In recent years, the global manufacturing industry has witnessed a new wave of netzero carbon reduction and smart manufacturing. With over two decades of expertise in precision fasteners and CNC components, Chin Tai Sing Precision Manufactory (CTSP) has emerged as a key partner in the international industrial supply chain, leveraging its multifaceted strengths in environmental sustainability, quality, and competitiveness. Its commendable manufacturing prowess and forward-looking expansion into mid-to-high-end and emerging markets have positioned it ahead of many peers in advancing green low-carbon initiatives, smart precision manufacturing, and global development.

To address the challenges posed by rising global awareness of low-carbon initiatives and the stringent requirements of the EU CBAM regulations, CTSP has fully integrated the concepts of “green environmental protection and low-carbon sustainability” into every production line. Through its low-pollution and high-efficiency production model, it has not only successfully obtained carbon footprint verification (CFV) but also meets customer demands by providing carbon footprint data compliant with CBAM requirements. In building future-ready green manufacturing lines that minimize environmental impact, CTSP concurrently optimizes energy usage within its facilities, reduces waste generation, and upgrades equipment and processes. For CTSP, low-carbon sustainability is not merely theoretical—it must be fully implemented and internalized as an integral part of the company's competitive edge.

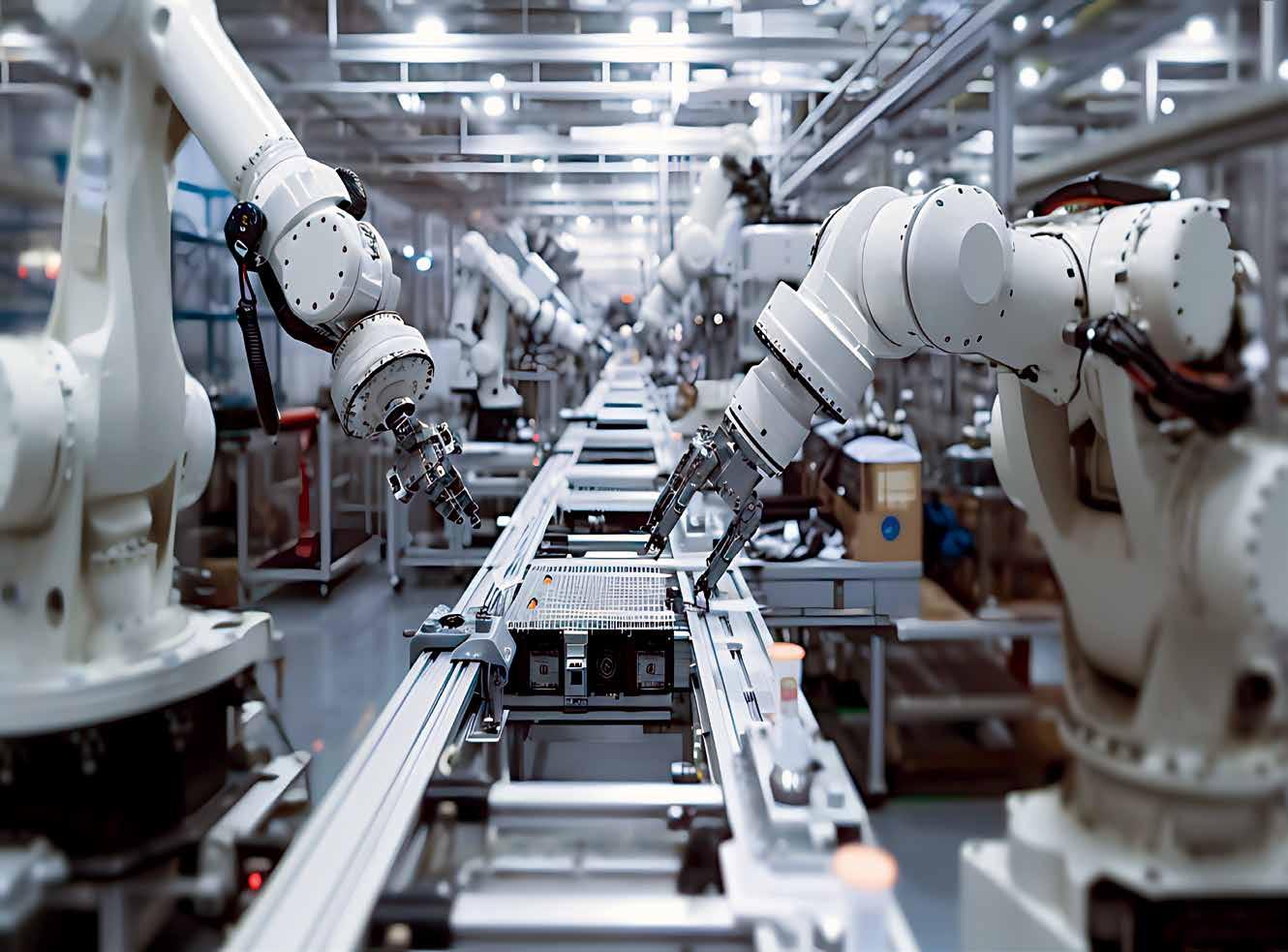

CTSP produces 20 million standard/special fasteners and CNC parts monthly. Production lines are progressively integrated with IoT and automated equipment alongside visual inspection systems. Through process management leveraging AI and machine learning tools, real-time data monitoring, demand forecasting, and autonomous process optimization mechanisms, the company comprehensively enhances smart manufacturing capabilities across the facility. Addressing customer priorities for product information transparency and reliability, CTSP pioneeres the industry by implementing a “Comprehensive Batch Number Management Framework,” which enables clients to track order progress and monitor product quality in real time. Its robust management systems and meticulous manufacturing processes have earned CTSP international certifications including ISO 9001:2015, IATF 16949, and RoHS compliance.

The demand for high-precision products is particularly stringent in advanced industries such as EVs, 5G, aerospace, and defense. CTSP's precision manufacturing capabilities, with tolerances as tight as ±0.01mm, perfectly meet these demanding requirements. Over the past few years, CTSP has not only maintained stable partnerships with European and U.S. clients, but has also expanded its footprint across Asia-Pacific and emerging markets to address demands driven by urbanization and infrastructure development. It has successfully penetrated markets in over 50 countries worldwide, serving sectors including automotive, aerospace, machinery, electronics, construction, defense, etc.

Exceptional quality is CTSP's fundamental standard for its products. Through automated and optimized production lines and the use of innovative materials, CTSP achieves a near-zero defect rate in the highly competitive fastener and precision parts market. Its integrated OEM and ODM customization services enable the company to deliver the most cost-effective product solutions to customers. Moving forward, CTSP will continue to pursue three core objectives: low-carbon manufacturing, smart management, and global expansion. With high-quality precision fasteners and components, CTSP is charting a sustainable future for the global supply chains.

CTSP’s contact: General Manager Lee / Email: inquiry@ctsp-insert.com.tw

US-Taiwan Reciprocal Tariffs Cut to 15% Without Stacking, Welcomed by Taiwan’s Hand Tool and Plumbing Hardware Associations 美台對等關稅降至15%不疊加

The US-Taiwan reciprocal tariffs have been finalized at 15% without stacking, bringing Taiwan back to the same baseline as competitors like Japan and South Korea. This move has been praised by Mr. Chia-lieh Chang, Chairman of Plumbing Association of Taiwan, as well as Jack Lai, former Chairman of Taiwan Hand Tool Manufacturers' Association as well as current Chairman Mr. Wu-Zhi Hsieh, who sees it as a major boost for the industries. Chia-lieh Chang noted that returning tariffs to the same level puts Taiwan on an equal starting line, especially compared to China's 40% tariffs, widening Taiwan's competitive edge. He forecasts that, barring major exchange rate fluctuations, long-term orders will stabilize in Q2, with benefits from redirecting orders from China becoming more evident. Wu-Zhi Hsieh stated that eliminating tariff instability and stacking is excellent news for the industry, with hopes for incoming orders. While Trump tariff rulings remain a variable, the current 15% level matches Japan and South Korea equally, marking a positive development. Though the steel industry remains under the US Section 232 at a 50% tariff, Taiwan CSC remains optimistic. CSC pointed out that for products not covered by Section 232 or with low steel/aluminum content, the reciprocal tariffs dropping to 15% without stacking on MFN rates significantly lowers effective rates, aligning competition with Japan, South Korea, and the EU, paving the way for steady steel market growth.

National Bureau of Statistics of China announced that the Chinese economy grew 5% in 2025, hitting its target, fueled by a historic USD 1.19 trillion trade surplus. Despite Q4 slowing to 4.5%, exports defy Trump tariffs, a slumping property market, and weak consumer spending. However, analysts call it a "dual-speed economy": robust manufacturing and exports contrast with lagging domestic demand and real estate. Capital Economics suggests the data overstates growth by 1.5 points. Compounding woes, China's births hit a record low of 7.9 million, with the population dropping 3.4 million to 1.4 billion. Natixis (France trade bank) warns low-price exports aren't sustainable. Last December saw home prices fall 2.7%, investment drop 17.2%, and retail rise just 0.9%. The head of National Bureau of Statistics of China acknowledges supply-demand imbalance but expects stability. Beijing plans proactive policies to boost confidence, curb debt, and reduce export reliance.

加墨關稅壁壘高築 台灣緊固件出口

恐損百億台幣

Mexico's and Canada's latest tariff policies are severely impacting Taiwan's fasteners industry. Mexico announced import tariff hikes of 5-50% on non-FTA countries starting 2026, while Canada imposed an additional 25% tariff on steel derivatives. Industry insiders worry that Taiwan's over NTD 10 billion annual North American export momentum is at risk, potentially leading to a complete loss of price competitiveness. Mexico and Canada account for 2.44% and 3.96% of Taiwan's exports respectively, totaling 6.4%, serving as key gateways into US automotive, aerospace, and construction supply chains. Mexico's move aims to block Chinese transshipment and origin laundering, but Taiwanese firms are caught in the crossfire. Canada's 25% tariff is even more devastating, effectively wiping out the thin margins in the mature fasteners sector and creating over NTD 1.3 billion in tax burdens, severely eroding Taiwan's North American market share. Experts urge Taiwanese manufacturers to accelerate transformation from traditional construction fasteners to high-value aerospace, medical, and EV fasteners to offset tariff impacts through premium pricing. Major firms are evaluating factory setups in Mexico to secure local production and certificates of origin.

India's Ministry of Finance issued an order on December 30, 2025, extending steel import tariffs for three years in its latest move to protect the domestic industry from global oversupply pressures. Tariffs on certain products will remain at 11% to 12%; the original measures were first introduced in April 2025 for 200 days. Facing a flood of low-priced exports from China that have driven global steel prices to multi-year lows, India is the latest country to respond. Cheap imports have hammered local producers like JSW Steel, forcing some smaller mills to shut down despite steady domestic demand. India's steel sector has expanded rapidly over the past decade, but output remains just a fraction of China's. Producers are banking on long-term gains from urbanization and industrial growth, with these tariffs providing long-awaited relief for mills. Analysts note that the policy bolsters supply chain resilience, supporting steady advancement in the local steel industry and is expected to spur investment and capacity upgrades.

印度電動車銷售2035年衝2200萬輛

KPMG's "Securing the Supply Chain: Preparing for the Electric Vehicle Raw Material Challenge" report predicts India's electric vehicle sales will reach 22 million units by 2035, with penetration exceeding 50% across vehicle segments. India's 2025 EV sales have neared 1.5 million units, with penetration surging from 0.7% in 2020 to 5.9%. Two-wheelers dominate India's EV market, accounting for 80-85% of sales due to affordability and suitability for urban commuting. Premium electric passenger vehicles with over 500 km range already capture 27% of that segment's sales. Electric scooters, three-wheelers, and intracity buses now offer lower total cost of ownership than internal combustion engine vehicles; fourwheeler commercial vehicles have achieved cost parity, with personal vehicles expected within the decade. Public charging stations exploded from 5,000 in 2022 to over 26,000 by early 2025. Government FAME and the PM E-DRIVE scheme—launched in September 2024 with INR 10,900 crore funding—has significantly accelerated adoption.

China Association of Automobile Manufacturers (CAAM) reports, based on customs data, that China's auto parts exports hit USD 7.88 billion in November 2025, up 14.3% from the previous quarter and 1.5% year-over-year. For JanuaryNovember, cumulative exports reached USD 86.59 billion, a 2.7% increase from 2024; on imports, November auto parts inflows totaled USD 1.89 billion, rising 12.6% quarter-on-quarter but down 20.2% annually. The January-November total imports stood at USD 19.49 billion, reflecting a 22.2% year-on-year decline.

馬來西亞緊固件進口逆差擴大

From January to September 2025, Malaysia's fastener trade showed persistent losses, with imports nearing USD 490 million against USD 260 million in exports—the former 1.9 times the latter, resulting in a clear deficit. Third-quarter imports surged while exports held steady, underscoring local capacity struggles to meet booming manufacturing needs.

Exports remained resilient, averaging USD 26-35 million monthly, peaking at USD 31.57 million in August, affirming international competitiveness. Imports accelerated sharply, hitting a nine-month high of USD 59.08 million in September (about 59,080 tons); Q2 hovered around USD 55 million, on an upward trend. The widening gap stems from manufacturing recovery and infrastructure projects boosting demand for high-strength fasteners; Malaysia's Southeast Asian hub status fueling re-export trade; and global supply chain shifts driving industrial imports. China leads as the primary source, bolstering Malaysian local chains. This signals a Southeast Asian manufacturing boom, urging Malaysia to accelerate localization and narrow the shortfall.

Automotive fasteners leader Sumeeko welcomes a turning point. The U.S. Section 232 grants Taiwan preferential treatment, slashing export tariffs to the U.S. from 50% to 15%. With customers progressively agreeing to tariff subsidies, Sumeeko's profit structure improves significantly this year, paving the way for operations to return to normal levels. Sumeeko's consolidated revenue last year reached NTD 2.554 billion, down 7.64% year-over-year, mainly due to advance payments for high tariffs and the ongoing optimization of its German plant. Around 60-70% of revenue comes from OEM clients. Last year, exports from its Taiwan plant to Europe and the US remained stable, but the model of shipping goods to U.S. warehouses first and awaiting client's replenishments required the company to advance the tariffs, severely impacting profits. In the second half, Sumeeko actively negotiated with clients; some have agreed to cover tariffs, while others adjusted shipping strategies. With the Taiwan-US tariff situation finalized, pressures have clearly eased.

Sumeeko announced that its German subsidiary, MAX MOTHES GmbH, invested €1.8 million to establish a wholly-owned new subsidiary, Beco Group GmbH, targeting acquisitions of suppliers to German OEM clients. This is expected to add €3-5 million in annual revenue, directly boosting this year's revenue and profits. Positive news also came from the US plant, which is undergoing customer certification and is slated for production in the first quarter, aligning with localization demands. Sumeeko's operations look promising this year, with the market optimistic about these dual positives driving a recovery.

Simpson Strong-Tie啟用投資1.25億美元建設的蓋拉廷新廠

Structural connectors and building solutions manufacturer Simpson Strong-Tie celebrated the grand opening of its latest manufacturing plant on January 15. The new plant launched with 227 employees, including machine operators, maintenance technicians, heat treatment technicians, and engineers, and is expected to add 20 more positions this year. Company CEO Mike Olosky stated that the facility significantly enhances production capabilities and the distribution network. "This is a one-of-a-kind manufacturing and training center in the construction industry, achieving end-to-end fastener production under one roof with the latest equipment and technology." This advanced 500,250 square-foot facility, built with a USD 125 million investment, will focus on testing and producing anchor bolts, fasteners, and "Quik Drive" fastening tools.

博世2025利潤率恐跌破2%,裁員與轉型壓力重

Global leading automotive components supplier Bosch is facing a severe financial crisis. CEO Stefan Hartung admitted in an internal email that the company's 2025 operating profit margin will be significantly below 2%, far short of initial targets. The 2024 margin had already slid from 4.8% in 2023 to 3.5%.

Hartung pointed to restructuring costs of €3.1 billion (3.5% of sales), mainly for layoffs and organizational adjustments, as the primary cause of shrinking profits. 2025 revenue is projected at €91 billion, up slightly from €90 billion in 2024, but growth stems largely from the Johnson Controls Hitachi acquisition (€4 billion contribution); excluding this, core business revenue actually declined, signaling weakening momentum. Hartung had already issued a warning on January 8, forecasting ongoing 2026 challenges with the 7% long-term margin target reachable no earlier than 2027. He blamed soaring tariffs and sluggish global growth for curbing auto demand.

To tackle the crisis, Bosch is ramping up layoffs: In October 2025, it announced 13,000 job cuts in its mobility division by end-2030, following 9,000 reductions in 2024. Weak EV demand, phasing out internal combustion engines, and fierce Chinese competition are key drivers.

Ironline Metals擴大漢普頓郡 營運 投資650萬美元創20 新職

US precision steel framing manufacturer Ironline Metals announced a USD 6.5 million expansion of its Hampton County plant in South Carolina, set to come online in Q2 2026. The project will add 20 jobs and boost capacity for cold-formed steel framing, studs, metal decks, fasteners, and ties.

President Sebastian Higdon stated: "South Carolina offers a superior workforce and business climate. We're proud to expand, enhancing customer service and creating opportunities for local families." The news drew enthusiastic support from local and state leaders. Governor Henry McMaster praised: "This expansion highlights South Carolina's manufacturing success, bringing growth opportunities to Hampton County families."

SouthernCarolina Alliance Chairman Steve Murdaugh added: "Ironline's deep roots here prove our region's labor and business strengths—we welcome their future growth."

Headquartered in Louisville, Kentucky, Ironline specializes in steel framing products. The expansion will strengthen the local economy and manufacturing sector.

South Korean fastener maker Young Mobility (YM) announced on November 18, 2025, that it has become the first domestic company to earn Ford Motor Company's top-tier Q1 certification. This award follows rigorous evaluation of quality, production capabilities, and supply chain management, designating YM as an official primary partner with rights to bid on new business. YM formed a cross-functional task force last October spanning quality, production, and sales, achieving certification after about one year. Currently supplying bolts for Ford Europe's (Germany, UK) powertrains, YM now targets North America and Ford Thailand for new opportunities. Ongoing projects with global giants like Hyundai-Kia (largest ICE and EV customer), Schaeffler, LG Magna, and BorgWarner continue expanding. YM is ramping up sales with Ford, GM, and Rivian, driving steady export and revenue growth.

Nitto Seiko announced that its Indian subsidiary Vulcan Forge's Jhajjar plant in Haryana began production in December 2025. Anchored by 5S systems, it strengthens customer engagement to optimize quality, delivery, and costs, integrating with group operations to enhance local manufacturing and supply stability. Located in Reliance MET City industrial park near the capital region—a smart city hub drawing major Japanese firms—the facility produces nuts and special cold-forged parts. Designed with second-floor expansion potential for future scaling. Future plans include accelerating client development for reliable Japanese supply; installing solar panels to cut power costs and emissions; consolidating HQ functions for optimized staffing, shorter lead times, and lower logistics expenses; and rolling out group training to build on-site personnel cohesion. This strategic move solidifies Nitto Seiko's Indian footprint, supporting global forging chains.

Sterling Tools財務長Pankaj Gupta於2025年底卸任

India's Sterling Tools Limited announced Group CFO Pankaj Gupta’s resignation, effective December 31, 2025. Having served nearly five years at the Faridabad plant, Gupta submitted his resignation to Chairman Atul Aggarwal, stating it is purely to pursue new opportunities aligned with his long-term career goals, with no other material reasons. He expressed gratitude for the company's trust and support over five years and committed to a smooth handover. Founded in 1979, Sterling Tools is headquartered in New Delhi, with its Faridabad facility producing automotive fasteners. As Key Managerial Personnel, Gupta's departure triggers regulatory requirements for a new appointment, which the company has yet to announce. This leadership change comes at a pivotal time for automotive industry transformation. The market is watching whether Sterling Tools' new financial leadership can stabilize operations. Deeply embedded in the automotive fasteners supply chain in recent years, the CFO role is crucial, and the successor's selection is under close scrutiny.

美軍維修M1艾布蘭戰車的秘密武器:Aircraft Dynamics公司專為戰場生產的衝擊扳手

When it comes to impact wrenches, most people think of popular civilian brands, but the U.S. Army actually relies on the Roboimpact impact wrench from Aircraft Dynamics' Robotools brand. This wrench doesn't chase maximum torque; instead, it prioritizes battlefield durability, safety, and adaptability. It ditches delicate gears and bearings for a rugged planetary gear system, traditional bearings, and an independent hammer mechanism—engineered for harsh environments to keep running even under extreme rough handling. Compared to civilian high-end cordless tools delivering 1,200 ft-lbs, the Roboimpact's "military-grade" ethos stands for reliable endurance over raw power. This maintenance tool, serving since the 1980s for tanks still in action today, embodies the engineering philosophy of military tools.

U.S. adhesive fastener specialist Click Bond has acquired surface intelligence and materials science firm Brighton Science, combining adhesion science with fastening innovation to boost scientific validation from surface to structure. Click Bond CFO Brandon Perlich stated: "Brighton Science brings exceptional scientific expertise to our engineering and manufacturing. Together, we'll make bonding more reliable, scalable, and trusted across industries." Post-acquisition, Brighton Science will operate independently, with its surface analysis research fueling Click Bond's R&D, product design, data science, and customer solutions—helping high-performance manufacturers achieve lighter, stronger, more efficient designs. Brighton Science CEO Andy Reeher noted: "Our surface analysis tech has enabled predictable bonds across industries for over a decade. Teaming with Click Bond merges our customer ties and tech leadership to deliver innovations that build manufacturing confidence." This strategic alliance arrives amid critical lightweighting demands in aerospace and automotive sectors, positioning Click Bond as a leader in adhesion-fastening solutions and driving product upgrades and market growth.

Germany's pgb-Holding Group has announced the acquisition of Dutch fasteners distributor GebuVolco, further strengthening its European market presence. Post-acquisition, GebuVolco will maintain independent operations, retaining its brand, organizational structure, and business contacts to offer customers a broader product range and customized solutions.

pgb-Holding stated that this move perfectly aligns with its growth strategy, consolidating European leadership through an expanded portfolio while creating sustainable value for customers, employees, and partners. GebuVolco distributes renowned brands like Silvermate and QZ while manufacturing hardware clamps and brackets, holding a leading position in the Netherlands' private label market. Under Mr. Dirk De Pijper and his team's leadership for over 30 years, GebuVolco traces its roots to 1947 when Gebu began producing fixing products. The 2000 acquisition of Volco International expanded its fasteners lineup, leading to the 2010 merger forming GebuVolco. This strategic alliance combines both firms' expertise, poised to drive product innovation and market penetration, especially in hardware and fastener applications. pgb-Holding thereby deepens its Dutch market foundation amid Europe's active M&A wave in the sector.

Swift Aerospace has completed its sale to Clarendon Specialty Fasteners, a subsidiary of Diploma Group. Swift Aerospace is a global aerospace distributor with operations across the UK, Europe, and Asia, specializing in approved fasteners and hardware. With over 30 years of experience, the company supplies products and services to some of the industry's largest original equipment manufacturers and has earned a reputation for sourcing hard-to-find specialist components.

Headquartered in Royal Wootton Bassett, Clarendon Specialty Fasteners is a leading supplier and distributor of fastening systems to manufacturers in the aerospace, defense, and motorsport industries. It is owned by FTSE 100 company Diploma, which employs 3,400 people across 17 businesses in the US, Canada, UK, Europe, and Australia. This investment will expand the product range, enhance supply chain resilience, and boost global service capabilities. Swift's international footprint and specialist products perfectly complement Clarendon's existing offerings, supporting Diploma's growth strategy.

TANGIBLE IND. CO., LTD, which has earned 100% trust from customers in Europe, USA, and Japan with its high-quality hand-operated staple guns in the fastening tools sector, has been in operation for nearly 50 years. Unlike many competitors vying for large-volume orders to maximize sales revenue and overall profit, Tangible possesses mass production capabilities yet prioritizes products with higher technical complexity and smaller batch requirements as the cornerstone of its business expansion. This approach has enabled Tangible to distinguish its products with unique characteristics throughout its development journey. By avoiding excessive price competition and steadily building its presence in less-explored areas, the company has firmly secured its own market niche.

Tangible contact: Mr. Richard Chang

Email: richard@tangible.com.tw

“We are willing to assist clients in developing staple guns or other products that may appear niche. As long as our production capacity and equipment meet the requirements, we can evaluate manufacturing. For instance, during the pandemic, we even received animal trap orders from clients and have continued supporting them ever since,” Tangible stated. Tangible's staple guns demonstrate a strong customer-centric approach, enabling comprehensive customization of gun body design and production to meet clients' market application requirements, dimensional specifications, wire thickness, and impact force. Representative products that have gained significant global popularity in recent years include staple guns supporting T50 and JT21 staples with spring-driven mechanisms for reduced effort, as well as cable tackers for securing wires.

Tangible's product portfolio extends beyond staple guns to encompass plastic/metal forming, metal stamping, spot welding, assembly, and packaging, delivering comprehensive one-stop solutions for clients. For smaller brands lacking sufficient production capacity, this integrated model significantly reduces the cost burden of sourcing multiple suppliers and logistics separately, creating a stronger competitive edge. “With years of extensive experience in collaborating with clients, we assist in developing products ranging from mechanically complex structures to standardized wire products or those requiring specific materials. After thorough communication, consultation, and evaluation of costs like shipping and tariffs, we complete testing, prototyping, and production. This approach helps reduce costs while ensuring consistent product quality. Recently, we've even expanded into the local motorcycle parts sector, assisting clients in developing carbon fiber components,” stated Tangible.

Tangible's stable technology, quality, and service enable up to 95% of its products to be exported to advanced markets such as the U.S., Europe, and Japan. To meet the stringent quality standards demanded by these countries and deliver exceptional product performance, the company fully implements rigorous Japanese manufacturing standards within its own production quality control, demonstrating an unwavering commitment to quality. Facing greater global market challenges and product development visions ahead, Tangible stated: “We sincerely welcome clients to inquire about development assessments for various products. Moving forward, in addition to maintaining stable supply of our professional staple guns, we also look forward to exploring diverse product categories while leveraging our diversified business model to showcase the formidable strengths of Taiwanese enterprises.”

Copyright owned by Fastener World / Article by Gang Hao Chang, Vice Editor-in-Chief

Compiled by Fastener World

IPS PLIERS (Japan) has recently unveiled the "Electrical Devil" plier with its compact and ultra-lightweight design. Measuring just 148mm in length and weighing only 107g, it securely grips objects from 9mm to 43mm in diameter with a 5-stage adjustment for ultimate flexibility. Perfect for electrical conduit connectors, knockout waterproof fittings, paint can opening, or tight-space maintenance.

It shines in professional electrical work and DIY tasks. Equip it with a drop-prevention strap for easy attachment, and it takes up minimal space in your tool pouch—far slimmer than traditional models. It is under 150mm long and 5mm wide. Shaped like a flathead screwdriver, it handles tightening and loosening without switching tools. Built tough with cation electrodeposition coating for wet environments (10x more durable than nickel-chrome plating).

Crafted from high-carbon steel body with PVC-coated handles, it features an 8mm head thickness, 43.6mm head length, and 40mm handle width. It blends practicality and portability—essential for electrical and DIY pros.

鑽石頂級螺絲起子(+2×100)

This stepped screwdriver bit, featuring an ultra-fine shank diameter of Φ3.8mm, comes from Japan's Anex Tool. Designed for the toughest screws, its diamond particles grip relentlessly—even non-magnetic stainless steel screws stay put without dropping. Boasting high toughness and top-tier hardness (HRC62.5), it resists breakage and wear, delivering twice the durability of traditional stepped bits.

Magnet-free design prevents iron filings from sticking, with uniform thick electroless nickel plating for perfect screw fit and superior rust resistance. Ideal for stainless steel, brass, aluminum, or resin screws, as well as interior, decorative, precision, and electronic applications. Hex shank (6.35mm across flats), no magnet, compatible with 40V tools (also 18V).

Made from chrome-molybdenum-vanadium steel for exceptional wear resistance. A must-have for professional interior and electronics work—say goodbye to slipping and snapping for smoother, more efficient jobs.

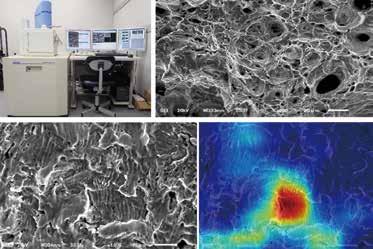

Osaka Research Institute of Industrial Science and Technology, in collaboration with Osaka Metropolitan University, has rolled out its AI-powered metal fracture analysis software "Fract(ure) AI" at public testing and research institutions across Japan. This service integrates scanning electron microscope (SEM) imagery for AI-driven metal fracture analysis, ushering manufacturing failure diagnostics into the intelligent era.

Manufacturing floors frequently encounter trial and error, where pinpointing failure (fracture) causes is crucial for boosting product reliability. "Metal fracture analysis" examines fracture surface features to uncover root causes. Fract AI uses just SEM images to automatically predict fracture types like fatigue or ductile failure with high precision, highlighting key areas via color contour maps.

Incorporating judgment criteria from veteran technicians' years of observations, it powerfully supports novices, sharpening their skills amid labor shortages and succession challenges—doubling as an invaluable training tool. Future updates will include fracture origin prediction features for ongoing evolution, accelerating product improvements and sharpening corporate competitiveness.

Hilti's brand-new "BX 3-22 Cordless Fastening Tool" is tailored for MEP and interior finishing This fully electric model with a 30-nail magazine replaces traditional drilling and anchoring, delivering faster, more consistent performance. A single lithium battery charge drives up to 850 nails for stunning efficiency.

Key features include an ergonomic contoured grip, short stroke design, and LED light for better handling, reduced recoil, and lower noise. Compact at 475 x 135 x 368 mm and just 3.5 kg, it offers Bluetooth connectivity, a 21.6V battery platform, and supports 14-30 mm nails on reinforced concrete, masonry, or steel.

Versatile applications: securing drywall tracks to floors, ceilings, and walls; fastening mesh, waterproof membranes with special washers to concrete; wall connectors; and light-duty fixes like cables, conduits, and grids. No gas cans or powder needed—batterypowered for 800/500/400 nails (model-dependent) at 1.3 nails per second. BX 3-22 boosts contractor productivity with reliable quality and zero waste.

NTK Cutting Tools has launched the all-new "ECO Series" for its Thread Whirling tools, dramatically cutting costs compared to traditional models. Users can now select the insert's number of teeth and corners based on workpiece needs, enabling production at minimal expense. This series newly supports left-hand thread cutters, expanding applications to meet diverse machining demands.

Key features: Unlike fixed 9-tooth conventional cutters, ECO offers 3, 6, or 9 teeth for flexible productivity and surface finish control. For small batches like medical screws, choose 1- or 2-corner inserts to minimize wear based on volume. Left-hand thread standard cutters are included for the first time, covering all thread types without custom orders.

The ECO Series empowers precision manufacturers with adaptability, reduced tool investment, and boosts competitiveness—for highvolume runs or custom medical parts alike.

「ALTIMA」鋁合金汽車螺栓

Born from a joint patent between Yamashina and Nippon Light Metal Company in Japan, the game-changing automotive aluminum bolt "ALTIMA" is now available. Surpassing traditional designs, it prioritizes durability and safety by mitigating stress corrosion cracking risks from prolonged stress concentration. Matching the corrosion resistance of legacy bolts used in European and select Japanese cars, ALTIMA boosts strength by over 10%. It is built on the July 11, 2024 joint patent (No. 7496106) and four years of rigorous safety validation.

Features: Tensile strength over 460 MPa, yield strength over 380 MPa—equivalent to JIS aluminum grade AL5 (one tier above conventional AL4)—with anti-cracking and void-free processing for flawless internals. Targeting EVs, unmanned aerial mobility, robots, inverters, batteries, aluminum busbars, and ecoinfrastructure, it excels in lightweighting, non-magnetism, conductivity, corrosion resistance, and anti-loosening, supporting low-carbon circular economies. Nippon Light Metal and other partners will continue collaborating to expand.

ALTIMA doesn't just enhance vehicle safety—it powers the green mobility revolution and sets new precision manufacturing benchmarks.

對等關稅

(Note: Part 1 has been published in Fastener World issue no. 216, Mandarin version, p.66)

In diplomatic negotiations, Japan has persistently urged the U.S. to exempt Japan from tariff measures. It has appointed a dedicated minister to lead negotiations with the U.S. and is conducting a swift, detailed assessment of the tariff impact on domestic industries and employment. It offers measures supporting manufacturers to ensure smooth cash flow and establish a special contact to assist companies in responding. Japan is also collaborating with other countries, forming an “Alliance for Autonomy” with the EU, Australia, and others to jointly counter the rise of protectionism.

The most notable aspect of the U.S.-Japan agreement is the imposition of a 15% “reciprocal tariff” on all imports from Japan. This rate is significantly lower than the 25% punitive tariff threatened by the Trump administration in its July 7th letter, which stated it would be fully implemented if no agreement was reached by the August 1st deadline. For Japan's vital automotive manufacturing and parts industries,

negotiations successfully secured a halving of automobile tariffs from 25% to 12.5%. Combined with the existing 2.5% base tariff, this results in a 15% rate, significantly easing pressure on Japan's auto sector.

The Japanese government has pledged to eliminate longstanding non-tariff barriers, with the most significant breakthrough being its first-ever agreement to recognize U.S. automotive safety standards (FMVSS). In the future, U.S. vehicles entering Japan will no longer undergo additional, cumbersome, and costly localized safety testing, creating a more level playing field for U.S. automakers that have long struggled to penetrate the Japanese market. The Japanese government will also employ fiscal and monetary measures to mitigate impacts and stabilize industry confidence, while simultaneously pursuing negotiations with the U.S. to secure more favorable tariff terms.

Adjusting production systems, some Japanese automakers may consider relocating production lines to the U.S. to avoid tariffs. To enhance supply chain resilience and reduce reliance on any single market, Japanese automakers will accelerate building more resilient, diversified global supply chains and market footprints. Alternatively, they may directly request governments to exempt them from tariff sanctions during negotiations—particularly manufacturers in critical industries like automobiles and auto parts. Others are assessing how tariffs will impact profitability and competitiveness, seeking to pass on some costs to customers or consumers. Still others are seeking manufacturer support, relying on government-provided working capital assistance (especially for SMEs) to ensure operational stability.

The S. Korean government has established a dedicated “One-Stop Tariff Response Support Headquarters” to assist in assessing the impact of tariffs across various industries and coordinate relevant countermeasures. Through policy-based financial support, additional assistance will be planned to help manufacturers navigate the trade crisis. In terms of manufacturing reshoring, measures to support manufacturers returning to Korea have been outlined, alongside increased subsidies and support for foreign-invested enterprises. In sectors like semiconductors and pharmaceuticals the response plans are being accelerated, while strategies to counter tariffs on steel, automobiles, and other items are being improved as well.

Korea provides financial support and its government has expanded the scale of industrial support funds, offering policy-based financial loans to the automotive industry and assisting SMEs impacted by tariffs. Tax relief measures allow affected companies to apply for extended deadlines for corporate income tax, value-added tax, and income tax payments. To promote market diversification and reduce reliance on the U.S. market, the government encourages manufacturers to expand into other overseas markets, such as Southeast Asia and the Middle East. To enhance industrial competitiveness, the government continues to promote technological upgrades and R&D to strengthen the technological edge of Korean automobiles in areas like new energy vehicles, thereby countering trade barriers.

They relocate production bases to lower-cost supply chains in regions such as Southeast Asia, moving manufacturing operations out of affected areas. Negotiating with brand clients or downstream manufacturers to jointly share tariff costs. In terms of bargaining power, manufacturers can pass on tariff costs to customers through price negotiations for certain products (e.g., auto parts). As for seeking local supply chains, they actively identify lower-cost supply chains within the U.S. to mitigate tariff impacts.

SMART MANUFACTURING AND AI TECH

HIGH-EFFICIENCY EQUIPMENT CENTRALIZING RAW MATERIAL PROCUREMENT

SUPPORT REVIEW THE EXCISE TAX POLICY

In response to potential impacts from reciprocal tariffs and exchange rates, Taiwanese government has proposed six countermeasures for the auto parts industry including 1. Adopt smart manufacturing and AI technologies to help component manufacturers enhance production line efficiency and reduce defect rates. 2. Through the replacement policy, manufacturers are guided to purchase new high-efficiency equipment, achieving energy conservation, carbon reduction, and lower long-term operating costs, thereby promoting sustainable development. 3. Centralizing raw material procurement to strengthen manufacturers' bargaining power, with the MOEA assisting in reducing production costs and passing benefits to midstream and downstream suppliers. 4. Increasing innovation support for manufacturers by raising R&D investment tax credits and expediting R&D subsidies with preferential terms to incentivize transformation R&D. 5. Recommending to the Ministry of Finance that it review the excise tax policy to accelerate the phase-out of old vehicles and expand the domestic market. 6. Promoting credit guarantee measures for SMEs to obtain hedging quotas, helping the industry mitigate exchange rate risks.

Taiwan's automotive parts supply chain comprises 2,236 manufacturers, operating as an export-oriented country. In 2024, total exports reached NT$187.32 billion, with exports to the U.S. accounting for NT$97.89 billion (52.3% of total exports). Manufacturers exhibit extreme sensitivity to reciprocal tariffs and exchange rate fluctuations, which directly impact profitability and operational performance with far-reaching consequences. Affected by electricity price hikes, exchange rate volatility, rising raw material costs, and sluggish domestic demand, the industry urgently requires government intervention to stabilize electricity prices and exchange rates. Additionally, it is imperative to reference international trends in promoting legislative amendments for repair liability exemptions. Concurrently, expanding domestic demand is essential to ensure the automotive industry's competitiveness and sustainable development.

The international economic and trade environment is constantly evolving with far-reaching impacts. It is imperative to establish more rapid and diverse communication channels to actively engage with the industry in real time, gather frontline insights, and swiftly integrate them into more precise and impactful industrial policies and support action plans. This will empower manufacturers to transform challenges into opportunities for global advancement, comprehensively strengthen operational resilience, forge the global competitiveness of Taiwan's vehicle industry, and turn adversity into opportunity.

Cost-saving strategies include establishing local manufacturing facilities in the U.S. and shifting production lines to domestic operations to avoid import tariffs and reduce production costs. Alternatively, shifting production focus to Southeast Asia is viable. Due to evolving global trade conditions, many industries are concentrating the majority of their production orders on Southeast Asia's domestic market, reducing reliance on exports and mitigating profit erosion from high tariffs. They enhance production efficiency to offset tariff costs by improving processes, increasing output per unit, and reducing scrap rates to boost profit margins, as well as adopting standardization and automation solutions to effectively elevate production line efficiency.

They introduce smart manufacturing by using robotic arms integrated with vision systems in auto part production to instantly identify and remove defective parts, effectively preventing NG parts from entering subsequent processes while reducing scrap losses and quality control pressures. Robotic arm applications in automotive parts classification include body system components such as external structures and trim parts (e.g., bumpers, exterior panels) and interior system components (e.g., instrument panels, gear shifters, seatbelt buckles). These serve as driver control interfaces and passenger safety devices, ensuring operational convenience and safety assurance.

The imposition of reciprocal tariffs on imported cars and components represents the largest single-industry tariff adjustment by the U.S. in recent years, covering core items such as complete vehicles, engines, transmissions, and electronic control modules, which aims to promote manufacturing reshoring and trade fairness. However, it may also exert long-term restructuring pressure on global supply chains. In the short term, Taiwanese auto parts manufacturers should focus on whether their brands and supply chain configurations possess localized advantages. Over the medium to long term, companies that can anticipate customer demand restructuring, accelerate local investment in the U.S. and integrate supply chains may have the opportunity to upgrade from mid-tier manufacturing to critical supply chain roles, making them the structural beneficiaries amid the global wave of order shifts.

Given the booming N. American complete vehicle and auto parts maintenance & repair service markets, auto parts manufacturers have successively invested in establishing factories in the U.S. By sourcing materials locally and supplying customers nearby, they have secured an advantageous position in the tariff war. Since Trump's first term, manufacturers have actively expanded facilities in the U.S. or Mexico and refined molds. LED automotive lighting module manufacturers, in addition to supplying U.S. automakers, are aggressively expanding production facilities to respond to potential policy shifts. Exterior parts suppliers, leveraging the USMCA agreement, have established manufacturing in Mexico and utilize local assembly plants and logistics networks to distribute products throughout N. America.

Some manufacturers transitioning from traditional production to high-value-added products are adjusting their exports to N. America (particularly the U.S.) market and accelerating the pace of establishing factories in Mexico, which currently enjoys temporary tariff exemptions, to reduce defect rates and enhance production efficiency. This enables them to offer customers more diversified services and mitigate the impact of tariffs. Leading manufacturers are responding to the trend of global supply chain diversification by planning collaborations with local suppliers in Thailand and Mexico, and are adopting a manufacturing division model to circumvent tariff barriers through “local manufacturing,” thereby mitigating trade risks.

Under rising cost pressures, manufacturers' bargaining power has become critical to survival, manifesting at both short-term and long-term levels. Short-term strategies involve cost negotiation and pass-through. Manufacturers possessing key technologies or long-standing, stable partnerships with clients—such as certain Taiwanese firms that successfully negotiated shared tariff burdens with customers—demonstrate their products' indispensable role within supply chains. The long-term strategy involves enhancing the added value of products. The more enduring path lies in fundamentally transforming the price-competition mindset inherent in “traditional OEM manufacturing.” Manufacturers must invest in R&D and innovation to develop high-valueadded products with “irreplaceable” characteristics, such as key components for EVs, lightweight materials, and smart cockpit technologies. Only when products evolve from “me too” to “me only” can manufacturers truly gain pricing power, transforming tariff costs into part of the value proposition rather than merely a profit drain.

The latest outcome of reciprocal tariff negotiations may create new opportunities for Taiwan. As the world's largest automotive market, China has not only cultivated a vast domestic consumer base in recent years but also seen its domestic automakers actively expanding into Europe, Mexico, Central & South America (e.g., BYD, etc.), and Southeast Asian countries (both complete vehicles and components). The imposition of punitive tariffs as high as 75% on Chinese auto parts by the U.S. has enhanced the competitive edge of Taiwanese auto parts in the U.S. automotive aftermarket (AM). This shift implies that substantial orders previously supplied by China to the U.S. market now face pressure to relocate. If Taiwanese manufacturers seize this opportunity and maintain superior DQC (Delivery, Quality, Cost) standards, they may capitalize on order transfers lost to Japanese and Korean competitors. Furthermore, during the global supply chain restructuring, they could expand their market share.

When external conditions cannot be fully controlled, manufacturers must look inward to refine operations and enhance efficiency as a key strategy for managing cost pressures. Implementing smart manufacturing technologies—such as artificial intelligence and automated production lines—is the critical pathway to achieving cost reductions.

Through smart production, companies can not only boost manufacturing efficiency and lower defect rates but also effectively address Taiwan's increasingly severe labor shortage. Among the six major countermeasures proposed by MOEA (Taiwan), the first is “adopting smart manufacturing and AI technology services.”

This reflects a consensus between the government and the industry on this trend. It is not only a response to the current tariff crisis but also lays a solid foundation for manufacturers' long-term competitiveness over the next decade.

The U.S. has FTAs with S. Korea and Japan, so both Korea and Japan enjoy a 0% tariff rate. Previously, Taiwan faced tariffs of 1.2% to 6.5% (varying by product category) when exporting auto parts to the U.S., placing Taiwanese auto parts at a competitive disadvantage. Through renegotiating reciprocal tariffs, the rates for Taiwan, Japan, and S. Korea have been aligned at 15%, which means Taiwan now stands on equal footing with major industrial competitors like Japan and S. Korea, representing a significant advantage.

The tariff negotiations between Taiwan and the U.S. are likely to be a process of mutual concessions. For Taiwan's auto parts industry, the U.S. tariff serves as both a stress test and an opportunity for restructuring and industrial transformation. This impact is structural and multifaceted, signaling the end of an era reliant solely on cost advantages. Manufacturers' “self-rescue” is the fundamental path to weathering this winter, including accelerating global deployment to diversify risks, investing in R&D to create irreplaceable value, deepening smart manufacturing, and enhancing production efficiency.

While the government's role in providing short-term relief is crucial, policy design must be more precise and timely to ensure resources truly flow to the most needy manufacturers. In the long run, proactive diplomatic negotiations and sound macroeconomic policies are essential to create a fair and predictable competitive environment for the industry. Taiwan's auto parts industry possesses a robust manufacturing foundation, flexible adaptability, and a comprehensive supply chain with industrial clusters. With strategic collaboration between manufacturers and the government, this crisis can be transformed into a catalyst for industrial upgrading. Amidst the global supply chain restructuring, the industry can not only stabilize its position but also carve out a new and irreplaceable niche.

Imports and exports in 2025 have become just as important as sales figures in understanding the direction of the U.S. automotive market. Over the first three quarters of 2025, the United States imported nearly USD 170 billion worth of automobiles from its foreign trade partners, while exporting approximately USD 55 billion, highlighting the scale and imbalance of vehicle trade flows shaping the industry. U.S. statistical trade data illustrates how deeply integrated global supply chains continue to underpin the American auto market, even as manufacturers expand domestic production and policymakers emphasize reshoring. Passenger vehicle imports remain a critical source of supply for U.S. consumers, while exports of U.S. built trucks and SUVs reinforce the country’s role as a key production hub for larger vehicles. Leading automakers including General Motors, Ford, Toyota, HyundaiKia, and Stellantis are competing not only on demand, but on how effectively they manage imports, exports, and North American production capacity.

Data note: The data for this article is derived from the US Census trade statistics. US Census trade statistics analyze imports and exports across all modes of transportation. That value is calculated in FOB USD. Automobiles in this article are categorized under HS 8703 (motor cars and other motor vehicles design for the transport of people), 8704 (motor vehicles for the transport of goods, i.e. commercial trucks, pickups and vans used for cargo), and 8702 (motor vehicles for the transport of ten or more people).

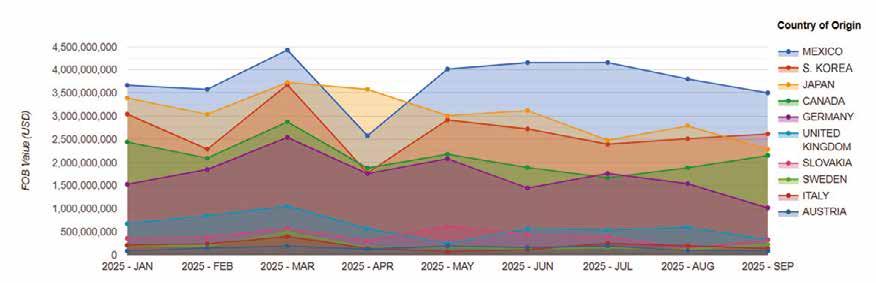

Trade flows continued to play a defining role in the U.S. automotive market in 2025. Passenger vehicle imports, classified primarily under HS 8703, accounted for more than 80% of inbound motor vehicle trade (Table 1) , showcasing the U.S. market’s sustained reliance on foreign made cars and cross-border production networks, particularly within North America and Asia. One notable exception occurred in April 2025, when newly implemented tariffs began to influence trade patterns and Japan’s share of passenger vehicle imports rose to nearly 27%, while Mexico’s share fell to 19%.

(Fig. 1) Mexico largely maintained its position as the United States’ primary automotive trade partner through the first three quarters of 2025, accounting for approximately 19% to 28% of total passenger vehicle imports. S. Korea followed with a share ranging between 13% and 20% over the same period.

Import volumes also reflected significant month-tomonth volatility during the first half of 2025. March saw higher-than-average import activity, followed by a sharp contraction in April, when total import values declined from approximately USD 20.5 million to USD 13.2 million. Subsequent months continued to trend below first-quarter levels, suggesting a period of adjustment following policy changes and shifting sourcing strategies. From a geographic perspective, the majority of imported passenger vehicles were destined for Michigan and California, which together accounted for roughly 35% of total monthly imports, reflecting their central roles in automotive distribution, manufacturing, and consumer demand.

25,331,212,277

6,407,059,524

9,721,259,848

4,754,066,508

6,251,746,137

3,941,188,238

6,526,828,838 6,499,356,688 5,056,678,330 3,882,075,347

3,836,972,760

3,659,622,168

Unit: FOB Value (USD)

0 20,000,000,000 40,000,000,000 60,000,000,000

A similar pattern emerged in the trade of trucks and pickups classified under HS 8704, where imports were overwhelmingly concentrated among North American partners. Mexico and Canada together accounted for over 90% of total U.S. imports in this category, while countries such as the United Kingdom and Japan each represented roughly 1%. Over the past several years, imports of trucks and pickups steadily increased, rising from approximately USD 35 billion in 2022 to USD 47.5 billion in 2024, representing growth of nearly 35%. This trend reflects persistent U.S. demand for light trucks and pickups, as well as the deeply integrated nature of North American production networks supporting these vehicle segments.

Motor vehicles designed for the transport of 10 or more passengers, classified under HS 8702, represent a more specialized import segment. U.S. sourcing in this category is concentrated primarily among Canada, Turkey, and North Macedonia. Canada’s role reflects its long-standing integration with U.S. transit and commercial vehicle

manufacturing, supplying a steady volume of buses built to U.S. specifications. At the same time, Turkey and North Macedonia function as important global export hubs for buses and coaches, supporting niche demand and specialized configurations. In Turkey, manufacturers such as TEMSA, Otokar, and Mercedes-Benz Türk dominate exports to the U.S., while Canadian suppliers including New Flyer, Motor Coach Industries, and Prevost remain key providers for U.S. transit agencies and fleet operators.

In export terms, the United States ships significantly fewer vehicles abroad than it imports, reflecting a trade profile driven more by production specialization than by overall market volume. U.S. auto exports are concentrated in larger frame vehicles and full-size pickup trucks, particularly those produced by manufacturers such as Ford, General Motors, and Stellantis, where domestic manufacturing remains globally competitive. In addition, a smaller but high-value share of exports consists of luxury sedans, premium SUVs, and performance vehicles produced in U.S. facilities serving global markets. Canada remains the dominant destination for U.S. vehicle exports, accounting for approximately 45% of export value in Q1 2025, 30% in Q2, and 34% in Q3, underscoring the depth of North American automotive integration. (Table 2) A significant portion of these exports originate in South Carolina, where manufacturers such as BMW, Volvo Cars, and Mercedes-Benz Vans operate major production facilities that supply both the U.S. market and international buyers.

Despite continued investment in domestic manufacturing, vehicle imports remained essential to meeting U.S. market demand in 2025. Imported vehicles, particularly passenger cars and compact SUVs, accounted for a substantial share of vehicles sold in the United States, filling segments that domestic production alone did not fully serve. While General Motors and Ford continued to dominate U.S. production with trucks and SUVs, much of the volume in passenger vehicles was supported by foreign-built models from manufacturers such as Toyota and Kia, whose global production networks supplied the U.S. market efficiently at scale. These import flows reflect long-established sourcing strategies rather than short-term market dislocation.

Vehicles imported from Mexico, Canada, Japan, and South Korea support price-sensitive and fuelefficient segments of the market, while U.S. based production is increasingly aligned with fullsize pickups, larger SUVs, and premium models that are also well positioned for export.

This reliance on imports helps explain why U.S. vehicle sales have remained relatively resilient in 2025, even as domestic production remained concentrated in higher-margin segments. For leading automakers, including GM, Ford, Toyota, and Kia, competitiveness in the U.S. market depends on balancing domestic manufacturing with strategic imports, an approach that highlights how deeply trade flows are embedded in the structure of the U.S. automotive industry.

The U.S. automotive market in 2025 is best understood through the intersection of production, sales, and trade. Import and export data reveal structural realities that sales figures alone cannot capture, while automaker performance reflects how effectively manufacturers navigate these dynamics. As leading OEMs continue to refine their production footprints and sourcing strategies, trade flows will remain a critical indicator of competitiveness in the U.S. auto market.

In 2025 the U.S. economy was valued at roughly US$29 trillion in GDP, with goods-producing sectors contributing a significant share of output. Manufacturing alone added nearly US$2.9 trillion, accounting for about 10 % of total U.S. economic output, and supporting millions of jobs across the industrial base. Construction activity contributed about 4.4 % of GDP, equivalent to nearly US$1.3 trillion, as residential, commercial, and infrastructure projects drove demand for both basic and advanced fastening tools. These figures underscore how fastening tools not only serve as physical connectors on job sites and assembly lines but also act as a barometer of productive activity in critical sectors like manufacturing and construction. Given this economic context—where capital investment, industrial output, and construction spending are central to growth—understanding the size, dynamics, and future trajectory of the U.S. fastening tools market is essential for investors, manufacturers, distributors, and strategic planners.

Global Baseline

The global fastening power tools sector alone is substantial. Estimates range widely due to different methodologies, but multiple credible sources converge on a multi-billion USD market:

• A 2024 market report estimates the global fastening power tools market at roughly USD 3.9 billion in 2024, with growth expected toward USD 7.8 billion by the early 2030s.

• Broad tooling and assembly fastening categories can be even larger when manual tools and consumable fasteners are included, with assembly fastening tools alone forecasted to exceed USD 9+ billion by 2035.

Crucially, North America is one of the leading regional markets, often capturing around 30–36% of global volume in broader assembly and fastening segments.

Pinning an exact number for the U.S. fastening tools market requires interpolation because many market intelligence reports do not separate the U.S. from broader North America. However:

• One estimate places the U.S. fastening power tools market at approximately USD 950 million in 2024.

• Broader assembly fastening tools (which include more than just powered devices) represented North America at roughly USD 1.22 billion in 2024, with the U.S. representing the lion’s share of that.

Add to that the vast fasteners themselves (nuts, bolts, screws), where the U.S. is estimated to account for around 30% of global fastener consumption—a market likely well over USD 30 billion when fasteners and tools are combined.

U.S. construction activity has long been one of the most powerful demand engines for fastening tools, driven by the scale and continuity of building activity across residential, commercial, and infrastructure segments. In 2024, the total U.S. construction spending exceeded USD 2.0 trillion, reflecting sustained demand despite higher interest rates. Residential construction accounted for roughly USD 880–900 billion, while non-residential and infrastructure projects contributed more than USD 1.1 trillion, including highways, bridges, utilities, and public facilities. Each of these segments relies heavily on fastening tools for structural framing, mechanical installations, finishing, maintenance, and retrofitting.

Although construction cycles fluctuate with financing conditions, long-term demand has been reinforced by federal infrastructure spending. The Infrastructure Investment and Jobs Act (IIJA) allocates approximately USD 1.2 trillion, including USD 550 billion in new federal spending over multiple years, targeting transportation, water systems, energy grids, and public works. These projects are tool-

intensive by nature and create sustained, multi-year demand for both manual and powered fastening solutions.

Reflecting this structural demand, the U.S. construction fasteners market alone was valued at nearly USD 4.85 billion in 2024 and is projected to grow to approximately USD 7.16 billion by 2035, indicating a steady expansion tied directly to construction output rather than short-term cycles. Because fastening tools are consumed continuously throughout construction workflows— rather than only at project initiation—stable or growing construction activity translates into repeat and non-discretionary demand for fastening equipment. As a result, the health of the U.S. construction sector remains one of the most reliable predictors of fastening tool consumption across the market.

Traditional U.S. manufacturing—covering machinery, industrial equipment, metal products, appliances, and legacy internal combustion engine (ICE) vehicles—continues to represent the largest volume base for fastening tool demand. As of 2024, U.S. manufacturing generated approximately USD 2.9 trillion in value added and employed close to 13 million workers, with transportation equipment, fabricated metals, and machinery among the top subsectors. These industries rely heavily on high-volume fastening operations, typically using pneumatic, electric, and cordless tools optimized for speed, durability, and repeatability rather than advanced data integration.

In automotive assembly, traditional ICE vehicle production still dominates unit volume. The United States produced over 10 million vehicles annually, with conventional vehicle platforms requiring 2,000–3,000 individual fastening points per vehicle, depending on model and complexity.

From a market perspective, this segment anchors the fastening tools industry in volume stability, but offers limited upside in terms of pricing power or margin expansion.

In contrast, high-precision manufacturing—particularly EV and advanced mobility production—is reshaping the value structure of fastening tool demand. While EVs still represent a minority of total vehicles produced, they exert a disproportionate impact on tooling requirements. In 2024, the U.S. produced approximately 1.2–1.4 million electric vehicles, accounting for roughly 12–14% of total light vehicle production, a share expected to continue rising.

EV platforms introduce fundamentally different fastening requirements. Battery packs alone can involve hundreds of critical fastening points, each requiring precise torque control, sequencing, and traceability to ensure safety, thermal stability, and structural integrity. Lightweight materials such as aluminum alloys and composites further increase sensitivity to over- or under-torque conditions. As a result, EV assembly lines increasingly depend on automated, torque-controlled, and sensor-enabled fastening systems, often integrated directly into robotic cells.

From a market standpoint, this segment delivers lower unit volumes but significantly higher value per tool, higher switching costs, and stronger customer lock-in. It represents the primary source of margin expansion and technological differentiation within the U.S. fastening tools market.

Beyond professional and industrial channels, the U.S. also has a large DIY power tools market, where fastening tools like cordless drills, impact drivers, and staplers represent a significant share of sales.

Although this segment is more volatile and consumer-driven, trends like:

• Home renovation popularity

• Rise of e-commerce tool retail

• Expanded hobbyist woodworking and home repair activities have broadened the total addressable market.

Aggregating multiple forecasts and applying regional weights:

• The U.S. fastening power tools submarket is expected to grow steadily, likely matching or exceeding the moderate global CAGR (≈ 5–7%) as construction and automotive sectors recover and innovate.

• Smart and connected tools represent the fastest-growing segment, with CAGRs approaching 10% through 2033, significantly above legacy tools.

• Hardware (fasteners) markets continue to expand at steady mid-single-digit rates ( ≈3–4% CAGR) tied to broad industrial output.

Overall, even conservative projections suggest that the combined U.S. fastening tools and fasteners ecosystem will continue to expand both in value and technological complexity, presenting opportunities for incumbents and new entrants alike.

The U.S. fastening tools market is structurally anchored to the country’s core economic engines—manufacturing, construction, and automotive production— which together account for trillions of dollars in annual output. With over US$2 trillion in construction spending and US$2.9 trillion in manufacturing value added, demand for fastening tools remains non-discretionary and resilient.

However, the market is increasingly divided. Traditional construction and legacy manufacturing sustain volume and replacement demand but offer limited margin growth. In contrast, high-precision manufacturing and electric vehicle assembly are redefining value creation, driving demand for automated, torque-controlled, and digitally integrated fastening systems. These applications deliver lower volumes but significantly higher value per tool and stronger customer lock-in.

Looking ahead, overall market growth is expected to remain steady, but competitive advantage will shift toward players aligned with complex, high-accuracy fastening environments. In the U.S. market, long-term success will be determined not by how many fasteners are installed, but by how critical precision, reliability, and traceability have become.

Germany’s home improvement market in 2025 stayed large, but demand was uneven and selective. The most reliable near-term demand proxy for fastening tools is the DIY and home improvement retail channel’s reported turnover. Through January to September 2025, that channel reported EUR 16.08 billion, down 1.4% year on year (like-for-like down 1.2%). The year did not deliver a clean rebound: Q2 turned positive, while Q1 and Q3 were negative.

For fastening tools, this pattern usually means essentials and consumables stay comparatively resilient, while discretionary upgrades and “nice-to-have” purchases remain under pressure. In parallel, official housing and construction indicators show early signs of improvement on permits and construction turnover toward late 2025. Those signals tend to influence fastening demand with a lag, meaning they are more relevant for 2026 planning than for explaining 2025 retail performance.

Retail sell-through matters because it captures what households and small trades are buying in real time. The latest publicly available 2025 update covers January to September.

The quarterly breakdown is the best way to understand how demand behaved:

• Q1 2025: EUR 4.57 billion, -4.0% year on year (like-for-like -3.5%).

• Q2 2025: EUR 6.47 billion, +1.2% year on year (like-for-like +1.4%).

• Q3 2025: EUR 5.04 billion, -2.3% year on year (like-for-like -2.2%).

• Jan–Sep 2025 total: EUR 16.08 billion, -1.4% year on year (like-for-like -1.2%).

This tells a practical story: demand activated in spring, but the market did not sustain momentum through late summer.

Fastening tool demand is not a single category. It is a chain of purchases that shifts depending on whether people are doing large renovations or small fixes. In a year like 2025, three demand layers matter:

Layer A:

Maintenance and replacement (most stable)

This is the everyday layer. People still need to mount, repair, replace, secure, and reinforce. Even when budgets tighten, this work does not disappear. This supports steady demand for:

• core screws, anchors, plugs, washers, brackets

• basic hand tools and small kits

• consumables such as bits, blades, and abrasives

Layer B:

Small projects and seasonal work (highly seasonal)

These are weekend and household projects that often activate in spring and early summer. Typical examples include fencing repairs, garden structures, outdoor fixtures, storage upgrades, and small carpentry. This layer supports demand for outdoor-rated fixings and corrosion-resistant hardware, plus the accessories that make work faster.

Layer C:

Big renovations and upgrade purchases (most volatile)

This layer drives the bigger baskets: multi-room upgrades, kitchens and bathrooms, flooring refits, large drywall work, and heavy structural improvements. It is also where discretionary power-tool upgrades happen. When the retail channel is down and choppy, this layer usually becomes selective. Many consumers either postpone, narrow scope, or trade down.

So the 2025 takeaway is that the mix likely leaned more toward Layers A and B, while Layer C remained cautious.

Fasteners and fastening tools are downstream of housing and construction. The official indicators help explain why 2025 looked selective at retail even as some upstream signs improved.

Housing completions weakened in 2024

Germany completed 251,900 dwellings in 2024, down 14.4% year on year. Completions matter because they trigger downstream spending: fit-outs, move-ins, and a wave of installation work.

Backlog remained substantial

At end-2024, the official backlog of approved but incomplete dwellings was 759,700, including 330,000 already under construction. A large backlog supports medium-term activity, but it can also signal that delivery is stretched and demand is spread out.

Permits are a leading indicator. In October 2025, permits were 19,900 dwellings, up 6.8% year on year. Over January to October 2025, permits totalled 195,400, up 11.2% year on year. This is constructive, but the demand impact typically arrives later via starts, completions, and trades activity.

Construction turnover turned positive

For October 2025, nominal turnover in the main construction industry was reported at EUR 11.6 billion, up 7.0% year on year, with real turnover up 4.5%. For January to October 2025, real turnover was up 1.8% versus the prioryear period.

These indicators help separate two realities:

• Retail demand in 2025 stayed cautious and seasonal.

• Upstream signals began to improve, supporting a more stable planning case for 2026.

Table 2. Housing and Construction Indicators Relevant to Fastening Demand

When growth is not broad-based, execution matters more than messaging.

Availability beats variety

In selective markets, shoppers are less patient. They want

the correct size, the correct anchor, and the correct tool accessory to finish a job. Out-of-stocks in core sizes can lose the entire basket, not just one item.

Promotions influence mix

A slightly declining market often triggers promotion intensity. That can move volume, but it changes what sells: buyers may shift to multipacks, entry-level ranges, or whichever accessory set is on offer. For suppliers, this makes forecasting by SKU more volatile than forecasting the overall category.

Small-basket behaviour increases

When consumers postpone bigger upgrades, they buy more frequently in smaller baskets. That supports steady unit movement in essentials, but it also increases the importance of packaging formats and shelf clarity. In fastening, the “search cost” matters. If selection is confusing, the customer either abandons or buys the simplest option.

Here are the 2025 implications that translate into concrete actions:

a. Treat consumables as your volume stabiliser

Bits, blades, anchors, and core fixings often provide the most predictable turnover in selective years. The priority is to protect service levels and reduce gaps in top movers.

b. Align assortment to common jobs, not only to categories

Retail customers do not think in “fasteners”. They think in tasks: mounting a TV, fixing a fence, hanging cabinets, repairing a hinge, reinforcing a joint. Packaging and planograms that map to jobs can lift conversion even in a soft market.

c. Improve the entry-to-mid ladder

When the market is cautious, many buyers trade down on big-ticket items while still buying reliable essentials. That is where mid-tier value positioning often outperforms premium-only positioning.

d. Expect uneven demand timing

The Q2 uplift in 2025 underlines how seasonal activation can still be strong even when the year-to-date headline is negative. Supply planning should focus on spring readiness for outdoor projects and maintenance spikes.

e. Watch upstream indicators for 2026 production planning

Permit improvement and construction turnover growth suggest the project-led layer could strengthen later. If that translates into activity, demand may shift toward larger trade packs, anchoring systems, and higherthroughput tool usage.

Given that the most recent published 2025 retail update covers only the first nine months of the year, this article does not present a full-year 2025 market size projection. Instead, the 2026 outlook is framed as the most likely direction based on the latest retail trend, housing pipeline signals, and construction activity indicators.

For 2026, the most likely outcome is a stabilising home improvement market, with demand shifting gradually from pure maintenance toward a higher share of project-led work as the housing pipeline improves. In this environment, fastening tools should track at least in line with the broader home improvement channel, with consumables and core fixings remaining the most resilient, and project-linked volumes recovering more slowly as renovation confidence returns.

• Expect steady baseline demand for essential fixings, anchors, and refills throughout the year.

• Plan for a firmer second half versus the first half, driven by gradual improvement in project timing and trades activity rather than a sudden market rebound.

• Prioritise range discipline and availability in core sizes and high-rotation accessories, because selective buying behaviour remains the defining feature even in a stabilising market.

Destatis: main construction industry turnover (2025).

Destatis: dwelling building permits (2025).

Destatis: housing completions and backlog (2024).

German DIY and garden retail trade association market reports (2024 results, 2025 updates).

Copyright owned by Fastener World / Article by Dr. Sharareh Shahidi Hamedani, UNITAR International University

Thailand’s industrial sector has long been a pillar of the nation’s economy, but its strength today lies not in isolated manufacturing firms but in intricate local and global supply chains that bind domestic producers to multinational investors. Over the past decade, foreign direct investment (FDI) has shaped how Thailand manufactures automotive parts, electronics, and high-tech components. These capital and knowledge flows have simultaneously bolstered productivity and exposed domestic manufacturers to external dependencies — both opportunities and vulnerabilities.

Thailand’s manufacturing sector is broad but concentrated in a few key component industries: automotive parts, electronics and electrical components, machinery, and increasingly, electric vehicle (EV) parts.

Industrial Manufacturing and GDP Contribution

Manufacturing has traditionally been a large share of Thailand’s economic output. Historically, manufacturing industry accounted for more than a third of GDP and employed a significant portion of the workforce, though the exact share fluctuates with economic cycles and global demand. The electrical and electronics (E&E) segment remains vital. For example, in 2024 Thailand’s electronics exports exceeded US$75 billion, with semiconductors alone contributing more than US$9.6 billion. The country now ranks among the top global producers of integrated circuits, with roughly 4% of global output, and is a major exporter of hard disk drives (HDDs).1

Thailand is Southeast Asia’s largest automotive manufacturing hub. In 2023 the automotive industry was valued at approximately US$12.67 billion, producing 2.55 million vehicles, a figure projected to rise toward nearly 3 million by 2028.

The domestic supply chain in this sector is deep:

• About 720 Tier-1 suppliers and 1,100+ Tier-2/3 firms operate locally, providing engines, chassis parts, electronics, and other critical components.

• Roughly 80% of vehicle components in Thailand are sourced locally, an unusually high localization rate for the region.

Yet the survival of this network depends on continuous integration with foreign multinational manufacturers, especially Japanese, European, and (increasingly) Chinese firms.

Thailand has aggressively courted foreign investment for decades, using targeted incentives and strategic industrial zones to attract capital and technology. The result: sustained growth in FDI into manufacturing and related supply chains.

In 2024: