S H E L L G A M E

R e p r e s e n t a t i v e C a s e s o f F E O C R i s k s t o U S E n e r g y

D o m i n a n c e

INTRODUCTION

Over the past two decades, China has established a dominant posi6on in the global solar industry. The PRC currently accounts for over 85 percent of global crystalline silicon solar PV manufacturing capacity, including more than 85 percent of module, 86 percent of cell, and 97 percent of wafer and ingot produc6on.i China has secured this dominance by leveraging Western technologies and non-market state support. China has cemented this dominance by undercuHng non-Chinese compe6tors across the supply chain; circumven6ng and manipula6ng trade restric6ons; and even posi6oning to benefit from, and therefore neutralize, US and other interna6onal incen6ve programs intended to support non-Chinese manufacturing.

America needs non-Chinese manufacturing in solar to execute on the energy dominance agenda. China’s efforts to subvert US manufacturing policy present a tractable, but also urgent, challenge: They threaten US energy security, US companies, and US market norms. America is at risk of depending on China for energy, and energy that is growing more and more cri6cal as the AI revolu6on picks up pace. America is at risk of not only missing out on a massive emergent market but also leHng China capture the profits. And America is at risk of ceding more cri6cal industrial capacity to Beijing, including industrial capacity relevant to other strategic sectors like semiconductors.

Increasingly, Washington has recognized these threats. The US government has ins6tuted trade barriers against Chinese crystalline silicon solar manufacturers to combat their dumping and other non-market policies, sought to crack down on Chinese en66es “trans-shipping” through third-party countries to access the US market, and placed “foreign en66es of concern” (FEOC) restric6ons on the tax breaks and other preferen6al policies intended for solar and other energy companies.

But again and again, China has found workarounds and loopholes. China has consistently developed new playbooks to circumvent and manipulate US defenses. Some of these take place in the ba\lefield of interna6onal trade, as with trans-shipment. But perhaps most dangerous – in that they threaten not only to neuter US defensive measures but also to co-opt US industry from the inside – are the ways in which Chinese companies “localize” in the US to evade FEOC “effec6ve control” regula6ons.

FEOC “effec6ve control” restric6ons focus primarily on ownership, as reflected in equity stakes. But Chinese companies forge joint ventures on American soil in which their equity stakes remain just below thresholds that ac6vate FEOC restric6ons. Chinese companies also leverage offshore and tax haven en66es, intermediaries and shell structures, and stock holdings via passive funds to obscure their ul6mate ownership. Chinese companies form tech licensing agreements with US partners such that those partners – while independent from an ownership perspec6ve – remain dependent on Chinese technology and therefore responsive to Chinese interests. And, a new model of “American localiza6on with Chinese characteris6cs,” Chinese companies invest in US companies, below thresholds that might trigger restric6ons and indirectly to obfuscate 6es. These investments allow Chinese companies to capture profit from and shape the technological direc6on of the US energy market.

This basket of tac6cs underscores how outdated typical US government conven6ons of foreign influence and control are – and why FEOC protec6ons urgently require upda6ng in the fight for reindustrializa6on and energy dominance. The US government’s framework for iden?fying “effec?ve control” needs to match China’s circumven?on tack. Otherwise, America risks not only losing strategic ground to China but in fact helping Chinese companies claim that ground.

To illustrate as much, this white paper focuses on two examples of Chinese companies that risk evading FEOC “effec6ve control” regula6ons: those of Canadian Solar and T1 Energy. Canadian Solar is a Canadian-headquartered en6ty that, since its incep6on more than 20 years ago, has used its North American presence as a beachhead into the US and global markets. T1 Energy represents a more evolved, sophis6cated, and recent model. The company is American. At first glance, it appears to be reclaiming US solar manufacturing from China. But T1’s largest shareholder is a Chinese solar giant – and T1 appears to depend on that giant for technology. This risks making T1 a wolf in sheep’s clothing; an obfuscated foothold for China in the US market and a dead-end for US re-industrializa6on.

These cases are representa6ve. But they are not exhaus6ve – or unique. The localiza6on playbook they demonstrate has become pervasive. And the PRC supply chain and industrial policy at work behind the scenes is well equipped to replicate and adapt that playbook as needed. This means that approaches to developing FEOC restric6ons need to be fully informed and structured to capture PRC beachheads and routes to sowing dependency on the ground in the US market. Those restric6ons also need to be enforced – and resourced appropriately for monitoring and enforcement throughout the lifecycle of US government industrial policy support. A signal of strict and effec6ve enforcement will allow these protec6ons fully to ac6vate the market forces needed to back American industrial renewal. And learnings from the solar supply chain case should be applied to protect against Chinese subversion in other sectors and supply lines cri6cal to US industrial renewal and energy dominance.

T1 ENERGY

In November 2024, Trina Solar (Schweiz AG), a subsidiary of Chinese solar energy giant Trina Solar, inked a deal to sell its Texas-based solar manufacturing assets to T1 Energy. A US domiciled company, T1 describes itself as “building an integrated US supply chain for solar and ba\eries.” ii At first glance, the transac6on seemed a victory for US domes6c energy produc6on and the bid to loosen China’s stranglehold on the solar industry. But the details of the deal, and the rela6onship that has developed since, suggest that T1 Energy is financially and technologically 6ed to, influenced by, and dependent on Trina. T1 risks serving as an obfuscated foothold through which Trina can profit from and influence the US market, all while evading the safeguards the Trump administra?on has worked to establish.

Trina holds a significant and growing stake in T1 Energy. T1 Energy (previously known as FREYR) also relies on technology licensed from and upstream inputs bought from Trina. T1’s business model rests on combining US ownership, that allows it to avoid regulatory restric6ons and benefit from government incen6ves, with market and technological support from China’s Trina. T1 Energy is explicit about this. The company’s form S-3 SEC registra6on statement describes its compe66ve differen6a6on as the combina6on of a partnership with Trina and a domes6c US presence: “The superior performance characteris6cs of the PV solar modules that we manufacture through our commercial partnership with Trina Solar (“Trina”) and our domes6c content will compe66vely differen6ate T1 Energy in the U.S. market.”iii

This represents an evolved model of Chinese localiza6on in the US. Trina is not repackaging a Chinese product as American. But the company’s equity and technological 6es to T1 allow Trina to reap economic rewards from and shape the direc6on of the US market. And while T1 might be manufacturing in the United States, reliance on Chinese technology and capital reinforces the overall dependence on the PRC that domes?c re-industrializa?on is supposed to prevent.

T1’s financial disclosures do indicate awareness that its 6es to the PRC risk running afoul of US regula6ons – more specifically, restric6ons on foreign en66es of concern. Its August 2025 Form S-3 noted that new US legisla6on:

eliminates the availability of tax credits for taxpayers that source a par6cular percentage of their products and components from, or have certain commercial arrangements with, foreign en66es of concern (“FEOC”). We are ac6vely working to ensure compliance with

the FEOC-related provisions of the OBBBA to allow us and our customers to retain the availability of tax credits in the future.

Trina as a Strategic Shareholder – with Board Influence

Trina is the largest holder of T1’s common shares, with a 16.6 percent stake that is posi6oned to increase to about 25 percent. The November 2024 deal between Trina and T1 Energy was not a simple acquisi6on. It also granted Trina, via its Swiss en6ty Trina Solar (Schweiz) AG, a significant stake in T1 Energy: In addi6on to 100 million USD in cash and a 150 million USD loan note, T1 gave Trina 15,437,847 common shares and an 80 million USD unsecured conver6ble note –conver6ble to 30,440,113 common shares.

As of September 2025, aier a first tranche of conversion, Trina held a 16.60 percent stake in T1 Energy (27,959,500 common shares). Based on T1 filings from October, Trina appears to be the largest holder of T1’s common stock. iv And Trina’s stake is posi6oned to almost double – to roughly 25 percent of T1 – as T1 con6nues common stock delivery.v

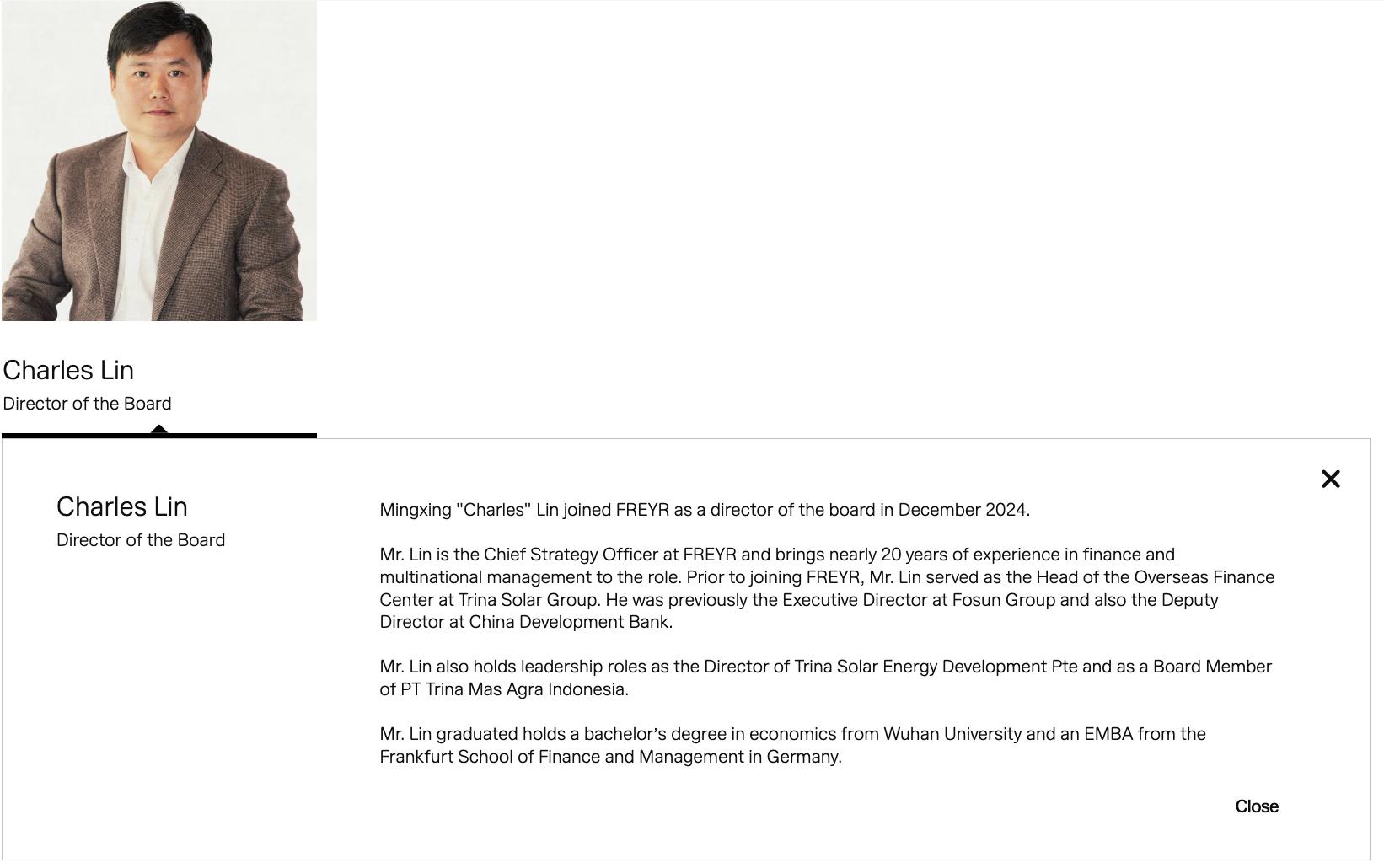

Trina’s stake in T1 grants the Chinese company influence over T1’s board of directors: As long as it holds 15 percent or more of T1’s common shares, Trina has the right to designate two directors to T1’s board. And T1’s board of directors is required to appoint one Trina-designated director to

each of a) its nomina6ng and corporate governance commi\ee and b) its compensa6on commi\ee.vi Trina’s current board designees appear to include Mingxing “Charles” Lin (林明星). Lin previously worked as head of the Overseas Finance Center at Trina Solar Group – and, before that, as deputy director at the China Development Bank. Lin con6nues to hold a leadership role at Trina, where he is director of Trina Solar Energy Development Pte.vii

Trina’s stake in T1 is so significant that PRC media sources refer to T1 Energy as a “Trina Solar joint venture partner.” For instance, when T1 Energy and Corning formed a sales agreement in 2025, Sina reported: “Trina Solar’s joint venture partner joins hands with glass giant.”viii

Another, O:shore Trina Investor

Moreover, Trina also appears to have a stake in, and therefore influence over, T1 via investment on the part of an en6ty that – despite its nondescript name, low profile, and Bri6sh Virgin Isles address – is described in Chinese documents as a “related en6ty” of Trina and controlled by Chunyan Wu, the wife of Trina’s CEO. An August 2025 filing from T1 notes that “on November 6, 2024, the Company and an investor who is a significant shareholder of Trina Solar entered into a share purchase agreement pursuant to which the investor subscribed to purchase a total of 14.8 million USD of common stock.”ix T1’s filing does not disclose who that shareholder was. But on November 7, 2024, days aier the 2024 presiden6al elec6on, Trina announced that one of its related en66es, Stellar Hann Investment Ltd. (formerly Trinaway Investment Second Ltd.) was directly acquiring 14,050,000 new shares of FREYR (aka T1 Energy) for 14.75 million RMB.x

The agreement has since been modified. But T1 appears to have issued 7,000,000 Penny Warrants to Stellar Hann that will become fully exercisable by March 10, 2026. Stellar Hann will be able to convert those warrants into shares without paying cash. If fully exercised, they will be worth about 4 percent of T1 Energy.xi

Technology Licensing and Supply Chain Dependence

T1 also con6nues to depend on technology and supply chain inputs from China. This risks exacerba6ng Chinese leverage over the US solar sector. It also risks making T1’s opera6ons effec6vely a pass through for Trina’s, and therefore China’s, solar products as they enter the United States.

T1’s November 2024 agreement with Trina Solar also involved commercial support and technology licensing agreements. These include a module opera6ons support agreement, IP license agreement, and IP sublicense agreement, among others.xii Such agreements risk meaning that T1 cannot operate without PRC technologies – and supports the Chinese rather than US innova6on base.

Trina’s Government Ties

Trina Solar is a Chinese photovoltaic giant. It holds roughly 15 to 20 percent of the global market. Trina has been able to claim that posi6on in no small part thanks to government subsidies: In 2024, the company reported receiving some 414 million RMB in direct government subsidies.xiii

Trina’s leadership in China, 6es to the Chinese government, and alignment with Chinese industrial policy – and corresponding threat to the United States – are also evident in its personnel. Gao Jifan, Trina’s founder and chairman, serves as a delegate to the 14th Na6onal People’s Congress, the highest organ of state power of the People's Republic of China. He is also a standing commi\ee member of the China Na6onal Democra6c Construc6on Associa6on, one of the eight minor democra6c par6es in China under the direc6on of the Chinese Communist Party.xiv

A Critical Mass in China

This division, and the corresponding concentra6on of Canadian Solar’s physical presence in China, is reflected in the distribu6on of the company’s long-lived assets, including property, plant and equipment, solar power and ba\ery energy storage systems, intangible assets, and ROU assets. More than half of those assets are based in China, as reflected in the table below.

Canadian Solar Long Lived Assets by Country/Regionxxii Country

Employment figures tell a similar story. As of December 31, 2024, Canadian Solar had almost 12,000 employees in China and less than half of that in all of the rest of the world combined, including the US, Canada, Japan, Australia, Singapore, Korea, Hong Kong, Taiwan, India, Thailand, Vietnam, Brazil, the United Arab Emirates, South Africa, the United Kingdom, La6n America, and the European Union. The company’s China-6ed reality is also evident in a quirk of its corporate filings: Those, filed by an ostensibly Canadian en6ty to the US Nasdaq, are audited by “Deloi\e Touche Tohmatsu Cer6fied Public Accountants LLP, an independent registered public accoun6ng firm located in China.”xxiii

The significance of the China-based por6on of the Canadian Solar apparatus is also evident in ownership structures within the company. Canadian Solar ’s main solar component subsidiaries in the United States, according to the company ’s annual report, are owned by CSI Solar Co., Ltd., Canadian Solar ’s majority-owned principal opera6ng subsidiary incorporated and publicly listed in the PRC. In other words, Canadian Solar ’s chief Chinese subsidiary owns the company ’s solar component facili6es in the United States.

Canadian Solar’s significant manufacturing footprint in the PRC also risks exposing the company to forced labor. The company has been accused of opera6ng manufacturing facili6es in the

Xinjiang region, home to the genocide of the Uyghur minority, and of sourcing from suppliers associated with forced labor, including GCL-Poly Energy.xxiv

Chinese Government Backing

Further underscoring Canadian Solar’s 6es to the PRC, its affiliates in China receive government incen6ves and support. Mul6ple Canadian Solar subsidiaries – including Suzhou Sanysolar Materials Technology Co., Ltd, Changshu Tegu New Material Technology Co., Ltd, CSI New Energy Development (Suzhou) Co., Ltd, CSI Solar Technologies (JiaXing) Co., Ltd, Canadian Solar Photovoltaic Technology (Luoyang) Co., Ltd. and CSI Energy Storage Co., Ltd. – have been designated by the Chinese government as “High and New Technology Enterprises.” xxv That designa6on, granted to preferred companies in key supply chain nodes, comes with, among other perks, preferen6al tax status. And in its 2024 annual report, CSI Solar Co., Ltd., Canadian Solar’s main opera6ng subsidiary in China, reported receiving more than one billion RMB in government subsidies.xxvi

Canadian’s affiliates – in Canada, the US, China, and across the world – exist in a complex web of subsidiaries and parents. Qu serves as a clear and unifying thread, as both a shareholder and manager.xxvii For example, he is chairman of both Canadian Solar, listed on the Nasdaq, and CSI Solar Co., Ltd., listed on Shanghai Stock Exchange's Sci-Tech Innova6on Board.xxviii

Qu’s personal biography further underscores the company’s 6es to China. Born in Beijing, he holds a bachelor’s degree from Tsinghua University, where he was made a visi6ng professor in 2011.xxix He has won major PRC government awards including the Jiangsu Province May 1st Labor Honorary Medal and the Jiangsu Province “Young and Middle-Aged Experts with Outstanding Contribu6ons” awards. xxx Qu has served in PRC government roles too: He was a member of the Changshu Municipal Commi\ee of the Chinese People’s Poli6cal Consulta6ve Conference. And he has held leadership roles on government-overseen industry associa6ons including the China Renewable Energy Society and Suzhou Photovoltaic Industry Associa6on.xxxi

CONCLUSION

Washington, DC is working to re-industrialize and unleash energy dominance by crea6ng the condi6ons for truly domes6c manufacturing to thrive. Yet, as the cases detailed here demonstrate, both US industry and US policy are at risk of Chinese co-op6on. So are the “domes6c manufacturing” and “American-made” labels.

China’s evolving, manipula6ve playbook demands a responsive US approach, one that not only updates but also stays ahead. For example, China uses “localiza6on” tac6cs to evade US FEOC restric6ons. These tac6cs include ownership through interna6onal subsidiaries, joint ventures, equity investment, intermediaries and offshore shell structures, and the use of tech licensing and dependence on Chinese supply. And these tac6cs risk succeeding. To avoid that – and the Chinese coop6on of US industry that it enables – Washington urgently needs comprehensive, forwardlooking FEOC regula?ons that go beyond addressing China’s methods and an?cipate new forms of circumven?on, control, and influence.

To that end, guidance from the Treasury Department should clearly define effec6ve control criteria that update for China’s means. That guidance should also document clear pathways for regulators to enforce restric6ons. All should be done in a fashion that sends a compelling signal that America’s tax incen6ves and broader reindustrializa6on efforts are resilient to Chinese subversion.

i “PV Supplier Market Intelligence Program Q2 2023,” Clean Energy Associates.

ii “Home,” T1 Energy, Accessed November 10, 2025. hKps://t1energy.com/

iii "T1 Energy Form S-3," T1 Energy, September 2025. hKps://ir.t1energy.com/staQc-files/971b1866-a469-4f16-bb4659476535aee1

iv “T1 Energy Schedule 14A,” T1 Energy, October 10, 2025. hKps://ir.t1energy.com/staQc-files/26aa31c7-b0ff-4ae18580-bc81504bca36

v " T1 Energy Form S-3," T1 Energy, September 2025. hKps://ir.t1energy.com/staQc-files/971b1866-a469-4f16bb46-59476535aee1

vi " T1 Energy Form S-3," T1 Energy, September 2025. hKps://ir.t1energy.com/staQc-files/971b1866-a469-4f16bb46-59476535aee1

vii “Charles Lin,” T1 Energy, Accessed October 17, 2025.

viii "从多晶硅到光伏组件...天合光能参股公司牵⼿玻璃巨头 [From Polysilicon to Photovoltaic Panels... Trina Solar's Joint Venture Partner Partners with Glass Giant]," Sina, August 18, 2025.

ix “T1 Energy Form 10-Q,” T1 Energy, August 19, 2025.

x "Trina Solar: Trina Solar Co., Ltd.'s Announcement on the ParQcipaQon of Related ParQes in Equity Investment and Related Party TransacQons," Yicai Global, November 7, 2024.

hKps://www.theglobeandmail.com/invesQng/markets/stocks/TE/pressreleases/34771808/t1-energy-terminatesagreement-with-stellar-hann/)

xi (T1 Energy Terminates Agreement with Stellar Hann,” Globe and Mail, September 12, 2025.

xii " T1 Energy Form S-3," T1 Energy, September 2025. hKps://ir.t1energy.com/staQc-files/971b1866-a469-4f16bb46-59476535aee1

xiii "天合光能:2024 年年度报告 [Trina Solar: 2024 Annual Report]," Trina Solar, 2025.

xiv “⾼纪凡 [Gao Jifan],” Sina Finance, Accessed November 2, 2025.

xv For example, Canadian Solar’s 2024 annual report states that, because of its extensive presence in China, “we are subject to risks arising from the PRC legal system,” including the Data Security Law, the Personal InformaQon ProtecQon Law, and the Cybersecurity Review Measures. (“Canadian Solar Form 20F,” Canadian Solar, April 30, 2025.)

xvi “Canadian Solar Form 20F,” Canadian Solar, April 30, 2025. hKps://investors.canadiansolar.com/staQcfiles/8c409658-082c-4758-b72b-964cd26eed05

xvii “Canadian Solar Form 20F,” Canadian Solar, April 30, 2025. hKps://investors.canadiansolar.com/staQcfiles/8c409658-082c-4758-b72b-964cd26eed05

xviii “Board of Directors,” Canadian Solar, Accessed October 71, 2025. hKps://investors.canadiansolar.com/corporate-governance/board-and-management

xix 阿特新阳光店⾥集团获 2015 中国原创技术 [Art New Sunshine Store Group won the 2015 China Original Technology],” China Economic Weekly, December 28, 2015.

xx See: “Canadian Solar AMENDMENT NO. 3 TO FORM F-1 REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933,” Canadian Solar, Accessed October 17, 2025.

xxi “Canadian Solar Form 20F,” Canadian Solar, April 30, 2025. hKps://investors.canadiansolar.com/staQcfiles/8c409658-082c-4758-b72b-964cd26eed05

xxii “Canadian Solar Form 20F,” Canadian Solar, April 30, 2025. hKps://investors.canadiansolar.com/staQcfiles/8c409658-082c-4758-b72b-964cd26eed05

xxiii “Canadian Solar Form 20F,” Canadian Solar, April 30, 2025. hKps://investors.canadiansolar.com/staQcfiles/8c409658-082c-4758-b72b-964cd26eed05

xxiv Kenneth Rapoza, “Canadian Solar Panels in Maine Accused of Using China Forced Labor, CoaliQon for a Prosperous America, January 10, 2023.

xxv “Canadian Solar Form 20F,” Canadian Solar, April 30, 2025. hKps://investors.canadiansolar.com/staQcfiles/8c409658-082c-4758-b72b-964cd26eed05

xxvi "阿特斯:2024 年年度报告 [Canadian Solar: 2024 Annual Report ]," Sina Finance, April 29, 2024.

xxvii “Canadian Solar Form 20F,” Canadian Solar, April 30, 2025. hKps://investors.canadiansolar.com/staQcfiles/8c409658-082c-4758-b72b-964cd26eed05

xxviii "阿特斯:2024 年年度报告 [Canadian Solar: 2024 Annual Report ]," Sina Finance, April 29, 2024.

xxix “

瞿晓铧 [Qu Xiaohua],” Sina East Money, Accessed October 17, 2025.

xxx "

阿特斯(中国)投资有限公司董事⻓、总裁兼⾸席执⾏官 瞿晓铧[Qu Xiaohua, Chairman, President and CEO of Canadian Solar (China) Investment Co., Ltd]," Xinhua, July 4, 2017.

xxxi “

瞿晓铧 [Qu Xiaohua],” SolarZoom, Accessed October 17, 2025.