Welcome to our H2 2025 issue which covers H1 to 30 June 2025

Welcome to the latest Baronsmead newsletter. In this edition, we provide an update on performance and portfolio activity for the first half of 2025, alongside perspectives from our fund managers on the wider market environment.

Highlights include strong progress across the unquoted portfolio, a successful exit from Panthera Biopartners, and continued momentum in key growth areas such as healthcare, SaaS, and AI. We also introduce Jens Düing, our new Head of Portfolio, and spotlight innovative companies including SciLeads and Penfold.

This issue also explores how we support founders in building the right culture, as well as insights into the growing role of AI agents in financial services.

We hope you find this update both informative and engaging, and as always, our team is available should you wish to discuss any aspect of the Baronsmead VCTs further.

Performance and portfolio overview - for the six month period to 30 June 2025 (H1)

The first half of 2025 presented a mixed picture across public and private markets. While global equity indices staged a notable recovery in Q2, UK smaller companies continued to face persistent investor caution. Broader macroeconomic pressures, including inflationary cost structures and shifting fiscal policy, weighed heavily on risk appetite.

Despite these challenges, the Baronsmead VCTs remained resilient. The quoted portfolios experienced valuation pressure in line with market trends, while the unquoted portfolio benefited from steady operational progress and continued revenue growth delivering a £2.6mn like-for-like uplift of NAV of the unquoted portfolio.

Performance – H1 2025

Baronsmead Venture Trust (BVT) returned +1.13% and Baronsmead Second Venture Trust (BSVT) returned +0.81% over the period.

In the quoted portfolio, Baronsmead Venture Trust (BVT) and Baronsmead Second Venture Trust (BSVT) returned negative 1.5% and 1.3% respectively during the first half of 2025. More broadly across UK equity markets, the FTSE 100 delivered a 9.5% return, the FTSE 250 a 6.8% return, the Deutsche Numis Smaller Companies plus AIM ex Investment Trust Index a 6.9% return, and the FTSE AIM All share an 8.1% return. Key positive contributions for the Baronsmead VCTs during the period, highest-to-lowest in terms of contribution to overall Fund performance, came from:

Property Franchise Group (+37% total shareholder return (TSR)), reflecting strong current trading, sell-side forecast upgrades, and a re-rating of the shares;

Netcall plc (+9% TSR), on the back of strong trading in H1 2025 including 20% organic cloud service revenue growth and a higher proportion of annual recurring revenues, net revenue retention of 115%, and a high drop-through to EBITDA and free cash flow; and

Inspired plc (+95% TSR), following a recommended all-cash takeover offer by HGGC, a US midmarket private equity firm, at 81p per share, a 33% premium to the share price immediately before the announcement.

Offsetting these gains during the period were the following key detractors, highest-to-lowest in terms of negative Fund performance contribution:

Cerillion plc (-11% TSR), despite good revenue and earnings growth ahead of market expectations in FY24 and continued positive contract win momentum;

Hvivo plc (-48% TSR), major contract loss drove a material profit warning and a reset of outer-year earnings expectations; and

PCI-PAL plc (-18% TSR), despite positive trading announcements and strong fundamental progress including over 24% annual recurring revenue growth in FY24, new contract wins, and for the first time delivering positive EBITDA and free cash flow.

The investments in the Gresham House open-ended equity strategies performed broadly in-line with their respective index benchmarks:

WS Gresham House UK Micro Cap Fund: 5.7%

WS Gresham House UK Smaller Companies Fund: 6.1%

WS Gresham House UK Multi Cap Income Fund: 4.5%

Within the unquoted portfolio, performance was encouraging despite ongoing headwinds. Strategic execution, commercial traction, and improved financial metrics contributed to net value growth across the portfolio.

The aggregate invested unquoted portfolio increased by £3.6mn over the half year, comprising £1.1mn of follow-on investments in Q1 and £8.3mn of investments in Q2 (£1.0mn in follow-ons and £7.3mn across four new companies).

43% of the portfolio delivered valuation uplifts in Q2 (up from 35% in Q1), with standout contributions from Panthera Biopartners, CitySwift, RevLifter, Huma, and Proximity Insight.

Valuation reductions were limited to 23% of companies in Q2 (down from 25% in Q1), with pressure largely confined to public sector-exposed or cost-sensitive segments.

67% of the portfolio delivered revenue growth by Q2, up from 50% in Q1 and 33% at the start of the year, reflecting gradually improving trading performance.

Built-in deal terms and investor protections acted as a safety net, smoothing out big swings in valuations and helping to keep overall results more stable.

The portfolio’s RAG ratings improved modestly over the half year, with a positive shift from red to amber and amber to green, driven more by companyspecific progress than macro trends.

Market dynamics & macro trends

Global trade & policy: Tariff-related uncertainty remained elevated throughout H1, with average global tariffs reaching 17.6% a multi-decade high. However, sentiment improved in late Q2 as key policymakers softened trade rhetoric. The Baronsmead VCTs remain largely insulated due to limited exposure to goods-based exports.

Inflation & yields: UK inflation increased from 2.6% to 3.6%, driven by wage growth and services inflation. Gilt yields rose to multi-year highs, prompting a surge in retail fixed income demand. While input cost pressures remain, GDP growth forecasts have edged slightly higher and interest rates have begun to ease.

Equity market trends: A notable rotation into growth sectors emerged in Q2. NASDAQ rose 17.7%, FTSE Techmark Focus climbed 15.7%, and UK small caps advanced 10.4%. Despite volatility, these movements suggest renewed investor appetite in selected areas.

Private markets & M&A: Private equity and strategic buyers are re-engaging, particularly in tech and infrastructure. UK AI companies raised $2.4bn in H1 - 30% of total UK venture capital - marking a record share. We are seeing increased inbound interest across several portfolio companies.

Investor sentiment: Caution remains, but sentiment is gradually improving. Asset managers are rotating toward non-US equities, alternatives, and incomegenerating strategies. Business confidence indices have rebounded from recent lows.

Outlook – H2 2025

We believe the Baronsmead VCTs remain well positioned for value realisation in a recovering environment. Over 70% of the portfolio is UK-focused and weighted toward capital-light, service-led businesses with limited exposure to supply chain or trade-related risk.

We expect M&A and funding conditions to further improve in H2, particularly across SaaS, healthcare, AI, and infrastructure sectors. Our focus remains on disciplined capital deployment, close engagement with management teams, and preparing businesses for long-term value creation and potential exit opportunities.

One such example is the recent successful exit of Panthera BioPartners, which was acquired by LDC following a competitive process led by EY, completed between the quarter-end and the publication of this commentary.

NAV at 30 June 2025

Six months portfolio returns to 30 June 2025 (H1)

Capital at risk. Past performance is not a reliable indicator of future performance. Portfolio investments in smaller companies typically involve a higher degree of risk. Investment selected for illustrative purposes only tand are not investment recommendations.

Creating value from first investment to successful exit: The Panthera Biopartners journey

When Gresham House Ventures first met Panthera Biopartners in 2019, we saw more than just a promising new player in clinical trials - we saw a team and model poised to redefine how patient recruitment and trial delivery could be done. Six years later, that vision has come full circle, culminating in our successful exit in August 2025.

This is the story of how we identified the opportunity, and the value we created together.

Spotting the opportunity

Panthera was founded by Dr Ian Smith and Professor John Lyon to address a growing bottleneck in the pharmaceutical sector: finding and retaining patients for Phase II and III clinical trials. As a Site Management Organisation (SMO), Panthera operates its own network of research sites, partnering with clinical research organisations (CROs), pharma, and biotech companies to speed up trial recruitment and delivery.

By 2019, the market was ripe for disruption. Demand for outsourced SMO services was accelerating, driven by biopharma’s need for faster, more reliable patient recruitment and the NHS’s inability to deliver at the necessary scale. Patient recruitment and retention is fundamental to trial success yet is a major pain point for providers with c.80% of trials missing enrolment timelines and estimated to cost as much as $8mn a day in lost revenue. Panthera’s founders had already built and exited a similar business under private equity ownership, giving them deep industry experience and an enviable network.

For Gresham House Ventures, this was a rare opportunity to back a proven team early in their commercial journey in a high-growth, structurally attractive market. Our investment thesis was clear: fund an aggressive UK site roll-out, leverage technology to improve patient acquisition and retention, and build strong commercial relationships with top-tier pharma and CROs.

Our investment and growth journey

We became Panthera’s first institutional investor, participating in multiple funding rounds to support expansion since 2020. The company’s early progress validated our thesis:

Rapid site growth: From two UK locations at investment to five operational sites, plus two affiliate sites in Sweden.

Market traction: By 2024, Panthera was working with eight of the world’s twelve largest pharma companies and all seven of the largest global CROs.

Operational excellence: Ranked as the top global recruiter in four international studies in 2024 and the first to enroll patients in nine separate trials that year.

Creating value through augmenting the team, supporting technology adoption and operational execution

We supported in augmenting the executive team. We built around the experienced core leadership team, supporting the recruitment of a CFO, CIO and Patient Engagement and Marketing Director. This depth of talent was instrumental in scaling operations and aligning with the value creation strategy.

We leveraged our strong understanding of the market and business model to improve operational execution through developing management information, as well as leveraging technology. Panthera implemented eSource to digitise documentation and leveraged digital tools such as teleconsultations to improve patient access.

These innovations boosted recruitment efficiency and patient engagement. Gresham House Ventures was also able to leverage its sector knowledge and insights to better inform Panthera’s digital strategy and introduce them to other tech innovators in the sector.

The operational improvements, combined with strong market demand and management’s strong execution drove exceptional revenue and EBITDA growth – with revenue growing over 75-fold since our initial investment in 2020 and by over 200% since 2022, moving the business to profitability and to being highly cash generative.

A successful exit

In August 2025, Panthera attracted significant investment from LDC to fund the next stage of its UK and European expansion. The existing leadership team, led by Stuart Young, remains in place.

For Gresham House Ventures, the exit delivered a strong return for our Baronsmead VCT investors and validated our model of backing high-growth, technology-enabled businesses in healthcare and life sciences. More importantly, Panthera is now even better positioned to accelerate the delivery of life-changing treatments to patients.

Panthera’s story demonstrates the power of aligning investor expertise with a capable leadership team in a market ready for change. For entrepreneurs seeking funding, it’s a reminder that capital is most powerful when it comes with partnership, insight, and a shared vision for value creation.

Director

Maya joined Gresham House in September 2019, and focuses on healthcare investments, including Orri, Metrion Biosciences and Panthera Biopartners.

Prior to Gresham House, she spent 4 years at Octopus Investments, investing in real estate-backed healthcare companies and entrepreneurs. Before this she worked at KPMG for 7 years in audit and corporate finance.

Maya holds a first-class degree in Modern History and is a Chartered Accountant (ICAEW).

Capital at risk. Past performance is not a reliable indicator of future performance. Portfolio investments in smaller companies typically involve a higher degree of risk. Investment selected for illustrative purposes only tand are not investment recommendations.

Article written by

Maya Ward Investment

Latest news and portfolio updates

Intention to fundraise

The Directors of Baronsmead Venture Trust plc and Baronsmead Second Venture Trust plc are pleased to announce that the Baronsmead VCTs intend to launch a new offer for subscription (the “Offers”) during the 2025/26 tax year.

Further details of the Offers will be contained in a prospectus that is expected to be published in October 2025. A further announcement will be made when the prospectus is available.

Why Baronsmead?

Gresham House is the second largest venture capital firm in the market by AUM with over 30 full-time investment professionals employed by the manager

Baronsmead VCTS are the largest hybrid VCTs in the market which gives us flexibility across unquoted and quoted markets depending on conditions and valuations

Baronsmead’s portfolio contains over 80 direct quoted and unquoted companies and diversification across the portfolio helps to reduce risk

Seeking to deliver long-term, consistent and attractive dividends

With the ability to top-slice to generate short-term liquidity in AIM portfolio and equity funds

Gresham House

Ventures

appoints

Jens

Düing as Head of Portfolio

We are delighted to welcome Jens Düing to Gresham House Ventures as our new Head of Portfolio.

Jens joins us with over 20 years of experience supporting growth businesses across Europe. Most recently a Senior Partner at Frog Capital, he has also held roles at Pioneer Point Partners, Fidelity Equity Partners and Apax, and has served on the boards of companies across payments, insurance, healthcare, edtech and property.

At Gresham House Ventures, Jens will lead on portfolio management and value creation strategies, working closely with our Managing Director and CIO, Trevor Hope.

“Jens brings significant experience of supporting growth businesses across several key sectors for Gresham House Ventures, so we are excited to have him on board as we look to take advantage of the strong demand we are seeing from investors for UK early-stage businesses.” - Trevor Hope, Managing Director

Read more here >>

Supporting founders to create the right culture

“We like to introduce the talent function very early on in the process, really for the founders to understand what our capabilities are and what it means to have a supportive investment partner.”

In the first of a three-part series, hear how we work with founders pre and post transaction to support them as they build out their teams, redefining the value in talent management.

We hear from Conor O’Neill, Co-Founder and CEO of OnSecurity and Peder Berger, CEO of Accredit Solutions1 as they discuss their experience of working with us.

1:

Investment companies selected for illustrative purposes only and are not investment recommendations.

1. Investment not held within the Baronsmead VCTs portfolio

Episode

Every time a

new computing revolution

arrives, headlines warn: ‘The robots are coming for our jobs.’

Unsurprisingly, the growth of generative AI in recent years has brought predictions of catastrophic turbulence as ChatGPT and its peers fill the place of humans.

However, history shows us that great leaps forward in computing create more jobs – just very different ones. From 1985 to 2005, as the personal computer became ubiquitous, the productivity rate across developed economies markedly improved while unemployment declined. The OECD attributed 30-40% of productivity growth during this period to IT investment. Mobile internet access had a similar impact, with McKinsey research showing that the internet created 2.6 jobs for every one that was lost.

Now, another shift is underway with the rise of AI agents.

Meet your new colleagues

If ChatGPT is the smart intern who takes notes and follows instructions, AI agents are the chief of staff – anticipating problems, delegating tasks, and making executive decisions. These programs hold the promise of providing entire services as a single software solution.

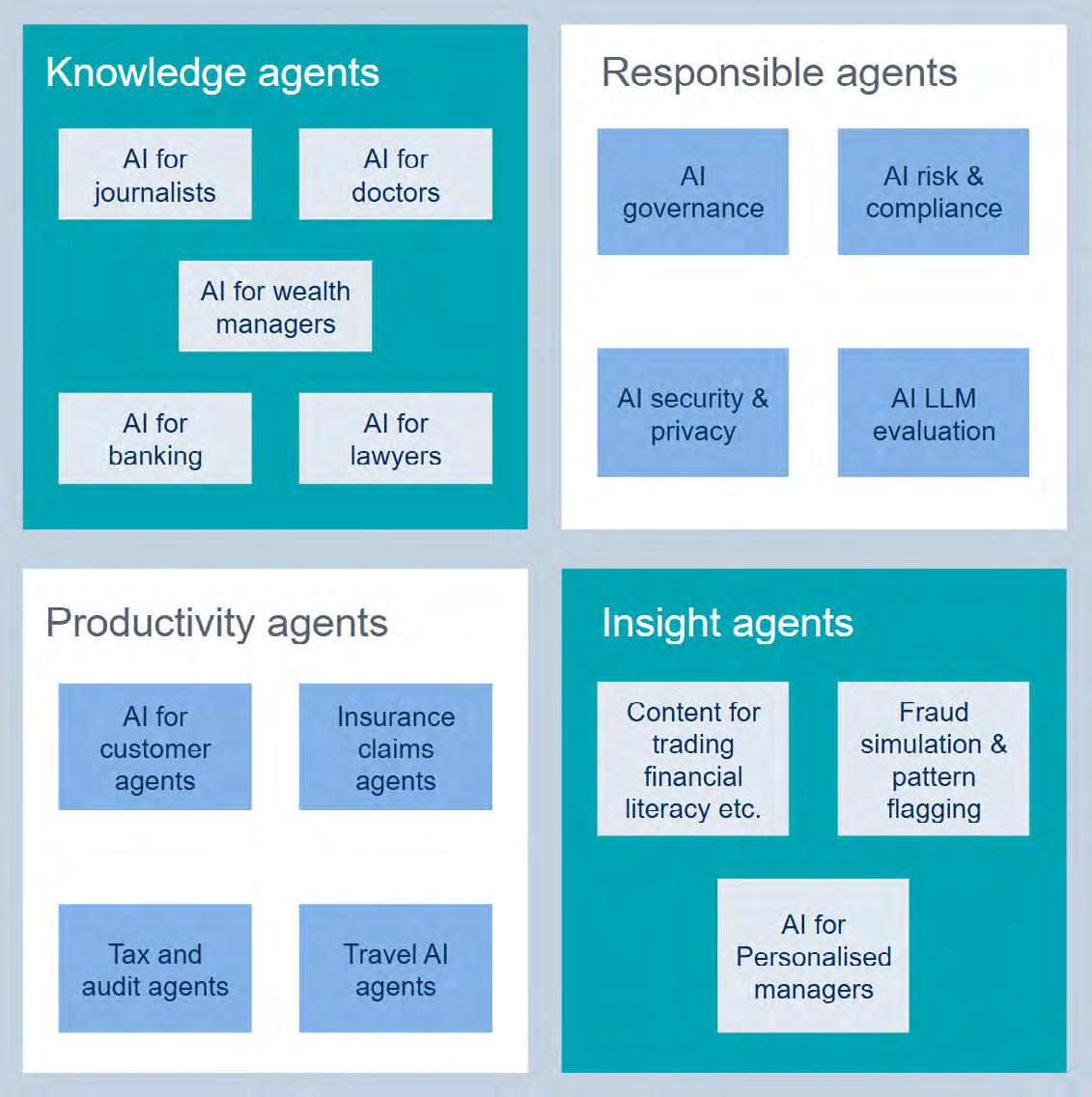

AI agents are already doing many routine tasks, with customer service chatbots the prime example. However, the technology is just scratching the surface of what is possible. AI agents fall into four main groups, with each playing a different role.

Knowledge agents are research whizzes. They consolidate information to assist with routine tasks like research and consultation, with the potential to act on behalf of doctors, journalists, lawyers and even wealth managers. Ava, the AI agent from Avantia Law, is a prime example of how AI agents are taking care of routine legal processes.

Capital at risk. Past performance is not a reliable indicator of future performance.

Responsible agents are designed for areas like risk, compliance, security and governance. They provide workflow oversight, detecting and highlighting anomalies and rogue agents. A good example is Zango AI, whose AI agent is like a tireless compliance analyst – scanning and reviewing thousands of regulations, flagging issues and proposing recommendations faster than any compliance team can.

Productivity agents are personalised, hyper-focused digital EAs, focused on supercharging efficiency across tedious, low risk but high-value tasks such as booking meetings, drafting responses and even pre-approving insurance claims. Tools like Fyxer AI can anticipate tasks and scale better than any human assistant.

Insight agents are pattern spotters, trawling through data to uncover trends and provide new insights. They are enabling businesses to create new products, better serve customers and improve profitability.

Framework for AI agents

Red tape or rocket fuel?

While some industries are rapidly adopting and integrating AI agents, others would seem to face more of a challenge in making use of the technology due to regulation.

In financial services, there is huge potential for AI agents to overhaul the burden of time-consuming manual processes facing the sector, but it seems unlikely that financial advice or mortgage advice could ever be provided entirely by an AI agent.

However, AI agents can still transform these services, just with a human touch. Investment decisions might not be made by AI, but a wealth manager could use AIbased overviews of clients’ financial circumstances to inform their recommendations, for example.

As the technology accelerates, it will be crucial for businesses in the sector to be on the right side of regulatory barriers, working closely with regulators to maximise their impact, minimise risks, and make the case for improvements to regulatory frameworks as AI agents evolve and improve.

Regulators also need to do more to encourage innovative technologies. Political and economic uncertainty in the US – historically the world’s computing superpower – is creating opportunities for the UK to show leadership, and the government has signalled it will reform the role of regulators to encourage growth. Truly ambitious reforms could significantly boost the UK’s already fastgrowing AI sector.

Startups, strap in

With enterprises scrambling to embrace AI agents to boost productivity, a new generation of startups is riding the wave, reimagining how services are delivered, decisions are made, and value is created.

However, building these companies is highly complex. Alongside capital, founders need sector specialists who can advise businesses on building a customer base, winning marquee clients and navigating regulatory mazes.

By 2030, we expect a third of tasks in financial services to be managed by an AI agent. This is a generational opportunity – the next Google or Salesforce might not be a search engine or CRM tool, but an AI agent orchestrating compliance for a major bank or managing portfolios for millions of savers.

So yes, the AI agents are coming for financial services. But they are not here to steal jobs –they are here to take on the boring parts, let people and businesses focus on what actually matters, and accelerate the sector’s growth for decades to come.

Article written by

Rohit Mathur Investment Partner

Rohit is a venture capital investor focused on late Seed to Series A Fintech, SaaS, and AI-first companies, with investments across the UK, EU, India, ME, and SEA, including Adsum, Refyne, Honest Bank, WealthKernel, and Penfold. He was previously Investment Partner at Digital Horizon VC and spent over a decade at Barclays Bank London, where he built its VC unit and launched its wealth management mobile app. Earlier in his career, he worked with startups, consulted at EY, and began as a software engineer at Infosys.

Passionate about diversity, he has held NED roles with startups and education institutions, including Manchester Business School’s Global Alumni Board. Rohit holds an MBA (Director’s List, AT Kearney Scholar) from Manchester Business School and a B.Eng. from Agra University.

Useful documents

Factsheets to 30 June 2025

Interim reports to 31 March 2025

Baronsmead Venture Trust

Baronsmead Second Venture Trust

Baronsmead Venture Trust

Baronsmead Second Venture Trust

Company spotlights

SciLeads

SciLeads is a Belfast-based sales enablement and market intelligence SaaS platform purpose-built for the Life Sciences sector. Aggregating over 300 million datapoints – including research grants, publications, conference activity and funding rounds – the platform enables leading Life Science Tools providers to identify, qualify and convert high-probability sales leads across academic and biopharma markets.

Since the Baronsmead VCTs initial investment in March 2024, the business has delivered strong revenue growth, increased average contract value and strengthened its leadership team - supported by Gresham House’s active board engagement and portfolio support.

The Baronsmead VCTs invested further in 2025 to support product development, deeper workflow integration and an expanded go-to-market strategy, positioning SciLeads to accelerate growth and capture significant opportunities in life sciences data and software.

Portfolio investments in smaller companies typically involve a higher degree of risk. Investments investment strategy and are not investment recommendations.

Penfold

Penfold, founded in 2018, is a technology-driven pension platform that enables individuals to consolidate, manage, and grow their pensions. Originally launched as a direct-to-consumer offering, the business has pivoted to focus on serving UK SMEs required to provide workplace pensions under auto-enrolment rules.

Through partnerships with HSBC and BlackRock, Penfold delivers a fully digital solution with strong adoption and customer retention. The platform enables employers to set up and manage pensions with ease, implement salary sacrifice, and offer employees a valuable workplace benefit.

In early 2025, Baronsmead invested c.£0.8mn as part of a £3.8mn funding round, which will support the acceleration of the go-to-market strategy and product development roadmap.

Investments selected for illustrative purposes only to demonstrate

Contact details

Chris Elliott

Managing Director, Wholesale

M: +44 (0) 78279 20066

E: c.elliott@greshamhouse.com

Andy Gibb

Sales Director

M: +44 (0) 78490 88033

E: a.gibb@greshamhouse.com

Rees Whiteley

Sales Manager

M: +44 (0) 75975 79438

E: r.whiteley@greshamhouse.com

Source for all information is Gresham House unless otherwise stated.

Risks to be aware of

The value of the Companies and the income from them is not guaranteed and may fall as well as rise

As your capital is at risk you may get back less than you originally invested

Past performance is not a reliable indicator of future performance

Any tax reliefs are dependent on your individual circumstances and may be subject to change

Funds investing in smaller, younger companies may carry a higher degree of risk than funds investing in larger, more established companies. Investments in smaller companies may be less liquid than investments in larger companies

Important information

This document is a financial promotion issued by Gresham House Asset Management Limited (Gresham House) as Investment Manager for the Baronsmead VCTs under Section 21 of the Financial Services and Markets Act 2000. Gresham House is authorised and regulated by the Financial Conduct Authority with reference number 682776 and has its registered office at 5 New Street Square, London EC4A 3TW. The information in this document should not be construed as an invitation, offer, solicitation of any offer, or recommendation to buy or sell investments, shares or securities or an invitation to apply for securities in any jurisdiction where such an offer or invitation is unlawful, or in which the person making such an offer is not qualified to do so. Whilst the information in this document has been published in good faith, Gresham House provides no guarantees, representations, warranties or other assurances (express or implied) regarding the accuracy or completeness of this information. Gresham House and its affiliates assume no liability or responsibility and owe no duty of care for any consequences of any person acting in reliance on the information contained in this document or for any decision based on it. Past performance is not a reliable indicator of how the investment will perform in the future. Your capital is at risk. Prospective investors should seek their own independent financial, tax, legal and other advice before making a decision to invest. This document has not been submitted to or approved by the securities regulatory authority of any state or jurisdiction. This document is intended for distribution in the United Kingdom only. Any dissemination or unauthorised use of this document by any person or entity is strictly prohibited. Please contact a member of the Gresham House team if you wish to discuss your investment or provide feedback on this document. Gresham House is committed to meeting the needs and expectations of all stakeholders and welcomes any suggestions to improve its service delivery.