10 Cybersecurity – a challenge for the market and the FMA

THEMATIC PAGES

38 Fintech – more than just new business models

46 European cryptomarket regulation

54 Cooperation within the European System of Financial Supervision

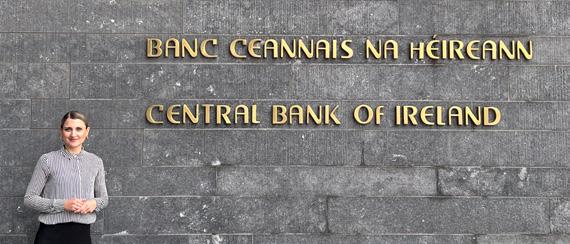

64 In Ireland for the FMA

70 From internship to Executive Board

76 New, more collaborative ways of working

4 SPOTLIGHT

6 FOREWORD

PROGRESS REPORT

12 SUPERVISION AND RESOLUTION

13 Impact of rising interest rates on the real and financial economy

15 Trends and risks

16 Quality assurance for auditors

17 Macroprudential supervision

18 Licences, approvals, registrations

20 Ongoing supervision

28 Ad hoc supervision of TT service providers

28 Due diligence supervision to combat money laundering

32 International administrative assistance

33 Enforcement

40 Activities of the resolution authority

41 Outlook

42 REGULATION

43 Regulatory developments continue to be dynamic

43 Redesign of the legal framework for the supervision of banks and investment firms

48 Outlook

50 EXTERNAL RELATIONS

51 Work meetings in Hong Kong and Singapore

51 Annual media conference

52 National cooperation

52 Bilateral cooperation

56 European cooperation

57 Global cooperation

57 Outlook

58 ENTERPRISE AND TEAM

59 More digital, more diverse, more sustainable

61 Development of the workforce

61 Educational background and nationalities

62 Corporate governance

62 Governance, risk & compliance

66 FMA funding

67 Changes and promotions

67 Opportunities for young talent

68 Outlook

72 New employer web presence for the FMA

72 Code of conduct for maintaining high quality

73 Digital excellence at all levels

ANNUAL REPORT AND FINANCIAL STATEMENT

81 Annual report

82 Balance sheet

83 Income statement

84 Notes on the financial statement

88 Attestation of the Audit Office

FMA Annual Report 2023

STABILITY IN TURBULENT TIMES

Last year was characterised by persistently high inflation, rising interest rates, and a weakening of the global economy. Despite this, the Liechtenstein financial centre once again proved its stability.

“A

UNIQUE OPPORTUNITY“

NEW FOUNDATIONS FOR THE BANKING CENTRE

The FMA was mandated by the Government in 2022 to completely revise the legal framework for the supervision of banks and investment firms and to align the system of domestic laws with the regulatory system of EEA law. This work is now well advanced.

The FMA offers employees the opportunity of secondments with foreign partner authorities. Alexandra Bickel is a legal specialist at the FMA and completed a secondment at the Central Bank of Ireland – “a unique opportunity,“ as she says.

SECONDMENTS WITH FOREIGN PARTNER AUTHORITIES TO CONTENTS

RECOGNITION …

… is what the FMA once again received for its attractive working conditions – with the Swiss Employer Award 2024. This means the FMA is one of the top employers in Switzerland and Liechtenstein. What makes us especially happy: Our employees were the jury. The FMA also made the podium in the NPO & Government category of the Digital Economy Award.

0 METRIC TONS …

is the FMA’s net CO 2 emissions target by 2035. This is set out in the FMA’s sustainability strategy. With this target, the FMA wants to make a contribution to mitigating climate change. The FMA is working closely with experts to implement and verify the target.

FROM INTERNSHIP TO EXECUTIVE BOARD

In September, the Board of Directors appointed Simone Edelmann-Boeniger as a member of the Executive Board effective 1 March 2024. Simone is not only a recognised expert, but has also worked for the FMA for many years – she joined as an intern in 2009.

Annual Report 2023

As in previous years, the situation in the financial sector during the reporting year was characterised by turbulence. After the Covid-19 pandemic, the outbreak of the Ukraine war, and the rise in energy and food prices, inflation in particular was a defining factor for the financial market. It almost seems as if crisis has become a constant. Turbulent times seem to be the new normal. What is likewise constant in this context, however, is the extremely high stability of Liechtenstein’s financial sector. Once again, the financial centre has demonstrated a high level of resilience.

To ensure that this continues to be the case, the FMA works closely together with financial intermediaries. Thanks to its in-depth analyses, the FMA provides the necessary basis for assessing risks appropriately and addressing them effectively using suitable micro- and macroprudential instruments.

Crises often also present opportunities and drive change. Key topics during the reporting year included, in particular, digitalisation, establishing new forms of work, and enshrining sustainability in our operations. At the same time, these topics offer numerous synergies and have a positive influence on each other. For example, digitalisation of the FMA is already well advanced. More and more processes can be mapped digitally from start to finish without media disruptions. This has already resulted in a significant reduction in paper consumption. Moreover, digitalisation also means that employees can now work from any location. This in turn has led to massive savings in carbon emissions thanks to reduced traffic. At the same time, digital and location-independent forms of work are also changing the demands on the FMA’s premises. The FMA has accordingly redesigned part

of its office space, offering employees a modern working environment in a pilot zone that meets the changed requirements.

In this way, the FMA is responding to a need of its employees and ensuring its long-term attractiveness as an employer. What also contributes to the FMA’s attractiveness is that it pays fair wages and does not discriminate against women or men, promotes the compatibility of family and career through part-time work, including in management positions, and offers attractive career opportunities. The best proof of this is our newest member of the Executive Board: Simone Edelmann-Boeniger started as an intern at the FMA more than ten years ago.

Developments in financial market regulation also continue to be dynamic. The FMA has been mandated by the Government to prepare an overview of possible options for redesigning the regulatory structure of the supervisory law applicable to banks and investment firms. The work is already well advanced, and the redesign of financial market law is due to be completed by 1 January 2025. New rules will also soon

apply to FinTechs. In order to continue to promote and exploit the potential of the digital transformation of the financial sector while addressing potential risks and ensuring the protection of investors and financial markets, the European Union has adopted a comprehensive package of measures – the Digital Finance Package. A key element of this package is the Markets in Crypto-Assets Regulation (MiCAR). The FMA was busy with implementation work during the reporting year.

In addition to the turbulent macroeconomic environment, supervision continues to focus in particular on combating money laundering, on climate, social and governance risks (ESG risks), and on ICT and cyber risks.

Dr. Christian Batliner Mario Gassner Chairman of the Board of Directors Chief Executive Officer

SUSTAINABILITY AT THE FMA

Sustainability plays a crucial role in the financial world as well and is one of the central issues of our time. The FMA considers sustainability in two dimensions: firstly in relation to its supervisory activities, and secondly as an enterprise itself. The role of sustainability in supervisory activities is largely determined by applicable EU regulations relating to sustainable finance. In its sustainability strategy, the FMA as an enterprise defines the four goals of “Climate neutrality by 2035“, “Avoidance of negative environmental impacts“, “Promotion of a sustainable human resources policy and management“, and “Ensuring sustainable governance structures“. These goals are based on the ESG (environmental, social, governance) criteria. The FMA sustainability strategy has been in effect since 1 January 2023.

In the first year after entering into effect, the focus was on drawing up the concrete implementation plan. The motto here is “As much as possible, as quickly as possible“. Accordingly, numerous improvements have already been introduced:

– The FMA’s operational mobility management has significantly reduced the amount of motorised private transport generated by employees. In 2022, about 40 % of motorised private transport was saved through remote work alone. This corresponds to about 750,000 car kilometres or 127 metric tons of CO 2 1 The savings for 2023 are at a similar level.

– In the reporting year, the FMA considered and approved the installation of e-charging stations in the FMA parking garage. The e-charging stations will be installed at the beginning of 2024 and will be available to both employees and visitors.

– In 2023, the introduction of a catering service in the FMA building was evaluated. An on-site catering option can help to further reduce motorised private transport. As a result of this evaluation, fresh and locally produced meals from a young Swiss company specialising in sustainable employee catering have been made available to employees since the

1 Based on average emissions of 170 grams of CO 2 per kilometre driven, according to Our World in Data.

beginning of 2024. The changing menus are freshly hand-cooked by regional partner chefs and are provided in a refrigerator. Attention is also paid to healthy, seasonal, and sustainable ingredients. The contents of the refrigerator are adapted and replenished according to the employees’ preferences based on data collected. This ensures a balanced selection and minimises food waste.

– During the reporting year, the switch to a full green electricity tariff was reviewed and implemented. As a result, the FMA’s electricity consumption is now climate-neutral.

– To further reduce motorised private transport, the decision was made to purchase FMA bicycles. The bicycles will be available to employees starting in March 2024 and will be used in particular for short business trips.

– The FMA’s new management training concept places a special focus on sustainability. As multipliers, managers play a key role in the transition to a more sustainable working environment and are called upon to contribute to cultural change.

– The FMA’s lighting concept was adjusted in the reporting year. In the parking garage in particular, lighting and energy consumption were reduced.

– Paper consumption was reduced significantly. Printing costs were reduced from roughly CHF 20,000 in 2022 to CHF 5,500 in the reporting year. This was made possible by increasing digitalisation.

As a public enterprise, the FMA bears a special responsibility towards the environment and society and has a particular obligation to make an effective contribution. To exploit synergies and share proven approaches, the FMA coordinates its activities with the Liechtenstein Government, the National Administration, and other relevant interest groups. At the international level, the Financial Market Authority cooperates with the Network for Greening the Financial System (NGFS), of which it has been a member since the end of 2022.

Seasonal and regional catering options support the goals of the sustainability strategy.

TO CONTENTS

CYBERSECURITY – A CHALLENGE FOR THE MARKET AND THE FMA

More than 10 terabytes of data are stolen in the EU through cyber attacks – every month. Phishing and ransomware Trojans are among the most significant cyber threats in the EU. DDoS (distributed denial of service) attacks also pose a significant threat. The worldwide cost of cybercrime to the economy amounted to an estimated EUR 5.5 trillion at the end of 2020, double the amount for 2015. The war in Ukraine has further exacerbated the threat situation. The conflict has activated numerous hacktivists, cybercriminals, and state-supported groups. Liechtenstein intermediaries are also affected. The FMA accordingly attaches great importance to cybersecurity.

Cyber risks pose challenges for both financial market participants and the FMA. Security incidents in the use of information and communication technologies (ICT), such as data leaks and system failures, can cause immense damage. Attacks with criminal intent are also becoming more prevalent.

Financial service providers are among the most popular targets of cyber attacks. Not only the companies themselves are at risk. The attacks jeopardise the protection of clients and ultimately also the stability of the entire Liechtenstein financial market. ICT security incidents such as data leaks and

system failures can result not only from external events such as cyber attacks, but also from internal errors or insufficient infrastructure. Greater networking increases the potential vulnerability of the ICT infrastructures of financial service providers. This is another reason why the FMA attaches great importance to cybersecurity.

The ICT Guideline, which entered into effect in 2022, defines the requirements in accordance with international standards that intermediaries must meet when dealing with ICT risks. These requirements were the focus of the FMA’s supervisory activities in 2023.

Clear requirements minimise the risk of ICT security incidents and show market participants how they can counter ICT risks. The ICT Guideline includes requirements for the strategy and governance of financial service providers as well as for information security risk management and the associated structures and processes. Proportionality is also taken into account. The requirements are based on the risk structure, complexity, size, scope, and type of business of a financial service provider. Since 2020, 18 attacks on Liechtenstein financial intermediaries have been reported to the FMA – some of which were carried out using a combination of methods. In two cases, it was possible to quantify the effective financial loss suffered by the financial intermediary.

TYPES OF CYBER INCIDENTS

Ransomware is a type of malware that restricts or prevents access to data and systems. A ransom is then demanded for releasing the data or system. Such a malicious program either blocks all access to the system or encrypts certain user data.

Malware is software developed with the aim of executing unwanted and usually harmful functions on an IT system. Malware often spreads on traditional IT systems via email attachments or manipulated websites or data carriers.

Phishing attacks are fraudulent emails, text messages, phone calls, or websites designed to trick people into downloading malware or giving away confidential information.

DDoS (Distributed Denial of Service) is a type of cyber attack that attempts to overload a website or network resource by flooding it with malicious traffic so that it can no longer be operated.

Social engineering exploits human characteristics such as helpfulness, trust, fear, or respect for authority to cleverly manipulate people and trick them into disclosing confidential information, bypassing security functions, making bank transfers, or installing malware.

Both incidents were caused by malware. In total, 12 incidents were attributable to ransomware, 10 to other malware, 2 to phishing, 6 to DDoS attacks, and 6 to social engineering.

Figure 1 Cyber incidents per year **Cases considered until mid-year.

SUPERVISION AND RESOLUTION PROGRESS REPORT

The past year was characterised by persistently high inflation, rising interest rates, and a weakening of the global economy. Against this backdrop, the financial stability risks at the international level remained high. The resolution authority updated three group resolution plans for the systemically important banking groups and one group resolution plan for smaller financial intermediaries. In addition, development of the Liechtenstein resolution financing mechanism was continued. During the reporting year, Macroprudential Supervision was closely involved in the preparatory work for Liechtenstein’s possible accession to the IMF. In this context, an initial balance of payments for Liechtenstein was estimated under the leadership of the FMA and in close cooperation with the SNB and the Office of Statistics. Providing this data was a prerequisite for Liechtenstein to submit its official application for membership to the IMF at the end of May 2023.

IMPACT OF RISING INTEREST RATES ON THE REAL AND FINANCIAL ECONOMY

The past year was characterised by persistently high inflation, rising interest rates, and a weakening of the global economy (Figure 2). Against this backdrop, the financial stability risks at the international level remained high. Although the financial sector in general and the banking sector in particular are benefiting from the recovery of the financial markets and rising interest rates, financial market players could face increasing challenges in the coming months. The financial markets are currently reflecting a relatively optimistic scenario, in anticipation of only a mild economic slowdown, a rapid decline in inflation, and an imminent reduction in interest rates. Against this backdrop, the financial markets remain vulnerable to unexpected negative developments, given that inflation may prove more persistent than predicted and economic fragility could intensify further. Risk premiums have also remained low over the past year, even though rising interest rates are increasing the financial burden on companies accordingly. Higher interest rates could also revive discussions about the sustainability of public debt, especially if interest rates remain high for an extended period of time (Figure 3).

Economic development remained below average last year in Liechtenstein as well. The KonSens economic indicator, which is published on a quarterly basis by the Liechtenstein Institute, has been in negative territory for almost two years now, signalling weak economic development. This phase represents the longest continuous period of negative KonSens values since the negative phase of 2001 to 2003. This is due in particular to weak export growth, given that both cyclical and structural factors are dampening external demand. The weakness in the domestic economy is currently being caused by both the slump in the global industrial sector and weak global trade. Structural factors also play a role in this regard. In particular, globalisation has slowed down noticeably since the

global financial crisis, with the ratio of global trade to gross domestic product stagnating in recent years. Rising geopolitical tensions and the increasing fragmentation of the global economy pose additional challenges for Liechtenstein’s economic prospects. These factors can create uncertainties and trade barriers and make it more difficult for small, exportoriented economies to be successful on the global market. The development of Liechtenstein’s economy therefore remains heavily dependent on global economic trends, in light of its high export orientation.

The turnaround in interest rates has increased vulnerabilities in the real estate and mortgage market as well. Although the financial burden on borrowers in the Swiss franc currency area remains limited due to moderate interest rate increases, the financial cycle has ultimately turned here as well. The correction on the real estate markets has been orderly so far in most European countries. In Liechtenstein as well, the short-term risks in the household sector are likely to be limited compared to other countries due to the moderate growth in real estate prices in recent years, the high proportion of fixed-interest loans, the high resilience of the banking sector, and the robust labour market. However, given that private household debt in Liechtenstein is among the highest in Europe, the structural vulnerabilities are elevated and must be addressed with appropriate measures in order to continue to ensure stability in the medium and long term.

The banking sector in Liechtenstein benefited from rising interest rates last year. Despite this, profitability in the Liechtenstein banking sector – measured in terms of return on equity – continues to lag significantly behind banks in the EU and the US. While the high capitalisation explains part of this difference, a closer analysis shows that – in contrast to other countries – costs have risen in line with interest income, which limits the increase in profitability accordingly. Against the backdrop of higher interest margins, the income structure in the banking sector has also

changed significantly over the past year. While the share of fee and commission income fell, the share of interest income in total income increased. Against the backdrop of higher interest rates, banks could be confronted with rising refinancing costs and increased credit risks in future. Although this constitutes an additional challenge for the banking sector, the impact is likely to be less pronounced than in other countries thanks to lower inflationary pressure, moderate interest rate increases in the Swiss franc currency area, and the robust capitalisation and liquidity situation.

Risks in the non-banking financial sector remain limited. Although the profitability of the insurance sector is below average compared to other European countries, the sector has robust capitalisation, which contributes significantly to the stability of the sector. At the same time, uncertainties in the insurance sector remain significant, given that rising inflation might directly increase the cost of claims and thus negatively impact margins and profits in future. While public pension provision (Old-Age, Survivors, and Disability Insurance; first pillar) and private pension schemes (second pillar) had to deal with significant market-related losses in 2022, the pension system benefited from the market recovery in the reporting year. The sector may benefit from higher interest rates

in the medium to long term as well. Investment funds in general are exposed to comparatively low risks. Identified risks in the area of consumer protection and supervisory powers are not specific to Liechtenstein. Beyond this, potential profitability risks for some (mostly smaller) domestic funds underscore the need for more in-depth regulatory supervision to ensure the resilience of the non-banking financial sector.

Overall, the Liechtenstein financial sector is characterised by continued stability and solidity, and systemic risks continue to be assessed as limited. The Liechtenstein financial sector is well equipped to master the challenges ahead. Nevertheless, in view of increasing global uncertainties, geopolitical tensions, and financial turbulence, it is essential to maintain a high level of capitalisation and resilience in the financial sector. For this purpose, a range of macroprudential tools are available that can continue to be deployed as required.

Sophia Doeme, Deputy Head of Section Macroprudential Supervision

Figure 2

Inflation (annual, in %)

Source: Bloomberg.

TRENDS AND RISKS

At the end of each year, the FMA publishes its priorities of supervision for the following year. These are based on a prior assessment of trends and risks, which are summarised below.

Macroeconomic environment: At the international level, financial stability risks remain high due to persistent inflation and weaker growth prospects. Due to a sharp rise in interest rates, global economic activity slowed last year, while inflation fell only gradually. The economic slowdown is especially noticeable in the industrial and manufacturing sector and is leading to subdued global trade. The financial markets remain susceptible to further corrections. While equity valuations recovered starting at the beginning of the year, the first corrections already followed in the course of the year. Moreover, the markets are currently optimistic with regard to future earnings and growth, as well as a relatively rapid decline in inflation, which could lead to possible negative surprises.

Money laundering: Due to the small size of the Liechtenstein domestic market, Liechtenstein financial service providers are predominantly active in crossborder business. The financial centre is therefore strongly oriented towards the provision of services for

persons abroad. This international orientation offers Liechtenstein financial market participants many opportunities, but also entails certain risks due to the persons and countries involved and the increasing complexity of business relationships. The FMA there-fore continues to assess the risk of money laundering as high. Violations of supervisory law can result in considerable sanctions and reputational damage for financial institutions both abroad and in Liechtenstein. The FMA has recently identified a number of violations of money laundering provisions by various players in the Liechtenstein financial centre. This indicates that the risks for financial institutions in the cross-border wealth management business remain high. The use of offshore companies and complex structures continues to increase risk. Liechtenstein last underwent a country assessment by MONEYVAL in 2022. In this international comparison of national anti-money laundering measures, Liechtenstein’s marks were very positive.

Climate, social, and governance risks (ESG risks):

The transition to a climate-friendly economy remains challenging. Assessing the impact of physical and transitory risks on financial institutions is complex. Although banks in Liechtenstein have limited exposure to companies with high emissions, some banks could be exposed to climate risks through their mortgage loans. Similarly, the insurance sector faces

Figure 3

Key rates of central banks (in %)

Source: Bloomberg.

rising climate risks caused by the increasing frequency and unpredictability of natural disaster events. Although the availability of data at an international level is still a problem, monitoring of climate-related risks must be improved in future, especially in order to assess climate risks appropriately. The EEA Financial Services Sustainability Implementation Act (EWR-FNDG), which entered into force on 1 May 2022, makes the EU Disclosure Regulation and Taxonomy Regulation applicable in Liechtenstein by way of national law. The implementation of the legal requirements poses a key challenge for intermediaries and the financial centre as a whole. These implementation challenges increase the risk of greenwashing.

ICT and cyber risks: The use of information and communication technology (ICT) by financial institutions and their clients has increased significantly in recent years. The number of cyber attacks is also steadily increasing. The war in Ukraine has made it clear that attacks on infrastructures represent a key risk. Further geopolitical developments could drive the number of cyber attacks even higher. Cyber incidents pose a systemic risk to the financial system, with the potential to severely disrupt critical financial services and operational processes. It should also be noted that dependencies exist outside the regulated domain as well. The loss of data suppliers due to cyber attacks would also have significant damage potential. Decentralised forms of work and digital business models have increased the dependency on a smoothly functioning infrastructure. The use of cloud computing and new technologies entails further vulnerability to cyber attacks.

Beat Waefler, Chief Supervisor and Head of Supervision Section in the Insurance and Pension Funds Division

QUALITY ASSURANCE FOR AUDITORS

The FMA has been responsible for the supervision of auditors since the amendment of the Auditors and Auditing Companies Act (WPRG) in 2011 transposing the EU Statutory Audit Directive. Since the initial implementation of the supervisory system, super-visory activities have been continuously further developed. For example, a cross-divisional interface was created, quality assurance reviews were introduced, and the follow-up enactments of the European Commission were implemented.

With the entry into force of the Auditors Act (WPG), which replaced the WPRG, the legal basis was comprehensively revised in 2021, and at the same time Directive 2014/56/EU of the European Parliament and of the Council of 16 April 2014 amending Directive 2006/43/EC on statutory audits of annual accounts and consolidated accounts was transposed.

Prudential supervision of auditors and audit firms includes issuing and withdrawing licenses, monitoring continued compliance with licensing requirements, disciplinary authority, conducting due diligence inspections, and maintaining the register of auditors. In addition, the FMA is responsible for issuing confirmations, announcing the auditor’s examination (authorisation or suitability examination), and authorising auditors. An important part of the supervision of auditors and audit firms is also the performance of quality assurance reviews.

The FMA supervises a total of 88 auditors and 36 audit firms. Of these, 38 auditors and 15 firms are financial service providers domiciled abroad engaged in the free movement of services. The quality assurance review comprises a firm review and a file review. As part of the firm review, the appropriateness of the quality management systems, the existence of ongoing training, the quantity of fees, and indepen-

dence are reviewed. The file review covers engagement-related quality assurance, the quantity and quality of resources, and compliance with auditing standards. In the current cycle (since 2019), 18 quality control reviews have already been carried out. An average of 4.5 findings were made. The findings include, for example, inadequate documentation of the quality assurance system, an unqualified audit opinion despite material and comprehensive misstatements in the financial statements, and the performance of an audit by an unlicensed firm. If findings were made, the FMA took appropriate measures. In the examples mentioned, a complete revision of the quality assurance manual and the quality assurance mechanisms was required, the recipient of the report was informed that the audit opinion issued could not be relied upon and, in the last case, a criminal complaint was filed.

The quality assurance reviews aim to ensure that auditors comply with the required standards. In this way, the reviews ultimately serve to protect clients and the reputation of Liechtenstein’s financial centre. With the introduction of the inspection system for auditors of public-interest entities (banks and insurance undertakings) and sustainability reporting audits, the supervision of auditors is currently undergoing a further significant expansion.

MACROPRUDENTIAL SUPERVISION

The financial crisis showed that – alongside the microprudential perspective, which focuses on the stability of individual institutions – macroprudential supervision is also necessary. Macroprudential supervision helps to protect the stability of the financial system as a whole, in particular by strengthening the resilience of the financial sector and reducing the accumulation of systemic risks.

Responsibility for macroprudential policy and supervision is divided among several actors in Liechtenstein.

Because Liechtenstein does not have its own central bank, the FMA assumes responsibility for the stability of the financial sector pursuant to Article 4 FMAG. Institutionally, this means the FMA plays the institutional role in the area of financial stability that central banks in other countries typically fulfil. To strengthen financial market stability and reduce systemic and procyclical risk, a Financial Stability Committee (FSC) was also established in 2019, composed of representatives of the Ministry of General Government Affairs and Finance and the FMA. By recommending macroprudential measures and issuing risk warnings, the FSC can initiate supervisory measures or amendments to ordinances or laws. The deliberations and discussions in the FSC are based on the financial stability analyses and expert opinions of the FMA.

In addition to the core tasks of macroprudential supervision, activities in the 2023 reporting year focused on two special topics in particular: Firstly, the measures to address the risks identified in the real estate and mortgage market were finalised in close cooperation with the banking sector, and secondly, Macroprudential Supervision was heavily involved in the preparatory work for Liechtenstein’s possible accession to the International Monetary Fund (IMF).

In recent years, the FMA has repeatedly drawn attention to the vulnerabilities arising from the high level of private household debt in Liechtenstein. Following a risk warning to this effect from the European macroprudential supervisory authority – the European Systemic Risk Board (ESRB) – regarding significant medium-term risks in the real estate market in Liechtenstein, a working group with representatives of the FMA and the Liechtenstein banking sector was established at the beginning of 2022 to develop proposals for solutions to address the identified risks. As a first step, the working group elaborated a common understanding of the risks in the Liechtenstein real estate and mortgage market in order to develop measures to address the risks in a targeted

manner. Based on this preliminary work, the FSC published a recommendation in July in three key areas, namely (1) to improve data availability, (2) to strengthen risk awareness, and (3) to adjust the existing borrower-based measures in Liechtenstein.

BORROWER-BASED MEASURES

To ensure adequate risk monitoring when a loan is declared as an exception to policy (ETP), the adjusted measures call in particular for the application of uniform market-wide standards not only in terms of the loan-to-value ratio, but also in terms of affordability. At the same time, the provisions do not stipulate a maximum limit on the number of such exceptional loans that can be granted, so as to allow banks appropriate flexibility in their risk management when granting loans.

Macroprudential Supervision was also closely involved in the preparatory work in the reporting year for Liechtenstein’s possible accession to the IMF. In this context, an initial balance of payments for Liechtenstein was estimated under the leadership of the FMA and in close cooperation with the SNB and the Office of Statistics. Providing this data was a prerequisite for Liechtenstein to submit its official application for membership to the IMF at the end of May 2023. The preparatory work continued intensively in the second half of the year with the visit of a high-ranking IMF delegation in July, the official membership mission in November and December, and numerous consultations with the various specialist departments of the IMF, the SNB, and the various offices of the National Administration. The accession negotiations are now so far advanced that the Liechtenstein Parliament is expected to be able to discuss and decide on accession before the summer of 2024.

As part of the core tasks of macroprudential supervision, the FMA and the FSC also dealt with the

TO CONTENTS BEGINNING OF THE CHAPTER

turbulence in the US and Swiss banking sector and the associated implications for Liechtenstein, with a recalibration of the various macroprudential capital buffers, and with the implementation of existing and new ESRB recommendations. The annual Financial Stability Report, which illuminates systemic risks in the entire Liechtenstein financial sector and was presented to the public at the Financial Stability Forum in November, also makes an important contribution to financial market stability. In addition, the quarterly National Economic Monitor on international economic and financial market developments also draws attention to the development of systemic risks in the Liechtenstein financial sector. Alongside the publication of risk warnings and recommendations, this contributes to strengthening the risk awareness of market participants.

Martin Gaechter, Head of Financial Stability Division

LICENSES, APPROVALS, REGISTRATIONS

In Liechtenstein, the provision of financial services subject to authorisation requires a licence issued by the FMA. The rules governing entry to the Liechtenstein financial market should be understood primarily in terms of client protection. The goal is to ensure the high quality of market participants and the seriousness of transactions. The licence is both a mark of quality and a preventive control instrument of the Financial Market Authority. The FMA not only issues licenses, however, but also monitors ongoing compliance with the licensing requirements. In the event of changes to a licensed financial intermediary, the financial intermediary is required to notify the FMA immediately.

Changes subject to notification and approval include, for example, changes to the general management or the board of directors, changes to qualifying holdings, or a change of auditor. If licensing conditions are not met on a permanent basis, the FMA will withdraw licences where necessary.

In the reporting year, the number of banks in Liechtenstein decreased again by one due to the liquidation of one institution. As of the end of 2023, 11 banks were licensed in Liechtenstein. The number of authorised insurance companies remained constant, with one company entering and one exiting the market. There were also market entries and exits in the asset management sector, while the total number of licensed asset management companies remained constant. One new electronic money institution was licensed in May 2023, bringing the total number to three. A decline can be observed due to consolidation in the fiduciary sector. Contrary to the long-term trend, the Liechtenstein fund centre did not record any major growth.

Approval of securities prospectuses

The FMA is responsible for reviewing and approving prospectuses and supplements for the public offer of securities or their approval for trading on a regulated market. Securities prospectuses are reviewed by the FMA for completeness, coherence, and comprehensibility. Securities prospectuses are intended to eliminate information asymmetries between investors and issuers. The number of approved prospectuses in the reporting year was 22.

Registrations under the TVTG

A consequence of the digital transformation of the financial sector is that the FMA’s licensing activity is increasingly focused on business models based on new financial technologies. The challenge for the FMA is to understand these often complex, very technology-heavy business models and to identify

risks. In order to prevent forum shopping – i.e. the exploitation of regulatory areas with differing structures – the practice of other supervisory authorities within Europe must also be taken into account. The Token and TT Service Provider Act (TVTG) creates legal certainty in this area. There was particular interest in registration as token issuers, as TT exchange service providers, and as token depositaries. At the end of 2023, registration applications from 13 companies for a total of 29 roles under the TVTG were being evaluated. The Regulatory Laboratory/Financial Innovation unit of the FMA is the contact point for questions regarding the obligation to register business models involving financial technologies. During the reporting year, it received a total of 101 enquiries from the market (previous year: 109). 21 of these were subordination enquiries. The examination of due diligence concepts to combat money laundering plays an important role in the registration of TT service providers. With the enactment of the TVTG, the FATF recommendations were implemented providing for due diligence supervision of such services. Due to the technological complexity of the business models, the examination of the due diligence concepts has proven to be time-consuming.

In 2023, 10 companies were registered for a total of 20 roles under the TVTG. During the same period, one company renounced its registration that had already been issued. As a result, 29 service providers were registered for 64 roles in the TT Service Provider Register at the end of 2023, providing services as TT exchange service providers (16), token depositaries (13), token issuers (10, including 6 own issuers), token generators (10), TT identity service providers (3), TT price service providers (2), TT key depositaries (3), and physical validators (1).

ONGOING SUPERVISION

Prudential supervision of the individual supervised financial intermediaries aims to ensure permanent compliance with the licensing conditions, including in particular the financial resources of market participants, and to identify risks at an early stage. Prudential supervision is governed by the relevant special laws, such as the Banking Act and the Insurance Supervision Act, and makes a significant contribution to client protection and to the stability of the financial market. In addition to prudential supervision, ongoing supervision also encompasses due diligence to combat money laundering as well as conduct of business supervision. The basic instruments of ongoing supervision include reporting, auditing, on-site inspections, and management meetings.

Based on the risk analysis, the FMA defines its supervisory priorities for the current audit period. In addition to cross-sectoral supervisory priorities, the FMA also sets targeted, sector-specific supervisory priorities, which are generally aligned with the supervisory programmes and strategic guidelines of the European Supervisory Authorities. In the reporting year, the FMA set the following cross-sectoral supervisory priorities:

– Monitoring of market developments, the interest rate environment, and inflation

– Monitoring of real estate and mortgage risks

– Money laundering prevention

– Establishment of sustainability-related supervisory review (ESG risks)

– ICT security

In addition, the European Supervisory Authorities are entitled to set strategic supervisory priorities of the European Union. These priorities must be taken into account by the national supervisory authorities, with the aim of supervisory convergence among the EEA Member States.

TO CONTENTS BEGINNING OF THE CHAPTER

With regard to market developments, the interest rate environment, and inflation, the focus was on the increased macrofinancial risks against the backdrop of high inflation and rising interest rates as well as the associated impact on the financial sector. This topic was addressed in the management meetings. In the case of banks, risks associated with interest rates, the quality of investments, and business continuity management were closely monitored. In the case of insurance undertakings, business models were increasingly monitored with regard to their sustainability in the current environment. This also included the formation of appropriate technical provisions due to rising inflation. At the same time, the development of coverage ratios at pension schemes was closely monitored.

With regard to real estate and mortgage risks, risk monitoring was expanded due to the high level of household debt. In addition, the identified risks were addressed in cooperation with the banking sector, and corresponding measures were adopted.

Money laundering prevention continued to be a key supervisory focus of the FMA in 2023. The FMA continued its rigorous risk-based supervision, taking up the recommendations of the MONEYVAL assessment. The focus was also on the control and monitoring mechanisms implemented to ensure compliance with international financial sanctions.

LEARN

MORE

The development of the FinTech sectors

SCAN ME

ESG risks were a key supervisory priority in 2023. Following improvement of the previous lack of clarity and transparency with the help of regulatory requirements in 2022, the focus in 2023 shifted to requirements from the Disclosure Regulation and the Taxonomy Regulation as well as the sectoral requirements regarding the consideration of sustainability risks and the requirements for accounting-related sustainability reporting.

With regard to ICT risks, in particular the implementation status of FMA Guideline 2021/3 on ICT security, which entered into effect in 2022, was determined at the intermediaries covered by the guideline. In 2023, the audit reports of the audit offices on the implementation of the guideline were available for the first time. The audit reports were used to gain an understanding of the existing risks and measures.

Investment firms that conduct transactions with financial instruments must report all transactions in detail to the competent authority. The aims include combating insider trading and market manipulation and strengthening investor protection. The transaction data received by the FMA is examined using various scenarios relating to insider trading and market manipulation. The stored parameters are adjusted on an ongoing basis according to market events and market behaviour. In addition to indications of market abuse, transaction monitoring can also identify risks that jeopardise the functioning of the markets. The FMA not only receives reports from investment firms domiciled in Liechtenstein, but is also connected to supervisory authorities throughout Europe via the system that has been established for that purpose.

Investment firms or other supervisory authorities submitted about 8.4 million (previous year: 9.5 million) transaction reports to the FMA in 2023, which amounts to more than 23,000 (26,000) reports daily. The volume of reported transactions amounted to approximately CHF 160 billion (189 billion). In general, the previous

BEGINNING OF THE CHAPTER

TO CONTENTS

year’s trading volume was not sustained in 2023. The months of February and March saw the highest trading activity, with March showing significantly less activity compared to the previous year.

The transmitted transactions were validated at the technical level, subjected to content-related data quality tests on an ongoing basis, and evaluated. If the scenarios give rise to suspicion that indicate misconduct on the part of market participants, the FMA carries out further clarifications or takes appropriate measures. In the reporting year, a total of 1,142 (1,268) hits were generated that were analysed and evaluated.

The sanctions imposed by the US Office of Foreign Assets Control (OFAC) were taken into account in the FMA’s supervisory activities. An OFAC sanction is potentially a major reputational risk for the Liechtenstein financial centre. Even if OFAC sanctions have no direct legal effect in Liechtenstein, as in all other European countries, they are highly relevant for the financial centre from a risk perspective.

Based on the risk analysis, the FMA defines its supervisory priorities for the current audit period.

On-site inspections

An on-site inspection is an institutionalised audit activity within the framework of ongoing supervision and enforcement on the premises of the financial intermediary. An on-site inspection is carried out by employees of the FMA. On-site inspections may be announced or unannounced. The FMA conducts a number of planned on-site inspections each year, as well as on an ad hoc basis where necessary. As a rule, on-site inspections are dedicated to one or more priority topics. In the reporting year, 30 on-site inspections were carried out.

Auditing

As part of prudential supervision, the FMA evaluates the audit reports submitted by auditors who, on behalf of the FMA, perform a risk-based audit of compliance with the regulatory requirements by the financial intermediaries. Where deficiencies arise, the FMA takes the necessary measures, or it sanctions the financial intermediary in accordance with the legal requirements. The audits are based on the FMA’s Audit Guideline. The Audit Guideline governs the procedure to be observed in the audits and reports of the external auditors authorised under the special laws, and it serves to ensure the high quality and uniform administration of supervisory audits. The uniform and detailed requirements governing audits make a significant contribution to the convergence of supervisory practice and implementation of risk-based supervision.

Reporting

Under the special laws, financial intermediaries are required to provide the FMA with the data necessary to evaluate the company and its risks. On the basis of the reports, the FMA verifies compliance with regulatory requirements and follows the business development of the supervised financial intermediaries

in a timely manner. “Reports“ refers to all legally required periodic or ad hoc information obligations of the financial intermediary vis-à-vis the FMA. This includes annual reports, semi-annual reports, quarterly reports, and other regular reports. Most reports under the reporting system are received via the FMA’s e-Service Portal. The portal was introduced in 2015 and provides a convenient way for notifying entities from all sectors to submit data online. In the reporting year, a total of 12,500 reports (previous year: 11,000) were submitted via the portal.

Management meetings

FMA representatives hold regular management meetings with members of the general management and board of directors of supervised entities. The business strategy and business development of the companies as well as current topics are discussed. A total of 45 management meetings were held in the reporting year, including five with banks, 12 with asset management companies, six in the fiduciary sector, and 17 with insurance undertakings. In addition to strategic orientation and business development, governance and organisational topics were discussed. ESG risks were also addressed. Client complaints and the implementation of complaints and recommendations were also discussed with asset management companies and management companies.

Table 4

On-site inspections. For inspection activities relating to due diligence supervision for the purpose of combating money laundering, see the chapter on due diligence supervision.

Table 5

Review of audit reports

This overview does not include audit reports for the purpose of preventing money laundering (see the chapter on due diligence supervision

TO CONTENTS BEGINNING OF THE CHAPTER

AD HOC SUPERVISION OF TT SERVICE PROVIDERS

The obligation to register under the Token and TT Service Provider Act (TVTG) sets minimum requirements for all TT service providers in Liechtenstein. These requirements are especially important from the perspective of user protection. TT service providers are not subject to the same regulatory requirements as classic financial service providers, however. The review conducted for the registration of a TT service provider is more limited in both scope and depth in comparison with the licensing of a financial service provider. TT service providers are also not subject to ongoing prudential supervision, but rather to ad hoc supervision. The level of protection of clients ensured by supervision accordingly differs from that of a licensed financial intermediary. To obtain a better overview of the market despite the lack of prudential supervision, the FMA collects general information on the business activities of registered FinTechs on an annual basis as part of periodic reporting.

The FMA continued to monitor market activity in 2023 and carried out in-depth clarifications in a large number of cases (also together with the supervisory divisions). This was particularly the case when the impression arose that services requiring registration were being offered without the requisite registration.

The FMA also took action in the case of other irregularities; in one case, for example, the FMA punished a breach of various reporting obligations by a registered TT service provider. In addition, the FMA published several warning notices in the FinTech sector and informed other authorities about relevant fact patterns.

Table 6

Reporting

This overview does not include reporting under the Due Diligence Act (SPG) for the purpose of combating money laundering, see the chapter on due diligence supervision

DUE DILIGENCE SUPERVISION TO COMBAT MONEY LAUNDERING

In the reporting year, the FMA once again rigorously pursued the change in strategy for due diligence supervision it initiated at the beginning of 2019. The riskbased supervisory approach was strengthened by continuing to focus the FMA’s inspections in particular on persons subject to due diligence and financial sectors with an increased risk profile. The risk profiles are established on the basis of information from the reporting system pursuant to the Due Diligence Act (SPG), as part of which financial market participants must report annually to the FMA on inherent money laundering risks and the quality of their risk mitigation. On a supplementary basis, the FMA continuously evaluates information it receives in the course of its supervisory activities (e.g. ongoing inspections, press or media articles, reporting by partner authorities in Liechtenstein and abroad, etc.).

In accordance with the risk-based supervisory approach, the content of the inspections also focused on the vulnerabilities identified in National Risk Assessment II. As a consequence of the change in strategy, the FMA has also significantly increased the number of its own on-site inspections, in order to obtain a direct and comprehensive picture of the quality of due diligence measures in addition to the findings derived from the mandated inspections (audits carried out by auditors).

Both the FMA’s own due diligence inspections and the mandated inspections were based on the supervisory priorities defined for 2023 in each sector. In the case of mandated due diligence inspections, the thematic SPG audits focused in particular on the four topics of risk-appropriate monitoring of business relationships and transactions, simple and special investigations, reports of suspicion, and the proper implementation of international financial sanctions. In the banking sector, the mandated due diligence inspections in 2023 once again focused in particular on high-risk transactions (such as transactions with a nexus to high-risk countries, pass-through and cash transactions, etc.).

The FMA’s own due diligence inspections additionally focused on the vulnerabilities identified in National Risk Assessment II and defined as priorities for action in the corresponding Government action plan. In this

context, special attention was paid to vulnerabilities such as product and service risks associated with transaction banking, service companies, sole signing authority, and cash and precious metal transactions.

Because of the special situation relating to the war in Ukraine since February 2022 and the resulting sanctions packages, the FMA continued to pay special attention in all of its own inspections on compliance with financial sanctions in accordance with the International Sanctions Act (ISG) and potential evasion of those sanctions.

During the reporting period, the FMA conducted its own on-site inspections at three banks. These were focused inspections with a risk-based emphasis. In addition to the organisational (firm) reviews in the priority areas, 32 random samples were drawn and examined. In several cases, deficiencies were identified in connection with the client risk assessment, the client business profiles, and inadequate transaction clarifications. Recommendations were also made during the on-site inspections in connection with the reports of the compliance and investigating officers as well as in the area of risk-appropriate monitoring of transactions.

The FMA carried out its own on-site inspections with risk-based priorities (focused inspections) at four life insurance undertakings and two life insurance intermediaries. A total of 40 random samples were drawn and examined last year, in addition to the firm review. Deficiencies were identified in particular with regard to client risk assessment, the informative value of business profiles (source of funds), and the audit procedures of the investigating officer.

The due diligence category “Trust and company service providers“ includes professional trustees and trust companies as well as persons under the 180a Act. The FMA carried out a total of 21 consolidated on-site inspections in the reporting period, three of

which were extraordinary on-site inspections. A total of 66 trust and company service providers (trust companies, professional trustees, and persons licensed under the 180a Act) were subject to a focused inspection in this context and, in addition to the firm review conducted in each case, a total of 144 random samples were drawn and examined.

The inspections showed that, in general, the quality of due diligence in the fiduciary sector is predominantly good, and only isolated or no findings were made in the majority of the inspections. Some significant exceptions in individual inspections concerned deficiencies with regard to the information in the business profile on the source of funds/source of wealth, compliance with reporting obligations in cases of suspected money laundering, and the review of client relationships with regard to possible violations of sanctions.

The FMA conducted a total of five focused inspections of asset management companies last year. 38 samples were drawn and examined. Apart from a few primarily formal weaknesses, only a few deficiencies were identified overall (in particular relating to business profiles, including verification of the origin of funds). In addition, the FMA conducted three of its own on-site inspections at management companies/ AIFMs authorised to carry out individual portfolio management.

In addition, 48 funds which are either self-managed or managed by six management companies and AIFMs were audited. It was ascertained that all of these funds were subject to a new risk assessment in accordance with the SPG. As a result of these reassessments, about half of the funds were no longer able to apply simplified due diligence pursuant to Article 22b(3) SPV. Overall, the FMA was able to satisfy itself that, with a few exceptions, the defence mechanism in the fund sector is robust.

BEGINNING OF THE CHAPTER

TO CONTENTS

Finally, the FMA also carried out three of its own on-site inspections of TT service providers during the reporting period. In addition to the risk-appropriate monitoring of business relationships, the focus was also on business profiles and the identification of beneficial owners. 32 random samples were drawn as part of these inspections. In two of the three inspections, significant deficiencies were identified in connection with the risk-appropriate monitoring of business relationships/transactions. In addition, isolated deficiencies were identified in the plausibility check of the source of funds and the risk assessment.

In addition to the FMA’s own inspections, focused inspections were mandated for three banks, 28 asset management companies, six life insurance companies, two life insurance intermediaries, 188 investment funds, one fund management company with individual portfolio management, and five TT service providers. In the fiduciary sector, 32 consolidated on-site inspections were commissioned.

In sum, the mandated inspections once again showed generally good results and robust defence mechanisms, with only a few inspections identifying an elevated number of deficiencies. Overall, the findings in each sector are consistent with the findings from the FMA’s own on-site inspections, as in the previous year.

Own / mandated inspections

inspections

inspections

Table 8

Due diligence inspections

* to ensure comparability, these figures were corrected and adjusted for life insurance agents and life insurance intermediaries without activities subject to due diligence (zero reporters) ** of which token issuers not subject to registration pursuant to Article 3(1)(s) SPG (7 in 2021; 15 in 2022; 11 in 2023) *** includes electronic money institutions, agents of EEA payment institutions, fund management companies with individual portfolio management, investment firms, casinos, and persons subject to due diligence pursuant to Article 3(3) SPG

INTERNATIONAL ADMINISTRATIVE ASSISTANCE

Supervisory authorities provide cross-border administrative assistance as needed. Administrative assistance is an important instrument in the cooperation between supervisory authorities. It supports the goals of financial market supervision to safeguard confidence in the financial markets, protect clients, and combat abuses. In 2023, a total of 70 requests for administrative assistance were submitted to the FMA asking for information. Conversely, the FMA submitted 94 requests to foreign supervisory authorities.

Non-client-related administrative assistance

Non-client-related information is information under supervisory law relating to the general activities of a supervised entity in its capacity as a market participant. In addition to information on solvency and liquidity, this includes in particular information on the governing bodies or ownership of a supervised entity as well as information on any supervisory or criminal proceedings against the supervised entity or its governing bodies or ownership. In 2023, 43 such non-client-related enquiries were addressed to the FMA by 27 supervisory authorities. Of these requests, 33 were good standing enquiries or requests for letters of confirmation. In the same period, the FMA submitted a total of 87 non-client-related requests for administrative assistance to 34 different foreign supervisory authorities.

Client-related administrative assistance

If the information to be transmitted concerns individual clients of financial institutions, this constitutes client-related administrative assistance, which is subject to strict formal requirements. The focus is on administrative assistance in the area of securities supervision on the basis of the multilateral memorandum of understanding with the International Organization of Securities Commissions

BEGINNING OF THE CHAPTER

TO CONTENTS

(IOSCO MMoU). The main topics here are violations of insider legislation, market manipulation, activities without a licence, and investment fraud. Outside of securities supervision, client-related administrative assistance takes place according to special laws such as the Banking Act. In 2023, the FMA was requested for client-related administrative assistance in 27 cases. Of these, 24 requests were made on the basis of the IOSCO MMoU, three on the basis of special laws.

The Market Abuse Regulation (MAR) and its Implementing Regulations have been in force in Liechtenstein since 2021. As a rule, administrative assistance in the area of securities supervision under the IOSCO MMoU falls within the scope of this regulation. MAR contains its own rules on the cooperation of supervisory authorities in the Member States and thus also on administrative assistance; these rules apply directly and compulsorily in Liechtenstein. If national rules contradict those of MAR, they must not

The inspections showed that, in general, the quality of due diligence in the fiduciary sector is predominantly good.

be applied. If, on the other hand, subject matters are covered by national rules that are not regulated by MAR, the national rules continue to apply. Liechtenstein provides a special procedure for administrative assistance in the area of securities supervision that goes beyond the scope of MAR or its Implementing Regulations. In particular, the procedure specifies the form in which the requested information must be obtained from the requested authority, that a ban on information must be imposed on persons concerned and third parties, and that the Administrative Court must approve administrative assistance before the requested information is transmitted.

ENFORCEMENT

The FMA clarifies any indications it finds of violations of general criminal law or of the laws assigned to the FMA for execution. If the FMA arrives at a justified suspicion as a result of these preliminary investigations, or if the circumstances indicate that the reputation of the Liechtenstein financial centre is jeopardised, it initiates administrative or administrative criminal

proceedings, establishes the facts of the case, and orders any necessary measures and fines.

As of the end of 2023, the FMA was conducting 16 administrative proceedings and 19 administrative criminal proceedings. Administrative proceedings are proceedings for the enforcement of financial market rules governed by public law. Administrative criminal proceedings are proceedings carried out by the FMA to sanction violations of (supplementary) criminal law provisions set out in financial market legislation. During the reporting year, 192 proceedings and preliminary investigations were completed. The subjects of the proceedings included capital adequacy requirements, violations in risk management, market manipulation, organisational requirements, head office requirements, accounting requirements, compliance with licensing conditions, and governance.

On 7 March, the FMA announced Sora Bank AG’s voluntary liquidation and the renunciation of its licence. To ensure client protection, the FMA took the measures necessary for the execution of the liquidation and the settlement of ongoing business

7 FINMA (Switzerland)

Total 27 requests for administrative assistance

5 AMF (France)

Figure 5

Client-related requests for administrative assistance by authority (IOSCO MMoU and special laws)

and issued the necessary instructions to the liquidators. The FMA also supervised the liquidators and the liquidation.

On 21 November, the FMA announced that it had withdrawn the licence granted on 18 November 2020 to XOLARIS Capital AG, Vaduz, as an alternative investment fund manager due to failure to meet the licensing requirements pursuant to Article 32 of the Alternative Investment Fund Managers Act (AIFMG). XOLARIS Capital AG, Vaduz, was thereupon no longer entitled to perform activities in connection with assets of collective investment undertakings (AIFs), including their sub-funds, or to manage them.

On 14 December, the FMA made public on its website that the banking services of Mason Privatbank Liechtenstein AG in Liquidation had been wound up since 30 October 2023 in accordance with Article 3 of the Banking Act (BankG). Accordingly, Mason Privatbank Liechtenstein AG in Liquidation no longer held any deposits or other repayable funds. Mason Privatbank Liechtenstein AG’s licence to operate a bank had lapsed on 15 March 2021 pursuant to renunciation in writing in accordance with Article 27(1)(c) of the

BEGINNING OF THE CHAPTER

TO CONTENTS

Reserve Bank of India (India) 1

BaFin (Germany) 1

SEC (USA) 1

ASC (Canada) 1

FMA (New Zealand) 1

DFSA (Denmark) 1

FCA (UK) 1

FMA (Austria) 2

CFTC (USA) 2

MNB (Hungary) 2

SECRS (Serbia) 2

Banking Act. The FMA had supervised the liquidators and the liquidation.

At the end of June, the FMA published its FMA Practice. The publication provides information in anonymised form on the FMA’s decisions and decrees as well as on decisions of the FMA Complaints Commission (FMA-CC) that concern the 2022 supervisory period. By describing selected cases, the FMA sets out each year how it applies and interprets supervisory law, thus creating transparency and predictability for financial intermediaries and setting out its expectations.

During the 2022 supervisory period, several decisions of particular relevance for the FMA’s further supervisory practice were taken. In one case, the FMA no longer considered a professional trustee to be trustworthy due to a criminal conviction abroad and withdrew his licence. The professional trustee was convicted of the crime of breach of trust in Austria and punished with a suspended prison sentence. The Administrative Court confirmed the withdrawal of the licence. For the Administrative Court, there is no doubt that a person subject to the supervision of the FMA

endangers and damages trust in the Liechtenstein financial centre if they have been convicted of a financial crime and sentenced to a high penalty and if, moreover, the act was also committed in the course of professional activities.

The same person was also active as a management body in several Liechtenstein insurance undertakings. The FMA determined that the person no longer had personal integrity and was therefore not suitable to perform the management functions. The person lodged an appeal against the administrative order, citing in part his largely good conduct since the completion of the offence a long time ago. The FMA Complaints Commission, the Administrative Court, and the Constitutional Court upheld the FMA’s decision. This is of particular relevance, given that it is the first time a decision has been made on the mere question of personal integrity as a permanent requirement for members of management bodies. The case also shows that it does not matter how long ago the incriminated conduct took place.

In another case, the FMA imposed a fine of CHF 400,000 on a legal person for a serious and repeated breach of due diligence obligations. The person subject to due diligence fully confessed to the administrative contraventions committed during a subordination procedure, acknowledged the fine imposed, and waived the right to appeal. In a separate administrative order, the FMA determined the total costs of the extraordinary inspection by an auditor and obliged the person subject to due diligence to pay those costs. Individual items claimed by the auditor had to be corrected or reduced after examination by the FMA. This shows that the FMA always strives to keep the costs caused by extraordinary on-site inspections as low as possible.

In 2023, the FMA imposed 16 legally enforceable fines amounting to CHF 1,498,500.

On 21 December 2023, the FMA imposed a fine of CHF 500,000 on a legal person for a serious breach of the provisions on risk management under the Banking Act and repeated breaches of due diligence obligations under the Due Diligence Act.

The FMA imposed a fine of CHF 120,000 on a legal person for repeated breaches of due diligence obligations (business profile). The FMA also imposed a fine of CHF 120,000 on a legal person for breaching the provisions on risk management.

Most of the fines were imposed for breaches of the provisions of the Due Diligence Act. Other fines related to the failure to report a change in the composition of the management body, the violation of reporting obligations under the Due Diligence Act and the Token and TT Service Provider Act, and the violation of information obligations under the UCITS Act. The penalties are published on the FMA website in anonymised or named form. The fines levied by the FMA are transferred to the National Treasury.

In 2023, the FMA filed nine criminal complaints with the Office of the Public Prosecutor. If the FMA becomes aware of a suspicion of a criminal act to be prosecuted ex officio that affects its legal sphere of action, it is required to file a criminal complaint. The criminal complaints filed included suspicion of market abuse, suspicion of accepting deposits without the required licence, suspicion of insider trading and unlawful disclosure of insider information, concealment of material facts, suspicion of fraud in connection with a clone firm, suspected violation of designation protection, and performance of activities without registration (TVTG). In a further 95 cases, the FMA filed charges against employers for neglecting their legal obligations, such as the payment of contributions or the obligation to join an occupational pension scheme.

During the reporting period, the FMA submitted 14 reports to the Financial Intelligence Unit (FIU). This occurs in cases of suspicion of money laundering, a predicate offence of money laundering, organised crime, or terrorist financing.

For the reporting year, the FMA received a total of 23 whistleblowing reports via the whistleblower section of the FMA’s website or by post. The reports contained information on potential violations of the law, such as a missing licence, information on violations relating to governance (compliance), lack of integrity on the part of managers, allegations of fraud, or tax offences. Of the reports received, six were forwarded to other domestic authorities, given the responsibilities concerned. In six cases, it was decided after reviewing the reports that the information did not provide sufficient grounds for suspicion to initiate further measures or that no violations of the law could be identified. Those reports for which the FMA was responsible were reviewed as part of its supervisory activities and, where necessary, appropriate measures were taken, e.g. warning notices were published as necessary, other official arrangements were made, or criminal charges were filed. Administrative proceedings and administrative criminal proceedings were also initiated.

The FMA published 14 warnings on its website in 2023. The FMA warned against ten clone firms and strongly advised against investing via their websites. Clone firms wrongfully claim the identity of a real company and attempt to induce users to invest via their websites or by sending emails. In four cases, companies also falsely gave the impression on their websites that they had a licence from the FMA. In each case, the FMA advised against making investments, responding to offers from the company, or transferring funds.

In May, the FMA also published an investor notice on investments in physical precious metals. The FMA had noticed an increase in enquiries about companies

BEGINNING OF THE CHAPTER

TO CONTENTS

SUPERVISION AND ENFORCEMENT OF LAWS

As of the end of 2023, the FMA is responsible for supervising and enforcing 42 laws (Article 5(1) of the FMA Act), including the associated implementing ordinances and European Level 2 measures. Laws newly included in 2023: – European Covered Bonds Act (EuGSVG).

domiciled in Liechtenstein that had developed various models for trading in and storing physical gold and other precious metals. These companies sold these precious metals via the internet or through distribution structures, especially in other German-speaking countries, and then stored them in Swiss or Liechtenstein storage companies. The FMA stated that the sale, together with the subsequent safekeeping of the physical precious metals and the reporting of the holdings to investors, does not in principle constitute an activity requiring a licence under special laws and therefore does not require a licence from the FMA. The FMA recommended that investors carefully examine the ancillary costs associated with such offers (contract and administration costs) and compare them with conventional offers.

TO CONTENTS BEGINNING OF THE CHAPTER

FINTECH

MORE THAN JUST NEW BUSINESS MODELS

Technological innovations in financial services (FinTech) are increasingly changing the way financial services are offered and demanded. While FinTech opens up opportunities, it also harbours potential risks. The FMA’s approach is to use and shape regulation in such a way that established financial service providers and new companies can implement their business models. As a supervisory authority, however, it of course also considers the risks of technology-based business models and ensures that client protection is guaranteed, trust in the financial market is maintained, and the stability of the financial system is not jeopardised. Technological change must be viewed holistically in this regard. FinTech not only consists of the activities of FinTech companies, but also depends on relevant technologies and an appropriate infrastructure and environment. The FinTech tree provides an overview.

ENABLERS

Figure 6

FinTech tree, Source: BIS-FSI

ACTIVITIES OF THE RESOLUTION AUTHORITY

In its function as the national resolution authority, the responsibilities of the FMA include ensuring the resolvability of banks domiciled in Liechtenstein and, if necessary, setting resolution measures. In doing so, it makes an important contribution to safeguarding financial market stability.

The legal basis for the FMA’s work as a resolution authority is the Law of 4 November 2016 on the Recovery and Resolution of Banks and Investment Firms (Recovery and Resolution Act; SAG). The SAG is the Liechtenstein transposition of the EU Bank Recovery and Resolution Directive (BRRD).

A key element of an effective resolution regime is the targeted preparation of banks for default scenarios. For this purpose, formal resolution plans are developed in cooperation with the undertakings. These plans contain not only analyses of the importance of the banks for the Liechtenstein financial centre, but also include specific crisis management strategies and resolution approaches. For large banks, this includes, for example, the implementation of debtequity swaps (“bail-in“; direct participation of creditors in the losses or capital cut) and merger & acquisition transactions, such as the sale of the shares of the crisis bank to interested buyers (“share deal“), the transfer of portfolios, or the establishment of a “bad bank“.

Resolution planning also includes an assessment of the resolvability of the company concerned and includes the identification and removal of potential impediments to resolution. To enhance the efficiency of the resolvability assessment, the FMA issued a guideline on the review of resolvability by auditors in 2023 (FMA Guideline 2023/2).

BEGINNING OF THE CHAPTER

TO CONTENTS