Sales Are Up, But Inventory Scales Faster, Leading To Mixed Conditions

COMMUNITY UPDATES

SouthPark

Myers Park & Eastover

Lake Wylie & The Palisades

Providence, Weddington & Waxhaw

Ballantyne & South Carolina

Center City Luxury Condos & Townhomes

FORECAST

Fiscal Uncertainty And Inventory Increases

Drive A More Balanced Luxury Market

PODCAST & VIDEOS

From market forecasts, interviews, and marketing ideas, join the team at Ivester Jackson I Christie's for the latest in the Carolinas luxury real estate content

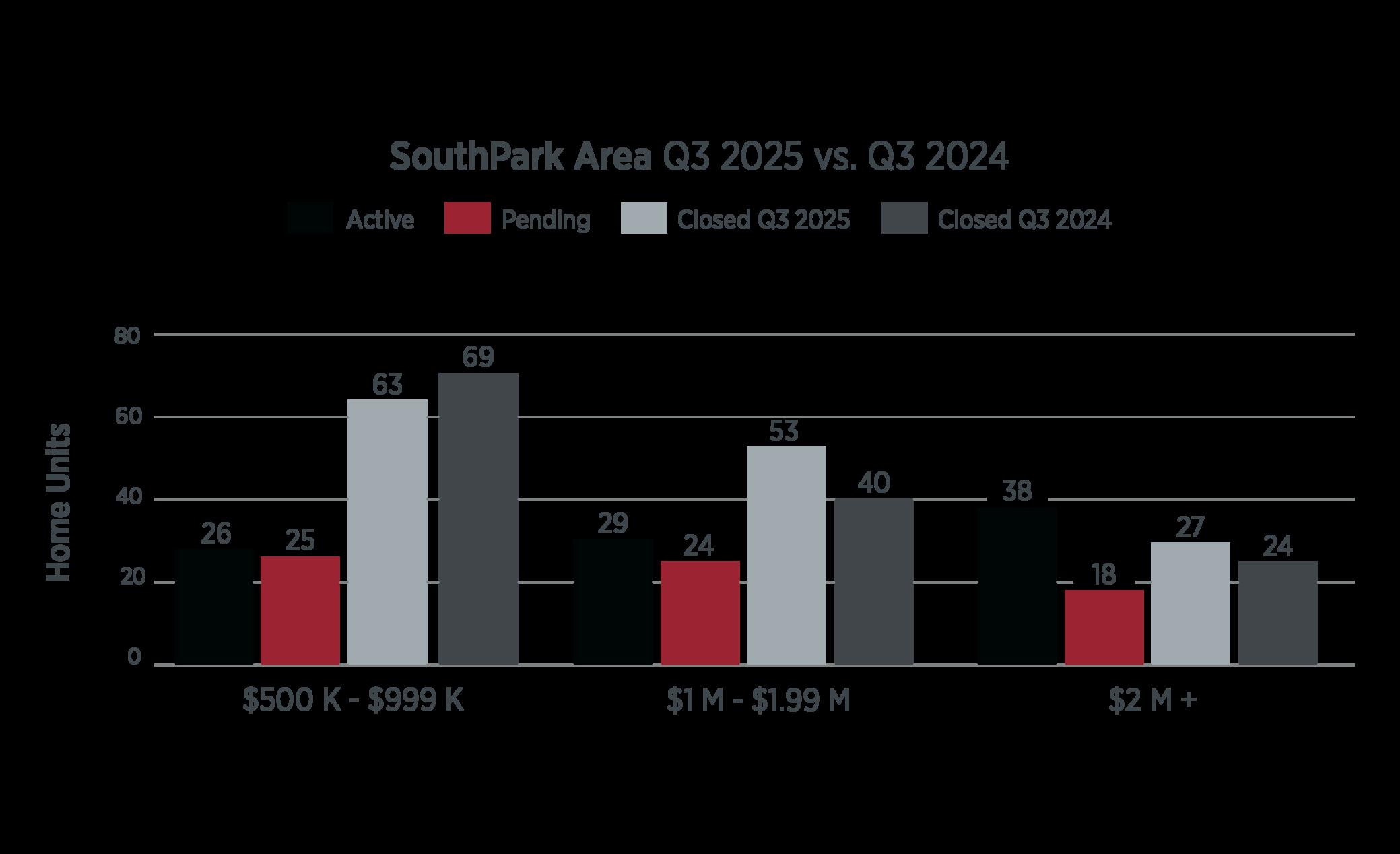

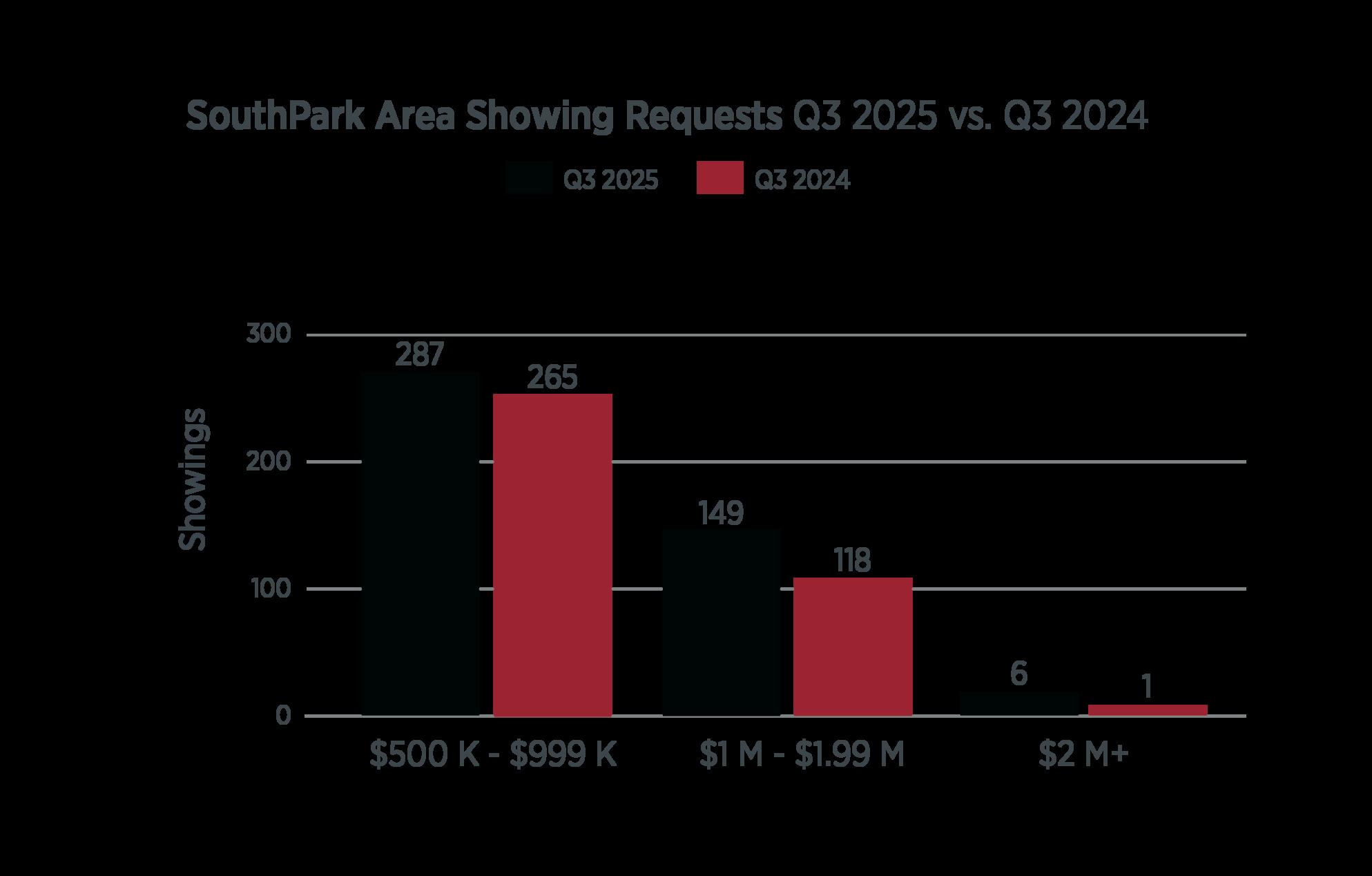

SOUTHPARK

The SouthPark area and below continued its high demand status, as the pricing segments from mid-market level to ultraluxury all showed unit closing increases, with the milliondollar and up segment posting gains of 10-25%. The strong activity kept inventory levels from increasing in the milliondollar range, while the ultra-luxury segment saw similar increases to other areas in the Charlotte region

SOUTHPARK AREA Q3 HOMES

SOLD & SHOWINGS

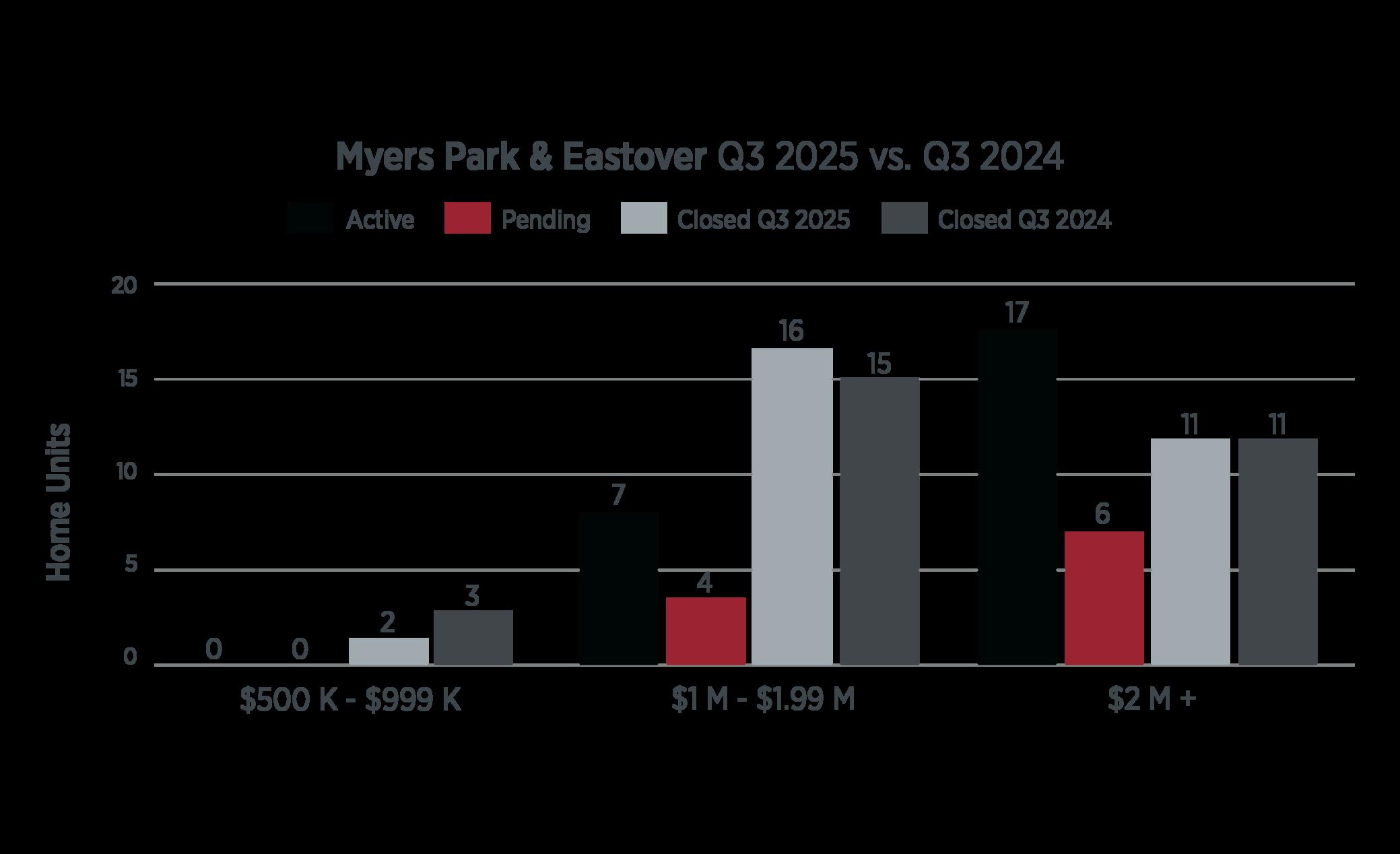

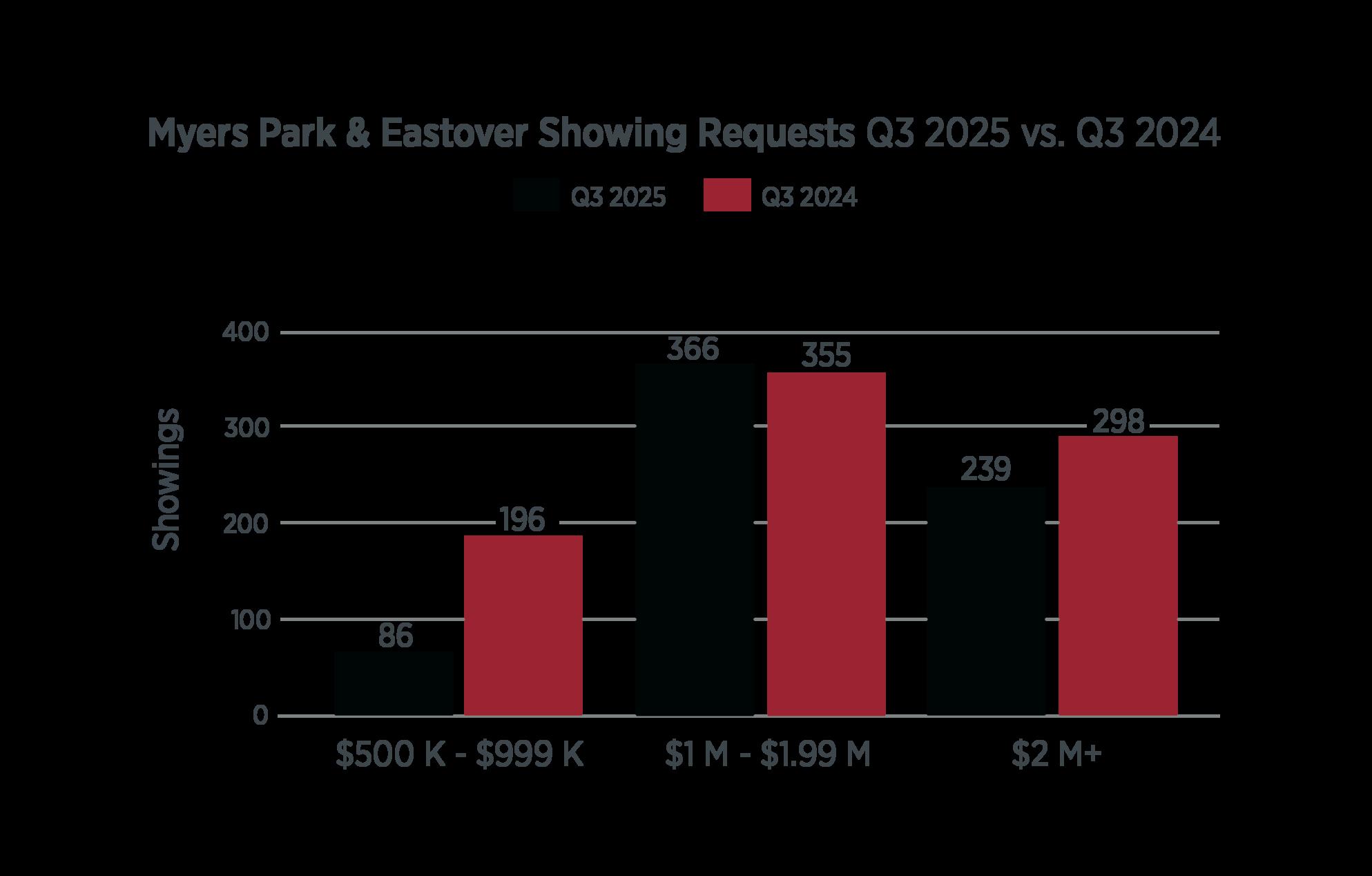

MYERS PARK & EASTOVER

Always in demand, Myers Park and Eastover had another solid quarter in sold units, mostly matching last year ' s totals for the same period Prices in this high-demand, low-supply area have continued to notch upward gains, although the area did see an atypical increase in ultra-luxury homes for sale, with 17 homes listed over $2 million while another 6 were under pending contracts. Looking at both pendings and recent solds, days on market forecasts in this price range and area look to be about 3-4 months on average

MYERS PARK Q3 HOMES SOLD & SHOWINGS

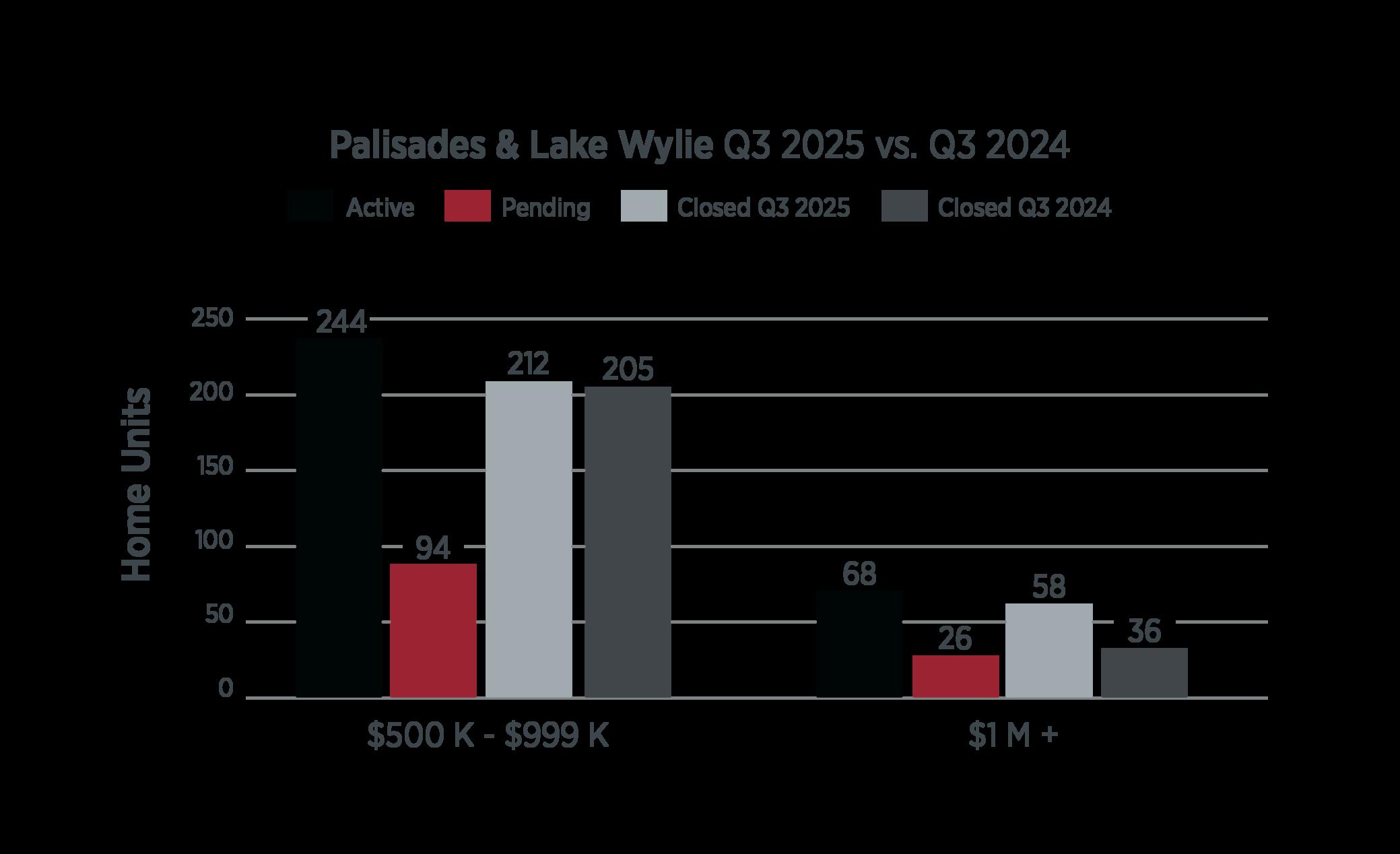

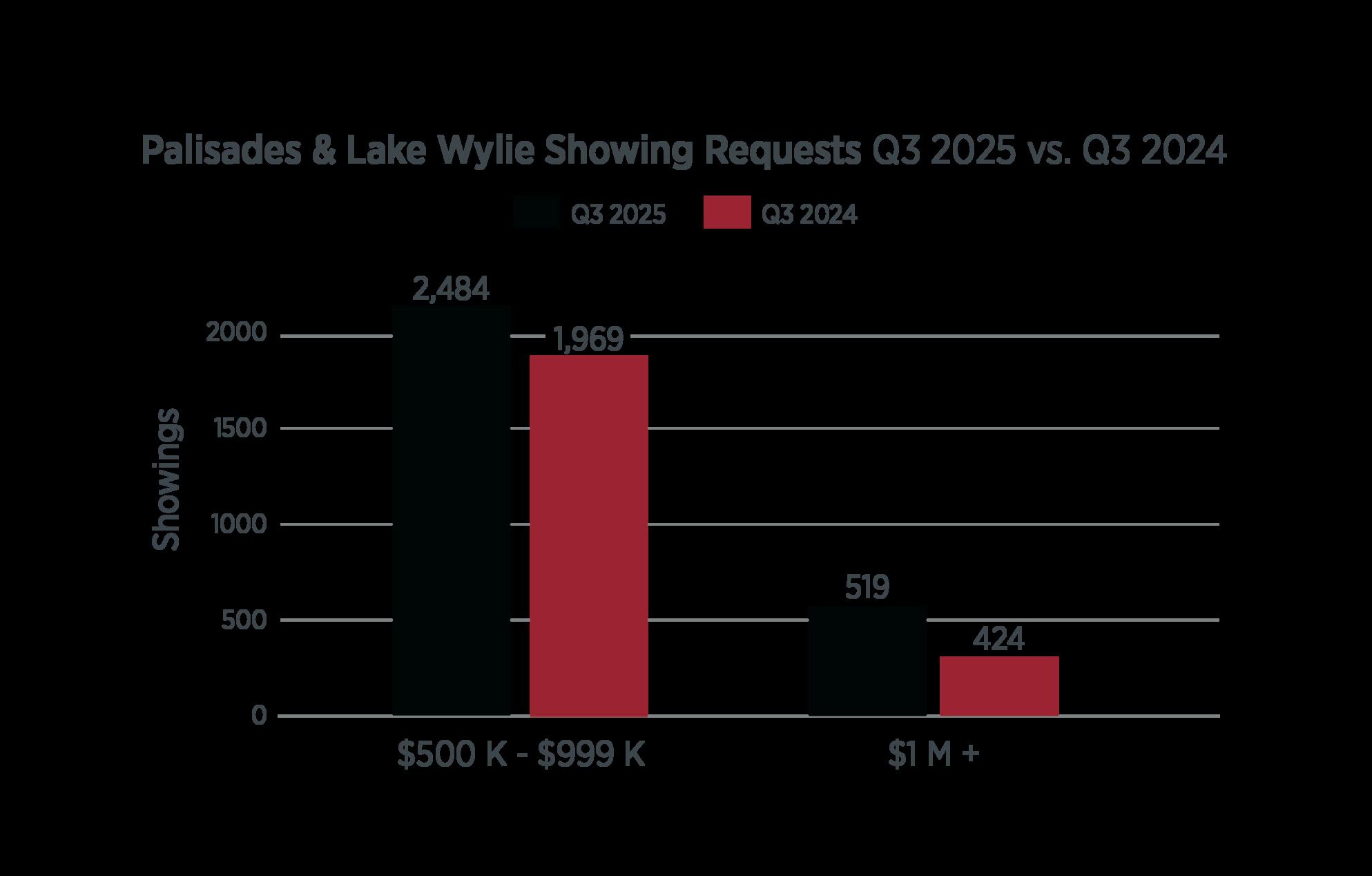

LAKE WYLIE & THE PALISADES

Bucking the region's overall slowing trend, the million-dollarplus luxury range in the Lake Wylie area showed a significant 60% spike in closings in the third quarter compared to last year While pending contracts currently stand at 26, with active inventory at 68, days on market will likely trend up into the 90-120 day range

LAKE WYLIE & PALISADES

Q3 HOMES SOLD & SHOWINGS

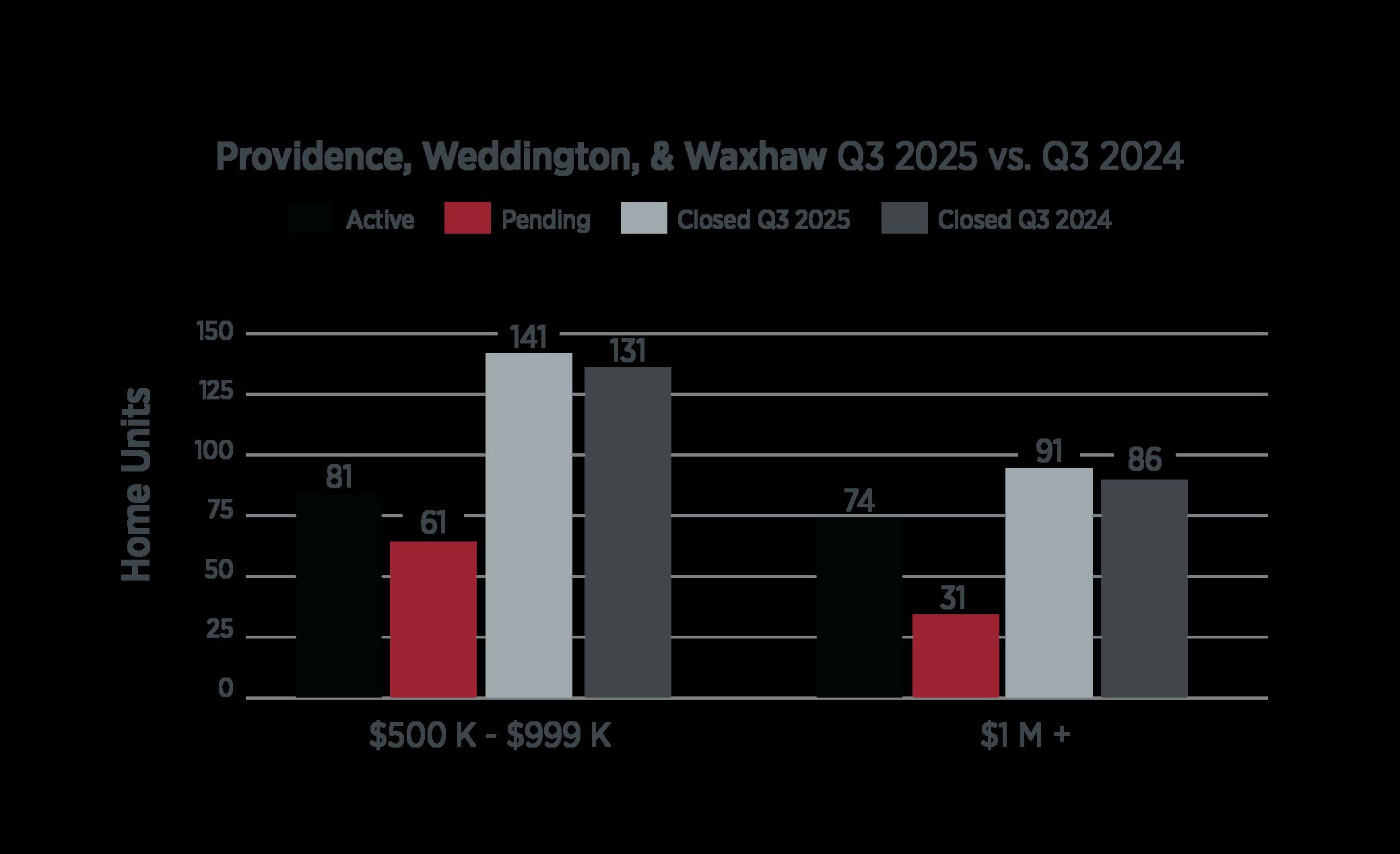

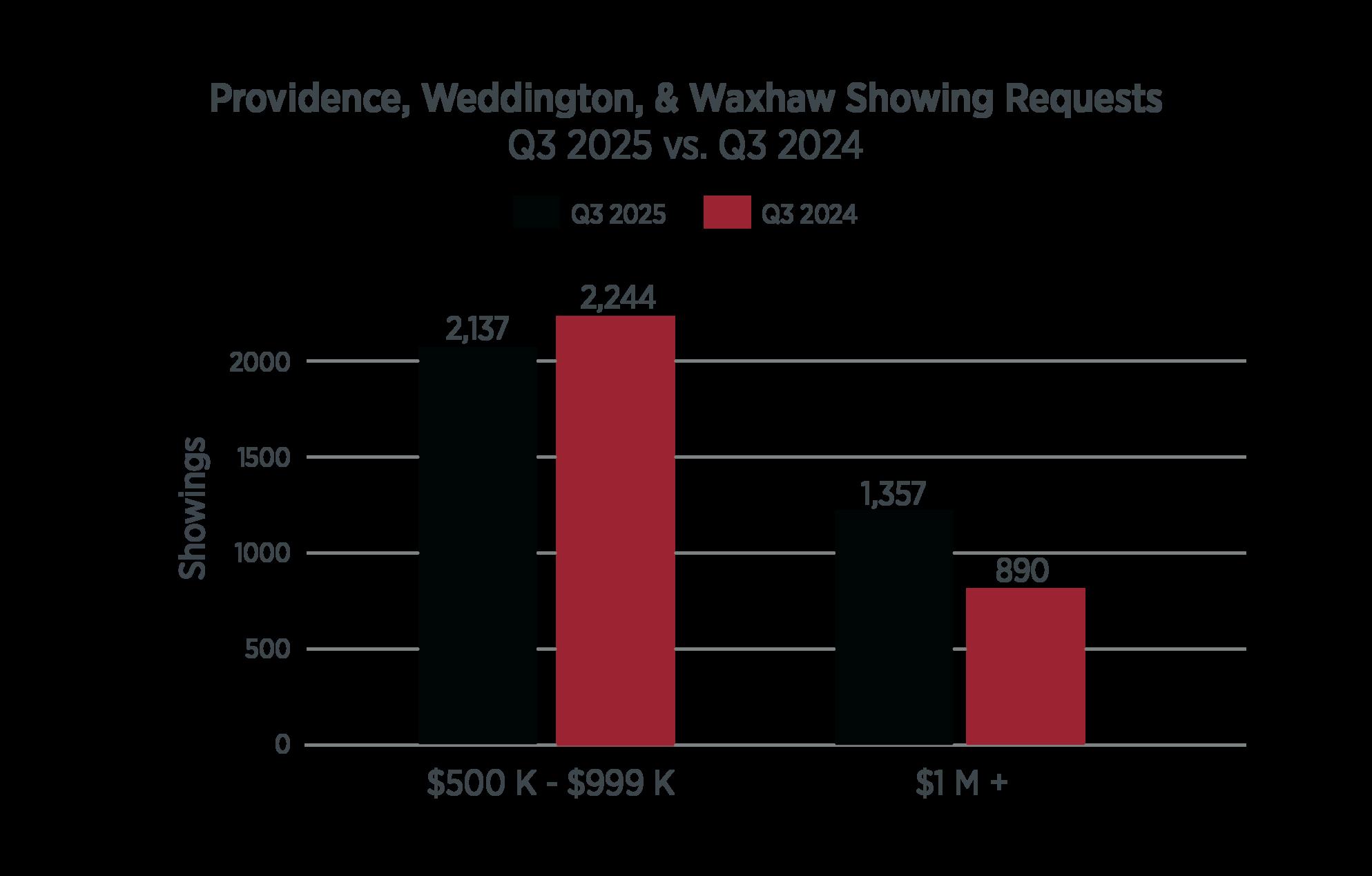

PROVIDENCE, WEDDINGTON, & WAXHAW

The highway 16 corridor continued to attract steady buyer activity, with sold results in both the mid-market and milliondollar-plus range up over last year ' s third quarter by single digit amounts While inventory has increased, the contractual activity remains solid, albeit pointing to days on market more in the 3-5 month range on average.

PROVIDENCE,WEDDINGTON & WAXHAW Q3 HOMES SOLD

& SHOWINGS

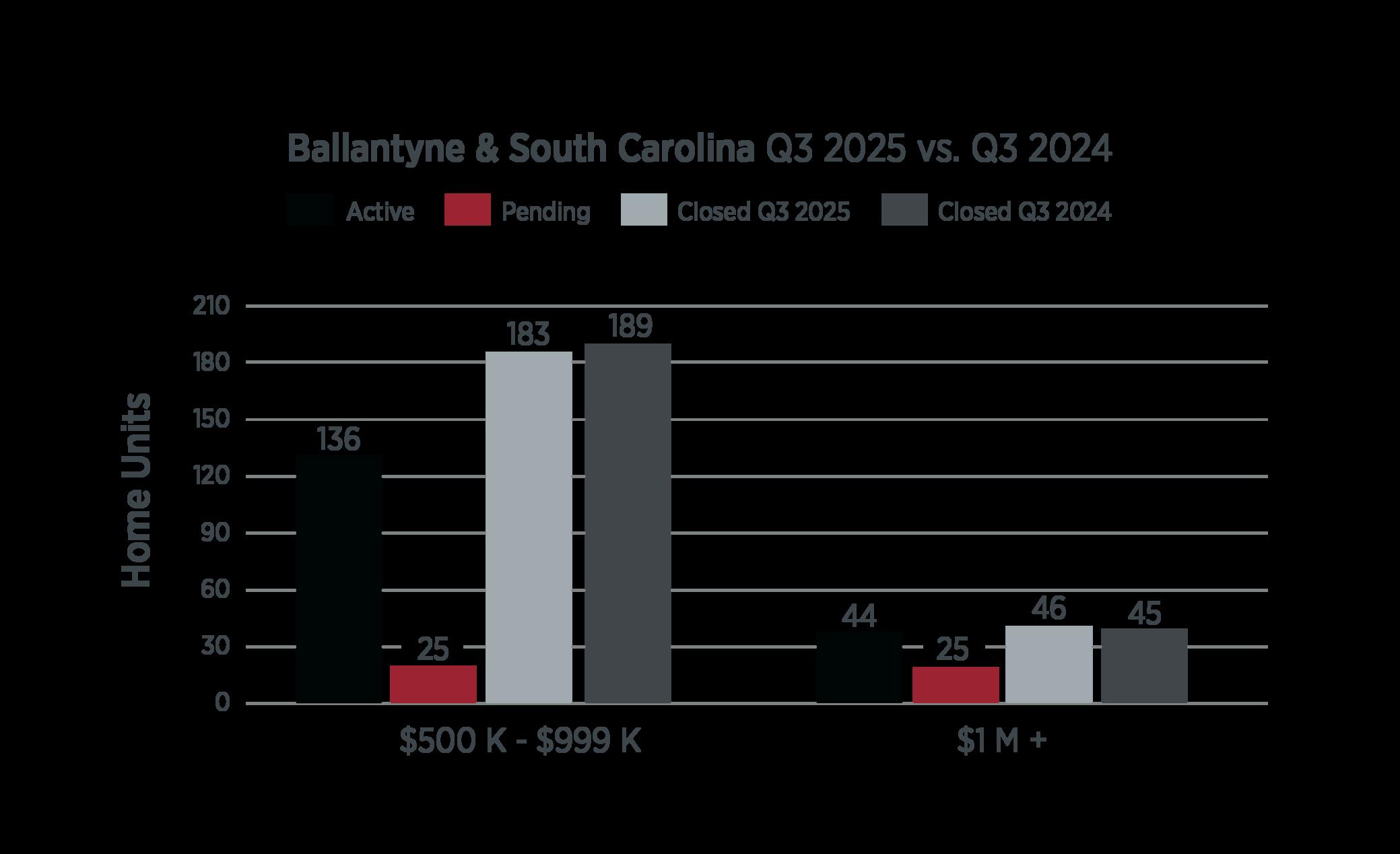

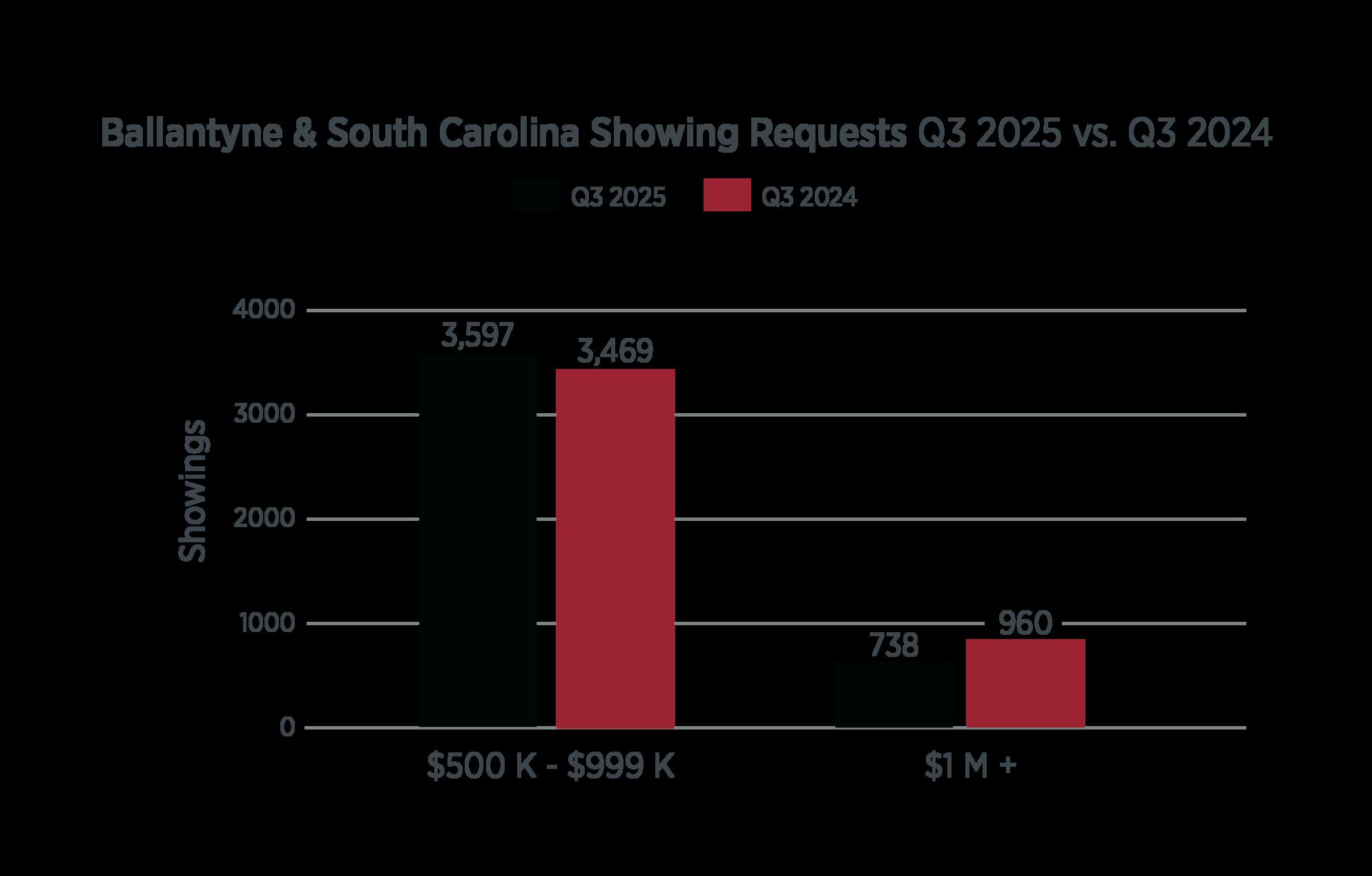

BALLANTYNE & SOUTH CAROLINA

Charlotte's South Carolina and border communities produced another solid quarter in sell-through, despite choppy economic conditions Luxury sales in the million-dollar-plus range rose 3%, while inventory rose to a four-year high yet stayed under 6 months’ worth of absorption in the luxury range.

BALLANTYNE & SOUTH CAROLINA Q3 HOMES SOLD & SHOWINGS

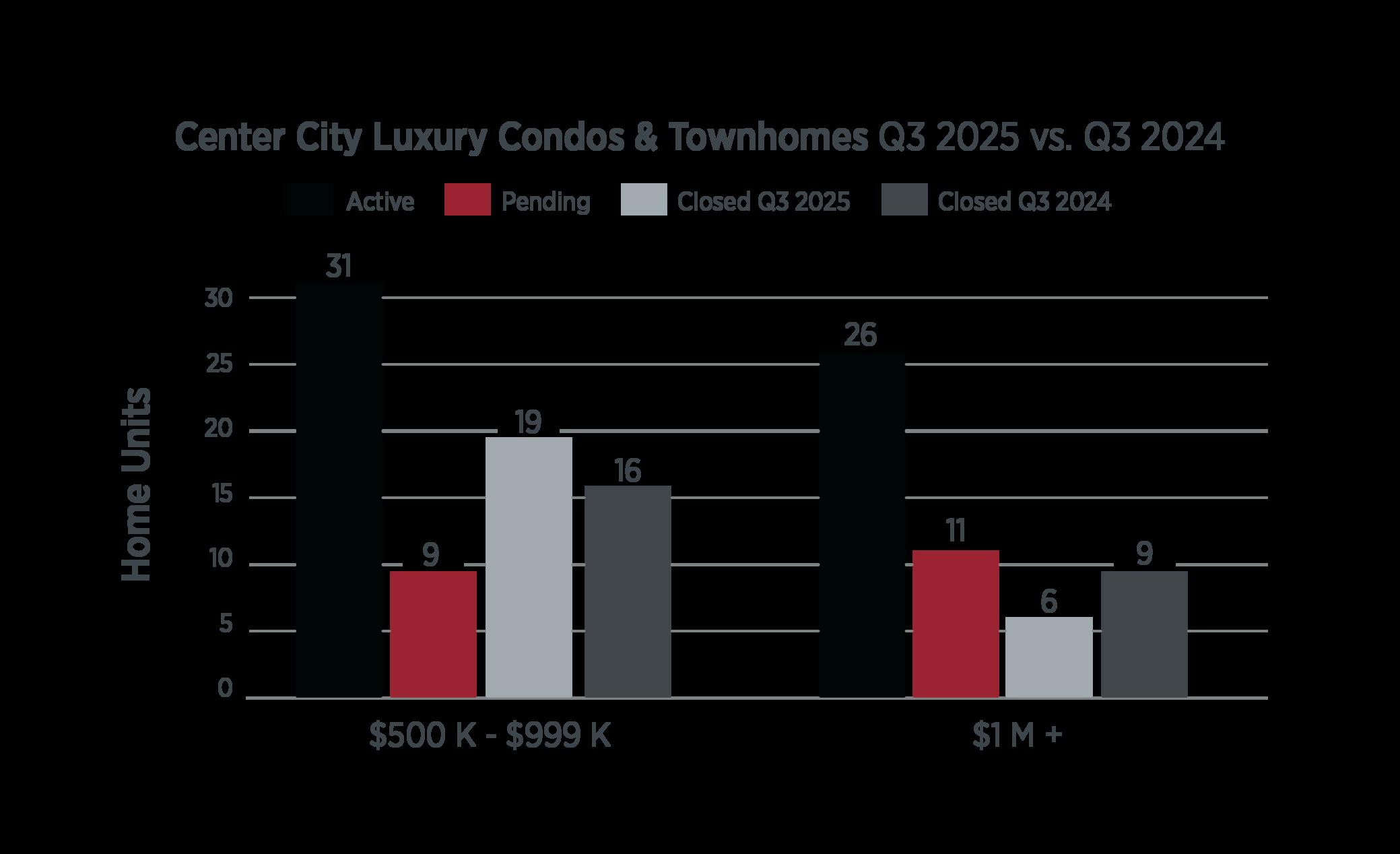

CENTER CITY LUXURY CONDOS & TOWNHOMES

The luxury multi-family segment around the 277 beltway continued its more recent trend of softening conditions. Several years of robust post Covid activity, including new projects selling out, has yielded to more conventional conditions There were 11 units in the million-dollar segment under pending contracts, with remaining inventory at 26 units. This after a quarter in which 6 units changed hands, off 33% from last year ' s 9 third quarter closings.

CENTER CITY CONDOS & TOWNHOMES Q3 HOMES SOLD

After several years of robust luxury real estate activity, 2025 s summer and early fall results point to some tapering of the prior frothiness, and a return to more conventional, albeit solid market conditions. Despite actual closings in the ultraluxury range running at a double digit pace ahead of last year ’ s record year, inventory has scaled at an even more rapid pace in most areas, creating more options for buyers While pricing and demand remain fairly solid and equity markets trade near all time highs, the inventory run up is likely attributable to several factors

Beyond some buyers waiting out a period of uncertainty despite healthy personal balance sheets, some sellers, sidelined coming out of Covid due to scarce housing supply and low interest debt on existing homes, have finally begun to re-engage in the natural historic housing cycle of downsizing, retirement, relocation, and are hitting the market with their homes. This appears to be a recalibrating of supply and demand that was disrupted during and immediately after the Covid years, and while the current ratios remain slightly balanced in the seller’s favor, there are many areas and pricing segments that have become more balanced over the summer and will likely head into 2026 with more of the same