ICPAC’s 64th AGM: A Milestone in Leadership and Global Standing

Kyriakos Iordanou GENERAL MANAGER OF ICPAC

Kyriakos Iordanou GENERAL MANAGER OF ICPAC

Usually, good things carry their inescapable drawbacks . . . This applies to Cyprus as well since antiquity, given its premium and much coveted geographical and geostrategic position.

Situated adjacent to the volatile Middle East region, we have been affected by all events happening in our neighbourhood. On the other side, Cyprus has for centuries been an attractive political, military, commercial, and business stronghold for bigger and stronger countries. For the last 4-5 decades, Cyprus’ activity as a place for international business surged, providing a safe harbour and a springboard, simultaneously, to international business players to extend their operations globally, capitalizing on the benefits offered by the country and its people.

The last 10 years, though, especially after the economic crisis, the Investment Programme termination, and the war in Ukraine, the story changed. Cyprus was forced to adapt to a new business environment and a stricter compliance regime, with a significant part of the traditional business and norms being lost.

Now, amid the turbulence in the Middle East region and the ongoing war in Ukraine, Cyprus strives to reposition itself in the business and on the political map, without forgetting that it remains a divided island because of an invasion and an illegal occupation. Hence, being pragmatic, we continue to operate in a context of relative uncertainty and instability. Despite all that, Cyprus’ economy demonstrates remarkable resilience and growth during the last few years, returning to investment ratings.

The question, however, remains: Is this sustainable? Does it depict the true picture for the average business and household? Are the numbers that prosper, or are the people prospering too? How optimistic is the new generation about the fulfillment of their aspirations and goals?

So, to put it in context, countries like Cyprus, that is small, limited in natural resources and industrial capacity, with open economies and susceptible to the globalized terms of trade and finance, usually must do more than others to keep up with the endeavored prosperity for its people.

I would dare suggest that the best defense in such circumstances for countries like ours is to strengthen the national economy, the business and commercial base, and internal infrastructures, the social cohesion and welfare of the citizens. In doing so, it is critical to maintain a disciplined stance towards enhancing innovation, fostering differentiation, and capitalizing on competitiveness! We must rethink the way we operate and bring in the changes before they find us!

At the same time, it is vital to forge international strategic and commercial collaborations and alliances. This includes

the attractiveness and trust that our country instills in third countries and foreign investors. It is therefore extremely important to align their interests with those of our homeland. So, we need to understand and appreciate the risks surrounding our country and our economy, and mitigate them. In this manner, Cyprus becomes increasingly relevant to third-party interests, hence enriching its diplomatic and business arsenal. The geostrategic and geopolitical location of the island can enhance its diplomatic and bargaining power, provided we do that reasonably. At this point, energy and hydrocarbons may come again into the agenda…

Diplomacy and good international relations are fundamental in today’s landscape. Without any doubt, the establishment of the Strategic Dialogue with the United States, the Republic’s diplomatic initiatives within and beyond the European Union, the toolbox offered by the EU membership, and the upcoming Presidency of the EU Council in the first half of 2026 pose as very optimistic opportunities for our country.

So, for sustainable growth, especially during challenging times, the state of the economy is the barometer, coupled with political stability and moral behavior. As a third eye, I would have liked to see the government placing much more emphasis on substance, on bringing about the much-needed reforms, on fostering innovation and productivity, on depleting the monsters of red tape and corruption, on promoting excellence, competence, and merit!

I would also like to see the political establishment being more coherent and congruent, seeing the bigger picture, despite any micro-difference. After all, the running of the country, i.e., governance, is a collective effort.

It would be equally important to see more public-private initiatives and cooperation, with the private sector and civic society, to complement the political agenda.

I would like to see a clear vision, showing where we want this country, its business orientation, and its people to be and do in the next 10 years, at the very least. We should strive to set top-quality standards and pursue long-term goals that would yield sustainable benefits, rather than chasing the so-called “low-hanging fruit”, just to score an “easy win”.

Again, this is not an isolated or one-man exercise; it is a collective activity based on knowledge, competence, acumen, resilience, foresight, and culture. And in this exercise, we all have a role to play, whether small or significant is irrelevant. Cyprus surely has the human capital to succeed; let’s utilize it. It is about time to learn from past mistakes and have a fresh start. Let’s be visionary, proactive, and methodical to uphold growth, relevance, competitiveness, and ultimately, sustainability and prosperity!

EDITOR OF “ACCOUNTANCY CYPRUS”

We wish to book the following advertisements in the “Accountancy Cyprus” Journal:

Thank you in advance. For more info: 22 870030

Book multiple ads in the same issue and get 10% off

E-mail:

Signature: Date:

ISSN 1450-2380

The Institute Council

Odysseas Christodoulou - P resident

Andreas Andreou - Vice P resident

Eleni P yrgou (Secretary)

Andreas Avraamides, Marios Demetriades, George Hadjineophytou, Stavros Ioannou, Constantinos Kallis, Savvas Kleitou, Eliza Livadiotou, Ioanna Nicolaidou, Nicolas Shiakallis, Spyros Spyrou, Nicos Stavrou, Afxentis Zemenides

Kyriakos Iordanou

11 Byron Avenue, 1096 Nicosia, Cyprus

P.O. Box 24935, 1355, Nicosia, Cyprus

Tel.: +357 22870030

Fax: +357 22766360

Ε-mail: info@icpac.org.cy www.icpac.org.cy

Design and Pagination

Maria Stylianou

The publication is prepared by RedwolfOgilvy 8 Ilioupoleos Street

Tel: +357 22252522

Fax: +357 22767970

E-mail: info@redwolfogilvy.cy www.redwolfogilvy.cy

Accountancy Cyprus is published quarterly by the Institute of Certified Public Accountants of Cyprus and is sent free to all members of the Institute as well as to many other persons, companies, and organizations.

A summary of the Institute’s most important recent initiatives, announcements, and activities.

• ICPAC Meets with the Commissioner for State Aid Control

• ICPAC General Manager Attends Anniversary of the Serbian Association of Accountants and Auditors

• ICPAC’s CSR Committee Hosts Tree-Planting Event in Nicosia

• 15th Nicosia Economic Congress

• ICPAC at Corporate Governance Today Conference 2025

• ΙCPAC Reinforces Its Enduring Commitment to Academic Excellence at the Cyprus University of Technology

“The Global Accountancy Profession Is a Pillar of Trust in the Economy”

IFAC President Jean Bouquot discusses the organisation’s mission, the ESG imperative, the attractiveness of the profession, and Cyprus’ position in the global accounting landscape.

• ICPAC leadership highlights transparency, sustainability, and strategic engagement at the 4th Mediterranean Finance Summit

• Dr. Christodoulos Patsalides outlines the road ahead at the 4th ICPAC Mediterranean Finance Summit

• Pavlos Kontides: Mastering Strategic Discipline and Informed Leadership

Unaffordable Housing for Our Youth

Investing in Social Cohesion and the Strategic Potential of the “Indian Touch”

On 28 March 2025, the Institute of Certified Public Accountants of Cyprus (ICPAC) had the distinct honour of meeting with Ms Stella Michaelidou, Commissioner for State Aid Control. The meeting, held in a spirit of mutual respect and constructive dialogue, focused on areas of common interest and on the evolving regulatory landscape surrounding state aid and its implications for the accounting and audit profession.

The visit formed part of ICPAC’s ongoing outreach to key public institutions, aiming to foster closer collaboration and create open channels of communication with stakeholders who play a critical role in Cyprus’s economic and regulatory framework.

During the meeting, Ms Michaelidou provided a comprehensive overview of the responsibilities, powers, and operational priorities of the Office of the Commissioner for State Aid Control. These include ensuring compliance with EU rules on state aid, monitoring support schemes, and evaluating public sector interventions to safeguard fair competition and transparency. The discussion shed light on the increasingly complex and technical nature of this regulatory area, which is becoming ever more relevant to accountants and auditors engaged in both advisory and assurance services.

The ICPAC delegation shared its perspectives on the importance of clarity, consistency, and collaboration in the interpretation and implementation of rules governing state aid. It was also noted that, as professional accountants often act as intermediaries between businesses and regulatory authorities, their understanding of such frameworks is essential for ensuring lawful and effective outcomes for their clients and the economy at large.

THE VISIT FORMED PART OF ICPAC’S ONGOING OUTREACH TO KEY PUBLIC INSTITUTIONS, AIMING TO FOSTER CLOSER COLLABORATION AND CREATE OPEN CHANNELS OF COMMUNICATION WITH STAKEHOLDERS WHO PLAY A CRITICAL ROLE IN CYPRUS’S ECONOMIC AND REGULATORY FRAMEWORK.

A significant portion of the meeting was devoted to exploring opportunities for deeper institutional coop eration. Both parties acknowledged the benefits of exchanging expertise and maintaining a regular dialogue, with a view to facilitating the work of accounting professionals and promoting a regulatory environment conducive to sustainable economic activity.

The ICPAC delegation was represented by Mr Spyros Spyrou, Member of the Board of Directors, Mr Kyriakos Iordanou, General Manager, and Ms Eleni Pyrgou, Legal Affairs Officer. Representing the Office of the Commissioner, alongside Ms Michailidou, were Mr Konstantinos Holevas and Ms Eleni Ioannidou.

ICPAC expresses its sincere appreciation to Ms Michaelidou and her team for the warm reception and the insightful exchange of views. The Institute looks forward to building upon this meeting with continued engagement, knowledge sharing, and policy dialogue — all aimed at supporting the public interest and strengthening Cyprus’s institutional integrity.

The General Manager of the Institute of Certified Public Accountants of Cyprus (ICPAC), Mr Kyriakos Iordanou, had the honour of representing the Institute at the official celebration marking the 70th anniversary of the Serbian Association of Accountants and Auditors (SAAA), held in Belgrade.

The commemorative event brought together representatives of national professional bodies, regional institutions, and international organisations, all united in their commitment to promoting high-quality financial reporting, professional integrity, and sound economic governance. The SAAA’s 70-year journey is a testament to the enduring value of professional accountancy in supporting economic development, transparency, and public trust.

During the celebrations, Mr Iordanou extended ICPAC’s warm congratulations to the leadership and members of the Serbian Association, recognising the significant contribution the SAAA has made to the accounting profession in Serbia and beyond. He emphasised that strong ties between national and regional professional accountancy organisations are essential in addressing today’s shared challenges — from regulatory complexity and technological disruption to the growing demand for sustainability and ESG-related reporting.

THE COMMEMORATIVE EVENT BROUGHT TOGETHER REPRESENTATIVES OF NATIONAL PROFESSIONAL BODIES, REGIONAL INSTITUTIONS, AND INTERNATIONAL ORGANISATIONS, ALL UNITED IN THEIR COMMITMENT TO PROMOTING HIGH-QUALITY FINANCIAL REPORTING, PROFESSIONAL INTEGRITY, AND SOUND ECONOMIC GOVERNANCE.

“The future of our profession lies in our ability to cooperate across borders, to exchange knowledge, and to support each other in maintaining the highest standards of professionalism and public service,” Mr Iordanou noted. He also highlighted the need for continuous dialogue on issues such as public sector reporting, audit quality, digital transformation, and the evolving role of accountants in a world shaped by sustainability imperatives and geopolitical uncertainties.

Participation in such milestone events is a key part of ICPAC’s broader strategy to maintain active engagement with the international professional community. Mr Iordanou expressed his appreciation for the opportunity to be part of this historic occasion and underlined ICPAC’s readiness to further strengthen bilateral and multilateral relationships with fellow organisations.

As ICPAC continues to expand its international footprint, its leadership remains committed to initiatives that promote collaboration, transparency, and sustainable economic progress — values that were at the very heart of the celebration in Belgrade.

Aheartwarming and meaningful event centred on tree planting and sustainability was organised by the Corporate Social Responsibility (CSR) Committee of the Institute of Certified Public Accountants of Cyprus (ICPAC) on Sunday, April 13, at Semelis Park, located on the border between the Palouriotissa and Aglantzia districts in Nicosia.

The event was held in collaboration with the Municipality of Nicosia, under the framework of the “Nicosia Together” programme, and brought together participants of all ages, with children playing a leading role throughout the day.

The Mayor of Nicosia, Mr Charalambos Prountzos, addressed the attendees and highlighted the importance of such initiatives in cultivating environmental awareness and responsibility within local communities.

Representing ICPAC, Communications Officer Ms Constantina Achilleos reaffirmed the Institute’s commitment to initiatives that embrace people, the environment, and sustainable development.

Throughout the event, a total of 50 trees, 44 shrubs, and aromatic plants were planted with the active participation of children, some as young as four years old, who enthusiastically got involved in every step of the process.

A key supporter of the initiative was the NGO Together Cyprus, known for its environmental awareness campaign Let’s Do It Cyprus. The organisation’s CSR Lead, Mr Panos Demetriou, introduced the children to the interactive educational game “Sustainable Neighbourhood”, inspiring them to imagine and design their ideal community based on the United Nations Sustainable Development Goals (SDGs), including good health, quality education, clean surroundings, equal

access, and environmental protection. Through painting and creative play, the children expressed their vision for a better world.

A particularly creative and multisensory contribution came from the VerboErgo therapeutic centre, whose team, led by registered occupational therapist Ms Myroulla Christoudia, facilitated engaging messy play activities. Children painted jars, planted purslane seeds, made spring wreaths, and created their miniature trees, developing motor, social, and creative skills through experiential learning.

A significant role was also played by Nevada Nurseries Ltd. Agronomist Ms Stavri Tofari and floral design educator Ms Chara Thomá guided the children in planting lentisk trees, rosemary, thyme, and oleanders. The children learned how to prepare the soil, dig, water, and care for plants, while also discovering the cultural and ecological value of native species such as the mastic tree (Pistacia lentiscus).

THE EVENT WAS HELD IN COLLABORATION WITH THE MUNICIPALITY OF NICOSIA, UNDER THE FRAMEWORK OF THE “NICOSIA TOGETHER” PROGRAMME, AND BROUGHT TOGETHER PARTICIPANTS OF ALL AGES, WITH CHILDREN PLAYING A LEADING ROLE THROUGHOUT THE DAY.

At the end of the day, the children took home their creations, and a small jar filled with soil and seeds –a symbol of growth, care, and responsibility toward the planet.

The event concluded in a festive atmosphere with the support of sponsors officestationery.com.cy, which provided the craft supplies, and KEO, which offered water and juices for all participants.

The 15th Nicosia Economic Congress convened once again as one of Cyprus’s most prestigious economic forums, bringing together senior executives, entrepreneurs, economists, academics, ministers, and key policymakers to discuss the state and prospects of the Cypriot economy.

Delivering the opening address, Mr. Kyriakos Iordanou, General Manager of the Institute of Certified Public Accountants of Cyprus (ICPAC), warned that “collateral effects will emerge if the commercial crisis proves to be prolonged.”

Mr. Iordanou stressed that the ongoing global trade war is reminiscent of earlier economic periods, noting a visible shift back towards national currencies and the reshoring of production capacity within national borders.

“The global political landscape is increasingly volatile,” he said, “with the United States and China questioning each other’s role and intentions in the world order.” He also did not rule out the possibility of long-standing alliances coming into confrontation, adding that “the geopolitical environment is changing rapidly, with more and more countries focusing on matters of defence and security.”

Given this international uncertainty, Mr. Iordanou underlined the urgent need for Cyprus to develop a resilient and stable economic model. He identified the strengthening of international relations, climate change adaptation, the ESG agenda, and tax reform as issues of strategic importance.

He also made a strong appeal for collective action and emphasized the importance of reinforcing Cyprus’s economic resilience. “The voices of the younger generation and tomorrow’s business leaders are critical to shaping a more sustainable and secure economic future,” he said.

MR. IORDANOU STRESSED THAT THE ONGOING GLOBAL TRADE WAR IS REMINISCENT OF EARLIER ECONOMIC PERIODS, NOTING A VISIBLE SHIFT BACK TOWARDS NATIONAL CURRENCIES AND THE RESHORING OF PRODUCTION CAPACITY WITHIN NATIONAL BORDERS.

The Nicosia Economic Congress, now in its fifteenth consecutive year, continues to provide a dynamic platform for discussing Cyprus’ economic trajectory, fostering informed debate, and generating actionable insights on the key challenges and opportunities facing the country.

The Institute of Certified Public Accountants of Cyprus (ICPAC) reaffirmed its commitment to promoting strong corporate governance and institutional integrity through its active participation in the Corporate Governance Today Conference 2025. The event, hosted by the European Institute of Management and Finance (EIMF) in collaboration with The Chartered Governance Institute UK & Ireland, brought together leading voices from the governance, compliance, and financial regulation sectors.

THE PANELLISTS SHARED INSIGHTS ON EMERGING REGULATORY CHALLENGES, RISK CULTURE, AND THE EVOLVING EXPECTATIONS OF BOARDS AND STAKEHOLDERS IN RELATION TO COMPLIANCE.

A key highlight of the conference was the panel discussion titled “Compliance as a Cornerstone”, moderated by ICPAC’s General Manager, Mr Kyriakos Iordanou. The discussion underscored how effective compliance frameworks can strengthen governance structures, enhance accountability mechanisms, and foster trust across the corporate ecosystem.

The panel featured distinguished experts, including:

• Ms Andrea Moundi Savvides, Chair of the Cyprus Compliance Association and Global Director of Risk and Compliance at Harneys

• Mr George Apostolides, Board Member and Chief Compliance Officer at Eurobank Cyprus Ltd

• Dr Marios Clerides, Board Member of the Fiscal Council and seasoned governance expert

The panellists shared insights on emerging regulatory challenges, risk culture, and the evolving expectations of boards and stakeholders in relation to compliance. They also examined how compliance is no longer a box-ticking exercise but a vital strategic function that ensures ethical business conduct and long-term resilience.

The conference was proudly sponsored by XM and supported by key institutions in the sector, including ACAMS Cyprus Chapter, TechIsland®, ICPAC, ACIFF MAP S.Platis, and the Cyprus Compliance Association. ICPAC’s participation reflects its ongoing advocacy for high standards in corporate responsibility and its belief that compliance is a cornerstone of sustainable and trustworthy governance.

The Institute of Certified Public Accountants of Cyprus (ICPAC) proudly participated once again in the Annual Awards Ceremony of the School of Business and Economics at the Cyprus University of Technology (CUT), held on Friday, 20 June 2025. The ceremony honoured high-achieving students from the School’s two academic departments — the Department of Finance, Accounting and Management Science, and the Department of Shipping — in recognition of their academic distinction, ethical conduct, and dedication to learning.

ICPAC’s sponsorship of selected student awards reflects the Institute’s broader strategy to promote academic excellence and support Cyprus’s long-term socio-economic development. Through initiatives such as these, ICPAC actively invests in the cultivation of a skilled, principled, and well-prepared professional workforce — a goal that remains central to its mission and vision.

The Institute believes that recognising and rewarding merit at university level is critical in motivating students, enhancing academic standards, and bridging the gap between academic theory and professional practice. Supporting the achievements of students at one of Cyprus’s leading public universities reinforces the Institute’s dedication to the advancement of the accounting and finance profession.

The long-standing collaboration between ICPAC and the Cyprus University of Technology stands as a model of how professional bodies and academic institutions can work together for mutual benefit and the public good. By supporting this event year after year, ICPAC helps cultivate an environment where education and industry align, creating tangible opportunities for student growth, mentorship, and career advancement.

This synergy is especially relevant in today’s rapidly changing business environment, where skills such as critical thinking, integrity, digital readiness and

sustainability awareness are more essential than ever. The Institute continues to advocate for an academic curriculum that reflects the evolving needs of the profession while preserving its ethical foundation.

The Awards Ceremony served not only as a platform to celebrate excellence but also as a reminder of the enduring value of education in shaping society. ICPAC congratulates all the students who were recognised and applauds their effort, determination, and academic discipline. Their success reflects both personal commitment and the quality of education delivered by the School of Business and Economics. The Institute also commends the faculty and administrative teams at CUT for their professionalism, dedication and partnership over the years. Together, we help build a future where knowledge, ethics and innovation form the pillars of economic growth.

As a forward-looking institution, ICPAC will continue to support initiatives that nurture talent, encourage excellence, and strengthen the links between the academic and professional worlds. The Institute remains steadfast in its role as a partner of educational institutions and a guardian of professional integrity, committed to shaping a resilient and competitive economy for the benefit of future generations.

Visits C y prus

The President of the International Federation of Accountants (IFAC), Mr. Jean Bouquot, paid an official two-day visit to Cyprus on 17–18 June 2025, following an invitation by the Institute of Certified Public Accountants of Cyprus (ICPAC). The visit marked a milestone in Cyprus’s efforts to strengthen its presence and influence within the global accounting and auditing landscape.

During his visit, Mr. Bouquot engaged in a series of high-level meetings with government officials, regulatory authorities, financial institutions, and academia, reaffirming IFAC’s strategic cooperation with Cyprus and acknowledging the country’s progress in promoting professional excellence, transparency, and financial integrity.

Meeting with the Governor of the Central

Mr. Bouquot met with Mr. Christodoulos Patsalides, Governor of the Central Bank of Cyprus, accompanied by the leadership of ICPAC, including the President of the Board, Mr. Nikos Chimarides, General Manager, Mr. Kyriakos Iordanou, and Head of Technical and Professional Matters, Ms. Eleni Assioti.

Discussions focused on Cyprus’ macroeconomic outlook, the regulatory evolution of the banking sector, and the growing need to embed environmental, social, and governance (ESG) standards into financial reporting. The role of technology and AI in enhancing

transparency, risk management, and combating economic crime was also explored.

Meeting with the Public Oversight Authority (PAOC)

The IFAC President held a separate meeting with the Chairman of the Cyprus Public Audit Oversight Board and Director General of the Ministry of Finance, Mr. Andreas Zachariades, and the Director General of CYPAOB and Chair of the CEAOB, Mr. Panos Prodromides.

The agenda included supervisory challenges in audit quality assurance, implementation of EU regulations, and global convergence of audit standards. The shared commitment to upholding professional ethics and public interest was reaffirmed.

Meeting with the Deputy Minister to the President

Mr. Bouquot was warmly received at the Presidential Palace by Deputy Minister to the President, Ms. Irene Piki. The meeting centered on Cyprus’s efforts to enhance its investment environment, public governance, and alignment with global transparency standards.

Ms. Piki highlighted the pivotal role of the accountancy profession in building economic credibility and emphasized the importance of international partnerships like that with IFAC.

Later that evening, Mr. Bouquot participated in a special meeting of the ICPAC Board, attended by managing partners of audit and advisory firms, committee chairpersons, and senior executives of the profession.

ICPAC President Mr. Nikos Chimarides presented the evolving challenges facing the profession in Cyprus, including the implementation of the EU’s Corporate Sustainability Reporting Directive (CSRD), attracting and retaining talent, and embracing digital transformation. Mr. Bouquot shared IFAC’s global strategy and discussed the future role of the profession as a trusted advisor in a rapidly changing world.

Meeting with the University of Cyprus Board Chairman

Mr. Bouquot met with the Chairman of the University of Cyprus Council, Mr. Tasos Anastasiou. The two discussed ways to strengthen collaboration between the academic and professional sectors, boost youth engagement in the profession, and promote innovation through joint initiatives.

The meeting reaffirmed the strategic importance of the Memorandum of Understanding between ICPAC and the University of Cyprus.

DURING HIS VISIT, MR. BOUQUOT ENGAGED IN A SERIES OF HIGH-LEVEL MEETINGS WITH GOVERNMENT OFFICIALS, REGULATORY AUTHORITIES, FINANCIAL INSTITUTIONS, AND ACADEMIA, REAFFIRMING IFAC’S STRATEGIC COOPERATION WITH CYPRUS AND ACKNOWLEDGING THE COUNTRY’S PROGRESS IN PROMOTING PROFESSIONAL EXCELLENCE, TRANSPARENCY, AND FINANCIAL INTEGRITY.

THE OFFICIAL VISIT OF THE IFAC PRESIDENT UNDERSCORED THE INTERNATIONAL RECOGNITION OF CYPRUS’ PROGRESS IN ALIGNING ITS PROFESSION WITH GLOBAL STANDARDS AND BEST PRACTICES. THE MEETINGS ALSO REAFFIRMED ICPAC’S ROLE AS AN ACTIVE AND CREDIBLE MEMBER OF THE GLOBAL ACCOUNTANCY COMMUNITY.

The IFAC President concluded his visit with a meeting at the House of Representatives with its President, Ms. Annita Demetriou, who is also President of the Democratic Rally Party.

Discussions focused on the institutional role of the profession in promoting accountability, ethical conduct, and financial discipline in the public and private sectors. Ms. Demetriou praised Cyprus’ professionals for their contribution to sustainable economic development and welcomed IFAC’s support in strengthening the country’s governance framework.

The official visit of the IFAC President underscored the international recognition of Cyprus’ progress in aligning its profession with global standards and best practices. The meetings also reaffirmed ICPAC’s role as an active and credible member of the global accountancy community.

Through strong regulatory cooperation, strategic public-private partnerships, and an unwavering commitment to professional excellence, Cyprus is wellpositioned to shape the future of the profession, both locally and globally.

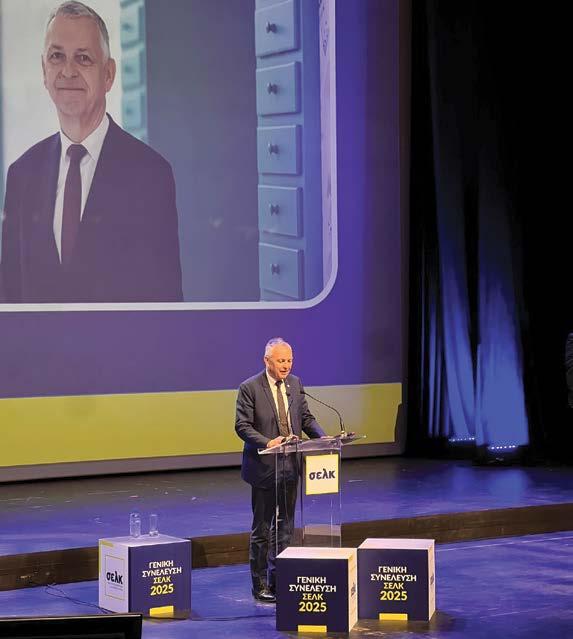

With the participation of highranking dignitaries from Cyprus and abroad, the 64th Annual General Assembly of the Institute of Certified Public Accountants of Cyprus (ICPAC) took place on Wednesday, 18 June 2025, at the Nicosia Municipal Theatre.

The event was honoured by the presence of the President of the House of Representatives, Ms. Annita Demetriou, and the President of the International Federation of Accountants (IFAC), Mr. Jean Bouquot.

The participation of Mr. Bouquot in a professional body’s general assembly in Cyprus marks a milestone in the growing international recognition of ICPAC’s work and its outward-looking engagement.

In his opening address, ICPAC’s General Manager, Mr. Kyriakos Iordanou, analysed the geoeconomic challenges of the present era, with particular emphasis on the effects of ongoing geopolitical tensions and conflicts in the broader region.

He emphasized the importance of de-escalation and a return to stability and social normalcy as essential conditions for prosperity and the protection of the public interest.

Mr. Iordanou also emphasized the need to enhance the resilience of the Cypriot economy, focusing on four key

strategic pillars: supporting small and medium-sized enterprises, leveraging artificial intelligence, integrating sustainable development, and investing in ongoing professional development.

Mr. Iordanou showcased Cyprus’s role as a stable regional hub for dialogue and cooperation between Europe, the Middle East, and Africa. He outlined the importance of multilateral collaboration and institutional interconnectivity, reaffirming ICPAC’s commitment to enhancing international outreach and actively contributing to key public policy matters.

The goal, he emphasised, is the continuous elevation of the accounting and auditing profession within the evolving global landscape.

From the podium of the General Assembly, the outgoing President of ICPAC’s Board of Directors, Mr. Nikos Chimarides, delivered a concise review of his tenure.

This period was marked by significant institutional reforms and strategic initiatives, including ICPAC’s active contribution to the national tax reform agenda, the embedding of ESG principles into the business environment, and the profession’s digital transformation.

Noteworthy highlights included the establishment of the CFO Society Cyprus – a modern platform for dialogue and professional networking – and the institutionalisation of the Mediterranean Finance Summit, which now operates as a regional forum for knowledge exchange and critical thinking.

Mr. Chimarides underscored the essential role of the accounting profession in promoting transparency and financial sustainability and stressed the need for the profession to maintain a leading presence in addressing contemporary challenges. He extended heartfelt thanks to the Board of Directors, committees, management, and staff for their unwavering support and cooperation.

In his address, IFAC President Mr. Jean Bouquot praised ICPAC’s progress in strengthening the professional and regulatory framework in Cyprus. He pointed to the consistent advancement of professional ethics, lifelong learning, and technological readiness, positioning ICPAC as a model of good practice on the global stage.

Mr. Bouquot noted that Cyprus represents a prime example of a small country with substantial international impact – a result of the high calibre of its human capital and the targeted strategic leadership of visionary professional bodies aligned with global compliance standards.

In a message delivered on behalf of the President of the Republic of Cyprus, Mr. Nikos Christodoulides, by the Deputy Minister to the President, Ms. Irene Piki, the multifaceted and long-standing contribution of ICPAC to the Cypriot economy and society was emphasised.

The President highlighted the decisive role of the accounting profession in advancing good governance, transparency, and tax compliance, recognising ICPAC as a credible institutional partner of the State.

He also reaffirmed the Government’s steadfast commitment to continuing its collaboration with ICPAC, in the broader context of modernising the state, enhancing competitiveness, and achieving sustainable development.

The President of the House of Representatives, Ms. Annita Demetriou, underscored the importance of collaboration between the legislative branch and professional bodies such as ICPAC. She noted that such partnerships form a cornerstone of justice, social cohesion, and the pursuit of sustainable economic growth.

She expressed the Parliament’s appreciation for ICPAC’s substantive and constructive role as a technical advisor and institutional partner, especially in times of geopolitical uncertainty. She emphasised the Institute’s contribution to safeguarding the Cypriot economy and advancing the values of transparency and accountability.

This year’s Annual General Meeting highlighted ICPAC’s strengthened role as an institutional partner of the State and a catalyst for positive change in the profession.

With international recognition, technocratic expertise, and a strategic focus on innovation, the Institute is shaping the next cycle of actions with responsibility and a steadfast orientation toward the public interest.

Following the Annual General Meeting, a networking party took place at The Garden, offering attendees the chance to connect, exchange ideas, and enjoy the night in a lively setting.

Odysseas Christodoulou has been elected as the new President of the Board of Directors of the Institute of Certified Public Accountants of Cyprus (ICPAC). The new Board was constituted ahead of the ceremonial part of the Institute’s 64th Annual General Meeting.

Mr. Christodoulou, who previously served as Vice President of ICPAC, succeeds Mr. Nicos Chimarides following the completion of his term. Andreas Andreou was elected as the new Vice President. Mr. Andreou has served on ICPAC’s Board since 2015.

• Odysseas Christodoulou - President

• Andreas Andreou - Vice President

· Andreas Avraamides - Member

· Marios Demetriades - Member

· George Hadjineophytou - Member

· Stavros Ioannou - Member

· Constantinos Kallis - Member

· Savvas Kleitou - Member

· Eliza Livadiotou - Member

· Ioanna Nicolaidou - Member

· Nicolas Shiakallis - Member

· Spyros Spyrou - Member

· Nicos Stavrou - Member

· Afxentis Zemenides - Member

Mr. Christodoulou brings more than 30 years of experience in accounting, finance, and professional education. He is currently the CEO of edBOS, the educational division of the eBOS technology platform, with a strong focus on innovation, upskilling, and workforce development.

A Fellow of the ACCA (FCCA), the Chartered Institute of Bankers (FCIB), and a Certified Management Accountant (CMA), Mr. Christodoulou holds an MBA in Accounting and Finance. He has served as Cyprus’ representative at the ACCA International Assembly and held senior roles, including co-founder and CEO of Globaltraining, COO and Board Member of EDEX, and Council Member of the University of Nicosia.

His early career includes positions at Coopers & Lybrand, Lombard NatWest Bank, and Cyprus Popular Bank. He currently serves on the Board of KEO Plc and has previously held non-executive board positions at Ancoria Bank and Laiki Financial Services.

Mr. Andreou is a Partner and Executive Committee member at Deloitte Cyprus, having joined the firm in 1997. He has extensive experience providing audit services to a broad range of public and private organizations, with specialisation in the insurance and financial services sectors.

He leads Deloitte Cyprus’ technical team on International Financial Reporting Standards (IFRS) and is a well-regarded speaker on technical accounting matters. A member of ICPAC’s Board since July 2015, he previously served on the Institute’s Accounting Standards Committee (2010–2014) and as its Vice Chair (2014–2015).

He holds a degree in Business Administration with a concentration in Accounting from the University of Cyprus and has been a member of the Institute of Chartered Accountants in England and Wales (ACA) since 2001. He is married and a father of three.

ICPAC held its 64th Annual General Assembly amidst a period of heightened warfare and military conflicts in our immediate and broader geographical region. Everyone hopes that these conflicts will soon come to an end, that human casualties will be minimized, and that the worst can be avoided on both a social and humanitarian level.

The events in the Middle East and Europe do not leave us indifferent or unaffected. Beyond the humanitarian aspect, they cause disruption and serious turbulence in the global geostrategic, political, economic, and business environment. Consequently, we continue to operate in a context of relative uncertainty and instability, remaining, however, vigilant for any new challenges that may arise.

For countries like ours, the best defence in such times is the strengthening of the national economy, the business base, and internal social infrastructures on one hand, and, on the other, the forging of international

strategic and commercial collaborations and alliances. This includes the attractiveness and trust that our country inspires in third countries and foreign investors. It is therefore extremely important to align their interests with those of our homeland.

Notably, the establishment of the Strategic Dialogue with the United States, the Republic’s diplomatic initiatives within and beyond the European Union, and the upcoming Presidency of the EU Council in the first half of 2026 are fundamental opportunities for our country.

As part of its internationalization and outward-looking strategy, this year, ICPAC had the great honor and pleasure of hosting Mr. Jean Bouquot, President of the International Federation of Accountants (IFAC), in Cyprus. This is the first time that a sitting President of our international federation attended our Annual General Assembly in person. This signifies IFAC’s interest in regional professional accountancy bodies like ICPAC, the importance our Institute may have in our geographical neighbourhood, and the good reputation ICPAC and the Cypriot profession enjoy at the international level.

Additionally, we were pleased to welcome to our AGM representatives from other foreign professional bodies, such as those from France and Lebanon, as well as diplomatic missions based in Nicosia, giving our assembly a distinctly international dimension.

From another perspective, one could safely argue that Cyprus has the potential to serve as a bridge for constructive cooperation between countries and peoples, as well as a springboard for business and commercial synergy among Asia, Africa, America, and Europe. As ICPAC, we are ready to contribute to these goals through our activities and networks, emphasizing that noble cooperation, a humanitarian approach, and our professional environment transcend any political or geostrategic considerations.

FOR COUNTRIES LIKE OURS, THE BEST DEFENCE IN SUCH TIMES IS THE STRENGTHENING OF THE NATIONAL ECONOMY, THE BUSINESS BASE, AND INTERNAL SOCIAL INFRASTRUCTURES ON ONE HAND, AND, ON THE OTHER, THE FORGING OF INTERNATIONAL STRATEGIC AND COMMERCIAL COLLABORATIONS AND ALLIANCES.

The Accounting Profession’s Role and Contribution ICPAC and the accountancy profession face their challenges. Our activities span three main pillars:

As a professional body that supports, serves, and educates its members.

As a competent supervisory authority, exercising institutional supervisory responsibilities assigned by the State.

As a productive stakeholder of the economy and society, supporting the State, the private sector, and the broader financial industry.

Our profession plays a multifaceted, multidimensional, and indispensable role in every form of business and corporate operation. Backed by knowledge, training, expertise, specialization, and capability, professional accountants are among the most vital levers in the productive machinery of the economy.

The work and the professional opinions we provide are essential and decisive both for the functioning of all companies and for their compliance with their legal obligations. The same applies to the smooth operation of capital markets, development projects, the financial sector, and corporate viability.

Moreover, the work of our sector contributes to the collection of taxes and other state revenues, the effective financial management of public finances and budgets, and the preparation of reliable financial information. It also plays a crucial role in the sound operation of companies and the management of insolvency cases, to the benefit of creditors and state funds.

Simultaneously, the professional accountant is instrumental in both attracting and continuously servicing foreign investments and international businesses through the provision of professional and corporate services.

ICPAC members serve as financial managers across the market and the public sector, ensuring their sustainable operation and growth. Accounting firms also serve as gatekeepers and protectors in matters of compliance.

In general, the professional accountant is the essential hub and conduit between businesses and employers, the State and its services, banks, and the real economy in all its forms. We operate across the full spectrum of social and business activity, granting us broad perspective, objectivity, and specialized insight.

ICPAC MEMBERS SERVE AS FINANCIAL MANAGERS ACROSS THE MARKET AND THE PUBLIC SECTOR, ENSURING THEIR SUSTAINABLE OPERATION AND GROWTH. ACCOUNTING FIRMS ALSO SERVE AS GATEKEEPERS AND PROTECTORS IN MATTERS OF COMPLIANCE.

A cornerstone of our identity is continuous education and training, interpreted as life-long learning, both for our current and prospective members. This is achieved through various initiatives and broad connections with academia, educational organizations, and international bodies, both within the accountancy field and beyond.

At the same time, ICPAC undertakes targeted actions to inform and educate students and citizens on financial literacy, ethics, and tax awareness.

In conclusion, the accountancy sector and our profession are among the most internationalized domains in Cyprus. Since 1981, we apply the International Accounting Standards and IFAC’s Code of Ethics. We maintain an active presence in European, regional, and global federations to which we belong, deriving knowledge and best practices through international cooperation. A solid proof of that is the fact that all the major international accounting networks have a presence in Cyprus for decades.

Over these 64 years in the public and economic arena, ICPAC continues to operate on robust foundations, inspiring trust, credibility, and value.

As a pillar of the economy, ICPAC and our profession are always available to assist the State with constructive and substantial contribution to a wide range of initiatives and priorities, including:

• The restoration and strengthening of the country’s credibility and reputation.

• The promotion of necessary structural reform initiatives.

• The implementation of the national long term growth strategy “Vision 2035”.

• The Tax reform.

• The expansion of the country’s economic capacity through support for local SMEs and start-ups.

• The attraction of foreign businesses for genuine physical presence in Cyprus.

• The enhancement of the overall compliance landscape of the country.

• The repatriation of talented Cypriots who work and thrive abroad.

Our future has a name: Technology, Sustainable Development, and Competitiveness. ICPAC and the accounting profession align with digital transformation, preparing for the use of artificial intelligence and its potential implications for the work environment as we know it today. Sustainable development is not only about the EU Green Deal, but also about encompassing the 17 UN Sustainable Development Goals.

The competitiveness of our country will determine our economic size, commercial relevance, and productive potential. We are pleased to see the EU shifting in this direction, and we can build upon the Draghi Report.

ICPAC continues to move forward with the strength given by its members, extending a hand of friendship and cooperation to all institutions, the State, the Parliament, the private sector, and academia. It remains committed to best serving its members, the business community, the economy, society, and the public interest.

Following the remarks made by the previous speakers, I would like to highlight a point of utmost importance: the power of collaboration. In an era marked by uncertainty and insecurity, the most critical task before us is to work together proactively to confront the challenges we face. That is the essence of our collective responsibility.

We have come to realise not just today, but in recent years as well, that so-called external factors do not simply pass us by. They are present, and they affect us all. The real challenge for each country is to find effective ways, through deliberate actions, to filter these influences, to stay ahead of developments, to compete, and ultimately to move forward. This is how we shield our economy and, just as importantly, a system that is often demanding and complex, as you, the professionals in this field, know far better than I do.

Earlier today, in conversation with the President of the International Federation of Accountants, we touched on a challenge that we must meet successfully: the legislative framework. Over the years, Cyprus has made significant progress in this regard. Our goal must always be to facilitate the ability of professionals to meet the evolving demands of the industry.

At times, this is far from easy. We are living in the digital age, and this reality brings with it an entirely new set of demands. It is therefore essential that we provide professionals with the right tools and resources to help them adapt. These requirements are often not only numerous but also more complex and demanding than those faced in other countries, whether within Europe or beyond.

Supporting the Profession for a Resilient Economy

Let me stress once again how important it is that we invest in supporting the accounting profession through sound legislation, through digital transformation, and above all, through strategic partnerships. In doing so, we not only empower professionals to succeed in their roles but also contribute to building a more resilient and future-ready economy.

It is with great pleasure that I join you today to address the 64th Annual General Assembly of the Institute of Certified Public Accountants of Cyprus an event that coincides with the presence of distinguished professionals from both the national and international arenas. I sincerely thank you for the invitation to be here with you.

WE ARE LIVING IN THE DIGITAL AGE, AND THIS REALITY BRINGS WITH IT AN ENTIRELY NEW SET OF DEMANDS. IT IS THEREFORE ESSENTIAL THAT WE PROVIDE PROFESSIONALS WITH THE RIGHT TOOLS AND RESOURCES TO HELP THEM ADAPT.

Since its establishment in 1961, ICPAC has made a significant contribution to the development of both the Cypriot economy and society. As one of the strongest professional associations in Cyprus, ICPAC has been an exemplary advisor and partner to the State, and an important stakeholder for the House of

Representatives, actively participating in consultations concerning the operational and legislative framework of the Republic, particularly in matters relating to the economy.

With the enactment by the House of Representatives of Law 76(I)/2001, aligning national legislation with EU law, ICPAC was officially designated in 2002 as the competent authority for the regulation and oversight

LET ME STRESS ONCE AGAIN HOW IMPORTANT IT IS THAT WE INVEST IN SUPPORTING THE ACCOUNTING PROFESSION THROUGH SOUND LEGISLATION, THROUGH DIGITAL TRANSFORMATION, AND ABOVE ALL, THROUGH STRATEGIC PARTNERSHIPS.

of the accounting profession in Cyprus. Undeniably, ICPAC stands as a model professional body one that adheres to international standards while ensuring the necessary level of regulation and supervision, promoting the highest professional values, and serving the public interest.

In recent years, both ICPAC and the State have been called upon to navigate the complex consequences of the sanctions and restrictive measures imposed by the European Union on Russia following its invasion of Ukraine. These include inflationary pressures, rising interest rates, supply chain disruptions, and escalating energy costs.

Despite these challenging circumstances, ICPAC has continued to operate with integrity within Cyprus’s economic and social fabric, reinforcing its credibility and, by extension, strengthening the institutions it works with. It would be unthinkable for us—as the Legislative or Executive branch—to disregard the challenges faced, or those anticipated, by the professionals in this sector.

ICPAC’s initiatives—including the advancement of a Cyprus Financial Reporting Standard for small enterprises, partnerships with professional and academic institutions both domestically and internationally, its engagement with the Registrar of Companies on relevant matters, and its monitoring of EU directives and regulations—underscore its decisive contribution to safeguarding business viability and strengthening entrepreneurship.

As a key pillar of our financial ecosystem, ICPAC plays a leading role in shaping economic developments in Cyprus. Through its consistent and meaningful presence, its well-targeted interventions—especially on high-priority economic issues—and its authoritative voice, the Institute continues to help chart a course for sustainable and responsible financial progress.

In doing so, the Institute contributes to enhancing the competitiveness of the Cypriot economy and promoting our country as a leading international business centre. Moreover, just as the outgoing President and Vice President of the Board of Directors have

demonstrated in their roles, I am fully confident that the new President and Vice President will continue the Institute’s mission with the same consistency, commitment, and sense of responsibility. Their leadership will continue to offer scientific support and technocratic insight whenever and wherever it is deemed necessary.

Economic stability is a fundamental prerequisite for sustainable growth, the preservation of social cohesion, and the strengthening of trust among both citizens and investors. A stable economy enables a predictable environment for business, ensures the effective functioning of institutions, and builds resilience against external shocks.

At present, in addition to the ongoing conflict in Ukraine and other global crises, our already troubled region is once again facing turmoil—this time in the Middle East.

We cannot afford to become complacent. On the contrary, we must remain vigilant, safeguard macroeconomic stability, and take timely action to shield our economy from external threats. In this collective effort, the Institute of Certified Public Accountants of Cyprus (ICPAC) is undoubtedly a key ally and partner.

The real challenge is to make both Cyprus and, more broadly, the European Union genuinely competitive. We must ensure that professionals are supported in implementing the policies we adopt, while also contributing to the broader objective of economic stability.

The credibility of our country is critical for attracting and managing investment, and not only that. Deliberate behaviours or narrow interests that undermine Cyprus and the hard-earned progress we’ve made over the years can no longer be tolerated. We all have a role to play in protecting and advancing the reputation and integrity of our nation. And that includes you.

Earlier, there was mention of the topic of tax reform and the importance of government intervention in this domain. Indeed, such reform is necessary, but it must be carried out in a manner that considers the views of professional stakeholders such as ICPAC.

As the House of Representatives, we await the relevant bills as soon as possible. Ideally, these will reflect a balanced synthesis of views that allows us to move forward in a meaningful way. I can assure you that we are ready and willing to support this process.

We must not forget that some institutions in this country, such as ICPAC, have “shouldered the burden” to get us where we are today. Their role has been pivotal.

We are indeed pleased that Cyprus has regained investment grade status. However, we must remain clear-eyed: economic stability is not a given. In today’s world, the only certainty is uncertainty.

We are called upon to move forward with clear goals, with determination, and with foresight to shield our economy and protect the public interest.

We, as the House of Representatives, will continue to stand by your side. We need a long-term strategic plan, and we are ready to work decisively alongside you to implement it, because at the end of the day, it is not just you who benefits. We all do. Cyprus benefits. Every citizen, individually and collectively, stands to gain.

It is with great pleasure that I address today the 64th Annual General Assembly of the Institute of Certified Public Accountants of Cyprus—an essential partner of the State in one of the most critical areas of public life: the economy.

Your Institute is a longstanding institution that has consistently contributed to our country. You have stood by Cyprus at every crucial turning point of its economy and have been key partners in every national effort towards progress and stability. The presence today of Mr. Jean Bouquot, President of the International Federation of Accountants, is a tangible recognition of ICPAC’s high professional standards and the international respect commanded by the Cypriot accounting and auditing profession.

As a government, we deeply value and acknowledge the role of ICPAC as a key institutional counterpart, one that actively participates in public dialogue with responsibility and well-documented contributions. Your input, especially in reforms, has always been meaningful and constructive.

We are currently experiencing an exceptionally demanding period, full of uncertainty. Armed conflicts in our wider neighbourhood, tensions with both regional and global dimensions, and a constantly shifting international reality, all contribute to a climate of increased pressure for states, markets, businesses, and institutions alike.

Within this context, the Eastern Mediterranean is regaining strategic importance in terms of security, regional cooperation, and the promotion of stability. Cyprus today faces a dual challenge: on the one hand, to remain a stable and credible partner in the region; and on the other, to ensure that, domestically, the necessary conditions for economic resilience, social cohesion, and institutional continuity are maintained.

Market disruptions, inflationary pressures, challenges in global supply chains, and high energy costs serve as daily reminders that prosperity cannot be taken for granted. We must pursue policies that strengthen the credibility of the country, safeguard macroeconomic stability, and foster trust among citizens, markets, and our strategic partners.

The government, fully aware of the challenges ahead, is working methodically and with clear targets to

AS A GOVERNMENT, WE DEEPLY VALUE AND ACKNOWLEDGE THE ROLE OF ICPAC AS A KEY INSTITUTIONAL COUNTERPART, ONE THAT ACTIVELY PARTICIPATES IN PUBLIC DIALOGUE WITH RESPONSIBILITY AND WELLDOCUMENTED CONTRIBUTIONS. YOUR INPUT, ESPECIALLY IN REFORMS, HAS ALWAYS BEEN MEANINGFUL AND CONSTRUCTIVE.

maintain stability and further enhance the resilience of our economy. Cyprus must and can remain an island of reliability amidst a landscape of growing international complexity.

Despite the volatile global environment, the Cypriot economy continues to post notable results: a growth rate of 3.4% in 2024, a return to investment-grade rating “A” by international credit rating agencies, historically low unemployment rates, and a continuing decline in public debt.

We understand external factors can easily disrupt economic balance. That is why we are working consistently to shield our economic institutions, fiscally, and structurally. At the heart of our efforts lie major reforms.

The tax reform promoted by the Government is the first comprehensive overhaul of the system in over two decades. Our ambition is to establish a fair, simple, efficient, and competitive tax system — one that meets the demands of a new era and serves as a lever for economic development and social policy.

In this endeavour, the role of the Institute of Certified Public Accountants of Cyprus (ICPAC) has been pivotal. ICPAC has submitted well-documented proposals, actively participated in the consultation process, and maintained a responsible and constructive stance, contributing decisively to the refinement of the reform proposals. I would like to sincerely thank you for your institutional contribution.

We are now in the final stage of preparing the relevant bills, intending to submit them to Parliament in the

coming period. The goal is for the new framework to come into effect on 1 January 2026.

Tax reform is part of a broader set of institutional reforms aimed not only at strengthening economic resilience but also at enhancing the credibility, transparency, and accountability of the state.

Within this context, the Government is moving forward with interventions that touch upon the core of supervision and compliance. The establishment of a Unified Supervisory Authority for administrative service providers, with the aim of consolidating and strengthening the regulatory framework, represents a key step towards addressing distortions observed in the past.

At the same time, the creation of a National Sanctions Unit under the Ministry of Finance — for which relevant bills are already under discussion in Parliament — responds to the need for a specialised mechanism to ensure Cyprus’ alignment with international and EU sanctions regimes.

These initiatives are fundamental shifts aimed at reinforcing Cyprus as a state governed by the rule of law, strengthening its institutional framework, and upgrading the country’s image as a reliable and secure business destination.

In tandem with these institutional reforms, we have launched the first organised international campaign to reposition Cyprus globally. This campaign is not limited to communication or promotion but reflects the Government’s reform-driven will, the tangible changes taking place in our country, and our strategic goal to establish Cyprus as a modern, reliable, and competitive business hub.

This is an effort grounded in real data — in reforms being implemented, institutions being reinforced, and frameworks being modernised.

In this effort, the contribution of your profession is crucial. Accountants and auditors in Cyprus, as carriers of expertise, transparency, and professional integrity, form the backbone of the international operations of our economy and serve as valuable ambassadors of the country’s credibility.

The first key initiative of this campaign was my visit last April to the United States, with stops in New York, Houston, and Silicon Valley.

During this mission, Cyprus’ potential role as a regional gateway and technology hub was showcased. At the same time, we promoted collaborations with universities, investment funds, and leading private sector organisations.

This mission forms part of the broader framework for upgrading Cyprus–United States relations, which, since the establishment of the Strategic Dialogue in October 2024, has evolved into a coherent cooperation framework in areas such as security, energy, technology, civil protection, and economic collaboration.

This is a strategic outward-looking policy choice of our government, one that enhances the international standing of the Republic of Cyprus, expands the potential for cooperation with strategic partners, and reaffirms Cyprus as a reliable interlocutor and stable partner in an increasingly uncertain global environment.

In the same direction, the recent official visit of the Prime Minister of India to Cyprus marked a historic milestone in the relations between our two countries.

As part of the visit, and in the presence of Prime Minister Modi, a dialogue was held with distinguished entrepreneurs from Cyprus and India. This exchange highlighted significant prospects for strengthening investment flows and, more specifically, for establishing the presence of two additional Indian companies in Cyprus, leveraging our country as a bridge to the European market.

Before concluding, I would like to address another growing global challenge that directly affects our businesses: the attraction and retention of talent. Cyprus no longer competes solely based on its favourable investment climate. Increasingly, competitiveness depends on the quality and availability of its human capital. Our ability to attract, repatriate, and utilise highly skilled professionals is a critical factor for the country’s long-term competitiveness.

In this context, the Government is implementing the “Minds in Cyprus” initiative — a targeted strategic campaign aimed primarily at Cypriots abroad with high levels of expertise. The objective is to encourage their repatriation and integration into the productive fabric of our economy.

This effort is part of a broader set of policies to promote knowledge, specialisation, and added value — elements that are essential for the sustainability of our economy.

I am confident that you are all too familiar with the challenges of attracting high-quality talent. That is why we believe this initiative will yield a positive impact, including within the accounting and auditing profession.

The Government is moving forward with consistency and determination, guided by a coherent plan that addresses present-day challenges while investing in the opportunities of tomorrow. We do not underestimate the difficulties, nor do we overlook the pressures faced by businesses, professionals, and households. On the contrary, through institutional reinforcement, economic stability, and an outward-looking strategy, we are laying the foundations for a more resilient, modern, and competitive state.

In this effort, our collaboration with institutions such as the Institute of Certified Public Accountants of Cyprus (ICPAC) acquires particular significance. We are inspired by the seriousness with which you engage with developments, the sense of responsibility you bring to public dialogue, and your steadfast commitment to the progress of our country.

I would therefore like to once again extend my sincere gratitude for your longstanding contribution and steadfast presence as partners in Cyprus’ journey towards a fairer, more dynamic, and more optimistic future.

Delivered at the 64th Annual General Assembly of the Institute of Certified Public Accountants of Cyprus (ICPAC)

Iam Jean Bouquot, President of IFAC, the International Federation of Accountants.

Thank you for welcoming me to Nicosia. It’s my first time in your country, and I have been truly grateful for the warm welcome I’ve received from everyone I’ve met, especially my hosts at ICPAC.

Let me briefly introduce IFAC to those who are not familiar with it.

We are the global organization of the accountancy profession. We represent millions of professional accountants through our 187 member organizations across 142 jurisdictions.

The value we bring to our members has three parts:

• Connection and Unity

• Integrity and Global Recognition

• A Collective Voice and Commitment to the Public Interest

Everything we do at IFAC is possible only with the collective efforts of our member organizations. ICPAC became a founding member of IFAC in 1977, and we have been proud to work with you ever since.

We have also benefited greatly from the volunteer service of talented ICPAC members over the years, including Eleni ASHIOTI, a current member of our Small- and Medium-Sized Practices Advisory Group.

I thank you all for the essential work you do on behalf of our profession and the public interest.

I want to say a few words today about three areas that are high on our agenda at IFAC, and which have been discussed nearly everywhere I have travelled as IFAC President: sustainability, digitalization, and public financial management.

Starting with sustainability.

In recent years, we at IFAC have been talking to our colleagues across the global accountancy profession— and to regulators and other stakeholders outside of the profession—about the opportunity and the public interest responsibility that professional accountants have for enabling the sustainability transformation that is happening in companies, in our economies, and society.

IFAC has unique contributions to make to these efforts in our role as both the profession’s global voice and as its global convener. I believe this is a critical role. The accountancy profession, as a trusted and influential public interest profession, should have a clear voice in how society can best undergo the sustainability transformation. And within the profession, we need to engage with each other through active, ongoing dialogue and support each other’s efforts by exchanging best practices and resources.

Financial markets need trustworthy, high-quality sustainability information so that investors and lenders can make efficient decisions that align with sustainability targets. A wider range of stakeholders in society also need this information so that they can fully understand the sustainability impacts of a business.

We are the profession in the best position to lead on sustainability reporting and assurance:

• We have the technical skills to integrate financial and non-financial information.

• Wherever we are in the value chain, we have the skills to transform high-quality standards into high-quality information.

• Our reputation will bring trust to this information, in the same way that we bring confidence to traditional financial statements.

SPEECH BY JEAN BOUQUOT, PRESIDENT OF

The sustainability transformation does call for individual professionals to upskill and reskill and collaborate with experts as needed to complement our work. PAOs are the best sources of the education and training their members need, so PAOS need to move swiftly and boldly with their members into the sustainable future. This will take a lot of hard work, and there will be bumps in the road on every PAO’s journey, but it’s imperative to keep going.

I want to recognize ICPAC for the great things you are doing for your members, including your webinars and CPD training on the ESRS. These are useful for professionals at any stage of their progress with sustainability, from their first steps. And with events like the 2024 ICPAC-ACCA Sustainability Conference, you are convening leaders in the profession to bring international best practices to Cyprus. I strongly encourage ICPAC members to take advantage of these resources and opportunities.

As a profession, we are challenging those of us who work inside companies, or who provide advisory services to companies, to view new sustainability disclosures not as a compliance exercise, but instead, as

empowering change in the way that companies are governed and the way they make decisions.

We are challenging ourselves to do everything we can to help build a harmonized, global system for reporting sustainability-related information. Crucially, for these disclosures to be useful to anyone, no actor can be outside the reporting system.

My focus, as President of IFAC, is on sustainability as it relates to all professional accountancy organizations within Europe, but also beyond Europe. We believe the IFRS standards, starting with S1 and S2, are the right foundation for this system. We welcome all well-intentioned initiatives for sustainability reporting standards, while strongly encouraging alignment. Ultimately, we are all on the same sustainability journey, so we should embark on it together.

We also believe widespread adoption and implementation of the ISSA 5000 standard, of the International Auditing and Assurance Standards Board (IAASB), will be crucial for ensuring that sustainability assurance truly builds trust and confidence in sustainability information.

ISSA 5000 is a profession-agnostic standard that allows for a broad range of assurance providers while maintaining a high level of quality. But I want to emphasize that we should not allow a two-tiered system to emerge—one where regulated, professional accountants are held to higher standards, while others operate without consistent oversight. It is all about investor and consumer protection. If the market for sustainability assurance doesn’t earn trust, then it doesn’t serve its intended purpose.

As with sustainability disclosure, all countries need to converge on a unified approach to sustainability assurance early on, before regulatory fragmentation can take hold and create unnecessary costs and complexity. Resolving a fragmented system only gets more difficult as time goes on.

The accountancy profession in Cyprus should speak strongly in favour of the adoption and implementation of ISSA 5000 as the path forward on sustainability assurance.

For our part, as individual professionals, we need to be ready to meet market expectations in the assurance space—and to compete with non-professionals.

I also want to offer you a view from the global level and a few thoughts on how digital technologies—especially artificial intelligence—are changing our profession, and how we should adapt.

AI is revolutionizing the way accountants and auditors work—in ways that enable us to process and analyse vast amounts of data with greater speed, accuracy, and impact.

For example, auditors can leverage AI to uncover hidden patterns, correlations, and insights, and these outputs can support predictive analytics, risk evaluation, and fraud detection. Generative AI is also proving to be a valuable tool for drafting audit reports and distilling complex information.

But perhaps the biggest changes are happening outside of formal systems and processes—in emails and spreadsheets, in team meetings, in presentations, and in countless one-off tasks that AI is transforming.

We have an incredible opportunity. We can use AI to shift from scorekeeping to strategy; to create more time to do higher-value work; and to participate in the transformation of our profession, rather than resist it.

WE ARE CHALLENGING OURSELVES TO DO EVERYTHING WE CAN TO HELP BUILD A HARMONIZED, GLOBAL SYSTEM FOR REPORTING SUSTAINABILITY-RELATED INFORMATION. CRUCIALLY, FOR THESE DISCLOSURES TO BE USEFUL TO ANYONE, NO ACTOR CAN BE OUTSIDE THE REPORTING SYSTEM.

The profession’s real challenge is not whether we can use AI—it is whether we will redefine our work before others redefine it for us.

I must add that we should always consider our professional responsibilities to meet the new and still emerging risks of AI, including cybersecurity, threats to privacy, lack of transparency, and bias within AI models.

I fully recognize that some in our profession feel anxious about how AI might impact our relevance. I want to emphasize that overall, AI is an opportunity to add more value and increase our relevance. But we should consider carefully whether we are prepared to seize this opportunity. The core skills of a professional accountant are strong, and we do not need to reinvent ourselves, but we must build on those skills.

Individually, we will need to increase our digital literacy and get practical experience with AI. As with sustainability, PAOs need to support their members to upskill and reskill for AI and a range of other digital competencies—and I encourage everyone to stay engaged with what ICPAC is doing, such as the training held in April on AI risks and compliance under the new EU AI Act.

PAOs also need to engage with educational institutions to make sure the curriculum for accounting students is keeping pace with technological change. IFAC’s International Panel on Accountancy Education oversees the International Education Standards—the global baseline for accountancy education—and ensures they remain relevant in a rapidly evolving world. Right now, the Panel is exploring the AI competencies that future accountants will need and how AI is reshaping the learning process.

On education, ICPAC’s continuing engagement with stakeholders on behalf of its members is vital to a successful digital transformation of the profession in Cyprus.

SPEECH BY JEAN BOUQUOT, PRESIDENT

The third and final theme I will turn to is public financial management, or PFM.

Public officials around the world are reckoning with an uncertain environment. They have very difficult decisions to make about how to use their limited resources to preserve and advance the welfare of their citizens. There is little margin for error. They need robust plans that account for the full scope of public needs and respond to them effectively, comprehensively, and sustainably. And all of this leads to PFM.

The issue of cash versus accrual-based accounting is an exceptionally important issue within PFM. It has a great effect on the public sector’s ability to plan, develop, and deliver services, and to manage its balance sheets. It is a top priority for IFAC and the IPSASB, the International Public Sector Accounting Standards Board.

This is a journey Cyprus is already on—but I want to revisit why you must keep going.

Accrual accounting is known to increase transparency, accountability, and credibility in public finances. This means better information reaches decision makers in the public sector. Better decisions lead to better outcomes in the management of public resources and the delivery of public services. With greater transparency and better outcomes of these decisions, public trust in government will rise.

IFAC offers a free-to-use tool on our website called Pathways to Accrual. It features resources to help governments and other public sector entities forge their paths towards adopting and implementing accrualbased reporting frameworks.

On PFM, I want to add that the most important variable in the public sector is people. So, I encourage our profession to convey a few key points to their stakeholders in government: public sector finance positions should be professionalized; they should have robust qualification requirements; and they should be attractive and competitive for professionals who also have private sector opportunities.

Within each of the three themes I’ve discussed today—sustainability, digitalization, and public financial management—our profession has a major strategic role and an obligation to lead the way in collaboration with our stakeholders.

I want to mention one more thing: our profession’s fundamental purpose of serving the public interest. The quality that enables us to do so, which sets us apart, is professional ethics. Our ethics define us and have earned us our trusted reputation and the central position we occupy in economies, financial markets, and organizations. At all times, we need to keep earning our trusted reputation and never take it for granted.

It is with great honour and satisfaction that I welcome you to the 64th Annual General Assembly of the Institute of Certified Public Accountants of Cyprus.

I would also like to express our sincere pleasure at the presence of the Speaker of the House of Representatives, Mrs. Annita Demetriou. Our cooperation with the Parliament has always been excellent, and our personnel possess specialised knowledge and expertise, always at your disposal for the joint effort of developing a legislative framework that will promote economic growth with both speed and sustainability. Mrs. Demetriou, we warmly welcome you.

With great honour, we welcome for the first time in the history of our Institute the President of the International Federation of Accountants (IFAC), Mr. Jean Bouquot. Your presence here is a clear recognition of the important and elevated role that ICPAC holds at both national and international levels. It also confirms the dynamic path of outward orientation, institutional strengthening, and global recognition that we have charted in recent years. Welcome, Mr. Bouquot.