ASKING RENTS MOVE BACKWARDS FOR THE FIRST TIME IN 15 YEARS

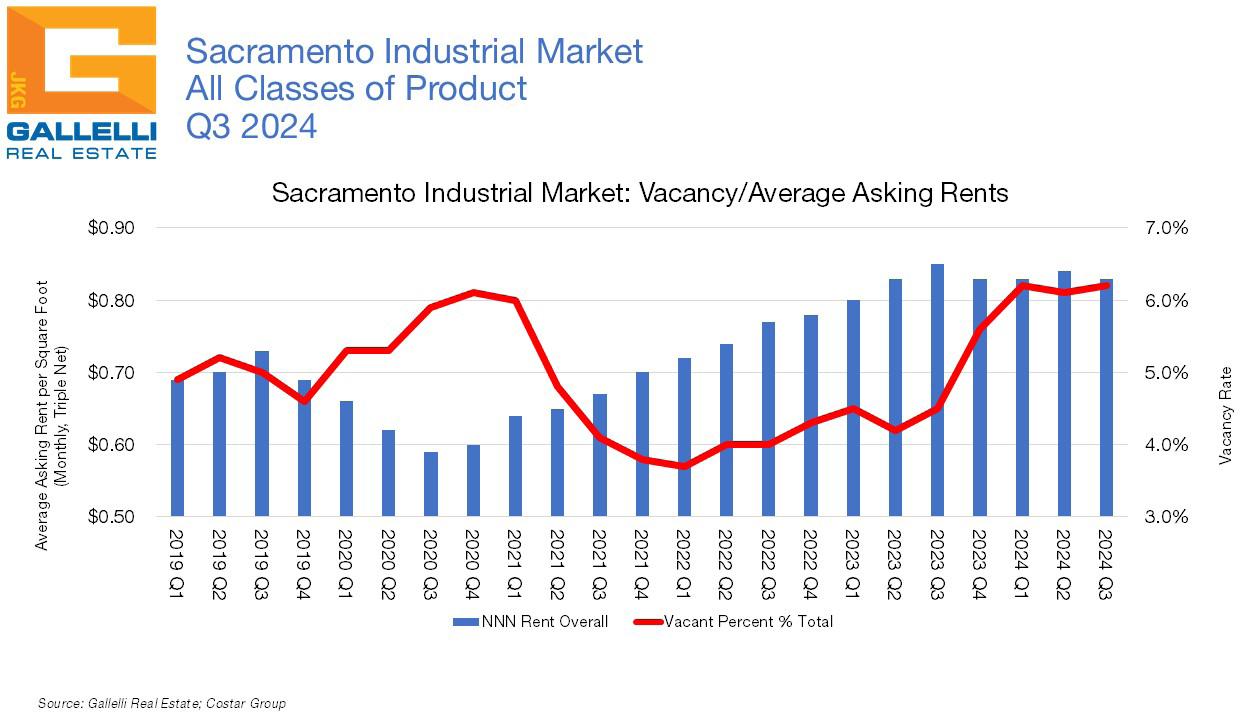

The average current asking rent for industrial space in the Sacramento region is $0.83 per square foot (PSF), on a monthly triple net basis. This metric has fallen slightly (by -2.4%) over the past year, reflecting negative rental rate growth (albeit modest) for the first time since 2009. These declines are modest and have not been spread evenly across either the region’s industrial subtypes or individual submarkets. We are not ready to state this is the beginning of a trend. But being that this is the first time in 15 years this metric has declined, it demands some exploration.

This quarter’s decline in overall asking rents has exclusively been driven by the warehouse sector. We track just under 180 MSF of industrial product in the Sacramento region; with the warehouse sector accounting for 89.2% or 160.3 MSF of the total inventory (this includes eCommerce fulfillment, distribution, cold storage and general warehouse space).

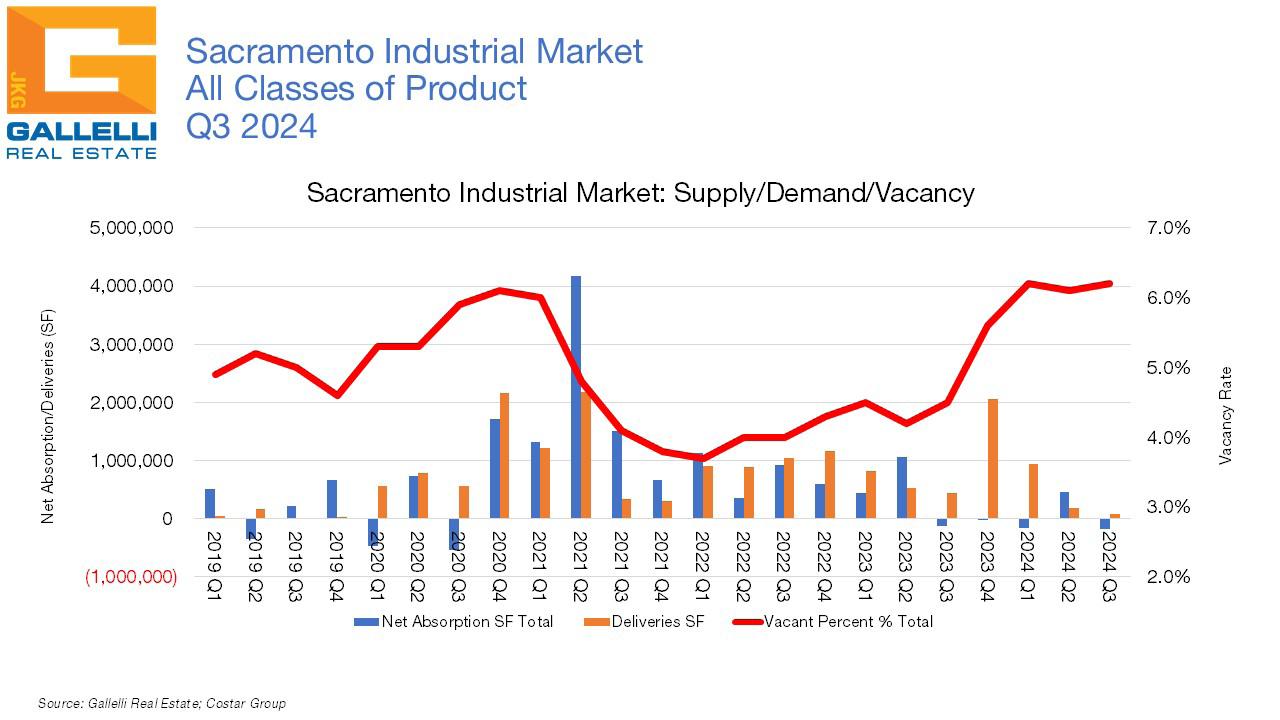

Local warehouse vacancy currently stands at 6.1%, up from 5.8% three months ago and up more substantially from the 4.1% rate of one

year ago. More than 3.1 MSF of new warehouse product has come to market over the past 12 months, while net absorption has been in negative territory (-208,000) over the past year. While the market has recorded occupancy growth in two of the past four quarters, losses in Q1 2024 and the most recent quarter (-373,000 SF) surpassed gains.

The current average asking rate for warehouse product in the Sacramento region is $0.78 PSF, down -3.7% from last year’s reading of $0.81 PSF. Rents for warehouse space grew aggressively in recent years thanks both to outsize demand and a surge of new, more expensive product, coming online. As recently as six years ago (Q3 2018), the average asking rate for warehouse space in the Sacramento region was $0.53 PSF, with the local market ranking in the US top ten for rent growth multiple times during the last few years.

The recent softening of warehouse demand in the last 18-24 months, combined with substantial levels of new development being delivered has created real headwinds for rent growth. But it is too soon to say if this trend has legs. New construction has already peaked—the region’s industrial development pipeline steadily emptying. Meanwhile, a stronger economy heading deeper into 2025 will almost certainly drive greater demand—though don’t expect the eCommerce fulfillment wave to ever return to the tsunami levels of 2018-2022.

One more factor that suggests warehouse rents have likely just plateaued, as opposed to starting a longer-term trend of moving backwards, is that the trend has not played out across every local submarket. The biggest decreases have come from submarkets where an aging inventory and functional obsolescence is increasingly an issue (Auburn/Newcastle, McClellan, Northeast, Power Inn and South

Sacramento) or where vacancy has spiked in recent months and competitive pressure mounted (Davis/Woodland). Markets with tight availability and relatively modern product like Elk Grove/Laguna, and Roseville/Rocklin have seen considerable upticks in rent. Meanwhile, the Natomas/Northgate submarket, despite having experienced a considerable uptick in vacancy (from 5.6% to 12.5% over the past year), has continued to post rent gains. This trade area has been a focal point of new development with its new institutional-grade product partially driving a reset in pricing even though much of this new inventory is taking longer to lease under current market conditions.

All these factors suggest that this quarter’s decline in asking rates may prove to be a brief blip. That blip, incidentally, hasn’t impacted flex properties and their landlords at all. As mentioned earlier, Flex vacancy now stands at 6.9%, down from a reading of 7.9% three months ago. The market recorded 197,000 SF of positive net absorption in Q3, bringing year-to-date totals to 605,000 SF. Keep in mind that from 2000 through 2023, Flex averaged 37,000 SF of positive net absorption during any given quarter. Through the first three quarters of 2024, it averaged 202,000 SF per quarter.

The current average asking rate for flex space of $1.07 PSF (on a monthly triple net basis) has increased by 8.1% over the last year. From 2000 through the end of 2023, Flex has averaged 37,000 SF of positive net absorption during any given quarter. Through the first three quarters of 2024, it averaged 202,000 SF per quarter.

SUBMARKET REVIEW

Industrial vacancy fell or remained the same in 11 of the region’s 16 distinct submarkets with each of those trade areas recording positive net absorption. The Sunrise submarket along Sacramento’s Highway

50 Corridor in Rancho Cordova led all other trade areas in terms of occupancy growth in Q3, recording 418,000 SF of positive net absorption as its vacancy rate fell from 9.9% to 6.7%. While most of the new deal activity here was for spaces of 15,000 SF or less, a couple of larger deals at the Sunrise 50 Business Center and elsewhere helped to propel this submarket into the black in Q3.

Roseville/Rocklin followed with 407,000 SF of positive net absorption helping to drive this submarket’s vacancy rate downward from 3.5% to an incredibly tight 1.4%. Smaller deals also drove much of the occupancy gains with the Rocklin Ranch Business Park, 100 Atkinson Street, the Lincoln Air Center, Vineyard Pointe Business Center and several other multitenant industrial projects in this trade area landing new space users. In both cases, occupancy gains were driven both by new warehouse and flex tenants.

West Sacramento was the only other trade area that recorded gains of more than 100,000 SF; a mix of new warehouse tenants there helped to drive 107,000 SF of positive net absorption in Q3 as vacancy fell from 7.9% to 6.7%. West Sacramento has posted positive net absorption in every quarter so far this year and has recorded occupancy growth in four of the past five. The fourth quarter of 2024 could see that streak coming to an end. In September Amazon announced plans to close two of their grocery warehouses in California; one in Irvine and the other at 3620 Ramos Drive in West Sacramento. The 182,000 Sf facility will be shut down in October.

The Auburn/Newcastle (+3,000 SF), Downtown (+11,000 SF), Elk Grove/ Laguna (+36,000 SF), Folsom/El Dorado Hills (+13,000 SF), McClellan (+21,000 SF), and Power Inn (+59,000 SF) submarkets all posted modest occupancy growth in Q3, with East Sacramento and the Northeast trade areas reporting flat activity.

Despite gains elsewhere, significant space givebacks in the Davis/ Woodland (-962,000 SF), Natomas/Northgate (-184,000 SF), Richards Boulevard (-51,000 SF), Mather (-28,000 SF), and South Sacramento (-25,000 SF) submarkets outpaced growth elsewhere and sent overall vacancy upward.

In the Davis/Woodland submarket, a new 160,000 SF sublease opportunity at Woodland Business Park, a 66,000 SF vacancy at the Ventura Industrial Park and a tenant giveback of 64,000 SF at the Woodland Distribution Center, were among the new vacancies that helped drive net absorption into negative territory.

In the Natomas/Northgate submarket but a new 340,000 SF sublease and a 54,000 SF direct vacancy at Metro Air Park offset occupancy gains from new tenants both at that project and across the trade area, Other new deals included a 54,000 SF lease at Metro Airpark, a 50,000 SF deal at 3443-3475 Airport Road and multiple smaller leases of 20,000 SF or less.

DEVELOPMENT PIPELINE RAMPING DOWN QUICKLY

We are currently tracking just over 1.5 MSF of new industrial product under construction in the region. One year ago, this number stood at 4.4 MSF. Since 2020, the local industrial inventory has grown by a whopping 10.0% in the largest wave of new development in the region since has been the late 1990s/early 2000s. The big difference is that vacancy levels were in their teens when that wave of building slowed, while the current 6.2% vacancy rate is much closer to the classic market definition of equilibrium. Market equilibrium is when there is enough available product in the marketplace to accommodate expansion from tenants (and economic growth), but not so much as to prevent sustainable rental rate growth in line with overall inflation.

The worst of the supply wave is over. There are currently 16 projects under construction across the Sacramento region totaling just over 1.5 MSF of new industrial space, the smallest amount to be in the pipeline since 2018. The Natomas/Northgate submarket leads the way with Target’s 525,000 SF distribution center slated for Q1 2025 delivery. In the Folsom/El Dorado Hills submarket. PacTrust’s Gateway El Dorado Park has two new advanced manufacturing buildings under construction that will add 148,000 SF of new speculative inventory upon their completion in September, while a 148,000 SF warehouse build-to-suit is under construction at 4490 Golden Foothill Parkway with a slated delivery of January 2025. Likewise, all the 150,000 SF of space under construction in the McClellan submarket is already leased. In fact, only 500,000 SF of the space currently under development in the Sacramento region is still available, the rest has lined up tenants already.

This noticeable deceleration in construction activity should give the market time to absorb much of the recent wave of development. This

slowing pace of development will help push rental rate growth back into positive territory once more robust economic expansion picks up (likely in the next 12-18 months).