When Kentucky businesses need a time-tested provider for their insurance needs, they turn to KEMI. As Kentucky’s leading provider of workers’ comp, employers in all 120 counties from Pikeville to Paducah have counted on KEMI for our financial stability, competitive rates, and superior service since 1995.

We’re committed to delivering on the promise to be here when our customers need us the most. Since 2010, KEMI has paid over $104 million in dividends to policyholders, and we’ve lowered rates by 40% thanks to our sound underwriting principles, a focus on workplace safety, and proactive claims management.

To learn more or obtain a workers’ comp quote, visit us online at kemi.com or speak with an underwriter at 1-800-640-KEMI (5364).

Chair From the

A MESSAGE FROM CHRIS WISEMAN

Planning Ahead

As we move from spring into the heart of summer, I hope your agency is feeling the momentum this season often brings. While Big I Kentucky continues to advocate and support our members in real time, we’re also focused on helping agencies look ahead, especially when it comes to one of the most important long-term decisions an agency owner will make: perpetuation.

Whether you’re currently in an ownership role or looking to move in that direction, succession planning isn’t something to put off. It takes time, strategy and the right resources… fortunately, Big I Kentucky is equipped to help on all fronts.

Here are a few core considerations as you begin thinking about your agency’s future:

1. Define Your Path

Perpetuation isn’t one-size-fits-all. You may be considering a third-party sale, transitioning ownership to a family member or structuring an internal plan. Each path has its pros and cons, and the best option depends on your goals, timeline and the legacy you want to leave.

2. Clarify Your Priorities

Are you focused on maximizing agency value? Preserving your brand? Supporting a seamless transition for your team and clients? Identifying your top priorities early in the process will help you stay focused and make strategic decisions with confidence.

3. Use Trusted Resources

This process can feel overwhelming, but you don’t have to navigate it alone. Big I Kentucky can connect you with specialists, tools and peer perspectives that are grounded in the independent agency model. Don’t hesitate to lean on the association. This is exactly why we’re here.

Stretching Your Marketing Budget

In addition to perpetuation planning, Big I Kentucky is also focused on helping members grow. The Trusted Choice Marketing Reimbursement Program is a great example. You can be reimbursed up to 50% (with a $1,000 cap) on costs related to digital marketing, vendor partnerships or marketing training. It’s a smart way to extend your reach without overspending.

Stay Engaged: Upcoming Opportunities

There’s no better way to maximize your membership than through active participation. Be sure to take advantage of these upcoming events:

• July 17 – Quarterly Call with the KY Insurance Commissioner

• August 14 – Emerging Leaders Clay Shoot

• August 19 – Board Service Project at the Bowling Green Hot Rods Game, supporting Donate Life

• August 26 & Sept 3 – Big I Law & Order (free virtual CE, 4 hours)

• November 19–21 – Big I Kentucky Annual Convention & Trade Show

Thank you for continuing to make Big I Kentucky the strong and connected association it is today. If you ever have questions, need guidance or want to get more involved, don’t hesitate to reach out.

Commissioner’s Desk

When you were in high school history classes were you bored? I enjoyed Kentucky and U.S. History but not so much European History. I bring this subject up because this year, insurance regulators and our organization, the National Association of Insurance Commissioners (NAIC), are celebrating 80 years of the McCarranFerguson Act. Why should you as an insurance agent care about legislation passed in 1945? The McCarran-Ferguson Act affirmed the authority of individual states to regulate insurance within their borders. So, as an agent, you do not have bureaucrats in Washington D.C. regulating your license just your friendly KY DOI regulators. In 1752 – 24 years before the United States Declaration of Independence was signed – Benjamin Franklin – yes, THE Benjamin Franklin – and his fellow firefighters founded the Philadelphia Contributorship, our first insurance company in the United States. The importance of insurance and its protections for our citizens has long been known.

From 1752 until the mid 1800s, insurance went unregulated in the U.S. By 1871, most states had established insurance regulation. Kentucky’s regulatory bureau was established in 1870. To give a very brief summary, in 1942 the Department of Justice and a grand jury in Georgia indicted the Southeastern Underwriters Association, 27 of its officers and 198 member companies charging them with antitrust violations for “fixing premium rates.” This litigation proceeded all the way to the U.S. Supreme Court and it was determined (though not by unanimous opinion) that insurance was “commerce among the states” and the Constitution permitted Congress to regulate insurance.

It is important to note that before this decision, insurance had been regulated since the mid 1800s by the states, so this U.S. Supreme Court decision was monumental. The prospect of

a federal takeover was upsetting to both the insurance industry and to its regulators. As a result, after a massive lobbying effort of Congress and the McCarran-Ferguson Act, was passed in 1845 restoring the regulation of the insurance industry back solely to the states.

It just makes sense doesn’t it. While there are similar issues across the states, each state can have different issues of concern. Kentucky has convective windstorms and tornadoes. Alaska has neither of these perils but has atmospheric rivers and permafrost melts. The Florida DOI has had to take measures to stabilize its marketplace that would have been detrimental to Kentucky’s marketplace.

Each state knows its marketplace and its consumers. We also know our companies and our agents. State based regulation allows the regulators to do their job based on local conditions and we are closest to our consumers. State based insurance regulation made sense 80 years ago and still makes sense today. Thank you for your trust in the Kentucky Department of Insurance to do its job. I am proud of our Department and we are here to serve the agents, the companies and the consumers.

•

WEST BEND

West Bend has a long history of writing workers’ compensation insurance. Our underwriters are knowledgeable and experienced. Our loss control reps have the expertise and tools to help keep employees safe. And our claims practices are the best in class.

From Main Street-type businesses to specialty businesses like childcare, West Bend has the experience and expertise to protect businesses of many kinds and many sizes. We want to write all of your workers’ compensation business, small to large!

When you select West Bend for your valued customers, you can rest assured you made the right choice. After all, we are the best remedy for workers’ compensation. Learn more by visiting thesilverlining.com

Upgrade your flood experience

�it� t�ree li�le moves.

“Our agency was approached by our Selective territory manager, Gregg Porter, to roll a portion of our ood business from another carrier to Selective. We were pleasantly surprised at how easy and seamless the whole process was. Gregg came into our office and basically did all the work for us. We had a high success rate and couldn’t be happier with Selective. Their customer service representatives and underwriters are very knowledgeable, friendly and always helpful. We are very satised with the whole experience and with Selective!” – IIABL Member

Selective makes the transfer process easy and profitable for IIABA members. Selective does not use any third party administrators for our processing, which allows us to tailor a transfer plan that works for both you and your customers. Our team will work directly with your agency to collect the required underwriting documents. Then our rollover underwriting team will handle the processing, including sending out a letter to your customers letting them know of the change. We also provide you with a real-time rollover tracking report to help monitor the status of the transfer.

Selective offers competitive commissions and transfer incentives for rollover business.

Selective began writing flood insurance in 1984 and has been the IIABA endorsed flood carrier since 2001. Point, click, roll and join us today!

To discuss transfer opportunities, or to place new �lood business with Selective, contact:

Don Burke

National Flood Marketing Manager Selective Insurance

don.burke@selective.com (765) 577-0330

HELP! A KEY CARRIER

IS CANCELING MY CONTRACT – HOW WILL IT AFFECT MY AGENCY VALUE?

By: Jeff Smith, IA Valuations

You just got one of your least favorite notices: one of your key carrier partners has given you the dreaded 180-day written notice to terminate your agency agreement. Whatever the reason given, it likely does not matter because it is damaging to your business on so many levels.

It will impact your relationship with your clients, retention rate, growth, stress on your staff, carrier lineup, profitability and agency value.

For the purposes of this article, we are going to explore how it will impact value and what to do about it to preserve your agency’s value.

How a Key Carrier Contract Cancellation Impacts Agency Value

First and foremost, it comes with an emotional blow. One of your key carrier partners has made the decision to terminate your relationship. It hurts. You

built your business with them, you gave them good, profitable business for years, but after a few years of low growth and/or high loss ratios, the longstanding relationship is now over and you both must move on.

The emotional turmoil is arguably the hardest to overcome. While this stings especially in a relationship business, remember, the company made a business decision that they feel is in its best business interest, and now you must do the same. You have clients, staff, a reputation and a legacy that you need to protect. It’s time to act. Clear your head, develop a plan to move on, and do it quickly, as you’ve got a lot of business to move.

Second, this cancellation questions the practical impact of your credibility with your clients. You’ve been insuring your clients with this carrier for years, and now they are going to get a cancellation notice from the carrier if you don’t move them first. You must get out in front of the carrier communication.

Once you receive notice from the carrier notifying you of the pending termination, run a list of your clients with the carrier, prepare a professional communication and reassure them that the relationship is with you, not the carrier, and that you have other options.

Third, it brings additional stress to have to move the book of business you have with that carrier, particularly in a hard market. The stress level on your staff will vary depending on the size and complexity of the book, your other carrier options and whether they are open for a book roll, and your staff’s experience with moving a book in a condensed timeframe.

In every valuation analysis conducted by IA Valuations, we evaluate your carrier concentration and strength of relationships with your carrier partners. We base this on the longevity of the relationship, loss ratio, growth, profit-sharing and percentage of business with each carrier.

In our analysis, we have found that small to midsized agencies are often top heavy with their lead carriers. In fact, our data shows that small agencies typically place almost 50% of their business with their lead carrier. With the exception of agencies over $5M in revenue, every other agency category on average exceeds the recommended percentage of business with their lead carrier.

We recommend an agency limit their carriers to no more than 25% market share. If you have 30%-80% of your business with one carrier and that relationship ends, it will have a profoundly greater impact than if you have 15%-25% of your business with the same carrier.

This is why we recommend every agency have a diverse mix of carrier relationships to meet the needs of their agency and clients. We focus much of our valuation analysis on the top 5 carrier relationships in an agency because, in most small to mid-size agencies, the top 5 carriers average as high as 89% and 71% of written premium in the agency. This represents an ideal balance, spread out enough to reduce risk but not so spread out that the agency misses out on the benefit of the carrier enticements like profit-sharing, overrides, personal underwriting, trips and advisory councils. This type

of spread in an agency keeps you relevant with all 5 carriers and gives you options in the event one relationship changes.

As to the profile of those carriers should be will depend on your business plan and goals, location and many other factors. Generally speaking, IA Valuations would recommend you have an anchor carrier partner relationship with a super-regional carrier like Cincinnati, Auto Owners, Erie, Hanover, Selective or other carrier of this size. You should add two to three regional and small mutual carriers into your lineup like Westfield, Grange, Encova, Donegal, Utica, and Central to name a few. Finally, your agency should have at least one national carrier relationship like Nationwide, Liberty Mutual/Safeco, Travelers, Progressive or other national option. It may also be beneficial for your agency to have a relationship with some of the new tech-driven specialty carriers like weSure, Branch and some of the other recent startup insurers.

One of the pillars of the IA system is having multiple carrier options. If an agency chooses to place a majority of its business with one carrier, that creates a higher risk and is much more akin to the captive business model than the independent. A higher concentration of business with one carrier has benefits of being in the President’s Club, qualifying for company trips, higher profit-sharing checks and more attention from the carrier reps and leadership. The tradeoff is greater risk to the agency’s stability and value if the relationship changes, the carrier’s underwriting appetite changes or the carrier has a string of bad years.

How to Protect Your Agency Value with Your Carrier Relationships

First, understand the provisions and protections in your agency agreement and state law. In your state, it is likely the law establishes the procedures a carrier must follow in order to cancel an agency agreement. If your agency agreement is at risk, you should contact the Big I Kentucky to get an interpretation of the law. In addition, you should become familiar with the provisions in the agency agreement that cover termination.

Document all the steps the carrier is taking to make sure they are incompliance with the agency

agreement and law. Carriers do not take those actions lightly, so it is likely they are working with their legal counsel to ensure they are following the letter of the law. In the event they have not followed the required steps, you should appeal the termination decision to the carrier leadership and ask for a reconsideration of the decision or a delay in the action.

Second, do an analysis of your book of business with that carrier. Get an understanding of the number, type, loss history and complexion of your accounts. Run reports in your agency management system and the carrier portal to get all the information you can on your book with the carrier terminating your appointment. Know the book of business inside and out – what are the good accounts that you must save, which are the middle accounts that you want but do not absolutely need and which are the accounts that you have been looking for a reason to part ways with? Prioritize the accounts in order of importance to your agency.

Third, develop a plan to retain the business. Prepare your staff with training, create a communication plan with your clients, and develop an appetite guide to market the accounts with your existing carriers and prospective carriers. Approach your current

term. Do your research on prospective partners so you don’t find yourself in a similar situation in the future.

Finally, move the business with purpose and precision. Retaining business is far easier than getting new business, so prioritize this effort with your team. Create goals and incentives with the team to get the book moved within the timeframe allotted by the agency agreement or state law, typically 180 days after notification of termination. Know you are going to bleed some business when word leaks out in the community that you have lost a key appointment, but do all you can to save those accounts and your business.

Conclusion

Agency-carrier relationships are prone to change. An agency must be prepared to deal with sudden, unexpected changes to key carrier relationships. Diversifying your agency relationships will ensure that your agency can survive unexpected carrier relationship changes – be it a termination, change in underwriting appetite, acquisition by another carrier or a carrier pulling out of a geographic location or type of business.

Do you sponsor a retirement plan for your agency?

There is a continuous stream of judicial and regulatory developments in the 401(k) plan world with many addressing the definition and duties of a plan fiduciary. Many plan sponsors mistakenly believe that they are not a plan fiduciary or have outsourced that role to another party. In reality, while steps can be taken to mitigate duciary risk, no agency owner can eliminate that role entirely.

The Department of Labor expects a plan fiduciary to perform responsibilities that include:

Acting solely in the interest of plan participants and their beneficiaries with the exclusive purpose of providing benefits to them

Carrying out their duties prudently

Following the plan documents

Diversifying plan investments

Paying only reasonable plan expenses

The Big “I” MEP 401(k) Plan, available exclusively to Big “I” members, has helped many agencies fulfill their fiduciary obligation by reviewing their plan expenses and educating them on the true cost of their plan. In addition, many were able to reduce their recordkeeping and investment expenses.

Let us compare your plan to our and industry benchmarks! Don’t hide–thrive. Contact us today for a complimentary plan consultation.

THE STATE OF THE HEALTHCARE MARKET 2025

By: Arlington/Roe

Our Healthcare & Human Services team recently attended the PLUS Healthcare & MedPL Symposium. The event brought together industry leaders for educational sessions and valuable networking opportunities. Below is a summary of the team’s key takeaways from the event.

Market-Wide Observations

The healthcare insurance landscape is experiencing heightened competition, with newer markets entering aggressively—particularly in pricing and underwriting. This volatility could lead to rapid market exits. Submission counts remain high, with expectations for growth from markets. However, despite the positive outlook, there are concerns with specific exposures such as abuse and HNOA, and

there is still a very limited appetite for correctional risks.

Physicians Market

Premiums in the physicians’ market are trending upward, with an average increase of 5%. A major development is the reduction of tort reform in New Mexico, which has led to significant verdicts such as the $35 million judgment that resulted in the collapse of Care RRG. This highlights the volatility of the market, especially for risk retention groups (RRGs), focused on high-risk specialties like family medicine and OB-GYN in states such as New York, Florida, and California.

With claim activity now double the national average,

carriers are becoming more cautious. Still, some markets remain committed, and others are even looking to expand their footprint in this space.

Social Services Market

The social services sector is facing disruption, particularly in coverage for adoption and foster care risks. This instability is expected to drive rate increases and has already prompted some carriers to exit the space. While these changes may create new opportunities, they also introduce challenges as the market adjusts.

Underwriting appetite remains largely unchanged for most social service accounts, except for larger accounts over $500k in premium. There’s a noticeable increase in submissions for behavioral health risks, including ABA therapy, outpatient and inpatient services, and sober living facilities. Large accounts ($250k–$1M) may attract primary coverage from carriers, which could indicate a potential strategy for how these risks are being approached from an underwriting perspective.

Long-Term Care

Several RRGs, including MIG and MMIC, continue to compete in the long-term care space, though some are showing signs of stress. Claims experience remains steady but costly, with frequent indemnity payouts for falls, improper care and wound-related

issues. These claims continue to be significant concerns for carriers in this segment.

Allied Healthcare

The allied health market is showing signs of softening. Despite carriers operating at combined ratios above 100%, the market remains competitive, and carriers are open for new business. We are continuing to see significant increases in GLP-1 related risks, specifically when used for weight-loss purposes. Classes that we are seeing carriers interested in writing include home health, hospice, clinics, surgery centers, labs, imaging and pharmacies.

Final Thoughts

The 2025 healthcare insurance market is marked by both volatility and opportunity. From shifting carrier strategies and market exits to evolving risks in social services and physician coverage, the landscape is dynamic and complex. Carriers are navigating rising loss costs and nuclear verdicts while staying alert to potential growth areas—particularly in allied healthcare.

At Arlington/Roe, our Healthcare & Human Services team is committed to staying ahead of market trends and sharing market knowledge. Whether you’re managing complex risks or exploring emerging coverage needs, we’re here to help you find the right solution.

We’ve been Doing the Right Thing since 1964. We are a third-generation, family-owned, independent managing general agency and wholesale insurance broker with a history of valuing and trusting business relationships. Our underwriters and brokers coordinate among specialty teams to meet the needs of multi-faceted risk opportunities, piecing each risk puzzle together for our producers. We strive to be a premier resource through our core pillars of honesty, integrity, respect and trust.

A Member of Harford Mutual Insurance Group

Clearpath Specialty, a Member of Harford Mutual Insurance Group provides monoline Workers' Compensation insurance through a network of independent agents in Georgia, Indiana, Kentucky, Tennessee, and West Virginia where we write business. We are committed to providing tailored solutions, ensuring businesses receive comprehensive coverage that meets their unique needs.

WHAT'S REALLY PUTTING YOUR AGENCY AT RISK?

By: the AgencyFocus team

Independent insurance agencies are built to manage risk, but most are only focused on their clients' risk profiles, not their own.

Ask yourself this: if a buyer or banker evaluated your agency tomorrow, what risks would they see? What would you learn that you have been ignoring?

Whether you're planning to grow, perpetuate, or sell, the risk inside your own business determines whether you are building something that lasts or something that stalls.

To help agencies see these blind spots clearly, we break risk into three main categories: Performance, Concentration, and Culture and Continuity. Each includes a set of key indicators that, when scored together, reveal the overall health and resilience of your agency.

Here’s what to look for and why it matters:

1. Performance: Is Your Business Healthy Today?

Performance risk reflects how efficiently and profitably your agency is operating. Many owners

focus on revenue and new business, but healthy agencies are also monitoring retention, account depth, and loss ratio.

Key Risk Factors:

• Growth Rate: Is your revenue growing organically, or just through rate increases?

• Profitability: How much profit are you truly generating once contingencies are removed?

• Size: Smaller agencies may face greater operational or talent risk due to limited resources.

• Retention: Are you tracking customer, policy, revenue, and premium retention accurately?

• Loss Ratio: High loss ratios erode carrier trust and impact contingency income?

• Policies per Client: A measure of account rounding and relationship strength.

• Account Age: Older accounts often signal loyalty and stability.

• Producer Age: Is your sales team aging without successors in place?

• Transferability: Can client relationships be smoothly handed off, or are they persondependent?

Why It Matters:

Performance indicators drive your agency's ability to predict and repeat success. Without clarity on

retention or profitability, you may be making decisions based on inaccurate assumptions. That creates risk and can limit long-term value.

2. Concentration: Where Are You Overexposed?

Concentration risk occurs when too much of your revenue, relationships, or operations depend on a single point of failure. That might be one producer, one carrier, or a handful of large clients.

Key Risk Factors:

• Owner Dependency: Do all roads lead back to you?

• WASA (Written and Signed Agreements): Are your producers contractually tied to the business?

• Producer Concentration: Is growth driven by one or two people?

• Carrier Concentration: Are you heavily reliant on just one or two carriers?

• Carrier Rating: Are you placing business with financially stable markets?

• Customer Concentration: What percentage of your revenue comes from your top clients?

• Top Ten Customer Dependency: Could you weather losing one major account?

• Niche Dependency: Are you too heavily invested in one vertical or industry?

• Regional Exposure: Would a change in one geographic area significantly impact your book?

• Mix of Business: Is your revenue diversified across personal, commercial, and other lines?

Why It Matters:

Buyers and lenders evaluate concentration risk closely. Too much reliance on a few relationships or revenue streams reduces your agency's resilience and its value. The more evenly distributed your income and influence, the more stable your business becomes.

3. Culture and Continuity: Can You Sustain What You Have Built?

This is where long-term risk lives. Even agencies with great numbers can falter if they lack leadership planning, staffing depth, or scalable systems.

Key Risk Factors:

• Age of Team: Is retirement looming without replacements identified?

• Ownership Structure: Is ownership clearly documented and aligned with your goals?

• Successor Identified and Trained: Do you have someone ready to take the reins?

• Account Management Age: Are your service team members nearing retirement too?

• Relationship Depth: Are client relationships shared across your team or siloed?

• Compensation Plan: Are your incentives driving the right behavior?

• Hiring and Training Plans: Can you reliably onboard and develop new talent?

• Incentives: Do rewards align with retention, service, and growth?

• Documentation: Are your processes and workflows repeatable without verbal instruction?

• Technology: Is your tech stack helping you grow or holding you back?

• Customer Experience: Are you delivering consistent and modern service across the board?

• Leadership Continuity: What happens if you or a key leader steps away?

Why It Matters:

These risks determine whether your business can evolve. Culture and continuity affect morale, retention, and value transfer. When buyers or successors see an agency built on verbal handoffs and aging talent, they see future problems instead of future opportunity.

What To Do Next

Start with a simple self-assessment. Score your agency on each of the 31 risk factors using a scale of 1 to 5, with 1 being high risk and 5 being low. Ask your leadership team to do the same. Then compare and discuss.

You might find you are stronger than you thought. Or you might discover blind spots that have been hiding in plain sight.

If you would like a copy of the full risk assessment worksheet, reach out to our team and we will send it your way.

There is no such thing as a zero-risk agency. But there is such a thing as an informed one. The better you understand your risk profile, the more confidently you can invest, grow, and lead.

All the agency tech guidance you need in one place.

Catalyit is the ultimate technology ally for independent insurance agents. We’re here to guide you through the tech landscape to help your agency thrive in the digital age.

Why Catalyit?

Smart Technology Choices

Avoid costly mistakes with our trusted guidance.

Enhanced Agency Performance

Leverage our insights to get the most out of your tech investments.

Stay Informed

Keep ahead with the latest in tech trends and updates.

Save Time

Efficient solutions that let you focus on what matters—your clients.

Achieve More

Stress less about tech and focus on growing your business.

Start transforming your agency today!

Agency Tech Assessment & TechSelectors™

Understand your tech needs and how to fulfill them.

Generative AI Guide

Get the latest AI news and recommended tools.

Guides & Reviews

Make informed decisions with our comprehensive reviews.

Consulting

Our advisors can help identify your agency’s tech challenges & implement the solutions.

DISASTER RECOVERY APPS

WHAT EVERY INDEPENDENT INSURANCE AGENT SHOULD HAVE IN 2025

By: Catalyit

Agents must be equipped with the right tools to respond swiftly to disasters. From wildfires in the West to hurricanes in the Southeast to storms with flooding just about anywhere, making sure you’re prepared for any situation is essential.

Essential Disaster Recovery Apps for 2025

FEMA App: Stay informed with real-time alerts from the Federal Emergency Management Agency. The app provides disaster resources, safety tips, and information on open shelters. It’s an indispensable tool for agents needing up-to-date information during emergencies.

Red Cross Emergency: This app offers comprehensive emergency preparedness information, including first aid instructions and real-time alerts for various disasters. It’s a valuable resource for both personal safety and client advisories.

Zello: Transform your phone into a walkie-talkie with Zello. This push-to-talk app is especially useful when

traditional communication networks are down, ensuring you stay connected with your team and clients.

Everbridge: Designed for critical event management, Everbridge allows agencies to send mass notifications to clients and staff, ensuring timely communication during crises.

Dropbox or Google Drive: Cloud storage solutions like Dropbox and Google Drive ensure that your essential documents are backed up and accessible from anywhere, facilitating remote work during disruptions.

LastPass: Securely store and manage your passwords with LastPass. In the event of a cyber incident, having access to your credentials is crucial for recovery and continued operations.

GasBuddy: In situations requiring evacuation or travel, GasBuddy helps locate nearby gas stations and compare fuel prices, ensuring efficient route planning.

Life360: Keep track of your family’s and team’s

locations with Life360. The app provides real-time location sharing, driving reports, and emergency SOS features.

Integrating Technology into Your Disaster Recovery Plan

Beyond individual apps, it’s essential to have a comprehensive disaster recovery strategy:

• Regular Backups: Ensure that all critical data is backed up regularly to cloud services.

• Communication Protocols: Establish clear communication channels and protocols for your team during emergencies.

• Client Outreach: Use mass notification tools to keep clients informed about your agency’s status and any necessary actions they should take.

• Training: Regularly train your staff on emergency procedures and the use of these essential apps.

For more insights, explore our Tech Assessment to evaluate your agency’s preparedness.

The new E&O Guardian insurance agency risk management web site is designed to arm Big “I” members with information and tools to mitigate agency errors and omissions. Big “I” members can tap into a variety of educational materials designed to safeguard your agency. Explore the site and dive into specialty agency risk management articles on a wide variety of topics, recorded webinars, sample checklists, sample letters, an archive of newsletters, and more.

Big I Kentucky has worked with Paul Buse of Real Insurance Solutions Consulting to provide you with data for the Kentucky property and casualty (P&C) insurance marketplace as a benefit of your membership. The following is a summary of that information.

Premiums Overall

In 2024, Kentucky property and casualty (P&C) Direct Premium Written reached $11.1 billion, ranking Kentucky 29 of 51 states for total premiums in the United States. That is 1.1% out of $1.04 trillion in premiums nationwide. On a per capita basis, Kentucky ranks 48 of 51 for all P&C premiums combined, 37 of 51 for Personal Lines, 48 of 51 for Commercial Lines, and 17 of 51 for Agricultural Lines.

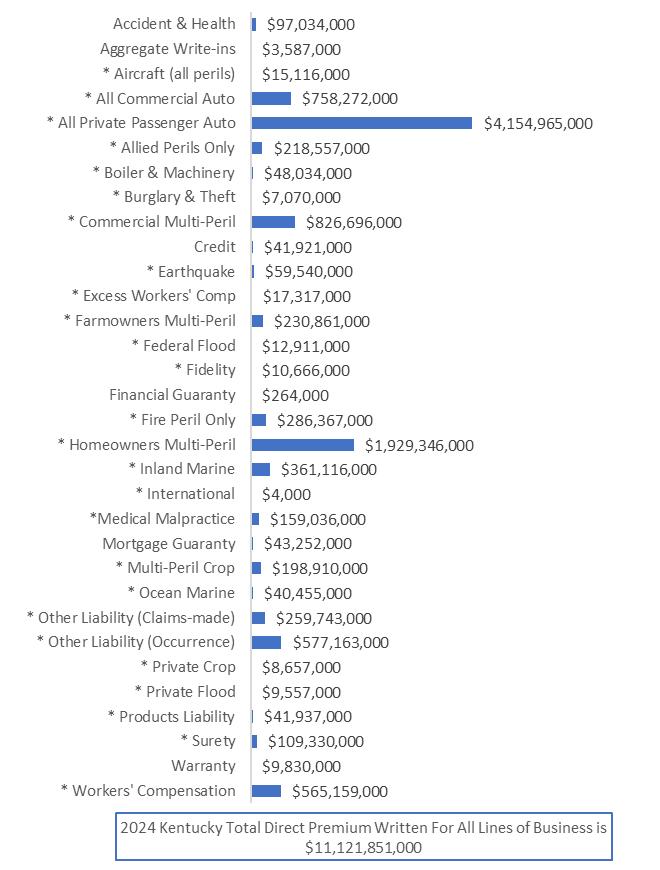

Lines of Business

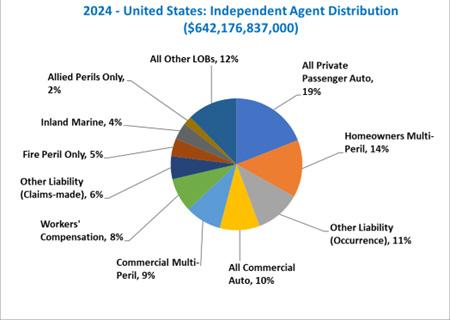

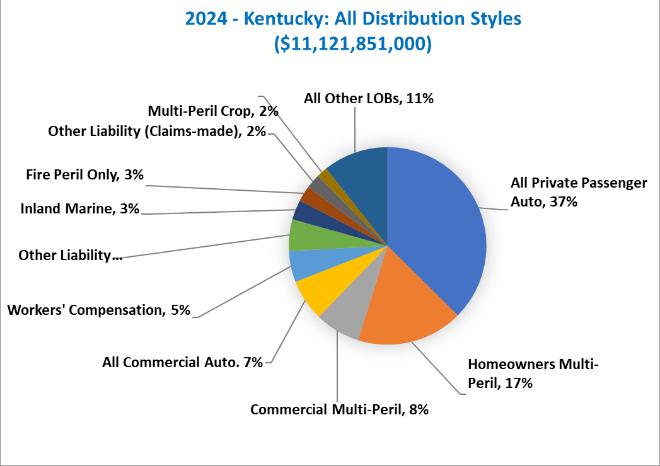

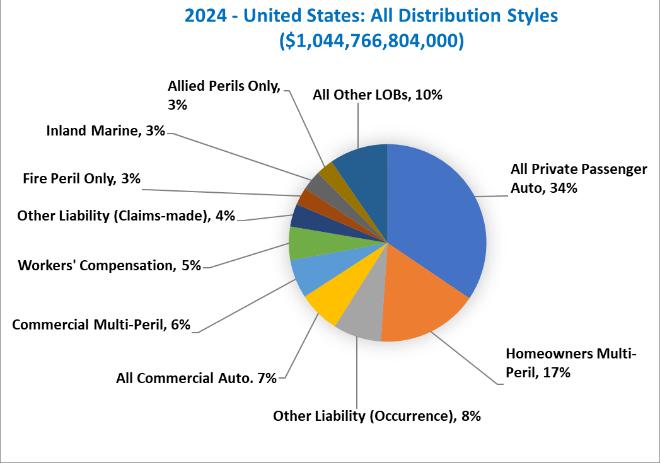

In Kentucky in 2024, the largest Line of Business for independent agents was All Private Passenger Auto, as determined by Direct Premium Written (DPW). The second largest Line of Business in Kentucky was HO Multi-Peril, and the third was Commercial Multi-Peril. For comparison, nationwide in 2024 those Top 3 Lines of Business were: All Private Passenger Auto, Homeowners Multi-Peril, and Other Liability (Occurrence).

Loss Ratios

In 2024 the Kentucky average Loss Ratio across all P&C Lines of Business was 58.3%, with the highest Loss Ratios occurring in Private Crop (166.7%), Medical Malpractice (84.8%), and Multi-Peril Crop (75.3%). Nationwide in 2024 the average Loss Ratio was 62.3%, with the highest state-wide average Loss Ratio being 82.2% (Nebraska), and the lowest being 47.5% (Hawaii). Across the United States, the Lines of Business with the highest Loss Ratios are Federal Flood (237.8%), Private Crop (93.0%), and Multi-Peril Crop (85.9%).

Premium Change Rates

From 2023 to 2024 premiums changed in Kentucky by +9.4% for all P&C Lines of Business combined, placing it 25 of 51 in the U.S. and D.C. The fastest-growing Lines of Business in Kentucky were Burglary & Theft (+23.7%), HO Multi-Peril (+14.5%), and Fire Peril Only (+14.2%). Nationally, P&C premium change averaged +9.6%, with the fastest growing percentage being + 15.2% (Washington), and the slowest being + 0.2% (North Dakota). The fastest-growing Lines of Business across the U.S. were Homeowners Multi-Peril (+13.4%), Farmowners Multi-Peril (+13.0%), and All Private Passenger Auto (+12.9%).

IA Penetration of the P&C Marketplace

During 2024, independent agents controlled 53.4% of the Kentucky P&C marketplace. This compares to the United States average of 61.5%, with the highest Penetration Rate being 78.8% (Massachusetts), and the lowest being 51.4% (Alaska). In Kentucky, the top Penetration Rates by Lines of Business were: International (100.0%), Private Crop (100.0%), and Ocean Marine (98.9%). In the United States, top penetration rates by Lines of Business were: International (100.0%), Multi-Peril Crop (96.9%), and Private Crop (96.4%).

Commissions

The average Commission Rate in Kentucky in 2024 was 11.9% for all P&C Lines of Business combined. By contrast, the average Commission Rate in the United States was 11.5%. The highest average Commission Rate was 13.6% (Massachusetts), and the lowest was 10.1% (Delaware).

Surplus Lines

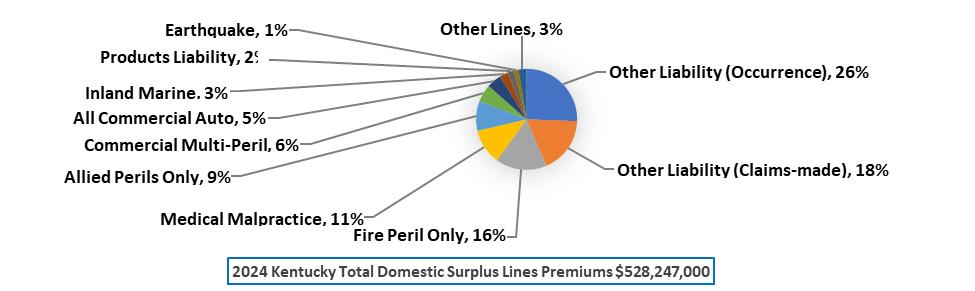

The percentage of P&C insurance premiums going to Surplus Lines is on the rise across all states. In Kentucky in 2024, the percentage of premiums going to Surplus Lines Domestic insurers was 4.7%. That percentage was 4.6% in 2023, and 3.2% in 2020. In the United States the corresponding figures were 9.7%, 9.4%, and 7.0%, respectively. In Kentucky, the top 3 Lines of Business with premiums going to Surplus Lines insurers were: Other Liability (Occurrence), Other Liability (Claims-made), and Fire Peril Only. In United States, the top 3 Lines of Business with premiums going to Surplus Lines insurers were: Other Liability (Occurrence), Other Liability (Claims-made), and Fire Peril Only.

Premium Taxes

All U.S. states levy a tax on property and casualty (P&C) insurance premiums, commonly referred to as a premium tax. In Kentucky in 2024, the average tax rate for Admitted premiums was 2.3%, while the Surplus Lines predominant tax

rate was 3.0%. Together these taxes generated $262 million for Kentucky in 2024, accounting for approximately 1.7% of Kentucky’s total tax and fee revenue, or about $57.0 per capita. Nationally, the average premium tax rates are 2.1% for Admitted premiums, and 3.9% for Surplus Lines premiums. In 2024 that equates to $25 billion in premium taxes nationwide, or about 2.0% of all state tax and fee revenue.

Largest Insurers

In 2024 State Farm Group (G) was the largest insurer group overall in Kentucky, writing 14.4% of all P&C premiums. Progressive Casualty Insurance Company emerged as the largest Pure Independent Agent-Broker Distribution Style individual insurer, State Farm Mutual Automobile Ins Co as the largest Exclusive-Captive Distribution Style individual insurer, and Kentucky Farm Bureau Mutual Insurance Co as the largest Direct Distribution Style individual insurer.

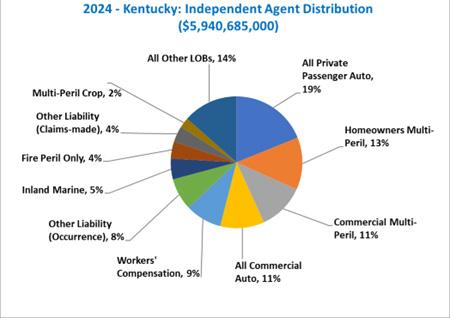

The above pie charts show the Top 10 Lines of Business written by independent agents in Kentucky and the United States. This is based on Direct Premium Written (DPW) for each Line of Business. Premiums for Lines of Business that fall below the Top 10 are combined in the “All Other Line of Business (LOBs)” pie chart section.

Kentucky Surplus Lines Perspective

Kentucky – All Lines of Business Additional Details

The chart below elaborates on the data in the previous figure, with expanded detail on Kentucky Premiums, Loss Ratios, Premium Change Rates, and Penetration Rates for the 32 P&C Lines of Business. The data is provided by Line of Business, for the reader’s overall reference.

Table 1 below, 2024 Kentucky: All Lines of Business Additional Details, elaborates on the data in the previous Figure 1, with expanded detail on Kentucky Premiums, Loss Ratios, Premium Change Rates, and Penetration Rates for the 32 P&C Lines of Business. The data is provided by Line of Business, for the reader’s overall reference. Again, the 26 Lines of Business primarily focused on by independent agents, are e mphasized with an asterisk (*). The 1-Year Loss Ratio and Premium Change rates are for 2024. The 5-Year Loss Ratio and Premium Changes rates are for the years 2020 to 2024.

Again, the 26 Lines of Business primarily focused on by independent agents, are emphasized with an asterisk (*). The 1-Year Loss Ratio and Premium Change rates are for 2024. The 5-Year Loss Ratio and Premium Changes rates are for the years 2020 to 2024.

2024 Kentucky: All Lines of Business Additional Details

Kentucky and United States P&C premiums are shown below in total, and on a per capita basis. Per capita premiums are provided to give a relative sense of the cost of premiums, but also allows for comparing premiums state to state. For deeper insight, per capita premiums are provided for the following four Line of Business groupings:

• Total (All Lines of Business Combined) includes premiums for all 32 P&C Lines of Business.

• Personal Lines includes All Private Passenger Auto, and Homeowners Multi-Peril.

• Commercial Lines includes All Commercial Auto, Commercial Multi-Peril, Other Liability (Claims-Made), Other Liability (Occurrence), Products Liability, and Workers’ Compensation.

• Ag-Farm Lines include Farmowners Multi-Peril, Multi-Peril Crop, and Private Crop.

In Table 2, also provided are the largest/highest state and the smallest/lowest state for total premiums and per capita premiums.

Note: The most recent population estimate from the United Census Bureau is the basis for the per capita comparative premium figures.

Full Report Available to Big I Kentucky Members

The full report may be accessed by Big I Kentucky members on our site at bigiky.org/Resources/ Pages/MarketplaceReport/default.aspx

SOCIAL MEDIA

CLASSIFIEDS

Owenton August 14

Acquisitions

Established Louisville agency interested in acquiring insurance agencies in Jefferson and surrounding counties. If you are interested in selling, merging, or need assistance with perpetuation, we would like to talk with you in confidence.

Call Kevin Lavin, CIC or Philip Anderton, CIC, CRM at Sterling Thompson Company at 502-585-3277

Looking for Producers

Independent with top best markets looking to expand presence in Jefferson, Oldham or Shelby counties. Wanting Personal lines Producer or book of business to move or purchase. All arrangements possible, in strict confidence.

Please send inquiries to:

Turner Insurance Agency, 2460 Shelbyville Road, Shelbyville, KY 40065 or call Kurt Turner, CPCU at 502-633-6060.

We would like to thank our advertisers for their support. This publication would not be possible without you! For classified ads or to advertise in the Kentucky IA, visit