And I’m not just referring to the Real Estate market!

You may know me well, or you may be hearing my name for the first time. Either way, I think it’s fitting to introduce myself properly since our newsletter is now in your hands My name is Bruce Gallagher, and it’s my privilege to serve the Lake Country area as managing partner of the Gallagher Lake Country Real Estate Team.

If you are familiar with our team, then you may remember that for many years our business used to be simply named “Beachy Gallagher” (since 1982, actually!) For over 30 years, Beachy Gallagher’s name was what people knew the business as, but when I joined her and my sister/partner Kathy Gallagher Rosenheimer in 2010, we became “Gallagher Lake Country Real Estate”

Much has changed in the past 15 years!

On a personal level - I and my wife, Rebecca, had our daughter, Beatrice (“Bea”) 12 years ago, my sister Kathy and her husband (also Bruce – aka “Louie”) became “empty nesters”, and my niece, Chelsea Rosenheimer Schmidt (Kathy and Louie’s daughter) joined our team as the 3rd generation in the business 3-1/2 years ago. Chelsea and her husband Andy also welcomed a potential 4th gen realtor, Henry, into the world almost 2 years ago Sadly, we lost Beachy 4 years ago after a valiant battle with Parkinson’s disease We proudly carry on the business with her spirit of appreciation for this community and its people, the lakes, her strong sense of fair play, hard work, fun, adventure, and gratitude

Professionally – we went from the depths of the “Great Recession” of 2007-2012 into the more recent unprecedented “Pandemic Real Estate Boom” of 2020-2023

Our team also grew with the addition in 2015 of Jennifer Wolf-Beaster as realtor and now our Director of Operations, and Debbie Taylor joining us 3 years ago to help provide fantastic general and administrative support.

We decided to begin communicating in a newsletter format to help keep our friends, clients and community current on what has become one of the most talked about (and often misunderstood) topics at the dinner table, cocktail parties and in the grocery store: the Lake Country Housing Market and Values!

However, we will endeavor to also share other interesting and helpful bits of information and profiles about our area –the things, events, people and businesses that make the Lake Country such a great place to live and enjoy

If you have an idea for a topic or feature for future editions, questions or comments, please email me (bruce@GallagherLakeCountry com) or give a call

Thanks for reading Gallagher Lake Cou

Bruce Gallagh

Community Spotlight: Stone Bank Farm Market

As you walk through the doors of Stone Bank Farm Market you’re greeted by the smell of fresh cut flowers, herbs picked from the garden mere hours before, delicious homemade pastries and a warm “welcome in!”

But Stone Bank Farm Market is so much more than a place to buy fresh produce, grass-fed meats and artisanal foods. This working farm has become a pillar of our Lake Country community, bringing people together for cooking classes, lectures on sustainability, farm tours, yoga classes, dinners in the historic barn, kids activities and so much more

The origin story of Stone Bank Farm Market dates back to 1844, when Scottish immigrant John Ferguson purchased 225 acres from the government. 14 years later he donated a portion of the acreage to build a Presbyterian church, which is home to the Market today

The Ferguson family built and operated a gristmill on the property and eventually turned to dairy farming due to fears of mill closure from the invention of electricity. For nearly 50 years no crops were planted or animals pastured at Stone Bank Farm Market However, in 2003 the Faye Gehl Conservation Foundation purchased the farm from the Rogers family and has been working to bring it back to life ever since.

In 2010, the Foundation began returning it to use, growing fresh greens and heirloom vegetables with organic practices. The farm is also raising a herd of Red Devon cattle using rotational grazing, which allows the soil and crops time to recover

In the midst of the pandemic, Stone Bank Farm Market added a commercial kitchen and forged a relationship with James Beard nominee Chef Kyle Knall (who co-owns Birch in downtown Milwaukee – a must visit if you haven’t already!) More recently, Stone Bank Farm welcomed Nourish Organic Juice Bar to the Market Nourish serves superfood-infused juices, smoothies, snacks and healthy made-to-order food.

Food is ideally meant to be grown, harvested and eaten almost immediately How lucky are we that Stone Bank Farm Market offers our community access to fresh, sustainably grown food right in our backyard? If you haven’t stopped in yet, we can’t recommend this Lake Country gem enough!

Market Recap and 2025 Projections – Lake Country

By Bruce Gallagher, Managing Partner

In each edition of this newsletter, we will present data and statistics from our local market – not the national market, or even the Southeastern Wisconsin or Milwaukee markets, but right here in the Lake Country There is often a meaningful difference, and it can be risky to make decisions or assumptions based on anything other than current and very local market information about where you live.

One of the primary goals of our family real estate practice is to give not only accurate data and information (often not available anywhere else and hopefully interesting), but to also provide our friends and clients with sound interpretations of the data formed by our first-hand experiences and observations about the trends and nuances in the local luxury and lake property markets We feel that it’s critical to combine the “art (subjective)” and the “science (objective)” to help paint an accurate and actionable understanding.

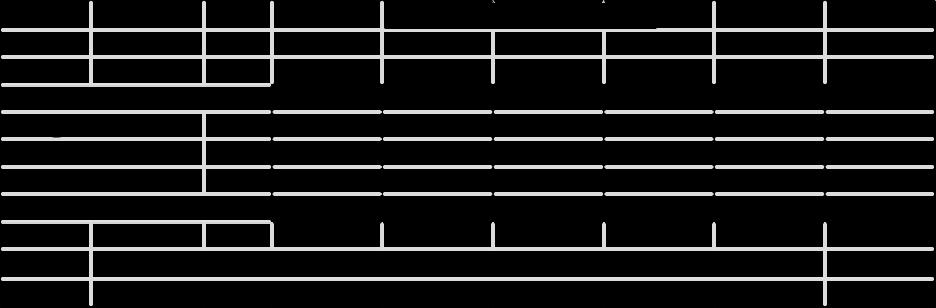

To that end, here are some interesting statistics showing changes in the Lake Country market from 2019 through the escalation of the “pandemic surge” market of 2020 – 2022, and into the post-pandemic climate of 2024:

Most obviously, average prices have increased to record levels since 2019, triggered by the unprecedented housing appreciation of the pandemic, huge demand for the Lake Country lifestyle and overall inflation. Some noteworthy facts include:

General property values increased by $225,956, or 51% from 2019 through 2024! Lake property values increased by $792,066, an astounding 73%!

What we saw in 2024:

This past year was challenging for both prospective buyers and sellers, as low inventory and continued high interest rates impacted both sides:

Sellers were able to capitalize on the benefit of record high prices in most sectors, assuming the homes were in good condition and locations However, many sellers and prospective sellers often found it difficult to justify moving if they had really low interest rates, with approximately 60% of all households having mortgages below 4% and 25% at 3% or less, as opposed to the 7%+/- rates which have been prevalent for the past 12 months. Add to that the challenge of very low inventory for potential sellers to move into whether upgrading or downsizing. Consequently, some decided to bite the bullet and accept the trade-offs, while others chose to stay put

Buyers have been faced with very low inventory, high rates, increasingly high prices (housing as well as general inflation) and a continued high level of demand/competition

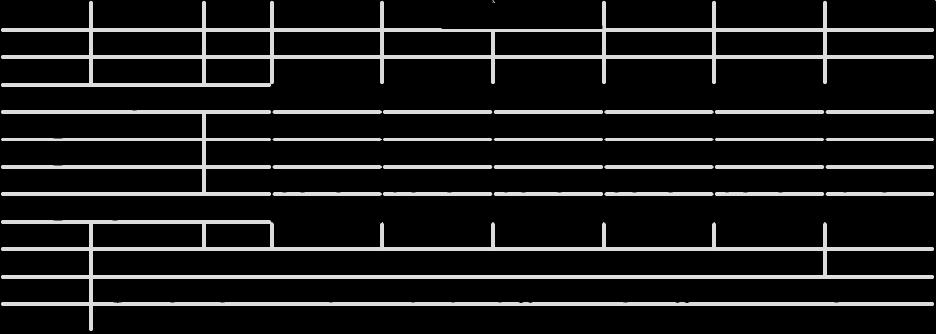

Inventory:

A major part of the story is about, you guessed it, INVENTORY! The fundamental lack of inventory has been a major factor in the steep increase in values and drop in quantity of properties sold in recent years. As this table demonstrates, from 2019 to 2024 inventory in the general market is -24% and the lake market -54%.

Fundamental demand has remained relatively strong for most kinds of homes and properties, even in spite of much higher interest rates, inflation, and other challenges However, many potential high-end sellers have been in a holding pattern largely due to the lack of options and choices for their “next move”, be it upgrading or downsizing. Many sellers-to-be-buyers are also sensitive to the interest rate climate and reluctant to leave behind historically low rates when they are faced with much more expensive financing for their next home (unless they will be cash buyers)!

All of this has continued to push the market to historically high prices that are all the conversation at coffee shops and cocktail parties

Looking forward to 2025:

Here are some trends that developed in 2024 that will likely impact where the market is headed in 2025: In 2024 we saw a reduction in the number of showings, and fewer competing offers for properties

The number of price reductions on listings increased substantially from 2023 Contingency-free offers became more of a rarity – and usually only occurred on the more “special” hard-to-find properties that garnered multiple offers. Most buyers were once again able to include inspection and financing contingencies.

Buyers placed more of a priority on purchasing homes that were updated, or at least appeared to have been well-maintained and cared for: “move-in ready” was coveted, and listings in poor condition were much more difficult to sell

List price matters again! Listings that were significantly overpriced often languished – and in this market if a home doesn’t find a buyer within the first few weeks, the buyer pool becomes suspicious. This dynamic usually diminishes perceived value and the listing takes much longer to sell.

We expect these same trends to continue for 2025 Pricing will be very sensitive, but with proper preparation and positioning, the top homes/properties will have the potential to meet or even exceed record prices, with most still being near recent all-time highs

If meaningfully more inventory does come to the market, it could prompt more balance and a softening of prices – especially for those homes that aren’t “top of class” in their respective niches with regard to condition, age, location, land/lakefront, and other subjective attributes.

As always, a major real estate and housing decision should focus primarily on the personal and lifestyle aspects and priorities of each buyer and seller, rather than “waiting for the perfect time” Hopefully this has been a helpful article for those of you contemplating a change In summary, 2025 will hold great opportunities for both buying and selling – especially when managed well with good advice and a sound plan based on the “market of the moment”.

Ask the Expert(s): All Things Mortgage in 2025

In this ever-changing real estate (and lending) market, we thought it would be interesting to chat with two of our trusted lenders, Dan Nielsen of Wintrust Mortgage and Patty Napgezek of Fairway Independent Mortgage Corporation about their outlook on the market and rates this year

Dan Nielsen, NMLS #553928

Residential Mortgage Specialist (262) 563-4134

Patty Napgezek, NMLS #553928

Branch Manager (262) 490-9050

What is the mortgage industry outlook for 2025? And where do you see rates headed? (we know you don’t have a crystal ball…)

Dan: Mortgage loan originations are predicted to increase by 28% in 2025, from $1 8 trillion in 2024 to $2 3 trillion in 2025 “In an environment where inflation is stubborn and economic growth is strong, there’s just not much to push long-term interest rates materially lower,” according Bankrate’s Chief Financial Analyst, Greg McBride The average 30 year fixed rate is currently 7 06% and is projected to end 2025 at 6 2% to 6 5% Bankrate, Fannie Mae, and the Mortgage Banker’s Association agree with this projection.

Patty: In 2025, the hope for the mortgage industry is that we are all anticipating that there will be a pickup in housing supply by Q2. Right now the demand is higher than the supply. Home affordability based on current rates does reduce the demand which in turn affects the supply for those buyers who can afford homes at this time We anticipate and hope that mortgage rates will decline to somewhere around 5 75% to 6 00% mid-year When rates reach the 6 00% threshold, the housing market becomes more favorable and the demand increases

What are some of the challenges a buyer might face when applying for a jumbo loan?

Dan: Jumbo loans typically have tighter underwriting guidelines than Conforming loans such as: Debt-to-income ratios are compressed from 50% to 43%, minimum credit score requirements are higher, ranging from 680 to 720 verses 600 to 620, minimum trade line requirements range from 2 to 4 tradelines verses no minimum requirements, minimum down payment is typically 20% verses 3% to 5% and monthly payment reserve requirements are typically six to 12 months verses no reserve requirements.

Patty: Many Jumbo investors that had pulled out of the market completely in 2023 due to risk are returning. From a lending perspective, we are required to obtain more documentation for jumbo loans as compared to conventional financing Documentation goes through a much more rigorous review in underwriting to minimize risk, however there are increasingly more programs and options available to the consumer The other piece of good news is that the conventional loan limit has increased to $806,500 Therefore, the need for a jumbo loan won’t be until the loan amount exceeds this new dollar amount: we may see lower demand for jumbo loans.

Where do you see rates for jumbo loans heading in 2025?

Dan: Jumbo rates should follow a similar pattern to the conforming rates. Jumbo loans are often ARM’s (Adjustable Rate Mortgages) and we might see a greater easing on ARM rates.

Patty: We do see/expect rates coming down by Q2 hopefully in the 6% range like conventional rates The risk of the ARM rates is forcing more loan products to be offered as a 30 yr fixed amortization rather than adjustablerate mortgages with competitive rates 20% down payments are more of the norm

From your perspective, what is your number #1 tip to get a transaction to a smooth closing?

Dan: The number #1 lending tip for a smooth closing is a fully verified buyer pre-approval from a reputable and qualified mortgage lending specialist in advance of the purchase contract The majority of issues that challenge a smooth closing is loan commitment; the majority of loan commitment issues relate to buyer’s documentation not supporting income, assets and credit; or the buyer’s documentation disqualifies income and assets necessary to support a loan commitment

Patty: As a lender, I believe strongly that the best thing you can do to get a transaction to a smooth closing is to work with a lender who spends the time on the front-end reviewing income and asset documents and providing a solid preapproval Due diligence and communication on the front end are key

Anything you’d like to add about the broader real estate market?

Dan: A tip on interest rates: follow the daily trading of the US 10 year treasury yield rather than the Federal Reserve’s announcements The bond market drives long term mortgage rates and the Federal Reserve drives short term line of credit rates The US 10 year treasury yield moves up or down based on actual inflation and future inflation expectations “Where inflation goes, so goes the mortgage rates ”

Patty: From a broader perspective, the secret to building wealth is through home ownership. Home equity is still the biggest wealth builder!

From the Gallagher Lake Country Kitchen

Say goodbye to store-bought salad dressing! This is one of Kathy’s favorites and is a weekly staple in the Rosenheimer house It comes together quickly, can be easily doubled (in fact, she recommends it) and can be stored in the fridge for a week!

Hummingbirds are the only creatures that can fly backwards

The lighter was invented before the match (a converted flintlock pistol in the 1500’s, before the match in 1826)

The average human will eat 8 spiders while asleep in their lifetime

The strongest muscle in the body is the tongue (often we wish it were the ears…!)

Upcoming Events in Lake Country

February 8: Oconomowoc Galentine's Day, 10am-5pm

February 15 & 16: Cedarburg Winter Festival

February 16: Tinctures & Salves Workshop at Gwenyn Hill Farm, 11am

February 22: The Art of Beekeeping Workshop at Gwenyn Hill Farm, 11am

February 28: American Red Cross Blood Drive - Hartland Public Library

March 14: Grow Your Own Organic Food - Stone Bank Farm Market 10am

April 10: Delafied Ladies Night Out, 5pm

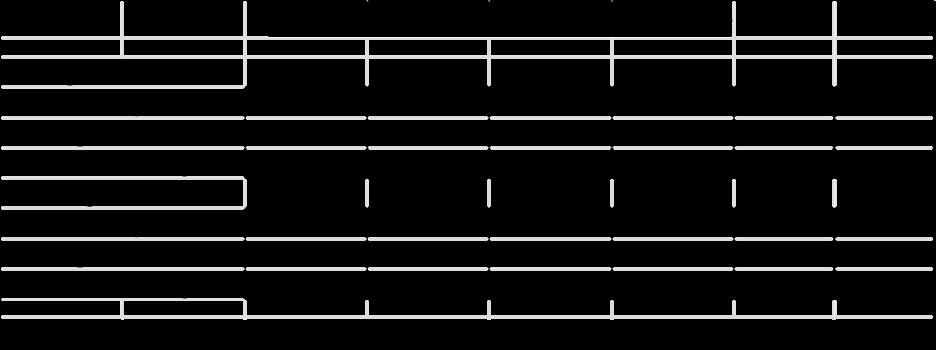

SOLD IN 2024

UPPERNASHOTAHLAKE UPPERNASHOTAHLAKE

BEAVERLAKE BEAVERLAKE

HARTLAND HARTLAND

SOLDFOR$7250000

DELAFIELD DELAFIELD

SOLDFOR$4250000 SOLDFOR$4,250,000

UPPER NEMAHBIN LAKE UPPER NEMAHBIN LAKE

FOR $4,000,000 SOLD FOR $4000000

We are proud to have sold all these fantastic homes and properties in 2024! Thanks to all our sellers and buyers who trusted our team to be part of such an important aspect of your lives. SOLDFOR$1,260,000

FOR $2,800,000 SOLD $2,800,000 LAC LA BELLE LAC LA BELLE

DELAFIELD DELAFIELD

SOLDFOR$1310000 SOLDFOR$1,310,000

SOLDFOR$1050000 SOLDFOR$1,050,000

OKAUCHEELAKE OKAUCHEELAKE

CHENEQUA CHENEQUA

DELAFIELD DELAFIELD

SOLDFOR$950,000 SOLDFOR$950000

MERTON MERTON

SOLDFOR$740,000 SOLDFOR$740000

SOLDFOR$820,000 SOLDFOR$820000

SOLDFOR$1,000,000 SOLDFOR$1000000

SOLDFOR$988100

SOLDFOR$820000

DELAFIELD DELAFIELD

SOLDFOR$795,000 SOLDFOR$795,000

If you are contemplating a sale, or simply wish to get an accurate estimate of value for financial planning purposes, my team and I are available to provide a valuation of your property at no cost, and with no obligation whatsoever.

We are also happy to confidentially explore either a private sale or a public listing on the MLS. There are advantages and trade-offs with both approaches, so it is a matter of matching those factors with the goals of each individual seller. Please call me at 414-881-8586 and we can schedule a time to get together!