By Eugene Davis

The Institute of Economic A airs (IES) has alluded that Ghana’s economy is generally growing below its potential due to several factors. This includes low public investments, macroeconomic instability and the high cost of doing business.

In its latest bi-monthly Economic Outlook, the IEA said achieving higher growth will require, in particular,

leveraging the country’s huge natural resource wealth to increase investments in physical and human capital, lowering the cost of doing business and sustaining macroeconomic stability.

Data published by the Ghana Statistical Service (GSS) showed that economic growth was generally on the upward trend between the second quarter of 2023 and the second

quarter of 2024, with year-on-year Gross Domestic Product growth increasing from 2.5% to 6.9%.

Non-oil GDP growth followed a similar trend as overall GDP growth during the period, increasing from 3.1% to 7.0%.

In terms of sectoral growth, agriculture showed a fairly steady positive growth throughout the period, ranging between 4.3-5.4%.

The services also grew by positive rates, ranging from 3.2-6.0%. Industry, on the other hand, recorded erratic growth, with negative rates in quarter 2, 2023 and quarter 3, 2023 and positive rates in quarter 4 2023; quarter 1, 2024 and quarter 2, 2024, ranging between 1.6-9.3%.

The erratic growth of industry, the IEA said re ected irregular

quarterly oil outputs during the period.

The International Monetary Fund (IMF) recently revised its growth projection for Ghana from 3.1% to 4.0%.

This indicated an expected stronger recovery from the e ects of Covid-19 and the general economic crisis that has plagued Ghana in the past four years or so.

Editor: Benson A ul

Bernard Owusu-Ansah, a Manager with KPMG Ghana’s Governance, Risk and Compliance Services (GRCS) unit, has urged Ghanaian businesses to rst align their organisational vision with their strategy to e ectively mitigate Environment, Social, Governance (ESG) risks in their businesses.

Mr. Owusu-Ansah made this call while speaking during a UK-Ghana Chamber of Commerce (UKGCC) webinar with KPMG Ghana on "Mitigating and Managing ESG Risks: Building Resilience for a Sustainable Future”.

According to Mr. Owusu-Ansah, recent studies indicate that over 70% of companies globally are now exposed to moderate to high ESG risks. This exposure makes businesses more vulnerable to ESG-related impacts that may weaken their ability to withstand and adapt to operational and nancial shocks.

Environmental risks involve potential adverse impacts from the natural environment, such as extreme weather conditions, pollutions and emissions and resource scarcity. These risks can a ect a business’s reputation, nancial

performance, and long-term sustainability. Social risks, on the other hand, are challenges related to a business’s impact on its workforce and communities. These include non-compliance with labour standards, inadequate compensation, or insu cient health protection for employees. Governance risks refer to issues around governance structures, ethical practices, and overall corporate conduct.

To e ectively manage these risks and strengthen business resilience, Mr. Owusu-Ansah remarked that, “It all starts with your strategy.

“Everything starts with strategy, and cascading your vision and ambition through the organisation, because if you are implementing a corporate strategy that runs parallel to your risk approach, you’re going to have a lot of issues”.

He advised that businesses rst establish a vision which that incorporates ESG principles, then consider available opportunities in the strategy.

Following this, business leaders must de ne the ESG ownership from the board level. Here, Mr. Owusu-Ansah cautioned that whoever is

appointed to own ESG in the business must be able to quantify how the business is bene ting from the ESG strategies that have been implemented to counter a potential perception that the business is ‘wasting money’.

He stressed, however, that “Risks are not always counter-productive to the business; they can also create opportunities.

“You can thrive by using risk as a competitive advantage or by developing new products that exploit these risks”, he explained.

To align your business’s vision with its strategy, Mr. Owusu-Ansah suggested that companies may assess their risk landscape and identify who matters to their objectives (i.e. key stakeholders) such as investors, regulators, community members, employees, customer and the supply chain.

“It is important to consider the community in which you operate because it is not only about the nancial impact on your business. For instance, there are powerful

people, leaders and social in uencers in communities who can change public opinion about your business. It is essential to understand and consider what matters to these people”.

He further advised businesses to focus on material issues that matter to their business, clarifying what they seek to achieve with ESG as a function, i.e. if they want to be simply compliant with regulations, strategic, or transformative with their entire operating model; and consider both the local and international regulatory landscape.

“There are a lot of issues. You cannot tackle everything simultaneously, but prioritising those most material to your business, and leads to what your ambition is”, he said.

ESG also presents opportunities such as enabling businesses to grow and innovate with new products and services, making it attractive to businesses leaders.

However, challenges such as integrating ESG with corporate strategy, a complex regulatory environment, and di culty in de ning what is sustainable, in addition to responsibility for reporting and measurement amongst others, can make its adoption arduous to several companies.

Despite these challenges, Mr. Owusu-Ansah emphasised that adopting ESG principles and managing its related risks is worth-

while.

“ESG is ultimately about doing the right thing. If you set out to do the right thing in every aspect of your business, you will realise that you are complying with most of the regulations, regardless of where your busi-

ness extends to”.

The webinar, moderated by Emma A. Opoku-Pare, an Assistant Manager with

KPMG Ghana’s Financial Risk Management Unit, also covered topics such as ESG risk drivers, Enterprise Risk Management Frameworks, creating value from ESG, risk identi cation and materiality assessment, and prioritisation and mitigation strategies, among others.

By Eugene Davis

The Speaker of Parliament, Alban Bagbin has expressed concerns that recent legislative developments could threaten democracy and disrupt Ghana’s constitutional order.

Nonetheless, he insists he will do whatever it takes to maintain control in the House, despite ongoing challenges.

Addressing the media on recent happenings in Parliament on Wednesday, Mr. Bagbin said “The current brouhaha may be christened a "power play between the arms of government," and it has the potential to undermine our democracy and the authority of Parliament. Its outcomes could subvert Ghana's constitutional order

and the democratic system Ghanaians have toiled, sacri ced their lives, and shed blood to establish for decades.”

According to the Speaker, the judiciary's authority ceases where parliamentary privilege begins. The Constitution clearly outlines the freedom of speech within parliamentary proceedings. Articles 115 and 116 grant Members of Parliament privileges and immunity concerning speech, debates, and proceedings on any matter brought before Parliament, whether by petition, bill, motion, or otherwise.

Acknowledging the Constitution's supremacy, Bagbin stressed that Parliament deserves respect as an independent

institution.

“ I believe in the supremacy of the Constitution, mark my words, the supremacy of the Constitution, not the supremacy of the Judiciary or Supreme Court. I also believe in a vibrant Parliament that is respected and accorded its due on political questions as long established by law and decided cases.

A Parliament that understands, re ects, and embodies the will of the people and defends its constitutional prerogatives only works in the interest of Ghana and Ghanaians. Not a rubber stamp Parliament, subservient to the whims and caprices of the Executive and/or the Judiciary.”

Judiciary, Executive “colluding”

He also raised serious concerns over what he describes as a coordinated e ort by Ghana’s Judiciary and Executive to undermine Parliament’s authority, framing it as an ongoing power struggle between the government branches.

Bagbin’s allegations follow a recent Supreme Court ruling, which upheld a previous decision blocking him from declaring four parliamentary seats vacant.

This development has intensi ed the debate over the constitutional boundaries of the Speaker’s powers and the judiciary’s in uence in parliamentary matters.

The Speaker had initially led an application challenging the Supreme Court’s intervention, arguing that Parliament, as a separate branch of government, should retain exclusive authority over its own decisions.

His application also sought to nullify a writ from Majority Leader Alexander Afenyo-Markin, which called for judicial intervention to prevent further declarations from Bagbin on the disputed seats.

Members running to Supreme court Further, he noted that Parliament weakens itself when its members keep running to

courts to settle or seek favorable determinations of not just legal matters but essentially political and governance questions.

“ It is my strong believe the matter before the Supreme Court can be settled within Parliament through matured deliberations and compromises. Please make no mistake; not all the strong men President Obama warned us about come in military uniforms. Some come dressed in suits. I hope, in my lifetime, Ghana shall have a Parliament and a Speaker who are truly independent from Jubilee/Flagsta House, or any Headquarters in the conduct of Parliamentary business.

Let me state unequivocally: Parliament owes its duty to the people who established and elected its members to serve and represent them. The wheels of Parliament will continue to turn, and no person would be allowed to disrupt Parliamentary proceedings or to undermine the democratic mandate of Parliament.”

Visa, the world leader in digital payments has partnered with Access Bank a leading nancial institution to introduce the Visa Business Debit Card, a new nancial product designed speci cally for Small and Medium Enterprises (SMEs) in Ghana. This collaboration aims to empower SMEs, which are the backbone of the Ghanaian economy, by providing them with a convenient and secure way to manage their business nances.

SMEs play a crucial role in driving economic growth and job creation in Ghana. They contribute signi cantly to the country's GDP and provide employment opportunities for a large segment of the population. The new Access Visa Business Debit Card is tailored to meet the unique needs of these businesses, o ering a range of bene ts that will help them streamline their nancial operations and enhance their growth potential.

Key Features of the Access Visa Business Debit Card:

• Global Acceptance: The card is accepted at millions of locations worldwide, providing SMEs with the exibility to make payments and withdrawals wherever they are.

•

Enhanced Security: With advanced security features, including EMV chip technology, businesses can have peace of mind knowing their transactions are protected.

• Reporting and Expense Management: The card allows businesses to track and manage their expenses more e ciently, with detailed transaction reports and spending limits. This feature will receive further enhancements and additional digital tools soon.

• Rewards and Discounts: Cardholders can take advantage of exclusive rewards and discounts on business-related purchases such as on advertising, logistics, travel, and redemption via https://smeoffers.poshvine.com

"This initiative underscores our commitment to supporting the growth and success of small businesses in Ghana. By providing SMEs with the tools they need to manage their nances more e ectively, we are helping to drive economic development and create opportunities for entrepreneurs across the country," said Andrew Uaboi, Vice President, Visa West Africa.

Speaking at the launch, Executive

Director of Retail and Digital Banking at Access Bank (Ghana) Plc, Pearl Nkrumah said “our aim is to fuel SME growth and this partnership rea rms our commitment to supporting and empowering SMEs across the country. Over the past years, we have impacted over 11 sectors, and we remain dedicated to providing our customers with innovative products like our newly launched Access Visa Business Debit Card that support their growth. The Access Visa Business Debit card is crafted to meet the unique business needs of SMEs, o ering nancial exibility, international access, and practical business solutions”.

Access Bank (Ghana) Plc, over the past 15 years, has demonstrated an unwavering commitment to understanding its customers’ needs, consistently delivering exceptional service, and em-

powering individuals and businesses alike. Since its inception, Access Bank (Ghana) Plc has been at the forefront of the nancial sector, providing a wide range of innovative banking solutions tailored to meet the unique needs of its customers. With a vision to be the world’s most respected African bank, Access Bank continues to build long-lasting partnerships that drive sustainable growth and economic transformation.

About Visa Visa (NYSE: V) is a world leader in digital payments, facilitating transactions between consumers, merchants, nancial institutions and government entities across more than 200 countries and territories. Our mission is to connect the world through the most innovative, convenient, reliable and secure payments network, enabling indi and economies to thrive. We believe that economies that include everyone everywhere, uplift everyone everywhere and see access as foundational to the future of money movement. Learn more at Visa.com.

About Access Bank (Ghana) PLC Access Bank (Ghana) Plc, a subsidiary of Access Corporation, is a leading full-service commercial bank in Ghana. Committed to driving nancial inclusion and providing innovative banking solutions, Access Bank continues to empower individuals and businesses across Ghana through its extensive product o ering. With a strong focus on superior customer service, sustainability and digital transformation, the bank remains dedicated to supporting the unbanked, creating opportunities for nancial growth, and ensuring that every customer enjoys seamless access to modern

Millicent Clarke, a global human capital leader whose work has covered 22 countries, has launched her rst book, Millie: My Gift of Bangles at the Ghana Association of Arts and Sciences, Airport Residential Area in Accra. The launch of the book, which highlights the power of resilience, self-belief, and leadership in overcoming life's challenges was attended by notable corporate individuals and leaders.

Millie: My Gift of Bangles re ects the numerous gurative bangles comprising precious and non-precious metals such as gold, silver, platinum, glass, wood, ferrous metals, plastic, and even paper, that were gifted to the author by her leaders. Speaking at the launch, Millicent Clarke captivated the audience with re ections on her own journey. She remarked that “Growing up as the rst child of ve, my initial experience of leadership came from managing my siblings and taking responsibility in our home,” she shared, recounting her journey from Achimota Primary to Archbishop Porter Girls and later to a ful lling corporate career. She emphasised that her book is not just about her career lessons but also some of the life lessons she had learnt from the leaders she had been privileged to

work with throughout her career.

Millie: My Gift of Bangles, written with aspiring leaders in mind, o ers a powerful message for anyone facing the pressures of leadership or breaking barriers, especially women in the corporate world. “Each story in Millie: My Gift of Bangles comes with a lesson, dedicated to all leaders and to those aspiring to lead. This is for anyone who feels the weight of being di erent and for women making strides in the corporate world,” she said, “Enjoy my gift of bangles, and let it remind you to break every barrier.”

Sir Sam Jonah, the Spe-

cial Guest of Honour at the book launch, Chairman of Jonah Capital, and Chancellor of the University of Cape Coast, lauded Millie: My Gift of Bangles as a guide for those striving to create their own opportunities and navigate challenges. “This book reminds us that opportunities do not simply appear before us, but we must make our own paths and build bridges over the challenges we encounter,” he said. Re ecting on the shared experiences of resilience, he added, “Every setback teaches resilience; every failure brings wisdom. While our backgrounds shape us, they should never con ne us. Through sheer determination and

belief in something greater, we rise.” Mr. Jonah further noted, “Leadership is a privilege, a responsibility, and above all, a profound trust shaped by the perspectives we share with others.”

FirstBank Ghana’s Managing Director and CEO, Victor Yaw Asante, who unveiled the book, Millie: My Gift of Bangles, said it is a compelling new book packaged in 20 unique chapters that explore exceptional leadership qualities and experiences, stating, “This book o ers profound insights into leadership, and I encourage everyone aspiring to lead to get a copy.” He also extended appreciation to all who purchased the

book, noting that they would be “rewarded with the bangles that Millie has shared with us,” symbolising the valuable lessons in the book.

Millicent Clarke was named Millicent Afriyie Donkor at birth. She is the immediate past Human Resource Director for StanChart Africa. Millicent is a deeply spiritual person who truly believes there is power in a name. She continually strives to meet the meaning of her name. Her mantra is “if you want to score, go to the eld and play.” Don’s sit on the sidelines.

Millie: My Gift of Bangles is now available at selected bookshops in the country and online.

The African Continental Engineering, Architecture, Construction and Real Estate Summit (ACEACRES) 2024 is set to bring together industry leaders, innovators, and stakeholders from across the continent and beyond. Scheduled for November 27-28, 2024, at the Berliner Platz Conference Centre in Accra, the summit aims to integrate the African built environment for socio-economic transformation.

Under the theme "Integrating Sustainable

Built Environment for Socio-Economic Transformation through New Generation Technology and Arti cial Intelligence," ACEACRES 2024 will provide a platform for over 400 in-person and 100 virtual participants to share knowledge, network, and explore business opportunities.

"The African built environment is at a crossroads," said Daniel Kontie, Founder and CEO of the Africa Continental Engineering & Construction Network Ltd, the summit's orga-

nizer. "We must harness innovative technologies and arti cial intelligence to drive sustainable growth and development."

Keynote speaker Engr. Margaret Aina Oguntala, National President of the Nigerian Society of Engineers, will share insights on the industry's future. Other notable speakers include Dr. Daniel McKorley, Executive Chairman of the McDan Group.

The summit's attendees will include building contractors, engi-

neers, architects, project managers, real estate developers, and government agencies from Nigeria, Rwanda, Kenya, Uganda, South Africa, Canada, Australia, New Zealand, the UK, and the US.

ACEACRES 2024 is made possible by principal sponsors Ger or Ghana Limited, Meprolim Ghana Limited, Premier Steel Ltd, McDan Group, Jemba Solutions Ltd, Fort Doors, Primus Group, Alusynco Hellas Services Ltd, Marbelino Marble Stones Décor, Mayfair Estate Ltd, Reroy Cables Ltd, Viva

Fiberglass Ltd, and J2 A able Properties.

The event will culminate in the African Continental Built Environment Industry Excellence Awards (ACBEIEA) Ceremony, recognizing outstanding achievements in construction technology, innovation, and sustainability.

By fostering collaboration and knowledge sharing, ACEACRES 2024 aims to propel Africa's built environment toward a more sustainable and prosperous future.

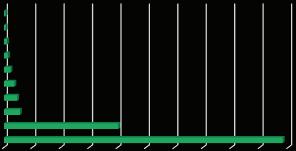

The Ghana Stock Exchange closed higher this week on the back of price increases by 7 counters The GSE Composite Index (GSE-CI) grew by 160.27 points (+3.67%) for the week to close at 4,529.30 points, reflecting a year-to-date (YTD) gain of 39.58%. The GSE Financial Index (GSE-FI) also gained 24.68 points (+1.11%) for the week to close at 2,239.89 points, reflecting a year-to-date (YTD) gain of 17.79%.

Market capitalization edged higher by 2.46% to close the week at GH¢101,938.10 million, from GH¢99,493.22 million at the close of the previous week. This reflects a YTD gain of 37.95%.

The week recorded a total of 5,920,591 shares valued at GH¢73,473,078.87, compared with 801,810 shares, valued at GH¢12,890,891.38 traded in the preceding week.

MTNGH dominated the volume of trades while New Gold Exchange Traded Fund dominated the value of trades for the week accounting for 91.28% and 82.70% of the volume and value of shares traded respectively.

The market ended the week with 7 advancers, as indicated in the table below.

Performance of GSE Market Indices

Volume and Value of Trades for Week Ending 01/11/2024

50,000,000

45,000,000

Capitalization for Week Ending 01/11/2024

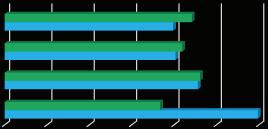

The Cedi furthered its depreciation run for the third straight week. It traded at GH¢16.3001/$, compared with GH¢16.1500/$ at week open, reflecting w/w and YTD depreciations of 0.92% and 27.12% respectively. This compar es with a loss of 25.44% a year ago.

The Cedi also depreciated against the GBP for the week. It traded at GH¢21.1126/£, compared with GH¢20.9579/£ at week open, reflecting w/ w and YTD losses of 0.73% and 28.32% respectively. This compares with a depreciation of 27.57% a year ago.

The Cedi slipped against the Euro for the week. It traded at GH¢17.6852/€, compared with GH¢17.4605/€ at week open, reflecting w/ w and YTD depreciations of 1.27% and 25.78% respectively This compares with a depreciation of 25.95% a year ago.

The Cedi lost grounds against the Canadian Dollar for the week. It opened at GH¢11.6352/C$ but closed at GH¢11.6916/C$, reflecting w/w and YTD losses of 0.48% and 22.93% respectively. This compares with a depreciation of 24.86% a year ago.

Performance of the Ghana Cedi against Selected Currencies

Source: Bank of Ghana

Source: Bank of Ghana

The government raised a sum of GH¢4,078.20 million for the week across the 91 -Day, 182-Day and 364-Day Treasury Bills. This compared with GH¢4,421.54 million raised in the previous week.

The 91-Day Bill settled at 26.56% p.a. from 26.19% p.a. last week whilst the 182 -Day Bill settled at 27.58% p.a. from 27.29% p.a. last week. The 364Day Bill settled at 29.04% p.a. from 28.97% p.a. last week

The tables below highlight primary market activity at the close of the week

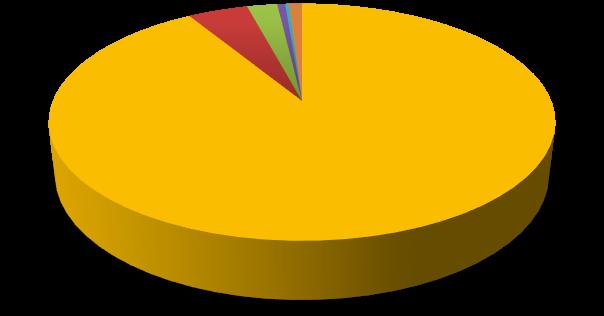

Oil prices closed slightly lower , on a report that Israeli Prime Minister Benjamin Netanyahu will hold a meeting for a diplomatic solution to the war in Lebanon. Brent futures traded at US$73.10 a barrel, compared to US$75.63 at week open, reflecting w/w and YTD depreciations of 3.35% and 5.11% respectively.

Gold prices edged higher , trading close to record highs as the run-up to the 2024 presidential election and uncertainty before upcoming data prints kept safe-haven demand in play Gold settled at US$2,749.20, from US$2,742.20 last week, reflecting w/w and YTD gains of 0.26 and 32.70% respectively

The price of Cocoa increased for the week. Cocoa traded at US$7,321 50 per tonne on Friday, from US$6,789.50 last week, reflecting w/w and YTD appreciations of 7.84% and 74.49% respectively.

CIDAN Investments Limited is an investment and fund management company licensed by the Securities & Exchange Commission (SEC) and the National Pensions Regulatory Authority (NPRA).

Name: Ernest Tannor

Email: etannor@cidaninvestments.com

Tel: +233 (0) 20 881 8957

Name: Moses Nana Osei-Yeboah

Email: moyeboah@cidaninvestments.com

Tel: +233 (0) 24 499 0069

Name: Julian Sapara-Grant

Email: jsgrant@cidaninvestments.com

Tel: +233 (0) 20 821 2079

YTD Performance of Selected Commodity Prices

CIDAN Investments Limited

CIDAN House

House No. 261

Haatso, North Legon – Accra

Tel: +233 (0) 27 690 0011/ 55 989 9935

Fax: +233 (0)30 254 4351

Email: info@cidaninvestments.com

Website: www.cidaninvestments.com

Movin g average convergenc e / divergence (MACD): It is a technical indicator to help investors identify price trends, measure trend momentum, and identify entry points for buying or selling

Source:

https://www.investopedia.com/terms/m/macd.as p

Disclaimer: The contents of this report have been prepared to provide you with general information only. Information provided in and available from this report does not constitute any investment recommendation.

The information contained herein has been obtained from sources that we believe to be reliable, but its accuracy and completeness are not guaranteed.

Following the total bid oversubscrip�on, the week-on-week yields also soared further, at least more significantly than the previous week’s increase , witnessing a n upward reac�on of 24.57bps, 26.03bps a nd 23.35bps increases across the 91-, 182- and 364-day bills respec�vely.

T-bills: Government to borrow GH¢4,010.00 Million this week across the 91, 182 and 364 day bills to cater for maturi�es totaling circa GH¢3,760.00 Million

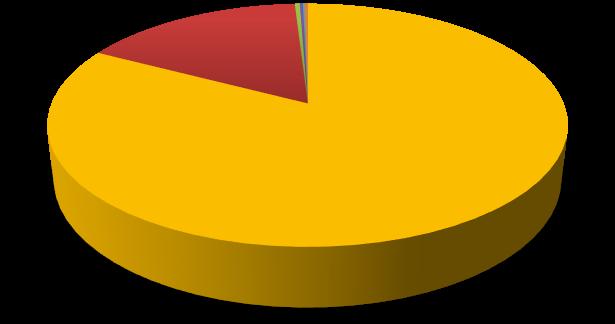

Shares: CAL Bank PLC Shares dominates GSE equity market trades despite a 0.02p price drop to close the week at GHS0.26 per share GLD shares on the other hand is the bigge st gainer with a price increase of GH¢4.15 to close at G H¢427.96 per share

Mutual Fund: NTHC Horizon Fund reports a Year-To-Date (Y TD) performance of 28.86% and a Net Asset Value (NAV) growth of 36.92% for the week ending O ctober 18, 2024

Economy

IMF Board scheduled to meet on Dec 2 to discuss Ghana’s Third Programme Review for a possible relea se of $360 million to the BOG to support Ghana’s budget and balance of payment needs

In today’s rapidly changing world, sustainability has become a critical component of business strategy across all industries. The nancial industry, which plays a critical role in the nancing and protection of businesses and their assets is now expected to drive greater sustainability by investing and protecting ventures which are sustainable. This trend therefore presents, the insurance industry which is an integral core of the nancial industry a unique opportunity to drive positive change and sustainability by incorporating Environmental, Social and Governance (ESG) considerations into its operations. Before I delve into the subject, one may ask; what is sustainability and how can the insurance industry drive sustainability and expected positive change?

Sustainability in business practice refers to strategies and operational processes that meet the needs of the present without compromising the ability of future generations to meet their own needs. It involves integrating environmental, social, and economic considerations into decision-making processes to create long-term value for both the business and society. Sustainable insurance involves integrating environmental, social, and governance (ESG) factors into insurance products, policies, processes, solutions and practices. This

includes promoting green technologies, supporting climate resilience, ensuring fair, ethical and governance practices. For businesses, especially SMEs, this means not only protecting assets and lives but also contributing to broader sustainability goals.

Sustainable insurance is increasingly recognized as a vital component of responsible business practices worldwide. For Small and Medium Enterprises (SMEs) in Africa, the integration of sustainability into insurance presents both signi cant opportunities and formidable challenges. This article delves into how African SMEs perceive and engage with sustainable insurance, highlighting the unique factors in uencing their adoption of eco-friendly and socially responsible insurance solutions. Barriers to Sustainable Insurance Small and Medium Scale Enterprises (SMEs) in Africa are faced with enormous challenges in the eld of sustainable insurance.

Limited awareness and understanding: One of the signi cant barriers for sustainable insurance among SMEs in Africa is the lack of awareness and understanding of sustainable insurance. Many small business owners are unfamiliar with the concept and how it can bene t their operations. The focus for many SMEs remains on traditional insurance products that address immedi-

ate risks rather than long-term sustainability. A medium sized real estate company may not prioritize sustainable practices due to a lack of awareness about how green insurance products could help mitigate environmental impacts and improve operational e ciency. High costs of sustainable insurance: Sustainable insurance products often come with higher premiums compared to traditional policies. SME operations are often very sensitive to cost due to their lower volumes and margins. Therefore, these increased costs can be a signicant deterrent. The higher upfront cost may outweigh the perceived bene ts, pushing SMEs to opt for less sustainable but more a ordable options. An SME in the agriculture industry might nd the cost of a climate-risk insurance policy prohibitive compared to standard coverage, impacting its ability to invest in sustainable practices. Not just the higher premiums, some of the practices that leads to sustainable business in themselves come at a high cost. For example, the cost of installing and maintaining green houses could be prohibitive to an SME in the agricultural industry just as the cost of installing green energies such as solar is very high to the average SME in the services industry. Limited availability of sustainable insurance

products: In many African countries, the insurance market is still developing, and there is a limited range of sustainable insurance products available. This scarcity makes it dicult for SMEs to nd products that align with their needs and sustainability goals. A tech startup in Ghana might struggle to nd insurance policies that cover risks associated with innovative green technologies or sustainable business practices.

Regulatory and policy gaps:

The regulatory environment for sustainable insurance in Africa is often underdeveloped. Without supportive policies and regulations, insurers may be reluctant to o er sustainable products, and SMEs may lack incentives to adopt them. The absence of regulations supporting green insurance products means insurers have little motivation to develop such o erings, leaving SMEs limited or unsuitable options.

In dealing with the barriers to sustainable insurance, raising awareness about the bene ts of sustainable insurance is crucial. Insurance providers and related stakeholders can play a signicant role in educating SMEs about how sustainable insurance can mitigate risks, enhance resilience, and contribute to long-term nancial stability.

Developing a ordable and tailored sustain-

able insurance products for SMEs would help overcome cost barriers. Insurers could design products that cater speci cally to the needs of small businesses, providing coverage that is both sustainable and economically viable. Parametric insurance for instance is a growing trend, particularly in regions vulnerable to climate change. It provides payouts based on prede ned parameters like weather conditions or natural events, rather than actual losses. A farmer in Kenya could purchase insurance that automatically pays out if rainfall drops below a certain level, protecting against drought. According to the World Bank, parametric insurance can reduce the time it takes to receive a payout by up to 90% compared to traditional claims, making it highly bene cial for SMEs in agriculture, which are exposed to climate-related risks. Insurance for Renewable Energy Projects: SMEs involved in renewable energy projects, such as solar installations, can bene t from specialized insurance that covers both equipment and operational risks. The African Development Bank estimates that Africa could see over $7 billion in investments in renewable energy by 2025, and insurers are creating products speci cally to cover these growing sectors.

Losses and Insurance

Uptake: According to Swiss Re, global losses from natural catastrophes reached $270 billion in 2021, of which only 40% were insured. This insurance gap is even larger in Africa, where climate risk insurance could mitigate signicant economic damages. The adoption of climate risk insurance, such as ood or drought coverage, could reduce losses for SMEs by up to 30%, providing a safety net for vulnerable sectors like agriculture

Microinsurance o ers a ordable and accessible insurance options for low-income individuals and businesses, making it a suitable model for SMEs in Africa. Companies like BIMA and Hollard in Ghana have introduced micro / SMEs insurance products that are tailored to the needs of small businesses. These initiatives provide essential coverage for business risk and could be expanded to include sustainable insurance products, o ering lower-cost options that support green practices. Microinsurance programs have reached over 60 million individuals globally, with a signi cant portion in Africa.

Public-private partnerships can facilitate the development and distribution of sustainable insurance products. Governments and its agencies such as Environmental Protection Agency (EPA), development partners like the IFC, GIZ, GIRSAL, World Bank to mention a few, and the Insurance industry can collaborate to create incentives and

frameworks that support sustainable practices among SMEs.

The African Development Bank’s Climate Risk Insurance Initiative aims to enhance access to climate risk insurance for SMEs through collaborative e orts between public and private sectors. Advocating for supportive policies and regulations is essential to foster a conducive environment for sustainable insurance.

The African Risk Capacity (ARC), an African Union initiative, provides weather-based insurance products to African countries and SMEs to improve disaster preparedness. ARC estimates that every $1 spent on insurance results in $4 of benets through reduced economic losses and quicker recovery times.

Sustainable insurance products are experiencing rapid growth.

A report by the Insurance Europe Federa-

tion found that the global market for green insurance products grew by 20% in 2022. In Africa, however, only about 10% of SMEs currently have access to these products. Expanding availability could increase resilience in sectors like energy and agriculture, which are crucial to economic development Below are some examples of Sustainable Business Practices SME’s can adopt.

• Implementing energy-e cient technologies in operations.

• O ering eco-friendly products or packaging.

• Partnering with suppliers who follow ethical and sustainable practices.

• Committing to reducing carbon footprints through renewable energy and carbon o set initiatives.

• Waste reduction, implementing recy-

cling programs, automate processes and reduce / eliminate paper usage.

• Encourage carpooling, use electronic/ hybrid vehicles.

• Diversity and inclusion, foster a diverse workforce, promote equal opportunities.

• Usage of recycled and biodegradable materials Incorporating sustainability into business practices not only bene ts the environment and society but would also drive innovation, resilience, and pro tability.

In conclusion, the journey towards sustainable insurance for SMEs in Africa presents both challenges and opportunities. While the nancial vulnerability of SMEs is evident, the need for insurance solutions that align with the unique risks of these businesses is equally urgent. Stakeholders, including

governments, insurers, and development organizations, must collaborate to create policies and products that are not only accessible but also adaptable and a ordable to the dynamic needs of African SMEs. By integrating sustainability into insurance frameworks, we can support the growth and resilience of this vital economic sector, fostering an environment where businesses thrive amidst uncertainty. The future of sustainable insurance in Africa depends on a collective e ort to innovate, invest, and ensure no business is left behind.

Writer: Iddrisu Nashiru, MD Hollard Life Assurance, 1st Vice President of Ghana Insurers Association. A chartered Insurer (CII UK and Ghana) a fellow of the Chartered Institute of Ghana (FCIIG) and a certi ed ESG professional.

The Institute for Liberty and Policy Innovation (ILAPI) has uncovered signi cant sums in dormant accounts with the Bank of Ghana (BoG). Between 2016 and 2023, over GH¢167.8 million, $14.6 million, GBP 2.4 million, and EUR 2.3 million accumulated in these accounts. Additionally, 1,448,660 dormant accounts

were transferred to the BoG between 2021 and July 2024.

ILAPI's Next of Kin project aims to facilitate access to these funds, streamlining legal procedures and addressing complexities. Currently, securing Letter of Administration, Death Extract, and navigating probate processes can be cum-

bersome, leading to abandoned claims and prolonged poverty.

The BoG transfers dormant accounts to its registry after ve years of inactivity, as per Section 92 of the Banks and Specialized Deposit-taking Institutions Act, 2016. ILAPI recommends:

- Enhancing public

education on next-of-kin appointments

- Issuing directives for banks to request Ghana Card information

- Clearly de ning dormant account management policies

- Reviewing laws to enable BoG to trace bene ciaries

- Releasing annual

reports on dormant accounts

- Collaborating with local government to identify bene ciaries

ILAPI commends the BoG's literacy campaigns but urges proactive measures to address transparency, nancial governance, and economic challenges faced by eligible families.