Healthcare

Pharma

Life Sciences

Veterinary

Social Care

Sector Insights

BARCELONA | BRUSSELS | DUSSELDORF | HAMBURG | LISBON | LONDON | MADRID | MUNICH | PARIS

HELP BUY, SELL AND CREATE VALUE IN BUSINESSES mansfieldadvisors.com

WE

4

Contents

8

Healthcare Insights

Location, location, location...

The supply-side market forces that drive location selection and the patterns created in the retail pharmacy, veterinary and private medicine sectors

Adam Scott and Ty Lantz

Roll up, roll up to HCIT investing

Private equity healthcare IT deals slowed in 2023, but add-ons have continued to grow

Adam Scott and Johan Ottosson

Pharma Insights

Female pharmaceutical gaining prominence

Examining opportunities for pharmaceuticals in women’s health

Penny Sherlock and Adam Scott

Life Science Insights

14

19

24

30

32

38

44

Quality matters - a closer inspection of the CQC

The CQC has moved to a system of more targeted inspections ‒ what are the implications for investors?

Abhishek Patel

Managed markets

Comparing the German and UK private hospital sectors

Arne Berndt and Paul Fegan

Investors show strong interest in ophthalmic product space

Deals in the surgical ophthalmic equipment and products market reached a record high in 2022, with PE backed transactions also attaining new highs

Johan Ottosson and Dr Victor Chua

Prospects for private investment in Spanish and British hospitals

Spanish and British health services are remarkably similar, but where the countries differ is the scale and scope of private hospitals

Paul Fegan and Henry Elphick

Scanning the opportunities

Increasing diagnostics capacity is key to driving down waiting times in the NHS. But despite claims of success, imaging remains surprisingly constrained

Tom Atherton and Adam Scott

NHS waiting lists - behind the headlines

Waiting lists are likely to be a key factor in the next General Election and there is renewed government focus on reducing them

Adam Scott and Ali Bahram

Is there wisdom in investing in European Dentistry?

Examining the state of dentistry across the UK and larger European countries and delving into some of the big trends affecting dentistry everywhere

Ty Lantz and Stephanie Yeung

Investing in non-theapeutic antibodies

Where are the trends in the non-therapeutic antibodies market and how can investors create value?

Victor Chua and Will Johnson

Veterinary Insights

No chicken feed

The global animal feed market is growing faster than the population at 4%. We consider the growing importance of this market

Arabella Zuckerman and Adam Scott

US veterinary consolidation - a land of opportunity

In 1987, VCA Animal Hospitals acquired its first independently owned companion animal clinic, sparking the beginning of a consolidation process

Freddie Evans and Adam Scott

Social Care Insights

Fostering - a brave new world

Where next for independent fostering agencies and yhy there is room for optimism

Paul Fegan and Henry Elphick

Breaking the cycle

We need to attract more people into social care and, importantly, retain them. What can be done to possibly transform the profession?

Paul Fegan and Ty Lantz

Leading the way

When it comes to care home construction in England, who is building what, where and for whom?

Johan Ottosson and Henry Elphick

48

52

58

64

69

75

79

Sector Insights | 3 To keep up to date with Mansfield Advisor's Insight features visit www.mansfieldadvisors.com/insights/

Every sector in health and care has its own nuances. However, in all of them, location is critical all the way down from the broad national level to individual site selection. Regarding site selection, when speaking to a real estate advisor, one might hear ‘many things matter and the first three are location, location, and location’. But, at Mansfield, we are strategy advisors so what does it mean to be strategic about site selection for healthcare businesses?

The topic comes up in several contexts:

• Market entry which are the best markets to enter, and where within a market should one operate?

• Portfolio analysis how can we optimally meet the needs of our customers? How are individual sites performing relative to the suitability of their locations? Which sites should be combined or split?

• Mergers and acquisitions how do two companies fit together? Are the locations complementary or is there risk of cannibalisation? Should the merged portfolio be rationalised?

Location, location, location…

• Roll-up runway what are the limiting factors of consolidation? How much further can the industry or any individual company go?

In healthcare services, location selection typically hinges on four dimensions: supply, demand, funding, and access to staff. The importance and scope of each varies by sub-sector, and many industry veterans will have an intuition for finding good locations, but often the interaction of variables is complex.

For example, care home operators targeting the private-pay market might locate in affluent areas with an aging population, but staff costs can be 60% or more of revenue and many workers rely on public transportation. Care homes with few nearby transit links can go understaffed, become reliant on locum workers, and fall out of profitability quickly.

We recently encountered a care home positioned a 10-minute walk up a steep hill from the nearest bus station. This walk was so troublesome that the operator had tried hiring a private driver and aligning shifts with the bus schedule, and they eventually bought a van to shuttle employees to and from the station. The lesson is,

in care homes, access to staff is so key to profitability that well-connected homes near the boundaries between affluent and less-affluent areas often perform best.

One can develop heuristics like this via long years in industry, by speaking with experts, or via examining large portfolios to discover what works. However, even the savvy industry vet can learn something from intense data interrogation, and the application of geographical and social sciences, and advances in computing allow us to explain and discover location phenomena that drive access to care and sustainable growth.

Forces

Imagine a sunny Spanish beach in Menorca or Ibiza (you decide). The beach is butted on both ends by cliffs, and a boardwalk runs parallel to the sea. Two entrepreneurs, who are competitors, decide to sell sunscreen from rolling carts to the beachgoers who are distributed evenly along the beach. The competitors are the only sellers on the beach. Where do they choose to put their carts?

In the simplest case, if they both position themselves equidistant from the

4 | Sector Insights Healthcare Insights

Adam Scott and Ty Lantz explore some of the supply-side market forces that drive location selection and the patterns that they create in the retail pharmacy, veterinary, and private medicine sectors

ends, anywhere along the beach, they share the market evenly. Regardless of the initial configuration, eventually one of the sellers will realise that moving either toward the other or the centre will gain him or her incremental market share. The other seller will react in turn by moving similarly, and so it goes until the carts are next to one another at the midpoint.

Once there, the sellers reach a state of a Nash equilibrium, named after the mathematician John Nash, in which a unilateral move away from the midpoint would cost the mover market share. This scenario is described by Hotelling’s law and is one of the reasons you might see competitors like Starbucks and Pret a Manger sharing street corners.

Now imagine the beach is very long and the tourists prefer not to walk long distances for sunscreen. If the sellers recognise that the tourists bear search costs, a different configuration will arise.

The carts will distance themselves, and each seller will be able to charge a premium up to the cost a tourist bears by walking all the way to the other cart. If the sellers get particularly wise, they may also realise that they can further change the ‘distance’ to the next cart by offering differentiated products. In this case, a buyer’s preference for a product may offset some of the burden of a far walk and win the seller with preferred products additional share. This phenomenon was first discussed by economists Edward Hastings Chamberlin and Joan Robinson and is known as monopolistic competition because the sellers remain in competition despite having small local monopolies.

One may experience this market force when comparing prices between corner stores and supermarkets. In most cases, a shopper chooses the corner store for convenience so shop owners charge inflated prices for late-night snacks.

Let’s add yet another kernel of reality to the situation: imagine the sellers bear greater transportation and delivery costs the further they distance themselves from the beach access point. With this constraint, the sellers would place themselves at the points that balance the benefits and costs of distance. If the costs are significant, the sellers may end up next to each other once more. The sellers may even benefit from overall lower delivery costs because the other is nearby. In the field of urban economics, this network effect is called the agglomeration effect,

which posits that businesses can profit from returns to scale not only as a single competitor grows but also as an industry within a region scales – perhaps without any single competitor growing.

In the classical theory, the benefits come from transportation costs, labour availability, and knowledge distribution. As a knock-on effect of agglomeration, some regions become famous for particular goods or services and companies can benefit from the signalling they are there. Examples include old-world tailors on Savile Row in London and new-world tech companies in Silicon Valley.

IN MOST CASES, A SHOPPER CHOOSES THE CORNER STORE FOR CONVENIENCE SO SHOP OWNERS CHARGE INFLATED PRICES FOR LATE-NIGHT SNACKS

Thinking more broadly about network effects in location strategy, one may also consider the presence of participants in other industries. For instance, restaurants, coffee shops, and clothing retailers thrive in areas with high foot traffic and are often seen together because they benefit from the presence of customers drawn by the other types of stores.

So how does this work in real-life healthcare sectors?

Patterns

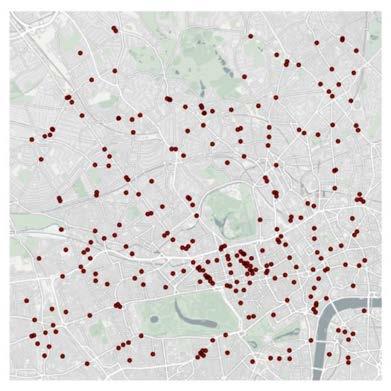

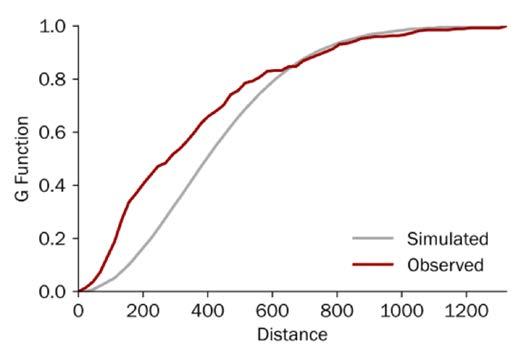

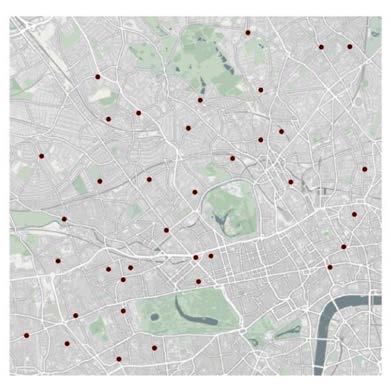

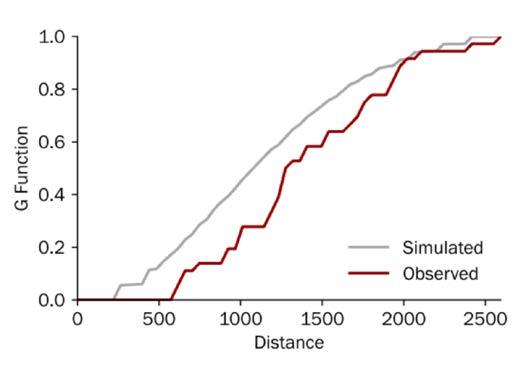

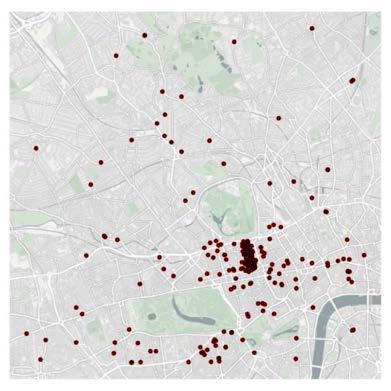

In the accompanying figures we examine the distribution of competitors in three healthcare industries, retail pharmacy, veterinary, and private medicine across a portion of London.

In the cases of veterinary clinics (see Figure Two) and private medical offices (see Figure Three), a visual inspection of each map can provide some quick insights. However, in the case of retail pharmacies (see Figure One), the pattern is more ambiguous.

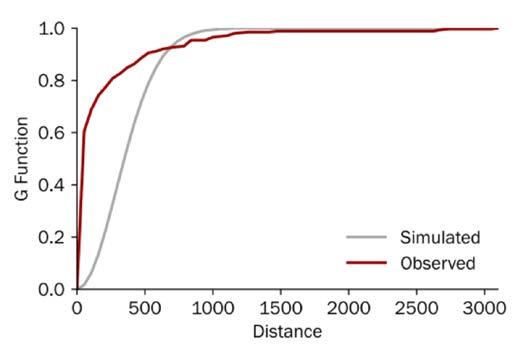

In general, humans are surprisingly bad at discerning patterns from randomness,1 so we lean on statistical approaches to identify and measure patterns. In this case, we use an analysis called Ripley’s G, which allows us to measure the level of clustering or dispersion for a range of sizes of ‘neighbourhood’ by measuring the proportion of locations whose nearest neighbour (think competitor) is within a given range. We then compare the observed distribution with a set of simulated random patterns: observed curves above the simulated curve exhibit clustering and curves below the simulated curve exhibit dispersion.

Retail pharmacies

Retail pharmacy is a relatively undifferentiated industry, so the sector mostly follows Hotelling’s Law: chemists are often best off on high streets, where there is the most foot traffic, and they split the local market with co-located competitors. While the distribution of pharmacies around London may visually appear random, nearly all have a competitor within a very short walking distance (see Figure One).

The line graph demonstrates that chemists are more often very close to one another than they would be under a random process (c.40% have another store within 200m), so the industry is exhibiting Hotelling-like features.

Chemists are primarily fixed cost businesses, and sites can usually move within a few hundred metres without a change of license, so being subtle about exactly where the pharmacy is on the high street can be quite impactful.

Furthermore, because competitors are piled onto the same street, there is opportunity to extend the ‘virtual distance’ by investing in the environment or improving the service level to lure customers the

Sector Insights | 5

RETAIL PHARMACIES

50 metres past competitors to a nicer experience.

Revisiting the chart, interestingly, the observed distribution mimics the random one in some cases, which indicates that there are some pharmacies that unexpectedly sit further apart from others. These more isolated locations may be on quieter streets with differentiated offerings, or they may be on streets with a supply/demand mismatch.

Veterinary clinics

In contrast to pharmacies, and the simulated distribution, veterinary practices are particularly dispersed (see Figure Two). In fact, in this region, no first-opinion practice has another one within 575

VETERINARY CLINICS

metre as the crow flies, an approximately 12-minute walk.

In our own research, we found that proximity is the number one reason for choosing a first-opinion clinic and it ranked well above perceived value, which means that customers want convenience, and the market is likely exhibiting monopolistic competition.

Importantly, this does not mean that veterinarians are exerting excess market power, it just means that customers are willing to pay for convenience and for many customers their nearest practice is a bit closer than others. On the contrary, we have also found that pet owners are perfectly willing to travel for differentiated services, for instance specialist care.

On the other hand, one could also argue that general practice vets are distributed in urban areas because the purchasing decision is driven so much by proximity, the distances people are willing to travel are small, and the population density is generally low enough that there is only enough demand to support one practice within the range that pet owners are willing to travel. In either case, we primarily find veterinary clinics on quiet residential streets because vet clinics are actually damaged by an over-abundance of nearby activity – no one wants to walk their sick puppy through a crowded street – which is why there are no practices in the busiest parts of town (the gap near the centre and bottom of the map).

6 | Sector Insights Healthcare Insights

SOURCE MANSFIELD ANALYSIS

FIGURE ONE

FIGURE TWO

SOURCE MANSFIELD ANALYSIS

Now that we know the typical distribution of practices, we can programmatically scour similar areas around the country to identify gaps in supply that could be attractive places to build new practices.

While dispersion among veterinary clinics benefits many pet owners, dispersion among hospitals would benefit much of society.

Emergency care is, tautologically, urgent, and universal access is in the mandate of state-sponsored care. However, as one can discern from cursory analysis of NHS Acute Trust catchment populations, services are not optimally located, and this is due to the constraints of the built environment.

Veterinarians can open, close, and move clinics with ease, which allows market forces to promote an optimal configuration, but hospitals are huge and have important infrastructure requirements, which makes their location subject to path dependence, and the equality of an arrangement of services erodes as people and needs move.

Private medical offices

Finally, private medical practices are intensely clustered, mostly around Harley Street, which has been a hub for private practitioners since the end of the 19th century.

In earlier years, the benefits of the agglomeration effect (knowledge sharing and so on) were likely more powerful than they

BUILDING MODELS THAT EFFECTIVELY EVALUATE WHETHER A LOCATION IS SUITABLE FOR A BUSINESS IS BOTH A COMMERCIAL AND ACADEMIC PROCESS

are today, but most practices on Harley Street are single-specialty or few-specialty groups and they benefit from the ability to refer patients to nearby practices.

Probably the greatest benefit of being on Harley Street today is the economic signal: most people in London assume that the best private doctors practice there. In addition to hefty lease payments, Harley Street doctors garner prestige from their choice of location.

Economics professors would argue that much of the signal comes from the high rents – the ability to afford the space means those doctors must create significant value for their patients. Anyone wanting to establish a premium brand would struggle to find a better place than Harley Street for a flagship clinic. Moving up a level, spontaneously creating these types of networks is very difficult, but local government, property estates, and landlords play a very important role in either limiting or fostering their development.

So, where next?

We have examined some phenomena and how we measure them, and you might be thinking this is all a bit academic. But building models that effectively evaluate whether a location is suitable for a business is both a commercial and an academic process. Much like in the beach example, we iteratively layer-in reality and theory and then test outputs using statistical methods. This requires deep understanding of how a market works, what makes a location good for a particular business, and the academic approaches to identify and quantify market opportunities.

NOTES

1 Williams, Joseph Jay and Thomas L. Griffiths. Why are People Bad at Detecting Randomness? Because it is Hard. (2008), princeton.edu.

Sector Insights | 7

SOURCE MANSFIELD ANALYSIS

THREE

MEDICAL OFFICES

FIGURE

PRIVATE

Roll-up, roll-up to HCIT investing

Riding the Covid-19 wave, PE healthcare IT (HCIT) deals, including buyouts, add-ons, and growth investments, grew by a record CAGR of 18.6% between 2019 and 2021. That level of exuberance has slowed in 2023, but the run-rate for addons continues to grow and this year is set to become the second most active for such transactions in the past decade.

Recent deals have included CVC Capital Partners’ acquisition of UK-based System C Healthcare and its partner company Graphnet Health in 2021 (HCIT systems and services), ARCHIMED’s acquisition of Italy-based Cardioline in 2021 (cardiology diagnostics and cardiology-focused telemedicine), and Hg and TA Associates backed The Access Group acquisition of UK-based Servelec in 2021 (provider of healthcare and case management software, which the previous month had acquired Elemental, the most widely used digital social prescribing platform in the UK and Ireland).

We believe the HCIT space offers an attractive theme for investors combining defensive (healthcare) with growth assets (tech) and offering strong customer stickiness and attractive recurring revenue streams. We forecast the market to grow, driven by system pressures and new models of care delivery, underpenetrated markets, and strong public funding tailwinds.

Investors should focus on rolling-up solutions that are geared towards clearly defined and prioritised problems that can easily integrate into existing HCIT landscapes, and that offer high security standards. To pick the right assets, investors will need to really understand the clinical and patient models of markets in which target assets operate.

Broad landscape

There is an ever-increasing number of digital health solutions, also covering apps and wearables, but we will focus on second generation technology in the care provider setting as this is a more mature market and hence more relevant for private equity (PE) investors. These assets include solutions for decision/risk analysis, enterprise system management, Electronic Health Records/Electronic Patient Records (EHR/EPR), outcome management, telehealth solutions, and other related HCIT services (see Figure One).

Grand View Research valued the European digital health market at US$45.3bn in 2022, expecting it to grow at a CAGR of 16.0% from 2023 to reach US$148.5bn by 2030.1

In the UK, LaingBuisson estimates that HCIT spend in 2020 was £5bn (US$6.33bn), of which c.33% went on clinical systems, c.30% to staffing and workforce, c.20% on infrastructure spending (e.g. hardware, networks), c.15% went on non-clinical systems (e.g. HR, finance, governance), and c.2% on so-called third generation technology (e.g. apps, patient facing services).2

Three players dominate the UK market with a combined c.40% to c.60% of the Electronic Prescribing and Medicines Administration (ePMA), EHR/EPR, and Patient Administration Systems (PAS) markets: Italy-based Dedalus (backed by Ardian), US-based Cerner (acquired by Oracle in 2022), and UK-based System C (backed by CVC Capital Partners). These markets differ slightly, however, in terms of exact make-up and who leads.

Remaining larger players in these markets tend to be US-based, and often listed. UK-based and privately held Nervecentre is a notable exception in the UK EHR/EPR market - the company has recently been chosen as the preferred

supplier for a new joint EPR system by two Derbyshire trusts.3

Some trusts have also constructed their own EHR/EPRs (c.8.3% or the market in England in 2022) and 10% of acute Trusts in England lack an EHR/EPR altogether. Further, c.30% lack an ePMA system, and c.50% lack a digital document management system.4,5,6

Record growth in Europe during pandemic

PE HCIT deals in Europe grew by a record CAGR of 18.6% between 2019 and 2021 (see Figure Two) and grew faster than PE deals overall (4.3% CAGR). HCIT deals as a percentage of the total also reached alltime highs of 1.5% in 2021 and 2022, and 1.6% in (year-to-date) 2023.

Although there has been a slowdown in the number of completed deals in the first three quarters of 2023 (see Figure Three), reaching its lowest point since Q3 2020. The current year is still positioned to be a strong year for HCIT.

For HCIT companies relying heavily on growth, inflation can diminish the value of future returns, especially for companies with lower pricing power. Inflation, coupled with a high interest rate environment impacting investor willingness to pay, has resulted in a decrease in both buyout and growth investment deals. Hence, Livingbridge’s investment in T-Pro (AI-powered speech technology and clinical documentation solutions) is the only growth investment in 2023 YTD. This is compared to five growth deals in 2022 and 2020, and three in 2021.

Add-ons have also been impacted, with the number of deals falling both in Q2 and Q3 this year, but these transactions remain at similar levels per quarter as registered in 2022.

8 | Sector Insights Healthcare Insights

in 2023,

Private

equity healthcare IT deals slowed

but add-ons continued to grow, say Adam Scott and Johan Ottosson, who look at the rationale for investing in the sector

FIGURE ONE THE HEALTHCARE IT LANDSCAPE IN CARE PROVISION SETTINGS

Article focus

Setting

Main industry specific systems (nonexhaustive)

Supporting industry agnostic systems

Care provider Setting

Clinical systems

• Screening and diagnostics

• Telehealth

• Electronic Patient Records Systems (EPR/EMR/EHR)

• Picture Archive and Communication System (PACS), and Radiology Information System (RIS)

• Electronic Prescribing and Medicines Administration (ePMA)

• Patient Administration Systems (PAS)

Non-clinical systems

• Workforce management

• Facilities and supply chain management

• Regulatory and legal

• Contract management

Homecare setting

Communication and patient engagement systems

• Patient portals

• Referral pathways

Platform and infrastructure

Analytics

Other support systems

Remote and self-care systems

• Apps

• ‘Doctor on demand’ services

• Home monitoring

• Social prescribing

Run-rating all deals in 2023, this year is still positioned to be the third most active for PE HCIT deals since 2014 illustrating that investor interest remains strong.

The UK: Europe’s largest HCIT deal market

Some 29.3% of all PE HCIT deals since 2014 have involved British assets, making it the most active market in Europe. The UK is followed by Germany (16.6%), and the Netherlands (12.7%)

Recent PE buyouts of UK HCIT assets include CVC Capital Partners’ acquisition of System C in 2021, Ardian backed Dedalus’ acquisition of swiftQueue Technologies in 2021 (healthcare appointment and patient engagement solutions), and Livingbridge’s acquisition of Nourish Care Systems in 2022 (digital care planning software).

Investor landscape consolidating

The investor landscape is very fragmented, with c.66% of HCIT investors having only completed one deal, and c. 18% only two deals in the past decade.7

There have, however, been examples of PE asset roll-ups, with HCIT add-ons growing more than both buyouts and growth investments in the past ten years. A prominent example is RLDatix, a UK-based company that develops and supplies risk management and patient safety software (see Figure Six).

Since TA Associates invested in RLDatix in 2018, joining existing investor Five Arrows Principal Investments, the software company has proceeded to roll up multiple other healthcare software businesses in the UK and the USA. These include Verge Solutions in 2020 (credentialing software), Allocate in 2021 (human capital management solutions), and

Galen Healthcare Solutions in 2022 (implementation, optimisation, data migration and archival solutions for HCIT systems provider).

Another example is Ardian backed Dedalus, which acquired Agfa HealthCare’s IT business in 2019 (healthcare information solutions and integrated care activities) as well as Dosing GmbH (SaaS medication safety solutions) and swiftQueue Technologies, both in 2021.

HCIT roll-ups makes sense to investors as it represents a shortcut to expanding an asset’s offering; it can offer salesforce synergies and economies of scale.

According to Martin Bell, a former board CIO in the NHS, the former deputy MD of EMIS Health, and the author of the LaingBuisson Digital Health UK market report, private equity is particularly well suited for these roll-up plays.

‘Especially medium to large sized companies can benefit from PE roll-ups. These companies often have quite a few bits

Sector Insights | 9

SYSTEMS WILL EXIST ACROSS ALL CARE SETTINGS. MAPPING EXCLUDES PHARMA, MEDTECH, GOVERNMENT AND RESEARCH

MANSFIELD ANALYSIS

NOTE NOT ALL

SOURCE

B2B

HEALTHCARE IT LANDSCAPE TARGETING THE CARE PROVIDER SETTING COVERS A BROAD RANGE

SERVICE

B2B2C THE

OF

FIGURE TWO GLOBAL PE HEALTHCARE IT DEALS ‒ ANNUAL

AFTER A SHARP INCREASE IN PE HEALTHCARE IT DEALS POST-COVID WE ARE NOW SEEING A SLOWDOWN NUMBER OF COMPLETED DEALS, EUROPE, 2014‒2023 YTD

WE ARE SEEING A STEADY DECLINE IN THE FIRST THREE QUARTERS OF 2023 NUMBER OF COMPLETED DEALS, EUROPE, PER QUARTER YTD

10 | Sector Insights Healthcare Insights NOTE HEALTHCARE IT ASSETS ARE DEFINED AS COMPANIES ENGAGED IN PROVIDING SOFTWARE OR TECHNOLOGY PLATFORMS TO THE HEALTHCARE INDUSTRY. THESE INCLUDE SOLUTIONS FOR DECISION/RISK ANALYSIS, ENTERPRISE SYSTEM MANAGEMENT, MEDICAL RECORD SYSTEM MANAGEMENT, OUTCOME MANAGEMENT, AND OTHER RELATED HEALTHCARE INFORMATION TECHNOLOGY SERVICES. 2023E RUN RATE SOURCE PREQIN – DATA UNTIL 30 SEPTEMBER 2023, MANSFIELD RESEARCH AND ANALYSIS 12 8 10 10 14 11 5 17 16 9 1 4 5 5 10 5 3 5 2 7 7 11 23 14 17 0 5 10 15 20 25 30 35 40 45 15 12 19 16 26 21 ‘14 43 35 27 2 1 ‘15 ‘16 1 ‘17 ‘18 ‘19 ‘20 ‘21 ‘22 ‘23E 21 Total CAGR ’14-’19 38.0% -1.7% 7.0% ’19-’22 ’19-’23E Buyout PE deals total across all industries Growth Add-on Run rate PE Healthcare IT deals as % of total deals 1.6% 1.5% 1.5% 1.0% 1.0% 1.1% 0.7% 1.0% 0.7% 1.0% -100% 14.7% -4.0% 7.5% N/A 11.9% 13.3% 18.6% N/A Covid-19

6 1 2 2 4 1 1 3 5 5 1 6 5 6 3 2 2 2 3 6 4 2 1 3 5 1 2 6 4 3 4 1 1 7 1 2 1 5 8 5 2 3 4 ‘19 Q2 ‘19 Q3 ‘19 Q4 ‘20 Q1 ‘20 Q2 ‘20 Q3 ‘20 Q4 ‘21 Q1 ‘21 Q2 ‘21 Q3 ‘21 Q4 ‘22 Q1 ‘22 Q2 ‘22 Q3 ‘22 Q4 ‘23 Q1 ‘23 Q2 ‘19 Q1 8 6 6 3 4 8 11 15 7 10 13 10 6 6 9 7 5 ‘23 Q3 Buyout Growth Add-on

FIGURE THREE GLOBAL PE HEALTHCARE IT DEALS ‒ QUARTERLY

missing that can’t be filled by third parties who may or may not be out there. It makes the cost of operations, partnerships, delivery operations so much higher. The ability to acquire add-ons and integrate them is what PE is good at. It’s a consolidation play.’

Conversely, some providers may be too small to succeed on their own ‒ for instance lacking the salesforce or capabilities needed to compete in larger tenders ‒ and will therefore benefit from the scale offered by a consolidator.

Profitable drivers to fuel growth

System pressures and new models

Demographic changes and staff shortages have led to significant pressures on healthcare systems, which have often been made worse by the pandemic and subsequent backlogs. Care providers therefore need to find efficiencies, something that digitalisation can offer.

Models of care delivery are also changing, and patients will have a growing want and need for data accessibility to support care provision outside of, but linked to, a hospital setting.

Consequently, the volume of healthcare data has been growing rapidly, with RBC Capital Markets projecting a CAGR of 36% in global healthcare data until 2025.8 With increasing volumes, however, there is a greater need to store, transfer, and process this data. Here HCIT solutions play an important role.

Underpenetrated markets

The percentage of clinicians using digital technologies varies significantly between European countries. In a 2020 Deloitte survey, 97% of Dutch clinicians reported using EHRs, versus 77% of German clinicians, and 69% of Italian clinicians. Similarly, digital prescription was used by 97% of Dutch clinicians, versus 73% or Danish clinicians, and only 13% of German clinicians.9 Further, 10% of acute Trusts in England lack an EPR, and 30% lack an ePMA system.10

These disparities should provide significant headroom for HCIT companies to grow.

Funding tailwinds across Europe

As the largest healthcare market outside of the US, Germany launched The German Hospital Future Act (KHZG) in 2020, making €4.3bn in funding available for investments into patient portals, electronic documentation of care and treatment services, digital medication management, and the introduction or improvement of telemedicine.11

In France, the Ségurdudigitalensanté programme, also launched in 2020, includes a €2bn (US$2.18bn) investment into development of digital health. The programme’s objective is to ensure the smooth and secure exchange of health data between health professionals and users.12

At the European level, the EU has committed €1bn towards digitalising healthcare over the coming seven years. This includes the creation of the European Health Data Space (EHDS), which among

Sector Insights | 11

NOTE HEALTHCARE IT ASSETS ARE DEFINED AS COMPANIES ENGAGED IN PROVIDING SOFTWARE OR TECHNOLOGY PLATFORMS TO THE HEALTHCARE INDUSTRY. THESE INCLUDE SOLUTIONS FOR DECISION/RISK ANALYSIS, ENTERPRISE SYSTEM MANAGEMENT, MEDICAL RECORD SYSTEM MANAGEMENT, OUTCOME MANAGEMENT, AND OTHER RELATED HEALTHCARE INFORMATION TECHNOLOGY SERVICES. 2023E RUN RATE SOURCE PREQIN – DATA UNTIL 30 SEPTEMBER 2023, MANSFIELD RESEARCH AND ANALYSIS 3 6 5 7 8 6 16 12 2 1 1 7 4 3 6 7 5 3 1 5 1 4 3 8 2 2 3 1 2 2 3 2 2 4 3 1 1 1 2 1 1 2 1 1 3 3 8 4 8 6 7 11 8 ‘14 ‘15 2 ‘16 2 ‘18 ‘21 2 2 ‘19 ‘22 2 ‘20 ‘17 ‘23 YTD 15 12 19 16 26 21 21 43 35 21 Covid-19 29 3% 16.6% 12 7% 10 5% 26 2% 4 8% UK Germany Netherlands France Spain

UK BASED ASSETS ARE THE MOST TRADED ONES NUMBER OF COMPLETED DEALS, EUROPE, 2014-2023 YTD FIGURE FOUR TARGET COUNTRIES

Other UK Germany Netherlands France Spain Other

THE INVESTOR LANDSCAPE IS FRAGMENTED, WITH c.66% OF HCIT INVESTORS HAVING ONLY COMPLETED ONE DEAL NUMBER OF COMPLETED DEALS, EUROPE, 2014-2023 YTD

Acc. Deals

other things, aims to digitise all medical records in the bloc by 2025, making it easier for individuals to access and share their data with medical professionals, particularly when in another EU country.13,14

In England, the Frontline Digitisation programme, launched by NHS England (NHSE) and the government in 2021, set a target that 90% of acute NHS trusts would have EPRs by December 2023. This was achieved in mid-November 2023. The remainder are to follow by March 2025.15,16,17,18

However, a NHSE guidance letter sent to trusts in November 2023 suggested that parts of the Frontline Digitisation programme could be pulled from all but the least digitised trusts to counter the impact of strike action. The programme had already been reduced from £2.6bn to £2bn in FY23.19

Funding will likely remain one of the key growth challenges in England. Hence, although 2020 digital health spending represented on average c.2% of NHS Acute Trust turnover (up from the c.1.4% a decade ago), this is significantly below, for instance, the Nordics at an estimated c.6‒8%.20

Focus for investors

Clearly defined and prioritised problems

For HCIT solutions to be attractive investments, they need to be geared towards clearly defined problems, and ideally, should prove either substantial risk mitigation or improved patient outcome, improved efficiency and cost reduction, revenue increase (preferably in-year if targeting public sector clients), and/or enhanced clinician experience.

Solving a problem is not enough, however, as healthcare providers will often have constrained budgets and will need to prioritise their spending.

‘If you’re selling something that has ringfenced specific funding, and if it’s really fixing an urgent thing, then you can get traction,’ says Bell.

Further, solutions, unless stand-alone, also need to easily integrate into the end users’ existing technology landscape, the broader organisational structure and ecosystem, and existing care pathways (both digital and physical).

Finally, solutions need to have high security standards (both cyber security and patient data compliance).

Proven growth track record

Healthcare providers are typically risk averse when it comes to changing systems and will want to see robust evidence of safety and efficacy before adopting a new system; changing systems requires a lot of effort in what are often strained organisations.

‘The reason for stickiness is multifactorial,’ says Bell. ‘One of the biggest things is the amount of effort required - write a business case and go through procurement - while you have so many other priorities as a healthcare provider.’

This slow pace of technological adoption and long sales cycles/adoption means that investors sometimes find it hard to validate returns. Companies with a track-record of growth ‒ by either displacing competition or growing accounts ‒ and that have long customer relationships and can show surviving evaluation cycles, should provide attractive targets for HCIT investors.

Roll-up recommendation

Roll-ups enable investors to rapidly build their capabilities: gaining clear salesforce synergies and the possibility to provide scale to smaller assets.

Investors must consider the local conditions of markets in which the target assets operate. This includes understanding diverse and often fragmented commissioning landscapes, regulatory variations by region and country, clinical and patient models (such as patient access to care and patient pathways), interoperability challenges, and privacy and data security concerns (mainly regulatory limitations, but sometimes also cultural perceptions). Though not all these challenges will be specific to HCIT, these can significantly limit the scalability of HCIT.

Conclusion

There has been a lot of investor interest in the HCIT space in recent years, and we expect that to continue.

Favourable market drivers and strong funding tailwinds, coupled by underpenetrated markets leaving headroom for growth, make the HCIT space an attractive theme for investors. Interested investors should focus their attention on solutions geared towards clearly defined, and prioritised problems, and roll up assets with a proven track record of growth.

12 | Sector Insights Healthcare Insights

ANALYSIS 4 deals 6 deals 2 deals 50% % of total deals # of deals 100%

of deals per investor

SOURCE

PREQIN – DATA UNTIL 30 SEPTEMBER 2023, MANSFIELD RESEARCH AND

Number

FIGURE FIVE HEALTHCARE IT DEALS INVESTORS

FIGURE SIX

RLDATIX HAS ROLLED UP MULTIPLE HCIT COMPANIES IN THE UK AND US CASE

SELECTION TA Associates invests in Datix Five Arrows Principal Investments, an existing investor, maintains a significant equity stake in Datix Datix acquires RL Solutions, a provider of healthcare quality and patient safety software and rebrands to RLDatix

RLDatix acquires Verge Health, a US based provider of credentialing software for healthcare sector

NOTE 2018 2018 2020 2021

RLDatix based provider of contract management solutions for healthcare, insurance, life sciences and other industries RLDatix acquires Galen Healthcare Solutions, a US-based implementation, optimisation, data migration and archival solutions for HIT systems provider

2022 2021

NOTES

1 Grand View Research - Europe Digital Health Market Size, Share & Trends Analysis Report By Technology (Tele-healthcare, mHealth, Healthcare Analytics, Digital Health Systems), By Component, By Region, And Segment Forecasts, 2023‒2030 - Press release

2 Digital Health UK market report – third edition, LaingBuisson

3 DigitalHealth.Net (3 November 2023): Two Derbyshire trusts pick Nervecentre as preferred supplier for joint EPR. Available at: https:// www.digitalhealth.net/2023/11/two-derbyshire-trusts-pick-nervecentre-as-preferredsupplier-for-joint-epr/#:c. :text=for%20joint%20 EPR-,Two%20Derbyshire%20trusts%20 pick%20Nervecentre%20as%20preferred%20 supplier%20for%20joint,patient%20record%20 (EPR)%20system. (accessed 27 November 2023)

4 Digital Health UK market report – third edition, LaingBuisson

5 Mansfield interview

6 NHS Digital (16 November 2023): 90% of NHS trusts now have electronic patient records. Available at: https://digital.nhs.uk/ news/2023/90-of-nhs-trusts-now-have-electronic-patient-records (accessed 21 November 2023)

7 Preqin

8 RBC Capital Markets: The healthcare data explosion. Available at: https://www.rbccm. com/en/gib/healthcare/episode/the_healthcare_data_explosion#:c. :text=Today%2C%20

ONLY SOURCE PREQIN – DATA UNTIL 30 SEPTEMBER 2023, MANSFIELD RESEARCH RLDatix acquires Allocate Software, a UK based provider of human capital management solutions for the healthcare sector

approximately%2030%25%20of%20the,for%20healthcare%20will%20reach%20 36%25.https://emerj.com/ai-sector-overviews/ where-healthcares-big-data-actually-comesfrom/ (accessed 20 November 2023)

9 Deloitte (September 2020): Digital transformation: Shaping the future of European Healthcare. Available at: https://www2.deloitte. com/content/dam/Deloitte/uk/Documents/lifesciences-health-care/deloitte-uk-shaping-thefuture-of-european-healthcare.pdf (accessed 16 November 2023)

10 Digital Health UK market report – third edition, LaingBuisson

11 Healthcare IT News (22 September 2020): German hospitals to get €3 billion funding boost for digitalisation. Available at: https:// www.healthcareitnews.com/news/emea/german-hospitals-get-3-billion-funding-boost-digitalisation (accessed 20 November 2023)

12 Ministry of Solidarites and Health (Ministère de la Santé et de la Prévention): Le Ségur du numérique en santé. Available at: https:// esante.gouv.fr/segur (accessed 16 November 2023)

13 Healthcare IT News (8 June 2023): European healthcare digitalisation at inflection point. Available at: https://www.healthcareitnews. com/news/emea/european-healthcare-digitalisation-inflection-point (accessed 16 November 2023)

14 European Commission: European Health Data Space. Available at: https://health. ec.europa.eu/ehealth-digital-health-and-care/

european-health-data-space_en (accessed 17 November 2023)

15 NHS England: Digitising the frontline. Available at: https://transform.england.nhs.uk/ digitise-connect-transform/digitising-the-frontline/ (accessed 21 November 2023)

16 NHS South, Central and West (SCW): Frontline digitisation programme supports ambitious Electronic Patient Records targets. Available at: https://www.scwcsu.nhs.uk/case-studies/ frontline-digitisation-programme-supports-ambitious-electronic-patient-records-targets (accessed 21 November 2023)

17 NHS Digital (16 November 2023): 90% of NHS trusts now have electronic patient records. Available at: https://digital.nhs.uk/ news/2023/90-of-nhs-trusts-now-have-electronic-patient-records (accessed 21 November 2023)

18 DigitalHealth.Net (25 July 2023): EPR frontline digitisation target declared ‘unachievable’. Available at: https://www.digitalhealth. net/2023/07/epr-frontline-digitisation-target-declared-unachievable/ (accessed 21 November 2023)

19 DigitalHealth.Net (15 November 2023): Frontline digitisation funds at risk to cover industrial action costs. Available at: https:// www.digitalhealth.net/2023/11/frontline-digitisation-funds-diverted-to-cover-industrial-action-costs/ (accessed 21 November 2023)

Sector Insights | 13

OF ACQUISITIONS

20 Digital Health UK market report – third edition, LaingBuisson AND ANALYSIS

EXAMPLE - RLDATIX ACQUISITIONS

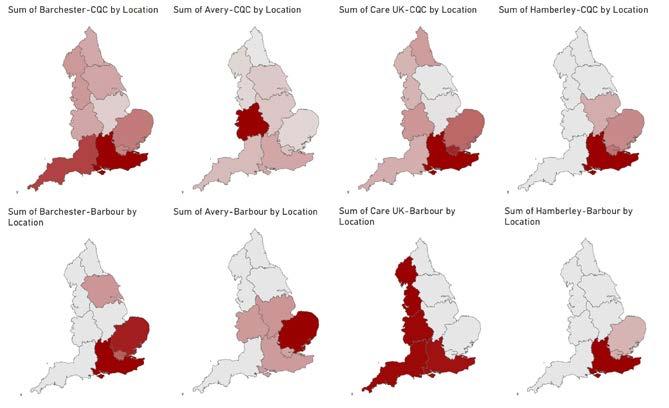

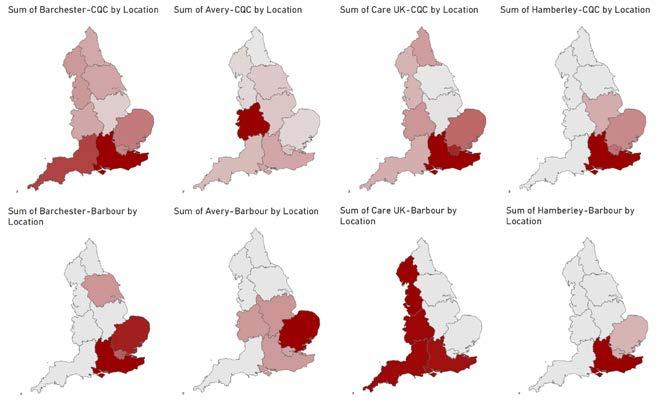

The CQC has moved to a system of more targeted inspections, designed to help accelerate improvement where it is most needed, but that can mean long gaps between inspections for the best performing facilities.

Abhishek Patel takes a deep dive into the impact of the changes on acute and mental health hospitals and discusses the implications for investors

AQuality matters a closer inspection of the CQC

t the forefront of any investor’s key priorities when assessing providers in health and adult social care, must be the topic of quality. Acquire a poor-quality service, and significant management time and resource will be required to turn things around; conversely, a good-quality service will be more profitable and more valuable.

In England all health and adult social care services are independently regulated by the Care Quality Commission (CQC), an arm’s length body of the Department of Health and Social Care which monitors and inspects sites and publishes quality reports with a simple 4-point rating scale (outstanding, good, requires improvement, inadequate). Other parts of the UK have equivalent independent regulatory bodies – Health Inspectorate Wales, the Care Inspectorate and Healthcare Improvement Scotland, and The Regulation and Quality Improvement Authority in Northern Ireland.

But while these reports provide a useful site-level proxy for quality, they mask the nuances behind ratings at a sub-sector and provider type level and are ultimately a ‘snapshot in time’ – the periods between inspections can be long and a lot can change. As a result, careful expert diligence is required to truly understand a provider’s real quality and their outlook.

This article analyses some key operational metrics for the CQC over the last five years, before taking a deep-dive into acute and mental health hospitals.

A brief background to the CQC

The CQC was established in 2009 to independently regulate all health and adult social care services in England, thereby consolidating its three predecessor organisations (the Healthcare Commission, the Commission for Social Care Inspection and the Mental Health Act Commission). Its primary aim is to ensure all services provide people with safe, effective, compassionate, high-quality care. More specifically, its key roles are to (1) register all health and adult social care providers; (2) monitor and inspect services to ensure they are safe, effective, caring, responsive and well-led, and subsequently publish quality ratings; (3) enforce changes through legal action when poor care is identified.

Ian Trenholm was appointed CEO in August 2018, taking over from Sir David Behan who had been in post since 2012. Whereas Behan had a strong social care background prior to joining the CQC, with executive positions at the Commission for Social Care Inspection and the Department of Health, Trenholm started his career as an Inspector in the Royal Hong Kong Police Service. He subsequently held executive positions at NHS Blood and Transplant, the Department of Environment Food and Rural Affairs (Defra), and the Royal Borough of Windsor and Maidenhead before joining the CQC. Under his leadership, the CQC has weathered the storm of Covid-19 which caused significant disruption to inspection activity, and

has moved towards a risk-based ratings approach where struggling providers are prioritised to drive improvement. In tone, the CQC is seen as moving from a more collaborative regulator seeking to help providers improve performance to a more proactive and assertive regulator, looking to prosecute more poor providers.

In 2021, the CQC set out four strategic priorities:

1. People and communities focus on the experience of people and what is important to them when they access, use and move between services

2. Smarter regulation provide up-todate and high-quality information and ratings, simplify interactions and ensure responses are more proportionate

3. Safety through learning prioritise learning and improvement to ensure stronger safety cultures

4. Accelerating improvement empower systems to improve quality of care where it is needed most

But how does this reflect in the numbers, and have we seen a change in activity since Trenholm’s appointment as CEO in 2018? We analysed some of the key operational metrics to understand how the CQC’s recent activity stacks up against its funding and resources.

14 | Sector Insights Healthcare Insights

FIGURE ONE

CQC INCOME AND EXPENDITURE

THE CQC RECEIVES c.50% OF ITS INCOME FROM INDEPENDENT SECTOR PROVIDERS

NOTES FINANCIAL YEARS END 31 MARCH 1 THIS CONSTITUTES c.90% OF TOTAL CQC REVENUE; THE REMAINDER IS MOSTLY DHSC-PROVIDED GRANT-IN-AID FUNDING 2 INCLUDES HOSPITALS, COMMUNITY, SINGLE SPECIALTY AND DENTISTS 3 INCLUDES ENFORCEMENT, INDEPENDENT VOICE AND OTHER ACTIVITY NOT FUNDED FROM FEES (SUCH AS THEMATIC REVIEWS)

SOURCE CQC ANNUAL REPORTS, MANSFIELD ANALYSIS

Stable resources, more complaints, fewer inspections

The CQC receives c.£200m income from fees charged to registered providers (see Figure One), which constitutes c.90% of its total revenue; the remainder is mostly DHSC-provided grant-in-aid funding. Around half of its fee income is from independent sector providers, predominantly adult social care (c.40%), but also hospitals, community and single specialty providers, and dentists (together c.10%). Income and employee numbers have remained largely flat over the last five years, which indicates relatively stable resource capacity, although funding may have been hit by recent inflationary pressures – the average salary for a CQC inspector is now estimated to be £38,328.

During the Covid-19 pandemic, expenditure shifted away from inspection towards monitoring, given extreme pressures which prevented on-site inspections. However, while expenditure on inspections has somewhat recovered to pre-pandemic levels, a closer look at overall inspection frequency reveals a longer-term decline that predates the pandemic (see Figure

Two). Mansfield sent an FOI request to the CQC to segment inspection activity by provider type; the results show adult social care and primary medical services have seen the greatest decline since 2016 of 12‒15%, but hospitals have also seen a marked 7% drop in inspection activity. Given all health and adult social care services must be registered with the CQC, fees charged to providers is effectively a ‘tax’ on the independent sector to be appropriately regulated and for quality standards to be maintained. It follows that all independent sector providers might reasonably expect frequent monitoring and inspections (and more importantly re-inspections) to give a current and relevant quality rating.

However, while CQC employee numbers have remained around 3,000 over the last six years, the number of inspections per employee has declined by c.2x since 2016. Taken together, this indicates inspection activity has been in sharp decline despite relatively stable resources and is yet to return to peak levels. This trend cannot be explained by the Covid-19 pandemic given inspections have not returned to pre-pandemic levels and resourcing is similar, but by key changes

in the CQC’s inspection strategy.

Historically, if a service was rated ‘good’ or ‘outstanding’, the CQC aimed to conduct a full inspection within five years. However, since 2021 the CQC has been taking a more ‘risk-based’, targeted approach to inspection, and only inspects sites where there is a clear risk to safety (i.e. prioritising struggling sites). For all other sites, the CQC has conducted c.20,000 ‘direct monitoring activity’ (DMA) assessments over the last three years – these entail speaking to service users and analysing data directly from providers, without going on-site to conduct a full inspection.

The CQC is also rolling out its new ‘single assessment framework’ for reports, which replaces key lines of enquiry (KLOEs) with new, standardised ‘quality statements’. However, there is an even greater risk of losing context at the expense of striving for consistency.

Caroline Barker, non-practising solicitor at the law firm Ridouts points out: ‘While these new quality statements are better aligned to regulations compared to the KLOEs they replace, it remains to be seen whether the proposed ‘ongoing assessments’, rather than inspection, will

Sector Insights | 15

70.4 FY20 18.2 17.5 68.2 Other independent2 94.1 95.8 FY18 20.9 19.6 NHS trusts and GP practices FY19 93.9 67.7 23.0 89.8 98.1 23.5 204.3 FY21 65.9 23.1 FY22 Adult social care (residential) Adult social care (community) 193.7 204.0 205.2 207.9 18.8 20.2 20.7 65.7 CAGR 2018-2022 1.8% 4.3% 6.2% -0.8% £m, income from fees charged to registered providers1 Income and employee numbers have remained largely flat Expenditure shifted away

inspection towards monitoring during the Covid-19 pandemic 2.2% £m, share of total revenue expenditure (excl. non-cash items) FY18 106.1 FY22 71.1 Monitoring 93.4 221.6 FY19 FY20 29.7 227.7 218.4 FY21 Inspection Registration Other3 212.2 215.4 79.7 22.8 31.9 110.8 30.2 59.8 17.7 33.2 42.4 33.9 86.2 28.0 Split not disclosed in annual reports CAGR 2019-2022 -1.8% 7.1% -3.7% -2.6% -1.8% 3.2k 3.1k 3.0k 3.1k 3.1k 3.0k Employees Covid-19

from

CQC INSPECTION ACTIVITY WAS DECLINING EVEN BEFORE COVID-19, AND REMAINS c.50% BELOW PRE-PANDEMIC LEVELS

‘000S, CQC INSPECTIONS

be used as a means to avoid the CQC’s statutory obligations to produce a full written report that a provider can review and respond to. We’ve also seen more enforcement action by the CQC over the last five years, and it’s become harder to get changes to reports than it used to be – so we might find more judicial reviews with the new system.’

So, while dedicating resources to struggling sites aligns with the CQC’s key strategic pillar to accelerate improvement where it is needed most, its implementation also creates uncertainty over the quality of services rated ‘good’ or ‘outstanding’ in inspections that in some cases were six or seven years ago. Moreover, complaints and whistleblowing enquiries (see Figure Three) are on the rise and at their highest ever levels, so it is surprising this has not resulted in more inspections.

Private acute and mental health hospitals: a tale of contrasting ratings

Private acute hospitals and mental health hospitals are two provider types that have seen contrasting trends in CQC ratings over the last five years.

16 | Sector Insights Healthcare Insights

15.2 3.8 2017 11.6 2016 2018 12.7 2.5 2019 6.2 2020 7.4 3.8 20231 1.1 17 7 2021 8.1 2022 23 0 18 5 16 2 7 7 9 6 11 7 9 0 6.5 4.4 3.7 1.1 1.5 1.3 1.1 1.2 1.0 1.0 0.7 13.1 (Annualised) Adult social care Hospitals Primary medical services Total inspections CAGR 2016-2023 -12 5% -12 1% -15 0% -6 8% Covid-19 7.9 5.8 5.2 5.8 2.5 3.1 3.8 N/A Inspections per employee2 NOTES 1 ACTUAL DATA FROM 1 JANUARY TO 15 AUGUST 2023 2 REVENUE AND EMPLOYEE NUMBERS ESTIMATED FOR EACH CALENDAR YEAR BY AVERAGING ACROSS PERIODS (AS ANNUAL REPORTS ARE BY FINANCIAL YEAR) SOURCE FOI REQUESTS, MANSFIELD ANALYSIS

2020 2018 2019 2021 2016 2017 2022 38.6 20231 39.9 43.2 43.2 47.6 65.6 40.3 60.0 +5.8% ‘000s ‘000s 2016 2017 20231 17.2 2018 2019 2021 2020 2022 7.6 7.7 8.9 14.4 10.6 14.5 15.9 +9.6% Complaints Whistleblowing enquiries COMPLAINTS AND WHISTLEBLOWING ENQUIRIES ARE AT THEIR HIGHEST LEVELS NOTES 1 ACTUAL DATA FROM JANUARY TO MAY 2023, ANNUALISED SOURCE PANNONE CORPORATE, FOI REQUESTS, CQC ANNUAL REPORTS, MANSFIELD ANALYSIS

INSPECTION ACTIVITY

FIGURE TWO

COMPLAINTS AND WHISTLEBLOWING ENQUIRIES

FIGURE THREE

THE QUALITY GAP BETWEEN THE NHS AND THE TOP SIX PRIVATE GROUPS HAS WIDENED SIGNIFICANTLY OVER THE LAST FIVE YEARS

%, SHARE OF LOCATIONS RATED ‘GOOD’ OR ‘OUTSTANDING’

The top six private acute hospitals have seen their CQC ratings increase consistently, whereas their NHS counterparts have seen a steady decline since Covid-19 (see Figure Four).

While these groups have always had superior quality ratings to the NHS, the gap has widened significantly. Roughly 95% of locations from the top six groups are rated ‘good’ or ‘outstanding’ compared to just c.55% of NHS acute hospitals; a stark difference which not only articulates the extreme pressures faced by the public healthcare system, but also indicates how strong leadership and effective collaboration with the CQC in the independent sector can drive quality improvements.

Private acute hospitals saw more inspections than pre-Covid-19 in 2022 (see Figure Five), with c.25% of rated locations inspected (similar to 2019 levels), following reduced activity during Covid-19. Of the 44 locations inspected, only three decreased in rating; 11 increased, 21 saw no change, and nine were inspected for the first time.

In contrast, NHS acute hospital inspection frequency has not recovered to pre-pandemic levels yet and many rating for both NHS and private are out

ROUGHLY 95% OF THE TOP SIX GROUPS ARE RATED ‘GOOD’ OR ‘OUTSTANDING’ COMPARED TO JUST c.55% OF NHS ACUTE HOSPITALS; A STARK DIFFERENCE WHICH ARTICULATES THE PRESSURES FACED BY PUBLIC HEALTHCARE

CQC filtering methodology

• Location primary inspection category: Acute hospital

• Top six private groups:

o Circle Health Group (formerly BMI Healthcare)

o Spire Healthcare

o Ramsay Health Care UK

o Nuffield Health

o HCA

o Practice Plus Group

of date. As at August 2023, the average time since last inspection for NHS acute hospitals was 3.8 years for ‘good’ or ‘outstanding’ sites compared to 1.9 years for ‘requires improvement’, and 1.2 years for ‘inadequate’; therefore, ‘good’ or ‘outstanding’ sites were being rated c.2x less frequently.

However, for the top six private groups, the average time since the last inspection was 3.7 years for ‘good’, ‘outstanding’ and ‘requires improvement’ locations, so the rating appears to have no impact on inspection frequency.

Private mental health hospitals have seen a very different profile – five years ago independent providers had 14% more ‘good’ and ‘outstanding’ ratings than the NHS, while today they have 9% fewer. They have seen a steady decline in CQC ratings by 10 percentage points since Covid-19, while NHS mental health trusts have largely been unchanged (see Figure Six).

A number of leading private providers including St Andrew’s Healthcare, InMind and CareTech have had multiple services downgraded. A closer look at the key lines of enquiry (KLOEs) in inspection reports reveals safety and leadership concerns

Sector Insights | 17

Jan-20 Jan-18 Jan-19 Jan-21 Jan-22 Jan-23 Jan-24 70% 50% 60% 80% 100% 0% 90% Top six private groups NHS +39pp +25pp

NOTES WE HAVE EXCLUDED LOCATIONS NOT RATED FROM THIS ANALYSIS SOURCE CQC CARE DIRECTORY, MANSFIELD ANALYSIS

FOUR ACUTE HOSPITALS – RATINGS

FIGURE

FIGURE FIVE ACUTE HOSPITALS – INSPECTION FREQUENCY

INSPECTED MORE IN 2022, FOLLOWING REDUCED INSPECTION ACTIVITY DURING COVID-19

INSPECTED

FIGURE SIX MENTAL HEALTH HOSPITALS – RATINGS

‘GOOD’ OR ‘OUTSTANDING’

as the key drivers for lower ratings. The mental health sector as a whole has faced profound system pressures since Covid-19, with high staff churn and persistent shortages, and a lack of training often cited.

Nevertheless, it is clear that staffing capacity and investment is needed in a sector which faces increasing demand and that often deals with the most challenging of patients in the health system.

Conclusion

Without consistent monitoring and frequent inspections, can providers be credibly held to account over service quality? The CQC rightly provides critical and necessary regulatory oversight to ensure patients receive the best care possible. However, when investors are looking to buy assets, CQC reports and summary ratings mask the nuances at the sub-sector and provider type level.

A private mental health hospital provider with a high proportion of ‘good’ or ‘outstanding’ sites should be considered particularly attractive when contextualised to the overall decline in ratings in this sub-sector.

Conversely, a private acute hospital provider with declining ratings should be approached with caution given the high and increasing ratings of the top six groups.

In addition, diligence now also needs to encompass how providers participate in an integrated health and care economy. Chris Day, director of engagement at the CQC, points out: ‘Six years ago, quality was about how well you manage inside your organisation – having good processes and workflows; what will define the next six to seven years will be how well they take part in that wider system, particularly in the NHS.’

Investors always require assurance on quality, but ratings from inspection reports are only a starting point - to truly understand quality, there is no substitute for in-depth site visits, conversations with key site-level personnel and the expertise of a commercial due diligence specialist.

18 | Sector Insights Healthcare Insights

25 43 14 15 44 15 147 150 83 131 132 79 2018 2019 2020 2022 2021 2023 YTD1 NHS Top six private groups 14.8% 24.2% 8.1% 8.7% 24.4% ~ 49.8% 48.2% 26.6% 42.4% 41.5% Top six private groups NHS %, share of hospitals rated Reduced inspection activity due to Covid-19 NOTES 1 ACTUAL DATA FROM 1 JANUARY TO 15 AUGUST 2023 2 REVENUE AND EMPLOYEE NUMBERS ESTIMATED FOR EACH CALENDAR YEAR BY AVERAGING ACROSS PERIODS (AS ANNUAL REPORTS ARE BY FINANCIAL YEAR) SOURCE FOI REQUESTS, CQC CARE DIRECTORY, MANSFIELD ANALYSIS PRIVATE HOSPITALS WERE

NUMBER

LOCATIONS

Jan-23 Jan-24 Jan-20 70% 80% 90% Jan-18 Jan-19 Jan-22 Jan-21 0% Private hospitals NHS mental health trusts +14% Covid-19 -9%

CQC RATINGS FOR INDIVIDUAL NHS MENTAL HEALTH HOSPITALS

COLLATED

CQC DIRECTORY;

WE HAVE

CQC REPORTS

EVERY NHS MENTAL HEALTH TRUST AT DECEMBER OF EACH YEAR SOURCE CQC CARE DIRECTORY, MANSFIELD ANALYSIS

MENTAL HEALTH HOSPITALS

SEEN

CQC RATINGS DOWNGRADED MORE THAN THE NHS

COVID-19 %, SHARE OF LOCATIONS

OF

NOTES

ARE NOT

IN

THEREFORE,

LOOKED AT

FOR

PRIVATE

HAVE

THEIR

SINCE

RATED

Germany has a large private hospital sector in comparison to the UK. Arne Berndt, partner at WMC Healthcare, and Paul Fegan consider whether the differences in respective sectors are due to contrasting healthcare systems, and whether any of the conditions that result in Germany’s large private hospital sector are transferable to the UK

Managed markets comparing the German and UK private hospital sectors

In April 2023, Mansfield Advisors compared UK and Spanish private hospitals, highlighting the significant differences in scale and scope of the two sectors, despite both having similar tax-funded universal healthcare systems with complementary private health insurance. Our article (see page 20) concluded that Spain has created the conditions for large private hospitals to thrive by having a far larger privately insured population and regional governments more willing to experiment with public-private solutions.

Germany has an even larger private hospital sector. Eurostat data shows nearly 60% of hospital beds in the €114bn acute hospital market are private , while only 40% are run by public hospitals. This is in marked contrast to the UK, where roughly 5% of beds are in the private sector, and Spain, with 32% in the private sector (see Figure One). Like Spain, German private hospitals include ‘full-service’ general hospitals, in contrast to the UK’s small sites offering a limited range of elective procedures.

Structure of Germany’s acute hospital sector

Germany has a lot of beds, both in absolute terms (437,000) and relative to population (see Figure Two).

Excluding psychiatric beds, German federal statistics for 2021 show 33% of beds (146,000) are not-for-profit and 19% (83,000) are for-profit. The for-profit sector is highly concentrated, with the four biggest groups accounting for 61% of for-profit beds (12% of total beds). By contrast, the not-for-profit sector is much more fragmented (the top five have 15% of not-for-profit beds) and public hospitals

are even more fragmented (see Figure Three).

About half (48%) of all hospital beds are in large hospitals (>500 beds), and nearly two-thirds of these are in public hospitals. At the other extreme, 15% of beds are in small hospitals (<200 beds), and 42% of these are for-profit. The latter partly reflects the prevalence of highly specialised small hospitals, such as those focussing on sports surgery, which can be highly profitable.

Social and private health insurance

Germany’s universal healthcare system is the original social insurance model. Employees and employers contribute to public health insurance funds, with the federal government setting a contribution rate for salaries up to c.€65,000. These insurance funds then reimburse providers on behalf of their members. All Germans are required to have insurance, and the funds cover family members, retirees and the unemployed.

Superficially, the German and UK systems look similar: instead of general taxation, Germans are, in effect, ‘taxed’ through social insurance. Unlike the UK, though, where private insurance is complementary (we cannot opt out of paying taxation), Germans who earn over €65,000 can choose substitutive private insurance and opt out of the public insurance system entirely. (There are controls on re-joining the public system to prevent adverse selection.)

However, the payor model is not the driver of Germany’s large private hospital sector per se. First, the proportion of the German population with private insurance

is not significantly greater than the UK. Around 12.5% have substitutive private insurance, compared with approximately 10% in the UK and c.25% in Spain covered by complementary private insurance, and this has been declining slowly as it becomes more expensive and relatively less attractive to Germany’s ageing population (see Figure Four). Secondly, private and social insurance payors are not limited to private or public hospitals exclusively.

Managed markets and dual financing

The critical difference between the UK and German models is that the latter enables individuals to be consumers of healthcare (‘demand-led’), whereas healthcare in the UK is viewed as a public good/service (‘supply-led’). To be clear, Germany’s social insurance system does not in itself create a large private sector (France has a similar model, but only 38% of beds are private). It simply creates the conditions for healthcare markets to develop.

Theoretically, markets are self-regulating, but governments usually intervene where consumers and/or producers cannot make economically rational choices. For example, governments don’t directly control the market for cars, but do set safety and environmental standards. Similarly, Germany manages the market for hospital services, providing a level-playing field where patients choose where they are treated. Patient and payor can be agnostic about whether that is a private or public hospital.

Dual financing is a key component of the managed market, with frameworks

Sector Insights | 19

GERMANY HAS A LARGE PRIVATE HOSPITAL SECTOR (NOT-FOR-PROFIT) COMPARED TO OTHER EU COUNTRIES %, AVAILABLE HOSPITAL BEDS1 BY SECTOR, EXCLUDING PSYCHIATRIC CARE, 2018

Public

Not-for-profit

GERMANY HAS A LOT OF BEDS, BOTH IN ABSOLUTE TERMS AND RELATIVE TO POPULATION 000s BEDS, 20211

NUMBER OF BEDS1, PER 100,000, 2021

20 | Sector Insights Healthcare Insights NOTE 1 INCLUDES CURATIVE CARE, LONG TERM CARE IN HOSPITAL SETTINGS, REHABILITATIVE CARE AND ‘OTHER’ 2 EXCLUDES IRELAND, HUNGARY, SLOVAKIA, SWEDEN & LUXEMBOURG 3 UK PRIVATE HOSPITAL BED DATA IS NOT INCLUDED IN THE EUROSTAT PUBLICATION. EXTRACTED FROM LAINGBUISSON REPORT AND MAY INCLUDE NOT-FOR-PROFIT BEDS SOURCE EUROSTAT HEALTHCARE RESOURCES STATISTICS - BEDS 2020; LAINGBUISSON PRIVATE ACUTE HEALTH CARE, SEVENTH EDITION (2021) 61% 41% 62% 68% 95% 18% 29% 14% 13% 22% 30% 24% 19% 5%3 2 3

NOTE 1 OECD DEFINITION OF ‘SOMATIC CARE’, INCLUDES CURATIVE, LONG TERM, REHABILITATION AND ‘OTHER SOURCE OECD HEALTHCARE RESOURCES – HOSPITAL BEDS BY FUNCTION; MANSFIELD/WMC HEALTHCARE ANALYSIS 536.7 329.1 123.3 140.1 645 486 260 208

HOSPITAL BEDS BY

FIGURE ONE

PROVIDER SECTOR

BED CAPACITY

FIGURE TWO

FIGURE THREE

SECTOR CONCENTRATION

HOSPITAL BEDS BY PROVIDER GROUP AND SECTOR, 2020

Bremen

Munich

Rheinland

for supporting capital investment and to cover operating costs (see Figure Five):

• Capital investment funds (3% of hospital funding) administered by German states for new buildings and other projects. Public and private hospitals can bid for funding. States also plan hospital capacity, although this does not necessarily translate to explicit targets for bed numbers, nor the relative share of private and public sectors

• Operating costs (97% of hospital funding) German hospitals are reimbursed for activity delivered. A federal agency, the Institute for the Hospital Remuneration System (InEK), defines services and sets prices using a Diagnosis-Related Group (DRG) system. DRG reimbursement covers around 80% of operating costs and is the product of a base rate and points per case, depending on complexity. It is used by all payors to reimburse all hospitals for inpatient services

There is a similar activity-based approach for reimbursing outpatient services, but different systems for social and private insurance. (Physicians receive 2.3 times more through private reimbursement.) Other services are generally billed on a fee-for-service basis.

In principle, the NHS in England is similar, and the architecture of hospital funding would be recognisable to German hospital operators. The National Tariff is comparable to the German DRG system, and private hospitals in England can contract to the NHS, receiving the appropriate tariff, just like their German counterparts. Capital funding for NHS hospitals is handled separately (although is not available to private operators). Yet, despite these similarities, we still do not have a large private hospital sector. What else is missing?

History, policy and culture

Different histories and cultures mean similar approaches to payment or organisation have different outcomes. When the NHS was founded in 1948, as an integrated, tax-funded service, there was still no reason why it had to own hospitals.

However, the existing patchwork of charity, church and municipal hospitals needed reorganisation, renewal, rationalisation and expansion, and centralised public ownership was seen as the best way to achieve that, as in other newly nationalised industries.

German charity, church and municipal hospitals have similar origins to the UK, but social insurance is much older than the NHS . Its decentralised separation of payor and provider meant public hospitals continued to be owned by municipalities and private hospitals remained independent not-for-profit institutions. However, with a demand-led system, Germans also became comfortable with choice. This is exemplified by supplementary private insurance which tops-up statutory cover for greater choice of consultant, private rooms, etc. Some 10% of Germans have supplementary private insurance and it has been growing. In the UK, there is resistance to anything which dilutes the idea of a universal ‘one-size-fits-all’ NHS.

It was the transition to dual financing which stimulated the growth of for-profit hospitals by forcing the privatisation of public and not-for-profit hospitals. The DRG system has been blamed for losses,

Sector Insights | 21

For-profit Not-for-profit Public 60.3% 39.7% To tal To p 4 14.5% 85.5% To tal To p 5 8.5% 91.5% To tal To p 5

SOURCE GERMAN FEDERAL STATISTICAL OFFICE; WMC HEALTHCARE ANALYSIS

Vivantes (Berlin)

Knappschaft (Ruhr)

Agaplesion

Barmherzige Bruder

Marienhaus

Franziskus Stiftung Helios

Alexianer Asklepios

Sana Kliniken

Ameos

97,000 158,000 233,000 58,000 23,000 20,000

THE

FOR-PROFIT SECTOR IS HIGHLY CONCENTRATED; NOT-FOR-PROFIT AND PUBLIC HOSPITALS ARE MUCH MORE FRAGMENTED %

FIGURE FOUR

FIGURE FIVE

ALL

% OF HOSPITAL FUNDING BY SOURCE,

22 | Sector Insights Healthcare Insights SOURCE GERMAN FEDERAL STATISTICAL OFFICE; PKV; WMC HEALTHCARE ANALYSIS 2016 2014 CAGR 2014 – 2020 2020 2018 Substitutive Supplementary 6.1 14.8 8.8 8.7 15.0 14.9 8.7 8.8 5.9 6.2 1.2% 14.7 6.3 -0.2% 0.4% Substitutive PHI premium development compared to consumer price index PHI penetration - supplementary vs. substitutive consumer price index substitutive insurance premiums 2015 2016 2017 2018 2019 2020 2021 130 120 110 100 90 SUBSTITUTIVE PRIVATE HEALTH INSURANCE IS SLOWLY DECLINING AS PRICES RISE, WHILE SUPPLEMENTARY (TOP-UP) INSURANCE GROWS INDEXED TO 100 NOTE 1 INCLUDES GRANTS THAT ARE ACCOUNTED FOR AS REVENUES, NEW EXAMINATION AND TREATMENT METHODS, AND OTHER OPERATING INCOME SOURCE GERMAN FEDERAL STATISTICAL OFFICE; GERMAN HOSPITAL ASSOCIATION; WMC HEALTHCARE ANALYSIS 97 % 2019 3 % Investment costs Operating costs Total = €104bn Source of funding: Statutory & private health insurances Type of funding: ! DRG System: hospitals receive lump-sum payments per patient day depending on case complexity ! Case rates for ambulatory care ! Fee-for-service for optional services ! Other: new examination and treatment methods 80 % 15 % 2 % Fees for optional services 3 % DRGs Other1 Funding split Case rates for ambulatory care Source of funding: Federal states Type of funding: ! Individual support (e g., for a new building) ! Lump-sum support based on individual federal state specific allocation process considering e.g hospital size, cases, guaranteed minimum payments 56 % 44 % Individual support for specific projects Lump-sum support for infrastructure Funding split Overall insufficient funding for investment costs by the federal states mean some capital investment needs to be covered by operational income

HOSPITALS,

OF SECTOR, BENEFIT

DUAL-FINANCING SYSTEM,

CAPITAL

REGARDLESS

FROM THE

ALTHOUGH

FUNDING IS INSUFFICIENT

2019

PRIVATE HEALTH INSURANCE IN

GERMANY

DUAL-FINANCING

with smaller hospitals particularly vulnerable, since they struggle to generate case mix points to be profitable. Meanwhile, capital investment funds have left hospitals underinvested and, without sufficient resources, municipalities and even federal states have opted for privatisation. For example, Giessen-Marburg was sold by the state of Hesse in 2006 to become the first privatised university hospital. The number and share of private hospitals, therefore, continues to grow (see Figure Six).

Overcapacity

There is another factor at work. As the government stimulates the development of outpatient, day patient and other ambulatory services to reduce reliance on inpatient services, the hospital system is consolidating. While there is no formal target for bed capacity, if Germany went as far as to converge on the EU27 average, there would be 173,000 fewer beds (almost as many beds as in the entire NHS across the UK). Hence, some hospitals will close.

Privatisation is seen as an alternative to closure. While the German public might be agnostic about who provides its healthcare, and is comfortable with choice and top-ups, they are perhaps still uncomfortable with the idea of making a profit out of ‘misfortune’. However, the private sector is also seen as a way to save hospitals which would otherwise be closed, and, for politicians, it is perhaps a way of shifting blame for those closures when they do happen.

Conclusions

Compared with the UK, Germany has a large private hospital sector because of a multitude of factors.

One is undoubtedly the fundamental difference between healthcare systems, creating the conditions in which hospitals of any sector could thrive within a managed market. However, the tools of managed markets, such as DRG reimbursement, also made it more difficult for public and not-for-profit hospitals to survive. In the UK – or at least in England – we have those same tools, but the

managed market still does not make large scale private general hospitals viable.

It is deliberate choice and culture which have played a much greater role. Culturally, Germans are accepting of their role as consumers of healthcare, and hence they are less concerned about whether the hospital is private, public, for-profit or not, as long as it meets their expectations on quality.

In terms of choice, the owners of loss-making hospitals have deliberately chosen to privatise as a way to sustain those hospitals that might struggle for investment or even close. The British are still a long way from seeing themselves as healthcare consumers, or accepting top-ups, and it would be a brave politician who decided to privatise a loss-making NHS trust. Mansfield Advisors and WMC Healthcare, together with Antares Consulting, form the Curis Alliance of specialist health and social care consultancies, with Europe-wide coverage.

FOR-PROFIT HOSPITALS HAVE BEEN GROWING AS NOT-FOR-PROFIT AND PUBLIC HOSPITALS ARE PRIVATISED AND THE MARKET CONSOLIDATES

Sector Insights | 23 NOTE INCLUDES PSYCHIATRIC BEDS SOURCE GERMAN FEDERAL STATISTICAL OFFICE; GERMAN HOSPITAL ASSOCIATION; WMC HEALTHCARE ANALYSIS XX % Hospitals by ownership Hospital beds by ownership 577 570 560 552 545 551 547 679 674 662 650 645 620 607 700 707 720 723 724 732 733 2017 1,942 2015 2020 2016 2018 2019 Private Non-profit Public 1,956 1,951 2021 1,925 1,914 1,903 1,887 97 499 163 168 239 93 167 2018 2015 241 93 Non-profit 96 2016 165 239 Public 164 2017 95 236 239 2019 97 488 159 232 2020 Private 91 499 497 498 494 2021 484 231 156 CAGR 2015 – 2021 -0.6% 0.8% -1.9% -0.9% -0.5% 1.0% -1.2% -0.7% CAGR 2015 – 2021

FIGURE SIX GROWTH IN FOR-PROFIT HOSPITALS

Deals in the surgical ophthalmic equipment and products market reached a record high of 31 deals in 2022, with PE backed transactions also attaining new highs. Johan Ottosson and Dr Victor Chua see significant opportunities for this sector of the market

Investors show strong interest in ophthalmic product space

Global surgical ophthalmic equipment and products deals grew with a CAGR of 19% 2018‒2022 to a record high of 31 deals last year. PE or PE backed deals grew faster than the market overall with a CAGR of 26.6%, reaching a record 13 deals in 2022, almost twice that of the previous year.

Recent notable PE deals include Eurazeo’s acquisition of Dutch Ophthalmic Research Center International (DORC, led by CEO Pierre Billardon) for an estimated

€300m in 2019,1 and CVC’s acquisition of Rayner Surgical Group (led by CEO Tim Clover) for an undisclosed amount in 2021.

The most active investor in recent years however has been TPG Capital. Since its 2016 acquisition of US-based Beaver-Visitec International’s (BVI, led by president and CEO Shervin Korangy) TPG Capital has proceeded to roll-up multiple, mainly European, ophthalmology assets. Through this, TPG Capital has built a leading global platform estimated to have seen a reve -

nue growth of around 19% CAGR between 2017 and 2021.

Investor interest in the space is driven by attractive market fundamentals such as an ageing population, increasing treatment of pathologies, better access to healthcare, as well as stable public or insurance funding. Ophthalmic procedures tend to be inexpensive because they are almost always day-cases, and impactful because good vision is so important to normal productive life.

We therefore expect ophthalmic pro-

24 | Sector Insights Healthcare Insights

cedure growth exceeding growth in other surgical specialities. There are significant roll-up opportunities for investors in this space, notably in the US and Western Europe.

A large and fast-growing market

We estimate the global ophthalmology equipment and surgical products market to be worth around £20bn in 2023. Around 84% of this market is made up of equipment and products for the operating room (see Figure One).