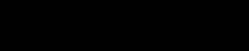

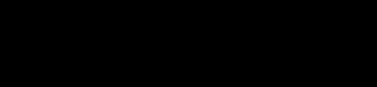

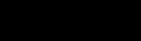

Figure 2. Development in economic vacancy rate

Source: The Danish Property Federation Market Statistics and own calculations based on data from IPD Danish Property Index and Ejendomstorvets Market Index.

Note: Data from January 2014 and onwards is from the Danish Property Federation’s market statistics. From 2001 to 2013, numbers from IPD Danish Property Index are processed based on differences in rate in 2014. In 2000, office data from Ejendomstorvets Market Index is included. The calculation methods are not similar which is why there i a gap in data between October 2013 and January 2014. From January 2014, the calculation is quarterly, while it is annual before 2014. From 2014, the data used is more detailed.

2

Percent

0,0 5,0 10,0 15,0 20,0 25,0 Jan. Jul. Jan. Jul. Jan. Jul. Jan. Jul. Jan. Jul. Jan. Jul. Jan. Jul. Jan. Jul. Jan. Jul. Jan. Jul. Jan. Jul. Jan. Jul. Jan. Jul. Jan. Jul. Jan. Jul. Jan. Jul. Jan. Jul. Jan. Jul. Jan. Jul. Jan. Jul. Jan. Jul. Jan. Jul. Jan. 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 20212022 Kontor Butik Industri Bolig I alt

Positive development in the retail sector

Just like the residential sector, the vacancy in the retail sector has decreased with 0.2 percentage points since last quarter, while it has decreased 0.4 percentage points since the same time last year.

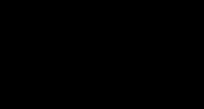

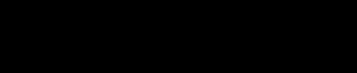

If the retail leases are divided into areas, it is the ones below 75 m2, that have had the largest quarterly decrease in vacancy with 1.6 percentage points, cf. figure 4. However, it must also be seen in the light of this group having the highest retail vacancy with 14.0 percent, as well as an increase of 0.5 percentage points since January 2021. It also applies that the vacancy has also decreased for the remaining sizes of retail leases – except the largest ones.

The largest retail leases – over 300 m2 – have had an unchanged vacancy compared to last quarter, while the vacancy has decreased with 0.2 percentage points compared to January 2021. The largest retail leases, however, also have the lowest vacancy among the groups. The vacancy for the largest retail leases is 5.5 percent this quarter. It can also be seen by figure 4 that the vacancy is lower the larger the retail leases are.

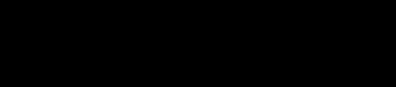

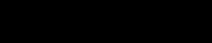

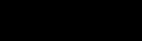

Figure 3. Residential vacancy divided by areas

/ The smallest retail leases with the largest quarterly decreases in vacancy. /

Source: The Danish Property Federation’s market statistics.

Figure 4. Retail vacancy divided by areas

/ Lower retai l vacancy for larger leases. /

Source: The Danish Property Federation’s market statistics.

The Danish Property Federation’s market statistics - vacancy, January 2022 3

Percent

0 2 4 6 8 10 12 14 16 18 < 75 kvm 75-124 kvm 125-299 kvm >300 kvm 2021 Januar 2021 Oktober 2022 Januar

Percent

0 1 2 3 4 5 6 7 8 9 < 75 kvm 75-99 kvm 100-124 kvm 125-149 kvm > 150 kvm 2021 Januar 2021 Oktober 2022 Januar

Office – Small increase

In January 2022, the office vacancy was 8.6 percent. Compared to last quarter, it is a small increase of 0.3 percentage points. If you compare to the same time last year, the office vacancy has decreased with 0.8 percentage points. It means that the office vacancy this quarter is 0.1 percentage point higher than the average of the period 2000-2022.

The increase can also be seen in the Capital Region, South Denmark and Central Denmark, where the office vacancy has increased with 0.4, 0.1 and 0.4 percentage points respectively since last quarter. In Zealand and North Denmark, the office vacancy has decreased with 2.0 and 0.3 percentage points respectively. Despite the decrease, Region Zealand has an office vacancy of 11.4 percent, which is the highest rate among the regions – however, closely followed by the Region of Southern Denmark, where the office vacancy is 11.3 percent. However, it looks like Region Zealand has been in a positive period, as the office vacancy here has decreased with 3.5 percent compared to the same time last year. The annual decreases are also seen in the remaining regions, where there have been decreases of between 0.3-2.1 percent. Compared to the same time last year, the office vacancy in North Denmark has decreased with 2.1 percentage points, which menas an office vacancy of 6.6 percent this quarter, which is the lowest rate among the regions.

The lower rate in North Denmark seems to be due to a relatively low rate in Aalborg, where the vacancy rate is at 5.1 percent. This is a consequence of a decrease of 0.1 percentage points compared to last quarter and an increase of 2.1 percentage points compared to the same time last year. The rate is the lowest among the large cities, where Aarhus is closest with an office vacancy of 6.1 percent after a quarterly increase of 0.5 percentage points.

The

-

January 2022 4

Danish Property Federation’s market statistics

vacancy,

/ Increases in the Capital Area, Southern Denmark and Central Denmark. /

/ Lower office vacancy in Aalborg. /

Economic vacancy rate

Table 1. Office

5

The Danish Property Federation’s market statistics - vacancy, January 2022

Source: The Danish Property Federation’s market statistics.

January

(percent) Quarterly change (percentage points) Annual change (percentage points) Capital Region 8.6 0.4 -0.6 Central Copenhagen 10.5 1.9 2.2 Other City of Copenhagen 6.6 -0.4 -2.4 Northern Zealand 6.1 -1.2 -2.2 Other Capital Region 9.9 0.4 -0.4 Region Zealand 11.4 -2.0 -3.5 Eastern Zealand 12.1 -1.1 -5.0 Western and Southern Zealand 10.8 -2.7 -2.4 The Region of Southern Denmark 11.3 0.1 -1.7 Odense 10.5 2.4 0.8 Triangle Area 14.2 -2.1 -1.6 Other Southern Denmark 9.9 -0.9 -4.6 Central Denmark Region 7.0 0.4 -0.3 Aarhus 6.1 0.5 -0.4 Other Central Denmark 10.3 0.4 0.2 North Denmark Region 6.6 -0.3 -2.1 Aalborg 5.1 -0.1 -2.7 Other North Denmark 15.1 -1.0 0.4 Total 8.6 0.3 -0.8

2022

Retail – Small decrease

In the retail sector, there has been a small quarterly decrease of 0.2 percentage points and a decrease of 0.4 percentage points compared to the same time last year. Therefore, the retail vacancy is 7.6 percent in this quarter. In the period 2000-2022, retail vacancy has been 6.9 percent on average. Despite the decrease this quarter, the retail vacancy is 0.7 percentage points higher than the average.

The overall decrease can also be seen in the Capital Region, Zealand and South Denmark, where the retail vacancy has decreased with 0.3, 1.1 and 0.6 percentage points respectively compared to last quarter and 0.4, 1.3 and 1.1 percentage points respectively compared to January 2021. Contrary, there is a quarterly increase of 0.3 and 0.9 percentage points in the Central Denmark Region and North Denmark respectively as well as an annual increase of 0.6 and 0.3 percentage points respectively. Despite the larger increase in North Denmark, it is the region with the lowest retail vacancy of 6.6 percent. At the other end of the scale, the Region of Southern Denmark has a retail vacancy rate of 9.5 percent. The aforementioned decreases in South Denmark show, however, that it seems to be going in the right direction for the region.

Aalborg is also the city with the lowest retail vacancy. The retail vacancy in Aalborg is 6.8 percent on January 2022. This is despite increases in vacancy, both quarterly and annually. Odense is approaching the rate in Aalborg with a retail vacancy of 7.0 percent after a quarterly decrease of 0.1 percentage points In Central Copenhagen the retail vacancy is somewhat higher, 8.8 percent, despite a relatively large quarterly decrease of 1.1 percentage points – while Aarhus has a vacancy rate of 7.8 percent.

Economic vacancy rate

Table 2. Retail

6

The Danish Property Federation’s market statistics - vacancy, January 2022

Source: The Danish Property Federation’s market statistics.

/ Lowest retail vacancy in North Denmark. /

/ Larger decrease in retail vacancy in Central Copenhagen. /

January 2022 (percent) Quarterly change (percentage points) Annual change (percentage points) Capital Region 7.5 -0.3 -0.4 Central Copenhagen 8.8 -1.1 0.3 Other City of Copenhagen 6.3 1.0 -0.2 Northern Zealand 6.5 -1.6 -2.1 Other Capital Region 7.7 -0.1 -0.5 Region Zealand 7.4 -1.1 -1.3 Eastern Zealand 7.4 -0.3 -1.3 Western and Southern Zealand 7.4 -2.1 -1.3 The Region of Southern Denmark 9.5 -0.6 -1.1 Odense 7.0 -0.1 -1.3 Triangle Area 9.0 0.0 -1.2 Other Southern Denmark 12.5 -1.6 -0.8 Central Denmark Region 7.7 0.3 0.6 Aarhus 7.8 0.3 1.4 Other Central Denmark 7.3 0.2 -0.7 North Denmark Region 6.6 0.9 0.3 Aalborg 6.8 1.9 2.8 Other North Denmark 6.1 -1.8 -6.7 Total 7.6 -0.2 -0.4

Industry – Decrease in vacancy

Since October, the industrial vacancy has decreased to 11.0 percent. This is a quarterly increase of 0.4 percentage points and an increase of 0.4 percentage points compared to the same time last year. Despite the annual increase the industrial vacancy is still below the average of 2000-2022. In that period, the industrial vacancy has been 11.5 percent on average, which is 0.5 percentage points higher than the rate this quarter.

The national decrease is driven by quarterly decreases in both Region Zealand, the Region of Southern Denmark and the Region of Central Denmark, where the industrial vacancy has decreased with 0.8, 1.7 and 1.7 percentage points respectively. Contrary, the industrial vacancy has increased with 0.1 and 1.3 percentage points in the Capital Region and North Denmark respectively since October 2021. These changes mean that the Region of Southern Denmark is the region with the highest industrial vacancy of 4.7 percent. Apart form a quarterly decrease in South Denmark, the industrial vacancy has also decreased with 1.6 percentage points compared to the same time last year, so the region has seen a positive development.

At the other end is the Capital Region, where the industrial vacancy is at 13.1 percent. Among other things, the quarterly increase is driven by an increase in Central Copenhagen, where the industrial vacancy has increased with 1.8 percentage points since last quarter. In Other City of Copenhagen and North Zealand, it has increased with 0.4 and 0.2 percentage points respectively, while it is unchanged in the other Capital Region

Economic vacancy rate

Table 3. Industry

/ Decrease means the lowest industrial vacancy in the Region of Southern Denmark. /

The Danish Property Federation’s market statistics - vacancy, January 2022 7

Source: The Danish Property Federation’s market statistics.

January 2022 (percent) Quarterly change (percentage points) Annual change (percentage points) Capital Region 13.1 0.1 0.5 Central Copenhagen 18.1 1.8 4.4 Other City of Copenhagen 14.9 0.4 0.5 Northern Zealand 23.1 0.2 -0.4 Other Capital Region 11.3 0.0 0.0 Region Zealand 12.4 -0.8 4.3 Western and Southern Zealand 17.0 -0.8 -0.2 The Region of Southern Denmark 4.7 -1.7 -1.6 Odense 4.1 1.0 -1.5 Triangle Area 5.8 -6.6 -3.1 Other Southern Denmark 4.3 0.3 0.4 Central Denmark Region 6.7 -1.7 -0.4 Aarhus 7.3 -2.2 -1.0 Other Central Denmark 6.2 -1.3 0.2 North Denmark Region 5.7 1.3 0.4 Aalborg 7.6 1.8 0.2 Total 11.0 -0.4 0.4

/ Still lower vacancy in the Capital Area. /

Residential – Still decreasing

The residential vacancy continues to decrease. Compared to last quarter, the residential vacancy has decreased with 0.2 percentage points and with 1.7 percentage points compared to the same time last year. It means that residential vacancy is at 3.3 percent in January 2022. Residential vacancy is thus 0.2 percentage points higher than the average from 2000-2022.

The overall decrease can also be seen in all regions except the Central Denmark Region, where the residential vacancy has increased with 0.4 percentage points since last quarter. However, the residential vacancy has decreased with 1.2 percentage points since the same time last year. In the remaining regions, the residential vacancy has decreased with 0.1-0.5 percentage points since October 2021, while the North Denmark Region is the only region, where the residential vacancy is unchanged compared to the same time last year. The latest changes mean that the Capital Region this quarter has a residential vacancy of 2.7 and thus, the region still has the lowest residential vacancy rate among the regions. However, the region is closely followed by Region Zealand with a residential vacancy of 2.9 percent. At the other end of the scale, the North Denmark Region has a vacancy of 6.5 percent.

Despite the Capital Region having the lowest residential vacancy among the regions, it is not Central Copenhagen with 5.8 percent that has the lowest residential vacancy among the cities. Here, Odense is still the city with the lowest residential vacancy rate of 3.3 percent, if you disregard other City of Copenhagen. This is after a quarterly decrease of 0.4 percentage points and an annual decrease of 1.2 percentage points. However, the residential vacancy has also decreased in Central Copenhagen with 0.2 and 1.5 percentage points on a quarterly and annually basis. Aarhus is the only city where the residential vacancy has increased since last quarter. There is a small increased of 0.3 percentage points, which means a residential vacancy rate of 4.2 percent. In Aalborg, the residential vacancy has decreased with 0.1 percentage points since October 2021, which brings it down to 6.2 percent.

Economic vacancy rate

Table 4.

The Danish Property Federation’s market statistics - vacancy, January 2022 8

Source: The Danish Property Federation’s market statistics.

Residential

January 2022 (percent) Quarterly change (percentage points) Annual change (percentage points) Capital Region 2.7 -0.4 -2.2 Central Copenhagen 5.8 -0.2 -1.5 Other City of Copenhagen 2.3 -0.5 -2.5 Northern Zealand 3.1 0.1 -0.6 Other Capital Region 2.6 -0.2 -2.2 Region Zealand 2.9 -0.3 -1.0 Eastern Zealand 2.8 0.1 -0.6 Western and Southern Zealand 3.0 -0.5 -1.2 The Region of Southern Denmark 3.3 -0.5 -1.2 Odense 3.3 -0.4 -2.1 Triangle Area 4.3 0.3 0.3 Other Southern Denmark 2.5 -1.3 -0.9 Central Denmark Region 4.2 0.4 -1.2 Aarhus 4.2 0.3 -0.5 Other Central Denmark 4.1 0.6 -3.1 North Denmark Region 6.5 -0.1 0.0 Aalborg 6.2 -0.1 0.0 Other North Denmark 10.4 -0.1 0.1 Total 3.3 -0.2 -1.7

Geographical overview

Central Copenhagen

Region Zealand

Western and Southern Zealand

Eastern Zealand

Northern Zealand

Capital Region

Central Copenhagen

Other City of Copenhagen

Other Capital Region

Source: The Danish Property Federation’s market statistics.

Note: Copenhagen Centre consist of the inner city with the post codes: 900, 1000-1431, 1434-1438, 14481559, 1562-1609, 1611-1614 and 1631-1634.

January 2022 9

The Danish Property Federation’s market statistics - vacancy,

North Denmark

Aalborg

Central Denmark Region

Aarhus

The Triangle area

The Region of Southern Denmark

Odense

About the survey

This web report is published on 14 March. January 2022. Next planned publication is January 2022

The portfolios have approx. 249,000 leases corresponding to an annual rental-bearing value of DKK 40.4bn and 35.9m m2 In comparison, the statistical base in January 2020 was 226,000 leases with an annual rental-bearing value of DKK 38,1 billion and 34,0 million m2

Today, 18,038 properties* are included in the market statistics. It is the current annual rent that is included in the calculation of the economic vacancy rate. The economic vacancy rate is defined as: The sum of current annual rent in all empty leases divided by the sum of current annual rent in both rented and empty leases.

The Market Statistics is based on quarterly processed property data for rentals and vacancies within the period in question. Compared to previous publications, the balance date has been changed from the last day of the last quarter to the first day of this quarter. This web report has thus been closed as of 01 January 2022 and is called January 2022. The quarterly change is from January 2022 (settled as of 01 January 2022) compared to October 2021 (settled as of 01 October 2021). The annual change is from January 2021 (settled as of 1 January 2021) compared to January 2021 (settled as of 01 January 2021).

The published market data is updated and valid on the day of publication. As the market statistics are continuously updated with e.g. new historical data, there may be updates of historical data. It has been chosen not to publish data in the statistics where the basis has been evaluated not to provide valid and representative data or in combinations where only one or a few portfolios are represented.

* The number of properties include properties and parent properties. A property can include one or more buildings and one or more residences or office units. A parent property includes a property, in which there are apartments, which are registered as independent properties. For these units it is the parent properties that are counted and not each freehold apartment.

2 + 3 Ejendomme, Aberdeen Asset Management, Advice, Advodan, Akelius, Alm. Brand, ALN Holding, Andersen Partners Ejendomsadministration, Anker Bay Petersen, AP Pension, Arbejdernes Landsbank, Arkitekternes Pensionskasse, Arup & Hvidt, ATP, Bagenkop Ejendomme A/S, Balder Ejendomme, Ballegaard Gruppen, Bangs Gård A/S, Bank Lauridsen, Barfoed Group, Bellevue 16 ApS, Bendtsen ApS, Bernhard Guhle, Bernstorrfhus, Bevica Fonden, Birch Ejendomme, BladhuseneApS, Blue Vision, Bodil og Co. I/S, Bolig Data Administration, Bolig og erhvervsudlejning I/S, Boligexperten Adm. A/S, Boliggruppen, Boligstandard ApS, BoStad A/S, Brdr. Christiansens Boligudlejning, Broen Shopping, Bruno Dall, Calum A/S, Carlsbergfondet, CBRE, CEJ Ejendomsadministration, Cieslak Ejendomme, CK Holding Odense I/S, Claus Sørensen, CMNRE II FV181 PropCo ApS, CMNRE II Goose PropCo II A/S, Cobblestone, Coller Capital, Compaz Ejendomme A/S, Cosmo Ejendomme ApS, Connla Administraion, CS Pensionsfond, CW Obel Ejendomme, DADES, Danica, Dansk Administrationscenter, Danagraf A/S, Dansk Sygeplejeråd, Danske Bank, Danske Shoppingcentre, DATEA, DEAS, DEAS Invest 1, De Københavnske Ejendomsselskaber, Demant Advokater, Difko, DIKEV, DIP, DK Ejendomme, DNP Ejendomme, Domhusgaarden Ejendomsadministration, Domis Ejendomme, Dreist-Storgaard, DSB Ejendomme, Egen Vinding & Datter ApS, Ejd. Selskabet Dronning Olgas Vej 15 ApS, Ejendommen Hauchsvej 16 I/S, EjendomDanmark, Ejendomskontoret, Ejendomsselskaberne, Ejendomsselskabet af 15. maj 1895, Ejendomsselskabet Aunbøll A/S, Ejendomsselskabet NEMP, Ejendomsselskabet Thy, Ejendomsselskabet Østervold, Elverhøj Investment Group ApS, Estate Invest, Etex Ejendomme, Erhverv Aalborg, EV bolig, Fast Ejendom Danmark, Flemming Jeppsson, Flemming Olsen, Flemming Sørensen, Fokus Asset Management, Frederiksberg Fonden, Freja Ejendomsadministration, Friheden Ejendomme A/S, Færchfonden, Goldschmidt Ejendomme A/S, Grosserer Schiellerup og Hustrus Fonde, Gudbjørg og Ejnar Honorés Fond, Grønløkkevej 10, Grønnegaarden Ejendomsselskab, Hans Nielsen, Haugaard|Braad, HEA Ejendomme, Hegela Erhvervsudlejning, Heimstaden, Helle Duun, Hestia, Hjørnet, Home Holbæk, Hovedstadens Ejendomsadministration, Hosta Ejendomme, Humlebogruppen, Højgaard Ejendomme, Industriens Pension, Investorgruppen, Jammerbugt Kommune, Jens Garfalk, Jeudan, JJ Ejendomsadministration, Jorcks Ejendomsselskab, JØP, Kaj Pedersen, Kalkværksgrundene, Kalvebod Ejendomme, Karberghus, Kayhan Development, KEBLOH ApS, Kereby A/S, KFI Erhvervsdrivende Fond, KIRKBI, KHK’s Legat, KGV Aarhus ApS, KLP Ejendomme, Koncenton, Kramers Legat, K/S Ingolf Nielsens Vej Sønderborg, K/S Roskilde Retail Park II, Københavns Kommune, Køge Kommune, Laros, Lars Wissing, LB Forsikring, Levring & Levring,Lindhart Ejendomsadministration, Lyngby Kommune, Lægernes Pensionskasse, Lærernes Pension, M7 Real Estate ApS, Michael Westh-Jensen, Midtbyens Ejendomme, Minova, Mogens WesthJensen, Moltzen Administration, Mogens Nielsen, Morten Norberg,MP Pension, MOWE Holding ApS, NEMO Ejendomsadministration, Nemp Ejendomsadministration, Niam, Niels Møller, Nielsen & Nielsen Ejendomme A/S, Nordea Ejendomme, Nordea Liv og Pension, North Property Asset Management, NREP, Odense Bolig ApS, Olav de Linde, Ole Hartvig, PBU, Pears, PenSam, PensionDanmark, Pensionskassen for Farmakonomer, PFA, Pfeiffer Ejendomme ApS, PIA, Rasch-Andersen Ejendomme ApS, Rathleff Ejendomme, International, Pitzner Ejendomme, PKA, PN Ejendomme, Postbudenes Byggeforening, Probus, ProDomus, Realdania, Revisorteamet, Roskilde Fællesbageri ApS, Rødovre Centrum A/S, Sampension, SEB, Samrådets Boligselskab / Dronning Louises Stiftelse, Siersbo ApS, Skovly Ejendomme, Sofus Administration ApS, SparNord Ejendomme Aalborg, Storck Holding, Svanholt Ejendomme, SPG Omsorg DK1, Steen & Strøm, Syddan A/S, Taurus Ejendomsadministration, TDC Pensionskasse, Thisted Kommune, Thylander Gruppen Sixpack, TLK Ejendomme, TLP ApS, Tom Jensen, Topdanmark, Totalbyg, Tox Development, Tryg, T.T. Invest ApS, UBSBOLIG A/S, Unico Finans ApS, Vagner P, Valby Maskinfabrik 1ApS, Valad, VEA ApS, Vestegnens Boligadministration, Vestjysk Ejendomsadministration ApS, Vestsjællandske Ejendomme ApS, Volantis A/S, VOPA Ejendomsadministration ApS, V.M. Brockhuus Ejendomme, Wagner Ejendomme, West Star Property Holding ApS, Wihlborg, Wind Administration, Øens Ejendomsadministration, Aalborg Boligadministration og Aage Larsens Boligudlejning.

The Danish Property Federation’s market statistics - vacancy, January 2022 10

The statistics are prepared based on data from

The Danish Property Federation’s market statistics - vacancy,

Figure 3. Spatial vacancy rate, January 2022

Source: The Danish Property Federation’s market statistics. Note: The vacancy rates for all sectors also include actual annual rent and space for other commercial and secondary spaces.

January 2022 11

Appendix

Other Business Change in percentage points Quarter Year -0.7 -1.9 5.1 Residential Change in percentage points Quarter Year -0.2 -1.3 3.5 Industry Change in percentage points Quarter Year -0.4 0.1 11.7 Retail Change in percentage points Quarter Year -0.2 -0.6 7.5 Office Change in percentage points Quarter Year 0.4 -0.7 9.5 Total Change in percentage points Quarter Year -0.1 -1.1 6.9

The Danish Property Federation’s market statistics - vacancy, January 2022

Spatial vacancy rate

Table 5. Office

12

Source: The Danish Property Federation’s market statistics.

January 2022 (percent) Quarterly change (percentage points) Annual change (percentage points) Capital Region 9.6 0.6 -0.5 Central Copenhagen 10.0 1.2 1.4 Other City of Copenhagen 5.8 -0.4 -1.8 Northern Zealand 6.9 -1.5 -2.8 Other Capital Region 13.4 1.6 0.2 Region Zealand 11.9 -1.7 -2.3 Eastern Zealand 11.8 -2.4 -4.2 Western and Southern Zealand 11.9 -1.3 -1.1 The Region of Southern Denmark 11.2 0.2 -2.1 Odense 9.1 2.4 -0.3 Triangle Area 15.2 -3.1 -1.3 Other Southern Denmark 11.2 -0.8 -4.2 Central Denmark Region 7.8 0.5 -0.1 Aarhus 6.2 0.6 -0.5 Other Central Denmark 12.5 0.6 1.4 North Denmark Region 7.5 -1.0 -3.4 Aalborg 6.1 -0.6 -3.8 Other North Denmark 12.6 -2.2 -2.6 Total 9.5 0.4 -0.7

Table 6. Retail

Spatial vacancy rate

2022

13

The Danish Property Federation’s market statistics - vacancy, January 2022

Source: The Danish Property Federation’s market statistics.

January

(percent) Quarterly change (percentage points) Annual change (percentage points) Capital Region 7.2 0.0 -0.1 Central Copenhagen 9.4 -0.8 1.7 Other City of Copenhagen 5.4 0.7 -0.3 Northern Zealand 6.3 -1.6 -2.6 Other Capital Region 8.1 0.2 -0.1 Region Zealand 7.1 -0.8 -1.3 Eastern Zealand 5.9 -0.2 -0.6 Western and Southern Zealand 8.0 -1.3 -1.8 The Region of Southern Denmark 9.2 -1.3 -1.6 Odense 6.6 -1.0 -2.5 Triangle Area 8.8 -0.4 -1.7 Other Southern Denmark 11.4 -1.9 -0.7 Central Denmark Region 7.5 0.1 0.2 Aarhus 7.2 0.0 0.7 Other Central Denmark 8.0 0.2 -0.5 North Denmark Region 6.7 0.8 -2.5 Aalborg 6.3 1.8 2.4 Other North Denmark 7.5 -0.9 -9.6 Total 7.5 -0.2 -0.6

The Danish Property Federation’s market statistics - vacancy, January 2022

Table 7. Industry

14

Source: The Danish Property Federation’s market statistics.

January 2022 (percent) Quarterly change (percentage points) Annual change (percentage points) Capital Region 16.1 0.3 1.0 Central Copenhagen 25.2 3.0 6.5 Other City of Copenhagen 20.9 0.4 0.4 Northern Zealand 25.9 0.7 4.0 Other Capital Region 12.8 0.3 0.3 Region Zealand 10.4 0.0 0.1 Western and Southern Zealand 18.8 -1.2 -1.3 The Region of Southern Denmark 4.6 -1.9 -1.4 Odense 3.3 0.3 -2.4 Triangle Area 6.9 -7.9 -2.2 Other Southern Denmark 4.1 0.4 0.7 Central Denmark Region 7.0 -1.8 -0.4 Aarhus 8.6 -3.3 -1.6 Other Central Denmark 6.1 -0.9 0.4 North Denmark Region 5.5 1.7 0.6 Aalborg 8.0 2.6 0.8 Total 11.7 -0.4 0.1

Spatial vacancy rate

Table 8.

The Danish Property Federation’s market statistics - vacancy, January 2022

Spatial vacancy rate

2022

15

Source: The Danish Property Federation’s market statistics.

Residential

January

(percent) Quarterly change (percentage points) Annual change (percentage points) Capital Region 2.7 -0.3 -1.6 Central Copenhagen 5.5 -0.3 -0.6 Other City of Copenhagen 2.3 -0.5 -2.0 Northern Zealand 3.2 0.1 -0.6 Other Capital Region 2.7 -0.2 -1.5 Region Zealand 3.3 -0.4 -1.0 Eastern Zealand 2.7 0.1 -0.5 Western and Southern Zealand 3.5 -0.5 -1.1 The Region of Southern Denmark 3.3 -0.4 -1.1 Odense 3.3 -0.2 -1.8 Triangle Area 4.0 0.3 -0.1 Other Southern Denmark 3.0 -1.1 -0.7 Central Denmark Region 4.3 0.4 -1.3 Aarhus 4.3 0.3 -0.3 Other Central Denmark 4.4 0.6 -2.8 North Denmark Region 6.8 -0.2 0.2 Aalborg 6.3 -0.3 0.2 Other North Denmark 11.2 -0.1 0.5 Total 3.5 -0.2 -1.3