The promises of industrial capitalism

In his 1913 book, The bourgeois, Werner Sombart gives an intriguing explanation of the development of long-term rationality, which is a typical trait of industrial capitalism. He starts with the assumption that the traditional economy of medieval feudalism with its separate logic of agrarian subsistence, craftsmanship and long-distance trade of luxury goods was transformed into a society in which the thirst for money governed the spirits of all members of society:

“We know manifold testimonies from the 15th and 16th century, which show that money everywhere in Western Europe had begun to claim a dominant position. Pecunia obediunt omnia laments Erasmus; money is the earthly god on earth claims Hans Sachs; lamentable is how Wimpheling labels his time, in which money has begun to govern.”

(Sombart, 1913, )

However, it was only gradually that this general quest for money translated itself into the systematic financing of industrial projects which would increase the overall productivity of the economy. In fact, Sombart claims that first there was the general quest for money of the Renaissance era, which had its origins in the accumulation of treasures by kings and noblemen during medieval times. This attitude was later combined with an unsystematic entrepreneurial spirit, which resulted in the craft of project-making. He cites Daniel Defoe which explains that it was “about the year 1680, the art or mystery of projecting began visibly to creep into the world” (ibid. p.54)1. The phenomenon of project-making was not limited to England but also widespread in France, where 'donneurs d'avis' and 'brasseurs d'affaires' tried to make quick money with all kinds of projects. A next step was the combination of project-making with the logic of the stock-exchange which lead to the development of “stock-jobbing”, i.e. a strong increase in the trade of stocks.

As the experience of the tulip mania or the South Sea Bubble demonstrate, the projects traded on the stock-exchange often had no reasonable base of gain. On the contrary, many projects attracted traders with their fantastic descriptions and worked because traders participated hoping that gains would materialize or that they would be able to sell the shares before their value would eventually precipitate.2

It was only with the rise of industrialism and industrial banking that the stock-exchange became a motor of productivity growth. Banks beforehand were reluctant to finance industrial projects as they

1Cfr. Defoe,D. “An essay on projects”

2Cfr. Keynes' famous comparison the functioning of the stock-exchange to the betting of who would win a beauty contest.

2

were considered risky and stuck with their tradition to give out loans against land or housing property. Therefore, it took the skills of gifted entrepreneurs to convince both bankers and political elites to finance industrial projects, as it was only after the so-called Glorious revolution of 1688 in England, in which the government made the whole British people liable for public debt, that banks started to view public debt as a safe form of investment.

In other words, there is no automatic connection between banking and the financing of innovative project which enhance overall productivity and therefore the Gross domestic product of a given nation. It needed entrepreneurs and often a war related interest in new technologies by the nation states to develop long-term industrial banking, instead of the financing of speculation and managing the money of the then rich and powerful. In Sombart's view, this new mentality was the typical trait of the 'bourgeois', who combined entrepreneurial thinking with a long-term calculation of risk, typical for the industrious and frugal citizen (Buerger). As a result, long-term rational thinking was generalized throughout the 19th century as the net worth of business projects of all kind was judged with the help of mathematical tools, of the sort we now know as fundamental analysis.3

This long-term mentality was fostered by 19th century nation states which in Europe where fighting for supremacy and began to invest heavily in education, technical knowledge and infrastructure, such as railroads and roads. Sovereigns soon realized how important banking was for industrial development and began not only to regulate the financial sector, but also to influence industrial relations. In Germany this lead on the one hand to the foundation of the Reichsbank in 18704, a central bank, like the bank of England, and on the other hand to the gradual introduction of social security.

Often it were the important entrepreneurs of the likes of Owen, Fourier and Bosch which nurtured paternalistic feelings for their workers and which had utopian visions, which they tried to realize partially with educational schemes and their manifold model projects (Siemensstadt, Hellerau in Dresden, etc.).

In other words, there seem to have existed a connection between industrial engineering and social engineering. At its high point, this lead to a progresive mentality which made important fractions of society believe that a planned economy, and therefore a planned society was possible. Marx himself, although a fierce critic of a capitalism that destroyed the traditional and often more human fabric of society via processes like urbanization and proletarization had high hopes for industrial communism and wished the construction of an enlightened society in which 'everybody lives according to his needs and gives what is in his possibilities.'

3As opposed to speculation and technical analysis, which tries to capture the behavior of the other market participants, and where gains are realized, because the trader is able to react more quickly than other traders 4Cfr. also the role

3

The progressive entrepreneurial spirit also transformed areas outside of industrial production and led to a general activation of society to organize and pool resources. Farmers gathered in cooperatives to enhance their bargaining power and to get access to loans to finance modern agricultural equipment. An exemple is Wilhelm Raiffeisen, the founder of the Raiffeisen banks. Thorstein Veblen tried to capture this progressive spirit with his famous distinction between 'engineers' and 'businessmen'. But he was pessimistic that enduring social progress was possible and claimed in his 1899 “The theory of the Leisure class” that the old traits of tribal and aristocratic societies with their quest for social distinction were still very present in modern American society. His book was therefore an attack on communitarian and democratic hopes and somehow anticipated Schumpeters “Capitalism, Socialism, and Democracy”. Veblen also attacked the ideal of perfect competition underlying economic theory in his 1904 book “The theory of business enterprise”, describing with colorful language such as 'robber barons' that the 'captains of industry often curtailed production' to realize monopolistic profits and that therefore markets needed regulation to function properly, anticipating the developing literature on industrial organization and monopolistic competition.

Despite these criticisms, state led industrial development led to an explosion of GDP per capita and to an unprecedented degree of social mobility from the 1950s to the 1980s and to the development of a middle class society in the USA and Western Europe.

Finance doubly unbound: the realities of postindustrial capitalism

It should have become clear from the first part that there is no automatic connection between the drive to make money and the financing of industrial projects which increase overall productivity and, thus total GDP. On the contrary it was a specific constellation of competition between nation states, scientific inventions and the progressive spirit of the Enlightenment which put financial institutions under pressure and provided them with unprecedented tools to calculate risk. With the advent of multinational companies, globalization and automation there were several reasons why finance returned to speculation as it already existed in the 17th century. First, the contribution of manufacturing to GDP declined from over 50% during the 1950s to often less than 20% today. This development made sectors like housing much more interesting for banks, also because large multinationals often rely on their own revenue to finance their investments. Second, in a highly developed economy and a general atmosphere of peace, savings are abundant and resources need not to be supervised strictly as it happens during war times. Third, financial regulations were overthrown in a conscious attempt by right-wing or movement conservatism and

4

special interest groups more in general to remove regulations which were deemed necessary after the Great Depression of the 1930, such as the Glass-Steagall or Banking Act of 1933, which limited securities activities and affiliations between commercial banks and securities firms, and was repealed in 1999 through the Gramm-Leach-Bliley-Act.5

As a result the world of finance is increasingly disconnected from the real economy as Luciano Gallino has masterly explained in his book on financial capitalism 6 This disconnection reveals itself in a divergence of performance of industrial sectors and the banking sector, as banks continue to focus on debt titles and investment banking, which however is often no investment in industrial risk. We therefore have a situation that is characterized by the financing of projects of the sort of the beauty contest, in which traders speculate on the hope that they can beat the market and which are often unreasonable from an macroeconomic point of view. (speculation on housing, etc.).

But finance is also free from another pressure it usually had to face: That of a independent and superior sovereign which had a strong regulatory power. This controlling instance, which will be explored from an historic point of view in the second part of the paper, was often able to cancel debt and to shape and control financial activities.

Today, instead, the financial elite is able to pressure the democratic and economic institutions to serve their interest, which consists in the strict enforcement to repay private and public debt as we can observe during the ongoing financial crisis in the US and the Eurozone and to a disregard of overall macroeconomic rationality, as proposed for example by Paul Krugman in his recent book “End this depression now!”.7

The supremacy of finance works through the financialization of industrial activity, as is evident in the structuring of departments into profit-centers, the short-terminism inherent normal accounting practice, which obliges management to report activity every three months and in the general dominance of controlling. Finance influences also the political realm, exploiting the fact that election campaigns in mass democracies are very expensive, a reason why in the US, both left- and right-wing parties are unable and/or unwilling to reform the financial sector. Furthermore, big hedge or pension funds can force a government indirectly to adopt certain reforms by accepting or declining public debt of that specific country. Therefore, instead of regulating finance, politicians are influenced by it and assimilate the values of the financial system much like syndicalists and social democrats used to adopt the values and lifestyle of the economic and political elites at the beginning of the 20th century.8 The result is a world in which the rentier sectors play a dominant

5Cfr. Krugman (2007) “The Conscience of a liberal”

6Cfr. Gallino, L. “Finanzcapitalismo. La società del denaro in crisi”

7Cfr. Krugman (2012) “End this depression now!”.

8This process has been masterly analized by Robert Michels in his 1919 “The Iron law of the oligarchy”.

5

role, as Michael Hudson has pointed out. He argues that in order to be able to understand the overall dynamics of the economy, new models are needed which incorporate the specific workings of the modern financial sector:

Now that the Bubble Economy has given way to debt deflation, the world is discovering the shortcoming of models that fail to explain how most credit creation today (1) inflates asset prices without raising commodity prices or wage levels, and (2) creates a reciprocal flow of debt service. This debt service tends to rise as a proportion of personal and business income, outgrowing the ability of debtors to pay – leading to (3) debt deflation. The only way to prevent this phenomenon from plunging economies into depression and keeping them there is (4) to write down the debts so as to free revenue for spending once again on goods and services.9

Hudson states that the “FIRE sector”, which stands for finance, insurance, and real estate, has become the dominant and controlling sector, given that “80 percent of bank loans in the Englishspeaking world are real estate mortgages, and much of the balance is lent against stocks and bonds already issued.”10 He furthermore claims that this sector is the modern form of the rentier class:

Just as landlords were the archetypal rentiers of their agricultural societies, so investors, financiers and bankers are in the largest rentier sector of today’s financialized economies: finance controls the economy’s engine of growth, which is credit in all its forms. Economies obviously need banking services, insurance services, and real estate development and so, of course, not all of finance is ‘without working, risking, or economizing’. The problem today remains what it was in the 13th century: how to isolate what is socially necessary for “retail” banking... from extortionate charges such as 29% interest on credit cards, penalty fees and other charges in excess of what is socially necessary cost-value.11

We therefore have a situation in which finance is doubly unbound. First, the finance and banking are by now only weekly related to judging and financing industrial projects. This leads to the paradoxical situation that financial actors dispose of very powerful and costly computer equipment to beat a market which is mainly devoted to speculation of Keynes' beauty contest type in which 9Cfr. Hudson, M. (2012) “Incorporating the rentier sectors into a financial model”. 10Ibid. 11Ibid.

6

making money is a zero-sum game, like it was already the case at the times of the tulip mania or the South Sea bubble. Economically speaking, most of these activities create no added value and have mere redistributive effects. Second, contrary to what happened from the 16th to the second half of the 20th century, finance is no longer related to a superior authority, which can effectively control its activities. Instead, the goals of the FIRE sector are increasingly in conflict with the needs of political communities, be it nations states or larger constructions, such as the European Union. Unbound finance leads to a segregation of society comparable to that practiced during aristocratic rule in medieval Europe or the Ancient Roman Empire.12 Talented individuals still can become part of the rentier class, but the social mobility based on hard work in hierarchically structured industrial firms, which was typical for post-war capitalism is no longer a predominant phenomenon, as people often take on too much debt to maintain what I would like to describe as middle class illusion in a moment where the middle class is shrinking. As a consequence, conflicts between social classes, nation states and even continents are reappearing, and the existing democratic institutions may not suffice to successfully manage these conflicts.13

The Post-Industrial crisis model: Debt service and Beggar-thy-neighbor strategies

With a dominant financial sector which secures the power of the new rentier class, politicians have not many possibilities to change the world. As already mentioned, there are close ties between financial and political elites and until now, with the exception of Lehman-Brothers, the politicians have saved the banks in difficulties after the 2008 Financial crisis, arguing that they were too big too fail. In the heat of the moment, it might have been necessary to save big players to avoid a major breakdown. What was not necessary, however, was the systematic replacement of private debt with government debt afterward, which is in line with Micheal Hudson's observation that we live in a world where debt service is abundant and debt deflation a constant risk.

In such a world, politicians do not have the power to take strong action, as it was partially the case during and after World War II, when a high income tax not only provided for the war expenses but also leveled the differences between the rich and the poor in the United States. As we will see in the remaining parts of the paper, the political and financial elites were always intertwined throughout history and income inequality seems to be a human constant, as already Vilfredo Pareto had pointed out more than a century ago. However, the relationship between political and financial elites

12Cfr. Neckel, S. “Refeudalisierung der Oekonomie: Zum Strukturwandel kapitalistischer Wirtschaft”, MPIfG Working Paper 10/6

13Cfr. Schimank, U. “Wohlfahrtsgesellschaften als funktionaler Antagonismus von Kapitalismus und Demokratie: Ein immer labilerer Mechanismus?

7

differed in some important aspects from what is the case today. Most importantly, kings were able to nullify debt when it had become too heavy a burden, thus avoiding the risk of depressing and socially destructive debt service.

Today, political leaders are confronted with the problem that only a concerted effort could invert the relationship between politics and finance and shift the balance back to political power. However, this seems unlikely to happen, as companies and financial institutions are organized and act on a global level, whereas politicians pursue the interest of nation states or even smaller regions. Moreover, they are under pressure to get reelected and have to deal with powerful media groups. Therefore, international coordination is very unlikely and occurs not even between the French and the Germans who by now have a long tradition of problem-solving in the European Union. Instead, national differences prevail and political leaders end up with the strategy to foster their national champions to secure low unemployment rates in their home countries.

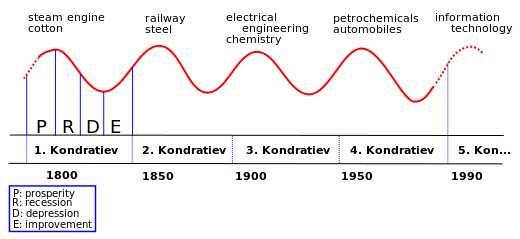

More specifically, the problem is that growth in the long term is driven by technological progress. And although investment in research and development is considerable all over the world, it might well be that the next Kondratieff cycle, i.e. the next technological breakthrough (the former five being 1.steam engine, cotton, 2. railway, steel, 3. electrical engineering chemistry, 4. petrochemicals, automobiles, 5. information technology) will not appear within short or will not have the desired employment effects.

Fig. 1 Kondratieff cycles from 1800 to 2010

The prospect of a rather stagnating economy, in which the rather low-productive non tradable-sector amounts to 60-70% of the economy, opens the door to beggar-thy-neighbor strategies to ensure that a high-productive tradable sector remains in one's region or country. Ultimately, this is an understandable strategy, as international supply chains have become highly mobile twenty years

8

after the introduction of the first web browser in 1993. The decision for a location of industry depends on a country's productivity relative to income and competitiveness14 and on how attractive the country is for a mobile creative class15 which by now is ready to work all over the world when certain economic conditions are assured.

Together with the debt service towards the financial sector and the rentier class which profits from it, the prospect of ongoing beggar-thy-neighbor strategies is a dire one, as it leads to a race to the bottom and pits regions, nations and even continents against each other. Studies have shown that the productivity gap of Eastern Germany compared to Western Germany is largely due to the absence of high productive manufacturing firms in the East. There is no reason for West German firms to invest in the East, whose overall productivity has stayed at around 60% of West-German productivity since 1996, because workers are mobile enough and move to where the production facilities are.

During the ongoing Eurozone crisis, the beggar-thy-neighbor behavior of German elites is particularly striking. After the fixation of the exchange rates in 1999 the Germans devalued internally in a somewhat hidden way with the Hartz IV reforms of the labor market.

Fig. 2 Unit labour costs in Germany, France and Southern Europe (chart by Prof. Heiner Flassbeck)

This move lead to an unfair competitive advantage for the German industry which most of the

14Spence, A. M. (2012). Tradable prosperity. Project Syndicate. http://www.project-syndicate.org/print/tradableprosperity

15Cfr. Florida, R. (2002) The Rise of the Creative Class. And How It's Transforming Work, Leisure and Everyday Life

9

German elites still deny. In fact, Germany is thriving today not only because of its highly competitive industries and products, but also because it did not reach the inflation goal (with salaries being the main driver of inflation) agreed upon in the Maastricht treaty.16 The problem is that countries in the Eurozone were and are not able to leave the Euro and devalue in the order of 20 to 30% relative to Germany as would be reasonable from a macroeconomic point of view. As a consequence, Italy has lost some 28% of its industrial production after the outburst of the financial crisis in 2008 and France has increasing employment problems as both countries are confronted with a stagnating or even shrinking GDP.

As Dani Rodrik has argued in his book The globalization paradox17, this behavior may ultimately lead to the breakup of the European Union as German financial elites are not willing to renounce on some of their debt claims and German industry is not willing to renounce on the unjust competitive advantage described in the last paragraph, which bestows them with unprecedented export surpluses.

However, beggar-thy-neighbor conflicts are not limited to regions within nation states or to members of unions with fixed exchange rates. As the cases of China and Japan demonstrate, countries can either manipulate their currency or overly pamper their manufacturing in order to keep parts of the highly mobile value chains in their countries. Ultimately, this may lead to currency wars or new forms of protectionism as high productive jobs are major drivers of GDP.

Lessons from the past: Conflicts over sovereignty and their solutions

The history of debt is very old. David Graeber describes it in his 2011 book Debt. The first 5000 years and Michael Hudson explains the relationship between debt and forms of government as described by Aristotle18:

Book V of Aristotle’s Politics describes the eternal transition of oligarchies making themselves into hereditary aristocracies – which end up being overthrown by tyrants or develop internal rivalries as some families decide to “take the multitude into their camp” and usher in democracy, within which an oligarchy emerges once again, followed by aristocracy, democracy, and so on throughout history.

Debt has been the main dynamic driving these shifts – always with new twists and 16Cfr. Beck, U. (2013) German Europe. Beck explains how Germans role as creditor transforms multilateralism into unilateralism, and equality into hegemony, although he insists that Germany's new dominance is a soft dominance, because other countries could leave the Eurozone if they wish it.

17Rodrik, D. (2011) The globalization paradox : Why global markets, states, and democracy can't coexist. 18Cfr. Hudson, M. (2011) Democracy and Debt.

10

turns. It polarizes wealth to create a creditor class, whose oligarchic rule is ended as new leaders (“tyrants” to Aristotle) win popular support by cancelling the debts and redistributing property or taking its usufruct for the state.

In the Torah, the sacred book of the Jews we find a mechanism to overcome this cycle of forms of governments in the form of the Jubilee year. Every 49 years, which is the same as every seven sabbatical years which occur every seven years, the land and other property except the houses of laymen within walled cities had to be given back to their original owners or their heirs. Indented servants of Israelite descent were also to be freed. This extraordinary prescription in a religious book of the importance of the Torah hints to fact that rising inequality was considered a real problem in early human settlements.

Karl Polanyi in his 1944 The Great Transformation has argued more in general that central power always had the function of redistributing food or money from the rich to the poor and it is probable that this included also the cancellation of debt.

During the middle ages we find a particular constellation, because the ruling aristocracies were not supposed to lend out money against interest, given that the Catholic church, which had become very powerful after the Investiture controversy which ended with the Concordat of Worms preached a general ban on interest from the beginning of the 12th century, which was strictly observed until the reformation.

This put Jews in the position to be the only moneylenders, a role they were officially allowed to occupy since the 1179. They, however, never got into a dominant position, mainly because their social position was weak and aristocrat rulers often defaulted on their debts, a behavior the creditors had to accept.

The ban on interest is similar to the Jubilee provision in the sense that it is a mechanism to prevent the accumulation of wealth in a static economy, and the abuse of power which can result from it. Interest becomes useful, once the economy starts to develop, as it is the measure to judge and propel investment projects. As a member of a very rich merchant and banking family, Jakob Fugger, asked to abolish the ban on interest, because he wanted to profit from the sale of benefits and indulgencies. This claim was severely criticized by Martin Luther and the humanist Ulrich von Hutten. The monopolistic power of the Fugger and other merchant families like the Welser was seen critical by many contemporaries, and consequently, imperial fiscal authorities brought action against them.

As a result, the Fugger had to be close to ruling imperial dynasty of the Habsburg, who on the one hand shielded them, but on the other hand did so only because they were eager to use their services

11

to finance their wars. This close relationship was fatal for the Welser who wentt bankrupt in 1603, but also the Fugger19 who had financed emperor Karl V. during the Schmalkalden war (1546/47) and the insurrection of the nobles (1552) had to accept huge losses towards the Habsburg dynasty. In fact, the Spanish state went bankrupt several times had triggered a period of international financial crises.

Defaulting on sovereign debt was also a common practice in England. Already in 1345, the Florentine bankers Bardi and Petruzzi went bankrupt when Eward III repudiated his war debt, which was considered a personal debt. In fact, such debt got canceled when the sovereign died, which put a heavy risk burden on the bankers. In 1672, another English king, Charles II, defaulted on the loans the goldsmith-bankers of London had granted him, a move that became known as the Stop of the Exchequer. This situation changed with the Glorious revolution of 1688, which made the whole people, reliable for state debt:

...the Stop of the Exchequer, resulted in the failure of many London goldsmith-bankers and made their notes unacceptable during the 1670s. However, after the Revolution, the people became liable for the debt obligations of the government regardless of who the king was. This political change enhanced the government’s commitment to and credibility in being able to repay its debt and thus became the basis for the development of the financial system in early modern England.20

Bankers had to bear a lot of risk in medieval and renaissance times. The tradition of debt to default on debt or to consider sovereign debt as a personal debt of the respective king or emperor ended only with the advent of the nation states and their transformations into republics. But until the crisis of the 1870s (Gründerkrach), debt repayment was a less dominant motive, basically because the economy was rapidly growing during the Industrial revolution.

Although the stock market crash of 1873 slowed growth for several years, because investors were reluctant after the huge losses during the preceding construction boom, its consequences cannot be compared to the aftermath of the 2008 Financial crisis, simply because technological innovation soon turned to be the motor of growth and industry. In fact, the Kondratieff cycle number 3, electrical engineering and chemistry began to unfold and industrial production soon reached new heights.

19Cfr. Karg, F. (1993) Die Fugger im 16. und 17. Jahrhundert in EICKELMANN, R. (Hrsg.): lautenschlagen lernen und leben. Die Fugger und die Musik – Anton Fugger zum 500. Geburtstag. Augsburg

20Cfr. Kim, J. “How politics shaped modern banking in early modern England: Rethinking the nature of representative democracy, public debt, and modern banking”, MPIfG Discussion Paper 12/11

12

This is also partly the case for the Great Depression which unfolded after the famous stock market crash of 1929. Here external factors, like the huge war debt England and France had towards the USA, and the resulting reparation claims towards Germany severely aggravated an economic crisis into an international political crisis, in which Fascism, Nazism, Liberal democracy, and Soviet communism tried to emerge as the winning political form. However, the debt service and the losses in the financial sector led to an Aristotle type of dynamic. In Germany a weak democracy was replaced by a dictatorship which gained ground because it repudiated the war debt and started to invest heavily in infrastructure, which restarted the business cycle. The silently accumulated war debt was canceled after World War II as the Reichsmark was replaced by the Deutsche Mark in 1948. After this debt cancellation, the worldwide economy was ready for Kondratieff cycle number four, petrochemicals and automobiles.

What lies ahead – Western decline and the rise of Asia?

Today, the situation differs in one important aspect from the Great Depression. In its aftermath, a political struggle broke lose during which global power shifted from the British Commonwealth to the United States of America, and which marked the beginning of a system of parliamentarian democracies. Albeit with dramatic consequences, the political realm was much like during medieval and renaissance times able to override the interest of the financial and industrial elites. To cover the war costs, income taxes were raised to unprecedented levels and currencies were inflated. Evenly, important, war debts were canceled after World War II, to avoid the repetition of the dynamics which had led to the war. The world was half destroyed but free of debt.

This is not true today, as the Western world seems to be under post-democratic rule in which a strong international financial and business elite which operates in huge global firms is not only able to influence politicians in the US and in Europe to act in their interest, but also seems to be flexible enough to avoid critical situations comparable to the major political disruptions during the 1930s which eventually lead to World War II.21 We are experiencing local uprisings and mass protests like 'Occupy Wall Street', but political tensions are often managed in a way that protests eventually vanish.22 Therefore, it is not clear how the nations will deal with the ongoing debt service in a basically stagnating post-industrial economy. There might be another cycle of strong technological innovation but it is unlikely to have the same effects the last two Kondratieff cycles had on employment and income distribution.

21Cfr. Crouch, C. (2004) “Post-Democracy”.

22Cfr. Schimank, U. (2011) “Nur noch Coping: Eine Skizze postheroischer Politik”.

13

So what lies ahead? If we want to learn from history, we have to look at historical constellations during which no strong boundaries or rules divided the reigning elite into factions in competition with each other. This was the case throughout the Roman Empire and during the Investiture controversy which lasted from 1059 to 1122.

In the Roman case the landed aristocracy was so powerful that it was able to prevent expropriation and redistribution. In a process which lasted more than three centuries, social mobility came to a halt (soldiers could no longer get rewarded with territories from new conquests), the critical christian church was assimilated when Constantine made Christianity the official state religion and inequality finally rose to a critical point. Critical because Roman elites, instead of being willing to share their wealth and to invest into a young and potentially interest-threatening young generation of soldiers and bureaucrats preferred to rely increasingly on barbaric tribes to protect the borders of the empire, being convinced that their money would eternally be able to secure their dominant position. When the pressure of incoming barbaric tribes grew too strong and the borders were overrun, the elites were incapable to organize a strong resistance because the former middle class had by then regressed into indented serfs, not only unable, but also unmotivated to defend the old structure. Max Weber has described this social process which increasingly separated the elites from the middle class and finally led to the disintegration of the Roman Empire in his famous essay The social reasons for the decline of the Ancient culture23

During the investiture controversy, the opposite happened as the Catholic church was able to break the tradition that the emperor appointed the pope. Eventually this led to the abolition of the tradition of investiture and simony and to the introduction .of a fruitful competition between church and state elites. Church leaders were able to impose their thoughts on interest and distribution of power and were thus able to guide the process of medieval expansion and relative unification of the West. The controversy is particularly interesting because a part of the elite was able to start a dynamic process which resulted in expansion (crusades), cultural development through the regulation of social behavior and the practice of fruitful competition (i.e. the development of music and art at courts and churches) and social progress as a culture of rights and duties redeveloped. During this process the church in the 13th century debated the function of interest and and more in general tried to find the “just price”. Producers and lenders of money needed to have an incentive to provide their services to the community, but the development of enormous inequalities was considered as harmful for the community. This fruitful competition was also central in the field of charity, where organizations of the church and private citizens tried to attract private funds with a mix of good governance and

23Cfr. Weber, M. (1896) “Die sozialen Gruende des Untergangs der antiken Kultur” after a presentation at the Academic Society in Freiburg im Breisgau.

14

patronage of the arts. One very instructive example is the city of Venice in which the citizen-run Great Schools (of St. Roch or of St. John the Evangelist) competed with the church run hospitals in which orphans were raised and educated.24 It was custom to leave consistent parts of private heritage to these organizations, a custom that not only channeled resources to public bureaucracy but also slowed the accumulation of private wealth and the development of unsustainable inequalities.25

In my opinion the West should learn from these historical experiences. Western elites can either collude completely, focusing on debt service and decline into a form of post-democratic regime in which beggar-thy-neighbor strategies are very prominent and in which inequality and social exclusion is rising. After a prolonged period of decline, internal devaluation and local uprisings could lead to a renewal of serious class struggle as some elites may want to break apart from the post-democratic reality and care for their populations.26 In this scenario it is also thinkable that some regions strive to become independent of the international financial elite drawing on cooperative forms of financing and investing. This already somewhat happening in the Trentino region which is much more capable than other Italian regions to manage unemployment and investment thanks to a network of cooperatives which are active in many sectors of the economy and which are organized in a umbrella organization which coordinates the overall strategy. In any case, renewal would be the result of a painful process during which life chances and happiness of many people in the West would be reduced.

The opposite opportunity lies in the possibility that a part of the elite will pick up the heritage of the Christian culture and develop and impose rules which make a stagnant postindustrial economy workable from a distributive point of view. At a culmination point this could lead to a new form of jubilee year and a new discussion of the right interest rate and which kind of banking is sustainable and what kind of speculative activities should be avoided. History teaches us that such a dynamic can be very powerful. In the 13th century, the Templar Order had become very powerful and very rich during the crusades as it had the right to lend and actually a very good reputation as moneylenders. However, it became a form of state within the state, a situation Philippe the

24Like Rome, Venice declined after its possibilities to expand where restricted by the advancement of the Turks in the mediterranian seas. The merchant city elites transformed into landed aristocracies who withdrew attention and resources from public life, a process that led to a divided society unable to keep up with the challenges of developing industrial modernity.

25In this light Adam Smith unfettered support of the interest of the producers comparing their interaction in markets to an almost divine invisible hand is a kind of regression because it abandons the notion that markets have to be given the right conditions to work well, a notion implicit in medieval thinking on the subject.

26It is impossible to foretell the exact dynamics of the years to come. However, an important factor is how much and according to which traditions and practices local elites are tied to their citizens, because often the communicative process and the resulting behavior makes the difference. Cfr. Tocqueville, A. “The ancient regime and the French revolution”.

15

Beautiful, the king of France was not willing to tolerate. Even though the king's actions were driven by self-interest to cancel his debts, eliminate an opponent and acquire new sources of income, he operated in a discursive climate which allowed him to legitimate his action on the ground that Christians should not work as moneylenders.

An historically informed development of a socially sustainable but stagnating mature capitalism is obviously no simple endeavor. It could start with the recognition that although some sectors are still developing thanks to technological innovation, we live in an era of social decline which calls for measures untypical for the history of modernity. A new Kondratieff cycle will sooner or later appear, but it is probable that it will not affect social mobility as the earlier cycles did. Recognition should be followed by the development of discourses which bring in the lessons of the past. Such a process could be started with the help of people who are willing to invest in change and give them a visible platform in a mass media environment where discourses of the “There is no alternative” or “We cannot do much because of complexity” type are dominant. Asian competition could be helpful as people observe that other institutional settings are possible27. Eventually, such a discursive climate could enable parts of the elite within politics and finance to redesign Western modernity along sustainable lines.

Conclusions

To summarize, the actual post-industrial crisis paradigm is unstable in the long run. Debt service and beggar-thy-neighbor strategies lead to decline and apathy as social mobility and investment is stagnating. Some countries will do relatively well as they are able to attract investment to secure a high-productive spot in the global supply chain, but others will have to face stagnation and class struggle, as elites focus on extraction and control. This scenario of a disunited West makes a shift of power to Asia more probable and could actually accelerate it. An alternative exit from the postindustrial crisis paradigm would consist in the development of new institutional arrangements which are compatible with a stagnating, but still very rich postindustrial economy. Such a development would mark a break with the neoliberal practices of middle class illusion through debt, stagnation and control typical for the last three decades. It could come about by a new awareness of a part of Western elites, comparable to the action of the Catholic church during the investiture struggle.

27 It might also be possible that a partnership between the USA and China modifies Western political philosophy and action along Confucian lines, according to which it is a duty of the government to act in the interest of its people to avoid tensions.

16

Bibliography

ARTUS, P., VIRARD, M. (2010) Pourquoi il faut partager les revenus : Le seul antidote à l'appauvrissement collectif. Paris : La Découverte.

BECK, U. (2013) German Europe. Cambridge: Polity Press

CROUCH, C. (2004) Post-Democracy. Cambridge: Polity Press

DOERING-MANTEUFFEL, A., RAPHAEL, L. (2010) Nach dem Boom : Perspektiven auf die Zeitgeschichte seit 1970. Goettingen : Vandenhoeck & Ruprecht.

DOERRE, K., LESSENICH, S., ROSA, H. (2009) Soziologie Kapitalismus Kritik : Eine Debatte. Frankfurt am Main : Suhrkamp.

ERBER, G., HAGEMANN, H., SEITER, S. (1998) Zukunftsperspektiven Deutschlands im internationalen Wettbewerb : Industriepolitische Implikationen der Neuen Wachstumstheorie.

FLASSBECK, H. (2007) Das Ende der Massenarbeitslosigkeit : Mit richtiger Wirtschaftspolitik die Zukunft gewinnen. Frankfurt : Westend Verlag.

FLORIDA, R. (2002) The Rise of the Creative Class. And How It's Transforming Work, Leisure and Everyday Life. Basic Books.

GALLINO, L. (2011) Finanzcapitalismo. La civiltà del denaro in crisi: Einaudi

GALLINO, L. (2012) La lotta di classe dopo la lotta di classe : Intervista a cura di Paola Borgna. Roma-Bari : Laterza.

GENEREUX, J. (2006/2011) La dissociété : A la recherche du progrès humain – 1. Paris: Editions du Seuil.

GENEREUX, J. (2009/2011) L'autre société: A la recherche du progrès humain – 2. Paris: Editions du Seuil.

GRAEBER, D. (2011) Debt, the first 5000 years. New York: Melville House Publishing

HOEPNER, M., SCHAEFER, A. (2010) Polanyi in Brussels? Embeddedness and the Three Dimensions of European Economic Integration. MPIfG Discussion Paper 10/8.

HUDSON, M. (2011) Democracy and Debt

http://michael-hudson.com/2011/12/democracy-and-debt/

HUDSON, M. (2011) Europes Transition from Social Democracy to Oligarchy

http://michael-hudson.com/2011/12/europes-transition-from-social-democracy-to-oligarchy/ HUDSON, M. (2012) Incorporating the Rentier sectors into a Financial Model http://michael-hudson.com/2012/09/incorporating-the-rentier-sectors-into-a-financial-model-3/ HUDSON, M. (2012) Financial predators v. Labor, Industry, and Democracy

http://michael-hudson.com/2012/08/financial-predators-v-labor-industry-and-democracy/

17

KAISER, W. (2007) Christian democracy and the origins of the European Union. Cambridge : Cambridge University Press.

KARG, F. (1993) Die Fugger im 16. und 17. Jahrhundert in EICKELMANN, R. (Hrsg.): lautenschlagen lernen und leben. Die Fugger und die Musik – Anton Fugger zum 500. Geburtstag. Augsburg

KEYNES, J. M. (1931/2009) Possibilità economiche per i nostri nipoti. Milano : Adelphi Edizioni.

KIM, J. (2012) How Politics Shaped Modern Banking in Early Modern England: Rethinking the Nature of Representative Democracy, Public Debt, and Modern Banking. MPIfG Discussion Paper 12/11.

KRUGMAN, P. (2012) End this depression now ! New York / London : Norton.

KRUGMAN, P. (2007) The Conscience of a Liberal. New York / London : Norton.

KUMAR, K. (2005) From Post-Industrial to Post-Modern Society : New Theories of the Contemporary World. Oxford : Blackwell Publishing.

NECKEL, S. (2010) Refeudalisierung der Oekonomie: Zum Strukturwandel kapitalistischer Wirtschaft. MPIfG Working Paper 10/6

OTTE, M. (2011) Fermate l'Euro-disastro ! Contro l'oligarchia finanziaria. Milano: Chiarelettere editore.

PERROUX, F. (1961) L'économie du XXe siècle. Paris : Presses Universitaires France.

PERROUX, F. (1970) Aliénation et société industrielle. Paris : Gallimard.

POLANYI, K. (1944/1983) La Grande Transformation : Aux origines politiques et économiques de notre temps. Paris : Gallimard.

RODRIK, D. (2011) The globalization paradox : Why global markets, states, and democracy can't coexist. New York : Oxford University Press.

SCHIMANK, U. (2011) Nur noch Coping: Eine Skizze postheroischer Politik. Zeitschrift fuer Politikwissenschaft, 21. Jahrgang (2011) Heft 3, S. 455-463

SOMBART, W. (1913) Der Bourgeois; zur Geistesgeschichte des modernen Wirtschaftsmenschen. Duncker und Humblot http://archive.org/details/derbourgeoiszurg00sombuoft

SPENCE, A. M. (2011). The Next Convergence: The Future of Economic Growth in a Multispeed World. New York: Farrar, Straus and Giroux.

SPENCE, A. M. (2012). Tradable prosperity. Project Syndicate. http://www.projectsyndicate.org/print/tradable-prosperity

STREECK, W. (2011) The Crisis in Context: Democratic Capitalism and Its Contradictions. MPIfG Discussion Paper 11/15.

VEBLEN, T. (1904) The theory of Business Enterprise. New Brunswick, New Jersey

18

http://socserv2.mcmaster.ca/~econ/ugcm/3ll3/veblen/busent/index.html

VEBLEN, T. (1915) The Theory of the Leisure class: An economic study of institutions. Macmillan, New York http://www.gutenberg.org/files/833/833-h/833-h.htm

WEBER, M. (1896) Die sozialen Gruende des Untergangs der antiken Kultur in WEBER, M. (1988) Gesammelte Aufsätze zur Sozial- und Wirtschaftsgeschichte. Hrsg. von Marianne Weber. 2. Auflage, Tübingen: J. C. B. Mohr (Paul Siebeck), http://www.zeno.org/Soziologie/M/Weber, +Max/Schriften+zur+Sozial-+und+Wirtschaftsgeschichte/Die+sozialen+Gr %C3%BCnde+des+Untergangs+der+antiken+Kultur

19