This report ranks 200 of the world’s largest fashion brands on disclosure of their climate and energy-related policies, practices and impacts in their own operations & supply chains.

2025 EDITION

ABOUT FASHION REVOLUTION

Fashion Revolution works towards a vision of a fashion industry that conserves and restores the environment and values people over growth and profit. The Rana Plaza disaster in Bangladesh instigated the creation of Fashion Revolution and spurred millions to join our call for greater industry transparency and accountability in the fashion industry. Fashion Revolution has become the world’s largest fashion activism movement, mobilising citizens, industry and policy makers through research, education and advocacy work.

The issues in the fashion industry never fall on any single person or brand. That’s why we focus on using our voices to transform the entire system. With systemic and structural change, the fashion industry can lift millions of people out of poverty and provide decent and dignified livelihoods. It can conserve and restore our living planet. It can bring people together and be a great source of joy, creativity and expression for individuals and communities.

This report was researched and written by Fashion Revolution CIC. www.fashionrevolution.org

LEAD AUTHORS & RESEARCHERS

Liv Simpliciano

Ciara Barry

Delphine Williot

Isabella Luglio

Ysabl Dobles

Designed by Molly Porteous

Published in September 2025

JAN ROSENOW, PROFESSOR OF ENERGY & CLIMATE POLICY, UNIVERSITY OF OXFORD

ELECTRIFYING FASHION: HOW TO PHASE OUT FOSSIL FUELS IN THE TEXTILES INDUSTRY FOREWORD

We all use textiles every single day: think of the clothes we wear, the sofas we sit on, and the beds we sleep in. But few people know that making those textiles is based on burning vast amounts of fossil fuels. That has to fundamentally change in a net-zero world. But how?

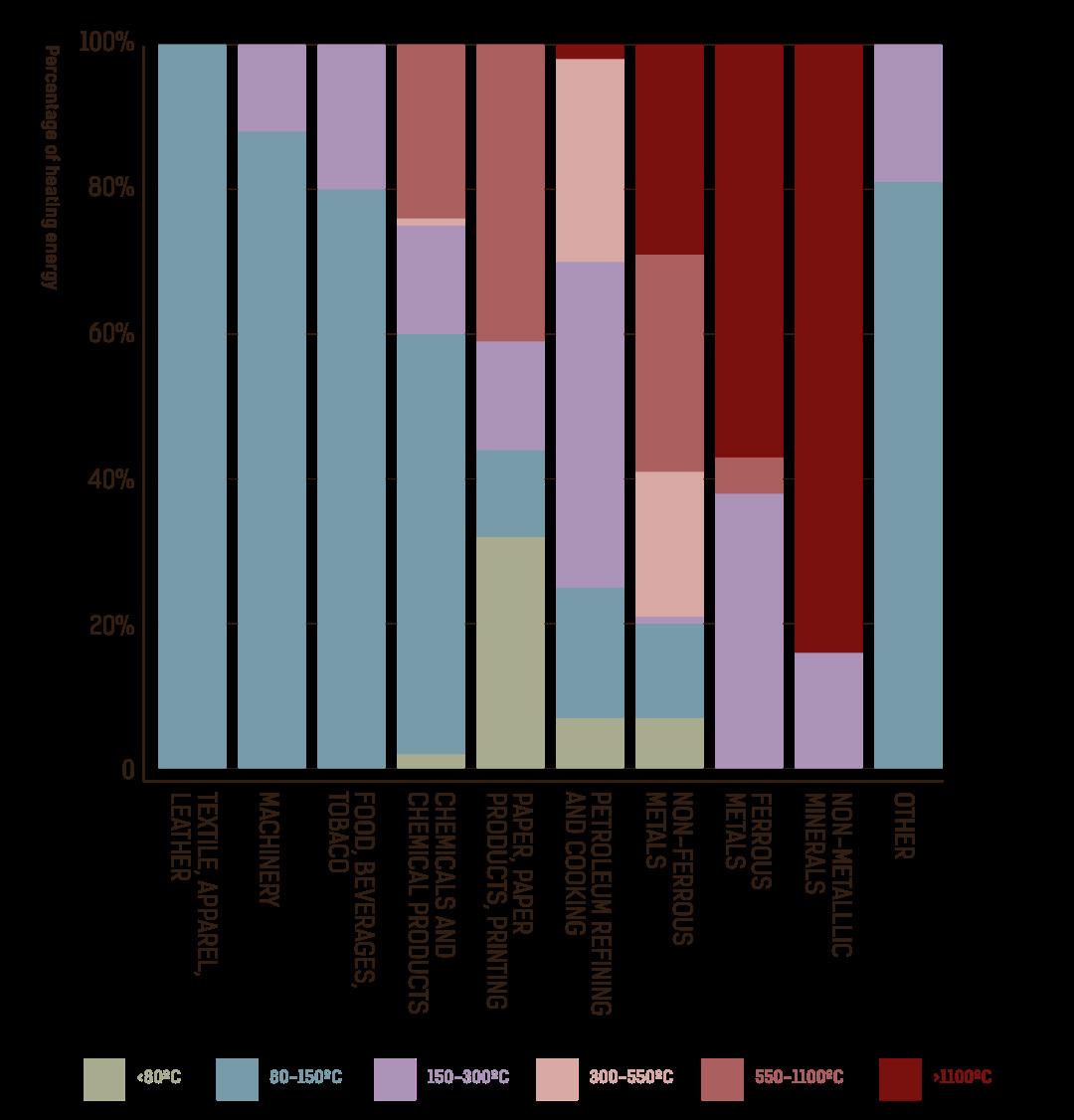

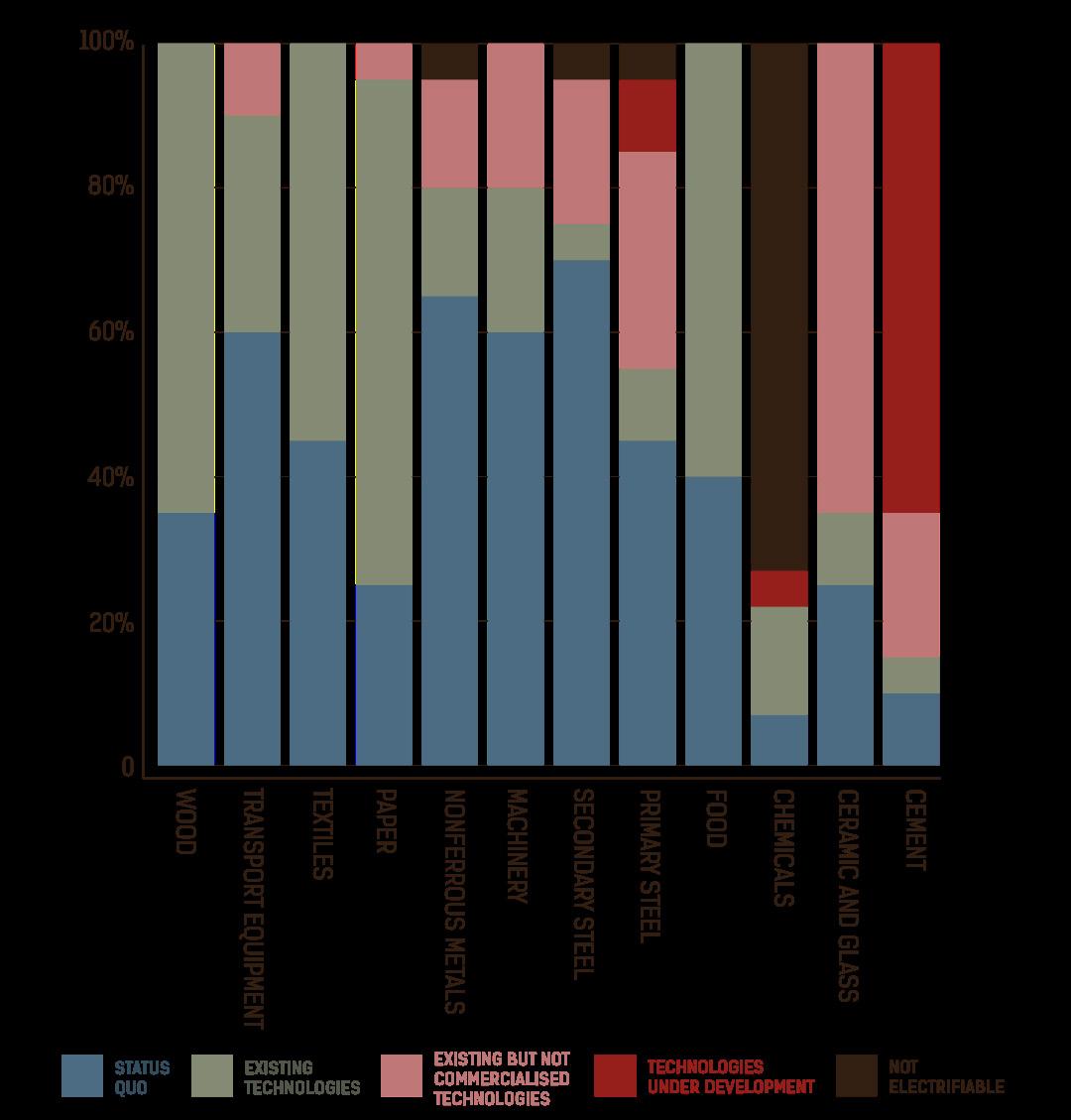

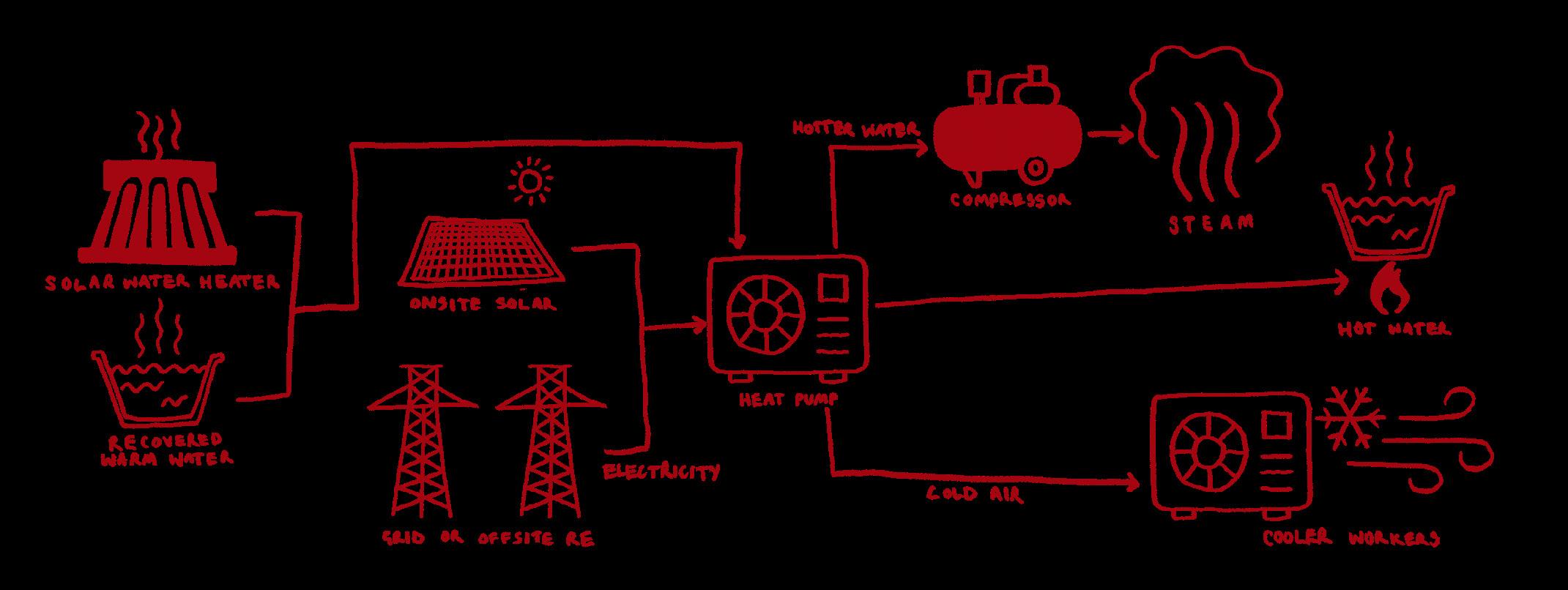

One of the most promising levers for phasing out fossil fuels in the textiles industry is the electrification of processes that currently use fossil fuels. Processes such as dyeing, printing, drying, washing and bleaching require large quantities of heat, and that heat can be provided with technologies such as heat pumps, electric boilers and heat batteries using electricity from clean power sources like solar and wind. This stops the use of fossil fuels and reduces carbon emissions but also improves air quality and reduces noise. Clean heat solutions therefore have the potential to improve worker safety and address overheating in factories. This means that electrification is not just a climate solution; it can also contribute to safer working environments and cleaner air for surrounding communities.

The potential for electrification of process heat in the textiles industry is very large: up to 100% of process heat used in the textiles sector can technically be provided with existing technologies. This is because the temperatures typically required in the textiles sector are comparably low and top out around 250 degrees Celsius. The main challenge is to move from potential to practice.

Historically, companies decided to use fossil fuels because they were readily available and often cheaper than using electricity. This puts the onus on governments to act and ensure that electrification is cost-competitive through clever taxation of energy and financial support programmes. More and more countries have started to understand this and changed policy. Companies that decide to transition would then see economic benefits rather than paying a premium.

But companies also have their work cut out: There are already technologies out there that can compete with fossil fuels. But it requires a clear strategy, a closer look at the options and a roadmap for a transition away from fossil fuels. Some corporates made inroads already and

have demonstrated what is possible. Leading by example rather than being dragged towards cleaner production pays off: Businesses along the supply chain and consumers pay increasing attention to the climate impact of the products they buy. Those companies that can demonstrate cleaner production methods may be able to charge a green premium for their products. Although not applicable to the fashion industry yet, new policies and regulations, such as the European Union’s Carbon Border Adjustment Mechanism (CBAM), make it less and less attractive to import carbon-intensive products as those face higher carbon taxes. This emerging policy landscape underscores the urgency for fashion to decarbonise heat and power now, before regulation and market forces leave no room for inaction.

Electrification is not just a climate solution, it can also contribute to safer working environments and cleaner air for surrounding communities

Finally, in a world of poly-crises and geopolitical tensions, relying on fossil fuel imports that are subject to increasingly volatile market prices is a risky strategy.

Electrification of the textiles sector offers a path towards more energy security and less dependency on imported fuels, the price of which is outside the control of individual countries or companies. We see more and more companies across sectors investing in on-site renewable electricity generation or contracting with renewable energy generators directly. Without similar investment, fashion’s reliance on fossil-powered heat will leave suppliers exposed to rising costs and supply disruptions.

Industrial electrification presents a tremendous opportunity for the textile sector. It is now up to policymakers and companies to make it a reality – let’s make it fashionable to electrify fashion.

GLOSSARY

24/7 HOURLY MATCHING

24/7 hourly matching ensures every hour of electricity usage is paired with locally or regionally sourced carbonfree generation, precisely aligning consumption with renewable production to reduce emissions.

ANNUAL MATCHING

Annual matching involves aligning a company’s yearly electricity use with renewable sources, but it may not fully decarbonise the grid due to timing mismatches between renewable availability and actual consumption, leading to lower emission reductions compared to hourly matching.

CARBON FOOTPRINT

This measures the total amount of carbon dioxide (CO2) emissions produced by an individual, organisation, or activity, typically through the burning of fossil fuels. It helps gauge the impact of these activities on climate change.

CLEAN HEAT

The use of truly renewable sources like wind and solar to meet manufacturing’s thermal energy demand, through solutions such as electric boilers and heat pumps.

CLIMATE ADAPTATION

Adaptation involves adjusting practices, processes, and systems to reduce the adverse impacts of the climate crisis. For example, developing supply chains that are resilient to climate hazards, such as installing flood defences in a factory.

CLIMATE MITIGATION

Mitigation refers to actions taken to reduce or prevent the emission of greenhouse gas. This can include measures like switching to renewable energy and improving energy efficiency

DEGROWTH

Degrowth challenges the paradigm of unlimited economic growth by advocating for a socially just and ecologically sustainable society. It promotes reducing global consumption and production, emphasising well-being over material accumulation and advocating for equitable distribution of resources.

ENERGY PROCUREMENT

How brands and retailers buy and report their energy — through tools like Renewable Energy Credits, Power Purchase Agreements, or onsite generation — which determines whether their renewable energy strategies deliver real carbon reductions.

GLOBAL MAJORITY

Refers to most of the population of the world that live in what is often referred to as ‘developing countries’ or ‘the Global South’. It recentres Black, Indigenous and People of Colour (BIPOC) as the majority, moving away from the minoritisation experienced in white supremacist and colonial history and culture.

GLOBAL MINORITY

Refers to the smaller population of the world that live in wealthier nations, often described as ‘the West’ or ‘the Global North’.

GRIDS

The backbone of electricity systems, responsible for transporting power from generation sources to end-users like garment factories. Some grids run on clean energy like wind and solar, some depend on dirty fossil fuels or a mix of both. Upgrading and expanding grids is vital to meet demand and power the clean energy transition.

JUST TRANSITION

A fair shift to a low-carbon fashion industry that puts garment workers at the centre of decisions about brand decarbonisation efforts that impact them. Workers, through their unions, co-design solutions that protect their jobs, wages, health, and communities. This includes the right to organise, bargain collectively, and engage in genuine dialogue with brands and suppliers. Brands must share the costs of decarbonisation instead of pushing them onto workers or suppliers, ensure living wages, and invest in protections suited to local contexts so no one is left behind.

CARBON OFFSETTING

Carbon offsetting is when companies compensate for their carbon emissions by investing in external projects that reduce or sequester GHGs, such as reforestation or renewable energy. While it allows companies to claim ‘carbon neutrality’, it often does not address the emissions produced directly within their own operations and can be controversial due to issues like doublecounting and the effectiveness of the projects.

CARBON PRICE

The cost assigned to each unit of carbon dioxide or its equivalent emissions, either through a carbon tax or the price of emission permits in carbon trading schemes. This price varies across different carbon trading systems globally and reflects the effort needed to mitigate climate change impacts.

RENEWABLE ELECTRICITY

Renewable electricity is power generated from sustainable sources like wind, solar, and hydro, which naturally replenish and have minimal environmental impact.

RENEWABLE ENERGY

Renewable energy comes from natural sources that are replenished faster than they are consumed, like sunlight and wind. It produces significantly lower emissions than fossil fuels, making it essential for combating climate change. However, not all renewable sources are entirely green or clean if they generate some emissions or environmental harm.

SCOPE 1 EMISSIONS

Scope 1 emissions are direct greenhouse gas emissions from sources that are owned or controlled by an organisation, such as emissions from fuel combustion in company-owned vehicles and facilities.

SCOPE 2 EMISSIONS

Scope 2 emissions are indirect greenhouse gas emissions from the generation of purchased electricity, steam, heat, or cooling consumed by the organisation.

SCOPE 3 EMISSIONS

Scope 3 emissions are all other indirect greenhouse gas emissions that occur in the value chain of the organisation, including both upstream (related to purchased goods and services) and downstream (related to sold goods and services) emissions.

THERMAL ENERGY

Heat used in factories to dye, wash, and dry clothes. In fashion, it is often generated by burning fossil fuels on site.

EXECUTIVE SUMMARY

INTRODUCTION

Fashion’s climate targets are falling dangerously out of step with reality. Instead of cutting emissions at the pace science demands, billion-dollar fashion brands are dragging their feet, withholding even the most basic data, all while emissions continue to soar.

Overproduction, fuelled by the industry’s pursuit of profit, is sacrificing a livable planet for garments too often treated as disposable — a throwaway culture that treats our shared home the same way.

The pressures of overproduction come into focus in Tier 2 processing facilities, hotspots of emissions and worker risk. These are the dye houses, laundries, and finishing mills where the fabrics of our clothes are made. Here, meeting demand means burning vast amounts of fossil fuels to generate heat for fabric processing. The result is toxic air inside factories and surrounding communities, overheated workplaces, and the single largest share of fashion’s emissions, alongside the industry’s toughest decarbonisation challenge.

Fashion’s climate future will be decided by how the industry tackles heat: ending its reliance on fossil fuels in manufacturing and scaling up clean heat — renewable, fossil-free energy for manufacturing processes.

Fashion’s climate future will be decided by how the industry tackles heat

The technologies needed to replace fossil fuels in production already exist (like heat pumps and electric boilers) and have the potential to offer a twofold benefit: cutting emissions at scale while addressing workplace and environmental harms. Electrification could lower indoor factory temperatures, reduce workers’ exposure to heat stress, and clear the air, contributing to safer conditions inside factories and in surrounding communities.

But technology alone is not enough. The climate crisis is also an inequality crisis: brands’ business models in the Global Minority drive emissions, while garment workers in the Global Majority face unsafe heat, polluted air, and unstable livelihoods on poverty wages. A Just Transition means workers and suppliers must not be left behind — brands must share the costs of decarbonisation, enable living wages, and engage in genuine social dialogue with unions and suppliers. Without this, clean heat risks replicating the same extractive patterns that created the crisis.

Underpinning the urgency of the transition is the reality that progress is stalling. After nearly a decade of pressure, transparency on suppliers’ list has plateaued. Without visibility of where production takes place, brands cannot map emissions hotspots or plan collective investments in clean heat. This roadblock exposes the limits of voluntary action — and comes just as EU Omnibus proposals threaten to weaken corporate accountability by limiting due diligence to Tier 1 suppliers and making climate transition plans optional. The potential rollbacks will keep Tier 2 — the greatest emissions hotspot — in the shadows, slowing electrification, leaving workers exposed and derailing climate progress.

The technologies needed to replace fossil fuels in production already exist and have the potential to cut emissions at scale while addressing workplace and environmental harms

The fashion industry has the chance to electrify much of its low-temperature processing now. Paired with renewable energy, this is low-hanging fruit for decarbonisation. If fashion fails to seize the clean heat opportunity, the industry risks losing credibility in a world moving beyond fossil fuels — and compromising the health, safety, and dignity of the people who make our clothes.

This report proposes a framework for industry adoption created by Fashion Revolution and climate campaigning organisation Action Speaks Louder. ‘ Clean Heat for Cool Work ’ is a scalable solution to address fossilpowered heat on two fronts: (1) continuous, low-cost monitoring and disclosure of factory heat and humidity data to help protect workers from unsafe heat now, and (2) investment in clean heat technologies like electric boilers and heat pumps powered by renewables to replace fossil fuels. Together, these tracks demonstrate how adaptation (protecting workers from heat stress and harmful air pollution) and mitigation (cutting fossil fuel use and greenhouse gas emissions) can reinforce each other when advanced together by brands who commit to paying their fair share. By acting now, fashion can lead an industrial decarbonisation revolution that delivers both climate action and safer conditions for the people who make our clothes.

KEY FINDINGS

Fashion fails to act on its most urgent decarbonisation opportunity: clean heat.

Fashion’s reliance on fossil-fuelled heat in dyeing, finishing, and processing facilities is the single largest source of supply chain emissions — and it is where urgent action is needed. Proven technologies like heat pumps and electric boilers are already available to replace fossil fuels, making this the industry’s most pressing and actionable decarbonisation challenge. Unlike heavy industry, fashion faces relatively low technical barriers to electrification. Research consistently shows that heat needs up to 150°C can already be electrified today using existing technologies and that process heat rarely exceeds 250°C, meaning the industry has the potential to move entirely away from fossil fuels. And yet, a mere 6% of brands disclose any efforts to electrify high-heat processes. Furthermore, only 10% of brands disclose supply chain renewable electricity targets, and just 6% disclose broader renewable energy targets, a serious shortfall. Without electrification, renewable targets risk being weak and ineffective as brands may lock in biomass or other stopgap solutions. Even if electricity is renewable, heating, cooling, and steam can still run on coal or gas. Decarbonisation therefore requires a comprehensive plan covering both power and heat. By failing to act, fashion’s billion-dollar brands are not only slowing progress — they are overlooking the industry’s clearest opportunity to cut emissions rapidly.

Brands’ coal phase-out targets stop

short: none include purchased steam, leaving coal embedded in

supply chains.

Less than a quarter of Big Fashion 1 brands (18%) disclose coal phase-out targets at the processing level, and the failure to cover purchased steam shows a lack of ambition. Many factories buy steam from nearby coalfired combined heat and power plants or district heating systems — meaning they can claim to be “coal-free” on-site while still relying on coal indirectly. Including purchased steam in a coal phase-out target closes this major loophole. By covering purchased steam, brands ensure their commitments tackle all coal-derived heat in production — not just what’s burned on their own premises – driving real emissions cuts and preventing coal use from being outsourced. Without closing this gap, coal can disappear from factory boilers yet still power production through external suppliers — keeping fashion locked into fossil fuels. Crucially, if multiple brands demand action on purchased steam, it could shift the equation entirely: collective pressure would create the leverage needed to push industrial zones to invest in cleaner infrastructure. While individual brands often claim they lack influence as “one buyer among dozens”, coordinated demand and financing are exactly what is required to unlock this transition.

Show us the money: Almost no brands disclose how they are funding decarbonisation or suppliers’ rising costs.

Brands set ambitious supply chain decarbonisation targets, but most stop short of showing how they support suppliers to deliver them, making financing the transition a guessing game. Only 6% disclose upfront (CapEx) support — for example supporting suppliers to replace coal-powered boilers with electric ones or heat pumps — and just 2% disclose help with ongoing (OpEx) costs such as renewable electricity bills or equipment maintenance. Without brand financing, suppliers cannot absorb the million-dollar costs of switching from coal to clean heat, leaving climate targets hollow.

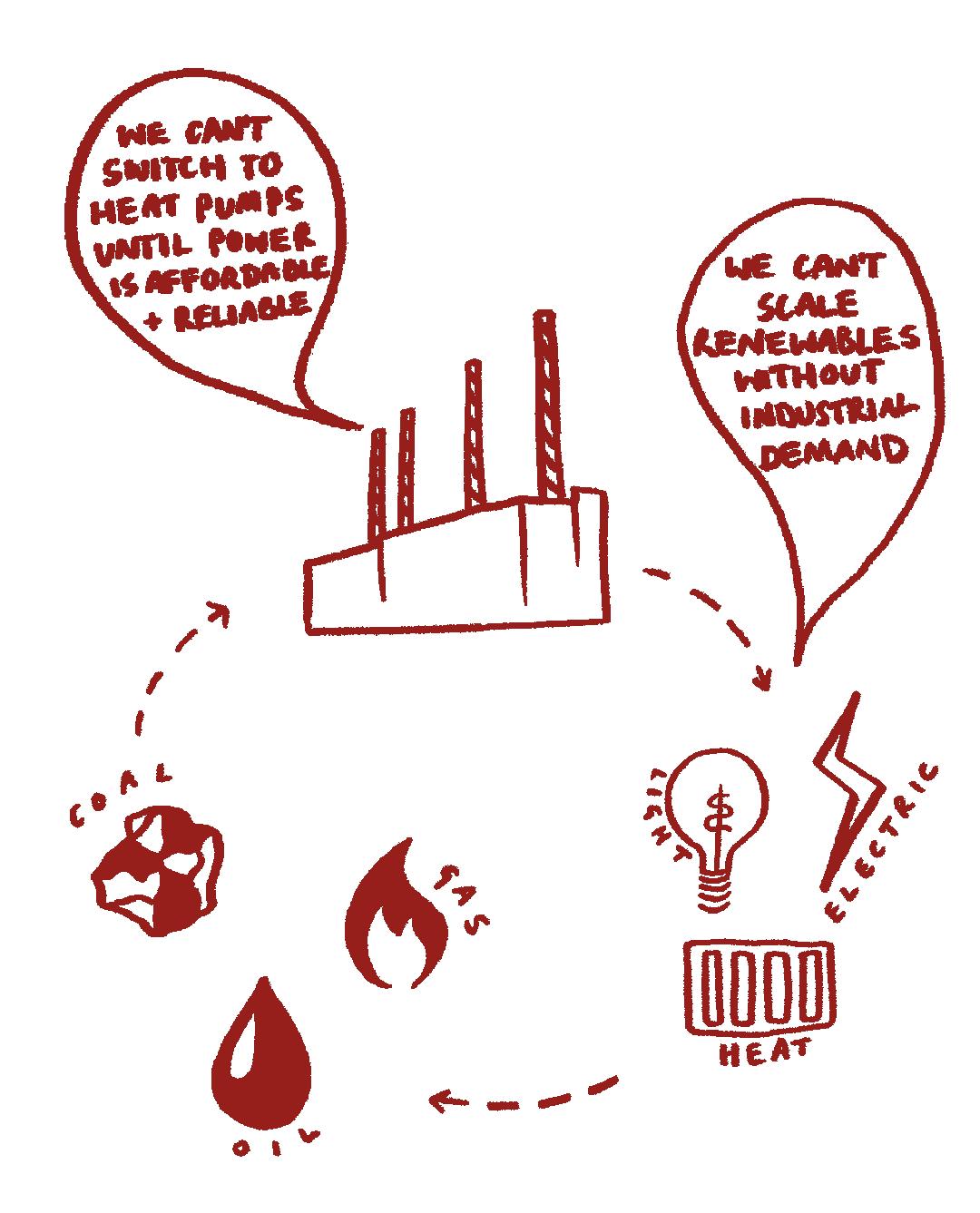

This creates a chicken-and-egg problem: suppliers are reluctant to electrify if the grids remain fossil-fuel heavy, while governments and utilities hesitate to invest in renewable infrastructure without clear industrial demand. Brands sit at the centre of this deadlock. On-site action is important, but without cleaner grids, electrified equipment may still run on coal or gas. This is why grid advocacy is essential — especially in countries where fashion is one of the largest export industries. When brands signal collective demand, they can help unlock renewable investment at the level required to drive the transition forward.

Breaking this cycle means brands must act on three fronts simultaneously: financing supplier electrification (e.g. replacing coal boilers with electric heat pumps), investing in or securing long-term power purchase agreements with renewable projects in production hubs, and using their influence to support national renewable energy scale-up. Doing this through a Just Transition lens — sharing costs, protecting jobs, and ensuring no community is left behind — will not only accelerate decarbonisation but also strengthen supply chain resilience.

1

Accounting, not accountability: Energy credits will not decarbonise supply chains.

60% of brands disclose energy sourcing in their own operations, but just 11% in supply chains, where it matters most. Many lean on Renewable Energy Credits (RECs) which mask fossil fuel use, making climate action for many brands an exercise in accounting, not accountability. Accounting fixes cannot replace true decarbonisation. To make this shift, brands must power supply chains with real-time renewable energy — not just on paper. Unlike annual or monthly accounting, 24/7 matching ensures consumption is met with clean generation each hour, sending a strong demand signal to decarbonise grids and cut reliance on fossil fuels. Yet with no brand disclosing this approach, the industry is lagging behind this urgent priority.

Billion-dollar brands fail to leverage their purchasing power for decarbonisation.

Fashion demands suppliers decarbonise, yet most brands do little to enable the structural change needed to make that transition possible. Expecting suppliers to decarbonise without advocating for structural change is self-defeating — it undermines brands’ own climate commitments. Only 7% of brands disclose evidence of renewable energy political advocacy in garment-producing countries, and just 2% report outcomes. Even fewer (6%) disclose direct investment in grid-scale renewable energy projects. Given their influence, brands have both an imperative and an opportunity to help shape enabling environments — from policies that let factories sell unused renewable power back to the grid (net-metering) and lower import duties on green technologies, to enabling power purchase agreements and phasing out coal. Supporting grid decarbonisation does not just help suppliers meet targets; it raises the floor for all industries and positions fashion to lead in driving collective climate progress.

Publicly-listed companies make up the majority (59%) of brands scoring zero on traceability — exposing a glaring accountability gap in ESG oversight.

Despite being answerable to shareholders and subject to sustainability reporting frameworks, many of the world’s biggest listed fashion companies are failing at the most basic level of supply chain transparency. This lack of disclosure prevents investors and stakeholders from assessing whether brands are phasing out coal, electrifying factories, or protecting workers from mounting heat risks. In short, fashion’s transparency plateau has become a direct climate action roadblock: without supplier visibility, credible decarbonisation is impossible.

Unprepared

for the future: almost half of big brands fail to disclose climate risks to their operations and supply chains.

Fashion supply chains are already being disrupted by the climate crisis , from floods and droughts to escalating heatwaves. For major brands and retailers, understanding these environmental risks and their financial implications is essential to future-proofing business. Yet, a little more than half (57%) of brands provide details of their climaterelated risks.

Beyond the moral imperative to do so, the fashion industry must gain an in-depth understanding of climate-related risks which in turn would support their strategy to reduce their greenhouse gas emissions (mitigation) and build resilient supply chains able to navigate the impacts of the climate crisis such as extreme heat and floods (adaptation). Climate risks directly affect productivity, supply chain stability, and operational costs — factors that are material to investors. Without this data, business resilience and investor confidence is undermined as they are left unable to assess risks that fall squarely within their fiduciary duty to consider. At a time when environmental and human rights due diligence rules are being weakened globally, visibility of these risks is more important than ever: not only to protect workers and supply chains, but to give investors the information they need to make sound financial decisions.

Big

Fashion needs a temperature check: the industry’s hottest climate risk is going unmeasured, with workers’ health and livelihoods on the line.

0% of brands disclose factory data on heat and humidity levels (also known as Wet Bulb Globe TemperatureWBGT), even as extreme temperatures leave garment workers fainting, falling ill, and losing income as productivity drops. Heat stress is not only a human rights issue but also a financially material risk for investors: economy wide, by 2030, global productivity losses are projected to reach $2.4 trillion annually, equivalent to 80 million jobs lost . For the fashion industry, the impact is acute. Cornell’s Hot Air report shows that in garment manufacturing hubs like Karachi and Phnom Penh, workers already face ~112–115 unsafe WBGT days each year — nearly one-third of the year in extreme heat, with serious consequences for both wellbeing and output. Public WBGT disclosure would give unions the evidence to bargain for protections, inform brands of the costs of adaptation like cooling systems, provide investors with a decision-useful metric to assess financial and operational risks, and unlock adaptation tools like parametric insurance. Without it, heat protections cannot be embedded into binding mechanisms like the International Accord, leaving workers unfairly exposed.

Fashion’s governance model remains profit-first, sidelining climate action even as risks escalate.

CEO pay continues to soar — up 23.5% on average for the 25 highest-paid US fashion executives — while only 15% of brands disclose whether bonuses are linked to absolute carbon reduction, and most of those tie just 10% of pay to climate performance. A slightly higher share (20%) discloses supplier incentives for decarbonisation, but power imbalances mean responsibility still falls on suppliers rather than brands. Investors, too, are missing a crucial opportunity: just 7% of brands disclose an internal carbon price, leaving fashion far behind other sectors in embedding climate accountability into financial decision-making. In addition, with the rise of climate skeptics politics, we are seeing a rollback on environmental legislation globally, with legislation such as the Corporate Sustainability Due Diligence Directive (CSDDD) being heavily watered down to remove the obligation to put climate transition plans into effect while the Trump administration wants to eliminate regulation for greenhouse gases – ultimately supporting the short term financial interests of big lobbies over people and the planet.

Emissions reduction and partnership — missing in action for the majority

Just over half of brands (55%) disclose having a ScienceBased Targets initiative (SBTi)-verified target that covers Scopes 1–3. However, fewer than a third (29%) provide evidence that they have actually reduced their greenhouse gas (GHG) emissions from the baseline. With only 20% of brands disclosing that they consult suppliers on their climate targets and just 9% disclose co-creating climate adaptation solutions, brands’ failure to work in genuine partnership is one factor stalling climate progress. Cocreating strategies with suppliers — who are experts in their own local context — would make decarbonisation and adaptation plans stronger and supply chains more resilient to climate shocks. Yet, very few brands are transparent about taking this approach.

Ownership Matters: Brands with skin in the game can drive decarbonisation.

Just a quarter of brands at the manufacturing level (23%) and 19% at the processing level disclose supply chain ownership. Even more telling is that among brands disclosing this information, levels of ownership are minimal: more than half report owning no manufacturing (62%) or processing (68%) facilities.

Brands with higher ownership levels are better placed to invest in renewable energy, pilot clean heat technologies, and coordinate adaptation strategies because they offer greater stability. By contrast, brands that rely on short-term contracts with opaque supply chains lack both visibility and leverage to deliver decarbonisation. Achieving real progress will require brands to move beyond extractive, short-term profit supply chain models and actively invest in stable, longer-term supplier partnerships. These relationships create the trust and stability required to share investment, accelerate the renewable energy transition, and deliver on broader climate goals.

RECOMMENDATIONS

MAJOR BRANDS AND RETAILERS, MUST:

• Electrify heat at scale. Replace coal, oil, and gas boilers with proven technologies like heat pumps and electric boilers, starting with pilot projects in brands’ own supply chains— even on fossil-heavy grids — to cut emissions today, build evidence across geographies, and de-risk wider adoption. Pair this with time-bound supply chain targets for 100% renewable power, full public disclosure, and prioritisation of truly renewable sources like wind and solar — not biomass or other stopgap fuels.

• Break the chicken-and-egg cycle. Finance supplier electrification, secure renewable power through Purchase Power Agreements (PPAs) or direct investment in new renewable projects, and use brand influence to advocate and co-fund systemic reforms that decarbonise factories and national grids.

• Implement continuous WBGT monitoring. Brands must roll out low-cost, continuous monitoring of heat and humidity in supplier factories — with workers and unions leading the process. This simple measure generates decision-useful data, ensures accuracy, and creates credible baselines for adaptation tools like parametric insurance.

• Guarantee fair and stable purchasing. Provide long-term, stable orders and fair contracts that give suppliers the security to invest in decarbonisation — instead of pushing costs down the chain.

• Enable living wages. Ensure workers and their unions can collectively bargain for living wages — the most effective adaptation strategy — giving communities resilience to withstand shocks and the agency to shape their own futures.

• Put worker-led due diligence at the centre of decarbonisation. Uphold freedom of association and collective bargaining, embed worker-led monitoring and meaningful social dialogue, and support protections designed with local communities — backed by binding agreements and jointly governed funds — so no one is left behind in the transition.

• Go beyond compliance. Align business practices with international climate and human rights standards, and adopt risk-based due diligence across all tiers — with priority on high-risk sites like dyehouses and finishing plants — ensuring workers and unions are central to defining and monitoring the most salient risks.

INVESTORS AND SHAREHOLDERS MUST:

• Pressure brands on heat risk. Press for continuous disclosure of factory heat and humidity levels (WBGT), with worker-led monitoring to ensure accuracy. This low-cost measure generates decision-useful data on productivity losses that are financially material, while enabling unions to bargain for safer conditions and unlocking adaptation tools like parametric insurance.

• Make clean heat a transition indicator. Use shareholder leverage to push brands to electrify all thermal processes with proven technologies like heat pumps and electric boilers.

• De-risk supplier investment. Use credit guarantees and blended finance tools to unlock capital for clean heat and renewable energy in fashion’s supply chains.

CITIZENS MUST:

• Use this research to inform your activism, not your consumption. Scrutinise brand claims and hold them to account.

• Demand worker protections. Push brands to disclose data on factory heat and humidity levels (WBGT) and address unsafe heat facing the people who make our clothes, and ensure that unions and communities have a central role in defining and addressing unsafe heat.

• Stay informed on policymaking. Understand how supply chain accountability, renewable energy access, and worker protections are shaped by regulatory debates — and scrutinise corporate lobbying that seeks to weaken them.

JOURNALISTS, ACADEMICS AND CIVIL SOCIETY MUST:

• JOURNALISTS

Platform workers’ voices. Expose the gap between brand claims and on-the-ground realities, spotlight workers facing heat stress and unsafe conditions, and report on lobbying efforts (e.g. Omnibus, CSDDD rollbacks) that undermine climate and labour rights.

• ACADEMICS

Provide independent evidence. Generate peerreviewed data on clean heat adoption, worker health impacts, and emissions reductions; translate complex technical findings into accessible insights for policymakers, investors, and the public; and ensure research actively incorporates worker and community perspectives on due diligence priorities.

• CIVIL SOCIETY

Advocate, mobilise and hold to account. Amplify unions and grassroots organisations, monitor whether brand commitments (coal phase-out, renewable targets, Just Transition plans) deliver in practice, and scrutinise government and corporate actions that shape regulatory frameworks. Leverage advocacy and campaigning strengths to ensure clean heat remains a priority — highlighting its dual potential to deliver major emissions reductions and protect workers from unsafe heat. Push to expand the International Accord to explicitly cover unsafe workplace heat, with worker-led monitoring of WBGT and factory conditions — particularly for brands with seats on the Accord steering committee.

ROLE AND AIMS OF THE REPORT

INTRODUCTION

This year, What Fuels Fashion? will aim to:

• Expose fashion’s dependence on fossil-fuelled process heat.

• Spotlight clean, electrified heat as the industry’s most urgently needed response to decarbonisation.

• Demonstrate that industrial electrification has the potential to deliver a dual solution: reducing greenhouse gas emissions (mitigation) and improving working conditions on the factory floor by protecting workers from heat stress and reduce harmful air pollution inside factories and in surrounding communities (adaptation).

• Push the world’s biggest fashion brands to phase out coal in supply chains and invest in scalable, electrified alternatives like heat pumps and electric boilers.

• Provide policymakers, investors, trade unions, and campaigners with the data needed to demand brand accountability and drive industrial electrification where it matters most — at the energy-intensive processing stage.

• Highlight heat stress as a frontline human rights and climate risk – recognising it as defined by workers themselves - and show that a credible Just Transition depends on worker-and communityled due diligence, underpinned by Freedom of Association and meaningful social dialogue.

• Raise public awareness of clean heat as fashion’s overlooked climate opportunity and build collective pressure so that brands act now, rather than waiting for fully decarbonised grids.

• Drive scrutiny, accountability, and systemic change by ranking 200 billion-dollar fashion brands on their transparency, revealing who is leading and who is lagging behind the clean heat transition.

Fashion Revolution began researching transparency eight years ago. Since then, the climate crisis has intensified and so has the cost of inaction. Today, the industry’s lack of transparency on climate and energy use is a direct barrier to decarbonisation and accountability.

Without visibility into how factories are powered, how much coal is being burned, or what conditions workers are experiencing on overheated factory floors, brands cannot credibly phase out fossil fuels, electrify supply chains, or deliver a Just Transition. Clean heat and industrial electrification are possible, but without disclosure, progress cannot be measured and responsibility cannot be enforced.

Despite mounting public pressure, much of the global fashion industry remains opaque. This opacity conceals continued reliance on coal and other fuels (like gas and biomass), obstructs accountability, and delays both mitigation and adaptation – from phasing out fossil fuels to protecting workers from dangerous heat stress.

Transparency is not a radical demand – it is the bare minimum. It is the first step toward climate accountability and a Just Transition. With transparent data, workers, communities, policymakers, investors, and civil society can hold fashion’s biggest brands accountable and push them to act at the speed and scale the climate crisis demands.

TRANSPARENCY

SCRUTINY

ACCOUNTABILITY

CHANGE

THE SCOPE OF OUR RESEARCH

REFINING OUR FOCUS: UPDATED BRAND SCOPE FOR 2025

We have updated the scope of brands included in our research through a strategic and data-led process.

Since our first edition, we have focused on evaluating fashion brands with an annual turnover of at least USD $400 million, measured at either the brand level or parent company level. For privately held brands, we have relied on the best available public data to estimate turnover.

In late 2024, we contacted the 250 brands2 included in the previous edition of WFF, asking for updated information on:

• Annual turnover (at brand or group level), with publicly available sources if possible.

• If reporting at group level, whether the group is primarily focused on apparel retail.

• For diversified companies (e.g. supermarkets), a breakdown of how much turnover is attributable to apparel, footwear, garments and/or textiles. Example: “Total turnover: £2bn, ofwhich approximately£500m (25%) is apparel.”

We recognise that privately held brands may not wish to disclose exact figures. In these cases, we encouraged brands to share a turnover range (e.g. £100m–£500m) or confirm whether turnover exceeds £5 billion. Where no data was provided, we used public sources to assess eligibility.

After reviewing brand responses and conducting our own research, we refined our focus for the 2025 edition. This year, we are focusing on 200 of the world’s largest fashion brands with a turnover of USD$1 billion. Our updated scope prioritises brands that are primarily apparel retailers, or where apparel makes up a significant proportion of overall revenue.

This shift allows us to:

• Prioritise brands with the greatest resources and responsibility to lead on climate and energy transition.

• Streamline our analysis to focus where the impact can be greatest.

• Dedicate more time to deep-dive research and sharper advocacy.

Together,

the 200 brands now in scope have a combined estimated turnover of approximately USD $2.7 trillion.3

By narrowing our lens, we strengthen our ability to hold the industry’s most powerful players accountable and push for urgent action where it is needed most.

Our research focuses on what brands choose to publicly disclose. Public self-disclosure matters because it creates accountability: data that is transparent, specific, and accessible can be used by workers, unions, policymakers, investors, and civil society to drive change on climate and human rights in fashion’s supply chains.

2 Fashion Revolution contacted all brands previously in scope of our research. Where brands did not respond, we relied on the most recent publicly available data to assess their eligibility for inclusion. Some brands contacted Fashion Revolution after the research began, including s.Oliver and Tom Tailor, who both fall below the USD $1bn threshold and therefore outside the formal scope. Both brands were invited and chose to voluntarily participate in the consultation and review process.

3 To calculate this figure, we summed the publicly available annual turnover data for each brand. If multiple brands belonged to the same parent company, we counted the parent company’s turnover only once to avoid double counting. All turnover figures in non-USD currencies were converted to USD using the United Nations Operational Rates from July 2025.

Public self-disclosure

What Fuels Fashion? evaluates what brands publicly self-disclose about their decarbonisation efforts in their operations and supply chain.

Verification of Claims

Points are awarded only for publicly disclosed information/data on major brands’ policies, procedures, performance, and progress on decarbonisation efforts across the value chain.

Up-to-date information

Most of our research indicators are timesensitive, and we only consider disclosure that has been published January 2022 or later.

Accepted Sources for Public Disclosure

Public self-disclosure

What Fuels Fashion? does not measure a brand’s decarbonisation impacts; it measures public disclosure.

Verification of Claims

Verification of claims made by brands and retailers is beyond the scope of this research. However, stakeholders are encouraged to use our research to hold brands accountable for their claims.

Up-to-date information

This does not apply to disclosure that is not timesensitive (e.g. we will allow relevant policies and commitments published before this date if they still apply and are publicly disclosed).

We award points only for information/data that has been publicly disclosed on the brand or parent company’s own website (or directly linked to it).

We review information which is publicly available from one of the following places:

• On the brand or parent company’s website

• Sustainability microsites (provided there is a direct web link to it from the main brand or parent company website)

• In annual reports or annual sustainability reports published on the brand or parent company website

• In any other documents which are publicly available and can be downloaded freely from the brands’ or parent company’s websites

• Via external, third-party websites, but only when there is a direct web link from the brand or parent company’s website to the third-party website where specific disclosures can be found

We do not count the following information sources:

• A third-party website or document where there is no web link from the brand’s own website, including press articles

• Clothing labels and hang tags on products

• In-store or other physical locations

• Smartphone apps

• Social media channels

• Information provided to us by a fashion brand that cannot be found on the brand’s website

Transparency ≠ ethics and sustainability

What Fuels Fashion? does not measure ethics or sustainability. A brand can score highly on transparency of their decarbonisation efforts, but this does not mean they are ethical or sustainable.

We do not endorse any brand in the research or suggest that consumers shop at specific brands based on their ranking. This is not a shopping guide.

Beyond black & white How to understand the data

The challenge of measuring climate plans through transparency alone

Transparency remains a central pillar of our theory of change, and we stand by the principle that no data is data — the absence of disclosure is itself a meaningful signal. But we also recognise the limitations of assessing complex climate transition plans through transparency alone.

Our methodology is designed to raise ambition by spotlighting emerging issues — such as 24/7 hourly matching and industrial electrification — and by rewarding detailed, comparable disclosures. Yet, nuance can sometimes be lost. Because we assess transparency in binary terms (disclosed or not disclosed), some brands may be marked down for failing to report on practices they do not actually use. Without clear public disclosure, however, we cannot tell the difference between a brand that genuinely does not use a practice and one that is simply choosing not to be transparent.

This tension underscores both the importance and the limits of public disclosure. Transparency remains the foundation of accountability but it cannot substitute for a deeper evaluation of the integrity of brand transition plans. For this, we look to complementary work from organisations like Action Speaks Louder, Stand.earth , NewClimate Institute , and others.

For this second edition of What Fuels Fashion? , some findings are comparable year-on-year, others are not. We refined our scope to focus on 200 of the world’s largest fashion brands, each with an estimated annual turnover of over USD $1 billion. As a result, some data from 2024 has been recalculated to reflect only those same 200 brands, ensuring a more accurate and consistent comparison where possible. In cases where year-on-year comparisons are valid, this is clearly stated in the report.

Additionally, we introduced new indicators to strengthen the analysis. For this reason, not all data points can be compared directly with those published in 2024. Unless otherwise specified, all percentages in the 2025 edition should be understood as out of the 200 brands reviewed this year.

As an example , 34% of brands reviewed disclosed a time-bound and measurable commitment to decarbonisation whereas less, 32% of brands, disclosed progress against their decarbonisation targets. This indicates that fewer brands report on their progress than those who state they have such targets. It does not mean that of the 34% of brands who have a decarbonisation target, 32% of them disclose progress against their target.

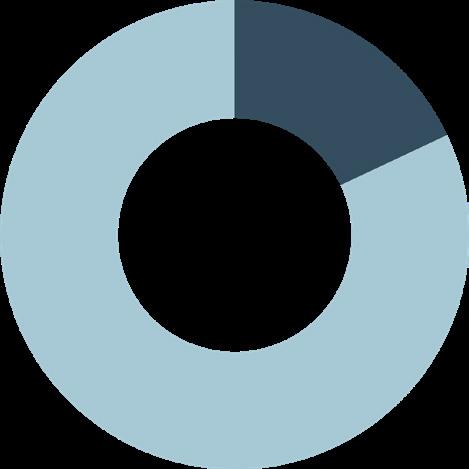

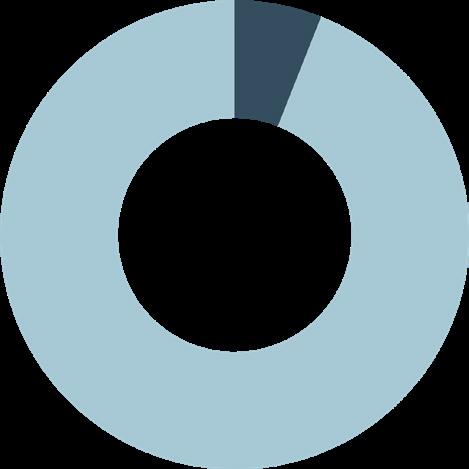

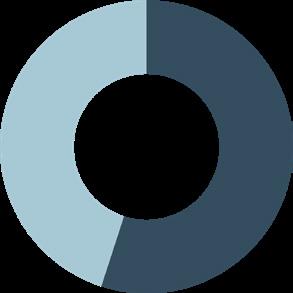

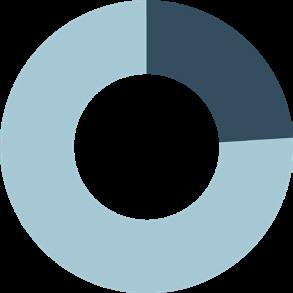

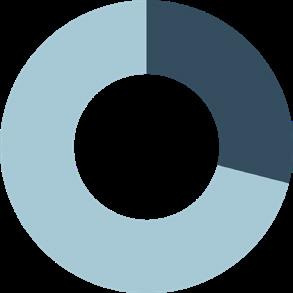

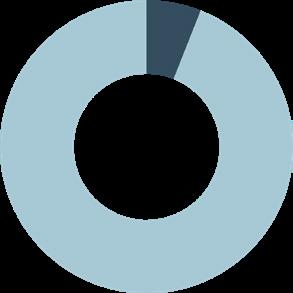

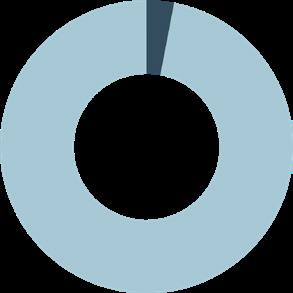

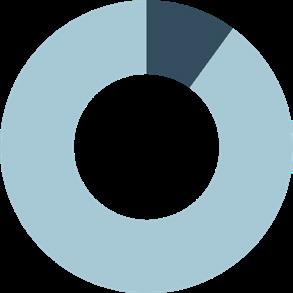

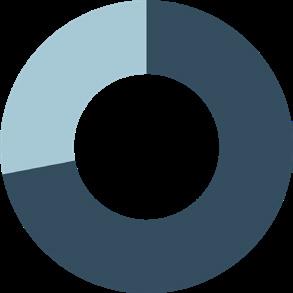

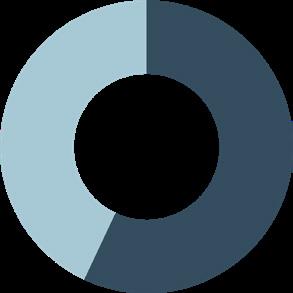

EMISSIONS VISUALISED

SUPPLY CHAIN EMISSIONS SPLIT

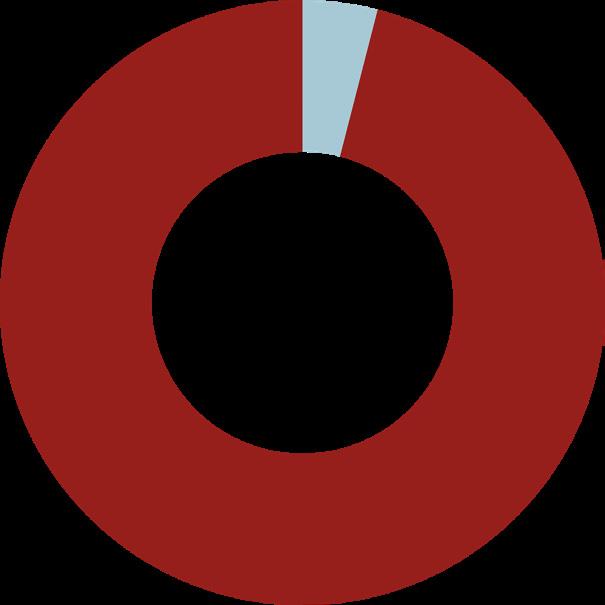

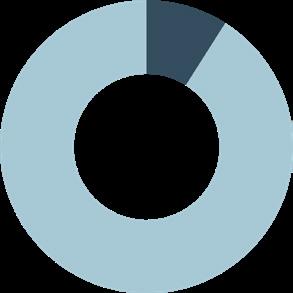

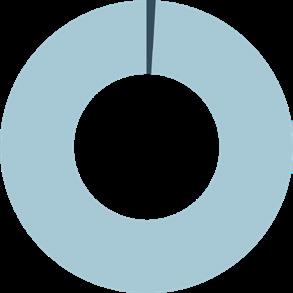

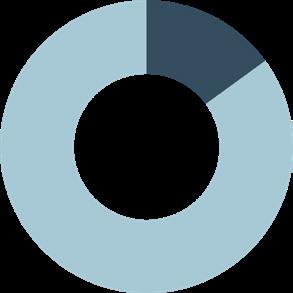

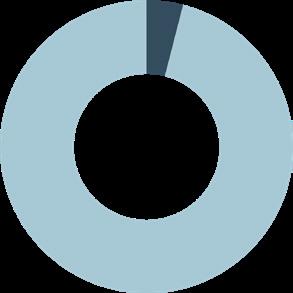

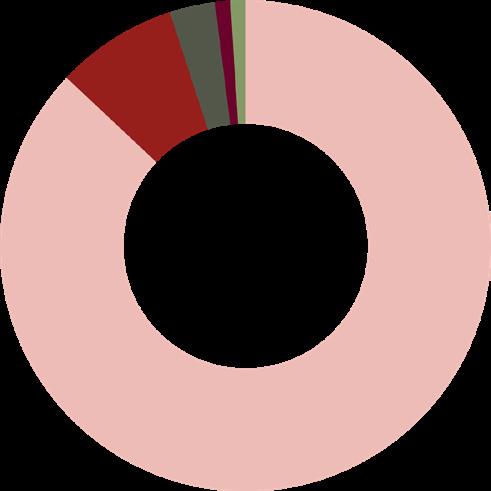

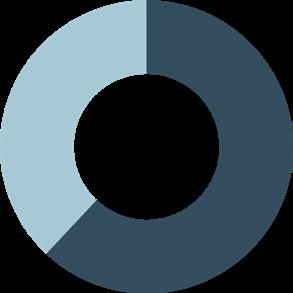

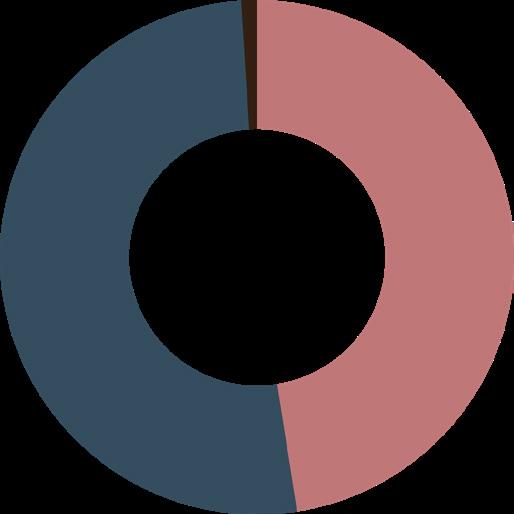

For apparel brands, scope 1 emissions (with Science Based Targets) typically account for 1% of their total emissions, while Scope 3 represents around 96%.

Data from Apparel Impact Institute

KEY FINDINGS

KEY RESULTS

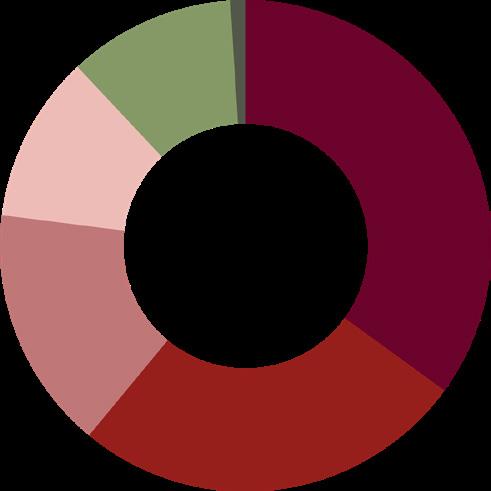

AVERAGE SCORES

BY SECTION

Average score across the 200 brands reviewed in 2025

RESULTS

OVERALL SCORE

PER BRAND

KEY RESULTS

HIGHEST SCORING BRANDS

LOWEST SCORING BRANDS

Lululemon Gildan

Chico’s

Tory Burch

Quiksilver

Nine West

Champion

Hudson’s Bay

New

Heusen

Beanpole

Billabong

Buckle

Deichmann

ACCOUNTABILITY

APPROACH ACCOUNTABILITY

Governance

In this subsection, we examine who in the company is accountable for the brand’s climate performance and impacts. We check if brands publish information on the percentage of CEO and executive-level pay and incentives tied to achieving absolute carbon reduction across the entire value chain. We also assess whether suppliers’ incentives, such as long-term contracts, increased order sizes, price premiums, and reduced audits, are tied to decarbonisation improvements.

Additionally, we are looking for whether brands disclose an internal price on carbon and what that price is.

Overproduction & Materials

Here we assess what brands are doing to address overproduction. We looked specifically at:

• Public disclosure on how many items were produced in the reporting period

• Brands’ public commitment to degrowth

Traceability

This subsection focuses on whether brands are publishing supplier lists, focusing on the level of detail provided at three different levels:

1. The factories where clothes are made, often referred to as the first-tier or tier 1 manufacturers — in other words, the facilities with which brands have a direct relationship and typically do the cutting, sewing and final trims of products;

2. The processing facilities further down the supply chain — knitting, weaving and spinning mills, wet processing, embroidery, printing and finishing, dye-houses, tanneries and laundries;

3. The suppliers of raw materials — primary materials such as fibres, hides, rubber, chemical and metals.

We check whether brands are sharing the following information:

• Name of parent company

• Address of the facility

• Type of products/services supplied

• If the list is in machine-readable format (csv, json, xls)

• If the list is contributed to the Open Supply Hub platform

This year, we also included a new indicator to help assess the level of brand ownership of their manufacturers and processing suppliers.

RESULTS

OVERALL

SCORE PER BRAND

GOVERNANCE

ANALYSIS GOVERNANCE

Fashion’s governance model remains profit-first, sidelining climate action even as climate risks escalate.

This past year has been particularly difficult for the fashion industry. Economic pressures have forced brands to make staff cuts , climate disruptions caused by rising temperatures and flooding continue to destabilise supply chains, and the luxury market is showing signs of strain amid global economic uncertainty and geopolitical tensions. The looming threat of Trump’s proposed tariffs adds further instability, with major implications for global supply chains. Yet, even against this backdrop, fashion CEOs’ pay continues to rise with an average increase of 23.5% for the 25 highest-paid CEOs in American fashion.

Fashion CEOs’ pay continues to rise, with an average increase of 23.5%

This imbalance is particularly striking given that only 15% of brands disclose the percentage of executive bonus or pay tied to achieving absolute carbon reduction. Of those 30 brands, about half disclose that just 10% of the bonus is tied to this target – a low figure considering fashion executives’ significant responsibility to achieve climate targets but also their urgent moral duty to act in the face of a devastating planetary crisis.

Fewer brands (20%) disclose supplier incentives tied to decarbonisation, compared to last year’s 24%. This backslide is concerning: incentives like long-term contracts, increased orders, price premiums, and fewer audits are critical to spur the investments needed in supply chains. However, to accelerate changes at the scale and speed needed, incentives and accountability systems must be built at brand AND supplier level. Given existing power imbalances between major brands and their suppliers, a Just Transition requires shifting the financial responsibility for decarbonisation back to major brands and their executives to work hand in hand with suppliers and drive meaningful decarbonisation across supply chains.

Carbon price

Major fashion brands and retailers must also embed climate accountability directly into their financial decision-making. One of the clearest ways to do this is by adopting an internal carbon price (ICP).

Setting an ICP is a crucial step in a brand’s climate strategy. It assigns a monetary value to greenhouse gas emissions across the value chain, creating clear pressure points to decarbonise. According to CDP, the most commonly cited reasons to set an ICP are:

• Driving low-carbon investment

• Improving energy efficiency

• Shifting internal behaviour

• Identifying new low-carbon opportunities

• Navigating GHG regulations

• Stress-testing investments

From an investor perspective, this tool is particularly useful: it helps define financial materiality to assess and manage carbon-related risks within operations and supply chains while helping investors understand how effective the application of a carbon price is to meet a company’s climate goals.

The way an ICP is designed also reveals a company’s approach to climate risk. According to Plan A, there are three commonly used approaches to set up an ICP:

• Shadow price: A company assigns a notional cost to each ton of greenhouse gas emissions when weighing up investment decisions. This helps compare the cost and benefit of different reduction strategies, but no money is transferred as part of this approach.

• Internal carbon fee or charge: The company sets a price on its emissions and charges itself accordingly. The money collected is then reinvested into energy efficiency or emissions reduction projects, helping manage climate-related risks and meet reduction targets.

• Implicit carbon price: The price is calculated based on the organisation’s cost to implement emissions reduction projects. This is then applied to where GHG emissions are emitted within the business. Companies can strategically use an implicit carbon price to allocate funds across the business.

These approaches signal the level of a brand’s ambition: while a shadow price is often used as a starting point, internal fees or charges directly generate funds for decarbonisation. Yet, only 7% of major fashion brands and retailers disclose their ICP. This lack of transparency signals that major brands are lagging far behind other sectors. For example, nearly 50% of the world’s largest 500 companies reported having an ICP in place in 2021 and 44% of chemical companies , according to KPMG.

Within the 14 brands disclosing their ICP, the price ranges from $10 to $108, with European companies such as JD Sports, LVMH and Puma setting higher ICPs compared to their Australian or American counterparts. It is interesting to note that while companies like H&M use a shadow price to define their ICP, luxury companies like LVMH and Burberry use a fee mechanism to invest in decarbonisation projects. Nevertheless, despite the sector’s significant carbon footprint and contribution to the climate crisis, this lack of disclosure may suggest that most major brands and retailers are failing to future proof their business against climate risks.

Setting an internal carbon price assigns a monetary value to greenhouse gas emissions, creating clear pressure points to decarbonise.

Higher carbon prices reported by Europeanheadquartered brands could reflect anticipation of upcoming carbon pricing legislation, including the EU’s Carbon Border Adjustment Mechanism (CBAM) — which applies a levy on carbon-intensive imports, though textiles are not yet included — as well as the EU Emissions Trading Scheme (ETS), a cap-and-trade system that sets an annual emissions cap and allows companies to buy and sell allowances.

In contrast, companies that adopt higher, more realistic ICPs signal to investors that they are preparing for a lowcarbon economy, aligning financial planning with climate targets, and creating dedicated funds for decarbonisation projects in their supply chains.

TRACEABILITYACCOUNTABILITY

FINDINGS TRACEABILITY

Without knowing where production takes place, brands cannot identify which factories are still running on coal, which regions are most exposed to climate risks like flooding or extreme heat, or where electrification and clean heat investments would have the greatest impact. Supply chain visibility is therefore the first step in phasing out fossil fuels, scaling industrial electrification, and protecting workers on the frontlines of the climate crisis.

“ The PRI welcomes Fashion Revolution’s efforts to drive systemic progress in the fashion sector by advancing transparency and accountability across global supply chains. The expansion of global fashion supply chains has heightened their complexity and opacity, making it more difficult for investors to assess material risks linked to climate, governance, and human rights issues in the sector. Current disclosures fall short in demonstrating how executive incentives, financial strategies, and supplier support align with credible decarbonisation pathways. Investors can play an important role here, by engaging companies towards adopting credible transition plans, strengthening supplier accountability, and ensuring board-level oversight. They can also steer capital allocation towards supply chain decarbonisation and due diligence initiatives. Taken together, these actions can drive greater transparency and resilience across the sector and its value chain, helping to ensure that risks are managed responsibly while unlocking long-term value for businesses, workers, and communities.

Soh-Won Kim Specialist, Stewardship, Social Issues and Human Rights at Principles for Responsible Investment (PRI)

Image: Fair Wear Foundation

BRANDS’ DISCLUSURE IN THEIR SUPPLY CHAIN

ANALYSIS TRACEABILITY

The fashion industry has reached a transparency plateau and it is a major climate roadblock.

Supply chain traceability has been central to Fashion Revolution’s mission from the very beginning. Since launching the #WhoMadeMyClothes campaign, we have challenged the fashion industry’s reliance on opaque, extractive supply chains built on the labour and resources of women and marginalised communities.

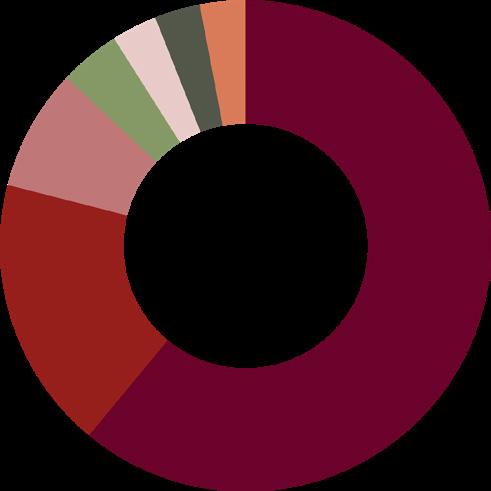

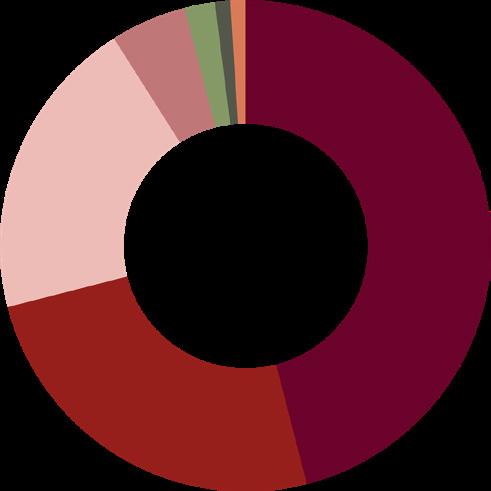

After nearly a decade of incremental progress, the disclosure levels of supplier lists is now stalling: 53% of brands disclose their manufacturers, 35% disclose processing facilities, and only 7% disclose raw material suppliers. These figures have barely shifted in recent years, revealing the limits of voluntary action.

Just over half (53%) of brands now disclose their finished goods facilities, a baseline level of transparency that has taken us nine years of persistent effort to reach. This plateau now poses a direct barrier to decarbonisation, highlighting the limits of voluntary action and reinforcing what we have long observed: a significant proportion of major fashion brands clearly will not disclose unless compelled by legally binding regulation.

After nearly a decade of incremental progress, the disclosure levels of supplier lists is now stalling

That is why Fashion Revolution has campaigned consistently for robust European legislation on corporate accountability — to hold major fashion brands accountable for the human rights and environmental impacts in their operations and supply chains.

For example, through the Good Clothes, Fair Pay European Citizens’ Initiative — led by Fashion Revolution and the largest ever campaign on living wages and collective bargaining in the fashion industry — we worked with garment worker trade unions, NGOs and allies to strengthen the Corporate Sustainability Due Diligence Directive (CSDDD). As part of the campaign, we jointly drafted a legal proposal addressing gaps in the directive on living wages and collective bargaining rights, critical to realising garment workers’ top demand: fair pay.

The Omnibus risks reversing advances on accountability that civil society, trade unions and worker organisations fought to secure in the CSDDD. Instead of raising ambition to meet the urgency of climate breakdown and workers’ demands, the the European Commission and Council are seeking to dilute core provisions and weaken accountability.

The EU Omnibus risks weakening the very laws needed to unlock clean heat

In February 2025, the European Commission proposed an Omnibus Simplification package to amend the Corporate Sustainability Reporting Directive (CSRD), CSDDD and the EU Taxonomy. Framed as cutting “administrative burden,” the proposal copies verbatim many demands of corporate lobby groups .

In June 2025, the Council adopted its negotiating position, in some cases going even further. The Council’s negotiating mandate widens the rollbacks, including raising thresholds for which companies are covered, delaying application by an additional year, and softening obligations around climate plans and due diligence.

The Omnibus will soon enter trilogues — closed-door talks between the European Commission, Parliament and Council. These negotiations, with little transparency or consultation, will decide whether the EU keeps meaningful accountability laws or locks in deregulation. Civil society groups, trade unions and human rights organisations have issued joint statement highlighting concerns that the Omnibus risks weakening accountability and exposes the proposal as a deregulatory package that guts due diligence, weakens accountability, and puts corporate interests ahead of human rights and climate action.

The most concerning changes

Although details are still shifting with differing proposals among the Commission and the Council, several potential rollbacks are clear and highly relevant to fashion supply chains:

• Climate transition plans made optional. The obligation to put plans into effect has been removed. The Council further dilutes ambition from “best efforts” aligned with 1.5°C to “reasonable efforts” that merely “contribute.”

• Civil liability weakened. Responsibility is left to Member States, representative actions by NGOs and trade unions are removed, and EU courts could be required to apply foreign law. This drastically limits victims’ access to justice.

• Due diligence cut to Tier-1 suppliers. Companies would only need to assess harms caused by their direct business partners. Further down the chain, action is required only if they hold vague “plausible” or “reasonably available” information.

• Monitoring delayed. Reviews of due diligence effectiveness fall from every year to once every five years, or only when measures are “no longer adequate.”

• Stakeholder voices excluded. NGOs, unions, human rights defenders and consumer groups are no longer counted as “directly affected” stakeholders.

• Sanctions diluted. Removing the 5% turnover cap risks symbolic penalties and competition between Member States to set the lowest bar.

Why this matters for clean heat in fashion supply chains

For fashion, these proposed changes would reduce accountability at exactly the point where it is most needed:

• Climate plans on paper = no action. Without enforceable implementation, transition plans risk becoming PR documents instead of investment drivers.

• Tier-1 only is a fatal flaw. If oversight stops at cutmake-trim workshops, the real hotspots of emissions and worker risk — dyehouses, printing and finishing units — will continue burning coal and fossil fuels unchecked. A proportionate, risk-based approach is needed: one that directs scrutiny and investment to where the risks are greatest, rather than limiting accountability to the most visible part of the chain.

• Coal phase-out stalls. These processing plants are the biggest users of coal and unreported steam. Without risk-based duties across the full chain, there is no push for electrification or renewable heat where it matters.

• Five-year monitoring hides risks. Energy use and worker heat exposure change year by year; long cycles mean regulators and investors lose visibility.

• Silencing unions and NGOs. Excluding those most able to flag problems cuts off information from the ground.

• Delay in application of the CSDDD – delay in accountability and action. The Council is now also suggesting delaying the application of the law to Jul 2029, despite the urgency to mitigate risks in supply chains.

The result is predictable: brands will do the minimum the law requires, workers will remain exposed to unsafe heat conditions, and the clean-heat transition will stall.

Limiting accountability to Tier-1 suppliers misses the real problem. Without knowing where production takes place, brands cannot map emissions hotspots, identify which factories still burn coal, or plan collective investments in decarbonisation and electrification. Nor can they address the mounting climate risks workers face, from heat stress on factory floors to droughts, floods and storms disrupting production. For this reason, the disclosure of supplier lists – from direct manufacturing down to raw material sources – is fundamental. Only a risk-based approach across the full supply chain can channel investment into clean heat where it is most urgently needed.

Finally, the mention of the CSDDD negatively affecting US businesses is also not new, as US-based lobbying groups were reportedly instrumental in the reopening of the CSDDD. This, in conjunction with the Trump administration wanting to eliminate regulation for greenhouse gases , once again places corporate interests ahead of human rights and climate action.

Global standards push supply chain transparency forward

Amidst the regulatory backslide and the plateau in brand disclosure of supplier lists, there can be cause for optimism. The Global Reporting Initiative (GRI) is finalising the first-ever Sector Standard for Textiles and Apparel , which, once approved and adopted, will recommend companies disclose information about their suppliers, including names, site locations, parent companies, the types of products or services offered, the percentage of significant suppliers at each tier, the share of business volume they represent, and the methodologies used to identify them. If any of these disclosures are considered not relevant, companies will be expected to provide a reason for the omission, offering insight into why critical data remains withheld. These recommendations will apply to all textile and apparel companies reporting under the GRI, the world’s most widely used sustainability reporting standard, adopted by over 14,000 organisations in more than 100 countries. By aligning with our methodology, the new Standard could raise the floor for supply chain transparency worldwide, embedding supplier disclosure into a global reporting framework and amplifying calls for stronger regulation.

Fashion Revolution’s Role in the Global Reporting Initiative (GRI)

Fashion Revolution was selected as one of 21 international experts appointed by the Global Sustainability Standards Board to join the GRI Working Group. Representing civil society, labour, business, and investment sectors from across all regions, the group is responsible for shaping the content of the Standard between 2024 and 2026. Our representative brought critical insights from Fashion Revolution’s nearly ten years of research experience on transparency to the group, ensuring the standard responds to the sector’s most urgent environmental and social challenges.

Ownership matters: brands with skin in the game can drive decarbonisation

Last year, despite not having a dedicated indicator, we observed that key brands with partial or full ownership of their supply chain scored higher, particularly those in sportswear and luxury, where long-term relationships with specialised suppliers are common. To explore this further, two new indicators were introduced this year to assess the extent to which Big Fashion brands disclose ownership of their manufacturing and processing facilities.

The data reveals that most brands either do not own production facilities or fail to disclose this information. Only 23% of brands disclose ownership information for manufacturing facilities, and just 19% do so for processing level – where the greatest decarbonisation challenges lie.

Vertical integration or concentrated purchasing power may give brands greater visibility, leverage and stronger transparency on climate issues.

Even more telling is that among brands disclosing this information, levels of ownership are minimal: more than half report owning no manufacturing (62%) or processing (68%) facilities.

The exceptions are concentrated in the intimates, sportswear, and luxury sectors, where higher ownership correlates with stronger performance overall. Of the brands disclosing this information, they own the following percentage of their supply chain: Fruit of the Loom and Russell Athletic (85%), Tezenis (71%), Calzedonia (68%), Intimissimi (97%), Hanes (70%), and Hermès (55%) 4. Most of these brands also rank among the top performers in this year’s research, suggesting that vertical integration or concentrated purchasing power may give brands greater visibility and leverage and with it, stronger transparency on climate issues. Other industries, like tech, show what’s possible: 95% of Apple’s suppliers — over 320 companies covering nearly all of its manufacturing spend — have pledged to power Apple production with 100% renewable electricity by 2030 .

Brands with higher ownership levels are typically better placed to invest in renewable energy, pilot clean heat technologies, and coordinate adaptation strategies because they offer greater stability. By contrast, brands that rely on short-term contracts with opaque supply chains lack both visibility and leverage to deliver decarbonisation where it matters.

For the majority of brands going back to an increased ownership level may be unlikely. However, an investment in stable, longer term partnerships is vital for progress, even outside of ownership. Achieving real progress will require brands to move beyond extractive, short-term profit supply chain models and actively invest in stable, longer-term supplier partnerships. These relationships create the trust and stability required to share investment, accelerate the renewable energy transition and deliver on broader climate goals.

Publicly-listed companies make up most (59%) of brands scoring zero on traceability

Voluntary frameworks aim to raise corporate accountability standards. However, our findings reveal that many publicly-listed fashion companies — who are answerable to shareholders and often subject to ESG reporting frameworks — are failing at the most basic level of supply chain transparency. Out of the 200 companies assessed, 136 are publicly listed and 64 are privately owned. Although public companies make up most of the sample, they also represent the majority of the worst performers: of the 90 brands scoring zero on traceability, 53 (59%) are publicly listed while 37 (41%) are privately owned.

Investors must demand that publiclylisted fashion companies disclose supplier lists as a baseline requirement

This exposes not only a regulatory gap but also a critical accountability gap in investor oversight. Investors appear to be missing a crucial opportunity to use their influence to demand even the most basic transparency standards. This failure matters for climate action. Without visibility into where production happens, investors and other stakeholders cannot assess whether companies are phasing out coal, electrifying factories, or addressing worker heat stress. A lack of traceability makes it impossible to evaluate material climate risks or to channel finance into credible decarbonisation.

In short, this is a glaring gap in ESG oversight: Investors, particularly those who claim alignment with sustainable finance and ethical governance, are overlooking a fundamental building block of climate accountability. To close this gap, investors must demand that publicly-listed fashion companies disclose supplier lists as a baseline requirement — without it, any claim of alignment with climate or social goals rings hollow.

BRANDS SCORING ZERO IN THE TRACEABILITY SECTION

Aeropostale

AJIO

ANTA

Anthropologie

Aritzia

Armani

BCBGMAXAZRIA

Beanpole

Belle

Bershka

Billabong

Bosideng

Brunello Cucinelli

Buckle

Burberry

Burlington

Carolina Herrera

CAROLL

CELINE

Champion

Chanel

Chico’s

Cortefiel

Decathlon

Deichmann

Diesel

Dillards

Dior

DKNY

Dolce & Gabbana

DSW

Eddie Bauer

El Corte Inglés

Express

Falabella

Famous Footwear

Fashion Nova

Fila

Foot Locker

Forever21

Foschini

Free People

Heilan Home

Hudson’s Bay

Jil Sander

Kohl’s

La Redoute

Lands’ End

LC Waikiki

LL Bean

Louis Vuitton

Marc Jacobs

Marni

Massimo Dutti

Max

Max Mara

Moncler

Monoprix

MRP

New Yorker

Nine West

Pull&Bear

Quiksilver

Reebok

Reliance Trends

REVOLVE

Ross Dress for Less

Roxy

Saks Fifth Avenue

Semir

Shimamura

Skechers

Smart Bazaar

Splash

Sports Direct

Steve Madden

Stradivarius

Takko

Ted Baker

The Children’s Place

TJ Maxx

Tod’s

TOPVALU COLLECTION

Tory Burch

Truworths

Urban Outfitters

Van Heusen

Walmart

Youngor

Zara

OVERPRODUCTION

FINDINGS

ANALYSIS

Discloses quantity of products produced annually

Discloses a commitment to degrowth

Overproduction is fashion’s most visible climate impact — but with 91% of brands failing to disclose volumes, few are willing to be held accountable.

Overproduction is fashion’s business model. It is a systemic problem at the heart of the industry, driving labour exploitation, environmental destruction and perpetuating colonial forms of extraction. The sector thrives on creating desire, fuelling consumption, and chasing endless growth — on a planet with finite resources. This equation doesn’t add up.

The sector thrives on creating desire, fuelling consumption, and chasing endless growth

Only 9% of brands in our research disclose their annual production volumes. Across the 17 brands that disclose this information, that’s a staggering 4.3 billion 5 items produced per year. To put that in perspective, with a global population of about 8 billion, that’s more than one item for every two people on the planet — from just 17 brands alone. The true scale of overproduction is likely far greater than even these staggering numbers suggest. Transparency of production volumes is critical to addressing this deeply rooted overproduction problem.

BRAND DISCLOSURES ON PRODUCTION VOLUMES

Brand

Calzedonia

Fendi

Gildan

GUESS

Hanes

Intimissimi

Kmart Australia

Kontoor Group (Lee and Wrangler)

Mango

OVS

s.Oliver

Tezenis

Tom Tailor

VF Corporation (The North Face, Timberland & Vans)

Disclosed number of products produced during the annual reporting period 92,380,000 1,277,500,000 1,600,000,000

New research from the Apparel Impact Institute found that in 2023, emissions from the apparel sector increased by 7.5% compared to the previous year – equivalent to 944 million tonnes. The primary reason for this increase in emissions? The growth in polyester fibre production. Polyester, the world’s most produced fibre , is derived from petrochemicals, making it inherently tied to the climate crisis. But the connection goes beyond raw materials composition as already stated across this report. Producing fabric and garment uses huge amounts of energy – from processing to transport. When these materials end up as waste, all of that energy is lost, and the emissions generated in the process have been released for nothing – and will continue to cause environmental impact throughout its lifecycle.

At Fashion Revolution, we define overproduction as making more clothes and textiles than people need – creating surplus stock that is discarded, destroyed, or simply left sitting in wardrobes. By this definition, “producing to demand” is not a solution. Our position is clear: we need to make less.

Big Fashion continues to ignore the need for degrowth

With only one brand publicly committing to reduce the number of new garments produced each year, the industry is sending a clear message: it has no intention of confronting its deeply unsustainable business model.

A recent study exploring possible future trajectories for world development within planetary boundaries warns that, under current trends and policies, we will see worsening outcomes in all but one of the Earth’s planetary boundaries by 2050. Even as we globally approach multiple tipping points, fashion continues to equate progress with exponential growth in production and consumption.

Among the 200 billion-dollar brands assessed in this report, only one — Paris, a brand under Chilean conglomerate Cencosud — made an explicit commitment to degrowth. In their Sustainability Roadmap , they: “made commitmentsto reducethe amount ofclothing we produce underourown brands, design and market garmentswith durabilityattributes, increase our customers’consumption ofsecond-hand clothing, and reintegrate into production cyclesthe materials obtained atthe end ofa garment’s useful life.”

It is telling—and alarming—that this was the only explicit reference to degrowth found in our research. Degrowth is the principle of reducing production and consumption in line with planetary boundaries while improving human well-being. Those who have gained most from decades of resource exploitation, particularly major brands in the Global Minority, must lead the way in cutting consumption and addressing climate impacts.

This concept challenges the GDP-driven growth model, which measures ‘progress’ without distinguishing between value-creating activities and those causing environmental or social harm. It calls for a fair and planned reduction in production and consumption, alongside a fundamental rethink of how brands fuel demand through endless marketing and promotions.

The industry has no intention of confronting its deeply unsustainable business model

A degrowth pathway demands rebalancing power in the industry: prioritising garment workers’ rights, ensuring living wages, distributing wealth more fairly and rejecting any approach that shifts the cost of change onto garment workers.

Continuing with business-as-usual will lead us further into dangerous territory.

We cannot shop our way out of the climate crisis but ambitious policy shifts can still limit the extent of the damage if action is bold, swift, and global.

As stated in the Global Tipping Points Conference Statement 2025 :

“Thewindowforpreventingthese cascading climate dynamics is rapidlyclosing, demanding immediate, unprecedented actionfrom policymakersworldwide— especiallyfrom leaders at COP30.This is a human rights and planetaryhealth imperative, and ultimately, a matterofsurvival.”

Holding brands accountable through legislation

Tackling fashion’s overproduction crisis requires more than voluntary pledges, it demands structural changes that make excessive production financially and operationally unsustainable. This is where legislation and control mechanisms come in.

Extended Producer Responsibility (EPR) and the concept of Targeted Producer Responsibility (TPR), for example, aim to manage fashion waste and disincentivise mass overproduction by holding brands accountable for the social and environmental impacts of products throughout their lifecycle. For deeper analysis on this, see pg. 39 of our 2024 What Fuels Fashion? Report .