In 2024, Simmons Bank further solidified its reputation as a leader in the banking industry and a "Best Place to Work" employer. These awards celebrate Simmons’ commitment to excellence in both customer service and employee satisfaction, reinforcing its position as a trusted, innovative, and people-focused financial institution.

Forbes America’s Best-In-State Banks 2024

Simmons Bank was named to Forbes America's Best-In-State Banks 2024 in the state of Tennessee. America's Best-In-State Banks 2024 ranking names the institutions that stood out for fulfilling the unique financial needs and expectations of their local communities, thereby being most valued by residents of each state. For the seventh annual ranking, Forbes partnered once again with market research firm Statista Inc., the worldleading statistics portal and industry ranking provider, to survey approximately 26,000 U.S. residents.

Forbes America’s Best-In-State Employers 2024

Simmons Bank was named to Forbes America's Best-In-State Employers 2024 in the state of Missouri. This prestigious award is presented by Forbes and Statista Inc., the leading statistics portal and industry ranking provider. America's Best-In-State Employers 2024 have been identified in an independent survey from a vast sample of over 160,000 employees working for companies employing at least 500 people within the U.S. Around 4.4 million employer evaluations were considered.

U.S.

News & World Report's 2024-2025 Best Companies to Work For in the South

Simmons Bank was recently recognized by U.S. News & World Report, the global authority in rankings and consumer advice, as one of the 2024-2025 Best Companies to Work For in the South. The U.S. News Best Companies Ratings are calculated through how well companies support their employees with metrics including quality of pay and benefits, work-life balance, professional development, job and company stability, and physical and psychological comfort. This year, the rankings consisted of 549 companies across the overall best company list, 24 industry lists and four regional lists.

America’s

Best Regional Banks and Credit Unions

2025

Simmons Bank was recently named to Newsweek’s America’s Best Regional Banks and Credit Unions 2025. Newsweek and data firm Plant-A Insights Group analyzed more than 9,170 institutions, surveyed over 71,000 U.S. residents, gathered over 845,000 reviews, and collected more than 1.9 million social media reviews to rank the top 500 regional banks and 500 credit unions in the United States.

LETTER TO SHAREHOLDERS

Fellow Shareholders,

I want to recognize the outstanding contributions to our organization by several key executives who retired from Simmons at the end of 2024. These gentlemen helped shape our organization during our growth from $3 billion in assets to over $27 billion in assets since 2013. Those individuals are Bob Fehlman who served as CFO, President, and most recently CEO during that time; Steve Massanelli, our SEVP and the owner of a variety of responsibilities, who led the integration of most of our acquisitions, but also managed our corporate insurance program, real estate and security, among other duties; Steve Wade who served as Chief Credit Officer and Assistant General Counsel and was responsible for the management of credit risk as we integrated 13 acquired banks; Johnny McCaleb who served as our Chief Audit Executive and rebuilt the entire audit program; and Pat Neeley who managed our operations functions. It is hard to describe how the expertise of this group and their dedication to the organization has influenced our substantial growth. We thank them for their service and will miss their guidance as we move into the next chapter of the company.

Speaking of the next chapter, we are very fortunate to have an outstanding lineup of talented executives ready to lead us forward. Ten years ago we set out to establish an opportunity to grow Simmons Bank. With our expansion into six mid-America states and some of the best growth markets in the country, we have accomplished that goal. I am optimistic about the future of Simmons Bank. I believe we are well positioned to thrive for the next 120 years.

We appreciate the support of our shareholders and your confidence in Simmons Bank.

Sincerely,

George A. Makris, Jr. Chairman and Chief Executive Officer Simmons First National Corporation

LETTER FROM THE PRESIDENT

The essential characteristic of a 120-plus year company is its strong foundation, built by visionary leaders whose contributions have shaped its success and whose shoulders we stand upon today. As George previously noted in his letter, 2024 marked the retirement of several executives who have contributed significantly to Simmons Bank over the years. I would especially like to recognize Bob Fehlman and Steve Massanelli, each of whom I worked closely with prior to joining Simmons, and who played a major role in my decision to join the bank. Well-respected for their knowledge and integrity, Bob and Steve were always willing to lend their expertise and mentorship to anyone in our organization, including myself, and for which I will be ever grateful.

While navigating this transition in leadership, we have been very successful in attracting proven talent, many times from larger banks. One of those individuals is Chris Van Steenberg, our Chief Operating Officer, who joined us prior to the end of the year. Chris brings a wealth of experience from a larger, Mid-South regional bank, with extensive experience leading areas that we have identified as significant organic growth opportunities given our footprint and positioning in the market.

Moreover, we believe we are ideally situated with a combination of high-growth markets, complemented with stable community markets, and the size (more than $20 billion in assets) to capitalize on organic growth opportunities. The success of our Better Bank Initiative has also enabled us to accelerate and fund strategic initiatives through ongoing expense management discipline.

Overall expenses grew less than the rate of inflation in 2024 and remain below our annualized run-rate from fourth quarter levels two years ago. While cost savings was an ancillary aspect of the Better Bank Initiative, the key component has been our ability to streamline processes, improve our ability to service our customers and create scale in our businesses that will enable us to serve a larger customer base. We believe this will be a competitive advantage given the prospects of ongoing disruption and consolidation in our industry and changes in the competitive environment.

Most importantly, our commitment to organic growth is built on the standards of soundness and profitability, driven by our ability to systematically measure and generate strong risk-adjusted returns on invested capital. Achieving our goals will require ongoing transformation, and I am encouraged by our team as they continue to demonstrate the capacity and focus to execute these initiatives.

Soundness, profitability and growth – and in that order – is the driving mantra that encapsulates our values and guides our business decisions that we believe will ultimately deliver sustainable value for our customers, the communities we serve, our associates and our shareholders.

On behalf of our the nearly 3,000 associates, we thank you for your continued interest and support.

Jay Brogdon President Simmons First National Corporation

HONORING REMARKABLE LEADERSHIP

As 2024 marks the retirement of five remarkable leaders, we take a moment to reflect on the profound impact they have had on Simmons Bank.

Bob Fehlman, Steve Massanelli, Pat Neeley, Steve Wade and Johnny McCaleb have each demonstrated unparalleled commitment, vision and integrity throughout their distinguished careers. Their leadership not only steered our institution through times of growth and challenge, but also set a lasting example of dedication to our customers, employees and the industry at large.

Over the years, their guidance has shaped Simmons’ strategies, improved operational efficiencies and enhanced customer satisfaction, all while fostering a culture of collaboration and excellence.

As they embark on this new chapter, we express our deepest gratitude and wish them all the best in their well-earned retirements, knowing their influence will continue to resonate for years to come.

Bob Fehlman, Chief Executive Officer

Fehlman began his banking career with Simmons in 1988, serving in a variety of leadership roles, culminating with his appointment as chief executive officer between 2023-2024.

Bob previously served as president and chief operating officer. With more than 30 years of experience, he also served as chief financial officer and treasurer, with responsibility for Simmons’ overall financial management and operations – in this role, his oversight included accounting, financial planning, investments, tax, bank operations, IT and risk. Bob also provided critical support for Simmons’ mergers and acquisitions (M&A) activity, analyst and investor meetings and led the company’s capital management.

He is a Certified Public Accountant and a member of the American Institute of CPAs and the Arkansas Society of CPAs. Bob is a Henderson State University alumnus and is a graduate of Vanderbilt Graduate School of Bank Financial Management.

Steve Massanelli, Senior Executive Vice President, Chief Administrative Officer

Steve served our company in many capacities since his 2014 arrival. As chief administrative officer, he was instrumental in supporting Simmons’ strong mergers and acquisitions (M&A) activity between 2014-2022 and has implemented numerous aspects of corporate strategy across all areas of the bank.

Steve also served as investor relations officer for the organization from 2018-2021, reaching many investors to grow the Simmons Bank brand across the United States.

Prior to joining Simmons, Steve served for three years as CFO of Treadstone Partners, a Dallas-based investment firm. Prior to Treadstone, he worked in several capacities, including his role as senior vice president and treasurer of Zale Corporation.

HONORING REMARKABLE LEADERSHIP

Pat Neeley, Executive Vice President of Bank Operations

Pat Neeley joined Simmons Bank in 2017 as executive vice president and executive director of Finance and Accounting. In September 2019 he was appointed to lead Bank Operations, spearheading Deposit and Lending Operations, Performance Improvement, Credit Card and Customer Service.

Pat previously served as chief financial officer and undersecretary of Business Affairs for Chickasaw Nation’s Department of Commerce. During his tenure, he led several large-scale, transformational process and technology initiatives for the tribe during a period when it experienced significant growth and doubled in size. He joined Simmons Bank as the company was aggressively pursuing growth and looking for ways to reinvent its processes and technology. The pairing was a great match, allowing Pat to apply his vast experience in consulting and transformational change.

Steve Wade, Assistant General Counsel

Steve most recently served in an advisory capacity for Simmons, capping his 23-year career at the bank that has included stints as chief credit officer and assistant general counsel, among other roles. He formerly chaired the bank’s Senior Credit Committee and Executive Loan Committee and was responsible for crafting much of the bank’s Credit Policy.

A licensed attorney, Steve has more than 40 years of total banking experience with a focus on commercial lending, lending management and market leadership. He previously served as Simmons’ first market president for Little Rock.

Johnny McCaleb, Chief Audit Executive

Johnny has most recently served in an advisory role for Simmons after contributing years of leadership for the bank’s Internal Audit group. As chief audit executive, Johnny reported directly to the Audit Committee of Simmons First National Corporation's Board of Directors to assist them in fulfilling their fiduciary responsibility to shareholders through monitoring the bank’s compliance with financial reporting laws, regulations, and internal system of accounting and financial controls.

With more than 45 years of experience, Johnny has been with Simmons Bank since 2016. Prior to his time with the bank, he served as an audit partner with Ernst & Young LLP from 1990 to 2005 and BKD, LLP from 2005 to 2015.

BETTER BANK INITIATIVE

Q&A with Jena Compton

Nine years after joining Simmons, Chief People Officer Jena Compton reflects on lessons learned, victories won and what’s next.

What are some key factors you believe contribute to the high levels of positive feedback from our annual Associate Engagement survey?

I think the high level of associate participation, and corresponding scores, only comes from a true demonstration of our values. Our actions match our words. We believe in supporting our communities, so we go out and volunteer and sponsor local events. We support our associates by investing in programs to help them grow professionally and personally. We continually reinforce our Build Loyalty cornerstone by emphasizing the importance of both internal and external customer service with training and recognition. Many companies say they believe in these things, but at Simmons, we are very intentional in putting actions behind our words.

The same holds true for our vision for the future. We communicate our strategy broadly and ask associates to do their part in making it happen through initiatives and goals. Each of us owns a piece of Simmons' success, so it’s critical we align and work together to make it happen!

This past year, Simmons was named as one of the Best Companies to Work For in the South by U.S. News & World Report. How have you utilized employee feedback to ensure Simmons Bank continues to be a best place to work?

Associate feedback is crucial to being a great place to work and so we gather it in many different ways. We created a Quality Improvement Program five years ago to help us identify how we could get better. We regularly do internal communication feedback sessions and surveys of all sorts, and most critically, we offer an annual Associate Engagement survey to provide a forum for associates to share what is working and not working for them. We get thousands of comments, and every single one is read and considered. We have a group of executives that meet monthly to determine feasibility and priority of those suggestions. No single person has all the ideas, and the engagement survey provides a mechanism to gather up ideas from across our footprint and business lines.

Q:

Since the launch of the High Performance Culture initiative, associates are encouraged to find their “why.” What benefits do we continue to see from this initiative?

I’m convinced that the best work an associate performs is that which is driven by a purpose. When we go to work every day focused on achieving our "why," we are passionate and driven in what we do. Helping associates find their "why" results in higher job satisfaction, higher levels of customer service and improved quality of work. It’s a win-win for the associate and Simmons.

BETTER BANK INITIATIVE

Q&A with Ann Madea

As an IT leader with global, regional and community banking experience, Chief Information Officer Ann Madea is fueled by driving growth. Her IT strategy has set Simmons on a path of transformation.

In 2024, Simmons focused on honing data and technological capabilities in order to assist associates with driving profitable relationships. How did your team collaborate with associates across the bank to deliver a seamless experience for our customers?

Our team collaborated closely with associates across the bank to deliver a seamless customer experience through two key initiatives: Profitability Analytics and Householding Relationship Management.

Profitability Analytics empowered us to precisely measure and analyze customer profitability across multiple dimensions, including individual product performance, branch-level contribution, and overall customer value. Householding Relationship Management enabled us to create a holistic view of interconnected customer relationships, identify cross-selling and upselling opportunities within household units, and deepen customer engagement through targeted, relationship-based offerings.

Together, these initiatives provided a robust framework for driving sustainable revenue growth and enhancing overall bank performance. They aligned perfectly with our strategic goals of customer-centricity and datadriven decision-making.

Looking back at 2024, what would you consider the most significant technological achievement for the bank, and how did it contribute to our overall business goals and customer experience?

A most notable achievement was the implementation of a new seamless integration layer for digital banking users through our API strategy. This allowed customers to access their debit and credit cards with enhanced capabilities, including card alerts, activations, payments, and travel notices, which improved the customer experience by providing more control and convenience.

We made substantial strides in operational stability by delivering faster support for our associates through the deployment of Virtual Desktop Infrastructure (VDI), network enhancements, and a new IT Service Management platform. This ensured a more reliable and efficient operational environment, supporting our commitment to excellence in service delivery and operational efficiency.

We also hosted the inaugural Tech Day event for associates, which featured inspiring addresses from both our President and CIO, valuable industry insights from a keynote speaker from the Arkansas Bankers Association, and sessions with our esteemed partners highlighting cutting-edge technologies. The afternoon Expo offered hands-on demonstrations and interactive experiences. This event enhanced our associates' understanding of emerging technologies and their applications in banking. It also reinforced our commitment to leveraging technology to improve operational efficiency, drive growth, and deliver exceptional customer experiences.

What are some wins from your group this year and what impact did they have on the bank?

A significant win from our group this year was the successful implementation of portfolio management that has greatly improved transparency, accountability, and resource allocation within the department. As a result, the bank has experienced enhanced operational efficiency, better project prioritization, and more effective use of IT resources, ultimately leading to improved service delivery and customer satisfaction.

We’re focused on numerous initiatives, including APIs that would enable streamlined integration and the ability to bring in Fintechs as well as going through our significant data and analytics journey enabling improved customer experience, increased efficiency, improved decision-making and innovation. We are continuing strong investment in AI and other emerging technologies and these achievements will continue to have a profound impact on Simmons Bank.

Q&A with Alex Carriles

As Chief Digital Officer, Alex Carriles oversees Simmons’ digital banking strategy and customer experience through digital channels and tools.

Since 2019, you’ve been working with your team to provide customers greater access to digital products and services. What new customer-facing technologies or tools were implemented this year, and what impact did they have on customer experience?

In 2024 we were able to launch the first phase of Banno Business, the Mobile and Online banking platform with services for our Business Customers. This initial phase provides a better experience to manage multiple users and will allow us to expand early in 2025 to include more payments products.

We also delivered additional functionality to our Credit Card customers, allowing them to automate their recurring payments and to pay their card using external accounts.

For our Trust customers we included direct access from our Mobile App and Online Banking to the Black Diamond platform to manage their finances all in one place within the Simmons Bank digital tools.

Finally, we significantly expanded the accounts available to be opened online to make it easier for our customers and consumers to be able to bank with us whenever and wherever they want. By adding Simply Checking, Simply Savings, Classic Checking, Elevate Money Market and Certificates of Deposit to our account origination solution, we were able to more than double the number of accounts opened monthly starting the second half of the year.

For the last five years you have been leading Simmons’ digital transformation. This year Simmons was recognized as a class-leader for Identity and Fraud controls. Tell us about this recognition and what it means for our customers.

As I mentioned before, we are growing the number of accounts opened digitally, and in order to keep things manageable, we have developed a sophisticated process has provided significant protection against identity fraud, identity takeovers or synthetic identities when opening a new account digitally. This is a significant achievement, particularly considering this is where most banks are seeing fraud attacks due to their vulnerabilities. Our process was designed from the beginning with fraud controls in place, and the results show it has been being very effective. And all of this is taking place while making it easy and fast for customers to open an account online in under five minutes.

Q:

What are some wins from your group this year and what impact did they have on the bank?

Every year we continue to refine and improve our digital solutions for our customers, and that is reflected in the Net Promoter Score (NPS), which measures customer satisfaction. We ended 2024 with an NPS of 72.7, which is at the high end of the scale for digital banking. Additionally, the changes and improvements in our digital account-opening platform allowed us to grow by 103 percent on the second half of the year compared to 2023, and will allow us to continue expanding our online presence in all the states where we do business.

BETTER BANK INITIATIVE

Q&A with Chad Rawls

Chief Commercial Banking Officer Chad Rawls oversees commercial and corporate banking activities across the six-state footprint.

In 2024 Simmons strategically aligned its banking divisions to strengthen its connection with customers. Tell us how this change amplified our commercial customers’ success now and in the future.

In 2024, Simmons took a strategic approach to align its banking divisions, enhancing our ability to support our commercial customers in a more integrated and personalized way. This change allowed us to foster deeper relationships with our commercial customers, focusing on understanding their evolving goals and providing solutions that directly contribute to their success. Whether it's providing access to working capital, growth financing, or advanced digital tools, our new alignment enabled us to be more agile and responsive.

As a result, our commercial customers have been able to optimize their financial strategies, scale their businesses more efficiently, and navigate challenges with the confidence that Simmons is a true partner in their growth journey.

How has your team worked to strengthen customer relationships and enhance overall client experience across the footprint?

The Commercial team has always prioritized building strong, lasting relationships with our customers, and in 2024, we took an even more proactive, customer-centric approach to further enhance the overall client experience across our footprint. We empowered our bankers to engage more deeply with customers by truly understanding their business challenges, goals and opportunities. We've also invested heavily in Treasury Management technology, making it easier for clients to manage their money while also ensuring our customers feel supported at every touch point. This blend of personalized service, advanced technology, and deep industry knowledge has allowed us to strengthen relationships and deliver exceptional value to clients across the footprint.

Each state has its unique business landscape. What innovative solutions were introduced this year to help your team remain agile and effective across our six-state footprint?

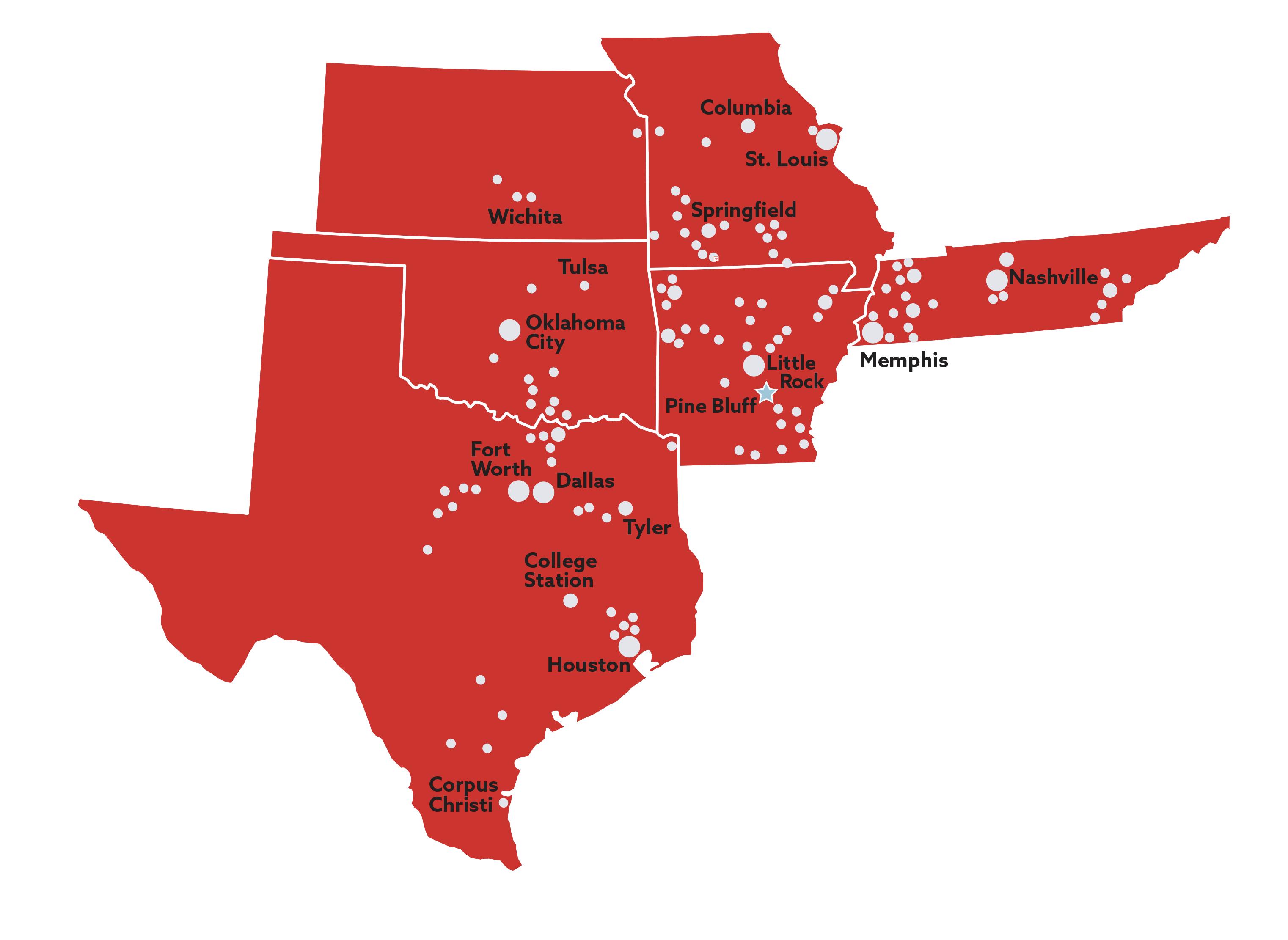

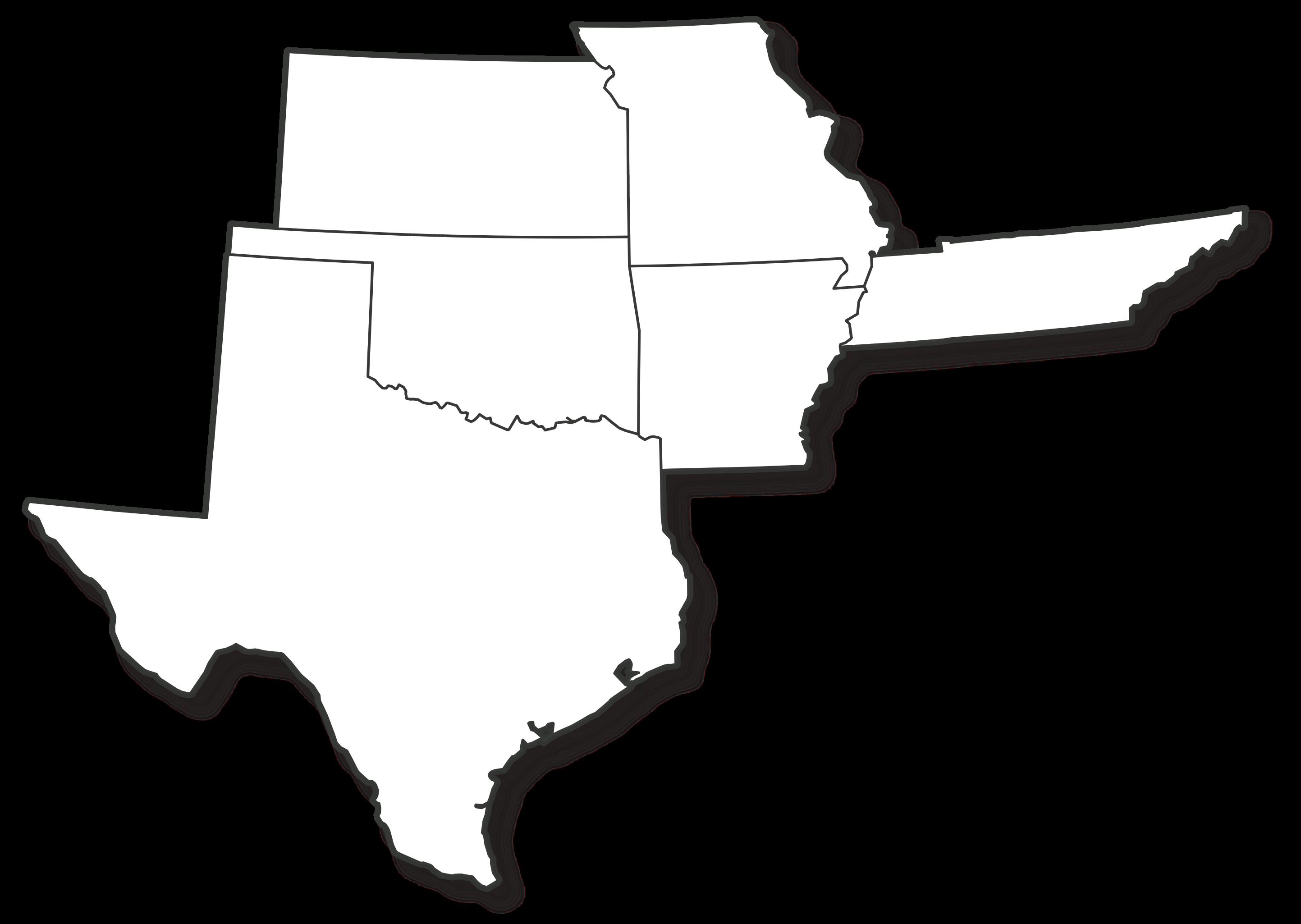

This year, we fully embraced the unique characteristics of each market within our footprint – from Houston to Nashville, St. Louis to Oklahoma City, Wichita to Little Rock. No two states have the same business landscape. To remain agile and effective, we empower local leaders to develop solutions tailored to the specific opportunities in their respective markets. This approach allows us to respond quickly to regional economic shifts, customer demands and industry trends.

At the same time, we encourage collaboration and knowledge-sharing among the team. By leveraging the diverse expertise across our footprint, we’ve been able to create best practices that can be adapted and scaled from market to market.

Q&A with Chris White

Chief Community Banking Officer Chris White oversees all community banking, mortgage, agriculture lending, consumer and branch business, as well as business development activities with responsibility for driving strategy and delivery of core banking services across Simmons' six-state footprint.

In 2024 Simmons strategically aligned its banking divisions to strengthen its connection with customers. Tell us how this change amplified our customers' success now and in the future. In January 2024, we implemented Community and Commercial Banking divisions. This restructure brought leaders closer to our customers and has allowed us to streamline processes to better serve our communities. In October 2024, we incorporated consumer, mortgage, contact center, and credit card functions into the Community Division. This alignment has enabled our associates to gain deeper insights into market trends and customer needs, empowering us to deliver tailored products and solutions across our entire footprint. With this structure, it also ensures our leaders across all business units share a unified strategic approach to hiring and retaining associates, while placing them in the roles best suited for their strengths.

You oversee production across several hundred communities and more than 200 branches. What innovative solutions were introduced this year to help your team remain agile and effective when servicing our customers?

Our Deposit Payment Optimization will continue to allow us to be more efficient when interacting with customers. We are implementing strategic partnerships for growing and retaining deposits, expanding payment channels to make it easy for customers to pay and transact with Simmons Bank while reducing manual efforts to support growth and scale.

We also introduced programs to increase branch revenue with add-on product sales to create a more consistent customer experience across the branch network. The goal is to provide a toolset that guides bankers and customers through a data-informed system. This system will enable bankers to engage in well-informed conversations with customers based on their responses and the extent of existing relationships, thereby increasing the number of appropriate products and services recommended.

As a top-25 farm lender in the U.S., Simmons has a storied history of supporting farmers in the communities we call home. How do you believe your department carried on this legacy in 2024? As the bank has grown, we remain committed to our customers especially our Agri communities. We moved up the ABA listing to #21 in the nation by strategically hiring Agri bankers in high-growth markets and by adding relationships across our footprint from South Texas to Northeast Arkansas. As we look to the future, we will continue to find ways to improve the approval and underwriting process to best serve our customers.

What are some wins from your group this year and what impact did they have on the bank?

We have had several wins from this group this year, but one that I am most proud of is the development of the Branch Banking Incentive plan. In 2024, a working group was formed to assess the compensation and incentive plan of the branch banking network at Simmons. As a result, we have developed and designed an incentive plan that is clear, competitive and rewarding for our Retail associates, which will drive even better service for our customers.

BETTER BANK INITIATIVE

Q&A with Joshua Jensen

Joshua Jensen joined Simmons in 2020 as Chief Deposit Officer. In addition to managing interest rate expense and Simmons’ liquidity, he constantly monitors changing economic conditions and the competitive environment to ensure we deliver an attractive rate to clients.

You oversee one of the most important areas for any bank – deposits. What are the main tactics your team used to drive deposit growth in the current market environment?

To help maintain and grow deposit volume, the team focused on customer service and improving the overall customer experience. We have seen significant success in our CD promotions, helping to further improve the savings for our consumer clients while deepening the relationship in what has been a very competitive deposit environment. Our integration of digital account opening for deposit accounts has also resulted in growth, providing clients the ease of opening and establishing a relationship with Simmons 24/7.

Simmons Bank is continuously looking to improve the products and services it offers customers. Business Banking was one of those areas for 2024. Tell us about the Business Banking enhancements you made this year for customers.

Our new Business Banking checking products launched in May 2024 – it was a complete success, driven by the partnership and coordination by multiple teams across Simmons. The products delivered a relationship focus – simplifying the customer’s account opening experience, streamlining the features and benefits with an easy-to-compare product guide, while also increasing the average account opening balance. Our customers are able to add banking services such as wires, ACH, and remote deposit seamlessly through the account opening experience, with the ability to digitally sign and approve those services – allowing our customers to do their banking at any time of day that is convenient for them.

Since your arrival four years ago, your team has grown to include Treasury Management. What advancements in Treasury Management have been made to enhance our customers’ success now and in the future?

Treasury Management is a critical focus for Simmons Bank, which has resulted in investments in people, technology, and processes. We have significantly improved our customer experience through an enhanced customer service team, secure messaging, and providing a white glove onboarding experience for our clients as they add new services. We are also investing in an expansion of new products and services for our clients, which will provide significantly enhanced functionality for our larger, more complex commercial clients who have unique and customized needs.

What are some wins from your group this year and what impact did they have on the bank?

Our Deposit Pricing team provided critical leadership in managing our deposit rates through the second half of the year, as rates were declining due to the Federal Funds rate cuts. Our diligence paid off, creating competitive rates to acquire and retain customers, driving cost savings to the bank, while our team provided additional support to our frontline groups with education and support on unique client needs.

Our Deposit Operations team provided significant support for our employees over the holiday season, helping to onboard and open over 200 new health savings accounts, helping our employees on their financial wellness journey.

We also saw significant wins for our business customers through the highly successful Business Banking deposit launch, approval to strategically improve our Treasury Management platform, and through deposit growth campaigns.

Q&A with Jimmy Crocker

As Executive Vice President for Wealth Management, Jimmy Crocker oversees more than 139 asscociates serving Simmons’ entire six-state footprint with nearly $8.5 billion in assets under management and custody.

Our 2024 focus was getting closer to the customer. What resonates with you about this focus and how does it impact Wealth?

Client service was a focus for Wealth in 2024 as well. We implemented a client segmentation and service standard program to ensure that all our clients were getting the attention and communication they deserve. This helped us monitor and measure our client outreach efforts, so that we can be more proactive with clients, get to know them better, and strengthen our relationships with them.

What unique challenges did your team face this year? How did you overcome those to ensure success for our clients?

It’s a continuing challenge to find individuals that possess the combination of technical knowledge and relationship skills that are required for us to be successful in this line of business. We were able to successfully fill several key positions in 2024. We also continue to build out our technology stack and compliance programs to allow us to be more efficient and effective in our service delivery.

For generations, our knowledgeable Wealth Management team has been a premier provider of trust, investment management and fiduciary services. How do you believe your team carries on this legacy? An effective Wealth Division requires a very particular set of skills. Our knowledge base requires an understanding of legal, accounting, and asset management concepts. Over the past five years, we have continued to upgrade our talent level, and have focused on hiring team members with more experience and qualifications, all the while committing to our existing team to provide education and professional designations that will help them be more effective advocates for our clients. We can say with confidence that the skills, experience, and credentials of our current team is the strongest that it has ever been.

What are some wins from your group this year and what impact did they have on the bank? 2024 was an especially successful year for Wealth at Simmons. Our investment performance was consistently strong across portfolios and strategies, and the strong financial markets meant that our clients had great outcomes with the growth of their assets, which in turn was positive for our topline revenue. Our teams across our footprint had great success implementing business development concepts that we put in place five years ago. As mentioned above, we had more face-to-face meetings with our clients than ever before, and our upgraded teams brought more estate and financial planning expertise than we would have been capable of in the past. This allowed us to bring in a record number of new client households, assets, and fees, resulting in a record year for new business.

Simmons Bank Championship: A Historic Success for Arkansas and PGA Tour Champions

The inaugural Simmons Bank Championship presented by Stephens, held in October in Little Rock’s Pleasant Valley Country Club, marked a historic milestone for both the state of Arkansas and the PGA Tour Champions.

The three-round competition, which ran from October 21-27, not only introduced Arkansas as a new host for a PGA-affiliated professional men’s golf tournament but also earned the prestigious 2024 Players Award, voted by the PGA Tour Champions players as their favorite event of the season. This recognition is a testament to the exceptional execution and player

experience provided by the tournament, making it just the second first-year event to receive the honor.

The Simmons Bank Championship was more than just a golf competition – it was a weeklong celebration of the sport, drawing significant excitement and attention to the Little Rock community. The event, which was also a key stop in the Charles Schwab Cup playoffs, featured the top 54 players in the PGA Tour Champions standings, competing for their share of a $2.3 million purse. Native Arkansas golfer, and Team Simmons Bank member, Ken Duke was among those in contention, adding to the local excitement.

SIMMONS BANK CHAMPIONSHIP

The Simmons Bank Championship was supported by local businesses and organizations, most notably the presenting sponsor, Stephens, an investment bank and wealth management firm with deep ties to the state. Curtis Jeffries, senior vice president and director of sports marketing at Stephens, emphasized the strong relationship between his company and Simmons Bank, noting that the event showcased Arkansas’s commitment to professional golf. The partnership between Simmons and Stephens was key in bringing the tournament to fruition, highlighting the strength of local collaboration.

The success of the event was built on a combination of careful planning, strong community engagement, and the stunning setting of the Pleasant Valley

Country Club. The course, a 7,100-yard par 71 layout, was a favorite among players and spectators alike. Tournament organizers, including Tournament Chairman Freddie Black, were quick to praise the club for its enthusiastic embrace of the event and its readiness to host such a major competition. The newly renovated clubhouse, which had undergone a $25 million overhaul, provided top-notch facilities, and the beautiful build-out around the lake created a spectacular backdrop for the final holes.

The tournament experience went beyond just a weekend of competition. The week included events such as women’s and junior golf clinics, pro-am tournaments, a dinner at the Governor’s Mansion, and Folds of Honor Friday. Player amenities included Parker Lexus courtesy vehicles, special outings for

Tournament Chairman Freddie Black addresses the crowd during Folds of Honor Friday.

SIMMONS BANK CHAMPIONSHIP

player families, as well as complimentary hotels for caddies. Tournament-goers were treated to kidfriendly zones, a tailgate party for the University of Arkansas football fans, extensive viewing areas and various public attractions, creating an atmosphere that echoed the excitement of a major championship. These activities helped engage the broader community and showcase Little Rock’s vibrant golf scene.

With Little Rock’s strong golfing community, the city proved to be an ideal location for a PGA Tour Champions event. Simmons Bank has committed to hosting the tournament for the next four years, ensuring that the success of the inaugural event will lay the groundwork for future tournaments.

Arkansas native and Team Simmons Bank Member Ken Duke participates in the final round of the PGA Tour Champions Simmons Bank Championship at Pleasant Valley Country Club in Little Rock on Sunday, Oct. 27, 2024.

PGA Tour Champions President Miller Brady received the Arkansas Traveler Certificate at a kickoff dinner at the Governor's Mansion.

Photo (left to right): George Makris, Jr., Miller Brady, Gov. Sarah Huckabee Sanders, Freddie Black

Golf Hall of Famer Padraig Harrington wins by two to capture inaugural title at Simmons Bank Championship.

MARKET HIGHLIGHTS

Six States, One Team

Since 1903, Simmons Bank has grown from a small community bank to a premier Mid-South bank spanning six states. With attention to service and detail, paired with a caring team, Simmons Bank is proud to provide a customer experience that exceeds expectations. Highlights from across the footprint illustrate the results.

Our Jonesboro team participated in the 2024 Women's Leadership Summit presented by Simmons Bank. This annual event, established by Arkansas Business Publishing Group, celebrated and inspired women in leadership with presentations from Arkansas-based women from a variety of industries.

Expanding our Reach

The newest Simmons Bank branch in Pine Bluff adds a fresh milestone to our 121-year history in the city. The new full-service branch provides customers with a full range financials services.

Our Fort Smith team hosted a grand reopening and ribbon-cutting of their newly renovated branch.

of Wisdom

At the annual Conway Chamber of Commerce meeting, Chairman George Makris, Jr. addressed a crowd of more than 1,000 guests as the keynote speaker. He shared his experience as a business owner and as chairman and CEO for Simmons Bank.

Simmons Bank CEO Bob Fehlman got soaked for a good cause at an event to honor Simmons First Foundation Chairman Tommy May. Inspired by the Ice Bucket Challenge, the CEO Soak engages business and community leaders to raise funds for finding a cure for ALS and to support people who fight the disease.

Words

CEO Soak

Community Commitment

Giving Back

After a devastating tornado ripped through the Northwest Arkansas community, our Simmons Bank team stepped up to help those impacted. The team cooked more than 600 hotdogs and hamburgers for tornado victims and volunteers.

Associates in El Dorado celebrated the 29th Simmons Bank Wildcat Invitational golf tournament at the Lions Club. Tournament participants included high schoolers from across south Arkansas.

Awards & Recognitions

U.S. News & World Report, “Best Companies to Work For in the South”

Arkansas Golfer, George Makris, Jr. named “ASGA Golfer of the Year”

Arkansas Business, Elizabeth Machen awarded “40 Under 40”

Arkansas Business, Justin McCarty named to "20 in Their Twenties"

United Way of Northeast Arkansas, AnnaLisa Meredith recognized with "Michael Nunnally Loaned Executive of the Year Award"

Little Rock Soirée Magazine, Christa Williams named a "Top Mortgage Professional 2024"

Paragould Board of Realtors, Dana Hedger received “Best Supporting Affiliate” Award

Pine Bluff Commercial, Simmons Bank named “Best Bank,” “Best Mortgage Company”

Employer Supporter of the Guard and Reserve, Cary Curzon receives "Patriot Award"

MARKET HIGHLIGHTS

Giving Back

Our Kansas associates participated in the 2024 Walk to End Alzheimer’s. Business Banker Chris Hemphill personally raised more than $1,000, earning her the ranking of Elite Champion for the Walk’s fundraising efforts.

Strong Partners

Our Olathe associates sponsored a coffee and networking event for the local Chamber of Commerce. The event was filled with residents, customers and chamber members, making for a successful networking time.

Pursuit of Growth

Associates from Wichita and Hutchinson, Kansas attended the Reno County Chamber of Commerce State of the City Breakfast Event, where they represented Simmons Bank while gleaning valuable insights from local leaders and speakers.

MARKET

Our Stillwater team and SFNC Board Member Russ Teubner participated in the groundbreaking ceremony for Block 34, a centralized gathering place and recreational space in downtown Stillwater. Building on Simmons’ $1.5 million commitment to support Block 34, the area will play host to a wide variety of events and feature a large green space known as the Simmons Bank Pavilion with gardens, seating areas, playgrounds, water features and more.

Community Commitment

Associates in Oklahoma City hosted a "Simmons Summer Bash" to celebrate the season with local vendors, giveaways and games. Community Ties

This year’s National Sand Bass Festival in Madill was a success as associates passed out Simmons-branded goods to attendees. This multi-faceted festival includes nightly concerts, carnival rides, contests and vendors for food, arts, crafts, and turtle races.

Simmons associates attend the rivalry football game between East Central University (ECU) and Southeastern Oklahoma State University in Ada. Simmons is the Presenting Sponsor for all sports games held at ECU between these in-state rivals, now known as the Great American Classic Game Series. A Simmonsbranded trophy is presented to the winning team at the end of the game.

Healthy Competition

MARKET HIGHLIGHTS

Expansion of Service

Associates in Kansas City hosted a ribbon cutting to unveil a new regional office. The 16,500-square-foot financial center features a full-service branch with a suite of services for commercial, business and individual customers in the region.

Community Ties

Simmons Bank leaders Krista Walker and Christian Lewis took a pie in the face to cheer on their teams’ efforts for raising more than $1,000 for Springfield public schools.

Our Columbia team was honored to receive the “Flag of the United States of America Committee Certificate Award” from the Daughters of the American Revolution. For more than 30 years, this financial center has proudly displayed a 15-by-30foot flag on special occasions and this unifying display has become a cherished tradition in the community

Allan Ivie Receives Civic Leadership Award

Allan Ivie, who serves as Private Wealth regional president for Missouri, Kansas, and Oklahoma, was recognized by the Urban League of Metropolitan St. Louis (ULSTL) and Saint Louis University with the organizations’ Civic Leadership Award. The award honors Allan’s “significant contributions in overcoming racial barriers throughout his impactful career.”

Generous Hearts

Better Together

Giving Back

Our team in Mountain View joined local educational partners to mark the opening of the Mountain View-Birch Tree School District’s new administration building, which was donated by Simmons Bank. This building stands as a testament to our company’s commitment to the community.

Our Columbia associates showed their support for Access Arts, a local arts organization, by participating in the organization’s fundraising event.

Awards & Recognitions

Pursue Growth

Through his involvement with the Springfield Area Chamber of Commerce, Christian Lewis connected with Missouri Governor Mike Parsons, local leaders and lawmakers to discuss policy impacts on the business community.

Forbes, Simmons Bank named to "America's Best-in-State Employers" list for Missouri

Urban League of Metropolitan St. Louis and Saint Louis University, Allan Ivie received “Civic Leadership Award”

Columbia Chamber of Commerce, Garrett Walker receives "Emerging Professional of the Year" Award

Connections to Success, Alonzo Shaw receives "Tribute Honoree" recognition

MARKET HIGHLIGHTS

Tennessee

Strong Partners

Honoring Veterans

Associates in Memphis assisted the Midsouth Veterans League with the installation of a traveling Vietnam Memorial. Our team helped assemble the wall to ensure the community could view the memorial to honor veterans.

The team in Middle Tennessee participated in the Inaugural Hendersonville Firefighters Association Golf Tournament by sharing Simmons Bank branded products with over 100 golfers and first responders on the course.

Better Together

Inspiring Generations

Our Martin team spoke to over 400 students about different career opportunities in banking during the Dresden Middle School's Career Day.

Our Southeast Tennessee team shared their Better Together spirit by sponsoring a Blount County Habitat for Humanity Home. Associates spent time volunteering and working on the home by building a ramp, assembling siding and even raising a wall.

Simmons Bank Open

The Simmons Bank Open – the 2022 Korn Ferry Tour Tournament of the Year – returned to Franklin at a new venue. During Foundation Friday, The Simmons First Foundation awarded checks of $10,000 each to two well-deserving nonprofits, The Refuge Center and Water Walkers.

Giving Back

Our Retail associates from Dresden and Martin teamed up to feed approximately 150 educators and educational board members from Dresden Elementary School, Dresden Middle School and Dresden High School.

Awards & Recognitions

Forbes, Simmons named to "Best-in-State Bank" list for Tennessee

Nashville Chamber of Commerce, Kristen Pickens named an "Emerging Leader in Finance"

Gallatin Rotary Club, Cherie Cline named "Rotary Rookie of the Year 2024"

Daily Post-Athenian, Simmons Bank named to top-three "Best Banks" and Stephanie Ghorley named to top-three "Best Tellers"

White House Chamber of Commerce, Kate Key received “The Horizon Award”

Lexington Progress, Simmons Bank voted “The Best Bank” in Readers Choice Awards

MARKET HIGHLIGHTS

Texas

Better Together

Our Simmons Bank team was proud to serve as an official sponsor of the Executive Women's Day at the Charles Schwab Challenge. Women leaders across the Dallas and Fort Worth markets joined tennis legend Martina Navratilova to support The Women's Center of Tarrant County and the Boys and Girls Club of Greater Tarrant County through Fort Worth Colonial Charities.

Giving Back

Brewing Loyalty

The Fort Worth team hosted a record-breaking “Coffee with the Chamber” event with the Fort Worth Hispanic Chamber of Commerce when more than 250 attendees showed for the monthly networking event.

Sharing Knowledge

Our Dallas team joined Junior Achievement to impact the next generation's lives through financial literacy classes. Associates attended the JA Biztown event to help equip young people with financial education through a real-world simulation.

Associates in College Station attended a groundbreaking ceremony to kick off construction of a new warehouse and donation center for Twin City Mission, a project financed by Simmons Bank. This new facility will help with distribution of donations to support community members in need, including those facing homelessness, domestic violence and poverty.

Building Loyalty

In Mabank, our team provided back-to-school goodie bags to the 177 new teachers in the area schools. Community Ties

Associates in Frisco hosted a breakfast for the National Breast Cancer Foundation in Frisco. The event supported a worthy cause while allowing the team to show appreciation for community partners and clients.

Awards & Recognitions

Community Pride

Associates in Sherman hosted a “Coffee with the Mayor” event to connect with community members and local leaders. The mayor and city communications director were on hand to walk participants through exciting projects underway in the area.

Herald Democrat, Aleesha Lance named "Best Bank Teller"

Hispanic Women's Network of Texas, Monica Flores receives "Estrella de Tejas" Award

Business and Community Lenders of Texas, Stacy Bowers awarded “Excellence in Small Business and Entrepreneurship Award”

CULTURE

Defining Our Culture

As Simmons Bank continues to grow, we have focused on the importance of our culture through continuing education, recognizing exceptional work and celebrating the strength of our associates. Building a vibrant culture and living in accordance with our values directly translates to customer service excellence and loyalty and will fulfill our vision of making Simmons Bank a great place to work. Since 1903, these values have set our Simmons Bank team apart in every community we serve.

Simmons Bank has six Culture Cornerstones that guide how Simmons serves our customers, our team and our communities.

Each September associates across the bank's footprint participate in Simmons Service Month, a companywide initiative to encourage volunteerism. Simmons gave all associates paid time off in September to volunteer, and associates notched the highest-ever achievement for volunteer hours, serving over 7,659 volunteer hours, donating 6,252 items, and contributing more than $29,000 in donations to charities.

Simmons associates who donated 15 or more volunteer hours during Simmons Service Month also received $150 for charities of their choice.

Simmons Bank Service Month

Simmons Associates: By the Numbers

At Simmons, we are focused on delivering on the promise of being a great place to work. We actively promote an environment where all associates have the opportunity to achieve personal success.

Training and Development

Associates at Simmons Bank completed 47,761 hours of training and development in 2024. On average, each associate completes more than 16 hours of training.

Associates across the bank are required to complete risk and compliance courses to be aware and accountable for risk management.

Simmons offers its associates a variety of education classes, including the following training courses:

Data Governance

Ethics at Simmons Bank

Financial Abuse of Elders: Common Schemes

General Cybersecurity Training

HIPAA-HITECH Requirements

Identity Theft Red Flags

Identity Theft: Minimize the Risk

Internal Controls

Internet Security Essentials for Financial Institutions

OFAC: Addressing Risks and Red Flags

Outgoing Domestic Wire Module Procedures

Password Security Awareness

Personally Identifiable Information (PII) & Sensitive

Information

Phishing Awareness

Preparing for an Active Shooter in the Workplace

Recognizing UDAAP Risks

Robbery Training

Segregation of Duties

Workplace Violence

CULTURE

Simmons First Foundation

Providing support to the communities we serve is foundational to who we are at Simmons Bank. Since 2014, Simmons First Foundation has provided support for youth access to health care and education and aiding low-to-moderate income families. Funding requests come to the Foundation from leaders across the footprint initiating grant requests based on the needs in their communities.

Since 2014, Simmons Bank contributed approximately $17.9 million to the foundation.

In 2024, Simmons First Foundation provided grants totaling more than $794,000 across our footprint.

Map Key

Make a Difference grants

Mini grants

Environmental grants

Community Enhancement grants

The Foundation created a new $3 million endowment in 2021 to support environmentally focused grants to aid conservation and sustainable projects. This year, $119,000 in environmental grants were provided.

In 2024, Simmons First Foundation presented The Allen School in Little Rock with a $25,000 grant to support its Sensory Gym Retrofit project. This grant allowed the school to renovate the gym to make it a safe, fun environment for the children to use during therapy sessions.

In today’s fast-paced environment, maintaining a strong, cohesive workforce across multiple states is essential. Simmons Bank is committed to fostering a culture of collaboration and engagement within its associate base, and the Town Halls represented a key initiative to strengthen those ties with local teams.

In 2024, members of the Executive Team traveled to more than 18 locations across five states. These visits by the Executive Team are not just about leadership visibility – they represent a vital opportunity for reinforcing company culture, driving alignment, and creating a shared sense of purpose. By strengthening connection across the footprint, the Town Halls will play a key role in the bank’s continued success and growth, helping every associate feel empowered and motivated to achieve their best.

Simmons Bank Town Halls

CULTURE

Undercover Boss

As he himself will tell you, Jay Brogdon, president of Simmons Bank, learned the industry in reverse of the typical bank executive.

Brogdon’s commitment to seeing the bank through the lens of Main Street has taken different tactics, one of the most unique of which happened in the spring when he spent April Fool’s Day observing associates of a busy retail branch go about their day. He came away impressed by what he saw.

While he did not actually work a counter window, (“We considered that and felt like the cost-benefit wasn’t there for me to have fingers on the keyboard,” he said.) Brogdon came away with a new perspective about what worked well in serving customers and what could be improved.

Brogdon said he continues to seek personal face time across different banking units as a means for sharpening his firsthand understanding of the bank’s systems and processes.

What our associates do in the branch every day is an incredibly challenging job. I didn’t walk in there thinking it was an easy job, but I have a much different appreciation for how challenging the job is. The most encouraging thing I got out of that day was seeing the quality of our people, and the biggest takeaway was the quality of service they provide to our customers.

– Jay Brogdon President

CORPORATE RESPONSIBILITY

Simmons Bank Helps Customers Save More Than $6 Million in "Change"

Through the Simmons Bank automatic savings program, Round-Up, customers saved more than $6 million during 2024. More than 25,000 customers utilized the program during this period.

Sustainability by the numbers

Simmons Bank’s environmentally conscious renovations have helped us reduce greenhouse gasses across our footprint.

Equivalent of 49,105 kWh saved

Equivalent to eliminating 7.5 cars from the roadways

Equivalent to eliminating 3,410 gallons of gas

LED lighting and retrofits have eliminated 44.19 metric tons of carbon dioxide

In 2024, more than 1 million pounds of paper were recycled through our partnership with Shred-it vendor.

Equivalent to eliminating environmental impact of 5.2 homes

Equivalent to eliminating more than 38,256 in pounds of coal burned

Equivalent of 8,796 trees saved

Equivalent of 1,544 cubic yards of landfill space saved

More than 3.6 million gallons of water saved

Simmons Bank implemented the recycling program, K-Cycle, for coffee grounds and K-cups in 2019. In 2024, more than 336.9 pounds of used K-cups and coffee grounds were recycled.

Branch Optimization

Over the last four years, Simmons has utilized a branch rationalization strategy that allow us to leverage data to assist us in creating a more efficient branch distribution network, while also reflecting our customers evolving needs as to how and where they want to bank. As a result, we were able to eliminate approximately:

1,021 metric tons of carbon dioxide in 202410

4,327 metric tons of carbon dioxide since 202010

CORPORATE RESPONSIBILITY

Community Reinvestment

Simmons Bank’s Community Reinvestment Act (CRA) efforts focus on affordable housing, economic development, revitalization and community service – each with a goal of providing greater access to financial products and services in low-to-moderate-income communities and families.

In 2024, Simmons Bank originated approximately 3,144 in single-family Home Mortgage Disclosure Act (HMDA) loans totaling approximately $716,780,969.9.

Simmons Bank provided more than 20 multi-family HMDA loans which totaled approximately $32,720,714.50 in 2024.

Combined, Simmons Bank provided approximately $749,501,684.49 in HMDA reportable loans in 2024. Simmons Bank originated more than 622 loans within low-to-moderate-income areas, or 21.15 percent of total originations. ($104,771,343.92)

Simmons Bank originated nearly 578 loans within majority-minority geographies or 19.65 percent of total originations. ($109,630,790.09)

Simmons Bank and Simmons First Foundation provided approximately $2,987,908 in eligible charitable donations, and foundation grants in 2024, including 15 community enhancement grants ($125,000), 29 make a difference grants ($402,241), five environmental grants ($51,294) and nine organization grants ($172,873) from the Foundation to organizations that offer work readiness programs, affordable housing, and community services.

Simmons provided $1.5 million to Stillwater, Oklahoma’s Block 34 initiative – the development of a lowincome census tract in downtown Stillwater for public space, including a music sound stage, pavilion, children’s playground, historical music green space, and mobile vendor spaces to support small businesses. Through the Federal Home Loan Bank of Dallas, the Bank secured, for our nonprofit community partners, $1,800,568 in Federal Home Loan Bank contributions in 2024 for; downpayment assistance, home rehabilitation, construction of affordable housing, operating grants, and Fortified roof repairs.

Simmons Bank provided approximately $7,413,237 in Community Development Investments under the Community Reinvestment Act in 2024.

Simmons provided approximately $724,517,281 in qualified community development loans (238 loans) furthering economic development, affordable housing and stabilization of communities in 2024.

Simmons provided $23 million to a CDFI (Arkansas Capital Corporation) to promote economic growth within the state of Arkansas.

Simmons Bank provided $1.5 million to Builders of Hope to construct five affordable homes within the Valwood Park Community with Dallas MSA.

The bank provided $2 million to Mayberry LLC supporting the Midtown Redevelopment Authority in Houston to construct affordable housing.

Simmons Bank provided approximately 2,680 loans benefiting businesses with less than $1 million in revenue totaling approximately $307,967,000 in 2024, of which 556 (21%) originated within low-tomoderate income census tracts.

Simmons Bank provided approximately 1,203 loans benefiting small farms with less than $1 million in revenue totaling approximately $115,232,000 in 2024, of which 216 (18%) originated within low-tomoderate income census tracts.

Commitment to the Community

Simmons’ associates performed approximately 1,653 community development service activities, including offering financial education to adults and children and extending technical services in 2024.

Simmons’ reach spanned across 211 nonprofit organizations.

Product Spotlights

Simmons Bank offers a variety of products to help ensure that our customers are served well.

Our Bank On-certified Affordable Advantage Checking Product:

Serving 1,328 account holders in 2024.

Includes safeguards against overdrafts.

The Individual Taxpayer Identification Number (ITIN) Mortgage Product was introduced:

An ITIN Advantage Mortgage is a loan designed for homebuyers who do not have a Social Security number.

In 2024, Simmons Bank funded approximately $18,485,392 (93 loans) of ITIN Advantage Mortgages

Strong production continued with the 100% Advantage Mortgage Product:

In 2024, Simmons Bank funded approximately $8,008,355 (46 loans) of 100% Advantage Mortgages

Simmons Bank worked with more than 11 down-payment-assistance programs across our footprint to lessen the burden of homeownership.

The launch of the Foundation Secured Credit Card in 2021 provided customers the opportunity to open a secured credit card that is designed to help them establish, strengthen or rebuild their credit:

In 2024, Simmons Bank funded 128 Credit Builder loans, also designed to help establish, strengthen and rebuild credit; 50 were originated in majority minority geographies (39%) and 45 within low-to-moderateincome geographies (35%).

The Affordable Advantage Emergency loan was designed to aid in shortcomings for family emergencies, such as roof repairs, medical expenses, or HVAC or heating needs. In 2024, Simmons Bank originated 427 loans where 165 loans penetrated low-to-moderate income geographies (39%) and 120 loans penetrated majority minority geographies (28%).

CORPORATE RESPONSIBILITY

Governance – Board of Directors

Marty D. Casteel

RETIRED CHAIRMAN, PRESIDENT & CHIEF EXECUTIVE OFFICER, SIMMONS BANK

Susan Lanigan

RETIRED EXECUTIVE VICE PRESIDENT AND GENERAL COUNSEL, CHICO’S FAS, INC.

William E. Clark, II FOUNDER AND CEO, CLARK CONTRACTORS, LLC

George A. Makris, Jr. CHAIRMAN AND CHIEF EXECUTIVE OFFICER, SIMMONS FIRST NATIONAL CORPORATION

Steven A. Cossé

RETIRED PRESIDENT & CHIEF EXECUTIVE OFFICER, MURPHY OIL CORPORATION

Tom Purvis PARTNER, L2L DEVELOPMENT ADVISORS, LLC

CHIEF FINANCIAL OFFICER, STEPHENS INC.

Robert L. Shoptaw

RETIRED EXECUTIVE, ARKANSAS BLUE CROSS & BLUE SHIELD

Independence Diversity

93%

23% of directors are independent1 of independent directors are women1

Mark C. Doramus

38%

Edward Drilling

RETIRED SENIOR VICE PRESIDENT, EXTERNAL AND REGULATORY AFFAIRS, AT&T, INC.

Julie Stackhouse

RETIRED EXECUTIVE VICE PRESIDENT, FEDERAL RESERVE BANK OF ST. LOUIS

Jerry Hunter

SENIOR COUNSEL, BRYAN CAVE LEIGHTON PAISNER, LLP

Russell W. Teubner

DISTINGUISHED ENGINEER, BROADCOM, INC.

EXECUTIVE VICE PRESIDENT & CHIEF OPERATING OFFICER, MURPHY USA, INC. Tenure

10.4 years (average tenure)

0-5 Years

of independent directors are women and minorities1

6-10 Years 11-15 Years 15+ Years

Mindy West

FINANCIAL HIGHLIGHTS 2024

Regulatory Capital and Asset Quality

Allowance for Credit Losses as a % of Total Loans AT DECEMBER 31, 2024 AT DECEMBER 31, 2024

Nonperforming Assets as a % of Total Assets

Allowance for Credit Losses as a % of Nonperforming Loans

REGULATORY “MINIMUM”

REGULATORY “WELL-CAPITALIZED”

SIMMONS FIRST NATIONAL CORPORATION

115 Consecutive Years Of Paying Dividends To Our Shareholders

PER SHARE4,5 YEARS ENDED DECEMBER 31

On January 30, 2025, Simmons announced that its board of directors declared a quarterly cash dividend on Simmons Class A common stock of $0.2125 per share. The indicated annualized cash dividend rate of $0.85 for 2025 represents a 10-year compound annual growth rate of 6 percent and marks the 116th consecutive year that Simmons has paid cash dividends.

According to research by Dividend Power, Simmons is one of only 26 publicly traded companies (listed below) that have paid dividends for 100-plus uninterrupted years.

3M Company

Abbott Laboratories

American Electric Power Company

Chubb Limited

Church & Dwight Co.

Colgate-Palmolive Company

Consolidated Edison

DuPont de Numours, Inc.

Edison International

Eli Lilly and Company

Exxon Mobil Corporation

Farmers & Merchants Bank of Long Beach

GATX Corporation

General Mills

International Business Machines Corporation

Johnson Controls International

National Fuel Gas Company

PPG Industries

Stanley Black and Decker

The Coca-Cola Company

The Procter & Gamble Company

The Timken Company

The York Water Company

UGI Corporation

Union Pacific Corporation

2025 also marks the 14th consecutive year that Simmons has increased its dividend, earning it Dividend Power’s designation as a “Dividend Contender,” a title exclusively for companies that have increased their dividend for 10 to 24 consecutive years. As of January 17, 2025, Dividend Power research noted that Simmons is one of only 343 companies out of nearly 6,000 companies listed on the New York Stock Exchange and NASDAQ to achieve this distinction.

FINANCIAL HIGHLIGHTS 2024

1 YEAR TOTAL SHAREHOLDER RETURN

DIVIDENDS + STOCK APPRECIATION | DECEMBER 31, 2023 — DECEMBER 31, 2024

LONG-TERM TOTAL SHAREHOLDER RETURN

DIVIDENDS + STOCK APPRECIATION | DECEMBER 31, 2007 — DECEMBER 31, 2024

FINANCIAL HIGHLIGHTS 2024

CONDENSED CONSOLIDATED BALANCE SHEETS AT DECEMBER 31 | $ IN THOUSANDS

ASSETS

Cash and cash equivalents

Investment securities

Mortgage loans held for sale

Loans

Allowance for loan losses

NET LOANS

Premises and equipment

Foreclosed assets

Goodwill and other intangible assets

Bank owned life insurance

Other assets

TOTAL ASSETS

LIABILITIES AND STOCKHOLDERS’ EQUITY

Noninterest bearing deposits

Interest bearing transaction accounts

Time deposits

TOTAL DEPOSITS

Federal funds purchased and securities sold under agreements to repurchase

Certain statements contained in this Company Report may not be based on historical facts and should be considered “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements may be identified by reference to a future period(s) or by the use of forward-looking terminology, such as “anticipate,” “believe,” “budget,” “contemplate,” “continue,” “estimate,” “expect,” “foresee,” “intend,” “indicate,” “likely,” “target,” “plan,” “positions,” “prospects,” “project,” “predict,” or “potential,” by future conditional verbs such as “could,” “may,” “might,” “should,” “will,” or “would,” by variations of such words or by similar expressions. These forward-looking statements include, without limitation, those relating to Simmons First National Corporation’s (“Company,” “we,” “us,” or “our”) future growth, business strategies, product development, acquisitions and their expected benefits, revenue, expenses, assets, asset quality, profitability, earnings, accretion, dividends, customer service, lending capacity and lending activity, loan demand, deposit levels, investment in digital channels, critical accounting policies and estimates, net interest income, net interest margin, noninterest income, non-interest expense, the Company’s stock repurchase program, consumer behavior and liquidity, the Company’s ability to recruit and retain key employees, the adequacy of the allowance for credit losses, the estimated cost savings associated with the Company’s Better Bank Initiative, income tax deductions, credit quality, the level of credit losses from lending commitments, net interest revenue, interest rates and interest rate sensitivity (including, among other things, the impact of rising or declining interest rates), economic conditions, repricing of loans and time deposits, loan loss experience, liquidity, the Company’s expectations regarding actions by the Federal Home Loan Banks (“FHLB”) and other agencies, capital resources, the expected expenses and cost savings associated with branch closures, market risk, plans for investments in (and cash flows from) securities and investment portfolio strategies, effect of pending and future litigation, staffing initiatives, estimated cost savings associated with the Company’s early retirement program and Better Bank Initiative, legal and regulatory limitations and compliance, and competition. These forward-looking statements are based on various assumptions and involve inherent risks and uncertainties, and may not be realized due to a variety of factors, including, without limitation: changes in the Company’s operating, acquisition, or expansion strategy; the effects of future economic conditions (including unemployment levels and slowdowns in economic growth), governmental monetary and fiscal policies (including the policies of the Federal Reserve), as well as legislative and regulatory changes; general business conditions, as well as conditions within the financial markets, developments impacting the financial services industry, such as bank failures or concerns involving liquidity; changes in real estate values; changes in interest rates and related governmental policies; changes in liquidity, and the availability of and costs associated with obtaining adequate and timely sources of liquidity; increased inflation; changes in tariff policies; changes in the level and composition of deposits, loan demand, deposit flows, and the values of loan collateral, securities and interest sensitive assets and liabilities; changes in credit quality; actions taken by the Company to manage its investment securities portfolio; changes in the securities markets generally or the price of the Company’s common stock specifically; changes in the assumptions used in making the forward-looking statements; developments in information technology affecting the financial industry; cyber threats, attacks or events, including at third parties on which we rely for key services; reliance on third parties for the provision of key services; the ability to collect amounts due under loan agreements; further changes in accounting principles relating to loan loss recognition; the costs of evaluating possible acquisitions and the risks inherent in integrating acquisitions; possible adverse rulings, judgements, settlements, fines and other outcomes of pending or future litigation or government actions; market disruptions, including pandemics or significant health hazards, severe weather conditions, natural disasters, terrorist activities, financial crises, political crises, war and other military conflicts (including the ongoing military conflicts between Russia and Ukraine) or other major events, or the prospect of these events; changes in customer behaviors and preferences, including consumer spending, borrowing, and saving habits; the soundness of other financial institutions and indirect exposure related to the closings of other financial institutions and their impact on the broader market through other customers, suppliers and partners (or that the conditions which resulted in the liquidity concerns that led to the large regional bank failures during 2023 may also adversely impact, directly or indirectly, other financial institutions and market participants with

which the Company has commercial or deposit relationships); the loss of key employees; increased unemployment; labor shortages; the Company’s ability to manage and successfully integrate its mergers and acquisitions to fully realize cost savings and other benefits associated with those transactions; increased delinquency and foreclosure rates on commercial real estate and other loans; the effects of government legislation; the effects of competition from other commercial banks, thrifts, mortgage banking firms, consumer finance companies, credit unions, securities brokerage firms, insurance companies, money market and other mutual funds, and other financial institutions operating in our market area and elsewhere, including institutions operating regionally, nationally, and internationally, together with such competitors offering banking products and services by mail, cellphone/tablet, telephone, computer, and the internet; the failure of assumptions underlying the establishment of reserves for possible credit losses, fair value for loans, other real estate owned, and those factors set forth from time to time in the Company’s press releases and filings with the U.S. Securities and Exchange Commission (“SEC”), including, without limitation, the Company’s Form 10-K for the year ended December 31, 2024 (which has been filed with, and is available from, the SEC). Many of these factors are beyond our ability to predict or control, and actual results could differ materially from those in the forward-looking statements due to these factors and others. In addition, as a result of these and other factors, our past financial performance should not be relied upon as an indication of future performance.

We believe the assumptions and expectations that underlie or are reflected in our forward-looking statements are reasonable, based on information available to us on the date hereof. However, given the described uncertainties and risks, we cannot guarantee our future performance or results of operations or whether our future performance will differ materially from the performance reflected in or implied by our forward-looking statements, and you should not place undue reliance on these forward-looking statements. Any forward-looking statement speaks only as of the date hereof, and we undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, and all written or oral forward-looking statements attributable to us are expressly qualified in their entirety by this section.

NON-GAAP FINANCIAL MEASURES

This Company Report contains financial information determined by methods other than in accordance with U.S. generally accepted accounting principles (“GAAP”). The Company’s management uses these non-GAAP financial measures in their analysis of the Company’s performance. These measures adjust GAAP performance measures to, among other things, include the tax benefit associated with revenue items that are tax-exempt, as well as exclude from net income (including on a per share diluted basis), pretax, pre-provision earnings, net charge-offs, income available to common shareholders, non-interest income, and non-interest expense certain income and expense items attributable to, for example, merger activity (primarily including merger-related expenses and Day 2 CECL provisions), gains and/or losses on sale of branches, net branch right-sizing initiatives, loss on redemption of trust preferred securities, gain on sale of intellectual property, FDIC special assessment charges and gain/loss on the sale of AFS investment securities. In addition, the Company also presents certain figures based on tangible common stockholders’ equity, tangible assets and tangible book value, which exclude goodwill and other intangible assets. The Company further presents certain figures that are exclusive of the impact of deposits and/or loans acquired through acquisitions, mortgage warehouse loans, and/or energy loans, or gains and/or losses on the sale of securities. The Company’s management believes that these non-GAAP financial measures are useful to investors because they, among other things, present the results of the Company’s ongoing operations without the effect of mergers or other items not central to the Company’s ongoing business, as well as normalize for tax effects. Management, therefore, believes presentations of these non-GAAP financial measures provide useful supplemental information that is essential to a proper understanding of the operating results of the Company’s core businesses. These nonGAAP disclosures should not be viewed as a substitute for operating results determined in accordance with GAAP, nor are they necessarily comparable to non-GAAP performance measures that may be presented by other companies. Where non-GAAP financial measures are used, the comparable GAAP financial measure, as well as the reconciliation to the comparable GAAP financial measure, can be found in the sections of this Company Report titled “Reconciliation of Non-GAAP Financial Measures.”