says.

“A good tech AI tool never forgets. It turns a chaotic list of contacts into a systematic prospecting machine. It should automatically log calls, schedule the 90-day follow-up, and prompt a broker when a relationship is going cold. Consistent deal flow is the direct result of consistent, disciplined activity. Technology is simply the tool that removes friction and excises from that process.”

One of the biggest challenges for brokers isn’t effort—it’s the sheer volume of tasks and relationships competing for their attention. AI cuts through that noise by simplifying follow-up, organizing outreach, and ensuring that nothing slips through the cracks.

By systematizing these touchpoints, AI supports a steady, predictable pipeline and gives brokers a clear, real-time view of their business. With this clarity, they can prioritize the highest-value activities each day rather than reacting to to urgent tasks.

Ultimately, technology reinforces the habits that top producers already rely on: timely follow-up, consistent outreach, and structured relationship management. When AI handles repetitive administrative work, brokers regain bandwidth to focus on conversations, insights, and client interactions that actually move deals forward.

“This is about the long game. Innovation isn’t about the next shiny object,” Matthews says.

“Every cold call, every agent lunch, every piece of intel my team gathers, that is our data. The innovation I care about is the platform that makes it effortless for Matthews™ agents to capture that data.”

The brokers who consistently outperform are the ones who treat each interaction as part of an ongoing progression: conversations documented, follow-ups tracked, and market signals organized in a way that compounds their understanding of the business. True innovation builds the structure that supports this compounding effect with minimal effort on the broker’s part.

When this information is captured automatically, brokers gain clearer visibility into where relationships stand, which owners are moving closer to a decision point, and where their attention will generate the most momentum. It replaces the uncertainty that once defined slower parts of the cycle with clarity and direction. Patterns become easier to recognize, timing becomes easier to judge, and pipelines become more predictable.

What matters most isn’t the pace of technological change, but the platforms that integrate seamlessly into a broker’s workflow, empowering them to stay organized, make informed decisions quickly, and build long-term leverage through better data. Sustainable deal flow comes from sustainable systems, and innovation is what keeps those systems operating at the speed the market now demands.

This brings it all together.

“Winning with AI means augmenting producers, not replacing them,” Matthews says.

“AI handles the science of brokerage: ‘Who to call,’ ‘When to call,’ ‘What property data to reference.’ This frees brokers to master the art of brokerage: the tonality of the call, the ability to build rapport in 30 seconds, the intuition to navigate an objection meeting.”

He adds:

“The broker who wins with AI is the one who treats it as their personal team, allowing them to increase their volume of high-quality, human-to-human connections.”

AI creates real lift by removing the need to split attention between research and outreach. Brokers start their day with precision, organization, and timing already built in, allowing them to pour their full energy into the conversations and decisions that move deals forward.

Those who excel in this environment use AI to sharpen their instincts rather than replace them. They begin each day with clarity on priorities such as who to call, what to reference, and where to focus, turning that clarity into stronger relationships, more consistent activity, and ultimately more closings.

At its core, brokerage remains a relationship-driven business. AI doesn’t change that. What it changes is a broker’s capacity to show up better prepared, more often, and with deeper insight. When technology removes the noise, brokers have more room for the work clients actually feel: presence, expertise, and human connection.

“ “

GlobeSt.com — the commercial real estate industry’s trusted national brand—delivering essential insights and strategic intelligence across every region and property sector. We offer high-impact visibility for marketers through trusted editorial, nationally recognized events, and dynamic digital platforms. Backed by a legacy of industry leadership, we connect and engage owners, investors, lenders, developers, and brokers with the information and opportunities that drive CRE forward.

Our trusted team of industry experts is dedicated to delivering the key insights, in-depth analysis, and proven best practices essential for commercial real estate owners, investors, developers, brokers, and finance professionals. We’re here to celebrate innovation and success, providing our readers with digestible, actionable information that transforms complex trends into real-world applications—ensuring you stay ahead of the curve.

GlobeSt’s vibrant event portfolio features a mix of local and national forums tailored to tackle the most pressing challenges across sectors like Healthcare, Multifamily, Net Lease, and Women of Influence. Connect, network, and learn from industry leaders in an inspiring environment designed to drive your business forward. Don’t miss out on your chance to navigate the future of commercial real estate with confidence!

Reaching more than 300,000 CRE professionals across all markets, sectors and business disciplines, GlobeSt.’s unique integrated business model allows us to deeply understand the dynamic real estate industry and the evolving needs of our audience. Join our community today!

Following the pandemic, the multifamily sector entered a period of strength driven by a rapid unfreezing of household formation. Vacancy rates plummeted to record lows as demand outpaced available units, fueling double-digit rent growth across many metros. This exceptionally strong fundamental performance sent a clear signal to developers and investors, sparking a massive wave of new development and recordbreaking sales figures. Capital flooded into the sector, initiating the largest construction pipeline seen in decades as the market rushed to meet the insatiable demand for housing.

The momentum shifted as the Federal Reserve began an aggressive series of interest rate hikes to combat inflation. On the demand side, economic uncertainty made renters more price-sensitive and cautious, causing absorption to moderate just as the record levels of new supply began to deliver. This supply-demand mismatch flattened rent growth in many areas, and even turned rent trends negative in the most high-supply markets. Simultaneously, the high cost of capital made financing new projects prohibitively expensive for developers. But now, new construction starts have ground to a halt, likely leading to medium-to-long term undersupply, once the market absorbs the 2024 and 2025 built inventory.

Beyond the operational shifts, rising interest rates caused a dramatic contraction in the capital markets. As borrowing costs surged past cap rates, the math for acquiring properties no longer worked at previous valuations, causing sales activity to fall as owners and sellers couldn’t get on the same page. Owners with existing low-interest debt held onto their assets rather than refinancing or selling into a down market, while buyers retreated due to negative leverage. This created a significant pricing gap between buyers and sellers, resulting in a prolonged period of transaction stagnancy while the market waits for rate stability. But, as we enter 2026, there are a lot of signs pointing to a major rebound for multifamily investment.

Source: Matthews™ Research, CoStar Group, Inc.

While the initial shock of inflation dominated headlines early in the decade, households actually have seen their earnings grow faster than inflation for most of the decade. Average hourly earnings growth continued to outpace inflation, widening the spread that had turned positive two years prior. By mid-2025, nominal wage growth held just below 4% while inflation cooled to the mid-to-high 2% range. This sustained period of real wage growth meant that renters, despite economic fear, have actually strengthened their finances over the last three years.

The average American’s balance sheet remains historically strong. A key metric to watch is the Household Debt Service Ratio, debt payments as a percentage of disposable personal income. Throughout 2025, this ratio hovered near 11.2%, a healthy level significantly below the peaks seen prior to the 2008 financial crisis. This data indicates that renters are not over-leveraged; even with higher interest rates on credit cards and auto loans, the consistent growth in disposable income has kept the monthly burden of debt manageable, preventing the wave of delinquencies that many analysts had incorrectly forecasted.

Source: Matthews™ Research, Federal Reserve

Perhaps the most defining characteristic of 2025 was the massive disconnect between how renters felt and how they actually performed. Consumer sentiment indices remained stubbornly low throughout the year, reflecting deep-seated nervousness about a potential recession. However, the economic pain renters feared largely failed to materialize. Unemployment has remained in the mid-4% range, a level that is considered balanced historically, and consumer spending continued to show surprising durability. Renters prepared for a hurricane that never made landfall, resulting in a dynamic where caution curbed positivity.

In 2026 we expect to see an increase in household formation, largely driven by the continued cutting of interest rates by the Federal Reserve and the impact that will have on the broader economy and labor market. If economic expectations turn positive, renters have the financial firepower to make 2026 a year where multifamily markets tighten significantly.

The primary catalyst for the 2026 outlook is the improvement in the cost of capital. As interest rate cuts work their way through the system, the cost of debt is finally receding, making leveraged returns attractive once again. This shift is expected to trigger heightened buy-side competition as capital that has been on the sidelines moves to deploy before the window of opportunity closes. The influx of bidders will likely halt the expansion of cap rates, causing yields to flatten and potentially compress in high-demand areas. We also expect a return to solid asset appreciation in the multifamily tranche, driven by both improving performance and lower lending rates.

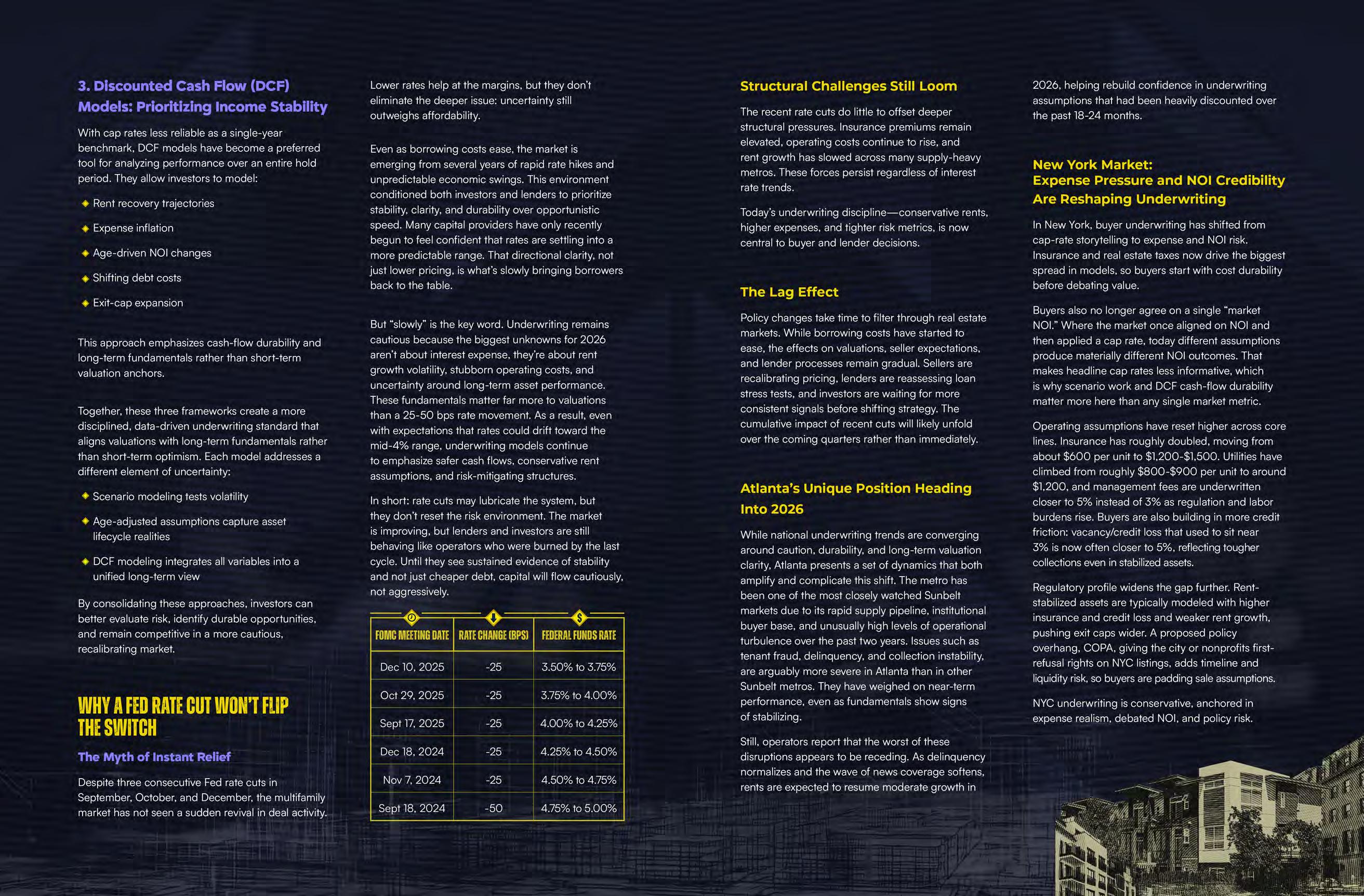

The Federal Reserve forecasted they would cut rates once next year during their December meeting, but media economists are expecting 3 or 4 rate cuts in 2026. We believe the most likely scenario for next year is a 50-basis point reduction to the Federal Funds Rate. It should be noted that due to Powell’s term ending next spring, it is more likely these current Fed projections are too conservative than too aggressive.

The combination of accessible financing and rising asset values is expected to break the investment logjam. We forecast a roughly 10% to 15% jump in transaction volume in 2026 compared to 2025. This increase represents a release of pent-up liquidity from institutional and private investors who have been waiting for the bid-ask spread to close. As confidence in the new valuations solidifies and lenders increase their allocations, the market is expected to transition from a 3-year period of stagnation to a period of more active deal flow.

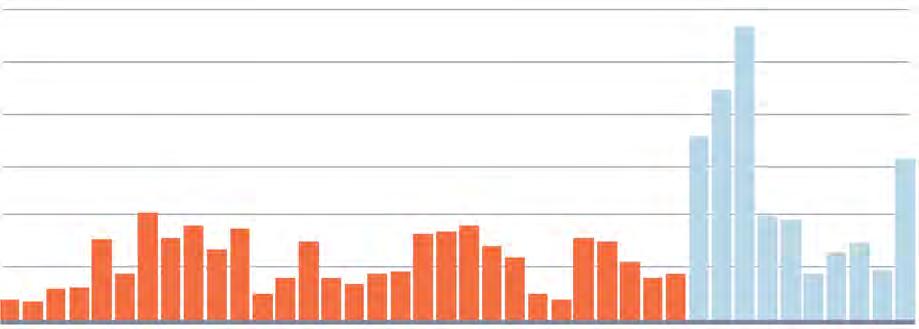

BY DAVID FERBER, CPA

After several cautious years, institutional investors, large, professionally managed funds such as private equity groups, pension funds, and insurance companies, are decisively returning to the multifamily market. In the first quarter of 2025 alone, U.S. multifamily investment totaled $28.8 billion, with institutions representing a substantial portion of that volume. Momentum accelerated through mid-year and into the fall, with apartment sales rising 13% year-overyear in the third quarter to $43.8 billion. Together, these figures underscore a renewed confidence in multifamily fundamentals and the broader capital markets.

Source: RCA

$50B

$40B

$30B $20B

$10B

$0

Evidence of this institutional re-engagement is already visible across the public REIT landscape, where capital deployment has meaningfully increased. AvalonBay Communities (AVB) has completed $618.5 million in year-to-date acquisitions, including the purchase of six Dallas-Fort Worth communities totaling 1,844 units for $431.5 million, a clear signal that major operators are once again pursuing scale in high-growth markets.

Similarly, Equity Residential (EQR) executed one of the largest multifamily trades of 2025, acquiring a stabilized Atlanta portfolio of 2,064 units for approximately $533.8 million at a 5.1% acquisition cap rate. The move marks the company’s strategic re-entry into key Sunbelt markets and aligns with its thesis that fundamentals in select growth metros are strengthening.

These transactions validate what private-market investors are beginning to experience in real time: capital is flowing back into multifamily,

Institutional capital doesn’t just participate in the market, it helps define it. These investors establish pricing benchmarks, influence underwriting standards, and restore liquidity when they reengage. As large funds return, their activity helps narrow bid-ask spreads, reprice assets more accurately, and reignite stalled deal flow.

They also serve as early indicators of sentiment. When institutions retreat, it often precedes a broader slowdown. When they return, it signals that investors once again see an opportunity worth pursuing. For 2026, this renewed participation suggests that the worst of the correction may be behind the multifamily sector.

Institutional activity effectively sets the tone for the entire industry. Their re-entry signals that confidence is rebuilding and valuations are stabilizing. As more funds re-engage, competition for quality assets will likely increase, gradually pushing prices upward,

Between 2022 and 2024, rising interest rates and tightening credit made financing more expensive and constrained deal flow. Sellers held out for 2021-level pricing, while buyers needed discounts to offset higher borrowing costs. Economic uncertainty, slower rent growth, and rising construction expenses compounded hesitation on both sides. Multifamily transaction volume declined more than 50% from 2021 to 2023, then began rebounding in 2024 as pricing reset.

Source: Forbes

Transaction volumes fell sharply as many funds shifted from acquisitions to asset management. Some firms focused on operational improvements, while others simplified their portfolios, selling topperforming properties to raise liquidity. For a time, sitting on the sidelines felt safer than overpaying in an unpredictable market.

That caution began to ease as prices reset and underwriting discipline took hold. Property values adjusted to more sustainable levels, rent growth stabilized, and buyer competition thinned, giving patient, well-capitalized investors a clear window to re-enter. Today, institutions are positioning for long-term ownership, emphasizing stability over speculation.

The map of institutional investment in 2025 looks more balanced than in previous cycles.

Sunbelt and Growth Markets: Metros such as Dallas, Atlanta, Tampa, and Nashville continue to draw attention for their job and population growth. However, investors are far more selective than in past years, steering clear of submarkets facing oversupply or softening rent trends. Several of the sector’s strongest performers are signaling improving fundamentals, with UDR’s CEO noting that “third-quarter operational results… exceeded our expectations and drove our second FFOA per share guidance raise of 2025.” This growing confidence reinforces why capital continues to gravitate toward markets where performance momentum is beginning to firm.

Secondary and Midwest Markets: Secondary metros including Kansas City, Columbus, and Raleigh are gaining traction for their relative affordability and resilient fundamentals. In the Midwest, places like Indianapolis, Minneapolis, and Omaha, stable performance, limited new supply, and strong occupancy are reinforcing investor confidence.

Coastal Gateways: Some institutions are cautiously returning to traditional gateway markets such as New York, Northern New Jersey, and Boston, but mainly for core, stabilized assets where pricing has reset and cash flow is durable. What’s notable about

Sunbelt

Secondary and Midwest Markets

Coastal

this cycle is how targeted that re-entry has become within the gateway universe. The PwC/ULI Emerging Trends 2026 rankings place the broader NYC ecosystem among the most institutionally favored areas in the country, with Jersey City emerging as a top national market to watch (ranked #2 overall) and Northern New Jersey also landing in the leading tier of U.S. markets. For multifamily, the survey sentiment skews positive toward apartment acquisitions in North Jersey, reinforcing that institutions see the North Jersey/Jersey City corridor as a neargateway location where renter demand, commuter connectivity, and long-term liquidity still justify fresh allocations.

Sales Volume ($M)

Source: RCA

Newer, high-quality properties in prime locations remain the cornerstone of institutional portfolios. Typically built within the last five years and supported by strong employment and income demographics, these assets offer consistent cash flow and low operational risk. Institutions value these assets for their predictability and inflation resilience, often using them as portfolio anchors. For example, a newly delivered high-rise in a prime urban employment corridor, featuring rooftop amenities, coworking suites, and EV-charging stations, can maintain exceptionally high occupancy and command premium rents due to strong demographic fundamentals.

Class B assets have become strategic targets for value creation. Pricing for this segment has corrected more sharply than for newer assets, allowing institutions to drive returns through operational execution rather than market timing. The focus is on steady repositioning over several years, moderate rent growth through modernization while maintaining affordability relative to new construction.

Properties serving middle-income renters continue to attract institutional attention. Undersupply in this segment and limited new construction make it one of the most resilient asset classes. These investments align with ESG priorities while offering consistent performance across cycles. Recent REIT activity in Q3 2025 underscores the trend, with several public funds increasing exposure to workforce housing due to strong occupancy and dependable rent collections.

In 2026, institutions are closely tracking interest rates, rent growth, employment trends, and new construction activity. With greater stability emerging across these indicators, the year is shaping up to be the next phase of capital deployment, defined by selective acquisitions, creative financing, and disciplined, fundamentals-driven expansion.

The overarching message remains clear: institutional investors are not pursuing quick wins. They are building portfolios engineered for resilience, emphasizing stable income and long-term value creation. Their renewed engagement reinforces a lasting truth, multifamily continues to be one of the most reliable asset classes in commercial real estate. Investment strategies are being anchored in fundamentals that outlast cyclical volatility. Markets with expanding job bases, steady population inflows, and limited new supply are capturing the most attention.

Institutions are also focused on durability, assembling portfolios that perform through full cycles rather than just during upswings. This requires prioritizing cash-flow consistency, maintaining prudent leverage, and emphasizing operational excellence. The mindset for 2026 is deliberate and measured: grow steadily, manage risk thoughtfully, and avoid the excesses that characterized the last expansion.

In a rare bipartisan move, Congress has permanently extended the New Markets Tax Credit (NMTC) program, one of the most effective yet underutilized tools in commercial real estate. For developers and investors focused on redevelopment, adaptive reuse, and community-oriented projects, this is a milestone moment. Here’s a breakdown on why it matters.

Created under the Community Renewal Tax Relief Act of 2000, the NMTC program is a federal incentive designed to attract private capital into low-income and underserved communities.

Administered by the U.S. Department of Treasury’s Community Development Financial Institutions (CDFI) Fund, the program allows private investors to receive federal tax credit for equity investments made through Community Development Entities (CDEs). In turn, these CDEs deploy that capital into qualified projects that stimulate job creation, local business growth, and neighborhood revitalization.

Since its inception, NMTC has spurred over $120 billion in investments nationwide. The program supports developments ranging from retail and healthcare facilities to industrial, educational, and mixed-use projects that might not otherwise secure conventional financing.

It was previously renewed every few years, and the NMTC’s future was often uncertain, discouraging long-term planning. The new permanent status eliminates that policy risk and transforms it into a stable, strategic financing mechanism for projects.

At the heart of the NMTC ecosystem are CDFIs or CDEs, mission-driven financial institutions that specialize in serving low-income or underserved communities. These entities include community development banks, credit unions, loan funds, and venture capital funds certified by the U.S. Treasury.

Through the CDFI Fund, developers and investors qualify for federal support such as grants, technical assistance, and tax credits, enabling them to structure below-market financing. For investors, aligning with a CDFI means access to long-term capital that blends impact with profit potential. Unlike the past, when NMTC renewals required periodic congressional approval and created uncertainty, this permanence removes policy risk and opens the door for long-term planning.

The NMTC provides investors with a 39% federal tax credit on their qualified investment, claimed over seven years–5% annually for the first three years, and 6% for the next four.

In practice, this credit serves as “soft equity,” filling funding gaps, lowering sponsor equity requirements, and improving project viability in markets where rents or redevelopment economics might otherwise fall short. Overall, it generates meaningful tax savings for investors.

Feature New Markets Tax Credit (NMTC)

Purpose

Investor Benefit

Capital Flow

Primary Motivation

Ideal Project Types

Geographic Scope

Time Horizon

Stimulate community development through subsidized financing to projects in low-income communities that cannot attract traditional capital

39% federal tax credit over 7 years (offsets income tax)

Investments made through certified Community Development Entities (CDEs)

Impact-driven: Focus on community development, job creation, and local revitalization

Retail redevelopments, healthcare facilities, industrial/mixed-use, schools

Low-income census tracts (often overlapping with OZs)

7-year compliance period

Program Status Permanent

Opportunity Zones (OZ)

Encourage long-term private investment through capital gains tax incentives

Deferral of existing capital gains; potential elimination after 10-year hold

Direct equity investments through Qualified Opportunity Funds (QOFs)

Profit-driven: Focus on capital appreciation and long-term gain exclusion

Multifamily, commercial, and mixed-use developments with strong appreciation potential

Federally designed Opportunity Zones

10-year investment hold for full tax exclusion

Authorized through 2028

Layering NMTC and OZ capital creates a hybrid structure that delivers both social and financial returns. NMTC funding lowers equity needs and boosts project feasibility, while OZ equity enhances long-term investor upside. Together, they enable projects that might not otherwise “pencil” while amplifying community impact.

Consider a small business expanding into a low-income opportunity zone. By combining NMTC financing with Opportunity Zone (OZ) incentives, the owner can craft a highly efficient capital stack:

1 2

CDFI/NMTC

A $1 million NMTC investment generates $390,000 in federal tax credits.

An outside investor contributes equity using deferred capital gains, potentially eliminating those taxes entirely after a 10-year hold.

3

The remainder is covered by bank debt and a modest owner contribution.

The result? A fully financed redevelopment that supports job creation, community growth, and strong investor returns–all while revitalizing an underserved corridor.

• The project must be located in a federally designated low-income census tract

• Ideal for projects generating jobs, services, or essential infrastructure

Submit applications to CDEs /CDFIs with allocation authority. Evaluation focuses on community impact, feasibility, and sponsor experience.

Combine NMTC equity with:

• Senior debt

• Sponsor equity

• CFI/NMTC funding

• State or local incentives

NMTC investors (often large banks or insurers) purchase the credits for equity, and the CDE manages compliance throughout the seven-year credit period.

Pro Tip

Start conversations early. CDEs allocate on a mission-alignment basis, and once annual allocations are spoken for, opportunities vanish quickly.

The permanent extension of the NMTC reshapes the investment landscape for community redevelopment. When paired with Opportunity Zone incentives, it creates an exceptionally powerful, tax-efficient capital stack that aligns financial return with measurable social impact.

For CRE investors and developers, this is a rare alignment of profitability and purpose, an opportunity hiding in plain sight.

Lleyton Buscher

lleyton.buscher@matthews.com (919) 750-3309

Jake Lurie

jake.lurie@matthews.com (813) 488-0853

By Geoffrey Arrobio

Let’s start at the top with a quote from the U.S. Department of Energy Secretary Chris Wright:

As the saying goes, “follow the money.” The data center sector, including its entire infrastructure, is said to be on track for approximately $7 trillion of capital investment by 2030, as reported by McKinsey & Company Global Management, with an estimated $500 billion for 2026 alone.

Most, if not all, of “big tech” is invested or investing in this space (Apple, Microsoft, Oracle, Alphabet, Meta, and the list goes on). It’s a tremendous amount of capital, and this administration is doing everything in its power to “win the race” over China, India, and others to secure its buildout and end-product.

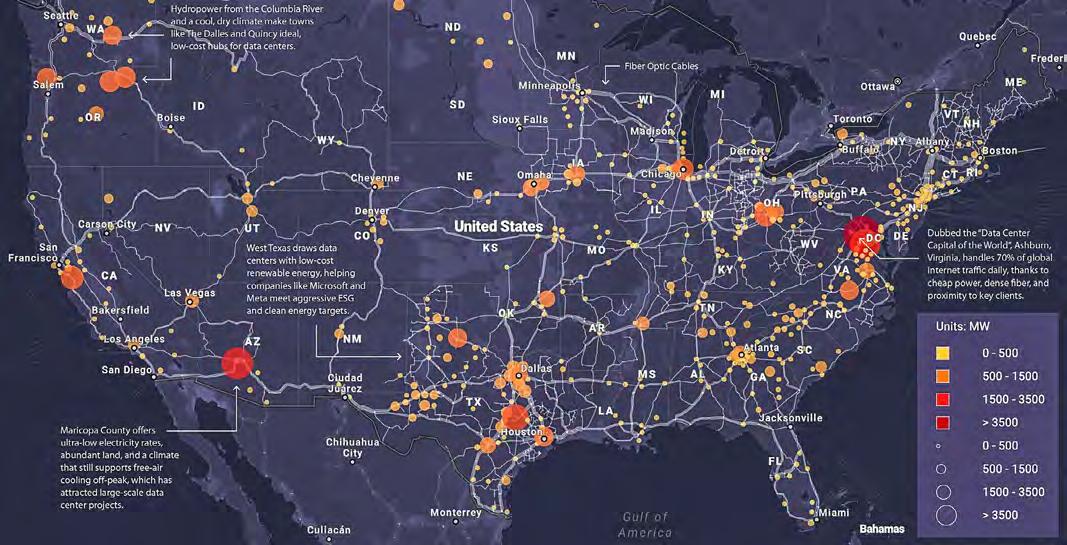

The question becomes which states and submarkets will benefit from these buildouts? The answers may be surprising.

Virginia, Texas, and Georgia are currently in the lead. However, the Pacific Northwest, Arizona, Nevada, and even Kansas City, MO, are hot on the heels of the initial three states.

Kansas City, MO, is in the planning stages of a $100 billion project near the Kansas City Airport. Even Google is getting into the game in eastern Iowa by

petitioning to reopen and recommission the Duane Arnold nuclear reactor, located in Fayette Township, Linn County, and using the surrounding area for an AI data center.

The reasons as to “why” these states are being chosen can be explained rather simply: cheap land, affordable electricity, and in place pro-growth development policies which can streamline the buildout process (unlike the California permitting process, for example). The electrical components of these centers are extremely important, as is the location. Not only do these centers use massive amounts of power, but they also require constant cooling, which in turn drains significant amounts of power, taking grid power away from the surrounding area. There are different ways to solve the electrical issue.

With the estimated $7 trillion of investment capital over the next five years, investors should follow these buildouts for opportunities in retail, hospitality, industrial, medical office, and multifamily sectors. These centers are run by people (and Nvidia CPUs) and will need support services and housing availability within the surrounding campuses for the foreseeable future. Note that both AMD and Qualcomm are also targeting this space.

Data Center Demand Capacity by County

(Source: visualcapitalist: Mapped: The Massive Network Powering U.S. Data Centers

Unfortunately, not everyone will be a winner in this game. Many critics argue that the evolution of AI will lead to massive job losses, degrade human critical thinking, and result in a monopolistic enterprise. However, as witnessed with the Dot.com bubble in 2000, similar issues will occur in this sector—not everyone can be a winner.

Dramatic strides in the digitization of everything going forward are on the horizon. The journey won’t be smooth, but the long-term net future positive outweighs the short- to medium-term negatives, including the “misallocation of capital” for some companies. With new plans announced every week for a new datacenter somewhere in the U.S., it’s prudent for investors to focus on where the momentum is heading.

For example, “Data center developer Crusoe has struck a deal with US Blue Energy to secure power of up to 1.5 GW for a nuclear-powered AI Campus located at Port of Victoria, Texas, expecting its first delivery of nuclear power electricity by 2031.”

The biggest driver of not only data centers/AI, but also economic well-being, is access to affordable energy. Data centers require non-intermittent power, as the flow of electricity must be static 24/7, to ensure accurate data processing. Wind and solar cannot offer 24/7 baseload power, forcing companies and municipalities to supplement their energy sources with nuclear power and natural gas turbine providers to provide continuous, 24/7 power.

As Goldman Sachs stated, we are now in the “Terawatt Era”. To put nuclear energy density into context, nuclear fission is a very high-density power source. 1 uranium fuel pellet, the size of a fingernail, creates as much fission energy as 17,000 cubic feet of natural gas, 120 gallons of oil, and 1 ton of coal. In addition, nuclear reactors (big or small) have a significantly smaller land footprint compared to wind and solar energy sources and can last for up to 100 years. As nuclear and natural gas expand to support data centers, surrounding areas may see renewed investment in industrial and infrastructure assets.

The U.S. and most of the industrialized nations (aside from Germany) are all on the precipice of major nuclear energy buildouts. Not just for data center demand, but also to meet current demand (pre data center development).

China alone is building 10 to 12 major nuclear plants per year, while the U.S. has only built two major nuclear reactors over the past 30 years (Vogtle 3 & 4, located in Georgia in 2023, with AP 1000 units - Westinghouse/Cameco). The U.S. is trailing China for carbon-free, clean baseload nuclear energy; however, as of October 28, 2025, that has changed. The United States Government, Cameco, and Brookfield Asset Management have announced at least $80 billion investment for the building of new large reactors across the U.S. (AP1000 units). These new buildouts will help create new high-paying jobs and energy security. Small Modular Reactors (SMRs) will also be added to the energy mix, providing “bolt-on” clean electric power and heat for hospitals, manufacturing plants, and in some instances replacing coal-fired plants. This technology is in its infancy; however, Terra Power (Bill Gates), NuScale, BWXT, X-Energy, Rolls-Royce, and others are nearing the testing of their SMR prototypes for mass manufacturing within the next three to five years.

Many other primary and secondary industrial countries, including Saudi Arabia, Poland, Sweden, the United Kingdom, and India, have plans or are expanding their nuclear power portfolios. As noted above, the German Green Party has dismantled Germany’s industrial base over the past five years by closing its fully functional nuclear power plants to focus on wind and solar energy. That mistake has led to the drastic decrease in industrial production within

Upstream covers finding, developing, and mining uranium deposits. These companies secure land, run the mines, and provide the raw materials.

Mining & Development Exploration

The U.S. government sees the best return in upstream companies, since mining is the least lucrative stage of the supply chain.

Midstream companies convert and enrich uranium, turning raw ore into reactor-ready fuels like UF₆ and HALEU.

Midstream has three segments, but the most actively traded stocks are in enrichment and isotopes.

Enrichment/ HALEU

Isotope Separation

Royalty and trust companies offer leveraged exposure to uranium prices, earning passive income from production or stored material without owning or running mines.

(Source: TannersTrades)

Downstream companies build and run nuclear plants, turning enriched uranium into steady baseload power.

SMRs/ Next Gen Equipment/ Components

Utilities/ Power Gen

Utilities use enriched uranium in their nuclear portfolios, with some relying on it more than others. Duke uses some of GLE’s laser-enriched uranium.

Next Gen tech refers to Silex and GLE, which enriches uranium using laser technology. Next Gen Tech Support

Germany and the European Union. There is ongoing discussion of reversing these “green policies” and turning the fully functional units back on, as the German economy is the largest GDP producer within the EU. It remains to be seen whether policies in Germany will shift toward re-endorsing nuclear power generation and lowering the cost of electricity for their industrial base.

The takeaway is that all forms of affordable and reliable energy are needed to help manufacturing bases remain competitive (keeping costs low) and to support daily life. Real estate investors will have the opportunity to strategically invest within these demand-driven areas of new buildouts. Data centers and reactors (both large and small) will employ hundreds, if not thousands, of people.

The support category includes spent-fuel storage, engineering, construction, components, and turbine and grid systems.

And if the U.S. can lower the cost of BTUs for everyone, we can maintain a competitive edge globally.

Above is a visual of the nuclear ecosystem. While not shown in its entirety, it provides a visual explanation of how this space works, from fuel exploration and enrichment to fabrication, and ultimately to the end users. As seen below, the cycle is more complex than oil and gas energy producers yet follow a similar path. It’s important to understand that about 90% of the current nuclear fleet in the U.S. receives its fabricated nuclear fuel from Russia, as we have outsourced everything over the past 30 years. Now that the government has banned imports from Russia, Energy Secretary Wright, with the help of the NEC, is pushing forward the regulatory framework to “onshore” the entire fuel cycle.

In the 1960s and 1970s, the U.S. was the largest nuclear fuel fabricator worldwide; that expertise was relinquished years ago (as hydrocarbons were cheaper to extract) and is now being rebuilt in response to rising energy demand. That in itself is a very challenging mission. Yet, it is taking place throughout the U.S. States like Texas, Utah, Idaho, and Wyoming are now at the forefront of these efforts, not only for uranium discovery and extraction, but also for fabrication and enrichment. These ecosystems need support systems, and therein lies future commercial real estate opportunities.

To address the concern about “nuclear waste,” or “tails” as it is known in the industry (spent fuel).

1. SMRs are very efficient and can run at decreased power levels at the same time, meaning the spent fuel or tails are negligible.

2. Larger reactors like the AP 1000 consume millions of pounds of uranium via fabricated fuel, and there also remains a very large stockpile of spent fuel/tails within the U.S. However, with Quantum Laser Technology (QLE) or ASPI Isotopes and Silex, these stored waste stockpiles can be re-enriched into working fuel stockpiles, drastically decreasing the storage capacity for waste.

One material poised to disrupt the marketplace over the next 5 to 10 years, and will actually improve everything it encounters, including commercial real estate, is pure SP2 bonded 100% crystalline graphene.

Graphene has been known for some time; however, until recently, graphene has been made from graphite, which does not provide the properties that true SP2-bonded graphene provides. Pure graphene, and in this case made by Hydrograph Clean Power, is 99.8% pure crystalline graphene.

What does that mean and why is this important?

Well, this crystalline pure graphene material (not derived via graphite), but from a proprietary

combustion process using acetylene, will be transformative for a host of industries. This material can improve material tension strength when applied or mixed by a function of “X”. In addition, this material is electrically conductive due to its pristine lattice composition and thin layering.

Staying within the commercial real estate sector, what advantages can this material improve? When added to cement, this material can increase compressive strength by 10% to 40% and its tensile strength by 50%. The cement material is reported to have 4X reduction in water permeability. This enhanced durability will dramatically extend the lifespan of infrastructures, thereby providing longterm cost reductions associated with maintenance, repair, and replacement.

By adding graphene to wood materials, it will drastically increase its tension strength and fire life safety characteristics. These material enhancements, once adopted, should drastically lower insurance premium costs, as these materials can withstand a much higher degree of wear and tear, including heat, pest invasion, water damage (such as mold) and in some cases, natural disasters. Other ways this material can be applied include solar panels, roofing materials, flooring, asphalt, and battery nodes, which can increase longevity and conductivity.

Not only will graphene be used in most building materials (paints, solvents, rubber, plastics, wood, cement, etc.,) it will also greatly enhance battery storage, medical monitoring, food storage (containers), nuclear power plants, automobiles, clothing, and almost everything we touch. Imagine if you didn’t have to replace your oil every 5,000 miles or tires every 40,000?

• When added to plastics, this material will enhance the service life of plastic by 8x (think industrial users).

• When added to lubricants, there is an 80% decrease in mechanical wear and reduced friction. Pure graphene can be added to computer chips, drastically lowering heat transference and increasing CPU speeds, think quantum computing.

When added to electrodes, battery life increases by 47%, increasing efficiency, performance, and storage. The application spectrum for this material is endless, let alone what the U.S. Department of War can use it for:

• Aircraft surfaces and structure

• Submarines

• Body armor

• Radar

• Electronics

• Missile systems

ELECTRON MOBILITY

As high as 200,000 cm²/V·s, much higher than silicon.

THINNESS

A single layer of graphene is just 0.345 nm.

TRANSPARENT

Single-layer graphene transmits approximately 97.2% of light.

UV RESISTANCE

Blocks harmful UV rays by up to 70%.

HIGH SURFACE AREA

As much as 2,630 m²/g – very high surface area.

ELECTRICAL RESISTANCE

Graphene electrical resistivity of just 0.2 × 10 - ⁶ Ω·cm.

STIFFNESS

Young’s modulus 0.95 to 1.1 TPa, some of the highest ever measured.

THERMAL CONDUCTIVITY

Highest ever measured at ~4000 W/m·K.

FLEXIBILITY

Graphene can stretch up to 25% of its original length.

IMPERMEABILITY

Blocks all other elements, even hydrogen.

STRENGTH

Graphene has a strength of 130 GPa, higher than steel.

There are many exciting advances taking place that are merging technology, materials, energy, and commercial real estate to advance efficiency, prosperity, safety, and competitiveness. The next five years will be an exciting period of time as these sectors all merge to play a bigger part within the U.S. economic landscape. As always, do your own due diligence and keep informed as much as possible as these trends and themes unfold. There are many exciting opportunities out there for those who like to dig in and be in the know.

Coffee shops have emerged as a “third place,” neither home nor work, where customers have the option to grab a drink, or use the location to relax, work, and enjoy their free time.

Recent National Coffee Association data shows that in 2025, 66% of American adults drink coffee daily, and consume an average of three cups per day. Specialty coffee consumption has reached a 14-year high, with 46% of American adults having specialty coffee in the past day, surpassing traditional coffee consumption.

As demand for premium coffee experiences intensified, national and regional operators are finding room to thrive, even in saturated markets already dominated by major chains, like California. Coffee tenants continue to expand rapidly across the state, with Southern California noting increased developments from coffee retailers. These tenants are actively seeking spaces that range from 1,000 to 4,000 square feet, attracting national brands and local operators.

For shopping center landlords, securing a quality coffee tenant can increase traffic and enhance the value of their center. Demographics and location are top priorities for coffee tenants with signalized intersections, strong car counts, and pedestrian inflows being factors that improve a coffee shop’s success. Outparcels or pads remain highly desirable, offering convenience and visibility. Drive-thru locations, end caps, and even select inline spaces are increasingly in demand as operators look to capture center traffic and attract more consumers.

While shopping pads and drive-thru locations are favorable, mixed-use spaces also prove beneficial for coffee shops. The ground-floor component creates vibrant street-level activity, and the mix with office and/or multifamily guarantees demand. For coffee shop operators, securing space within a mixed-

use property allows for access to residents, office workers, and everyday consumers, guaranteeing built-in customers and traffic upon opening.

Footprint sizes for coffee shops across the region vary widely depending on format. Small kiosk/drive-thru concepts note locations under 1,000 square feet, while freestanding locations can reach up to 4,000 square feet.

Starbucks, in particular, leads national coffee tenants with the most locations in California. The coffee giant has a strong focus on Southern California, with 155 locations in Los Angeles, 131 stores in San Diego, and over 100 across Orange County. In order to maintain its positive performance in the region, Starbucks has begun new initiatives across its stores, including renovating locations to align with the Back to Starbucks plan. CEO Brian Niccol launched the initiative in September 2024 to bring more customers back to stores across the country. New features of the plan include lounge seating, warmer lighting, and reintroducing ceramic mugs for in-store orders. The goal of this plan is to create a community feel within their locations. A new site with these features has already opened in Los Angeles at the intersection of Sunset and Palisades Village.

Source: Placer.AI, January 2019-October 2025

Dutch Bros has become one of the fastestgrowing national coffee chains across Southern California. The tenant first began operations in 2022 when it opened a location in San Diego County. Since then, it has spread to cities like Barstow, Apple Valley, Victorville, Baldwin Park, and Palmdale. Dutch Bros is planning its move in the Los Angeles metro, with a store under construction near the University of Southern California campus. The location will be similar to its other stores featuring a walk-up window, and it is expected for completion by year-end 2025. Other new sites for Dutch Bros across Southern California include Carson and Temecula, with both shops already approved for construction.

Source: Placer.AI

Regional coffee shops attract consumers seeking high-quality products, with goods like specialty beverages or artisan-roasted beans. Younger consumers, like Gen Z, often drive visits as they are willing to pay more for premium, trending goods. These locations offer a unique setting that reflects the local population, attracting consumers that seek an authentic and community-focused experience. While national operators offer a convenient visit, regional operators create competition by prioritizing quality, community, and exclusive experiences.

California is home to the greatest number of coffee shops across the country, with local tenants playing a significant role in the state’s coffee performance. Regional coffee tenants most often lease 800- to 1,500-square-foot spaces with in-line or end-cap formats, as seen with regional operator Better Buzz. The coffee chain, which started as a coffee cart in San Diego, has become a staple in Southern California. Most of its locations are found in San Diego and Orange County, reaching as north as Fullerton. Upon its success in Southern California, the company has also expanded to Nevada and Arizona, with its first out-of-state store located in Phoenix. Better Buzz has around 40 locations across the three states, and it plans to double its size in the next few years.

Regional tenants that feature Vietnamese coffee are also aiding coffee shop activity. The nation’s coffee began to grow internationally in the 1990s when it became one of the world’s largest coffee producers. Since then, it has maintained its popularity for creating a unique coffee culture for consumers in the Southern California market. Trung Nguyen Legend Café, originally from Vietnam, began U.S. operations in 2023 with its Westminster location. The company is still growing across Southern California, with Matthews™ recently securing a 2,700-square-foot space for them in Huntington Beach. The coffee shop sought this location because of the end cap, visibility, patio and large seating area, as well as the community impact.

Source: ScrapeHero

Blk Dot Coffee has also expanded the presence of Vietnamese coffee in Southern California. The company is a family-run business with a focus on providing traditional Vietnamese coffee, as well as some food items. Its first location opened at the Orange County Google offices in 2015, and has had a strong presence across the county ever since. Locations range from areas like Irvine, Newport Coast, Fountain Valley, and Long Beach, with many of its stores placed in shopping centers to take advantage of high foot traffic levels.

Tierra Mia Coffee opened its first location in 2008, and has since expanded its reach to both Los Angeles and Orange counties. Known for roasting its coffee and baking their pastries in store, as well as serving Latin specialty drinks and unique latte art, the company has now grown to 20 stores.

The national coffee market is projected for continued growth as consumers seek coffee shops for a third place experience. The U.S. coffee market size was estimated at $47.8 billion in 2024, and is forecast to grow at a CAGR of 9.5% to 2030. By providing free Wi-Fi, coffee shops continue to attract work-from-home employees, as well as create an environment for other consumers to relax and socialize.

Further growth across the sector will be aided by consumers seeking more unique flavors and highquality products. This movement is advantageous for local operators as they can adjust menus to provide enticing options not found at national brands. To stay competitive, national tenants are prioritizing loyalty programs and drivethru convenience, while local tenants leverage community connection and handcrafted goods to maintain performance levels.

Matthews™ Capital Markets (MCM) is a fully integrated and dedicated financing division of Matthews™, providing capital solutions ranging from $500,000 to $100 million for all property types across the U.S. Through long-standing lender relationships, we have the ability to customize and structure financing solutions that best suit our clients’ needs.

From Funding to Close, Matthews™ Provides a One-Stop Shop

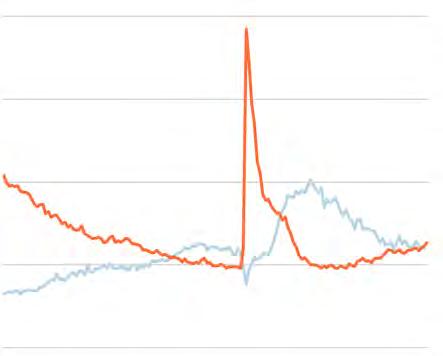

Higher interest rates. Rent caps that limit increases. Rising insurance premiums. These forces aren’t just background noise in today’s multifamily market—they suggest that markets are once again factoring risk back into pricing. Valuations now hinge on the volatility of a property’s underlying cost structure and its flexibility to grow revenue. Before COVID, pricing followed a predictable hierarchy, as cheap financing and aggressive rent growth pushed values higher. In turn, cap rate spreads compressed, reducing price dispersion across quality tiers.

Today, that pricing logic has eroded into a renewed focus on risk-based pricing and wider dispersion amongst asset classes and location fundamentals. Cap rates have held firm amid higher expenses, regulatory limits, and more disciplined rent-growth assumptions. CoStar Group Inc.’s forecast projects modest movement with cap rates stabilizing at 6% through 2026, signaling that the valuation reset is being priced into fundamentals rather than a quick return to cheap debt. Cap rates remain tiered by asset quality, with Class A and B assets clustering in the low-to-mid 5% range while Class C properties often price around 6%.

The recalibration of valuations between 2023 and 2026 centralizes on the disruption of NOI. Insurance instability, above-yield borrowing costs, and stringent rent control each distinctly strain income performance, widening the bandwidth of operating outcomes investors must price, and pushing cap rate dispersion across asset quality and markets.

Insurance costs have become a defining variable. Premiums rose about 28% year-over-year as of early 2024, according to Yardi Matrix’s national multifamily expense data, which showed a cumulative increase of 129% since 2018. Premiums remain structurally elevated relative to pre-pandemic levels, with projections tapering to 3-6% through 2026.

As multifamily insurance premiums increasingly outpaced total operating expenses, average insurance costs climbed from about $278 to $636 per unit, materially eroding NOI.

In many portfolios, Yardi Matrix’s data shows these insurance-driven increases have pushed operating expenses up roughly 30-40% above pre-pandemic levels, tightening NOI margins and expanding the “pricing band” investors require, especially for older Class C assets in disaster-exposed markets where volatility is highest.

Wider borrowing spreads have translated into more conservative pricing, often requiring greater yield cushion and/or price adjustment, and cap rates have been slow to compress as investors prioritize cash-flow certainty over rate-cut expectations.

Even with continued rate cuts expected by late 2026, pricing remains anchored to property-level risk and NOI sustainability under higher borrowing costs. As a result, negative-leverage deals should continue to fade throughout 2026, with investors demanding durable yield.

Myth: Value-add pricing will normalize once rates fall.

Reality: The value-add spread is being driven less by rates and more by execution uncertainty, including higher all-in improvement costs and less reliable rentpremium capture.

Historical and Forecast Average U.S. Multifamily Cap Rates

Pricing Impact: Investors are assigning a larger risk premium to transitional business plans, keeping value-add yields wider and basis expectations tighter.

Between 2021 and 2026, the national average cap rate is projected to move from a low of 4.90% to a stabilized 6.00%. This shift in fundamentals is driven by a transition to more conservative underwriting, with the $237,000 average price per unit in 2026 reflecting a 1.10% annual rent growth assumption, compared with the more aggressive 9.00% growth seen at the 2021 market peak.

Rent regulation introduces a structural mismatch between rising operating costs and capped revenue growth. Hard rent ceilings prevent owners from adjusting income to keep pace with inflation, tax increases, or insurance expenses, creating a predictable drag on scalable cash flow. Concurrently, rent-controlled properties typically trade at liquidity and pricing discounts, reflecting the regulatory risk embedded in their operating profiles.

Even modest rent resets allow owners to absorb cost pressures better, giving these properties a measurable pricing premium in today’s environment. The divide between regulated and unregulated income streams has become one of the most persistent valuation gaps between 2023 and 2026.

Revenue flexibility has become a central factor in valuation. Market-rate assets can adjust rents to absorb higher taxes, insurance, and operating costs, preserving NOI stability and attracting tighter yields.

Rent-controlled properties, by contrast, face capped income growth while expenses continue to climb, creating a structural drag on long-term performance. Trepp Research shows that multifamily property values declined roughly 30% in New York City following HSTPA and that rent-controlled assets in Los Angeles and the San Francisco Bay Area trade at discounts to unrestricted peers, with Bay Area tenants staying up to 20% longer—slowing rent resets and revenue growth. Investors price these constraints with wider yields, lower liquidity, and deeper discounts.

In 2026, investors continue to price this constraint through wider yields, lower liquidity, and deeper discounts.

Rent-Regulated vs. Market-Rate

Source: CoStar Group, Inc. | Q4‘ 25

Cap Rate: 6.4%

Sale Price / Unit: $171,927

Positioning: Trades at wider yields and discounted pricing due to regulated rent growth

Cap Rate: 6.1%

Sale Price / Unit: $233,197

Positioning: Higher pricing supported by rent-reset flexibility and deeper liquidity

Rent-regulated multifamily trades at a 30 bps higher cap rate, which translates into 26% lower pricing per unit. The higher required yield compensates for restricted rent growth and limited rent reset flexibility, which constrain NOI upside and make it harder to absorb rising operating costs.

Rent-regulated multifamily continues to trade at a meaningful valuation discount relative to market-rate assets nationally.

Uniform pricing spreads have come and gone, and the market has returned to a tiered pricing structure. Investors are particularly meticulous, assigning substantial differences between asset quality, revenue flexibility, and geographic resilience.

Pricing differences between Class A and Class C assets are contingent on the stability of the property type. Class A properties tend to show more predictable NOI, lower operating expense volatility, and modern building systems that reduce unexpected capital needs. That stability supports tighter pricing and more consistent liquidity.

At the opposite end of the spectrum, Class C assets are often characterized by aging infrastructure, longer repair cycles, elevated insurance exposure, and higher turnover rates, all of which introduce greater execution risk and greater performance variability. Investors now incorporate a broader risk premium in pricing.

In 2026, investors continue to price this constraint through wider yields, lower liquidity, and deeper discounts.

Myth: Class A and Class C spreads will tighten back to pandemic levels.

Reality: Risk differentiation was temporarily muted between 2022 and 2024, when debt was cheap and aggressive growth assumptions compressed spreads across quality tiers. As that anomaly fades and the hierarchy of asset classes returns, RCA reports that the spread between Class A and Class C now ranges from 150 to 200 basis points, restoring a risk hierarchy more in line with historical norms.

Pricing Impact: Spreads are likely to remain wider as long as operating costs and revenue outcomes remain volatile, particularly in Class C, where aging systems, insurance sensitivity, turnover, and capital expenditures introduce greater variability.

Myth: Stabilized assets are insulated from volatility.

Reality: Even Class A properties can see NOI pressure when rent growth stalls and operating costs move higher, limiting nearterm upside versus value-add execution.

Pricing Impact: Investors increasingly underwrite wider going-in yield cushions for stabilized deals when expense uncertainty rises, widening dispersion versus assets with clearer NOI growth pathways.

The widening gap between asking and effective rents, particularly as quality declines, underscores how concessions and price sensitivity are shaping real revenue outcomes, with weaker absorption in Class C reinforcing downside risk in lower-quality stock.

Geographic fundamentals have also reasserted themselves in pricing. Suburban assets generally benefit from stronger household formation, steadier occupancy, and reduced concession pressure, supporting more defensible income profiles and steadier valuations.

Urban assets face different dynamics, including slower rent growth, higher concession packages, elevated turnover, and increased competition from new supply in many core metros. These headwinds support wider yields and more conservative underwriting.

The suburban-urban spread reflects investors’ focus on relative risk and transaction depth. CoStar data shows suburban cap rates modestly above urban levels, indicating investors may still require additional yield for suburban assets even when operating performance is more stable.

This Gulf Coast growth market illustrates how quickly multifamily pricing can separate when operating costs rise and supply accelerates, making it one of the most telling barometers for today’s valuation environment.

• Premiums up 30-70% since 2022

Source: FannieMae

• Older assets are seeing 15-20% Operating Expenses (vs. 8% national avg)

Source: FannieMae

• Class C assets absorb the steepest surcharges due to aging systems and elevated claims history

Rent Fundamentals

• Effective rents flat to negative in several submarkets

• Renewal spreads compressing

• Rising vacancy in new deliveries

Wide dispersion in NOI trajectories

Wider pricing cushions required

• ~45,000 units projected to deliver from 2024-2026

Source: CoStar Group, Inc.

• Urban cores face the most extended lease-up timelines

• Concessions up 8–12% YoY across Class A in 2024-2025

Source: FannieMae

• Class A-Class C differential: 175-225 bps

• Suburban assets trade 50-100 bps tighter than urban

• Class C discounts deepest due to OpEx + CapEx exposure

Suburban stability priced at a premium

Even with near-term pressure from supply and insurance-driven operating expenses, Houston’s long-term growth outlook remains intact. Population and job gains continue to expand the renter base, supporting demand as the current delivery wave works through lease-up.

• Suburban assets win because occupancy and concessions fluctuate less, not because they’re “hot”

• Urban assets face wider valuation ranges due to supply, turnover, and concession cycles

• Class A: stability benchmark

• Class B: execute and churn risk premium

• Class C: greater OpEx variability, CapEx burden, and turnover risk result in the widest cap rate levels

• Cap rate compression will be slow and uneven, as pricing is driven by operational risk, rather than macro relief

• The Class A/C spread remains structurally wide as aging stock absorbs higher insurance, CapEx, and turnover risk

Multifamily pricing has shifted toward what can actually be defended at the property level. In an environment defined by cost pressure and uneven demand, valuations reward assets that keep income steady and expenses predictable, and penalize those with wider operating variance. Reading the market now requires focusing less on broad narratives and more on the mechanics that determine whether NOI holds or erodes.

Looking ahead, the reset is likely to remain selective and spread-driven. Properties with flexible revenue, resilient systems, and stable tenant behavior will continue to command a clear pricing premium, while assets with heavier operating drift should face persistent valuation pressure and wider yields. Success in this cycle comes from aligning strategy with what is durable, measurable, and repeatable as the market continues to reprice risk.

Daniel Withers

daniel.withers@matthews.com (818) 923-6107

Luke Matthews

luke.matthews@matthews.com (281) 809-4006

Nathan Shields

nathan.shields@matthews.com (346) 326-8993

After two years of rate-driven paralysis, the freeze is over, and the next wave for the healthcare real estate market has begun. The sector established a clear market floor in the second half of 2025, with cap rates leveling around 7%. The bid-ask gap between buyers and sellers is narrowing as stakeholders realign on pricing, triggering a significant rebound in transactional activity across the sector.

Healthcare real estate is anchored by strong fundamentals that help it withstand broader market slowdowns, with occupancy nearing 93% across the top 100 metros and performance driven by the predictability of

Healthcare real estate operates on a distinct rhythm from the broader market, driven not by volatility but by the steady, real-time demand for patient care and accessible treatment. By 2030, one in five Americans will be over the age of 65, embedding long-term, non-cyclical demand directly into the medical real estate sector, according to the U.S. Census Bureau.

An aging population isn’t a trend.

It’s a demographic certainty driving the need for expanded clinics, specialists, & ongoing care.

The shift toward distributed care is redefining where medicine happens, as healthcare undergoes a broad rebrand away from hospitalcentric delivery and toward models that prioritize convenience, flexibility, and care closer to home. Outpatient clinics, surgery centers, and specialty practices now handle procedures once limited to hospitals at operating costs 30-60% lower, making them the preferred setting for both patients and providers, according to a JAMA Network study. It’s a system built around people in their everyday life, powered by adaptable clinics rooted in the communities they serve.

physician and healthcare group tenancy, according to PwC’s Medical Office Real Estate Outlook. That durability is supported by long lease terms, steady patient volumes, and limited new supply as high construction costs sideline many developers, while Future Market Insights projects the U.S. outpatient clinics market is projected to grow from about 44.3 billion in 2025 to roughly 67.4 billion by 2035, setting the stage for the next leg of the medical real estate cycle.

2026 is the turning point; but timing will determine who leads the cycle & who chases it.

Amid accelerating demand for outpatient and specialty clinics, the market is now running into a shortage of high-quality medical space. With construction costs still elevated, most developers remain sidelined, creating tight supply conditions just as tenant demand accelerates. That scarcity gives existing property owners real pricing power. Strategic partnerships are expected to account for only 10-15 healthcare projects breaking ground in 2026, including new behavioral health facilities in smaller markets, rural cancer treatment centers, university-affiliated hospitals, community health hubs paired with recreation amenities, and specialized units such as regional burn centers.

Capital that spent the last two years on the sidelines is beginning to move again, with underwriting steadying and debt costs no longer swinging week-to-week. Investors are stepping back in with clearer expectations, and their return signals renewed confidence as pricing stabilizes and debt becomes predictable. This tightening supply, paired with the sector’s resilient fundamentals, is drawing fresh interest from REITs and institutional buyers, elevating outpatient medical office buildings and intensifying competition for high-quality clinical assets as early-cycle capital begins to reemerge.

Source: CoStar Group, Inc.

Moderate absorption & limited deliveries keep vacancy nearly flat through 2028, signaling demand pressure & an undersupplied market.

Modern care delivery is generating clear momentum in certain specialties, while others are stabilizing through consolidation or adapting to reimbursement pressures. Outpatient-oriented, cash-flow-stable, and platform-backed specialties will take the lead as the next cycle unfolds.

Growth Leaders

Strongest Demand, Tightest Cap Rates

• ASCs: More procedures migrating from hospitals

• Imaging: Diagnostics rising across all specialties

• Urgent Care: Convenience-based, steady

• Dialysis: Essential-care, zero elasticity

Why it matters: Early compression drivers will anchor the first wave of institutional capital.

Scarcity-Driven Upside

• Behavioral Health: Payer-mix attention required, but demand surging

• Dental/Oral Surgery: DSO consolidation strengthening credit

Why it matters: Limited supply & resilient demand push rents higher and widen spreads.

Credit Bifurcation

• Aesthetics/Med Spas: Cash-pay, high margin, platform roll-ups

• Dermatology/Plastic Surgery: Demand steady, credit tied to scale vs. boutique operations

Why it matters: Pricing hinges on operator scale & backing as platform-backed groups trade tighter.

Shifting Credit Profiles

• Urology, Ophthalmology, Dermatology: MSO roll-ups reshaping credit consistency

• Oncology & OB/GYN: Reimbursement pressure pushing system-backed lease tenancy

Why it matters: These segments won’t set pricing, they will redefine credit strength & underwriting.

Essential-care specialties trade in tight bands, reflecting strong credit, high renewal probability, & limited relocation risk. ASCs, imaging, & dialysis anchor lower yields, while urgent care & behavioral health cap rates are slightly wider but remain firmly within core medical ranges.

Elective specialties rely on discretionary spending, which creates wider pricing spreads and more volatility. Those backed by scale or private equity/MSO platforms perform far better, while standalone boutiques see higher cap rates that reflect their revenue swings.

Source: BGL & CO 2025 Healthcare Real Estate Mid-Year Market Update

As institutional owners control over $537 billion in assets, according to RevistaMed’s 2025 report, the next market cycle presents a unique opportunity for private practitioners and physician-owned groups to leverage ownership and exert a new degree of influence over the sector’s evolution.

Ownership transforms the practice location into an economic engine, supporting growth today and enhancing valuation tomorrow.

Owning the facility gives physicians the flexibility to expand services, add providers, and modernize layouts, while predictable occupancy costs provide stability to reinvest in operations and support longterm growth. As physicians near succession or retirement, a well-structured lease to the real estate entity becomes key to preserving value; renewing or adjusting that lease 12-18 months ahead of a sale— and securing successor providers or MSO support— helps solidify income and boost buyer confidence.

Elective & consumer-driven specialties trade at wide cap rate ranges, reflecting greater revenue variability, higher discretionary exposure, & a broader spread in operator credit quality.

Liquidity tools like sale-leasebacks and 1031 exchanges let physicians unlock equity without disrupting care. In a sale-leaseback, the physician sells the building and stays under a new long-term lease, which buyers underwrite closely. Before pursuing a transaction, physician-owners should ensure lease terms meet market standards and align the deal with their long-term practice goals.

Owners, developers, & investors should evaluate their assets before cap rate compression & institutional competition reduce margins.

Essential Market Signals & Strategies to Track over the Next 12-18 Months

Cap rates are stabilizing and will likely compress as institutional capital re-engages. As bid-ask spreads tighten, competitive pressure will rise quickly, making early positioning essential to secure strong pricing and yield.

Monitor shifts in credit quality as consolidation accelerates in specialty sectors. Aligning with platform-backed groups or health systems will reinforce stability and mitigate reimbursementdriven volatility.

New construction remains minimal, and the scarcity will continue to push rents upward while accelerating lease-up for high-quality outpatient assets. Any 2026-27 deliveries will benefit from this imbalance.

ASCs, imaging, urgent care, and dialysis will anchor low-cap-rate demand. Behavioral health and dental/oral surgery continue to show strong rental upside due to undersupply. Elective segments will vary widely depending on operator scale and platform credit.

Rising construction costs make execution a competitive edge. Developers and owners who deliver on time and tailor spaces to clinical workflows will earn better rents and retention.

Expect increased utilization of sale-leasebacks, 1031 exchanges, and joint-venture structures as physicians and private groups leverage real estate to support expansion, liquidity planning, and succession strategies in the new cycle.

Shock

Capital takes a step back; pricing discovery begins. Rebuild

Momentum returns, setting up for 2025-26 activity. Expansion

Early movers lock in yield before competition rises. Maturity

Market stabilizes; long-term income dominates.

Reset

Market finds footing; investors re-engage.

(949) 432-4513

Transition

Confidence returns; bid-ask gap narrows.

(310) 955-5834

Competition

Institutional surge compresses yields.

(949) 432 4517

By David Treadwell

The U.S. multifamily market finds itself at an inflection point. On a national level, the country remains structurally undersupplied relative to long-term housing demand. Many median income. Yet, at the same time, many major multifamily metros are grappling with elevated vacancy, slowing rent growth, and over building. This contradiction has raised demand or merely a temporary imbalance in