Photo: London Stock Exchange closing ceremony, 2nd December 2025

OPENING HOURS

Monday–Friday, 08:00–17:00

GIVE FEEDBACK publications@redmayne.co.uk HEAD OFFICE 0113 243 6941

RISK WARNING

Investments and income arising from them can fall as well as rise in value. Past performance and forecasts are not reliable indicators of future results and performance. There is an extra risk of losing money when shares are bought in some smaller companies. Redmayne Bentley has taken steps to ensure the accuracy of the information provided.

IN THIS 150TH ANNIVERSARY EDITION:

Please note that this communication is for information only and does not constitute a recommendation to buy or sell the shares of the investments mentioned.

TOPIC OF THE MONTH

FAMILY, MARKETS AND INVESTOR

OUTCOMES

THOMAS HYDE | JUNIOR INVESTMENT RESEARCH ANALYST

Family-controlled listed companies are often assumed to be relics of the past when dynasties such as the Rockefellers or Vanderbilts dominated their respective industries. In reality, a significant number of the world’s largest public companies remain meaningfully influenced or controlled by founding families. Whether that’s through concentrated shareholdings or voting rights long after their Initial Public O ering (IPO). A listing has the benefit of raising capital for expansion and providing liquidity for an exit, as founders reduce exposure to

highly concentrated personal risk. Ceding shareholding, however, does not necessarily mean ceding control. Many IPO structures are designed to preserve family influence through voting rights. Depending on the context, this can provide strategic direction to pursue long-term capital growth and resist short-term market pressure. Equally, it can increase the risk of confl ict with minority shareholders. In this article, we examine familycontrolled public companies and how they can enhance, or undermine, long-term shareholder outcomes.

In aggregate, family-owned public companies have outperformed their non-family peers. To assess their performance, Credit Suisse previously produced the Family 1000 Index, a benchmark tracking global listed companies where a family holds at least a 20% ownership stake, which is no longer maintained. Studies have shown that these companies have outperformed their local market indices since 2006, with their defensive nature allowing them to perform well during periods of market volatility. A key factor is having a vested interest. These families often have a large portion of their personal wealth invested in their business, which can incentivise better stewardship and decision-making. It follows that poor outcomes would negatively affect the owner fi nancially, so a greater effort is put into running the business. This approach is reflected in superior fundamentals compared to non-family peers. Family-controlled companies record higher margins and pursue greater reinvestment rather than buybacks, which would increase concentration risk and potentially dilute control. Furthermore, they are less indebted and less likely to engage in ‘empire building.’

By adopting a long-term perspective, family-controlled companies can avoid an excessive focus on short-term market performance. Public markets tend to reward nearterm earnings as quarterly or semi-annual reporting exerts pressure on management. Professional managers cannot typically resist negative market sentiment for extended periods before facing being replaced. Families that retain control over the business via board appointments and capital allocation decisions may overcome short-term market pressure and pursue investments with longer payback periods. Even when those investments hurt near-term reported earnings. When done well, this patience is rewarded with a dominant market position.

Walmart illustrates how effective family control, with professional management, can support long-term performance. The world’s largest retailer by revenue is majority-owned by the Walton family, yet no family member is involved in day-to-day operations. This separation between ownership and management ensures leadership is meritocratic rather than inherited which reduces the risk of nepotism while preserving long-term oversight. Despite this separation, the Waltons remain selective in management appointments, favouring senior operators who are long-time employees, aligned with Walmart’s operating model. The business has a history of tolerating lower margins in the pursuit of scale and reinvestment. Despite being publicly listed, it is reasonable to argue that without stable family control, Walmart’s operating model would have struggled to survive the market’s relatively short performance horizon. However, a long-term operating model is not indicative of future performance as companies that focus on near-term execution can deliver equally strong shareholder returns. Ownership structure influences behaviour, not investment merit.

Yet, the very concentration of control inherent in family ownership can become a weakness when incentives diverge. Investing alongside a controlling family is often assumed to imply a shared desire for value creation over time, but this

is not always the case. Families may prioritise non-fi nancial objectives such as legacy or managing succession, even where this confl icts with the interests of minority shareholders, who have limited ability to influence outcomes. This influence is frequently reinforced through dual class share structures. At an IPO, companies may issue founder and public shares which offer the same economic rights but unequal voting power, enabling families to retain control over key decisions. For example, the Ford family owns only 2% of the company’s equity but retains 40% of the voting power. While this can maintain strategic direction, it can also weaken governance by enabling the appointment of under-qualified family members, entrenching management, or blocking potential takeovers that would benefit wider shareholders. As a consequence, familycontrolled companies may trade at a ‘minority discount’ to the broader market, reflecting minority shareholders’ inability to influence strategy or affect governance change.

In spite of family-ownership, JCDecaux, is an example of why ownership structure alone does not guarantee superior performance. The Decaux family own over 65% of the physical advertising agency, which in theory should allow for strategic continuity and an alignment of incentives to promote long-term stewardship. However, the share price has fallen nearly 40% over the last 10 years versus an almost 200% gain of the French CAC 40 index. Family control has been stable for years and governance has not been challenged by activist investors, suggesting that execution has not succumbed to short-term pressures. Instead, the underperformance reflects a structural decline in the physical advertising industry. Companies are spending more on digital platforms, supported by customer analytics which makes advertising more effective. As this example shows, family ownership can support stability and discipline, but it does not protect a business from shifts in consumer preferences or competitive pressures.

Overall, no family-controlled company is the same. Many display superior economic performance, reflecting the benefits of long-term stewardship. Families with a vested interest are incentivised to manage the business responsibly, enabling investment that may be unattractive in the shortterm but ultimately beneficial. At the same time, concentrated control carries risk. Families may prioritise non-fi nancial objectives such as legacy preservation or succession planning. Investors should therefore view family ownership as a double-edged sword. A family’s long-term perspective does not guarantee a good investment, rather its value depends on whether it aligns with the interests of investors.

Please note that this communication is for information only and does not constitute a recommendation to buy or sell the shares of the investments mentioned. Investments and income arising from them can fall as well as rise in value. Past performance and forecasts are not reliable indicators of future results and performance. The information and views were correct at time of publishing but may have changed at point of reading.

150 YEARS OF TRUSTED GUIDANCE: A PERSONAL REFLECTION

JAMES S. ANDREWS PARTNER & DIRECTOR OF INVESTMENT MANAGEMENT

As we celebrate our 150th anniversary, I am humbled by the privilege of helping our clients achieve their goals. For a century and a half, ever since our founding in 1875, our mission has been simple: to serve individuals by guiding them in the world of investing. This enduring purpose, to put clients fi rst and support their ambitions, has remained the heart of our fi rm’s identity.

It’s easy in modern fi nance to lose sight of the market’s simple purpose. At its core, the market exists to provide capital to companies so they can grow and, in turn, share their success with those who invest. That fundamental cycle, investors funding enterprises, and enterprises rewarding investors, is the bedrock of economic progress. Remembering this basic truth keeps us grounded. It reminds us that every portfolio we manage is not just a collection of numbers but a partnership in growth, linking our clients’ futures with the progress of businesses around the world.

In this light, we see ourselves as custodians of our clients’ capital. Our role is to allocate our clients resources to enterprises we believe truly deserve it, companies with sound values and promising futures. By doing so, we aim to enhance our clients’ wealth responsibly and sustainably. Every decision is made with a long-term perspective, honouring the confidence that generations of clients have placed in us. Reaching 150 years is a remarkable milestone. Our longevity, I believe, stands as testament to something deeper than market cycles or investment strategies: it reflects consistent excellence in service and steadfast trust. Through decades of change, we have remained committed to putting our clients’ objectives at the forefront, always striving to deliver results aligned with their long-term interests.

On a personal note, since joining the fi rm in 2016, I’ve witnessed an era of significant evolution, both within our company and across our industry. Many of our competitors have merged or been absorbed by big banks, often trading a personal touch for scale. Meanwhile, we have chosen a different path. We continue to refi ne and expand our offerings

without ever losing focus on what makes us unique: a truly bespoke, exceptional service for each and every client. In an age of consolidation, we’re proudly independent, believing that tailor-made solutions and one-on-one relationships are the keys to real value.

Looking ahead, I feel proud and excited. This commemorative edition is not just about reflecting on the past; it’s about recommitting to the principles that got us here. The trust you place in us, the goals you share with us, and the successes we build together are the real story of our 150 years. Thank you for allowing us to be part of your journey. Here’s to the next chapter of prosperity we will create, side by side.

James S. Andrews (centre) is pictured with Stuart Davis, Chief Executive, at a market close ceremony at London Stock Exchange to mark our 150th anniversary.

REDMAYNE BENTLEY CELEBRATES 150 TH ANNIVERSARY AT THE LONDON STOCK EXCHANGE

STUART DAVIS | CHIEF EXECUTIVE

We are incredibly proud to be celebrating 150 years in this industry. It’s a profession that we are privileged to be part of.

I was honoured to close the markets at the London Stock Exchange (LSE) to celebrate our 150th anniversary. Members of our Main and Executive Boards, colleagues from across the UK with representation from all business areas, and a number of guests were also invited to mark the milestone.

We were welcomed by Lindsay Hardcastle, Head of Memberships at LSE, on 2nd December 2025 for the ceremony which signals the end of the day’s trading. It was an occasion that will live long in our memories.

The ceremony took place almost exactly 150 years to the day that Redmayne Bentley was founded on 5th December 1875. It felt fitting to celebrate this significant milestone at the London Stock Exchange, a place that is at the heart of investment and innovation.

There’s been many changes over the thirty-four or so years that I have been at the fi rm, in terms of regulation, in terms of technology. However, one thing has remained the same and that’s our dedication to our clients and ensuring we offer them the personal service we believe they deserve.

Dame Julia Hoggett, CEO of the London Stock Exchange plc, recognised our achievement in a statement saying: “We are delighted to have welcomed Redmayne Bentley to the London Stock Exchange to close our markets in celebration of their 150th anniversary.

“Our member fi rms are integral to the success of the UK capital markets and are deeply valued across the Exchange. It is wonderful to be a part of their journey and celebrate this significant milestone with the team at Redmayne Bentley,” she added.

I’m really proud of the journey we’ve been on for the last 150 years. We’ve supported clients in good times and bad, whether it’s helping them navigate significant world events like the Wall Street crash or the bursting of the dot-com bubble, or helping them plan for their and their families futures.

The strong values John Redmayne held in 1875 - integrity and personal service to clients - remain at the centre of our identity today. We are proud of our journey, but also looking ahead to an exciting future as we build the foundations for the next 150 years and the fi rm’s continued growth and development.

We are grateful to the London Stock Exchange for this honour and all those who have been part of our story, from clients to colleagues, your support really does mean a lot to us.

Q&A: DAVID LOUDON

Redmayne Bentley’s history has been somewhat of a family a air, with members of the Loudon family involved in its running for more than a century. Here, David Loudon, now a non-executive director, shares memories of his time with the business and reflects on the 150th anniversary and the changes he’s seen in the sector.

1: Can you tell us a bit about your and your family’s history at Redmayne Bentley?

My grandad, Gavin Loudon, joined John Redmayne & Co as the office boy just after the First World War. He stayed with the fi rm for the rest of his career until his eventual retirement in the mid-1980s. He was a partner for many years and drove the formation of Redmayne Bentley through the merger with two other Leeds stockbrokers (FW Bentley and J Grainger) in 1965, at a time when The London Stock Exchange was trying to improve the resilience of member fi rms by increasing their size and resources. I did holiday work during his time as Senior Partner. There were about a dozen members of staff then, most of whom worked in the general office, where I was. I noticed a catering sized can of Nescafé by the kettle from which we were all allowed a cup of coffee mid-morning. I enjoyed that, and one day when my grandad was out of the office, I fancied a second cup so offered to make one for everyone else. There were 100% acceptances and I only found out later that there was a strict ‘one coffee a day’ policy!

My dad, Keith Loudon, qualified as a chartered accountant but joined Redmayne Bentley and became a stockbroker in the late 1950s. As well as being responsible for building the fi rm in its current form, he was also prominent in Leeds City Council and was Lord Mayor of Leeds in 1993. I grew up with my dad and grandad working in the fi rm and remember helping my dad sort statements when he brought them home in evenings and at weekends. After school, I left Leeds for university in Manchester and after that worked in London for several years. Later, I did an MBA and later returned to Leeds and joined Redmayne Bentley in 1993. At that time, our office was in Albion Street, and the Partners were my dad, Allan Collins and Bob Howe. There were about 30 staff in total and eight offices. There were only three departments - Dealing, Settlement and Investments - no compliance, marketing, HR, etc. I started off in Dealing but gradually got involved in all those ‘new’ areas and became a Partner in 1995.

We saw great growth in the number of trades, colleagues and offices in the following years as the stock market boomed and slumped through the dot-com boom, the demutualisation of building societies etc and the Financial Crisis of 2008 and more recent times. Regulation, of course, was perhaps the biggest growth area alongside the gradual move of clients from execution-only to managed and discretionary services and wider fi nancial planning.

2: What does the 150th anniversary mean to you personally?

With my father and grandfather’s roles as context, I’m very proud of how the fi rm has grown and endured over such a long period. I was fi rst involved, although very much as a side story, over 50 years ago with my grandad involved for 50 years before that, and with my dad providing a massive and instrumental bridge between us as the industry started serious growth, formalisation and maturing. Change in the last few decades has been relentless and very few organisations have been able to survive, let alone prosper.

Critical to our success has always been our colleagues and our focus on our clients. My grandad may have been strict in his ‘one coffee a day’ rule, but it was still free to staff, and that in itself reflected his progressive ideas which still underpin the way we try and work with and support all our colleagues to this day.

3: If you could go back and witness one pivotal moment in fi nancial history, what would it be and why?

The 1986 ‘Big Bang’ deregulation of the London Stock Exchange (LSE) was just a few years before I was involved properly in the business - although a handful of our current colleagues were just starting out at that time.

I’d have liked to have seen that fi rst-hand because it fundamentally transformed the UK’s fi nancial markets, moving the City of London toward its current position as a leading international fi nancial centre. It led to the introduction of several major changes:

• Electronic Trading: Traditional face-to-face trading was replaced by screen-based, computerised trading,

Keith Loudon

significantly increasing speed and efficiency. Truly electronic dealing for retail brokers like us didn’t come for several more years, but it did mean we no longer needed a ‘London Agent’ to make our trades on the LSE trading floor and could deal directly with jobbers/market makers by phone.

David Loudon has held a number of positions at Redmayne Bentley including Joint-CEO and Chair of the Main Board. He was also a board member of the Personal Investment Management and Financial Advice Association (PIMFA) for 10 years. He has also been a media commentator, including for the BBC TV and radio and CNBC and was formerly a Trustee of Leeds Cares, now known as Leeds Hospitals Charity.

• Negotiated Commissions: Fixed minimum brokerage commissions were abolished in favour of negotiated rates, which drastically increased competition and lowered transaction costs for investors. We started being able to offer reduced commissions to clients who traded often and/ or in high values. Most clients were unaffected, although the privatisations (British Gas, BT, British Airways, water and electric companies) soon came along where we offered reduced commissions and attracted new clients from all over the country. Many of these stayed with us for years, opening Personal Equity Plans (the forerunner to ISAs).

• Increased Activity: The changes resulted in a massive increase in trading volume and market capitalisation. The biggest change for our sector of the market was that owning shares suddenly became something ‘ordinary’ people did - encouraged by the privatisations brought in by the Thatcher government.

• Growth of Investment Banking: Old, traditional fi rms were largely absorbed by large, integrated investment banks, which led to the modern structure of the City’s fi nancial sector and the rise of the bonus culture. A biproduct of this led to the growth of our branch network. Small stockbrokers with personal relationships with loyal clients were swallowed up by big institutions. We never ‘sold out’ in this way but others who did, soon found their new bosses didn’t understand their businesses and found it increasingly hard to help their clients. They started to look

for a fi rm they could work with who did understand the business and would give them the freedom to manage their clients in ways they always had. Regulation was beginning to change, but we had a good reputation for controlling our business in tune with the traditional stock exchange culture of “my word is my bond”. We started with new offices in areas including London, Glasgow, Henley and Harrogate.

4: Which historical events - such as market crashes, regulatory changes, technology, or other innovationsdo you think have had the most profound impact on our industry?

Several are already mentioned. It’s easy to focus on the booms, but we can probably learn more from the crashes and their aftermaths. These are often painful and even traumatic and they’re particularly important to keep in the back of your mind during the good days. But also remember, that markets can often recover quickly from the downs.

5: What piece of advice would you give to the next generation of investors?

Modern investment management is much more disciplined than it ever used to be. This helps protect fi rms, markets and individuals from some of the worst possible outcomes. Individuals need to remember that long-term performance is the most important and to keep their long-term goals under review without getting obsessed with the short-term view.

6: Finally, what’s a tradition that has stood the test of time at Redmayne Bentley?

The motto of the Stock Exchange was always “My word is my bond.” At its simplest this harked back to physical trading on the old Stock Exchange ‘floor’ when commitments were made to buy and sell shares on the shake of a hand and were paid for hours or weeks later when the prevailing price may have moved substantially. The integrity of any market depends on all parties following through on the commitments they make, even if prices move against them. This type of integrity is important in all parts of life. If we say we will do something,

Gavin Loudon, who joined John Redmayne & Co as the offi ce boy just after the First World War.

Stuart Davis, Chief Executive, Redmayne Bentley, closes the day’s trading at the London Stock Exchange. Pictured (L-R): Philip Carpenter, Neil Talbot, Stuart Davis, Glen Cummins, Lindsay Hardcastle, James S. Andrews. Tuesday 2nd December 2025.

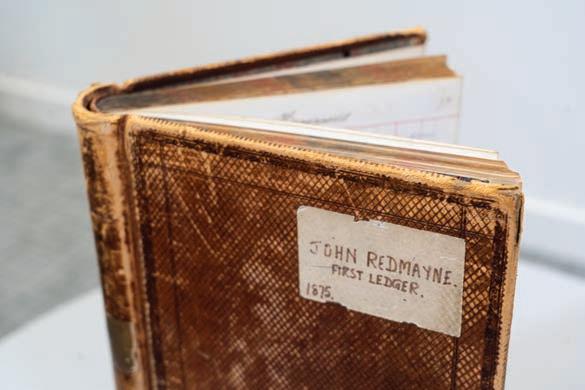

John Redmayne’s purchase ledger, used to record trades, circa 1875.

The London Stock Exchange.

Members of the Redmayne Bentley team at the London Stock Exchange. Tuesday 2nd December 2025.

Redmayne Bentley’s Marta Mamon setting up at a Leeds Heritage Open Days event.

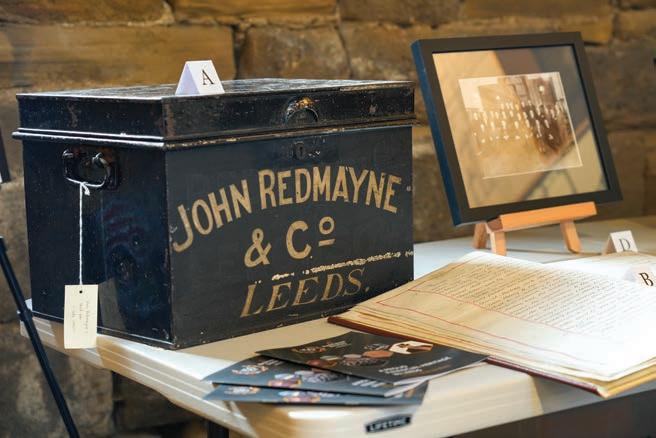

John Redmayne’s deed box.

Historian Cliff ord Stead, with a daily share list from the Leeds Stock Exchange, circa 1845.

Redmayne Bentley colleagues at the London Stock Exchange closing ceremony. Tuesday 2nd December 2025.

Redmayne Bentley’s mini exhibition, showcased at Bowcliffe Hall, West Yorkshire.

THE EVOLUTION OF UK EQUITIES

ANDREW RHODES | MARKETING EXECUTIVE

As part of our 150th anniversary souvenir edition of 1875, we revisit a topic featured in November’s edition of its sister publication, Market Insight .

In our fi rst publications video, Alastair Power, Investment Research Manager, explores the UK equity market, with a particular focus on the FTSE All-Share index. The video offers insight and analysis of the index and how it has developed in the past 63 years.

Created in 1962, the FTSE All-Share index started at a base level of 100 points and the index today stands at more than 5,000 points. During the late 1980s and early 1990s, events such as the ‘Big Bang’ and the Conservative government’s privatisation campaign paved the way for the rise of the retail investor. British Telecom (BT) was the fi rst major public sector flotation in November 1984, and the issue was greatly oversubscribed. Around 2.1m members of the public were allocated to nearly two-fi fths of the shares to ensure wider ownership, while British fi nancial institutions bought almost one half.

Other fi rms soon followed BT in listing and, by 1990, 42 major businesses employing nearly 900,000 people had been sold off. This was followed by coal, rail and energy fi rms in the mid-tolate 1990s.

By the late 1990s, the market had shifted and after the dot-com bubble had burst at the turn of the century, the FTSE AllShare’s heavy weighting toward fi nancials made it vulnerable during the Great Recession of the mid-2000s. After years of

loose monetary policy and banking regulation, the US housing bubble burst as many borrowers defaulted on their mortgage payments.

The resulting liquidity crisis saw major fi nancial institutions, including the US bank Lehman Brothers and the UK’s Northern Rock, collapse. The FTSE All-Share fell more than 48% between October 2008 and March 2009, but the event led to an overhaul of fi nancial regulation in the UK. While regulation improved fi nancial stability, it also contributed to a more cautious, compliance-driven investment environment, potentially dampening innovation and risk-taking in listed fi rms.

Driven by technological advances, privatisation campaigns, changing dynamics of retail and institutional investors, and more, the FTSE All-Share is today home to around 550 of the total companies traded on the London Stock Exchange.

Other events such as the Global Oil Crisis, Black Monday, the Eurozone debt crisis and, more recently, COVID-19 and geopolitical tensions have impacted its growth.

With artificial intelligence (AI) being the current potential catalyst for great change in global markets, investors wait in anticipation of what it could mean for global fi rms, including those within the FTSE All-Share index.

Click the image below or scan the QR code on the image below to watch the video, The Evolution of UK Equities

2025 TRUMP LIBERATION DAY TARIFFS 2016 BREXIT REFERENDUM 2007 GLOBAL FINANCIAL CRISIS 1987 BLACK MONDAY 1973 GLOBAL OIL CRISIS 2011 EUROZONE DEBT CRISIS 2000 DOT-COM BUBBLE BURST

STOCK FOCUS GOODWIN PLC

For minority shareholders, investment in family-run businesses can o er management teams with longterm thinking, thoughtful decision making, and deep industry knowledge. One such company is Goodwin Plc, a specialist in mechanical and refractory engineering, which involves heat resistant materials. Goodwin is based in Stoke-on-Trent and started as a casting business in the 1880s. In 2019, the company handed over the running of the business to the sixth generation of Goodwin family members. Over the years, it has grown primarily organically through investing in the research and development of new technologies, while pursuing

cost e ciencies in existing product lines. This has been supplemented with several bolt-on acquisitions to access new markets or customers. It became a member of the FTSE 250 in July 2024, putting it on the radar of investors interested in smaller UK companies, and strong operational performance led to a total shareholder return of 284% in 2025.

Goodwin is structured as a group of 22 subsidiary companies operating across different sectors and geographies. The group is divided into the mechanical engineering and refractory engineering sectors but has a broad range of end users

RUTH HARRIS | INVESTMENT RESEARCH ANALYST

including those within jewellery, defence, power, construction, radar, oil and gas, and mining. This spread of different industries, some with low correlations to each other, has been key to limiting exposure to any one market. The company has no one customer representing over 10% of revenues, and offers investors diversified industrial exposure.

Many products within the engineering sector are commoditised, meaning it is easy for competitors to copy and therefore offers the manufacturer limited pricing power. For this reason, it can be hard for some industrial companies to increase revenues and drive strong profit growth for shareholders. Goodwin’s approach, potentially informed by a long-term view taken by the family management team, has been to specialise in niche, high-tech engineering, with a strong emphasis on new product development, which can often be patented, and investment in nurturing the next generation of engineering talent through its apprenticeship programme. It looks to supply these technically advanced products into growing end markets to drive cash generation and support strong margins.

Goodwin also has significant exposure to recurring revenues, where it signs an often multiyear contract with a customer to supply a particular product, often designed for the customer on a bespoke basis. This provides better visibility on future cashfl ows, as well as cultivating long-term client relationships and improving client retention.

cashflows, as well as cultivating long-term client relationships and improving client retention. In 2025, this focus on client relationships and highly specialised engineering led to a significant agreement with strategic customer Northrop Grumman, a major US aerospace and defence company. The deal covers key submarine programmes, with an initial order of US$16m and an expected total order of over US$200m in the coming years. The contract was well received by investors, with the shares jumping 14% after the announcement.

Outside of the recent deal with Northrop Grumman, Goodwin is also seeing growth in other key areas. In the most recent fi nancial report covering the six months to 31st October 2025, Goodwin announced that its radar company, Easat Radar Systems, won a contract for the primary surveillance radar (PSR) for Cornwall Airport in Newquay, as well as reporting strong performance in axial valve sales from its German manufacturing business Noreva GmbH driven by liquid natural gas (LNG) projects in the US and Qatar.

While Goodwin has seen exceptional share price performance in recent years, it also offers a dividend as part of total shareholder return. Dividend policy is often key to fi rms with significant family ownership, where individuals may rely on dividends to support their lifestyle. Accordingly, Goodwin has a policy of paying out 58% of post-tax profits, with some non-cash items like depreciation and amortisation added back, in dividends to shareholders. Given that it pays out a fi xed percentage of profits, this could lead to uneven dividends between years, or even no payout if the group failed to make a profit. However, strong operational performance has driven annualised growth of dividends of 24.2% over the last five years. While the current dividend yield of 1.2% is below the index, and many of its income-focussed peers, this has been driven by the exceptional share price performance and, if profits grow as expected, investors could expect to see corresponding growth in dividend in the coming years.

Given the significant ownership of the business, the family management team are well incentivised to maintain a dividend, as well as stewarding the business for future generations. For minority shareholders taking a long-term view, Goodwin’s niche engineering experience and diversified revenue exposure may make it an attractive opportunity within the UK smaller company sector. However, the share price is now optically expensive and incorporates elevated expectations for future profits. Any difficulty in meeting these expectations could cause a sharp fall in share prices. Furthermore, investing in family run businesses brings about its own risks, including potential governance issues, nepotism, and family emotions and relationships confl icting with business decisions.

Goodwin also has significant exposure to recurring revenues, where it signs an often multi-year contract with a customer to supply a particular product, often designed for the customer on a bespoke basis. This provides better visibility on future

Please note that this communication is for information only and does not constitute a recommendation to buy or sell the shares of the investments mentioned. Investments and income arising from them can fall as well as rise in value. Past performance and forecasts are not reliable indicators of future results and performance. The information and views were correct at time of publishing but may have changed at point of reading.

John Redmayne, Founder, Redmayne Bentley

Redmayne Bentley’s 150th anniversary celebrations will continue throughout 2026. Readers will be able to fi nd more anniversary content on our social media channels and by visiting: redmayne.co.uk/150.

Everyone at Redmayne Bentley would like to thank clients, readers and listeners for your support throughout our history, and we look forward to an exciting future with you.