Delaware Corporation – Prepared for Qualified Investors (Rule 506(c) Offering)

Intellectual Property Securities Corporation ("IPSE") is a pioneering financial technology company specializing in the securitization of intellectual property assets. The company provides innovative solutions for monetizing patents, trademarks, and other intellectual property through sophisticated securitization structures and blockchain technology. nature of the business.

This is our private offering, and no market exists currently exists for our shares. The offering price has been decided by our management and may not reflect the market price of our shares after the offering. This offering is distributed by Market Street Capital Inc. https://www.marketstreetcp.com

+1 713.338.9415

Team@MarketStreetCP.com 5718 Westheimer Rd., Suite 1000 Houston, TX 77057, USA

The Offering Terms:

Securities Offered: Up to 10,010,000 shares of common stock (par USD0.001) of Intellectual Property Securities Corporation.

Minimum Investment: USD 100,000 (40,000 shares). The Company reserves the right to accept subscriptions for lesser amounts in its discretion on a case-by-case basis.

Use of Exemption: Rule 506(c) of Regulation D (general solicitation permitted; sales only to Accredited Investors).

Commissions/Fees: Selling commissions and related offering expenses may be up to 12% of the gross proceeds. The Company may engage placement agents or finders and pay commissions out of this amount. (No commissions will be paid on funds raised directly by the Company from its own contacts.) Net proceeds after any commissions and offering expenses will be used by the Company as described in “Use of Funds.”

Subscription Procedure: Investors will subscribe by executing a Subscription Agreement and related documents (see “How to Subscribe” section). Subscription funds will be held in a separate

account until a minimum amount is raised (see “Escrow of Funds”). The Company may accept or reject subscriptions in its sole discretion.

The Offering Terms:

Shares offered: 10,010,000

Price per share: USD 2.50

Minimum investment: USD 100,000.00

Selling commissions, including expenses, and promotion: Up to 12%

This investment involves a High Degree of Risk. you should buy shares only if you can afford a complete loss. See “Risk Factors” beginning on page 20

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved these securities, or determined if this memorandum is truthful or complete. Any representation to the contrary is a criminal offense.

I. IMPORTANT DISCLOSURES

1. No Approval

The U.S. Securities and Exchange Commission (SEC) has not approved or disapproved these securities nor passed upon the accuracy or adequacy of this memorandum. Any representation to the contrary is a criminal offense.

2. No Market

The securities offered herein are restricted and not registered. No public market for the shares currently exists, and there is no guarantee that a trading market will develop or that the shares will ever be listed on any exchange. Investors should be prepared to hold their shares for an indefinite period.

3. No Registration

The offering is being made pursuant to an exemption from registration under Rule 506(c) of Regulation D of the Securities Act of 1933. The securities have not been registered with the SEC or any state regulator.

4. Transfer Restrictions

Transfer or resale of the shares is restricted by law and the terms of the Subscription Agreement. Investors will not be free to resell shares without compliance with applicable securities laws (e.g. holding period requirements under Rule 144 and transfer only to accredited investors or other exempt purchasers).

5. Offering Price

The offering price of the shares (USD2,5.00 per share) has been determined by our management and is not necessarily related to the Company’s asset value, book value, or earnings. The price was set based on management’s valuation of the Company’s future prospects and may not reflect the price of the shares if and when they trade in a market.

6. Information Use

Investors should rely only on the information contained in this Confidential Private Offering Memorandum. No other information or representation, whether from the Company or any other source, is authorized. This Memorandum supersedes any prior information provided.

7. Accredited Investor Status:

You must be an “Accredited Investor” as defined in Regulation D. Generally, this means individuals must have a net worth over USD1,000,000 (excluding primary residence) or income over USD200,000 (USD300,000 with spouse) for the last two years (with a reasonable expectation of the same in the current year). Entities must have total assets in excess of USD5,000,000 or all equity owners who are accredited investors, or otherwise meet the accredited investor criteria. You will be required to represent and verify your accredited status in the Subscription Agreement.

8. Financial Capacity:

You should have adequate financial means to bear the loss of your entire investment. Your overall commitment to illiquid investments should be reasonable relative to your net worth. An investment

in IPSE shares is illiquid and may need to be held for an indefinite period; you should not invest if you require liquidity or cannot afford to lose the funds.

9. Investment Intent:

You must represent that you are purchasing the shares for your own account, for investment purposes only, and not with a view to resale or distribution.

10. Legal Capacity:

Individuals must have the legal capacity to enter into the investment. If the investor is an entity, it must duly authorize the investment and the person signing must have authority to do so.

11. Advisor Consultation:

Prospective investors are encouraged to consult with their own legal, tax, financial, and investment advisors to determine whether an investment in the Company is suitable for their circumstances.

12. No Representations or Warranties

While we have provided all the information in this memorandum, we do not make any explicit or implied representation or warranty that it is complete or accurate. This includes projections, estimates, future plans, or forward-looking statements. Estimates of our performance are uncertain and may differ significantly from actual results. You should conduct your own independent investigation.

13. No Solicitation

This is not a solicitation, advertising or an offer to buy securities if this is unauthorized in your jurisdiction or if you are not qualified to.

14. Right to Withdrawal

We may withdraw, cancel, or modify this offering without notice. We may also refuse any subscription or allot fewer shares than bought.

15. Private and Confidential Nature

This memorandum is solely for your information or those you have authorized to advise you. You may not distribute, reproduce or disclose it to anyone else, except with our prior written consent. By accepting this memorandum, you agree to return it and all documents if your subscription is not accepted or if the offering is terminated.

16. Jurisdictional (NASAA) Legends

16.1. For residents of all states:

The presence of a legend for any given state simply indicates that a legend may be required by that state and does not mean that specific state allows an offer or sale of securities. If you are unsure about whether offers or sales are lawful in any state, please contact us. The securities described in this memorandum have not been registered under any state securities laws (commonly called "Blue Sky" laws). You must buy them for investment purposes only and may not sell or transfer them without either an effective registration under such laws, or an opinion of counsel acceptable to us that such registration is not required.

16.2. For California residents only:

The sale of the securities hereunder has not been qualified by the Commissioner of

Corporations of the State of California. This means we cannot sell or receive payment for these securities unless:

i) These securities are qualified by the Commissioner of Corporations of the State of California; or

ii) There is an exemption under sections 25100, 25102, or 25104 of the California Corporations Code.

By executing the Subscription Agreement, investors will make certain representations regarding the above matters. The Company will rely on the truth and accuracy of such representations in accepting any subscription.

II. Summary of the Offering

a) Company

Name of company:

Intellectual Property Securities Corporation ("IPSE" or the “Company”)

Start of operations: January 2026 (commercial launch of services)

Purpose:

IPSE is a financial technology company specializing in the securitization of intellectual property assets. The Company’s mission is to transform intellectual property rights (e.g. patents, copyrights, trademarks, film & music rights) into tradable securities, enabling IP owners to raise capital and investors to participate in the revenue streams of IP assets. IPSE’s innovative business model –including a proprietary, patented securitization method and structured compliance framework – facilitates Initial Intellectual Property Rights Offerings (IIPROs), a new form of financing that monetizes IP rights. The Company will generate revenue by structuring IP-backed securities offerings, managing those securities (through its digital platform “Securitizor”), and earning fees and/or equity stakes in the IP projects. IPSE plans to begin operations in January 2026, targeting a large, untapped market for IP financing globally.

Legal structure: C-Corporation (Delaware)

Place of incorporation: State of Delaware, USA

Date of incorporation: 10th May 2018

Headquarters: 30 Wall Street Suite 807, New York, NY, 10005

Branch Office California: 1334 Westwood Boulevard, Suite 6, Los Angeles, CA 90049 (California)

Officers:

President: Marc Deschenaux

World-renowned expert in corporate finance and inventor of the IIPRO concept.

Chief executive officer (CEO): Jeremy Oades

Seasoned finance executive with 35+ years in global banking and investment management across Europe, Asia-Pacific, and North America.

Chief operations officer (COO): Neddy Otmani

Technology strategist with a strong execution track record; fosters collaboration and innovation in building highperforming teams.

Chief financial officer (CFO): Dourgam Kummer

35+ years of expertise in structured, trade, project and equity financing;/fundraising, company structuration and restructuration using process management, including going public at the Swiss Stock Exchange as well as the Nasdaq

b) Company summary

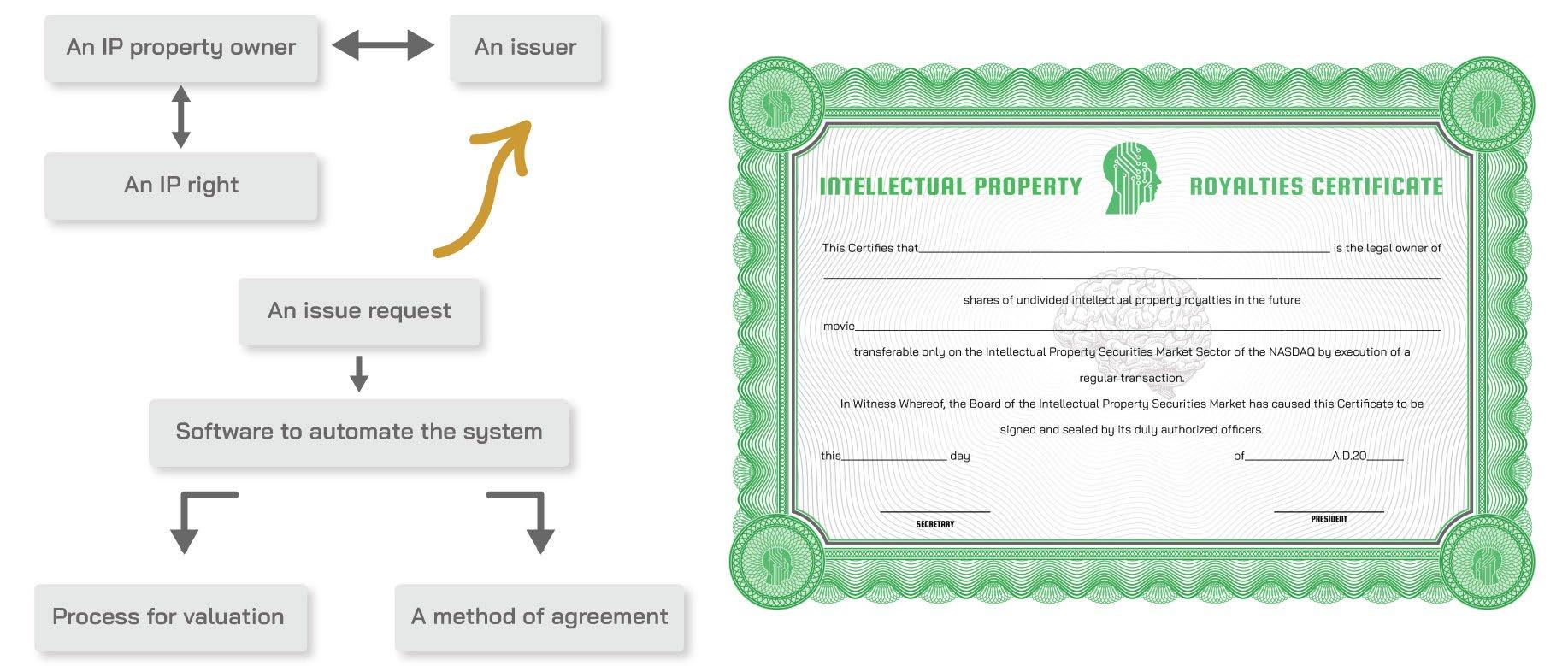

IPSE is at early stage of development. The company’s activities will revolve around financing intellectual property by issuing Intellectual Property Securities (IPS) – financial instruments backed by IP assets (for example, royalty streams from a patent or a film). IPSE’s proprietary platform, Securitizor, will facilitate the creation, offering, and management of these IPS in digital form, ensuring compliance with securities laws through built-in structured protocols. By covering the full cost and lifecycle of selected IP projects (e.g. funding the production of a film or the development of a patentable technology) and then securitizing the associated IP rights, IPSE creates a new avenue for creators to obtain funding and for investors to gain exposure to IP asset returns. The Company’s key strengths include a patented securitization method, a highly experienced management team, and first-mover advantage in a largely untapped market. Management believes the addressable market – spanning industries such as entertainment, technology, and brand licensing – is substantial, with billions of dollars of intellectual property created annually that could benefit from monetization. IPSE intends to leverage its innovative approach and deep expertise to become a leading marketplace for IP-backed securities. (See “Business of the Company” section for more details.)

c) Use of Proceeds

The Company intends to use the proceeds of this offering to build out and launch the Securitizor platform, fund initial intellectual property deals, pursue regulatory compliance and licensing, market its services to IP owners and investors, and for general corporate purposes. A detailed breakdown of the use of funds is provided in the “Use of Funds” section of this memorandum. In summary, the majority of funds will go toward technology development and IP project financing, with significant allocations for marketing/business development, operations and staffing, and legal/regulatory expenses.

We are offering 10,000,000 shares of common stock, representing 10% of IPSE's equity, to raise USD 25,025,000. We will use the proceeds from the sale of shares hereunder as follows:

D) Capitalization & Share Structure

The total issued share capital is 25’010’000 shares with a nominal value of $0.00001 per share.

• 87,900,100 common shares have been issued and paid in.

• 12,099,900 common shares are held in “Treasury” by the company There are no other classes of stock, options or warrants issued

We are offering up to 10,010,000 new shares of common stock in this offering, representing approximately 10% of the Company’s equity post-offering (if fully subscribed). If the maximum number of shares is sold, a total of 98,210,000 shares will be outstanding.

Current owners (founders, management and early investors) will then hold about 88.20% of the Company’s shares, and new investors will hold roughly 10% to 12.10%. (If fewer shares are sold, new investors will own a smaller percentage and existing shareholders a larger percentage.) The shares being offered are common stock with a USD 0.001 par value per share. Each share carries one vote and equal economic rights. There are no preferred shares authorized or outstanding, and none are expected to be issued at this time. The offered shares have no redemption or conversion rights; they are being issued as fully paid and non-assessable.

If the maximum number of shares offered herein is reached, the number of total shares issued and outstanding will be held as follows:

III. Requirements for Investors and Suitability Standards

Before investing, prospective investors must satisfy certain suitability and eligibility requirements, including the following:

a) General Suitability Standards

You, or your duly authorized representative, may only invest if you represent in writing, in the subscription agreement, the following:

i. You have the legal capacity to make the investment;

ii. If you are a company, your directors are fully responsible for it and must authorize the commitment to the representations, signing the subscription forms legally;

iii. You are financially capable of making the investment and are not subject to any legal judgments, liens, or bankruptcy;

iv. You have adequate means of providing for your current needs and personal contingencies;

v. Your overall commitment to investments which are not readily sellable is not disproportionate to your net worth and the investment in the shares will not cause such overall commitment to become excessive;

vi. You are an “Accredited Investor” (as defined below); and

vii. You represent that are buying the shares for your own account for investment purposes and not with a view to resell or distribute them

b) Accredited Investors

Each investor will be required to represent that they meet the SEC’s accredited investor criteria (see “Investor Suitability Standards” below).

You may only invest if you are an accredited investor under applicable laws. To qualify as an “Accredited Investor”, you must meet any one of the following criteria:

i. If you are a natural person/ individual, you must have:

a. a net worth, or joint net worth with your spouse (if you are married), of at least USD1,000,000 at the time of your investment; or

b. an individual income of at least USD200,000 in each of the two most recent years, or joint income with your spouse (if you are married), of at least USD300,000 in each of those years and you reasonably expect to have the same income in this year;

ii. If you are:

a. a bank as defined in Section 3(a)(2) of the Securities Act, a savings or loan association, or other institution as defined in Section 3(a)(5)(A) of the Securities Act (acting in an individual or fiduciary capacity);

b. a broker or dealer registered pursuant to Section 15 of the Securities and Exchange Act of 1934 (the “Exchange Act”);

c. an insurance company as defined in Section 2(13) of the Exchange Act;

d. an investment company registered under the Investment Company Act of 1940 or a business development company as defined in Section 2(a)(48) of that Act;

e. a Small Business Investment Company (SBIC) licensed by the U.S. Small Business Administration under Section 301(c) or (d) of the Small Business Investment Act of 1958;

f. a plan established and maintained by a state, its political subdivisions, or any agency or instrumentality of a state or its political subdivisions, for the benefit of its employees, if such plan has total assets of more than USD5,000,000;

g. an employee benefit plan within the meaning of the Employee Retirement Income Security Act of 1974, if the investment decision is made by a plan fiduciary, as defined in Section 3(21) of such Act, which is either a bank, savings and loan association, insurance company, or registered investment advisor, or if the employee benefit plan has total assets of more than USD5,000,000 or, if a self-directed plan, with investment decisions made solely by persons who are Accredited Investors;

iii. A private business development company as defined in Section 202(a)(22) of the Investment Advisors Act of 1940;

iv. An organization described in Section 501(c)(3)(d) of the Internal Revenue Code, corporation, business trust, or partnership, not formed for the specific purpose of acquiring the securities offered, with total assets of more than USD5,000,000;

v. A director or executive officer, or general partner of the company selling the shares, or any director, executive officer, or general partner of a general partner of that company;

vi. A trust, with total assets of more than USD5,000,000, not formed for the specific purpose of acquiring the securities offered, whose purchase is directed by a sophisticated person as described in Section 506(b)(2)(ii) of Regulation D adopted under the Act; and

vii. An entity in which all the equity owners are Accredited Investors.

c) Other Requirements

You may only buy shares hereunder if you are buying these:

a) for your own account (or accounts over which you have sole investment discretion);

b) for investment purposes only;

c) without any intention to sell, distribute or transfer them.

We may ask you to provide specific information to determine if you qualify as an Accredited Investor

IV. Forward Looking Information

We provide some future expectations and forward-looking information in this memorandum. These statements are subject to risks, uncertainties, and factors beyond our control, which could lead to actual results differing from what we anticipated.

The forward-looking information is based on various factors and assumptions. Given the risks and uncertainties involved, we cannot guarantee that this forward-looking information will actually happen or prove to be accurate.

Important factors may include the following:

a) We may not succeed in marketing our products and services as scheduled;

b) We may not be able to attract, build, and maintain a customer base;

c) We may not be able to attract and retain quality employees;

d) Our results may be impacted by changing economic conditions;

e) We may fail to obtain adequate debt financing if we only sell part of the shares offered herein;

We make no representation and are not obliged to update the forward looking information to reflect actual results or changes in assumptions or other factors that could affect those statements.

These and other risks are further described under “Risk Factors” section.

V. Risk Factors

Investing in IPSE’s common shares is speculative and involves significant risks. In addition to the other information in this memorandum, you should carefully consider the following risk factors before investing. The order of risks below does not necessarily reflect their relative importance. Only invest if you can withstand the loss of your entire investment. Before you invest, you should carefully consider the following factors:

a) Early-stage Company

Limited Operating History: IPSE is a development-stage company with no operating history or revenues to date. The Company was recently incorporated (2024) and has not yet commenced commercial operations. As a result, evaluating our business and prospects is difficult. Our business model is unproven at scale, and we will face all of the challenges, uncertainties, and risks that early-stage companies typically encounter. We expect to incur losses in the initial years of operation. There is no assurance that we will ever achieve profitability. Investing in a startup like IPSE is highly risky, and you should be prepared for the possibility that the business does not succeed.

b) Nature of the products

If the product or service can be as harmful, subject to the cyclical nature of international trade/ wild fluctuations in input prices, explain why and what can be the consequences of this.

c) Insufficient funds

We aim to raise between USD 500,000 and USD 25,000,000, but we may not achieve this range. Our management believes that these proceeds will sufficiently capitalize and enable us to implement our business plans. However, if we only sell part of the shares being sold herein, or if certain of our assumptions are wrong, we may not have enough funds to fully develop our business. If that is the case, we may need to seek additional debt financing or other capital investment.

d) Unproven Market and Novel Business Model:

IPSE’s business model – securitizing intellectual property assets and offering them as “IP securities” to investors – is innovative and relatively untested. The concept of Initial Intellectual Property Rights Offerings (IIPROs) is new. There can be no assurance that IP owners will choose to use our platform or that investors will embrace IP-backed securities. We must educate the market about this new financing method. Our assumptions regarding market demand could prove incorrect. It is possible that the market for IP securitization may develop more slowly or differently than we anticipate, or not at all. If creators and investors do not adopt our platform as expected, our business would suffer. Additionally, new business models often face unforeseen obstacles in execution, and our model may require significant adjustments over time to meet market needs.

e) Intellectual Property Asset Risks:

The value of the securities IPSE facilitates will ultimately depend on the value and performance of the underlying intellectual property assets (e.g. the success of a movie or the profitability of a patent). IP assets are inherently uncertain – for example, a film or music project’s revenues can be unpredictable and subject to audience tastes; a patent’s value can be eroded if a new technology renders it obsolete or if it faces legal challenges. If the IP assets underlying the securities fail to generate expected income (such as royalties or licensing fees), investors in those

securities (and by extension, the appeal of IPSE’s offerings) will be adversely affected. This could harm IPSE’s reputation and ability to attract future business. Moreover, intellectual property rights themselves carry risks: patents can be invalidated or expire, copyrights can be infringed, and trademarks can be contested. Such events would negatively impact the IP-backed securities and our business.

f) Need for Substantial Funding

Uncertain Availability of Capital: We require significant capital to execute our business plan. The USD 25 million we seek to raise in this offering is intended to fund our platform development, hire personnel, market our services, and finance initial IP projects. There is no guarantee that we will raise the full amount. If we raise substantially less than USD 25 million, we may not have sufficient cash to develop our technology or fund enough IP deals to achieve meaningful revenue. In that case, we would need to scale back our plans or seek additional financing (such as debt or future equity rounds) sooner than anticipated. Additional financing might not be available when needed, or could be available only on unfavourable terms (potentially diluting existing investors). Failure to obtain adequate funding could impede our growth or even jeopardize our ability to continue as a going concern. Even if we raise the full USD 25 million, our future capital needs could be larger than expected if our expenses are higher or revenue is delayed; we might need to raise more capital before reaching profitability, which could dilute investors.

g) Challenges of Scaling and Execution:

Executing our business plan will require that we scale up operations rapidly once funding is obtained. We will need to build a complex technological platform (for IP securitization and compliance), establish workflows for evaluating and structuring IP deals, navigate various legal frameworks (securities law, intellectual property law in multiple jurisdictions), and manage a growing number of relationships with IP owners and investors. These tasks present significant operational and managerial challenges. If our management processes, internal controls, or systems are inadequate to handle our growth, the business could suffer. Potential challenges include: technical risks (the platform may take longer to develop or not perform as expected; data security breaches or system outages could occur), hiring risks (scaling the team quickly with qualified personnel), and process risks (establishing effective deal underwriting criteria and compliance checks for a new asset class). Rapid expansion may strain our limited resources. Any missteps in scaling – such as technology deployment delays, operational inefficiencies, or failure to implement proper controls – could result in setbacks, higher costs, or inability to meet obligations to customers. Our management’s experience in growing businesses and managing complexity will be critical, but there is no assurance that growth will be smooth or successful.

h) Competition and Technological Disruption

While IPSE’s approach is novel, we will likely face competition from multiple fronts. Traditional financing sources for intellectual property (such as film financiers, music label advances, venture capital for patents, banks making IP-backed loans) may compete with our offerings. These incumbents have established track records and relationships. We also expect that if our model shows promise, new competitors could emerge, potentially including fintech companies, crowdfunding platforms, or blockchain/tokenization firms that target IP monetization. Some competitors might attempt to replicate our business model or develop similar financial products. Many potential competitors may have greater resources and funding than we do, allowing them to market aggressively or undercut our fees. Additionally, the fast pace of financial technology means our digital platform must continually evolve – technological disruption is a risk. For example, blockchain or smart contract platforms could offer alternative means of fractionalizing IP ownership that bypass our system. If we fail to stay at the forefront of technological innovation in

securitization, we could lose relevance. There is also the risk that large tech or finance companies could enter the IP investment space once it appears attractive, bringing significant capital and brand recognition. We will need to establish a strong brand, proprietary processes (protected by patent where possible), and a network effect to maintain a competitive edge. Nonetheless, competition could impact our pricing, margins, and ability to achieve sufficient market share.

i) Illiquidity of Investment / No Exit Until IPO or Buyout:

An investment in IPSE’s shares is a long-term, illiquid investment. The shares are being sold in a private offering under Regulation D and are restricted securities. There is currently no public market for the shares, and you will not be able to freely resell your shares. You may not be able to liquidate your investment in the event of an emergency or for any other reason. Although we intend to eventually pursue a public listing (IPO) for IPSE, there is no guarantee if or when that will occur. Even if we are successful, it could be years before an IPO or other liquidity event. We do not have an obligation to redeem or repurchase your shares (and we currently do not intend to do so). As a result, investors must be prepared to hold their shares indefinitely. Even in a future IPO, the value of the shares could be lower than the price paid in this offering, or broader market conditions could prevent liquidity. In short, you should not invest in this offering if you need liquidity or are not prepared to hold the investment without the ability to sell.

j) Regulatory and Compliance Risks:

IPSE operates at the intersection of securities law and intellectual property law, which is a complex and heavily regulated space. We face multiple layers of regulatory risk:

k) Dependence on Key Management and Personnel

In its early stages, IPSE’s success will heavily depend on our management team and key personnel. In particular, we rely on the vision, expertise, and relationships of our President (Marc Deschenaux), our CEO (Jeremy Oades), and other top executives. These individuals possess unique knowledge of financial structuring, intellectual property finance, and our business strategy. If we were to lose the services of any of our key executives, especially in the early years of operations, it could have a material adverse effect on the Company. We currently have no operating history and a small team, so each key person fills multiple critical roles. Replacing such individuals could be difficult and time-consuming, and there is no guarantee we could find suitable replacements with comparable skills or connections. We intend to enter employment agreements and offer equity incentives to retain talent, but there is still a risk that one or more key team members could depart. Additionally, as we grow, our success will depend on our ability to attract and retain qualified staff (such as software engineers, IP analysts, and compliance experts). Competition for talent is intense, and we are a small, early-stage venture. Inability to hire or keep the right personnel could impair our execution.

l) Securities Law Compliance:

Each IP offering we facilitate must comply with applicable securities regulations in relevant jurisdictions (e.g. U.S. federal and state securities laws, and potentially foreign regulations if offerings are extended internationally). We are currently conducting a Rule 506(c) exempt offering for our own equity; in the future, IPSE may itself sponsor or manage separate offerings of IP securities (which could be treated as securities offerings needing exemption or registration). Navigating these laws requires careful structuring. Any mistake or oversight in compliance (such as an offering that fails to meet exemption requirements) could result in enforcement actions, penalties, or rescission rights that could severely impact the business. The regulatory environment

could also evolve – new laws or SEC rules could impose additional requirements on crowdfunding or securitization of IP, which might increase our costs or limit our activities.

m) Broker-Dealer / Exchange Regulations:

There is a risk that regulators could deem our activities as those of a broker-dealer, investment adviser, or even an exchange/ATS (Alternative Trading System) if we facilitate trading of IP securities among investors. We currently do not plan to create a trading marketplace (initially focusing on primary issuance of IP securities), but if secondary transactions among investors are enabled on our platform, we may need to register as an exchange or broker-dealer or partner with one. Failure to obtain required licenses or regulatory status in a timely manner could limit our business model. Complying with such regulations will require additional infrastructure and expense.

n) Intellectual Property Law:

We must ensure that the IP rights being securitized are valid, enforceable, and properly transferred or licensed into the securitization vehicles. Complex legal agreements will be needed for each deal. Any failure in legal due diligence (e.g., not detecting a flaw in a patent’s chain of title or a copyright’s validity) could lead to litigation or losses on that security. We could face lawsuits from IP owners or investors if a securitization is alleged to infringe on others’ rights or if promised cash flows do not materialize due to legal defects.

o) Global Operations and Jurisdictional Issues:

Intellectual property is global, and we may engage in deals involving rights in various countries. This introduces compliance challenges with different countries’ laws on securities, IP, taxation, etc. For example, royalty streams from overseas might incur withholding taxes; different jurisdictions have different rules on securitization and special purpose entities. Ensuring compliance across borders will be resource-intensive.

Any regulatory action, investigation, or litigation could distract management, damage our reputation, and impose heavy costs, even if we ultimately prevail. We are dedicating significant effort to structured compliance (indeed, our business model includes a “structured compliance” framework to proactively manage these issues), but regulations are subject to interpretation and change. Adverse regulatory developments could force us to alter or curtail our operations, which would harm our prospects.

p) Dilution and Future Capital Needs:

Investors in this offering will experience immediate and substantial dilution in the net tangible book value of their shares. The current net tangible book value of the Company is very low (close to USD 0.01 per share, as the Company has only recently been capitalized and has primarily intangible assets such as plans and intellectual property). After the sale of 10,000,000 shares for USD 25,025,000, the pro forma net tangible book value of the Company is expected to be on the order of USD 25 million (assuming full proceeds), which, spread over 25,025,000 shares, would equal about USD 1.00 per share. This means that new investors paying USD 2,50 per share are effectively contributing capital that results in a book value of ~USD1.00 per share post-offering –an immediate dilution of approximately USD9.00 per share relative to the offering price. Existing shareholders will benefit from an increase in book value from near USD0 to USD1.00 per share, whereas new investors will bear this dilution in book value. Furthermore, if the Company issues additional shares in the future (for example, to raise more capital or to grant stock options to employees/advisors), your ownership percentage in the Company would be diluted, and the value of your shares could be adversely affected. While we will attempt to use the proceeds of this

offering to reach self-sustaining operations, there is no guarantee that additional funding will not be required. Any future issuance of equity (or equity-linked securities) could be at terms unfavorable to existing investors and could occur at a lower valuation per share than this offering, resulting in further dilution.

q) Economic and Market Conditions:

Our business prospects and the success of both IPSE and the IP securitizations we structure are subject to general economic, market, and geopolitical conditions. A downturn in financial markets or in investor sentiment could reduce the appetite for alternative investments like IP securities or for our own fundraising efforts. During recessions or tight credit conditions, investors often become more risk-averse, which could make it difficult for us to place IP offerings or to secure investors for this or future rounds. Likewise, adverse trends in the entertainment industry, technology sector, or other areas of intellectual property (for example, a decline in global box office revenues, or changes in patent laws that weaken patent value) could indirectly hurt our business model. Broader issues such as inflation, rising interest rates (which make fixed-income investments more attractive relative to equity), currency fluctuations, or international trade disputes could also have unpredictable effects on our operations and the willingness of investors to allocate capital to IP assets. These macroeconomic factors are outside our control, and we may not be able to insulate the Company from their impacts.

r) Risks Associated with Expansion

The management's experience and the controls in place to manage the growth of the business are essential factors in determining the success of the company's expansion plans.

Without the necessary resources, including financial, personnel, and experience, the company may face several risks:

(i) Financial Resources: Without adequate financial resources, we may struggle to fund our expansion plans, leading to delays or incomplete development phases. This could result in missed opportunities or loss of market share to competitors.

(ii) Personnel: Insufficient skilled personnel may harm our ability to execute our growth strategy effectively. This could lead to operational inefficiencies, decreased productivity, and difficulty in meeting customer demands.

(iii) Experience: Lack of experience in managing rapid growth may result in missteps or bad decisions, when it comes to scaling operations, managing increased complexity, and maintaining quality standards, among others.

(iv) Competitive Disadvantage: Inadequate resources may put the company at a competitive disadvantage, as competitors with more resources can capitalize on opportunities more effectively. This could result in loss of market share and diminished long-term prospects.

Overall, the risk of not having the necessary resources to support development in the future is significant. It may impede the company's ability to achieve its growth objectives, damage its competitive position, and ultimately impact its long-term sustainability.

s) Customer Base and Market Acceptance

Describe customer base – SAMPLE: Our customer base includes specific demographics:

(i) females aged 18-45,

(ii) males aged 35-60, and

(iii) females and males from these age groups primarily located in the western United States.

However, we cannot guarantee that we will capture a significant portion of these demographics. Even if we do, we cannot guarantee that these customers will be suitable or profitable enough to sustain our business.

t) Competition

IPSE, with its innovative IP Structured Finance proposal and its unique Securitizor solution, stands without direct competitors in the market. The target audience/competitor consists of global financial players engaged in patent financial lending and debt financing sectors that have become essential for leveraging intellectual property (IP) assets to secure capital, particularly for companies driven by innovation.

By using patents as collateral, firms can obtain loans or credit lines, gaining access to funding without diluting ownership or relinquishing control. This method is especially advantageous for businesses with robust patent portfolios and predictable revenue streams, as it allows them to maintain ownership while financing growth and market expansion.

IPSE seeks to position itself as a direct competitor to existing financial institutions specializing in IP-backed debt financing by delivering a solution that is both highly attractive and cost-efficient for the market.

u) Shortage of Financial Comparisons

Indicate why there may not be adequate financial comparisons available to either the firm or the investor. Is this due to the unique nature of the product, the speed of change within the market etc?

For this reason, the Company cannot predict with certainty its projections.

v) Lack of Operational Profits

When are the operations due to generate a profit?

We cannot guarantee that we will make payments on a timely basis.

w) Trend in Consumer Preferences and Spending

Our operating results can vary significantly from period to period due to various factors, including customer purchasing patterns, competitive pricing, debt payments, and general economic conditions. We cannot guarantee success in marketing our products or that the revenue from sales will be substantial. As a result, our revenues may fluctuate each quarter, leading to fluctuations in our operating results.

x) Risks of Borrowing

If we take on debt, a portion of our cash flow will need to go towards paying off the amount of money borrowed (principal) and the cost of borrowing that money (interest). Loan agreements often come with conditions or limitations that can limit the company's operating flexibility (financial covenants). These agreements also set conditions for default, such as failing to meet financial covenants. If there is a default, the lender can demand immediate repayment of the loan. If unpaid, the lender could obtain a judgment against the company, which would take priority over the rights of shareholders. A judgment creditor could then take possession of the

company's assets which may have been pledged as security for such loan (foreclosure), causing a significant negative impact on our business, operating results, or financial condition.

y) Unanticipated Obstacles to Execution of the Business Plan

The company’s business plans may change significantly. Some of our potential business ventures requires a lot of capital and may be subject to legal or regulatory requirements. However, management believes that the company’s chosen activities and strategies are achievable given the current economic and legal conditions, as well as the expertise of the company’s personnel Management may modify the company’s stated strategies depending on future events.

z) Management Discretion as to Use of Proceeds

The net proceeds from this offering will be used as described under “XVII Use of Funds.”

However, we may use the funds for other purposes not presently planned if we believe it to be in the best interests of the company and its shareholders due to changed circumstances or opportunities. Therefore, our success will largely depend on the discretion and judgment of management regarding how the net proceeds are used. By investing, you will be entrusting funds to the company’s management, upon whose judgment and discretion you must depend.

aa) Control by Management

As of January 2026, when the company intends to commence commercial operations, the company’s management owns 100% of its issued shares. After this offering is completed, the company’s management will own approximately 90% of the issued and outstanding shares, maintaining control of the company Investors in this offering will own a minority percentage of the company and will have minority voting rights. Therefore, they will not have the ability to control the company’s board of directors or any appointed officers.

bb) Return of Profits

We intend to retain any initial future earnings to fund operations and expand our business. The company’s managing shareholders will determine a profit distribution plan based upon the company’s results of operations, financial condition, capital requirements, and other circumstances. Each shareholder will receive revenue profits in proportion to their shares.

See “Description of Shares” section.

cc) No Assurances of Protection for Proprietary Rights; Reliance on Trade Secrets

In some cases, we will use trade secrets to protect intellectual property, proprietary technology and processes, which we have acquired, developed or may develop in the future. However, we cannot guarantee that secrecy obligations will be respected or that others will not independently develop similar or superior products or technology. Protecting intellectual property and/or proprietary technology through trade secrets has led to increasing claims and litigation by various companies both to protect proprietary rights and for competitive reasons, even where those claims are unproved. Suing or defending against such lawsuits is expensive and uncertain due to the evolving legal principles in this area. Like others, the company may also face claims from other parties regarding the use of intellectual property, technology information, and data deemed proprietary by others.

dd) Litigation

There are two primary areas of litigation risk:

(i) Competitive Litigation: We may face litigation from competitors, which could include challenges to our products, services, management, activities, and results. This could result in significant costs, expenses, and negative publicity, potentially jeopardizing the company's future.

(ii) Contractual Obligations: We intend to pursue legal action against individuals or entities who fail to fulfill their contractual obligations to the company.

ee) Dilution

If you buy these shares, you will be diluted in your ownership of USD 9.00 per share in net tangible book value, or approximately 90% of the assumed offering price of USD 2.50 per share (assuming we raise the maximum offering proceeds of USD 25,025,000 for 10,010,000 shares). If additional shares are issued and offered by the company in the future, existing shareholders will also be diluted

ff) Limited Transferability and Liquidity

To meet certain exemptions from registration under the Securities Act, and comply with applicable state securities laws, each investor must buy their shares for investment purposes only and not to distribute them. This means certain conditions of the Securities Act must be met before any sale, transfer, or other disposal of the shares. These conditions may include:

(i) a minimum holding period,

(ii) availability of certain reports (like financial statements),

(iii) limits on the percentage of shares sold, and how they are sold.

We may prevent any sale, transfer, or disposal unless we receive, at the holder's expense, an opinion of counsel satisfactory to management, stating that the proposed action will not breach applicable federal or state securities laws. There is no public market for the shares, and one is not expected to develop. Therefore, shareholders may have to hold onto their investment indefinitely and may not be able to sell them or use them as collateral for a loan in an emergency.

gg) Broker - Dealer Sales of Shares

Our shares are not currently traded on any exchange, and there is no guarantee they will be in the future.

NASDAQ recently changed its criteria for listing on the Small Cap Market. Entry standards include USD4 million in net tangible assets or USD750,000 net income in two of the last three years, among other requirements. Maintenance standards require at least USD2 million in net tangible assets or USD500,000 net income in two of the last three years, among other criteria. Until the shareholders decide otherwise, there is no assurance the shares will qualify for inclusion on NASDAQ or any other trading market. Therefore, the shares are subject to a Securities and Exchange Commission rule that imposes additional sales practice requirements on broker-dealers who sell them to non-established customers and accredited investors. This rule may affect the ability of broker-dealers to sell these shares and the ability of shareholders to sell their shares in the secondary market.

hh) Long Term Nature of Investment

Since the offer and sale of the shares will not be registered under the Securities Act or state securities laws, investors will need to represent in writing that they are buying the shares for their own account for long-term investment, not for resale or distribution. Therefore, investors must be prepared to bear the economic risk of their investment for an indefinite period.

ii) No Current Market for Shares

There is no current market for the shares offered in this offering and no market is expected to develop in the near future.

jj) Compliance with Laws

The shares are being offered for sale under exemptions from the registration requirements of the Securities Act, applicable California securities laws, and other state securities laws. If the sale of shares were to fail to qualify for these exemptions, investors may undo (by way of rescission) their purchases. If multiple investors were to do so, we could face significant financial demands, which could adversely affect the company and any remaining shareholders.

Other changes in regulations, whether new or modified, could impact our profitability. This includes changes in interpretation or application of existing rules and regulations.

kk) Offering Price

The price of the shares offered has been decided by us, taking into account factors like the state of the company’s business development and the general condition of the industry. The offering price does not reflect the assets, net worth, or any other objective criteria of value applicable to us.

ll) Dependence on this Private Offering

There is no minimum number of shares that needs to be sold herein and we cannot assure you that all shares will be sold. We rely on raising funds through this private offering to develop our business. If we fail to sell all shares, we may have to modify our plans and this could adversely affect our development. If additional funds are needed, we cannot guarantee they can be raised in a timely manner or on terms acceptable to us.

mm) Conflicts of Interest

The company has several agreements that may be considered conflicts of interest, granting rights to investors who are aware of them. These include agreements stating that commissions will be paid for specific results, such as going public on a stock exchange. This incentive could influence decisions. Additionally, a director of the company could be involved with another company that does business with us. By investing, an investor acknowledges these conflicts, agrees not to pursue legal action against the company or its representatives, and accepts their existence.

nn) Force Majeure

In case of force majeure events like war, riots, or supplier insolvency affecting the company's marketplace and financial results, there is no guarantee of achieving profitability or meeting financial projections.

oo) Lack of Firm Underwriter

Certain designated members of our management and/or board of directors, and/or certain FINRA registered broker-dealers are selling the shares herein. Broker-dealers will enter into participating broker-dealer agreements with the company. While we cannot assure you that any of the securities will be sold, we will use our best efforts to sell the shares (“best efforts basis”).

pp) Hostile Actions

While our board of directors may refuse new investments permitted under this private offering, there is no assurance against shareholders seeking to use their influence to create disputes or litigation involving the company.

qq) Future Projections

The existing projections are based on our anticipated financial performance. These projections are hypothetical and are based on different assumptions which our management believes are reasonable, such as a strong marketing plan and other factors affecting the business. They represent our management's best estimate of the likely results of operations, based on current circumstances, and have not been reviewed by independent accountants. However, some assumptions may not materialize due to unforeseen events and circumstances beyond our management's control. Therefore, actual results may vary significantly from the projections. Assumptions about future changes in sales and revenues are speculative. Moreover, projections cannot account for factors such as economic conditions, regulatory changes, new competitors entering the market, future capitalization terms, and other inherent risks. While management believes the projections accurately reflect potential future results, they are not guaranteed.

rr) General Economic Conditions

Our financial success may be affected by adverse changes in general economic conditions in the United States, such as recession, inflation, unemployment, and interest rates. These changes could lower demand for our products. However, management believes that the targeted product line and the anticipated growth of the market will help offset any significant decrease in demand. Nonetheless, management has no control over these changes.

ss) Liquidation

In the event of liquidation, the Company's activities would cease, and investors may not receive repayment of their investment. Although the Company's know-how and technology could potentially be sold to repay some of the prior investment if a buyer is available, we cannot guarantee that we will have sufficient funds to repay any portion of the funds raised through the Private Offering.

tt) Other risks

Explain any other material risks which a reasonably informed investor would want to know before taking a decision on whether to invest or not.

The above list of risk factors is not exhaustive. Prospective investors should read this entire memorandum and carefully consider all of the information set forth herein (including the exhibits) before making an investment decision. Additional risks and uncertainties not presently known to the Company or that we currently deem immaterial may also impair our business operations. An investment in the Company’s shares is suitable only for persons who can afford a high-risk, illiquid investment.

VI. Future Activities of the Business (Milestones

and Growth Strategy

a) General

The company’s principal offices are located at 30 Wall Street Suite 807, New York, NY, 10005, with additional branches at 10287 NW 135th Street, Hialeah Gardens, FL, 33018 and 1334 Westwood Boulevard Suite 6, Los Angeles, CA 90049.

b) Nature of the Business

State the operations of the business. Be precise about what exactly the company does, and how it operates.

Provide information on the good or service in general terms in a way that a reasonably informed investor would be able to understand. Provide information on the success to date, and proposed future steps.

c) History

Founded in December 2014 by Marc Deschenaux, Philippe Froehlicher, and Richard Ormond, Intellectual Property Securities Corporation (IPSE) emerged as a visionary enterprise aiming to transform intangible assets into tradable financial instruments. Building upon Deschenaux's earlier initiative, the World Intellectual Property Securities Exchange Corporation (WIPSEC) established in 1998, IPSE sought to actualize the concept of securitizing intellectual property (IP) rights, enabling creators to monetize their innovations through capital markets.

2014–2018: Establishing the Foundation

In its formative years, IPSE concentrated on developing a robust framework for IP securitization. The company introduced innovative financial instruments such as Intellectual Property Assignment Shares (IPAS), facilitating the conversion of IP assets including patents, trademarks, and copyrights into securities. This approach provided inventors and artists with new avenues to access funding, while offering investors opportunities to participate in the value of creative works.

2019–2022: Strategic Partnerships and Technological Advancements

Recognizing the need for strategic alliances, IPSE partnered with Swiss Financiers Inc. in 2018. This collaboration aimed to streamline the process of taking companies public, particularly those with significant IP assets. The partnership enhanced IPSE capabilities in facilitating Initial Public Offerings (IPOs) and broadened its reach within the financial sector.

2023–2025

: Market Integration and Global Recognition

In recent years, IPSE has focused on integrating its securitization operations with emerging financial technologies. The company has explored the tokenization of real-world assets, aligning with trends in blockchain and decentralized finance. This evolution has positioned IPSE at the forefront of financial innovation, garnering recognition for its contributions to the development of IP-based securities markets.

Marc Deschenaux: The Visionary Behind IPSE

Marc Deschenaux, co-founder and President of IPSE, is renowned for his expertise in corporate finance and securities law. With a career spanning over three decades, Deschenaux has been instrumental in orchestrating numerous IPOs and private offerings globally. His commitment to empowering creators through financial innovation has been the driving force behind IPSE mission to democratize access to capital for IP holders.

Conclusion

From its inception in 2014, IPSE has evolved into a pioneering entity that bridges the gap between intellectual property and financial markets. Through innovative securitization strategies and strategic partnerships, the company has redefined the landscape of IP monetization, providing creators with unprecedented opportunities to capitalize on their innovations. As IPSE continues to adapt to the dynamic financial ecosystem, it remains committed to its vision of transforming intangible assets into tangible value

d) The Future

IPSE has a clear roadmap for development and growth. The funds raised in this offering are intended to propel the Company through several key phases of execution:

2025 – Platform Development and Regulatory Readiness: Upon securing funding, IPSE will focus on completing the build-out of the Securitizor platform. This includes developing the secure online infrastructure for IP owners to submit assets and for investors to review and purchase IP securities. Parallel to tech development, we will solidify our regulatory compliance structure –establishing any required legal entities (such as special purpose vehicles for securitizations), obtaining any necessary licenses or regulatory approvals, and creating standard offering documents/contracts for IP deals. We will also begin curating a pipeline of intellectual property projects (e.g. identifying high-potential film projects, patent portfolios, music catalogs) that could be securitized once the platform launches. By Q4 2025, our goal is to have a beta version of the platform operational and a handful of inaugural IP deals under due diligence or contract.

Early 2026 – Commercial Launch of Services: In January 2026, IPSE plans to commence commercial operations, launching the platform to the public (initially focusing on accredited investors per securities law requirements). We expect to roll out our first Initial IP Rights Offerings (IIPROs) in early 2026. These initial transactions will likely serve as proof-of-concept cases across different IP categories – for example: a motion picture financing securitization (offering investors participation in a film’s royalties), a music rights offering (securitizing an artist’s catalog royalties), and a technology patent licensing income securitization. Successful execution of these first deals will be critical for demonstrating our model. During 2026, we aim to refine the platform’s user experience, implement feedback from early users, and establish IPSE’s brand in the market. We will also ramp up business development efforts, forging relationships with content creators, studios, inventors, research institutions, and IP-rich companies to generate deal flow. On the investor side, we will conduct outreach to family offices, institutional investors (such as IP-focused funds), and high-net-worth individuals to build the investor base for IP securities.

2026–2027 – Scaling Transaction Volume and Revenue Growth: As 2026 progresses into 2027, our focus will shift to scaling. This involves increasing the number and size of IP securitization deals on our platform. We plan to expand into additional verticals of intellectual property finance for instance, beyond entertainment and tech patents, into areas like trademarks/brands (franchise securitization) or pharmaceutical IP (drug royalty securitization). We will continue enhancing the platform’s features, possibly including a secondary trading bulletin board if allowable (to provide liquidity for investors, subject to regulatory constraints). The Company will invest in marketing and education to attract a wider range of IP creators globally, including in Europe and Asia (leveraging our advisors with international reach). We anticipate by late 2026 or 2027 to have a steady pipeline of offerings, generating transaction fee revenues for IPSE and building a track record of successful IP financings. We will also explore strategic partnerships –for example, with law firms (for IP due diligence), banks or exchanges (for custody/clearing services), and industry associations. By mid-2027, the goal is for IPSE to be recognized as a leading platform for IP monetization, with a growing community of issuers and investors.

2027 and Beyond – Potential Liquidity Event (IPO) and Long-Term Vision: If the Company demonstrates strong performance and the market conditions are favorable, management’s longterm plan includes a potential Initial Public Offering (IPO) for IPSE itself (separate from the IP deals we facilitate). An IPO could occur as early as late 2027 or 2028, which would provide liquidity for our investors and additional capital for expansion. It must be emphasized that the timing and likelihood of an IPO are uncertain and heavily dependent on achieving interim milestones (revenue growth, profitability or clear path to profitability, regulatory compliance maturity, etc.). Long term, IPSE’s vision is to establish a new asset class around intellectual property rights. We aim to eventually host a wide array of IP-backed securities and potentially develop a regulated exchange or trading platform specifically for IP securities, improving liquidity and price discovery in this niche. We also foresee expanding our services to include asset management (for investors who want exposure to a portfolio of IP assets) and consulting for companies seeking to unlock value from their IP holdings. As the market evolves, IPSE will adapt, potentially incorporating technologies like blockchain for transparent tracking of royalties or smart contracts for automatic distribution of revenue to security holders. The overarching goal is to solidify IPSE’s position as an innovator in structured finance, bridging the worlds of intellectual property and capital markets.

The timeline and activities above are subject to change based on business conditions and the amount of capital raised. Achieving our milestones will depend on successful execution and external factors (market acceptance, regulatory approvals, etc.). Management will continuously evaluate the Company’s strategy and adjust tactics as necessary to drive growth and value for shareholders.

e) Unique Aspects of Business

IPSE is the First-to-Market Platform Transforming Intellectual Property into Regulated, Publicly Traded Financial Securities. It is the world’s first platform to securitize intellectual property (IP) and list it as equity on public capital markets. Through its patented, automated infrastructure, the Company transforms IP assets such as patents, copyrights, and trademarks into fractionalized, regulated securities eligible for listing on major exchanges like NASDAQ and CBOE. These instruments offer creators non-dilutive capital and investors access to an entirely new asset class.

Founded by a capital markets innovator and IPO expert, Project Intellect operates a full-stack securitization engine that integrates compliance, legal structuring, and exchange compatibility. With a defensible patent portfolio, active engagement across entertainment and healthcare verticals ($500M+ pipeline), and imminent NASDAQ integration, the Company is positioned to lead the creation of a $7.8 trillion global IP securities market by 2030.

f) Platform, Products and Services

IPSE Platform enables the transformation of IP into IP Investment Shares (IPIS) and IP Royalty Shares (IPRS), allowing creators to raise capital without giving up full ownership. The Company’s platform automates legal structuring, onboarding, rights verification, and exchange compliance.

With integrations across 675 APIs and regulatory systems, Project Intellect’s infrastructure is adaptable across jurisdictions and IP types. Core IP classes include music, film, patents (particularly in biotech and software), academic innovations, and digital content libraries. The platform also supports tokenization, escrow management, and KPI-driven fund release tracking for structured transactions.

Competitive Advantage

With no direct competitors, IPSE is the first and only platform enabling direct, regulated IP securitization on public markets, with a defensible moat built on:

• Multiple utility patents covering securitization structures and compliance automation.

• Exclusive integration with NASDAQ for IP securities listing.

• Proprietary legal process patents and alignment w/ global IP certification body.

• A pipeline of $500M–$1.1B in securitization-ready IP assets.

Traction & Milestones

• $12M+ invested in tech, platform, and patent development.

• $24M invested pre-incorporation via WIPSEC (established 1998) in IP securitization and legal infrastructure.

• Assessment and rights clearing platform in Alpha, currently onboarding IP assets for public offerings.

• Multiple patents granted and pending, covering core securitization methodologies and digital compliance systems.

• IP pipeline includes assets in music, film, biotech, and university research.

g) Industry and Markets

IPSE market position serves both IP asset originators (e.g., filmmakers, musicians, inventors, academic institutions) and IP asset investors (institutional investors, high-net-worth individuals, and fintech-native retail participants). It offers a first-mover advantage in a fragmented and underleveraged market where more than 85 million U.S. creators are unable to monetize valuable IP. With strategic partnerships and embedded compliance, the Company bridges the gap between cultural and scientific innovation and liquid financial markets.

The global shift toward intangible asset dominance has left a vacuum in capital markets for structured, liquid access to intellectual property. Over 90% of S&P 500 company value is now attributable to intangible assets, yet monetization remains elusive for the majority of IP holders.

Project Intellect addresses a $74.9 billion IP licensing market and is positioned to tap into $23.3 trillion in alternative assets under management by 2027. The Company uniquely enables monetization of underutilized IP, opening new capital channels for creators, researchers, corporations, and institutions that have historically lacked liquidity options. Demand is accelerating from both supply-side creators and institutional investors seeking non-correlated, yield-generating assets.

h) Value Proposition

With a concrete Value Proposition, IPSE delivers more than just a capital formation tool. It legally and technologically engineers a new investable asset class. Unlike debt-based IP financing models, the Company creates public equity instruments rooted in real ownership, automated compliance, and performance-based payout mechanisms.

This offers investors access to structured royalty income or equity-style upside in sectors like film, music, life sciences, and software. Creators retain control, while investors receive

regulated, tradeable access to high-value IP portfolios. The platform’s scalability, patent protection, and NASDAQ integration establish it as the foundational infrastructure for a new generation of IP capital markets.

i) The Solution and Offering

IPSE Solutions offering What Are IP Securities?

IP Securities are a new class of financial instruments that transform intellectual property, such as patents, copyrights, trademarks, into fractionalized, tradable securities. Unlike traditional IPbacked loans or collateralized debt models, IP Securities represent direct ownership interests or revenue-sharing rights tied to the underlying IP. These securities can be structured to reflect equity participation (e.g., future value upside) or royalty income (e.g., recurring cash flows), and they are eligible for listing on public markets. This innovation allows IP holders to raise capital without giving up full ownership or control; while offering investors access to regulated, yieldgenerating assets rooted in creativity and innovation.

Types of IP Assets IPSE Securitize

IPSE is sector-agnostic and capable of securitizing a broad range of intellectual property across industries:

Music and Audio Rights

Streaming catalogs, publishing rights, and performance royalties. Rights holders gain upfront capital while retaining future revenue participation.

Film and Television

Scripts, production-stage projects, distribution rights, and merchandising IP. Creators finance development without losing ownership or creative control.

Patents and Inventions

Particularly in healthcare, biotech, energy, and software sectors. Inventors access early-stage funding without equity dilution.

Literary and Digital Content

Books, games, YouTube content, and podcasts with monetized IP. Creators unlock capital from IP libraries and scale content production.

University and Corporate IP

Research-based patents and proprietary technologies from R&D institutions and corporations. Institutions monetize underutilized IP and fund further innovation.

The process description and the issued Intellectual Property Assignment Securities

j) Products and Services

IPSE offers a comprehensive suite of services designed to unlock the financial potential of intellectual property by transforming it into tradable securities.

1 - IP Securitization

At the core of IPSE’s model is the direct securitization of intellectual property. IPSE enables inventors, creators, and rights holders to fractionalize their IP into equity-like securities. These instruments represent real ownership or participation in future revenues, allowing for transparent, regulated fundraising without relinquishing full control of the asset.

2 - Financing of IP on Public Capital Markets

Through its proprietary platform and strategic integration with NASDAQ and other major exchanges, IPSE facilitates the listing and trading of IP-backed securities. Creators are therefore enabled to raise capital from public investors in a way traditionally reserved for companies issuing stock or debt, democratizing access to funding for IP-rich but liquidity-constrained entities.

3 - IP Securities Brokerage & Trading

IPSE provides a secure marketplace for the buying and selling of intellectual property securities. Benefiting from compliance and liquidity, investors can trade ownership shares or royalty rights in IP-backed assets. The Company also supports brokerage services for high-value IP transactions and investor matchmaking across sectors.

4 Licensing In addition to capital markets access

IPSE supports monetization through licensing. The Company enables partial or full licensing of rights (e.g., distribution, performance, manufacturing) to third parties by structuring IP into tradable securities. Licensing revenues are tracked and distributed through IPSE’s platform, offering consistent income streams to both IP originators and investors.

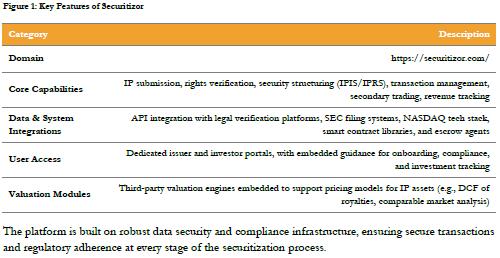

k) The Technology – The Securitizor® Platform

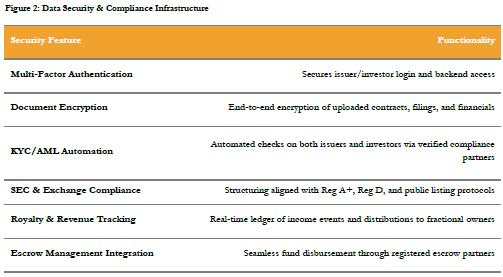

At the core of IPSE’s infrastructure is Securitizor, a proprietary, patent-backed, fully automated digital platform accessible at www.securitizor.com. Purpose-built to support the compliant, scalable securitization of intellectual property, it manages the entire lifecycle of IP Securities, from asset onboarding and rights validation to legal structuring, investor compliance, and secondary trading.

Unlike fragmented legacy systems, Securitizor automates high-risk, high-cost processes including smart contract generation, royalty modelling, KPI-based escrow release tracking, and revenue distribution. The platform integrates with over 675 apps and APIs, including SEC filing systems, exchange infrastructures like NASDAQ, and legal verification tools. This makes Securitizor adaptable across asset types and jurisdictions.

For rights holders and investors, it provides a secure, regulated, and auditable pathway to public capital markets. Securitizor also functions as an insurance wrapper, validating every participant contract (e.g., actor agreements, music licenses, movie scripts) within an IP package and certifying rights coverage. This feature substantially reduces legal uncertainty for investors and lowers due diligence costs for issuers, particularly in complex verticals like media and biotech.

The platform’s robust architecture and features are highlighted below.

The platform is built on robust data security and compliance infrastructure, ensuring secure transactions and regulatory adherence at every stage of the securitization process.

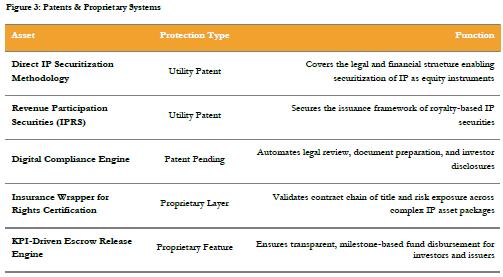

The platform is also protected by a portfolio of patents and proprietary systems, collectively forming an end-to-end infrastructure for listing and trading IP-based securities.

l) The Securitization Process

The workflow is designed to be transparent, standardized, and scalable across industries:

Submission & Onboarding: IP holders (e.g., creators, inventors, or rights owners) submit their IP to the IPSE platform along with supporting documentation. Assets can include copyrights, patents, trademarks, and licenses with monetization potential.

Legal Validation & Due Diligence: The IP is reviewed for ownership clarity, enforceability, prior monetization, and licensing structure. Third-party experts and legal professionals may be engaged to validate the asset's legal standing and market readiness.

Structuring: IPSE structures the asset into one of two security types: Intellectual Property Investment Shares (IPIS), offering equity-style participation in the future value of the IP; or Intellectual Property Royalty Shares (IPRS), offering revenue participation through ongoing royalty streams.

Regulatory Preparation: IPSE prepares necessary disclosures and legal filings to comply with SEC and listing exchange requirements. A full prospectus and investor documentation are created.

Listing & Capital Raise: Once approved, the IP Securities are listed on partner exchanges such as NASDAQ or CBOE, where investors can purchase fractional ownership.

Secondary Trading & Revenue Distribution: Post-listing, IPSE facilitates secondary trading of IP securities and manages the distribution of royalties or profit shares to investors

m) The Rollout Plan: Vertical and Regional Strategy

IPSE’s market rollout strategy is designed to maximize adoption and visibility by focusing first on sectors and regions with the highest commercial readiness, investor appetite, and IP monetization potential.

o Vertical Priorities: The initial rollout will target three high-opportunity verticals: healthcare, music, and film. These sectors are rich in monetizable IP yet underserved by traditional capital markets. Future expansion will include publishing, software, and technology, where innovation cycles and IP intensity are high, but capital access remains limited.

o Regional Focus: The US will be IPSE’s initial geographic focus, given its status as the largest and most liquid securities market. US-based IP offers the clearest regulatory path for public listing and investor access. Despite a fragmented IP litigation landscape, the US remains a global leader in entertainment, life sciences, and media innovation.

In Europe, particularly Germany and other advanced R&D markets, IPSE will focus on commercialization gaps. Many European entities possess strong IP portfolios, but lack efficient exit mechanisms or capital markets infrastructure for monetization.

n) Disputes/Litigation

IPSE is a new company, recently incorporated. The management of IPSE is not involved in any litigation or pending litigation nor is it aware of aware of any suit or litigation that is threatened against XYZ. There is no dispute with anyone, nor have we received any judgments that attack the business or individual persons related thereto.

o) Rules and Regulations

IPSE, as a US-based fintech company, is subject to a comprehensive set of federal and state regulations governing employment rights, fiscal obligations, and general corporate operations.

In addition to adhering to rules related to the right to work and standard business practices, IPSE must comply with specific financial regulations that shape its core activities. These include anti-money laundering (AML) and know-your-customer (KYC) requirements under the Bank Secrecy Act (BSA), enforced by agencies such as the Financial Crimes Enforcement Network (FinCEN) and the Department of the Treasury’s Office of Foreign Assets Control (OFAC).

Depending on its services, IPSE may also be regulated by the Securities and Exchange Commission (SEC), the Federal Deposit Insurance Corporation (FDIC), and the Consumer Financial Protection Bureau (CFPB), among others. Additionally, fintech companies offering money transmission services must register with FinCEN and may need state-level licenses.