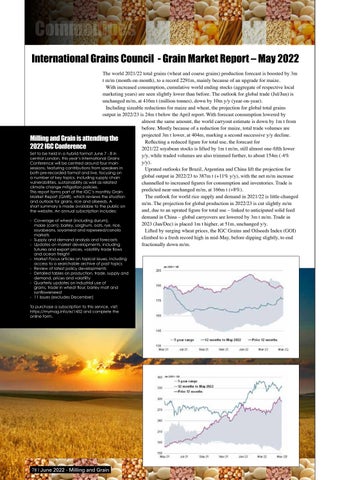

International Grains Council - Grain Market Report – May 2022 The world 2021/22 total grains (wheat and coarse grains) production forecast is boosted by 3m t m/m (month-on-month), to a record 2291m, mainly because of an upgrade for maize. With increased consumption, cumulative world ending stocks (aggregate of respective local marketing years) are seen slightly lower than before. The outlook for global trade (Jul/Jun) is unchanged m/m, at 416m t (million tonnes), down by 10m y/y (year-on-year). Including sizeable reductions for maize and wheat, the projection for global total grains output in 2022/23 is 24m t below the April report. With forecast consumption lowered by almost the same amount, the world carryout estimate is down by 1m t from before. Mostly because of a reduction for maize, total trade volumes are projected 3m t lower, at 404m, marking a second successive y/y decline. Milling and Grain is attending the Reflecting a reduced figure for total use, the forecast for 2022 IGC Conference 2021/22 soyabean stocks is lifted by 1m t m/m, still almost one-fifth lower Set to be held in a hybrid format June 7 - 8 in y/y, while traded volumes are also trimmed further, to about 154m (-4% central London, this year’s International Grains y/y). Conference will be centred around four main sessions, featuring contributions from speakers in Uprated outlooks for Brazil, Argentina and China lift the projection for both pre-recorded format and live, focusing on global output in 2022/23 to 387m t (+11% y/y), with the net m/m increase a number of key topics, including supply chain vulnerabilities, sustainability as well as related channelled to increased figures for consumption and inventories. Trade is climate change mitigation policies. predicted near-unchanged m/m, at 166m t (+8%). This report forms part of the IGC’s monthly Grain Market Report (GMR), which reviews the situation The outlook for world rice supply and demand in 2021/22 is little-changed and outlook for grains, rice and oilseeds. A m/m. The projection for global production in 2022/23 is cut slightly m/m short summary is made available to the public on and, due to an uprated figure for total use – linked to anticipated solid feed the website. An annual subscription includes: demand in China – global carryovers are lowered by 3m t m/m. Trade in - Coverage of wheat (including durum), 2023 (Jan/Dec) is placed 1m t higher, at 51m, unchanged y/y. maize (corn), barley, sorghum, oats, rye, rice, soyabeans, soyameal and rapeseed/canola Lifted by surging wheat prices, the IGC Grains and Oilseeds Index (GOI) markets climbed to a fresh record high in mid-May, before dipping slightly, to end - Supply and demand analysis and forecasts - Updates on market developments, including fractionally down m/m. -

futures and export prices, volatility trade flows and ocean freight Market Focus articles on topical issues, including access to a searchable archive of past topics Review of latest policy developments Detailed tables on production, trade, supply and demand, prices and volatility Quarterly updates on industrial use of grains, trade in wheat flour, barley malt and sunflowerseed 11 issues (excludes December)

To purchase a subscription to this service, visit: https://mymag.info/e/1452 and complete the online form.

78 | June 2022 - Milling and Grain