“c05AggregateSupplyPolicies_PrintPDF” — 2022/6/14 — 4:32 — page 420 — #36

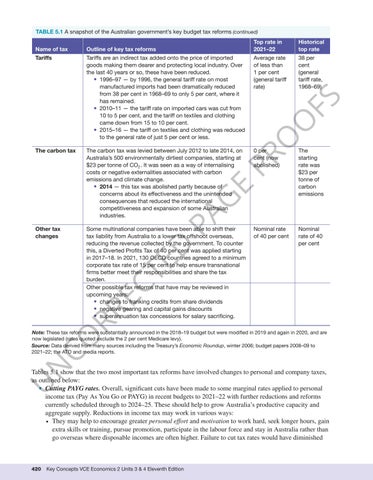

TABLE 5.1 A snapshot of the Australian government’s key budget tax reforms (continued) Historical top rate

Tariffs are an indirect tax added onto the price of imported goods making them dearer and protecting local industry. Over the last 40 years or so, these have been reduced. • 1996–97 — by 1996, the general tariff rate on most manufactured imports had been dramatically reduced from 38 per cent in 1968–69 to only 5 per cent, where it has remained. • 2010–11 — the tariff rate on imported cars was cut from 10 to 5 per cent, and the tariff on textiles and clothing came down from 15 to 10 per cent. • 2015–16 — the tariff on textiles and clothing was reduced to the general rate of just 5 per cent or less.

Average rate of less than 1 per cent (general tariff rate)

38 per cent (general tariff rate, 1968–69)

The carbon tax

The carbon tax was levied between July 2012 to late 2014, on Australia’s 500 environmentally dirtiest companies, starting at $23 per tonne of CO2 . It was seen as a way of internalising costs or negative externalities associated with carbon emissions and climate change. • 2014 — this tax was abolished partly because of concerns about its effectiveness and the unintended consequences that reduced the international competitiveness and expansion of some Australian industries.

0 per cent (now abolished)

The starting rate was $23 per tonne of carbon emissions

Other tax changes

Some multinational companies have been able to shift their tax liability from Australia to a lower tax offshoot overseas, reducing the revenue collected by the government. To counter this, a Diverted Profits Tax of 40 per cent was applied starting in 2017–18. In 2021, 130 OECD countries agreed to a minimum corporate tax rate of 15 per cent to help ensure transnational firms better meet their responsibilities and share the tax burden. Other possible tax reforms that have may be reviewed in upcoming years: • changes to franking credits from share dividends • negative gearing and capital gains discounts • superannuation tax concessions for salary sacrificing.

Nominal rate of 40 per cent

Nominal rate of 40 per cent

O

Tariffs

CO RR EC

TE

D

PA

G

E

PR O

Outline of key tax reforms

FS

Top rate in 2021–22

Name of tax

N

Note: These tax reforms were substantially announced in the 2018–19 budget but were modified in 2019 and again in 2020, and are now legislated (rates quoted exclude the 2 per cent Medicare levy). Source: Data derived from many sources including the Treasury’s Economic Roundup, winter 2006; budget papers 2008–09 to 2021–22; the ATO and media reports.

U

Tables 5.1 show that the two most important tax reforms have involved changes to personal and company taxes, as outlined below: • Cutting PAYG rates. Overall, significant cuts have been made to some marginal rates applied to personal income tax (Pay As You Go or PAYG) in recent budgets to 2021–22 with further reductions and reforms currently scheduled through to 2024–25. These should help to grow Australia’s productive capacity and aggregate supply. Reductions in income tax may work in various ways: • They may help to encourage greater personal effort and motivation to work hard, seek longer hours, gain extra skills or training, pursue promotion, participate in the labour force and stay in Australia rather than go overseas where disposable incomes are often higher. Failure to cut tax rates would have diminished

420

Key Concepts VCE Economics 2 Units 3 & 4 Eleventh Edition