Employee Benefits Guide

The High companies are committed to helping co-workers and their families live the healthiest lives possible. Your health and wellness are important to you and your family; they are also important to High. After all, a healthy workforce is the key to the sustainability and future of the company. Over the past several years, High’s Health Management Program has worked to support co-workers in building health-ier lifestyles through programs and activities that encourage taking small steps to making health-ier changes.

Throughout the course of the year, High offers various wellness activities for co-workers and their families to participate in and earn incentives and rewards. Co-workers and their spouses who participate in the High health plan can participate in the annual biometric screening to earn reduced rates on their annual health care premiums.

Who: All full-time co-workers and their medical plan-covered spouse.

What: Participants will have six key health indicators measured: glucose, waist circumference, blood pressure, HDL, LDL, and triglycerides.

When: Biometric screenings are conducted annually at various High locations during the month of September. Individuals who wish to have their biometrics completed by their physician can submit values taken any time between June 1 and September 30, 2025. All affidavits must be received by Penn Medicine Health Works by end of business September 30, 2025.

Why: Meet or improve upon four out of the six key health indicators from last year’s screening and avoid paying an additional $7 per week or an additional $10 per week for not participating at all. That is a savings of up to $520 annually, or $1,040 if both you and your covered spouse choose not to participate.

Who: All co-workers enrolled in High’s health plan.

What: Complete the nicotine affidavit indicating whether you and/or your spouse (if enrolled in the medical plan) are nicotine users.

Co-workers who attest to being non-nicotine users may receive a cotinine test (measures nicotine in the bloodstream) during the biometric screening or during random testing throughout the year.

When: Complete the nicotine affidavit during a biometric screening event. Co-workers who complete the screening through their own physician should see their HR representative or general manager, or contact Jenni Simmons, Benefits Administrator.

Why: A co-worker who uses nicotine or a co-worker who does not complete the nicotine affidavit pays an additional $30 per month. A co-worker pays an additional $30 per month for a spouse who also uses nicotine for a possible total of $60 per month. Contact Jenni Simmons in benefits to find out details on how to stop this deduction and get your year-to-date deduction refunded.

Tobacco use is the leading cause of preventable death, disease, disability, and loss of productivity in the United States. High is committed to assisting co-workers with improving their health by providing tobacco cessation resources. Take advantage of:

• 80% reimbursement of over-the-counter cessation products up to a lifetime maximum of $300 for all co-workers and spouses, regardless of benefit plan enrollment. With a prescription, many over-the-counter cessation products, including the nicotine patch, gum and lozenge, are covered at 100% up to a 180-day treatment regimen.

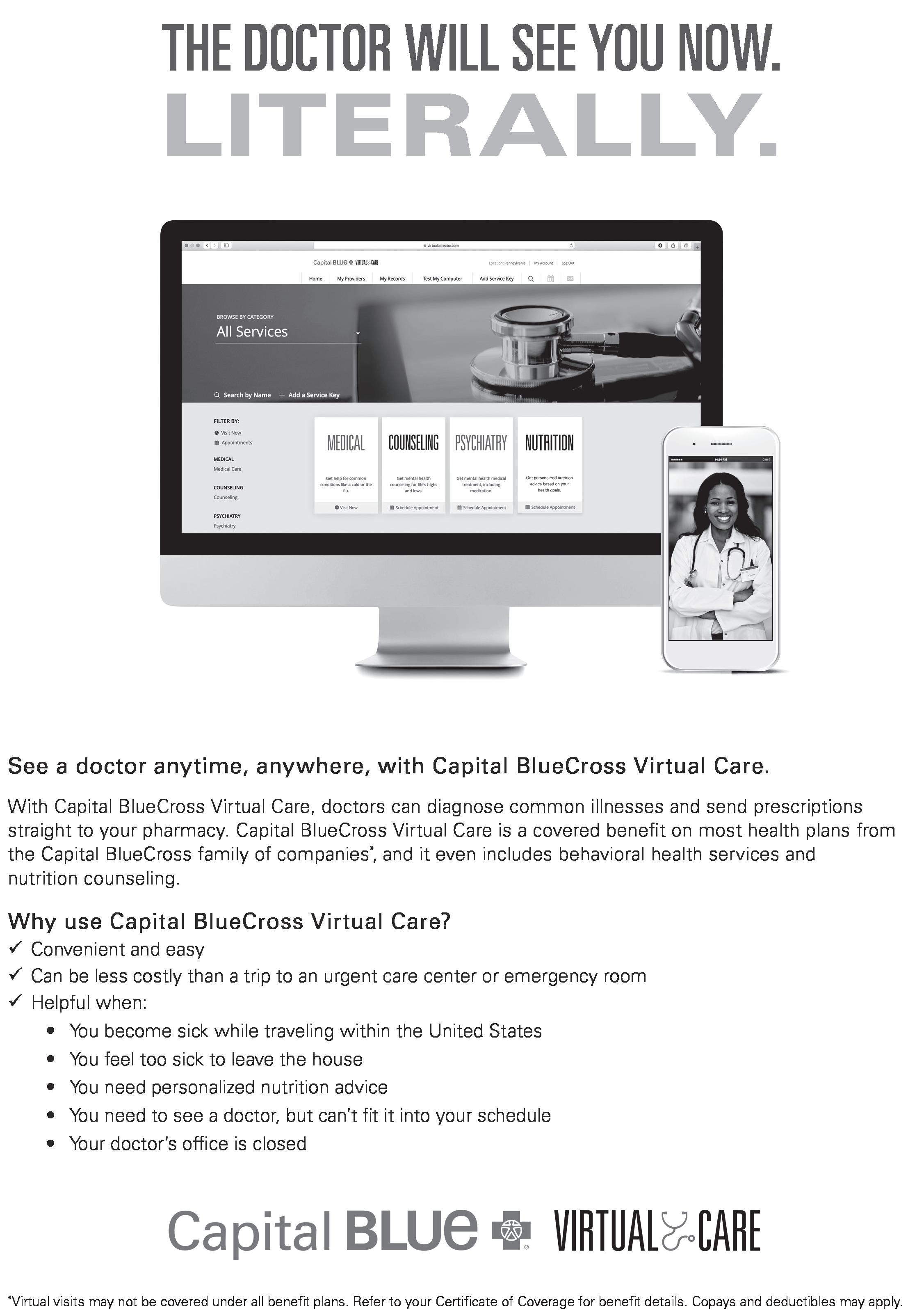

Opening November 12, 2024! All full-time coworkers and any medical plan enrolled dependents are invited to visit the High Health and Wellness Center at 1858 Charter Lane, Suite 203, Lancaster or any other Penn Medicine Healthworks locations open to our coworkers. Get access to same-day or nextday appointments, free commonly prescribed medications, counseling services, primary care services and virtual visits with no copay. Schedule an appointment by calling 717-544-8085. Get the care you need, when you need it most!

HIGH’S HEALTH MANAGEMENT PROGRAM IS COMMITTED TO HELPING YOU BE YOUR BEST SELF!

GET ACTIVE…For substantial health benefits, adults should do at least 150 minutes a week of moderate-intensity (or 75 minutes of vigorousintensity) aerobic activity, or an equivalent combination of moderate- and vigorous-intensity aerobic activity, plus two days of strength training. Strong evidence suggests that physical activity reduces the risks of chronic conditions and several cancers.

BE PROACTIVE…Chronic diseases are responsible for 7 of every 10 deaths among Americans each year and account for 75% of health spending. These chronic diseases can be largely preventable and detected through appropriate screenings. (Source: CDC)

Submit proof of purchase of any of the health-related products or services listed below and receive up to a maximum of $300 annually.

COVID-19 VACCINE

FITNESS EQUIPMENT:

per full vaccine cycle $50 for New Hires received prior to hire date

Cross Country Ski Machine, Treadmill, Elliptical Trainer, Stationary Bike, Rowing Machine, Stair Stepper, Ankle & Hand Weights, Resistance Bands and Tubing, Weight Bench, Fitness Tracker, Pedometer, Bicycle, Bicycle or Rollerblade Helmet, Roller Blades, Knee/Elbow Pads, Jump Rope, Exercise Videos, foam rollers, TENS units Up to $150

FITNESS CLASSES: (not included in a gym membership); examples include yoga, Zumba®, Pilates, POUND® and boot camp

GYM MEMBERSHIP Membership fee, up to $25 per month

BOUTIQUE GYM/STUDIOS (ex: Orangetheory, yoga): Ifunlimitedaccessyoumustattendatleast12timespermonth

FITNESS EVENT PARTICIPATION examples include a 5K, half/full marathon, cycling event or mud/obstacle course run

PREVENTIVE TESTS OR EXAMS: Colon cancer screening (age 50+), Skin Cancer Exam, COVID-19 vaccine Booster, Pneumonia Vaccine, Meningococcal Vaccine, MMR Vaccine, Tetanus Vaccine, Hepatitis Vaccine, Routine Physical Examination at Primary Care Physician, Shingles Vaccine (ages 50+), HPV Vaccine (ages 19-26), Dental Exam, Vision Exam Women Only: Pap Test, Bone Density Scan, Mammogram Men Only: Prostate Screening, Abdominal Aortic Aneurysm Screening

WEIGHT LOSS PROGRAM (pre-approval needed by health coach)

TOBACCO/NICOTINE CESSATION PROGRAM (pre-approval needed by health coach)

Up to $25 per month

to 100 per event

$50 per test or exam

Enrolled spouses can submit proof of preventative tests/exams to receive $50 up to $300 max.

Payment receipt & High form signed by instructor

Payment receipt from gym plus printout from swipe card showing you worked out at least 12 times per month

Payment receipt plus attendance printout or complete High form signed by instructor

Payment receipt & copy of race bib or finishing time

Explanation of Benefits from the insurance carrier or copy of your bill from the provider showing what service was performed

RETIRE SECURE MEETING attendance with a representative from Principal Financial Group, in person or telephonically $25 per meeting (limit one per year) Verified by Principal Financial Group

PEACE UNIVERSITY Cost of Program Certificate of Completion

Submit a copy of your receipt, Explanation of Benefits, and/or proof of gym attendance to: Jenni Simmons, Corporate Benefits Administrator, jsimmons@high.net

Regular, full-time and part-time co-workers are encouraged to participate. Products and services must be purchased for the benefit of the co-worker. Excludes fitness attire, nutritional supplements, food items, and fitness equipment maintenance and repairs.

You

www.mylifevalues.com

www.virtualcarecbc. com 833-433-5914

A Health Care Flexible Spending Account (FSA) is a way to pay for out-of-pocket medical, dental, vision, prescription expenses and some over-the-counter items on a pre-tax basis.

The minimum annual pledge is $100 and the maximum annual election is $3,300. Your annual election is divided by the number of pay periods in a year and deducted from your pay on a pre-tax basis. IRS regulations allow you to carry over unused balances of up to $660 for expenses incurred in the next year and still contribute up to $3,300 annually.

An FSA debit card is a convenient tool that is linked directly to your FSA account. In order to comply with IRS regulations, WEX, the plan administrator, may ask you to provide a detailed receipt to show that your purchase is eligible under the IRS guidelines. Always keep your receipts and Explanation of Benefits for items you purchase with your debit card.

Claims may also be submitted online, via fax, WEX’s mobile app or US mail. Unsubstantiated claims will be considered an ineligble expense and subject to payroll withholding.

Dependent Care Flexible Spending Accounts are designed to help you pay for childcare expenses on a pre-tax basis.

You may contribute up to $5,000 annually on a pre-tax basis to pay for childcare which allows you to work outside of the home. This includes daycare, before and after-school care and day camps. Unlike a Health Care FSA, a Dependent Care FSA does not allow you to be reimbursed for expenses greater than your current account balance.

For more information about the benefits of Flexible Spending Accounts call 866-451-3399 or visit Wex’s website benefitslogin.wexhealth.com

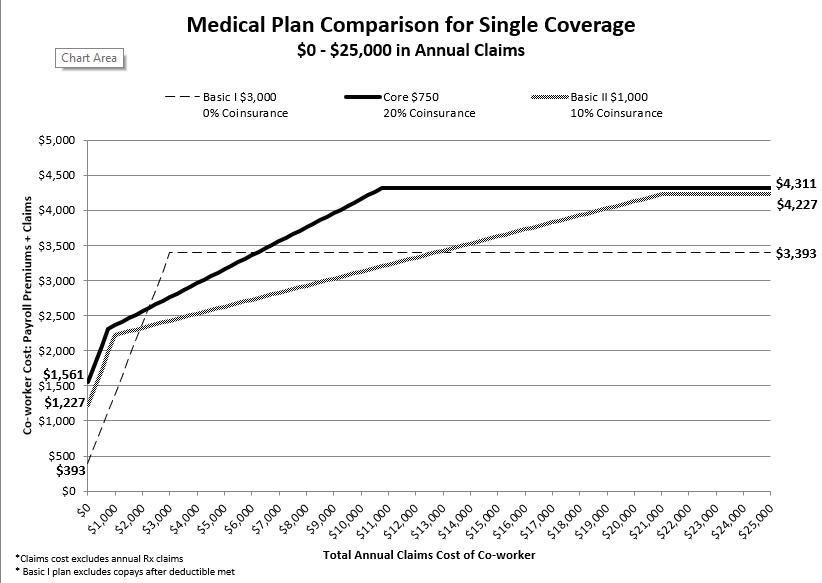

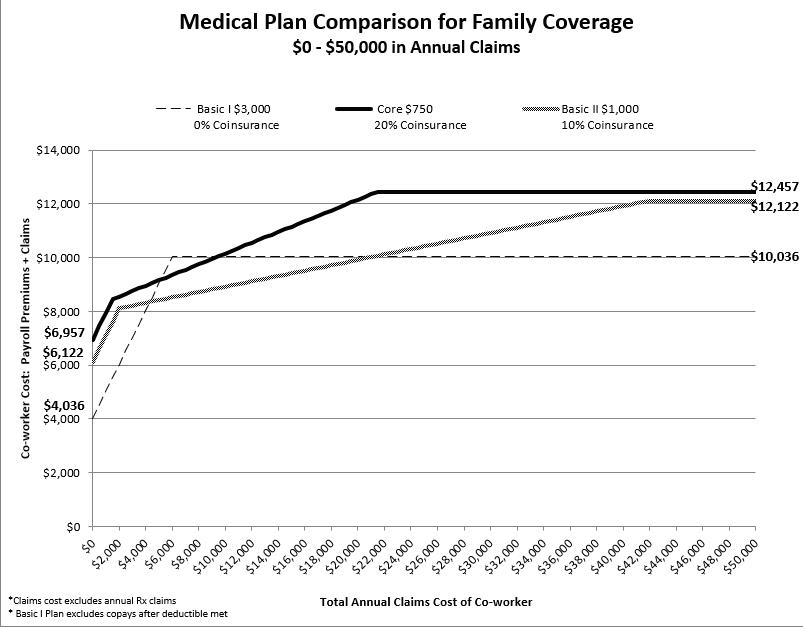

An overview of our Capital Blue Cross medical plan options and costs is shown below. High wants you to understand the differences between the options so you select the right plan for you and your family. Please refer to your Certificate of Coverage for specific terms, conditions, exclusions, and limitations relating to our coverage.

How does my medical coverage work? See pages 25-45 for the Summary of Benefits Coverage.

1Once deductible is met, only co-pays (both medical & Rx) apply until the out-of-pocket maximum of $6,850/$13,700 is reached. 2Add an additional $10.00/week surcharge if you elected not to participate in the biometric

or $7.00/week if you did not meet or improve upon four of the six key health indicators. If you did not complete a nicotine affidavit, if you and/or your spouse attest to using nicotine products or you attested to not using nicotine but did not produce a negative

will be added.

Your decision could be based on a number of factors, including your age, number of dependents and anticipated health care expenses. To guide you in your decision making, illustrations of potential in network out-of-pocket expenses for each plan are shown below.

1 Excludes additional $10/week surcharge paid by screening nonparticipants or $7/week surcharge paid by those who did not meet or improve upon four of six key health indicators, and/or did not sign a nicotine affidavit.

2 For all plans, co-pays still apply once the out-of-pocket maximum is met.

3For Basic I plan, only copays apply until OOP Max is met. Figures rounded to the nearest dollar.

90DayMyWay® allows members to fill maintenance medications – ones they take regularly to manage chronic conditions – through home delivery or at any participating retail pharmacies. Express Scripts is your home delivery pharmacy for 90-day maintenance drugs. Please allow 14 days for delivery. Call 855-924-8421 or visit www. capbluecross.com to set up your account and provide payment information.

Generic Substitution programs help to reduce out-ofpocket expenses and help to contain the rising costs of providing prescription drug benefits. Our program allows your doctor to specify that a brand name drug be dispensed by indicating “No Generic Substitution Permissible” on the written prescription. In this case, you will only be charged the brand name cost share. But, if you request a brand name drug when a generic is available, you will be charged the brand name cost share plus the cost difference between the generic and brand name medication.

Auto Refill is available for mail order medications so they are automatically sent to you until all refills are used or your prescription expires. You must sign up for this feature for each new prescription sent to Prime Therapeutics®

Prior Authorization is a process to help ensure that certain drugs are prescribed appropriately and within FDA guidelines. You can identify these drugs on the Prime Therapeutics® formulary list as those listed with a PAR symbol next to them. To help prevent possible delays in filling your prescription, you or your physician should request a prior authorization before your prescriptions are filled.

Step Therapy applies to certain medications subject to enhanced prior authorization. In order to have these medications covered under your prescription drug benefit,

you may be required to first try a formulary alternative or complete the authorization process. To obtain authorization, your physician should call or fax a request with supporting clinical information to Prime Therapeutics®

Please refer to your Certificate of Coverage for specific terms, conditions, exclusions, and limitations relating to our coverage.

For questions regarding your prescription plan contact Blue Cross Member Services at 866-802-4780.

www.e-nva.com • 800-672-7723

Each covered individual is eligible for an exam plus one pair of lenses and frames or one set of contact lenses each calendar year.

Each member has an Eye Essential plan which provides plan discounts once you have exhausted your annual vision benefits. This plan is only for network providers. Using a participating provider will give you a greater benefit. Find a participating provider near you who provides full or limited services on NVA’s website.

A regular eye exam will cost you $5.00 at a participating NVA provider. Contact lens exams are not part of the $5.00 benefit.

You are able to purchase your lenses and frames at wholesale prices which can add

up to significant savings.

If you purchase contact lenses at a participating provider you will receive a 25% discount off of retail cost.

If you choose not to use a participating provider the reimbursement schedule is as follows:

$56 for exam and tomometry

$54 for lenses

$40 for frames

$94 for contacts only (uses both lens and frame allowance)

The maximum reimbursement for nonnetwork provider services is $150.00.

www.deltadentalins.com 800-932-0783

100% paid for preventive care – 2 exams per calendar year

$50 deductible for all services except preventive care.

$1500 annual maximum paid per covered individual.

$2000 lifetime maximum for orthodontia for dependent children

80% coverage for fillings, extractions, root canals, endodontics and periodontics.

50% coverage for crowns, bridges, dentures and implants.

Bony impacted wisdom teeth are considered a medical procedure. All other impactions are covered under your dental plan at 80%.

Find a participating Delta provider near you at www.deltadentalins.com

If you select a Delta Dental provider you will receive a greater benefit and will not need to file claim forms. Going out-of-network will result in you having to file a claim, receiving reimbursement from Delta Dental, and paying your provider an amount which may be over usual and customary rates with Delta Dental.

NVA has partnered with NationsHearing to offer a hearing aid discount program. Schedule a no-cost hearing test and receive up to 60% savings on hearing aids starting as low as $500.

Get started now by visiting NationsHearing. com/NVA to find additional information on program benefits. Call 877-272-9627 for assistance locating a provider.

Supplemental Life is a voluntary benefit. You can purchase coverage valued at 1/2, 1, 2 or 3 times your salary. When selecting your coverage please use ONLY THOSE AMOUNTS. No other values will be honored by UNUM, the insurance carrier. This is in addition to the basic life and accidental death dismemberment insurance the company provides at no cost to you. If you are not a new coworker and this is your first time enrolling in this benefit, you will be required to complete Evidence of Insurability paperwork, which will be mailed to your home.

The cost of this benefit is determined by a combination of your salary and your age. (Below is a list of the amounts charged per $1000 of coverage.)

Age: Rate per $1000:

25 .048

25 to 29 .057

30 to 34 .067

35 to 39 .076

40 to 44

45 to 49

to 54 .218

to 59 .410

to 64 .627

Coverage for child(ren) is $4,000. The cost for one child is $0.16 per week and the cost for two or more children is $0.32 per week.

Spouse life insurance is available in increments of $10,000, up to a maximum of 50% of a your total life insurance value. Spouse life insurance coverage can be calculated using the above supplemental life rates and the age band based on the your age (not your spouse’s age).

If you elect this benefit for the first time after your initial enrollment or increase your current supplemental life insurance amount above $50,000 you’ll be required to complete a health questionaire mailed to your home.

1. Multiply your hourly rate by 40 (hours)

2. Multiply the result by 52 (weeks). This is your annual base earnings.

3. Decide if you want coverage in the amount of:

• Half your annual base salary (divide by 2)

• Your annual base salary (remains the same)

• Twice your annual base salary (multiply by 2)

• Three times your annual base salary (multiply by 3)

4. Then round the figure up to the next $1000.

5. Move the decimal point three spaces to the left.

6. Multiply the premium listed for your age range as above.

7. This is your monthly premium. Multiply this figure times 12, then divide by 52 for your weekly premium, or divide by 26 for your bi-weekly premium.

Assume your hourly rate is $12.00 AND you are choosing 3X your annual base earnings:

$12.00 x 40 (hours) = $480.00

$480.00 x 52 (weeks) = $24,960.00 (this is your annual base earnings)

Multiply $24,960 x 3 (3x base salary) = $74,880.00

Round to the next $1000 = $75,000.00

Move decimal point three spaces to the left = $75.00

Assume your age is 42. You fall into the “40 to 44” category and your rate per $1000 would be .094.

Multiply .094 x 75 = $7.05 per month

7.05/month x 12 months = $84.60

Divided by 52 (weeks) = $1.63 per pay

You will be enrolled in the High Company 401(k) Retirement Plan after completing 30 days of service.

Highlights of this retirement plan benefit include:

• Automatic enrollment at 6% with a 1% annual auto-increase up to 12%.

• Company match of 100% of the first 2% and 50% of the next 4% deferred.

• 100% vesting after two years of service (minimum of 1000 hours worked).

• Contribute up to 100% of your pre-tax income up to the annual 401(k) contribution limits.

• After-tax Roth salary deferral contributions allowed.

• Salary deferral amounts may be changed weekly.

Your account is administered by Principal Financial Group and once enrolled, you can log in to your account at principal.com to take advantage of these helpful resources.

• Get your Retirement Wellness Score and check out the Retirement Wellness Planner to see if you’re on track with your retirement savings.

• Monitor your investments and their performance.

• Improve your financial wellness by visiting Principal Milestones.

• Download the Principal app to manage your account on-the-go.

• Meet with a Principal Retire Secure™ representative by scheduling a time at principal.com/1on1.

Refer to the Summary Plan Description for additional details. Account information can be found at www.principal.com or by calling Principal Financial Group at 800-547-7754.

Do you or your dependents have diabetes or prediabetes? Diabetes Connections aims to link you and your dependents who have diabetes with the support, education and tools necessary to improve health and well-being.

Any co-worker or dependent on High’s medical insurance plan who has diabetes or prediabetes is eligible. New to Diabetes Connections, any co-worker (or dependent) at any work location may participate (either in person or over the phone). Together, the participant and health coach will make and work towards long-term health and well-being goals. A participant in Diabetes Connections will be expected to meet with the health coach monthly for the first six months and then quarterly, or on a different schedule as determined by the health coach and participant. Participants also will be required to provide to the health coach proof of meeting health guidelines (like getting an annual eye exam, an annual flu shot, getting your A1c checked, etc.). Results will remain confidential with the health coach.

Along with the support that a participant will receive, all co-pays for medications for diabetes, high cholesterol and high blood pressure, as well as diabetic supplies, will be paid by High for up to three years. Also, you will receive $35 towards each A1c test. These incentives are payable as long as you fulfill the program requirements. Depending on the frequency of meetings, you also may be eligible for a Healthy Rewards incentive.

Applying for Diabetes Connections is simple— just contact Jenni Simmons (jsimmons@high. net or 717-293-4503) or the health coach to get started. Questions are welcomed!

To Enroll: Go to myinfo.high.net OR https://e14.ultipro.com . The log in screen will appear, then proceed to #1.

1. Logon

User Name: Your last name + last 4 digits of your SSN

If you have been hired in the past year and have not accessed UKG, your password is your birthday. Password: Your date of birth as MMDDYYYY. Example: March 17, 1958 would be 03171958

If you do not remember your password, use the password reset option under the Log In button.

If your account has become inactive or you require a password reset, contact:

2.

3. HR Solution Center 717-209-4034 or email hrsolutions@high.net

To add information for dependents that you wish to add to your plan or as a beneficiary. Go to Menu – Myself –Personal – Contacts – Add Contact (top right)

To begin the annual Open Enrollment process, go to Menu – Myself – Open Enrollment -- select 2025 AE Enrollment Session.

To begin New Hire process, go to Menu – Myself – Life Events --- I am a new coworker

4. Click on the Blue Arrows ( Back & Next ) at the top of the screen to navigate through the enrollment session.

5. To save an incomplete enrollment session, click the Draft button at the top of the screen. Verify Beneficiary and Dependent Information

Medical

Dental

Vision

Group Term Life Insurance

Employee Supplemental Life

Spouse Supplemental Life

Child Supplemental Life

Flexible Spending Account

Confirm Your Changes

Make election

Make election

Make election

Make election

Make election

Make election

Make election

Make election

Submit

6. To elect or change your Medical election, click Medical then choose the plan and coverage option you wish to enroll OR select “I decline” coverage.

a. If you chose a coverage level which includes dependent(s) coverage, within the Enroll Dependents box, check the box for each dependent you wish to enroll.

b. Use the at the top of the screen to proceed to the next election.

7. To elect or change your Dental election, click Delta Dental then choose the coverage option you wish to enroll OR select “I decline” coverage.

a. If you chose a plan option which includes dependent(s) coverage, within the Enroll Dependents box, check the box for each dependent you wish to enroll.

b. Use the at the top of the screen to proceed to the next election.

8. To change your Vision election, click Vision then choose the coverage option you wish to enroll OR select “I decline” coverage.

a. If you choose a coverage level which includes dependent(s) coverage, within the Enroll Dependents box, check the box for each dependent you wish to enroll.

b. Use the at the top of the screen to proceed to the next election.

9. You are automatically enrolled in Group Term Life. If you wish to change your beneficiaries, click Group Term Life / AD&D, otherwise use the to proceed to the next election.

a. Select coverage (only a single benefit amount is available).

b. Within the Enroll Beneficiaries box, check the box for each beneficiary you wish to enroll.

c. Primary and secondary beneficiary percentages must total 100%.

d. Use the at the top of the screen to proceed to the next election.

10. If you wish to elect or change your Employee Supplemental Life election, click Supplemental Life, then enter the Benefit Rate OR select “I decline” coverage.

a. The only allowed benefit rate values are .5, 1, 2 or 3 times base salary.

b. If you choose supplemental life coverage, within the Enroll Beneficiaries box, check the box for each beneficiary you wish to enroll.

c If you are enrolling in this plan for the first time or if you are increasing more than 1 step you will need to complete an evidence of insurability questionaire.

d. Primary and Secondary beneficiary percentages must total 100%.

e. Use the at the top of the screen to proceed to the next election.

11. If you wish to elect or change your Spouse Supplemental Life election, click Spouse Life Insurance OR select “I decline” coverage

a. The Spouse Life benefit amount can only be elected in $10,000 increments with a $10,000 minimum and a $500,000 maximum.

b. The benefit is capped at ½ the co-worker total Basic Life + Supplemental Life Benefits rounded down to the nearest $10,000 level.

c. Use the at the top of the screen to proceed to the next election.

12. If you wish to elect or change your Child Supplemental Life election, click Dependent Life – Child / Children plan OR select “I decline” coverage.

a. If you chose a coverage level which includes dependent(s) coverage, within the Enroll Dependents box, check the box for each dependent you wish to enroll.

b. Use the at the top of the screen to proceed to the next election.

13. To enroll in a Flexible Spending Account (Healthcare), you must click Flexible Spending Health (FSA) or select “I decline” the Flexible Spending Health plan.

a. If you chose to enroll in the Health FSA, you must select a contribution amount. Enter the contribution amount in the per pay period option.

Amount Per Pay Period

$0.00 per pay period

b. Tab to the Goal Amount box to automatically calculate your annual contribution. You may override the calculated annual goal with a lower amount.

c. Use the at the top of the screen to proceed to the next election.

14. To enroll in a Flexible Spending Account (Dependent Care) for your dependents, you must click Flexible Spending Dependent or select “I decline” the Flexible Spending Dependent plan. (This is DAYCARE for your children)

a. If you chose to enroll in the Dependent FSA, you must select a contribution amount. Enter the contribution amount in the per pay period option.

Amount Per Pay Period

$0.00 per pay period

b. Tab to the Goal Amount box to automatically calculate your annual contribution. You may override the calculated annual goal with a lower amount.

15. At this point you have completed the enrollment elections. You may now exit OR submit FINAL elections.

a. To Exit and not submit FINAL elections, click the DRAFT button at the top of the page to save your work, then click the Cancel button to leave the enrollment session. (Your work has been saved)

b. If you are ready to confirm and submit your final elections, use the at the top of the screen to proceed to Confirm Your Changes.

16. Confirm your selections and changes.

a. If you wish to make changes, use the BLUE ARROW keys to navigate back to the benefit election page

b. Click the DRAFT button at the top of the page to save your work.

c. To print a summary of your old and new elections click the PRINT button at the top of the page.

d. If you are ready to FINALIZE your elections, click the SUBMIT button at the top of the page. When elections have been submitted, only a system administrator or HR Representative can reopen your elections. Make certain they are correct!

Click Log Off (top right of screen)

Q:Myspouseisnotemployed.CansheremainonHigh’s healthplanin2025?

A: A spouse can be covered under High’s health plan if she is not employed, is not eligible for her employer’s coverage, pays more than 35% of her employer’s lowest cost single coverage plan, or is self-employed. If employed, she will need to have her employer verify her coverage using the Spousal Verification form available on the last page of this guide.This form needs to be completed annually during open enrollment. This form is due in the benefits office by end of business day Friday, November, 22, 2024.

Q:Whycan’tIaddorremovedependentsfrommyhealth plancoverageatanytimeduringtheyear?

A: Our plan is considered a Section 125 plan which allows you to pay for your medical, dental and vision premiums with pre-tax dollars and lowers your taxable income by the amount of the premiums you pay. A Section 125 plan restricts you from making changes to your benefit elections unless you have a qualifying event (marriage, divorce, death of a covered dependent, birth of a child, dependent exceeding age limit, or loss of coverage under another medical plan). It is the coworker’s responsibility to notify the Benefits Department of a qualifying event within 30 days of its occurrence. No changes can be made after 30 days have lapsed. The next time you will be permitted to make a change to your election will be at open enrollment. Please note that all premiums for changes due to a qualifying event will be retroactive back to the actual date the event happened, not when you reported it.

Q: Can I still submit claims incurred in 2024 for reimbursementthroughmyflexiblespendingaccount (FSA)bytheendofMarch2025?

A:You can still submit claims incurred in 2024 to WEX through March 31, 2025. FSA participants can carry over up to $640 of their unused account balance from 2024 for use in 2024. The amount carried over will appear in your FSA account by May 2025. For example, if you had $400 remaining in your account as of December 2024, and elected to contribute $3,200 in 2025, your available account balance would be $3,600 in 2025. You cannot have any more than $640 in the rollover account.

Q:DoIneedtocompleteanothernicotineaffidavit ifIdidonelastyear?

A: Yes, each year you will be asked to complete the affidavit indicating whether you and /or your covered dependents are nicotine users. If you did not complete the affidavit during the on-site biometric screening events, you will need to

complete one and return it to Human Resources by the last date of open enrollment. Covered coworkers who attest to being nicotine free must complete a cotinine test with a negative result during a biometric screening event in order to avoid the nicotine surcharge. If you are covered under our benefits and choose not to participate in the screening process, you are still encouraged to complete the nicotine affidavit to avoid paying the nicotine surcharge.

Q:WilltherebeadifferenceinwhatIpayforhealthcoverageif Ididnotparticipateinthebiometricscreening?

A: If you chose not to participate, you will pay an additional $10 per week for coverage. If you did participate but did not meet or improve upon four of the six key health indicators from last year’s screening, you will pay an additional $7 per week. If you were hired after August 1st, 2024, you will automatically receive the preferred contribution rate assuming you participated in this year’s screening. A spouse covered under High’s health plan must also participate in the biometric screening or you will pay an additional $10 per week. If a spouse participated and did not meet or improve upon four of the six key health indicators from last year’s screening, you will pay an additional $7 per week.

Q:WillIbechargedformyannualphysicalorwillitbecovered 100%asapreventiveservice?

A: Although many preventive services are provided at no cost to you, the out-of-pocket expense depends on how your physician submits the claim to Capital Blue Cross. A list of preventive services can be found on www.capbluecross.com/ highindustries. There are limits to the number of physicals covered based on a member’s age and some, but not all, services done during a physical may be considered preventive. Call member services at Capital Blue Cross 866-802-4780 for specific coverage questions.

Q:WhydoIhavetosubstantiatemyFSAdebitcardtransactions?

A: When you swipe your debit card for vision and dental expenses, WEX only receives the total amount of the transaction and cannot tell if it is eligible for reimbursement. WEX preloads all of High’s copay amounts into their system, so you should not have to substantiate a standard copay. If you are required to substantiate a claim, send receipts or EOBs to them via fax, mail or online. Do not pay for 2024 expenses with your debit card in 2025 and instead file a claim online or by fax. IRS regulations prohibit you from paying a previous year’s expenses with money elected in the current year. Unsubstantiated claims may be considered an ineligible expense and subject to payroll withholding.

Allowed Amount – Maximum amount on which payment is based for covered health care services. This may be called “eligible expense,” “payment allowance” or “negotiated rate.” If your provider charges more than the allowed amount, you may have to pay the difference. (See Balance Billing.)

Appeal – A request for your health insurer or plan to review a decision or a grievance again. Balance Billing – When a provider bills you for the difference between the provider’s charge and the allowed amount. For example, if the provider’s charge is $100 and the allowed amount is $70, the provider may bill you for the remaining $30. A preferred provider may not balance bill you for covered services.

Co-insurance – Your share of the costs of a covered health care service, calculated as a percent (for example, 20%) of the allowed amount for the service. You pay co-insurance plus any deductibles you owe. For example, if the health insurance or plan’s allowed amount for an office visit is $100 and you’ve met your deductible, your co-insurance payment of 20% would be $20. The health insurance or plan pays the rest of the allowed amount.

Complications of Pregnancy – Conditions due to pregnancy, labor and delivery that require medical care to prevent serious harm to the health of the mother or the fetus. Morning sickness and a non-emergency caesarean section aren’t complications of pregnancy.

Co-payment – A fixed amount (for example, $15) you pay for a covered health care service, usually when you receive the service. The amount can vary by the type of covered health care service.

Deductible – The amount you owe for health care services your health insurance or plan covers before your health insurance or plan begins to pay. For example, if your deductible is $2500, your plan won’t pay anything until you’ve met your deductible for covered health care services subject to the deductible. The deductible may not apply to all services.

Durable Medical Equipment (DME) – Equipment and supplies ordered by a health care provider for everyday or extended use. Coverage for DME may include: oxygen equipment, wheelchairs, crutches or blood testing strips for diabetics.

Emergency Medical Condition – An illness, injury, symptom or condition so serious that a reasonable person would seek care right away to avoid severe harm.

Emergency Medical Transportation – Ambulance services for an emergency medical condition.

Emergency Room Care – Emergency services you get in an emergency room.

Emergency Services – Evaluation of an emergency medical condition and treatment to keep the condition from getting worse.

Excluded Services – Health care services that your health insurance or plan doesn’t pay for or cover.

Grievance – A complaint that you communicate to your health insurer or plan.

Habilitation Services – Health care services that help a person keep, learn or improve skills and functioning for daily living. Examples include therapy for a child who isn’t walking or talking at the expected age. These services may include physical and occupational therapy, speech-language pathology and other services for people with disabilities in a variety of inpatient and/or outpatient settings.

Home Health Care – Health care services a person receives at home.

Hospice Services – Services to provide comfort and support for persons in the last stages of a terminal illness and their families.

Hospitalization – Care in a hospital that requires admission as an inpatient and usually requires an overnight stay. An overnight stay for observation could be outpatient care.

Hospital Outpatient Care – Care in a hospital that usually doesn’t require an overnight stay.

In-network Co-insurance – The percent (for example, 20%) you pay of the allowed amount for covered health care services to providers who contract with your health insurance or plan. In-network co-insurance usually costs you less than out-of-network co-insurance.

In-network Co-payment – A fixed amount (for example, $20) you pay for covered health care services to providers who contract with your health insurance or plan.

Medically Necessary – Health care services or supplies needed to prevent, diagnose or treat an illness, injury, condition, disease or its symptoms and that meet accepted

standards of medicine.

Network – The facilities, providers and suppliers your health insurer or plan has contracted with to provide health care services.

Non-Participating Provider – A provider who doesn’t have a contract with your health insurer or plan to provide services to you. You’ll pay more to see a non-participating provider.

Out-of-network Co-insurance – The percent (for example, 40%) you pay of the allowed amount for covered health care services to providers who do not contract with your health insurance or plan. Out-of-network co-insurance usually costs you more than in-network co-insurance.

Out-of-Pocket Limit – The most you pay during a calendar year before your health insurance or plan begins to pay 100% of the allowed amount. This limit never includes your premium, balance-billed charges or health care your health insurance or plan doesn’t cover. Our health insurance plans count all of your co-payments, deductibles, and co-insurance payments toward this limit.

Physician Services – Health care services a licensed medical physician (M.D. – Medical Doctor or D.O. – Doctor of Osteopathic Medicine) provides or coordinates.

Preauthorization – A decision by your health insurer or plan that a health care service, treatment plan, prescription drug or durable medical equipment is medically necessary. Sometimes called prior authorization, prior approval or precertification. Your health insurance or plan may require preauthorization for certain services before you receive them, except in an emergency. Preauthorization isn’t a promise your health insurance or plan will cover the cost.

Participating Provider – A provider who has a contract with your health insurer or plan to provide services to you at a discount.

Premium – The amount that must be paid for your health insurance or plan. You usually pay it weekly or bi-weekly.

Prescription Drug Coverage – Health insurance or plan that helps pay for prescription drugs and medications.

Primary Care Physician – A physician (M.D. – Medical Doctor or D.O. – Doctor of Osteopathic Medicine) who directly provides or coordinates a range of health care services for a patient.

Primary Care Provider – A physician (M.D. – Medical Doctor or D.O. – Doctor of Osteopathic Medicine), nurse practitioner, clinical nurse specialist or physician assistant, as allowed under state law, who provides, coordinates or helps a patient access a range of health care services.

Provider – A physician (M.D. – Medical Doctor or D.O. – Doctor of Osteopathic Medicine), health care professional or health care facility licensed, certified or accredited as required by state law.

Reconstructive Surgery – Surgery and follow-up treatment needed to correct or improve a part of the body because of birth defects, accidents, injuries or medical conditions.

Rehabilitation Services – Health care services that help a person keep, get back or improve skills and functioning for daily living that have been lost or impaired because a person was sick, hurt or disabled. These services may include physical and occupational therapy, speech-language pathology and psychiatric rehabilitation services in a variety of inpatient and/or outpatient settings.

Skilled Nursing Care – Services from licensed nurses in your own home or in a nursing home. Skilled care services are from technicians and therapists in your own home or in a nursing home.

Specialist – A physician specialist focuses on a specific area of medicine or a group of patients to diagnose, manage, prevent or treat certain types of symptoms and conditions. A non-physician specialist is a provider who has more training in a specific area of health care.

UCR (Usual, Customary and Reasonable) – The amount paid for a medical service in a geographic area based on what providers in the area usually charge for the same or similar medical service. The UCR amount sometimes is used to determine the allowed amount.

Urgent Care – Care for an illness, injury or condition serious enough that a reasonable person would seek care right away, but not so severe as to require emergency room care.

Please read this information carefully and furnish the documents requested to provide proof of dependent eligibility. THIS DOCUMENTATION IS FOR NEWLY ADDED DEPENDENTS AND SPOUSES . IF YOUR DEPENDENTS AND SPOUSE ARE CURRENTLY COVERED BY OUR PLAN, YOU DO NOT NEED TO FURNISH THIS AGAIN. Failure to provide documentation within 30 days of your benefits eligibility date will result in non-coverage of those dependents until the next plan year.

The below matrix outlines the documentation options that you can submit to verify eligibility for each dependent enrolled with health coverage. Please note the following:

• Send photocopies only. Do not send original documents.

• Mark out any personal financial information such as income, account balances, payment amounts, etc.

• If documentation is not received within 30 days of benefit eligibility, dependent(s) will have coverage terminated retroactively to the effective date of coverage.

• A certified birth certificate is the only required documentation for a natural or step child less than one year of age.

• A Social Security card is not an acceptable form of documentation for a dependent.

Provide ONE document from EACH section to verify proof of relationship and proof of joint ownership.

• Certified Marriage Certificate or License - Photocopy of certified marriage certificate with appropriate signature and stamp/ seal showing on photocopy or legally valid marriage license from appropriate state or local government.

• Immigration Paperwork - Photocopy of immigration papers with appropriate signature and stamp/seal showing on photocopy that identifies employee/spouse relationship.

• Home Ownership - Photocopy of mortgage statement dated within the past 3 months showing both names as mortgage holders/tenants. Note: Please mark out all financial information.

• Joint Rental Property - Photocopy of lease or rental agreement dated within the past 12 months showing both names as tenants. Note: Please mark out all financial information.

• Home/Rental Insurance - Photocopy of homeowner’s insurance, renter’s insurance, or property tax receipt dated within the past 12 months showing both names as mortgage holders/tenants. Note: Please mark out all financial information.

• Bank Statement - Photocopy of joint bank account statement dated within the past 3 months showing both names as account holders. Note: Please mark out all financial information.

• Credit Card Statement - Photocopy of credit card statement dated within the past 3 months showing both names as card holders. Note: Please mark out all financial information.

• Loan Statement - Photocopy of a loan agreement dated within the past 12 months showing both names as co-borrowers. Note: Please mark out all financial information.

• Miscellaneous Bills - Photocopy of two different types of current bills dated within the past 3 months showing one of the spouse’s names on each bill and the same common mailing address, e.g. telephone bill, electric bill, cable bill. Note: Please mark out all financial information.

• Beneficiary Statement - Photocopy of designation as the primary beneficiary for life insurance or retirement benefits. Note: Please mark out all financial information.

• Driver’s License - Photocopy of the employee’s and spouse’s driver’s licenses listing a common address.

• Automobile Statement - Photocopy of automobile title or registration dated within the past 12 months listing both names as co-owners.

Provide ONE document from EACH section to verify proof of relationship and proof of Principal Support.

• Certified Birth Certificate - Photocopy of certified birth certificate with appropriate signature and stamp/seal showing on photocopy that identifies the parent/child relationship with the employee or spouse

• Hospital Verification of Birth (Less than 6 months old) - For children under 6 months old, photocopy of hospital verification of birth that identifies the employee or spouse as the child’s parent

• Certified Adoption Certificate - Photocopy of certified court approved adoption document with appropriate signature and stamp/seal showing on photocopy that identifies the employee or spouse as the child’s parent

• Adoption Agreement - Photocopy of placement letter/agreement from court or adoption agency that identifies the employee or spouse as the child’s parent

• Report of Birth Abroad - Photocopy of report of birth abroad of a citizen of the United States (issued by the State Department with appropriate signature and stamp/seal showing on photocopy) that identifies the employee or spouse parent/child relationship

• Court Ordered Health Coverage - Photocopy of Qualified Medical Child Support Order (QMCSO). Note: This document satisfies both Proof of Relationship and Proof of Principal Support.

• Court Ordered Health Coverage - Photocopy of National Medical Support Notice (NMSN). Note: This document satisfies both Proof of Relationship and Proof of Principal Support Court Ordered Health Coverage - Photocopy of court document with appropriate signature ordering child health coverage. Note: This document satisfies both Proof of Relationship and Proof of Principal Support.

• Certified Divorce Decree - Photocopy of certified Divorce Decree with appropriate signature and stamp/seal showing on photocopy that documents required child health coverage. Note:ThisdocumentsatisfiesbothProofofRelationshipandProof of Principal Support.

• Certified Legal Guardianship - Photocopy of certified court ordered legal guardianship document with appropriate signature and stamp/seal showing on photocopy that documents required child health coverage. Note: This document satisfies both Proof of Relationship and Proof of Principal Support.

• Immigration Paperwork - Photocopy of immigration papers with appropriate signature and stamp/seal showing on the photocopy that identifies the parent/child relationship with the employee or spouse.

• Court Ordered Health Coverage - Photocopy of Qualified Medical Child Support Order (QMCSO). Note: This document satisfies both Proof of Relationship and Proof of Principal Support.

• Court Ordered Health Coverage - Photocopy of National Medical Support Notice (NMSN). Note: This document satisfies both Proof of Relationship and Proof of Principal Support.

• Court Ordered Health Coverage - Photocopy of court document with appropriate signature ordering child health coverage. Note: This document satisfies both Proof of Relationship and Proof of Principal Support.

• Certified Divorce Decree - Photocopy of certified Divorce Decree with appropriate signature and stamp/seal showing on photocopy that documents required child health coverage. Note:ThisdocumentsatisfiesbothProofofRelationshipandProof of Principal Support.

• Certified Legal Guardianship - Photocopy of certified court ordered legal guardianship document with appropriate signature and stamp/seal showing on photocopy that documents required child health coverage. Note: This document satisfies both Proof of Relationship and Proof of Principal Support.

• Federal Tax Return - Photocopy of the first page of the employee’s or spouse’s most recent Federal Tax return showing the child listed as an eligible dependent. Note: Please mark out all financial information

• School or Medical Records - Photocopy of school or medical records for the child that indicates the employee’s address.

Proof of Relationship Documents continued on next page....

For Dependent Children over the age of 19 who qualify as an eligible dependent under the plan, you must provide additional documentation to continue dental and vision coverage up to age 24. Medical coverage for an eligible dependent child may continue up to age 26 regardless of student status

FULL TIME STUDENT - For Full-Time Students, you must also provide one of the following:

• Photocopy of the student’s current class schedule verifying full-time student status

• Letter from the Bursar, Registrar, or Admissions Office on school stationary verifying your child’s full-time student status.

• Photocopy of paid tuition bill indicating full-time student status

- For Full-Time Students on a medical leave of absence, you must also provide one of the following:

• Photocopy of the student’s current class schedule verifying full-time student status

• Letter from the Bursar, Registrar, or Admissions Office on school stationary verifying your child’s full-time student status.

• Photocopy of paid tuition bill indicating full-time student status

• AND Photocopy of signed physician Health Care Statement for a Leave of Absence (Michelle’s Law) certifying that the dependent is suffering from serious illness/injury and a leave of absence is medically necessary. To request a blank Health Care Statement for a Leave of Absence (Michelle’s Law), contact the Corporate Benefits Department at 717-293-4503.

- For disabled dependent children, you must also provide one of the following:

• Photocopy of Social Security disability award letter

• Photocopy of current Social Security disability payment

• Photocopy of signed physician Health Care Statement for Disabled Dependents certifying that the dependent is incapable of self-sustaining employment and dependent upon the employee or spouse due to a mental and/or physical disability. To request a blank Health Care Statement for Disabled Dependents, contact the Corporate Benefits Department at 717-293-4503.

The Summary of Benefits and Coverage (SBC) document will help you choose a health plan . The SBC shows you how you and the plan would share the cost for covered health care services. NOTE: Information about the cost of this plan (called the premium ) will be provided separately.

This is only a summary. For more information about your coverage, or to get a copy of the complete terms of coverage, call 1-866-802-4780. For general definitions of common terms, such as allowed amount , balance billing , coinsurance , copayment , deductible , provider , or other underlined terms see the Glossary. You can view the Glossary at www.healthcare.gov/sbc-glossary or call 1-888-428-2566 to request a copy.

This plan covers some items and services even if you haven't yet met the deductible amount. But a copayment or coinsurance may apply. For example, this plan covers certain preventive services without cost-sharing and before you meet your deductible . See a list of covered preventive services at https://www.healthcare.gov/coverage/preventive-care-benefits/.

Generally, you must pay all the costs from providers up to the deductible amount before this plan begins to pay. If you have other family members on the plan , each family member must meet their own individual deductible until the total amount of deductible expenses paid by all family members meets the overall family deductible . Are there services covered before you meet your deductible ? Yes. In-network preventive services , emergency services or emergency medical transportation .

$750 individual / $1,500 family in-network providers ; $1,500 individual / $3,000 family out-of-network providers .

What is the overall deductible ?

Yes. $125 individual / $250 family for prescription drug . Applies to brand only. There are other specific deductibles . You must pay all the costs for these services up to the specific deductible amount before this plan begins to pay for these services.

Are there deductibles for specific services?

The out-of-pocket limit is the most you could pay in a year for covered services. If you have other family members in this plan , they have to meet their own out-of-pocket limits until the overall family outof-pocket limit has been met.

What is the out-ofpocket limit for this plan ? For in-network providers $2,750 individual / $5,500 family; for out-of-network providers $4,000 individual / $8,000 family and $4,100 /person/ $8,200 /family for prescription drugs .

What is not included in the outof-pocket limit ? Premiums , balance billing charges, and health care this plan doesn't cover. Even though you pay these expenses, they don't count toward the out-of-pocket limit .

This plan uses a provider network . You will pay less if you use a provider in the plan's network . You will pay the most if you use an out-of-network provider , and you might receive a bill from a provider for the difference between the provider's charge and what your plan pays ( balance billing ). Be aware your network provider might use an out-of-network provider for some services (such as lab work).

Yes. For a list of in-network providers , see capbluecross.com or call 1-800-962-2242.

Will you pay less if you use a network provider ?

Check with your provider before you get services.

Do you need a referral to see a specialist ? No. You can see the specialist you choose without a referral .

All copayment and coinsurance costs shown in this chart are after your deductible has been met, if a deductible applies.

Deductible does not apply to services at innetwork providers . You may have to pay for services that aren't preventive. Ask your provider if the services you need are preventive. Then check what your plan will pay for.

Provider (You will pay the most)

In-network Provider (You will pay the least)

None Imaging (CT/PET scans, MRIs) 20% coinsurance If you visit a health

*See preauthorization schedule attached to your plan document. No charge

If you have a test Diagnostic test (x-ray, blood work) 20% coinsurance for Facility Owned Labs, no charge for Independent Clinical Labs and 20% coinsurance for tests. 20% coinsurance for outpatient radiology. 40% coinsurance

*For more information about preauthorization, see the requirements document at https://www.capbluecross.com/preauthorization . 40% coinsurance

Covers up to 30-day supply (retail) 90-day supply (home delivery)

Covers up to 30-day supply $30 minimum copayment /prescription $60 maximum copayment /prescription (retail) 90-day supply $60 minimum copayment /prescription $120 maximum copayment /prescription (home delivery)

Out-of-network Provider (You will pay the most)

You May Need What You Will Pay

In-network Provider (You will pay the least)

$8 copayment /prescription

and $8 copayment /prescription non-preferred (retail) $16

and $16 copayment /prescription

Generic drugs

Preferred brand drugs

Covers up to 30-day supply

$60 minimum copayment /prescription $120 maximum copayment /prescription (retail) 90-day supply $120 minimum copayment /prescription $240 maximum copayment /prescription (home delivery)

Prescription written for up to 30 days supply. (generic) / $30 minimum copayment /prescription/$60 maximum copayment /prescription preferred and $60 minimum copayment /prescription/$120 maximum copayment /prescription nonpreferred (brand)

No coverage for services at out-of-network ambulatory surgical facilities

*See preauthorization schedule attached to your plan document.

does not apply. Copayment waived if admitted inpatient.

does not apply.

Deductible does not apply for services at innetwork providers .

Non-preferred brand drugs

If you need drugs to treat your illness or condition. More information about prescription drug coverage is available by calling 1-866-802-4780

and $8 copayment /prescription non-preferred (generic) 20% coinsurance

$8 copayment /prescription

Specialty drugs

*For more information about preauthorization, see the requirements document at https://www.capbluecross.com/preauthorization .

Pay

(You will pay the most)

*See preauthorization schedule attached

document.

Depending on the type of services, a copayment , coinsurance , or deductible may apply.

schedule

None

*For more information about preauthorization, see the requirements document at https://www.capbluecross.com/preauthorization

Excluded Services & Other Covered Services:

.)

Services Your Plan Generally Does NOT Cover (Check your policy or plan document for more information and a list of any other excluded services

• Glasses

• Routine eye care

• Routine foot care (unless medically necessary)

• Weight loss programs

• Hearing aids • Long-term care

• Private-duty nursing

• Acupuncture

• Bariatric surgery (unless medically necessary)

• Cosmetic surgery

• Dental care

Other Covered Services (Limitations may apply to these services. This isn’t a complete list. Please see your plan document.)

• Non-emergency care when traveling outside the

• Infertility treatment

• Chiropractic care

Your Rights to Continue Coverage: There are agencies that can help if you want to continue your coverage after it ends. The contact information for those agencies

Does this plan meet Minimum Value Standards? Yes If your plan doesn’t meet the Minimum Value Standards , you may be eligible for a premium tax credit to help you pay for a plan through the Marketplace . Is: 1-866-444-EBSA (3272) or www.dol.gov/ebsa/healthreform . Other coverage options may be available to you too, including buying individual insurance coverage through the Health Insurance Marketplace . For more information about the Marketplace , visit pennie.com or call 1-844-844-8040.

Your Grievance and Appeals Rights: There are agencies that can help if you have a complaint against your plan for a denial of a claim . This complaint is called a grievance or appeal For more information about your rights, look at the explanation of benefits you will receive for that medical claim Your plan documents also provide complete information on how to submit a claim, appeal, or a grievance for any reason to your plan For more information about your rights, this notice, or

Assistance, contact: Capital Blue Cross at 1-866-802-4780 or the Department of Labor’s Employee Benefits Security Administration at 1-866-444-EBSA (3272) or www.dol.gov/ebsa/healthreform . To see examples of how this plan might cover costs for a sample medical situation, see the next section.––––––––––––––––––––––

Does this plan provide Minimum Essential Coverage? Yes

Minimum Essential Coverage generally includes plans, health insurance available through the Marketplace or other individual market policies, Medicare, Medicaid, CHIP, TRICARE, and certain other coverage. If you are eligible for certain types of Minimum Essential Coverage , you may not be eligible for the premium tax credit.

About these Coverage Examples: This is not a cost estimator. Treatments shown are just examples of how this plan might cover medical care. Your actual costs will be different depending on the actual care you receive, the prices your providers charge, and many other factors. Focus on the cost sharing amounts (deductibles, copayments and coinsurance ) and excluded services under the plan . Use this information to compare the portion of costs you might pay under different health plans . Please note these coverage examples are based on self-only coverage.

Peg is Having a Baby (9 months of in-network pre-natal care and a hospital

In this example, Peg would pay: In this example, Joe would pay: In this example, Mia would

*Note: This plan has other deductibles for specific services included in this coverage example. See "Are there other deductibles for specific services?” row above. The total Peg would pay is The total Joe would pay is The

Mia would pay is The plan would be responsible for the other costs of these EXAMPLE covered services.

Healthcare benefit programs issued or administered by Capital Blue Cross and/or its subsidiaries, Capital Advantage

Assurance Company® and Keystone Health Plan® Central. Independent licensees of the Blue Cross Blue Shield Association. Communications issued by Capital Blue Cross in its capacity as administrator of programs and provider relations for all companies.

Coverage For: Individual and Family | Plan Type: PPO

w/Rx

The Summary of Benefits and Coverage (SBC) document will help you choose a health plan . The SBC shows you how you and the plan would share the cost for covered health care services. NOTE: Information about the cost of this plan (called the premium ) will be provided separately.

This is only a summary. For more information about your coverage, or to get a copy of the complete terms of coverage, call 1-866-802-4780. For general definitions of common terms, such as allowed amount , balance billing , coinsurance , copayment , deductible , provider , or other underlined terms see the Glossary. You can view the Glossary at www.healthcare.gov/sbc-glossary or call 1-888-428-2566 to request a copy.

Important Questions Answers Why This Matters:

Generally, you must pay all the costs from providers up to the deductible amount before this plan begins to pay. If you have other family members on the plan , each family member must meet their own individual deductible until the total amount of deductible expenses paid by all family members meets the overall family deductible . Are there services covered before you meet your deductible ? Yes. In-network preventive services , emergency services or emergency medical transportation . This plan covers some items and services even if you haven't yet met the deductible amount. But a copayment or coinsurance may apply. For example, this plan covers certain preventive services without cost-sharing and before you meet your deductible . See a list of covered preventive services at https://www.healthcare.gov/coverage/preventive-care-benefits/.

$1,000 individual / $2,000 family in-network providers ; $2,500 individual / $5,000 family out-of-network providers .

What is the overall deductible ?

Are there deductibles for specific services? Yes. $125 individual / $250 family for prescription drug . Applies to retail, mail and specialty. There are other specific deductibles You must pay all the costs for these services up to the specific deductible amount before this plan begins to pay for these services.

The out-of-pocket limit is the most you could pay in a year for covered services. If you have other family members in this plan , they have to meet their own out-of-pocket limits until the overall family outof-pocket limit has been met.

For in-network providers $3,000 individual / $6,000 family; for out-of-network providers

$4,000 individual / $8,000 family and $3,850 /person/ $7,700 /family for prescription drugs .

What is the out-ofpocket limit for this plan ?

This plan uses a provider network . You will pay less if you use a provider in the plan's network . You will pay the most if you use an out-of-network provider , and you might receive a bill from a provider for the difference between the provider's charge and what your plan pays ( balance billing ). Be aware your network provider might use an out-of-network provider for some services (such as lab work).

Premiums , balance billing charges, and health care this plan doesn't cover.

What is not included in the outof-pocket limit ?

Even though you pay these expenses, they don't count toward the out-of-pocket limit . Will you pay less if you use a network provider ? Yes. For a list of in-network providers , see capbluecross.com or call 1-800-962-2242.

Check with your provider before you get services.

Do you need a referral to see a specialist ? No. You can see the specialist you choose without a referral .

All copayment and coinsurance costs shown in this chart are after your deductible has been met, if a deductible applies.

Deductible does not apply to services at innetwork providers . You may have to pay for services that aren't preventive. Ask your provider if the services you need are preventive. Then check what your plan will pay for.

You Will Pay

Provider (You will pay the most)

In-network Provider (You will pay the least)

If you have a test Diagnostic test (x-ray, blood work) 10% coinsurance for Facility Owned Labs, no charge for Independent Clinical Labs and 10% coinsurance for tests. 10% coinsurance for outpatient radiology. 30% coinsurance None

*See preauthorization schedule attached to your plan document.

(CT/PET scans, MRIs) 10% coinsurance If you visit a health

*For more information about preauthorization, see the requirements document at https://www.capbluecross.com/preauthorization . 30% coinsurance

In-network Provider (You will pay the least) Out-of-network Provider (You will pay the most)

Covers up to 30-day supply (retail) 90-day supply (home delivery)

Covers up to 30-day supply $30 minimum copayment /prescription $60 maximum copayment /prescription (retail) 90-day supply $60 minimum copayment /prescription $120 maximum copayment /prescription (home delivery)

You May Need

$8 copayment /prescription

and $8 copayment /prescription non-preferred (retail) $16 copayment /prescription

and $16 copayment /prescription

Generic drugs

(home delivery)

Preferred brand drugs

Covers up to 30-day supply

$60 minimum copayment /prescription $120 maximum copayment /prescription (retail) 90-day supply $120 minimum copayment /prescription $240 maximum copayment /prescription (home delivery)

Prescription written for up to 30 days supply. (generic) / $30 minimum copayment /prescription/$60 maximum copayment /prescription preferred and $60 minimum copayment /prescription/$120 maximum copayment /prescription nonpreferred (brand)

*See preauthorization schedule attached to your plan document.

does not apply. Copayment

if admitted inpatient.

Deductible does not apply for services at innetwork providers .

Non-preferred brand drugs

If you need drugs to treat your illness or condition. More information about prescription drug coverage is available by calling 1-866-802-4780

and $8 copayment /prescription non-preferred (generic) 20% coinsurance

$8 copayment /prescription

Specialty drugs

does not apply. Urgent care

*For more information about preauthorization, see the requirements document at https://www.capbluecross.com/preauthorization .

*See preauthorization schedule attached

(You will pay the most)

Depending on the type of services, a copayment , coinsurance , or deductible may apply.

more information about preauthorization, see the requirements document at https://www.capbluecross.com/preauthorization .

.)

Services Your Plan Generally Does NOT Cover (Check your policy or plan document for more information and a list of any other excluded services

• Routine eye care

• Routine foot care (unless medically necessary)

• Weight loss programs

• Glasses

• Hearing aids • Long-term care

• Private-duty nursing

• Non-emergency care when traveling outside the U.S.

Excluded Services & Other Covered Services: Your Rights to Continue Coverage: There are agencies that can help if you want to continue your coverage after it ends. The contact information for those agencies

• Acupuncture

• Bariatric surgery (unless medically necessary)

• Cosmetic surgery

• Dental care

Other Covered Services (Limitations may apply to these services. This isn’t a complete list. Please see your plan document.)

• Infertility treatment

• Chiropractic care

Does this plan meet Minimum Value Standards? Yes If your plan doesn’t meet the Minimum Value Standards , you may be eligible for a premium tax credit to help you pay for a plan through the Marketplace . Is: 1-866-444-EBSA (3272) or www.dol.gov/ebsa/healthreform . Other coverage options may be available to you too, including buying individual insurance coverage through the Health Insurance Marketplace . For more information about the Marketplace , visit pennie.com or call 1-844-844-8040.

Your Grievance and Appeals Rights: There are agencies that can help if you have a complaint against your plan for a denial of a claim . This complaint is called a grievance or appeal For more information about your rights, look at the explanation of benefits you will receive for that medical claim Your plan documents also provide complete information on how to submit a claim, appeal, or a grievance for any reason to your plan For more information about your rights, this notice, or

Assistance, contact: Capital Blue Cross at 1-866-802-4780 or the Department of Labor’s Employee Benefits Security Administration at 1-866-444-EBSA (3272) or www.dol.gov/ebsa/healthreform . To see examples of how this plan might cover costs for a sample medical situation, see the next section.––––––––––––––––––––––

Does this plan provide Minimum Essential Coverage? Yes

Minimum Essential Coverage generally includes plans, health insurance available through the Marketplace or other individual market policies, Medicare, Medicaid, CHIP, TRICARE, and certain other coverage. If you are eligible for certain types of Minimum Essential Coverage , you may not be eligible for the premium tax credit.

About these Coverage Examples: This is not a cost estimator. Treatments shown are just examples of how this plan might cover medical care. Your actual costs will be different depending on the actual care you receive, the prices your providers charge, and many other factors. Focus on the cost sharing amounts (deductibles, copayments and coinsurance ) and excluded services under the plan Use this information to compare the portion of costs you might pay under different health plans . Please note these coverage examples are based on self-only coverage.

Healthcare benefit programs issued or administered by Capital Blue Cross and/or its subsidiaries, Capital

Assurance Company® and Keystone Health Plan® Central. Independent licensees of the Blue Cross Blue Shield Association. Communications issued by Capital Blue Cross in its capacity as administrator of programs and provider relations for all companies.

Summary of Benefits and Coverage: What this Plan Covers & What You Pay

Coverage For: Individual and Family | Plan Type: PPO

01/01/202512/31/2025 Administered by Capital Blue Cross 1 PPO 3000 w/Rx

The Summary of Benefits and Coverage (SBC) document will help you choose a health plan . The SBC shows you how you and the plan would share the cost for covered health care services. NOTE: Information about the cost of this plan (called the premium ) will be provided separately.

This is only a summary. For more information about your coverage, or to get a copy of the complete terms of coverage, call 1-866-802-4780. For general definitions of common terms, such as allowed amount , balance billing , coinsurance , copayment , deductible , provider , or other underlined terms see the Glossary. You can view the Glossary at www.healthcare.gov/sbc-glossary or call 1-888-428-2566 to request a copy.

This plan covers some items and services even if you haven't yet met the deductible amount. But a copayment or coinsurance may apply. For example, this plan covers certain preventive services without cost-sharing and before you meet your deductible . See a list of covered preventive services at https://www.healthcare.gov/coverage/preventive-care-benefits/.

Generally, you must pay all the costs from providers up to the deductible amount before this plan begins to pay. If you have other family members on the plan , each family member must meet their own individual deductible until the total amount of deductible expenses paid by all family members meets the overall family deductible . Are there services covered before you meet your deductible ? Yes. In-network preventive services , emergency services or emergency medical transportation .

You must pay all the costs for these services up to the specific deductible amount before this plan begins to pay for these services.

$3,000 individual / $6,000 family in-network providers ; $5,000 individual / $10,000 family out-of-network providers .

What is the overall deductible ?

The out-of-pocket limit is the most you could pay in a year for covered services. If you have other family members in this plan , they have to meet their own out-of-pocket limits until the overall family outof-pocket limit has been met.

Are there deductibles for specific services? Yes. $125 individual / $250 family for prescription drug . Applies to brand only. There are other specific deductibles

This plan uses a provider network . You will pay less if you use a provider in the plan's network . You will pay the most if you use an out-of-network provider , and you might receive a bill from a provider for the difference between the provider's charge and what your plan pays ( balance billing ). Be aware your network provider might use an out-of-network provider for some services (such as lab work).

What is the out-ofpocket limit for this plan ? For in-network providers $6,850 individual / $13,700 family; for out-of-network providers $6,850 individual / $13,700 family combined out-of-pocket limit for network medical and prescription drug .

Premiums , balance billing charges, and health care this plan doesn't cover.

What is not included in the outof-pocket limit ?

Even though you pay these expenses, they don't count toward the out-of-pocket limit . Will you pay less if you use a network provider ? Yes. For a list of in-network providers , see capbluecross.com or call 1-800-962-2242.

Check with your provider before you get services.

Do you need a referral to see a specialist ? No. You can see the specialist you choose without a referral .

All copayment and coinsurance costs shown in this chart are after your deductible has been met, if a deductible applies.

(You will pay the least)

Deductible does not apply to services at innetwork providers . You may have to pay for services that aren't preventive. Ask your provider if the services you need are preventive. Then check what your plan will pay for. If you have a test Diagnostic test (x-ray, blood work) No charge

*See preauthorization schedule attached to your plan document. No charge

Imaging (CT/PET scans, MRIs) No charge If you visit a health care provider’s office or clinic

*For more information about preauthorization, see the requirements document at https://www.capbluecross.com/preauthorization .

Covers up to 30-day supply (retail) 90-day supply (home delivery)

/prescription non-preferred (retail)

Covers up to 30-day supply

Generic drugs

$30 minimum copayment /prescription $60 maximum copayment /prescription (retail) 90-day supply $60 minimum copayment /prescription $120 maximum copayment /prescription (home delivery) Non-preferred brand drugs

Preferred brand drugs

Covers up to 30-day supply

$60 minimum copayment /prescription $120 maximum copayment /prescription (retail) 90-day supply $120 minimum copayment /prescription $240 maximum copayment /prescription (home delivery)

Prescription written for up to 30 days supply. (generic) / $30 minimum copayment /prescription/$60 maximum copayment /prescription preferred and $60 minimum copayment /prescription/$120 maximum copayment /prescription nonpreferred (brand)

*See preauthorization schedule attached to your plan document.

does not apply. Copayment waived if admitted inpatient.

does not apply.

Deductible does not apply for services at innetwork providers .

Specialty drugs

If you need drugs to treat your illness or condition. More information about prescription drug coverage is available by calling 1-866-802-4780

*For more information about preauthorization, see the requirements document at https://www.capbluecross.com/preauthorization .

Depending on the type of services, a copayment , coinsurance , or deductible may apply.

(You will pay the most)

*For more information about preauthorization, see the requirements document at https://www.capbluecross.com/preauthorization

.)

Services Your Plan Generally Does NOT Cover (Check your policy or plan document for more information and a list of any other excluded services

• Routine eye care

• Routine foot care (unless medically necessary)

• Weight loss programs

• Glasses

• Hearing aids • Long-term care

• Private-duty nursing

Excluded Services & Other Covered Services: Your Rights to Continue Coverage: There are agencies that can help if you want to continue your coverage after it ends. The contact information for those agencies

• Acupuncture