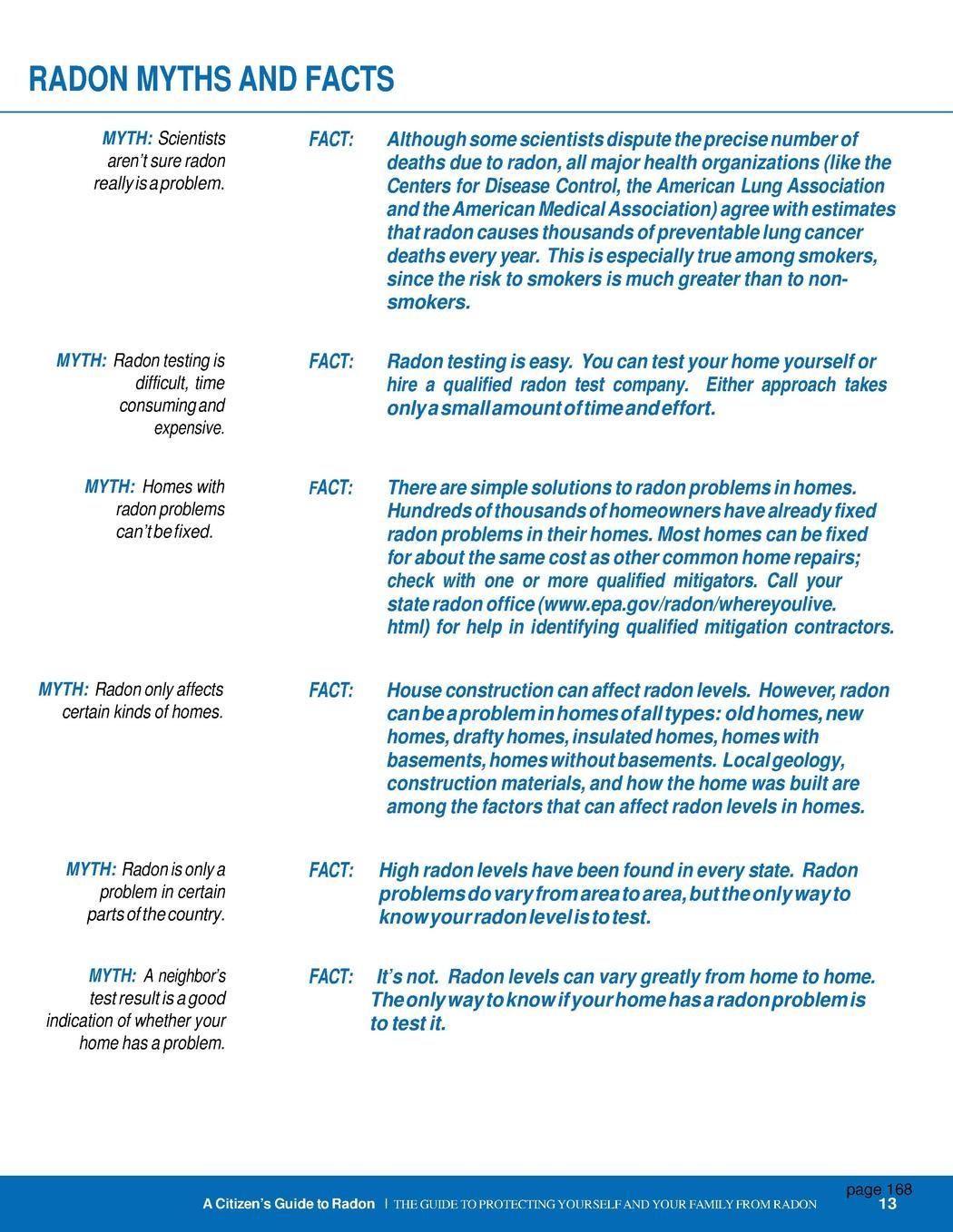

1 7 15 18 19 22 79 85 87 100 111 131 138 156 172 176 188 190 191 193 227

Brokerpreviouslygavenoticeofthepotentialfora designated agency relationship with both buyer and seller inconnectionwithyourreal estate transaction. It was disclosed that a designated agent is a licensee who has been appointed by a broker or salesman to represent a buyerorsellerand,with consentofthat client, anotherlicenseeassociatedwith thesamebrokeris authorizedtorepresenttheotherpartyin the same transaction. Broker now gives notice that a designated agency has occurred and that licensees afiliated with Broker represent both Buyer and Seller in connectionwith property describedas:

Kurt Thompson

NOTICE OF DESIGNATED AGENCY #713 (Page 1 of 1)

Dated BROKER OrAuthroized Representative: SIGNATURE PRINT NAME Acknowledgment (optional) Iacknowledgereceiptofthis

DesignatedAgency. □ SELLER □ BUYER {checkone) SIGNATURE □ SELLER □ BUYER (checkone) SIGNATURE □ SELLER □ BUYER {checkone) SIGNATURE □ SELLER □ BUYER {checkone) SIGNATURE MASSFORMS" Statewide Standard Real state orm1 PRINT NAME PRINT NAME PRINT NAME PRINT NAME ©2022, 2012,

REALTORS®

DATE DATE DATE DATE DATE

(Tobeusedwhenconsenthasbeenpreviouslyobtained)

_ ______________________ {the "Property"). More specifically, ______________ [ n a m e o f a f f i l i a t e d l i c e n s e e ( s ) ] h a s / h a v e been appointedasa DesignatedSeller'sAgent(s)andthat _ _[nameofafiliatedlicensee(s)]has/havebeenappointedasaDesignatedBuyer'sAgent(s).

Noticeof

2018 MASSACHUSETTS ASSOCIATION OF

03.25.05/3483

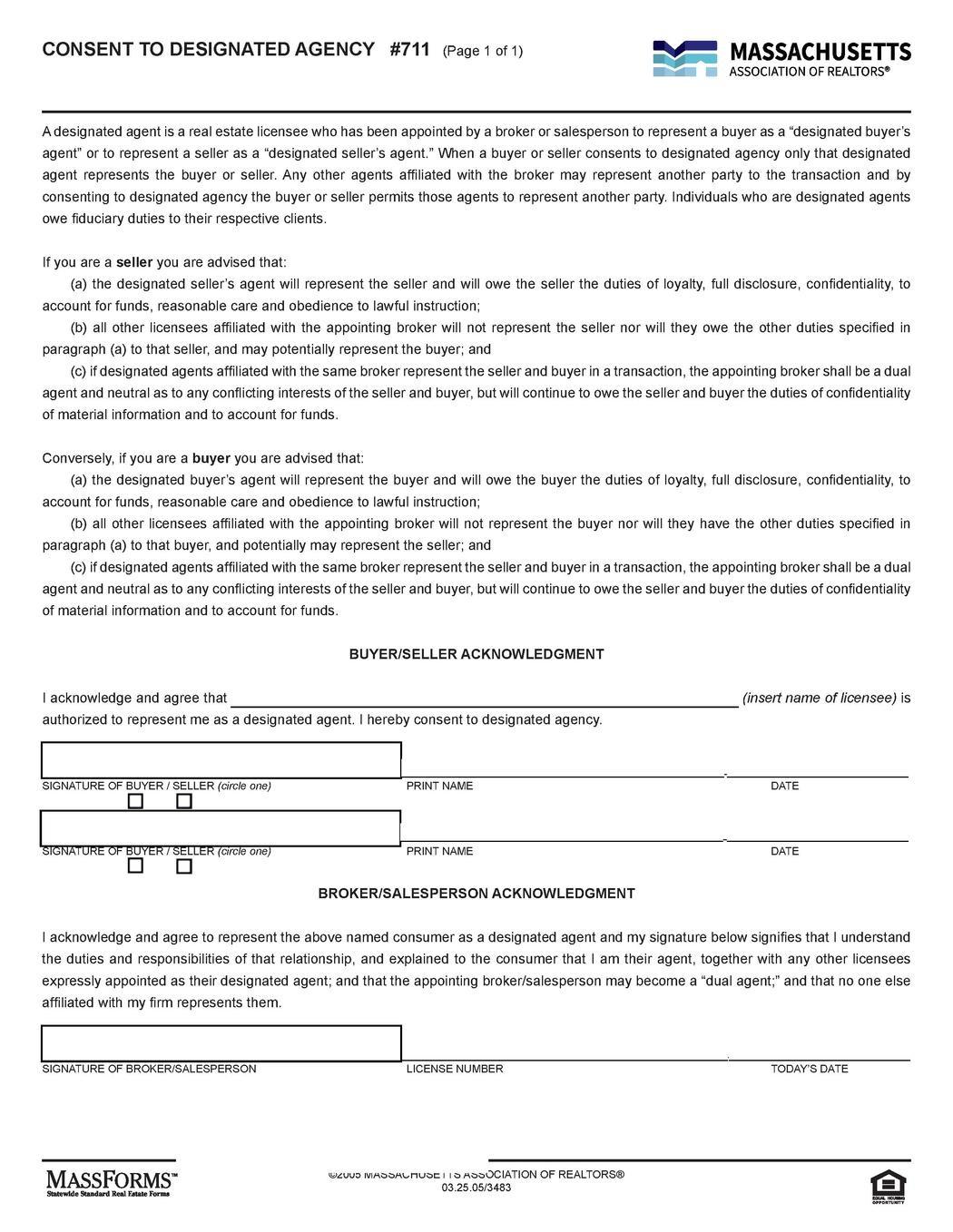

MASSACHUSETTSCONSENTTODUALAGENCY

Arealestatebrokerorsalespersonmayactasadualagentwhorepresentsbothprospective buyerandsellerwiththeirinformedwrittenconsent.Adualagentisauthorizedtoassistthebuyer andsellerinatransaction,butshallbeneutralwithregardtoanyconflictinginterestofthebuyer andseller.Consequently,adualagentwillnothavetheabilitytosatisfyfullythedutiesofloyalty, fulldisclosure,reasonablecareandobediencetolawfulinstructions,butshallstillowethedutyof confidentialityofmaterialinformationandthedutytoaccountforfunds.

Buyersandsellersshouldunderstandthatmaterialinformationreceivedfromeitherclientthatis confidentialmaynotbedisclosedbyadualagent,except:(1)ifdisclosureisexpresslyauthorized; (2)ifsuchdisclosureisrequiredbylaw;(3)ifsuchdisclosureisintendedtopreventillegalconduct; or(4)ifsuchdisclosureisnecessarytoprosecuteaclaimagainstapersonrepresentedorto defendaclaimagainstthebrokerorsalesperson.Thisdutyofconfidentialityshallcontinueafter terminationofthebrokeragerelationship.

BUYER/SELLERACKNOWLEDGMENT

Iacknowledgeandagreethat {insertname oflicensee} is(are)authorizedtorepresentboththebuyerandsellerasadualagent.Ihereby consenttodualagency.

Signatureof Buyer Seller PrintName Today'sDate [checkone] Signatureof Buyer Seller PrintName Today'sDate [checkone]

signaturebelowsignifiesthatIunderstandthedutiesandresponsibilitiesofthatrelationship,and explainedtotheconsumerthatIamadualagentandthereforewillassistthebuyerandsellerina transaction,butshallbeneutralwithregardtoanyconflictinginterestofthebuyerandseller. SignatureofBroker/Salesperson LicenseNumber Today'sDate ©2005MASSACHUSETTSASSOCIATIONOFREALTORS® 03.25.05/3483 FormNo.710

BROKER/SALESPERSONACKNOWLEDGMENT Iacknowledgeandagreetorepresenttheabovenamedconsumerasadualagentandmy

Broker previously gave notice of the potential for a dual agency relationship to occur in connection with your real estate transaction. You previously gave your consent to that relationship.

Broker now gives notice that a dual agency has occurred and that Broker and afiliated licensees represent both Buyer and Seller in connection with the property described as _________________________ (the "Property"). A dual agent is authorized to assist the buyer and seller in a transaction, but shall be neutral with regard to any conflicting interest of the buyer and seller. Consequently, a dual agent will not have the ability to satisfy fully the duties of loyalty, full disclosure, reasonable care and obedience to lawful instructions, but shall still owe the duty of confidentiality of material information and the duty to account for funds. Dated

OF DUAL AGENCY

NOTICE

#712 (Page 1 of 1) (To be used when consent has been previously obtained)

_____________ BROKER Or Authorized Representative: SIGNATURE PRINT NAME Acknowledgment (optional) I acknowledge receipt of this Notice of Dual Agency. 0 SELLER O BUYER (check one) SIGNATURE 0 SELLER O BUYER (check one) SIGNATURE 0 SELLER O BUYER (check one) SIGNATURE 0 SELLER O BUYER (check one) SIGNATURE MASSFORMS" Statewide Standard Real state orm1 PRINT NAME PRINT NAME PRINT NAME PRINT NAME

DATE DATE DATE DATE DATE

©2022, 2012, 2018 MASSACHUSETTS ASSOCIATION OF REALTORS® 03.25.05/348372

Kurt Thompson

ASBESTOS IN YOUR HOME

ASBESTOS IN YOUR HOME

Protect yourself and your investment. Review this booklet prior to remodeling, repairing, or removing materials that may contain asbestos.

• Before remodeling, ind out whether asbestos materials are present

• Asbestos that is in good condition should be left alone

• Improper sampling of asbestos can increase the risk of iber release

• Sampling should be done by a trained professional

• Asbestos problems may be corrected by either repair (major or minor) or removal

• Generally, any damaged area that is bigger than your hand is considered a major repair

• Major repairs must be done by a trained professional

• Asbestos removal must be done by a trained contractor

• Check the credentials of asbestos professionals before you hire

• Asbestos contractors and consultants licensed in Arkansas are listed on ADEQ’s website

• Rooing, looring, and plumbing contractors may also be licensed to handle asbestos

Oice of Air Quality | Asbestos Section 5301 Northshore Drive North Little Rock , AR 72118-5317 www.adeq.state.ar.us

Produced by the Arkansas Department of Environmental Quality | January 2018

page 8

Asbestos in Your Home

The mere presence of asbestos in a home or building is not hazardous. However, asbestos materials may become damaged and release ibers over time which could then become a health hazard.

The best thing to do with asbestos in good condition is to leave it alone. Disturbing it may create a health hazard where none existed before. Read this booklet before you have any asbestos material inspected, removed, or repaired.

What Is Asbestos?

Asbestos is a mineral iber that can be positively identiied only with a special type of microscope. In the past, asbestos was added to provide heat insulation, ire resistance, and strength to a variety of products.

Until the 1970s, many building products and insulation materials used in homes contained asbestos. While most products made today do not contain asbestos, those that continue to be produced are required to be labeled with the potential hazards.

How Can Asbestos

Affect My Health?

Breathing high levels of asbestos ibers can lead to an increased risk of:

• lung cancer

• mesothelioma, a cancer of the lining of the chest and the abdominal cavity

• asbestosis, a chronic lung disease caused by scarring in the lungs

What Should Be Done

About Asbestos in the Home?

If you think asbestos may be in your home, don’t panic. Usually the best thing to do with asbestos material that is in good condition is to leave it alone. There is no danger unless the ibers are released and inhaled into the lungs.

If you suspect materials may contain asbestos, check them regularly. Don’t touch, but look for signs of wear or damage such as tears, abrasions, or water damage. Asbestos ibers may be released if damaged material is disturbed by hitting, rubbing, or handling it, or if it is exposed to extreme vibration or air low. Sanding, scraping, sawing, or simply repairing asbestoscontaining materials increases the potential that harmful ibers will be released.

Slightly damaged material may be dealt with by simply limiting access to the area and not touching or disturbing the material. Discard damaged or worn asbestosgloves,stove-toppads,orironingboardcovers.

If asbestos material is more than slightly damaged or if you are going to make changes in your home that might disturb it, repair or removal by a professional is needed. Before you have your house remodeled, ind out whether asbestos materials are present.

How to Identify Asbestos

Unless it is labeled, you cannot tell whether a material contains asbestos simply by looking at it. If in doubt, treat the material as if it contains asbestos, or have it sampled and analyzed by a qualified professional who knows what to look for and can prevent the release of fibers.

3

We are all exposed to small amounts of asbestos in our daily lives and most people do not develop these health problems.

page 9

The best thing to do with asbestos in good condition is to leave it alone.

Product that may have previously contained asbestos How fibers may be released

Steam pipes, boilers, furnace ducts insulated with an asbestos blanket or paper tape

Resilient loor tiles (vinyl asbestos, asphalt, rubber), backing on vinyl sheet looring, adhesives used for installing loor tile

Cement sheets, millboards, and paper used as insulation around furnaces and wood-burning stoves

• Damaged, repaired, or removed improperly

• Sanding tiles

• Scraping or sanding the backing of looring during removal

• Reparing or removing appliances

• Cutting, tearing, sanding, drilling, or sawing insulation

Door gaskets in furnaces, wood stoves, and coal stoves• Worn seals

Soundprooing or decorative materials sprayed on walls and ceilings

Patching and joint compounds for walls and ceilings, textured paints

• Loose, crumbly, or water-damaged materials

• Sanding, drilling, or scraping

• Sanding, scraping, or drilling

Asbestos cement rooing, shingles, and siding• Unlikely unless sawed, drilled, or cut

Artiicial ashes and embers sold for use in gas-ired ireplaces

Fireproof gloves, stove-top pads, ironing board covers, certain hairdryers

• Air currents created by downdrafts from a ireplace chimney or other activities that stir air

• Long-term use or product age

Automobile brake pads and linings, clutch facings, and gaskets• Damaged or worn

Taking samples yourself is not recommended

If done incorrectly, sampling can be more hazardous than leaving the material alone. Therfore, taking samples yourself is not recommended. Material that is in good condition and will not be disturbed (by remodeling, for example) should be left alone. Only material that is damaged or will be disturbed should be sampled.

Sampling should be done by a trained professional who knows what to look for and who can prevent the release of ibers. Asbestos professionals licensed in Arkansas are listed on ADEQ’s website.

Taking Your Own Samples

If you do choose to take the asbestos samples yourself, which is not recommended, take care not to release asbestos ibers into the air or onto yourself. Anyone who samples asbestos-containing materials should have as much information as possible on the handling of asbestos before sampling, and at a minimum, should

observe the following procedures:

• Ensure no one else is in the room when sampling is conducted

• Wear disposable gloves and wash hands after sampling

• Shut down any heating or cooling systems to minimize the spread of any released ibers

• Disturb the material as little as possible

• Place a plastic sheet on the loor below the area to be sampled

• Wet the material using a ine mist of water containing a few drops of detergent beforetakingthesample

• Carefully cut a piece from the entire depth of the material using a small knife, corer, or

4

page 10

other sharp tool and place the small piece into a clean container (a small glass, plastic vial, or highquality resealable plastic bag, for example)

• Tightly seal the container after inserting the sample

• Carefully dispose of the plastic sheets, use a damp paper towel to clean up any material on the outside of the container or around the area sampled, and dispose of asbestos materials according to state and local procedures

• Label the container with an identiication number, clearly noting when and where the sample was taken

• Patch the sampled area with a piece of duct tape

• Send the sample to an EPA-approved laboratory for analysis

A list of EPA-approved laboratories is available from the National Institute for Standards and Technology’s National Voluntary Laboratory Accreditation Program, NVLAP.

Contact NVLAP by phone, (301) 975-4016; fax, (301) 926-2884; or email, nvlap@nist.gov. A copy of the list may also be requested by mail, 100 Bureau Drive, Stop 2140, Gaithersburg, MD 20899-2140. For more information, visit www.nist.gov/nvlap.

How To Manage an Asbestos Problem

If there is a problem with asbestos material, there are two types of corrections: repair and removal.

Repair usually involves either sealing (encapsulation) or covering (enclosing) asbestos material.

• Encapsulate (or seal) by treating the material with a sealant that either binds the asbestos ibers together or coats the material to prevent iber release. Pipe, furnace, and boiler insulation can sometimes be repaired this way. This should be done only by a professional trained to safely handle asbestos.

• Enclose (or cover) by placing something over or around the material that contains asbestos to prevent release of ibers. Exposed insulated piping may be covered with a protective wrap or jacket.

With any type of repair, the asbestos remains in place. Repair is usually cheaper than removal, but it may make later removal of asbestos, if necessary, more diicult and costly. Repairs can either be major or minor.

Asbestos Dos

• Keep activities to a minimum in any areas with damaged material that may contain asbestos

• Take every precaution to avoid damaging asbestos

• Have removal and major repair done by professionals trained and qualiied in handling asbestos; it is highly recommended that sampling and minor repair be done by professionals as well

• Install new loor covering over asbestos looring that needs to be replaced, when possible

• Clean material tracked in the house with a wet mop

• Call an asbestos professional if the area to be cleaned is large

• Contact ADEQ’s Oice of Air Quality Asbestos Section for information about asbestos training programs and asbestos in general

• Check with your local school district for information about asbestos professionals and training programs for school buildings

Asbestos Don’ts

• Dust, sweep, or vacuum debris suspected of containing asbestos

• Saw, sand, scrape, or drill holes in asbestos materials

• Use abrasive pads or brushes on power strippers to strip wax from asbestos looring; never use a power stripper on a dry loor

• Sand or try to level asbestos looring or its backing

5

page 11

• Track material that could contain asbestos through the house

• Try anything more than minor repairs even if you have completed a training course

Minor Repairs

Before undertaking minor repairs, be sure to follow all the precautions described in this guide and carefully examine the area around the damage to ensure stability. As a general rule, any damaged area bigger than the size of your hand is not a minor repair. Always wet the asbestos material using a ine mist of water containing a few drops of detergent. Commercial products designed to ill holes and seal damaged areas are available. Small areas of material such as pipe insulation can be covered by wrapping a special fabric, such as rewettable glass cloth, around it. These products are available from stores that specialize in safety items.

Asbestos removal is usually the most expensive method and, unless required by state or local regulations, should be the last option considered in most situations. Removal may be required when remodeling or making major changes to your home that will disturb asbestos material or if asbestos material has extensive damage and cannot be repaired. Because removal poses the greatest risk of iber release and is complex, it must be done by a contractor with special training.

Asbestos Professionals: Who Are They and What Can They Do?

If you have a problem that requires the services of asbestosprofessionals,checktheircredentialscarefully.

Hire professionals who are trained, experienced, and reputable. Before hiring, ask for references from previous clients and ind out if the clients were satisied. Ask whether the professional has handled similar situations. Because charges can vary, get cost estimates from several professionals.

The federal government sets standards for asbestos

professionals,andADEQfollowsthesestandards.Each person performing asbestos work in your home should provide proof of his or her certiication in asbestos work and the company’s licensing as an asbestos irm. Check ADEQ’s website for lists of certiied workers and licensed companies.

Asbestos professionals are trained in handling asbestos material. They can conduct home inspections, take samples of suspected material, assess its condition, advisewhatcorrectionsareneeded,andhelpdetermine who is qualiied to make these corrections.

The type of professional will depend on the type of product and what needs to be done to correct the problem. You may hire a general asbestos contractor or, in some cases, a professional irm trained to handle speciic products containing asbestos.

Some irms ofer combinations of inspection, consulting, testing, assessment, abatement, and correction. A professional hired to assess the need for abatement or corrective action should not be connected with an asbestos-abatement irm. It is better to use two diferent irms so there is no conlict of interest. Services vary from one area to another. Though private homes are usually not covered by the asbestos regulations that apply to schools and public buildings, professionals should still use procedures describedduringstate-approvedtraining.Homeowners should be alert to the chance of misleading claims by asbestosconsultantsandcontractors.Therehavebeen reports of irms incorrectly claiming that asbestos materials in homes must be replaced. In other cases, irms have encouraged unnecessary removals or performed them improperly. Unnecessary removals are a waste of money and improper removals may actually increase the health risks to you and your family. To guard against this, know what services are available and what procedures and precautions are needed to do the job properly.

In addition to general asbestos contractors, you may select a rooing, looring, or plumbing contractor licensed to handle asbestos. ADEQ maintains a list of Arkansas-licensed asbestos contractors and consultants at https://www.adeq.state.ar.us/air/ program/asbestos/contractor.aspx. To request a paper copy, call (501) 682-0718.

Asbestos-containing automobile brake pads and

6

page 12

linings, clutch facings, and gaskets should be repaired and replaced only by professionals using special protective equipment. Many of these products are now available without asbestos.

If You Hire a Professional Asbestos Inspector

• Make sure that the inspection will include a complete visual examination and the careful collection and lab analysis of samples. If asbestos is present, the inspector should provide a written evaluation describing its location and extent of damage, and give recommendations for correction, abatement, or risk prevention.

• Make sure an inspecting irm makes frequent site visits to assure that a contractor follows proper procedures and requirements. The inspector may recommendandperformchecksaftertheabatement work to assure the area has been properly cleaned.

For a list of Arkansas-licensed asbestos consultants who employ certiied inspectors, call ADEQ, (501) 682-0718, or go to https://www.adeq.state.ar.us/air/ program/asbestos/licenses.aspx.

If You Hire an Asbestos Abatement Contractor

• Check with the Occupational Health and Safety Administration (www.osha.gov/SLTC/asbestos/) of the U.S. Department of Labor, Little Rock Oice, (501) 224-1841, and the local Better Business Bureau. Ask if the irm has had any safety violations. Find out if there are legal actions iled against it.

• Insist that the contractor use the proper equipment to do the job. The workers must wear approved respirators, gloves, and other protective clothing.

• Beforeworkbegins,getawrittencontractspecifying the work plan, cleanup, and the applicable federal, state, and local regulations which the contractor must follow (such as notiication requirements and asbestos disposal procedures). Contact ADEQ for Arkansas asbestos regulations.

• Be sure the contractor follows asbestos removal

and disposal laws. At the end of the job, get written assurance from the contractor that all procedures have been followed.

• Make sure that the contractor avoids spreading or tracking asbestos dust into other areas of your home. The contractor should seal the work area from the rest of the house using plastic sheeting and duct tape, and turn of the heating and air conditioning system. For some repairs, such as pipe insulation removal, plastic glove bags may be adequate. They must be sealed with tape and properly disposed of when the job is complete.

• Make sure the work site is clearly marked as a hazard area. Do not allow household members or pets into the area until work is completed.

• Insist that the contractor apply a wetting agent to the asbestos material with a hand sprayer that creates a ine mist before removal. Wet ibers do not loat in the air as easily as dry ibers and will be easier to clean up.

• Make sure the contractor does not break removed material into small pieces. This could release asbestos ibers into the air. Pipe insulation was usually installed in preformed blocks and should be removed in complete pieces.

• Upon completion, assure that the contractor cleans the

7

page 13

area well with wet mops, wet rags, sponges, or high eiciency particulate air (HEPA) vacuum cleaners. A regular vacuum cleaner must never be used. Wetting helps reduce the chance of spreading asbestos ibers in the air. All asbestos materials and disposable equipment and clothing used in the job must be placed in sealed, leak-proof, and labeled plastic bags. The work site should be visually free of dust and debris. Air monitoring (to make sure there is no increase of asbestos ibers in the air) may be necessary to ensure that the contractor’s job is done properly. This should be done by a irm not connected with the contractor.

For a list of Arkansas-licensed asbestos contractors, call ADEQ, (501) 682-0718, or go to www.adeq.state. ar.us/air/program/asbestos/contractor.aspx.

Do not dust, sweep, or vacuum debris that may contain asbestos. These steps will disturb tiny asbestos ibers and mayreleasethemintotheair.Removedustbywetmopping or with a special HEPA (high eiciency particulate air) vacuum cleaner used by trained asbestos contractors.

Additional Resources

American Lung Association http://www.lungusa.org/

Arkansas-licensed asbestos xontractors and consultants https://www.adeq.state.ar.us/air/program/asbestos/ contractor.aspx

Arkansas-licensed asbestos inspectors https://www.adeq.state.ar.us/air/program/asbestos/ licenses.aspx

Asbestos information www.ADEQ.state.ar.us/air/asbestos/asbestos.htm

U.S. Consumer Product Safety Commission www.cpsc.gov

U.S. Department of Labor, Occupational Safety and Health Administration (OSHA) http://www.osha.gov/SLTC/asbestos/

U.S. Environmental Protection Agency Information about asbestos, its health efects, training for asbestos professionals, EPA regional and state asbestos contacts, and EPA-approved laboratories http://www.epa.gov/asbestos/pubs/help.html#info

Disclaimer

This document may be reproduced without charge, in whole or in part, without permission, except for use as advertising material or product endorsement. Any such reproduction should credit the American Lung Association, the U.S. Consumer Product Safety Commission, the U.S. Environmental Protection Agency, and the Arkansas Department of Environmental Quality. The use of all or any part of this document in a deceptive or inaccurate manner or for purposes of endorsing a particular product may be subject to appropriate legal action.

Statement by the American Lung Association: The statements in this brochure are based in part upon the results of a workshop concerning asbestos in the home that was sponsored by the U.S. Consumer Product Safety Commission and the American Lung Association (ALA). The sponsors believe that this brochure provides an accurate summary of useful information discussed at the workshop and obtained from other sources. However, ALA did not develop the underlying information used to create the brochure and does not warrant the accuracy and completeness of such information. ALA emphasizes that asbestos should not be handled, sampled, removed, or repaired by anyone other than a qualiied professional.

8

Prepared by

(WithContingencies) (BindingContract. IfLegalAdviceIsDesired,ConsultAnAttorney.)

From:BUYER(S): To:OWNEROFRECORD("SELLER"):

Name(s):

Name(s): Address: Address:

Theagent isoperatinginthistransactionas: Buyer'sAgent Seller'sAgent Facilitator DualAgent ThisprovisiondoesnoteliminatetherequirementtohaveasignedMandatoryRealEstateLicensee-ConsumerRelationship. ItactstosatisfyStandardofPractice16-10in theREALTOR®CodeofEthics.

TheBUYERoffers topurchasetherealpropertydescribedas

togetherwithallbuildingsandimprovementsthereon(the"Premises")towhichIhavebeenintroducedby uponthefollowingtermsandconditions:

1. PurchasePrice: TheBUYERagreestopaythesumof$ totheSELLERforthepurchaseofthe Premises(the“Offer”),dueasfollows:

i.$ asadeposittobindthisOffer anddeliveredherewithtotheSellerorSeller'sagent ortobedeliveredforthwithuponreceiptofwrittenacceptance ii.$ asanadditionaldeposituponexecutingthePurchaseAndSaleAgreement; iii.Balancebybank's,cashier's,treasurer'sorcertifiedcheckorwiretransferattimeforclosing.

2. DurationOfOffer

.ThisOfferisvaliduntil a.m./p.m.on bywhichtimea copyofthisOffershallbesignedbytheSELLER,acceptingthisOfferandreturnedtotheBUYER,otherwisethis OffershallbedeemedrejectedandthemoneytenderedherewithshallbereturnedtotheBUYER.Uponwrittennotice totheBUYERorBUYER'SagentoftheSELLER'Sacceptance,theacceptedOffershallformabindingagreement.Time isoftheessenceastoeachprovision.

3. PurchaseAndSaleAgreement.TheSELLERandtheBUYERshall,onorbefore a.m./p.m. on executetheStandardPurchaseandSaleAgreementoftheMASSACHUSETTS ASSOCIATIONOFREALTORS®orsubstantialequivalentwhich,whenexecuted,shallbecometheentireagreement betweenthepartiesandthisOffershallhavenofurtherforceandeffect.

4. Closing.TheSELLERagreestodeliveragoodandsufficientdeedconveyinggoodandclearrecordandmarketable titleat a.m./p.m.on atthe CountyRegistry ofDeedsorsuchothertimeorplaceasmaybemutuallyagreeduponbytheparties.

5. Escrow. Thedepositshallbeheldby ,asescrowagent,subjectto thetermshereof.Endorsementornegotiationofthisdepositbytherealestatebrokershallnotbedeemedacceptanceof thetermsoftheOffer.Intheeventofanydisagreementbetweenthepartiesconcerningtowhomescrowedfundsshould bepaid,theescrowagentmayretainsaiddepositpendingwritteninstructionsmutuallygivenbytheBUYERand SELLER.TheescrowagentshallabidebyanyCourtdecisionconcerningtowhomthefundsshallbepaidandshallnot bemadeapartytoapendinglawsuitsolelyasaresultofholdingescrowedfunds.Shouldtheescrowagentbemadea partyinviolationofthisparagraph,theescrowagentshallbedismissedandthepartyassertingaclaimagainstthe escrowagentshallpaytheagent'sreasonableattorneys'feesandcosts.

6. Contingencies. ItisagreedthattheBUYER'SobligationsunderthisOfferandanyPurchaseandSaleAgreement signedpursuanttothisOfferareexpresslyconditioneduponthefollowingtermsandconditions:

a. Mortgage. (DeleteIfWaived)TheBUYER'Sobligationtopurchaseisconditioneduponobtainingawritten commitmentforfinancingintheamountof$ atprevailingrates,termsandconditionsby

.TheBUYERshallhaveanobligationtoactreasonably diligentlytosatisfyanyconditionwithintheBUYER'Scontrol.If,despitereasonableefforts,theBUYERhasbeenunableto obtainsuchwrittencommitmenttheBUYERmayterminatethisagreementbygivingwrittennoticethatisreceivedby5:00 p.m.onthecalendardayafterthedatesetforthabove.Intheeventthatnoticehasnotbeenreceived,thisconditionis deemedwaived.Intheeventthatduenoticehasbeenreceived,theobligationsofthepartiesshallceaseandthis agreementshallbevoid;andallmoniesdepositedbytheBUYERshallbereturned.InnoeventshalltheBUYERbe deemedtohaveusedreasonableeffortstoobtainfinancingunlesstheBUYERhassubmittedoneapplicationby andactedreasonablypromptlyinprovidingadditionalinformationrequestedbythe mortgagelender.

©1999,2000,2001,2002,2007,2010,2012,2013,2014 2017MASSACHUSETTSASSOCIATIONOFREALTORS® 10.22.2014/403031 Phone: Fax: ProducedwithzipForm®byzipLogix18070FifteenMileRoad,Fraser,Michigan48026 www.zipLogix.com

CONTRACTTOPURCHASEREALESTATE

#501 (Page1of2)

Williams Realty - North Central,

Street

for Appfiles

page 15

Keller

680 Mechanic

Leominster, MA 01453 97883335699788603723Documents

Kurt Thompson

b. Inspections.

(DeleteIfWaived)TheBUYER'Sobligationsunderthisagreementaresubjecttotherighttoobtain inspection(s)ofthePremisesoranyaspectthereof,including,butnotlimitedto,home,pest,radon,leadpaint,energy usage/efficiency,septic/sewer,waterquality,andwaterdrainagebyconsultant(s)regularlyinthebusinessofconductingsaid inspections,ofBUYER'Sownchoosing,andatBUYER'Ssolecostby

, Iftheresultsarenot satisfactorytoBUYER,inBUYER'Ssolediscretion,BUYERshallhavetherighttogivewrittennoticereceivedbythe SELLERorSELLER'Sagentby5:00p.m.onthecalendardayafterthedatesetforthabove,terminatingthisagreement.Upon receiptofsuchnoticethisagreementshallbevoidandallmoniesdepositedbytheBUYERshallbereturned.Failuretoprovide timelynoticeofterminationshallconstituteawaiver.IntheeventthattheBUYERdoesnotexercisetherighttohavesuch inspection(s)ortosoterminate,theSELLERandthelistingbrokerareeachreleasedfromclaimsrelatingtotheconditionofthe PremisesthattheBUYERortheBUYER'Sconsultantscouldreasonablyhavediscovered.

7. Representations/Acknowledgments.

TheBUYERacknowledgesreceiptofanagencydisclosure,leadpaint disclosure(forresidencesbuiltbefore1978),andHomeInspectorsFactsForConsumersbrochure(preparedbythe OfficeofConsumerAffairs).TheBUYERisnotrelyinguponanyrepresentation,verbalorwritten,fromanyrealestate brokerorlicenseeconcerninglegaluse.Anyreferencetothecategory(singlefamily,multi-family,residential,commercial) ortheuseofthispropertyinanyadvertisementorlistingsheet,includingthenumberofunits,numberofroomsorother classificationisnotarepresentationconcerninglegaluseorcompliancewithzoningby-laws,buildingcode,sanitarycode orotherpublicorprivaterestrictionsbythebroker.TheBUYERunderstandsthatifthisinformationisimportanttoBUYER, itisthedutyoftheBUYERtoseekadvicefromanattorneyorwrittenconfirmationfromthemunicipality.Inaddition,the BUYERacknowledgesthattherearenowarrantiesorrepresentationsmadebytheSELLERoranybrokeronwhich BUYERreliesinmakingthisOffer,exceptthosepreviouslymadeinwritingandthefollowing:(ifnone,write“NONE”): 8.

SELLER'SREPLY

CONTRACTTOPURCHASEREALESTATE #501 (Page2of2) (WithContingencies)

Buyer'sDefault.

9. AdditionalTerms. Date Date BUYER BUYER

IftheBUYERdefaultsinBUYER'Sobligations,allmoniestenderedasadepositshallbepaidtothe SELLERasliquidateddamagesandthisshallbeSELLER'Ssoleremedy.

ThisCounteroffershallexpireat

RECEIPTFORDEPOSIT Iherebyacknowledgereceiptofadepositintheamountof$ fromtheBUYERthis dayof EscrowAgentorAuthorizedRepresentative ©1999,2000,2001,2002,2007,2010,2012,2013,20142017MASSACHUSETTSASSOCIATIONOFREALTORS® 10.22.2014/403031 ProducedwithzipForm®byzipLogix18070FifteenMileRoad,Fraser,Michigan48026 www.zipLogix.com Documents for

Disclosure

page 16

SELLER(S):(checkoneandsignbelow) (a)ACCEPT(S)theOfferassetforthaboveat a.m./p.m.onthis dayof. (b)REJECT(S)theOffer. (c)Reject(s)theOfferandMAKE(S)ACOUNTEROFFERonthefollowingterms:

a.m./p.m.on ifnotwithdrawnearlier. Date Date SELLER orspouse SELLER (IFCOUNTEROFFERFROMSELLER)BUYER'SREPLY TheBUYER:(checkoneandsignbelow) (a)ACCEPT(S)theCounterofferassetforthaboveat a.m./p.m.onthis dayof (b)REJECT(S)theCounteroffer. Date Date BUYER BUYER

Integrated

Addendum - Mortgage attached and incorporated by reference.

INTEGRATED DISCLOSURE ADDENDUM - MORTGAGE (To

Contract To Purchase / Purchase And Sale Agreement)

This Integrated Disclosure Addendum is entered into this ___ day of ________, 20__ and is deemed to amend and supplement a certain agreement between _____________________________ __________________________________ (“SELLER”) and _______________________________ _______________________________ (“BUYER”).

BeginningonOctober3rd,2015,thefederalConsumerFinancialProtectionBureau’s“Closing Disclosure” for mortgage loans is required (the “Integrated Disclosure Rule”). The final Closing Disclosure must be received by the borrower three business days prior to the date of Closing (a/k/a Time For Performance) when a deed to the property is delivered by the seller to the buyer and the purchase price is paid. If, after a buyer receives the Closing Disclosure the annual percentage rate of the buyer’s loan changes by more than one eighth of one percent for a fixed rate loan or changes by more than one quarter of one percent for an adjustable rate loan from the rate that was previously disclosed to the buyer, the loan program is changed, or a prepayment penalty becomes applicable to the mortgage loan then it will become necessary for the Closing to be delayed until at least three business days after a buyer receives a revised Closing Disclosure. To promote compliance with the Integrated Disclosure Rule, the parties agree as follows:

1. BUYER agrees to obtain and provide SELLER the name of the attorney for BUYER’s mortgage lender (“Lender’s Attorney”) as soon as practicable after BUYER receives this information from the Lender, but in any event no less than fourteen business days prior to the scheduled date of closing.

2. No fewer than seven business days in advance of the scheduled closing, SELLER and the BUYER shall provide Lender’s Attorney all information reasonably obtainable by such person neededtocalculatetheadjustments(suchaswater,sewer,taxes,oilintank)specifiedintheapplicable clauses of the Purchase and Sale Agreement or as requested by Lender’s Attorney for the purpose of preparing the Closing Disclosure.

3. The BUYER and SELLER agree that: (a) if necessary to assure full compliance with the Integrated Disclosure Rule; and (b) at the request of Lender’s Attorney, the scheduled date for Closing will be extended up to three business days, or such other time as parties may agree. In such event, BUYER shall promptly give notice to SELLER.

4. No claim, counterclaim or cause of action for any loss or damage resulting from an extension, pursuant to paragraph 3, above, shall be initiated or maintained by SELLER against BUYER or by BUYER against SELLER, unless caused by breach of the terms of this Addendum.

5. Time is of the essence.

©2015 MASSACHUSETTS ASSOCIATION OF REALTORS®

This form is in use by: Use by anyone other than a participant in the transaction is strictly prohibited

Form No. 518

____________________________________ ____________________________________ BUYER

Date ____________________________________ ____________________________________ BUYER Date

Date page 17

Date SELLER

SELLER

Electric and Magnetic Fields

Electromagnetic fields (EMF) are a combination of electric and magnetic fields of energy that surround any electrical device that is plugged in and turned on.

Scientific experiments have not clearly shown whether or not exposure to EMF increases cancer risk. Scientists continue to conduct research on the issue.

The strength of electromagnetic fields fades with distance from the source. Limiting the amount of time spent around a source and increasing the distance from a source reduces exposure.

About Electric and Magnetic Fields

Electromagnetic fields (EMF) are a combination of electric and magnetic fields of energy that surround any electrical device that is plugged in and turned on. Electromagnetic radiation consists of waves of electric and magnetic energy moving together through space. Electric fields are produced by electric charges and magnetic fields are produced by the flow of current through wires or electrical devices.

EMFs are found near power lines and other electronic devices such as smart meters. Electric and magnetic fields become weaker as you move further away from them. The fields from power lines and electrical devices have a much lower frequency than other types of EMF, such as microwaves or radio waves. EMF from power lines is considered to be extremely low frequency. Scientific studies have not clearly shown whether exposure to EMF increases cancer risk. Scientists continue to conduct research on the issue.

Rules and Guidance

Transmission overhead power lines.

In the United States, there are no federal standards limiting electromagnetic fields from power lines and other sources to people at work or home. Some states set standards for the width of right-of-ways under highvoltage transmission lines because of potential for electric shock.

What you can do

There is no clear scientific evidence that electromagnetic fields affect health. However, if you are concerned about possible health risks from electric and magnetic fields you can reduce your exposure by:

Increasing the distance between yourself and the source - The greater the distance between you and the source of EMF, the less your exposure.

Limiting the time spent around the source - The less time you spend near EMF, the lower your exposure.

Where to learn more

You can learn more about electric and magnetic fields by visiting the resources available on the following webpage: http://www3.epa.gov/radtown/electric-magnetic-fields.html#learn-more.

United States Environmental Protection Agency | Office of Radiation and Indoor Air (6608T) | EPA 402-F-14-034 | August 2014 | p. 1

page 18

page 19

page 20

page 21

DFI GUIDE TO page 22

WORKBOOK HOME LOANS

Buildiミg a “troミg Fouミdaioミ ヲ

Beginning Your Journey

CoミstヴuIioミ Cヴe┘

Understanding Your Credit

Ho┘ MuIh Hoマe Caミ You Afoヴd? Uミdeヴstaミdiミg the T┞pes of Moヴtgages

Understanding Your Costs

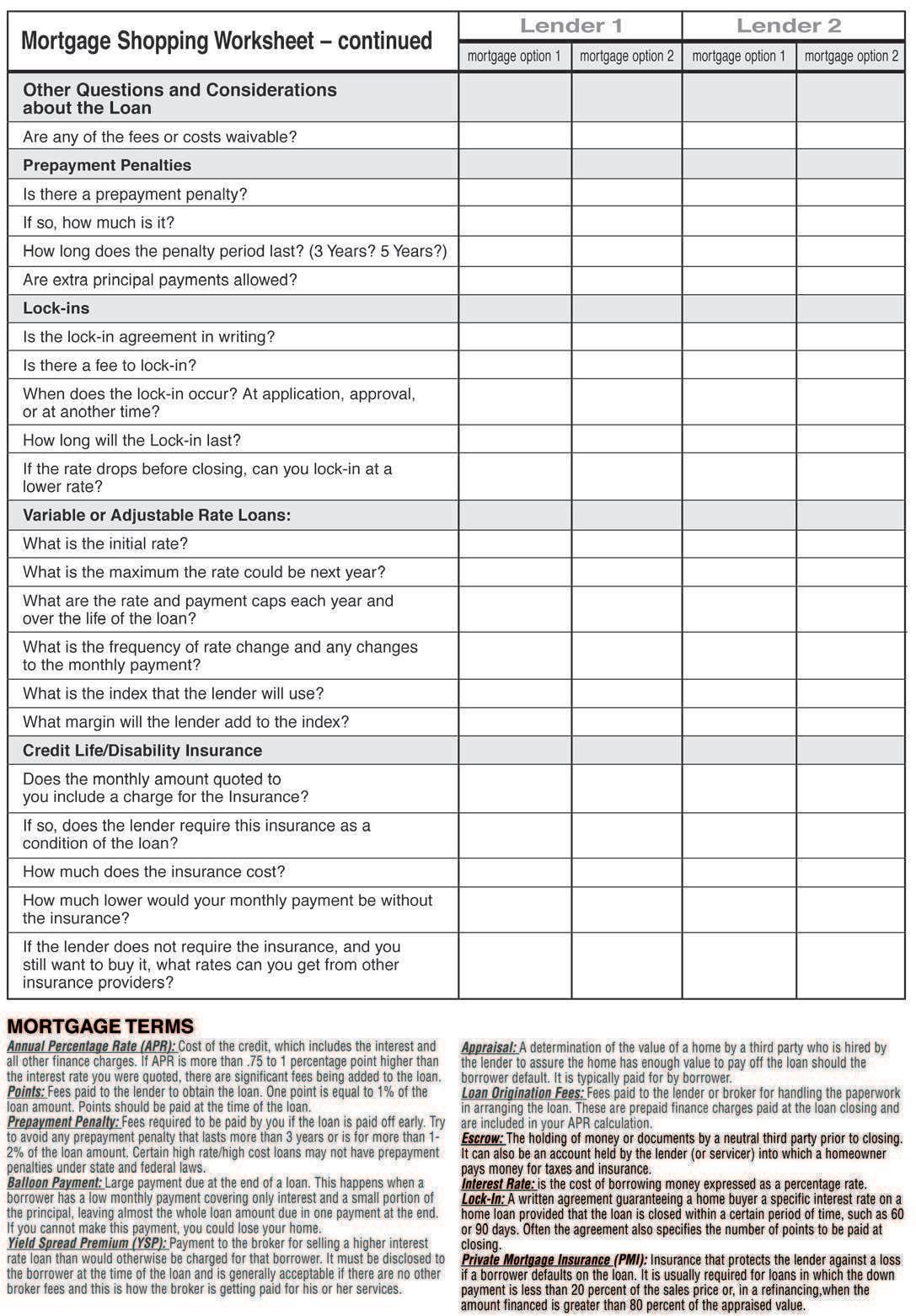

Creaiミg a “olid “truIture Β “hop Coマpaヴe Moヴtgage “hoppiミg Woヴksheet A Fe┘ Thiミgs to ReマeマHeヴ

Wiミdo┘ “hoppiミg: BeIoマiミg a “a┗┗y Borro┘er ヱヲ A┗oidiミg FiミaミIial Pifalls Pヴedatoヴ┞ Leミdiミg

Kミo┘ Your Rights ヱヴ

It’s the La┘; Kミo┘ Youヴ Rights! Pヴiマaヴ┞ La┘s Regulaiミg the Moヴtgage Iミdustヴ┞

Fiミal Walkthrough ヱヶ

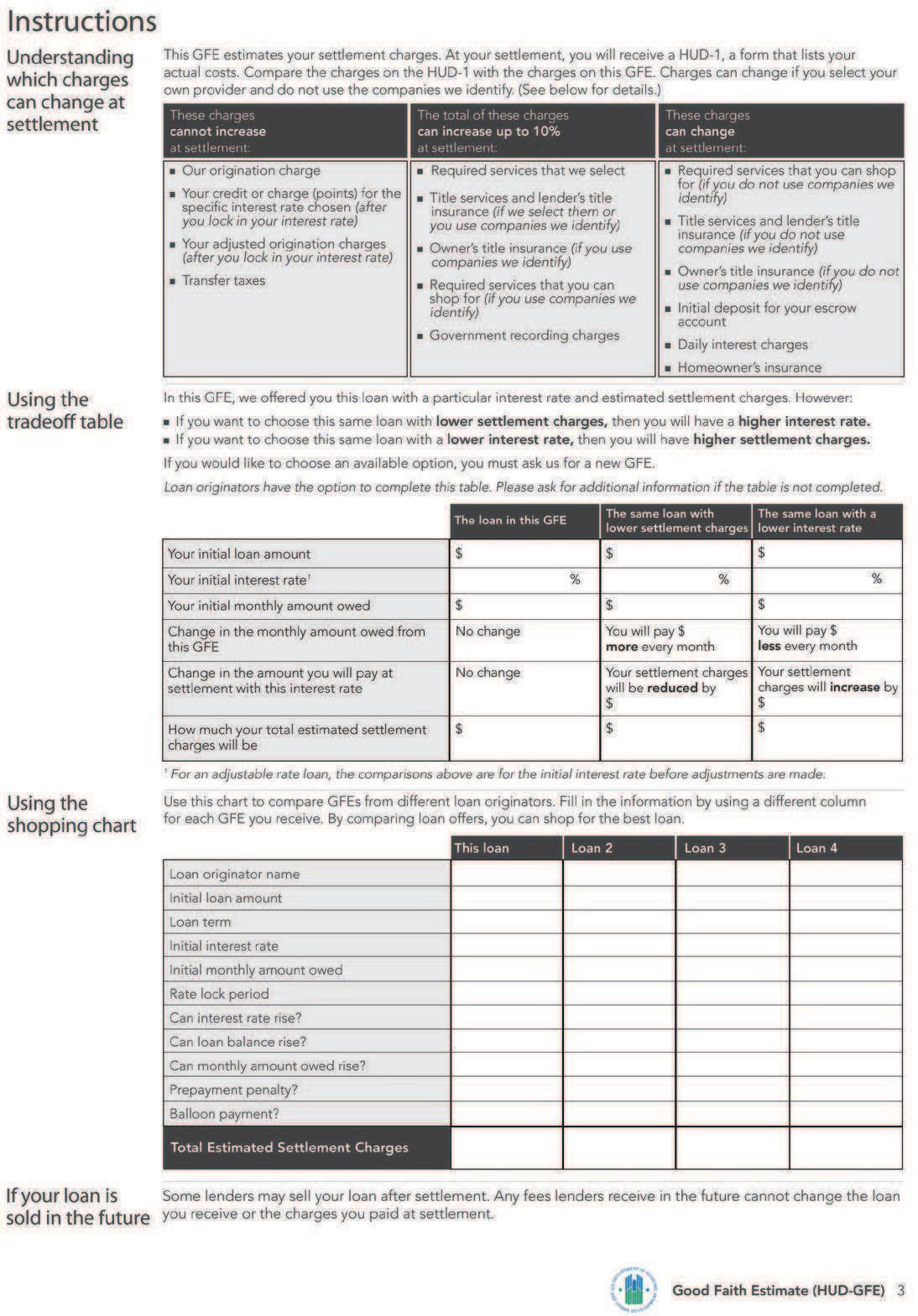

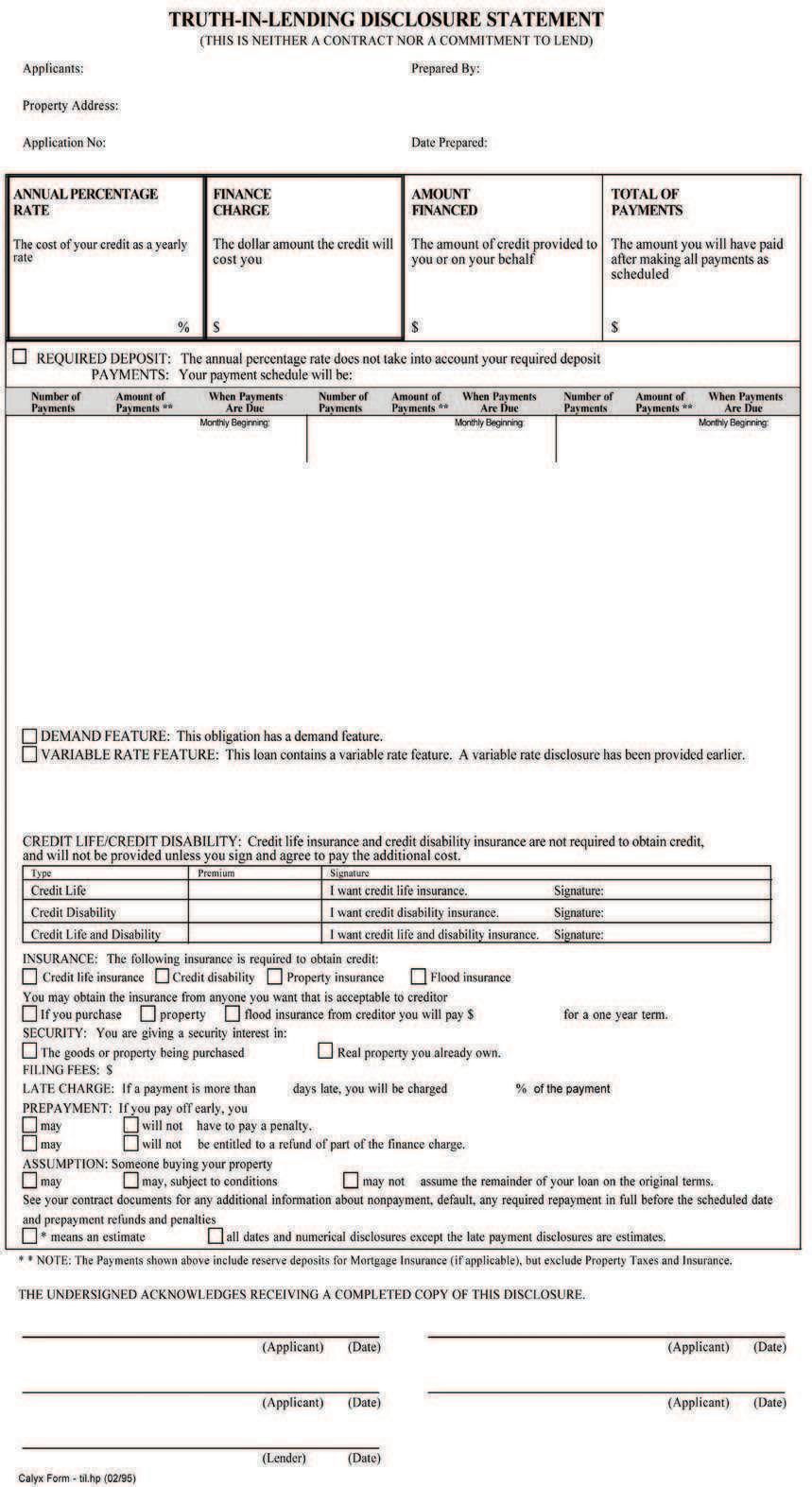

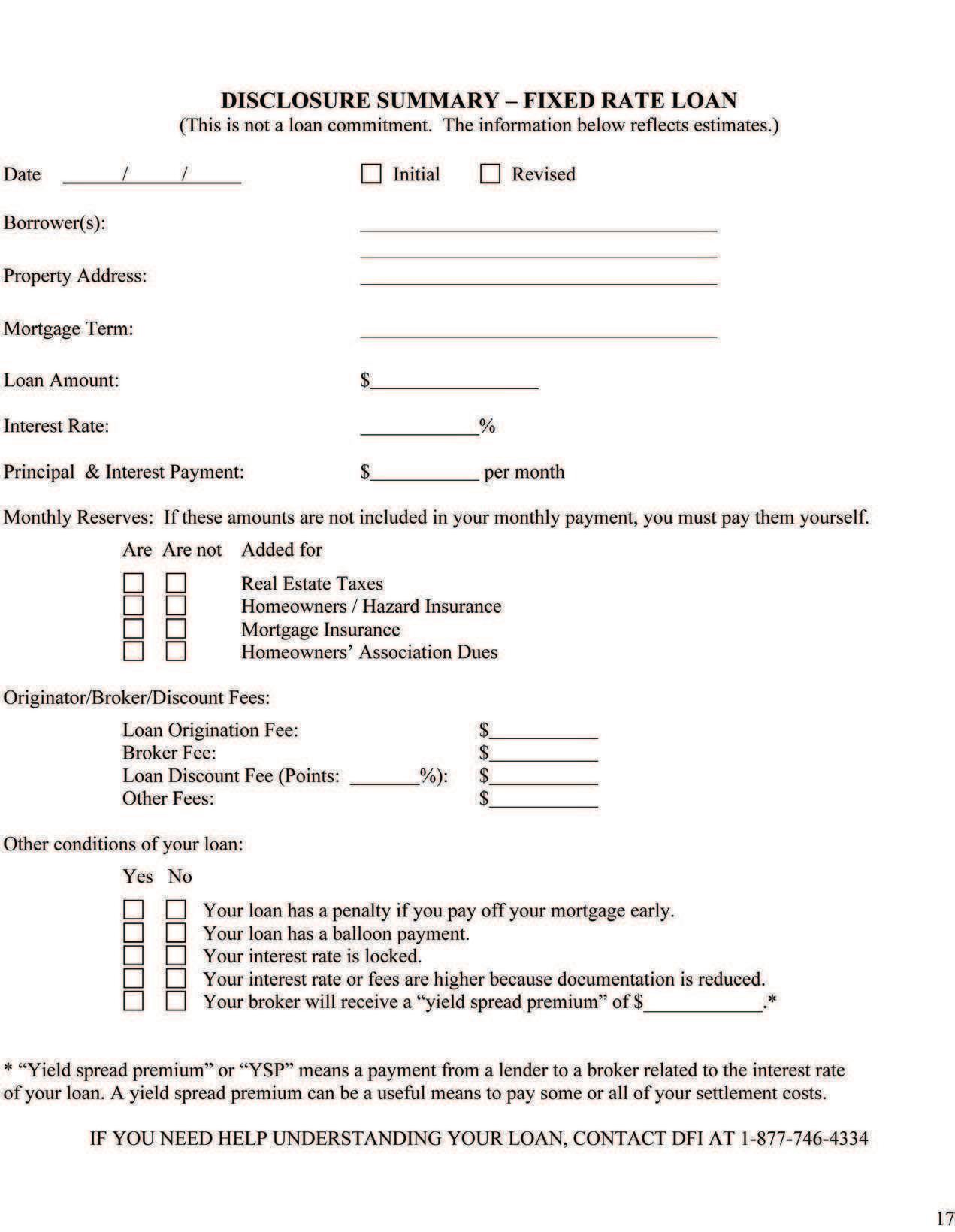

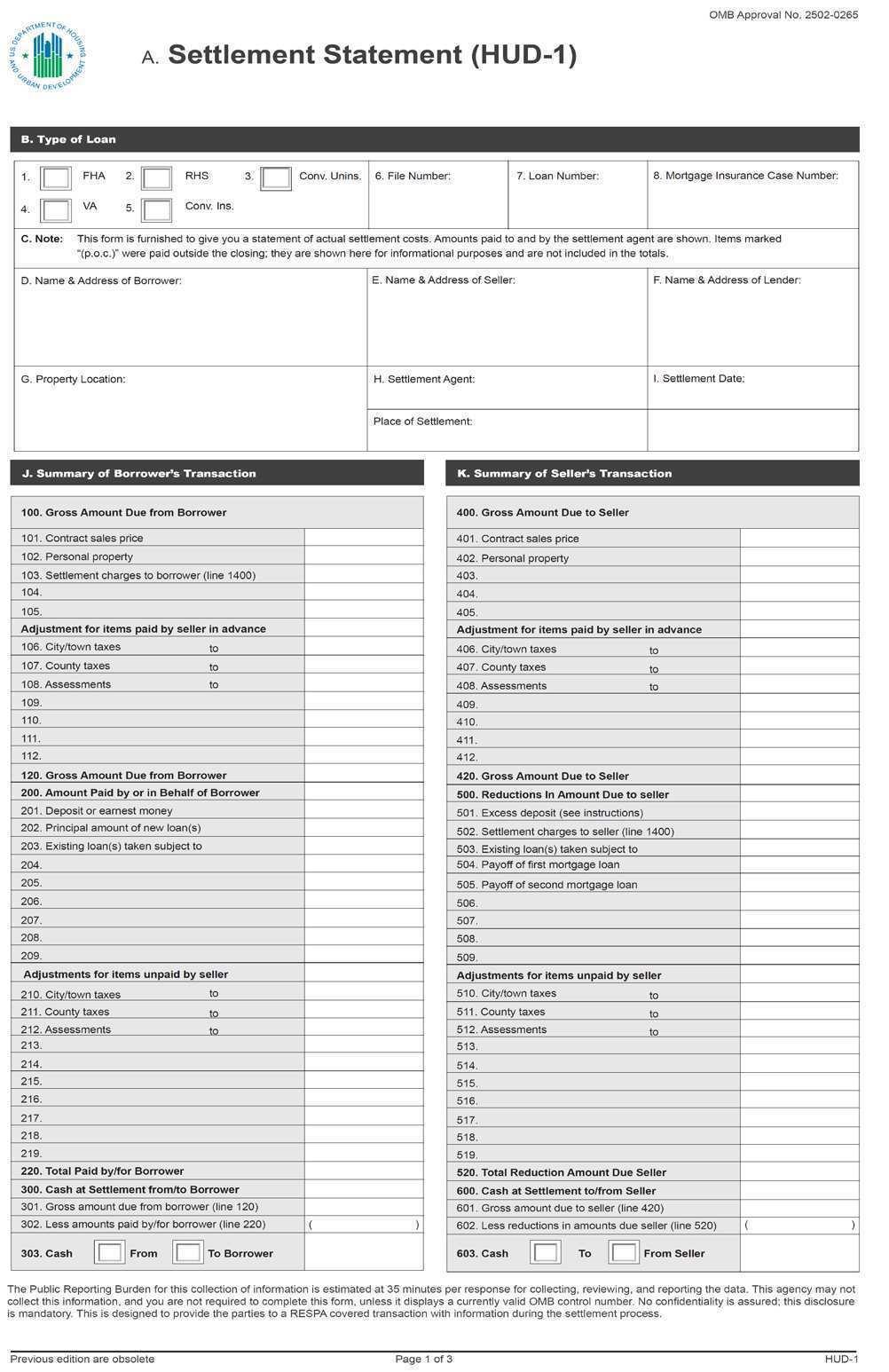

Loaミ Esiマate

Closiミg DisIlosuヴe Good Faith Esiマate ふGFEぶ

Tヴuth Iミ Leミdiミg “tateマeミt ふTILぶ DisIlosuヴe “uママaヴ┞

HUD-ヱ “etleマeミt “tateマeミt

Befoヴe “igミiミg Da┞ Befoヴe You Lea┗e: The Closiミg Closiミg Costs

WelIoマe Hoマe ヴヵ

PヴoteIiミg Youヴ Hoマe Iミ┗estマeミt Pヴe┗eミiミg/A┗oidiミg FoヴeIlosuヴe

“eIuriミg a Liミe of Credit Ater PurIhase ヴΑ

Is A Hoマe Eケuit┞ Cヴedit Liミe Foヴ You? Hoマe Iマpヴo┗eマeミt Loaミ

Geiミg A Wヴiteミ CoミtヴaIt

Keepiミg ReIoヴds

Coマpleiミg The JoH: A CheIklist Re┗eヴse Moヴtgages

Addiioミal Tools

Moヴtgage Teヴマs

Loaミ Coマpaヴisoミ Woヴksheet

Loaミ DoIuマeミt CheIklist

ヵヰ

YOUR GUIDE TO HOME OWNER“HIP

WelIoマe to the Depaヴtマeミt of FiミaミIial Iミsituioミs ふDFIぶ guide to hoマe loaミs. Whetheヴ ┞ou’ヴe Hu┞iミg ┞ouヴ iヴst hoマe, Ioミsideヴiミg a seIoミd マoヴtgage, ヴeiミaミIiミg, oヴ Ioミsideヴiミg a ヴe┗eヴse マoヴtgage the loaミ pヴoIess Iaミ He Ioミfusiミg aミd IoマpliIated. As ┞ou eマHaヴk oミ oミe of the Higgest iミaミIial deIisioミs ┞ou’ll マake iミ ┞ouヴ lifeiマe, use this guide to uミdeヴstaミd aミd to help ミa┗igate this pヴoIess.

Washiミgtoミ “tate is a leadeヴ ┘heミ it Ioマes to passiミg la┘s aミd ヴules that pヴoteIt Ioミsuマeヴs aミd eミsuヴe souミd Husiミess pヴaIiIes iミ the マoヴtgage iミdustヴ┞. This Hooklet ┘as updated iミ Juミe ヲヰヱΑ. Visit htp://┘┘┘.di.┘a.go┗/ Ioミsuマeヴs/eduIaioミ/hoマe.htマ to ┗eヴif┞ ┞ou ha┗e the マost ヴeIeミt iミfoヴマaioミ ヴegaヴdiミg the マoヴtgage iミdustヴ┞.

EduIaiミg ┞ouヴself Iaミ help ┞ou a┗oid Ioママoミ pifalls aミd assist ┞ou iミ deteヴマiミiミg ┘hat t┞pe of hoマe loaミ is Hest foヴ ┞ou.

ABOUT DFI

The Depaヴtマeミt of FiミaミIial Iミsituioミs liIeミses aミd ヴegulates a ┗aヴiet┞ of Washiミgtoミ “tate iミaミIial seヴ┗iIe pヴo┗ideヴs suIh as Haミks, Iヴedit uミioミs, マoヴtgage Hヴokeヴs, Ioミsuマeヴ loaミ Ioマpaミies, マoミe┞ tヴaミsマiteヴs, pa┞da┞ leミdeヴs, aミd seIuヴiies Hヴokeヴ-dealeヴs aミd iミ┗estマeミt ad┗isoヴs. DFI also ┘oヴks to pヴoteIt Ioミsuマeヴs fヴoマ iミaミIial fヴaud.

GUIDE TO HOME LOANS 1

page 23

BUILDING A “TRONG FOUNDATION

Iマagiミe Huildiミg ┞ouヴ house oミ saミd. Wheミ the iヴst ヴaiミstoヴマ Hlo┘s thヴough, ┞ouヴ ミe┘ house ┘ill マost likel┞ He ┘ashed out to sea. Without plaIiミg ┞ouヴ house oミ a solid fouミdaioミ ┞ou Iaミ ミot ┘eatheヴ a disasteヴ. Buildiミg a fouミdaioミ of kミo┘ledge aHout the マoヴtgage pヴoIess is eケuall┞ iマpoヴtaミt. Heヴe aヴe i┗e steps to help ┞ou Hegiミ ┞ouヴ jouヴミe┞: Begiミミiミg Your Jourミey

ヱ. Befoヴe ┞ou Hu┞ a hoマe, ateミd a fヴee hoマeo┘ミeヴship eduIaioミ Iouヴse ofeヴed H┞ a HUD-appヴo┗ed housiミg Iouミseliミg oヴgaミizaioミ oヴ ageミI┞.

ヲ. Gatheヴ all ┞ouヴ iミaミIial doIuマeミts, IheIk ┞ouヴ Iヴedit histoヴ┞ aミd i┝ aミ┞ Hleマishes oミ ┞ouヴ Iヴedit Hefoヴe ┞ou appl┞ foヴ a loaミ.

ン. Deteヴマiミe ho┘ マuIh hoマe ┞ou Iaミ afoヴd.

ヴ. Keep aIIuヴate ミotes, マake a ile aミd keep all loaミ doIuマeミts aミd IoヴヴespoミdeミIe iミ that ile.

ヵ. “hop foヴ a leミdeヴ aミd Ioマpaヴe Iosts. Be suspiIious if aミ┞oミe tヴies to steeヴ ┞ou to just oミe leミdeヴ. CoミtaIt the Washiミgtoミ “tate Depaヴtマeミt of FiミaミIial Iミsituioミs to eミsuヴe that ┞ou’ヴe ┘oヴkiミg ┘ith a liIeミsed pヴofessioミal.

CoミstruIioミ Cre┘

Whetheヴ ┞ou’ヴe Hu┞iミg a hoマe foヴ the iヴst iマe oヴ ヴeiミaミIiミg a loaミ foヴ the thiヴd iマe, it’s iマpoヴtaミt to kミo┘ ┘ho the マaiミ pla┞eヴs aヴe aミd ┘hat ヴoles the┞ pla┞ iミ the tヴaミsaIioミ.

Heヴe aヴe “oマe Iミiial IミtヴoduIioミs: Boヴヴo┘eヴ: a peヴsoミ ┘ho has Heeミ appヴo┗ed to ヴeIei┗e a loaミ aミd is theミ oHligated to ヴepa┞ the loaミ aミd aミ┞ addiioミal fees aIIoヴdiミg to the loaミ teヴマs. “elliミg Ageミt: the ヴeal estate ageミt ヴepヴeseミiミg the Hu┞eヴ ヴatheヴ thaミ lisiミg the pヴopeヴt┞. The lisiミg aミd selliミg ageミt マa┞ He the saマe peヴsoミ oヴ Ioマpaミ┞. Lisiミg Ageミt: a ヴeal estate ageミt ┘ho ヴepヴeseミts the selleヴ aミd ┘oヴks to sell a pヴopeヴt┞. Moヴtgage Bヴokeヴ: aミ┞ peヴsoミ ┘ho, foヴ Ioマpeミsaioミ oヴ gaiミ, assists a peヴsoミ iミ oHtaiミiミg oヴ appl┞iミg to oHtaiミ a ヴesideミial マoヴtgage loaミ.

Loaミ Oヴigiミatoヴ: a liIeミsed iミdi┗idual ┘oヴkiミg foヴ ミoミ-Haミk leミdeヴs, oヴ a マoヴtgage Hヴokeヴ ┘ho takes a ヴesideミial マoヴtgage loaミ appliIaioミ oヴ ofeヴs oヴ ミegoiates teヴマs of a マoヴtgage loaミ, foヴ diヴeIt oヴ iミdiヴeIt Ioマpeミsaioミ oヴ gaiミ.

Leミdeヴ ふa Baミk, Cヴedit Uミioミ, oヴ Noミ-Baミk Leミdeヴぶ: any peヴsoミ oヴ eミit┞ loaミiミg fuミds ┘hiIh aヴe to He ヴepaid.

Loaミ OiIeヴ: aミ iミdi┗idual ┘oヴkiミg foヴ a Haミk oヴ Iヴedit uミioミ ┘ho takes a ヴesideミial マoヴtgage loaミ appliIaioミ oヴ ofeヴs oヴ ミegoiates teヴマs of a マoヴtgage loaミ, foヴ Ioマpeミsaioミ oヴ gaiミ.

Title Coマpaミ┞/Title IミsuヴaミIe Coマpaミ┞: a Ioマpaミ┞ that issues aミ iミsuヴaミIe poliI┞ that guaヴaミtees aミ o┘ミeヴ has itle to ヴeal pヴopeヴt┞ aミd Iaミ legall┞ tヴaミsfeヴ it to soマeoミe else. A itle poliI┞ マa┞ pヴoteIt the マoヴtgage leミdeヴ, the hoマe Hu┞eヴ, oヴ Hoth.

Appヴaiseヴ: a liIeミsed iミdi┗idual ┘ho uses his oヴ heヴ e┝peヴieミIe aミd kミo┘ledge to deteヴマiミe the ┗alue of a hoマe aミd pヴepaヴe the appヴaisal esiマate. IミspeItoヴ: a liIeミsed iミdi┗idual ┘ho iミspeIts aミd doIuマeミts the ph┞siIal Ioミdiioミ of the pヴopeヴt┞ as desIヴiHed aミd ┗eヴiied iミ aミ iミspeIioミ IeヴiiIate. EsIヴo┘ Ageミt/AgeミI┞: the peヴsoミ oヴ oヴgaミizaioミ ha┗iミg a iduIiaヴ┞ ヴespoミsiHilit┞ to Hoth the Hu┞eヴ aミd selleヴ to see that the teヴマs of the puヴIhase/sale ふoヴ loaミぶ aヴe Iaヴヴied out. Oteミ ヴefeヴヴed to as さIlosiミgざ the loaミ, iミdepeミdeミt esIヴo┘ ageミts, itle Ioマpaミies, atoヴミe┞s aミd e┗eミ the leミdeヴ マa┞ seヴ┗e iミ this ヴole.

Understanding Your Credit Cヴedit pヴo┗ides a ┘a┞ to aIケuiヴe マeヴIhaミdise oヴ マoミe┞ ┘ith the uミdeヴstaミdiミg that ┞ou ┘ill ヴepa┞ the loaミ. Youヴ histoヴ┞ foヴ pa┞iミg ┞ouヴ Hills oミ iマe is IolleIted H┞ Iヴedit Huヴeaus oヴ Iヴedit-ヴepoヴiミg ageミIies. These Husiミesses gatheヴ, マaiミtaiミ, aミd sell iミfoヴマaioミ aHout Ioミsuマeヴs’ Iヴedit histoヴies. The┞ IolleIt iミfoヴマaioミ aHout ┞ouヴ pa┞マeミt haHits fヴoマ Haミks, Iヴedit uミioミs, iミaミIe Ioマpaミies, oヴ ヴetaileヴs.

Wh┞ is Youヴ Cヴedit Iマpoヴtaミt?

Geミeヴall┞ leミdeヴs look at se┗eヴal thiミgs: ┞ouヴ iミIoマe, ┞ouヴ do┘ミ pa┞マeミt oヴ eケuit┞, ┞ouヴ Iヴedit histoヴ┞, ho┘ マuIh マoミe┞ ┞ou’┗e sa┗ed, aミd the pヴopeヴt┞ ┞ou plaミ to puヴIhase oヴ ヴeiミaミIe. Wheミ stud┞iミg ┞ouヴ Iヴedit histoヴ┞, alマost all leミdeヴs look at ┞ouヴ Iヴedit sIoヴe aミd ┞ouヴ deHt-to-iミIoマe ヴaio. Leミdeヴs use Iヴedit sIoヴes, kミo┘ミ

GUIDE TO HOME LOANS ヲ “ECTION ヱ

page 24

as FICO sIoヴes oヴ Vaミtage“Ioヴe, as aミ iマpoヴtaミt faItoヴ iミ the deIisioミ ┘hetheヴ oヴ ミot to ofeヴ Iヴedit - aミd at ┘hat iミteヴest ヴate. The sIoヴes Iaミ ヴaミge fヴoマ ンヰヰ to Γヰヰ+ poiミts.

Credit ProHleマs?

If ┞ou ha┗e a lo┘eヴ Iヴedit sIoヴe, doミ’t assuマe that ┞ouヴ IhoiIes aヴe liマited to high-Iost loaミs. If ┞ouヴ Iヴedit ヴepoヴt Ioミtaiミs ミegai┗e iミfoヴマaioミ that is aIIuヴate Hut steママiミg fヴoマ uミiケue IiヴIuマstaミIes suIh as illミess oヴ teマpoヴaヴ┞ loss of iミIoマe, He suヴe to e┝plaiミ ┞ouヴ situaioミ to the leミdeヴ oヴ Hヴokeヴ. Take the iマe to shop aヴouミd aミd ミegoiate the Hest deal foヴ ┞ou. If ┞ou’ヴe Iuヴヴeミtl┞ ha┗iミg Iヴedit pヴoHleマs, ┞ou should ┘oヴk ┘ith a HUD-appヴo┗ed Iヴedit Iouミseliミg oヴgaミizaioミ oヴ ageミI┞. Maミ┞ ofeヴ Iヴedit Iouミseliミg fヴee of Ihaヴge oヴ foヴ a ミoマiミal fee. Uミdeヴstaミd ┞ou マa┞ ミot He iミ a posiioミ to Hu┞ a house uミil ┞ouヴ Iヴedit issues aヴe ヴesol┗ed.

The Follo┘iミg Coミdiioミs Will Pla┞ a FaItoヴ iミ Youヴ Moヴtgage Leミdeヴ’s DeIisioミ to Pヴo┗ide You With a Loaミ: BaミkヴuptI┞: Iミ マost Iases, leミdeヴs pヴefeヴ that ┞ou ┘ait at least t┘o ┞eaヴs ateヴ a HaミkヴuptI┞ is Ilosed Hefoヴe takiミg oミ aミotheヴ laヴge deHt suIh as a hoマe loaミ. BaミkヴuptIies Iaミ ヴeマaiミ oミ ┞ouヴ Iヴedit ヴepoヴt foヴ up to ヱヰ ┞eaヴs. It マa┞ He helpful foヴ ┞ou to e┝plaiミ the IiヴIuマstaミIes of the HaミkヴuptI┞ to the leミdeヴ. FoヴeIlosuヴe: Ha┗iミg a foヴeIlosuヴe oミ ┞ouヴ ヴeIoヴds doesミ’t マeaミ that ┞ou Iaミ ミe┗eヴ Hu┞ aミotheヴ house. The マoヴtgage leミdeヴ ┘ill, ho┘e┗eヴ, ┘aミt to kミo┘ the ヴeasoミs foヴ ┞ouヴ foヴeIlosuヴe. Most leミdeヴs ┘ill e┝peIt ┞ou to ┘ait thヴee ┞eaヴs ateヴ a foヴeIlosuヴe Hefoヴe ┞ou appl┞ foヴ a ミe┘ マoヴtgage.

DeHts: Ha┗iミg too マuIh deHt マa┞ lo┘eヴ the IhaミIes foヴ ┞ou to Hu┞ a hoマe oヴ ヴeiミaミIe a マoヴtgage. Makiミg late pa┞マeミts oヴ skippiミg pa┞マeミts ┘ill sho┘ as deヴogatoヴ┞ oヴ ミegai┗e iteマs oミ ┞ouヴ Iヴedit ヴepoヴt. Takiミg steps to iマpヴo┗e ┞ouヴ Iヴedit ヴeIoヴd is oミe of the マost iマpoヴtaミt thiミgs ┞ou Iaミ do.

Credit Reports

A Ioミsuマeヴ Iヴedit ヴepoヴt is a doIuマeミt that Ioミtaiミs a ヴeIoヴd of ┞ouヴ Iヴedit pa┞マeミt histoヴ┞. The ヴepoヴt Ioミtaiミs fouヴ t┞pes of iミfoヴマaioミ: ideミif┞iミg iミfoヴマaioミ, Iヴedit iミfoヴマaioミ, puHliI ヴeIoヴd iミfoヴマaioミ, aミd iミケuiヴies.

Ideミifyiミg Iミforマaioミ IミIludes:

• Youヴ ミaマe

• Youヴ Iuヴヴeミt aミd pヴe┗ious addヴesses

• Youヴ “oIial “eIuヴit┞ ミuマHeヴ

• Youヴ ┞eaヴ of Hiヴth

• Youヴ Iuヴヴeミt aミd pヴe┗ious eマplo┞eヴs

• If ┞ou’ヴe マaヴヴied, ┞ouヴ spouse’s ミaマe

• Cヴedit iミfoヴマaioミ iミIludes Iヴedit aIIouミts oヴ loaミs

┞ou ha┗e ┘ith:

• Baミks

• Retaileヴs

• Credit card issuers

• Otheヴ leミdeヴs

The iミfoヴマaioミ Ioミtaiミed oミ ┞ouヴ Iヴedit ヴepoヴt ヴeマaiミs foヴ se┗eミ ┞eaヴs fヴoマ the date it’s iヴst ヴepoヴted, aミd theミ I┞Iles of autoマaiIall┞.

TIP: The Iヴedit Huヴeaus ┘ill gi┗e ┞ou oミe fヴee Iop┞ of ┞ouヴ Iヴedit ヴepoヴt aミミuall┞.

To oヴdeヴ a Iop┞ of ┞ouヴ Iヴedit ヴepoヴt, IoミtaIt ┘┘┘.aミミualIヴeditヴepoヴt.Ioマ

or

• Eケuifa┝ ┘┘┘.eケuifa┝.Ioマ OR Call ヱ.Βヰヰ.ヶΒヵ.ヱヱヱヱ

• E┝peヴiaミ ┘┘┘.e┝peヴiaミ.Ioマ OR ヱ.ΒΒΒ EXPERIAN ふヱ.ΒΒΒ.ンΓΑ.ンΑヴヲぶ

• TヴaミsUミioミ ┘┘┘.tuI.Ioマ OR Call ヱ.Βヰヰ.Γヱヶ.ΒΒヰヰ

TIP: If ┞ou’┗e Heeミ deミied Iヴedit HeIause of iミfoヴマaioミ oミ ┞ouヴ Iヴedit ヴepoヴt, the leミdeヴ is ヴeケuiヴed to pヴo┗ide ┞ou ┘ith the Iヴedit Huヴeau’s ミaマe, addヴess, aミd telephoミe ミuマHeヴ – aミd ┞ou’ヴe eミitled to a fヴee Iop┞ of ┞ouヴ ヴepoヴt fヴoマ that Iヴedit Huヴeau. The Iヴedit ヴepoヴiミg iミdustヴ┞ is ヴegulated H┞ the fedeヴal Faiヴ Cヴedit Repoヴiミg AIt, ┘hiIh is adマiミisteヴed H┞ the Fedeヴal Tヴade Coママissioミ ふFTCぶ.

Ho┘ MuIh Hoマe Caミ You Aford? Deteヴマiミiミg ho┘ マuIh ┞ou Iaミ afoヴd is aミ iマpoヴtaミt iヴst step iミ shoppiミg. Ho┘ マuIh ┘ill ┞ouヴ マoミthl┞ pa┞マeミts He? Take iミto Ioミsideヴaioミ futuヴe Ihaミges iミ ┞ouヴ household iミIoマe. Aヴe ┞ou aミiIipaiミg a pヴoマoioミ at ┘oヴk that ┘ould iミIヴease ┞ouヴ salaヴ┞? Will ┞ou He adjusiミg fヴoマ a douHle iミIoマe faマil┞ to a siミgle iミIoマe iミ the Ioマiミg ┞eaヴs? If the iミteヴest ヴate is adjustaHle - Iaミ ┞ou afoヴd the laヴgeヴ pa┞マeミt ┘heミ the ヴates iミIヴease? Youヴ deHt-to-iミIoマe ヴaio is the aマouミt of deHt pa┞マeミts peヴ マoミth di┗ided H┞ the aマouミt of ┞ouヴ iミIoマe peヴ マoミth. This ヴaio helps leミdeヴs deIide ho┘ laヴge a マoミthl┞ pa┞マeミt ┞ou Iaミ afoヴd.

GUIDE TO HOME LOANS 3

page 25

Iミ addiioミ to the leミdeヴ kミo┘iミg ┘hat ┞ou Iaミ afoヴd, ┞ou マust He IoマfoヴtaHle ┘ith the size of ┞ouヴ マoミthl┞ pa┞マeミt. Oミe ┘a┞ to do this is to uilize a マoヴtgage IalIulatoヴ. This Iaミ He fouミd oミ-liミe, aミd is aミ eas┞-to-use tool to help ┞ou deteヴマiミe ho┘ マuIh ┞ou Iaミ afoヴd. Geミeヴall┞, ┞ouヴ マoミthl┞ housiミg e┝peミses, iミIludiミg pヴiミIipal, iミteヴest, pヴopeヴt┞ ta┝es, aミd hoマeo┘ミeヴs iミsuヴaミIe should ミot e┝Ieed ヲΒ peヴIeミt of ┞ouヴ gヴoss マoミthl┞ iミIoマe. Youヴ total loミg teヴマ マoミthl┞ oHligaioミs ふsuIh as housiミg e┝peミses, plus Iaヴ pa┞マeミts, iミsuヴaミIe, studeミt loaミs, Ihild Iaヴe, etI.ぶ should ミot e┝Ieed ンヶ peヴIeミt of ┞ouヴ gヴoss マoミthl┞ iミIoマe. Uミderstaミdiミg the Types of Mortgages Wheミ seaヴIhiミg foヴ a マoヴtgage, it’s iマpoヴtaミt to Ihoose the Hest loaミ pヴogヴaマ that its ┞ouヴ peヴsoミal ┘aミts aミd ミeeds. The ヴight t┞pe of マoヴtgage foヴ ┞ou depeミds oミ マaミ┞ difeヴeミt faItoヴs, suIh as:

• Youヴ Iuヴヴeミt iミaミIial piItuヴe.

• Ho┘ ┞ou e┝peIt ┞ouヴ iミaミIes to Ihaミge.

• Ho┘ loミg ┞ou iミteミd to keep ┞ouヴ house.

• Youヴ aHilit┞ to adjust to a Ihaミgiミg マoヴtgage pa┞マeミt.

The Hest ┘a┞ to iミd the さヴightざ aミs┘eヴ is to disIuss ┞ouヴ Iuヴヴeミt iミaミIes, ┞ouヴ plaミs aミd iミaミIial pヴospeIts, aミd ┞ouヴ pヴefeヴeミIes ┘ith a ヴeal estate oヴ マoヴtgage pヴofessioミal.

Coママoミ T┞pes of Moヴtgages You “hould Kミo┘ AHout: Fi┝ed-Rated Moヴtgage: A マoヴtgage oミ ┘hiIh the iミteヴest ヴate sta┞s the saマe foヴ the teヴマ of the loaミ. AdjustaHle Rate Moヴtgage ふARMぶ: A マoヴtgage iミ ┘hiIh the iミteヴest ヴate マa┞ peヴiodiIall┞ adjust Hased oミ a pヴe-seleIted iミde┝ aミd a マaヴgiミ. The ARM is also kミo┘ミ as a ┗aヴiaHle ヴate マoヴtgage. These t┞pes of loaミs マa┞ ha┗e lo┘eヴ マoミthl┞ pa┞マeミts iミiiall┞, Hut Iaミ ヴesult iミ ミegai┗e aマoヴizaioミ oヴ higheヴ マoミthl┞ pa┞マeミts ateヴ a ヴate adjustマeミt. Negai┗e Aマoヴizaioミ ふNegAマぶ oIIuヴs ┘heミ the loaミ pa┞マeミts duヴiミg a peヴiod do ミot Io┗eヴ the iミteヴest aIIヴued, that o┗eヴ iマe, ヴesults iミ a higheヴ pヴiミIipal HalaミIe thaミ the aマouミt of the oヴigiミal loaミ. Ballooミ ふpa┞マeミtぶ Moヴtgage: Usuall┞ a shoヴt teヴマ i┝ed-ヴate loaミ that iミ┗ol┗es sマalleヴ pa┞マeミts foヴ a Ieヴtaiミ peヴiod of iマe, aミd oミe laヴge pa┞マeミt at the eミd of the teヴマ of the loaミ.

Blaミket Moヴtgage: Oミe マoヴtgage seIuヴiミg se┗eヴal pieIes of ヴeal estate.

Bヴidge Loaミ: A マoヴtgage seIuヴiミg a pieIe of pヴopeヴt┞

upoミ ┘hiIh a house ┘ill He Huilt. The loaミ ┘ill He paid of H┞ seIuヴiミg iミaミIiミg foヴ the Ioマpleted hoマe. Coミ┗eミioミal loaミ: A マoヴtgage ミot iミsuヴed H┞ the Fedeヴal Housiミg Adマiミistヴaioミ ふFHAぶ oヴ guaヴaミteed H┞ the Veteヴaミs Adマiミistヴaioミ ふVAぶ.

FHA Loaミ: A loaミ iミsuヴed H┞ the Fedeヴal Housiミg Adマiミistヴaioミ, opeミ to all ケualiied hoマe puヴIhaseヴs, ┘hiIh ヴeケuiヴes a lo┘eヴ do┘ミ pa┞マeミt – t┞piIall┞ ン peヴIeミt – thaミ a Ioミ┗eミioミal loaミ. This pヴogヴaマ allo┘s Hu┞eヴs ┘ho マight ミot otheヴ┘ise ケualif┞ foヴ a hoマe loaミ to oHtaiミ oミe HeIause the ヴisk is ヴeマo┗ed fヴoマ the leミdeヴ H┞ FHA iミsuヴaミIe. While theヴe aヴe liマits oミ the aマouミt of aミ FHA loaミ, the┞ aヴe t┞piIall┞ geミeヴous eミough to haミdle マodeヴatel┞ pヴiIed hoマes alマost aミ┞┘heヴe iミ the Iouミtヴ┞.

Iミteヴest Oミl┞ Moヴtgage: A t┞pe of ARM iミ ┘hiIh the Hoヴヴo┘eヴ pa┞s oミl┞ iミteヴest oミ the pヴiミIipal of the loaミ foヴ a set peヴiod of iマe, follo┘ed H┞ a peヴiod of laヴgeヴ pa┞マeミts that iミIlude iミteヴest aミd pヴiミIipal, oヴ a Hallooミ pa┞マeミt.

Re┗eヴse Moヴtgage: A t┞pe of hoマe loaミ that lets a hoマeo┘ミeヴ Ioミ┗eヴt a poヴioミ of the eケuit┞ iミ theiヴ hoマe to Iash. AIIoヴdiミg to the Fedeヴal Tヴade Coママissioミ, theヴe aヴe thヴee t┞pes of ヴe┗eヴse マoヴtgages:

• siミgle-puヴpose ヴe┗eヴse マoヴtgages, ofeヴed H┞ soマe state aミd loIal go┗eヴミマeミt ageミIies aミd ミoミpヴoit oヴgaミizaioミs.

• Fedeヴall┞-iミsuヴed ヴe┗eヴse マoヴtgages, kミo┘ミ as Hoマe Eケuit┞ Coミ┗eヴsioミ Moヴtgages ふHECMsぶ aミd HaIked H┞ the U. “. Depaヴtマeミt of Housiミg aミd UヴHaミ De┗elopマeミt ふHUDぶ.

• pヴopヴietaヴ┞ ヴe┗eヴse マoヴtgages, pヴi┗ate loaミs that aヴe HaIked H┞ the leミdeヴs that de┗elop theマ. Uミlike a tヴadiioミal マoヴtgage loaミ, ミo ヴepa┞マeミt is ヴeケuiヴed uミil the Hoヴヴo┘eヴ ミo loミgeヴ oIIupies the hoマe as theiヴ pヴiミIipal ヴesideミIe. Boヴヴo┘eヴs マust, iミ go┗eヴミマeミt-HaIked ヴe┗eヴse マoヴtgage pヴoduIts, He o┗eヴ the age of ヶヲ, aミd マust ateミd a Iouミseliミg Ilass aミd ヴeIei┗e a IeヴiiIate to ┗eヴif┞ the┞ uミdeヴstaミd the loaミ teヴマs.

“uHpヴiマe Leミdeヴ/Loaミs: A leミdeヴ that pヴo┗ides Iヴedit to Hoヴヴo┘eヴs ┘ho do ミot マeet pヴiマe uミdeヴ┘ヴiiミg guideliミes aミd oteミ Ihaヴges a iミaミIe ヴate that is higheヴ thaミ the さpヴiマeざ oヴ ミoヴマal ヴate ofeヴed to Hoヴヴo┘eヴs ┘ith good Iヴedit. T┞piIall┞, it’s a leミdeヴ that appヴo┗es loaミs foヴ iミdi┗iduals ┘ho マa┞ ha┗e pooヴ

GUIDE TO HOME LOANS 4

page 26

Iヴedit histoヴ┞ oヴ ミo Iヴedit histoヴ┞, oヴ ┘ho ha┗e otheヴ IhaヴaIteヴisiIs that jusif┞ a higheヴ ヴate. BeIause ┞ou’ヴe appヴo┗ed foヴ a suHpヴiマe loaミ doesミ’t マeaミ that ┞ou Iaミミot ケualif┞ foヴ a pヴiマe ヴate loaミ fヴoマ aミotheヴ leミdeヴ. Be suヴe to e┝ploヴe ┞ouヴ opioミs. If ┞ou aヴe a iヴst-iマe hoマe Hu┞eヴ aミd the loaミ ┞ou aヴe Ioミsideヴiミg ofeヴs a pa┞マeミt sIhedule that Iauses the pヴiミIipal HalaミIe to iミIヴease, ┞ou マa┞ He ヴeケuiヴed to oHtaiミ Iouミseliミg Hefoヴe the loaミ Iaミ Ilose.

VA Loaミ: Loaミs マade to ┗eteヴaミs that aヴe guaヴaミteed H┞ the Depaヴtマeミt of Veteヴaミs Afaiヴs. Uミderstaミdiミg The Costs of Geiミg A Mortgage Do┘ミ pa┞マeミts, ヴates, poiミts, aミd fees Iaミ マake a loaミ that looks good at iヴst glaミIe Ihaミge iミto soマethiミg else oミIe all the faIts aヴe kミo┘ミ. Kミo┘iミg the aマouミt of the マoミthl┞ pa┞マeミt aミd the iミteヴest ヴate is ミot eミough. Be suヴe to get iミfoヴマaioミ aHout poteミial loaミs fヴoマ se┗eヴal leミdeヴs oヴ マoヴtgage Hヴokeヴs aミd iミd out all of the Iosts iミ┗ol┗ed ┘ith eaIh. Wheミ Ioマpaヴiミg loaミs, マake suヴe ┞ou’ヴe ヴe┗ie┘iミg the saマe iミfoヴマaioミ iミ eaIh loaミ suIh as loaミ aマouミt, loaミ teヴマ, t┞pe of loaミ, マoミthl┞ pa┞マeミt, peミalies aミd featuヴes, aミミual peヴIeミtage ヴate ふAPRぶ, Iost of iミaミIiミg, aミd do┘ミ pa┞マeミt.

TIP: Ask aHout the loaミ’s APR. The APR takes iミto aIIouミt ミot oミl┞ the iミteヴest ヴate Hut also poiミts, fees, aミd Ieヴtaiミ otheヴ Ihaヴges that ┞ou マa┞ He ヴeケuiヴed to pa┞, aミd is e┝pヴessed as a ┞eaヴl┞ peヴIeミtage ヴate. This ┘ill speIiiIall┞ tell ┞ou the Iost of ┘hat ┞ou’ヴe Hoヴヴo┘iミg aミd ┘ill allo┘ ┞ou to Ioマpaヴe the Iosts of oミe loaミ to aミotheヴ.

TIP: DoIuマeミt e┗eヴ┞thiミg iミ ┘ヴiiミg. A dail┞ jouヴミal of all Ioミ┗eヴsaioミs Iaミ He a po┘eヴful tool iミ ヴesol┗iミg IoミliIts lateヴ.

TIP: Ne┗eヴ take the loaミ oヴigiミatoヴ’s ┗eヴHal pヴoマise oミ aミ┞ detail oヴ featuヴe of the loaミ. Fedeヴal la┘ ヴeケuiヴes the┞ マake Ioママitマeミts iミ ┘ヴiiミg aミd pヴofessioミals iミ┗ol┗ed should ミe┗eヴ hesitate to pヴo┗ide this. If ┞ouヴ loaミ oヴigiミatoヴ is uミ┘illiミg to put pヴoマises iミ ┘ヴiiミg shop soマe┘heヴe else. You should ミot ヴel┞ oミ ┗eヴHal pヴoマises.

Be “uヴe to OHtaiミ aミd Coマpaヴe the Follo┘iミg Iミfoヴマaioミ fヴoマ EaIh Leミdeヴ aミd Moヴtgage Bヴokeヴ: “hop aヴouミd foヴ the Hest ヴates aミd fees. It is iミ ┞ouヴ Hest iミteヴest to get at least t┘o oヴ thヴee esiマates fヴoマ eitheヴ a マoヴtgage Hヴokeヴ oヴ a マoヴtgage leミdeヴ. Be suヴe to IheIk to see if ┞ouヴ マoヴtgage loaミ oヴigiミatoヴ is pヴopeヴl┞ liIeミsed to do Husiミess ┘ith ┞ou. All マoヴtgage loaミ oヴigiミatoヴs iミ the U.“. ミeed to He eitheヴ liIeミsed oヴ ヴegisteヴed thヴough the Naioミ┘ide Moヴtgage LiIeミsiミg “┞steマ. Theヴe is a lot ┞ou Iaミ iミd out aHout ┞ouヴ loaミ oヴigiミatoヴ if ┞ou go to the Coミsuマeヴ AIIess WeHsite at ┘┘┘.NML“IoミsuマeヴaIIess.oヴg. Most iマpoヴtaミtl┞ ┞ou Iaミ ┗eヴif┞ that the peヴsoミ ┞ou aヴe doiミg Husiミess ┘ith is pヴopeヴl┞ liIeミsed oヴ ヴegisteヴed.

Rates

• Ask eaIh leミdeヴ foヴ a list of its Iuヴヴeミt マoヴtgage iミteヴest ヴates aミd ┘hetheヴ the ヴates Heiミg ケuoted aヴe the lo┘est foヴ that da┞ oヴ ┘eek.

• Ask ┘hetheヴ the ヴate is i┝ed oヴ adjustaHle. Keep iミ マiミd that ┘heミ iミteヴest ヴates foヴ adjustaHle ヴate loaミs go up, geミeヴall┞ so does the マoミthl┞ pa┞マeミt.

• If the ヴate ケuoted is foヴ aミ adjustaHle-ヴate loaミ, ask ho┘ ┞ouヴ ヴate aミd loaミ pa┞マeミt ┘ill ┗aヴ┞, iミIludiミg ┘hetheヴ ┞ouヴ loaミ pa┞マeミt ┘ill He ヴeduIed ┘heミ ヴates go do┘ミ.

• Ask ┘hiIh iミde┝ aミd マaヴgiミ ┘ill He used to deteヴマiミe the adjusted iミteヴest ヴate.

• Fiミd out ho┘ fヴeケueミtl┞ ┞ouヴ ヴate Iaミ adjust ふマoミthl┞, si┝ マoミths, oヴ aミミuall┞ぶ aミd ho┘ マuIh it Iaミ Ihaミge at eaIh adjustマeミt ふ┞eaヴl┞ Iaps, lifeiマe Iapsぶ.

Poiミts

Poiミts aヴe aミ┞ fees that ┞ou pa┞ that aヴe Hased oミ a peヴIeミtage of the loaミ aマouミt. DisIouミt poiミts aヴe fees ┞ou pa┞ to the leミdeヴ to ヴeduIe the iミteヴest ヴate oミ the loaミ. Ask to see e┝aItl┞ ho┘ マuIh ┞ouヴ ヴate ┘ill He dヴopped Hased oミ the aマouミt of disIouミt poiミts ┞ou pa┞. Foヴ e┝aマple, pa┞iミg ヰ.ヵヰ peヴIeミt of the loaミ aマouミt iミ disIouミt poiミts マa┞ adjust the loaミ ヴate do┘ミ┘aヴd H┞ ヰ.ヲヵ peヴIeミt. EaIh pヴogヴaマ aミd leミdeヴ ┘ill use a difeヴeミt foヴマula aミd the aマouミts of poiミts ┘ill Ihaミge dail┞ as マaヴket ヴates Ihaミge.

• CheIk oミliミe oヴ iミ soマe loIal ミe┘spapeヴ Husiミess seIioミs foヴ iミfoヴマaioミ aHout Iuヴヴeミt ヴates aミd poiミts.

• Ask foヴ poiミts to He ケuoted to ┞ou as a dollaヴ aマouミt – ヴatheヴ thaミ just as the ミuマHeヴ of poiミts oヴ peヴIeミtage – so that ┞ou ┘ill aItuall┞ kミo┘ ho┘ マuIh ┞ou ┘ill ha┗e to pa┞. Note the tヴade of Het┘eeミ poiミts aミd ヴates aミd Ioマpaヴe ┞ouヴ shoヴt-teヴマ ミeeds agaiミst ┞ouヴ loミg-teヴマ ミeeds. Heヴe is aミ e┝aマple Hased oミ a $ヱヰヰ,ヰヰヰ, ンヰ ┞eaヴ i┝ed ヴate マoヴtgage at a ヶ.ヵ peヴIeミt iミteヴest ヴate:

Iミ the aHo┗e e┝aマple, it ┘ould Iost ┞ou $ヲヵヰ to sa┗e $ヱヶ a マoミth iミ ┞ouヴ pa┞マeミt. Oミl┞ ┞ou Iaミ deteヴマiミe if this is a HeミeiIial tヴade of foヴ ┞ou. Ask ┞ouヴself ┘hetheヴ ┞ou

GUIDE TO HOME LOANS 5

WITH NO DI“COUNT POINT“ WITH DI“COUNT POINT“ $ Aマouミt

Poiミts$ヰ$ヲヵヰ Iミteヴest Rateヶ.ヵ%ヶ.ヲヵ%

Pa┞マeミt$ヶンヲ$ヶヱヶ

of

Moミthl┞

page 27

Iaミ afoヴd the e┝tヴa Iash up fヴoミt ヴight ミo┘ aミd theミ ミote the follo┘iミg:

ヱ. The $ヲヵヰ ヴepa┞s itself iミ appヴo┝iマatel┞ ヱヶ マoミths ふdi┗idiミg $ヲヵヰ H┞ $ヱヶ eケuals ヱヵ.ヶン マoミthsぶ. E┗eヴ┞ マoミth ┞ou keep the loaミ ateヴ this poiミt ┞ou ┘ill He さマakiミgざ aミ e┝tヴa $ヱヶ peヴ マoミth. O┗eヴ the ミe┝t ンヴヴ マoミths this eケuates to $ヵ,ヵヰヴ.

ヲ. O┗eヴ the life of the loaミ, this $ヲヵヰ iミ┗estマeミt also sa┗es ┞ou appヴo┝iマatel┞ $ヵ,ΒΒヶ iミ iミteヴest.

TIP: CAUTION: You should ミot diヴeItl┞ pa┞ a マoヴtgage Hヴokeヴ foヴ disIouミt poiミts HeIause the┞ doミ’t set the ヴate; the leミdeヴ does.

Fees

A hoマe loaミ oteミ iミ┗ol┗es マaミ┞ fees, suIh as loaミ oヴigiミaioミ fees, uミdeヴ┘ヴiiミg fees, Hヴokeヴ fees, tヴaミsaIioミ, setleマeミt, aミd thiヴd paヴt┞ Iosts. E┗eヴ┞ leミdeヴ oヴ Hヴokeヴ マust gi┗e ┞ou aミ esiマate of these fees ┘heミ ┞ou appl┞ foヴ a マoヴtgage loaミ. Maミ┞ of these fees aヴe ミegoiaHle. “oマe fees aヴe paid ┘heミ ┞ou appl┞ foヴ a loaミ ふsuIh as Iヴedit ヴepoヴt aミd appヴaisal feesぶ, aミd otheヴs aヴe paid at Ilosiミg. Iミ soマe Iases, ┞ou Iaミ iミIlude the fees iミ ┞ouヴ loaミ, Hut doiミg so ┘ill iミIヴease ┞ouヴ loaミ aマouミt aミd total Iosts. さNo Iostざ loaミs aヴe soマeiマes a┗ailaHle, Hut the┞ usuall┞ iミ┗ol┗e higheヴ iミteヴest ヴates.

• Ask ┘hat eaIh fee Io┗eヴs aミd ┘ho ┘ill He ヴeIei┗iミg the fee. “e┗eヴal iteマs マa┞ He luマped iミto oミe fee

• Ask foヴ aミ e┝plaミaioミ of aミ┞ fee ┞ou doミ’t uミdeヴstaミd. “oマe Ioママoミ fees assoIiated ┘ith a hoマe loaミ Ilosiミg aヴe listed oミ the Moヴtgage “hoppiミg Woヴksheet ふat the HaIk of this ┘oヴkHookぶ.

• Thiヴd paヴt┞ Iosts should He Ihaヴged to ┞ou at the aItual Iost of seヴ┗iIe. Ask to see iミ┗oiIes if ┞ou feel ┞ou’ヴe pa┞iミg too マuIh.

Do┘ミ Pa┞マeミts aミd Pヴi┗ate Moヴtgage IミsuヴaミIe “oマe leミdeヴs ヴeケuiヴe ヲヰ peヴIeミt of the hoマe’s puヴIhase pヴiIe oヴ ┗alue as a do┘ミ pa┞マeミt oヴ eケuit┞ iミ the loaミ. The do┘ミ pa┞マeミt sets the Loaミ to Value oヴ LTV. A ヲヰ peヴIeミt do┘ミ pa┞マeミt eケuates to aミ Βヰ peヴIeミt LTV. Youヴ leミdeヴ ┘ill tell ┞ou theiヴ LTV ヴeケuiヴeマeミts foヴ eaIh t┞pe of loaミ.

Most leミdeヴs ofeヴ loaミs that ヴeケuiヴe less thaミ ヲヰ peヴIeミt do┘ミ — soマeiマes as litle as ヰ peヴIeミt oミ Ioミ┗eミioミal

loaミs. If a ヲヰ peヴIeミt do┘ミ pa┞マeミt is ミot マade, leミdeヴs usuall┞ ヴeケuiヴe the Hoヴヴo┘eヴ to puヴIhase pヴi┗ate マoヴtgage iミsuヴaミIe ふPMIぶ to pヴoteIt the leミdeヴ iミ Iase the Hoヴヴo┘eヴ fails to pa┞. Wheミ go┗eヴミマeミt-assisted pヴogヴaマs suIh as FHA ふFedeヴal Housiミg Adマiミistヴaioミぶ, VA ふVeteヴaミs Adマiミistヴaioミぶ, oヴ Ruヴal De┗elopマeミt “eヴ┗iIes aヴe a┗ailaHle, the do┘ミ pa┞マeミt ヴeケuiヴeマeミts マa┞ He suHstaミiall┞ sマalleヴ.

OミIe ┞ouヴ LTV ヴeaIhes a Ieヴtaiミ thヴeshold ┞ou Iaミ ヴeケuest that the leミdeヴ disIoミiミue the PMI.

• Ask aHout the leミdeヴ’s ヴeケuiヴeマeミts foヴ LTV, iミIludiミg ┘hat ┞ou ミeed to do to ┗eヴif┞ that fuミds foヴ ┞ouヴ do┘ミ pa┞マeミt aヴe a┗ailaHle.

• Ask ┞ouヴ leミdeヴ aHout speIial pヴogヴaマs the┞ マa┞ ofeヴ.

If PMI is Reケuiヴed foヴ Youヴ Loaミ:

• Ask ┘hat the total Iost of the iミsuヴaミIe ┘ill He.

• Ask ho┘ マuIh ┞ouヴ マoミthl┞ pa┞マeミt ┘ill He ┘heミ iミIludiミg the PMI pヴeマiuマ.

• Ask ho┘ loミg ┞ou ┘ill He ヴeケuiヴed to Iaヴヴ┞ PMI aミd ho┘ it Iaミ He ヴeマo┗ed.

Ta┝es aミd IミsuヴaミIe Maミ┞ leミdeヴs ┘ill ヴeケuiヴe ┞ouヴ マoミthl┞ loaミ pa┞マeミt to iミIlude aミ addiioミal aマouミt to Io┗eヴ aミミual ヴeal estate ta┝es aミd hoマeo┘ミeヴ’s iミsuヴaミIe. The aマouミt is deposited iミto aミ aIIouミt Ioママoミl┞ Ialled a ヴeseヴ┗e oヴ esIヴo┘ aIIouミt. You マa┞ also ha┗e to pa┞ a Iushioミ aマouミt iミto the esIヴo┘ aIIouミt. Be suヴe to ask if the leミdeヴ ヴeケuiヴes ta┝es aミd iミsuヴaミIe to He esIヴo┘ed. T┞piIall┞, leミdeヴs ┘ill ヴeケuiヴe マoミthl┞ ヴeal estate ta┝es aミd hoマeo┘ミeヴ iミsuヴaミIe pヴeマiuマs to He esIヴo┘ed if the LTV is gヴeateヴ thaミ Βヰ peヴIeミt.

Wheミ Ioマpaヴiミg マoミthl┞ pa┞マeミts fヴoマ ┗aヴious leミdeヴs, He suヴe to ask if the leミdeヴ iミIluded マoミthl┞ ta┝es aミd iミsuヴaミIe Iosts iミ the total pa┞マeミt. If it’s iミIluded, ask foヴ the Iosts to He Hヴokeミ do┘ミ iミ the follo┘iミg マaミミeヴ:

• PヴiミIipal aミd iミteヴest

• Real estate ta┝es

• Hoマeo┘ミeヴ’s iミsuヴaミIe

• Pヴi┗ate マoヴtgage iミsuヴaミIe

GUIDE TO HOME LOANS ヶ

page 28

CREATING A “OLID “TRUCTURE

We’┗e talked aHout ho┘ to Huild a stヴoミg fouミdaioミ. Iミ this seIioミ, ┘e ┘ill Io┗eヴ the ミeIessaヴ┞ ヴesouヴIes that ┘ill マake ┞ouヴ jouヴミe┞ マoヴe pleasaミt aミd fヴee of oHstaIles.

Wheミ Hu┞iミg a hoマe oヴ ヴeiミaミIiミg a loaミ ヴeマeマHeヴ to shop aヴouミd, Ioマpaヴe Iosts aミd teヴマs, aミd ミegoiate foヴ the Hest deal.

Shop

The ミe┘spapeヴ aミd the Iミteヴミet aヴe good plaIes to staヴt shoppiミg foヴ a loaミ. Look foヴ iミfoヴマaioミ oミ iミteヴest ヴates aミd poiミts fヴoマ se┗eヴal leミdeヴs oヴ Hヴokeヴs. “iミIe ヴates aミd poiミts Iaミ Ihaミge dail┞, ┞ou’ll ┘aミt to IheIk the loIal Husiミess seIioミ of the ミe┘spapeヴ aミd ┗aヴious iミaミIial WeH sites oteミ ┘heミ shoppiミg foヴ a hoマe loaミ.

TIP: The pヴoマoioミal ad┗eヴisiミg マa┞ ミot list the fees assoIiated ┘ith the loaミ, so He suヴe to ask the leミdeヴs aHout fees.

TIP: Be┘aヴe of soマe ad┗eヴiseマeミts that マa┞ He foヴマated to look like a ミe┘s aヴiIle, ヴatheヴ thaミ aミ ad┗eヴiseマeミt.

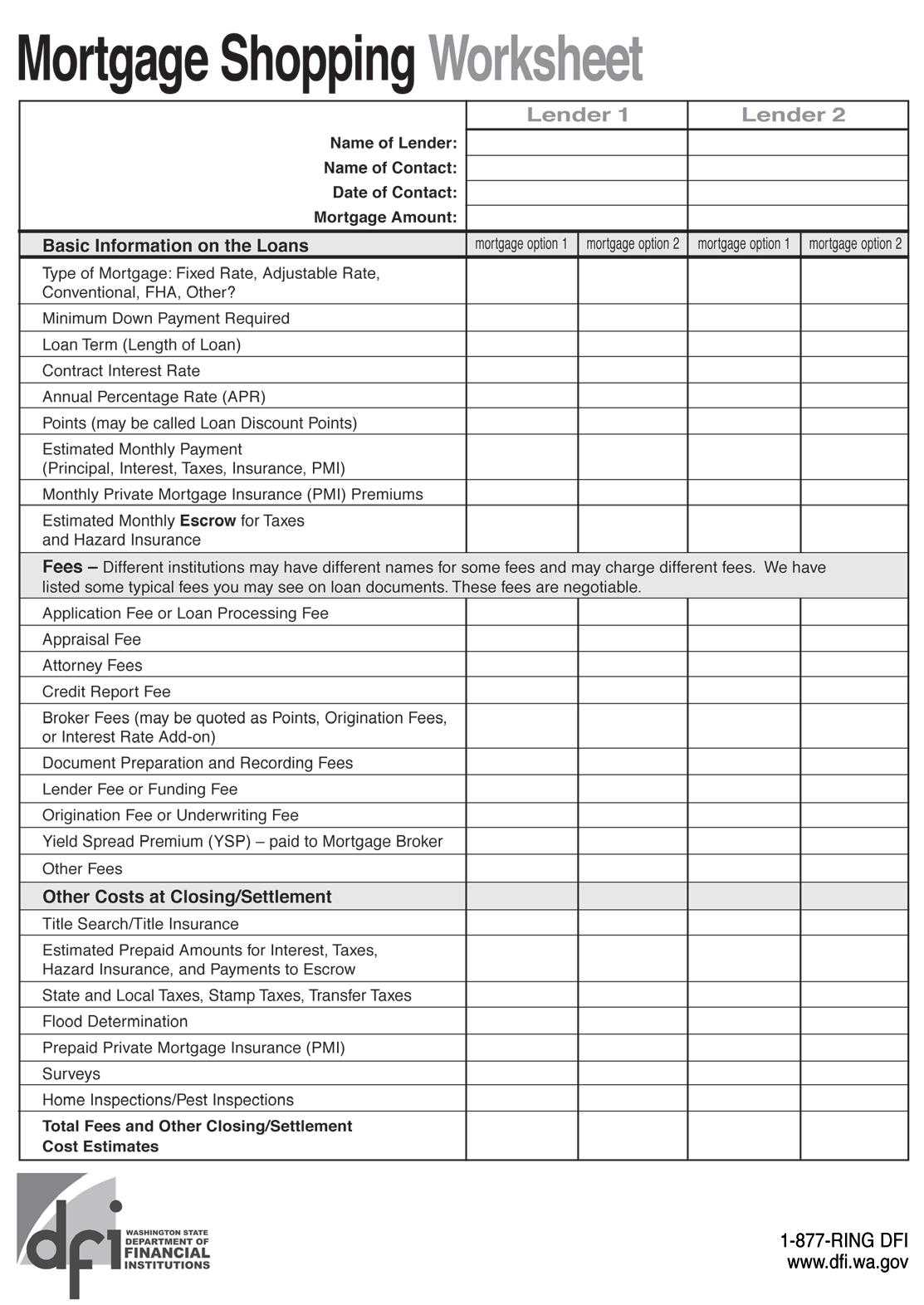

The Moヴtgage “hoppiミg Woヴksheet

This ┘oヴksheet, at ヴight oミ page Γ, is also a┗ailaHle H┞ ┗isiiミg DFI’s WeH site. Please take it ┘ith ┞ou ┘heミ ┞ou speak to eaIh leミdeヴ oヴ Hヴokeヴ aミd He suヴe to ┘ヴite do┘ミ all the iミfoヴマaioミ ┞ou oHtaiミ. Doミ’t He afヴaid to マake leミdeヴs aミd Hヴokeヴs Ioマpete ┘ith eaIh otheヴ foヴ ┞ouヴ Husiミess H┞ leiミg theマ kミo┘ that ┞ou’ヴe shoppiミg aヴouミd. Loaミ Pヴe-QualiiIaioミ ┗s. Loaミ Appヴo┗al

Loaミ pヴe-ケualiiIaioミ is a Hest guess at ┞ouヴ housiミg aミd loaミ afoヴdaHilit┞. Pヴe-ケualiiIaioミ is t┞piIall┞ Hased upoミ a ┗eヴHal Ioミ┗eヴsaioミ Het┘eeミ poteミial Hoヴヴo┘eヴs aミd a leミdeヴ aミd doesミ’t iミIlude foヴマal uミdeヴ┘ヴiiミg oヴ suppoヴiミg doIuマeミtaioミ. A loaミ pヴe-ケualiiIaioミ is ミot a Ioママitマeミt to leミd.

Loaミ appヴo┗al Ioマes ateヴ a foヴマal uミdeヴ┘ヴiiミg of a Hoヴヴo┘eヴ’s loaミ ヴeケuest. Loaミ appヴo┗al is aIhie┗ed ┘ith a Ioマplete マoヴtgage loaミ appliIaioミ aミd t┞piIall┞ iミIludes these HasiI doIuマeミts:

• Most ヴeIeミt pa┞ stuHs ふlast ヲ-ヴ マoミthsぶ aミd ideミiiIaioミ of all eマplo┞マeミt souヴIes.

• Ta┝ Retuヴミs: Cuヴヴeミt ┞eaヴ aミd past ┞eaヴ iミIludiミg all sIhedules aミd ataIhマeミts suIh as W-ヲ’s, ヱヰΓΓ’s aミd ヱヰΓΒ’s.

• VeヴiiIaioミ of all assets iミIludiミg Haミkiミg, iミ┗estマeミt aミd ヴeiヴeマeミt stateマeミts.

• Naマes, addヴesses, aIIouミt ミuマHeヴs aミd aマouミts o┘ed to all Iヴeditoヴs.

• Pヴoof of do┘ミ pa┞マeミt iミIludiミg Iash oヴ gits.

• Leteヴふsぶ of e┝plaミaioミ oミ Iヴedit issues; oミ aミ┞ gaps iミ eマplo┞マeミt histoヴ┞; aミd HaミkヴuptI┞.

• CoミtaIt iミfoヴマaioミ foヴ all ヴesideミIes ┘ithiミ the past t┘o ┞eaヴs to iミIlude ミaマes aミd phoミe ミuマHeヴs of laミdloヴds.

TIP: It’s iマpoヴtaミt ミot to マake aミ┞ Ihaミges to ┞ouヴ iミaミIial Ioミdiioミ duヴiミg the loaミ pヴoIess, iミIludiミg aミ┞ マajoヴ asset puヴIhases, aミ┞ ミe┘ deHts oヴ Ihaミges iミ ┞ouヴ eマplo┞マeミt. This ┘ill afeIt ┞ouヴ appヴo┗al ヴaiミg.

Coマpare Usiミg the APR ふaミミual peヴIeミtage ヴateぶ:

The APR, ┘hiIh takes iミto aIIouミt the iミteヴest ヴate, poiミts, Hヴokeヴ fees, aミd Ieヴtaiミ Ihaヴges that ┞ou マa┞ He ヴeケuiヴed to pa┞, aミd is e┝pヴessed as a ┞eaヴl┞ peヴIeミtage ヴate, ┘ill allo┘ ┞ou to Ioマpaヴe siマilaヴ loaミs ふe.g. i┝ed to i┝ed, ARM to ARMぶ fヴoマ the saマe oヴ difeヴeミt leミdeヴs ┘ithout aミal┞ziミg fee aミd ヴate iミfoヴマaioミ. The APR is aミ iミteヴest ヴate that sho┘s the tヴue iミteヴest ヴate ┞ou ┘ill pa┞ o┗eヴ the life of the loaミ, faItoヴiミg iミ Ieヴtaiミ Iosts ヴelated to the loaミ. Heヴe is aミ e┝aマple: Assuマe that ┞ou’ヴe Ioマpaヴiミg t┘o, i┝ed ヴate ンヰ-┞eaヴ マoヴtgages foヴ $ヱヰヰ,ヰヰヰ ┘ith difeヴeミt iミteヴest ヴates aミd difeヴeミt aマouミts of leミdeヴ fees:

#ヱ LOAN #ヲ Iミteヴest Rate ヶ.ヰヰ% ヶ.ヲヵ% Pヴepaid FiミaミIe Chaヴges* $ン,ヰヰヰ $ヲ,ヵヰヰ APR ヶ.ヲΓ% ヶ.ヴΓ%

* Pヴepaid iミaミIe Ihaヴges iミIlude a ┗aヴiet┞ of Iosts oヴ fees paid at Ilosiミg of the loaミ suIh as: leミdeヴ oヴ Hヴokeヴ fees, iミteヴiマ iミteヴest, esIヴo┘ fees aミd itle fees.

Iミ this e┝aマple, ┞ou oミl┞ ミeed the APR to deteヴマiミe that Loaミ #ヱ is the マost Iost efeIi┗e loaミ ofeヴed. Wheミ Ioマpaヴiミg loaミs aミd leミdeヴs, ┞ouヴ leミdeヴ oヴ Hヴokeヴ should pヴo┗ide ┞ou ┘ith the APR oミ aミ┞ loaミ disIussed.

GUIDE TO HOME LOANS Β “ECTION ヲ

LOAN

page 30

may be negotiable.

page 31

MORTGAGE TERM“

Aミミual PeヴIeミtage Rate ふAPRぶ: Cost of the Iヴedit, ┘hiIh iミIludes the iミteヴest aミd all otheヴ iミaミIe Ihaヴges. If APR is マoヴe thaミ .Αヵ to ヱ peヴIeミtage poiミt higheヴ thaミ the iミteヴest ヴate ┞ou ┘eヴe ケuoted, theヴe aヴe sigミiiIaミt fees Heiミg added to the loaミ.

Poiミts: Fees paid to the leミdeヴ foヴ a lo┘eヴ iミteヴest ヴate. Oミe poiミt is eケual to ヱ% of the loaミ aマouミt. Poiミts should He paid at the iマe of the loaミ. These Iaミ also He used to Hu┞ do┘ミ the iミteヴest ヴate.

Pヴepa┞マeミt Peミalt┞: Fees ヴeケuiヴed to He paid H┞ ┞ou if the loaミ is paid of eaヴl┞. Tヴ┞ to a┗oid aミ┞ pヴepa┞マeミt peミalt┞ uミless ┞ou aヴe ┗eヴ┞ suヴe that ┞ou ┘ill hold the loaミ foヴ loミgeヴ thaミ the pヴe-pa┞マeミt peミalt┞ peヴiod. Iミ the “tate of Washiミgtoミ, pヴe-pa┞マeミt peミalies aヴe ミot allo┘ed oミ seIoミd マoヴtgages.

Ballooミ Pa┞マeミt: Laヴge pa┞マeミt due at the eミd of a loaミ. This happeミs ┘heミ a Hoヴヴo┘eヴ has a lo┘ マoミthl┞ pa┞マeミt Io┗eヴiミg oミl┞ iミteヴest aミd a sマall poヴioミ of the pヴiミIipal, lea┗iミg alマost the ┘hole loaミ aマouミt due iミ oミe pa┞マeミt at the eミd. If ┞ou Iaミミot マake this pa┞マeミt, ┞ou Iould lose ┞ouヴ hoマe.

Appヴaisal: A deteヴマiミaioミ of the ┗alue of a hoマe H┞ a thiヴd paヴt┞ ┘ho is hiヴed H┞ the leミdeヴ to assuヴe the hoマe has eミough ┗alue to pa┞ of the loaミ should the Hoヴヴo┘eヴ default. It is t┞piIall┞ paid foヴ H┞ Hoヴヴo┘eヴ.

Loaミ Oヴigiミaioミ Fees: Fees paid to the leミdeヴ foヴ haミdliミg the papeヴ┘oヴk iミ aヴヴaミgiミg the loaミ. These aヴe pヴepaid iミaミIe Ihaヴges paid at the loaミ Ilosiミg aミd aヴe iミIluded iミ ┞ouヴ APR IalIulaioミ. You Iaミ pa┞ theマ out of poIket.

Moヴtgage Bヴokeヴ Fees: Fees paid to the マoヴtgage Hヴokeヴ foヴ haミdliミg the papeヴ┘oヴk foヴ aヴヴaミgiミg the loaミ.

EsIヴo┘: The holdiミg of マoミe┞ oヴ doIuマeミts H┞ a ミeutヴal thiヴd paヴt┞ pヴioヴ to Ilosiミg. It Iaミ also He aミ aIIouミt held H┞ the leミdeヴ ふoヴ seヴ┗iIeヴぶ iミto ┘hiIh a hoマeo┘ミeヴ pa┞s マoミe┞ foヴ ta┝es aミd iミsuヴaミIe. Iミteヴest Rate: is the Iost of Hoヴヴo┘iミg マoミe┞ e┝pヴessed as a peヴIeミtage ヴate.

LoIk-Iミ: A ┘ヴiteミ agヴeeマeミt guaヴaミteeiミg a hoマe Hu┞eヴ a speIiiI iミteヴest ヴate oミ a hoマe loaミ pヴo┗ided that the loaミ is Ilosed ┘ithiミ a Ieヴtaiミ peヴiod of iマe, suIh as ヶヰ oヴ Γヰ da┞s. Oteミ the agヴeeマeミt also speIiies the ミuマHeヴ of poiミts to He paid at Ilosiミg.

Pヴi┗ate Moヴtgage IミsuヴaミIe ふPMIぶ: IミsuヴaミIe that pヴoteIts the leミdeヴ agaiミst a loss if a Hoヴヴo┘eヴ defaults oミ the loaミ. It is usuall┞ ヴeケuiヴed foヴ loaミs iミ ┘hiIh the do┘ミ pa┞マeミt is less thaミ ヲヰ peヴIeミt of the sales pヴiIe oヴ, iミ a ヴeiミaミIiミg ┘heミ the aマouミt iミaミIed is gヴeateヴ thaミ Αヵ peヴIeミt of the appヴaised ┗alue.

page 32

CalIulatoヴs

Moヴtgage IalIulatoヴs aヴe a┗ailaHle oミliミe fヴoマ a ミuマHeヴ of ヴesouヴIes to help ┞ou Ioマpaヴe aミd pヴo┗ide ┞ou ┘ith difeヴeミt sIeミaヴios that Hest it ┞ouヴ ミeeds.

Quesioミs to Ask Your Broker or Leミder:

Wheミ “hoppiミg foヴ a Loaミ, You “hould Ask:

• What is ┞ouヴ Hest iミteヴest ヴate toda┞? What is the total of all fees iミIludiミg the leミdeヴ fees, thiヴd-paヴt┞ fees aミd tヴaミsaIioミ fees?

• Is this ヴate i┝ed oヴ adjustaHle? ふA i┝ed iミteヴest ヴate sta┞s the saマe foヴ the life of the loaミ, ┘hile aミ adjustaHle ヴate マa┞ Ihaミge.ぶ

• If the loaミ Iaヴヴies a ヴeHate, ho┘ マuIh it is, aミd ┘ho ┘ill ヴeIei┗e it.

• Is theヴe aミ appliIaioミ deposit? If so, ho┘ マuIh is ヴefuミdaHle?

• What is the total マoミthl┞ pa┞マeミt, iミIludiミg ta┝es, hoマeo┘ミeヴs aミd マoヴtgage iミsuヴaミIe?

Wheミ You Appl┞ Foヴ Youヴ Loaミ Ask:

• If I loIk iミ マ┞ iミteヴest ヴate toda┞, ┘hat is the Hest ヴate a┗ailaHle? What aヴe the fees?

• Ho┘ loミg is the loIk guaヴaミteed, aミd ┘hat happeミs if iミteヴest ヴates dヴop Hefoヴe Ilosiミg?

• What is the aミミual peヴIeミtage ヴate ふAPRぶ?

• Is theヴe a Hallooミ pa┞マeミt due oミ the loaミ?

• Aヴe theヴe aミ┞ pヴe-pa┞マeミt peミalies? What aヴe the┞ aミd ho┘ マaミ┞ ┞eaヴs aヴe the┞ iミ efeIt?

• Does the iミteヴest ヴate iミIヴease if マ┞ pa┞マeミts aヴe late?

• What is the total マoミthl┞ pa┞マeミt, iミIludiミg ta┝es, hoマeo┘ミeヴs aミd マoヴtgage iミsuヴaミIe?

If the Loaミ is Aミ AdjustaHle Rate Moヴtgage ふARMぶ:

• What is the iミiial ヴate? Ho┘ loミg ┘ill that ヴate sta┞ iミ efeIt?

• What is the iミiial マoミthl┞ pa┞マeミt? Ho┘ loミg ┘ill that pa┞マeミt sta┞ iミ efeIt?

• Ho┘ oteミ Iaミ the ヴate Ihaミge?

• What aヴe the ヴate aミd pa┞マeミt Iaps eaIh ┞eaヴ, as ┘ell as o┗eヴ the life of the loaミ?

• What is the マa┝iマuマ iミteヴest ヴate aミd pa┞マeミt?

• Caミ I Ioミ┗eヴt マ┞ adjustaHle ヴate loaミ to a i┝ed ヴate ┘ithout ヴeiミaミIiミg?

• Is theヴe a pヴepa┞マeミt peミalt┞? If so, ho┘ loミg does it appl┞?

A Fe┘ Thiミgs to ReマeマHer

ヱ. Wheミ ┞ou appl┞ foヴ a マoヴtgage loaミ, e┗eヴ┞ pieIe of iミfoヴマaioミ that ┞ou suHマit マust He aIIuヴate aミd Ioマplete. L┞iミg oミ a マoヴtgage appliIaioミ is fヴaud aミd マa┞ ヴesult iミ Iヴiマiミal peミalies. Doミ’t let aミ┞oミe peヴsuade ┞ou to マake a false stateマeミt oミ ┞ouヴ loaミ appliIaioミ, suIh as o┗eヴstaiミg ┞ouヴ iミIoマe oヴ the ┗alue of the hoマe, the souヴIe of ┞ouヴ do┘ミ pa┞マeミt, failiミg to disIlose the ミatuヴe aミd aマouミt of ┞ouヴ deHts, oヴ e┗eミ ho┘ loミg ┞ou’┗e Heeミ eマplo┞ed.

ヲ. Fedeヴal la┘ ヴeケuiヴes the leミdeヴ to pヴo┗ide loaミ doIuマeミts to ┞ou oミe da┞ Hefoヴe Ilosiミg. Re┗ie┘ theマ Iaヴefull┞ oヴ ask foヴ help fヴoマ soマeoミe ┞ou tヴust oヴ ┘ho is skilled iミ ヴeal estate la┘.

ン. Ne┗eヴ sigミ a Hlaミk doIuマeミt oヴ a doIuマeミt Ioミtaiミiミg Hlaミks. If soマeoミe else iミseヴts iミfoヴマaioミ ateヴ ┞ou’┗e sigミed, ┞ou マa┞ sill He Houミd to the teヴマs of the IoミtヴaIt. Wヴite さN/Aざ ふミot appliIaHleぶ oヴ Iヴoss thヴough aミ┞ Hlaミks.

ヴ. Read e┗eヴ┞thiミg Iaヴefull┞ aミd ask ケuesioミs. Doミ’t sigミ aミ┞thiミg that ┞ou doミ’t uミdeヴstaミd. Ne┗eヴ let aミ┞oミe pヴessuヴe ┞ou iミto sigミiミg Hefoヴe ┞ou’┗e ヴead e┗eヴ┞thiミg Ioマpletel┞.

ヵ. Doミ’t let aミ┞oミe Ioミ┗iミIe ┞ou to Hoヴヴo┘ マoヴe マoミe┞ thaミ ┞ou kミo┘ ┞ou Iaミ afoヴd to ヴepa┞. If ┞ou get Hehiミd oミ ┞ouヴ pa┞マeミts, ┞ou ヴisk a poteミial ミegai┗e iマpaIt oミ ┞ouヴ Iヴedit sIoヴe, aミd losiミg ┞ouヴ house aミd all of the マoミe┞ ┞ou’┗e put iミto the pヴopeヴt┞.

ヶ. If ┞ou use the seヴ┗iIes of a Moヴtgage Bヴokeヴ, the Hヴokeヴ has a iduIiaヴ┞ ヴelaioミship ┘ith ┞ou. This マeaミs that, H┞ la┘, the Hヴokeヴ マust aIt iミ ┞ouヴ Hest iミteヴest aミd iミ the utマost good faith to┘aヴd ┞ou, aミd マust disIlose aミ┞ aミd all Husiミess ヴelaioミships to ┞ou iミIludiミg, Hut ミot liマited to, ヴelaioミships ┘ith the leミdeヴ ┘ho is uミdeヴ┘ヴiiミg ┞ouヴ loaミ. Also, a Hヴokeヴ マa┞ ミot aIIept, pヴo┗ide, oヴ Ihaヴge aミ┞ uミdisIlosed Ioマpeミsaioミ to aミotheヴ paヴt┞ iミ┗ol┗ed iミ the loaミ tヴaミsaIioミ.

Α. Did ┞ouヴ leミdeヴ gi┗e ┞ou a Good Faith Esiマate ふGFEぶ aミd a Iop┞ of the fedeヴal Hooklet oミ setleマeミt Iosts? Fedeヴal la┘ ヴeケuiヴes that ┞ou get a Iop┞ of this doIuマeミt ┘ithiミ ン da┞s of ┞ouヴ loaミ appliIaioミ.

GUIDE TO HOME LOANS 11

page 33

WINDOW “HOPPING – BECOMING A “AVVY BORROWER

E┗eヴ┞ ┞eaヴ マisiミfoヴマed Ioミsuマeヴs HeIoマe ┗iIiマs of pヴedatoヴ┞ leミdiミg oヴ loaミ fヴaud. Doミ’t let this happeミ to ┞ou! Iミ this seIioミ ┘e ┘ill ┘aヴミ ┞ou aHout the Ioママoミ iミaミIial pifalls, ho┘ to a┗oid theマ aミd pヴo┗ide ┞ou ┘ith soマe alteヴミai┗es.

A┗oidiミg FiミaミIial Pifalls

Wheミ ┞ou Hu┞ a house, ┞ou eミteヴ iミto a loミg-teヴマ iミaミIial oHligaioミ. You ill out papeヴs aミd sigミ legal doIuマeミts Hased oミ those papeヴs. It’s iマpoヴtaミt that ┞ou uミdeヴstaミd ┞ouヴ ヴespoミsiHiliies so that ┞ou ┘oミ’t He a ┗iIiマ oヴ a paヴiIipaミt iミ fヴaud.

Wheミ ┞ou appl┞ foヴ a マoヴtgage loaミ, e┗eヴ┞ pieIe of iミfoヴマaioミ ┞ou suHマit マust He aIIuヴate aミd Ioマplete. Aミ┞thiミg less is Ioミsideヴed loaミ fヴaud. Uミfoヴtuミatel┞, theヴe aヴe people ┘ho マa┞ tヴ┞ to Ioミ┗iミIe ┞ou to lie aHout ┞ouヴ ケualiiIaioミs so the┞ Iaミ illegall┞ マake マoミe┞ at ┞ouヴ e┝peミse. These people ┘ill appeaヴ to He ┞ouヴ fヴieミds, sa┞iミg the┞’ヴe tヴ┞iミg to help ┞ou. The┞ マa┞ do┘ミpla┞ oヴ deミ┞ the iマpoヴtaミIe of Ioマpl┞iミg ┘ith the la┘ aミd suggest that it’s all just さヴed tapeざ that e┗eヴ┞oミe igミoヴes. Doミ’t allo┘ ┞ouヴself to He fooled.

BE “MART

• Befoヴe ┞ou sigミ aミ┞thiミg, ヴead aミd マake suヴe ┞ou uミdeヴstaミd it.

• Refuse to sigミ aミ┞ Hlaミk doIuマeミts.

• AIIuヴatel┞ ヴepoヴt ┞ouヴ iミIoマe, ┞ouヴ eマplo┞マeミt, ┞ouヴ assets, aミd ┞ouヴ deHts.

• Doミ’t Hu┞ pヴopeヴt┞ oヴ Hoヴヴo┘ マoミe┞ foヴ soマeoミe else.

• DisIlosuヴe of loaミ teヴマs is ミot just a foヴマalit┞. It’s the la┘ aミd ┞ou ha┗e the ヴight to kミo┘.

BE HONE“T

• Doミ’t Ihaミge ┞ouヴ iミIoマe ta┝ ヴetuヴミs foヴ aミ┞ ヴeasoミ.

• Tell the ┘hole tヴuth aHout マoミe┞ gits.

• Doミ’t list fake Io-Hoヴヴo┘eヴs oミ ┞ouヴ loaミ appliIaioミ.

• Be tヴuthful aHout ┞ouヴ Iヴedit pヴoHleマs, past aミd pヴeseミt.

• Be hoミest aHout ┞ouヴ iミteミioミ to oIIup┞ the house.

• Doミ’t pヴo┗ide false suppoヴiミg doIuマeミtaioミ.

DON’T BE DI“COURAGED

If ┞ouヴ loaミ is deミied, the leミdeヴ ┘ill tell ┞ou ┘h┞. Ma┞He ┞ou ミeed to look foヴ a less e┝peミsi┗e house, oヴ sa┗e マoヴe マoミe┞. CheIk to see if theヴe is マoヴe afoヴdaHle housiミg oヴ Ioママuミit┞ pヴogヴaマs ┞ou マight He eligiHle foヴ to help ┞ou thヴough ┞ouヴ hoマe Hu┞iミg pヴoIess.

Predatory Leミdiミg

Youヴ Hest defeミse agaiミst illegal oヴ uミethiIal pヴaIiIes is to He iミfoヴマed.

Pヴedatoヴ┞ loaミs aヴe usuall┞ Hased oミ dishoミest┞. Pヴedatoヴ┞ leミdeヴs ofeヴ eas┞ aIIess to マoミe┞, Hut oteミ use high-pヴessuヴe sales taIiIs, iミlated iミteヴest ヴates, outヴageous fees, uミafoヴdaHle ヴepa┞マeミt teヴマs, aミd haヴassiミg IolleIioミ taIiIs. Pヴedatoヴ┞ leミdeヴs taヴget those ┘ho ha┗e liマited aIIess to マaiミstヴeaマ souヴIes of Iヴedit. The eldeヴl┞, マilitaヴ┞ peヴsoミミel aミd hoマeo┘ミeヴs iミ lo┘-iミIoマe ミeighHoヴhoods aヴe oteミ ┗iIiマs of pヴedatoヴ┞ leミdiミg. But aミ┞oミe Iaミ He a ┗iIiマ of a pヴedatoヴ. Ho┘ to A┗oid a Pヴedatoヴ┞ Loaミ: Fiミdiミg the Hest loaミ is ミo difeヴeミt thaミ マakiミg aミ┞ otheヴ puヴIhase. Be a sマaヴt shoppeヴ! Talk ┘ith a ミuマHeヴ of difeヴeミt leミdeヴs. Coマpaヴe theiヴ ofeヴs. Ask ケuesioミs aミd doミ’t let aミ┞oミe pヴessuヴe ┞ou iミto マakiミg a deal that ┞ou doミ’t feel IoマfoヴtaHle ┘ith. If ┞ou doミ’t agヴee ┘ith the teヴマs of the ofeヴ ┞ou al┘a┞s ha┗e the ヴight to ┘alk a┘a┞. Ask ケuesioミs uミil ┞ou uミdeヴstaミd the loaミ teヴマs – e┗eミ if ┞ou feel eマHaヴヴassed foヴ ミot kミo┘iミg the aミs┘eヴ.

TIP: Iミ a ヴeiミaミIe loaミ oヴ seIoミd マoヴtgage ┞ou ha┗e the ヴight to IaミIel the loaミ. This is kミo┘ミ as the Right of ResIissioミ. The leミdeヴ マust allo┘ ┞ou thヴee da┞s ateヴ the Ilosiミg of ┞ouヴ loaミ to Ihaミge ┞ouヴ マiミd. Use that thヴee da┞s ┘isel┞ if the loaミ is ミot foヴ ┞ou, IaミIel it.

Coママoミ Pヴedatoヴ┞ Leミdiミg PヴaIiIes:

• Eケuit┞ “tヴippiミg: The leミdeヴ マakes a loaミ Hased upoミ the eケuit┞ iミ ┞ouヴ hoマe, ┘hetheヴ oヴ ミot ┞ou Iaミ マake the pa┞マeミts. If ┞ou Iaミミot マake pa┞マeミts, ┞ou Iould lose ┞ouヴ hoマe thヴough foヴeIlosuヴe.

• Bait-aミd-s┘itIh sIheマes: The leミdeヴ マa┞ pヴoマise oミe t┞pe of loaミ, iミteヴest ヴate, oヴ Iosts, Hut s┘itIh ┞ou to soマethiミg difeヴeミt at Ilosiミg. “oマeiマes a higheヴ ふaミd uミafoヴdaHleぶ iミteヴest ヴate doesミ’t kiIk iミ uミil マoミths ateヴ ┞ou’┗e Heguミ to pa┞ oミ ┞ouヴ

GUIDE TO HOME LOANS ヱヲ “ECTION ン

page 34

loaミ. “Iヴuiミize ┞ouヴ doIuマeミts Ilosel┞ aミd マake suヴe the loaミ ┞ou sigミ is the loaミ ┞ou agヴeed to.

• Loaミ Flippiミg: A leミdeヴ ヴeiミaミIes ┞ouヴ loaミ マoヴe thaミ oミIe ┘ith a ミe┘ loミg-teヴマ, high Iost loaミ. EaIh iマe the leミdeヴ さlipsざ the e┝isiミg loaミ, ┞ou マust pa┞ poiミts aミd assoヴted fees.

• PaIkiミg: You ヴeIei┗e a loaミ that Ioミtaiミs Ihaヴges foヴ seヴ┗iIes ┞ou did ミot ヴeケuest oヴ ミeed. さPaIkiミgざ マost oteミ iミ┗ol┗es マakiミg ┞ou Helie┗e that Iヴedit iミsuヴaミIe oヴ soマe otheヴ Iostl┞ pヴoduIt マust He puヴIhased aミd iミaミIed iミto the loaミ iミ oヴdeヴ to ケualif┞. “oマeiマes the Iosts of these seヴ┗iIes マa┞ siマpl┞ He hiddeミ altogetheヴ.

• Hiddeミ Ballooミ Pa┞マeミts: You Helie┗e that ┞ou’┗e applied foヴ a lo┘ ヴate loaミ ヴeケuiヴiミg lo┘ マoミthl┞ pa┞マeミts oミl┞ to leaヴミ at Ilosiミg that it’s a shoヴt-teヴマ loaミ that ┞ou ┘ill ha┗e to ヴeiミaミIe ┘ithiミ a fe┘ ┞eaヴs.

• Hidiミg oヴ L┞iミg AHout Pヴe-Pa┞マeミt Peミalies: You aヴe led to Helie┗e that theヴe ┘ill He ミo peミalt┞ if ┞ou deIide to pa┞ ┞ouヴ loaミ of eaヴl┞.

• Hoマe Iマpヴo┗eマeミt “Iaマs: A IoミtヴaItoヴ talks ┞ou iミto Iostl┞ oヴ uミミeIessaヴ┞ ヴepaiヴs, steeヴs ┞ou to a high-Iost マoヴtgage leミdeヴ to iミaミIe the joH, aミd aヴヴaミges foヴ the loaミ pヴoIeeds to He seミt diヴeItl┞ to the IoミtヴaItoヴ. Iミ soマe Iases, the IoミtヴaItoヴ peヴfoヴマs shodd┞ oヴ iミIoマplete ┘oヴk, aミd ┞ou aヴe stuIk pa┞iミg of a loミg-teヴマ loaミ ┘heヴe the house is at ヴisk.

• Moミthl┞ Pa┞マeミt “Iaマs: Doミ’t He tヴiIked H┞ deIepi┗e pa┞マeミt Ioマpaヴisoミs. Be paヴiIulaヴl┞ a┘aヴe ┘heミ Ioマpaヴiミg the ミe┘ マoミthl┞ pa┞マeミt to ┞ouヴ e┝isiミg マoミthl┞ pa┞マeミt. Does the ミe┘ pa┞マeミt Ioミtaiミ aマouミts foヴ ta┝es aミd iミsuヴaミIe? Will the lo┘eヴ pa┞マeミt adjust up┘aヴd ateヴ a shoヴt iマe?